Financial Performance Reporting, IFRS Implementation, and ...

IFRS 9 – Implementation challenges

18 June 2015

Page 2

Introduction: What you need to know?

Page 3

Introduction to IFRS 9 (1)

What do you need to know about IFRS 9 in relation to the classification and measurement

► The objective of the IFRS 9 is to set out the requirements for recognizing and measuring financial assets, financial liabilities and some contracts to buy or sell non-financial items.

► Financial assets are measured at amortized cost, FVPL or FVOCI.

► The new FVOCI measurement category has different treatment for debt and equity instruments. In case of equity securities, unlike debt instruments, gains and losses in OCI are not recycled upon sale and there is no impairment accounting.

Page 4

Introduction to IFRS 9 (2)

What do you need to know about IFRS 9 in relation to the classification and measurement

► The classification of debt assets depends on two principle-based assessments:

► the entity’s business model for managing the financial asset, and

► the financial asset’s contractual cash flow characteristics.

► Apart from the ‘own credit risk’ requirements, classification and measurement of financial liabilities is unchanged from existing requirements of IAS 39.

► The rules for embedded derivatives treatment for financial assets are changed as are the rules for reclassifications, while derecognition rules remain widely unchanged.

Page 5

Introduction to IFRS 9 (3)

What do you need to know about IFRS 9 in relation to impairment

► The impairment requirements in IFRS 9 are based on an expected credit loss model

► The expected credit loss model applies to all debt assets recorded at amortized costs or at fair value through other comprehensive income

► Entities are required to recognize either 12-month or lifetime expected credit losses

► The measurement of expected credit losses should reflect a probability-weighted outcome, the time value of money and reasonable and supportable information that is available without undue cost or effort

Page 6

Classification and Measurement

Page 7

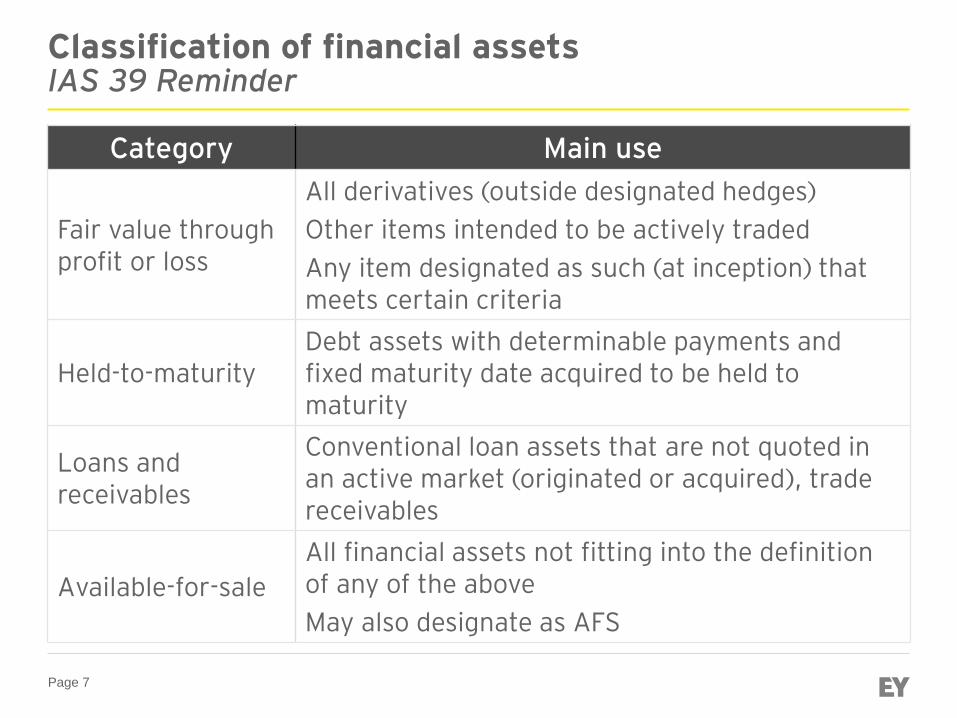

Classification of financial assets IAS 39 Reminder

Category Main use

Fair value through profit or loss

All derivatives (outside designated hedges)

Other items intended to be actively traded

Any item designated as such (at inception) that meets certain criteria

Held-to-maturity Debt assets with determinable payments and fixed maturity date acquired to be held to maturity

Loans and receivables

Conventional loan assets that are not quoted in an active market (originated or acquired), trade receivables

Available-for-sale

All financial assets not fitting into the definition of any of the above

May also designate as AFS

Page 8

Financial instruments at FV through P&L IAS 39 Reminder

► A financial asset (or financial liability) at fair value through profit or loss is one that is either: ► Held for trading (by definition) Or ► Designated at initial recognition (so-called ‘fair value option’)

► A financial instrument shall be classified as held for trading if it is: ► Acquired or incurred principally for the purpose of selling or

repurchasing it in the near term ► Part of a portfolio of identified financial instruments that are

managed together and for which there is evidence of a recent actual pattern of short-term profit-taking

Or ► A derivative (except for designated and effective hedging

instruments)

Page 9

IFRS 9 classification and measurement model

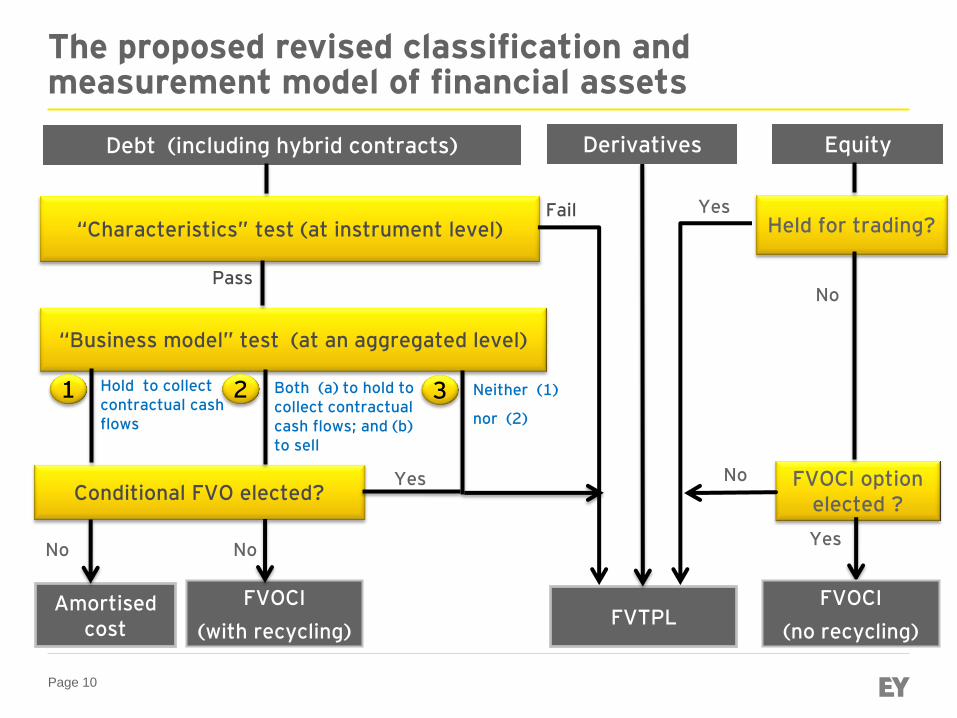

IFRS 9 defines 3 categories:

► Amortised cost: if the contractual cash flows characteristics represent solely payments of principal and interest AND the asset or portfolio has a ‘held to collect’ business model

E.g. Plain vanilla debt securities including hybrid contracts

► Fair value through other comprehensive income: for assets that: - Pass the ‘contractual cash flow characteristics’ test; and - Are managed in a ‘hold and sell’ business model Debt instruments including loans (some AFS in IAS 39)

► Fair value through profit or loss: residual category

E.g. Derivatives, equity, structured instruments, contractually linked instruments

Page 10

The proposed revised classification and measurement model of financial assets

Debt (including hybrid contracts)

“Characteristics” test (at instrument level)

“Business model” test (at an aggregated level)

Conditional FVO elected?

Fail

Pass

No

Amortised cost

FVTPL FVOCI

(with recycling)

Hold to collect contractual cash flows

Neither (1)

nor (2)

Both (a) to hold to collect contractual cash flows; and (b) to sell

1 3 2

No

Yes

Derivatives Equity

Held for trading?

FVOCI option elected ?

Yes

No

No

Yes

FVOCI

(no recycling)

Page 11

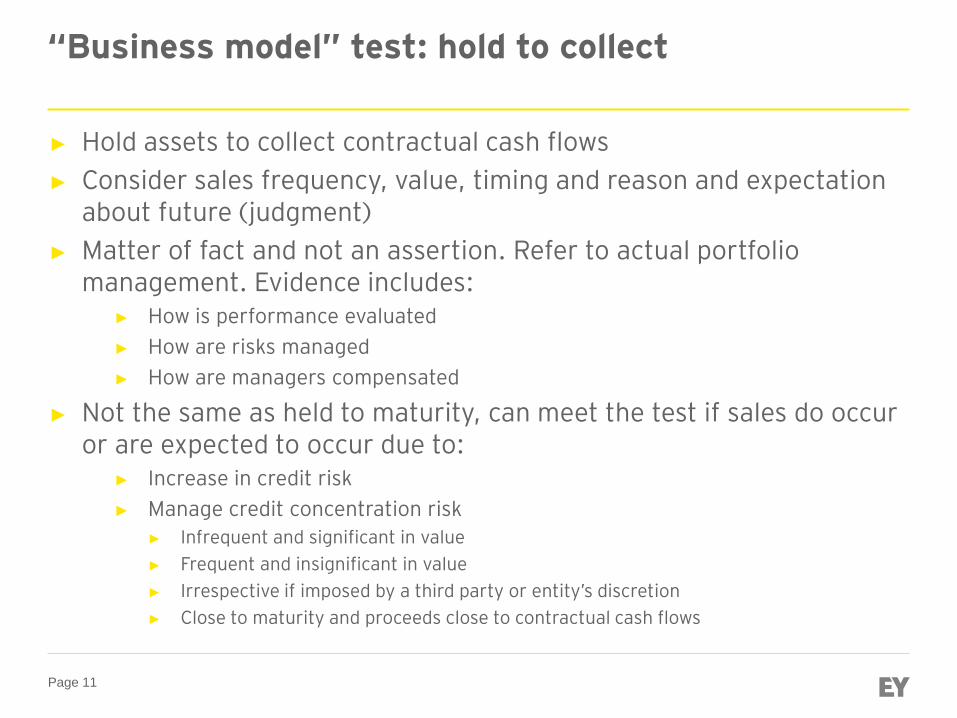

“Business model” test: hold to collect

► Hold assets to collect contractual cash flows

► Consider sales frequency, value, timing and reason and expectation about future (judgment)

► Matter of fact and not an assertion. Refer to actual portfolio management. Evidence includes:

► How is performance evaluated

► How are risks managed

► How are managers compensated

► Not the same as held to maturity, can meet the test if sales do occur or are expected to occur due to:

► Increase in credit risk

► Manage credit concentration risk

► Infrequent and significant in value

► Frequent and insignificant in value

► Irrespective if imposed by a third party or entity’s discretion

► Close to maturity and proceeds close to contractual cash flows

Page 12

“Business model” test: hold to collect

► The entity does not hold its receivables to collect cash

flows, it actually sells them. Consequently the business

model is not “hold to collet”.

► The entity should classify such receivables as fair value

thought profit or loss.

An entity has a past practice of factoring its receivables, such that the significant risks and rewards are transferred from the entity, resulting in the original receivables being derecognised from the statement of financial position. Is the business model “hold to collect”? How should the receivables be classified?

Page 13

“Business model” test: hold to collect

► The entity’s business model might still be “hold to collet”

as the receivables are not derecognised.

► Classification depends on the “Contractual characteristics”

test – will most probably be passed.

Same scenario as in previous example but this time the significant risks and rewards of the receivables are not transferred from the entity, and the receivables do not qualify for derecognition. Is the business model “hold to collect”? How should the receivables be classified?

Page 14

“Business model” test: both to collect and sell

► Hold assets both to collect cash flows and to sell

► For example:

► Manage everyday liquidity needs

► Involves greater frequency and value of sales (as compared to ‘hold to collect’), however no threshold

► The same as ‘Not held for trading’?

► Implementation considerations:

► Change in business model?

► Business model on first time application

Page 15

FVOCI category – debt investments

► Fair Value through Other Comprehensive Income measurement will apply to a portfolio where the entity’s primary objective is both:

► (1) To hold to collect contractual cash flows, and

► (2) To sell financial assets

► As compared to AfS in IAS 39:

► Only financial assets with contractual cash flows that are solely principal and interest would qualify for FVOCI

► Not a free choice nor a residual category

Page 16

FVOCI category – ED Example

► A non-financial entity anticipates a capital expenditure in a few years.

► The entity invests its excess cash in financial assets in order to fund the expenditure when the need arises.

► The entity’s objective for managing the financial assets is to maximise the return on those financial assets.

► Accordingly, the entity will sell financial assets and re-invest the cash in financial assets with a higher yield when an opportunity arises.

► The managers responsible for the portfolio are remunerated based on the return generated by the financial assets.

Page 17

FVOCI mechanics – debt investments treatment

► Interest income will be recognised using the EIR method

► Impairment losses / reversals will be recognised in profit or loss in a similar manner as for assets measured at amortised cost

► Net cumulative fair value gains or losses (except for impairment and foreign currency) are recognised in other comprehensive income

► then recycled to profit or loss only upon derecognition (parallel AfS in IAS 39)

Page 18

Impairment

Page 19

Impairment under IAS 39 Reminder

► Impairment losses are required to be recognised in profit

or loss if there is objective evidence that a ‘loss event’

has occurred, and that loss event has an impact on the

estimated future cash flows of the financial asset or group

of financial assets that can be reliably estimated.

► Includes observable data

► Excludes losses expected on future events

► An entity shall assess, at the end of each reporting period,

whether there is any objective evidence that a financial

asset or group of financial assets is impaired.

Page 20

► Examples of loss events:

► significant financial difficulty of issuer

► a breach of contract such as failure to make interest/principal

payments

► high probability of bankruptcy or other financial reorganization

► for economic or legal reasons relating to borrower’s financial

difficulty, lender grants concessions that the lender would not

otherwise consider

► historical pattern or observable data indicating a measurable

decrease in estimated cash flows from a group of financial

assets since initial recognition, although decrease cannot be

identified with individual assets

IAS 39 requirements for loans and receivables

Page 21

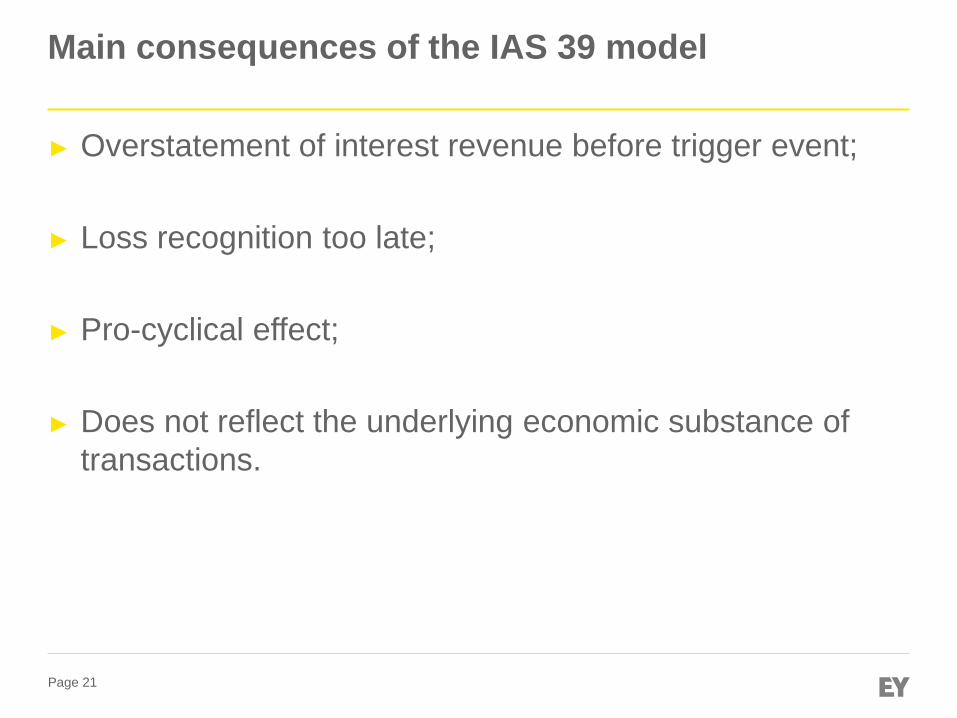

Main consequences of the IAS 39 model

► Overstatement of interest revenue before trigger event;

► Loss recognition too late;

► Pro-cyclical effect;

► Does not reflect the underlying economic substance of

transactions.

Page 22

From IAS 39 to IFRS 9 Impairment

Good book

(no impairment)

IAS 39

Method A

Impaired

Specific allowances

Lifetime EL

Impaired

Specific allowances

Lifetime EL

IFRS 9

Receivables

Stage 1

Method B

IBNR

provisions

‘Emergence

Period’ length

expected loss

No change

expected

Expected

increase of

impairments

Receivables

12M EL Impairment allowance

Exposures without significant

deterioration since initial

recognition

Lifetime EL Impairment

allowance

Exposures with significant

deterioration since initial

recognition

Significant

deterioration ► Key

methodological

analysis

► Choice of

indicator

► Calibration

Example based on common impairment approaches under IAS 39:

After

Good Book

IBNR

provisions

‘Emergence

Period’ length

expected loss Stage 2

Stage 3

Before

Page 23

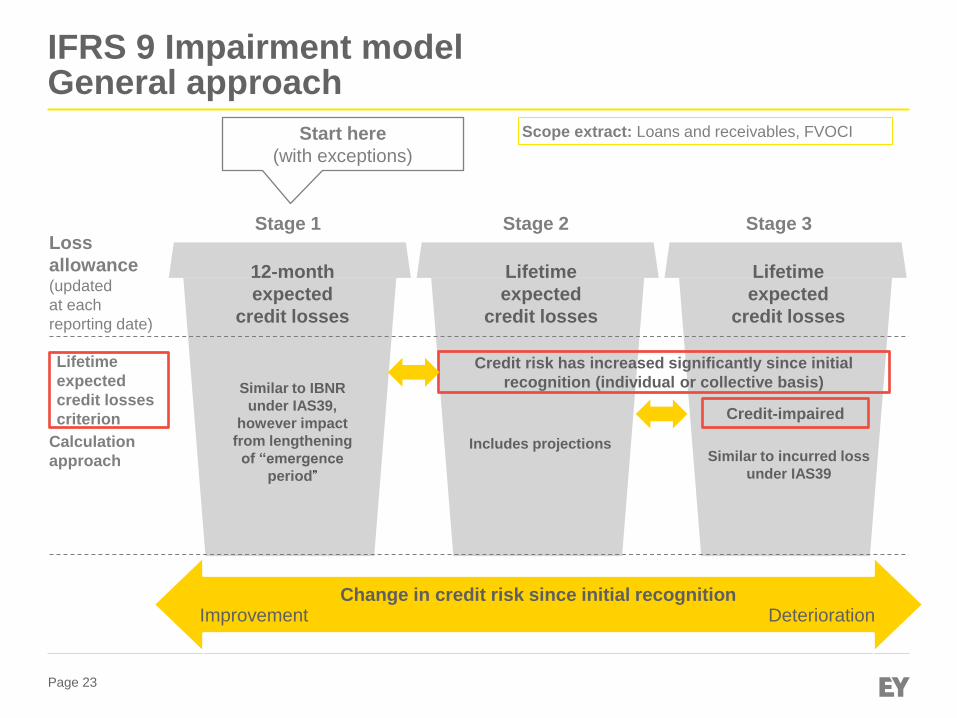

IFRS 9 Impairment model General approach

Change in credit risk since initial recognition Improvement Deterioration

Loss

allowance (updated

at each

reporting date)

Lifetime

expected

credit losses

criterion

12-month

expected

credit losses

Lifetime

expected

credit losses

Lifetime

expected

credit losses

Credit risk has increased significantly since initial

recognition (individual or collective basis)

Stage 1 Stage 2 Stage 3

Start here

(with exceptions)

Credit-impaired

Similar to IBNR

under IAS39,

however impact

from lengthening

of “emergence

period”

Similar to incurred loss

under IAS39

Includes projections

Scope extract: Loans and receivables, FVOCI

Calculation

approach

Page 24

Overview of approach for assessing significant deterioration in credit risk

Assessment on a

collective basis

30 days past due

(DPD) ‘backstop’

Set transfer

threshold by

determining

maximum

initial credit risk

‘Low’ credit risk

– equivalent to

‘investment

grade’

Use change in 12-

month risk as

approximation for

change in lifetime

risk

Assessing

significant

increases

in credit

risk

Assessment at

counterparty

level

► No specific or mechanistic approach is

imposed by the standard

► The appropriate approach will vary

depending on the level of sophistication of

entities, the financial instruments and the

availability of data

► Transfer to Stage 2 when “significant increase in credit risk of financial instrument since initial recognition”

Based on reasonable and supportable

information at the reporting date about:

► Past events

► Current conditions

► Forecasts of future economic conditions

Indicators of deterioration in risk of default General approach – simplifications and

presumptions for assessing deterioration

A B

Page 25

Significant deterioration Use of delinquency & 30 Days Past Due presumption

► If reasonable and supportable forward looking

information is available without undue cost or effort, an

entity cannot rely solely on past due information ► Days past dues are lagging indicators

► More leading indicators must be used (e.g.: macroeconomic, industry etc.)

► There is a rebuttable presumption that the credit risk

has increased significantly since initial recognition

when contractual payments are more than 30 days

past due ► It is presumed to be the latest point at which lifetime expected credit losses

should be recognised even when using forward-looking information

► An entity can rebut this presumption but in practice it will be difficult

Page 26

Simplifications to the general model

IFRS 15 contract assets or

trade receivables with no

significant financing component

(including contracts ≤ 1 year)

IFRS 15 contract assets or

trade receivables with a

significant financing component

Lease receivables

Other financial assets

measured at amortised cost

Other financial assets

measured at FVOCI

Specific approach

• initially measured using credit-

adjusted Effective Interest Rate

• loss allowance recognised at

change in lifetime EL

Simplified approach

• initial and subsequent

loss allowance at lifetime

expected credit losses

General 3-stage model

• initial loss allowance at 12M

expected credit losses

• lifetime expected credit

losses recognised when

credit risk deteriorates

significantly (and is not low)

Purchased or originated credit-

impaired financial assets

Ac

co

un

tin

g P

oli

cy

Page 27

Application roadmap

No

Recognise lifetime expected credit losses

Yes

Is the asset purchased or originated credit-impaired?

Is the simplified approach applicable?

Does the instrument have low credit risk?

Has there been a significant increase in credit risk?

No

No

Yes

Calculate credit-adjusted effective interest rate and

recognise a loss allowance for changes in lifetime expected

credit losses

Is the low credit risk simplification applied?

Recognise 12-month expected credit losses

Yes

Yes

No

Yes No

Is the instrument credit impaired?

Calculate interest on gross carrying amount

Calculate interest on net carrying amount

And

Yes

No

And

Page 28

Measurement of ECL – Key Features

► Measurement of Expected Credit Loss (ECL) must reflect

► Unbiased and probability-weighted amount that is determined by

evaluating a range of possible outcomes,

► the time value of money,

► reasonable and supportable information, that is available without

undue cost or effort at the reporting date, about past events, current

conditions and forecasts of future economic conditions

► It must be directionally consistent with changes in related

observable data from period to period (such as changes in

unemployment rates, property prices, commodity prices, payment

status etc.).

► ECL is the probability-weighted estimate of the present

value of all cash shortfalls over the expected life of the

instrument

Page 29

Expected credit losses for trade receivables

► Results in a day-1 loss ► However initial recognition of financial assets remains at fair value

► Impact limited when trade receivables are short term

► Practically for trade receivables without a financing

component (i.e.: maturities of less than 12 months – refer

to IFRS 15) the lifetime expected credit loss is equivalent

to the 12 months expected credit loss

► Discounting generally not required, however closely

analyse restructuring operations.

Page 30

Practical expedients – Provision matrix

► A manufacturer has a portfolio of trade receivables of RON30

million in 20X1. It operates only in Romania.

► The customer base consists of a large number of small

clients and the trade receivables are categorised by common

risk characteristics that are representative of the customers’

abilities to pay all amounts due in accordance with the

contractual terms.

► The trade receivables do not have a significant financing

component in accordance with IFRS 15 Revenue from

Contracts with Customers.

► In accordance with IFRS 9 the loss allowance for such trade

receivables is always measured at an amount equal to lifetime

time expected credit losses.

Page 31

Practical expedients – Provision matrix

► To determine the expected credit losses for the portfolio, the

entity uses a provision matrix.

► The provision matrix is based on its historical observed

default rates over the expected life of the trade receivables

and is adjusted for forward-looking estimates.

► At every reporting date the historical observed default rates are

updated and changes in the forward-looking estimates are

analysed.

Page 32

Considerations for using provision matrix

► An entity that applies provision matrixes should consider:

► Segmentation of trade receivable portfolio, e.g.:

► Corporate vs. Individual

► Large entities vs. Medium and Small entities

► Recurring client vs. New clients

► Geography

► Length of historical loss experience considered,

► Adjustment of historical loss experience to incorporate

current and forward looking conditions, e.g.:

► Unemployment rates,

► Industry trends,

► GDP.

Page 33

Significant impact expected

► Expected increase in total provisions (e.g.: 19% to 49% increase for UK

banks)

► The impact on individual receivables portfolios can vary significantly

depending also on the type of portfolio and magnitude of currently

impaired receivables

Direct impact on provision levels

Risk of inducing significant

volatility in provision levels

► The new IFRS 9 can increase volatility in impairment figures which is

then translated to volatility in income statement and equity

► Generally the sources of this volatility can be the application of forward

looking models with the use of macro-economic forecasts and the nature

of the indicators used to determine transfer to Lifetime Expected Loss

Page 34

Hedge Accounting

Page 35

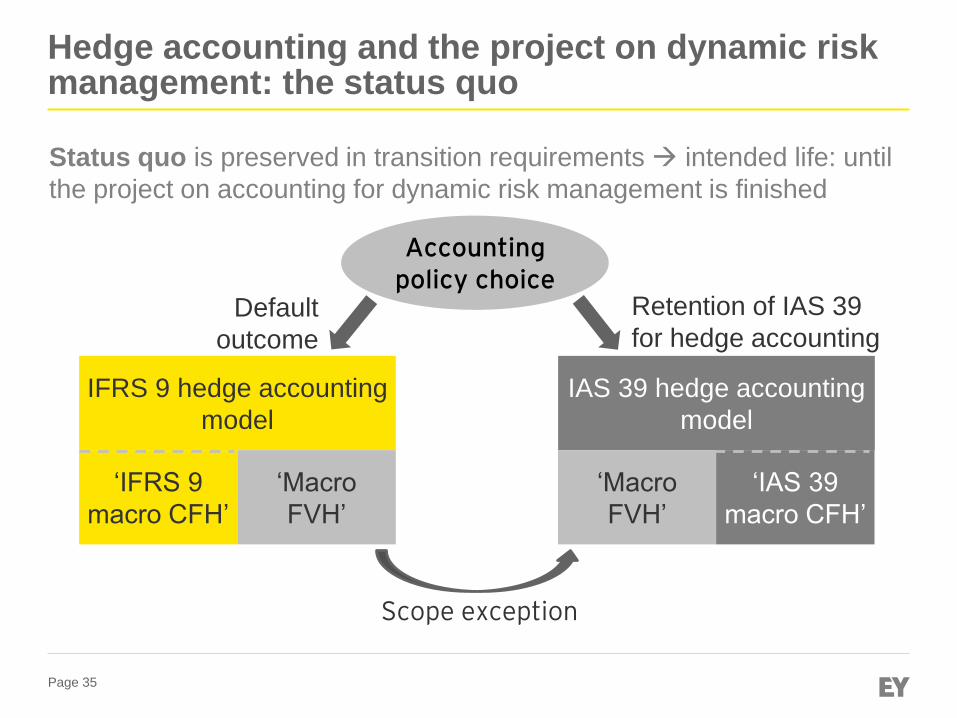

Hedge accounting and the project on dynamic risk management: the status quo

Status quo is preserved in transition requirements intended life: until

the project on accounting for dynamic risk management is finished

Accounting policy choice

IFRS 9 hedge accounting

model

‘IFRS 9

macro CFH’

‘Macro

FVH’

IAS 39 hedge accounting

model

‘Macro

FVH’

‘IAS 39

macro CFH’

Default

outcome

Retention of IAS 39

for hedge accounting

Scope exception

Page 36

Questions?

37

EY | Assurance | Tax | Transactions | Advisory

2015 EY — All Rights Reserved.

Proprietary and confidential. Do not distribute without written permission.

About EY

EY is a global leader in assurance, tax, transaction and advisory services. Worldwide, our 167,000 people are united by our shared values and an unwavering commitment to quality. We make a difference by helping our people, our clients and our wider communities achieve their potential. EY refers to the global organization of member firms of EY Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information about our organization, please visit www.ey.com.

Contacts:

Gelu Gherghescu

Audit Partner

+40 21 402 4000

Adrian Bunea

Executive Director (FAAS Leader)

+40 21 402 4016

Stelian Vezentan

Senior Manager

+40 21 402 4000

EY’s Financial Accounting Advisory Services (“FAAS”) can advice and assist you, amongst others, in the following areas: Compilation and assistance in the preparation of the separate and consolidated financial statements

Assistance in the process of transition to IFRS

Drafting of accounting manuals, methodologies, processes or procedures

Advice and conclusions on the accounting treatment of specific contracts or transactions, including business combinations

Professional training programs tailored to your needs

Adoption of new standards

Advice and conclusions on accounting for financial instruments, including hedge accounting