IIF to Acquire and Lease Ten Properties in Japan · However, in the case where (i) the tenant...

50

1 Note: This press release is intended as general information for the press regarding IIF’s acquisition and lease of real estate and trust beneficiary interests in real estate in Japan, and has not been prepared for the purpose of solicitation of investment. February 20, 2018 To all concerned parties: Investment Corporation Industrial & Infrastructure Fund Investment Corporation (Tokyo Stock Exchange Company Code: 3249) Representative: Yasuyuki Kuratsu, Executive Director URL: http://www.iif-reit.com/english/ Asset Management Company Mitsubishi Corp.-UBS Realty Inc. Representative: Toru Tsuji, President & CEO Inquiries: Hidehiko Ueda, Head of Industrial Division TEL: +81-3-5293-7091 IIF to Acquire and Lease Ten Properties in Japan Industrial & Infrastructure Fund Investment Corporation (“IIF”) announced today that Mitsubishi Corp.– UBS Realty Inc., IIF’s asset manager (the “Asset Manager”), decided to acquire and lease domestic real estate and real estate trust beneficiary rights (the “Anticipated Acquisitions”) as outlined below. 1. Summary of Anticipated Acquisitions Property number (Note 1) Property name (Note 2) Location Seller (Note 3) Anticipated acquisition price (million yen) Appraisal value (Note 4) (million yen) NOI yield (Note 5) NOI yield (after depreciation) (Note 5) Anticipated acquisition date F-13 IIF Hiroshima Manufacturing Center (land with leasehold interest) Hiroshima-sh i, Hiroshima Metal One Corporation (Note 6) 1,608 1,820 6.2% 6.2% March 8, 2018 F-14 IIF Totsuka Manufacturing Center (land with leasehold interest) Yokohama-shi , Kanagawa MITSUIKE CORPORATION 2,300 2,580 5.0% 5.0% March 8, 2018 F-15 IIF Atsugi Manufacturing Center (land with leasehold interest) Atsugi-shi, Kanagawa Business Company in Japan (Note 7) 4,940 5,180 5.0% 5.0% April 2, 2018 L-36 IIF Itabashi Logistics Center (40% co-ownership interest) Itabashi-ku, Tokyo SPC (Note 6) 686 756 4.4% 3.7% March 8, 2018 L-39 IIF Osaka Suminoe Logistics Center I (25% co-ownership interest) Osaka-shi, Osaka Business Company in Japan (Note 6) 3,025 3,500 4.2% 3.3% March 8, 2018 L-40 IIF Osaka Suminoe Logistics Center II (25% co-ownership interest) Osaka-shi, Osaka Business Company in Japan (Note 6) 635 683 4.7% 4.1% March 8, 2018 L-42 IIF Sapporo Logistics Center Sapporo-shi, Hokkaido SPC 2,480 2,600 5.4% 4.7% March 8, 2018 Additional Acquisition Additional Acquisition Additional Acquisition

Transcript of IIF to Acquire and Lease Ten Properties in Japan · However, in the case where (i) the tenant...

1

Note: This press release is intended as general information for the press regarding IIF’s acquisition and lease of real estate and trust beneficiary interests in real estate in Japan, and has not been prepared for the purpose of solicitation of investment.

February 20, 2018 To all concerned parties:

Investment Corporation Industrial & Infrastructure Fund Investment Corporation (Tokyo Stock Exchange Company Code: 3249) Representative: Yasuyuki Kuratsu, Executive Director URL: http://www.iif-reit.com/english/ Asset Management Company Mitsubishi Corp.-UBS Realty Inc.

Representative: Toru Tsuji, President & CEO Inquiries: Hidehiko Ueda, Head of Industrial Division TEL:+81-3-5293-7091

IIF to Acquire and Lease Ten Properties in Japan

Industrial & Infrastructure Fund Investment Corporation (“IIF”) announced today that Mitsubishi Corp.–UBS Realty Inc., IIF’s asset manager (the “Asset Manager”), decided to acquire and lease domestic real estate and real estate trust beneficiary rights (the “Anticipated Acquisitions”) as outlined below.

1. Summary of Anticipated Acquisitions

Property number

(Note 1) Property name(Note 2) Location Seller(Note 3)

Anticipated acquisition

price (million yen)

Appraisal value(Note 4)

(million yen)

NOI yield (Note 5)

NOI yield (after

depreciation)

(Note 5)

Anticipated acquisition

date

F-13 IIF Hiroshima Manufacturing Center (land with leasehold interest)

Hiroshima-shi,

Hiroshima

Metal One Corporation

(Note 6) 1,608 1,820 6.2% 6.2%

March 8, 2018

F-14 IIF Totsuka Manufacturing Center (land with leasehold interest)

Yokohama-shi,

Kanagawa

MITSUIKE CORPORATION 2,300 2,580 5.0% 5.0%

March 8, 2018

F-15 IIF Atsugi Manufacturing Center (land with leasehold interest)

Atsugi-shi, Kanagawa

Business Company in

Japan (Note 7)

4,940 5,180 5.0% 5.0% April 2,

2018

L-36

IIF Itabashi Logistics Center (40% co-ownership interest)

Itabashi-ku, Tokyo

SPC (Note 6) 686 756 4.4% 3.7%

March 8, 2018

L-39

IIF Osaka Suminoe Logistics Center I (25% co-ownership interest)

Osaka-shi, Osaka

Business Company in

Japan (Note 6)

3,025 3,500 4.2% 3.3% March 8,

2018

L-40

IIF Osaka Suminoe Logistics Center II (25% co-ownership interest)

Osaka-shi, Osaka

Business Company in

Japan (Note 6)

635 683 4.7% 4.1% March 8,

2018

L-42 IIF Sapporo Logistics Center

Sapporo-shi, Hokkaido

SPC 2,480 2,600 5.4% 4.7% March 8,

2018

Additional Acquisition

Additional Acquisition

Additional Acquisition

2

Note: This press release is intended as general information for the press regarding IIF’s acquisition and lease of real estate and trust beneficiary interests in real estate in Japan, and has not been prepared for the purpose of solicitation of investment.

L-43 IIF Hitachinaka Port Logistics Center (land with leasehold interest)

Naka-gun, Ibaraki

Business Company in

Japan 1,145 1,210 4.8% 4.8%

March 9, 2018

L-44 IIF Koriyama Logistics Center

Koriyama-shi, Fukushima

Sumitomo Mitsui Finance

and Leasing Co., Ltd. (Note 6)

2,585 3,160 7.4% 5.6% March 9,

2018

L-45 IIF Kobe Nishi Logistics Center (land with leasehold interest)

Kobe-shi, Hyogo

Kohnan Shoji Co., Ltd. (Current

Owner:Kobe City) (Note 8)

1,960 2,100 4.6% 4.6% March 29,

2018

(Note 1) “Property number” classifies properties owned by IIF into three categories, namely, L (logistics facilities), F (manufacturing, research and development facilities) and I (infrastructure facilities).

(Note 2) “Property name” indicates the name that IIF will use for each property after the Anticipated Acquisitions. These properties do not have registered names as of the date of this news release. The same shall apply hereafter.

(Note 3) When the property is acquired through a bridge structure, the name of an actual seller is indicated. If any consent to disclosure is not obtained by the seller or the bridge seller, the name of the seller is simply indicated as SPC or Business Company in Japan, according to the type of such seller.

(Note 4) The appraisal value is based on the figure shown on the appraisal report as of January 1, 2018. (Note 5) For “NOI yield” and “NOI yield (after depreciation)”, please refer to “Reference: Definitions of Individual Calculation

Formulas” at the end of this news release. (Note 6) IIF acquires these properties by using a bridge function, which will be through Godo Kaisha Industrial Asset Holdings 5

for IIF Koriyama Logistics Center and a business company in Japan for other properties (for IIF Osaka Suminoe Logistics Center I and IIF Osaka Suminoe Logistics Center II, another business company in Japan than the seller).

(Note 7) IIF has entered into a succession agreement, which stipulates that the contractual status of the buyer in the sale and purchase agreement executed between the business company in Japan as the seller and a business company in Japan as the buyer would be transferred from the latter to IIF. When a construction agreement for the purpose of construction of a plant on this property will not be executed by March 31, 2018 between Ichikoh Industries, Ltd. as a contractee and the seller as a contractor, or if it has become clear by March 31, 2018 that a plant will not be constructed at all, the sale and purchase agreement will become invalid and IIF will not succeed the status as purchaser. Thus, if such construction agreement is not executed or it becomes clear that the plant will not be constructed, IIF will not be able to acquire this property.

(Note 8) With respect to Kobe Nishi Logistics Center (land with leasehold interest) the seller of the property will be Kohnan Shoji Co., Ltd., while it is Kobe City that owns this property as of today. As of today, IIF has entered into a memorandum of understanding which stipulates that Kohnan Shoji Co., Ltd. will acquire this property by March 6, 2018 pursuant to the purchase agreement between Kobe City and Kohnan Shoji Co., Ltd., complete administrative procedures and execute a purchase agreement for the sale of this property by March 9, 2018 or by the closing day with which IIF and Kohnan Shoji Co., Ltd. agree. However, IIF will not be able to acquire this property if Kohnan Shoji Co., Ltd. could not acquire the property from Kobe City. A sales and purchase agreement of the trust beneficiary right will be executed between IIF and Kohnan Shoji Co., Ltd. on March 9, 2018.

2. Reason for Acquisitions and Leases

IIF decided to acquire the anticipated properties based on its judgment that the characteristics of the properties are aligned with IIF’s investment strategies, specifically, the acquisition of quality assets that would contribute to increase cash distributions per unit. In deciding whether to acquire the ten properties, we evaluated the properties in terms of profitability, long-term usability and versatility.

Please refer to section “3. Summary of Anticipated Acquisitions and Leases” for the details of each property.

With regards to the reasons for the lease of the Anticipated Acquisitions, we are of the view that each tenant of the Anticipated Acquisitions meets the tenant selection criteria set forth in the “Report on the Management Structure and System of the Issuer of REIT Units and Related Parties”, released as of October 31, 2017. With regards to the reasons for the lease of the individual properties, please refer to section “3.

3

Note: This press release is intended as general information for the press regarding IIF’s acquisition and lease of real estate and trust beneficiary interests in real estate in Japan, and has not been prepared for the purpose of solicitation of investment.

Summary of Anticipated Acquisitions and Leases”.

4

Note: This press release is intended as general information for the press regarding IIF’s acquisition and lease of real estate and trust beneficiary interests in real estate in Japan, and has not been prepared for the purpose of solicitation of investment.

3. Summary of Anticipated Acquisitions and Leases 【IIF Hiroshima Manufacturing Center (land with leasehold interest)】

(1) Summary of Property Type of asset Trust beneficiary right in real estate Anticipated acquisition date (Note)

March 8, 2018

Anticipated acquisition price

1,608 million yen

Appraisal value 1,820 million yen Appraiser Japan Real Estate Institute Date of trust beneficiary rights set

May 31, 2017

Trustee Sumitomo Mitsui Trust Bank, Limited Anticipated trust period end

March 31, 2028

Location (address) 1461-1, Eba-minami 2-chome, Naka-ku, Hiroshima-shi, Hiroshima, Japan Land area 23,106.75 m2

Building structure / stories

-

Zoning Industrial area FAR/building-to-land ratio 200%/60%

Type of Possession Ownership

Earthquake PML - Completion

-

Collateral conditions None

Gross floor area

-

Type of building -

Special notes This property is located in the harbor district.

(Note) “Anticipated acquisition date” is the delivery date with regards to the property expected as of today.

(2) Description of Leases Relating to Anticipated Acquisitions

Tenant(s) Number

of tenant(s)

Total leased area

(occupancy rate)

Annual rent (excluding

consumption tax)

Period of contract Deposit

Metal One Corporation

1 23,106.75 m2

(100%)

Not disclosed

(Note)

20 years (from March 23, 2017 until March 31, 2037)

Not disclosed

(Note) Revision of rent or termination during the lease period

Contract Type: Fixed-term leasehold for business purposes Contract Renewal and Revision: • Rent shall not be revised during the contract period. • When significant changes in economic conditions etc. occur, lessor and lessee shall consult regarding rent revision. • Contract cannot be terminated with a termination date between commencement date of the lease period till August

31, 2021 (“penalty period”) • Lessee may terminate the lease agreement during the penalty period by paying relevant amount of rent for the

remaining period from the termination date till the expiry date as penalty charges to the lessor on the termination date. However, in the case where (i) the tenant candidate which lessee introduced to the lessor has the credit which the lessor is satisfied with (includes but not limited to; satisfaction with the rent payment ability and that it does not

5

Note: This press release is intended as general information for the press regarding IIF’s acquisition and lease of real estate and trust beneficiary interests in real estate in Japan, and has not been prepared for the purpose of solicitation of investment.

correspond to anti-social forces), and (ii) it could be entered into a lease agreement better than that of the conditions of this agreement for the lessor (the lessor may not reject nor reserve the conclusion without a justified reason), lessee can avoid all payment obligations and the duty to put it back to raw land after the cancellation date.

Others: • None (Note) IIF has not obtained the necessary permission from the lessee to disclose this information. (3) Reasons for the Acquisition

■Acquisition Highlights • Acquired through the second CRE proposal to Metal One, a leading steel trading company of

Mitsubishi Corporation group. • Steady tenant demand can be expected with its versatility as a good location for

manufacturing and for securing workforce.

■Long-term Usability (Likelihood of Long-term Use by Current Tenant) • Tenant (land lessee / building owner) is Metal One, a major steel trading company invested by

Mitsubishi Corporation. Metal One leases buildings to several companies (including its affiliates); to companies which processes, stores and uses as a distribution point for coil/steal pipe in manufacturing and construction industry.

• IIF set a non-cancellation period until August 2021, any cancellation during this period is subject to termination fees in the lease agreement executed with the tenant in order to ensure continuity in use in the midterm.

■Versatility (Versatility as a Real Estate Asset)

<Location> • Good access to Hiroshima city; approximately 1.3km from Hiroshima Highway Route 3 Yoshijima

IC, approximately 1.2km from Hiroshima Electric Railway Eba Station. Also, close to residential area and good for securing workforce.

• Close to Mitsubishi Heavy Industry Hiroshima Machinery Works Eba Plant, located in area where plants concentrate. Products can be unloaded from the sea by the crane installed to the building.

6

Note: This press release is intended as general information for the press regarding IIF’s acquisition and lease of real estate and trust beneficiary interests in real estate in Japan, and has not been prepared for the purpose of solicitation of investment.

【IIF Totsuka Manufacturing Center (land with leasehold interest)】

(1) Summary of Property Type of asset Trust beneficiary right in real estate Anticipated acquisition date (Note 1)

March 8, 2018

Anticipated acquisition price

2,300 million yen

Appraisal value 2,580 million yen Appraiser Daiwa Real Estate Appraisal Co., Ltd. Anticipated date of trust beneficiary rights set (Note 2)

March 8, 2018

Trustee (Note 2) Mizuho Trust & Banking Co., Ltd. Anticipated trust period end (Note 2)

March 31, 2028

Location (address) 2277-4, Kamiyabe-cho Aza Kunichiyato, Totsuka-ku, Yokohama-shi, Kanagawa, Japan Land area 19,458.49 m2

Building structure / stories

-

Zoning Industrial area FAR/building-to-land ratio 200%/60%

Type of Possession Ownership

Earthquake PML - Completion

-

Collateral conditions None

Gross floor area

-

Type of building -

Special notes

• As it is less likely that the soil of the subject land is contaminated with specific toxic substances as specified by the Soil Contamination Countermeasures Act (Act No.53 of 2002; as amended), it is considered that the possibility of health hazards by specific toxic substances is small. The impact of soil contamination from the surrounding area is not considered, but even if there is any impact from the surroundings, as long as you do not drink ground water, the possibility of health hazard is limited. On the other hand, it is considered that there are no denying the possibility of soil contamination by oil, but as there are currently no oil odor or oil film found in the subject land, it is reported that there is a low possibility that living environment conservation will be at risk due to oil contained soil straight away.

• The structure of the second floor and stair of the property on the adjacent land on the northwestern side (2354-3) cross the boundary into this property. Regarding this cross, a memorandum with the neighbor landowner has been executed; the memorandum stipulates that as long as the object crosses the boundaries, the parties shall acknowledge using the property as it is, and whenever there is a reconstruction of their own structure, the parties are to remove the object at their own responsibility.

• The trustee gives consent to TEPCO Power Grid, Inc. to enter into a part of the subject land for the purpose of maintaining power transmission lines, etc.

(Note 1) “Anticipated acquisition date” is the delivery date with regard to the property expected as of today. (Note 2) “Anticipated date of trust beneficiary rights set”, “Trustee”, and “Anticipated trust period end” are the dates for setting the

real estate trust beneficiary right expected as of today.

7

Note: This press release is intended as general information for the press regarding IIF’s acquisition and lease of real estate and trust beneficiary interests in real estate in Japan, and has not been prepared for the purpose of solicitation of investment.

(2) Description of Leases Relating to Anticipated Acquisitions

Tenant(s) Number

of tenant(s)

Total leased area

(occupancy rate)

Annual rent (excluding

consumption tax)

Period of contract Deposit

MITSUIKE CORPORATION 1

19,458.49 m2 (100%)

Not disclosed

(Note)

50 years (from March 8, 2018

until February 7, 2068)

Not disclosed

(Note) Revision of rent or termination during the lease period

Contract Type: Fixed-term leasehold for business purposes Contract Renewal and Revision: • Rent shall not be revised during the lease period. • When significant changes in economic conditions etc. occur, lessor and lessee shall consult regarding rent revision. • Lessee may not apply for any mid-term termination for five years since the commencement date of the lease period

and may cancel the agreement on two year’s notice after five years have passed.

Others: • If the trustee wants to transfer the property to a third party (except where the property is transferred to the

beneficiary of the trust agreement upon termination of the relevant trust agreement) during the contract period, the trustee shall notify the lessee a transfer request on written notice. Lessee can negotiate with the trustee with priority during the period for first refusal right regarding transfer by notifying the trustee a transfer request in written notice. Above is not applicable for the transfer of trust beneficiary rights.

(Note) IIF has not obtained the necessary permission from the lessee to disclose this information. (3) Reasons for the Acquisition

■Acquisition Highlights • Acquired the land of a manufacturing facility based on the off balance sheet needs of MITSUIKE

CORPORATION, a manufacturer of automobile bodies and parts, though CRE proposal to the company.

• Sustainable for business use for approximately 50 years (remaining term of rent 49.9 years) under the terms stipulated in the fixed-term lease agreement.

• High potential with good access to city area and versatility as an industrial location in the city area.

■Long-term Usability (Likelihood of Long-term Use by Current Tenant) • Sustainable for business use for approximately 50 years (remaining term of rent 49.9 years) under

the terms stipulated in the fixed-term lease agreement. • Main plant with Headquarter of MITSUIKE CORPORATION, a manufacturer of automobile bodies

and parts. Its main business partners are group companies of Nissan Motor Co., Ltd. • Good access from Nissan Motor Co., Ltd. group’s Nissan Shatai Co., Ltd. Headquarters and Nissan

Motor Co., Ltd. Oppama plant, making distribution of products smooth.

■Versatility (Versatility as a Real Estate Asset) <Location> • Located within the Totsuka industrial park, where plants of automotive-part manufactures and

various other sectors are based. As a result, the area is attractive to a variety of tenants. • Near Yokohama Shindo and has potential as an industrial location in the city area as it is easily

accessed to urban area. • Located within the Totsuka industrial park, just approx.1.3 km from Kamiyabe IC through

8

Note: This press release is intended as general information for the press regarding IIF’s acquisition and lease of real estate and trust beneficiary interests in real estate in Japan, and has not been prepared for the purpose of solicitation of investment.

Yokohama Shindo giving good traffic access to National Highway Route 16, Daisan Keihin Road, and Metropolitan Expressway. Also, it is in an advantageous location where residents integrate as a bed town, good for securing a workforce.

•

9

Note: This press release is intended as general information for the press regarding IIF’s acquisition and lease of real estate and trust beneficiary interests in real estate in Japan, and has not been prepared for the purpose of solicitation of investment.

【IIF Atsugi Manufacturing Center (land with leasehold interest)】

(1) Summary of Property

Type of asset Trust beneficiary right in real estate (Note 4)

Summary of building structure evaluation

Evaluator -

Anticipated acquisition date (Note

1) April 2, 2018

Evaluation date

-

Anticipated acquisition price 4,940 million yen

Immediate repair cost

-

Appraisal value 5,180 million yen Short-term repair cost

-

Appraiser Daiwa Real Estate Appraisal Co., Ltd.

Long-term repair cost

-

Anticipated date of trust beneficiary rights set (Note 2)

April 2, 2018 Repair cost for the forthcoming 12 years (annualized average)

- Trustee (Note 2) Mizuho Trust & Banking Co.,

Ltd. Anticipated trust period end (Note 2) April 30, 2028

Location (address) (Note 3)

1-1, Atsugi Morinosato Higashi District Land Readjustment Business area, Kanagawa, Japan., etc. (Lot number) 857, Shimo-furusawa Aza Momijiyama, Atsugi-shi, Kanagawa, Japan., etc.

Land area 64,327.54 m2 (Note 5)

Building structure / stories

-

Zoning Industrial area FAR/building-to-land ratio 200%/60%

Type of Possession Usage(Note 6)

Earthquake PML - Completion

-

Collateral conditions

None

Gross floor area

-

Type of building -

Special notes

• This property is reserved land under the Atsugi Morinosato Higashi District Land Readjustment Business of the Atsugi Urban Redevelopment Project, which is to be carried out by Atsugi Morinosato Higashi District Land Readjustment Association and is scheduled to be completed by the end of the fiscal year 2023. Since any property right of reserved land shall not be obtained until the following day of the date of public notice on land substitution under the Land Readjustment Act (Act No. 119 of 1954, as amended), IIF will neither be allowed to obtain the property right of such reserved land or to register the transfer of such property right until the following day of the date of public notice on land substitution. Any transfer of the reserved land requires approval of the Atsugi Morinosato Higashi District Land Readjustment Association. Boundaries of this property will be eventually determined at the time of land substitution.

• If IIF transfers this property, or grants any security or usufruct over this property or rights regarding this property, IIF is required to gain approval of the Atsugi Morinosato Higashi District Land Readjustment Association (which shall not reserve or reject such approval unreasonably, and shall cooperate with the procedures necessary for such transfer).

• It is provided that Ichikoh Industries, Ltd. may, if a building is constructed on the subject land and a building lease agreement in which the company is specified as a lessee is executed regarding such building, make an offer of purchase the subject land to IIF when three years pass since the commencement of leasing under the relevant building lease agreement and every three years since then. IIF must give prior notification to Ichikoh Industries, Ltd. if it sells the subject land to any third party. If Ichikoh Industries, Ltd. offers to purchase the subject land to IIF within 20 days of receipt of such notification, it may have priority on consultations with IIF on a sale and purchase price and other

10

Note: This press release is intended as general information for the press regarding IIF’s acquisition and lease of real estate and trust beneficiary interests in real estate in Japan, and has not been prepared for the purpose of solicitation of investment.

conditions for 30 days from such offer, and IIF shall make consultation in good faith.

(Note 1) “Anticipated acquisition date” is the delivery date with regard to the property expected as of today. (Note 2) “Anticipated date of trust beneficiary rights set”, “Trustee”, and “Anticipated trust period end” are the dates for setting

the real estate trust beneficiary right expected as of today. (Note 3) Based on the certificate of registration ledger items of reserved land rights. (Note 4) As of today, IIF has executed an agreement concerning status succession between a business company in Japan regarding

IIF Atsugi Manufacturing Center (land with leasehold interest). Under such agreement IIF will succeed the status as a buyer in the real estate sales and purchase agreement for this property from a business company in Japan. Under this agreement, in the case of the buyer and seller amending this agreement into an agreement for sale and purchase of the trust beneficiary rights for the land, or when carrying out necessary procedures such as executing amendment to the agreement for that purpose, the parties shall consult in good faith. Since IIF intends to acquire the land as trust beneficiary rights and plans to consult regarding the amendment to the agreement into an agreement for sale and purchase of the trust beneficiary rights after IIF succeeds the status as a buyer pursuant to the agreement on status succession, the property is classified as trust beneficiary right in real estate. However, in the case where consultation with the seller is not successful, there is a possibility that IIF would acquire the land as a real estate.

(Note 5) Based on the plan as of February 2018, which may be updated after consultation with relevant authorities. (Note 6) Ownership of the underlying land will be transferred to the trustee on the following day of the date of public notice on

land substitution.

(2) Description of Leases Relating to Anticipated Acquisitions As of the date of this news release, IIF and IBJ Leasing Company, Limited. agree to execute the lease

contract for temporary use of land and the contract establishing fixed-term leasehold for business purposes outlined as below respectively, based on the agreement concerning the execution of the lease contract for temporary use of land and the contract establishing fixed-term leasehold for business purposes.

<Outline of the Agreement on Execution of the Lease Contract for Temporary Use of Land(Note 1)>

Tenant(s) Number

of tenant(s)

Total leased area

(occupancy rate)

Annual rent (excluding

consumption tax)

Period of contract Deposit

IBJ Leasing Company, Limited. 1 64,327.54 m2

(100%)

Not disclosed

(Note 2)

1.2 years (from April 2, 2018

until May 31, 2019)(Note 3)

Not disclosed

(Note 2)

Revision of rent or termination during the lease period

Contract Type: Lease contract for temporary use of land Contract Renewal and Revision: • There are no provision on mid-term cancellation and rent revision.

(Note 1) Matters agreed under the fixed-term land lease agreement to be executed between IIF and IBJ Leasing Company, Limited. are outlined, as IBJ Leasing Company, Limited. will construct a building on the subject land after such land is acquired by IIF.

(Note 2) IIF has not obtained the necessary permission from the lessee to disclose this information. (Note 3) The period of contract will end on the same day as the scheduled date of completion of the building. If the completion

of the building gets behind schedule, the lease period will be extended.

11

Note: This press release is intended as general information for the press regarding IIF’s acquisition and lease of real estate and trust beneficiary interests in real estate in Japan, and has not been prepared for the purpose of solicitation of investment.

<Outline of the Agreement on Execution of the Contract Establishing Fixed Term Leasehold for Business Purposes(Note 1)>

Tenant(s) Number

of tenant(s)

Total leased area

(occupancy rate)

Annual rent (excluding

consumption tax)

Period of contract Deposit

IBJ Leasing Company, Limited. 1 64,327.54 m2

(100%)

Not disclosed

(Note 2)

30 years (from May 31, 2019

until May 30, 2049) (Note 3)

Not disclosed

(Note 2)

Revision of rent or termination during the lease period

Contract type: Fixed-term leasehold for business purposes Renewal and Revision: • Rent shall not be revised during the period of contract. • However, the lessor and the lessee may discuss potential revision of rent if there are material fluctuations in

economic conditions, etc. • The period of this contract shall not be extended because of renewal thereof (including renewal upon request or

due to continued use of land) and construction of a building. Provided, however, that a new contract establishing fixed-term leasehold may be executed if any agreement is reached upon mutual consultation.

• If the lessee gives a written notification to the lessor for requesting renewal of the contract from one year prior to the two year before the expiry thereof (the “Notification of Request for Renewal”), the lessor and the lessee shall hold discussions about any execution of renewed contract until the date one year before the expiry thereof.

• The lessor shall not enter into any lease contract regarding the subject land (regardless of whether such agreement is intended for business use or not, and any preliminary agreement thereof) with any other party than the lessee during such discussions.

• The lessor shall also, upon receipt of the Notification of Request for Renewal, give the lessee priority over other potential lessees to negotiate and hold discussions about land lease until the date one year before the expiry of this contract.

Other: • None

(Note 1) Matters agreed under the contract establishing fixed term leasehold for business purposes to be executed between IIF and IBJ Leasing Company, Limited after IBJ Leasing Company Limited constructs a building on the subject land are outlined.

(Note 2) IIF has not obtained the necessary permission from the lessee to disclose this information. (Note 3) The period of the contract will commence on the same day as the scheduled date of completion of the building. If the

completion of the building delays, the commencement of leasing contract will also be delayed.

(3) Reasons for the Acquisition ■Acquisition Highlights

• Development project based on the identified needs of Ichikoh Industries, Ltd., a manufacturer of lamps and other auto parts, to set up a new manufacturing plant on an off-balance basis.

• First-ever “off-balance sheet development project of a manufacturing plant” (Note 1) using our accumulated know-how in which IIF involves.

• Acquired important base via CRE proposal to reflect new facility demand of Ichikoh Industries, Ltd by the scheme of off-balance development collaborating with the lease company. ‒ IIF will acquire the subject land at the commencement of construction work, identifying

needs for new construction of a plant on an off-balance basis. ‒ IIF has “Preferential Negotiation Rights” (Note 2) for the building.

• The location of the subject land is where Ichikoh Industries, Ltd., a subsidiary of Valeo Group that is a major automotive-parts supplier operating globally located in 32 countries, plans new factory.

12

Note: This press release is intended as general information for the press regarding IIF’s acquisition and lease of real estate and trust beneficiary interests in real estate in Japan, and has not been prepared for the purpose of solicitation of investment.

‒ Ichikoh Industries, Ltd., a subsidiary of Valeo Group, holding a leading share in the domestic market of LED for auto head lamps, will set up a new plant as a head lamp production site on this property, as more and more auto head lamps use LED lamps as a light source.

(Note 1) “Off-balance sheet development project” indicates a project implemented by a company that wants to develop a facility while maintaining its financial soundness, in which it has a third party owning land and buildings during and after completion of the project but engages itself in development of the facility for its own use, and then uses the developed facility after completion. During the whole process of such project, neither the land nor buildings to be developed is recorded on the company’s balance sheet. The same shall apply hereinafter.

(Note 2) Although IIF has obtained preferential negotiation rights with respect to the acquisition of the building, no decision has been made with respect to acquisition, and IIF cannot assure that IIF will be able to acquire the building in the future as of today.

■Long-term Usability (Likelihood of Long-term Use by Current Tenant)

• The new factory of Ichikoh Industries, Ltd., the 114 years old manufacture of automotive-parts including head lamp will be the base plant for automotive head lamp, their main product. Production function is planned to be transferred gradually from Isehara manufacturing plant.

• Scheduled to execute a 30 year fixed-term business lease agreement with the land lessee after completion.

■Versatility (Versatility as a Real Estate Asset) <Location>

• Situated on newly developed land within the industrial park, allowed for 24- hours operation. • Located approximately 7.0km from Tomei Expressway Atsugi IC, good accessible to central of west

Tokyo and Kawasaki/Yokohama via National Route 246.

<Facilities> • New building has high versatility as an industrial real estate building; scheduled to be equipped

with span length approximately 16m×12m, minimum beams under effective height approximately 6.7m, and floor load 1.5t / m2.

13

Note: This press release is intended as general information for the press regarding IIF’s acquisition and lease of real estate and trust beneficiary interests in real estate in Japan, and has not been prepared for the purpose of solicitation of investment.

【IIF Itabashi Logistics Center (40% co-ownership interest)】 (1) Summary of Property

Type of asset Trust beneficiary right in real estate (Note 1)

Summary of building structure evaluation

Evaluator Tokyo Marine & Nichido Risk Consulting Co., Ltd.

Anticipated acquisition date (Note 2)

March 8, 2018 Evaluation date

December 6, 2017

Anticipated acquisition price 686 million yen

Immediate repair cost

0 yen

Appraisal value 756 million yen Short-term repair cost

0 yen

Appraiser CBRE K.K. Long-term repair cost

34,782,000 yen

Date of trust beneficiary rights set

May 31, 2007 Repair cost for the forthcoming 12 years (annualized average)

2,898,000 yen Trustee

Mizuho Trust & Banking Co., Ltd.

Anticipated trust period end March 31, 2028

Location (address) 28-3, Higashi-sakashita 2-chome, Itabashi-ku, Tokyo, Japan., etc. Land area 2,522.30 m2

Building structure / stories

4-story steel structure with galvanized steel sheet roof

Zoning Restricted industrial area FAR/building-to-land ratio 200%/60%

Type of Possession Ownership

Earthquake PML 5.8% Completion May 18, 2007

Collateral conditions

None

Gross floor area

5,057.68 m2

Type of building Warehouse

Special notes None

(Note 1) IIF acquired a 60% co-ownership interest in this property (acquisition price: 1,031 million yen) on February 20, 2017, and will acquire the remaining 40% co-ownership interest in this property after this offering.

(Note 2) “Anticipated acquisition date” is the delivery date with regard to the property expected as of today.

(2) Description of Leases Relating to Anticipated Acquisitions

Tenant(s) Number

of tenant(s)

Total leased area

(occupancy rate)

Annual rent (excluding

consumption tax)

Period of contract Deposit

Higashi Twenty One Co., Ltd.

1 5,057.68 m2

(100%)

Not disclosed

(Note)

20 years (from May 31, 2007 until May 31, 2027)

Not disclosed

(Note)

14

Note: This press release is intended as general information for the press regarding IIF’s acquisition and lease of real estate and trust beneficiary interests in real estate in Japan, and has not been prepared for the purpose of solicitation of investment.

Revision of rent or termination during the lease period

Contract Type: Other type of building lease (futsu tatemono chintaishaku keiyaku) Contract Renewal and Revision: • The rent may be revised upon mutual agreement after three years have elapsed since the commencement date of

the lease period, and every three years subsequently, if there are material fluctuations in prices, taxes and other dues imposed on land and buildings, rents of the surrounding land and buildings, or other economic conditions.

• The lease agreement may be renewed upon mutual agreement six months prior to the expiry date of the lease agreement.

• The lessee may not terminate the lease agreement until ten years have elapsed since the commencement date of the lease period.

• The lessee shall pay the relevant amount of rent to the lessor from the month which includes the scheduled date of termination thereof to May 31, 2017 as penalty charges, if the lessee terminates the lease agreement at the lessee’s convenience before ten years have elapsed since the commencement date of the lease period.

• From June 1, 2017, the lessee may terminate the lease agreement without paying termination fees, by giving the lessor six months’ advance written notice.

• Rent specified in this agreement shall remain unchanged for three years following the commencement date of the lease period.

Other: • None (Note) IIF has not obtained the necessary permission from the lessee to disclose this information.

(3) Reasons for the Acquisition

■Long-term Usability (Likelihood of Long-term Use by Current Tenant) • The property, constructed based on the premise of the tenant’s occupation, functions as a key

logistics base of the tenant’s 3PL (third party logistics) (Note) operation, under the name of “Tokyo Integrated Logistics Center” (Note) 3PL (third party logistics) is a company’s use of third party businesses to outsource elements of such company’s

distribution and fulfillment services.

• High-degree of continuity backed by the long-term contract of 20 years (remaining term of rent 9.2 years)

■Versatility (Versatility as a Real Estate Asset) <Location> • Logistics hub located in northern Tokyo near the Outer Tokyo Beltway, with good access to National

Route 17 and Metropolitan Expressway No.5 Ikebukuro Route

<Facilities> • Specifications offering versatility as an urban-type distribution site, as represented by floor load

and ceiling height

15

Note: This press release is intended as general information for the press regarding IIF’s acquisition and lease of real estate and trust beneficiary interests in real estate in Japan, and has not been prepared for the purpose of solicitation of investment.

【IIF Osaka Suminoe Logistics Center I (25% co-ownership interest)】

(1) Summary of Property

Type of asset Trust beneficiary right in real estate (Note 1)

Summary of building structure evaluation

Evaluator Tokyo Marine & Nichido Risk Consulting Co., Ltd.

Anticipated acquisition date (Note 2)

March 8, 2018 Evaluation date

November 23, 2016

Anticipated acquisition price 3,025 million yen

Immediate repair cost

0 yen

Appraisal value 3,500 million yen Short-term repair cost

0 yen

Appraiser The Tanizawa Sogo Appraisal Co., Ltd.

Long-term repair cost

192,435,000 yen

Date of trust beneficiary rights set

March 21, 2017 Repair cost for the forthcoming 12 years (annualized average)

16,036,000 yen Trustee

Sumitomo Mitsui Trust Bank, Limited

Anticipated trust period end March 31, 2028

Location (address) 10-34, Shibatani 1-chome, Suminoe-ku, Osaka-shi, Osaka, Japan., etc. Land area 35,386.00 m2

Building structure / stories

Main building:6-story steel structure with alloy plated steel sheet roof Annex 1:1-story steel structure with alloy plated steel sheet roof Annex 2:1-story steel structure with alloy plated steel sheet roof

Zoning Restricted industrial area FAR/building-to-land ratio 200%/60%

Type of Possession Ownership

Earthquake PML 4.8% Completion

March 31, 2006

Collateral conditions

None

Gross floor area

51,846.21 m2

Type of building

Main building:Warehouse and office Annex 1:Garbage storage Annex 2:Guard office

Special notes • Servitude is established for part of the subject land (3,128.38 m2) for the purpose of passing through the relevant land. .

(Note 1) IIF acquired a 75% co-ownership interest in this property (acquisition price: 9,075 million yen) on March 21, 2017, and will acquire the remaining 25% co-ownership interest in this property after this offering.

(Note 2) “Anticipated acquisition date” is the delivery date with regard to the property expected as of today.

(2) Description of Leases Relating to Anticipated Acquisitions

Tenant(s) Number

of tenant(s)

Total leased area

(occupancy rate)

Annual rent (excluding

consumption tax)

Period of contract Deposit

Toshiba Logistics Corporation

1 52,201.30 m2

(100%)

Not disclosed

(Note)

20 years (from March 31, 2006 until March 30, 2026)

Not disclosed

(Note)

16

Note: This press release is intended as general information for the press regarding IIF’s acquisition and lease of real estate and trust beneficiary interests in real estate in Japan, and has not been prepared for the purpose of solicitation of investment.

Revision of rent or termination during the lease period

Contract Type: Fixed-term leasehold Contract Renewal and Revision: • Rent may be revised upon consultation, in consideration of economic conditions, etc. • Rent may be revised every three years upon consultation after ten years have passed since the commencement date

of the lease period. • The lessee may not apply for any mid-term termination for ten years since the commencement date of the lease

period and may cancel the agreement on one year’s written notice after ten years have passed. Other: • None (Note) IIF has not obtained the necessary permission from the lessee to disclose this information.

(3) Reasons for the Acquisition

■Acquisition Highlights • Acquired logistics facility in favorable locations in the Osaka waterfront area, which is close to

both Osaka city center and the industrial area, and provides good traffic access through expressways and railways.

■Long-term Usability (Likelihood of Long-term Use by Current Tenant) • High-degree of continuity backed by the long-term contract of 20 years (from March 31, 2006 until

March 30, 2026) • Hub for logistics in western Japan, functioning a role as a warehouse of home appliances

■Versatility (Versatility as a Real Estate Asset)

• Advantageous location for both land and sea transportation: it is approximately 2.3km from the closest expressway interchange and approximately 5km from Osaka Nanko Container Wharf, located in an area designated as a restricted industrial zone in which 24-hour operations are allowed

• Sought after large-scale, functional logistics facility with strong market competitiveness <Location>

• Distribution hub located in an area adjacent to Osaka City, the center of consumption in the Kansai area

• Capability to distribute not only to Central Osaka but also to wider Kansai area • Location with good transportation • No problem with securing workforce for the work in the facility • A restricted industrial zone which allows 24-hour operations

<Facilities>

• Two exits and truck berths on the east, west and north faces on the first floor • Floor plan focusing on distribution efficiency • Two freight elevators and 10 vertical conveyers, and effective ceiling height of about 6 m • Floor loading capabilities of about 1.5 t/m2

17

Note: This press release is intended as general information for the press regarding IIF’s acquisition and lease of real estate and trust beneficiary interests in real estate in Japan, and has not been prepared for the purpose of solicitation of investment.

18

Note: This press release is intended as general information for the press regarding IIF’s acquisition and lease of real estate and trust beneficiary interests in real estate in Japan, and has not been prepared for the purpose of solicitation of investment.

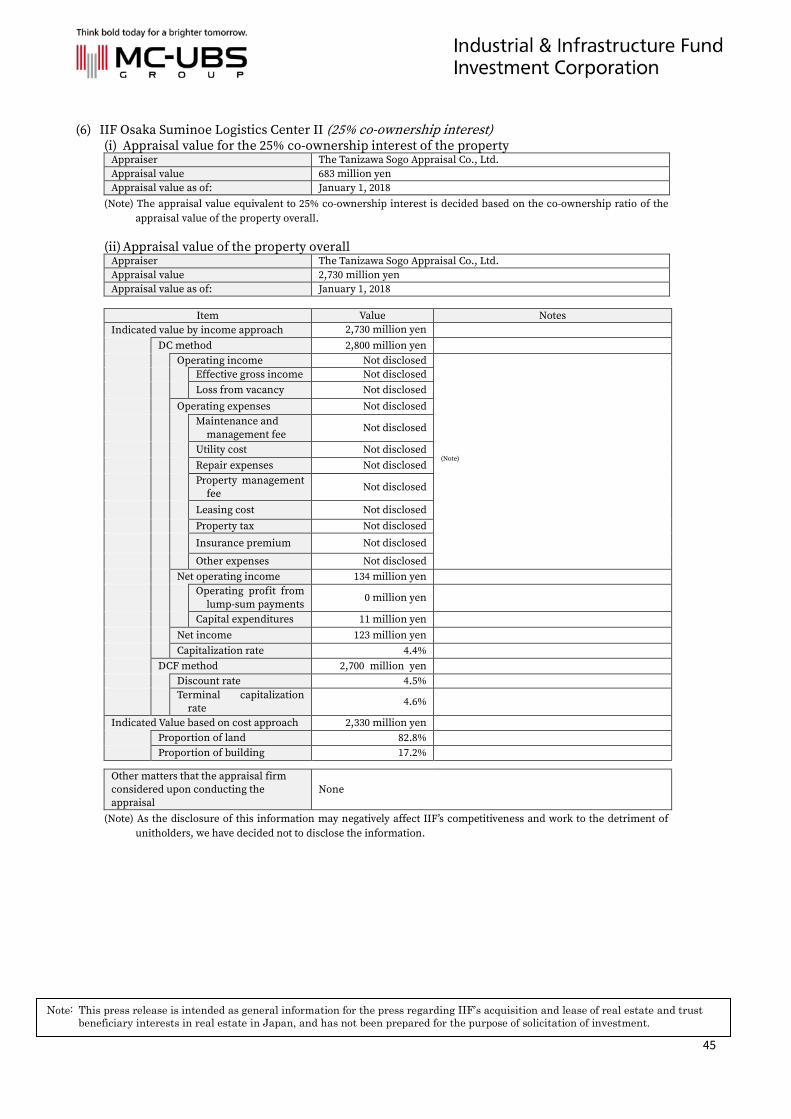

【IIF Osaka Suminoe Logistics Center II (25% co-ownership interest)】

(1) Summary of Property

Type of asset Trust beneficiary right in real estate (Note 1)

Summary of building structure evaluation

Evaluator Tokyo Marine & Nichido Risk Consulting Co., Ltd.

Anticipated acquisition date (Note 2)

March 8, 2018 Evaluation date

November 23, 2016

Anticipated acquisition price 635 million yen

Immediate repair cost

0 yen

Appraisal value 683 million yen Short-term repair cost

0 yen

Appraiser The Tanizawa Sogo Appraisal Co., Ltd.

Long-term repair cost

130,921,000 yen

Date of trust beneficiary rights set

March 21, 2017 Repair cost for the forthcoming 12 years (annualized average)

10,910,000 yen Trustee

Sumitomo Mitsui Trust Bank, Limited

Anticipated trust period end March 31, 2028

Location (address) 10-20, Shibatani 1-chome, Suminoe-ku, Osaka-shi, Osaka, Japan., etc. Land area 7,588.47 m2

Building structure / stories

5-story steel structure with galvanized steel sheet roof

Zoning Restricted industrial area FAR/building-to-land ratio 200%/60%

Type of Possession Ownership

Earthquake PML 3.9% Completion

July 10, 1991

Collateral conditions

None

Gross floor area

12,166.17 m2

Type of building Warehouse and office

Special notes None

(Note 1) IIF acquired a 75% co-ownership interest in this property (acquisition price: 1,905 million yen) on March 21, 2017, and will acquire the remaining 25% co-ownership interest in this property after this offering.

(Note 2) “Anticipated acquisition date” is the delivery date with regard to the property expected as of today.

(2) Description of Leases Relating to Anticipated Acquisitions

Tenant(s) Number

of tenant(s)

Total leased area

(occupancy rate)

Annual rent (excluding

consumption tax)

Period of contract Deposit

Toshiba Logistics Corporation

1 12,299.76 m2

(100%)

Not disclosed

(Note)

1 year (from September 1, 2017

until August 31, 2018)

Not disclosed

(Note)

19

Note: This press release is intended as general information for the press regarding IIF’s acquisition and lease of real estate and trust beneficiary interests in real estate in Japan, and has not been prepared for the purpose of solicitation of investment.

Revision of rent or termination during the lease period

Contract Type: Other type of building lease (futsu tatemono chintaishaku keiyaku) Contract Renewal and Revision • Rent shall not be revised during the lease period. • However, the rent may be revised upon consultation between the lessor and the lessee during the lease period if it

is expressly considered that the rent is not at a proper level because of tax revisions with regard to the property and the subject land and other increase or decrease in public dues, comparisons with rents of similar properties in the neighborhood and rapid changes in economic conditions, etc.

• The lease agreement will be automatically renewed for one year period unless otherwise either party has manifested a different intention.

Other: • None (Note) IIF has not obtained the necessary permission from the lessee to disclose this information.

(3) Reasons for the Acquisition

■Acquisition Highlights • Acquired logistics facility in favorable locations in the Osaka waterfront area, which is close to

both Osaka city center and the industrial area, and provides good traffic access through expressways and railways

■Long-term Usability (Likelihood of Long-term Use by Current Tenant)

• Hub for both domestic transportation and export, functioning as a warehouse of semiconductor products

■Versatility (Versatility as a Real Estate Asset)

<Location> • Advantageous location for both land and sea transportation: it is approximately 2.1km from the

closest expressway interchange and approximately 5km from Osaka Nanko Container Wharf, located in an area designated as a restricted industrial zone in which 24-hour operations are allowed

• Location within walking distance from Kitakagaya Station of the Osaka Municipal Subway Yotsubashi Line that is surrounded by residential area, which allows the tenant to secure workforce

• Located in an area adjacent to Osaka City, the center of consumption in the Kansai area • Capability to distribute not only to Central Osaka but also to wider Kansai area

<Facilities>

• One exit • Truck berth on the south face on the 1st floor • 1 freight elevator and 3 vertical conveyers • Effective ceiling height of about 6 m • Floor loading capacity of 2.0 t/m2 on the 1st floor, 1.0 t/m2 on the 2nd floor through 4th floor • Standard type as logistics warehouse

20

Note: This press release is intended as general information for the press regarding IIF’s acquisition and lease of real estate and trust beneficiary interests in real estate in Japan, and has not been prepared for the purpose of solicitation of investment.

21

Note: This press release is intended as general information for the press regarding IIF’s acquisition and lease of real estate and trust beneficiary interests in real estate in Japan, and has not been prepared for the purpose of solicitation of investment.

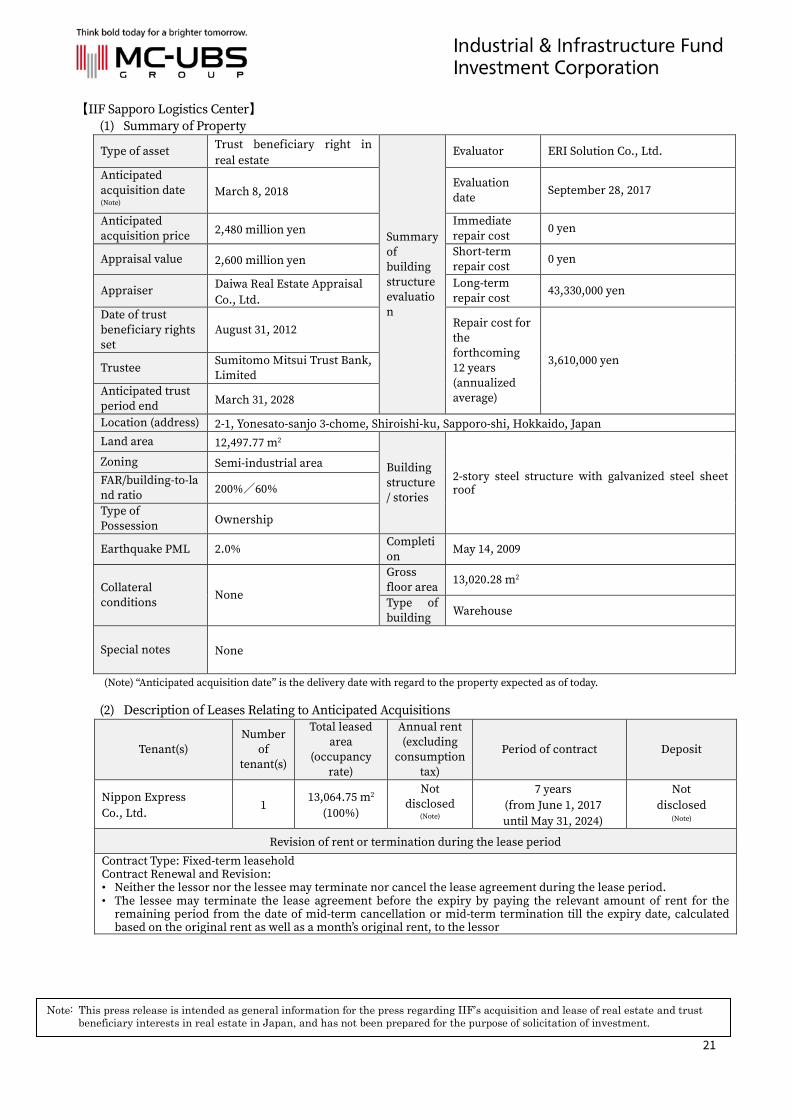

【IIF Sapporo Logistics Center】 (1) Summary of Property

Type of asset Trust beneficiary right in real estate

Summary of building structure evaluation

Evaluator ERI Solution Co., Ltd.

Anticipated acquisition date (Note)

March 8, 2018 Evaluation date

September 28, 2017

Anticipated acquisition price 2,480 million yen

Immediate repair cost

0 yen

Appraisal value 2,600 million yen Short-term repair cost

0 yen

Appraiser Daiwa Real Estate Appraisal Co., Ltd.

Long-term repair cost

43,330,000 yen

Date of trust beneficiary rights set

August 31, 2012 Repair cost for the forthcoming 12 years (annualized average)

3,610,000 yen Trustee

Sumitomo Mitsui Trust Bank, Limited

Anticipated trust period end March 31, 2028

Location (address) 2-1, Yonesato-sanjo 3-chome, Shiroishi-ku, Sapporo-shi, Hokkaido, Japan Land area 12,497.77 m2

Building structure / stories

2-story steel structure with galvanized steel sheet roof

Zoning Semi-industrial area FAR/building-to-land ratio 200%/60%

Type of Possession Ownership

Earthquake PML 2.0% Completion

May 14, 2009

Collateral conditions

None

Gross floor area

13,020.28 m2

Type of building Warehouse

Special notes None

(Note) “Anticipated acquisition date” is the delivery date with regard to the property expected as of today.

(2) Description of Leases Relating to Anticipated Acquisitions

Tenant(s) Number

of tenant(s)

Total leased area

(occupancy rate)

Annual rent (excluding

consumption tax)

Period of contract Deposit

Nippon Express Co., Ltd.

1 13,064.75 m2

(100%)

Not disclosed

(Note)

7 years (from June 1, 2017 until May 31, 2024)

Not disclosed

(Note)

Revision of rent or termination during the lease period

Contract Type: Fixed-term leasehold Contract Renewal and Revision: • Neither the lessor nor the lessee may terminate nor cancel the lease agreement during the lease period. • The lessee may terminate the lease agreement before the expiry by paying the relevant amount of rent for the

remaining period from the date of mid-term cancellation or mid-term termination till the expiry date, calculated based on the original rent as well as a month’s original rent, to the lessor

22

Note: This press release is intended as general information for the press regarding IIF’s acquisition and lease of real estate and trust beneficiary interests in real estate in Japan, and has not been prepared for the purpose of solicitation of investment.

• The lessor, only when lessee agrees, can terminate the contract by paying an amount equivalent to 6 months rent. • Rent may be revised upon consultation due to major fluctuations in economic conditions and rent of properties in

the neighborhood. Others: • None (Note) IIF has not obtained the necessary permission from the lessee to disclose this information.

(3) Reasons for the Acquisition

■Long-term Usability (Likelihood of Long-term Use by Current Tenant) • Important distribution base of major beverage manufacture group covering Sapporo city and

Hokkaido area. • Concluded a long-term stable fixed-term lease contract for a period of 7 years.

■Versatility (Versatility as a Real Estate Asset)

<Location> • Located approximately 8 km (20 mins by car) from Sapporo city, the largest consumption area in

Hokkaido, good access to the city center and logistics hubs of the region. • Center point for all transportation (air and sea). Located near Hokkaido Expressway Sapporo IC,

allowing good access to Tomakomai Port and New Chitose Airport.

<Facilities> • Parking lots for car commuters. • Located in manufacturing and logistics concentrated area, allowing 24 hours operation.

23

Note: This press release is intended as general information for the press regarding IIF’s acquisition and lease of real estate and trust beneficiary interests in real estate in Japan, and has not been prepared for the purpose of solicitation of investment.

【IIF Hitachinaka Port Logistics Center (land with leasehold interest)】

(1) Summary of Property Type of asset Real estate

Summary of building structure evaluation

Evaluator - Anticipated acquisition date (Note)

March 9, 2018 Evaluation date

-

Anticipated acquisition price 1,145 million yen

Immediate repair cost

-

Appraisal value 1,210 million yen Short-term repair cost

-

Appraiser Daiwa Real Estate Appraisal Co., Ltd.

Long-term repair cost

-

Date of trust beneficiary rights set

- Repair cost for the forthcoming 12 years (annualized average)

- Trustee - Anticipated trust period end -

Location (address) 768-42, Terunuma aza nagisa, Tokai-mura oaza, Naka-gun, Ibaraki, Japan., etc. Land area 20,000.00 m2

Building structure / stories

-

Zoning Semi-industrial area FAR/building-to-land ratio 200%/60%

Type of Possession Ownership

Earthquake PML - Completion

-

Collateral conditions

None

Gross floor area

-

Type of building -

Special notes None

(Note) “Anticipated acquisition date” is the delivery date with regard to the property expected as of today.

(2) Description of Leases Relating to Anticipated Acquisitions

Tenant(s) Number

of tenant(s)

Total leased area

(occupancy rate)

Annual rent (excluding

consumption tax)

Period of contract Deposit

Aono Sangyo Corporation

1 20,000.00 m2

(100%)

Not disclosed

(Note)

30 years (from September 22, 2017 until September 20, 2047)

Not disclosed

(Note)

Revision of rent or termination during the lease period

Contract Type: Fixed-term leasehold for business purposes Contract Renewal and Revision: • The rent shall not be revised in principle. However, the lessor or the lessee may request an increase or decrease of

rent if rent is significantly apart from a reasonable range due to major fluctuations in economic conditions, public dues and rent of properties in the neighborhood.

• The agreement cannot be terminated during the contract period in principle. However, it can be terminated during

24

Note: This press release is intended as general information for the press regarding IIF’s acquisition and lease of real estate and trust beneficiary interests in real estate in Japan, and has not been prepared for the purpose of solicitation of investment.

the term when the lessee finds a third party who wishes to rent instead of the lessee and conclude a new fixed-term business lease contract that satisfies the lessor.

Other: • None (Note) IIF has not obtained the necessary permission from the lessee to disclose this information.

25

Note: This press release is intended as general information for the press regarding IIF’s acquisition and lease of real estate and trust beneficiary interests in real estate in Japan, and has not been prepared for the purpose of solicitation of investment.

(3) Reasons for the Acquisition

■Acquisition Highlights <Privately negotiated deal>

• Long-term fixed-term leasehold for business purposes contract for the land of warehouse which plays an important role by storing imported rice and emergency rice stocks under the policy of Japanese government

• Located in a versatile area, situated within Hitachinaka port district of Ibaraki Port, which is the gateway to North Kanto and the base of the companies for export industries, such as Hitachi Construction Machinery Co., Ltd. and Komatsu Ltd., etc.

■Long-term Usability (Likelihood of Long-term Use by Current Tenant) • Long term contract for a period of 30 years (non-cancellable) • Available for broad use demand, located in Hitachinaka port district of Ibaraki Port and used for

storing imported rice including government’s emergency rice stocks, soybeans produced in Ibaraki and other food.

• Providing a stable and sustainable supply of rice by importing government’s minimum access rice (Note) and by storing government’s emergency rice stocks in a lean year, etc. (Note) “Minimum access rice” refers to imported rice that minimum import volume is agreed in 1993 at the

Uruguay Round negotiation for General Agreement on Tariffs and Trade (GATT).

■Versatility (Versatility as a Real Estate Asset)

<Location> • Located in Hitachinaka port district of Ibaraki Port designated as an important port, and

warehouse, distribution/process facilities, and waste disposal facilities can be constructed in the harbor/commercial port area of the district.

• Approximately 3 km from Hitachinaka Port IC of Hitachinaka Toll Road, easy access to north Kanto.

• With the whole line opening of the Kita-Kanto Expressway and opening of all sections of Metropolitan Inter-city Expressway within Ibaraki (Feb. 2017), role as a gateway to north Kanto can be expected.

26

Note: This press release is intended as general information for the press regarding IIF’s acquisition and lease of real estate and trust beneficiary interests in real estate in Japan, and has not been prepared for the purpose of solicitation of investment.

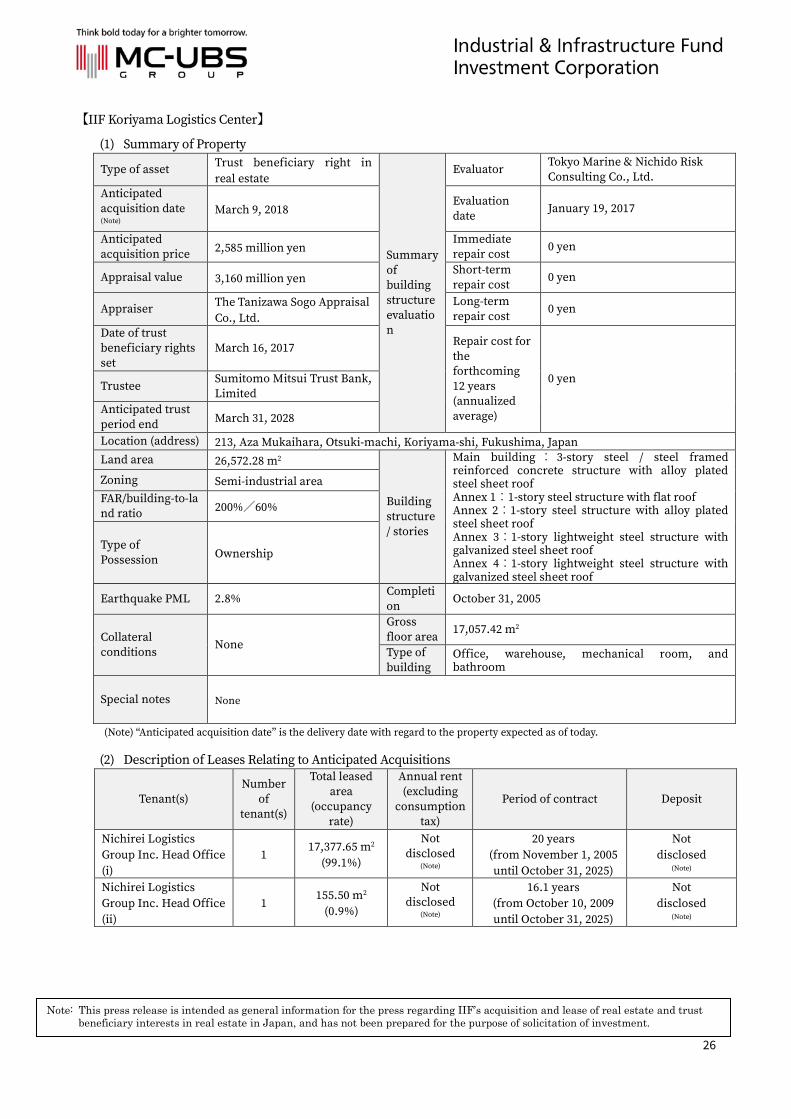

【IIF Koriyama Logistics Center】

(1) Summary of Property

Type of asset Trust beneficiary right in real estate

Summary of building structure evaluation

Evaluator Tokyo Marine & Nichido Risk Consulting Co., Ltd.

Anticipated acquisition date (Note)

March 9, 2018 Evaluation date

January 19, 2017

Anticipated acquisition price 2,585 million yen

Immediate repair cost

0 yen

Appraisal value 3,160 million yen Short-term repair cost

0 yen

Appraiser The Tanizawa Sogo Appraisal Co., Ltd.

Long-term repair cost

0 yen

Date of trust beneficiary rights set

March 16, 2017 Repair cost for the forthcoming 12 years (annualized average)

0 yen Trustee

Sumitomo Mitsui Trust Bank, Limited

Anticipated trust period end March 31, 2028

Location (address) 213, Aza Mukaihara, Otsuki-machi, Koriyama-shi, Fukushima, Japan Land area 26,572.28 m2

Building structure / stories

Main building : 3-story steel / steel framed reinforced concrete structure with alloy plated steel sheet roof Annex 1:1-story steel structure with flat roof Annex 2:1-story steel structure with alloy plated steel sheet roof Annex 3:1-story lightweight steel structure with galvanized steel sheet roof Annex 4:1-story lightweight steel structure with galvanized steel sheet roof

Zoning Semi-industrial area FAR/building-to-land ratio 200%/60%

Type of Possession Ownership

Earthquake PML 2.8% Completion

October 31, 2005

Collateral conditions

None

Gross floor area

17,057.42 m2

Type of building

Office, warehouse, mechanical room, and bathroom

Special notes None

(Note) “Anticipated acquisition date” is the delivery date with regard to the property expected as of today.

(2) Description of Leases Relating to Anticipated Acquisitions

Tenant(s) Number

of tenant(s)

Total leased area

(occupancy rate)

Annual rent (excluding

consumption tax)

Period of contract Deposit

Nichirei Logistics Group Inc. Head Office (i)

1 17,377.65 m2

(99.1%)

Not disclosed

(Note)

20 years (from November 1, 2005 until October 31, 2025)

Not disclosed

(Note) Nichirei Logistics Group Inc. Head Office (ii)

1 155.50 m2

(0.9%)

Not disclosed

(Note)

16.1 years (from October 10, 2009 until October 31, 2025)

Not disclosed

(Note)

27

Note: This press release is intended as general information for the press regarding IIF’s acquisition and lease of real estate and trust beneficiary interests in real estate in Japan, and has not been prepared for the purpose of solicitation of investment.

Revision of rent or termination during the lease period

• Nichirei Logistics Group Inc. Head Office (i) Contract Type: Fixed-term leasehold Contract Renewal and Revision: • Lessor shall offer new rent revised according to changes in lessee’s expense such as changes in pubic dues. • The lessor and the lessee will revise rent every 5 years during the lease period, and the standards of the review shall

be defined in a separate memorandum between lessor and lessee. • Neither the lessor nor the lessee may terminate the lease agreement during the lease period. • Lessee submit a six months prior written proposal against the lessor giving the conditions of that (i) Lessee finds a

third party that lessor approves and a new lease agreement is entered into between the lessor and the third party, or (ii) if Lessee pays penalty for the remaining lease amount of unexpired lease period and returns the building to the lessor, and the lessor approves such proposal, contract may be terminated when the lessor agrees to this.

• Nichirei Logistics Group Inc. Head Office (ii) The same as above Others: • Nichirei Logistics Group Inc. Head Office (i) • The lessor and the lessee without counterparty’s consent, shall not transfer to a third party or pledge as collateral

its rights of this contract. The lessee shall not violate the lessor’s ownership of the building by giving use to a third party. Notwithstanding the above, lessor may for the purpose of liquidation of the real estate, transfer real estate and rights to SPC and real estate investment corporation. In this case, lessor shall give lessee three months prior written notice. Lessee may reject if the there is a rational reason such as transferee being a lessee’s competitor.

• Lessee shall bear the expenses of electricity, gas and water supply associated with the use of the building, light bulb replacement fee, utility fee due to increase in electric capacity etc. and other costs incurred due to the usage, maintenance and repair of the building.

• Nichirei Logistics Group Inc. Head Office (ii) The same as above (Note) IIF has not obtained the necessary permission from the lessee to disclose this information.

(3) Reasons for the Acquisition

■Long-term Usability (Likelihood of Long-term Use by Current Tenant) • Long term agreement for a period of 20 years (non-cancelable in general) with Nichirei Logistics

Group Inc. Head Office, the largest frozen-foods provider. • Located near headquarter of the largest supermarket operator in Tohoku area covering its stores

and its partner’s stores within Fukushima.

■Versatility (Versatility as a Real Estate Asset) <Location>

• Good location for wide area distribution; approximately 2km from Tohoku Expressway Koriyama South IC, approximately 2.5km from National Route 4.

• Located within an industrial park where Koriyama Regional Wholesale Market and food-related logistic facilities locate and allowed for 24-hour operation.

28

Note: This press release is intended as general information for the press regarding IIF’s acquisition and lease of real estate and trust beneficiary interests in real estate in Japan, and has not been prepared for the purpose of solicitation of investment.

【IIF Kobe Nishi Logistics Center (land with leasehold interest)】 (1) Summary of Property

Type of asset Trust beneficiary right in real estate

Summary of building structure evaluation

Evaluator -

Anticipated acquisition date (Note 1)

March 29, 2018 Evaluation date

-

Anticipated acquisition price 1,960 million yen

Immediate repair cost

-

Appraisal value 2,100 million yen Short-term repair cost

-

Appraiser The Tanizawa Sogo Appraisal Co., Ltd.

Long-term repair cost

-

Anticipated date of trust beneficiary rights set (Note 2)

March 29, 2018 Repair cost for the forthcoming 12 years (annualized average)

- Trustee (Note 2)

Sumitomo Mitsui Trust Bank, Limited

Anticipated trust period end (Note 2) March 31, 2028

Location (address) 10-4, Mitsugaoka 4-chome, Nishi-ku, Kobe-shi, Hyogo, Japan Land area 33,000.00 m2

Building structure / stories

-

Zoning Semi-industrial area FAR/building-to-land ratio 200%/60%

Type of Possession Ownership

Earthquake PML - Completion

-

Collateral conditions

None

Gross floor area

-

Type of building -

Special notes

• A surface right will be established for this property as follows: Purpose: tunnel facilities Scope: from 132 m to 141 m above the average sea level of Tokyo Bay Period of duration: from the date of establishment of the right to Kobe City’s termination of use of the tunnel facilities Land rent: free Special arrangements:

(i) Consultation with the Kobe City is required before any use of land at which a sectional surface right is established, and the user of such land shall give due consideration not to interfere with the Kobe City’s use of the tunnel facilities

(ii) If the trust beneficiary right holder damages the tunnel facilities for the reason attributable to itself, it shall be liable for the damages.

(iii) The trust beneficiary right holder shall agree not to remove the tunnel facilities even after Kobe City ends the use of these facilities.

(iv) If the trust beneficiary right holder disposes of the subject land and/or sells it to any third party in the future, it shall have such third party succeed the provisions (i) through (iii) as above.

Surface right holders: Kobe City • Kohnan Shoji Co., Ltd. (“seller”) has agreed with the Kobe City, the current owner of the land

portion of the property, to obtain written approval from the Kobe City if the seller transfers ownership, establishes superficies or other usufruct, establishes collaterals such as pledge or mortgages, establishes leasehold or establishes other rights of use within the 10-year period

29

Note: This press release is intended as general information for the press regarding IIF’s acquisition and lease of real estate and trust beneficiary interests in real estate in Japan, and has not been prepared for the purpose of solicitation of investment.

from the execution date of the purchase and sale agreement (February 9, 2018), and the trustee shall succeed such agreement from the seller. The seller will obtain such approval from the Kobe City for acquisition of the property.

• The seller has agreed with the Kobe City, the current owner of the land portion of the property, that if the seller breaches obligations under the purchase and sales agreement such as limitation of usage, within the 10-year period from the execution date of the purchase and sale agreement (February 9, 2018), the Kobe City shall exercise the right to buy back the subject land, and the trustee shall assume such agreement. However, after payment and transfer of the subject land pursuant to the agreement between Kobe City and the seller, this agreement is expected to lose effect before IIF acquires the subject property.

(Note 1) “Anticipated acquisition date” is the delivery date with regard to the property expected as of today. (Note 2) “Anticipated date of trust beneficiary right set”, “Trustee”, and “Anticipated trust period end” are the dates for setting the

real estate trust beneficiary right expected as of today.

(2) Description of Leases Relating to Anticipated Acquisitions

Tenant(s) Number

of tenant(s)

Total leased area

(occupancy rate)

Annual rent (excluding

consumption tax)

Period of contract Deposit

Kohnan Shoji Co., Ltd 1 33,000.00 m2

(100%) Not

disclosed(Note)

20 years (from March 29, 2018 until March 28, 2038)

Not disclosed(Note)

Revision of rent or termination during the lease period

Contract Type: Fixed-term leasehold for business purposes Contract Renewal and Revision: • Rent shall not be revised during the lease period. • In the event where economic conditions rapidly change, the lessor and the lessee shall consult regarding rent

revision. • The lessee may not apply for any mid-term termination for fifteen years since the commencement date of the lease

period and may cancel the agreement on two year’s notice after fifteen years have passed. Others: • None (Note) IIF has not obtained the necessary permission from the lessee to disclose this information.

(3) Reasons for the Acquisition

■Acquisition Highlights <Privately negotiated deal>

• Dual project with a mixture of our second PRE (Public Real Estate) proposal to Kobe City and CRE proposal for Kohnan Shoji Co., Ltd.

• Located in a good accessible area as a distribution base to a wide area. Scheduled to conclude a contract establishing fixed-term leasehold for business purposes of 20 years with the tenant (non-cancellation period of 17 years).

■Long-term Usability (Likelihood of Long-term Use by Current Tenant) • Located within Kobe Techno Logistics Park, which is an industrial complex in Kobe City Nishi-ku. • Important facility of Kohnan Shoji Co., Ltd. as a logistics center in western Japan, completed in

February 2005. • Sustainable for business use for 20 years (non-cancellation period of 17 years) under the terms

stipulated in the contract establishing fixed-term leasehold for business purposes.

30

Note: This press release is intended as general information for the press regarding IIF’s acquisition and lease of real estate and trust beneficiary interests in real estate in Japan, and has not been prepared for the purpose of solicitation of investment.

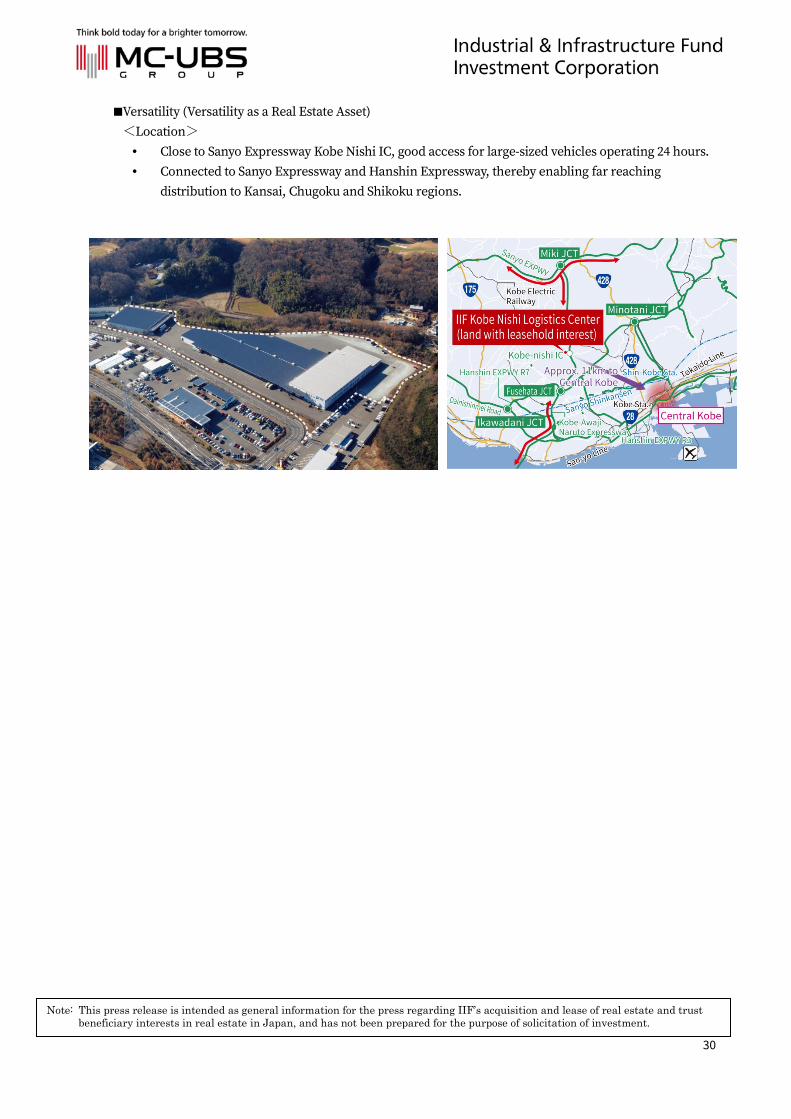

■Versatility (Versatility as a Real Estate Asset) <Location>

• Close to Sanyo Expressway Kobe Nishi IC, good access for large-sized vehicles operating 24 hours. • Connected to Sanyo Expressway and Hanshin Expressway, thereby enabling far reaching

distribution to Kansai, Chugoku and Shikoku regions.

31

Note: This press release is intended as general information for the press regarding IIF’s acquisition and lease of real estate and trust beneficiary interests in real estate in Japan, and has not been prepared for the purpose of solicitation of investment.

<Reference> Designer/Constructor/Confirmation and Inspection Organization for Anticipated Acquisitions

Property number

Property name Designer(Note) Structure designer(Note) Constructor(Note)

Confirmation and

Inspection Organization

(Note)

L-36 IIF Itabashi Logistics Center (40% co-ownership interest)

Nippon Steel Engineering Co., Ltd. First-Class Registered Architects Office

Nippon Steel Engineering Co., Ltd. First-Class Registered Architects Office

Nittoh Koei Co., Ltd. UHEC (Toshi-kyojyu Hyoka Center)

L-39 IIF Osaka Suminoe Logistics Center I (25% co-ownership interest)

Sumitomo Mitsui Construction Co., Ltd. First-Class Registered Architects Office

Sumitomo Mitsui Construction Co., Ltd. First-Class Registered Architects Office

Sumitomo Mitsui Construction Co., Ltd., Osaka Branch

Center of International Architectural Standard

L-40 IIF Osaka Suminoe Logistics Center II (25% co-ownership interest)

Makoto Sekkei Jimusho Makoto Sekkei Jimusho Toyo Construction Osaka-shi

L-42 IIF Sapporo Logistics Center

Sekisui House, Ltd., SapporoTokken Branch First-Class Registered Architects Office

Hokuei Kogyo K.K ELM Corporation Japan ERI Co., Ltd.

L-44 IIF Koriyama Logistics Center

Azusa Sekkei Co., Ltd. Azusa Sekkei Co., Ltd. Nishimatsu Construction Co., Ltd., Tohoku Branch

Japan ERI Co., Ltd.

(Note) Each name of the designer, structure designer, constructor, and confirmation and inspection organization above refers to the name at the time of obtainment of the certificate of inspection upon completion of the relevant property or trust property or when such property was a newly constructed building.

32

Note: This press release is intended as general information for the press regarding IIF’s acquisition and lease of real estate and trust beneficiary interests in real estate in Japan, and has not been prepared for the purpose of solicitation of investment.

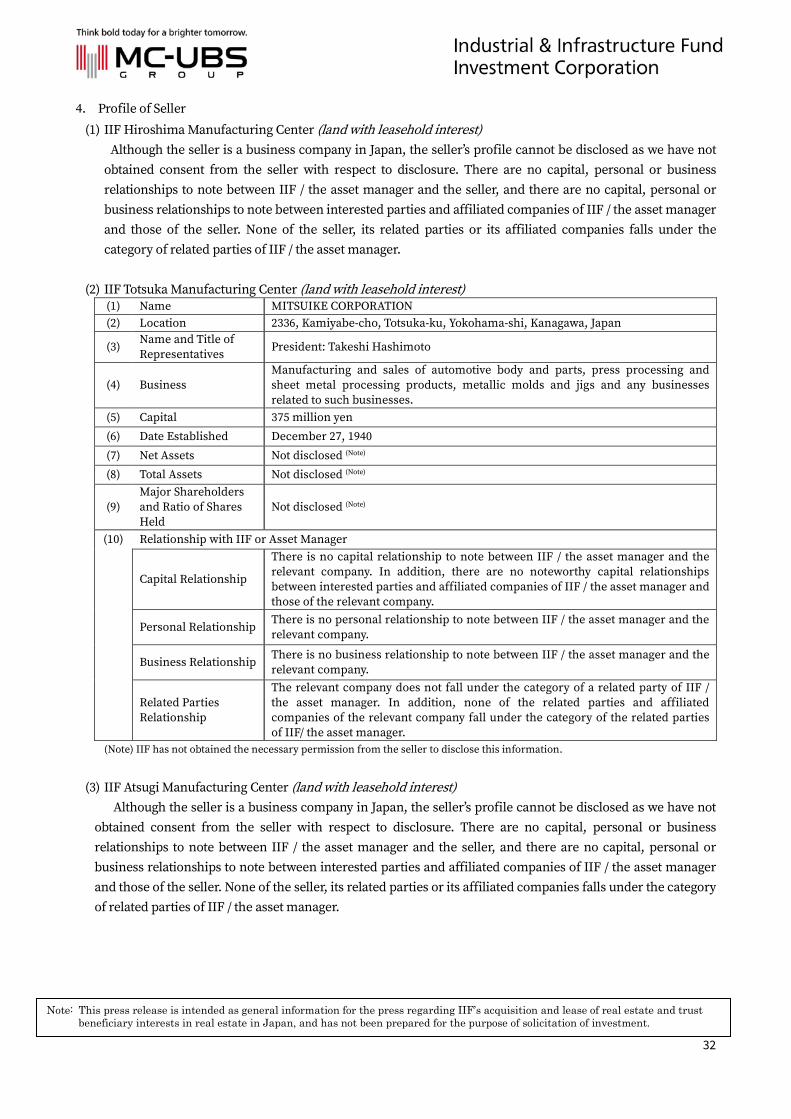

4. Profile of Seller

(1) IIF Hiroshima Manufacturing Center (land with leasehold interest) Although the seller is a business company in Japan, the seller’s profile cannot be disclosed as we have not

obtained consent from the seller with respect to disclosure. There are no capital, personal or business relationships to note between IIF / the asset manager and the seller, and there are no capital, personal or business relationships to note between interested parties and affiliated companies of IIF / the asset manager and those of the seller. None of the seller, its related parties or its affiliated companies falls under the category of related parties of IIF / the asset manager.

(2) IIF Totsuka Manufacturing Center (land with leasehold interest)

(1) Name MITSUIKE CORPORATION (2) Location 2336, Kamiyabe-cho, Totsuka-ku, Yokohama-shi, Kanagawa, Japan

(3) Name and Title of Representatives

President: Takeshi Hashimoto

(4) Business Manufacturing and sales of automotive body and parts, press processing and sheet metal processing products, metallic molds and jigs and any businesses related to such businesses.

(5) Capital 375 million yen

(6) Date Established December 27, 1940

(7) Net Assets Not disclosed (Note)

(8) Total Assets Not disclosed (Note)

(9) Major Shareholders and Ratio of Shares Held

Not disclosed (Note)

(10) Relationship with IIF or Asset Manager

Capital Relationship