IFRS in India - Its Status, Overview of Concepts and ... · PDF file• Project management...

96

IFRS in India – Its Status, Overview of Concepts and Impact in India Rakesh Agarwal Associate Director, PricewaterhouseCoopers E-mail : [email protected] Mobile : +91 9820273458 January 2011

Transcript of IFRS in India - Its Status, Overview of Concepts and ... · PDF file• Project management...

IFRS in India – Its Status, Overview of

Concepts and Impact in India

Rakesh Agarwal

Associate Director, PricewaterhouseCoopers

E-mail : [email protected]

Mobile : +91 9820273458 January 2011

ContentsApplicability of IFRS in India

Mapping IFRS and CIAS

Broad understanding of IFRS impact on India Inc.

Common Experiences (adjustments) from Indian GAAP to IFRS (refer annexure 2)

Essential of IFRS conversion approach

• Managing change

• Phased approach – Transition IFRS methodology

• Project management framework

• Project structure

• Centralised approach v/s decentralised approach

• Detailed Training program

• Key challenges - mitigation steps / management calls

Preparation of IFRS Financial Statements

Carve Outs in CIAS from IFRS

Impact – Indian Experience

Annexures

1 : Accounting concepts relatively new in India

2 : Common adjustments from Indian GAAP to IFRS

3 : Select IFRS tools & publications

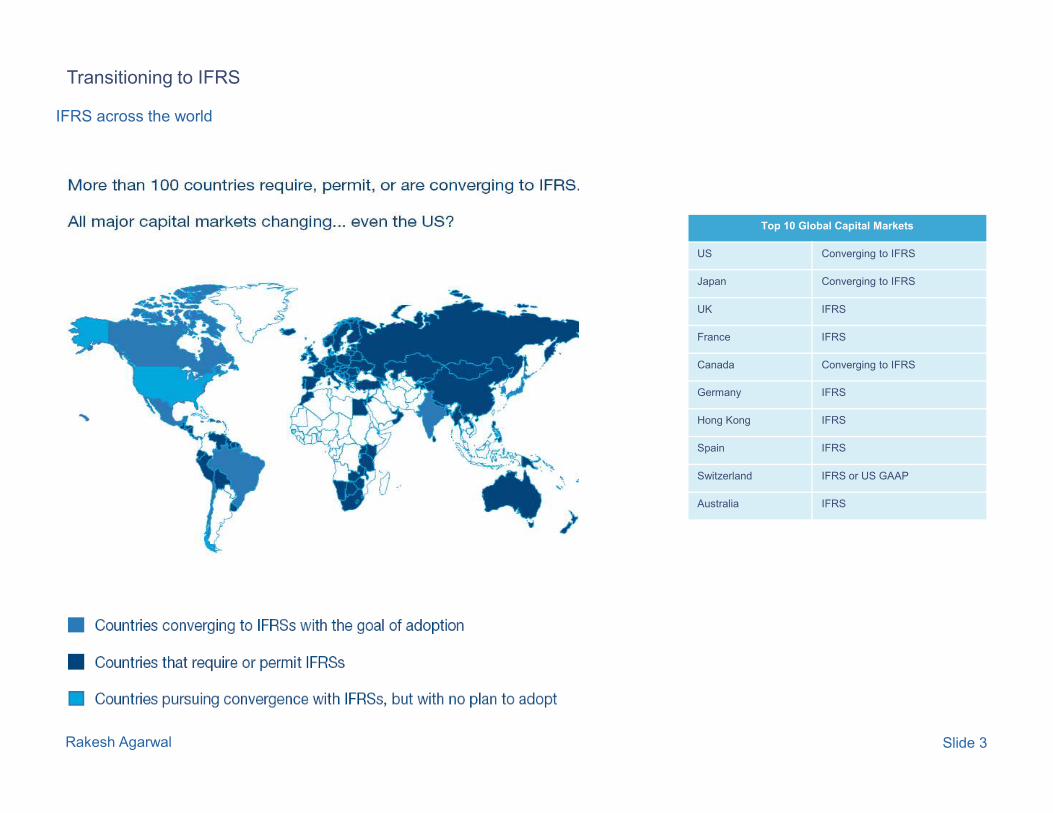

IFRS across the world

Top 10 Global Capital Markets

US Converging to IFRS

Japan Converging to IFRS

UK IFRS

France IFRS

Canada Converging to IFRS

Germany IFRS

Transitioning to IFRS

Slide 3Rakesh Agarwal

Hong Kong IFRS

Spain IFRS

Switzerland IFRS or US GAAP

Australia IFRS

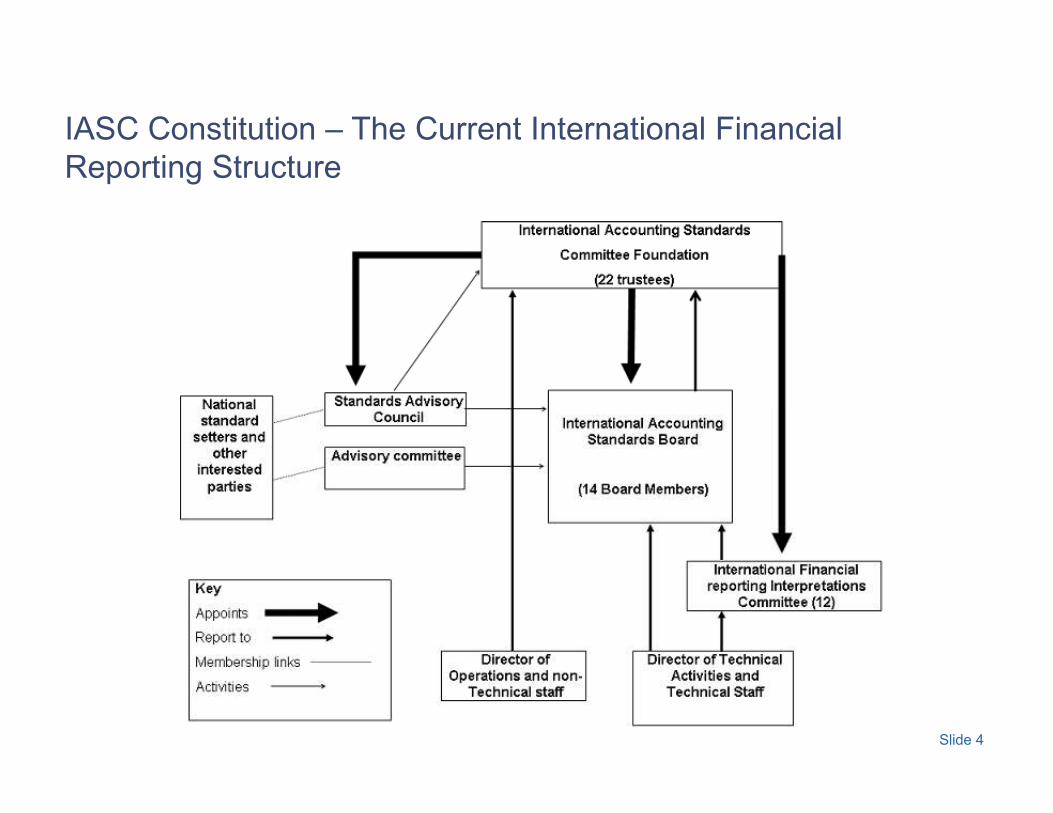

IASC Constitution – The Current International Financial

Reporting Structure

Slide 4

The Preface and The Framework

Preface to IFRS

1. Objectives

• A single set of high quality, enforceable global accounting standards

• Work with various national standard Setters for convergence

2. Scope and Authority of IFRS

• Designed for profit oriented enterprises

Slide 5Rakesh Agarwal

• General purpose financial statements

• Bold and plain type, have equal authority

3. Due Process

4. English Language

Framework for Preparation and Presentation of Financial Statements

1. Objectives of Financial Statements; includes cash flows

2. Underlying assumption

3. Qualitative characteristics of financial statements

4. Elements of financial statements, recognition and measurement

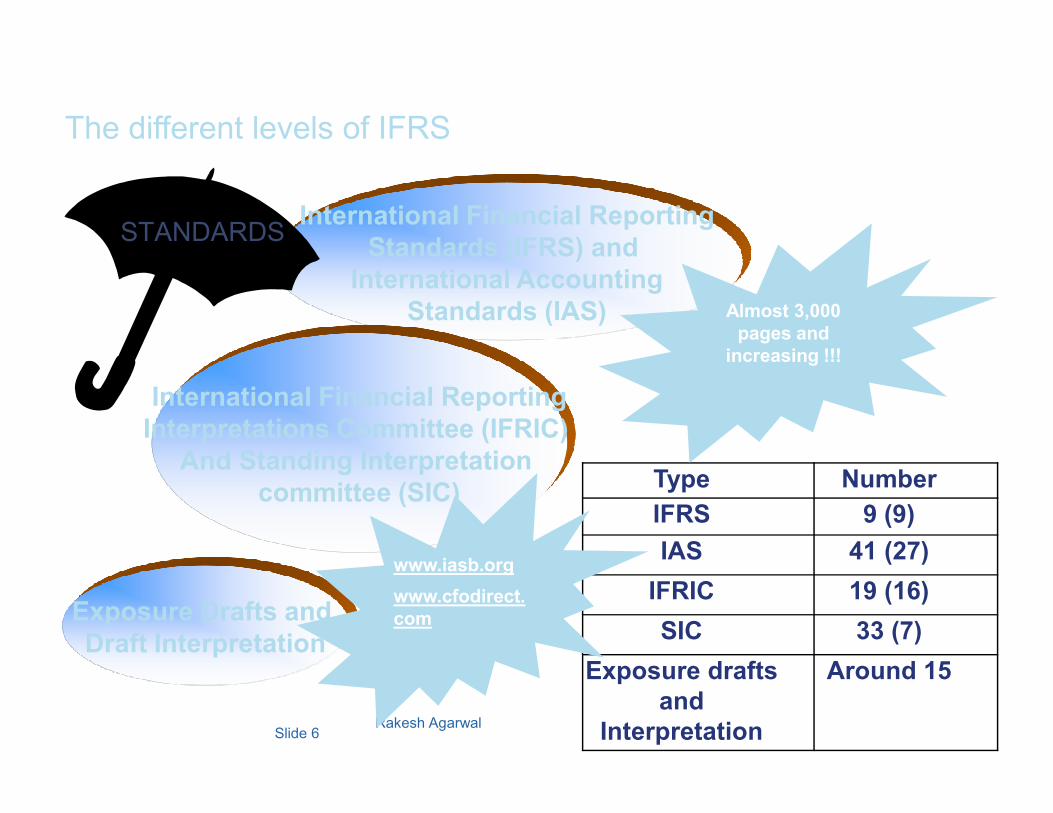

International Financial Reporting

Standards (IFRS) and

International Accounting

Standards (IAS)

International Financial Reporting

STANDARDS

Almost 3,000

pages and

increasing !!!

The different levels of IFRS

Slide 6Rakesh Agarwal

International Financial Reporting

Interpretations Committee (IFRIC)

And Standing Interpretation

committee (SIC)

Exposure Drafts and

Draft Interpretation

Type Number

IFRS 9 (9)

IAS 41 (27)

IFRIC 19 (16)

SIC 33 (7)

Exposure drafts

and

Interpretation

Around 15

www.iasb.org

www.cfodirect.

com

2011 2012 2013 2014• NSE - Nifty 50 companies,

• BSE - Sensex 30

companies,

• Companies whose shares

or other securities listed

• All insurance companies • Companies listed or not,

having a net worth between

Rs.500 crores and Rs.1000

crores [Note 1]

• Listed companies having a

net worth of less than

Rs.500 crores [Note 1]

• All scheduled commercial • Urban co-operative banks

Applicability of IFRS in IndiaOpening balance sheet as at April 1* using IFRS-converged accounting standards

IFRS in India – Its Status, Overview of Concepts and Impact in India

or other securities listed

outside India;

• Companies listed or not,

having a net worth in

excess of Rs. 1,000 crores

[Note 1]

• All scheduled commercial

banks

• Urban co-operative banks

having net worth between

Rs. 200 to Rs. 300 crores

• Urban co-operative banks

having a net worth in excess

of Rs. 300 crores

• NBFCs (all other Listed)

• NBFCs (other Unlisted)

having net worth between

Rs. 500 to Rs. 1000 crores• NBFCs - Nifty 50 or Sensex

30

• NBFCs listed or not, having a

net worth > Rs.1,000 crores

Note 1: Companies not covered in the above chart will apply ‘existing Indian accounting standards’ OR voluntarily opt to

apply the ‘IFRS-converged accounting standards’.

Slide 7

Std. No. Name of the standard

Corresponding to standards issued by

IASBWhether

significant

differences

between CIAS and

IFRSIAS/IFRS IFRIC SIC

CIAS 01 Presentation of financial statements IAS 1 No

CIAS 02 Inventories IAS 2 No

CIAS 03 Statement of Cash Flows IAS 7 No

CIAS 04 Events after the Reporting Period IAS 10 IFRIC 17 No

CIAS 05Accounting Policies, Changes in Accounting Estimates and

ErrorsIAS 8 No

CIAS 07 Construction Contracts IAS 11 IFRIC 12 No

CIAS 09 Revenue IAS 18IFRIC 13, 15,

18No

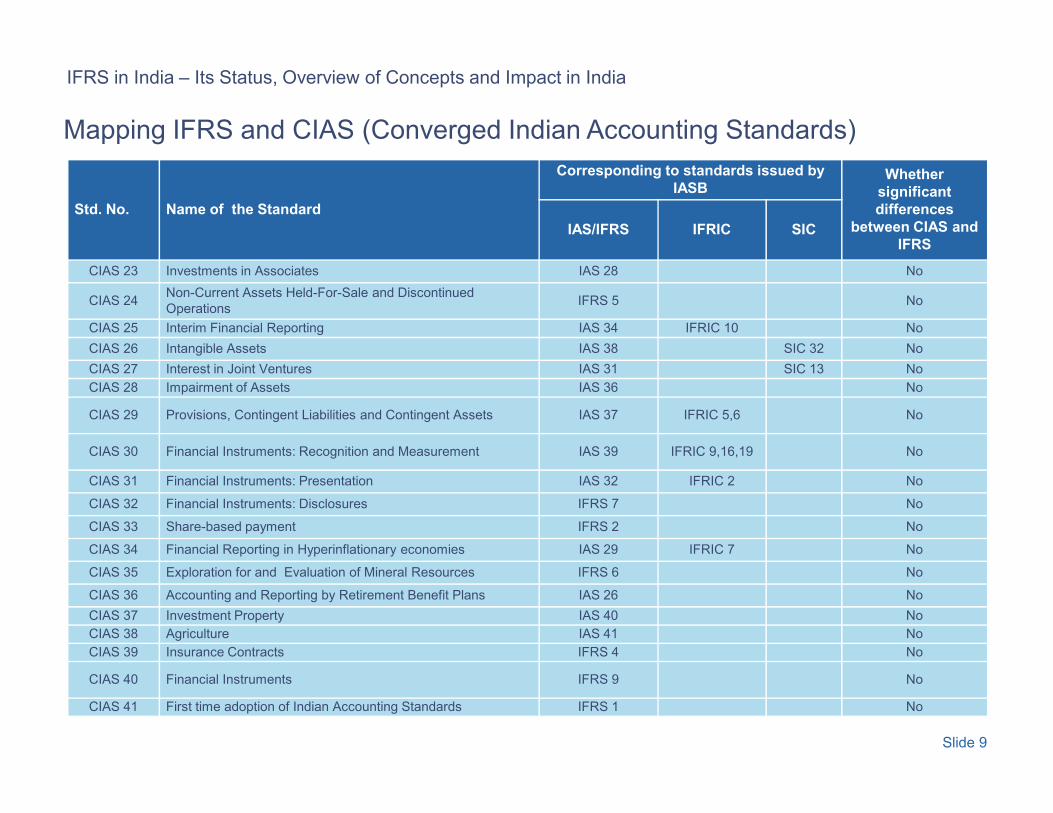

Mapping IFRS and CIAS (Converged Indian Accounting Standards)

IFRS in India – Its Status, Overview of Concepts and Impact in India

Slide 8

18

CIAS 10 Property, Plant and Equipment IAS 16 IFRIC 1 No

CIAS 11 The effects of changes in Foreign Exchange Rates IAS 21 No

CIAS 12Accounting for Government Grants and Disclosure of

Government AssistanceIAS 20 No

CIAS 14 Business Combinations IFRS 3 No

CIAS 15 Employee Benefits IAS 19 IFRIC 14 No

CIAS 16 Borrowing Costs IAS 23 No

CIAS 17 Operating Segments IFRS 8 No

CIAS 18 Related Party DisclosureIAS 24

No

CIAS 19 Leases IAS 17 IFRIC 4 SIC 15, 27 No

CIAS 20 Earnings Per Share IAS 33 No

CIAS 21 Consolidated and Separate Financial Statements IAS 27 No

CIAS 22 Income Taxes IAS 12 No

Std. No. Name of the Standard

Corresponding to standards issued by

IASBWhether

significant

differences

between CIAS and

IFRSIAS/IFRS IFRIC SIC

CIAS 23 Investments in Associates IAS 28 No

CIAS 24Non-Current Assets Held-For-Sale and Discontinued

OperationsIFRS 5 No

CIAS 25 Interim Financial Reporting IAS 34 IFRIC 10 No

CIAS 26 Intangible Assets IAS 38 SIC 32 No

CIAS 27 Interest in Joint Ventures IAS 31 SIC 13 No

CIAS 28 Impairment of Assets IAS 36 No

IFRS in India – Its Status, Overview of Concepts and Impact in India

Mapping IFRS and CIAS (Converged Indian Accounting Standards)

Slide 9

CIAS 29 Provisions, Contingent Liabilities and Contingent Assets IAS 37 IFRIC 5,6 No

CIAS 30 Financial Instruments: Recognition and Measurement IAS 39 IFRIC 9,16,19 No

CIAS 31 Financial Instruments: Presentation IAS 32 IFRIC 2 No

CIAS 32 Financial Instruments: Disclosures IFRS 7 No

CIAS 33 Share-based payment IFRS 2 No

CIAS 34 Financial Reporting in Hyperinflationary economies IAS 29 IFRIC 7 No

CIAS 35 Exploration for and Evaluation of Mineral Resources IFRS 6 No

CIAS 36 Accounting and Reporting by Retirement Benefit Plans IAS 26 No

CIAS 37 Investment Property IAS 40 No

CIAS 38 Agriculture IAS 41 No

CIAS 39 Insurance Contracts IFRS 4 No

CIAS 40 Financial Instruments IFRS 9 No

CIAS 41 First time adoption of Indian Accounting Standards IFRS 1 No

Broad understanding of IFRS impact on India Inc.

IFRS in India – Its Status, Overview of Concepts and Impact in India

Areas Impact

A Select Components of Financial Statements Net worth Net Income Disclosures Efforts

1Consolidation

(SIC 12, DT on outside basis)Medium – High Medium - High Low Medium

2

Business Combinations

(common control transactions, Fair value vs. Book value, Merger – Scope

exemption presumed)

Nil - Low Low Nil Low

Potential Impact of IFRS on consolidated financial statements of

ABC Limited for the Y.E. March 31, 2010

Rakesh Agarwal Slide 11

exemption presumed)

3Property, Plant and Equipment

Medium - High Medium - High Low High

4Share based payments

e.g. Fair value accounting vs. Book value.Nil-Low Low-Medium Nil High

5Financial Instruments

e.g. Forward contracts, IFRS 7 disclosureLow-Medium Medium High High

6Employee Benefits

e.g. Policy of actuarial gains and losses. VRS.Low Low Low Low

7Revenue Recognition

IFRIC 13, Multiple Elements, etc.Low Low Low Medium

(See sample list of applicable GAAP differences)

Areas Impact

A Select Components of Financial Statements Net worth Net Income Disclosures Efforts

8Taxes on Income

(B/S Approach, IFRS Adjustments, Defferred Tax on Outside basis etc.)Medium – High Medium – High Medium Medium

9Foreign Currency Transactions

(Functional Currency determination of foreign branches, Cost plus contracts)Low Low Low Medium

First Time Adoption

Potential Impact of IFRS on consolidated financial statements of

ABC Limited for the Y.E. March 31, 2010

IFRS in India – Its Status, Overview of Concepts and Impact in India

Rakesh Agarwal Slide 12

10

First Time Adoption

(Selecting exemptions and exceptions, 1) FV of Fixed Assets, 2) Business

Combinations and Mergers, 3) Actuarial Gains and Losses)

Medium – High Medium - High High High

11 Restructuring and Discontinued Operations Low-Medium Low-Medium Low Low

12EPS

(Impact of IFRS adjustments, Dilution option in subsidiary, if any.)Nil Nil Low Low

13Operating Segment

(MIS data vs. Audited Segmental information)Nil Nil High Low

14Presentation of Financial Statements

(Making policy choices of format and benchmarking, Fixed deposits)Nil Nil High High

15New Businesses/Transactions/ Others

(New Acquisitions, Dividend)Future Future Future Future

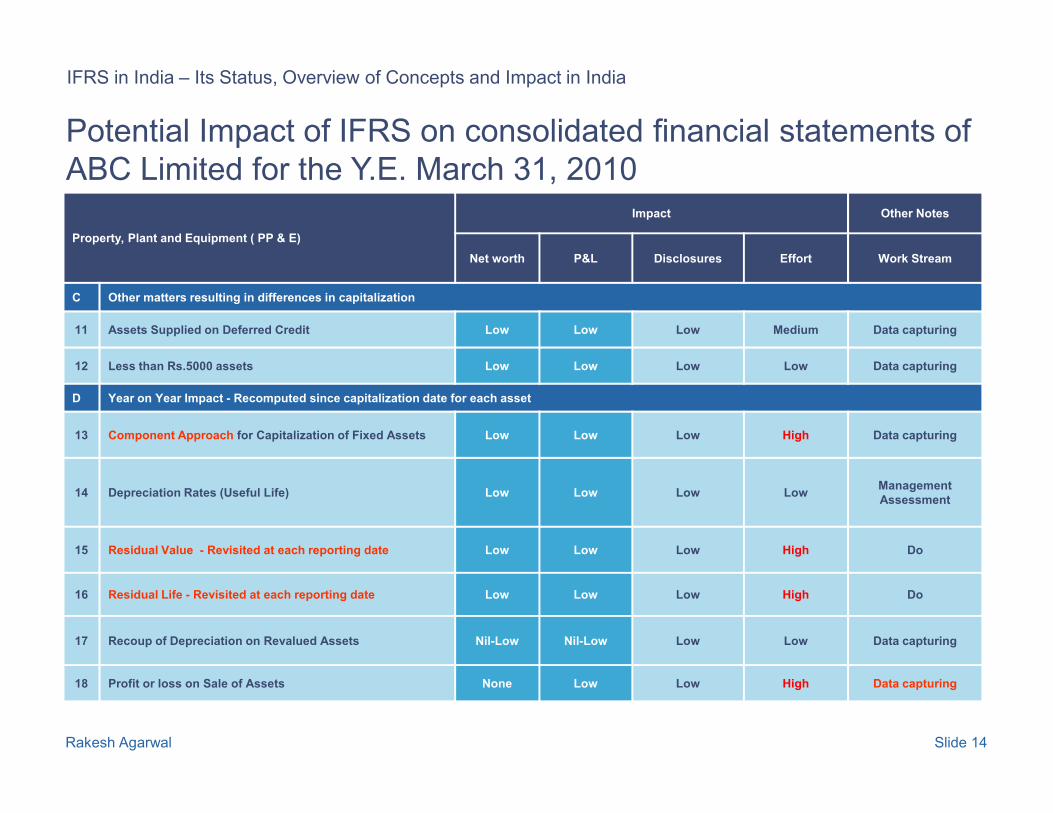

Property, Plant and Equipment ( PP & E)

Impact Other Notes

Net worth P&L Disclosures Effort Work Stream

A Significant areas

1 IFRS 1 - Deemed Fair Value, Event Driven Organisation High High Low High Policy Decision

2 Revaluation Model High High Medium High Policy Decision

3 Fair Value at time of Business Combinations Low Low Low Low Policy Decision

Potential Impact of IFRS on consolidated financial statements of

ABC Limited for the Y.E. March 31, 2010

IFRS in India – Its Status, Overview of Concepts and Impact in India

Rakesh Agarwal Slide 13

3 Fair Value at time of Business Combinations Low Low Low Low Policy Decision

4 Exchange of Assets Low Low Low LowIdentifying +

Valuation

B Differences in Indian Accounting Standards for earlier periods

5 Asset Retirement Obligation Nil – Low Nil - Low Low LowValuation +

Data capturing

6 Capitalisation of Borrowing Costs Low Low Low Low Data Capturing

7 Indirect expenditure during trial run Low Low Low Low Data Capturing

8IFRIC - 4; Capital leasing arrangement within Service

ContractsLow-High Low-High Low High

Renewal of

Contracts

9 Leased Assets acquired before April 1, 2000 Nil Nil Nil Low N.A.

10 Capitalization of Exchange Fluctuation Low Low Nil High Data capturing

Property, Plant and Equipment ( PP & E)

Impact Other Notes

Net worth P&L Disclosures Effort Work Stream

C Other matters resulting in differences in capitalization

11 Assets Supplied on Deferred Credit Low Low Low Medium Data capturing

12 Less than Rs.5000 assets Low Low Low Low Data capturing

D Year on Year Impact - Recomputed since capitalization date for each asset

Potential Impact of IFRS on consolidated financial statements of

ABC Limited for the Y.E. March 31, 2010

IFRS in India – Its Status, Overview of Concepts and Impact in India

Rakesh Agarwal Slide 14

13 Component Approach for Capitalization of Fixed Assets Low Low Low High Data capturing

14 Depreciation Rates (Useful Life) Low Low Low LowManagement

Assessment

15 Residual Value - Revisited at each reporting date Low Low Low High Do

16 Residual Life - Revisited at each reporting date Low Low Low High Do

17 Recoup of Depreciation on Revalued Assets Nil-Low Nil-Low Low Low Data capturing

18 Profit or loss on Sale of Assets None Low Low High Data capturing

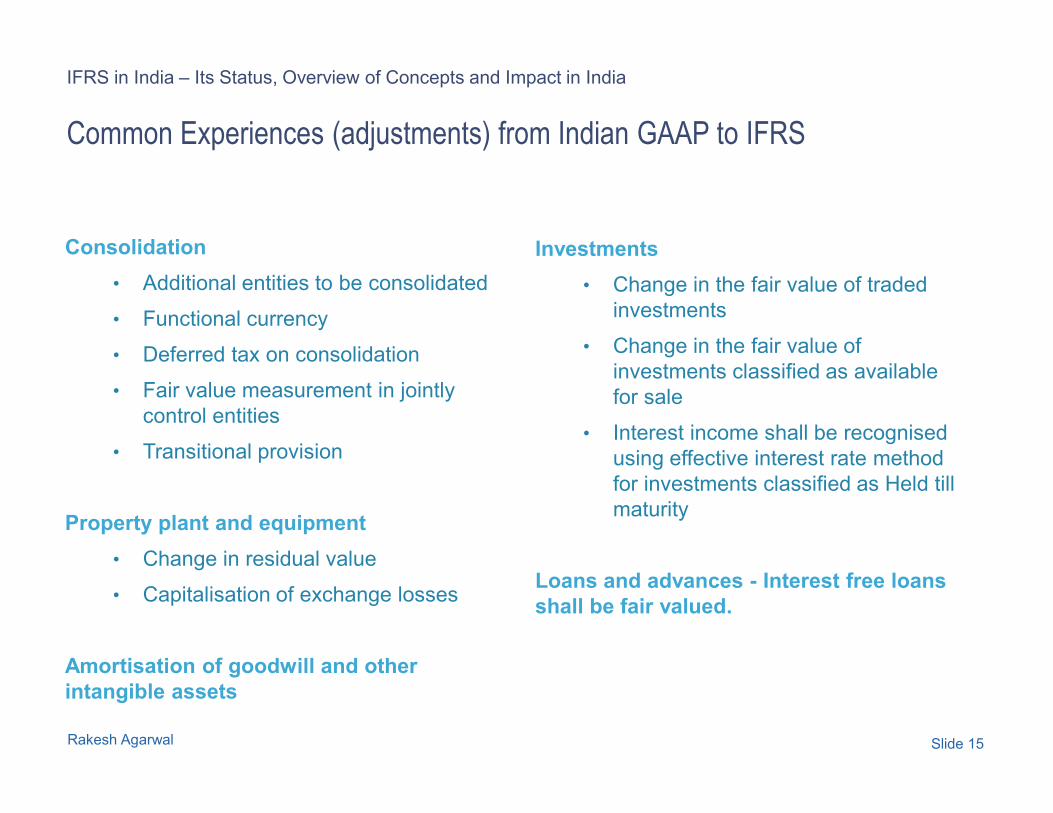

Consolidation

• Additional entities to be consolidated

• Functional currency

• Deferred tax on consolidation

• Fair value measurement in jointly

control entities

IFRS in India – Its Status, Overview of Concepts and Impact in India

Investments

• Change in the fair value of traded

investments

• Change in the fair value of

investments classified as available

for sale

Common Experiences (adjustments) from Indian GAAP to IFRS

Rakesh Agarwal Slide 15

control entities

• Transitional provision

Property plant and equipment

• Change in residual value

• Capitalisation of exchange losses

Amortisation of goodwill and other

intangible assets

for sale

• Interest income shall be recognised

using effective interest rate method

for investments classified as Held till

maturity

Loans and advances - Interest free loans

shall be fair valued.

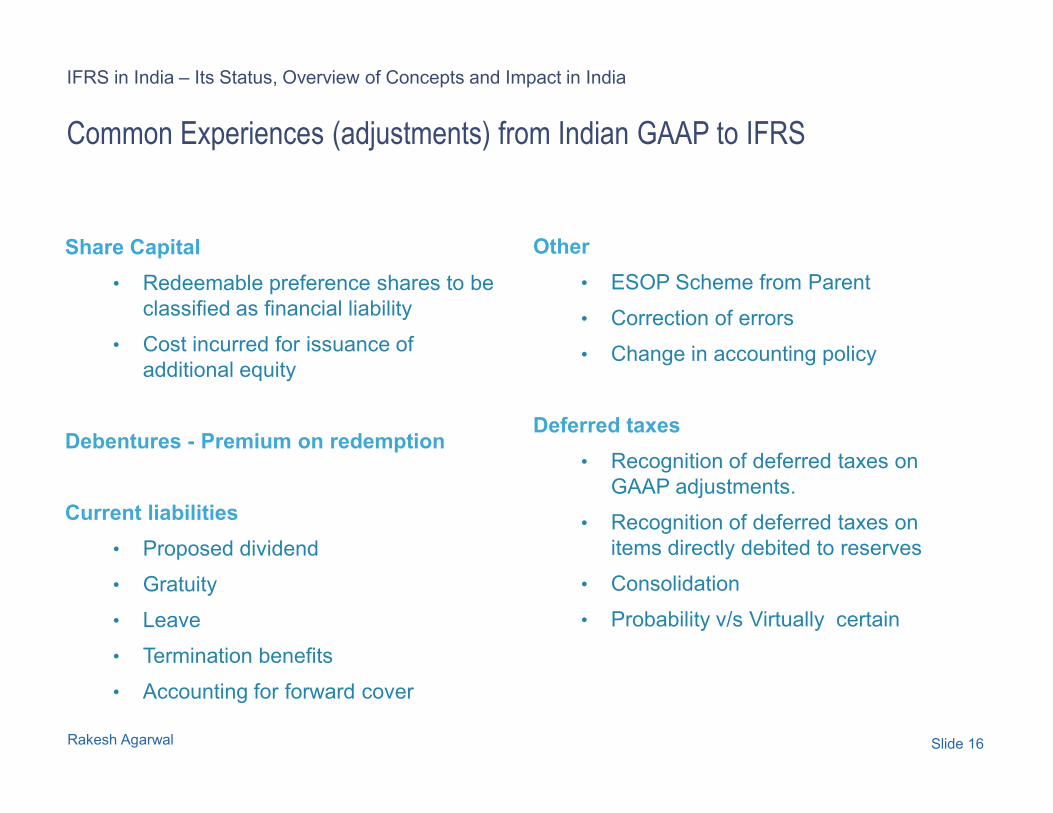

Share Capital

• Redeemable preference shares to be

classified as financial liability

• Cost incurred for issuance of

additional equity

IFRS in India – Its Status, Overview of Concepts and Impact in India

Other

• ESOP Scheme from Parent

• Correction of errors

• Change in accounting policy

Common Experiences (adjustments) from Indian GAAP to IFRS

Rakesh Agarwal Slide 16

Debentures - Premium on redemption

Current liabilities

• Proposed dividend

• Gratuity

• Leave

• Termination benefits

• Accounting for forward cover

Deferred taxes

• Recognition of deferred taxes on

GAAP adjustments.

• Recognition of deferred taxes on

items directly debited to reserves

• Consolidation

• Probability v/s Virtually certain

Essentials of IFRS

Conversion Approach

Essentials of IFRS Conversion Approach

IFRS in India – Its Status, Overview of Concepts and Impact in India

Rakesh Agarwal Slide 18

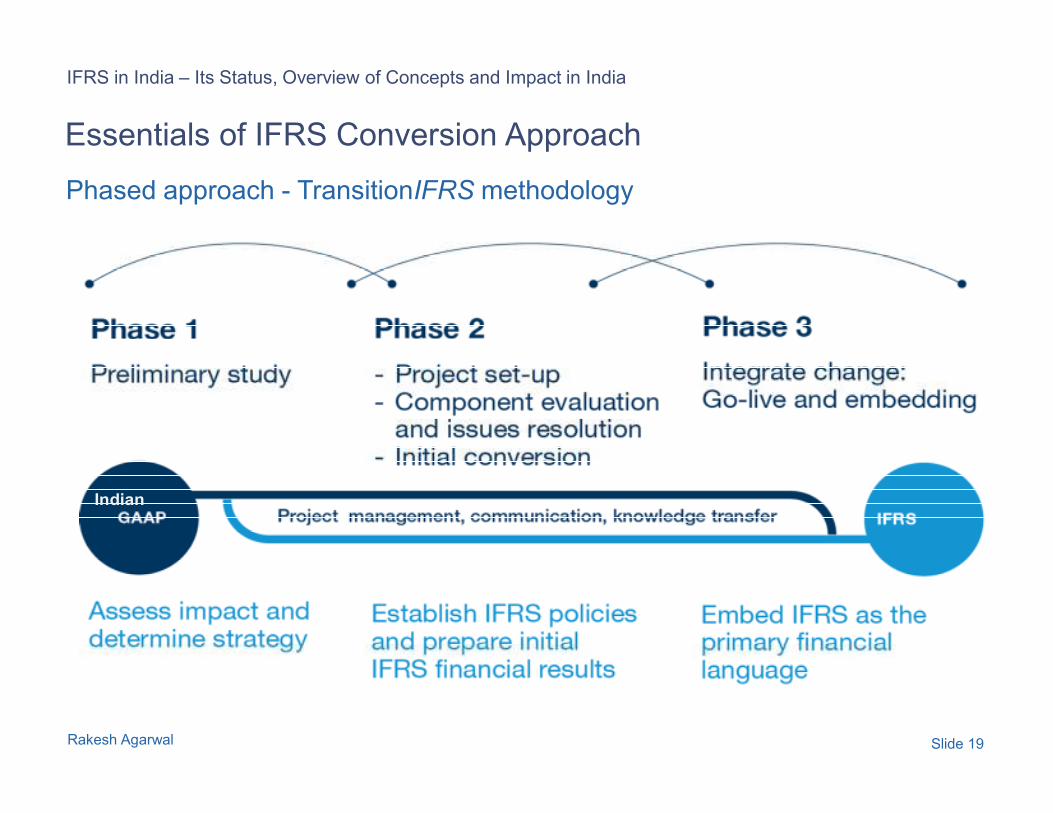

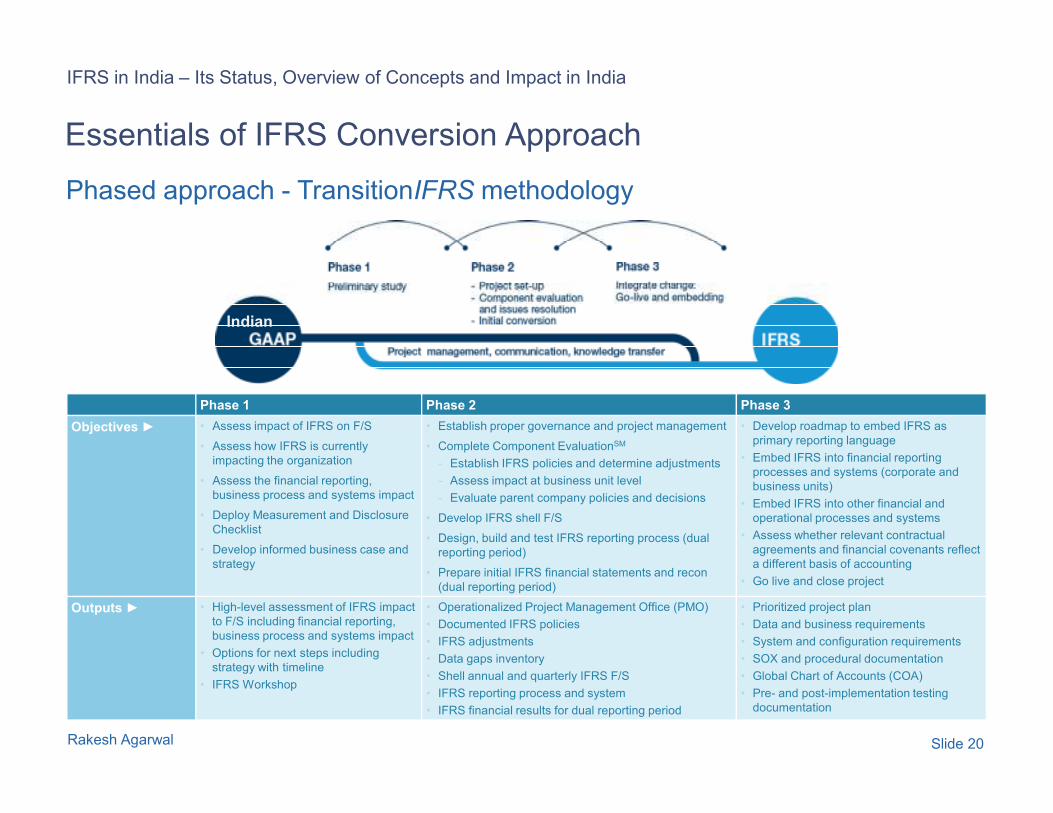

Essentials of IFRS Conversion Approach

Phased approach - TransitionIFRS methodology

IFRS in India – Its Status, Overview of Concepts and Impact in India

Rakesh Agarwal Slide 19

IndianIndian

Essentials of IFRS Conversion Approach

Phased approach - TransitionIFRS methodology

Phase 1 Phase 2 Phase 3

IndianIndian

IFRS in India – Its Status, Overview of Concepts and Impact in India

Rakesh Agarwal Slide 20

Phase 1 Phase 2 Phase 3

Objectives ► • Assess impact of IFRS on F/S

• Assess how IFRS is currently

impacting the organization

• Assess the financial reporting,

business process and systems impact

• Deploy Measurement and Disclosure

Checklist

• Develop informed business case and

strategy

• Establish proper governance and project management

• Complete Component EvaluationSM

- Establish IFRS policies and determine adjustments

- Assess impact at business unit level

- Evaluate parent company policies and decisions

• Develop IFRS shell F/S

• Design, build and test IFRS reporting process (dual

reporting period)

• Prepare initial IFRS financial statements and recon

(dual reporting period)

• Develop roadmap to embed IFRS as

primary reporting language

• Embed IFRS into financial reporting

processes and systems (corporate and

business units)

• Embed IFRS into other financial and

operational processes and systems

• Assess whether relevant contractual

agreements and financial covenants reflect

a different basis of accounting

• Go live and close project

Outputs ► • High-level assessment of IFRS impact

to F/S including financial reporting,

business process and systems impact

• Options for next steps including

strategy with timeline

• IFRS Workshop

• Operationalized Project Management Office (PMO)

• Documented IFRS policies

• IFRS adjustments

• Data gaps inventory

• Shell annual and quarterly IFRS F/S

• IFRS reporting process and system

• IFRS financial results for dual reporting period

• Prioritized project plan

• Data and business requirements

• System and configuration requirements

• SOX and procedural documentation

• Global Chart of Accounts (COA)

• Pre- and post-implementation testing

documentation

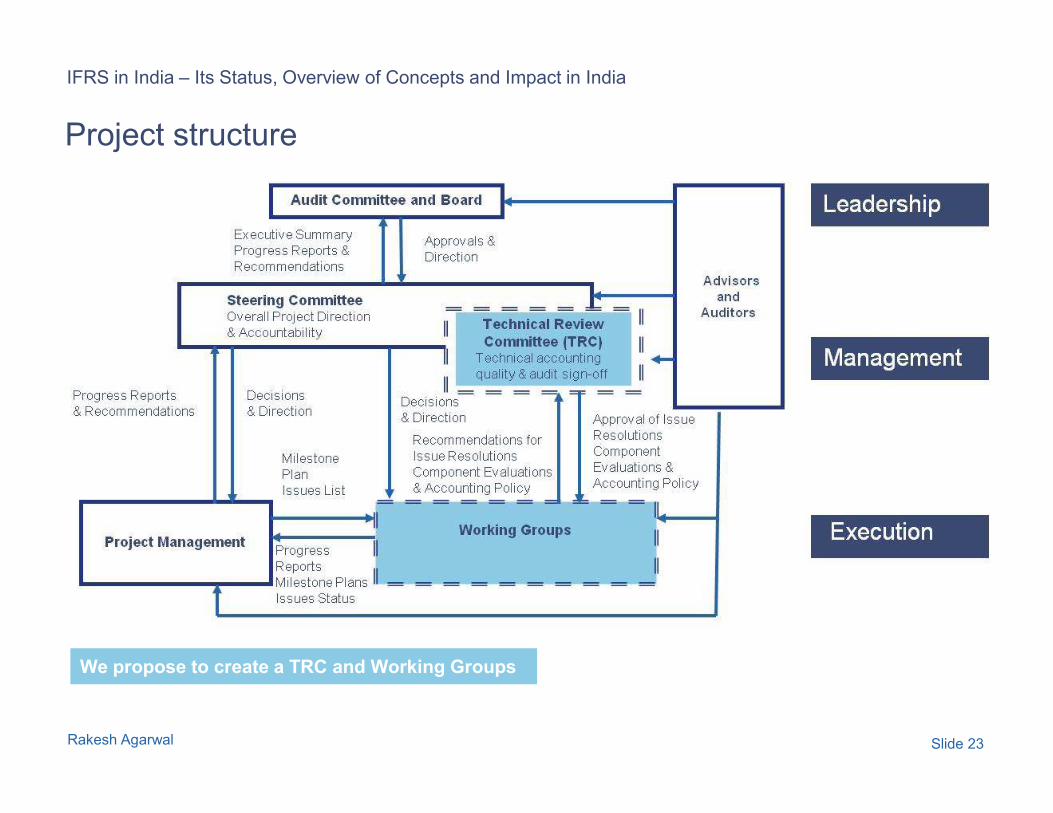

Project Management Framework

Steering Committee

TRC

Decision Maker

Issue

Auditor

Technical Review

Committee INVITEES

A well thought out project structure on lines below ensures that an entity is able to get

appropriate management focus on project and on technical front “get it right the first time” which

is very essential for a successful project.

IFRS in India – Its Status, Overview of Concepts and Impact in India

Rakesh Agarwal Slide 21

Work Streams

Issue

OriginatorsExpert

WS1 WS2 WS3 WS4

o Loans

o Investments

o Consolidatio

n

o Financial

Reporting

o Employee

benefits

o Income

Recognition

o Deferred

Taxes

o Derivatives

o IFRS 1

o Cash Flows

• Technical support material

• Roles & Responsibilities

• Timelines

• Nodal offices

Technical

Champions

Needs

Project Management Framework

IFRS in India – Its Status, Overview of Concepts and Impact in India

Rakesh Agarwal Slide 22

Project structure

IFRS in India – Its Status, Overview of Concepts and Impact in India

Rakesh Agarwal Slide 23

We propose to create a TRC and Working Groups

Project structureCentralised vs Decentralised Approach

Levels in IFRS implementation

assistance

Service

ProvidedCentralised

AdditionalTotal

Location 1-0

A. Base Scenario (Advisory services)

Training Yes

Rs 1x N.A. Rs 1x

Implementation workshop Yes

IFRS financial sketch for ABC

Limited (in word file)Yes

IFRS issue log for ABC Limited Yes

Ad

vis

or’

s

IFR

S i

mp

lem

en

tati

on

se

rvic

es A

dv

iso

ry

se

rvic

es

IFRS in India – Its Status, Overview of Concepts and Impact in India

Rakesh Agarwal Slide 24

IFRS issue log for ABC Limited Yes

Ongoing IFRS issue resolution

and memo’sYes

B. Additional services (Blend of advisory services and reasonable involvement in actual conversion)

Excel template (Broad level)

prepared by managementYes

Rs 1x

Rs 2x X 1 = 2x

Rs 2x X 0.5 = 0.5x

Rs 2x X 0.2 = 0.4x

Rs 3.9xAssisting management in project

planYes

Guidance by Advisor during

execution by managementYes

Actual implementation - Full

fledge conversion from ledger or

trail balance

No N.A. N.A. N.A.

Total Rs 2x Rs 2.9x Rs 4.9x

Ad

vis

or’

s

IFR

S i

mp

lem

en

tati

on

se

rvic

es

Ad

vis

or’

s

IFR

S i

mp

lem

en

tati

on

se

rvic

es

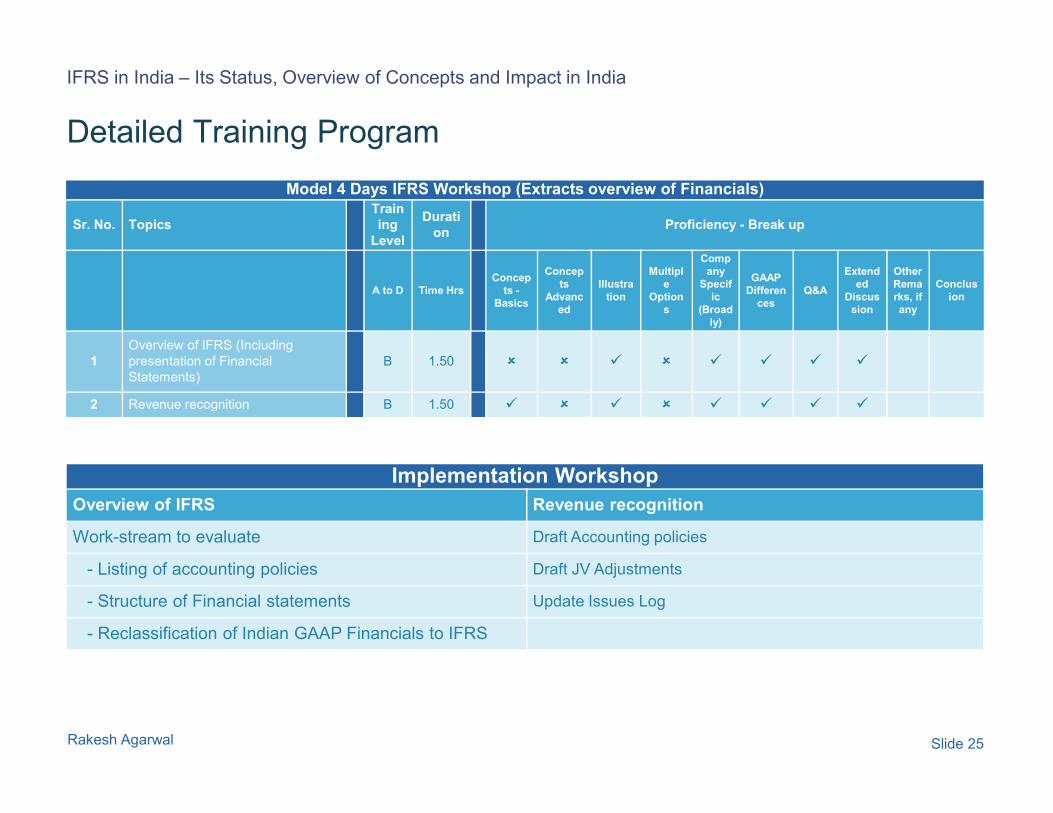

Model 4 Days IFRS Workshop (Extracts overview of Financials)

Sr. No. Topics

Train

ing

Level

Durati

onProficiency - Break up

A to D Time Hrs

Concep

ts -

Basics

Concep

ts

Advanc

ed

Illustra

tion

Multipl

e

Option

s

Comp

any

Specif

ic

(Broad

ly)

GAAP

Differen

ces

Q&A

Extend

ed

Discus

sion

Other

Rema

rks, if

any

Conclus

ion

1

Overview of IFRS (Including

presentation of Financial

Statements)

B 1.50 � � � � � � � �

2 Revenue recognition B 1.50 � � � � � � � �

Detailed Training Program

IFRS in India – Its Status, Overview of Concepts and Impact in India

Rakesh Agarwal Slide 25

Ad

vis

or’

s

IFR

S i

mp

lem

en

tati

on

se

rvic

es

2 Revenue recognition B 1.50 � � � � � � � �

Implementation Workshop

Overview of IFRS Revenue recognition

Work-stream to evaluate Draft Accounting policies

- Listing of accounting policies Draft JV Adjustments

- Structure of Financial statements Update Issues Log

- Reclassification of Indian GAAP Financials to IFRS

Key challenges - mitigation steps / management calls

IFRS in India – Its Status, Overview of Concepts and Impact in India

Key Challenges Mitigation steps / management calls

Volatility due to fair valuation SEC study states only 25% are total assets are fair

valued out of which for over 90% of the assets

reference price is readily available.

Change in IT systems Most IT packages are capable to respond to dual

reporting.

Change in MIS systems The impact with respect to IFRS 8 is manageable

Rakesh Agarwal Slide 26

Taxes Some implication on MAT.

Managing market, investors and analysts Early communication – Europe experience

Regulatory uncertainty Worst case scenario, additional cost for early doing –

Management to take decision based on corporate

philosophy

Preparation of IFRS financial statement

Rakesh Agarwal

Ad

vis

or’

s

IFR

S i

mp

lem

en

tati

on

se

rvic

es

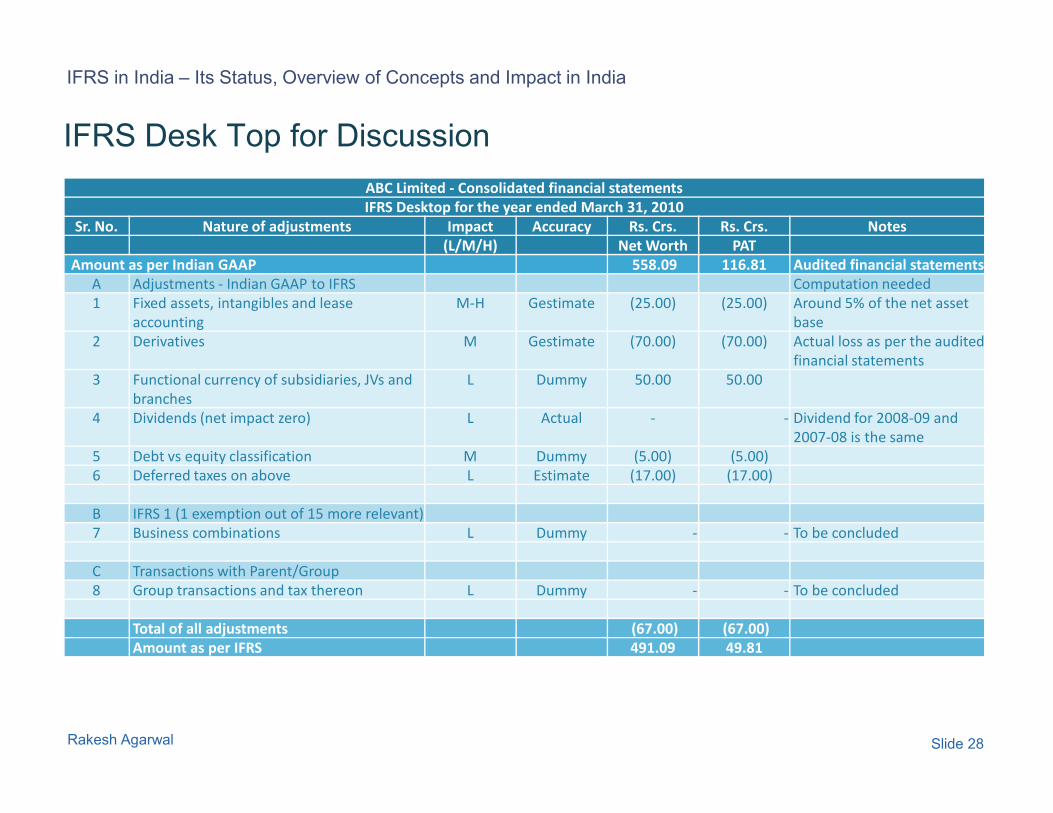

IFRS Desk Top for Discussion

ABC Limited - Consolidated financial statements

IFRS Desktop for the year ended March 31, 2010

Sr. No. Nature of adjustments Impact Accuracy Rs. Crs. Rs. Crs. Notes

(L/M/H) Net Worth PAT

Amount as per Indian GAAP 558.09 116.81 Audited financial statements

A Adjustments - Indian GAAP to IFRS Computation needed

1 Fixed assets, intangibles and lease

accounting

M-H Gestimate (25.00) (25.00) Around 5% of the net asset

base

2 Derivatives M Gestimate (70.00) (70.00) Actual loss as per the audited

financial statements

3 Functional currency of subsidiaries, JVs and

branches

L Dummy 50.00 50.00

IFRS in India – Its Status, Overview of Concepts and Impact in India

Rakesh Agarwal Slide 28

Ad

vis

or’

s

IFR

S i

mp

lem

en

tati

on

se

rvic

es

4 Dividends (net impact zero) L Actual - - Dividend for 2008-09 and

2007-08 is the same

5 Debt vs equity classification M Dummy (5.00) (5.00)

6 Deferred taxes on above L Estimate (17.00) (17.00)

B IFRS 1 (1 exemption out of 15 more relevant)

7 Business combinations L Dummy - - To be concluded

C Transactions with Parent/Group

8 Group transactions and tax thereon L Dummy - - To be concluded

Total of all adjustments (67.00) (67.00)

Amount as per IFRS 491.09 49.81

Ad

vis

or’

s

IFR

S i

mp

lem

en

tati

on

se

rvic

es

Preparation of IFRS financial statement

Issue log Template financial Sketch financial

ABC LimitedIssues Log

Sr Type of Issue Issue Requirements under IFRS Technical

Reference

Requirements under Indian

GAAP

Priority

(H, M, L)

Enquiries / Discussion with

management during the workshop

Property, plant and equipment

1 Measurement Component Approach The Company is required to depreciate each

significant component of an item of PPE

separately, if they have significantly different

useful life.

IAS 16 There is no specific requirement. H To assess whether any significant

component of an item of PPE having

significantly different useful life.

2 Measurement Major overhaul expenses The cost of major overhaul occurring at regular

intervals to be capitalized.

IAS 16 The cost of major overhaul

occurring at regular intervals is

charged to Profit and loss A/c

M Subsequent expenditure incurred for every

seven years in rayon plant (spinning

machine) needs to capitalised

3 Measurement Subsequent expenditure Subsequent costs should be capitalized, that

is recognized as an asset, only if they meet

the recognition criteria that:

a) It is probable that future economic benefits

associated with the item will flow to the entity;

and

b) The cost of the item can be measured

reliably

IAS 16 Subsequent maintenance

expenditure will be capitalized as

part of PPE, if they increase the life

of the plant or increase capacity or

has a benefit for more than a year.

L No such cases were reported

4 Measurement Deferred term basis If the Company has acquired a PPE on

deferred term basis and terms are beyond

normal credit terms, PPE will be recognized

on cash price equivalent, i.e. discounted

amount.

IAS 16 PPE is recorded on purchase price. L No, any purchases are done on deferred

term basis

5 Recognition Environmental obligation and Asset

retirement obligation

Costs of dismantling and removing the item or

restoring the site on which it is located be

recorded when an obligation exists. A liability

IAS 16 No provision has been made for

environment and asset retirement

obligation.

L As discuss the amount is not material

ABC Limited - <--- If this cell is red - there is problem in this sheet

Financial Statements - <--- If this cell is red - there is problem in this sheetTemplate for IFRS conversion for year ended March 31, 2009

Rs. In Crore Rs. in Crores

PARTICULARS AS PER Indian

GAAP

AS PER IFRS PPE INVESTMENT

PROPERTY

HELD TO

MATURITY

AVAILABLE FOR

SALE FINANCIAL

ASSET

OTHER

FINANCIAL

ASSETS

DEFERRED TAX

ASSETS

TRADE & OTHER

RECEIVABLES

SOURCES OF FUNDS

Share Capital 93.04 93.04

Reserves and Surplus 1,402.48 1,402.48

-

Loan Funds -

Secured Loans 1,714.98 1,714.98

Unsecured Loans 43.31 43.31

-

Deferred tax liability (Net) 290.08 290.08 -

NON CURRENT ASSETS

Statement of financial position

Note As on March

31, 2009 ASSETS Non–current assets

Property, Plant and equipment 6 Intangible Assets 7 Available for sale financial asset 9 Deferred income tax assets 21

Derivative financial instruments 10 Trade and other receivables 11

Current assets Inventories 12

Trade and other receivables, net of allowance for doubtful debts 11 Derivative financial instruments 10 Investments in bank deposits Cash and cash equivalents 14

Assets held for sale and discontinued operations 15

Total assets

EQUITY Capital and reserves attributable to equity holders of the

IFRS in India – Its Status, Overview of Concepts and Impact in India

Rakesh Agarwal Slide 29

Ad

vis

or’

s

IFR

S i

mp

lem

en

tati

on

se

rvic

es

recorded when an obligation exists. A liability

for the present value of the costs of

dismantling, removal or restoration as a result

of a legal or constructive obligation is

recognized and the corresponding cost

included as part of the related PPE.

obligation.

6 Measurement Expenditure during construction

period

Indirect expenses during construction period

which are not required to bring the asset in

the condition for its intended use are

expensed off as incurred.

IAS 16 Indian GAAP allows pre-operative

expenses to be generally

capitalized as part of PPE.

L No such cases were reported

7 Measurement Change in method of depreciation Change in method of depreciation is

considered as change in accounting estimate

and thereby accounted for prospectively.

IAS 16 Change in depreciation method is

considered as change in

accounting policy, the impact of

change in depreciation method is

determined retrospectively;

computing depreciation under the

new method.

L The Company has not changed its method

of depreciation in past.

8 Recognition Borrowing Cost General borrowings shall include working

capital loan amount

IAS 23R Similar to IFRS L To assess whether working capital loan has

been included in the general borrowing for

the purpose of calculation of WACC.

9 Recognition Borrowing Cost The borrowing cost shall be capitalized for

exchange differences on the amount of

principal of the foreign currency borrowings to

the extent of difference between interest on

local currency borrowings and interest on

foreign currency borrowings.

IAS 23R Similar to IFRS L To assess whether difference in exchange

fluctuation of foreign currency borrowing

cost has been capitalized.

10 Classification Leasehold land The land is normally classified as an

operating lease unless title passes to the

lessee at the end of the lease term.

Accordingly leasehold land is classified as

operating lease and disclosed as prepaid

assets.

IAS 17 Leasehold land is classified as a

part of fixed assets

M To assess whether the title would pass to

the company at the end of the lease term.

Cost of leasehold land is amortised over the

lease period.

11 Measurement Periodic Review Residual value, residual life and method of

depreciation of the asset is required to be

assessed at each balance sheet.

IAS 16 No specific requirement. M Whether the current SLM reflects the useful

life of the assets?

There are some PPE which are still in use

but they are fully depreciated viz. cement

plant, paper plant etc.

To assess further any such case where the

life of the PPE has been fully depreciated

Deferred tax liability (Net) 290.08 290.08 -

-

3,543.89 3,543.89

APPLICATION OF FUNDS

Fixed Assets (Net Block Incl. CWIP) 2,810.83 2,810.83 2,810.83

-

Investments 46.54 46.54 6.56 39.28 0.70

-

Current Assets, Loans and Advances -

Inventories 670.57 670.57

Sundry Debtors 150.89 150.89

Cash and Bank Balances 66.54 66.54

Other Current Assets 33.78 33.78

Loans and Advances 672.24 672.24

-

Less: Current Liabilities and Provisions -

Liabilities 681.02 681.02

Provisions 327.74 327.74

-

Miscellaneous Expenditure 101.26 101.26 3.21

-

3,543.89 3,543.89 2,814.04 - 6.56 39.28 0.70 - -

Capital and reserves attributable to equity holders of the Company

Ordinary shares 16 Share premium 16 Retained earnings 17 Other component of equity 18

Total equity LIABILITIES Non–current liabilities Borrowings 20

Retirement benefit obligations 22 Other non–current liabilities Deferred income tax liabilities 21

Current liabilities

Trade and other payables 19 Current income tax liabilities Other current liabilities

Retirement benefit obligations 22 Borrowings 20

Provisions for other liabilities and charges 23 Derivative financial instruments 10

Liabilities of disposal group classified as held-for-sale

Total liabilities

Total equity & liabilities

The accompanying notes form an integral part of these financial statements.

IFRS Converged Indian Accounting Standard

ED AS 1(R) Presentation of Financials Statements

• Required that the components of profit or loss and

statement of other comprehensive income shall be

presented in a two statement.

• Required that the components of profit or loss and

statement of other comprehensive income shall be

presented in a single statement of profit or loss.

ED AS 3(R) Statement of Cash Flows

• Provide an option to other than financial entities to

classify the interest paid and interest and dividends

received as an item of operating cash flows also.

• Have to classify the interest paid and interest and

dividends received as an item of financing and investing

cash flows activity.

Carve Outs in CIAS from IFRS

IFRS in India – Its Status, Overview of Concepts and Impact in India

Slide 30

• Provide an option to classify the dividend paid as an

item of operating cash flows also.

• Have to classify the dividend paid as an item of

financing activity.

ED AS 15(R) Employee Benefits

• Permits various options for treatment of actuarial gains

and losses

• Requires immediate recognition of actuarial gain and

loss in profit or loss

• Does not provide guidance about the interval for

actuarial valuation of defined benefit obligation

• Provide guidance about the actuarial valuation of

defined benefit obligation may be made at interval not

exceeding three years

• Rate of government bond can be used as a discount

rate only where there is no deep market of high quality

corporate bonds.

• Rate of government bond shall be used to discount post

employment benefits obligation.

IFRS Converged Indian Accounting Standard

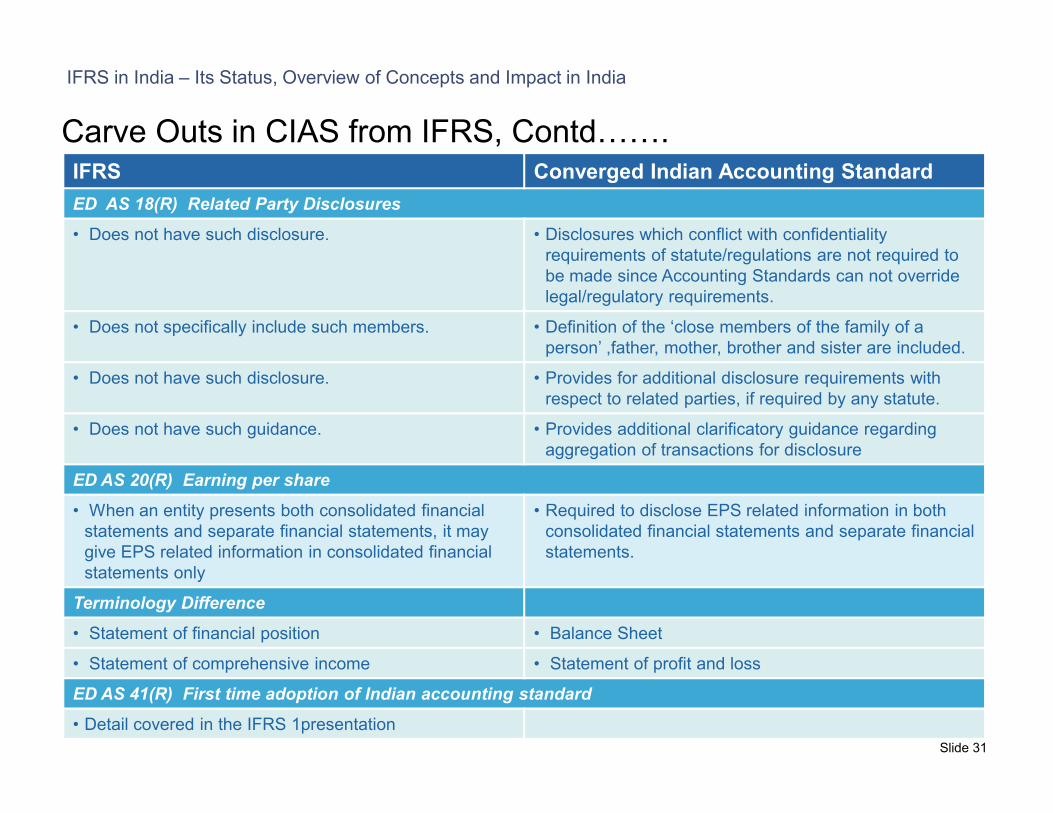

ED AS 18(R) Related Party Disclosures

• Does not have such disclosure. • Disclosures which conflict with confidentiality

requirements of statute/regulations are not required to

be made since Accounting Standards can not override

legal/regulatory requirements.

• Does not specifically include such members. • Definition of the ‘close members of the family of a

person’ ,father, mother, brother and sister are included.

• Does not have such disclosure. • Provides for additional disclosure requirements with

respect to related parties, if required by any statute.

IFRS in India – Its Status, Overview of Concepts and Impact in India

Carve Outs in CIAS from IFRS, Contd…….

Slide 31

respect to related parties, if required by any statute.

• Does not have such guidance. • Provides additional clarificatory guidance regarding

aggregation of transactions for disclosure

ED AS 20(R) Earning per share

• When an entity presents both consolidated financial

statements and separate financial statements, it may

give EPS related information in consolidated financial

statements only

• Required to disclose EPS related information in both

consolidated financial statements and separate financial

statements.

Terminology Difference

• Statement of financial position • Balance Sheet

• Statement of comprehensive income • Statement of profit and loss

ED AS 41(R) First time adoption of Indian accounting standard

• Detail covered in the IFRS 1presentation

Comparison between CIAS and

IFRS issued by IASB

Publication

IFRS in India – Its Status, Overview of Concepts and Impact in India

Carve Outs in CIAS from IFRS, Contd…….

Slide 32Slide 32

Source: PwC Publication Moving Towards Future........

Indian GAAP.

Exposure Draft issued by ICAI

IFRS in India – Its Status, Overview of Concepts and Impact in India

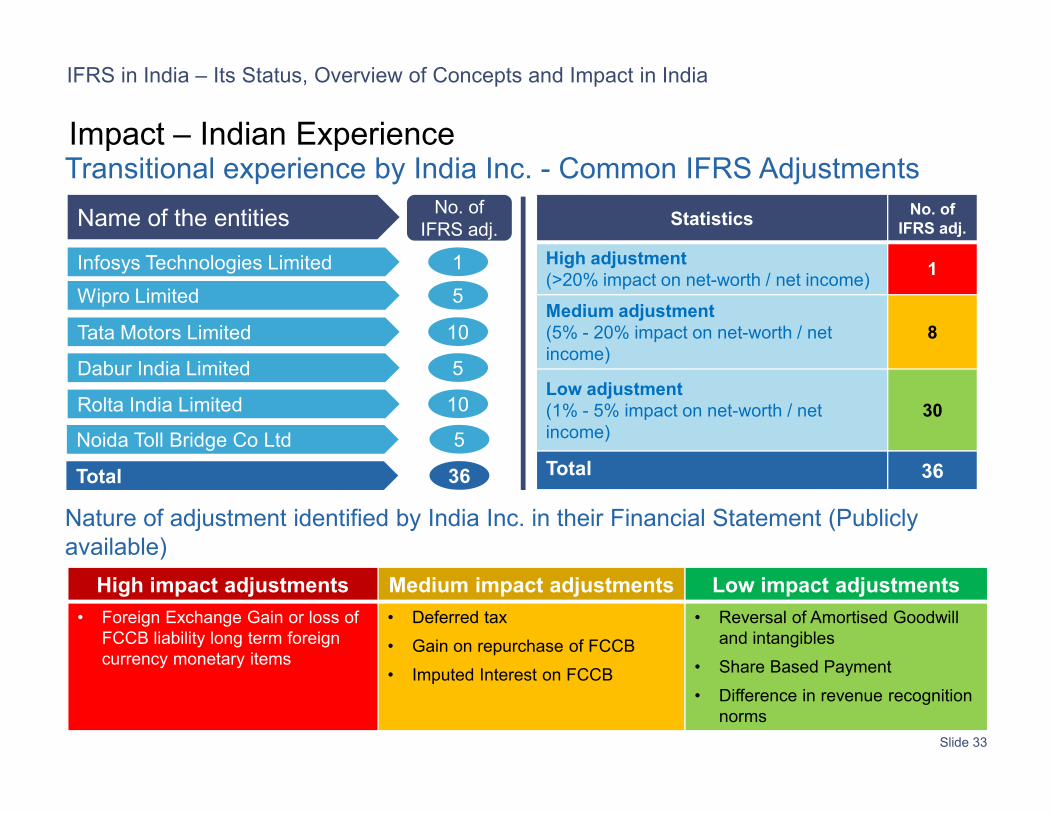

Transitional experience by India Inc. - Common IFRS Adjustments

1Infosys Technologies Limited

10Rolta India Limited

5Dabur India Limited

5Wipro Limited

10Tata Motors Limited

StatisticsNo. of

IFRS adj.

High adjustment

(>20% impact on net-worth / net income)1

Medium adjustment

(5% - 20% impact on net-worth / net

income)

8

Low adjustment

(1% - 5% impact on net-worth / net 30

Name of the entitiesNo. of

IFRS adj.

Impact – Indian Experience

Slide 33

10Rolta India Limited

5Noida Toll Bridge Co Ltd

(1% - 5% impact on net-worth / net

income)

30

Total 36

High impact adjustments Medium impact adjustments Low impact adjustments

• Foreign Exchange Gain or loss of

FCCB liability long term foreign

currency monetary items

• Deferred tax

• Gain on repurchase of FCCB

• Imputed Interest on FCCB

• Reversal of Amortised Goodwill

and intangibles

• Share Based Payment

• Difference in revenue recognition

norms

Nature of adjustment identified by India Inc. in their Financial Statement (Publicly

available)

36Total

• Presentation of financial statement

• Consolidation

• Business combination

• Leases

Annexure 1: Concepts relatively

new in Indian GAAP

Rakesh Agarwal

• Functional currency

• Deferred taxes

• Employee benefits (including

ESOP)

• Financial instruments

• First time adoption of IFRS

Slide 34

Presentation of financial statement

Free form presentation

A complete set of financial statements

comprises:

(a) a statement of financial position as at the end of

the period;

(b) a statement of comprehensive income for the

period;

Annexure 1: Concepts relatively new in Indian GAAP

IFRS in India – Its Status, Overview of Concepts and Impact in India

period;

(c) a statement of changes in equity for the period;

(d) a statement of cash flows for the period;

(e) notes, comprising a summary of significant

accounting policies and other explanatory

information; and

An entity may use titles for the statements

other than those prescribed in IAS 1R,

however the titles used shall not be

misleading.

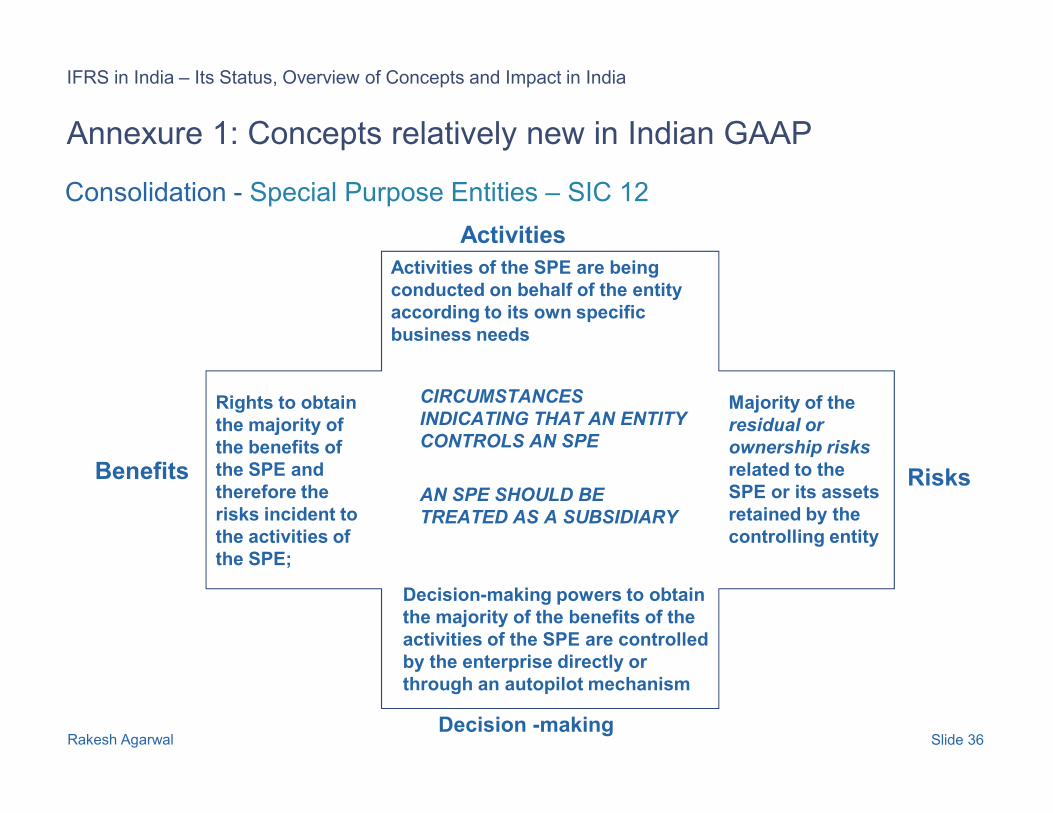

Consolidation - Special Purpose Entities – SIC 12

CIRCUMSTANCES

Activities of the SPE are being

conducted on behalf of the entity

according to its own specific

business needs

Rights to obtain Majority of the

Activities

Annexure 1: Concepts relatively new in Indian GAAP

IFRS in India – Its Status, Overview of Concepts and Impact in India

Rakesh Agarwal Slide 36

INDICATING THAT AN ENTITY

CONTROLS AN SPE

AN SPE SHOULD BE

TREATED AS A SUBSIDIARY

Decision-making powers to obtain

the majority of the benefits of the

activities of the SPE are controlled

by the enterprise directly or

through an autopilot mechanism

Rights to obtain

the majority of

the benefits of

the SPE and

therefore the

risks incident to

the activities of

the SPE;

Majority of the

residual or

ownership risks

related to the

SPE or its assets

retained by the

controlling entity

Benefits Risks

Decision -making

Consolidation

Key GAAP differences

Uniform accounting policy

More entities are required to be consolidated under IFRS

Annexure 1: Concepts relatively new in Indian GAAP

IFRS in India – Its Status, Overview of Concepts and Impact in India

Rakesh Agarwal Slide 37

Consolidation

Our experience

Companies need to develop group accounting manual and reporting packages for

preparation of consolidated financial statement with uniform accounting policy and

IFRS compliant figures

Ensuring uniform accounting policy for all the consolidating entity is difficult

Annexure 1: Concepts relatively new in Indian GAAP

IFRS in India – Its Status, Overview of Concepts and Impact in India

Rakesh Agarwal Slide 38

Ensuring uniform accounting policy for all the consolidating entity is difficult

Determination of functional currency is complex under certain situation

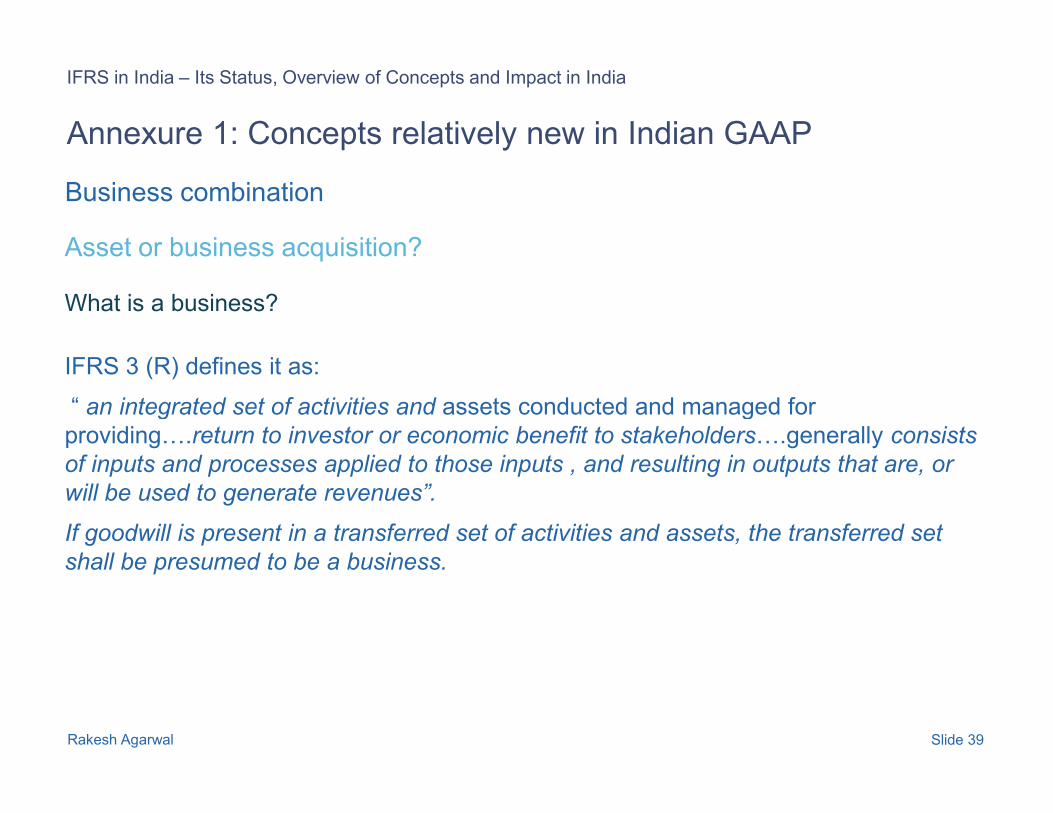

Business combination

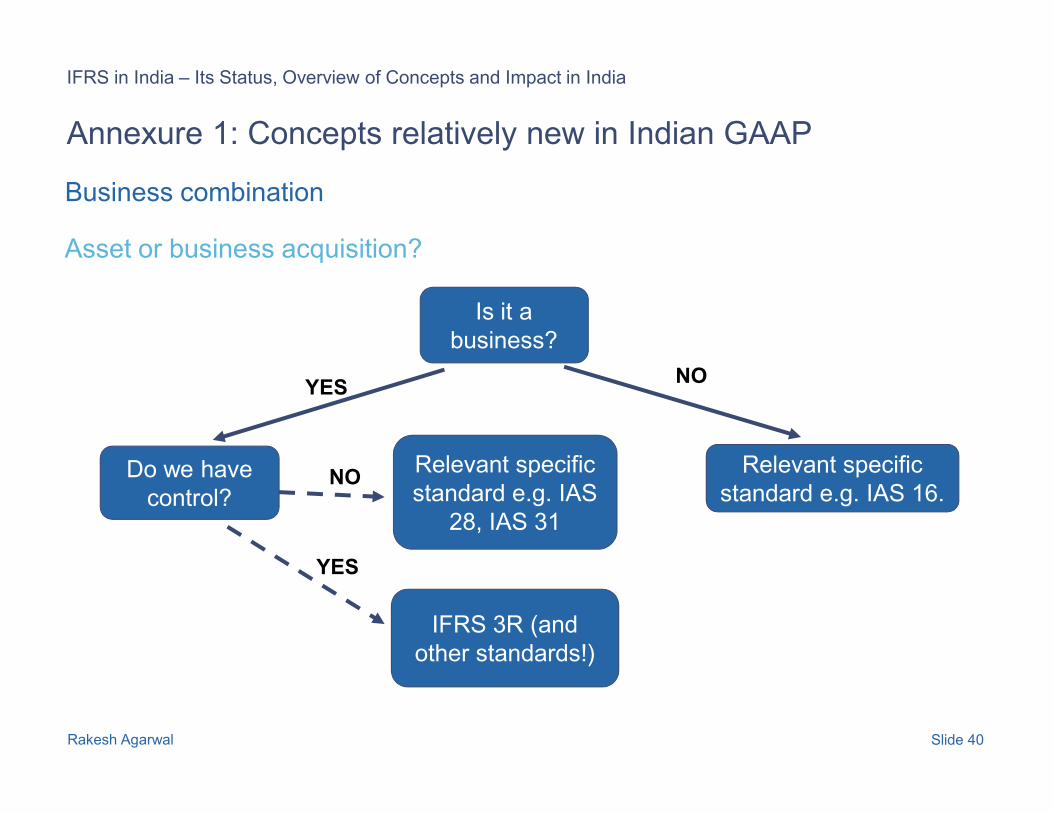

What is a business?

IFRS 3 (R) defines it as:

“ an integrated set of activities and assets conducted and managed for

Asset or business acquisition?

Annexure 1: Concepts relatively new in Indian GAAP

IFRS in India – Its Status, Overview of Concepts and Impact in India

Rakesh Agarwal Slide 39

“ an integrated set of activities and assets conducted and managed for

providing….return to investor or economic benefit to stakeholders….generally consists

of inputs and processes applied to those inputs , and resulting in outputs that are, or

will be used to generate revenues”.

If goodwill is present in a transferred set of activities and assets, the transferred set

shall be presumed to be a business.

Business combination

Asset or business acquisition?

Is it a

business?

YESNO

Annexure 1: Concepts relatively new in Indian GAAP

IFRS in India – Its Status, Overview of Concepts and Impact in India

Rakesh Agarwal Slide 40

Relevant specific

standard e.g. IAS 16.

IFRS 3R (and

other standards!)

Do we have

control?

YES

NORelevant specific

standard e.g. IAS

28, IAS 31

Business combination

Purchase Price Allocation

Fair value everything!

almostOnce we have determined

the cost of a business

combination we need to

Annexure 1: Concepts relatively new in Indian GAAP

IFRS in India – Its Status, Overview of Concepts and Impact in India

Rakesh Agarwal Slide 41

Fair value everything!

Areas to watch out for!

Consequences of fair valuing

combination we need to

allocate the cost to the

identifiable assets,

liabilities and contingent

liabilities acquired.

Business combination

Key GAAP differences

Assets and liabilities are recognised based on fair value

Amortisation of Goodwill is prohibited

Additional Intangible assets to be recognised on business combinations

Annexure 1: Concepts relatively new in Indian GAAP

IFRS in India – Its Status, Overview of Concepts and Impact in India

Rakesh Agarwal Slide 42

Additional Intangible assets to be recognised on business combinations

Date of acquisition - Transfer on control vs high court orders

Business combination are accounted using purchase method only

Contingent liabilities to be recognised to Income statement

Contingent consideration

Reverse acquisitions

Business combination

Our experience

IFRS 1 - Optional exemption for Business combination has been applied by most of

the companies

Valuation experts with IFRS experience are necessary for purchase price allocation

Annexure 1: Concepts relatively new in Indian GAAP

IFRS in India – Its Status, Overview of Concepts and Impact in India

Rakesh Agarwal Slide 43

Issues like reverse merger, merger of entities under common control are very

common under Indian scenario

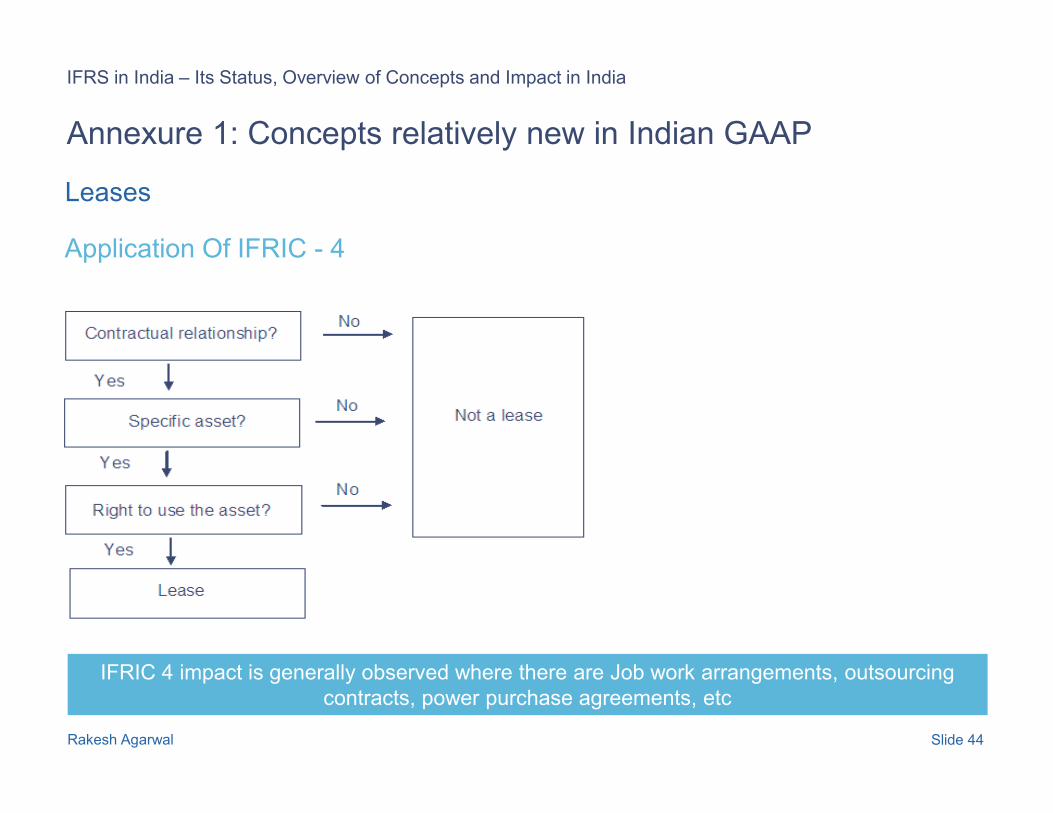

Leases

Application Of IFRIC - 4

Annexure 1: Concepts relatively new in Indian GAAP

IFRS in India – Its Status, Overview of Concepts and Impact in India

Rakesh Agarwal Slide 44

IFRIC 4 impact is generally observed where there are Job work arrangements, outsourcing

contracts, power purchase agreements, etc

Annexure 1: Concepts relatively new in Indian GAAP

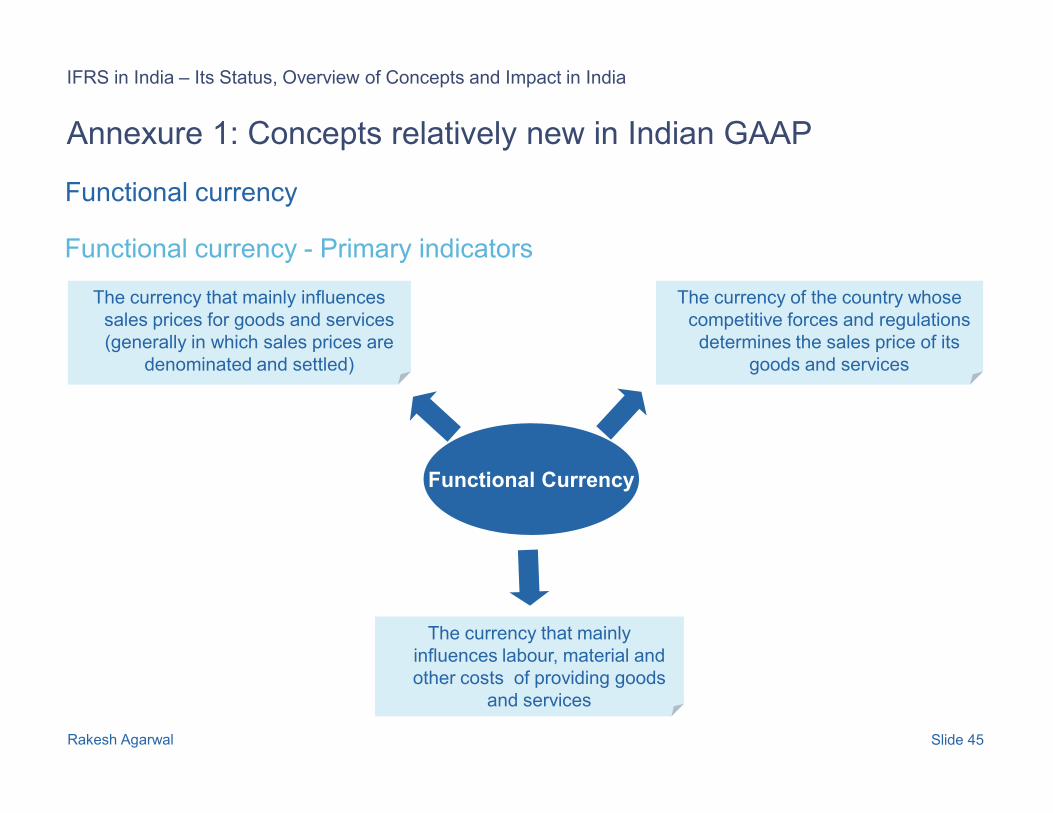

Functional currency

Functional currency - Primary indicators

The currency that mainly influences

sales prices for goods and services

(generally in which sales prices are

denominated and settled)

The currency of the country whose

competitive forces and regulations

determines the sales price of its

goods and services

IFRS in India – Its Status, Overview of Concepts and Impact in India

Rakesh Agarwal Slide 45

The currency that mainly

influences labour, material and

other costs of providing goods

and services

Functional Currency

Annexure 1: Concepts relatively new in Indian GAAP

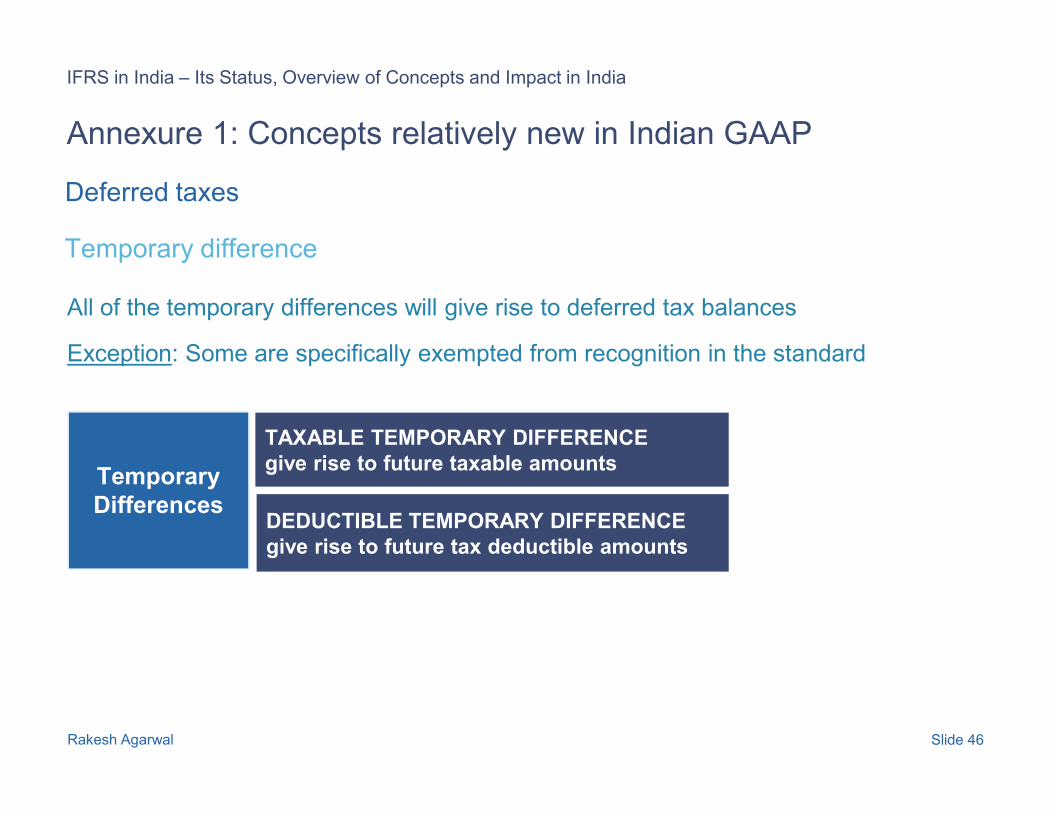

Deferred taxes

Temporary difference

All of the temporary differences will give rise to deferred tax balances

Exception: Some are specifically exempted from recognition in the standard

IFRS in India – Its Status, Overview of Concepts and Impact in India

Rakesh Agarwal Slide 46

Temporary

Differences

TAXABLE TEMPORARY DIFFERENCE

give rise to future taxable amounts

DEDUCTIBLE TEMPORARY DIFFERENCE

give rise to future tax deductible amounts

Annexure 1: Concepts relatively new in Indian GAAP

Deferred taxes

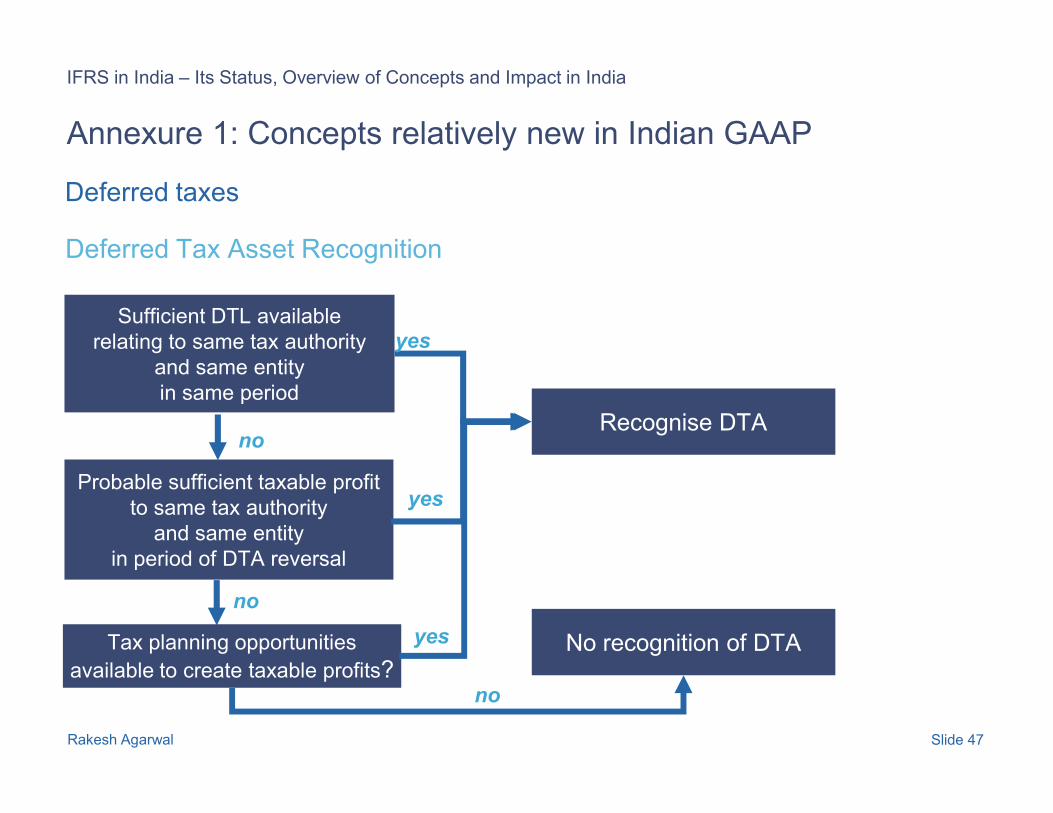

Sufficient DTL available

relating to same tax authority

and same entity

in same period

yes

Deferred Tax Asset Recognition

IFRS in India – Its Status, Overview of Concepts and Impact in India

Rakesh Agarwal Slide 47

Probable sufficient taxable profit

to same tax authority

and same entity

in period of DTA reversal

no

yes

Recognise DTA

no

Tax planning opportunities

available to create taxable profits?No recognition of DTAyes

no

Annexure 1: Concepts relatively new in Indian GAAP

Deferred taxes

Deferred Tax journal entries

Situation Where deferred tax is recorded

General rule Income statement

Adjustment to FV on acquisition Adjust goodwill

IFRS in India – Its Status, Overview of Concepts and Impact in India

Rakesh Agarwal Slide 48

Adjustment to FV on acquisition Adjust goodwill

Transaction or event recognised in equity Equity

Annexure 1: Concepts relatively new in Indian GAAP

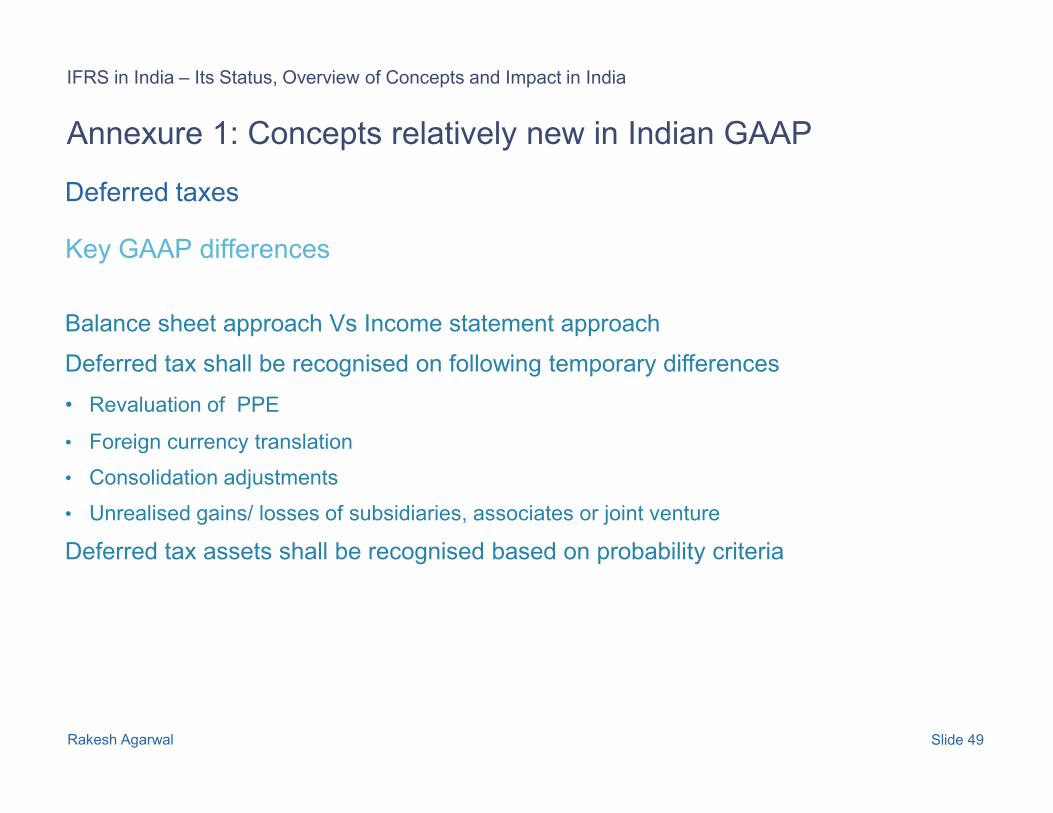

Deferred taxes

Key GAAP differences

Balance sheet approach Vs Income statement approach

Deferred tax shall be recognised on following temporary differences

• Revaluation of PPE

IFRS in India – Its Status, Overview of Concepts and Impact in India

Rakesh Agarwal Slide 49

• Revaluation of PPE

• Foreign currency translation

• Consolidation adjustments

• Unrealised gains/ losses of subsidiaries, associates or joint venture

Deferred tax assets shall be recognised based on probability criteria

Annexure 1: Concepts relatively new in Indian GAAP

Employee benefits

Key GAAP differences

Option for recognition of actuarial gain or losses to income statement or Other

comprehensive income or corridor approach

Fair value method shall be applied for ESOP accounting

IFRS in India – Its Status, Overview of Concepts and Impact in India

Rakesh Agarwal Slide 50

Annexure 1: Concepts relatively new in Indian GAAP

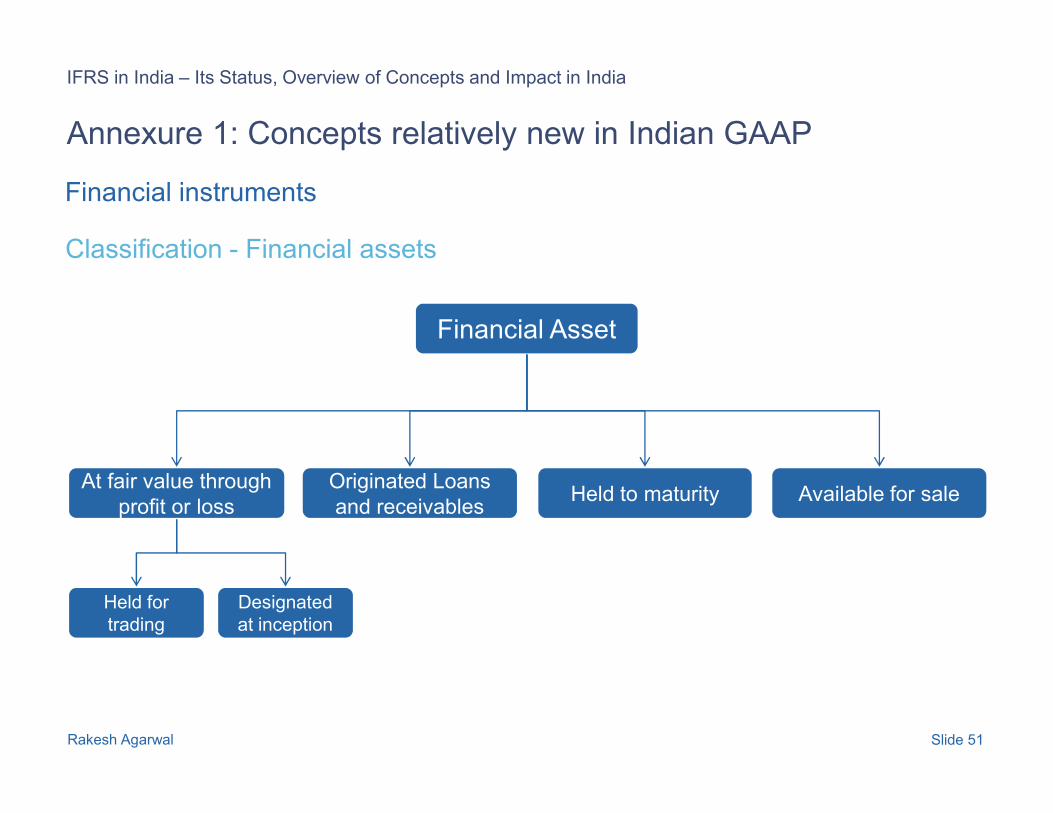

Financial instruments

Classification - Financial assets

Financial Asset

IFRS in India – Its Status, Overview of Concepts and Impact in India

Rakesh Agarwal Slide 51

At fair value through

profit or loss

Originated Loans

and receivablesHeld to maturity Available for sale

Held for

trading

Designated

at inception

Annexure 1: Concepts relatively new in Indian GAAP

Financial instruments

Classification – Financial Liabilities (Two categories)

1. At fair value through profit or loss

Held for tradingDesignated at

IFRS in India – Its Status, Overview of Concepts and Impact in India

Rakesh Agarwal Slide 52

Held for tradingDesignated at

inception

Intention of short term profit;Derivatives – unless if hedges

Voluntary designation subject to Certain conditions;

Irrevocable – cannot be moved

2. Other financial liabilities

Annexure 1: Concepts relatively new in Indian GAAP

Financial instruments

Subsequent measurementAssets/Liabilities at fair value through profit or loss

Loans and receivables

At FV through profit

or loss

IFRS in India – Its Status, Overview of Concepts and Impact in India

Rakesh Agarwal Slide 53

Held to maturity

Available for sale

Other liabilities

At amortised cost

At FV through equity

Annexure 1: Concepts relatively new in Indian GAAP

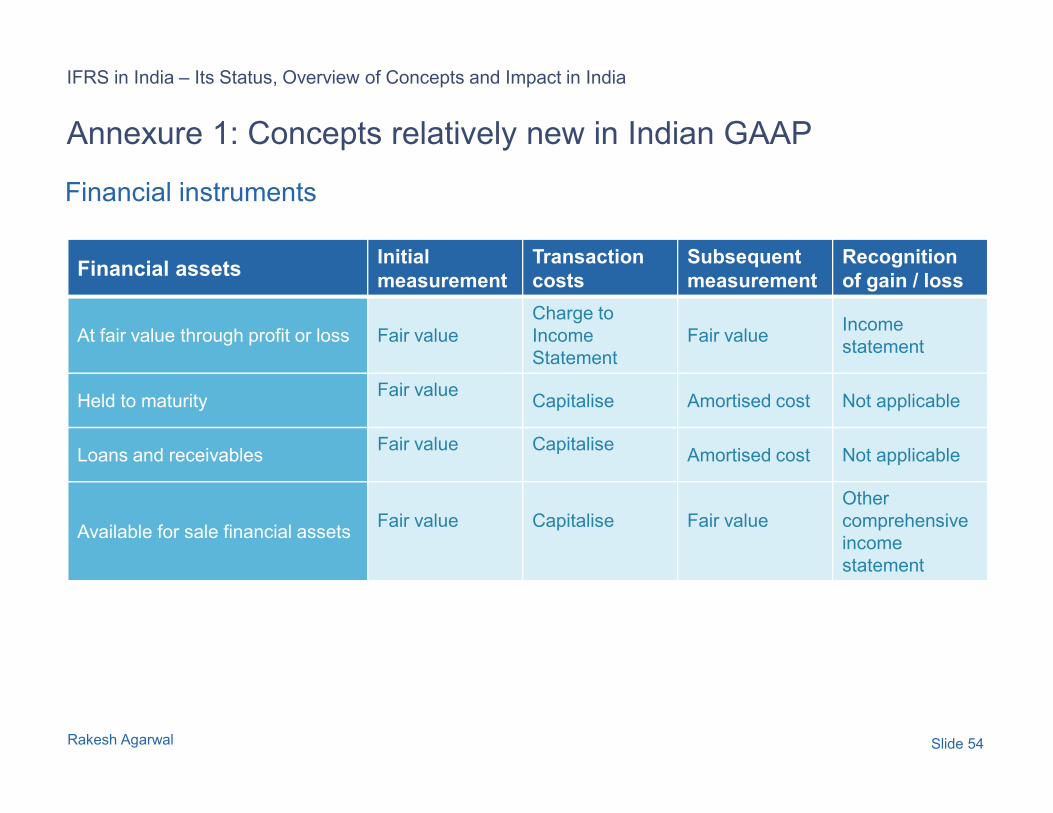

Financial instruments

Financial assetsInitial

measurement

Transaction

costs

Subsequent

measurement

Recognition

of gain / loss

At fair value through profit or loss Fair value

Charge to

Income

Statement

Fair valueIncome

statement

Held to maturityFair value

Capitalise Amortised cost Not applicable

IFRS in India – Its Status, Overview of Concepts and Impact in India

Rakesh Agarwal Slide 54

Held to maturity Capitalise Amortised cost Not applicable

Loans and receivablesFair value Capitalise

Amortised cost Not applicable

Available for sale financial assetsFair value Capitalise Fair value

Other

comprehensive

income

statement

Annexure 1: Concepts relatively new in Indian GAAP

Financial instruments

Use of experts required to handle complex areas

Involvement of treasury professionals is crucial

Volatility in Income statement due to accounting of embedded derivative

Our experience

IFRS in India – Its Status, Overview of Concepts and Impact in India

Rakesh Agarwal Slide 55

Volatility in Income statement due to accounting of embedded derivative

Documentation for hedge accounting

Annexure 1: Concepts relatively new in Indian GAAP

First time adoption of IFRS

Optional Exemptions

Business combinations

Property, plant and equipment,

investment properties, intangibles

Compound instruments

Fair value measurement of financial

Instruments on initial recognition

IFRS in India – Its Status, Overview of Concepts and Impact in India

Rakesh Agarwal Slide 56

Designation of financial assets and

Financial liabilities

Insurance contracts*

Employee benefits Standards

in force at

reporting date Cumulative translation differences

Transition date for subsidiaries,

associates and joint ventures

Share-based payments

Decommissioning liabilities

Leases

Borrowing cost Service concessions arrangements

Instruments on initial recognition

Investments in subsidiaries,

associates and joint control entities.

Annexure 1: Concepts relatively new in Indian GAAP

First time adoption of IFRS

Mandatory Exceptions

Standards

Estimates Non controlling interest*

IFRS in India – Its Status, Overview of Concepts and Impact in India

Rakesh Agarwal Slide 57

Hedge accounting

Standards

in force at

reporting date

*applicable on or after 1st July 2009,

can be early adopted

Annexure 2

Common adjustments

from Indian GAAP to

IFRS

a. Entities to be consolidated – ESOP

Q The ESOP trust has XX shares aggregating to USD 50 M

Q The interest on loan given for financing stocks amounted to USD 3 M

Consolidated Financial Statement

IFRS in India – Its Status, Overview of Concepts and Impact in India

Annexure 2: Common adjustments from Indian GAAP to IFRS

Rakesh Agarwal Slide 59

Answer

A – Dr NW 53, Dr NI 3

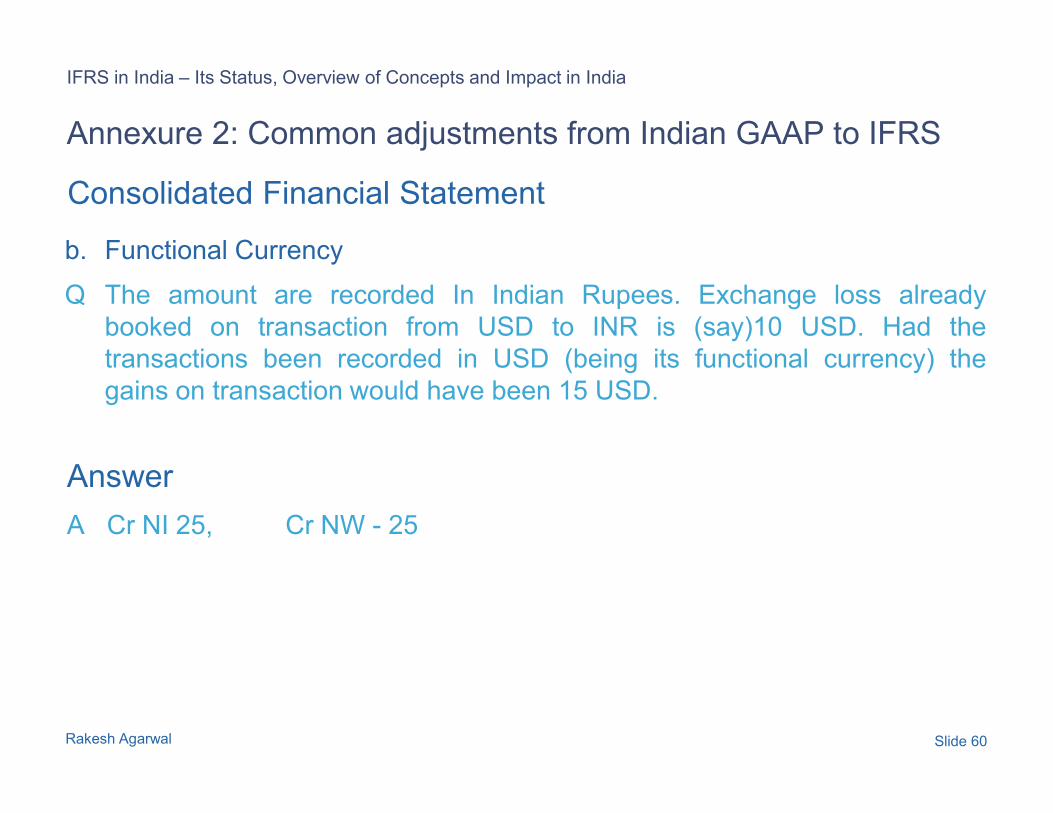

b. Functional Currency

Q The amount are recorded In Indian Rupees. Exchange loss already

booked on transaction from USD to INR is (say)10 USD. Had the

transactions been recorded in USD (being its functional currency) the

gains on transaction would have been 15 USD.

IFRS in India – Its Status, Overview of Concepts and Impact in India

Annexure 2: Common adjustments from Indian GAAP to IFRS

Consolidated Financial Statement

Rakesh Agarwal Slide 60

Answer

A Cr NI 25, Cr NW - 25

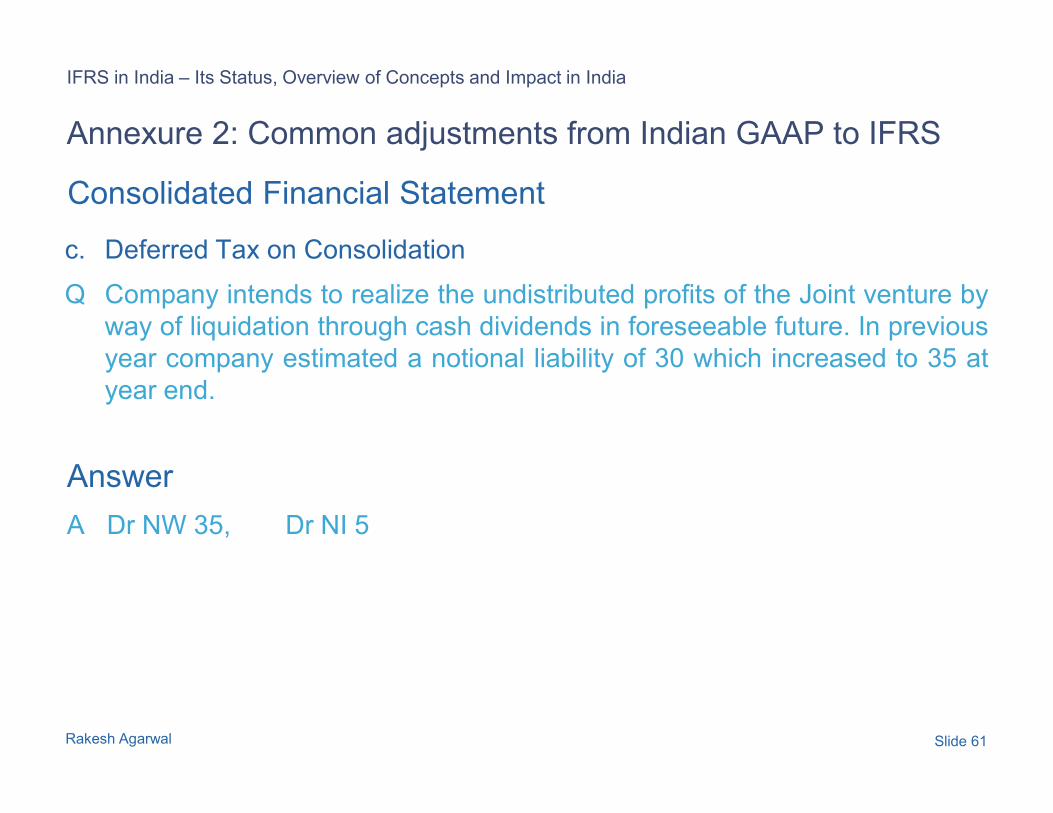

c. Deferred Tax on Consolidation

Q Company intends to realize the undistributed profits of the Joint venture by

way of liquidation through cash dividends in foreseeable future. In previous

year company estimated a notional liability of 30 which increased to 35 at

year end.

IFRS in India – Its Status, Overview of Concepts and Impact in India

Annexure 2: Common adjustments from Indian GAAP to IFRS

Consolidated Financial Statement

Rakesh Agarwal Slide 61

Answer

A Dr NW 35, Dr NI 5

d. Fair Value measurement in Jointly Control Entities

Q Company has recorded its investment in JCE at Book value. The net fair

value of all adjustments (excluding goodwill of 100) has the impact of

increase by 50. The depreciation on such increase in FV is 5

IFRS in India – Its Status, Overview of Concepts and Impact in India

Annexure 2: Common adjustments from Indian GAAP to IFRS

Consolidated Financial Statement

Rakesh Agarwal Slide 62

Answer

A Dr NW 5, Dr NI 5.

e. Transitional Provisions

Q The impact of transitional provisions under Indian GAAP is Dr NW 20

IFRS in India – Its Status, Overview of Concepts and Impact in India

Annexure 2: Common adjustments from Indian GAAP to IFRS

Consolidated Financial Statement

Rakesh Agarwal Slide 63

Answer

A. Cr NW 20, NI 0

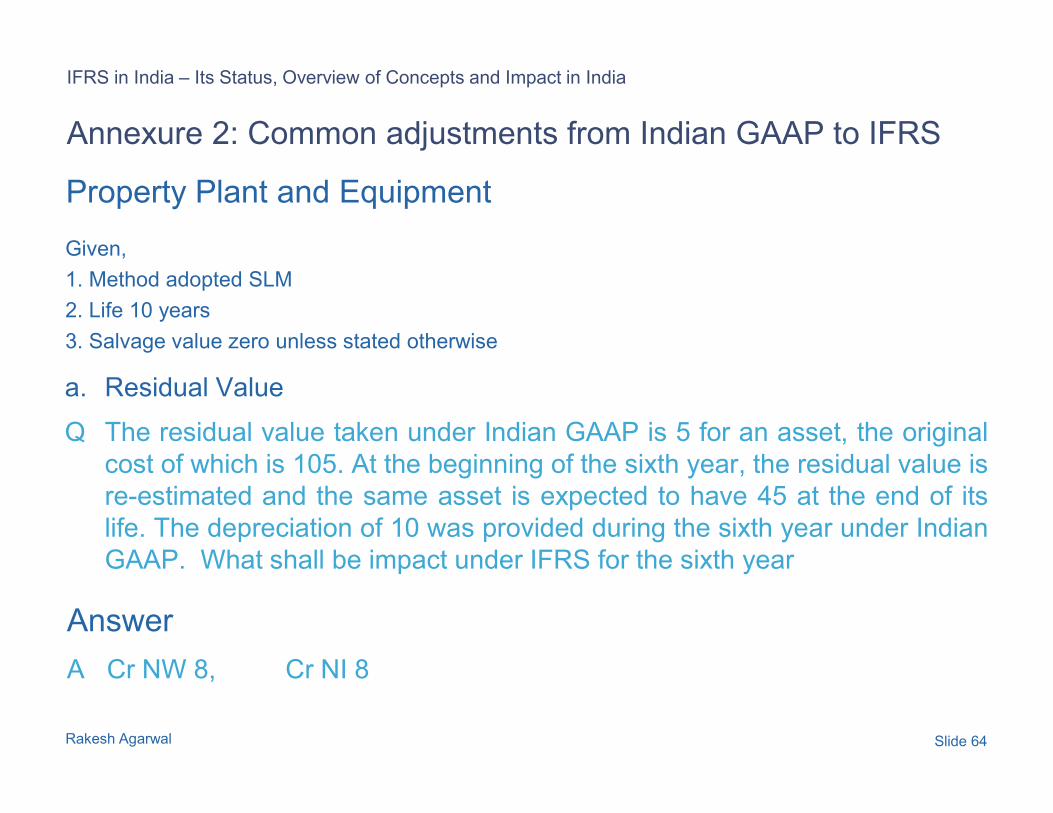

a. Residual Value

Given,

1. Method adopted SLM

2. Life 10 years

3. Salvage value zero unless stated otherwise

Property Plant and Equipment

IFRS in India – Its Status, Overview of Concepts and Impact in India

Annexure 2: Common adjustments from Indian GAAP to IFRS

Rakesh Agarwal Slide 64

Q The residual value taken under Indian GAAP is 5 for an asset, the original

cost of which is 105. At the beginning of the sixth year, the residual value is

re-estimated and the same asset is expected to have 45 at the end of its

life. The depreciation of 10 was provided during the sixth year under Indian

GAAP. What shall be impact under IFRS for the sixth year

Answer

A Cr NW 8, Cr NI 8

b. Exchange gains and losses

IFRS in India – Its Status, Overview of Concepts and Impact in India

Annexure 2: Common adjustments from Indian GAAP to IFRS

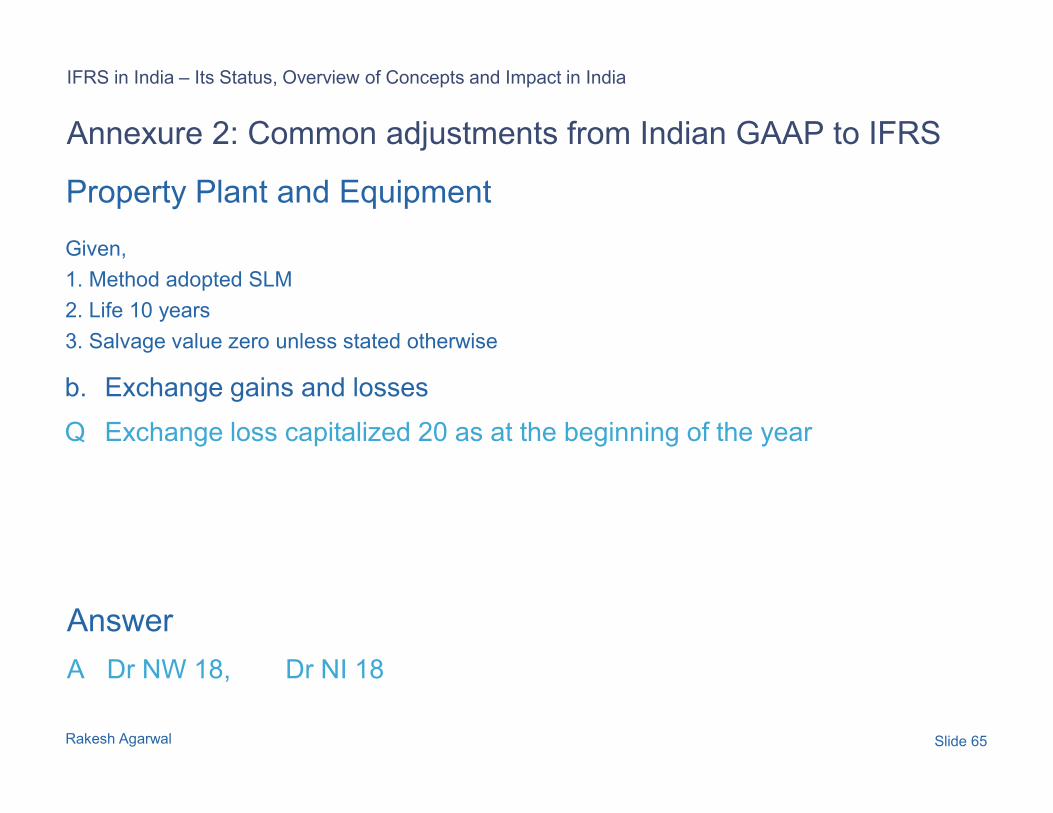

Given,

1. Method adopted SLM

2. Life 10 years

3. Salvage value zero unless stated otherwise

Property Plant and Equipment

Rakesh Agarwal Slide 65

Q Exchange loss capitalized 20 as at the beginning of the year

Answer

A Dr NW 18, Dr NI 18

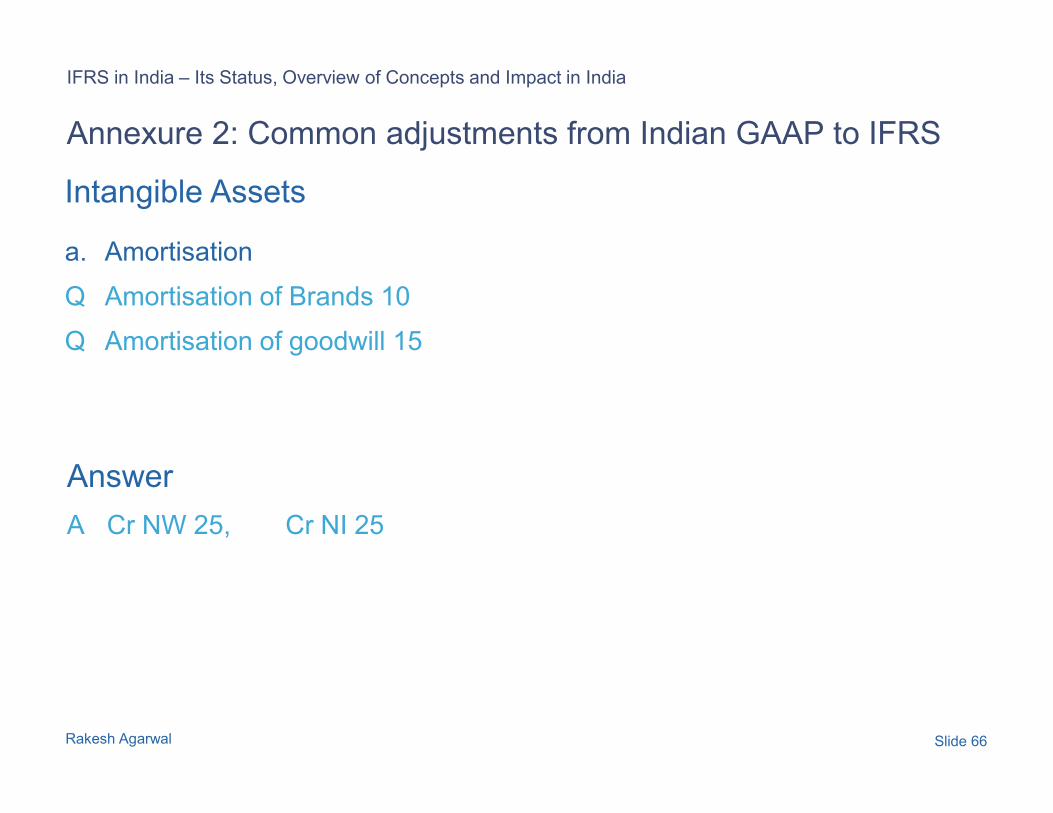

a. Amortisation

Q Amortisation of Brands 10

Q Amortisation of goodwill 15

Intangible Assets

IFRS in India – Its Status, Overview of Concepts and Impact in India

Annexure 2: Common adjustments from Indian GAAP to IFRS

Rakesh Agarwal Slide 66

Answer

A Cr NW 25, Cr NI 25

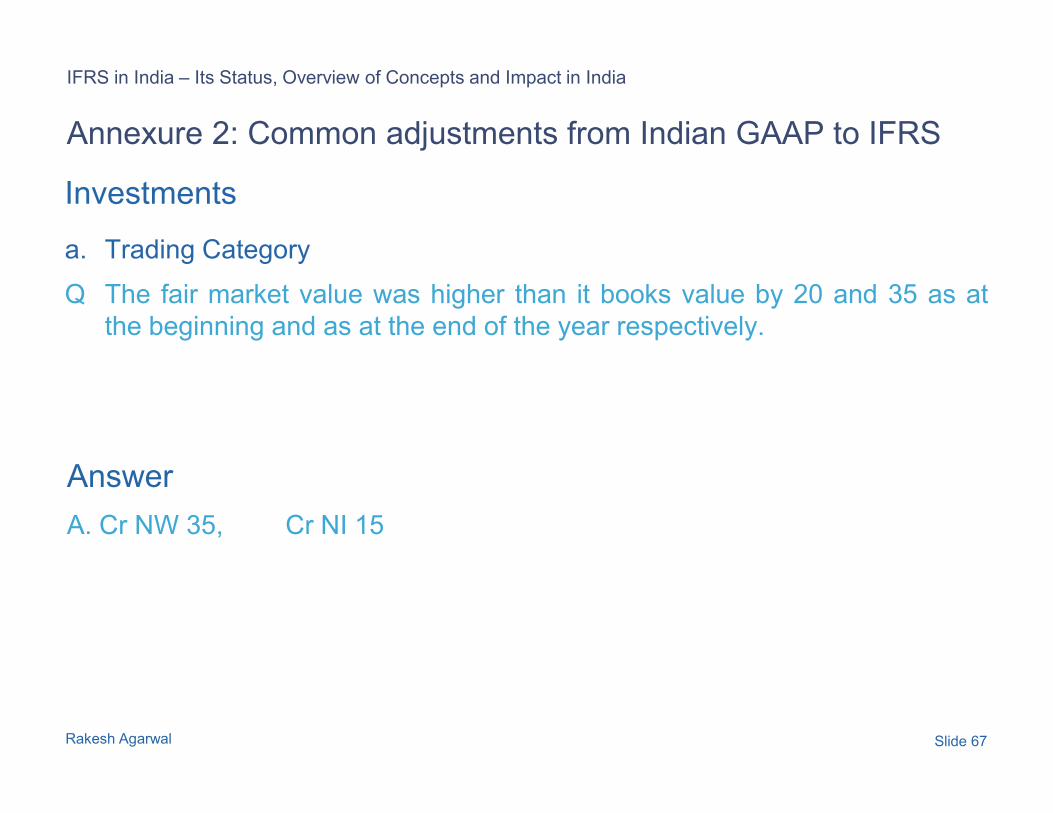

a. Trading Category

Q The fair market value was higher than it books value by 20 and 35 as at

the beginning and as at the end of the year respectively.

Investments

IFRS in India – Its Status, Overview of Concepts and Impact in India

Annexure 2: Common adjustments from Indian GAAP to IFRS

Rakesh Agarwal Slide 67

Answer

A. Cr NW 35, Cr NI 15

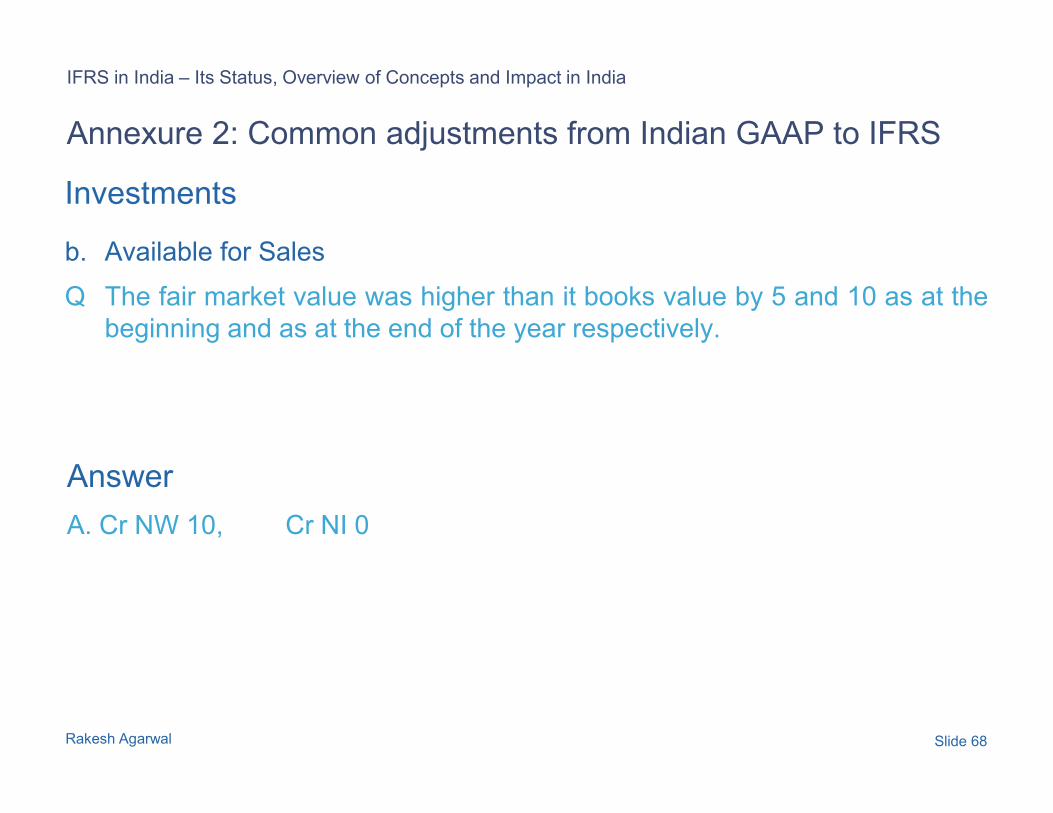

b. Available for Sales

Q The fair market value was higher than it books value by 5 and 10 as at the

beginning and as at the end of the year respectively.

IFRS in India – Its Status, Overview of Concepts and Impact in India

Annexure 2: Common adjustments from Indian GAAP to IFRS

Investments

Rakesh Agarwal Slide 68

Answer

A. Cr NW 10, Cr NI 0

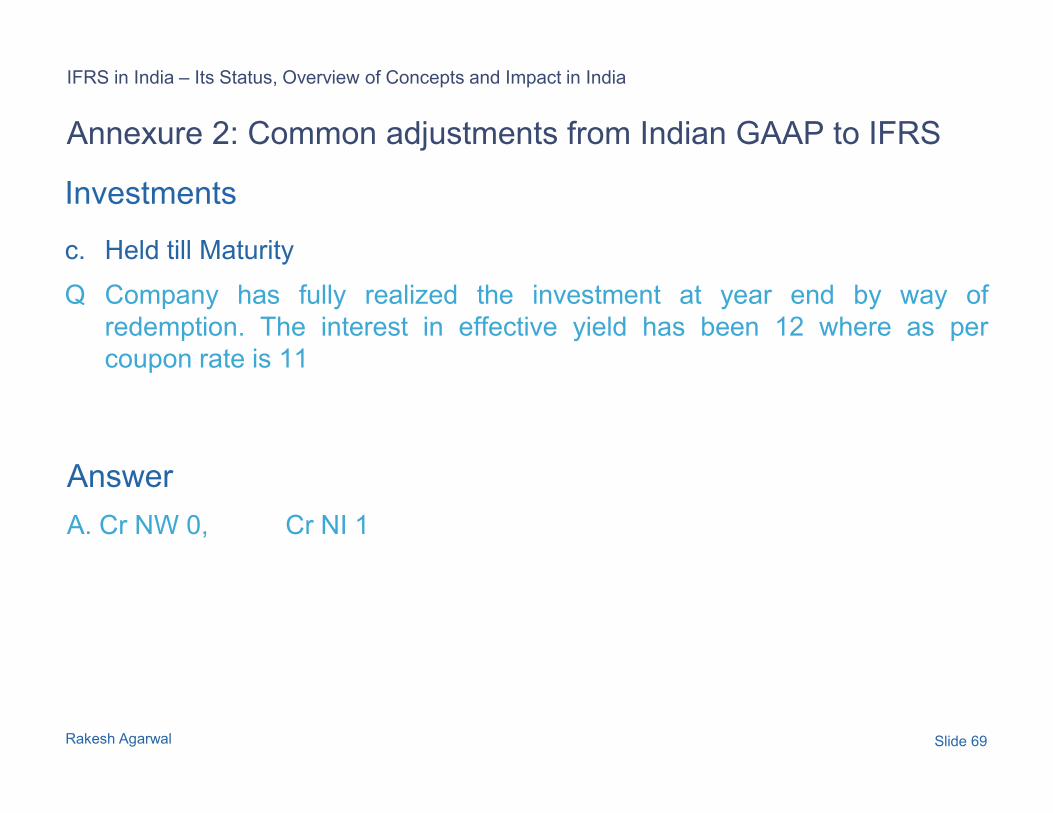

c. Held till Maturity

Q Company has fully realized the investment at year end by way of

redemption. The interest in effective yield has been 12 where as per

coupon rate is 11

Investments

IFRS in India – Its Status, Overview of Concepts and Impact in India

Annexure 2: Common adjustments from Indian GAAP to IFRS

Rakesh Agarwal Slide 69

Answer

A. Cr NW 0, Cr NI 1

a. Present Values

Q Fair value of interest free loan aggregating to 100 was 70 at the beginning

of the year which increased to 80 during the year

Loans and Advances

IFRS in India – Its Status, Overview of Concepts and Impact in India

Annexure 2: Common adjustments from Indian GAAP to IFRS

Rakesh Agarwal Slide 70

Answer

A. Dr NW 20, Dr NI 10

a. Redeemable Preference Shares

Q The aggregate of redeemable preference shares aggregates to 200

Share Capital

IFRS in India – Its Status, Overview of Concepts and Impact in India

Annexure 2: Common adjustments from Indian GAAP to IFRS

Rakesh Agarwal Slide 71

Answer

A. Dr NW 200, Dr NI 0

b. The Initial Cost on account of issuance of additional Equity Shares

Q The initial cost of equity issued during the year is 20. As the same was not

allowed to be carried forward under Indian GAAP (AS 26, intangible asset),

it was expensed off.

IFRS in India – Its Status, Overview of Concepts and Impact in India

Share Capital

Annexure 2: Common adjustments from Indian GAAP to IFRS

Rakesh Agarwal Slide 72

Answer

A. Dr NW 0, Cr NI 20

a. Premium on redemption

Q It is the contention of the company that the redemption of premium

aggregating to 50 shall be debited to share premium at the end of the loan

debenture term i.e. 5 years. This is the second year closing.

Debenture

IFRS in India – Its Status, Overview of Concepts and Impact in India

Annexure 2: Common adjustments from Indian GAAP to IFRS

Rakesh Agarwal Slide 73

Answer

A NW Dr 20, NI Dr 10

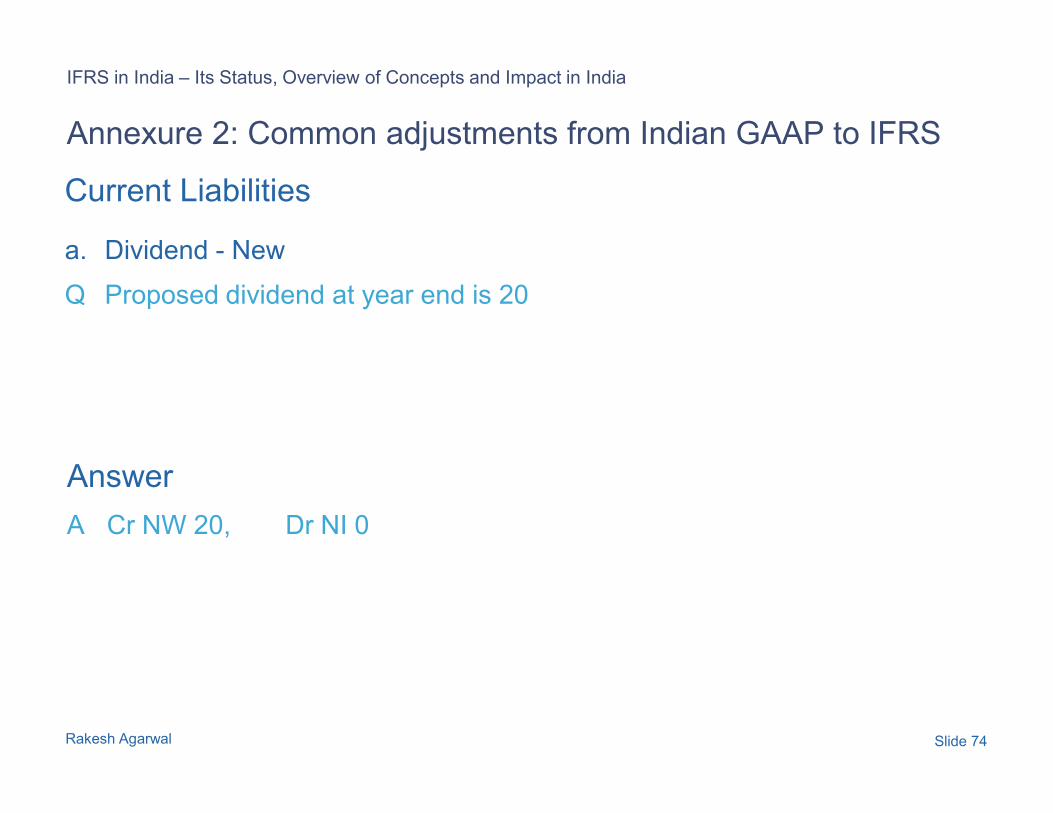

a. Dividend - New

Q Proposed dividend at year end is 20

Current Liabilities

IFRS in India – Its Status, Overview of Concepts and Impact in India

Annexure 2: Common adjustments from Indian GAAP to IFRS

Rakesh Agarwal Slide 74

Answer

A Cr NW 20, Dr NI 0

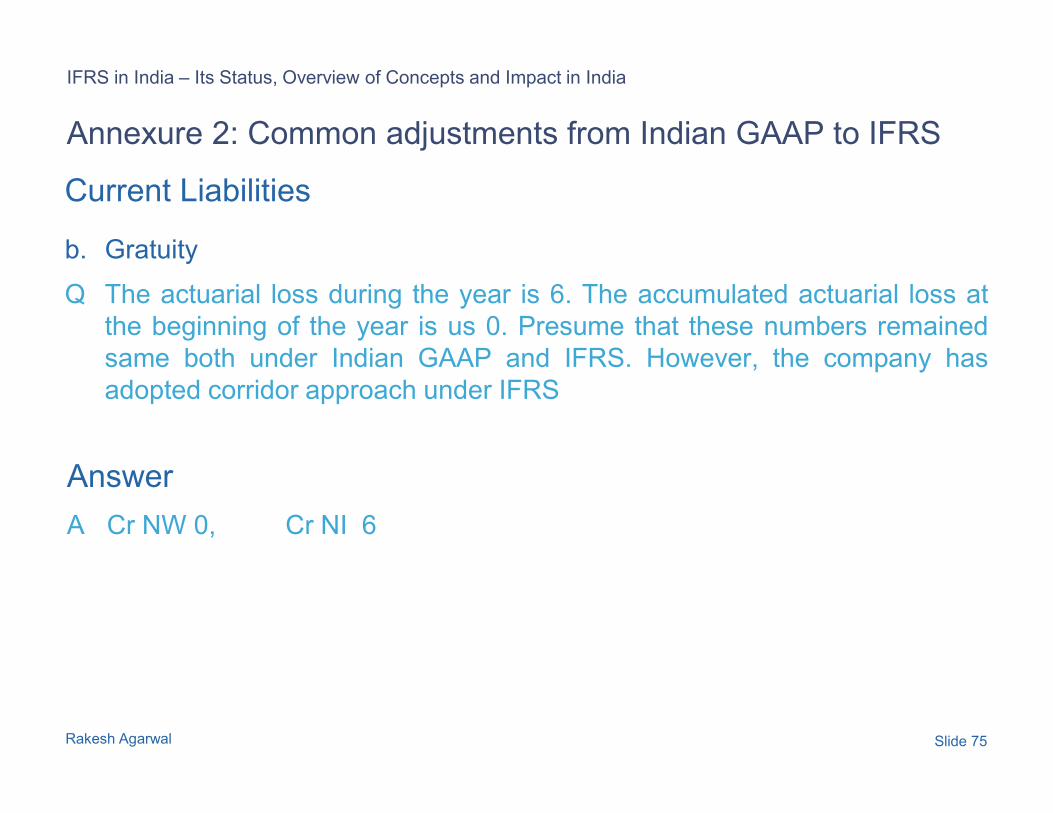

b. Gratuity

Q The actuarial loss during the year is 6. The accumulated actuarial loss at

the beginning of the year is us 0. Presume that these numbers remained

same both under Indian GAAP and IFRS. However, the company has

adopted corridor approach under IFRS

IFRS in India – Its Status, Overview of Concepts and Impact in India

Annexure 2: Common adjustments from Indian GAAP to IFRS

Current Liabilities

Rakesh Agarwal Slide 75

Answer

A Cr NW 0, Cr NI 6

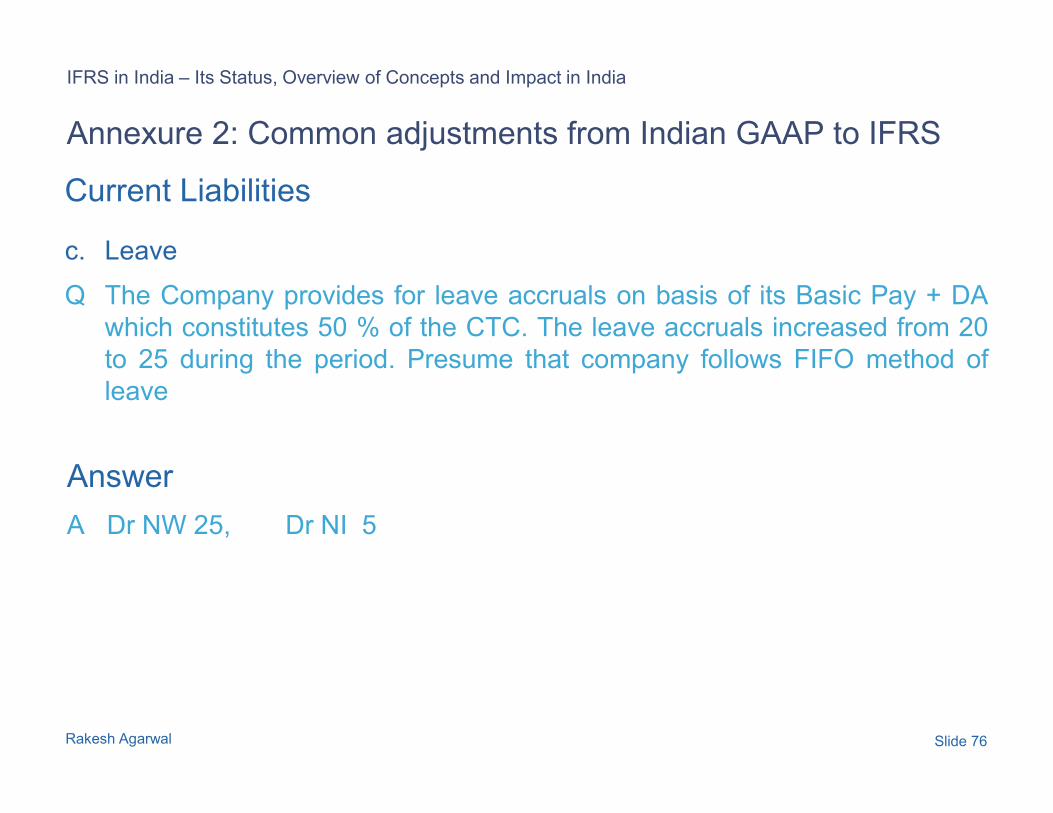

c. Leave

Q The Company provides for leave accruals on basis of its Basic Pay + DA

which constitutes 50 % of the CTC. The leave accruals increased from 20

to 25 during the period. Presume that company follows FIFO method of

leave

IFRS in India – Its Status, Overview of Concepts and Impact in India

Annexure 2: Common adjustments from Indian GAAP to IFRS

Current Liabilities

Rakesh Agarwal Slide 76

Answer

A Dr NW 25, Dr NI 5

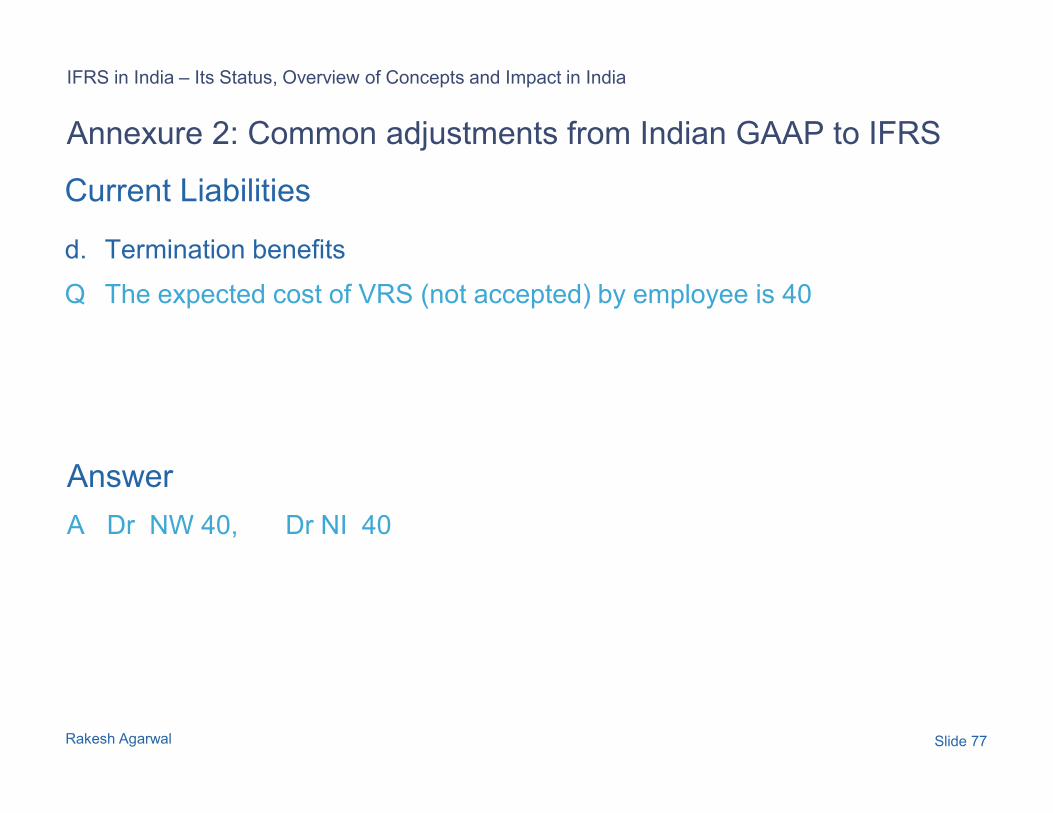

d. Termination benefits

Q The expected cost of VRS (not accepted) by employee is 40

IFRS in India – Its Status, Overview of Concepts and Impact in India

Annexure 2: Common adjustments from Indian GAAP to IFRS

Current Liabilities

Rakesh Agarwal Slide 77

Answer

A Dr NW 40, Dr NI 40

e. Accounting of Forward Cover – New

Q The company has entered into forward contracts having its gross premium

20 for a period of 6 months. As on the year end 3 months has expired, the

company amortized Rs.10 under Indian GAAP, it also obtained Mark to

Market on the said forward cover for the remaining term of maturity where

IFRS in India – Its Status, Overview of Concepts and Impact in India

Annexure 2: Common adjustments from Indian GAAP to IFRS

Current Liabilities

Rakesh Agarwal Slide 78

the Market Value is Rs.16.

Answer

A Cr NW 6, Cr NI 6

a. Entitlement basis

Q Oil Extracted but another venturer at MV 100. The company shall lift the

extra quantities in subsequent month. Presume impact of depletion and

other operating cost as 20

Revenue

IFRS in India – Its Status, Overview of Concepts and Impact in India

Annexure 2: Common adjustments from Indian GAAP to IFRS

Rakesh Agarwal Slide 79

Answer

A Cr NW 80, Cr NI 80

b. Production Testing Revenue – Oil and Gas

Q Production testing revenue taken to income 10. Net margin is 80 %

IFRS in India – Its Status, Overview of Concepts and Impact in India

Annexure 2: Common adjustments from Indian GAAP to IFRS

Revenue

Rakesh Agarwal Slide 80

Answer

A Cr NW 0, Dr NI 8

a. ESOP Scheme from Parent

Q The value of stock options granted and vested during the period by parent

co. to employees of the co is 80

Expenses

IFRS in India – Its Status, Overview of Concepts and Impact in India

Annexure 2: Common adjustments from Indian GAAP to IFRS

Rakesh Agarwal Slide 81

Answer

A Cr NW 0, Dr NI 80

b. Leave – As above

Done in current liabilities

IFRS in India – Its Status, Overview of Concepts and Impact in India

Annexure 2: Common adjustments from Indian GAAP to IFRS

Expenses

Rakesh Agarwal Slide 82

c. Gratuity – Actuarial Gains and Losses

Done in current liabilities

IFRS in India – Its Status, Overview of Concepts and Impact in India

Annexure 2: Common adjustments from Indian GAAP to IFRS

Expenses

Rakesh Agarwal Slide 83

d. Correction of Errors

Q Included in Income statement are errors of prior period charged to P& L

aggregating to 8

IFRS in India – Its Status, Overview of Concepts and Impact in India

Annexure 2: Common adjustments from Indian GAAP to IFRS

Expenses

Rakesh Agarwal Slide 84

Answer

A Cr NW 0, Cr NI 8

e. Changes in Accounting Policy

Q The cumulative catch up adjustments for a change in accounting policy

(depreciation) is reduction in depreciation by 16

IFRS in India – Its Status, Overview of Concepts and Impact in India

Annexure 2: Common adjustments from Indian GAAP to IFRS

Expenses

Rakesh Agarwal Slide 85

Answer

A Cr NW 0, Dr NI 16

a. GAAP Adjustments from Indian GAAP

Q How do you work out the DT impact of US GAAP ADJUSTMENTS

Deferred Tax

Given - The tax rate is 30 %

IFRS in India – Its Status, Overview of Concepts and Impact in India

Annexure 2: Common adjustments from Indian GAAP to IFRS

Rakesh Agarwal Slide 86

Answer

A Balance Sheet Approach

b. Items debited to reserves

Q An item of expenditure amounting to 30 was debited to reserves.

IFRS in India – Its Status, Overview of Concepts and Impact in India

Deferred Tax

Given - The tax rate is 30 %

Annexure 2: Common adjustments from Indian GAAP to IFRS

Rakesh Agarwal Slide 87

Answer

A Cr NW 9, Cr NI 0

c. Consolidation

Q List of inter-company profits getting eliminated on consolidation 20

IFRS in India – Its Status, Overview of Concepts and Impact in India

Deferred Tax

Given - The tax rate is 30 %

Annexure 2: Common adjustments from Indian GAAP to IFRS

Rakesh Agarwal Slide 88

Answer

A Cr NW 6, Cr NI 6

d. Outside Basis

Done in Consolidation

IFRS in India – Its Status, Overview of Concepts and Impact in India

Deferred Tax

Given - The tax rate is 30 %

Annexure 2: Common adjustments from Indian GAAP to IFRS

Rakesh Agarwal Slide 89

e. Probable v/s Virtually certain

Q The unabsorbed losses c/f from earlier period reduced from 200 to 150.

The was not recognized under Indian GAAP as the Company was not

virtually certain though it was probable

IFRS in India – Its Status, Overview of Concepts and Impact in India

Deferred Tax

Given - The tax rate is 30 %

Annexure 2: Common adjustments from Indian GAAP to IFRS

Rakesh Agarwal Slide 90

virtually certain though it was probable

Answer

A Cr NW 45, Dr NI 15

Annexure 3

Select IFRS tools and

publications

“Similarities and Differences:

A Comparison of IFRS, US GAAP and Indian GAAP.”

This new edition has been completely redesigned to

make it user-friendly and the key features of the new

publication are:

Annexure 3: Select IFRS tools and publicationsPricewaterhouseCoopers has a range of tools and publications to help companies apply IFRS

IFRS in India – Its Status, Overview of Concepts and Impact in India

Rakesh Agarwal Slide 92

1) Provides insight as to the impact of key differences

between IFRS, US GAAP and Indian GAAP,

2) Provides context of how the conversion to IFRS has

ramifications far beyond the accounting department, and

3) Encourages early consideration of what IFRS means to

your organisation.

This publication is available on www.pwc.com/india

A practical guide to share-based payments

Answers the questions we have been asked by entities

and includes practical examples to help management

draw similarities between the requirements in the

standard and their own share-based payment

arrangements. November 2008.

IFRS 3R: Impact on earnings – the crucial Q&A for

decision-makers

Guide aimed at finance directors, financial controllers

and deal-makers, providing background to the

standard, impact on the financial statements and

controls, and summary differences with US GAAP.

A practical guide to new IFRSs for 2009

40-page guide providing high-level outline of the key

requirements of new IFRSs effective in 2009, in

question and answer format.

IFRS disclosure checklist 2009

Outlines the disclosures required by all IFRSs

published up to October 2009.

Annexure 3: Select IFRS tools and publicationsPricewaterhouseCoopers has a range of tools and publications to help companies apply IFRS

IFRS in India – Its Status, Overview of Concepts and Impact in India

Rakesh Agarwal Slide 93

question and answer format.

A practical guide to capitalisation of borrowing

costs

Guidance in question and answer format addressing the

challenges of applying IAS 23R, including how to treat

specific versus general borrowings, when to start

capitalisation and whether the scope exemptions are

mandatory or optional.

IFRS pocket guide 2009

Provides a summary of the IFRS recognition and

measurement requirements. Including currencies,

assets, liabilities, equity, income, expenses, business

combinations and interim financial statements.

IAS 39 – Derecognition of financial assets in

practice

Explains the requirements of IAS 39, providing answers

to frequently asked questions and detailed illustrations

of how to apply the requirements to traditional and

innovative structures.

IFRS news

Monthly newsletter focusing on the business

implications of the IASB’s proposals and new

standards. Subscribe by emailing

A practical guide to segment reporting

Provides an overview of the key requirements of IFRS

8, ‘Operating Segments’ and some points to consider

as entities prepare for the application of this standard

for the first time. Includes a question and answer

section. Also available: Eight-page flyer on high level

management issues.

Illustrative consolidated financial statements

• Banking, 2009

• Insurance, 2009

• Investment property, 2009

• Private equity, 2009

• Investment funds, 2009

Realistic sets of financial statements – for existing

IFRS preparers in the above sectors – illustrating the

required disclosure and presentation.

Adopting IFRS – A step-by-step illustration of the Understanding financial instruments –

A guide to IAS 32, IAS 39 and IFRS 7

Annexure 3: Select IFRS tools and publicationsPricewaterhouseCoopers has a range of tools and publications to help companies apply IFRS

IFRS in India – Its Status, Overview of Concepts and Impact in India

Rakesh Agarwal Slide 94

Adopting IFRS – A step-by-step illustration of the

transition to IFRS

Illustrates the steps involved in preparing the first IFRS

financial statements. It takes into account the effect on

IFRS 1 of the standards issued up to and including

March 2004.

A guide to IAS 32, IAS 39 and IFRS 7

Comprehensive guidance on all aspects of the

requirements for financial instruments accounting.

Detailed explanations illustrated through worked

examples and extracts from company reports.

Financial instruments under IFRS

High-level summary of the revised financial instruments

standards issued in December 2003, updated to reflect

IFRS 7 in September 2006. For existing IFRS preparers

and first-time adopters.

SIC-12 and FIN 46R – The substance of control

Helps those working with special purpose entities to

identify the differences between US GAAP and IFRS

in this area, including examples of transactions and

structures that may be impacted by the guidance.

IAS 39 – Achieving hedge accounting in practice

Covers in detail the practical issues in achieving hedge

accounting under IAS 39. It provides answers to

frequently asked questions and step-by-step

illustrations of how to apply common hedging

strategies.

Acquisitions – Accounting and transparency

under IFRS 3Rd

Assesses the impact of the standard, highlighting the

key issues for management and raising questions for

the Board

IFRS manual of accounting 2010

Global guide to IFRS providing comprehensive practical

guidance on how to prepare financial statements in

accordance with IFRS. Includes hundreds of worked

examples and extracts from company reports. The

Manual is a three-volume set comprising:

• Manual of accounting – IFRS 2010

• Manual of accounting – Financial instruments 2010

• Illustrative IFRS corporate consolidated financial

statements for 2010 year ends

Comperio Your path to knowledge

Online library of financial reporting and assurance literature. Provides the full text of IASB International Auditing Practice Statements and

Annexure 3: Select IFRS tools and publicationsPricewaterhouseCoopers has a range of tools and publications to help companies apply IFRS

IFRS in India – Its Status, Overview of Concepts and Impact in India

Rakesh Agarwal Slide 95

Online library of financial reporting and assurance literature. Provides the full text of IASB International Auditing Practice Statements and

IPSAS. Also contains PwC’s IFRS and corporate publications, and Applying IFRS. For more information, visit www.pwc.com/comperio

Making the change to IFRS

This 12-page brochure provides a high-level overview of the key issues that companies need to consider in making the change to IFRS

IFRS for SMEs – Is it relevant for your business?

It outlines why some unlisted SMEs have already made the change to IFRS and illustrates what might be involved in a conversion process.

Thank You

Rakesh Agarwal

Associste Director, PricewaterhouseCoopers

E-mail : [email protected]

Mobile : +91 9820273458