IFRS 8 Operating segments - ey.com · IFRS 8 Operating segments Implementation guidance 5...

32

IFRS 8 Operating segments Implementation guidance

Transcript of IFRS 8 Operating segments - ey.com · IFRS 8 Operating segments Implementation guidance 5...

IFRS 8 Operating segments Implementation guidance

This publication is intended to assist readers in understanding the requirements of and does not attempt to explain all of the requirements of IFRS 8. In case of doubt as to the requirements, it is essential to refer to the relevant paragraph of IFRS 8 and, when necessary, to seek appropriate professional advice.

Contents

Introduction 2

Section 1 4IFRS 8 and IAS 14: The key differences

Section 2 6Application of the requirements of IFRS 8

Section 3 16Illustrative example

Section 4 25Frequently asked questions

1IFRS 8 Operating segments Implementation guidance

2 IFRS 8 Operating segments Implementation guidance

This publication provides information about the requirements of the newly issued IFRS 8 Operating Segments, which becomes effective for annual reporting periods beginning on or after 1 January 2009. It has been designed to help those responsible for preparing IFRS-based financial statements apply and understand the new requirements.

Our commentary and analysis of the Standard is divided into four sections:

Section 1: Provides an analysis of •the key differences between the requirements of IFRS 8 and the standard it will replace, IAS 14 Segment Reporting.Section 2: Explains how to identify •reportable operating segments, using flowcharts to highlight the decisions that need to be made. It also contains a number of examples to illustrate what is intended by the Standard.Section 3: Provides an illustration of •the disclosures required by IFRS 8, with commentary highlighting when the disclosures may differ from those required by IAS 14.Section 4: Answers some frequently •asked questions (FAQs) about the application of IFRS 8.

IFRS 8 differs from its predecessor because it introduces a management reporting approach to identifying and measuring the results of reportable operating segments. As the measurement of the segment results reported is no longer dictated by the measurement and recognition criteria of financial reporting standards, reconciliations are required where information being presented to management differs from IFRS information in the primary financial statements. Some entities may need to develop new processes in order to address these reconciliation requirements.

As entities manage their businesses in different ways, segment reporting disclosures made by similar-sized entities in similar industries are unlikely to be directly comparable. Our publication, Observations on the Implementation of IFRS, indicated that there was diversity in the way entities reported their segments using IAS 14. Disclosures may be even less comparable when IFRS 8 comes into effect.

The disclosure requirements in IFRS 8 are extensive, and we encourage all entities to study the Standard carefully well ahead of its adoption.

Segment reporting was identified as part of the International Accounting Standards Board’s (IASB or Board) short-term project to reduce the differences between International Financial Reporting Standards and US GAAP. In January 2005 the IASB decided the best way to achieve convergence in relation to segment reporting was to adopt the approach of the equivalent US standard (SFAS 131: Disclosures about Segments of an Enterprise and Related Information). As a result ED 8 Operating Segments was issued in January 2006, and the final Standard, IFRS 8, was released in November 2006. IFRS 8 will replace IAS 14 for reporting periods beginning on or after 1 January 2009. However, comparative information is required when IFRS 8 becomes effective, which means that entities need to capture IFRS 8 segment information from 1 January 2008.

The IASB believes that financial reporting will improve because the management approach to the reporting of segments allows users of financial statements to examine an entity’s operations through the eyes of management. An important

Overview

Introduction

Background

3IFRS 8 Operating segments Implementation guidance

aspect of IFRS 8 is the requirement to disclose information that is actually being used internally by management. The IASB maintains that, because the segment information required to be disclosed will be readily available, it should help entities save time and money.

Although adopting the management approach does have benefits, in commenting on ED 8, some, including Ernst & Young, argued that it is inferior to IAS 14 because segment information does not have to be reported on the same basis as the financial statements (using IFRS) and that key terms such as ‘segment revenue’ and ‘segment assets’ are not defined. To counter this criticism the final Standard requires increased disclosure regarding the basis on which the information has been prepared.

Overall, the IASB believes the benefits of the management approach, together with some expanded disclosure, will outweigh the lack of comparability that might arise, which is why the decision to adopt the US GAAP approach was made.

Background

4 IFRS 8 Operating segments Implementation guidance

The key differences between IFRS 8 and IAS 14 in identifying and measuring reportable segments are outlined below and are followed by a summary of the disclosures required by the new Standard.

IFRS 8 adopts the management •reporting approach to identifying operating segments. It is likely that in many cases, the structure of operating segments will be the same under IFRS 8 as under IAS 14, because IAS 14, like IFRS 8, defines reporting segments as the organisational units for which information is reported to key management personnel for the purpose of performance assessment and future resource allocation. When an entity’s internal structure and management reporting system are not based either on product lines or on geography, IAS 14 requires the entity to choose one as its primary segment reporting format. IFRS 8, however, does not impose this requirement to report segment information on a product or geographical basis and in some cases this may result in different segments being reported under IFRS 8 compared with IAS 14.An entity is first required to identify •all operating segments that meet the definition in IFRS 8 (refer to detailed discussion in Section 2). Once all

operating segments have been identified, the entity must determine which of these operating segments are reportable. If a segment is reportable, then it must be separately disclosed. This approach is the same as that required by IAS 14 except that it does not require the entity to determine a ‘primary’ and a ‘secondary’ basis of segment reporting.Under IFRS 8, for the purpose of •identifying reportable segments, no distinction is made between revenues and expenses relating to transactions with third parties and revenues and expenses relating to transactions with other parts of the group. This means that vertically integrated operations may be composed of several segments for the purpose of IFRS 8. However, under IAS 14 a business segment or geographical segment qualifies as a reportable segment only if a majority of its revenue is earned from sales to external customers. This is an important difference that may result in additional segments being disclosed under IFRS 8.

Section 1

IFRS 8 and IAS 14: The key differences

Identification of segments

5IFRS 8 Operating segments Implementation guidance

Measurement of segment information

IFRS 8 requires that the amount •of each segment item reported is the measure reported to the chief operating decision maker (CODM) in internal management reports, even if this information is not prepared in accordance with the IFRS accounting policies of the entity. This may result in differences between the amounts reported in segment information and those reported in the entity’s primary financial statements. Contrast this with IAS 14, which requires the segment information to be prepared in conformity with the entity’s accounting policies for preparing its financial statements (i.e., IFRS).Unlike IAS 14, IFRS 8 does not define •terms such as ‘segment revenue’, ‘segment profit or loss’, ‘segment assets’, and ‘segment liabilities’. As a result, diversity of reporting practice will increase.

As IFRS 8 does not define segments •as either business or geographical segments and does not require measurement of segment amounts based on an entity’s IFRS accounting policies, an entity must disclose an explanation of how it determined its reportable operating segments, and the basis on which the disclosed amounts have been measured. These disclosures include reconciliations of the totals of key segment amounts to the corresponding entity amounts reported in the IFRS financial statements.A measure of profit or loss and assets •for each segment must be disclosed. Additional line items, such as interest revenue and interest expense, are required to be disclosed if they are provided to the CODM (or included in the measure of segment profit or loss reviewed by the CODM). IAS 14, by contrast, specifies the items that must be disclosed for each reportable segment.

Disclosures are required when an entity •receives more than 10% of its revenue from a single customer. In this instance, the entity must disclose this fact, the total amount of revenue earned from each such customer, and the name of the operating segment that reports the revenue. This is not required by IAS 14.Consequential amendments •have been made to the segment disclosures required by IAS 34 Interim Financial Reporting.

Disclosure

6 IFRS 8 Operating segments Implementation guidance

This section addresses the following:Core principleA – What is the aim of IFRS 8?ScopeB – Which entities does IFRS 8 apply to?Operating segmentsC – What are operating segments and how are they determined?Reportable segmentsD – What are reportable segments and how are they determined?MeasurementE – How are the amounts to be disclosed measured?DisclosuresF – What disclosures are required?Transition and effective dateG – When is it applicable?

A. Core principle – What is the aim of IFRS 8?The objective of IFRS 8 is characterised in paragraph 1 as a ‘core principle’ and states that an entity must: “Disclose information to enable users of its financial statements to evaluate the nature and financial effects of the different business activities in which it engages and the economic environments in which it operates.”

Where an entity with a matrix organisational structure is unable to clearly identify operating segments (because the CODM regularly reviews the operating results on both a product line and a geographical area basis) it is required to look to the core principle in determining the appropriate basis of segmentation.

B. Scope – Which entities does IFRS 8 apply to?IFRS 8 applies to the financial statements of entities:

whose debt or equity instruments are •traded in a public market, orthat file, or are in the process of •filing, their financial statements with a securities commission or other regulatory organisation for the purpose of issuing any class of instruments in a public market.

These are the same entities that were subject to IAS 14.

If an entity that is not required to apply IFRS 8 chooses to disclose information about its segments that does not comply with all the requirements of IFRS 8, it cannot refer to this information as segment information.

When financial statements contain both consolidated financial statements and the parent’s separate financial statements, segment information is required only for the consolidated financial statements.

Section 2

Application of the requirements of IFRS 8

7IFRS 8 Operating segments Implementation guidance

These factors include:

the nature of the business activities •of each component of the entity, the existence of managers responsible for them, and information presented to the board of directors. an operating segment will usually have •a segment manager who is directly accountable to, and has regular contact with, the CODM to discuss the performance of the segment. However, a single manager may be the segment manager for more than one operating segment. If the characteristics in the definition quoted above apply to more than one set of components of an entity (e.g., to both products-based and geographical components) but there is only one set for which segment managers are held

responsible, then that set constitutes the operating segments. when an entity has a matrix •management structure resulting in two or more overlapping sets of components for which different segment managers are responsible and the CODM regularly reviews the operating results of both components, an entity must consider the core principle of the Standard in order to determine its operating segments.

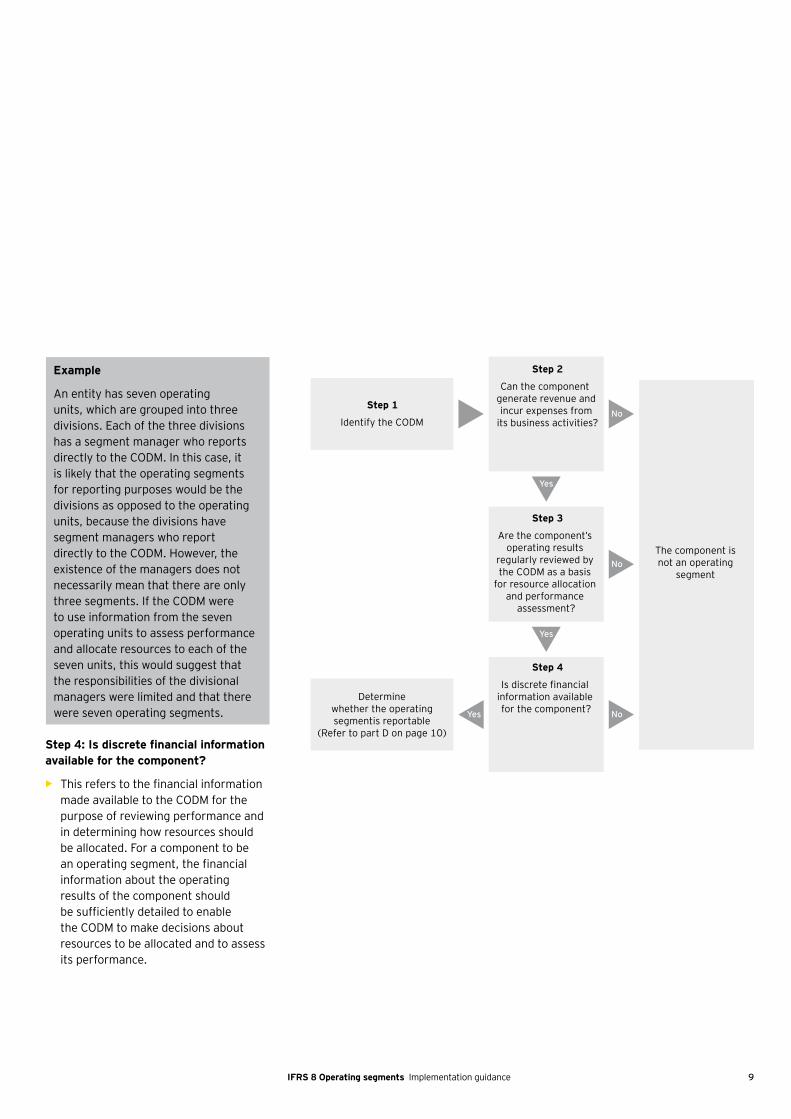

To identify operating segments, four decision steps are required as illustrated in the flowchart on the following page.

C. Operating segments – What are operating segments and how are they determined?

An operating segment is defined as: “A component of an entity:

that engages in business activities •from which it may earn revenues and incur expenses (including revenues and expenses relating to transactions with other components of the same entity),whose operating results are regularly •reviewed by the entity’s chief operating decision maker to make decisions about resources to be allocated to the segment and assess its performance, andfor which discrete financial information •is available.”

Most entities will be able to identify their operating segments easily by reference to these characteristics. However, when this is not the case, for example if the CODM uses more than one set of segment information, other factors may enable the operating segments to be identified.

8 IFRS 8 Operating segments Implementation guidance

Step 1: Identify the CODM

The term ‘chief operating decision •maker’ defines a function rather than an individual with a specific title. The function of the CODM is to allocate resources to and assess the operating results of the segments of an entity. The CODM could be an individual, such as the chief executive officer or the chief operating officer, or it could be a group of executives, like the board of directors or a management committee.

Example

Assume that an entity has a president, a chief executive officer, and a chief operating officer. All three individuals serve on a management committee, which exists to make operating decisions related to the different business activities of the entity, and the committee operates on the basis of consensus among its members. In this case, the CODM would be the management committee itself. However, the fact that a management committee exists does not necessarily mean that the committee is the CODM. For example, if the chief executive officer can override the decisions made by the committee, then the chief executive officer may be the CODM, because the CODM essentially controls the management committee, and therefore the CODM has control over the operating decisions made. However, it is unlikely in practice to make any difference whether the management committee or the chief executive officer is regarded as the CODM, since the operating results information that is regularly reviewed by both is likely to be identical.

Step 2: Can the component generate revenue and incur expenses from its business activities?

Since the test is whether the •component may earn revenues and incur expenses from its business activities, a start-up operation that has not yet earned revenues may be an operating segment, as may a component of an entity that sells primarily or exclusively to other components of the same entity. Conversely, operations, such as corporate treasury or headquarters, which generate no revenues or generate revenues that are only incidental to the activities of the entity, will not be operating segments.

Step 3: Are the component’s operating results regularly reviewed by the CODM as a basis for resource allocation and performance assessment?

A component of the entity that is •regularly reviewed by the CODM is likely to be an operating segment. In practice, a key issue in identifying operating segments is the extent to which the operating results of business units are aggregated for the purpose of review by the CODM. In many cases, the CODM will receive and review information about the operating results of individual business units as well as of groups of business units, and it may be difficult to establish which set of information the CODM uses in order to make decisions

about resources to be allocated and to assess performance. In these circumstances, IFRS 8 states that other factors may help identify a single set of components as constituting an entity’s operating segments, including the nature of the business activities of each component, the existence of managers responsible for them, and information presented to the board of directors. In this regard, IFRS 8 refers in particular to the role of what it describes as the ‘segment manager’.

For example, the CODM may review •one type of result based on product lines and another type based on geographic area. IFRS 8 states that, in these situations, operating segments should be determined based on the accountability for performance of the managers who report directly to the CODM. If the managers who report directly to the CODM each have responsibility for a particular product family, then each of those product families is an operating segment. In a matrix management structure with dual or overlapping management responsibilities (e.g., product-based and geographical areas of responsibility) judgment may need to be exercised in identifying the set of operating segments that best applies the core principle of IFRS 8.

9IFRS 8 Operating segments Implementation guidance

Example

An entity has seven operating units, which are grouped into three divisions. Each of the three divisions has a segment manager who reports directly to the CODM. In this case, it is likely that the operating segments for reporting purposes would be the divisions as opposed to the operating units, because the divisions have segment managers who report directly to the CODM. However, the existence of the managers does not necessarily mean that there are only three segments. If the CODM were to use information from the seven operating units to assess performance and allocate resources to each of the seven units, this would suggest that the responsibilities of the divisional managers were limited and that there were seven operating segments.

Step4:Isdiscretefinancialinformationavailable for the component?

This refers to the financial information •made available to the CODM for the purpose of reviewing performance and in determining how resources should be allocated. For a component to be an operating segment, the financial information about the operating results of the component should be sufficiently detailed to enable the CODM to make decisions about resources to be allocated and to assess its performance.

Yes

No

No

No

Yes

Yes

Identify the CODM

Step 1

Can the component generate revenue andincur expenses from

its business activities?

Step 2

Are the component’s operating results

regularly reviewed by the CODM as a basis

for resource allocation and performance

assessment?

Step 3

Is discrete financial information available for the component?

Step 4

The component is not an operating

segment

Determine whether the operating segmentis reportable

(Refer to part D on page 10)

10 IFRS 8 Operating segments Implementation guidance

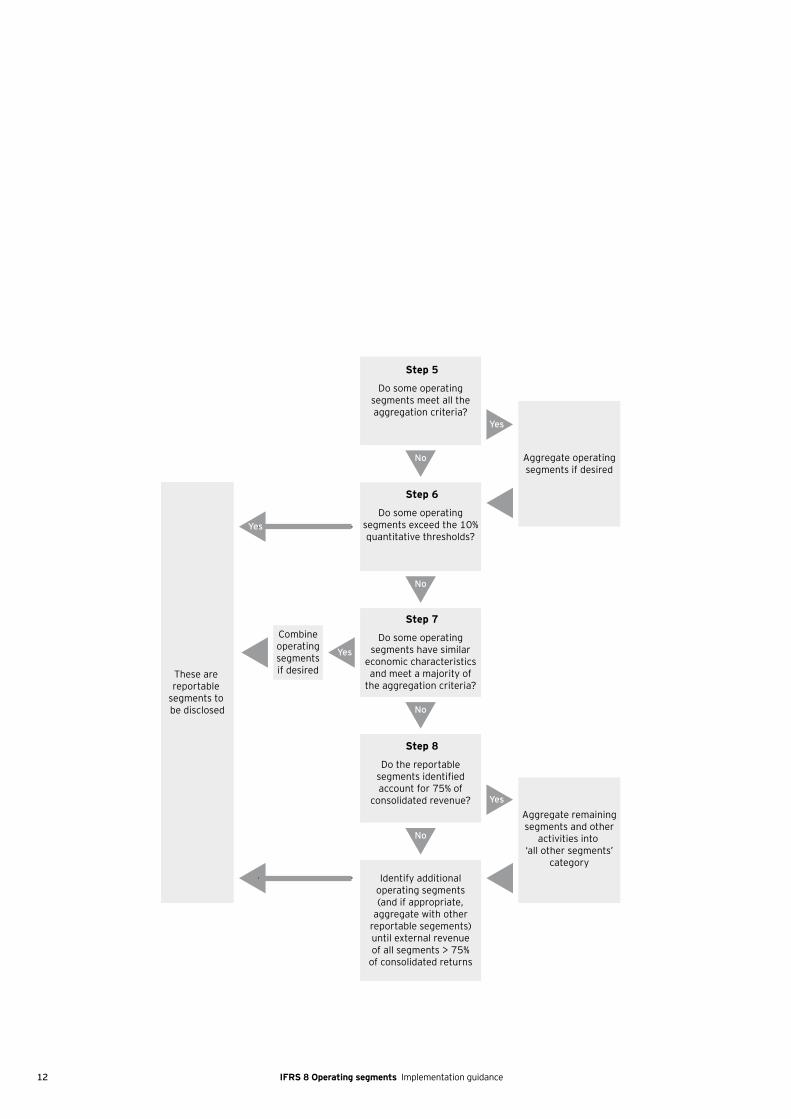

Although the definition of operating segments in IFRS 8 differs from the definition in IAS 14, the rules in IFRS 8 enabling entities, if they so wish, to aggregate two or more operating segments (into ‘reportable segments’) for the purpose of disclosing segment information in the financial statements are identical to those in IAS 14. (Note that aggregation of operating segments is not required, although IFRS 8 acknowledges that there may be a practical limit to the number of reportable segments that an entity separately discloses, beyond which segment information may become too detailed, and suggests that the practical limit may be around 10.)

Multiple operating segments may be aggregated into a single reportable segment if aggregation is consistent with the core principle of IFRS 8, the segments have similar economic characteristics, and the segments are similar in all of the following respects:

the nature of the products and services•the nature of the production processes•the type of class of customer for their •products and servicesthe methods used to distribute their •products or provide their servicesif applicable, the nature of the •regulatory environment, for example, banking, insurance or public utilities.

The Standard does not elaborate on the meaning of ‘similar economic characteristics’ except to say that: “Similar long-term average gross margins for two operating segments would be expected if their economic characteristics were similar.” This is a somewhat roundabout way of saying the same thing as IAS 14, under which operating segments could be combined if they ‘exhibit similar long-term performance’ and are similar in all of the respects listed above.

In determining whether or not operating segments have similar long-term average gross margins, an entity must consider past, current and future performance. For example, consider two operating segments that have had similar gross margins over the last five years. In the current year, a warehouse is destroyed by fire, resulting in a large inventory write-down impacting the gross margin of only one of the operating segments. In this instance, while the gross margins of the two operating segments may differ significantly in the current year, past performance is expected to be maintained in the future because the warehouse fire has not altered the underlying operations or profitability of the operating segment. In this case, the two operating segments may still be considered to have similar economic characteristics.

D. Reportable segments – What are reportable segments and how are they determined?

11IFRS 8 Operating segments Implementation guidance

In addition, while IFRS 8 highlights similar long-term gross margins as an indicator that operating segments have similar economic characteristics, other measures could be used to assess whether this criterion is met. For example, sales metrics, return on investment, or other standard industry measures such as earnings before interest, taxes, depreciation and amortisation (EBITDA) may be more relevant than gross margins if the CODM assesses performance and allocates resources based on other such key economic characteristics. Ultimately the assessment will be dependent on the facts and circumstances of each situation, and judgment will be required in determining whether or not operating segments may be combined.

Information must be reported for each (aggregated) operating segment that:

contributes 10% or more of the entity’s •total sales (combining internal and inter-segment sales),earns 10% or more of the combined •reported profit of all operating segments that did not report a loss (or 10% or more of the combined reported loss of all operating segments that reported a loss), or has 10% or more of the combined •assets of all operating segments.

These are exactly the same thresholds as in IAS 14. However, under IAS 14 a segment must earn a majority of its revenue from sales to external customers. This is not the case under IFRS 8 (i.e., an operating segment for IFRS 8 purposes may earn a majority of its revenues from sales to other segments).

D. Reportable segments – What are reportable segments and how are they determined?

After the aggregation process described above, if the total external revenue reported by operating segments constitutes less than 75% of the entity’s revenue, additional operating segments must be identified until at least 75% of the entity’s revenue is included in reportable segments. For this purpose, operating segments that do not meet the quantitative thresholds described above may be combined to produce a reportable segment only if they share similar economic characteristics and a majority of the aggregation criteria listed above.

Where an entity is required to disclose further operating segments in order to meet the 75% threshold described, it should be noted that IFRS 8 does not require an entity to disclose the next largest operating segment. This may be the most logical approach. However, an entity may disclose any other operating segment in order to meet the 75% threshold.

Once reportable segments that, in aggregate, account for at least 75% of consolidated revenue have been identified, information about all other operating segments, and other activities that are not part of an operating segment, are combined and disclosed in an ‘all other segments’ category.

The flowchart on the following page summarises the steps involved in identifying reportable segments, and a case study illustrates some of the considerations in determining reportable segments.

12 IFRS 8 Operating segments Implementation guidance

No

Do some operatingsegments meet all theaggregation criteria?

Step 5

Do some operatingsegments exceed the 10%quantitative thresholds?

Step 6

Do some operatingsegments have similar

economic characteristicsand meet a majority of

the aggregation criteria?

Step 7

Yes

Do the reportablesegments identifiedaccount for 75% of

consolidated revenue?

Step 8

Identify additionaloperating segments(and if appropriate,

aggregate with otherreportable segements)until external revenueof all segments > 75%

of consolidated returns

Aggregate operating segments if desired

Aggregate remainingsegments and other

activities into ‘all other segments’

category

Combineoperatingsegmentsif desiredThese are

reportable segments to be disclosed

No

No

No

Yes

Yes

Yes

13IFRS 8 Operating segments Implementation guidance

The operating segments of a transport and logistics group are:

Operating segment

% of consolidated revenue

Logistics/distribution services

55

Parcels 8

Van hire 7

Home moving 9

Commercial moving 8

Document storage 6

Refuse collection services

7

No two operating segments share all the IFRS 8 aggregation criteria.

Only the logistics/distribution services segment meets the 10% quantitative threshold for a reportable segment. However, as it accounts for 55% of consolidated revenue, additional operating segments must be identified as reportable segments. The entity concludes that the home moving and commercial moving segments share a majority of the aggregation criteria and decides to combine them to produce a reportable segment. However, that combined segment (accounting for 17% of consolidated revenue) and the logistics/distribution services segment together

account for only 72% of consolidated revenue. Accordingly, it is necessary to designate another operating segment as a reportable segment so that at least 75% of consolidated revenue is included in reportable segments. It would be logical to designate the next largest operating segment, in this case parcels, but the entity may choose to report the van hire, document storage or refuse collection services segment in order to satisfy the 75% revenue threshold.

Case Study

E. Measurement – How are the amounts to be disclosed measured?The amount of each segment item disclosed must be the measure reported to the CODM — any adjustments and eliminations made in preparing the financial statements may not be reflected in a reportable segment amount unless those adjustments and eliminations are included in amounts used by the CODM.

If the CODM uses more than one measure of a segment’s profit or loss, assets or liabilities, the reported measures should be those that management believes are most consistent with those used in the entity’s consolidated financial statements.

Example

If the CODM uses a measure of segment profit before income taxes that includes depreciation expense and one that does not, the appropriate measure to be reported for operating segments is the measure that includes depreciation expense, because depreciation expense is included in the measurement of the corresponding amount (i.e., profit before income taxes) in the consolidated financial statements.

The key practical benefit for an entity using the measurement approach required by IFRS 8 is that it should be quick and easy to produce the information.

As the amounts to be disclosed are based solely on the amounts the CODM reviews, it follows that, unlike segment information reported under IAS 14, these amounts may not be measured in accordance with IFRS. As discussed in Part F on pages 14 and 15, IFRS 8 requires the reportable segment amounts to be reconciled to the relevant (IFRS) amounts for the entity as a whole, but only in total and not on a segment-by-segment basis. For users of financial statements, therefore, the measurement approach in IFRS 8 may reduce comparability of the segment information presented by entities in similar industries compared with IAS 14.

14 IFRS 8 Operating segments Implementation guidance

IFRS 8 requires the following disclosures:

General information:1

the factors used to identify the entity’s •reportable segments, discussion of how the entity is organised and whether operating segments have been aggregatedthe types of products and services •from which each reportable segment receives its revenues

For each reportable segment, 2 information about profit or loss, assets and liabilities including:a measure of profit or loss•a measure of total assets•a measure of liabilities if such an •amount is regularly provided to the CODMthe amount of any of the following •items that are either included in the measure of segment profit or loss reviewed by the CODM or otherwise regularly provided to the CODM:

revenues from external customers —revenues from transactions with —other operating segments within the entityinterest revenue and expense —(interest revenue and expense may only be reported on a net basis when a majority of a segment’s revenues are from interest and the

CODM relies primarily on net interest revenue to assess the performance of the segment and make decisions about resources to be allocated to the segment)depreciation and amortisation —material items of income and —expense disclosed in accordance with paragraph 86 of IAS 1 Presentation of Financial Statementsthe entity’s interest in profit or loss —of associates and joint ventures accounted for by the equity methodincome tax expense or income —material non-cash items other than —depreciation and amortisation.

any of the following items that are 3 either included in the measure of segment assets reviewed by or otherwise regularly provided to the CODM:the investment in equity-accounted •associates and joint venturestotal additions to non-current assets •other than financial instruments, deferred tax assets, post-employment benefits and rights arising under insurance contracts (i.e., property, plant and equipment and intangible assets and investments, for the most part)

An explanation of the measurement 4 basis of segment information, including:the basis of accounting for inter-•segment transactionsif not apparent from the reconciliations •described below, the nature of any differences between the measurement of the following items in the reported segment information and the same items in the entity’s financial statements in accordance with IFRS:

profit or loss before income tax and —discontinued operationsassets —liabilities —

As well as accounting policy 5 differences, measurement differences might include policies for allocating central costs or jointly used or shared assets and liabilities to individual segments:the nature of any changes from prior •periods in the measurement methods used to determine segment profit or loss and the effect, if anythe nature and effect of any •asymmetrical allocations to reportable segments (e.g., an allocation of depreciation expense when the related depreciable assets are not allocated to the same segment)

F. Disclosure – What disclosures are required?

15IFRS 8 Operating segments Implementation guidance

Reconciliations of:6

the total of the reportable segments’ •revenues to the entity’s revenuethe total of the reportable segments’ •profit or loss to the entity’s profit or loss before income tax and discontinued operations (or, if items such as income tax are allocated to segments, to profit or loss after tax)the total of the reportable segments’ •assets to the entity’s assetsthe total of the reportable segments’ •liabilities to the entity’s liabilitiesthe total of the reportable segments’ •amounts for every other material item of information disclosed to the corresponding amount for the entity.

All material reconciling items must be 7 separately identified and described.

Entity-wide disclosures, to the 8 extent that this information is not provided as part of the reportable segment information:external revenues on an IFRS basis •for each group of similar products and servicesexternal revenues on an IFRS basis •attributed to (1) the entity’s country of domicile and (2) all foreign countries, with separate disclosure of revenues attributed to individual foreign countries, if material; the entity must disclose the basis on which revenues have been attributed to different countries

non-current assets on an IFRS basis •other than financial instruments, deferred tax assets, post-employment benefit assets, and rights arising under insurance contracts (i.e., property, plant and equipment, intangible assets and investments, for the most part):located in the entity’s country of domicile•located in all foreign countries.•Separate disclosure of assets in an 9 individual foreign country must be made if the assets are material.

Where any of the entity-wide 10 information required to be disclosed is not available, and the cost to develop it would be excessive, an entity must disclose that fact.

If revenues from a single external 11 customer (for which purpose entities under common control and entities under the control of a particular government are in each case considered to be a single customer) amount to 10% or more of an entity’s revenues, the total revenues from the customer concerned and the identity of the segments reporting the revenues must be disclosed. Disclosure of the name of the customer(s) is not required.

If an entity changes the structure of 12 its internal organisation in a manner that causes the composition of its reportable segments to change, the corresponding information for earlier periods must be restated unless the information is not available and the cost to develop it would be excessive, in which case segment information for the year in which the change occurs must be disclosed on both the old basis and the new basis of segmentation (unless the necessary information is not available and the cost to develop it would be excessive).

Many of the disclosures required by 13 IFRS 8 should come from readily available information within the entity so that a minimal amount of time and effort should be required to prepare them. More effort may be required, however, in preparing the reconciliations of the segment information to the relevant IFRS amounts appearing in the financial statements and the associated explanations. Prior to the adoption of IFRS 8 an entity should assess its systems and processes to ensure that the required information can be prepared.

F. Disclosure – What disclosures are required?

16 IFRS 8 Operating segments Implementation guidance

The following example applies the steps set out in the flowcharts and related guidance in Section 2 to arrive at the information that a fictional entity, Super Food Limited, based in Germany, must disclose in its consolidated financial statements to comply with IFRS 8. In Part A, IFRS 8 requirements are applied to Super Food Limited to ascertain what disclosures are required. In Part B the financial statement disclosures required in annual financial statements are illustrated for the year ended 31 December 200X. Part C illustrates the disclosure requirements of IAS 34 for the six-month period ended 30 June 200X.

No comparative information is included in the example, as the disclosure requirements apply equally to both current year and comparative periods included in an entity’s financial statements.

A. Identification of operating segments and reportable segmentsThe following information has been obtained as a basis for determining the entity’s reportable segments:

Per Step 1 of the flowchart on page 9, •the CODM is the chief executive officer.Per Step 2, the following 10 business •activities, ranked by the size of their revenues, also incur expenses:

retail sales of bakery products —direct catering services to the —business marketdirect catering services to the —domestic marketmanufacturing of bakery products —cook book publishing —food magazine publishing —web publishing —leasing of offices —leasing of manufacturing sites —mail order distribution of —bakery products.

Per Step 3, the CODM reviews the •results of the following eight business activities:

mail order distribution of —bakery productsretail sales of bakery products —direct catering services to the —business marketdirect catering services to the —domestic marketmanufacturing of bakery products —cook book publishing —food magazine publishing —leasing of property (includes —intra-group leasing and property leased to third parties).

Per Step 4, discrete financial •information is available for all the business activities identified in Step 3. The entity, therefore, has eight operating segments as defined by IFRS 8.Per Step 5 of the flowchart on page •13, only the cook book and food magazine publishing operations are

Section 3

Illustrative example

17IFRS 8 Operating segments Implementation guidance

similar in all the respects listed in IFRS 8 and therefore meet all of the segment aggregation criteria. These two segments are combined into one reportable segment called ‘Publishing’ for financial reporting purposes.Per Step 6, the mail order distribution •of bakery products, direct catering services to the domestic market, direct catering services to the business market, and leasing of property do not exceed any of the 10% quantitative thresholds, and so they are not required to be separately reported.Per Step 7, the two operating •segments providing catering services (which individually do not meet the quantitative thresholds) are regarded as having similar economic characteristics and share a majority of the aggregation criteria and so are combined into ‘Catering’. However, mail order and leasing of property do not share a majority of the aggregation criteria with any other segment and so they are not combined with any other segments.

Per Step 8, the reportable segments •identified thus far (retail sales of bakery products, catering, manufacturing of bakery products and publishing) account for more than 75% of consolidated revenue and so no additional reportable segments are required to be identified. As shown in the flowchart, the remaining operating segments (mail order and investment property) are aggregated into an ‘All other segments’ category.

The majority of the revenues of the bakery products manufacturing segment arise from sales to other operating segments. It is reported as an operating segment under IFRS 8 because it exceeds the 10% quantitative threshold, even though a majority of its revenues are earned through sales to other operating segments. Under IAS 14, it would not have been reported because it does not earn a majority of revenues from sales to external customers.

B. Example disclosure: IFRS 8 in annual financial statementsIn the Super Food Limited example, the information provided to the CODM is based on the same accounting policies as the financial statements (i.e., IFRS) with the following exceptions:

segment profit or loss before tax •excludes any expenses associated with share-based payments and other management bonusesfinance costs, other income and income •taxes are managed on a group basis and are not allocated to any segmentsegment revenues in the publishing •segment and the related receivables are recognised on shipment of the books and magazines, rather than on delivery to the customer.

CommentaryThe following illustration shows the consolidated income statement and balance sheet of Super Food Limited, as well as the required disclosures under IFRS 8. Commentary boxes highlight where key IFRS 8 disclosures differ from those required by IAS 14 and where entirely new disclosures are required. References to the relevant paragraphs of IFRS 8 are also provided to the right of each disclosure.

18 IFRS 8 Operating segments Implementation guidance

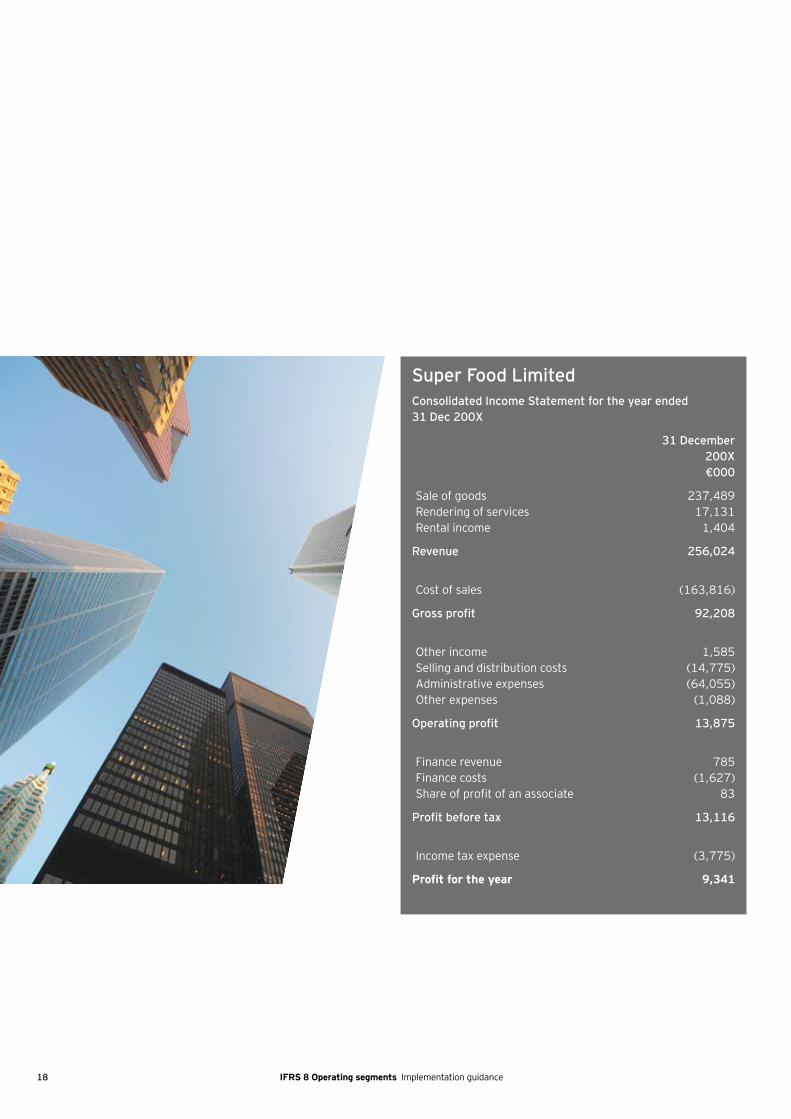

Super Food LimitedConsolidated Income Statement for the year ended 31 Dec 200X

31 December 200X €000

Sale of goods 237,489Rendering of services 17,131Rental income 1,404

Revenue 256,024

Cost of sales (163,816)

Gross profit 92,208

Other income 1,585Selling and distribution costs (14,775)Administrative expenses (64,055)Other expenses (1,088)

Operating profit 13,875

Finance revenue 785Finance costs (1,627)Share of profit of an associate 83

Profit before tax 13,116

Income tax expense (3,775)

Profitfortheyear 9,341

19IFRS 8 Operating segments Implementation guidance

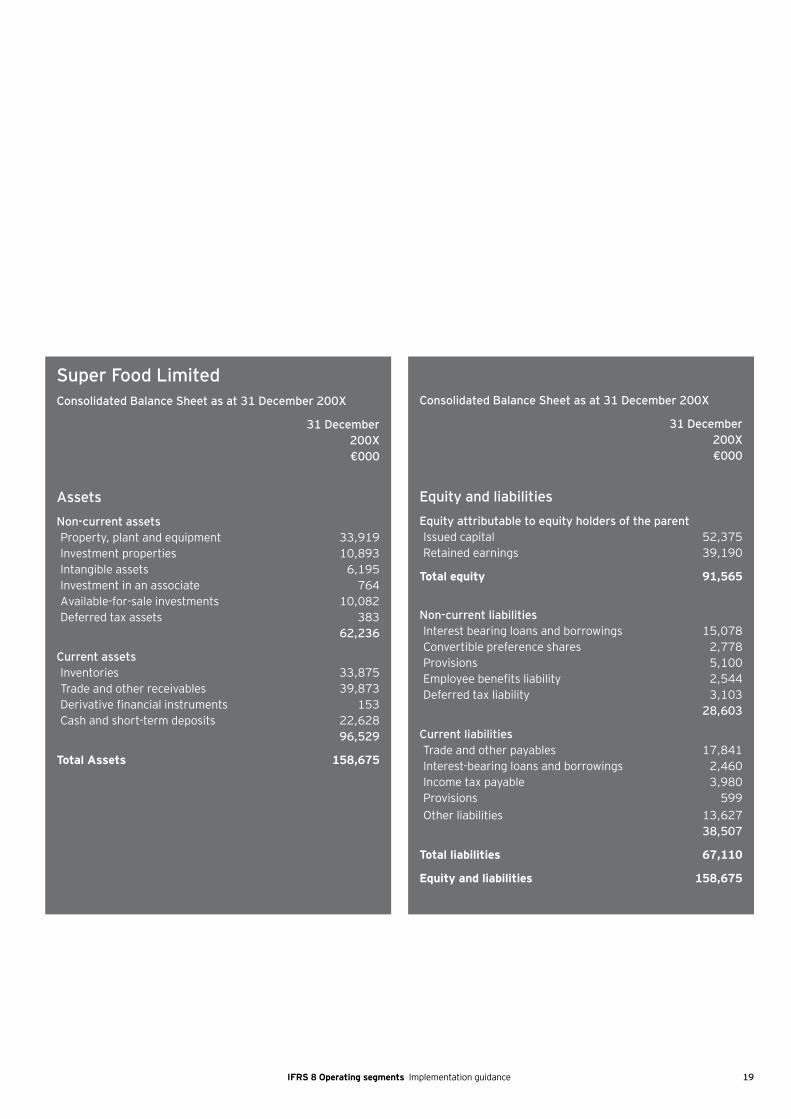

Super Food LimitedConsolidated Balance Sheet as at 31 December 200X

31 December 200X €000

AssetsNon-current assetsProperty, plant and equipment 33,919Investment properties 10,893Intangible assets 6,195Investment in an associate 764Available-for-sale investments 10,082Deferred tax assets 383

62,236

Current assetsInventories 33,875Trade and other receivables 39,873Derivative financial instruments 153Cash and short-term deposits 22,628

96,529

TotalAssets 158,675

Consolidated Balance Sheet as at 31 December 200X

31 December 200X €000

Equity and liabilitiesEquity attributable to equity holders of the parentIssued capital 52,375Retained earnings 39,190

Totalequity 91,565

Non-current liabilitiesInterest bearing loans and borrowings 15,078Convertible preference shares 2,778Provisions 5,100Employee benefits liability 2,544Deferred tax liability 3,103

28,603

Current liabilitiesTrade and other payables 17,841Interest-bearing loans and borrowings 2,460Income tax payable 3,980Provisions 599Other liabilities 13,627

38,507

Totalliabilities 67,110

Equityandliabilities 158,675

20 IFRS 8 Operating segments Implementation guidance

CommentaryThe first paragraph of the segment information note is similar to what is required under IAS 14. However, the subsequent narrative responds to new requirements to provide sufficient detail for the reader to understand how the organisation is structured, on what basis management has determined the reportable segments, and whether any operating segments have been combined.

IFRS 8 and IAS 14 both require the basis of pricing inter-segment transfers to be disclosed. Discussion of the differences between the measurement of segment results and the consolidated financial statements is a new requirement, because no such differences could arise under IAS 14.

Note X – Segment informationThe group’s reportable segments are as follows:

The retail segment sells bakery products produced by the manufacturing segment •through retail outlets.The catering segment provides catering services to both the domestic and •business market.The manufacturing segment produces bakery products for sale primarily to other •segments.The publishing segment produces books and magazines on food and cooking.•The ‘Other’ category consists of:•

mail order distribution of bakery products, and —leasing of property to group companies and third parties. —

For management purposes, the group is organised into eight business segments based on their products and services. For financial reporting purposes, the publishing segment combines the cook book publishing and magazine publishing businesses, while the catering segment combines the business direct catering services and domestic direct catering services.

Management monitors the operating results of business segments separately for the purpose of making decisions about resources to be allocated and of assessing performance. Segment performance is evaluated based on operating profit or loss which in certain respects, as explained in the table below, is measured differently from operating profit or loss in the consolidated financial statements. Finance costs, finance income and income taxes are managed on a group basis.

IFRS disclosure requirement

IFRS 8.22(a)

IFRS 8.22(b)

IFRS 8.22(a)

Operating segments – 31 December 200X

Retail Catering Manufacturing Publishing Other Eliminations and Adjustments

Consolidated

€000 €000 €000 €000 €000 €000 €000 IFRS 8.23(a)

Revenues

Third party 129,842 59,388 2,704 32,306 32,686 (902)1 256,024 IFRS 8.23(b)

Inter-segment – 7,465 36,791 – 4,761 (49,017)2 –

Total revenues 129,842 66,853 39,495 32,306 37,447 (49,919) 256,024

1. Segment revenue and the related receivables for the publishing segment are recognised on shipment of goods. In the consolidated financial statements, such revenue and receivables are recognised when the goods are delivered to the retailer.

IFRS 8.27

2. Sales between segments are made at prices that approximate market prices. IFRS 8.27(a)

21IFRS 8 Operating segments Implementation guidance

Note X – Segment information (continued)Operating segments – 31 December 200X

Retail Catering Manufacturing Publishing Other Eliminations and Adjustments

Consolidated IFRS disclosure requirement

€000 €000 €000 €000 €000 €000 €000

Profit before tax 6,887 4,716 1,283 1,169 3,284 (4,223)3 13,116 IFRS 8.23

Depreciation and amoritisation

2,609 819 206 – 183 – 3,817 IFRS 8.23(e)

Decrease in fair value of investment property

– – – – 306 – 306 IFRS 8.23(i)

Gain on disposal of property, plant and equipment

341 – – – 191 – 532 IFRS 8.23(i)

Share of profit of associate

– 83 – – – – 83 IFRS 8.23(g)

Segment assets 52,647 45,145 24,620 14,165 23,829 (1,731)4 158,675 IFRS 8.23

Investment in associate – 764 – – – – 764 IFRS 8.24(a)

Capital expenditure5 8,579 1,207 1,842 216 63 – 11,907 IFRS 8.24(b)

Segment liabilities 14,839 9,783 3,609 4,704 6,776 27,3996 67,110 IFRS 8.23

3. Profit before tax does not include management bonus expense (€1,489), share-based payment expense (€990), finance revenue (€785) or finance costs (€1,627), while the additional segment revenue recognised on shipment of goods (€902) included in segment profit before tax is not included in the consolidated profit before tax.

IFRS 8.27(b)

4. As noted above, segment assets include receivables related to recognition of revenue on shipment (€2,114) and do not include deferred tax assets managed on a group basis (€383).

IFRS 8.27(c)

5. Capital expenditure consists of additions of property, plant and equipment and intangible assets.

6. Loans and borrowings (€17,538), convertible preference shares (€2,778), and tax liabilities (€7,083) are managed on a group basis, and are not allocated to operating segments.

IFRS 8.27(d)

CommentaryThe disclosure of liabilities by segment is required under IAS 14. However, it is only required by IFRS 8 if it is provided to the CODM. In this example, a measure of segment liabilities for operating segments is provided to the CODM, and is therefore disclosed.

IFRS 8 requires ‘additions to non-current assets’ other than financial instruments, deferred tax assets, post-employment benefit assets and rights arising under insurance contracts to be disclosed. Under IAS 14, only additions to property, plant and equipment and intangible assets were disclosed. In most cases the amount to be disclosed under IFRS 8 will be the same as the amount disclosed under IAS 14.

22 IFRS 8 Operating segments Implementation guidance

Note X – Segment information (continued)

IFRS disclosure requirement

Geographic information

Revenue from external customers

€000 IFRS 8.33(a)

Germany 75,123

France 30,476

United Kingdom 38,272

United States 62,349

Other countries 49,804

256,024

The revenue information above is based on the location of the customer. Revenue from one customer amounted to €27,506,000, arising from sales by the catering and publishing segments.

IFRS 8.33(a) IFRS 8.34

Location of non-current assets

€000 IFRS 8.33(b)

Germany 22,165

France 12,370

United Kingdom 10,518

United States 5,230

Other countries 1,488

51,771

Non-current assets for this purpose consist of property, plant and equipment, investment properties, intangible assets and investment in an associate.

CommentaryThe above table shows the entity-wide disclosures required by IFRS 8 to the extent that the information concerned is not already disclosed elsewhere.

C. Example disclosure: IFRS 8 and IAS 34This section provides an illustrative example of the disclosures required in interim financial statements when applying IFRS 8, and the consequential amendments to IAS 34. The example uses the same fictional company, Super Food Limited, and applies the revised requirements of IAS 34 to interim financial statements.

Super Food LimitedConsolidated Income Statement for the six months ended 30 June 200Y

30 June 200Y €000

Sale of goods 118,745Rendering of services 8,566Rental income 702

Revenue 128,013

Cost of sales (81,908)

Gross profit 46,105

Other income 793Selling and distribution costs (7,388)Administrative expenses (32,028)Other expenses (544)

Operating profit 6,938

Finance revenue 393Finance costs (814)Share of profit of an associate 42

Profit before tax 6,559

Income tax expense (1,888)

Profit for the period 4,671

23IFRS 8 Operating segments Implementation guidance

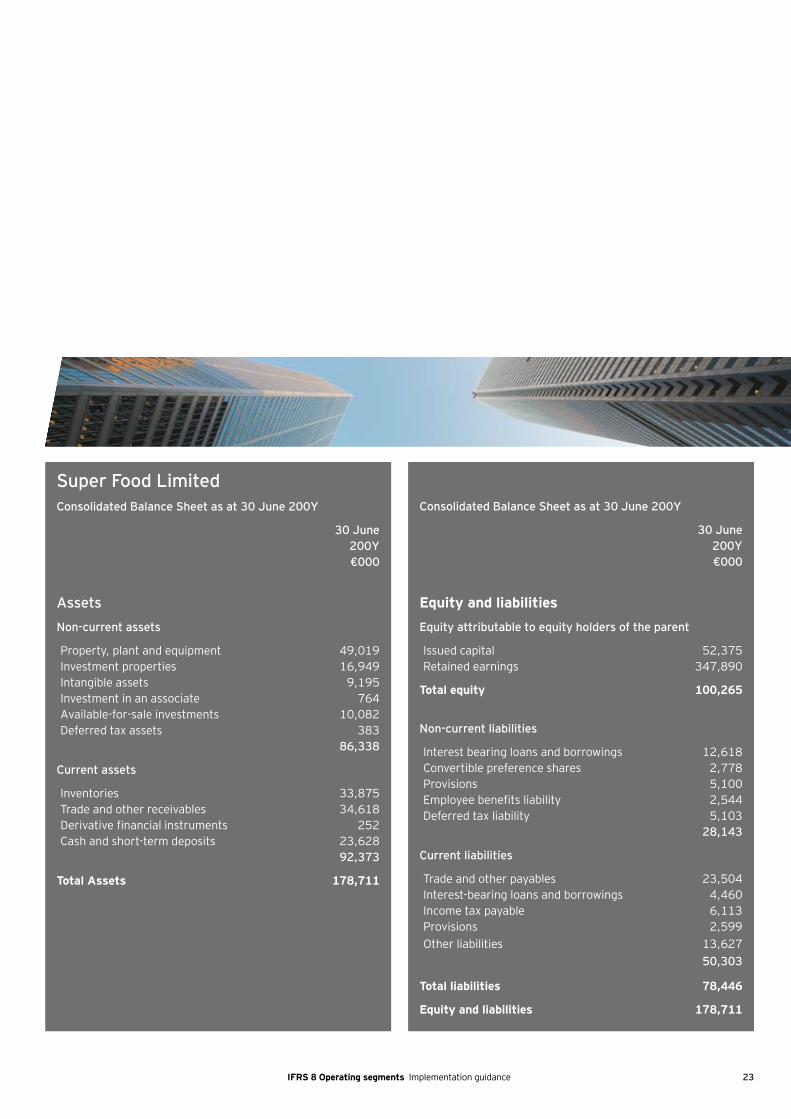

Super Food LimitedConsolidated Balance Sheet as at 30 June 200Y

30 June 200Y €000

AssetsNon-current assets

Property, plant and equipment 49,019Investment properties 16,949Intangible assets 9,195Investment in an associate 764Available-for-sale investments 10,082Deferred tax assets 383 86,338

Current assets

Inventories 33,875Trade and other receivables 34,618Derivative financial instruments 252Cash and short-term deposits 23,628

92,373

TotalAssets 178,711

Consolidated Balance Sheet as at 30 June 200Y

30 June 200Y €000

Equity and liabilitiesEquity attributable to equity holders of the parent

Issued capital 52,375Retained earnings 347,890

Totalequity 100,265

Non-current liabilities

Interest bearing loans and borrowings 12,618Convertible preference shares 2,778Provisions 5,100Employee benefits liability 2,544Deferred tax liability 5,103 28,143

Current liabilities

Trade and other payables 23,504Interest-bearing loans and borrowings 4,460Income tax payable 6,113Provisions 2,599Other liabilities 13,627 50,303

Totalliabilities 78,446

Equityandliabilities 178,711

24 IFRS 8 Operating segments Implementation guidance

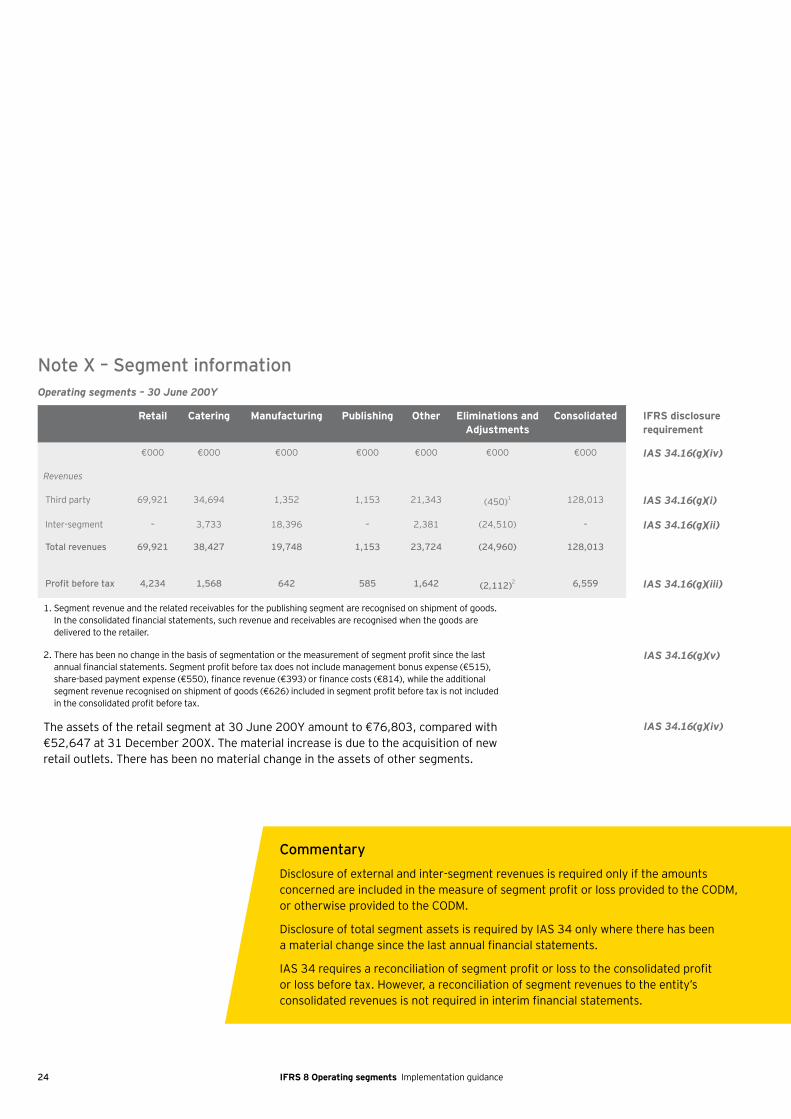

Note X – Segment informationOperating segments – 30 June 200Y

Retail Catering Manufacturing Publishing Other Eliminations and Adjustments

Consolidated IFRS disclosure requirement

€000 €000 €000 €000 €000 €000 €000 IAS 34.16(g)(iv)

Revenues

Third party 69,921 34,694 1,352 1,153 21,343 (450)1 128,013 IAS 34.16(g)(i)

Inter-segment – 3,733 18,396 – 2,381 (24,510) – IAS 34.16(g)(ii)

Total revenues 69,921 38,427 19,748 1,153 23,724 (24,960) 128,013

Profit before tax 4,234 1,568 642 585 1,642 (2,112)2 6,559 IAS 34.16(g)(iii)

1. Segment revenue and the related receivables for the publishing segment are recognised on shipment of goods. In the consolidated financial statements, such revenue and receivables are recognised when the goods are delivered to the retailer.

2. There has been no change in the basis of segmentation or the measurement of segment profit since the last annual financial statements. Segment profit before tax does not include management bonus expense (€515), share-based payment expense (€550), finance revenue (€393) or finance costs (€814), while the additional segment revenue recognised on shipment of goods (€626) included in segment profit before tax is not included in the consolidated profit before tax.

IAS 34.16(g)(v)

The assets of the retail segment at 30 June 200Y amount to €76,803, compared with €52,647 at 31 December 200X. The material increase is due to the acquisition of new retail outlets. There has been no material change in the assets of other segments.

IAS 34.16(g)(iv)

CommentaryDisclosure of external and inter-segment revenues is required only if the amounts concerned are included in the measure of segment profit or loss provided to the CODM, or otherwise provided to the CODM.

Disclosure of total segment assets is required by IAS 34 only where there has been a material change since the last annual financial statements.

IAS 34 requires a reconciliation of segment profit or loss to the consolidated profit or loss before tax. However, a reconciliation of segment revenues to the entity’s consolidated revenues is not required in interim financial statements.

25IFRS 8 Operating segments Implementation guidance

Section 4

Frequently asked questions

This section addresses some frequently asked questions relating to IFRS 8. The questions have been grouped by topic.

ScopeAre there any scope exclusions?

Yes, as in the case of IAS 14, IFRS 8 applies only to entities whose securities are traded in a public market. (IFRS 8.2)

Does IFRS 8 apply to entities that are not required to prepare consolidated financial statements?

Yes. IFRS 8 applies to separate and to individual financial statements. If a listed entity is not required to prepare consolidated financial statements then it must comply with IFRS 8. When a financial report includes both consolidated financial statements and the parent’s financial statements, segment information is required only in the consolidated financial statements. (IFRS 8.2)

Reportable operating segmentsIn order to be able to aggregate operating segments, must all of the aggregation criteria be satisfied?

In order to aggregate two (or more) operating segments that individually meet any of the 10% quantitative thresholds for a reportable segment, all criteria must be satisfied. However, operating segments that do not meet any of the quantitative thresholds for reportable

segments may also be combined if they exhibit similar economic characteristics and satisfy a majority of the aggregation criteria (rather than all of the criteria). (IFRS 8.12, IFRS 8.14)

Why are key terms such as ‘segment profit’, ‘segment assets’ and ‘segment liabilities’ not defined by IFRS 8?

Such terms are not defined by IFRS 8 because the amounts disclosed are based on each entity’s internal management reporting system. However, IFRS 8 requires an entity to explain how the measurement of these items differs from the measurement bases applied in preparing the entity’s IFRS financial statements and to reconcile the total of the segment amounts to the relevant amount in the entity’s IFRS financial statements. (IFRS 8.27)

How is a discontinued operation to be treated under IFRS 8?

IFRS 8 assumes that segment profits or losses will not include the results of discontinued operations. However, if a non-current asset or disposal group has been classified as held for sale or sold during the year and has been presented in a reportable segment, IFRS 5 requires the reporting segment concerned to be identified. Reportable segments’ profit or loss should be reconciled to the entity’s IFRS profit or loss before income tax and discontinued operations unless the measure of segment profit or loss provided to the CODM includes such amounts. (IFRS 8.25(b), IFRS 5.41(d))

MeasurementIf the measurement bases of the information provided to the CODM differ from the measurement bases of the IFRS financial statements, what needs to happen?

Reconciliations are required that separately identify and describe each adjustment needed to reconcile the total of all the reportable segments’ profits or losses to the consolidated profit or loss. To the extent that the nature of the measurement differences is not apparent from the reconciliations, they must be explained. (IFRS 8.27-28)

DisclosuresIs there an upper limit on the number of reportable segments that an entity should disclose?

IFRS 8 does not place any limit. However, it does advise that if the number of reportable segments identified exceeds 10, an entity should consider whether a practical limit has been reached. (IFRS 8.19)

If a company has only a single operating segment, what disclosures, if any, are required?

If an entity determines that it has only a single reportable operating segment then the entity-wide disclosures are still required. Entity-wide disclosures must be based on IFRS information and include:

26 IFRS 8 Operating segments Implementation guidance

revenues from external customers from •each product or service (or group of similar products or services)

revenues from external customers •(i) attributed to the entity’s country of domicile, (ii) attributed to an individual foreign country if material, and (iii) attributed to all other foreign countries, together with the basis on which revenues have been allocated to different countries

non-current assets (i) located in the •entity’s country of domicile, (ii) located in an individual foreign country if material, and (iii) located in all other foreign countries

when it is the case, the fact that the •entity receives more than 10% of its revenue from a single customer the total amount of revenues from each such customer, and the identity of the operating segment or segments reporting the revenues. (IFRS 8.31-34)

Have the segment information disclosure requirements in IAS 34 been amended in the light of IFRS 8?

Yes. The disclosures now required in IAS 34 include:

segment revenues from external •customers and inter-segment revenues, if included in the measure of profit or loss provided to the CODM or otherwise regularly provided to the CODM

a measure of segment profit or loss•

total assets of a segment where there •has been a material change from the amount disclosed in the annual financial statements

a description of any differences from •the last annual financial statements in the basis of segmentation or in the basis of measurement of segment profit or loss

a reconciliation of the total of the •reportable segments’ measures of profit or loss to the entity’s profit or loss before income tax and discontinued operations (or, if items such as income tax are allocated to segments, to profit or loss after tax). Material reconciling items must be separately identified and described. (IAS 34.16)

Does an entity have to disclose segment information that may be competitively harmful?

Yes. IFRS 8 does not grant any exemption from disclosing segment information on the grounds that it may be competitively harmful. (IFRS 8.BC109-111)

Where an entity changes its measurement of segment profit or loss, are the comparatives required to be restated?

IFRS 8 requires disclosure of any changes in measurement methods used to determine reported segment profit or loss and the effect, if any, of those changes on the measure of segment profit or loss. IAS 1 requires comparative amounts to be reclassified when the presentation or classification of items in the financial statements is amended. (IFRS 8.27, IAS 1.38)

ImpairmentIs it possible that the adoption of IFRS 8 will impact the allocation of goodwill for impairment testing under IAS 36 Impairment of Assets?

Yes. IAS 36 requires goodwill to be allocated to each cash-generating unit (CGU) or to groups of CGUs. The relevant CGU or group of CGUs must represent the lowest level within the entity at which the goodwill is monitored for internal management purposes, and may not be larger than an operating segment. If different segments are reported under IFRS 8 than were reported under IAS 14, it follows that there will be differences between the CGUs that make up an IFRS 8 segment and those that made up an IAS 14 segment. As a result, the CGUs supporting goodwill may no longer be in the same segment under IFRS 8 as under IAS 14. This could occur in particular where goodwill has been allocated to groups of CGUs at or close to the level of a segment. It may therefore be necessary to reallocate goodwill associated with CGUs that are affected by the change from IAS 14 to IFRS 8. It is possible that this reallocation of goodwill could ‘expose’ CGUs for which the carrying amount, including the allocated goodwill exceeds the recoverable amount, thereby giving rise to an impairment loss.

27IFRS 8 Operating segments Implementation guidance

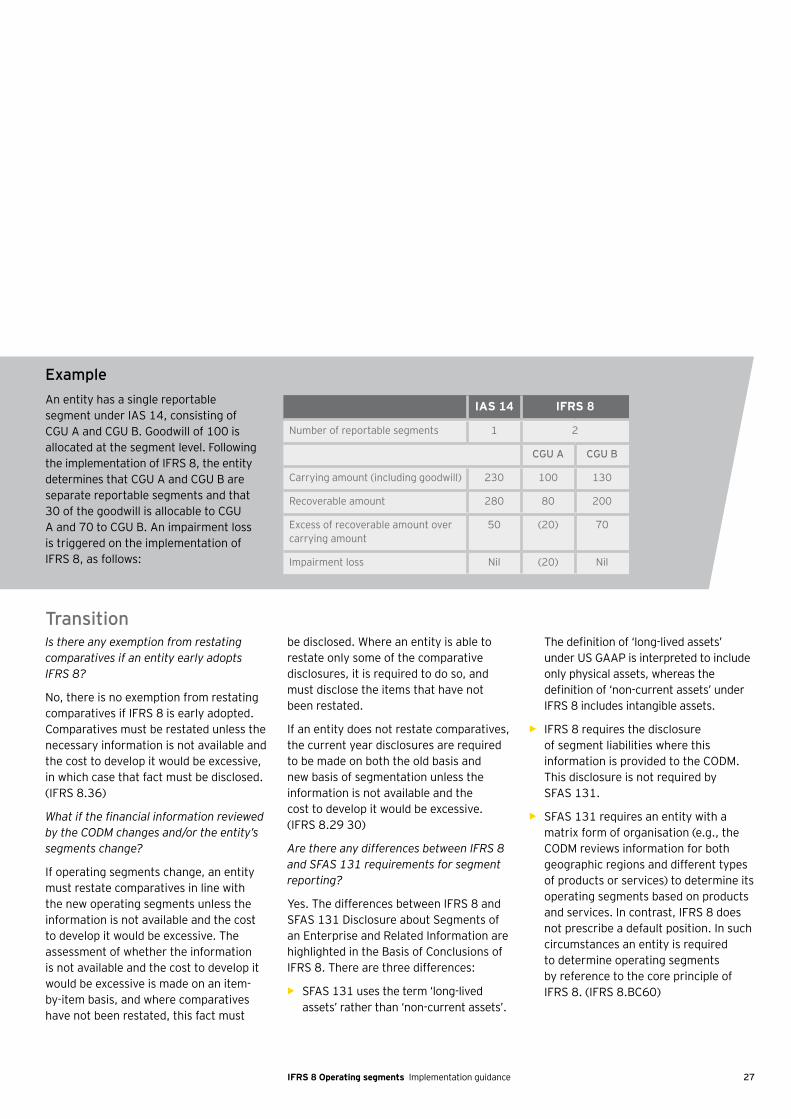

An entity has a single reportable segment under IAS 14, consisting of CGU A and CGU B. Goodwill of 100 is allocated at the segment level. Following the implementation of IFRS 8, the entity determines that CGU A and CGU B are separate reportable segments and that 30 of the goodwill is allocable to CGU A and 70 to CGU B. An impairment loss is triggered on the implementation of IFRS 8, as follows:

IAS 14 IFRS 8

Number of reportable segments 1 2

CGU A CGU B

Carrying amount (including goodwill) 230 100 130

Recoverable amount 280 80 200

Excess of recoverable amount over carrying amount

50 (20) 70

Impairment loss Nil (20) Nil

Example

Is there any exemption from restating comparatives if an entity early adopts IFRS 8?

No, there is no exemption from restating comparatives if IFRS 8 is early adopted. Comparatives must be restated unless the necessary information is not available and the cost to develop it would be excessive, in which case that fact must be disclosed. (IFRS 8.36)

What if the financial information reviewed by the CODM changes and/or the entity’s segments change?

If operating segments change, an entity must restate comparatives in line with the new operating segments unless the information is not available and the cost to develop it would be excessive. The assessment of whether the information is not available and the cost to develop it would be excessive is made on an item-by-item basis, and where comparatives have not been restated, this fact must

be disclosed. Where an entity is able to restate only some of the comparative disclosures, it is required to do so, and must disclose the items that have not been restated.

If an entity does not restate comparatives, the current year disclosures are required to be made on both the old basis and new basis of segmentation unless the information is not available and the cost to develop it would be excessive. (IFRS 8.29 30)

Are there any differences between IFRS 8 and SFAS 131 requirements for segment reporting?

Yes. The differences between IFRS 8 and SFAS 131 Disclosure about Segments of an Enterprise and Related Information are highlighted in the Basis of Conclusions of IFRS 8. There are three differences:

SFAS 131 uses the term ‘long-lived •assets’ rather than ‘non-current assets’.

The definition of ‘long-lived assets’ under US GAAP is interpreted to include only physical assets, whereas the definition of ‘non-current assets’ under IFRS 8 includes intangible assets.

IFRS 8 requires the disclosure •of segment liabilities where this information is provided to the CODM. This disclosure is not required by SFAS 131.

SFAS 131 requires an entity with a •matrix form of organisation (e.g., the CODM reviews information for both geographic regions and different types of products or services) to determine its operating segments based on products and services. In contrast, IFRS 8 does not prescribe a default position. In such circumstances an entity is required to determine operating segments by reference to the core principle of IFRS 8. (IFRS 8.BC60)

Transition

28 Document title Additional text

Ernst & Young’s International Financial Reporting Standards Group

A global set of accounting standards provides the global economy with one measure to assess both the potential and progress companies have made in achieving their goals. The move to International Financial Reporting Standards (IFRS) is the single most important initiative in the reporting world, the impact of which stretches far beyond accounting to affect every key decision you make, not just how you report it. Authoritative, responsive and timely advice is essential as the new system evolves — wherever you are in the world. We have acted to develop deep global resources — people and knowledge — to support our advisory teams working with clients, to help make this transition happen and to help our assurance teams who independently audit performance using the new standards. And because we understand that, to achieve your potential, you need a tailored service as much as consistent methodologies, we work to give you the benefit of our broad sector experience, our deep subject matter knowledge and the latest insights from our work worldwide. It’s how Ernst & Young makes a difference.

Assurance | Tax | Transactions | Advisory

Ernst & Young

About Ernst & YoungErnst & Young is a global leader in assurance, tax, transaction and advisory services. Worldwide, our 135,000 people are united by our shared values and an unwavering commitment to quality. We make a difference by helping our people, our clients and our wider communities achieve their potential.

For more information, please visit www.ey.com .

Ernst & Young refers to the global organization of member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients.

www.ey.com

EYG no. AU0257

© 2009 EYGM Limited. All Rights Reserved.This publication contains information in summary form and is therefore intended for general guidance only. It is not intended to be a substitute for detailed research or the exercise of professional judgment. Neither EYGM Limited nor any other member of the global Ernst & Young organization can accept any responsibility for loss occasioned to any person acting or refraining from action as a result of any material in this publication. On any specific matter, reference should be made to the appropriate advisor.