IFRS 9 - experis.us · financial instruments that are subject to impairment accounting under the...

12

IFRS 9: Implementing the New Impairment Standard for Foreign Financial Institutions

Transcript of IFRS 9 - experis.us · financial instruments that are subject to impairment accounting under the...

IFRS 9: Implementing the New Impairment Standard for Foreign Financial Institutions

IFRS 9 – IMPLEMENTING THE NEW IMPAIRMENT STANDARD FOR FOREIGN FINANCIAL INSTITUTIONS 1

TABLE OF CONTENTS

Overview . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .2

Key provisions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .3

Implementation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .4

Planning . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .8

How Experis Finance can help . . . . . . . . . . . . . . . . . . . . . . . . . . .10

2

OVERVIEW In July 2014, the International Accounting Standards Board (IASB) issued the final version of the International Financial Reporting Standard 9 – Financial Instruments (the “Standard”).1 The Standard codifies previously issued guidance on financial instruments, IAS 39 plus previous versions of IFRS 9, along with new updates impacting the following areas:

• Classification and Measurement

• Impairment

• Hedge Accounting

Scope and Effective DatesThe Standard applies to all entities and financial instruments. The final mandatory application date is for fiscal years beginning on or after January 1, 2018 with earlier adoption permitted. One provision of the Standard, relating to the classification of the change in the value of the entity’s own debt carried at fair value, is available for early adoption on a stand-alone basis. The hedge accounting requirements of the Standard do not have to be adopted until the IASB completes its Macro Hedging project and releases that guidance as discussed in the discussion paper published in April 2014.2

Impact on foreign financial institutions In the U.S, the introduction of the Standard is expected to have the most impact on entities that are domestic branches or subsidiaries of financial institutions owned by foreign parent companies (FFI’s), which will include mainly banks and insurance companies. It is likely that the parent company of an FFI is an issuer of financial statements prepared in accordance with international financial reporting standards issued by the IASB. Analysis of the Standard indicates that its transitional impact will be greatest on FFI’s that have a greater percentage of the assets on their balance sheets dedicated to traditional lending and/or investing businesses.

Assets that have typically been classified as held to maturity or available for sale will now have to meet two qualifications in order to avoid fair value through profit and loss treatment. Once passed, those assets will then be subject to the new impairment approach of establishing allowance accounts. In addition to calculating a new minimum loss allowance for each non-fair value through profit and loss asset, entities will need to monitor their portfolios for any assets that have experienced a significant increase in credit risk. When an asset experiences such an increase in its credit risk, its allowance account will need to increase in a significant manner.

Focus of this analysisDue to the broad scope of the final Standard in its entirety, this article focuses on the challenges faced by FFI clients as they seek to apply the new requirements to their basic lending and investment portfolio assets. This includes an analysis of how the new impairment guidance drives the loss allowances that need to be

1 http://www.ifrs.org/current-projects/iasb-projects/financial-instruments-a-replacement-of-ias-39-financial-instruments-recognitio/Pages/Financial-Instruments-Replacement-of-IAS-39.aspx2 http://www.ifrs.org/Current-Projects/IASB-Projects/Financial-Instruments-A-Replacement-of-IAS-39-Financial-Instruments-Recognitio/Phase-III-Macro-hedge-accounting/DP-April-2014/Documents/Discussion-Paper-Accounting-for-Dynamic-Risk-Management-April-2014.pdf

The standard is expected to have the most impact on entities that are domestic branches

or subsidiaries of financial institutions owned by foreign parent companies (FFI’s)

IFRS 9 – IMPLEMENTING THE NEW IMPAIRMENT STANDARD FOR FOREIGN FINANCIAL INSTITUTIONS 3

established for these assets. The overall move to the new impairment calculations is expected to be challenging for all entities involved. Two developments lead to this statement:

1. The long lead time to the mandatory conversion date.

2. The fact that the IASB has established the Transition Resource Group for Impairment of Financial Instruments (“ITG”).3

The ITG will provide a discussion forum to support stakeholders on implementation issues that may arise because of the new impairment requirements under the Standard.

KEY PROVISIONSClassification categories for financial assetsThe Standard contains three available classification categories for an entity’s financial assets:

1. Amortized Cost

2. Fair Value through Other Comprehensive Income (FVOCI)

3. Fair Value through Profit and Loss (FVTPL)

Changes in the fair value of assets classified in the Amortized Cost and FVOCI categories do not pass through the income statement. For ease of presentation, we will refer to assets in these categories on a combined basis as “Non-FVTPL”. The classification of any financial asset, FVTPL and Non-FVTPL alike, depends on two factors:

1. The business model used in managing the asset.

2. The contractual cash flow characteristics of the asset (note that FVTPL is effectively the automatic or default treatment under the Standard).

MeasurementFor Non-FVTPL financial assets, in USD, current period income is comprised of (a) interest income plus (b) loss allowance changes. Interest income for a non-impaired Amortized Cost asset is calculated by applying its effective interest rate against its current carrying amount excluding the loss allowance. If the asset becomes impaired, the loss allowance is used to reduce the asset’s carrying amount before the current period accrual is calculated.

IFRS 9: IMPAIRMENT – GENERAL APPROACH

IMPLEMENTATION

Identify non-fair value assetsBusiness model assessmentSPPI criterion assessmentThree state model

ONGOINGSignifican increase assessmentLoss allowance (ECL)Interst calculations

3 http://www.ifrs.org/About-us/IASB/Advisory-bodies/ITG-Impairment-Financial-Instrument/Pages/home.aspx

4

New requirements for loss allowances The Standard introduces new requirements for establishing loss allowances for Non-FVTPL assets. The previous methodology has been known as the incurred loss model. The new method is referred to as the expected loss model. With all things equal, credit losses will be recognized earlier under the expected loss methodology than under the incurred loss model. This change represents a response to criticisms received by the IASB during and after the Financial Crisis of 2008.4

The same impairment model, referred to in the Standard as the General Approach, is applied to all financial instruments that are subject to impairment accounting under the final IFRS 9 models. This includes Non-FVTPL assets, lease receivables, trade receivables, and commitments to lend money and financial guarantee contracts. The new impairment guidance follows a “three-stage” model, performing, under-performing and non-performing. Our analysis will be limited to the treatment of debt instruments, specifically loans, bonds, and typical Non-FVTPL assets.

For any Non-FVTPL financial asset, there will always be a loss allowance recorded at each reporting date. There are two types of loss allowance calculations:

1. The first type of loss is referred to as the 12-Month Expected Credit Loss (12-Month ECL) which is applicable to any asset that is performing (i.e., Stage 1) as expected on the date of its original recognition.

2. The second type of loss allowance is called the Lifetime Expected Credit Loss (“Lifetime ECL”) which is used for any asset that has experienced a significant increase in credit risk since its initial recognition.

There is a substantial difference between the two loss allowance calculations. 1. The 12-Month Forward ECL, applicable to all performing assets, is being introduced in a more

general manner as a method to (a) reduce the overstatement of coupon income applicable to expected losses at the time of initial recognition and (b) to make the loss allowance more forward- looking as suggested by regulators.

2. The Lifetime ECL represents, in very simplistic terms, a one-time move from cost to fair value for an asset that has experienced a significant increase in its credit risk as of the reporting date at the end of the period in which that determination became effective.

IMPLEMENTATION Implementation of the new guidance will require the following steps:

1. Business model assessment

2. Solely on payments of principal and interest (SPPI) determination

3. Three-stage categorization

4. Significant increase determination

5. Loss allowance calculations

6. Current period interest calculations

Business Model AssessmentIn order to proceed with the implementation, an entity will have to analyze the nature of its key operating units, especially those that will be holding Non-FVTPL assets. This will be accomplished by reviewing how groups of 4 http://www.ifrs.org/Current-Projects/IASB-Projects/Financial-Instruments-A-Replacement-of-IAS-39-Financial-Instruments-Recognitio/Documents/IFRS-9-Project-Summary-July-2014.pdf, p.4.

With all things equal, credit losses will be recognized earlier under the expected loss methodology

than under the incurred loss model.

IFRS 9 – IMPLEMENTING THE NEW IMPAIRMENT STANDARD FOR FOREIGN FINANCIAL INSTITUTIONS 5

financial assets are managed together in order to achieve a particular business objective. The Standard provides entities with three relevant business models:

1. Holding assets in order to receive contractual cash flows (“HTC Business Model”);

2. Collecting contractual cash flows and selling financial assets (“HTC&S Business Model”)

3. Other business models (for example, realizing cash flows through the sale of the assets) (“FVTPL Business Model”)

Non-FVTPL assets need to qualify under at least one of the first two models. The HTC Business Model is appropriate for assets that are measured at Amortized Cost while the HTC&S Business Model is appropriate for assets that are to be measured at FVOCI. The other business models would be used for FVTPL (in most cases, trading businesses).

Determination of the appropriate business model to use is an exercise in judgment. The entity must consider all relevant evidence that is available as of the date of the assessment. The Application Guidance (Appendix B) of the Standard suggests reviewing objective criteria to determine the model including reporting to senior management, risks that affect the performance of the business and how they are managed, along with, how management is compensated. An entity might hold the same type of instrument, such as government bonds, in all three classification categories (Amortized Cost, FVOCI and FVTPL) depending on its intention and model for managing the assets.

Assets held by an operating unit following the HTC Business Model would be subject to initial and ongoing credit reviews. The HTC&S Business Model would contain assets required to undergo initial and ongoing credit reviews as well. However, the entity may use sales of these assets to strategically manage the entity’s liquidity position or its asset and liability duration mismatch. Furthermore, under this business model, selling assets would be considered an integral part of achieving its business objectives. As a point of reference, FVTPL assets would be expected to be held in a business model where market risk (interest rate, foreign exchange, credit and equity) exposures were more of a primary concern in addition to higher volume of purchases and sales supporting the business unit’s operating objectives.

SPPI DeterminationDetermining cash flow is done at the asset level and seeks to establish whether the contractual cash flows of an asset are based “solely on payments of principal and interest” (or SPPI). Only assets that meet this criterion can qualify for Non-FVTPL treatment, in addition to being held in an operating unit that qualifies within one of the two acceptable business models. The minimum standard for meeting the SPPI determination is that the contractual cash flows compensate the holder for (a) the time value of money plus (b) credit risk plus (c) other allowable components such as liquidity risk. As such, for the contractual cash flows of an asset to qualify as SPPI, they must be consistent with a basic lending arrangement.

Contractual cash flows that contain an element of return over and above this basic level would not qualify as SPPI. Contractual features that introduce exposure to risks or volatility into the contractual cash flows that are unrelated to a basic lending arrangement, such as exposure to changes in equity or commodity prices via a structured note security, would not pass the SPPI assessment. The IASB is setting a higher standard so that an asset that contains leverage or other risk factors cannot be classified as Non-FVTPL and thus be hidden from mark-to-market accounting. Since there are many structured products traded today, the Application Guidance provides examples of the types financial instruments that may be challenging in making the SPPI determination. The SPPI determination should only be performed once for each individual type of asset. This should not be a recurring, periodic test. However, entities will need to establish procedures to ensure that newly purchased or originated assets are tested.

6

Three-Stage ModelOnce an entity completes its business model reviews and SPPI determinations, it will be able to assign each Non-FVTPL debt instrument to one of the three stages of the new impairment model. (Note: Reference to the “three stages” occurs in the IFRS 9 Project Summary of July 2014, the Standard itself does not use this terminology).5

Stage 1A newly purchased or originated financial asset is placed in Stage 1 of the new model. An asset stays in this category as long as it performs in line with the expectations that were set for the asset at the time of initial recognition. In Stage 1, the 12-Month ECL is the minimum required loss allowance. An asset will stay in Stage 1, even if there is an increase in its credit risk, as long as the asset is deemed to be of low credit risk.

Stage 2A financial asset moves from Stage 1 to Stage 2 if the entity determines that there has been a significant increase in its credit risk from the time of initial recognition, origination or purchase, and the new level of risk is considered to be greater than low. In stage 2, the loss allowance of assets must equal their Lifetime ECL.

Stage 3A financial asset moves to Stage 3 when its credit risk increases to the point where the asset is considered credit-impaired. A financial asset is considered to be in this category when one or more events, as defined in Appendix A of the Standard, that have a detrimental impact on its estimated future cash flows have occurred. The loss allowance moves to Lifetime ECL if it is has not already done so.

Significant increase assessmentAs mentioned previously, all financial assets that have not experienced a significant increase in their credit risk since their date of initial recognition will fall into Stage. On each subsequent reporting date, the entity is required to repeat its assessment as to whether there has been any significant increase in credit risk in that asset, “significant increase assessment.” If there has been a significant increase in credit risk, the asset moves to Stage 2 and the loss allowance is then set at Lifetime ECL. The Standard requires that an entity makes the significant increase assessment by reference to the change in the risk of a default occurring over the expected life of the financial asset. As such, the risk of default as of the current reporting date needs to be compared to the risk of default that existed on the date of initial recognition.

The Standard requires that reasonable and supportable information be used to make the significant increase assessment and that such information be available without undue cost or effort. If reasonable and supportable forward-looking information is available, also without undue cost or effort, the entity is prohibited from making the assessment by relying solely on past due information.

It may be necessary to perform the significant increase assessment on a collective basis in some cases as evidence of increases in credit risk at the individual instrument level may not yet be available. The Standard permits recognizing loss allowances on a collective basis under certain conditions as well as establishing an allowance on a portion of a group of assets.

The Standard also introduces two very important concepts in making the significant increase assessment: a) the “rebuttable presumption” and b) the “low credit risk” asset. In order to bring a clear line of objectivity to the

5 http://www.ifrs.org/Current-Projects/IASB-Projects/Financial-Instruments-A-Replacement-of-IAS-39-Financial-Instruments-Recognitio/Documents/IFRS-9-Project-Summary-July-2014.pdf, p.16

The Standard also introduces two very important concepts in making

the significant increase assessment: a) the “rebuttable presumption” and

b) the “low credit risk” asset.

IFRS 9 – IMPLEMENTING THE NEW IMPAIRMENT STANDARD FOR FOREIGN FINANCIAL INSTITUTIONS 7 7

significant increase assessment, the Standard states that any asset that is 30 days or more past due must be considered to have had a significant increase in credit risk unless the entity can prove otherwise, without undue cost or effort. As an expedient to the significant increase assessment, the Standard states that an entity may assume that there has been no significant increase in the credit risk of an asset that is deemed to have “low credit risk” on the reporting date. The Application Guidance section of the Standard provides more details on how this determination is to be made but makes it clear that an investment grade asset is to be considered as having low credit risk.

It is at this point in the process that there is a critical juncture with the classification and measurement standards noted above. This critical juncture takes place at the date of initial recognition of a financial asset. On the date of initial recognition, the entity must be able to capture or generate the following data elements for any Non-FVTPL asset:

• Current credit risk profile of the asset

• Future cash flows

• Components of the carrying amount

• Computation of effective interest rate

All of these elements will be needed to apply the Standard on a prospective basis. The entity will need the data required to assess whether there has been (a) a significant increase in credit risk – requiring the asset to be moved from Stage 1 to Stage 2 or (b) an event has occurred that causes the asset to become impaired – requiring that it be moved to Stage 3. The implications in the preceding sentence are important. Correct implementation will require asset accounting systems to reflect measures of credit risk in ways not yet seen. It is anticipated that FFI’s will use their internal credit ratings scaled to the three-stage model in order to identify when a change in stage status has occurred. The internal models may, or may not, be calibrated to external pricing sources. For example, a “significant increase in credit risk since initial recognition” may be defined by a move in default probabilities gleaned from current market data.

The determination of whether there has been a significant deterioration can be made in either a quantitative or qualitative manner. However, the Standard does suggest the preference for the use of quantitative methods which will in some cases parallel regulatory calculations. Assets can move back and forth between categories or stages as credit deteriorates and then improves. Please note that separate rules apply to (a) assets that are already impaired at the date of initial recognition and (b) assets whose terms are modified or re-structured. Note that we have omitted discussion of these items.

Calculation of expected credit losses

The next step in the process will be the calculation of the appropriate loss allowance for each financial asset at each reporting date. As stated at the outset, each asset will have a loss allowance, the major challenge being whether the Lifetime ECL is used instead of the 12-Month ECL. Expected credit losses are defined as a probability-weighted estimate of credit losses, which is the present value of all cash shortfalls, over the expected life of a financial instrument. A cash shortfall is the difference between the cash flows that are due to an entity in accordance with the contract and the cash flows that the entity expects to receive. The Standard states that an entity shall measure the ECL of a financial instrument in a way that reflects:

1. An unbiased and probability-weighted amount that is determined by evaluating a range of possible outcomes

2. The time value of money

3. Reasonable and supportable information that is available without undue cost or effort at the reporting date about past events, current conditions, and forecasts of future economic conditions.

8

The Standard requires that each entity determine the most appropriate definition of default for each relevant asset type in its portfolio, provided the definition is consistent with the entity’s own internal credit risk management process. The Standard introduces the second rebuttable presumption here which is that default cannot occur later than 90 days past due.

The Lifetime ECL is used when the entity has determined that an asset has had a significant increase in its credit risk since initial recognition. Calculation of the Lifetime ECL requires an entity to estimate its expected losses on the asset using probability-weighted future cash shortfalls (the loss on the asset less any recovered amounts) discounted back to the reporting date. In theory, this would approximate the amount that the entity would need to pay to another financial institution to assume ownership of the asset going forward.

The 12-Month ECL is a portion of the Lifetime ECL and represents (a) the lifetime cash shortfalls that will result if a default occurs within the next 12 months after the reporting date, or a shorter period if the expected life of a financial instrument is less than 12 months, weighted by (b) the probability of that default occurring. The 12-Month ECL is used to calculate the loss allowance for all performing assets, Stage 1, as of the reporting date.

The IASB has taken the position that, in general, future ECL’s are reflected in the price of any financial asset on the date of its initial recognition and that any future period interest income contains an element of that previously-existing ECL that will later be needed to establish an allowance. The 12-Month ECL loss allowance (applicable to assets that are performing) was introduced in the Standard to address that timing issue. The 12-Month ECL also addresses, to some extent, the goal of regulators to have the allowance accounts be more forward-looking and build-up prior to an incurred loss. In theory, the 12-Month ECL would approximate the premium on a 1-year credit default option on the relevant asset.

PLANNINGThe new guidance will have a significant impact on FFIs whose balance sheets reflect a more traditional mix of buy-and-hold businesses. Entities that are more trade-oriented will have more expeditious conversions as the impairment infrastructure build will be less of a burden. The acknowledged effect of the new impairment guidance will be to speed up the provisions that were later recognized using the incurred loss method.

We expect that most of the process will be driven by the head office locations of our FFI clients. Overall policy, in particular the

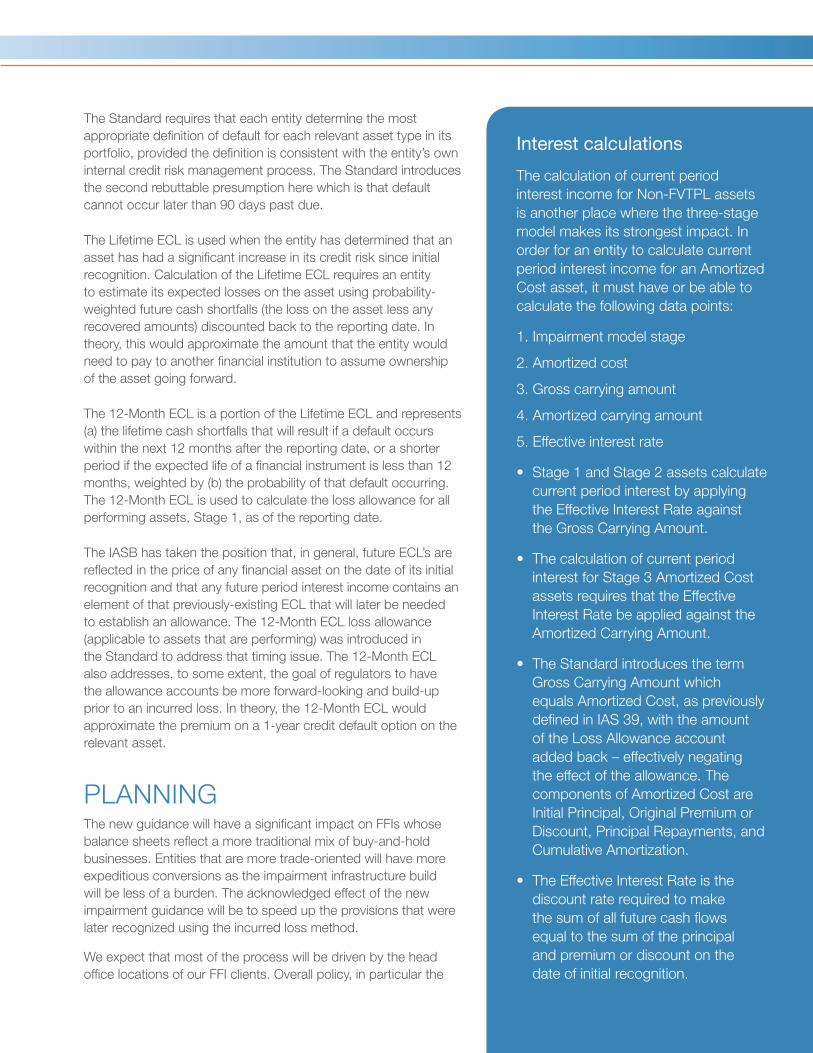

Interest calculations

The calculation of current period interest income for Non-FVTPL assets is another place where the three-stage model makes its strongest impact. In order for an entity to calculate current period interest income for an Amortized Cost asset, it must have or be able to calculate the following data points:

1. Impairment model stage

2. Amortized cost

3. Gross carrying amount

4. Amortized carrying amount

5. Effective interest rate

• Stage 1 and Stage 2 assets calculate current period interest by applying the Effective Interest Rate against the Gross Carrying Amount.

• The calculation of current period interest for Stage 3 Amortized Cost assets requires that the Effective Interest Rate be applied against the Amortized Carrying Amount.

• The Standard introduces the term Gross Carrying Amount which equals Amortized Cost, as previously defined in IAS 39, with the amount of the Loss Allowance account added back – effectively negating the effect of the allowance. The components of Amortized Cost are Initial Principal, Original Premium or Discount, Principal Repayments, and Cumulative Amortization.

• The Effective Interest Rate is the discount rate required to make the sum of all future cash flows equal to the sum of the principal and premium or discount on the date of initial recognition.

IFRS 9 – IMPLEMENTING THE NEW IMPAIRMENT STANDARD FOR FOREIGN FINANCIAL INSTITUTIONS 9

date of initial adoption, must be driven from headquarters as it is easy to see how these implementations will need to be performed on a global scale. Local offices and subsidiaries will most likely spend most of their efforts developing the resources needed to record and report transactions according to the new guidelines. This will mean new sets of operating and accounting procedures as well as the need to work closely with the local credit and risk management functions. The IT aspects of these changes will be significant. Local Area Controllers will need to pinpoint areas requiring judgment so that they can be communicated to head office, internal and external audit.

Additionally, depending on overall complexity, local area offices may need to implement formal PMO efforts. Timetables, milestones and deliverables may need to be tracked. Controllers will need to stay abreast of the ITG activities as developments may have an impact on the entity’s implementation. An initial impact assessment is recommended and will allow entities the opportunity to evaluate the need for additional resources to prepare for the changes that may be required across the organization.

We have noted a few key implementation considerations to help you with this process:

1. Steering Committee and PMOGiven the multi-function impact of the project, a Steering Committee should be established with senior representatives of all key contributing groups. Implementation should be given full PMO status so that the correct level of resources and monitoring are available.

2. Head Office – Policy and Communication Essentially, all the financial data generated by the FFI rolls up to the head office for use in the entity’s published financial statements. As such, we expect the main office to also issue overall project guidance, in particular milestones and deliverables. A key item is the determination of the date of initial adoption which must be set by this office as well. And lastly, we expect this office to also establish its own PMO resource for this project.

3. IT Support – Analysis and Development The guidance requirements are significant enough that IT will likely play a major role in achieving the transition. IT will be called on to develop software and tools to allow asset profiles to be matched with credit risk data in order to categorize assets correctly and calculate current period income. The testing phase will be especially important. Be sure to plan for a long period of parallel testing in a control environment so that the conversion impact can be monitored.

4. Assessments, ECL Calculations & DisclosuresControllers will need to work with teams from front office, treasury, credit and risk to plan and execute the Business Model, SPPI Criterion and Significant Increase Assessments. The expected loss calculations will be another area of focus for all. Accounting policy and financial reporting groups will need to prepare for extensive disclosure requirements that are being introduced. Monitoring ITG developments will be helpful.

5. Monitor Financial ImpactThe transition to the Standard is already anticipated by some to have a potentially significant impact on profit and loss. We expect that both local area and head office senior management will want to be kept abreast of current estimates. Controllers may be requested to implement an attribution analysis that shows the source of the change to the current provision for each asset. This could be particularly helpful in situations where the existing asset has some underlying complexity that results in an incorrect allowance.

6. Internal AuditInternal Audit may be asked to perform an independent check on the progress of the overall conversion. In that case, Internal Audit will want to attend meetings of the Steering Committee and monitor key milestones. Testing could be initiated once a test portfolio and environment are created by IT. Internal Audit and the businesses will need to update their process documentation and key control analysis.

10

7. External AuditExternal Auditors will need to be concerned with areas most impacted by judgment, such as the Business Model, SPPI and Significant Increase assessments. Calculations driving the new loss allowance balances will also be an area of interest. Controllers should ensure that proper files are kept regarding conversion and reconciliation.

8. TrainingControllers, as well as the steering committee, should compile a library of training material so that staff and project team members will have access to the correct level of knowledge when executing their tasks.

.

HOW EXPERIS FINANCE CAN HELPExperis Finance, a Manpower Group product solutions and financial advisory organization, is uniquely positioned to assist companies in efficiently and effectively implementing the key requirements set forth in the Standard. Our profesionals provide many public and private companies with accounting and financial reporting consulting services, including SEC consulting and support.

We count many FFI entities as valued clients. We have many professionals on staff with significant banking/capital markets expertise to assist with this implementation. From the early stages of Business Model and SPPI Criterion assessments through the development of ECL methodologies, our team has the ability to add value throughout the entire term of the implementation. Our broad experience and deep expertise enables us to help clients with policy development, procedure writing, developing IT specifications and training. Additionally, one of our strong fields of expertise is Project Management, which is especially relevant to ensuring the success of the implementation.

Contact us to arrange a meeting to discuss your specific situation with an Experis Finance professional. We are here to help you achieve your goals.

Experis Finance Financial Services Industry IFRS 9 Update

John R. Fleming, Consultant – Risk Advisory Services Professional, New York [email protected] • 917-975-3252

Experis • 100 Manpower Place • Milwaukee, WI 53212 • USA

www.experis.com

© 205 MANPOWERGROUP. ALL RIGHTS RESERVED.

![FY16 Financial Results [IFRS] - Hitachi · Trade Receivables 1,466 +120 Others 774 +196 Inventories 1,009 +75 Non-Current Liabilities 318 -104 Others 360 +215 Retirement](https://static.fdocuments.in/doc/165x107/6033bb6412879148596582a8/fy16-financial-results-ifrs-hitachi-trade-receivables-1466-i120-others-774.jpg)