IFRS 9 Lessons learned from first implementations 16 … · Discover and unlock your potential…...

43

Discover and unlock your potential… Hot topics treasury seminar IFRS 9 – Lessons learned from first implementations 16 June 2016

Transcript of IFRS 9 Lessons learned from first implementations 16 … · Discover and unlock your potential…...

Discover and unlockyour potential…

Hot topics treasury seminarIFRS 9 – Lessons learned from first implementations

16 June 2016

PwC

Program

Introduction and objectives Phase 1 – Classification and measurement Phase 2 – Impairments Phase 3 – Hedge Accounting Transition

16 June 2016Hot topics treasury seminar

2

Introduction and objectives

PwC

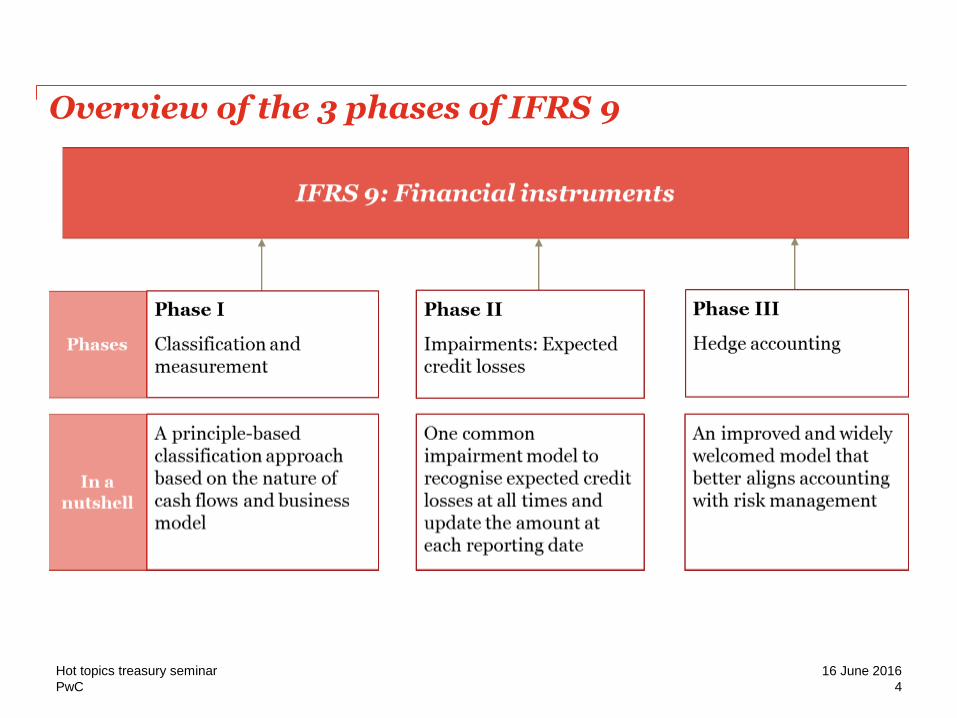

Overview of the 3 phases of IFRS 9

16 June 2016Hot topics treasury seminar

4

PwC

16 June 2016Hot topics treasury seminar

5

IFRS 9 – key milestones

Nov 2009 – Nov 2013

IASB develops the 3 phases of IFRS 9

2015-2016 (TBD)

Macro Hedging –IASB publishes exposure draft

Second half of 2016 (expected)

Expected EU endorsement of

IFRS 9, after which early adoption is

possible

July 2014

IASB publishes final IFRS 9

standard

2018

Effective date (excluding Macro

Hedging)

TBD

Effective date –Macro Hedging

PwC

16 June 2016Hot topics treasury seminar

6

Overview transition

• The effective date will be for annual periods starting on or after 1 January 2018.

• Retrospective application is required (in accordance with IAS 8) except:

- If transition application requires undue cost or effort, operational simplifications are provided.

- No requirement to restate comparatives.

• If a company does not restate its comparatives, the opening balance of the retained earnings should be adjustment to reflect the first time application

Phase 1 – Classification and measurement

PwC

Financial assets

16 June 2016Hot topics treasury seminar

8

IAS 39

Held to Maturity

Trading

Loans and receivables

IFRS 9

Available for Sale

Amortised cost

Fair Value

P&L

OCI

PwC

16 June 2016Hot topics treasury seminar

9

Decision tree

Phase 1 – Classification and measurement

Lessons learned from first implementations

PwC

Phase 1 – Classification and measurement

16 June 2016Hot topics treasury seminar

11

Step 1: Gap analysis

Accounting analysis per FSLI to determine the classification and measurement according to IFRS 9.

Challenges:

• Create homogeneous portfolios (per type, geographic area, etc.) of financial assets to perform the analysis;

• Detailed knowledge of the contracts is required and the information is sometimes only available locally;

• When performing the assessment for IFRS 9, discussions with respect to the IAS 39 classification might reopen (e.g. prefinancing contract).

Outcome:

• Scoping of the relevant financial instruments assets for further procedures;

• For the straightforward assets (i.e. no risk on change of measurement), the classification and measurement were determined during this phase.

PwC

Phase 1 – Classification and measurement

16 June 2016Hot topics treasury seminar

12

Step 2: Business Model Assessment

Determination of the classification for the debt instruments based on the business model assessment.

Challenges:

• Translate accounting requirements and terminology to a tailor made questionnaire, understandable for people without an accounting background;

• Determine a sample of contracts to be tested per portfolio to determine the business model of the portfolio;

• For financial assets that do not belong to a portfolio, the assessment should be performed on an individual level. Please note that this is an exceptional case;

• Review of the questionnaire filled in by different persons and reach homogeneous conclusion.

Outcome:

• The business model is assessed and documented per portfolio

PwC

Phase 1 – Classification and measurement

16 June 2016Hot topics treasury seminar

13

Step 3: SPPI test

Determination of the classification for the debt instruments based on SPPI test.

Challenges:

• Interpret the SPPI requirements and scope the relevant requirements. The requirements are extensive and can be difficult to assess;

• Design tailor made SPPI test understandable for people with no accounting background;

• Review of the questionnaire filled in by different persons and reach homogeneous conclusion.

Outcome:

• The test was deemed to be irrelevant for the trade debtors with short maturity contracts;

• The SPPI test was performed and documented per portfolio.

Phase 2 – Impairments

PwC

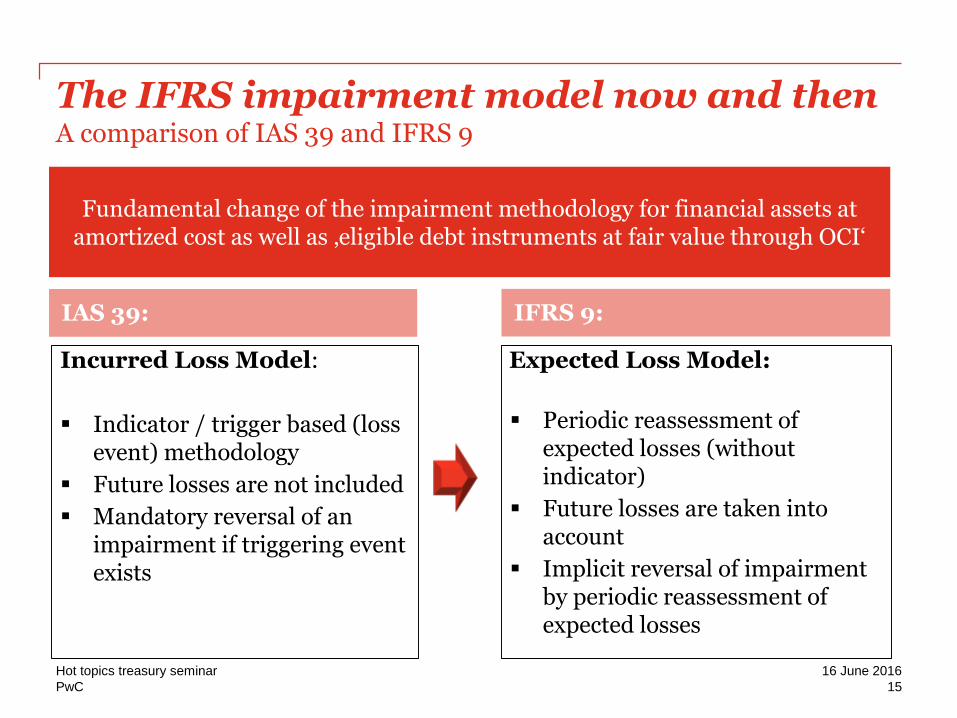

The IFRS impairment model now and thenA comparison of IAS 39 and IFRS 9

16 June 2016Hot topics treasury seminar

15

IAS 39: IFRS 9:

Fundamental change of the impairment methodology for financial assets at amortized cost as well as ‚eligible debt instruments at fair value through OCI‘

Incurred Loss Model:

Indicator / trigger based (loss event) methodology

Future losses are not included

Mandatory reversal of an impairment if triggering event exists

Expected Loss Model:

Periodic reassessment of expected losses (without indicator)

Future losses are taken into account

Implicit reversal of impairment by periodic reassessment of expected losses

PwC

The IFRS impairment model now and thenA comparison of IAS 39 and IFRS 9

16 June 2016Hot topics treasury seminar

16

• Risk provision model depends on IAS 39 category:

• LAR/HTM: recoverable amount as reference for calculation of risk provision

• AFS: impairment based on fair value

• Loan commitments and financial guarantees in accordance with IAS 37 and IAS 18

• No rules for purchased or originated credit-impaired financial assets (POCI)

• No exemptions for lease and trade receivables

IFRS 9Expected Loss Model

• Generally one impairment model for:

• instruments at amortised cost

• fair value through OCI debt instruments

• loan commitments

• financial guarantees

• Special rules for purchased or originated credit-impaired financial assets (POCI)

• Simplified approach for lease and trade receivables

IAS 39Incurred Loss Model

PwC

Expected credit lossesOverview on the model of IFRS 9

16 June 2016Hot topics treasury seminar

17

Financial Assets at Amortised Cost

Approach for purchased or originated credit-impaired

financial assets (POCI)

Simplified Approach‘Full Lifetime-ECL Model’

General Approach‘Credit Deterioration Model’

• 12-months expected credit loss (ECL) at initial recognition

• Lifetime-ECL if significant increase in credit risk (unless they have low credit risk at the reporting date)

• No risk provision at initial recognition• Recognition of a (positive or negative)

risk provision in amount of the change of the Lifetime-ECL

• Lifetime ECL at initial recognition and subsequent measurement

Financial Assets FVOCI

Irrevocable loan commitments and financial guarantees (if not FVPL)

Lease receivable (option)

Trade receivable or contract asset that contain a significant

financing component (option)

Financial Assets at AC or FVOCI, that are ‚credit-impaired‘ at initial

recognition (Impairment definition similar to IAS 39)

Trade receivable or contract asset that do not contain a significant

financing component(or when the practical expedient

for contracts that are one year or less is applied)

Trade receivable or contract asset that contain a significant

financing component (option)

Lease receivable (option)Accounting policy choice

Accounting policy choice

PwC

Impairment of financial assetsGeneral model

16 June 2016Hot topics treasury seminar

18

Effective interest on gross carrying amount

Lifetime ECL12 month ECL

Recognition of ECL

Interest revenue

Change in credit quality since initial recognition

Stage 1 Stage 2 Stage 3

Performing(Initial recognition*)

Underperforming(Assets with significant increase

in credit risk since initial recognition* )

Non-performing(Credit impaired assets)

Lifetime ECL

Effective interest on gross carrying amount

Effective interest on amortised cost carrying

amount (i.e. net of credit allowance)

Phase 2 – Impairments

Lessons learned from first implementations

PwC

Phase 2 – Impairments

16 June 2016Hot topics treasury seminar

20

Step 1: Scoping

Define the scope of instruments for which an impairment analysis should be performed.

Challenges:

• Timing issue: Phase 1 was not finished, therefore the scoping process was complicated. Ideally, phase 1 should be finished before phase 2 can be started.

Outcome:

• Debt instruments recorded at amortized cost or fair value through OCI are in scope. Impairment analysis was to be performed for loan receivables and trade receivables.

PwC

Phase 2 – Impairments

16 June 2016Hot topics treasury seminar

21

Step 2a: Impairment of loan receivables

Define how to implement phase 2 on loan receivables of corporates.

Challenges:

• Limited policies and information regarding credit risk were available;

• Create groups based on shared credit risk characteristics (e.g. instrument, rating, term to maturity, etc.)

• Determine whether practical expedient for low credit risk assets can be applied;

• How to determine the PD and LGD without public information available.

Outcome:

• The practical expedient was applied for performing assets, on an individual basis;

• A sensitivity analysis was performed to quantify fluctuations in PD and LGD;

• No significant credit risk was present at reporting date.

PwC

Phase 2 – Impairments

16 June 2016Hot topics treasury seminar

22

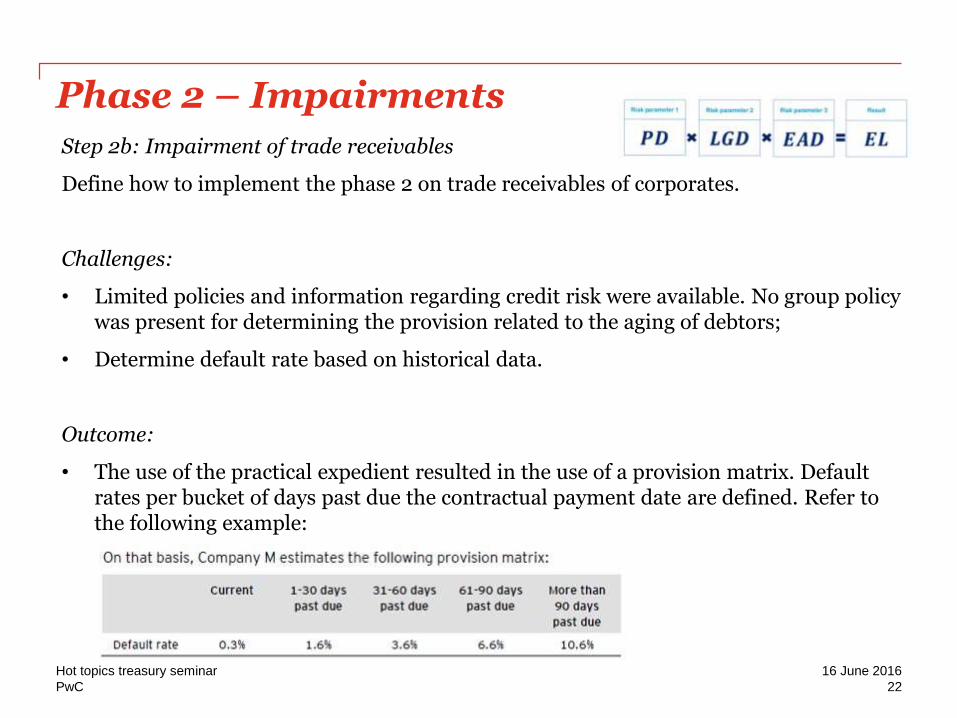

Step 2b: Impairment of trade receivables

Define how to implement the phase 2 on trade receivables of corporates.

Challenges:

• Limited policies and information regarding credit risk were available. No group policy was present for determining the provision related to the aging of debtors;

• Determine default rate based on historical data.

Outcome:

• The use of the practical expedient resulted in the use of a provision matrix. Default rates per bucket of days past due the contractual payment date are defined. Refer to the following example:

Phase 3 – Hedge accounting

PwC

IFRS 9 – what has changed?

16 June 2016Hot topics treasury seminar

24

Good news Challenges

• Hedging/hedged instruments: Allowed to hedge components of non-financial items Ability to hedge a net position, bottom layer and

aggregated exposures Possible to defer changes in aligned time value of

options in OCI Possible to recognise fair value changes of forward

points in OCI• Hedge effectiveness:

Reduces administrative burden of testing effectiveness retrospectively

Removal of arbitrary 80-125% bright line Rebalancing – no need for de-designation

• Voluntary de-designation prohibited• Hedge needs to reflect risk management strategy• Risk policy has to be formalised• IAS 39 can still be applied• Cash flow hedges of net positions only allowed for FX

risk• Re-balancing mandatory• TMS able to support all IFRS 9 requirements?

Background:

• Hedge accounting under IAS 39 is complex and difficult to achieve

• Risk management activities cannot be understood by analysing hedge accounting in the financial statement

Objective

• Allow companies to better reflect their risk management activities in the financial statements

• Help investors to understand the effect of hedging on the financial statements and on future cash flows

PwC

IFRS 9 – what has NOT changed?

16 June 2016Hot topics treasury seminar

25

Basic hedge accounting models

retained(i.e. FVH, CFH & NIH)

Hedge accounting is optional/priviliged Detailed rules on

eligible hedged items and hedging instruments

Documentation still needed

Derivatives still at fair value

(Classification)

Ineffectiveness recognised in P&L

PwC

Hedge accounting is a right, you need to work hard to earn it….

16 June 2016Hot topics treasury seminar

26

An entity’s risk management strategy is central to the objective of hedge accounting under IFRS 9.

Hedge accounting is an exception to the normal accounting rules and so some restrictions are necessary to determine whether or not a proposed hedging relationship qualifies for hedge accounting.

An entity is only allowed to apply hedge accounting if it meets the specified qualifying criteria.

To qualify for hedge accounting all of the following three conditions should be met:

Only eligible hedging instruments and eligible hedged items

Meet the hedge effectiveness requirements

Formal designation and hedge documentation on time

Phase 3 – Hedge accounting

Lessons learned from first implementations

PwC

Phase 3 – Hedge accounting

16 June 2016Hot topics treasury seminar

28

Step 1:

Align existing hedge relationships with the IFRS 9 requirements.

Challenges:

• Converting the IAS 39 hedge documentation to IFRS 9 compliant hedge documentation;

• Determining the required level of detail for the hedging strategy.

Results:

• Hedge documentation is aligned with IFRS 9;

• IAS 39 hedge relationships can be continued when they are adjusted to qualify with hedge accounting requirements from IFRS 9.

Transition

PwC

Overview transition

16 June 2016Hot topics treasury seminar

30

• The effective date will be for annual periods starting on or after 1 January 2018.

• Restatement of the comparatives is not required but permitted if no use of hindsight

• If a company does not restate its comparatives, the opening balance of the retained earnings should be adjustment to reflect the first time application

PwC

Phase 1 – Classification and measurementTransition requirements

16 June 2016Hot topics treasury seminar

31

• If a company does not restate its comparatives, the opening balance of the retained earnings should be adjustment to reflect the first time application (e.g. difference between previous carrying amount and the carrying amount at initial application)

• Management is required to perform:

− the Business Model test based on circumstances and facts that exist as at the date of initial application

− the Solely Payment of Principal and Interest (SPPI test) based on the facts and circumstances that exist on the date of the instrument’s initial recognition

• Designation at fair value through P&L or OCI (equity investments) is performed at the date of initial application.

• Additional Disclosure requirements related to the transition

PwC

Phase 1 – Classification and measurementTransition disclosures (1/4)

16 June 2016Hot topics treasury seminar

32

• Additional quantitative disclosures are required on transition

• Reconciliation between the original measurement categories under IAS 39 and the new measurement categories under IFRS 9.

• Additional disclosures for reclassifications between categories upon transition

• Additional qualitative information is required to be disclosed

PwC

Phase 1 – Classification and measurementTransition disclosures (2/4)

16 June 2016Hot topics treasury seminar

33

• Example disclosures for Financial Assets at FVTPL / FVTOCI

PwC

Phase 1 – Classification and measurementTransition disclosures (3/4)

16 June 2016Hot topics treasury seminar

34

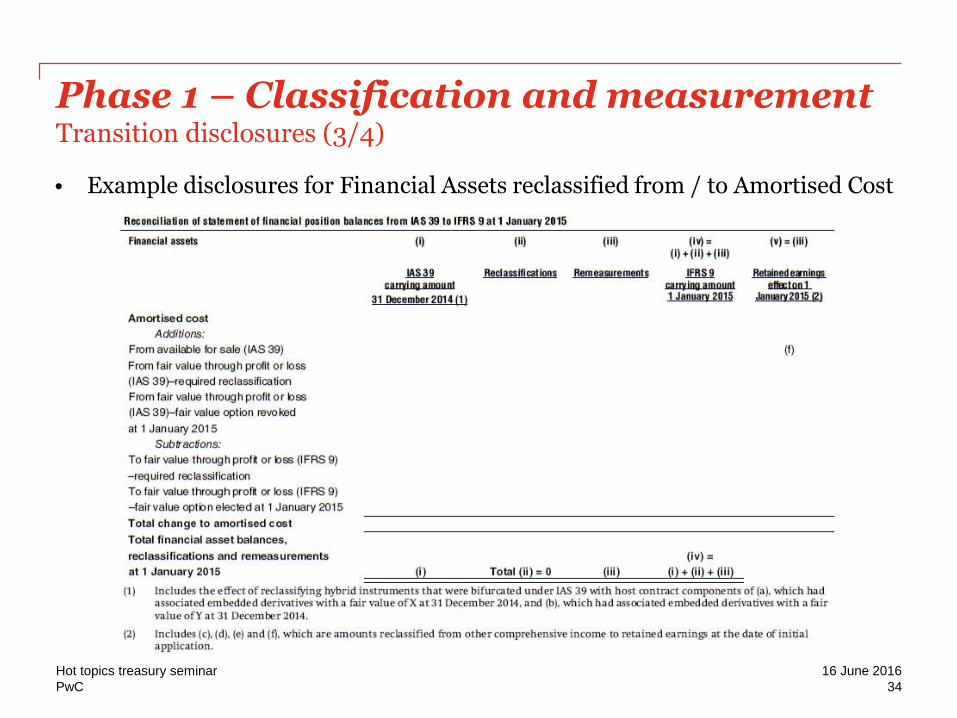

• Example disclosures for Financial Assets reclassified from / to Amortised Cost

PwC

Phase 1 – Classification and measurementTransition disclosures (4/4)

16 June 2016Hot topics treasury seminar

35

• Example disclosures for Financial Liabilities

PwC

Phase 2 – ImpairmentsTransition requirements

16 June 2016Hot topics treasury seminar

36

• At the date of initial application, an entity must determine whether there has been a significant increase in credit risk since initial recognition however an entity may apply:

− the low credit risk simplification for those financial instruments that are deemed to have a low credit risk at the date of initial application;

− The ‘30 days past due’ rebuttable presumption if, and only if, management identifies significant increases in credit risk since initial recognition.

• The entity approximates the credit risk on initial recognition by considering information that is reasonably available without undue cost or effort. The following source of information could be used:

− Information from internal reports and statistics

− Information about similar products

− Peer group experience for comparable financial instruments.

PwC

Phase 2 – ImpairmentsTransition disclosures (1/4)

16 June 2016Hot topics treasury seminar

37

• At the date of Initial Application

• Reconciliation of the ending allowances in accordance to IAS 39 (incurred loss model) and the opening loss allowance determined under IFRS 9 (expected loss model)

• Entity provide these disclosures by measurement category in accordance with IAS 39 and IFRS 9, showing separately the effect of changes in measurement category on the loss allowance at the Date of Initial Application.

PwC

Phase 2 – ImpairmentsTransition disclosures (2/4)

16 June 2016Hot topics treasury seminar

38

• Loss allowances provision for loan to customers

Eur'MPerform ing

Under-

perform ing

Non-

perform ingT otal

Closing loss allowance as at 30 December 2017

(calculated under IAS 39)

Amounts restated through the opening retained

earnings

Opening loss allowance as at 1 January 2018

(calculated under IAS 39)

Indiv idual financial assets transferred to under-

performing (lifetime expected credit losses)

Indiv idual financial assets transferred to non-

performing (credit-impaired financial assets)

New financial assets originated or purchased

Write-offs

Recoveries

Other changes

Closing loss allowance as at 31 Decem ber 2015

(calculated under IFRS 9)

PwC

Phase 2 – ImpairmentsTransition disclosures (3/4)

16 June 2016Hot topics treasury seminar

39

• Qualitative information related to loans to customers

PwC

Phase 2 – ImpairmentsTransition disclosures (4/4)

16 June 2016Hot topics treasury seminar

40

• Provision matrix Trade Receivables (IFRS 9.IE74-IE77)

PwC

Phase 3 – Hedge accountingTransition requirements

16 June 2016Hot topics treasury seminar

41

• Accounting policy choice to apply IFRS 9 or IAS 39

• Prospective application of IFRS 9 except in some specific situations (IFRS 9.7.7.26)

• To apply IFRS 9 from the date of initial application, all IFRS 9 qualifying criteria must be met as at that date

• On initial application of the IFRS 9 hedge accounting requirements, an entity:

− may start to apply those requirements from the same point in time as it ceases to apply the hedge accounting requirements of IAS 39; and

− shall consider the hedge ratio in accordance with IAS 39 as the starting point for rebalancing the hedge ratio of a continuing hedging relationship, if applicable. Any gain or loss from such a rebalancing shall be recognised in profit or loss.

• Hedge documentation must be updated in accordance to IFRS 9 requirements

• No additional transition disclosures are required

PwC

Questions…

16 June 2016Hot topics treasury seminar

42

More information

Trainer:Kees-Jan de VriesPhone number: +31 (0)88 792 4922E-mail: [email protected]

Trainer:Aliénor FromontPhone number: +31 (0)88 792 6494E-mail: [email protected]