IDEO: A Study in Core Competence - Towson University - Search

26

PUBLIC DISCLOSURE December 1, 2008 COMMUNITY REINVESTMENT ACT PERFORMANCE EVALUATION Southern Bancorp Bank of Arkansas RSSD # 852544 601 Main Street Arkadelphia, Arkansas 71923 Federal Reserve Bank of St. Louis P.O. Box 442 St. Louis, Missouri 63166-0442 NOTE: This document is an evaluation of this institution’s record of meeting the credit needs of its entire community, including low- and moderate- income neighborhoods, consistent with safe and sound operation of the institution. This evaluation is not, nor should it be construed as, an assessment of the financial condition of this institution. The rating assigned to this institution does not represent an analysis, conclusion or opinion of the federal financial supervisory agency concerning the safety and soundness of this financial institution.

Transcript of IDEO: A Study in Core Competence - Towson University - Search

PUBLIC DISCLOSURE

December 1, 2008

COMMUNITY REINVESTMENT ACT PERFORMANCE EVALUATION

Southern Bancorp Bank of Arkansas RSSD # 852544

601 Main Street

Arkadelphia, Arkansas 71923

Federal Reserve Bank of St. Louis P.O. Box 442 St. Louis, Missouri 63166-0442 NOTE: This document is an evaluation of this institution’s record of meeting

the credit needs of its entire community, including low- and moderate-income neighborhoods, consistent with safe and sound operation of the institution. This evaluation is not, nor should it be construed as, an assessment of the financial condition of this institution. The rating assigned to this institution does not represent an analysis, conclusion or opinion of the federal financial supervisory agency concerning the safety and soundness of this financial institution.

Table of Contents

TABLE OF CONTENTS Institution’s CRA Rating .................................................................................................................1 Scope of Examination ......................................................................................................................1 Description of Institution .................................................................................................................1 Conclusions with Respect to Performance Criteria .........................................................................3 Full Scope Review - Assessment Area Conclusions Non-Metropolitan Statistical Area: Clark and Hot Springs Counties ........................................8 Metropolitan Statistical Area: Garland County .......................................................................14 Appendix A: Listing of Census Tracts in CRA Assessment Area……………………………….20 Appendix B: Glossary……………………………………………………………………………21

Southern Bancorp Bank of Arkansas CRA Performance Evaluation Arkadelphia, Arkansas December 1, 2008

INSTITUTION’S CRA RATING: This institution is rated Satisfactory. Southern Bancorp Bank of Arkansas (SBB) meets the criteria for a satisfactory rating based upon an evaluation of the bank’s overall lending performance. This conclusion is based on the satisfactory distribution of loans to borrowers of different income levels, especially among low- and moderate-income (LMI) individuals, and to businesses of varying revenues. Also, a significant majority of the bank’s loans were made within its assessment area. The loan-to-deposit (LTD) ratio is considered reasonable, given the institution’s size, financial condition, performance of its competitors, and the credit needs of the assessment area. The geographic distribution of loans is adequate. Lastly, no Community Reinvestment Act (CRA) related complaints were filed against the bank for this review period. SCOPE OF EXAMINATION The bank’s CRA performance was evaluated using the small bank examination procedures. This review period covered the date of the bank’s previous CRA evaluation on September 20, 2004, to December 1, 2008. The bank’s lending performance in residential real estate was evaluated using information from Home Mortgage Disclosure Act (HMDA) data for the period from January 1, 2007, through May 15, 2008. The evaluation of consumer motor vehicle and small business loans was based on a statistical sample of loans for the period from January 1, 2007, through September 30, 2008.1 These three loan categories are considered the bank’s primary lines of business, based upon lending volume by number and dollar amount, and are indicative of the overall lending by the bank. The loan data evaluation involved an analysis of the bank’s distribution of loans by borrower income and business revenues, lending within the bank’s assessment area, lending volume relative to bank deposits, and the distribution of loans among different geographical categories. One community contact was performed in the Garland County assessment area to establish a performance context for the communities in which the bank operates and to better understand the credit needs of those communities. Information was solicited on the overall economic condition of the bank’s assessment area and how financial institutions meet any credit needs identified. Specific comments from the community contact are addressed in the applicable section relating to the assessment area. DESCRIPTION OF INSTITUTION2 SBB is owned by Southern Bancorp, a multi-bank holding company located in Arkadelphia, Arkansas, and designated as a Community Development Financial Institution by the Community Development Financial Institution Fund, a division of the U. S. Department of Treasury. Community Development Financial Institutions have a primary mission of promoting community development, principally serving and maintaining accountability to an eligible target market or markets, and providing development services. SBB currently operates six full-service

1 In the narrative and applicable tables that follow in this document, the reference to HMDA loans, consumer motor vehicle loans, and small business loans will use the loans originated in the time periods shown here. 2 Any percentage row or column “Total” figure displayed throughout this evaluation that does not equal exactly 100 percent is strictly due to rounding differences, which are considered immaterial to overall performance conclusions.

1

Southern Bancorp Bank of Arkansas CRA Performance Evaluation Arkadelphia, Arkansas December 1, 2008

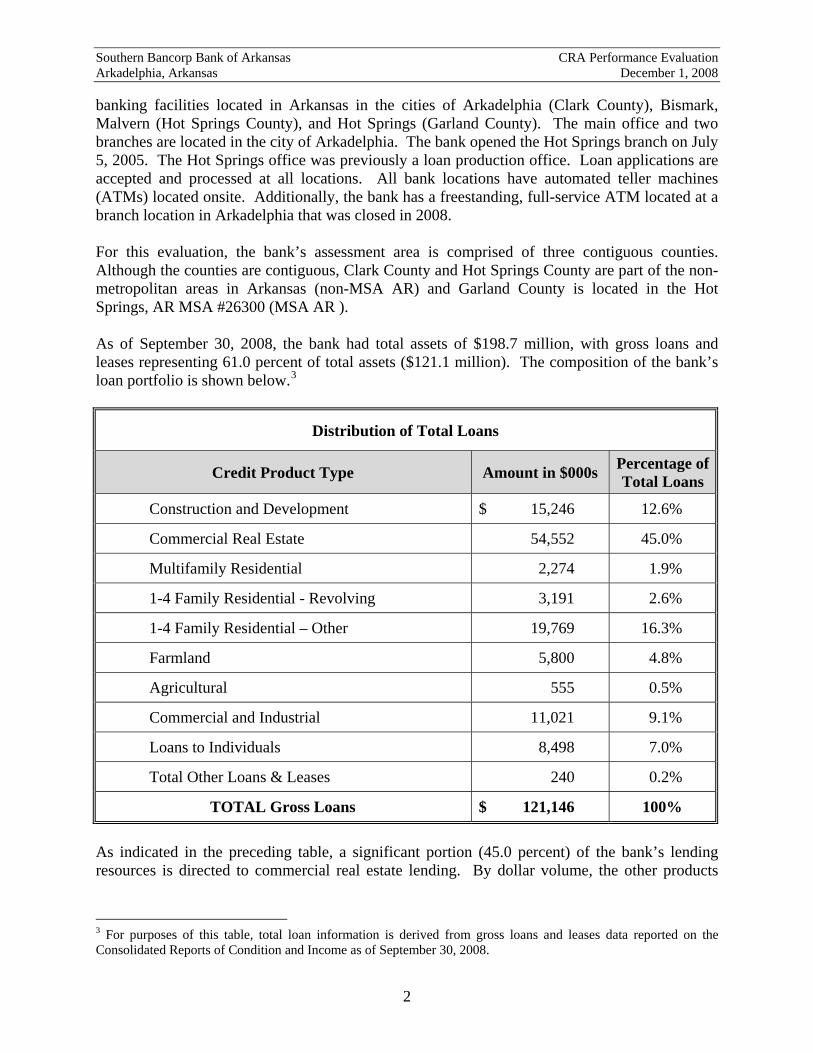

banking facilities located in Arkansas in the cities of Arkadelphia (Clark County), Bismark, Malvern (Hot Springs County), and Hot Springs (Garland County). The main office and two branches are located in the city of Arkadelphia. The bank opened the Hot Springs branch on July 5, 2005. The Hot Springs office was previously a loan production office. Loan applications are accepted and processed at all locations. All bank locations have automated teller machines (ATMs) located onsite. Additionally, the bank has a freestanding, full-service ATM located at a branch location in Arkadelphia that was closed in 2008. For this evaluation, the bank’s assessment area is comprised of three contiguous counties. Although the counties are contiguous, Clark County and Hot Springs County are part of the non-metropolitan areas in Arkansas (non-MSA AR) and Garland County is located in the Hot Springs, AR MSA #26300 (MSA AR ). As of September 30, 2008, the bank had total assets of $198.7 million, with gross loans and leases representing 61.0 percent of total assets ($121.1 million). The composition of the bank’s loan portfolio is shown below.3

Distribution of Total Loans

Credit Product Type Amount in $000s Percentage of Total Loans

Construction and Development $ 15,246 12.6%

Commercial Real Estate 54,552 45.0%

Multifamily Residential 2,274 1.9%

1-4 Family Residential - Revolving 3,191 2.6%

1-4 Family Residential – Other 19,769 16.3%

Farmland 5,800 4.8%

Agricultural 555 0.5%

Commercial and Industrial 11,021 9.1%

Loans to Individuals 8,498 7.0%

Total Other Loans & Leases 240 0.2%

TOTAL Gross Loans $ 121,146 100%

As indicated in the preceding table, a significant portion (45.0 percent) of the bank’s lending resources is directed to commercial real estate lending. By dollar volume, the other products

3 For purposes of this table, total loan information is derived from gross loans and leases data reported on the Consolidated Reports of Condition and Income as of September 30, 2008.

2

Southern Bancorp Bank of Arkansas CRA Performance Evaluation Arkadelphia, Arkansas December 1, 2008

with a high concentration of loans is 1-to-4 family residential loans (16.3 percent) and construction and development loans (12.6 percent). As part of this evaluation under the CRA, the bank’s performance was evaluated in relation to local competitors. Four financial institutions were identified as regional competitors with asset sizes ranging from $90.8 million to $1.0 billion as of September 30, 2008. There are no apparent legal or financial impediments that would prevent the bank from meeting assessment area credit needs. The bank received a satisfactory rating at its previous CRA evaluation conducted by the Federal Deposit Insurance Corporation (FDIC) on September 20, 2004. CONCLUSIONS WITH RESPECT TO PERFORMANCE TESTS SBB meets the criteria for a satisfactory rating based upon its lending performance as measured by the CRA small bank performance standards. This lending performance was based upon HMDA residential mortgages, consumer motor vehicle, and small business loans.4 These loan categories are considered the bank’s primary lines of business, based upon lending volume by number and dollar amounts. Therefore, loan activity represented by these credit products is deemed indicative of the overall lending performance of the bank. The CRA small bank performance standards evaluate the following five criteria as applicable: • The bank’s level of lending within the assessment area. • The bank’s average LTD ratio. • The bank’s distribution of loans by borrower income and business revenue. • The bank’s geographic distribution of loans. • A review of written complaints directed to the bank. The remaining sections of this evaluation are based upon analyses of the bank’s lending performance under these five performance criteria.

4 Refer to page 1 for the time periods used for the loans in this evaluation.

3

Southern Bancorp Bank of Arkansas CRA Performance Evaluation Arkadelphia, Arkansas December 1, 2008

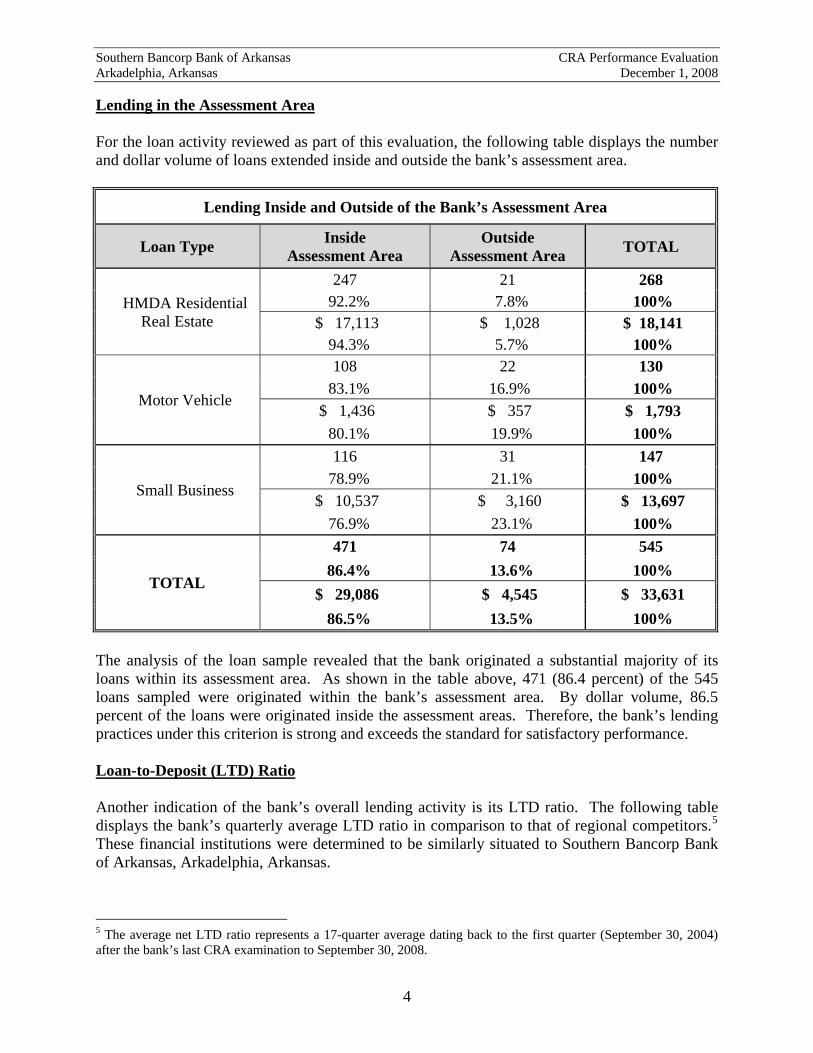

Lending in the Assessment Area For the loan activity reviewed as part of this evaluation, the following table displays the number and dollar volume of loans extended inside and outside the bank’s assessment area.

Lending Inside and Outside of the Bank’s Assessment Area

Loan Type Inside Assessment Area

Outside Assessment Area TOTAL

HMDA Residential Real Estate

247 21 268 92.2% 7.8% 100%

$ 17,113 $ 1,028 $ 18,141 94.3% 5.7% 100%

Motor Vehicle

108 22 130 83.1% 16.9% 100%

$ 1,436 $ 357 $ 1,793 80.1% 19.9% 100%

Small Business

116 31 147 78.9% 21.1% 100%

$ 10,537 $ 3,160 $ 13,697 76.9% 23.1% 100%

TOTAL

471 74 545 86.4% 13.6% 100%

$ 29,086 $ 4,545 $ 33,631 86.5% 13.5% 100%

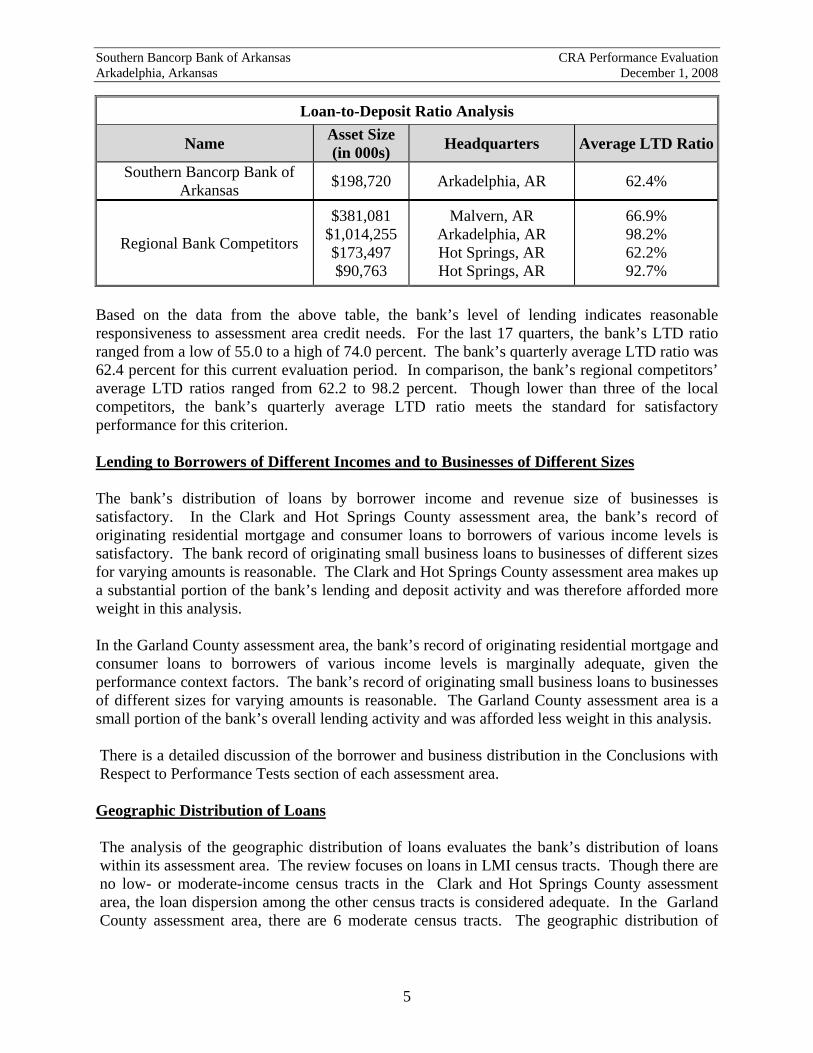

The analysis of the loan sample revealed that the bank originated a substantial majority of its loans within its assessment area. As shown in the table above, 471 (86.4 percent) of the 545 loans sampled were originated within the bank’s assessment area. By dollar volume, 86.5 percent of the loans were originated inside the assessment areas. Therefore, the bank’s lending practices under this criterion is strong and exceeds the standard for satisfactory performance. Loan-to-Deposit (LTD) Ratio Another indication of the bank’s overall lending activity is its LTD ratio. The following table displays the bank’s quarterly average LTD ratio in comparison to that of regional competitors.5 These financial institutions were determined to be similarly situated to Southern Bancorp Bank of Arkansas, Arkadelphia, Arkansas.

5 The average net LTD ratio represents a 17-quarter average dating back to the first quarter (September 30, 2004) after the bank’s last CRA examination to September 30, 2008.

4

Southern Bancorp Bank of Arkansas CRA Performance Evaluation Arkadelphia, Arkansas December 1, 2008

Loan-to-Deposit Ratio Analysis

Name Asset Size (in 000s) Headquarters Average LTD Ratio

Southern Bancorp Bank of Arkansas $198,720 Arkadelphia, AR 62.4%

Regional Bank Competitors

$381,081 $1,014,255 $173,497 $90,763

Malvern, AR Arkadelphia, AR Hot Springs, AR Hot Springs, AR

66.9% 98.2% 62.2% 92.7%

Based on the data from the above table, the bank’s level of lending indicates reasonable responsiveness to assessment area credit needs. For the last 17 quarters, the bank’s LTD ratio ranged from a low of 55.0 to a high of 74.0 percent. The bank’s quarterly average LTD ratio was 62.4 percent for this current evaluation period. In comparison, the bank’s regional competitors’ average LTD ratios ranged from 62.2 to 98.2 percent. Though lower than three of the local competitors, the bank’s quarterly average LTD ratio meets the standard for satisfactory performance for this criterion. Lending to Borrowers of Different Incomes and to Businesses of Different Sizes The bank’s distribution of loans by borrower income and revenue size of businesses is satisfactory. In the Clark and Hot Springs County assessment area, the bank’s record of originating residential mortgage and consumer loans to borrowers of various income levels is satisfactory. The bank record of originating small business loans to businesses of different sizes for varying amounts is reasonable. The Clark and Hot Springs County assessment area makes up a substantial portion of the bank’s lending and deposit activity and was therefore afforded more weight in this analysis. In the Garland County assessment area, the bank’s record of originating residential mortgage and consumer loans to borrowers of various income levels is marginally adequate, given the performance context factors. The bank’s record of originating small business loans to businesses of different sizes for varying amounts is reasonable. The Garland County assessment area is a small portion of the bank’s overall lending activity and was afforded less weight in this analysis. There is a detailed discussion of the borrower and business distribution in the Conclusions with Respect to Performance Tests section of each assessment area. Geographic Distribution of Loans The analysis of the geographic distribution of loans evaluates the bank’s distribution of loans within its assessment area. The review focuses on loans in LMI census tracts. Though there are no low- or moderate-income census tracts in the Clark and Hot Springs County assessment area, the loan dispersion among the other census tracts is considered adequate. In the Garland County assessment area, there are 6 moderate census tracts. The geographic distribution of

5

Southern Bancorp Bank of Arkansas CRA Performance Evaluation Arkadelphia, Arkansas December 1, 2008

loans in this assessment area is reasonable, based upon performance context information obtained from the community contacts interviewed during this examination. A detailed discussion of the geographic distribution in the non-metropolitan statistical area and the metropolitan statistical area sections that follow. Complaints No CRA-related complaints were received for this institution during the time frame used for this evaluation (September 20, 2004, through December 1, 2008). Additional Information During the Consumer Affairs examination conducted concurrently with this CRA evaluation, a fair lending analysis was performed to assess the bank’s compliance under Regulation B (Equal Credit Opportunity) and the Fair Housing Act. The analysis concluded that the bank is in compliance with the substantive provisions of the antidiscrimination laws and regulations for the products and services reviewed. DESCRIPTION OF COMMUNITY DEVELOPMENT INVESTMENTS AND SERVICES As part of the performance analysis of the bank during this examination, this Reserve Bank’s examiners were asked by senior management at the bank to consider the bank’s community development investment and services activities to enhance the CRA performance. Based upon the examiners’ review of the bank’s five core lending criteria, it was determined that the bank did not exceed the standard in any of the loan categories and therefore was not eligible to receive an enhanced rating. Consequently, the bank maintained a satisfactory rating for the evaluation period. Even though the rating could not be raised to an outstanding rating, it is noted that the bank’s community development investment and services activities were considered excellent in addressing the community development needs of its assessment areas considering its capacity and the need and availability of such opportunities. Community Development Investments The bank, holding company, and affiliates had numerous investments. These largely took the form of grants and donations to various community groups and organizations which met various community development purposes. The total amount of grants and donations was $1,332,065. The largest of the grants and donations included affordable housing, construction of a childcare center, and implementation of various aspects of the Clark County strategic plan. In addition, the bank’s investment portfolio contains $3,425,000 in school bond issues. Greater than 50 percent of the student population in each school district receives free or subsidized lunches.

6

Southern Bancorp Bank of Arkansas CRA Performance Evaluation Arkadelphia, Arkansas December 1, 2008

The bank’s total community development investments demonstrate an excellent responsiveness to community development needs of the assessment area based upon the opportunities for such investments. Community Development Services Officers and employees of the bank, holding company, and affiliates were involved in numerous community organizations within the Clark and Hot Springs County assessment area. To a lesser extent, staff was also involved in community organizations in the Garland County assessment area. A significant portion of these organizations had a primary purpose of community development. The bank often assumed a leadership role in these organizations and provided significant financial guidance. The bank provides ready access to financial services in all parts of its assessment area. The bank has six offices, with four located in middle-income census tracts and two located in the same upper-income census tract. The Clark and Hot Springs County assessment area does not contain any low- or moderate-income tracts; however, three of the four middle-income tracts in Clark are classified as distressed in 2008 due to the levels of poverty of the residents. The bank has only one office currently in the Garland County assessment area, which is located in a middle-income tract and somewhat removed from the two moderate-income tracts in that county. All branches have ATM availability. The bank has closed one branch since the previous evaluation that was located in an upper-income tract in Clark. Banking services do not vary in a manner that would inconvenience certain portions of the bank’s assessment areas. The level of community development services demonstrates the bank is a leader in providing community development services in its assessment areas.

7

Southern Bancorp Bank of Arkansas CRA Performance Evaluation Arkadelphia, Arkansas December 1, 2008

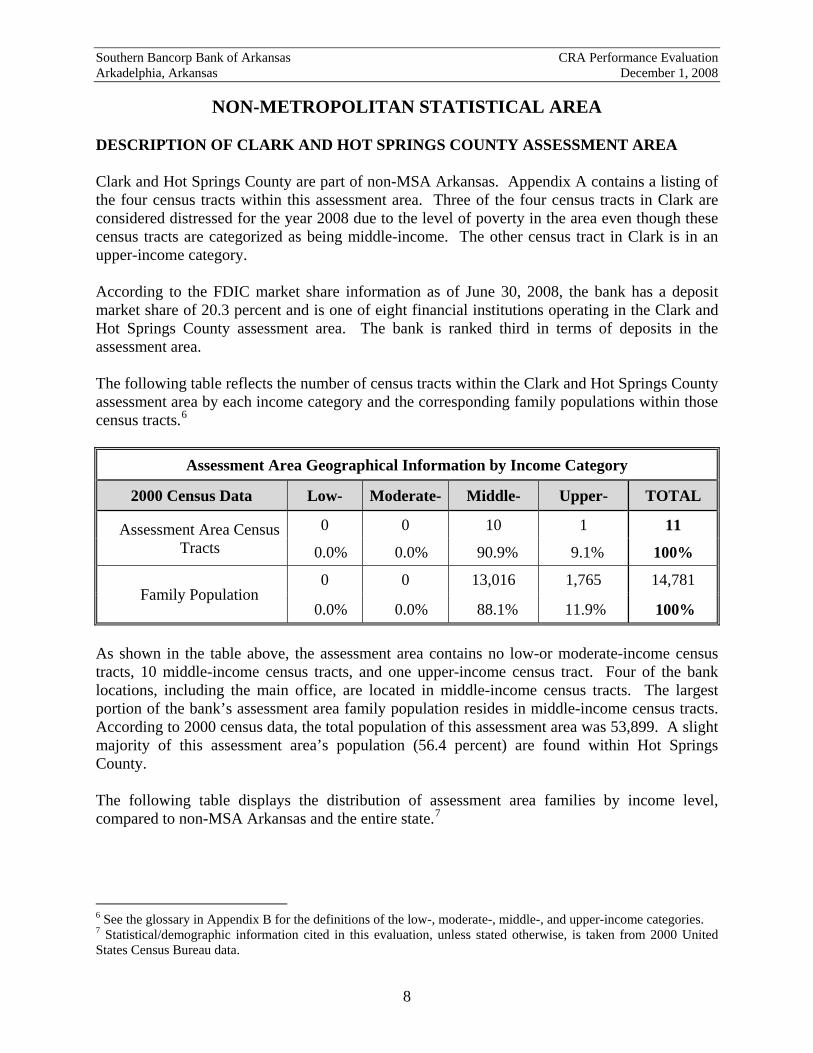

NON-METROPOLITAN STATISTICAL AREA DESCRIPTION OF CLARK AND HOT SPRINGS COUNTY ASSESSMENT AREA Clark and Hot Springs County are part of non-MSA Arkansas. Appendix A contains a listing of the four census tracts within this assessment area. Three of the four census tracts in Clark are considered distressed for the year 2008 due to the level of poverty in the area even though these census tracts are categorized as being middle-income. The other census tract in Clark is in an upper-income category. According to the FDIC market share information as of June 30, 2008, the bank has a deposit market share of 20.3 percent and is one of eight financial institutions operating in the Clark and Hot Springs County assessment area. The bank is ranked third in terms of deposits in the assessment area. The following table reflects the number of census tracts within the Clark and Hot Springs County assessment area by each income category and the corresponding family populations within those census tracts.6

Assessment Area Geographical Information by Income Category

2000 Census Data Low- Moderate- Middle- Upper- TOTAL

Assessment Area Census Tracts

0 0 10 1 11

0.0% 0.0% 90.9% 9.1% 100%

Family Population 0 0 13,016 1,765 14,781

0.0% 0.0% 88.1% 11.9% 100% As shown in the table above, the assessment area contains no low-or moderate-income census tracts, 10 middle-income census tracts, and one upper-income census tract. Four of the bank locations, including the main office, are located in middle-income census tracts. The largest portion of the bank’s assessment area family population resides in middle-income census tracts. According to 2000 census data, the total population of this assessment area was 53,899. A slight majority of this assessment area’s population (56.4 percent) are found within Hot Springs County. The following table displays the distribution of assessment area families by income level, compared to non-MSA Arkansas and the entire state.7

6 See the glossary in Appendix B for the definitions of the low-, moderate-, middle-, and upper-income categories. 7 Statistical/demographic information cited in this evaluation, unless stated otherwise, is taken from 2000 United States Census Bureau data.

8

Southern Bancorp Bank of Arkansas CRA Performance Evaluation Arkadelphia, Arkansas December 1, 2008

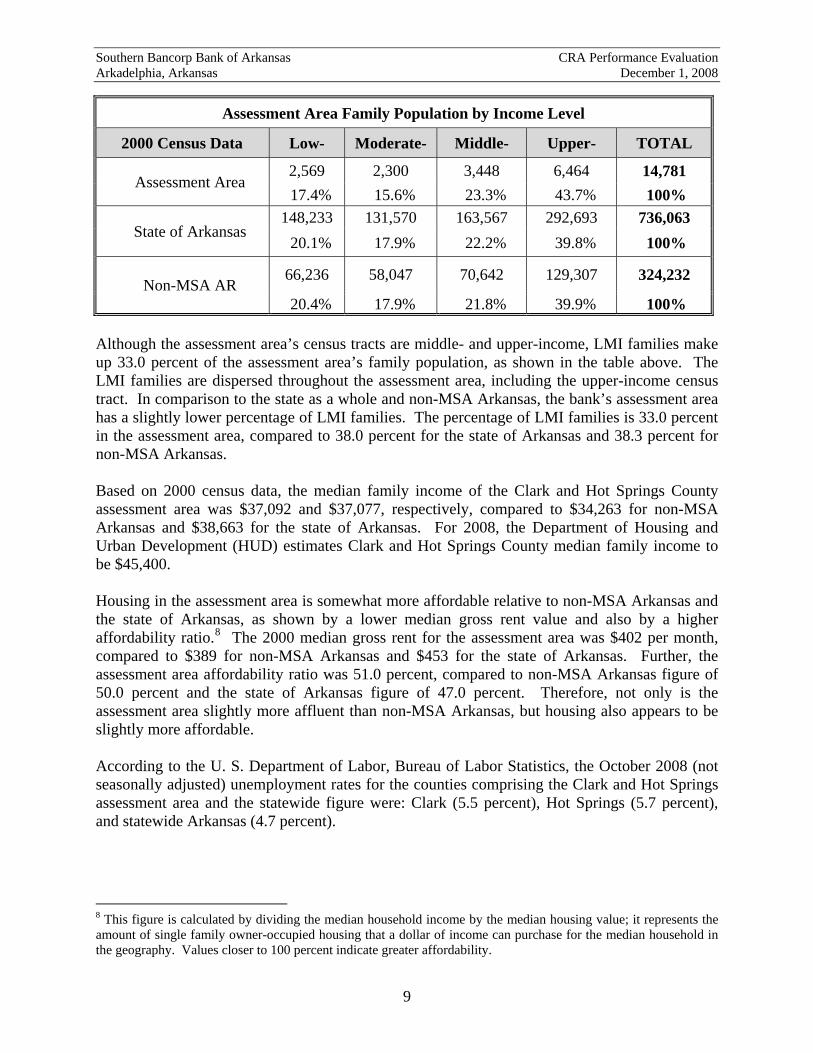

Assessment Area Family Population by Income Level

2000 Census Data Low- Moderate- Middle- Upper- TOTAL

Assessment Area 2,569 2,300 3,448 6,464 14,781

17.4% 15.6% 23.3% 43.7% 100%

State of Arkansas 148,233 131,570 163,567 292,693 736,063 20.1% 17.9% 22.2% 39.8% 100%

Non-MSA AR 66,236 58,047 70,642 129,307 324,232

20.4% 17.9% 21.8% 39.9% 100% Although the assessment area’s census tracts are middle- and upper-income, LMI families make up 33.0 percent of the assessment area’s family population, as shown in the table above. The LMI families are dispersed throughout the assessment area, including the upper-income census tract. In comparison to the state as a whole and non-MSA Arkansas, the bank’s assessment area has a slightly lower percentage of LMI families. The percentage of LMI families is 33.0 percent in the assessment area, compared to 38.0 percent for the state of Arkansas and 38.3 percent for non-MSA Arkansas. Based on 2000 census data, the median family income of the Clark and Hot Springs County assessment area was $37,092 and $37,077, respectively, compared to $34,263 for non-MSA Arkansas and $38,663 for the state of Arkansas. For 2008, the Department of Housing and Urban Development (HUD) estimates Clark and Hot Springs County median family income to be $45,400. Housing in the assessment area is somewhat more affordable relative to non-MSA Arkansas and the state of Arkansas, as shown by a lower median gross rent value and also by a higher affordability ratio.8 The 2000 median gross rent for the assessment area was $402 per month, compared to $389 for non-MSA Arkansas and $453 for the state of Arkansas. Further, the assessment area affordability ratio was 51.0 percent, compared to non-MSA Arkansas figure of 50.0 percent and the state of Arkansas figure of 47.0 percent. Therefore, not only is the assessment area slightly more affluent than non-MSA Arkansas, but housing also appears to be slightly more affordable. According to the U. S. Department of Labor, Bureau of Labor Statistics, the October 2008 (not seasonally adjusted) unemployment rates for the counties comprising the Clark and Hot Springs assessment area and the statewide figure were: Clark (5.5 percent), Hot Springs (5.7 percent), and statewide Arkansas (4.7 percent).

8 This figure is calculated by dividing the median household income by the median housing value; it represents the amount of single family owner-occupied housing that a dollar of income can purchase for the median household in the geography. Values closer to 100 percent indicate greater affordability.

9

Southern Bancorp Bank of Arkansas CRA Performance Evaluation Arkadelphia, Arkansas December 1, 2008

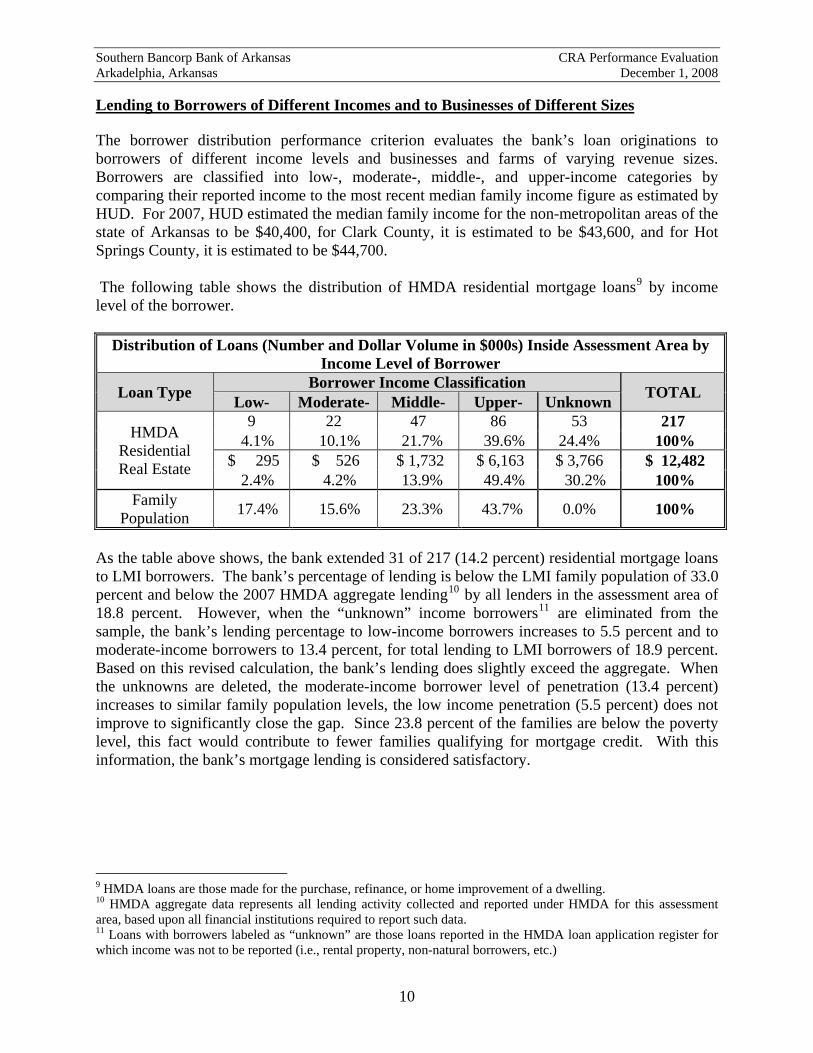

Lending to Borrowers of Different Incomes and to Businesses of Different Sizes The borrower distribution performance criterion evaluates the bank’s loan originations to borrowers of different income levels and businesses and farms of varying revenue sizes. Borrowers are classified into low-, moderate-, middle-, and upper-income categories by comparing their reported income to the most recent median family income figure as estimated by HUD. For 2007, HUD estimated the median family income for the non-metropolitan areas of the state of Arkansas to be $40,400, for Clark County, it is estimated to be $43,600, and for Hot Springs County, it is estimated to be $44,700. The following table shows the distribution of HMDA residential mortgage loans9 by income level of the borrower.

Distribution of Loans (Number and Dollar Volume in $000s) Inside Assessment Area by Income Level of Borrower

Loan Type Borrower Income Classification TOTAL Low- Moderate- Middle- Upper- Unknown

HMDA Residential Real Estate

9 22 47 86 53 217 4.1% 10.1% 21.7% 39.6% 24.4% 100%

$ 295 $ 526 $ 1,732 $ 6,163 $ 3,766 $ 12,482 2.4% 4.2% 13.9% 49.4% 30.2% 100%

Family Population 17.4% 15.6% 23.3% 43.7% 0.0% 100%

As the table above shows, the bank extended 31 of 217 (14.2 percent) residential mortgage loans to LMI borrowers. The bank’s percentage of lending is below the LMI family population of 33.0 percent and below the 2007 HMDA aggregate lending10 by all lenders in the assessment area of 18.8 percent. However, when the “unknown” income borrowers11 are eliminated from the sample, the bank’s lending percentage to low-income borrowers increases to 5.5 percent and to moderate-income borrowers to 13.4 percent, for total lending to LMI borrowers of 18.9 percent. Based on this revised calculation, the bank’s lending does slightly exceed the aggregate. When the unknowns are deleted, the moderate-income borrower level of penetration (13.4 percent) increases to similar family population levels, the low income penetration (5.5 percent) does not improve to significantly close the gap. Since 23.8 percent of the families are below the poverty level, this fact would contribute to fewer families qualifying for mortgage credit. With this information, the bank’s mortgage lending is considered satisfactory.

9 HMDA loans are those made for the purchase, refinance, or home improvement of a dwelling. 10 HMDA aggregate data represents all lending activity collected and reported under HMDA for this assessment area, based upon all financial institutions required to report such data. 11 Loans with borrowers labeled as “unknown” are those loans reported in the HMDA loan application register for which income was not to be reported (i.e., rental property, non-natural borrowers, etc.)

10

Southern Bancorp Bank of Arkansas CRA Performance Evaluation Arkadelphia, Arkansas December 1, 2008

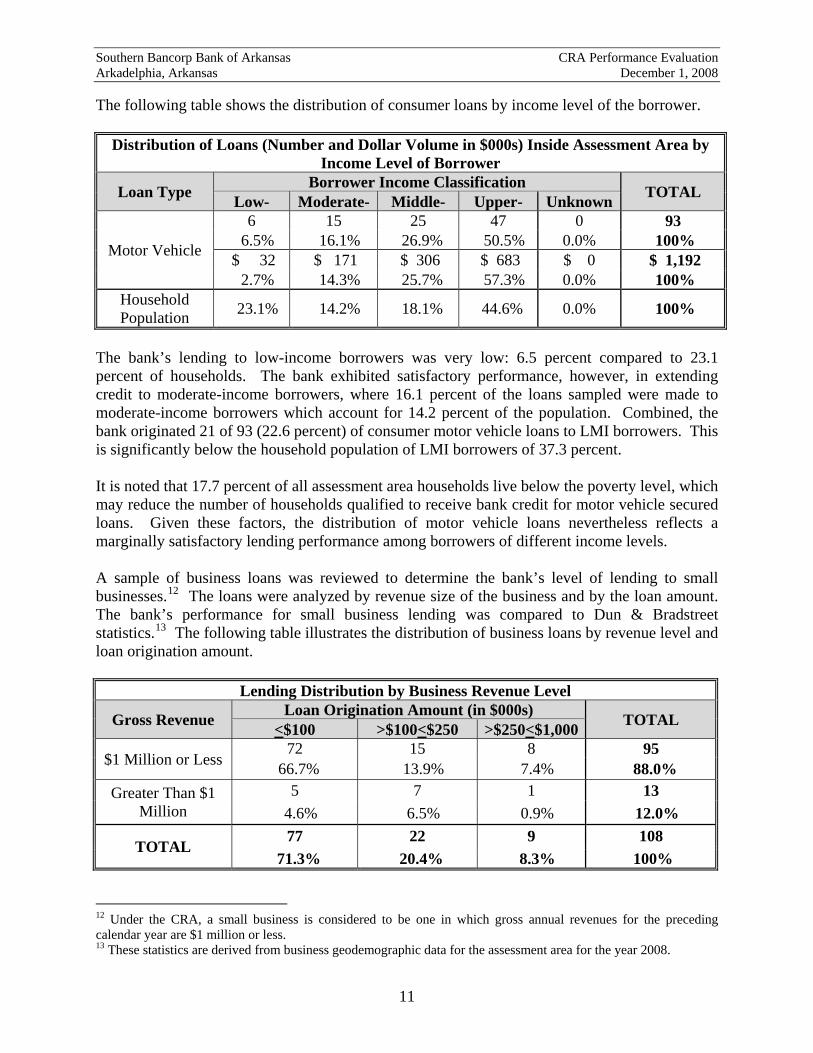

The following table shows the distribution of consumer loans by income level of the borrower.

Distribution of Loans (Number and Dollar Volume in $000s) Inside Assessment Area by Income Level of Borrower

Loan Type Borrower Income Classification TOTAL Low- Moderate- Middle- Upper- Unknown

Motor Vehicle

6 15 25 47 0 93 6.5% 16.1% 26.9% 50.5% 0.0% 100% $ 32 $ 171 $ 306 $ 683 $ 0 $ 1,192 2.7% 14.3% 25.7% 57.3% 0.0% 100%

Household Population 23.1% 14.2% 18.1% 44.6% 0.0% 100%

The bank’s lending to low-income borrowers was very low: 6.5 percent compared to 23.1 percent of households. The bank exhibited satisfactory performance, however, in extending credit to moderate-income borrowers, where 16.1 percent of the loans sampled were made to moderate-income borrowers which account for 14.2 percent of the population. Combined, the bank originated 21 of 93 (22.6 percent) of consumer motor vehicle loans to LMI borrowers. This is significantly below the household population of LMI borrowers of 37.3 percent. It is noted that 17.7 percent of all assessment area households live below the poverty level, which may reduce the number of households qualified to receive bank credit for motor vehicle secured loans. Given these factors, the distribution of motor vehicle loans nevertheless reflects a marginally satisfactory lending performance among borrowers of different income levels. A sample of business loans was reviewed to determine the bank’s level of lending to small businesses.12 The loans were analyzed by revenue size of the business and by the loan amount. The bank’s performance for small business lending was compared to Dun & Bradstreet statistics.13 The following table illustrates the distribution of business loans by revenue level and loan origination amount.

Lending Distribution by Business Revenue Level

Gross Revenue Loan Origination Amount (in $000s) TOTAL <$100 >$100<$250 >$250<$1,000

$1 Million or Less 72 15 8 95

66.7% 13.9% 7.4% 88.0% Greater Than $1

Million 5 7 1 13

4.6% 6.5% 0.9% 12.0%

TOTAL 77 22 9 108

71.3% 20.4% 8.3% 100% 12 Under the CRA, a small business is considered to be one in which gross annual revenues for the preceding calendar year are $1 million or less. 13 These statistics are derived from business geodemographic data for the assessment area for the year 2008.

11

Southern Bancorp Bank of Arkansas CRA Performance Evaluation Arkadelphia, Arkansas December 1, 2008

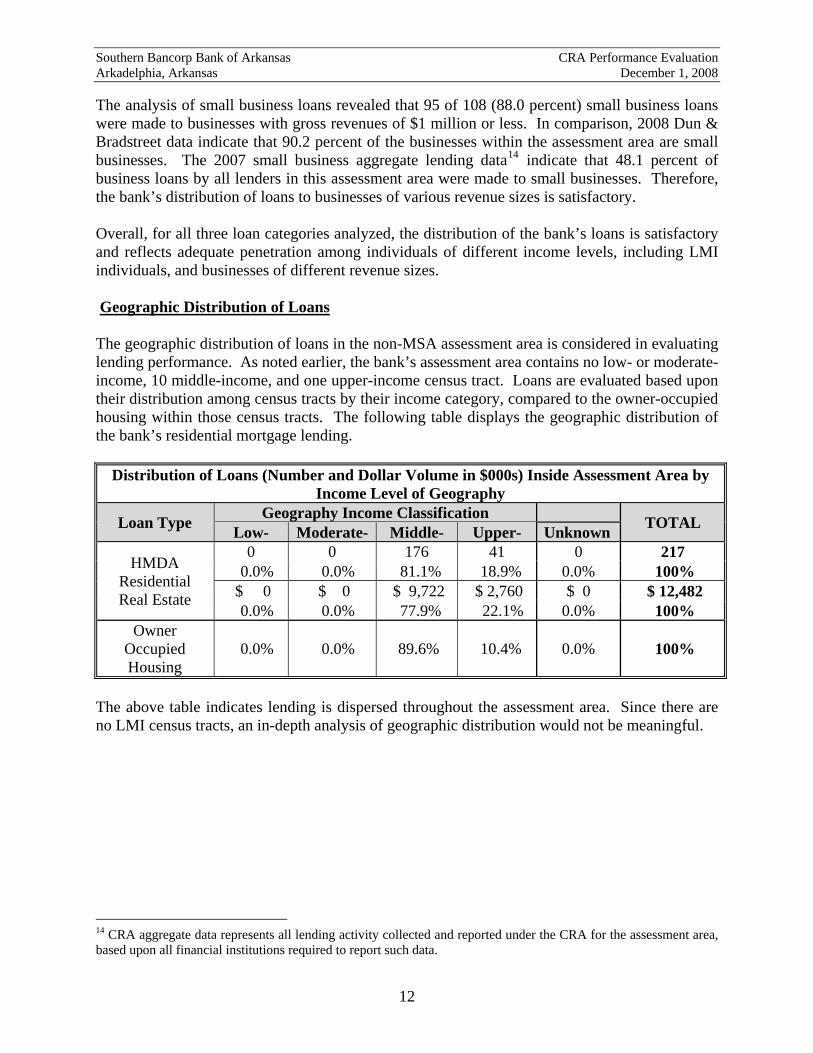

The analysis of small business loans revealed that 95 of 108 (88.0 percent) small business loans were made to businesses with gross revenues of $1 million or less. In comparison, 2008 Dun & Bradstreet data indicate that 90.2 percent of the businesses within the assessment area are small businesses. The 2007 small business aggregate lending data14 indicate that 48.1 percent of business loans by all lenders in this assessment area were made to small businesses. Therefore, the bank’s distribution of loans to businesses of various revenue sizes is satisfactory. Overall, for all three loan categories analyzed, the distribution of the bank’s loans is satisfactory and reflects adequate penetration among individuals of different income levels, including LMI individuals, and businesses of different revenue sizes. Geographic Distribution of Loans The geographic distribution of loans in the non-MSA assessment area is considered in evaluating lending performance. As noted earlier, the bank’s assessment area contains no low- or moderate-income, 10 middle-income, and one upper-income census tract. Loans are evaluated based upon their distribution among census tracts by their income category, compared to the owner-occupied housing within those census tracts. The following table displays the geographic distribution of the bank’s residential mortgage lending.

Distribution of Loans (Number and Dollar Volume in $000s) Inside Assessment Area by Income Level of Geography

Loan Type Geography Income Classification TOTAL Low- Moderate- Middle- Upper- Unknown

HMDA Residential Real Estate

0 0 176 41 0 217 0.0% 0.0% 81.1% 18.9% 0.0% 100% $ 0 $ 0 $ 9,722 $ 2,760 $ 0 $ 12,482 0.0% 0.0% 77.9% 22.1% 0.0% 100%

Owner Occupied Housing

0.0% 0.0% 89.6% 10.4% 0.0% 100%

The above table indicates lending is dispersed throughout the assessment area. Since there are no LMI census tracts, an in-depth analysis of geographic distribution would not be meaningful.

14 CRA aggregate data represents all lending activity collected and reported under the CRA for the assessment area, based upon all financial institutions required to report such data.

12

Southern Bancorp Bank of Arkansas CRA Performance Evaluation Arkadelphia, Arkansas December 1, 2008

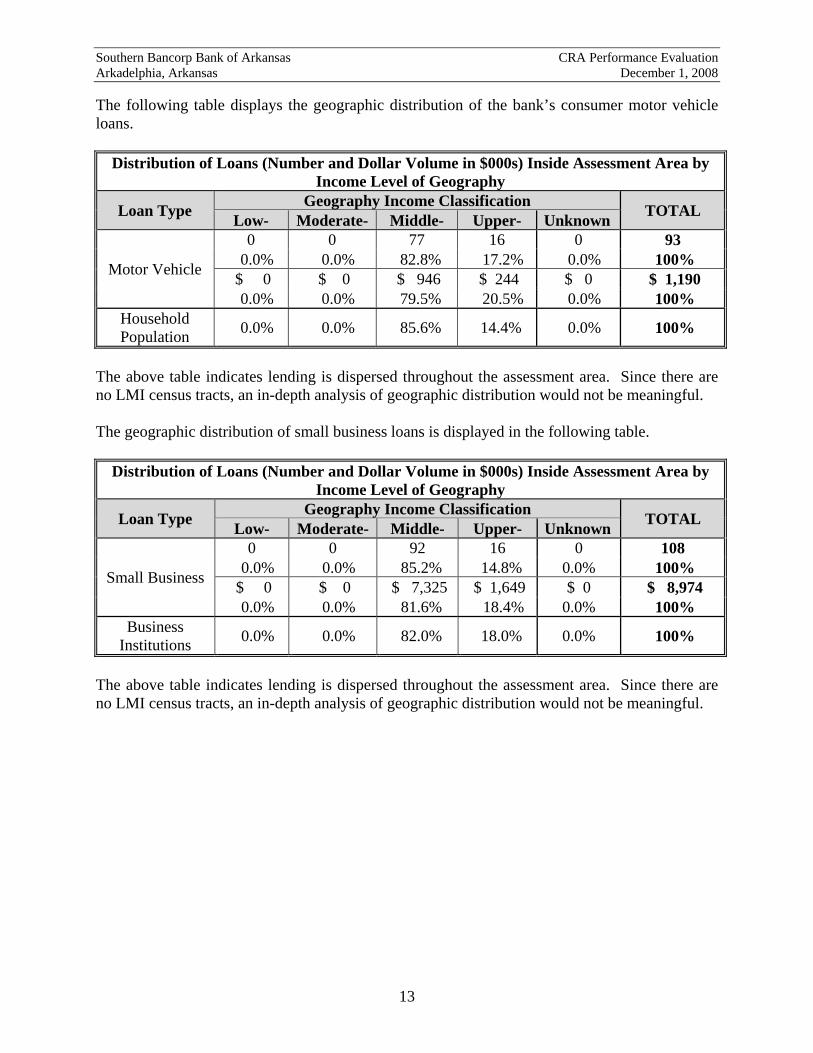

The following table displays the geographic distribution of the bank’s consumer motor vehicle loans.

Distribution of Loans (Number and Dollar Volume in $000s) Inside Assessment Area by Income Level of Geography

Loan Type Geography Income Classification TOTAL Low- Moderate- Middle- Upper- Unknown

Motor Vehicle

0 0 77 16 0 93 0.0% 0.0% 82.8% 17.2% 0.0% 100% $ 0 $ 0 $ 946 $ 244 $ 0 $ 1,190 0.0% 0.0% 79.5% 20.5% 0.0% 100%

Household Population 0.0% 0.0% 85.6% 14.4% 0.0% 100%

The above table indicates lending is dispersed throughout the assessment area. Since there are no LMI census tracts, an in-depth analysis of geographic distribution would not be meaningful. The geographic distribution of small business loans is displayed in the following table.

Distribution of Loans (Number and Dollar Volume in $000s) Inside Assessment Area by Income Level of Geography

Loan Type Geography Income Classification TOTAL Low- Moderate- Middle- Upper- Unknown

Small Business

0 0 92 16 0 108 0.0% 0.0% 85.2% 14.8% 0.0% 100% $ 0 $ 0 $ 7,325 $ 1,649 $ 0 $ 8,974 0.0% 0.0% 81.6% 18.4% 0.0% 100%

Business Institutions 0.0% 0.0% 82.0% 18.0% 0.0% 100%

The above table indicates lending is dispersed throughout the assessment area. Since there are no LMI census tracts, an in-depth analysis of geographic distribution would not be meaningful.

13

Southern Bancorp Bank of Arkansas CRA Performance Evaluation Arkadelphia, Arkansas December 1, 2008

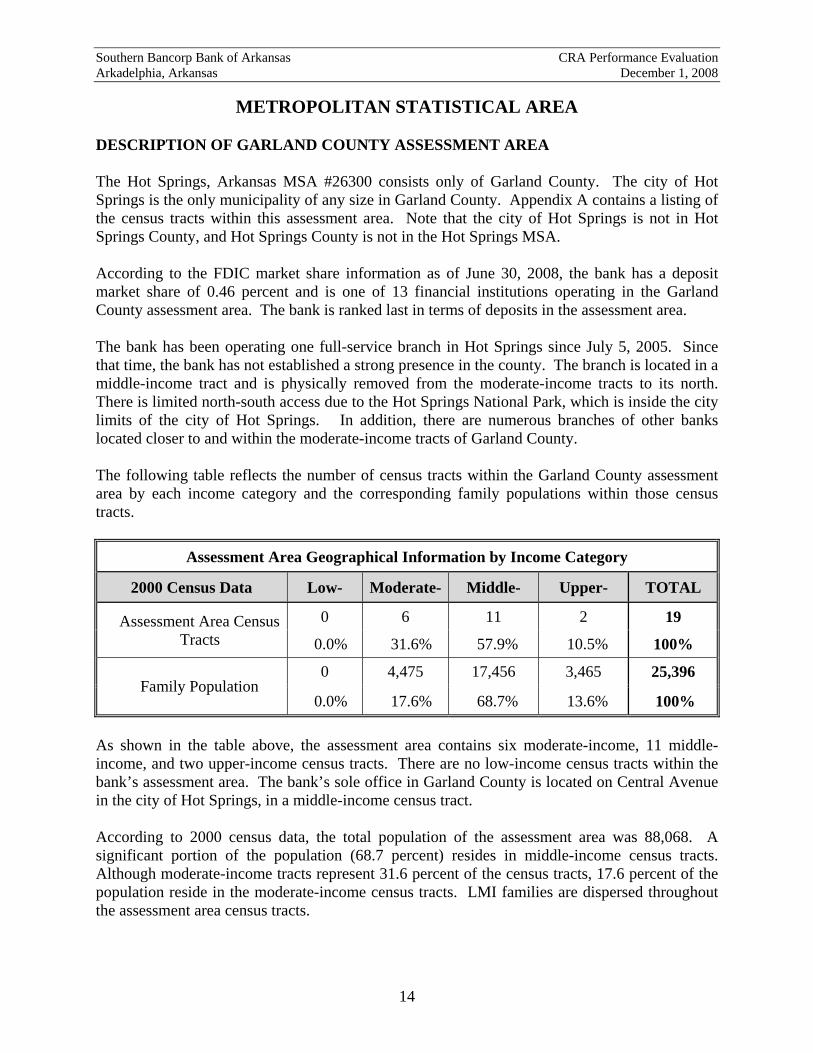

METROPOLITAN STATISTICAL AREA DESCRIPTION OF GARLAND COUNTY ASSESSMENT AREA The Hot Springs, Arkansas MSA #26300 consists only of Garland County. The city of Hot Springs is the only municipality of any size in Garland County. Appendix A contains a listing of the census tracts within this assessment area. Note that the city of Hot Springs is not in Hot Springs County, and Hot Springs County is not in the Hot Springs MSA. According to the FDIC market share information as of June 30, 2008, the bank has a deposit market share of 0.46 percent and is one of 13 financial institutions operating in the Garland County assessment area. The bank is ranked last in terms of deposits in the assessment area. The bank has been operating one full-service branch in Hot Springs since July 5, 2005. Since that time, the bank has not established a strong presence in the county. The branch is located in a middle-income tract and is physically removed from the moderate-income tracts to its north. There is limited north-south access due to the Hot Springs National Park, which is inside the city limits of the city of Hot Springs. In addition, there are numerous branches of other banks located closer to and within the moderate-income tracts of Garland County. The following table reflects the number of census tracts within the Garland County assessment area by each income category and the corresponding family populations within those census tracts.

Assessment Area Geographical Information by Income Category

2000 Census Data Low- Moderate- Middle- Upper- TOTAL

Assessment Area Census Tracts

0 6 11 2 19

0.0% 31.6% 57.9% 10.5% 100%

Family Population 0 4,475 17,456 3,465 25,396

0.0% 17.6% 68.7% 13.6% 100% As shown in the table above, the assessment area contains six moderate-income, 11 middle-income, and two upper-income census tracts. There are no low-income census tracts within the bank’s assessment area. The bank’s sole office in Garland County is located on Central Avenue in the city of Hot Springs, in a middle-income census tract. According to 2000 census data, the total population of the assessment area was 88,068. A significant portion of the population (68.7 percent) resides in middle-income census tracts. Although moderate-income tracts represent 31.6 percent of the census tracts, 17.6 percent of the population reside in the moderate-income census tracts. LMI families are dispersed throughout the assessment area census tracts.

14

Southern Bancorp Bank of Arkansas CRA Performance Evaluation Arkadelphia, Arkansas December 1, 2008

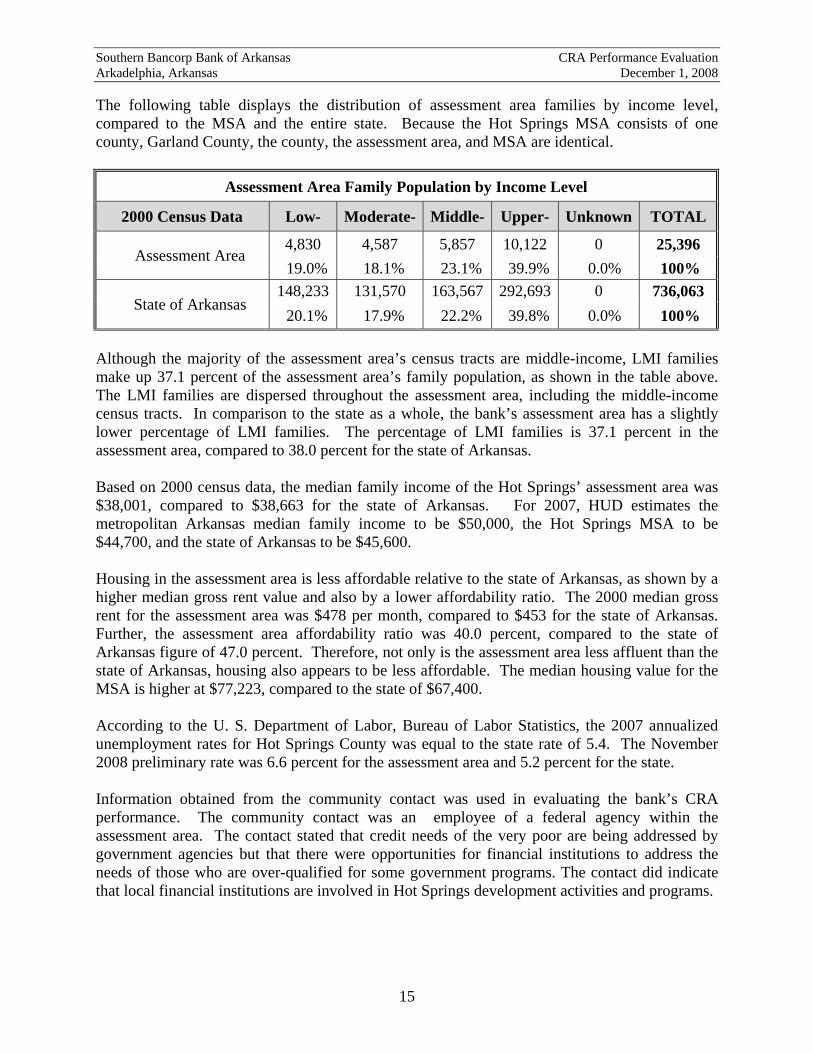

The following table displays the distribution of assessment area families by income level, compared to the MSA and the entire state. Because the Hot Springs MSA consists of one county, Garland County, the county, the assessment area, and MSA are identical.

Assessment Area Family Population by Income Level

2000 Census Data Low- Moderate- Middle- Upper- Unknown TOTAL

Assessment Area 4,830 4,587 5,857 10,122 0 25,396

19.0% 18.1% 23.1% 39.9% 0.0% 100%

State of Arkansas 148,233 131,570 163,567 292,693 0 736,063 20.1% 17.9% 22.2% 39.8% 0.0% 100%

Although the majority of the assessment area’s census tracts are middle-income, LMI families make up 37.1 percent of the assessment area’s family population, as shown in the table above. The LMI families are dispersed throughout the assessment area, including the middle-income census tracts. In comparison to the state as a whole, the bank’s assessment area has a slightly lower percentage of LMI families. The percentage of LMI families is 37.1 percent in the assessment area, compared to 38.0 percent for the state of Arkansas. Based on 2000 census data, the median family income of the Hot Springs’ assessment area was $38,001, compared to $38,663 for the state of Arkansas. For 2007, HUD estimates the metropolitan Arkansas median family income to be $50,000, the Hot Springs MSA to be $44,700, and the state of Arkansas to be $45,600. Housing in the assessment area is less affordable relative to the state of Arkansas, as shown by a higher median gross rent value and also by a lower affordability ratio. The 2000 median gross rent for the assessment area was $478 per month, compared to $453 for the state of Arkansas. Further, the assessment area affordability ratio was 40.0 percent, compared to the state of Arkansas figure of 47.0 percent. Therefore, not only is the assessment area less affluent than the state of Arkansas, housing also appears to be less affordable. The median housing value for the MSA is higher at $77,223, compared to the state of $67,400. According to the U. S. Department of Labor, Bureau of Labor Statistics, the 2007 annualized unemployment rates for Hot Springs County was equal to the state rate of 5.4. The November 2008 preliminary rate was 6.6 percent for the assessment area and 5.2 percent for the state. Information obtained from the community contact was used in evaluating the bank’s CRA performance. The community contact was an employee of a federal agency within the assessment area. The contact stated that credit needs of the very poor are being addressed by government agencies but that there were opportunities for financial institutions to address the needs of those who are over-qualified for some government programs. The contact did indicate that local financial institutions are involved in Hot Springs development activities and programs.

15

Southern Bancorp Bank of Arkansas CRA Performance Evaluation Arkadelphia, Arkansas December 1, 2008

Lending to Borrowers of Different Incomes and to Businesses of Different Sizes The borrower distribution performance criterion evaluates the bank’s loan originations to borrowers of different income levels and businesses and farms of varying revenue sizes. Borrowers are classified into low-, moderate-, middle-, and upper-income categories by comparing their reported income to the most recent median family income figure as estimated by HUD. For 2007, HUD estimated the median family income for the metropolitan areas of the state of Arkansas to be $50,000. The following table shows the distribution of residential mortgage loans (HMDA reportable loans) by income level of the borrower.

Distribution of Loans (Number and Dollar Volume in $000s) Inside Assessment Area by Income Level of Borrower

Loan Type Borrower Income Classification TOTAL Low- Moderate- Middle- Upper- Unknown

HMDA Residential Real Estate

0 2 3 29 2 36 0.0% 5.6% 8.3% 80.6% 5.6% 100% $ 0 $ 139 $ 186 $ 3,779 $ 527 $ 4,631 0.0% 3.0% 4.0% 81.6% 11.4% 100%

Family Population 19.0% 18.1% 23.1% 39.9% 0.0% 100%

As shown in the table above, the bank originated very few residential loans to LMI borrowers in the Hot Springs assessment area. The bank extended two loans, which represents 5.6 percent of its lending, to LMI borrowers. This is substantially lower than the percentage of LMI families (37.1 percent). The 2007 aggregate lending reflects that 17.1 percent of residential real estate lending by all lenders was to LMI families. The bank’s lending is below expectations. The bank’s limited presence, with only one office, and the short time operating within the Hot Springs market, has partially contributed to the limited residential mortgage lending activity. The community contact indicated that there was opportunity for banks to extend mortgage credit to those applicants that did not qualify for federal assistance. Also the Hot Springs community is working on a city-wide development plan, which will allow for participation by financial institutions. Based upon the above information, there is opportunity for the bank to improve its level of lending.

16

Southern Bancorp Bank of Arkansas CRA Performance Evaluation Arkadelphia, Arkansas December 1, 2008

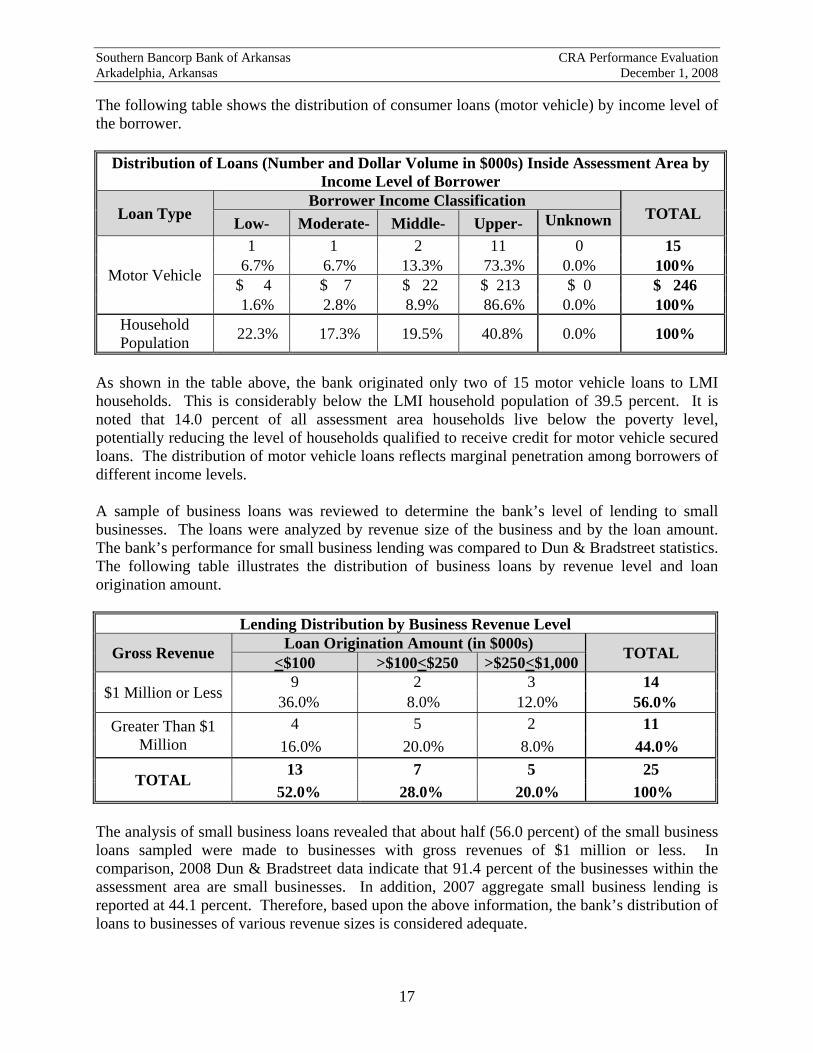

The following table shows the distribution of consumer loans (motor vehicle) by income level of the borrower.

Distribution of Loans (Number and Dollar Volume in $000s) Inside Assessment Area by Income Level of Borrower

Loan Type Borrower Income Classification

TOTAL Low- Moderate- Middle- Upper- Unknown

Motor Vehicle

1 1 2 11 0 15 6.7% 6.7% 13.3% 73.3% 0.0% 100% $ 4 $ 7 $ 22 $ 213 $ 0 $ 246 1.6% 2.8% 8.9% 86.6% 0.0% 100%

Household Population 22.3% 17.3% 19.5% 40.8% 0.0% 100%

As shown in the table above, the bank originated only two of 15 motor vehicle loans to LMI households. This is considerably below the LMI household population of 39.5 percent. It is noted that 14.0 percent of all assessment area households live below the poverty level, potentially reducing the level of households qualified to receive credit for motor vehicle secured loans. The distribution of motor vehicle loans reflects marginal penetration among borrowers of different income levels. A sample of business loans was reviewed to determine the bank’s level of lending to small businesses. The loans were analyzed by revenue size of the business and by the loan amount. The bank’s performance for small business lending was compared to Dun & Bradstreet statistics. The following table illustrates the distribution of business loans by revenue level and loan origination amount.

Lending Distribution by Business Revenue Level

Gross Revenue Loan Origination Amount (in $000s) TOTAL <$100 >$100<$250 >$250<$1,000

$1 Million or Less 9 2 3 14

36.0% 8.0% 12.0% 56.0% Greater Than $1

Million 4 5 2 11

16.0% 20.0% 8.0% 44.0%

TOTAL 13 7 5 25

52.0% 28.0% 20.0% 100% The analysis of small business loans revealed that about half (56.0 percent) of the small business loans sampled were made to businesses with gross revenues of $1 million or less. In comparison, 2008 Dun & Bradstreet data indicate that 91.4 percent of the businesses within the assessment area are small businesses. In addition, 2007 aggregate small business lending is reported at 44.1 percent. Therefore, based upon the above information, the bank’s distribution of loans to businesses of various revenue sizes is considered adequate.

17

Southern Bancorp Bank of Arkansas CRA Performance Evaluation Arkadelphia, Arkansas December 1, 2008

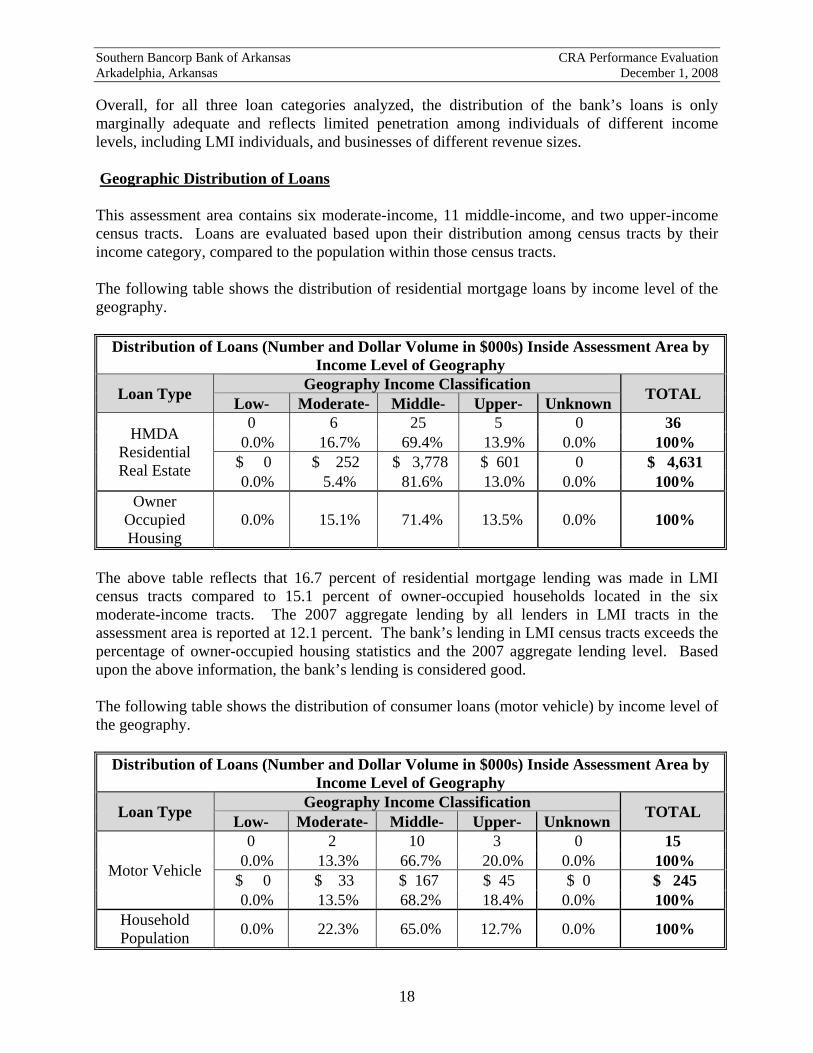

Overall, for all three loan categories analyzed, the distribution of the bank’s loans is only marginally adequate and reflects limited penetration among individuals of different income levels, including LMI individuals, and businesses of different revenue sizes. Geographic Distribution of Loans This assessment area contains six moderate-income, 11 middle-income, and two upper-income census tracts. Loans are evaluated based upon their distribution among census tracts by their income category, compared to the population within those census tracts. The following table shows the distribution of residential mortgage loans by income level of the geography.

Distribution of Loans (Number and Dollar Volume in $000s) Inside Assessment Area by Income Level of Geography

Loan Type Geography Income Classification TOTAL Low- Moderate- Middle- Upper- Unknown

HMDA Residential Real Estate

0 6 25 5 0 36 0.0% 16.7% 69.4% 13.9% 0.0% 100% $ 0 $ 252 $ 3,778 $ 601 0 $ 4,631 0.0% 5.4% 81.6% 13.0% 0.0% 100%

Owner Occupied Housing

0.0% 15.1% 71.4% 13.5% 0.0% 100%

The above table reflects that 16.7 percent of residential mortgage lending was made in LMI census tracts compared to 15.1 percent of owner-occupied households located in the six moderate-income tracts. The 2007 aggregate lending by all lenders in LMI tracts in the assessment area is reported at 12.1 percent. The bank’s lending in LMI census tracts exceeds the percentage of owner-occupied housing statistics and the 2007 aggregate lending level. Based upon the above information, the bank’s lending is considered good. The following table shows the distribution of consumer loans (motor vehicle) by income level of the geography.

Distribution of Loans (Number and Dollar Volume in $000s) Inside Assessment Area by Income Level of Geography

Loan Type Geography Income Classification TOTAL Low- Moderate- Middle- Upper- Unknown

Motor Vehicle

0 2 10 3 0 15 0.0% 13.3% 66.7% 20.0% 0.0% 100% $ 0 $ 33 $ 167 $ 45 $ 0 $ 245 0.0% 13.5% 68.2% 18.4% 0.0% 100%

Household Population 0.0% 22.3% 65.0% 12.7% 0.0% 100%

18

Southern Bancorp Bank of Arkansas CRA Performance Evaluation Arkadelphia, Arkansas December 1, 2008

19

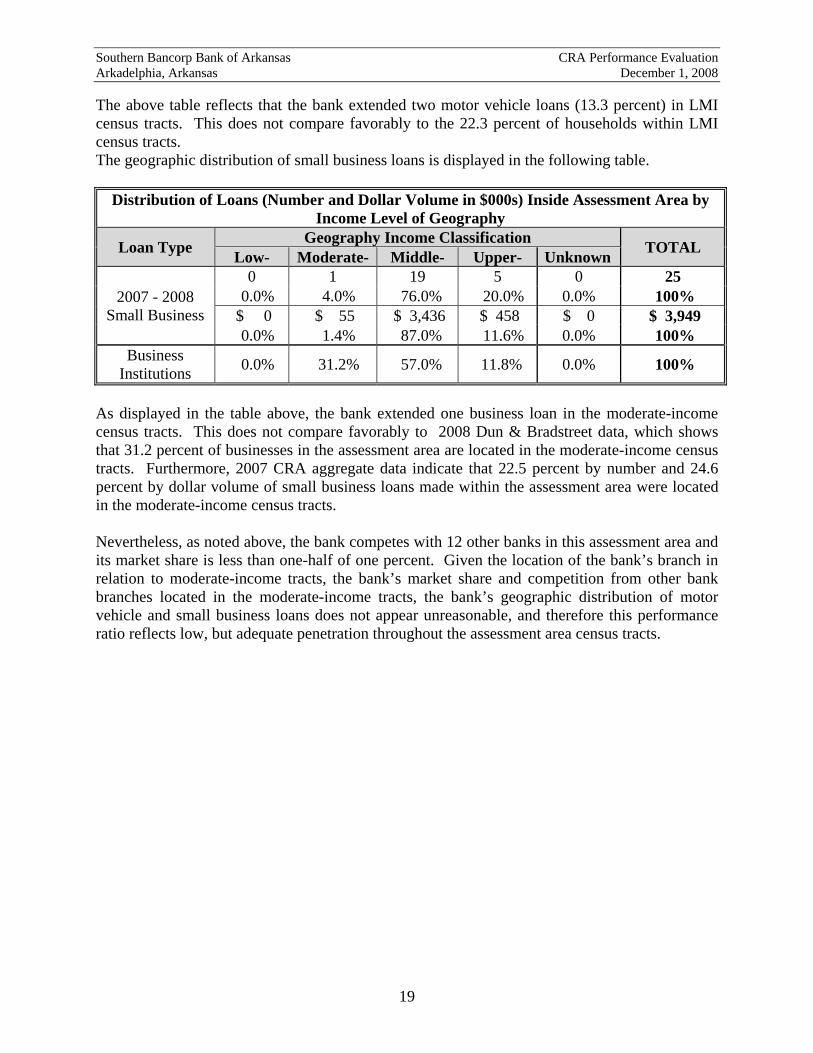

The above table reflects that the bank extended two motor vehicle loans (13.3 percent) in LMI census tracts. This does not compare favorably to the 22.3 percent of households within LMI census tracts. The geographic distribution of small business loans is displayed in the following table.

Distribution of Loans (Number and Dollar Volume in $000s) Inside Assessment Area by Income Level of Geography

Loan Type Geography Income Classification TOTAL Low- Moderate- Middle- Upper- Unknown

2007 - 2008 Small Business

0 1 19 5 0 25 0.0% 4.0% 76.0% 20.0% 0.0% 100% $ 0 $ 55 $ 3,436 $ 458 $ 0 $ 3,949 0.0% 1.4% 87.0% 11.6% 0.0% 100%

Business Institutions 0.0% 31.2% 57.0% 11.8% 0.0% 100%

As displayed in the table above, the bank extended one business loan in the moderate-income census tracts. This does not compare favorably to 2008 Dun & Bradstreet data, which shows that 31.2 percent of businesses in the assessment area are located in the moderate-income census tracts. Furthermore, 2007 CRA aggregate data indicate that 22.5 percent by number and 24.6 percent by dollar volume of small business loans made within the assessment area were located in the moderate-income census tracts. Nevertheless, as noted above, the bank competes with 12 other banks in this assessment area and its market share is less than one-half of one percent. Given the location of the bank’s branch in relation to moderate-income tracts, the bank’s market share and competition from other bank branches located in the moderate-income tracts, the bank’s geographic distribution of motor vehicle and small business loans does not appear unreasonable, and therefore this performance ratio reflects low, but adequate penetration throughout the assessment area census tracts.

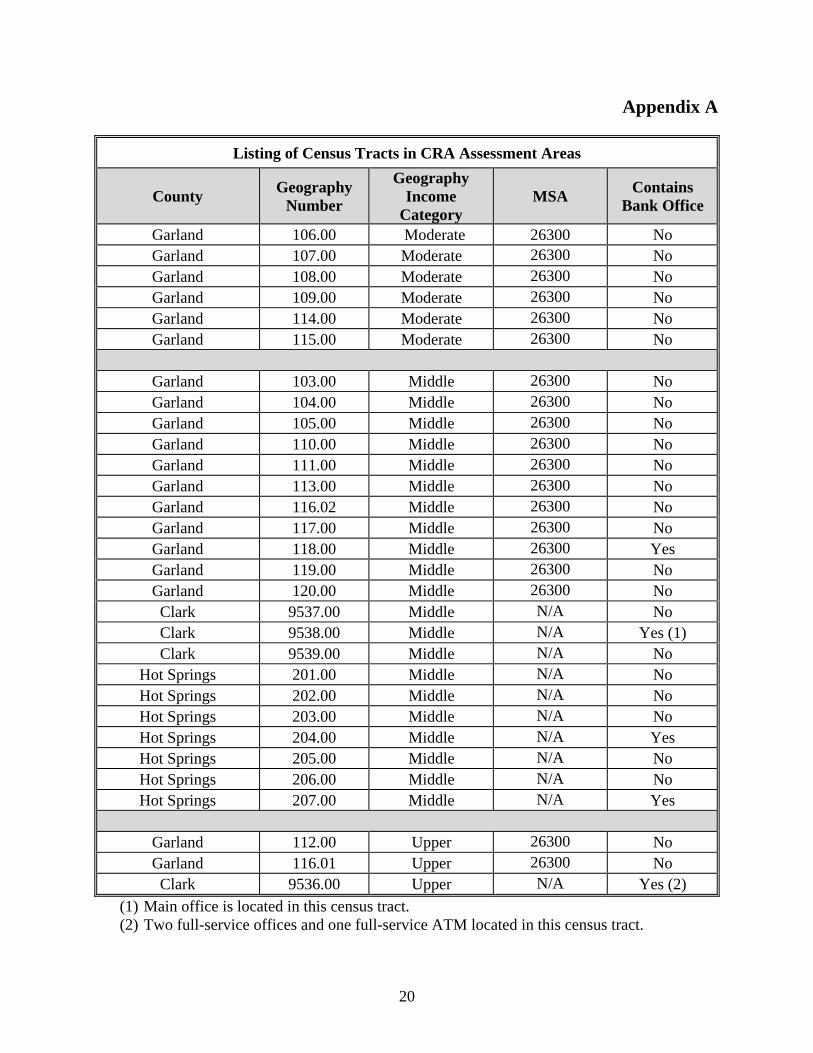

Appendix A

Listing of Census Tracts in CRA Assessment Areas

County Geography Number

Geography Income

Category MSA Contains

Bank Office

Garland 106.00 Moderate 26300 No Garland 107.00 Moderate 26300 No Garland 108.00 Moderate 26300 No Garland 109.00 Moderate 26300 No Garland 114.00 Moderate 26300 No Garland 115.00 Moderate 26300 No

Garland 103.00 Middle 26300 No Garland 104.00 Middle 26300 No Garland 105.00 Middle 26300 No Garland 110.00 Middle 26300 No Garland 111.00 Middle 26300 No Garland 113.00 Middle 26300 No Garland 116.02 Middle 26300 No Garland 117.00 Middle 26300 No Garland 118.00 Middle 26300 Yes Garland 119.00 Middle 26300 No Garland 120.00 Middle 26300 No Clark 9537.00 Middle N/A No Clark 9538.00 Middle N/A Yes (1) Clark 9539.00 Middle N/A No

Hot Springs 201.00 Middle N/A No Hot Springs 202.00 Middle N/A No Hot Springs 203.00 Middle N/A No Hot Springs 204.00 Middle N/A Yes Hot Springs 205.00 Middle N/A No Hot Springs 206.00 Middle N/A No Hot Springs 207.00 Middle N/A Yes

Garland 112.00 Upper 26300 No Garland 116.01 Upper 26300 No Clark 9536.00 Upper N/A Yes (2)

(1) Main office is located in this census tract. (2) Two full-service offices and one full-service ATM located in this census tract.

20

Appendix B

GLOSSARY

Aggregate lending: The number of loans originated and purchased by all reporting lenders in specified income categories as a percentage of the aggregate number of loans originated and purchased by all reporting lenders in the metropolitan area/assessment area. Census tract: A small subdivision of metropolitan and other densely populated counties. Census tract boundaries do not cross county lines; however, they may cross the boundaries of metropolitan statistical areas. Census tracts usually have between 2,500 and 8,000 persons, and their physical size varies widely depending upon population density. Census tracts are designed to be homogeneous with respect to population characteristics, economic status, and living conditions to allow for statistical comparisons. Community development: All Agencies have adopted the following language. Affordable housing (including multifamily rental housing) for low- or moderate-income individuals; community services targeted to low- or moderate-income individuals; activities that promote economic development by financing businesses or farms that meet the size eligibility standards of the Small Business Administration’s Development Company or Small Business Investment Company programs (13 CFR 121.301) or have gross annual revenues of $1 million or less; or, activities that revitalize or stabilize low- or moderate-income geographies. Effective September 1, 2005, the Board of Governors of the Federal Reserve System, Office of the Comptroller of the Currency, and the Federal Deposit Insurance Corporation have adopted the following additional language as part of the revitalize or stabilize definition of community development. Activities that revitalize or stabilize-

(i) Low-or moderate-income geographies; (ii) Designated disaster areas; or (ii) Distressed or underserved non-metropolitan middle-income geographies

designated by the Board, Federal Deposit Insurance Corporation, and Office of the Comptroller of the Currency, based on-

a. Rates of poverty, unemployment, and population loss; or b. Population size, density, and dispersion. Activities that revitalize and

stabilize geographies designated based on population size, density, and dispersion if they help to meet essential community needs, including needs of low- and moderate-income individuals.

Consumer loan(s): A loan(s) to one or more individuals for household, family, or other personal expenditures. A consumer loan does not include a home mortgage, small business, or small farm loan. This definition includes the following categories: motor vehicle loans, credit card loans, home equity loans, other secured consumer loans, and other unsecured consumer loans.

21

Family: Includes a householder and one or more other persons living in the same household who are related to the householder by birth, marriage, or adoption. The number of family households always equals the number of families; however, a family household may also include non-relatives living with the family. Families are classified by type as either a married-couple family or other family, which is further classified into ‘male householder’ (a family with a male householder and no wife present) or ‘female householder’ (a family with a female householder and no husband present). Full-scope review: Performance under the Lending, Investment, and Service Tests is analyzed considering performance context, quantitative factors (for example, geographic distribution, borrower distribution, and total number and dollar amount of investments), and qualitative factors (for example, innovativeness, complexity, and responsiveness). Geography: A census tract delineated by the United States Bureau of the Census in the most recent decennial census. Home Mortgage Disclosure Act (HMDA): The statute that requires certain mortgage lenders that do business or have banking offices in a metropolitan statistical area to file annual summary reports of their mortgage lending activity. The reports include such data as the race, gender, and the income of applicants, the amount of loan requested, and the disposition of the application (for example, approved, denied, and withdrawn). Home mortgage loans: Includes home purchase and home improvement loans as defined in the HMDA regulation. This definition also includes multifamily (five or more families) dwelling loans, loans for the purchase of manufactured homes and refinancing of home improvement and home purchase loans. Household: Includes all persons occupying a housing unit. Persons not living in households are classified as living in group quarters. In 100 percent tabulations, the count of households always equals the count of occupied housing units. Limited-scope review: Performance under the Lending, Investment, and Service Tests is analyzed using only quantitative factors (for example, geographic distribution, borrower distribution, total number and dollar amount of investments and branch distribution). Low-income: Individual income that is less than 50 percent of the area median income, or a median family income that is less than 50 percent, in the case of a geography. Market share: The number of loans originated and purchased by the institution as a percentage of the aggregate number of loans originated and purchased by all reporting lenders in the metropolitan area/assessment area.

22

Metropolitan area (MA): A metropolitan statistical area (MSA) or a metropolitan division (MD) as defined by the Office of Management and Budget. An MSA is a core area containing at least one urbanized area of 50,000 or more inhabitants, together with adjacent communities having a high degree of economic and social integration with that core. An MD is a division of an MSA based on specific criteria including commuting patterns. Only an MSA that has a population of at least 2.5 million may be divided into MDs. Middle-income: Individual income that is at least 80 percent and less than 120 percent of the area median income, or a median family income that is at least 80 percent and less than 120 percent, in the case of geography. Moderate-income: Individual income that is at least 50 percent and less than 80 percent of the area median income, or a median family income that is at least 50 percent and less than 80 percent, in the case of a geography. Multifamily: Refers to a residential structure that contains five or more units. Other products: Includes any unreported optional category of loans for which the institution collects and maintains data for consideration during a CRA examination. Examples of such activity include consumer loans and other loan data an institution may provide concerning its lending performance. Owner-occupied units: Includes units occupied by the owner or co-owner, even if the unit has not been fully paid for or is mortgaged. Qualified investment: A qualified investment is defined as any lawful investment, deposit, membership share, or grant that has as its primary purpose community development. Rated area: A rated area is a state or multi-state metropolitan area. For an institution with domestic branches in only one state, the institution’s CRA rating would be the state rating. If an institution maintains domestic branches in more than one state, the institution will receive a rating for each state in which those branches are located. If an institution maintains domestic branches in two or more states within a multi-state metropolitan area, the institution will receive a rating for the multi-state metropolitan area. Small loan(s) to business (es): A loan included in 'loans to small businesses' as defined in the Consolidated Report of Condition and Income (Call Report) and the Thrift Financial Reporting (TFR) instructions. These loans have original amounts of $1 million or less and typically are secured either by nonfarm or nonresidential real estate or are classified as commercial and industrial loans. However, thrift institutions may also exercise the option to report loans secured by nonfarm residential real estate as "small business loans" if the loans are reported on the TFR as non-mortgage, commercial loans.

23

24

Small loan(s) to farm(s): A loan included in ‘loans to small farms’ as defined in the instructions for preparation of the Consolidated Report of Condition and Income (Call Report). These loans have original amounts of $500,000 or less and are either secured by farmland, or are classified as loans to finance agricultural production and other loans to farmers. Upper-income: Individual income that is 120 percent or more of the area median income, or a median family income that is 120 percent or more, in the case of a geography.