IES WEBINAR: Q3 ENERGY OUTLOOK, RENEWABLES IN YOUR EMISSIONS REDUCTION STRATEGY

30

WEBINAR SERIES INSIDE ENERGY & SUSTAINABILITY Q3 ENERGY OUTLOOK: RENEWABLES IN YOUR EMISSIONS REDUCTION STRATEGY August 18, 2016

Transcript of IES WEBINAR: Q3 ENERGY OUTLOOK, RENEWABLES IN YOUR EMISSIONS REDUCTION STRATEGY

WEBINAR SERIES INSIDE ENERGY & SUSTAINABILITY

Q3 ENERGY OUTLOOK: RENEWABLES IN YOUR EMISSIONS REDUCTION STRATEGY

August 18, 2016

WELCOMEOUR PRESENTERS

CLAYT TABOR | DISTRIBUTED ENERGY RESOURCE MANAGER

JONATHAN LEE | SENIOR ENERGY MARKET INTELLIGENCE MANAGER

INSIDE ENERGY & SUSTAINABILITY

TODAY’S TOPICS

RENEWABLES Opportunities and risk of leveraging renewables and

attributes within emission reduction strategies

ENERGY MARKET UPDATE: Q3 2016 Natural Gas Production, Storage: Supply rebalancing with demand What a potential La Niña could mean for this upcoming winter

CAPITALIZE ON LOW ENERGY RESOURCES Wholesale natural gas and electricity prices are expected to slowly rise during 2017

INSIDE ENERGY & SUSTAINABILITY

CORPORATE SUSTAINABILITY & EMISSIONS TARGETS

Renewables Landscape Corporate Goals Corporate Sustainability Strategies Procurement Complexities And Risks

INSIDE ENERGY & SUSTAINABILITY

RENEWABLES LANDSCAPE

NV

States and territories with Renewable Portfolio Standards

States and territories with voluntary renewable energy standard or target

States and territories with no standard or target

AS GU MP PR VI

29 states and the District of Columbia, have Renewable Portfolio Standards

Image sources: National Conference of State Legislatures, Energy Sage

2016 2017 2018 2019 2020 2021 2022

30% 30% 30% 30%

26%

22%

10%Permanent 10% for commercial credit

The Extension of the ITC

INSIDE ENERGY & SUSTAINABILITY

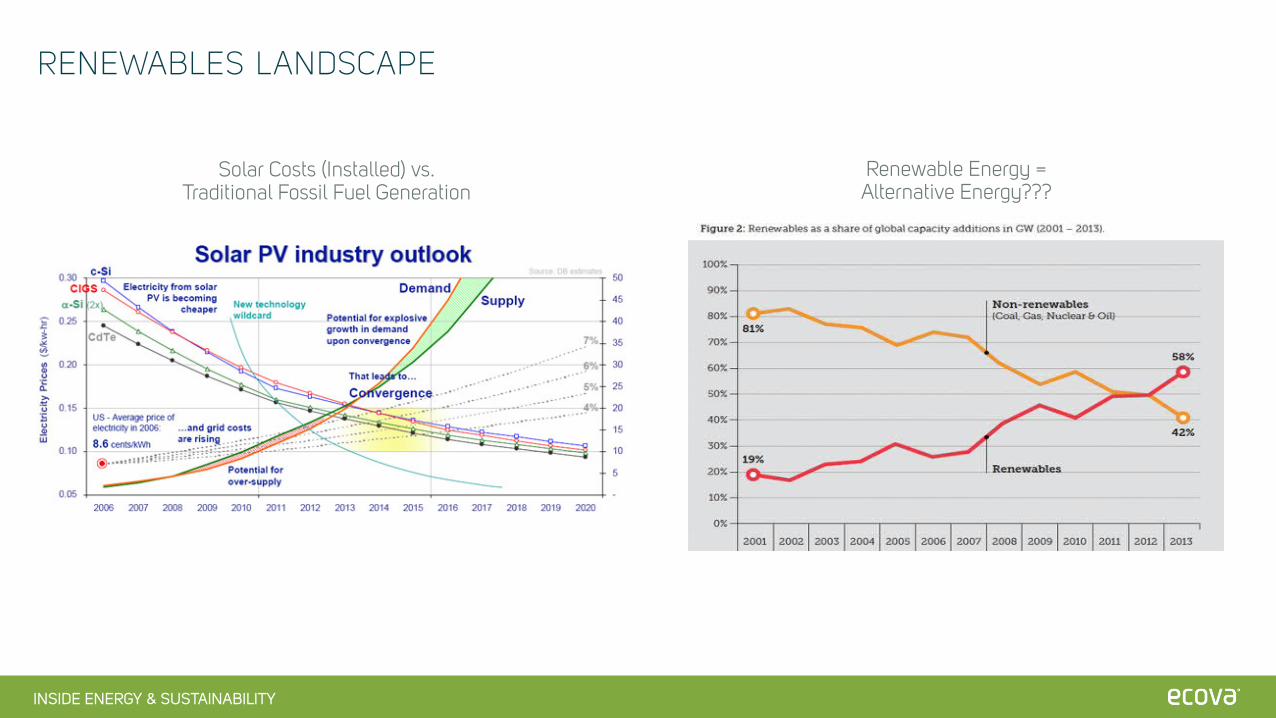

RENEWABLES LANDSCAPE

Solar Costs (Installed) vs. Traditional Fossil Fuel Generation

Renewable Energy = Alternative Energy???

INSIDE ENERGY & SUSTAINABILITY

POLL

INSIDE ENERGY & SUSTAINABILITY

CORPORATE GOALS & PROCUREMENT STRATEGIES

Corporate Goals Renewable Generation: RE100 Emissions Reductions: CDP

INSIDE ENERGY & SUSTAINABILITY

CORPORATE GOALS & PROCUREMENT STRATEGIES

Corporate Goals Renewable Generation: RE100 Emissions Reductions: CDP

Strategies Unbundled Renewable Energy Certifications (RECs) Emission Offsets Utility Green Power Programs / Sleeve Projects (Emerging Option) De-Regulated Renewable Procurement (aka Direct Access) On & Off-Site Generation Community / Shared Solar (Emerging Option) Virtual Power Purchase Agreements (VPPAs)

INSIDE ENERGY & SUSTAINABILITY

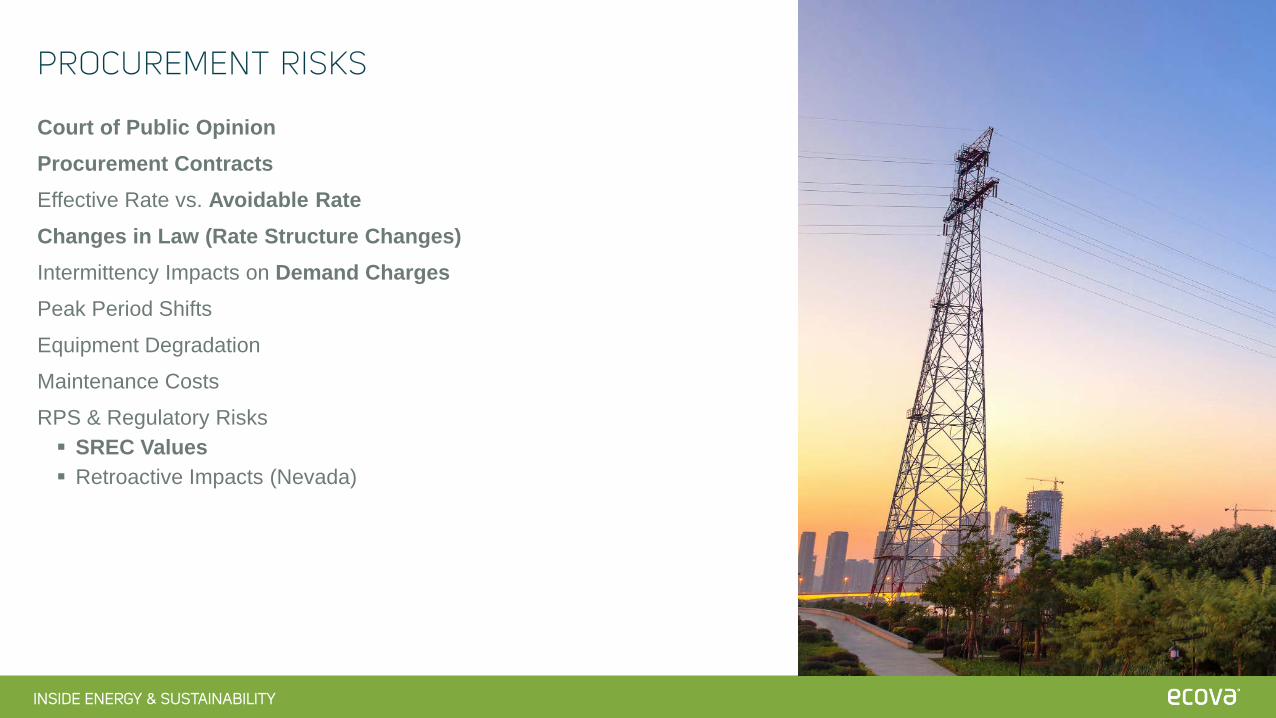

PROCUREMENT RISKS

Court of Public OpinionProcurement ContractsEffective Rate vs. Avoidable RateChanges in Law (Rate Structure Changes)Intermittency Impacts on Demand ChargesPeak Period Shifts

Equipment Degradation

Maintenance Costs

RPS & Regulatory Risks SREC Values Retroactive Impacts (Nevada)

INSIDE ENERGY & SUSTAINABILITY

A STRUCTURED APPROACH

Clearly Define Renewable Objectives & Constraints

Analyze Energy Performance, Supply Mix, & Market Dynamics

Develop/Refine Renewable Procurement Strategy

Finalize Opportunity Targets, Procure Assets & Monitor Results

INSIDE ENERGY & SUSTAINABILITY

Q3 2016 ENERGY MARKET UPDATE

INSIDE ENERGY & SUSTAINABILITY

ELECTRIC AND NATURAL GAS MARKET DRIVERS18 August 2016

Bearish – Market Influencers Driving Prices Lower:

Natural Gas Production – Declined from February high, but still in line with last year at this time.

Natural Gas Storage – Storage surplus 12.2% above last year and 15.3% above the 5-year average.

Demand – Industrial and residential/commercial sector demand lower than last year.

Economy – Q2 2016 GDP grew at 1.2% annualized rate.

Coal – Weak coal prices lower baseline electric generation costs.

Bullish – Market Influencers Driving Prices Higher:

Gas-Fired Electric Generation – At record high. Higher natural gas prices would drive electric prices higher.

Weather Forecast – Summer temperaturessupporting wholesale natural gas and electric prices.

LNG – Sabine Pass LNG exporting supplies to global markets.

Mexico Pipeline Exports – Exports up to 3.7 Bcf/day.

ISO Reliability – Retiring coal plants forcing ISO’s to evaluate grid reliability.

Interest Rate Hike – Fed considering another interest rate hike, which would increase the cost of capital and could slow natural gas and oil production.

INSIDE ENERGY & SUSTAINABILITY

$2.00

$4.00

$6.00

$8.00

$10.00

$12.00

$14.00

$/M

MBt

u

12-Month Strip Lows1/28/2002: $2.374/19/2012: $2.562/25/2016: $2.10 On February 25th, the

strip fell to its lowest level since early-1999.

Since that point, the strip has climbed back up to $3.00, which is in line with 2015 levels.

Katrina & Rita

Polar Vortex

Commodity Bubble & Collapse

Cold Winter, Supply/Demand

rebalance

Shale Gas Revolution

Supply Glut

Hurricane Ivan

NATURAL GAS 12-MONTH STRIP HOVERING AROUND $3.00$/MMBtu – 18 August 2016

INSIDE ENERGY & SUSTAINABILITY

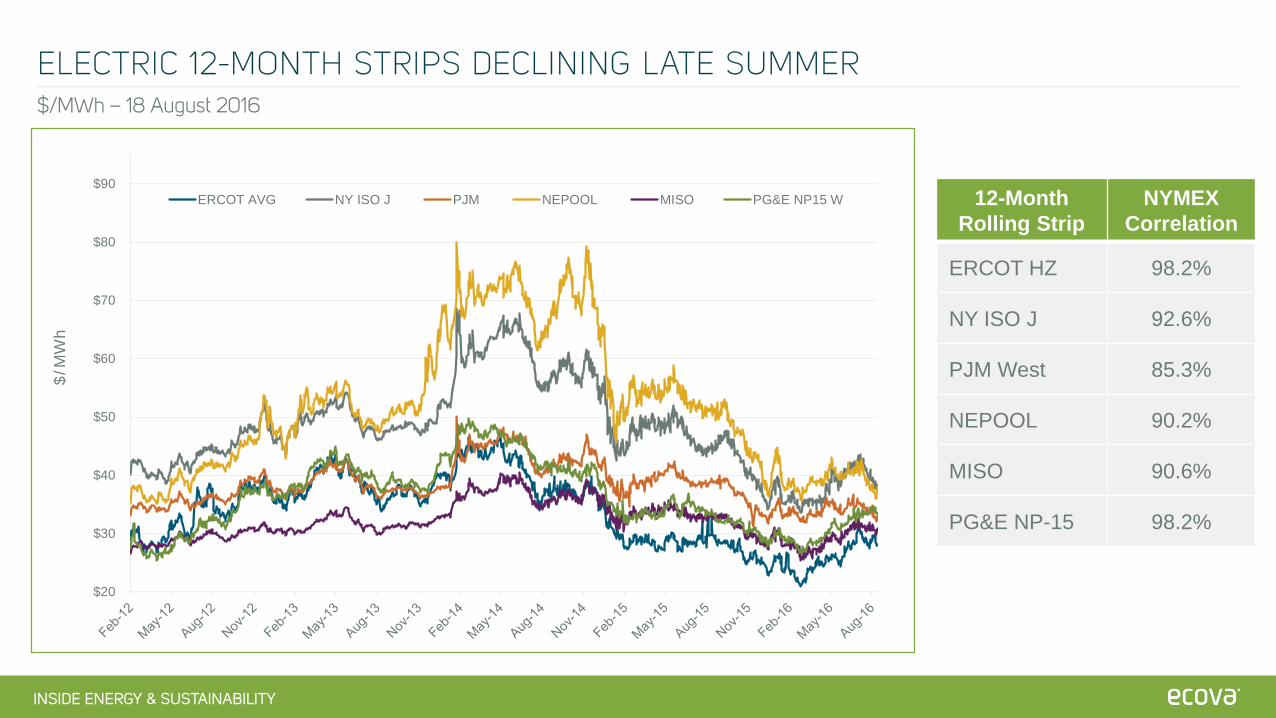

12-MonthRolling Strip

NYMEX Correlation

ERCOT HZ 98.2%

NY ISO J 92.6%

PJM West 85.3%

NEPOOL 90.2%

MISO 90.6%

PG&E NP-15 98.2%

ELECTRIC 12-MONTH STRIPS DECLINING LATE SUMMER$/MWh – 18 August 2016

$20

$30

$40

$50

$60

$70

$80

$90

$/M

Wh

ERCOT AVG NY ISO J PJM NEPOOL MISO PG&E NP15 W

INSIDE ENERGY & SUSTAINABILITY

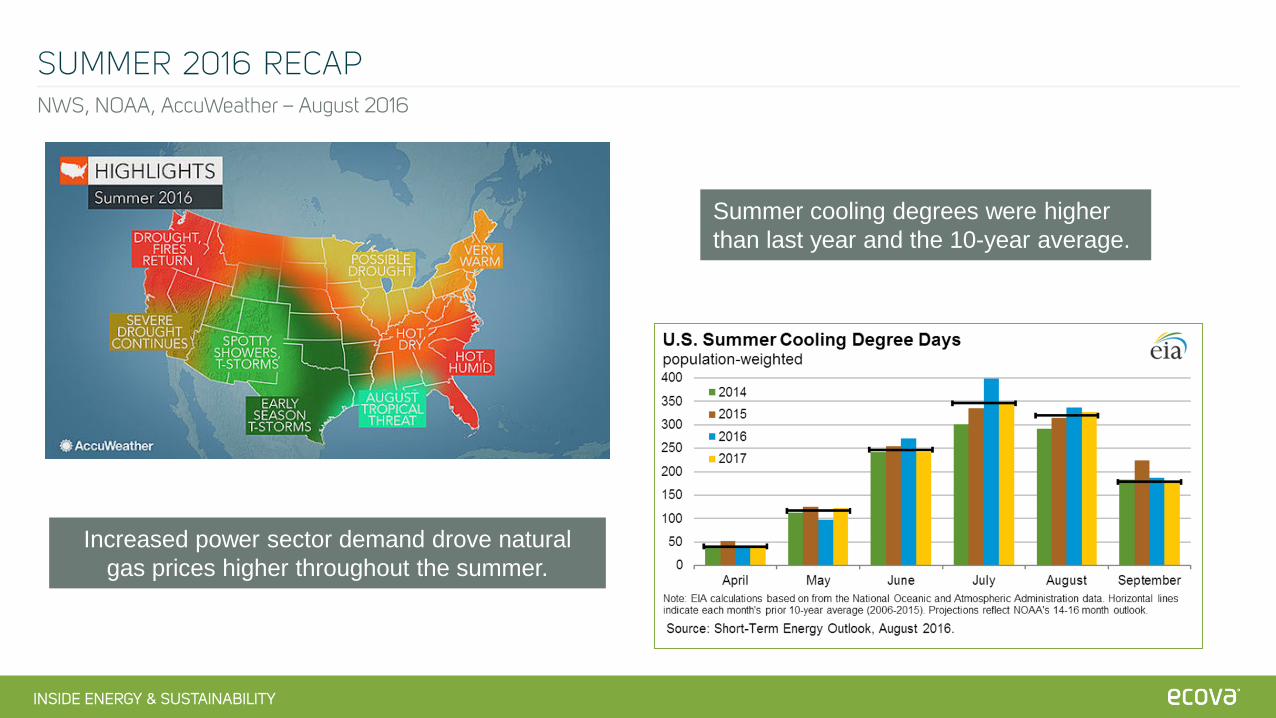

Summer cooling degrees were higher than last year and the 10-year average.

Increased power sector demand drove natural gas prices higher throughout the summer.

SUMMER 2016 RECAPNWS, NOAA, AccuWeather – August 2016

INSIDE ENERGY & SUSTAINABILITY

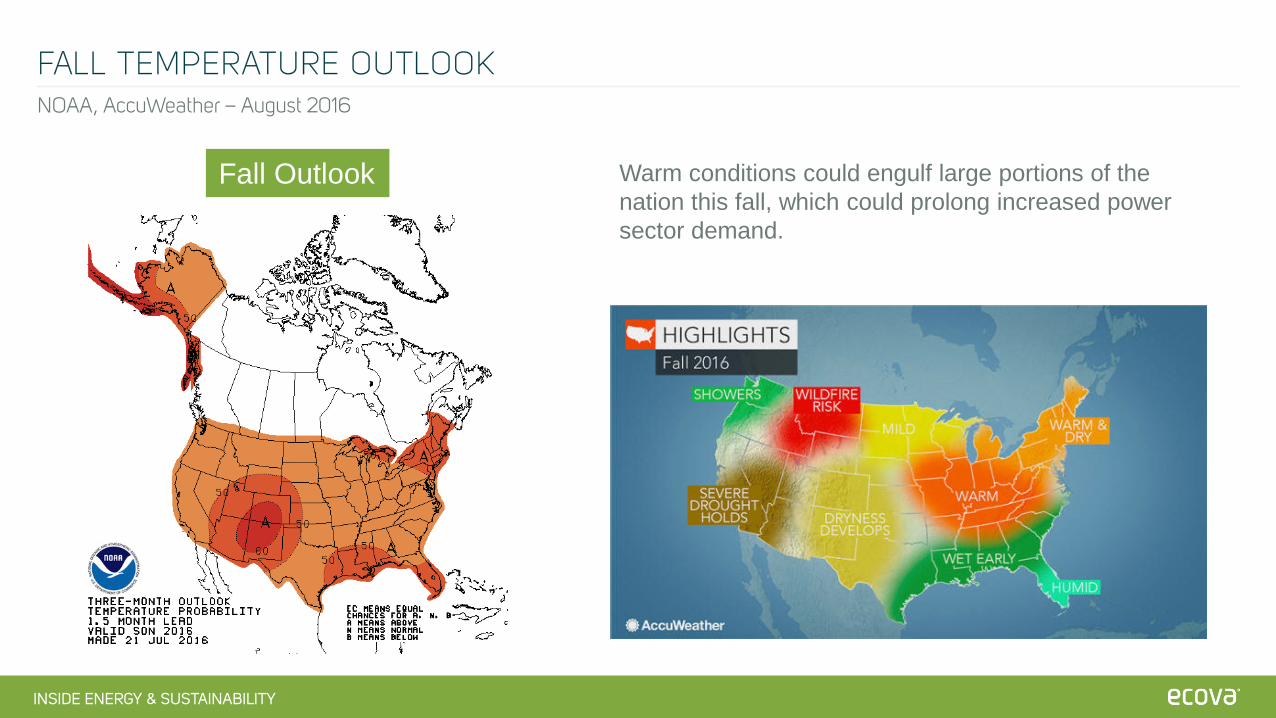

FALL TEMPERATURE OUTLOOKNOAA, AccuWeather – August 2016

Warm conditions could engulf large portions of the nation this fall, which could prolong increased power sector demand.

Fall Outlook

INSIDE ENERGY & SUSTAINABILITY

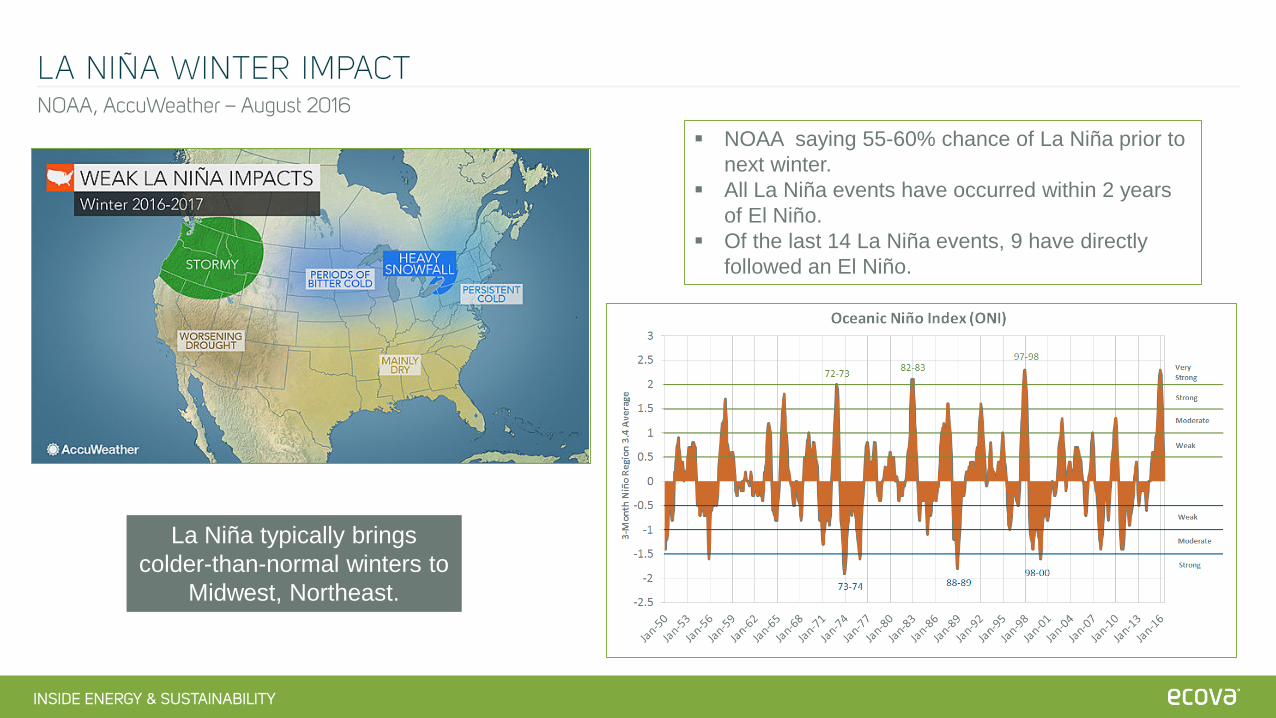

LA NIÑA WINTER IMPACTNOAA, AccuWeather – August 2016

NOAA saying 55-60% chance of La Niña prior to next winter.

All La Niña events have occurred within 2 years of El Niño.

Of the last 14 La Niña events, 9 have directly followed an El Niño.

La Niña typically brings colder-than-normal winters to

Midwest, Northeast.

INSIDE ENERGY & SUSTAINABILITY

Natural gas production peaked in Feb 2016 at 80.1 Bcf/day and bottomed out in May 2016 at 78.1 Bcf/day.

Since May, production has steadily and slowly climbed back to 78.9 Bcf/day.

During 2017, production is expected to climb back above 80 Bcf/day.

NATURAL GAS PRODUCTION STABILIZINGEIA – August 2016

Budget Impact:If demand doesn’t keep pace with rising supply, natural gas prices will weaken.

INSIDE ENERGY & SUSTAINABILITY

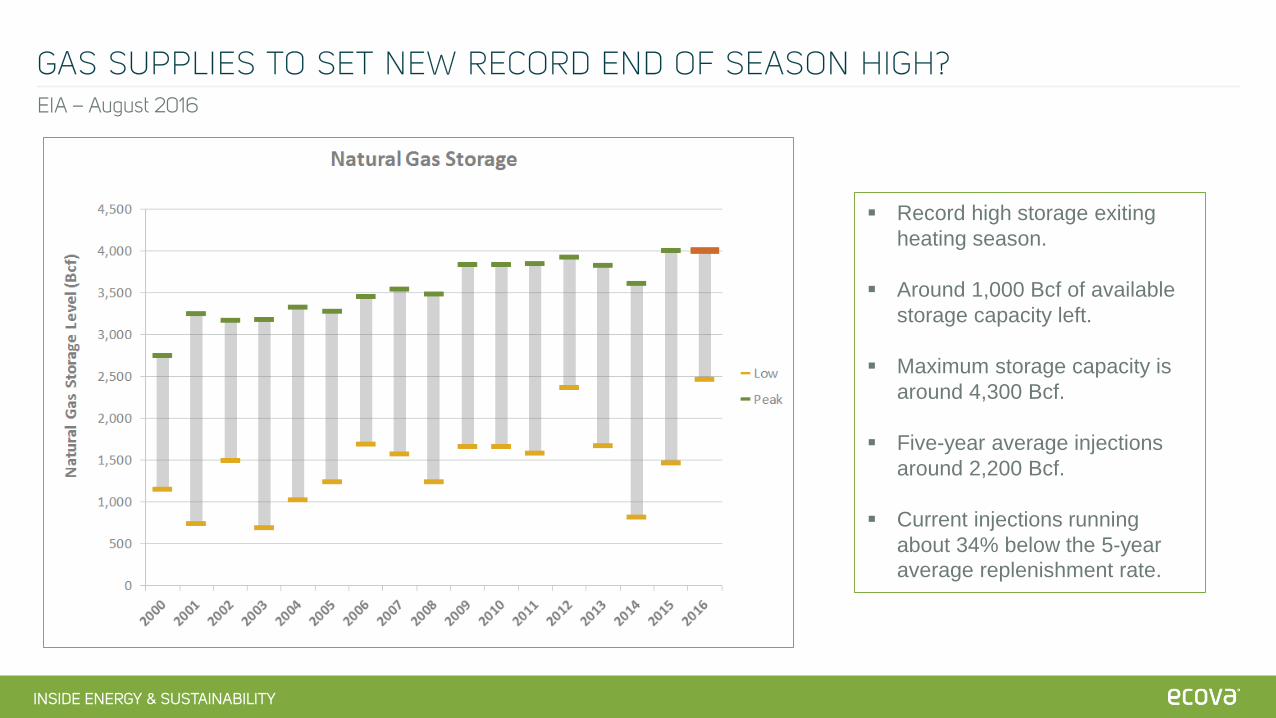

Record high storage exiting heating season.

Around 1,000 Bcf of available storage capacity left.

Maximum storage capacity is around 4,300 Bcf.

Five-year average injections around 2,200 Bcf.

Current injections running about 34% below the 5-year average replenishment rate.

GAS SUPPLIES TO SET NEW RECORD END OF SEASON HIGH?EIA – August 2016

INSIDE ENERGY & SUSTAINABILITY

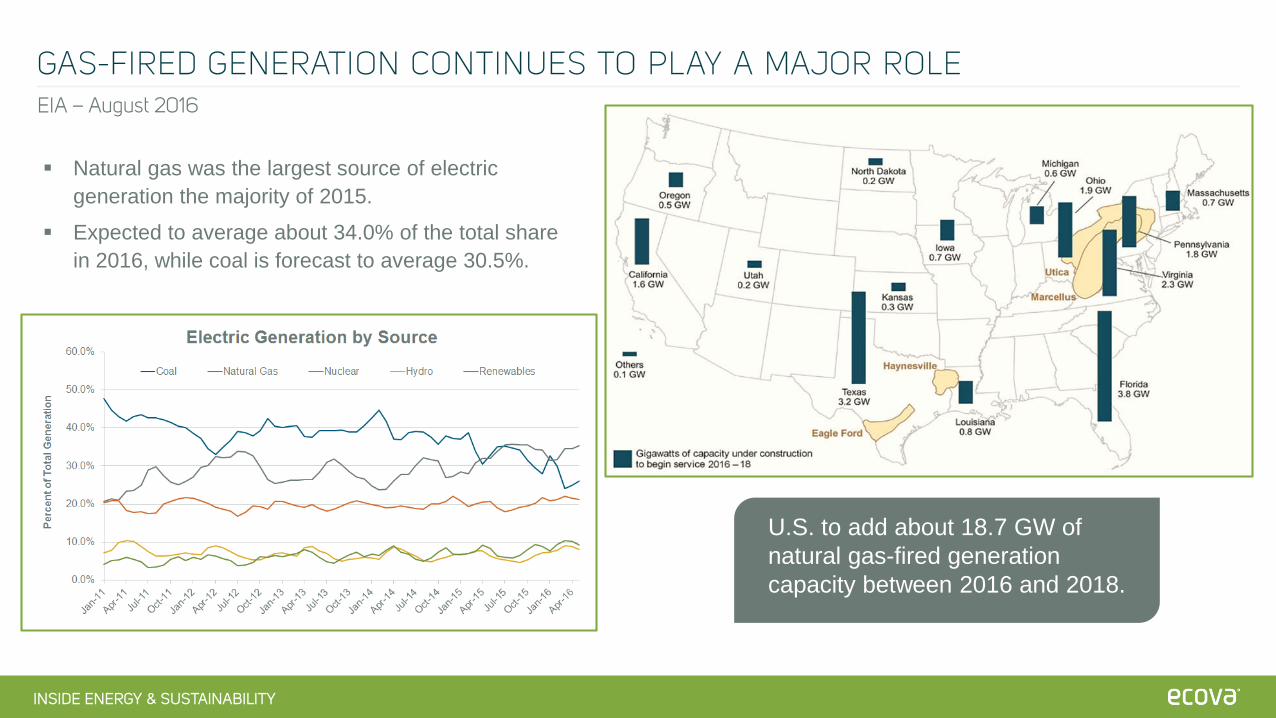

Natural gas was the largest source of electric generation the majority of 2015.

Expected to average about 34.0% of the total share in 2016, while coal is forecast to average 30.5%.

U.S. to add about 18.7 GW of natural gas-fired generation capacity between 2016 and 2018.

GAS-FIRED GENERATION CONTINUES TO PLAY A MAJOR ROLE EIA – August 2016

INSIDE ENERGY & SUSTAINABILITY

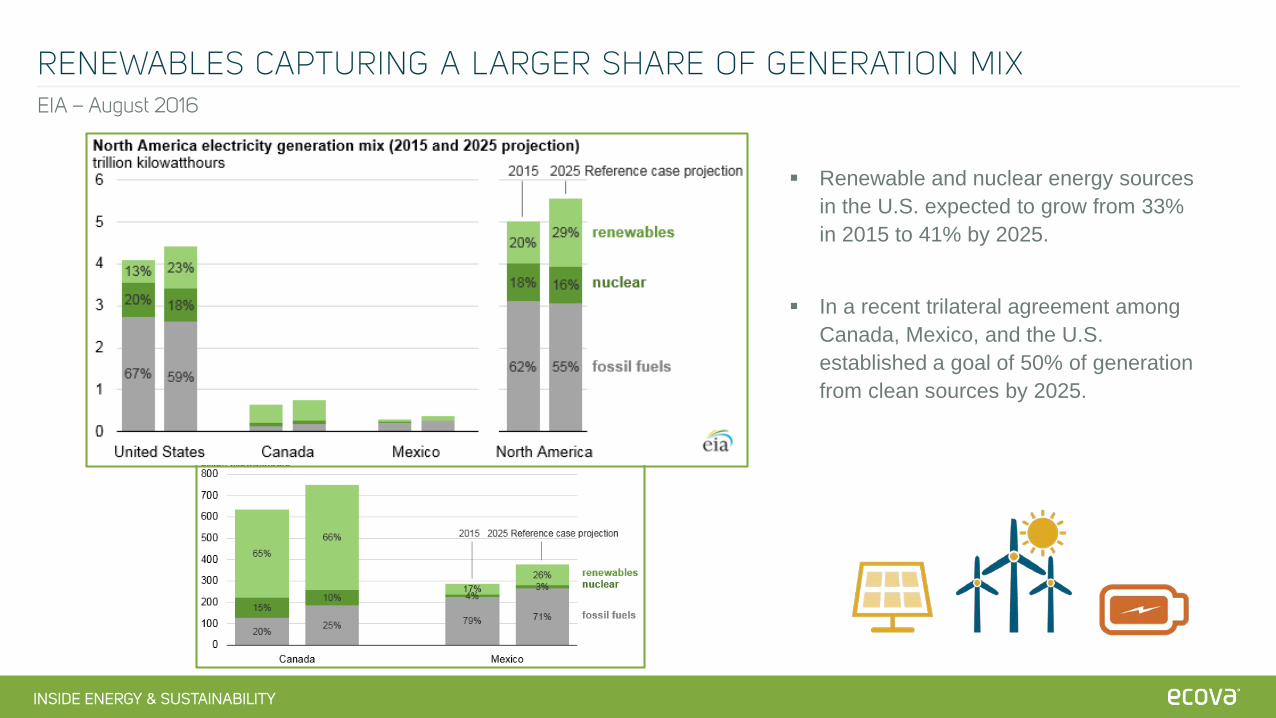

Renewable and nuclear energy sources in the U.S. expected to grow from 33% in 2015 to 41% by 2025.

In a recent trilateral agreement among Canada, Mexico, and the U.S. established a goal of 50% of generation from clean sources by 2025.

RENEWABLES CAPTURING A LARGER SHARE OF GENERATION MIXEIA – August 2016

INSIDE ENERGY & SUSTAINABILITY

NATURAL GAS PIPELINE EXPORTS TO MEXICOEIA, PGJ – August 2016

Midway through 2016, U.S. pipeline exports to Mexico increased substantially.

INSIDE ENERGY & SUSTAINABILITY

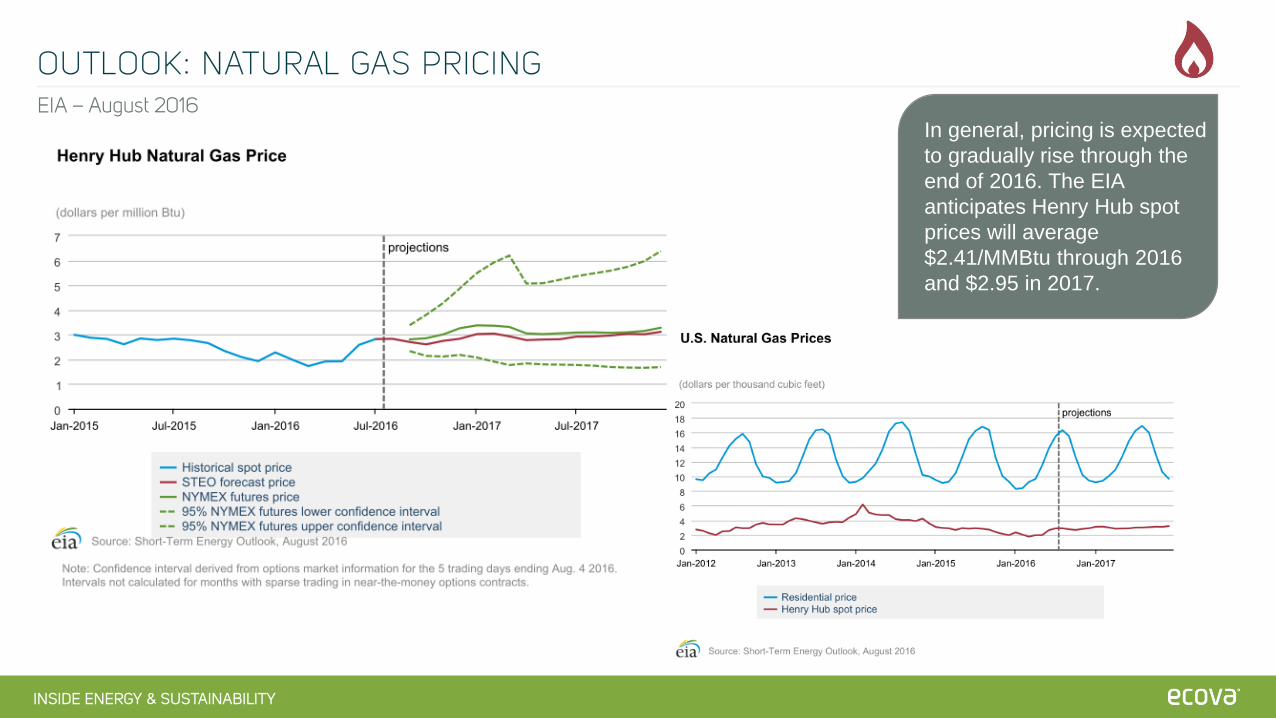

OUTLOOK: NATURAL GAS PRICINGEIA – August 2016

In general, pricing is expected to gradually rise through the end of 2016. The EIA anticipates Henry Hub spot prices will average $2.41/MMBtu through 2016 and $2.95 in 2017.

INSIDE ENERGY & SUSTAINABILITY

OUTLOOK: COMMERCIAL ELECTRIC PRICINGEIA – August 2016

Average 2017 Commercial Rates Compared to 2016:

East North Atlantic: +2.2%Mid-Atlantic: +2.2%New England: +3.9%Pacific: +2.4%South Atlantic: +3.1%South Central: +3.0%

$60

$80

$100

$120

$140

$160

$180

$200

$/M

Wh

East North Central Mid-Atlantic New England Pacific South Atlantic South Central

INSIDE ENERGY & SUSTAINABILITY

MAJOR TAKEAWAYS

UNDERSTAND OPPORTUNITIES AND RISKS OF LEVERAGING RENEWABLES WITHIN AN EMISSION REDUCTION STRATEGY.

WHOLESALE NATURAL GAS PRICES IN LINE WITH LAST YEAR. Supply and demand slowly rebalancing, but oversupply conditions still remain.

NATURAL GAS THE LARGEST SOURCE OF ELECTRIC GENERATION IN THE U.S. Regional electric markets have a higher correlation to natural gas now that it is the predominant source to

generate power.

DEPRESSED ENERGY PRICE LEVELS PRESENT OPPORTUNITY FOR LONG-TERM APPROACH TO DEREGULATED THIRD PARTY SUPPLY CONTRACTS. Wholesale natural gas and electricity prices are expected to slowly rise during 2017. Opportunities still exist to

contract low electric and natural gas contracts in deregulated markets.

UPCOMING WEBINARS

Questions, comments, suggestions?

INSIDE ENERGY & SUSTAINABILITY Complying with Waste Regulations – Food Waste 301 –

Thursday, September 29th at 11A PST

RELATED RESOURCES

Questions, comments, suggestions?

BLOG POSTS La Nina and Energy Price Increases on the Way? Early Impacts of the Brexit Decision Distributed Energy Resources – A Disruptive Opportunity

NEWSLETTER Energy Market Watch

SOLUTION Distributed Energy Resources

INSIDE ENERGY & SUSTAINABILITY

Q&A

INSIDE ENERGY & SUSTAINABILITY

THANK YOU!