IDENTIFICATION OF PERFORMANCE INDICATORS FOR AUDIT OF COMMERCIAL TAX ANU JOSE & MONICA RAJAMANOHAR.

25

IDENTIFICATION OF PERFORMANCE INDICATORS FOR AUDIT OF COMMERCIAL TAX ANU JOSE & MONICA RAJAMANOHAR

-

Upload

benedict-jenkins -

Category

Documents

-

view

217 -

download

0

Transcript of IDENTIFICATION OF PERFORMANCE INDICATORS FOR AUDIT OF COMMERCIAL TAX ANU JOSE & MONICA RAJAMANOHAR.

IDENTIFICATION OFPERFORMANCE INDICATORS FORAUDIT OF COMMERCIAL TAX

ANU JOSE & MONICA RAJAMANOHAR

OUTLINE TAX BASE

FILING OF RETURNS

CALCULATION OF TAX LIABILITY

CROSS VERIFICATION OF THIRD PARTY DATA

AUDIT

ENFORCEMENT

APPEAL

COLLECTION

PERFORMANCE INDICATORS FOR AUDIT OF COMMERCIAL TAX

TAX BASE

IDENTIFICATION OF TAX BASE

Indicator Performance

Frequency of street survey If Monthly, Yes

Adequacy of information sharing with other relevant departments

Central Excise, Customs, Income Tax 50%

Railways, Transport 75%

Registration, Forests, Mines & Geology, CPWD 90%

Adequacy of action taken on the information >90%, Yes

Existence of policy regarding e-Commerce traders If exists, Yes

REGISTRATION

Indicator Performance

Transparency of application process If Online, Yes

Adequacy of verification of dealer’s premises > 70%, Yes

Timeliness of issue of registration certificate > 90%, Yes

MAINTENANCE OF TAX BASE

Indicator Performance

Frequency of street survey to ensure business continuity

If Quarterly, Yes

Adequacy of action on stopped / discontinued businesses

> 90% of cancellation of registration certificates

CANCELLATION OF REGISTRATIONIndicator Performance

Adequacy of cancellation of registration certificates of non-filers

> 95%, Yes

Adequacy of cancellation of registration certificates on the basis of violation of any other prescribed norms

> 95%, Yes

Adequacy of follow up action (treatment of purchases, finalization of assessment)

> 90%, Yes

Conduct of audit of dealers who apply for cancellation

> 90%, Yes

PERFORMANCE INDICATORS FOR AUDIT OF COMMERCIAL TAX

FILING OF RETURNS

FILING OF RETURNSIndicator Performance

Adequacy of forms Qualitative

Provision for online filing the returns along annexures and prescribed documents and e-payment

If available, Yes

Adequacy of action taken on non-filers > 90%, Yes

Adequacy of action taken on persistent nil return filers > 90%, Yes

Adequacy of action taken on belated filing of returns > 90%, Yes

Payment of tax liability along with / before filing of return If available, Yes

Adequacy of action taken on belated payment / dishonoured Cheques

> 90%, Yes

PERFORMANCE INDICATORS FOR AUDIT OF COMMERCIAL TAX

CALCULATION OF TAX LIABILITY

RATES & CLASSIFICATION

Indicator Performance

Adoption of HSN classification Yes

If No, Extent of deviation from HSN < 30%, Yes

Timeliness of issue of clarification and advance ruling

> 90%, Yes

Extent of adoption of rates prescribed by clarification and advance ruling

> 90%, Yes

ASSESSMENT

Indicator Performance

Presence of system of automatic calculation of liability based on purchase and sales data filed by the dealers

If available, Yes

Presence of system of automatic issue of self / deemed assessment notices

If available, Yes

Adequacy of follow up of incomplete / incorrect returns through system provisional and/or Best Judgment assessment

> 90%, Yes

Adequacy of follow up of issue of notices (other than deemed) by revision of assessment

> 90%, Yes

REFUND

Indicator Performance

Extent of scrutiny of returns before approval of refund

> 90%, Yes

Timeliness of issue of refund > 90%, Yes

PERFORMANCE INDICATORS FOR AUDIT OF COMMERCIAL TAX

CROSS VERIFICATION OF THIRD PARTY DATA

CROSS VERIFICATION OF THIRD PARTY DATA

Indicator Performance

Adequacy of information sharing with other relevant departments

Central Excise, Customs, Income Tax 50%

Railways, Transport 75%

Registration, Forests, Mines & Geology, CPWD 90%

Presence of system of risk rating of dealers If available, Yes

PERFORMANCE INDICATORS FOR AUDIT OF COMMERCIAL TAX

AUDIT

AUDITIndicator Performance

Whether audit and assessment are independent of each other?

If available, Yes

Whether selection of dealers for audit is based on set criteria or subjective?

If available, Yes

Adequacy of coverage of high risk dealers in selection > 90%, Yes

Timeliness of selection > 90%, Yes

Timeliness of conduct of audit > 90%, Yes

Timeliness of follow up of audit proposals by assessing authority

> 90%, Yes

PERFORMANCE INDICATORS FOR AUDIT OF COMMERCIAL TAX

ENFORCEMENT

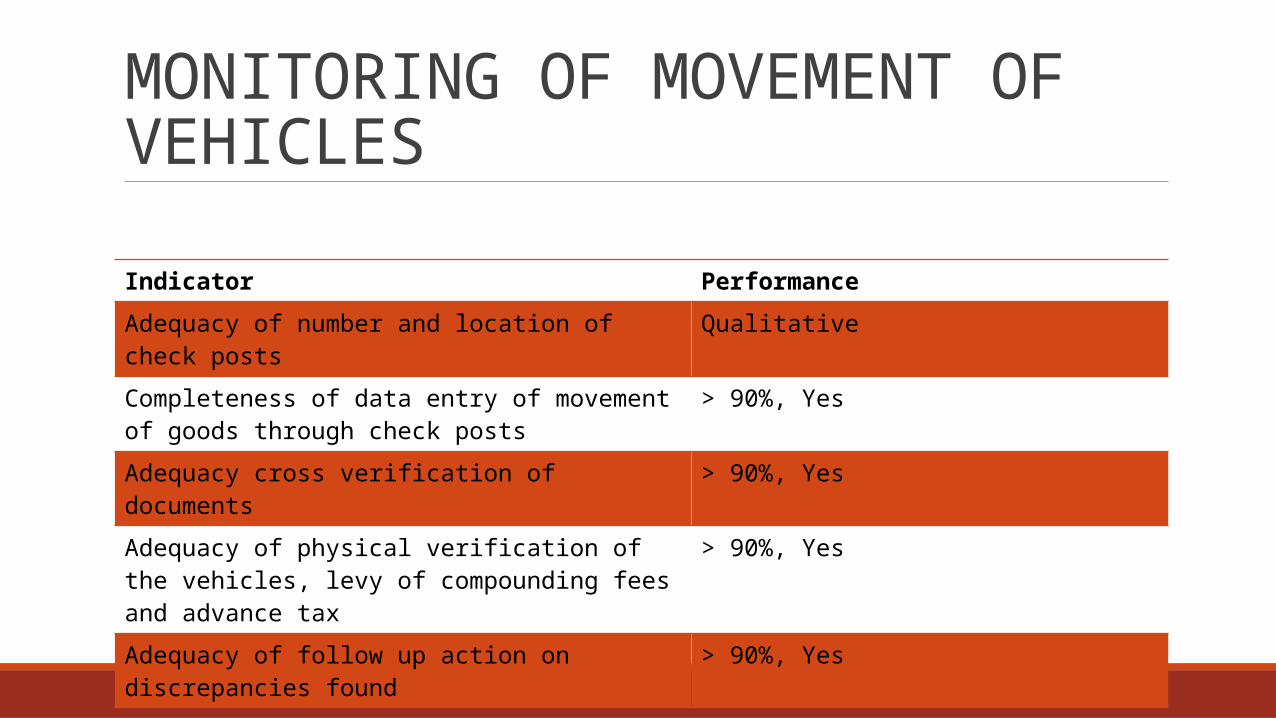

MONITORING OF MOVEMENT OF VEHICLES

Indicator Performance

Adequacy of number and location of check posts Qualitative

Completeness of data entry of movement of goods through check posts

> 90%, Yes

Adequacy cross verification of documents > 90%, Yes

Adequacy of physical verification of the vehicles, levy of compounding fees and advance tax

> 90%, Yes

Adequacy of follow up action on discrepancies found > 90%, Yes

INTER STATE INVESTIGATION CELL

Indicator Performance

Pendency of verification of Extract Verification by ISIC < 30%, Yes

Presence of system of identification of bogus dealers and black listing

If available, Yes

PERFORMANCE INDICATORS FOR AUDIT OF COMMERCIAL TAX

APPEAL

APPEAL

Indicator Performance

Timely disposal of cases > 90%, Yes

Efficiency of system of appeal by department > 60%, Yes (Success)

Adequacy of follow-up made on cases decided by appellate forums within stipulated time

> 90%, Yes

Presence of system of intimation about identical issues pending in court by the dealers

If available, Yes

PERFORMANCE INDICATORS FOR AUDIT OF COMMERCIAL TAX

COLLECTION

COLLECTION

Indicator Performance

Percentage of arrear collection > 20%, Yes

Percentage of ineligible dealers whose arrears were settled under settlement schemes

< 5%, Yes

Percentage of revenue recovered through RR act > 10%, Yes

THANK YOU