Identify Similarities Between Battlefield Management and Cost Management ©1.

52

Identify Similarities Between Battlefield Management and Cost Management Intermediate Cost Analysis and Management © 1

-

Upload

ann-dorsey -

Category

Documents

-

view

216 -

download

0

Transcript of Identify Similarities Between Battlefield Management and Cost Management ©1.

Identify Similarities Between Battlefield Management and Cost Management

Intermediate Cost Analysis and Management

© 1

Program of Instruction Overview

Understanding Cost Applying the ProcessLearning the Process

Accounting Basics Cost Relationships Cost Tradeoffs Cost Projection Cost Explanation

Cost Benefit Analysis CBA Examples Cost Management After Action Review Cost Management Cases

Cost Control Theory Org Based Control Role Based Control Output Based Control Change Management

Week One Week ThreeWeek Two

Why are We Interested in Cost Management?

• How many brigade combat teams can you afford if:• Each costs $2B and you have $30B?• Each costs $3B and you have $30B?• Each costs $5B and you have $30B?

© 3

Unit Cost Total Cost Units

$2B $30B 15 BCTs

$3B $30B 10 BCTs

$5B $30B 6 BCTs

Which provides the stronger

Army?

Terminal Learning Objective

• Task: Identify Similarities Between Battlefield Management And Cost Management

• Condition: You are training to become an ACE with access to ICAM course handouts, readings, and spreadsheet tools and awareness of Operational Environment (OE)/Contemporary Operational Environment (COE) variables and actors.

• Standard: with at least 80% accuracy• Identify symptoms of the Cost War• Demonstrate understanding and awareness of the purpose and

motivations for managerial costing• Describe the importance of Commander’s Intent

© 4

Cost Management and Control: National Security Implications

• What if the cost of a BCT could be reduced by one-third while maintaining the same effectiveness?

• Simplify the math by considering Army Budget to be 30 and initial BCT cost to be 3

© 5

ARMY Budget 30 initial BCT cost 3

= = 10 BCTs ARMY Budget 302/3 initial BCT cost 2

= = 15 BCTs

A one-third cost reduction yields a 50% increase in BCTs

“My guess is that a third of the defense budget goes into the friction of following bad regulations – doing work that doesn’t need to be done.”

Bob Stone former DASD Installations, Reinventing Government

x x x xx

x x x xx

x x x xx

x x x xxx x x xx

Risk to Mission = Cost War

• The Cost War is the struggle:• To accomplish and enhance your organization’s

mission • With fewer financial resources than you would

wish• While meeting specifications for quality,

customer service, and ethics

© 6

Are You in a Cost War?

• Do you need more resources?• Have your budgets been cut?

• More than once?• Almost always?

• Is your list of unfunded requirements increasing?

• Do you have limits on hiring?• Are you getting unfunded mandates?

© 7

Assess Before Continuing

STOP: You need not proceed if your organization is not in a Cost War

GO: Proceed only if your organization is engaged in a Cost War

© 8

What are You Going to Do About It?

• Alternative 1: Try to get more budget• Better define and document “needs”• Highlight deficiencies and problems• Contrast funding levels to others’• React to cuts with downsizing, reduced service

levels, personnel cuts

© 9

The old way of doing things

BudgetAppropriated

MissionAccomplished

$

Traditional View of Budget

© 10

Traditional View of Budget

© 11

Budget Appropriated

Mission Accomplished

$

What are You Going to Do About It?

• Alternative 2: Manage cost better• Seek, but don’t count on, budget increases• Develop a cost management paradigm• Measure costs as needed• Motivate a culture of continuous

improvement in productivity• Reprogram/redirect savings to self fund needs

© 12

What This Course is All

About

$

BudgetAppropriated

Management

Better MissionExecution

$ $

RedirectedEfficiencies

$

Payoff: Better Execution,Not Cost Savings

© 13

Top 10 Reasons Government Orgs Manage Cost

1. Enhance Mission Execution2. Enhance Mission Execution3. Enhance Mission Execution4. Enhance Mission Execution5. Enhance Mission Execution6. Enhance Mission Execution7. Enhance Mission Execution8. Enhance Mission Execution9. Enhance Mission Execution10. Enhance Mission Execution

© 14

Productivity: Getting More Mission for Less Cost

• Private sector productivity is the cornerstone of recent economic success

• National statistics show sustained 3-4% annual rate of productivity improvement

• What did you pay for your first calculator? iPod? Cell phone? Computer?

© 15

Conclusion: The Cost War

• Period of plenty (The Cold War) is over• Period of limited resources (The Cost War) has

begun• Losing the Cost War will result in excessive loss of

mission capability or missed opportunities for enhancement

• Winning the Cost War Requires a strong cost management process and a culture of continuous improvement

© 16

Learning Check

• You know you’re in a Cost War if…..?• What are the two alternatives for dealing with

reduced resources?

© 17

Assess Before Continuing

STOP: Do not proceed if you would emphasize resource acquisition or if you don’t want this mission

GO: Proceed only if you wish to more efficiently use the resources you have and you want this job

© 18

Can Government Manage?

• Many believe “Government Management” is an oxymoron• Do you?

• Academics typically cite:• Lack of profit motive• History of government spending

© 19

How Important is Profit Motive?

• Most managers in corporations are not profit managers• Cost center managers outnumber profit center

managers 40 or 50 to 1• Owner control is typically weak unless an

individual owns a large share block• Probably not much different than power of voters

in political elections

© 20

Can Government Manage?

• History of last 60 years of Government spending • Cited as evidence by skeptics of Government’s

inability to manage• Used here as rationale that Government has

not needed to manage

© 21

Government Management Improvement Strategies

© 22

A-76 Business Process Reengineering

Budget Mgmt PART

Cost Management & Control Processes

Centralized Decentralized

Discontinuous

Continuous

Requirements for Cost Management and Control

• Cost Data: Providing the raw materials needed for decision making and process

• Process: Institutionalizing a method of stimulating continuous improvement

• Cost Staff: Translating data into information• Leadership: Driving management, setting and

achieving intent

© 23

Cost Management & Control Processes Must

• Require frequent management attention• Stimulate learning: frequent feedback • Generate goals that challenge• Encourage performance to meet goals• Eliminate entitlements • Create continuous improvement culture• Emphasize constant reduction of needs

© 24

Battlefield Management

• Provides a useful template for cost management

• Good military commanders are inherently cost conscious in achieving missions • Minimize cost in casualty losses• Minimize cost in resources and capabilities

• Good financial managers must also be cost conscious in achieving their missions

© 25

Battlefield Management

• Unique to government management arena• No profit motive exists• We’re pretty good at it• Command, control, and communication

paradigm provides a useful template for cost based management

© 26

Cost Command and Control

Process

Battlefield Intelligencebecomes

Managerial Costing

Warrior Pullbecomes

Cost Warrior Pull

Modeling and Simulation

becomes

Cost Planning

After Action Reviewbecomes

Cost After ActionReview

Command, Control, and Communication of Cost

© 27

The Role of Cost Planning

• Provides proactive alternative to annual budget crisis

• Stimulates learning/training in financial consequences of alternative actions cheaply

• Provides a basis to evaluate mission success• Clarifies short term assignments

© 28

Cost CommandAnd Control

Cost Planning

: Cost Projection: What- Iffing: Ad Hoc Analysis

The Role of theCost After Action Review

• Document and explain performance• Evaluate performance and create

accountability• Stimulate learning for:

• Better reconnaissance• Better planning• Better execution

© 29

Cost CommandAnd Control

Cost After Action Review

È Performance MeasurementÈ Fixed AccountabilityÈ Continuous Improvement

The Role of Cost Warrior Pull

• Specify managerial costing requirement• Perform intelligence prep of the battlefield• Determine essential elements of info

• Lead the cost management process• Set the agenda• Negotiate and approve plans• Critically review execution• Signal the importance of cost management

© 30

Process

Cost Warrior Pull« Command Specification

« Command Review

« Command Goal SettingCost Command

And Control

Cost CommandAnd Control

The Role ofManagerial Costing

• Develop needed intelligence for the cost manager fighting the cost war • Needed: credible measurement of true costs of

resource consumption• Provide information to the cost management

process• Needed for decision making, planning processes,

and after action reviews

© 31

Managerial Costing

$ Relevant Costs$ Customized Views$ True Resource Use

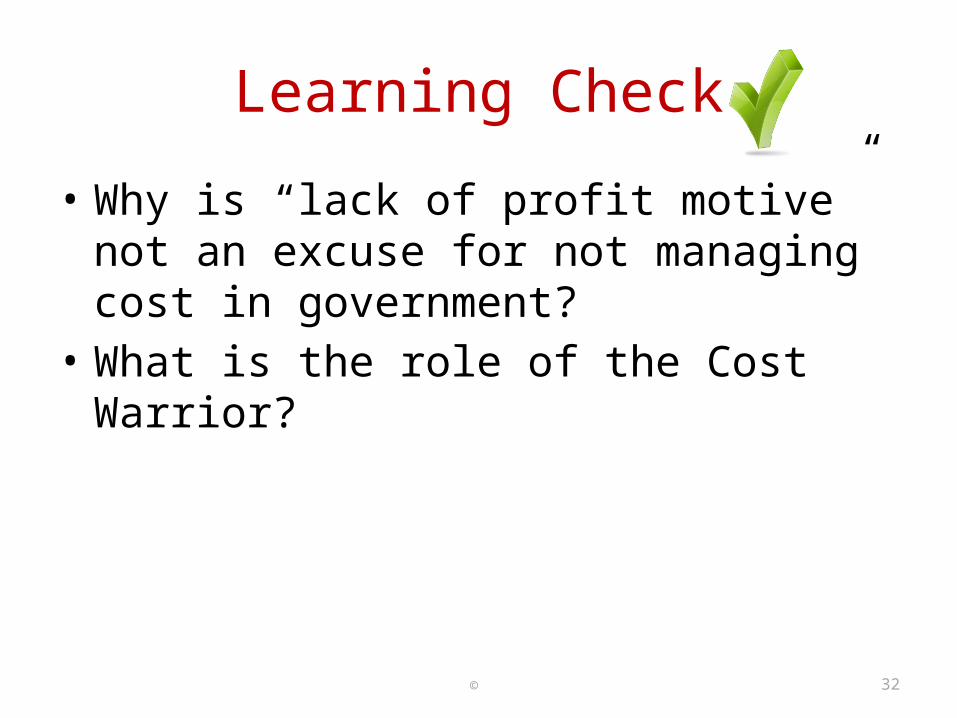

Learning Check

• Why is “lack of profit motive” not an excuse for not managing cost in government?

• What is the role of the Cost Warrior?

© 32

© 33

Costing Systems Differ

Internally SpecifiedRequire-ments

Externally SpecifiedRequire-ments

Goals: Consistency Comparability EquityUsers: Shareholders Congress Regulators Tax AuthoritiesMethodology: Laws Rules GAAP

Goals: Fit Functionality Relevance

Users: Managers

Methodology: Situation Dependent

Financial &Regulatory

Managerial

Cost CommandAnd Control

Managerial Costing

$ Relevant Costs$ Customized Views$ True Resource Use

© 34

Managerial Cost Accounting

• Seeks to understand true economic cost• Based on cause-effect relationships• Reflecting drivers of resource consumption• With reasonable, but not precise, accuracy

• Enables cost based management for continuous improvement

• Enables better decision making• Enables rational consumption behavior

Cost CommandAnd Control

Managerial Costing

$ Relevant Costs$ Customized Views$ True Resource Use

© 35

Why Do Managerial Costing?

1. Enhance decision making2. Provide reconnaissance necessary for

Cost Based Management process3. Influence resource consumption behavior

Cost CommandAnd Control

Managerial Costing

$ Relevant Costs$ Customized Views$ True Resource Use

© 36

1. Cost Measurement’s Role in Decision Making

• Which Metal is Best for Transmission?

Metal A Metal B Metal C

Conductivity + ++ +++

Cost CommandAnd Control

Managerial Costing

$ Relevant Costs$ Customized Views$ True Resource Use

© 37

2. Cost Managed OrgsNeed Cost Measurement

• Cost managers must have cost measurement to fight Cost War

• Cost measurement• Informs Cost Warriors of financial implications of

management decisions• Provides a basis of accountability• Is prerequisite to cost reduction

Cost CommandAnd Control

Managerial Costing

$ Relevant Costs$ Customized Views$ True Resource Use

© 38

3. Cost Measurement’s Influence on Consumption

• The Demand Curve - Economics 101

Cost

Quantity Demanded

Cost CommandAnd Control

Managerial Costing

$ Relevant Costs$ Customized Views$ True Resource Use

© 39

Not Knowing Cost Makes Everything Appear Free

• Cost influences consumption• Quantity demanded rises as cost falls• Free goods have infinite demand

• Things that aren’t free, but appear free, get overconsumed

• Attempts to prevent overconsumption lead to rules, regulations, restrictions

Cost CommandAnd Control

Managerial Costing

$ Relevant Costs$ Customized Views$ True Resource Use

© 40

Learning Check

• How does demand for a good change as cost decreases?

• What is the logical result of not knowing what something costs?

Commander’s Intent

“Commanders must develop and communicate a clear vision or intent”

--United States Army Field Manual FM 25-101 Battle Focused Training (emphasis added)

© 41

Process

Cost Warrior Pull« Command Specification

« Command Review

« Command Goal SettingCost Command

And Control

Why is Commander’s Intent Important?

• We are in a dynamic environment• Changing conditions under fog of war• Unanticipated enemy actions/reactions• Unforeseen opportunities and threats

• We wish to capitalize on the skills of subordinates who are best positioned to make decisions

© 42

Process

Cost Warrior Pull« Command Specification

« Command Review

« Command Goal SettingCost Command

And Control

Commander’s Intent

© 43

--United States Army Field Manual FM 25-101 Battle Focused Training

Process

Cost Warrior Pull« Command Specification

« Command Review

« Command Goal SettingCost Command

And Control

Why is Commander’s Intent Important?

• Commander physically cannot make all decisions

• Commander is not best qualified to make all decisions

• Command must insure control while reaping all possible advantages of decentralization

© 44

Process

Cost Warrior Pull« Command Specification

« Command Review

« Command Goal SettingCost Command

And Control

A Military Analogy

• Consider the economy of force sector• Some sectors in the front line are deliberately

allocated fewer forces• This permits concentration of force for

• The main attack• The secondary attack

• The Cost War now places many government organizations in the fiscal economy of force sector

© 45

Process

Cost Warrior Pull« Command Specification

« Command Review

« Command Goal SettingCost Command

And Control

One Way to Think About Your Options

• Grant Me . . . • The Serenity to Accept the

Things I Cannot Change;• The Courage to Change the

Things I Can;• And the Wisdom to Know

the Difference

Þ Resource Level

Þ Resource Management

Þ Your Decision

© 46

Process

Cost Warrior Pull« Command Specification

« Command Review

« Command Goal SettingCost Command

And Control

How Would You Spend Your Time as Commander in the Economy of Force Sector?

• Your time and energy are limited• You must allocate them between:

• Going to higher HQ to plead for more resources to increase your effectiveness

• Staying at your sector maximizing the effectiveness of the resources you have

• Would you:• Spend 80% of your time at HQ?• Divide your efforts equally between the two actions?• Spend 80% of your time in your area of operation

making the best of what you’ve got? © 47

Process

Cost Warrior Pull« Command Specification

« Command Review

« Command Goal SettingCost Command

And Control

Group Activity

• Break into groups• Address the previous slide’s question

Write a one page PowerPoint slide with your

Commander’s Intent

• Present your statement to the class in 20 minutes

© 48

Process

Cost Warrior Pull« Command Specification

« Command Review

« Command Goal SettingCost Command

And Control

Commander’s Intent: Leadership Foundation

• Development of clear vision and intent is key to: • Leading the continuous improvement process• Developing and institutionalizing the cost

based performance management process and needed cost measurement capabilities

© 49

Process

Cost Warrior Pull« Command Specification

« Command Review

« Command Goal SettingCost Command

And Control

The Leader’s Evolution of Cost Thinking

1. Recognition that continuously reduced resources have become a way of life

2. Awareness that sound management of resources has become more important

3. Search for a workable management paradigm becomes critically important

4. Development of actionable measurement capability becomes indispensable

© 50

Process

Cost Warrior Pull« Command Specification

« Command Review

« Command Goal SettingCost Command

And Control

The Leader’s Objective in Cost Management

• Change culture to one which:• Aggressively seek better ways to operate• De-emphasize defense of past practice

(assumed best practice at that time)• Require and expect development of continuous

improvement initiatives • Today, tomorrow, next week, next month,

next year, forever

© 51

Process

Cost Warrior Pull« Command Specification

« Command Review

« Command Goal SettingCost Command

And Control

Learning Check

• Why is Commander’s Intent important?• What does it mean to be in the fiscal economy

of forces sector?

© 52