Internet Marketing Malaysia-LINs Advertising & Marketing Sdn Bhd

THIS INDEPENDENT ADVICE CIRCULAR (“IAC”) IS IMPORTANT AND REQUIRES YOUR IMMEDIATE ATTENTION. YOU SHOULD READ THIS IAC IN CONJUNCTION WITH THE OFFER DOCUMENT DATED 5 MARCH 2018 ISSUED BY KENANGA INVESTMENT BANK BERHAD ON BEHALF OF WIDAD BUSINESS GROUP SDN BHD (“OFFEROR”) WHICH HAS BEEN SENT TO YOU. If you are in any doubt as to the action to be taken in relation to the Offer (as defined herein), please consult your stockbroker, solicitor, bank manager, accountant or other professional advisers immediately. If you have sold or transferred all your Offer Shares (as defined herein), you should at once hand this IAC to the purchaser or stockbroker or agent through whom you effected the sale or transfer for onward transmission to the purchaser or transferee of such Offer Shares. Pursuant to Rule 11 of the Rules on Take-overs, Mergers and Compulsory Acquisitions, the Securities Commission Malaysia (“SC”) has notified that it has no further comments to the contents of this IAC. However, such notification shall not be taken to suggest that the SC agrees with our recommendation or assumes responsibility for the correctness of any statements made or opinions or reports expressed in IAC.

IDEAL JACOBS (MALAYSIA) CORPORATION BHD

(Company No. 857363-U) (Incorporated in Malaysia under the Companies Act, 1965)

INDEPENDENT ADVICE CIRCULAR TO THE HOLDERS OF THE OFFER SHARES IN RELATION TO THE UNCONDITIONAL MANDATORY TAKE-OVER OFFER

BY

WIDAD BUSINESS GROUP SDN BHD

(Company No. 602380-P) (Incorporated in Malaysia under the Companies Act, 1965)

THROUGH

KENANGA INVESTMENT BANK BERHAD

(Company No. 15678-H) (A Participating Organisation of Bursa Malaysia Securities Berhad)

TO ACQUIRE ALL THE REMAINING ORDINARY SHARES IN IDEAL JACOBS (MALAYSIA) CORPORATION BHD (“IDEAL JACOBS”) AS WELL AS ANY NEW ORDINARY SHARES ARISING FROM THE EXERCISE OF OPTIONS GRANTED PURSUANT TO IDEAL JACOBS’ EMPLOYEE SHARE OPTION SCHEME NOT ALREADY HELD BY THE OFFEROR (“OFFER SHARES”) FOR A CASH CONSIDERATION OF RM0.23 PER OFFER SHARE (“OFFER”)

Independent Adviser

M&A SECURITIES SDN BHD (15017-H) (A Wholly-Owned Subsidiary of Insas Berhad)

(A Participating Organisation of Bursa Malaysia Securities Berhad)

This Independent Advice Circular is dated 15 March 2018

THIS INDEPENDENT ADVICE CIRCULAR (“IAC”) IS IMPORTANT AND REQUIRES YOUR IMMEDIATE ATTENTION. YOU SHOULD READ THIS IAC IN CONJUNCTION WITH THE OFFER DOCUMENT DATED 5 MARCH 2018 ISSUED BY KENANGA INVESTMENT BANK BERHAD ON BEHALF OF WIDAD BUSINESS GROUP SDN BHD (“OFFEROR”) WHICH HAS BEEN SENT TO YOU. If you are in any doubt as to the action to be taken in relation to the Offer (as defined herein), please consult your stockbroker, solicitor, bank manager, accountant or other professional advisers immediately. If you have sold or transferred all your Offer Shares (as defined herein), you should at once hand this IAC to the purchaser or stockbroker or agent through whom you effected the sale or transfer for onward transmission to the purchaser or transferee of such Offer Shares. Pursuant to Rule 11 of the Rules on Take-overs, Mergers and Compulsory Acquisitions, the Securities Commission Malaysia (“SC”) has notified that it has no further comments to the contents of this IAC. However, such notification shall not be taken to suggest that the SC agrees with our recommendation or assumes responsibility for the correctness of any statements made or opinions or reports expressed in IAC.

IDEAL JACOBS (MALAYSIA) CORPORATION BHD

(Company No. 857363-U) (Incorporated in Malaysia under the Companies Act, 1965)

INDEPENDENT ADVICE CIRCULAR TO THE HOLDERS OF THE OFFER SHARES IN RELATION TO THE UNCONDITIONAL MANDATORY TAKE-OVER OFFER

BY

WIDAD BUSINESS GROUP SDN BHD

(Company No. 602380-P) (Incorporated in Malaysia under the Companies Act, 1965)

THROUGH

KENANGA INVESTMENT BANK BERHAD

(Company No. 15678-H) (A Participating Organisation of Bursa Malaysia Securities Berhad)

TO ACQUIRE ALL THE REMAINING ORDINARY SHARES IN IDEAL JACOBS (MALAYSIA) CORPORATION BHD (“IDEAL JACOBS”) AS WELL AS ANY NEW ORDINARY SHARES ARISING FROM THE EXERCISE OF OPTIONS GRANTED PURSUANT TO IDEAL JACOBS’ EMPLOYEE SHARE OPTION SCHEME NOT ALREADY HELD BY THE OFFEROR (“OFFER SHARES”) FOR A CASH CONSIDERATION OF RM0.23 PER OFFER SHARE (“OFFER”)

Independent Adviser

M&A SECURITIES SDN BHD (15017-H) (A Wholly-Owned Subsidiary of Insas Berhad)

(A Participating Organisation of Bursa Malaysia Securities Berhad)

This Independent Advice Circular is dated 15 March 2018

THIS INDEPENDENT ADVICE CIRCULAR (“IAC”) IS IMPORTANT AND REQUIRES YOUR IMMEDIATE ATTENTION. YOU SHOULD READ THIS IAC IN CONJUNCTION WITH THE OFFER DOCUMENT DATED 5 MARCH 2018 ISSUED BY KENANGA INVESTMENT BANK BERHAD ON BEHALF OF WIDAD BUSINESS GROUP SDN BHD (“OFFEROR”) WHICH HAS BEEN SENT TO YOU. If you are in any doubt as to the action to be taken in relation to the Offer (as defined herein), please consult your stockbroker, solicitor, bank manager, accountant or other professional advisers immediately. If you have sold or transferred all your Offer Shares (as defined herein), you should at once hand this IAC to the purchaser or stockbroker or agent through whom you effected the sale or transfer for onward transmission to the purchaser or transferee of such Offer Shares. Pursuant to Rule 11 of the Rules on Take-overs, Mergers and Compulsory Acquisitions, the Securities Commission Malaysia (“SC”) has notified that it has no further comments to the contents of this IAC. However, such notification shall not be taken to suggest that the SC agrees with our recommendation or assumes responsibility for the correctness of any statements made or opinions or reports expressed in IAC.

IDEAL JACOBS (MALAYSIA) CORPORATION BHD

(Company No. 857363-U) (Incorporated in Malaysia under the Companies Act, 1965)

INDEPENDENT ADVICE CIRCULAR TO THE HOLDERS OF THE OFFER SHARES IN RELATION TO THE UNCONDITIONAL MANDATORY TAKE-OVER OFFER

BY

WIDAD BUSINESS GROUP SDN BHD

(Company No. 602380-P) (Incorporated in Malaysia under the Companies Act, 1965)

THROUGH

KENANGA INVESTMENT BANK BERHAD

(Company No. 15678-H) (A Participating Organisation of Bursa Malaysia Securities Berhad)

TO ACQUIRE ALL THE REMAINING ORDINARY SHARES IN IDEAL JACOBS (MALAYSIA) CORPORATION BHD (“IDEAL JACOBS”) AS WELL AS ANY NEW ORDINARY SHARES ARISING FROM THE EXERCISE OF OPTIONS GRANTED PURSUANT TO IDEAL JACOBS’ EMPLOYEE SHARE OPTION SCHEME NOT ALREADY HELD BY THE OFFEROR (“OFFER SHARES”) FOR A CASH CONSIDERATION OF RM0.23 PER OFFER SHARE (“OFFER”)

Independent Adviser

M&A SECURITIES SDN BHD (15017-H) (A Wholly-Owned Subsidiary of Insas Berhad)

(A Participating Organisation of Bursa Malaysia Securities Berhad)

This Independent Advice Circular is dated 15 March 2018

THIS INDEPENDENT ADVICE CIRCULAR (“IAC”) IS IMPORTANT AND REQUIRES YOUR IMMEDIATE ATTENTION. YOU SHOULD READ THIS IAC IN CONJUNCTION WITH THE OFFER DOCUMENT DATED 5 MARCH 2018 ISSUED BY KENANGA INVESTMENT BANK BERHAD ON BEHALF OF WIDAD BUSINESS GROUP SDN BHD (“OFFEROR”) WHICH HAS BEEN SENT TO YOU. If you are in any doubt as to the action to be taken in relation to the Offer (as defined herein), please consult your stockbroker, solicitor, bank manager, accountant or other professional advisers immediately. If you have sold or transferred all your Offer Shares (as defined herein), you should at once hand this IAC to the purchaser or stockbroker or agent through whom you effected the sale or transfer for onward transmission to the purchaser or transferee of such Offer Shares. Pursuant to Rule 11 of the Rules on Take-overs, Mergers and Compulsory Acquisitions, the Securities Commission Malaysia (“SC”) has notified that it has no further comments to the contents of this IAC. However, such notification shall not be taken to suggest that the SC agrees with our recommendation or assumes responsibility for the correctness of any statements made or opinions or reports expressed in IAC.

IDEAL JACOBS (MALAYSIA) CORPORATION BHD

(Company No. 857363-U) (Incorporated in Malaysia under the Companies Act, 1965)

INDEPENDENT ADVICE CIRCULAR TO THE HOLDERS OF THE OFFER SHARES IN RELATION TO THE UNCONDITIONAL MANDATORY TAKE-OVER OFFER

BY

WIDAD BUSINESS GROUP SDN BHD

(Company No. 602380-P) (Incorporated in Malaysia under the Companies Act, 1965)

THROUGH

KENANGA INVESTMENT BANK BERHAD

(Company No. 15678-H) (A Participating Organisation of Bursa Malaysia Securities Berhad)

TO ACQUIRE ALL THE REMAINING ORDINARY SHARES IN IDEAL JACOBS (MALAYSIA) CORPORATION BHD (“IDEAL JACOBS”) AS WELL AS ANY NEW ORDINARY SHARES ARISING FROM THE EXERCISE OF OPTIONS GRANTED PURSUANT TO IDEAL JACOBS’ EMPLOYEE SHARE OPTION SCHEME NOT ALREADY HELD BY THE OFFEROR (“OFFER SHARES”) FOR A CASH CONSIDERATION OF RM0.23 PER OFFER SHARE (“OFFER”)

Independent Adviser

M&A SECURITIES SDN BHD (15017-H) (A Wholly-Owned Subsidiary of Insas Berhad)

(A Participating Organisation of Bursa Malaysia Securities Berhad)

This Independent Advice Circular is dated 15 March 2018

THIS INDEPENDENT ADVICE CIRCULAR (“IAC”) IS IMPORTANT AND REQUIRES YOUR IMMEDIATE ATTENTION. YOU SHOULD READ THIS IAC IN CONJUNCTION WITH THE OFFER DOCUMENT DATED 5 MARCH 2018 ISSUED BY KENANGA INVESTMENT BANK BERHAD ON BEHALF OF WIDAD BUSINESS GROUP SDN BHD (“OFFEROR”) WHICH HAS BEEN SENT TO YOU. If you are in any doubt as to the action to be taken in relation to the Offer (as defined herein), please consult your stockbroker, solicitor, bank manager, accountant or other professional advisers immediately. If you have sold or transferred all your Offer Shares (as defined herein), you should at once hand this IAC to the purchaser or stockbroker or agent through whom you effected the sale or transfer for onward transmission to the purchaser or transferee of such Offer Shares. Pursuant to Rule 11 of the Rules on Take-overs, Mergers and Compulsory Acquisitions, the Securities Commission Malaysia (“SC”) has notified that it has no further comments to the contents of this IAC. However, such notification shall not be taken to suggest that the SC agrees with our recommendation or assumes responsibility for the correctness of any statements made or opinions or reports expressed in IAC.

IDEAL JACOBS (MALAYSIA) CORPORATION BHD

(Company No. 857363-U) (Incorporated in Malaysia under the Companies Act, 1965)

INDEPENDENT ADVICE CIRCULAR TO THE HOLDERS OF THE OFFER SHARES IN RELATION TO THE UNCONDITIONAL MANDATORY TAKE-OVER OFFER

BY

WIDAD BUSINESS GROUP SDN BHD

(Company No. 602380-P) (Incorporated in Malaysia under the Companies Act, 1965)

THROUGH

KENANGA INVESTMENT BANK BERHAD

(Company No. 15678-H) (A Participating Organisation of Bursa Malaysia Securities Berhad)

TO ACQUIRE ALL THE REMAINING ORDINARY SHARES IN IDEAL JACOBS (MALAYSIA) CORPORATION BHD (“IDEAL JACOBS”) AS WELL AS ANY NEW ORDINARY SHARES ARISING FROM THE EXERCISE OF OPTIONS GRANTED PURSUANT TO IDEAL JACOBS’ EMPLOYEE SHARE OPTION SCHEME NOT ALREADY HELD BY THE OFFEROR (“OFFER SHARES”) FOR A CASH CONSIDERATION OF RM0.23 PER OFFER SHARE (“OFFER”)

Independent Adviser

M&A SECURITIES SDN BHD (15017-H) (A Wholly-Owned Subsidiary of Insas Berhad)

(A Participating Organisation of Bursa Malaysia Securities Berhad)

This Independent Advice Circular is dated 15 March 2018

THIS INDEPENDENT ADVICE CIRCULAR (“IAC”) IS IMPORTANT AND REQUIRES YOUR IMMEDIATE ATTENTION. YOU SHOULD READ THIS IAC IN CONJUNCTION WITH THE OFFER DOCUMENT DATED 5 MARCH 2018 ISSUED BY KENANGA INVESTMENT BANK BERHAD ON BEHALF OF WIDAD BUSINESS GROUP SDN BHD (“OFFEROR”) WHICH HAS BEEN SENT TO YOU. If you are in any doubt as to the action to be taken in relation to the Offer (as defined herein), please consult your stockbroker, solicitor, bank manager, accountant or other professional advisers immediately. If you have sold or transferred all your Offer Shares (as defined herein), you should at once hand this IAC to the purchaser or stockbroker or agent through whom you effected the sale or transfer for onward transmission to the purchaser or transferee of such Offer Shares. Pursuant to Rule 11 of the Rules on Take-overs, Mergers and Compulsory Acquisitions, the Securities Commission Malaysia (“SC”) has notified that it has no further comments to the contents of this IAC. However, such notification shall not be taken to suggest that the SC agrees with our recommendation or assumes responsibility for the correctness of any statements made or opinions or reports expressed in IAC.

IDEAL JACOBS (MALAYSIA) CORPORATION BHD

(Company No. 857363-U) (Incorporated in Malaysia under the Companies Act, 1965)

INDEPENDENT ADVICE CIRCULAR TO THE HOLDERS OF THE OFFER SHARES IN RELATION TO THE UNCONDITIONAL MANDATORY TAKE-OVER OFFER

BY

WIDAD BUSINESS GROUP SDN BHD

(Company No. 602380-P) (Incorporated in Malaysia under the Companies Act, 1965)

THROUGH

KENANGA INVESTMENT BANK BERHAD

(Company No. 15678-H) (A Participating Organisation of Bursa Malaysia Securities Berhad)

TO ACQUIRE ALL THE REMAINING ORDINARY SHARES IN IDEAL JACOBS (MALAYSIA) CORPORATION BHD (“IDEAL JACOBS”) AS WELL AS ANY NEW ORDINARY SHARES ARISING FROM THE EXERCISE OF OPTIONS GRANTED PURSUANT TO IDEAL JACOBS’ EMPLOYEE SHARE OPTION SCHEME NOT ALREADY HELD BY THE OFFEROR (“OFFER SHARES”) FOR A CASH CONSIDERATION OF RM0.23 PER OFFER SHARE (“OFFER”)

Independent Adviser

M&A SECURITIES SDN BHD (15017-H) (A Wholly-Owned Subsidiary of Insas Berhad)

(A Participating Organisation of Bursa Malaysia Securities Berhad)

This Independent Advice Circular is dated 15 March 2018

DEFINITIONS

ii

Unless the context requires otherwise, the following definitions shall apply throughout this IAC: Act : Companies Act, 2016

Accepting Holder(s) : Holder(s) who accepts the Offer

Acquisition

: Acquisition by Ideal Jacobs of the entire equity interest in Widad Builders for a total purchase consideration of RM520.0 million to be satisfied through a combination of cash and issuance of Consideration Shares

Acquisition LTD : 17 August 2017, being the last full trading day prior to the date of Acquisition SPA

Acquisition SPA

: Conditional sale and purchase agreement dated 18 August 2017 entered into between Ideal Jacobs and WBGSB for the Acquisition

Amendment : Amendment to Ideal Jacobs’ Memorandum of Association

AMLR : ACE Market Listing Requirements issued by Bursa Securities and includes any amendments from time to time

Bursa Depository : Bursa Malaysia Depository Sdn Bhd (165570-W)

Bursa Securities : Bursa Malaysia Securities Berhad (635998-W)

CAGR : Compounded annual growth rate

Closing Date : First Closing Date, or in the event the Offer is revised or extended in accordance with the Rules and the terms and conditions of the Offer Document, such other revised or extended closing date as the Offeror may decide and as may be announced by Kenanga IB on behalf of the Offeror, no later than 2 days before the Closing Date

CMSA : Capital Markets and Services Act, 2007

Consideration Issue Price : Issue price of RM0.23 per Consideration Share

Consideration Shares : 1,782,608,695 new IJ Shares to be issued at the Consideration Issue Price pursuant to the Acquisition

Dato’ Rizal : Dato’ Mohd Rizal Bin Mohd Jaafar

DCF : Discounted cash flow

Disposal

: Disposal by Ideal Jacobs of Ideal Jacobs (HK) Corporation Ltd, Ideal Jacobs (Xiamen) Corporation, Xiamen Ideal Jacobs International Ltd Company and Suzhou Ideal Jacobs Corporation for a cash consideration of RM28.0 million

Disposal SPA

: Conditional sale and purchase agreement dated 18 August 2017 entered into between Ideal Jacobs and Oriental Dragon Incorporation Limited for the Disposal

Dissenting Shareholder : A holder of the Offer Shares who has not accepted the Offer and/or failed or refused to transfer the Offer Shares to the Offeror in accordance with the terms and conditions of the Offer Document

i

DEFINITIONS (Cont’d)

iii

Disposal Subsidiaries : Ideal Jacobs (HK) Corporation Ltd, Ideal Jacobs (Xiamen) Corporation, Xiamen Ideal Jacobs International Ltd Company and Suzhou Ideal Jacobs Corporation

Distribution : Any declaration or payment of dividend and/or any other distribution by the Offeree

ESOS Options : Options granted pursuant to Ideal Jacobs’ employee share option scheme. As at the LPD, 1,150,075 ESOS Options are outstanding in Ideal Jacobs

FBM KLCI : FTSE Bursa Malaysia KLCI Index

FCFE : Free cash flows to equity

First Closing Date : 5.00 p.m. on 26 March 2018, being 21 days from the Posting Date

Form of Acceptance and Transfer

: Form of acceptance and transfer for the Offer enclosed with the Offer Document

FPE

: Financial period ended/ending, as the case may be

Free Warrants Issue : Issuance of free Warrants on the basis of 1 Warrant for every 5 existing IJ Shares held upon completion of the Acquisition, Disposal and Placement at an entitlement date and exercise price to be determined later

FYE : Financial year ended/ending, as the case may be

HOA : Non-binding heads of agreement dated 5 June 2017 entered into between Ideal Jacobs and WBGSB for the Acquisition with an exclusivity period of 45 days, which was extended for an additional 30 days as supplemented by the letter dated 20 July 2017

Holders : Holders of the Offer Shares

IAC : The independent advice circular dated 15 March 2018 in relation to the Offer

IAL : The independent advice letter dated 15 March 2018 issued by M&A Securities as attached in Part B of this IAC

IFM

: Integrated facilities management

Independent Adviser or M&A Securities

: M&A Securities Sdn Bhd, the Independent Adviser appointed by the Board to advise the IJ Board and Holders on the Offer

Ideal Jacobs or Offeree : Ideal Jacobs (Malaysia) Corporation Bhd (857363-U)

IJ Board or Board

: Board of Directors of Ideal Jacobs

IJ Group or Group

: Ideal Jacobs and its subsidiaries, collectively

IJ Share(s) or Share(s)

: Ordinary shares in Ideal Jacobs

Joint Ultimate Offerors : Collectively, Tan Sri Ikmal and Puan Sri Jamilah

Kenanga IB : Kenanga Investment Bank Berhad (15678-H) ii

DEFINITIONS (Cont’d)

iv

LPD : 8 March 2018, being the latest practicable date which is not more than 7 days before the date of this IAC

Market Day : A day on which Bursa Securities is open for trading in securities

New IJ Group : Ideal Jacobs and its subsidiaries, collectively after the completion of the Acquisition, Placement and Disposal

Notice : Notice of the Offer dated 12 February 2018, served on the Board by Kenanga IB on behalf of the Offeror

Notice LTD : 9 February 2018, being the last full trading day prior to the serving of the Notice

Offer : Unconditional mandatory take-over offer by the Offeror through Kenanga IB to acquire the Offer Shares at the Offer Price in accordance with the terms and conditions of the Offer Document

Offeror or WBGSB : Widad Business Group Sdn Bhd (602380-P)

Offer Document : The document dated 5 March 2018 together with the Form of Acceptance and Transfer issued by Kenanga IB on behalf of the Offeror, which sets out the details of the Offer as well as procedures for acceptance of the Offer and method of settlement of the Offer

Offer Document LPD : 1 March 2018, being the latest practicable date which is not more than 7 days before the date of the Offer Document

Offer Period : Period commencing from 18 August 2017, being the date of Acquisition SPA, until the earlier of either (i) the Closing Date; or (ii) the date the Offer lapses or is withdrawn with the consent of the SC

Offer Price : Cash offer price of RM0.23 per Offer Share

Offer Share(s) : All the remaining IJ Shares that are not already held by the Offeror and Joint Ultimate Offerors as well as any new IJ Shares that may be issued prior to the Closing Date pursuant to the exercise of the ESOS Options. As at the LPD, the Offer Shares comprise 136,124,275 IJ Shares (excluding 1,150,075 new IJ Shares that may be issued from the potential exercise of the ESOS Options), representing 99.47% of Ideal Jacobs’ total number of issued shares as at the LPD

Official List : A list specifying all securities which have been admitted for listing on Bursa Securities and not removed

Placement : Private placement of up to 534,032,115 new IJ Shares representing 25% of the enlarged total issued share capital of Ideal Jacobs upon completion of the Acquisition at an issue price to be determined later

Posting Date : 5 March 2018, being the date of posting of the Offer Document

Proposals

: Collectively, the Acquisition, Disposal, Placement, Free Warrants Issue and Amendment

Puan Sri Jamilah : Puan Sri Jamilah Binti Mahamad Isa

iii

DEFINITIONS (Cont’d)

v

Public Spread Requirement

: The requirements pursuant to paragraph 8.02(1) of the AMLR, whereby a listed issuer must ensure that at least 25% of its total listed shares (excluding treasury shares) are held by public shareholders to ensure its continued listing on the ACE Market of Bursa Securities

Rules : Rules on Take-overs, Mergers and Compulsory Acquisitions issued by the SC

SC : Securities Commission Malaysia

SOPV : Sum-of-parts valuation

Substantial Shareholders’ Undertakings

: Irrevocable undertakings by Ideal Jacobs’ existing substantial shareholders, namely Andrew Conrad Jacobs and Dato’ Meng Bin not to participate in or accept the Offer in respect of the IJ Shares held directly and indirectly by them, which collectively amount to 41.28% of Ideal Jacobs’ issued share capital as at the Offer Document LPD, made through their respective undertaking letters dated 15 December 2017

Tan Sri Ikmal : Tan Sri Muhammad Ikmal Opat Bin Abdullah

VWAMP : Volume weighted average market price

Warrants

: Up to 490,928,392 free warrants to be issued pursuant to the Free Warrants Issue

WBGSB group of companies

: WBGSB and its subsidiaries and associated companies, collectively

Widad Builders : Widad Builders Sdn Bhd (536572-D)

Widad Builders Group : Widad Builders and its subsidiaries, collectively

CURRENCIES

CNY : Chinese Yuan Renminbi

RM and sen : Ringgit Malaysia and sen respectively

Words importing the singular shall, where applicable, include the plural and vice versa. Words denoting the masculine gender shall, where applicable, include the feminine and neuter genders and vice versa. References to persons shall include corporations. Unless otherwise indicated, all references to dates and times in this IAC refer to Malaysian dates and times. Where a period specified in the Rules, as appearing in this IAC, ends on a day which is not a Market Day, the period is extended until the next Market Day. All references to “you” or “Holder” in this IAC are to the holder of the Offer Shares, being the person to whom the Offer is being made. All references to “we”, “us” or “our” in this IAC, save for the Letter from the IJ Board, are to M&A Securities, the Independent Adviser for the Offer. Any reference in this IAC to any enactment is a reference to that enactment for the time being amended or re-enacted. Any discrepancies in the tables included in this IAC between the amounts listed, actual figures and the totals thereof are due to rounding.

DEFINITIONS (Cont’d)

v

Public Spread Requirement

: The requirements pursuant to paragraph 8.02(1) of the AMLR, whereby a listed issuer must ensure that at least 25% of its total listed shares (excluding treasury shares) are held by public shareholders to ensure its continued listing on the ACE Market of Bursa Securities

Rules : Rules on Take-overs, Mergers and Compulsory Acquisitions issued by the SC

SC : Securities Commission Malaysia

SOPV : Sum-of-parts valuation

Substantial Shareholders’ Undertakings

: Irrevocable undertakings by Ideal Jacobs’ existing substantial shareholders, namely Andrew Conrad Jacobs and Dato’ Meng Bin not to participate in or accept the Offer in respect of the IJ Shares held directly and indirectly by them, which collectively amount to 41.28% of Ideal Jacobs’ issued share capital as at the Offer Document LPD, made through their respective undertaking letters dated 15 December 2017

Tan Sri Ikmal : Tan Sri Muhammad Ikmal Opat Bin Abdullah

VWAMP : Volume weighted average market price

Warrants

: Up to 490,928,392 free warrants to be issued pursuant to the Free Warrants Issue

WBGSB group of companies

: WBGSB and its subsidiaries and associated companies, collectively

Widad Builders : Widad Builders Sdn Bhd (536572-D)

Widad Builders Group : Widad Builders and its subsidiaries, collectively

CURRENCIES

CNY : Chinese Yuan Renminbi

RM and sen : Ringgit Malaysia and sen respectively

Words importing the singular shall, where applicable, include the plural and vice versa. Words denoting the masculine gender shall, where applicable, include the feminine and neuter genders and vice versa. References to persons shall include corporations. Unless otherwise indicated, all references to dates and times in this IAC refer to Malaysian dates and times. Where a period specified in the Rules, as appearing in this IAC, ends on a day which is not a Market Day, the period is extended until the next Market Day. All references to “you” or “Holder” in this IAC are to the holder of the Offer Shares, being the person to whom the Offer is being made. All references to “we”, “us” or “our” in this IAC, save for the Letter from the IJ Board, are to M&A Securities, the Independent Adviser for the Offer. Any reference in this IAC to any enactment is a reference to that enactment for the time being amended or re-enacted. Any discrepancies in the tables included in this IAC between the amounts listed, actual figures and the totals thereof are due to rounding.

DEFINITIONS (Cont’d)

v

Public Spread Requirement

: The requirements pursuant to paragraph 8.02(1) of the AMLR, whereby a listed issuer must ensure that at least 25% of its total listed shares (excluding treasury shares) are held by public shareholders to ensure its continued listing on the ACE Market of Bursa Securities

Rules : Rules on Take-overs, Mergers and Compulsory Acquisitions issued by the SC

SC : Securities Commission Malaysia

SOPV : Sum-of-parts valuation

Substantial Shareholders’ Undertakings

: Irrevocable undertakings by Ideal Jacobs’ existing substantial shareholders, namely Andrew Conrad Jacobs and Dato’ Meng Bin not to participate in or accept the Offer in respect of the IJ Shares held directly and indirectly by them, which collectively amount to 41.28% of Ideal Jacobs’ issued share capital as at the Offer Document LPD, made through their respective undertaking letters dated 15 December 2017

Tan Sri Ikmal : Tan Sri Muhammad Ikmal Opat Bin Abdullah

VWAMP : Volume weighted average market price

Warrants

: Up to 490,928,392 free warrants to be issued pursuant to the Free Warrants Issue

WBGSB group of companies

: WBGSB and its subsidiaries and associated companies, collectively

Widad Builders : Widad Builders Sdn Bhd (536572-D)

Widad Builders Group : Widad Builders and its subsidiaries, collectively

CURRENCIES

CNY : Chinese Yuan Renminbi

RM and sen : Ringgit Malaysia and sen respectively

Words importing the singular shall, where applicable, include the plural and vice versa. Words denoting the masculine gender shall, where applicable, include the feminine and neuter genders and vice versa. References to persons shall include corporations. Unless otherwise indicated, all references to dates and times in this IAC refer to Malaysian dates and times. Where a period specified in the Rules, as appearing in this IAC, ends on a day which is not a Market Day, the period is extended until the next Market Day. All references to “you” or “Holder” in this IAC are to the holder of the Offer Shares, being the person to whom the Offer is being made. All references to “we”, “us” or “our” in this IAC, save for the Letter from the IJ Board, are to M&A Securities, the Independent Adviser for the Offer. Any reference in this IAC to any enactment is a reference to that enactment for the time being amended or re-enacted. Any discrepancies in the tables included in this IAC between the amounts listed, actual figures and the totals thereof are due to rounding.

DEFINITIONS (Cont’d)

v

Public Spread Requirement

: The requirements pursuant to paragraph 8.02(1) of the AMLR, whereby a listed issuer must ensure that at least 25% of its total listed shares (excluding treasury shares) are held by public shareholders to ensure its continued listing on the ACE Market of Bursa Securities

Rules : Rules on Take-overs, Mergers and Compulsory Acquisitions issued by the SC

SC : Securities Commission Malaysia

SOPV : Sum-of-parts valuation

Substantial Shareholders’ Undertakings

: Irrevocable undertakings by Ideal Jacobs’ existing substantial shareholders, namely Andrew Conrad Jacobs and Dato’ Meng Bin not to participate in or accept the Offer in respect of the IJ Shares held directly and indirectly by them, which collectively amount to 41.28% of Ideal Jacobs’ issued share capital as at the Offer Document LPD, made through their respective undertaking letters dated 15 December 2017

Tan Sri Ikmal : Tan Sri Muhammad Ikmal Opat Bin Abdullah

VWAMP : Volume weighted average market price

Warrants

: Up to 490,928,392 free warrants to be issued pursuant to the Free Warrants Issue

WBGSB group of companies

: WBGSB and its subsidiaries and associated companies, collectively

Widad Builders : Widad Builders Sdn Bhd (536572-D)

Widad Builders Group : Widad Builders and its subsidiaries, collectively

CURRENCIES

CNY : Chinese Yuan Renminbi

RM and sen : Ringgit Malaysia and sen respectively

Words importing the singular shall, where applicable, include the plural and vice versa. Words denoting the masculine gender shall, where applicable, include the feminine and neuter genders and vice versa. References to persons shall include corporations. Unless otherwise indicated, all references to dates and times in this IAC refer to Malaysian dates and times. Where a period specified in the Rules, as appearing in this IAC, ends on a day which is not a Market Day, the period is extended until the next Market Day. All references to “you” or “Holder” in this IAC are to the holder of the Offer Shares, being the person to whom the Offer is being made. All references to “we”, “us” or “our” in this IAC, save for the Letter from the IJ Board, are to M&A Securities, the Independent Adviser for the Offer. Any reference in this IAC to any enactment is a reference to that enactment for the time being amended or re-enacted. Any discrepancies in the tables included in this IAC between the amounts listed, actual figures and the totals thereof are due to rounding.

DEFINITIONS (Cont’d)

v

Public Spread Requirement

: The requirements pursuant to paragraph 8.02(1) of the AMLR, whereby a listed issuer must ensure that at least 25% of its total listed shares (excluding treasury shares) are held by public shareholders to ensure its continued listing on the ACE Market of Bursa Securities

Rules : Rules on Take-overs, Mergers and Compulsory Acquisitions issued by the SC

SC : Securities Commission Malaysia

SOPV : Sum-of-parts valuation

Substantial Shareholders’ Undertakings

: Irrevocable undertakings by Ideal Jacobs’ existing substantial shareholders, namely Andrew Conrad Jacobs and Dato’ Meng Bin not to participate in or accept the Offer in respect of the IJ Shares held directly and indirectly by them, which collectively amount to 41.28% of Ideal Jacobs’ issued share capital as at the Offer Document LPD, made through their respective undertaking letters dated 15 December 2017

Tan Sri Ikmal : Tan Sri Muhammad Ikmal Opat Bin Abdullah

VWAMP : Volume weighted average market price

Warrants

: Up to 490,928,392 free warrants to be issued pursuant to the Free Warrants Issue

WBGSB group of companies

: WBGSB and its subsidiaries and associated companies, collectively

Widad Builders : Widad Builders Sdn Bhd (536572-D)

Widad Builders Group : Widad Builders and its subsidiaries, collectively

CURRENCIES

CNY : Chinese Yuan Renminbi

RM and sen : Ringgit Malaysia and sen respectively

Words importing the singular shall, where applicable, include the plural and vice versa. Words denoting the masculine gender shall, where applicable, include the feminine and neuter genders and vice versa. References to persons shall include corporations. Unless otherwise indicated, all references to dates and times in this IAC refer to Malaysian dates and times. Where a period specified in the Rules, as appearing in this IAC, ends on a day which is not a Market Day, the period is extended until the next Market Day. All references to “you” or “Holder” in this IAC are to the holder of the Offer Shares, being the person to whom the Offer is being made. All references to “we”, “us” or “our” in this IAC, save for the Letter from the IJ Board, are to M&A Securities, the Independent Adviser for the Offer. Any reference in this IAC to any enactment is a reference to that enactment for the time being amended or re-enacted. Any discrepancies in the tables included in this IAC between the amounts listed, actual figures and the totals thereof are due to rounding.

DEFINITIONS (Cont’d)

v

Public Spread Requirement

: The requirements pursuant to paragraph 8.02(1) of the AMLR, whereby a listed issuer must ensure that at least 25% of its total listed shares (excluding treasury shares) are held by public shareholders to ensure its continued listing on the ACE Market of Bursa Securities

Rules : Rules on Take-overs, Mergers and Compulsory Acquisitions issued by the SC

SC : Securities Commission Malaysia

SOPV : Sum-of-parts valuation

Substantial Shareholders’ Undertakings

: Irrevocable undertakings by Ideal Jacobs’ existing substantial shareholders, namely Andrew Conrad Jacobs and Dato’ Meng Bin not to participate in or accept the Offer in respect of the IJ Shares held directly and indirectly by them, which collectively amount to 41.28% of Ideal Jacobs’ issued share capital as at the Offer Document LPD, made through their respective undertaking letters dated 15 December 2017

Tan Sri Ikmal : Tan Sri Muhammad Ikmal Opat Bin Abdullah

VWAMP : Volume weighted average market price

Warrants

: Up to 490,928,392 free warrants to be issued pursuant to the Free Warrants Issue

WBGSB group of companies

: WBGSB and its subsidiaries and associated companies, collectively

Widad Builders : Widad Builders Sdn Bhd (536572-D)

Widad Builders Group : Widad Builders and its subsidiaries, collectively

CURRENCIES

CNY : Chinese Yuan Renminbi

RM and sen : Ringgit Malaysia and sen respectively

Words importing the singular shall, where applicable, include the plural and vice versa. Words denoting the masculine gender shall, where applicable, include the feminine and neuter genders and vice versa. References to persons shall include corporations. Unless otherwise indicated, all references to dates and times in this IAC refer to Malaysian dates and times. Where a period specified in the Rules, as appearing in this IAC, ends on a day which is not a Market Day, the period is extended until the next Market Day. All references to “you” or “Holder” in this IAC are to the holder of the Offer Shares, being the person to whom the Offer is being made. All references to “we”, “us” or “our” in this IAC, save for the Letter from the IJ Board, are to M&A Securities, the Independent Adviser for the Offer. Any reference in this IAC to any enactment is a reference to that enactment for the time being amended or re-enacted. Any discrepancies in the tables included in this IAC between the amounts listed, actual figures and the totals thereof are due to rounding.

DEFINITIONS (Cont’d)

v

Public Spread Requirement

: The requirements pursuant to paragraph 8.02(1) of the AMLR, whereby a listed issuer must ensure that at least 25% of its total listed shares (excluding treasury shares) are held by public shareholders to ensure its continued listing on the ACE Market of Bursa Securities

Rules : Rules on Take-overs, Mergers and Compulsory Acquisitions issued by the SC

SC : Securities Commission Malaysia

SOPV : Sum-of-parts valuation

Substantial Shareholders’ Undertakings

: Irrevocable undertakings by Ideal Jacobs’ existing substantial shareholders, namely Andrew Conrad Jacobs and Dato’ Meng Bin not to participate in or accept the Offer in respect of the IJ Shares held directly and indirectly by them, which collectively amount to 41.28% of Ideal Jacobs’ issued share capital as at the Offer Document LPD, made through their respective undertaking letters dated 15 December 2017

Tan Sri Ikmal : Tan Sri Muhammad Ikmal Opat Bin Abdullah

VWAMP : Volume weighted average market price

Warrants

: Up to 490,928,392 free warrants to be issued pursuant to the Free Warrants Issue

WBGSB group of companies

: WBGSB and its subsidiaries and associated companies, collectively

Widad Builders : Widad Builders Sdn Bhd (536572-D)

Widad Builders Group : Widad Builders and its subsidiaries, collectively

CURRENCIES

CNY : Chinese Yuan Renminbi

RM and sen : Ringgit Malaysia and sen respectively

Words importing the singular shall, where applicable, include the plural and vice versa. Words denoting the masculine gender shall, where applicable, include the feminine and neuter genders and vice versa. References to persons shall include corporations. Unless otherwise indicated, all references to dates and times in this IAC refer to Malaysian dates and times. Where a period specified in the Rules, as appearing in this IAC, ends on a day which is not a Market Day, the period is extended until the next Market Day. All references to “you” or “Holder” in this IAC are to the holder of the Offer Shares, being the person to whom the Offer is being made. All references to “we”, “us” or “our” in this IAC, save for the Letter from the IJ Board, are to M&A Securities, the Independent Adviser for the Offer. Any reference in this IAC to any enactment is a reference to that enactment for the time being amended or re-enacted. Any discrepancies in the tables included in this IAC between the amounts listed, actual figures and the totals thereof are due to rounding.

iv

TABLE OF CONTENTS

vi

PAGE EXECUTIVE SUMMARY 1 PART A: LETTER FROM THE BOARD 1. INTRODUCTION 7 2. SALIENT TERMS AND CONDITIONS OF THE OFFER 9 3. DETAILS OF ACCEPTANCES 9 4. DIRECTORS’ VIEWS 9 5. INDEPENDENT ADVICE LETTER 11 6. DISCLOSURE OF DIRECTORS’ INTEREST 11 7. DIRECTORS’ RESPONSIBILITY STATEMENT 11 8. DIRECTORS’ RECOMMENDATION 12 PART B: INDEPENDENT ADVICE LETTER FROM M&A SECURITIES 1. INTRODUCTION 14 2. SALIENT TERMS AND CONDITIONS OF THE OFFER 15 3. DETAILS OF ACCEPTANCES 15 4. SCOPE AND LIMITATIONS TO THE EVALUATION OF THE OFFER 16 5. EVALUATION OF THE OFFER 17 6. FAIRNESS EVALUATION OF THE OFFER 18 7. REASONABLENESS EVALUATION OF THE OFFER 28 8. RATIONALE FOR THE OFFER AND FUTURE PLANS FOR IDEAL JACOBS AND

ITS EMPLOYEES 30

9. FURTHER INFORMATION 32 10. CONCLUSION AND RECOMMENDATION 32 APPENDICES I INFORMATION ON IDEAL JACOBS 35 II FURTHER INFORMATION 44

v

EXECUTIVE SUMMARY

EXECUTIVE SUMMARY

1

THIS EXECUTIVE SUMMARY HIGHLIGHTS ONLY THE PERTINENT INFORMATION OF THE OFFER. WE ADVISE HOLDERS TO READ CAREFULLY THE CONTENTS OF THIS IAC FOR FURTHER INFORMATION AND RECOMMENDATIONS FROM THE DIRECTORS AND M&A SECURITIES (THE INDEPENDENT ADVISER). THIS IAC SHOULD ALSO BE READ TOGETHER WITH THE OFFER DOCUMENT ISSUED BY THE OFFEROR. 1. INTRODUCTION

On 5 June 2017, Ideal Jacobs entered into the HOA with WBGSB for the Acquisition. On 18 August 2017, Ideal Jacobs and WBGSB entered into the Acquisition SPA. Under the Acquisition SPA, the purchase consideration of RM520 million for the Acquisition is to be satisfied through cash (RM110 million) and the issuance of the Consideration Shares at the Consideration Issue Price (RM410 million). In conjunction with the Acquisition, Ideal Jacobs is also undertaking the other Proposals, which comprise: (a) disposal of Ideal Jacobs (HK) Corporation Ltd, Ideal Jacobs (Xiamen) Corporation,

Xiamen Ideal Jacobs International Ltd Company and Suzhou Ideal Jacobs Corporation for a cash consideration of RM28.0 million, that is, the Disposal;

(b) private placement of up to 534,032,115 new IJ Shares representing 25% of the enlarged total issued share capital of Ideal Jacobs upon completion of the Acquisition at an issue price to be determined later, that is, the Placement;

(c) issuance of free warrants on the basis of 1 warrant for every 5 existing IJ Shares held upon completion of the Acquisition, Disposal and Placement at an entitlement date to be determined later, that is, the Free Warrants Issue; and

(d) amendment to its Memorandum of Association, that is, the Amendment.

Ideal Jacobs’ shareholders had approved the Proposals at its extraordinary general meeting held on 29 January 2018. Please refer to Ideal Jacobs’ circular to shareholders dated 4 January 2018 for further information on the Proposals.

Upon the issuance of the Consideration Shares and before the Placement, WBGSB's shareholding in Ideal Jacobs will increase from nil to 92.87% and the collective shareholdings of the Offeror and Joint Ultimate Offerors will increase from 0.53% to 92.91%.

Therefore, the Offeror is obligated to extend the Offer to acquire the Offer Shares that are not already held by the Offeror and Joint Ultimate Offerors pursuant to Section 218(2) of the CMSA and Paragraph 4.01(a) of the Rules at a cash consideration of RM0.23 per Offer Share, which is equal to the Consideration Issue Price. On 12 February 2018, the Acquisition SPA became unconditional. On even date, Kenanga IB, on the Offeror’s behalf, served the Notice on the IJ Board informing them of the Offeror’s obligation to undertake the Offer. On the same day, the Offeree announced the receipt of the Notice, a copy of which was sent to you on 14 February 2018. On 14 February 2018, in accordance with Paragraph 3.06 of the Rules, the Offeree announced the appointment of M&A Securities as the Independent Adviser to advise the IJ Board and the Holders on the fairness and reasonableness of the Offer.

1

EXECUTIVE SUMMARY (Cont’d)

2

The Joint Ultimate Offerors for the Offer are Tan Sri Ikmal and Puan Sri Jamilah. There are no persons acting in concert (as defined in Section 216 of the CMSA) with the Offeror pursuant to the Offer. As at the LPD, the Offeror and Joint Ultimate Offerors: (a) have not received any irrevocable undertaking from any Holder to accept the Offer;

and

(b) have not received any other irrevocable undertaking from any Holder to reject the Offer except for the Substantial Shareholders’ Undertakings.

2. SALIENT TERMS AND CONDITIONS OF THE OFFER

The salient terms and conditions of the Offer are set out below: 2.1 Consideration for the Offer

The Offeror will pay a cash consideration of RM0.23 per Offer Share to Accepting Holders. If you are entitled to retain any Distribution that Ideal Jacobs may declare, make or pay on or after the date of the Notice but before the Closing Date, the Offeror will reduce the Offer Price by an amount equivalent to the net Distribution per Offer Share that you are entitled to retain. As at the LPD, Ideal Jacobs has not declared any Distribution. You may accept the Offer for all or part of your Offer Shares. The Offeror will round down the cash consideration payable to an Accepting Holder to the nearest whole sen. The Offeror will not pay fractions of a sen, if any, to Accepting Holders.

2.2 Condition of the Offer The Offer is not conditional upon any minimum acceptance level as the Offeror and Joint Ultimate Offerors will collectively hold more than 50% of Ideal Jacobs’ voting shares upon the issuance of the Consideration Shares.

2.3 Duration of the Offer

The Offer will remain open for acceptances until 5:00 p.m. on 26 March 2018, that is, the First Closing Date unless extended or revised by the Offeror in accordance with the Rules.

Please refer to Section 2 of Appendix I of the Offer Document for further details on the duration of the Offer.

2.4 Method of settlement

The Offeror will settle the consideration for the Offer Shares in the form of cheque, banker’s draft or cashier’s order which will be despatched to Accepting Holders or their designated agents by ordinary mail within 10 days from the date of receipt of the valid acceptances. Please refer to Appendix I of the Offer Document for the full terms and conditions of the Offer and Appendix II of the Offer Document for the procedures for acceptance and method of settlement of the Offer.

2

EXECUTIVE SUMMARY (Cont’d)

3

3. DETAILS OF ACCEPTANCES

As disclosed in the Offer Document, as at the Offer Document LPD, the Offeror has received irrevocable undertakings from the existing substantial shareholders of Ideal Jacobs, namely Andrew Conrad Jacobs and Dato’ Meng Bin, that they will not accept the Offer in respect of shares held directly and indirectly by them, which amounts in aggregate to 41.28% of Ideal Jacobs’ issued share capital as at the Offer Document LPD. Save as disclosed above, the Offeror has not received any irrevocable undertakings from any Holder to accept or reject the Offer and/or acceptances of the Offer from any Holder. As at the LPD, there is no announcement made by Kenanga IB, on behalf of the Offeror of any acceptance of the Offer Shares.

4. EVALUATION OF THE OFFER

In arriving at its conclusion and recommendation, M&A Securities has assessed the fairness and reasonableness of the Offer in accordance with Paragraphs 1 to 6 under Schedule 2: Part III of the Rules, where the term “fair and reasonable” should generally be analysed as 2 distinct criteria, i.e. whether the offer is “fair” and whether the offer is “reasonable”, rather than as composite term.

4.1 Fairness evaluation of the Offer

(a) Valuation of the entire equity interest in Ideal Jacobs

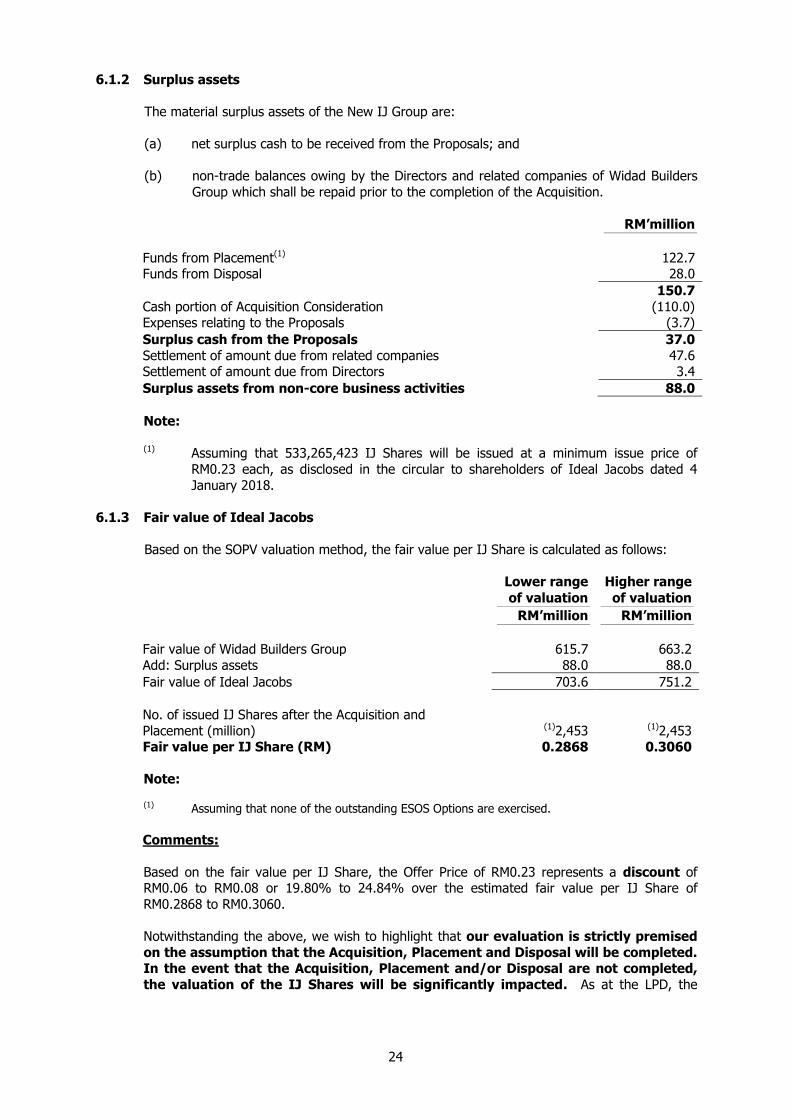

Upon the completion of the Acquisition and Disposal, Ideal Jacobs will assume the entire business of the Widad Builders Group and will no longer continue with its existing manufacturing, fabrication and trading businesses. Therefore, in arriving at the fair value of IJ Shares, M&A Securities has adopted the SOPV model as the sole valuation method, which comprises a DCF valuation of the FCFE to be generated from the core business activities of the Widad Builders Group, and adding the value of assets which are not utilised in the core business activities of the Widad Builders Group. M&A Securities views that the SOPV model to be the most appropriate method to estimate the value of the Shares for the reasons as set out in Section 6 in Part B of this IAC. Based on the SOPV method, M&A Securities has derived an estimated fair value for the entire equity interest in Ideal Jacobs of approximately RM703.6 million to RM751.2 million or a fair value per IJ Share of between RM0.2868 to RM0.3060. Further information on the assessment on the valuation of the IJ Shares is set out in Section 6.1 in Part B of this IAC.

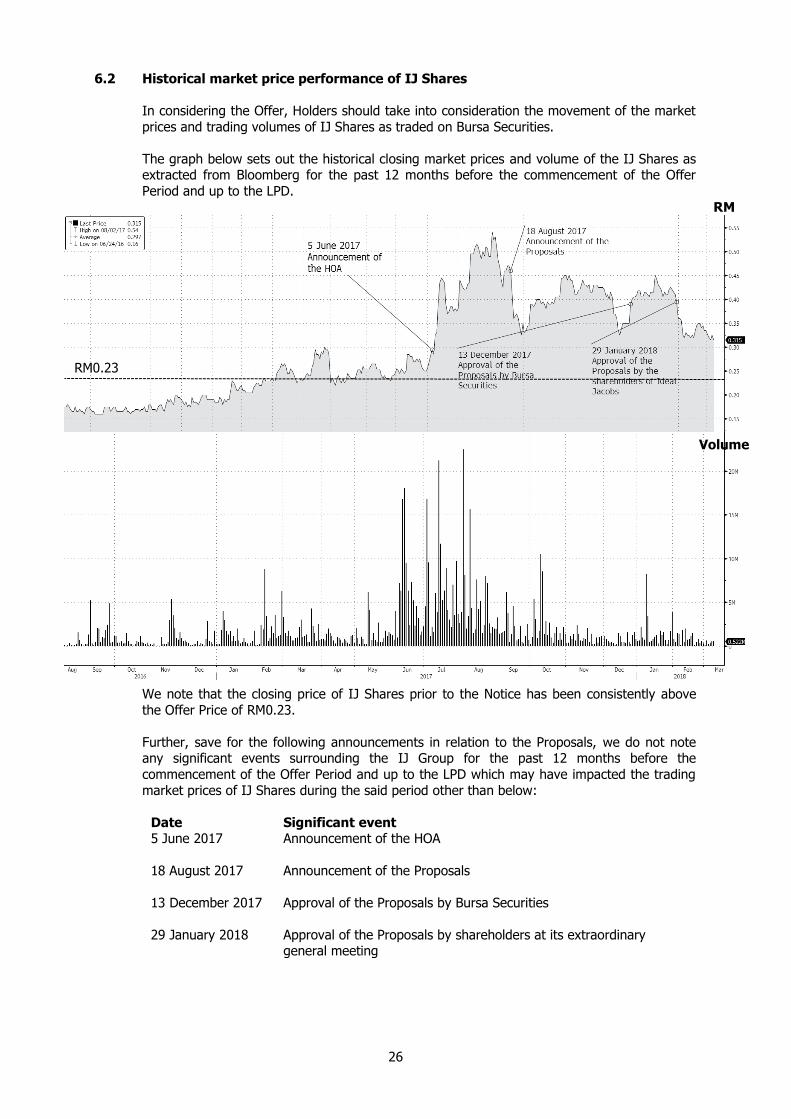

(b) Historical market price performance of IJ Shares

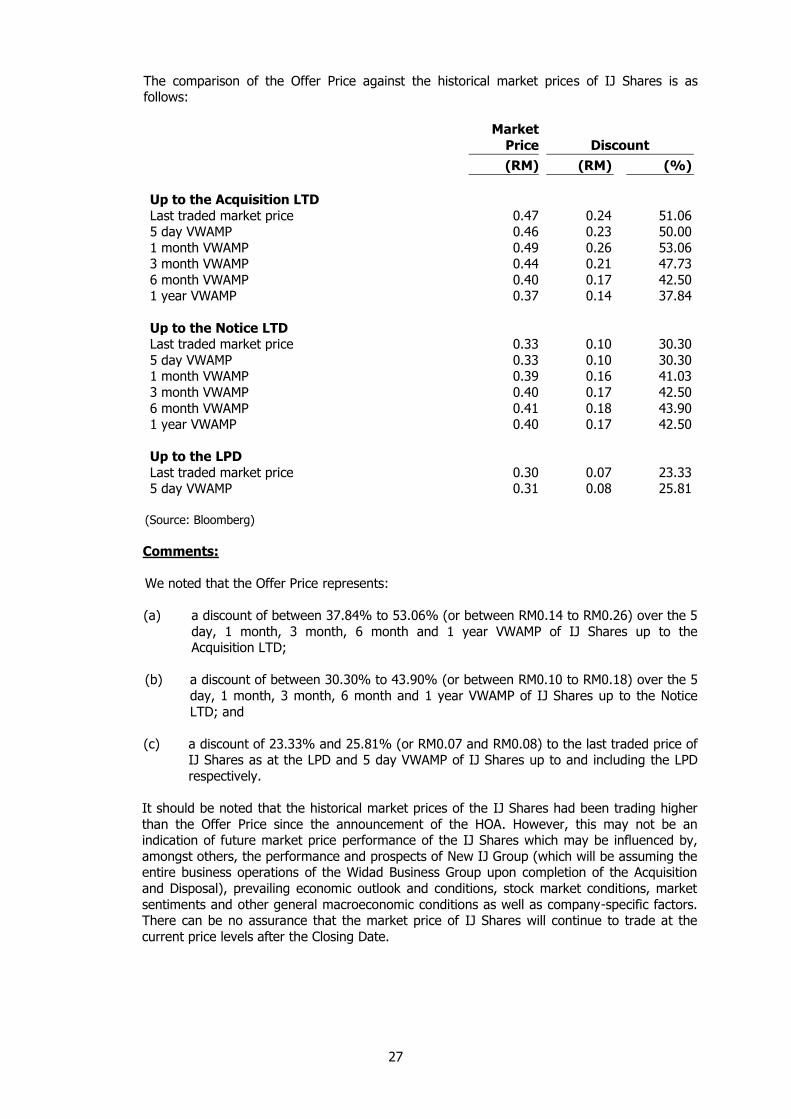

The Offer Price represents: (i) a discount of between 37.84% to 53.06% (or between RM0.14 to RM0.26)

over the 5 day, 1 month, 3 month, 6 month and 1 year VWAMP of IJ Shares up to the Acquisition LTD;

(ii) a discount of between 30.30% to 43.90% (or between RM0.10 to RM0.18)

over the 5 day, 1 month, 3 month, 6 month and 1 year VWAMP of IJ Shares

EXECUTIVE SUMMARY (Cont’d)

3

3. DETAILS OF ACCEPTANCES

As disclosed in the Offer Document, as at the Offer Document LPD, the Offeror has received irrevocable undertakings from the existing substantial shareholders of Ideal Jacobs, namely Andrew Conrad Jacobs and Dato’ Meng Bin, that they will not accept the Offer in respect of shares held directly and indirectly by them, which amounts in aggregate to 41.28% of Ideal Jacobs’ issued share capital as at the Offer Document LPD. Save as disclosed above, the Offeror has not received any irrevocable undertakings from any Holder to accept or reject the Offer and/or acceptances of the Offer from any Holder. As at the LPD, there is no announcement made by Kenanga IB, on behalf of the Offeror of any acceptance of the Offer Shares.

4. EVALUATION OF THE OFFER

In arriving at its conclusion and recommendation, M&A Securities has assessed the fairness and reasonableness of the Offer in accordance with Paragraphs 1 to 6 under Schedule 2: Part III of the Rules, where the term “fair and reasonable” should generally be analysed as 2 distinct criteria, i.e. whether the offer is “fair” and whether the offer is “reasonable”, rather than as composite term.

4.1 Fairness evaluation of the Offer

(a) Valuation of the entire equity interest in Ideal Jacobs

Upon the completion of the Acquisition and Disposal, Ideal Jacobs will assume the entire business of the Widad Builders Group and will no longer continue with its existing manufacturing, fabrication and trading businesses. Therefore, in arriving at the fair value of IJ Shares, M&A Securities has adopted the SOPV model as the sole valuation method, which comprises a DCF valuation of the FCFE to be generated from the core business activities of the Widad Builders Group, and adding the value of assets which are not utilised in the core business activities of the Widad Builders Group. M&A Securities views that the SOPV model to be the most appropriate method to estimate the value of the Shares for the reasons as set out in Section 6 in Part B of this IAC. Based on the SOPV method, M&A Securities has derived an estimated fair value for the entire equity interest in Ideal Jacobs of approximately RM703.6 million to RM751.2 million or a fair value per IJ Share of between RM0.2868 to RM0.3060. Further information on the assessment on the valuation of the IJ Shares is set out in Section 6.1 in Part B of this IAC.

(b) Historical market price performance of IJ Shares

The Offer Price represents: (i) a discount of between 37.84% to 53.06% (or between RM0.14 to RM0.26)

over the 5 day, 1 month, 3 month, 6 month and 1 year VWAMP of IJ Shares up to the Acquisition LTD;

(ii) a discount of between 30.30% to 43.90% (or between RM0.10 to RM0.18)

over the 5 day, 1 month, 3 month, 6 month and 1 year VWAMP of IJ Shares

EXECUTIVE SUMMARY (Cont’d)

3

3. DETAILS OF ACCEPTANCES

As disclosed in the Offer Document, as at the Offer Document LPD, the Offeror has received irrevocable undertakings from the existing substantial shareholders of Ideal Jacobs, namely Andrew Conrad Jacobs and Dato’ Meng Bin, that they will not accept the Offer in respect of shares held directly and indirectly by them, which amounts in aggregate to 41.28% of Ideal Jacobs’ issued share capital as at the Offer Document LPD. Save as disclosed above, the Offeror has not received any irrevocable undertakings from any Holder to accept or reject the Offer and/or acceptances of the Offer from any Holder. As at the LPD, there is no announcement made by Kenanga IB, on behalf of the Offeror of any acceptance of the Offer Shares.

4. EVALUATION OF THE OFFER

In arriving at its conclusion and recommendation, M&A Securities has assessed the fairness and reasonableness of the Offer in accordance with Paragraphs 1 to 6 under Schedule 2: Part III of the Rules, where the term “fair and reasonable” should generally be analysed as 2 distinct criteria, i.e. whether the offer is “fair” and whether the offer is “reasonable”, rather than as composite term.

4.1 Fairness evaluation of the Offer

(a) Valuation of the entire equity interest in Ideal Jacobs

Upon the completion of the Acquisition and Disposal, Ideal Jacobs will assume the entire business of the Widad Builders Group and will no longer continue with its existing manufacturing, fabrication and trading businesses. Therefore, in arriving at the fair value of IJ Shares, M&A Securities has adopted the SOPV model as the sole valuation method, which comprises a DCF valuation of the FCFE to be generated from the core business activities of the Widad Builders Group, and adding the value of assets which are not utilised in the core business activities of the Widad Builders Group. M&A Securities views that the SOPV model to be the most appropriate method to estimate the value of the Shares for the reasons as set out in Section 6 in Part B of this IAC. Based on the SOPV method, M&A Securities has derived an estimated fair value for the entire equity interest in Ideal Jacobs of approximately RM703.6 million to RM751.2 million or a fair value per IJ Share of between RM0.2868 to RM0.3060. Further information on the assessment on the valuation of the IJ Shares is set out in Section 6.1 in Part B of this IAC.

(b) Historical market price performance of IJ Shares

The Offer Price represents: (i) a discount of between 37.84% to 53.06% (or between RM0.14 to RM0.26)

over the 5 day, 1 month, 3 month, 6 month and 1 year VWAMP of IJ Shares up to the Acquisition LTD;

(ii) a discount of between 30.30% to 43.90% (or between RM0.10 to RM0.18)

over the 5 day, 1 month, 3 month, 6 month and 1 year VWAMP of IJ Shares

EXECUTIVE SUMMARY (Cont’d)

3

3. DETAILS OF ACCEPTANCES

As disclosed in the Offer Document, as at the Offer Document LPD, the Offeror has received irrevocable undertakings from the existing substantial shareholders of Ideal Jacobs, namely Andrew Conrad Jacobs and Dato’ Meng Bin, that they will not accept the Offer in respect of shares held directly and indirectly by them, which amounts in aggregate to 41.28% of Ideal Jacobs’ issued share capital as at the Offer Document LPD. Save as disclosed above, the Offeror has not received any irrevocable undertakings from any Holder to accept or reject the Offer and/or acceptances of the Offer from any Holder. As at the LPD, there is no announcement made by Kenanga IB, on behalf of the Offeror of any acceptance of the Offer Shares.

4. EVALUATION OF THE OFFER

In arriving at its conclusion and recommendation, M&A Securities has assessed the fairness and reasonableness of the Offer in accordance with Paragraphs 1 to 6 under Schedule 2: Part III of the Rules, where the term “fair and reasonable” should generally be analysed as 2 distinct criteria, i.e. whether the offer is “fair” and whether the offer is “reasonable”, rather than as composite term.

4.1 Fairness evaluation of the Offer

(a) Valuation of the entire equity interest in Ideal Jacobs

Upon the completion of the Acquisition and Disposal, Ideal Jacobs will assume the entire business of the Widad Builders Group and will no longer continue with its existing manufacturing, fabrication and trading businesses. Therefore, in arriving at the fair value of IJ Shares, M&A Securities has adopted the SOPV model as the sole valuation method, which comprises a DCF valuation of the FCFE to be generated from the core business activities of the Widad Builders Group, and adding the value of assets which are not utilised in the core business activities of the Widad Builders Group. M&A Securities views that the SOPV model to be the most appropriate method to estimate the value of the Shares for the reasons as set out in Section 6 in Part B of this IAC. Based on the SOPV method, M&A Securities has derived an estimated fair value for the entire equity interest in Ideal Jacobs of approximately RM703.6 million to RM751.2 million or a fair value per IJ Share of between RM0.2868 to RM0.3060. Further information on the assessment on the valuation of the IJ Shares is set out in Section 6.1 in Part B of this IAC.

(b) Historical market price performance of IJ Shares

The Offer Price represents: (i) a discount of between 37.84% to 53.06% (or between RM0.14 to RM0.26)

over the 5 day, 1 month, 3 month, 6 month and 1 year VWAMP of IJ Shares up to the Acquisition LTD;

(ii) a discount of between 30.30% to 43.90% (or between RM0.10 to RM0.18)

over the 5 day, 1 month, 3 month, 6 month and 1 year VWAMP of IJ Shares

EXECUTIVE SUMMARY (Cont’d)

3

3. DETAILS OF ACCEPTANCES

As disclosed in the Offer Document, as at the Offer Document LPD, the Offeror has received irrevocable undertakings from the existing substantial shareholders of Ideal Jacobs, namely Andrew Conrad Jacobs and Dato’ Meng Bin, that they will not accept the Offer in respect of shares held directly and indirectly by them, which amounts in aggregate to 41.28% of Ideal Jacobs’ issued share capital as at the Offer Document LPD. Save as disclosed above, the Offeror has not received any irrevocable undertakings from any Holder to accept or reject the Offer and/or acceptances of the Offer from any Holder. As at the LPD, there is no announcement made by Kenanga IB, on behalf of the Offeror of any acceptance of the Offer Shares.

4. EVALUATION OF THE OFFER

In arriving at its conclusion and recommendation, M&A Securities has assessed the fairness and reasonableness of the Offer in accordance with Paragraphs 1 to 6 under Schedule 2: Part III of the Rules, where the term “fair and reasonable” should generally be analysed as 2 distinct criteria, i.e. whether the offer is “fair” and whether the offer is “reasonable”, rather than as composite term.

4.1 Fairness evaluation of the Offer

(a) Valuation of the entire equity interest in Ideal Jacobs

Upon the completion of the Acquisition and Disposal, Ideal Jacobs will assume the entire business of the Widad Builders Group and will no longer continue with its existing manufacturing, fabrication and trading businesses. Therefore, in arriving at the fair value of IJ Shares, M&A Securities has adopted the SOPV model as the sole valuation method, which comprises a DCF valuation of the FCFE to be generated from the core business activities of the Widad Builders Group, and adding the value of assets which are not utilised in the core business activities of the Widad Builders Group. M&A Securities views that the SOPV model to be the most appropriate method to estimate the value of the Shares for the reasons as set out in Section 6 in Part B of this IAC. Based on the SOPV method, M&A Securities has derived an estimated fair value for the entire equity interest in Ideal Jacobs of approximately RM703.6 million to RM751.2 million or a fair value per IJ Share of between RM0.2868 to RM0.3060. Further information on the assessment on the valuation of the IJ Shares is set out in Section 6.1 in Part B of this IAC.

(b) Historical market price performance of IJ Shares

The Offer Price represents: (i) a discount of between 37.84% to 53.06% (or between RM0.14 to RM0.26)

over the 5 day, 1 month, 3 month, 6 month and 1 year VWAMP of IJ Shares up to the Acquisition LTD;

(ii) a discount of between 30.30% to 43.90% (or between RM0.10 to RM0.18)

over the 5 day, 1 month, 3 month, 6 month and 1 year VWAMP of IJ Shares

EXECUTIVE SUMMARY (Cont’d)

3

3. DETAILS OF ACCEPTANCES

As disclosed in the Offer Document, as at the Offer Document LPD, the Offeror has received irrevocable undertakings from the existing substantial shareholders of Ideal Jacobs, namely Andrew Conrad Jacobs and Dato’ Meng Bin, that they will not accept the Offer in respect of shares held directly and indirectly by them, which amounts in aggregate to 41.28% of Ideal Jacobs’ issued share capital as at the Offer Document LPD. Save as disclosed above, the Offeror has not received any irrevocable undertakings from any Holder to accept or reject the Offer and/or acceptances of the Offer from any Holder. As at the LPD, there is no announcement made by Kenanga IB, on behalf of the Offeror of any acceptance of the Offer Shares.

4. EVALUATION OF THE OFFER

In arriving at its conclusion and recommendation, M&A Securities has assessed the fairness and reasonableness of the Offer in accordance with Paragraphs 1 to 6 under Schedule 2: Part III of the Rules, where the term “fair and reasonable” should generally be analysed as 2 distinct criteria, i.e. whether the offer is “fair” and whether the offer is “reasonable”, rather than as composite term.

4.1 Fairness evaluation of the Offer

(a) Valuation of the entire equity interest in Ideal Jacobs

Upon the completion of the Acquisition and Disposal, Ideal Jacobs will assume the entire business of the Widad Builders Group and will no longer continue with its existing manufacturing, fabrication and trading businesses. Therefore, in arriving at the fair value of IJ Shares, M&A Securities has adopted the SOPV model as the sole valuation method, which comprises a DCF valuation of the FCFE to be generated from the core business activities of the Widad Builders Group, and adding the value of assets which are not utilised in the core business activities of the Widad Builders Group. M&A Securities views that the SOPV model to be the most appropriate method to estimate the value of the Shares for the reasons as set out in Section 6 in Part B of this IAC. Based on the SOPV method, M&A Securities has derived an estimated fair value for the entire equity interest in Ideal Jacobs of approximately RM703.6 million to RM751.2 million or a fair value per IJ Share of between RM0.2868 to RM0.3060. Further information on the assessment on the valuation of the IJ Shares is set out in Section 6.1 in Part B of this IAC.

(b) Historical market price performance of IJ Shares

The Offer Price represents: (i) a discount of between 37.84% to 53.06% (or between RM0.14 to RM0.26)

over the 5 day, 1 month, 3 month, 6 month and 1 year VWAMP of IJ Shares up to the Acquisition LTD;

(ii) a discount of between 30.30% to 43.90% (or between RM0.10 to RM0.18)

over the 5 day, 1 month, 3 month, 6 month and 1 year VWAMP of IJ Shares

3

EXECUTIVE SUMMARY (Cont’d)

4

up to the Notice LTD; and (iii) a discount of 23.33% and 25.81% (or RM0.07 and RM0.08) to the last traded

price of IJ Shares as at the LPD and 5 day VWAMP of IJ Shares up to and including the LPD respectively.

As the Offer Price of RM0.23 is:

(a) lower than and represents a discount of RM0.06 to RM0.08 or 19.80% to

24.84% over the estimated fair value per IJ Share of RM0.2868 to RM0.3060 derived from the SOPV method of valuation in (a) above; and

(b) represents a discount of between RM0.07 to RM0.26 or 23.33% to 53.06%

to the historical market price of IJ Shares as set out in (b) above,

the Offer is NOT FAIR.

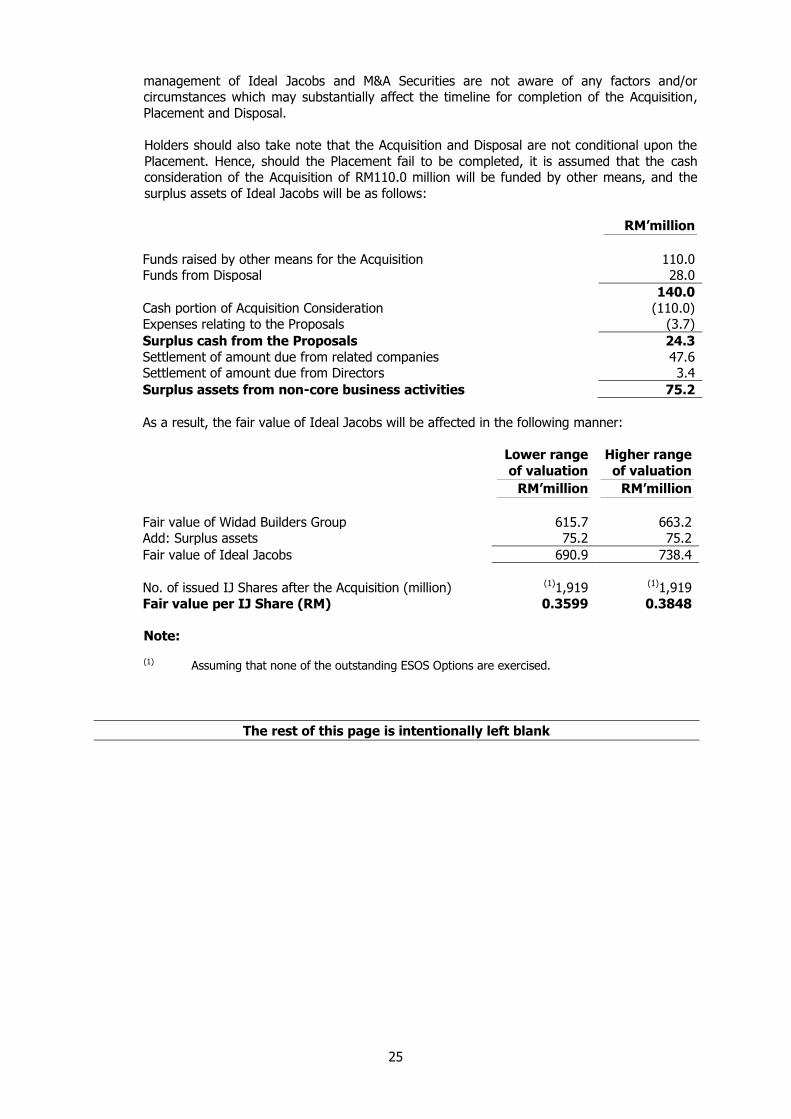

Notwithstanding the above, we wish to highlight that our evaluation is strictly premised on the assumption that the Acquisition, Placement and Disposal will be completed. As at the LPD, the management of Ideal Jacobs and M&A Securities are not aware of any factors and/or circumstances which may substantially affect the timeline for completion of the Acquisition, Placement and Disposal.

Nevertheless, the Holders are advised to read the ensuing sections of this IAC for a comprehensive evaluation of the Offer and not to rely solely on the above valuations of the IJ Shares as the sole criteria when assessing the Offer.

4.2 Reasonableness evaluation of the Offer

We note that: (a) the Offeror intends to maintain the listing status of Ideal Jacobs on the ACE Market of

Bursa Securities, thereby allowing the Holders to sell their IJ Shares in the open market after the Closing Date;

(b) the Offeror does not intend to invoke the provisions of Section 222(1) of the CMSA to

compulsorily acquire any outstanding Offer Shares for which valid acceptances have not been received prior to the Closing Date; and

(c) Holders who choose to reject the Offer will receive free Warrants which will allow

them to participate in the potential upside of Ideal Jacobs moving forward. Premised on the above, we are of the view that the Offer is NOT REASONABLE.

The rest of this page is intentionally left blank

4

EXECUTIVE SUMMARY (Cont’d)

5

5. RECOMMENDATION

Premised on the above evaluation, M&A Securities is of the opinion that the Offer is NOT FAIR and NOT REASONABLE. Accordingly, M&A Securities recommends that the Holders REJECT the Offer. Please refer to Section 10 in Part B of this IAC for further details. Nonetheless, Holders are advised to closely monitor the announcements made by the Offeror and market price of IJ Shares prior to the Closing Date before making the decision as to whether to accept or reject the Offer. The Directors of Ideal Jacobs, after careful assessment of the terms and conditions of the Offer as contained in the Offer Document and the evaluation as contained in this IAC, have CONCURRED with the opinion of the Independent Adviser that the Offer is NOT FAIR and NOT REASONABLE. Accordingly, the Directors also concur with the Independent Adviser’s recommendation that you REJECT the Offer.

6. IMPORTANT DATES AND EVENTS

The important relevant dates in relation to the Offer are as follows:

Event Date

Date of the Notice 12 February 2018

Despatch of the Offer Document 5 March 2018

Issuance of this IAC 15 March 2018

First Closing Date(1) 26 March 2018 Note: (1) The Offer will remain open for acceptances until 5.00 p.m. (Malaysian time) on the

First Closing Date unless extended in accordance with the Rules or as the Offeror may decide and announced by Kenanga IB, on behalf of the Offeror, no later than 2 days before the Closing Date. Notices of such extension will be posted to you accordingly.

The rest of this page is intentionally left blank

5

6

PART A

LETTER FROM THE BOARD

6

LETTER FROM THE BOARD

7

IDEAL JACOBS (MALAYSIA) CORPORATION BHD

(Company No. 857363-U) (Incorporated in Malaysia under the Companies Act, 1965)

Registered Office

Level 15-2, Bangunan Faber Imperial Court

Jalan Sultan Ismail 50250 Kuala Lumpur

15 March 2018

Board of Directors: Andrew Conrad Jacobs (Executive Chairman) Dato’ Meng Bin (Chief Executive Officer and Managing Director) Koong Lin Loong (Independent Non-Executive Director) Hing Kim Tat (Independent Non-Executive Director) Tan Kean Huat (Independent Non-Executive Director) Rizvi Bin Abd Halim (Independent Non-Executive Director) To: The Holders Dear Sir/Madam, UNCONDITIONAL MANDATORY TAKE-OVER OFFER BY THE OFFEROR THROUGH KENANGA IB TO ACQUIRE ALL THE OFFER SHARES FOR A CASH OFFER PRICE OF RM0.23 PER OFFER SHARE 1. INTRODUCTION

On 5 June 2017, Ideal Jacobs entered into the HOA with WBGSB for the Acquisition. On 18 August 2017, Ideal Jacobs and WBGSB entered into the Acquisition SPA. Under the Acquisition SPA, the purchase consideration of RM520 million for the Acquisition is to be satisfied through cash (RM110 million) and the issuance of the Consideration Shares at the Consideration Issue Price (RM410 million). In conjunction with the Acquisition, Ideal Jacobs is also undertaking the other Proposals, which comprise: (a) disposal of Ideal Jacobs (HK) Corporation Ltd, Ideal Jacobs (Xiamen) Corporation,

Xiamen Ideal Jacobs International Ltd Company and Suzhou Ideal Jacobs Corporation for a cash consideration of RM28.0 million, that is, the Disposal;

(b) private placement of up to 534,032,115 new IJ Shares representing 25% of the enlarged total issued share capital of Ideal Jacobs upon completion of the Acquisition at an issue price to be determined later, that is, the Placement;

LETTER FROM THE BOARD

7

IDEAL JACOBS (MALAYSIA) CORPORATION BHD

(Company No. 857363-U) (Incorporated in Malaysia under the Companies Act, 1965)

Registered Office

Level 15-2, Bangunan Faber Imperial Court

Jalan Sultan Ismail 50250 Kuala Lumpur

15 March 2018

Board of Directors: Andrew Conrad Jacobs (Executive Chairman) Dato’ Meng Bin (Chief Executive Officer and Managing Director) Koong Lin Loong (Independent Non-Executive Director) Hing Kim Tat (Independent Non-Executive Director) Tan Kean Huat (Independent Non-Executive Director) Rizvi Bin Abd Halim (Independent Non-Executive Director) To: The Holders Dear Sir/Madam, UNCONDITIONAL MANDATORY TAKE-OVER OFFER BY THE OFFEROR THROUGH KENANGA IB TO ACQUIRE ALL THE OFFER SHARES FOR A CASH OFFER PRICE OF RM0.23 PER OFFER SHARE 1. INTRODUCTION

On 5 June 2017, Ideal Jacobs entered into the HOA with WBGSB for the Acquisition. On 18 August 2017, Ideal Jacobs and WBGSB entered into the Acquisition SPA. Under the Acquisition SPA, the purchase consideration of RM520 million for the Acquisition is to be satisfied through cash (RM110 million) and the issuance of the Consideration Shares at the Consideration Issue Price (RM410 million). In conjunction with the Acquisition, Ideal Jacobs is also undertaking the other Proposals, which comprise: (a) disposal of Ideal Jacobs (HK) Corporation Ltd, Ideal Jacobs (Xiamen) Corporation,

Xiamen Ideal Jacobs International Ltd Company and Suzhou Ideal Jacobs Corporation for a cash consideration of RM28.0 million, that is, the Disposal;

(b) private placement of up to 534,032,115 new IJ Shares representing 25% of the enlarged total issued share capital of Ideal Jacobs upon completion of the Acquisition at an issue price to be determined later, that is, the Placement;

LETTER FROM THE BOARD

7

IDEAL JACOBS (MALAYSIA) CORPORATION BHD

(Company No. 857363-U) (Incorporated in Malaysia under the Companies Act, 1965)

Registered Office

Level 15-2, Bangunan Faber Imperial Court

Jalan Sultan Ismail 50250 Kuala Lumpur

15 March 2018

Board of Directors: Andrew Conrad Jacobs (Executive Chairman) Dato’ Meng Bin (Chief Executive Officer and Managing Director) Koong Lin Loong (Independent Non-Executive Director) Hing Kim Tat (Independent Non-Executive Director) Tan Kean Huat (Independent Non-Executive Director) Rizvi Bin Abd Halim (Independent Non-Executive Director) To: The Holders Dear Sir/Madam, UNCONDITIONAL MANDATORY TAKE-OVER OFFER BY THE OFFEROR THROUGH KENANGA IB TO ACQUIRE ALL THE OFFER SHARES FOR A CASH OFFER PRICE OF RM0.23 PER OFFER SHARE 1. INTRODUCTION

On 5 June 2017, Ideal Jacobs entered into the HOA with WBGSB for the Acquisition. On 18 August 2017, Ideal Jacobs and WBGSB entered into the Acquisition SPA. Under the Acquisition SPA, the purchase consideration of RM520 million for the Acquisition is to be satisfied through cash (RM110 million) and the issuance of the Consideration Shares at the Consideration Issue Price (RM410 million). In conjunction with the Acquisition, Ideal Jacobs is also undertaking the other Proposals, which comprise: (a) disposal of Ideal Jacobs (HK) Corporation Ltd, Ideal Jacobs (Xiamen) Corporation,

Xiamen Ideal Jacobs International Ltd Company and Suzhou Ideal Jacobs Corporation for a cash consideration of RM28.0 million, that is, the Disposal;

(b) private placement of up to 534,032,115 new IJ Shares representing 25% of the enlarged total issued share capital of Ideal Jacobs upon completion of the Acquisition at an issue price to be determined later, that is, the Placement;

7

PART A – LETTER FROM THE BOARD (Cont’d)

8

(c) issuance of free warrants on the basis of 1 warrant for every 5 existing IJ Shares held upon completion of the Acquisition, Disposal and Placement at an entitlement date and exercise price to be determined later, that is, the Free Warrants Issue; and

(d) amendment to its Memorandum of Association, that is, the Amendment.

Ideal Jacobs’ shareholders had approved the Proposals at its extraordinary general meeting held on 29 January 2018. Please refer to Ideal Jacobs’ circular to shareholders dated 4 January 2018 for further information on the Proposals.

Upon the issuance of the Consideration Shares and before the Placement, WBGSB's shareholding in Ideal Jacobs will increase from nil to 92.87% and the collective shareholdings of the Offeror and Joint Ultimate Offerors will increase from 0.53% to 92.91%.

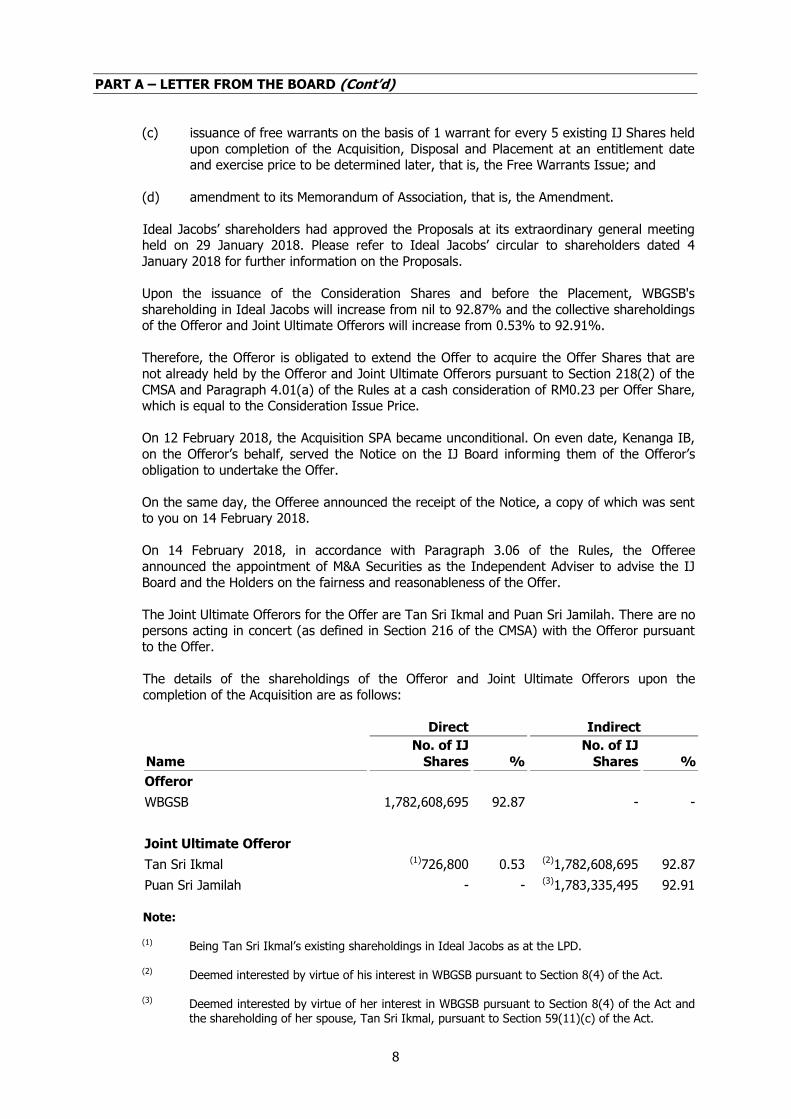

Therefore, the Offeror is obligated to extend the Offer to acquire the Offer Shares that are not already held by the Offeror and Joint Ultimate Offerors pursuant to Section 218(2) of the CMSA and Paragraph 4.01(a) of the Rules at a cash consideration of RM0.23 per Offer Share, which is equal to the Consideration Issue Price. On 12 February 2018, the Acquisition SPA became unconditional. On even date, Kenanga IB, on the Offeror’s behalf, served the Notice on the IJ Board informing them of the Offeror’s obligation to undertake the Offer. On the same day, the Offeree announced the receipt of the Notice, a copy of which was sent to you on 14 February 2018. On 14 February 2018, in accordance with Paragraph 3.06 of the Rules, the Offeree announced the appointment of M&A Securities as the Independent Adviser to advise the IJ Board and the Holders on the fairness and reasonableness of the Offer. The Joint Ultimate Offerors for the Offer are Tan Sri Ikmal and Puan Sri Jamilah. There are no persons acting in concert (as defined in Section 216 of the CMSA) with the Offeror pursuant to the Offer. The details of the shareholdings of the Offeror and Joint Ultimate Offerors upon the completion of the Acquisition are as follows:

Direct Indirect

Name No. of IJ

Shares % No. of IJ

Shares % Offeror WBGSB 1,782,608,695 92.87 - - Joint Ultimate Offeror Tan Sri Ikmal (1)726,800 0.53 (2)1,782,608,695 92.87 Puan Sri Jamilah - - (3)1,783,335,495 92.91 Note: (1) Being Tan Sri Ikmal’s existing shareholdings in Ideal Jacobs as at the LPD.

(2) Deemed interested by virtue of his interest in WBGSB pursuant to Section 8(4) of the Act.

(3) Deemed interested by virtue of her interest in WBGSB pursuant to Section 8(4) of the Act and

the shareholding of her spouse, Tan Sri Ikmal, pursuant to Section 59(11)(c) of the Act.

8

PART A – LETTER FROM THE BOARD (Cont’d)

9

In addition to this IAC, you should have by now received a copy of the Offer Document dated 5 March 2018, which sets out the details, terms and conditions of the Offer as well as the procedures for acceptance and method of settlement of the Offer. On 14 March 2018, the SC notified that it has no further comments to the contents of this IAC. However, such notification shall not be taken to suggest that the SC agrees with the recommendations contained herein or assumes responsibility for the correctness of any statements made or opinions or reports expressed in this IAC. The purpose of this IAC is to provide you with the relevant information on the Offer, Directors’ views and recommendation on the Offer as well as the recommendation of M&A Securities. You are advised to read both this IAC and the Offer Document and carefully consider the recommendations contained herein before taking any action.

2. SALIENT TERMS AND CONDITIONS OF THE OFFER

The salient terms and conditions of the Offer are set out in Section 2 in Part B of this IAC. Please refer to Appendix I of the Offer Document for the full terms and conditions of the Offer as well as Appendix II of the Offer Document for the procedures for acceptance and method of settlement of the Offer.

3. DETAILS OF ACCEPTANCES

As disclosed in the Offer Document, as at the Offer Document LPD, the Offeror has received irrevocable undertakings from the existing substantial shareholders of Ideal Jacobs, namely Andrew Conrad Jacobs and Dato’ Meng Bin, that they will not accept the Offer in respect of shares held directly and indirectly by them, which amounts in aggregate to 41.28% of Ideal Jacobs’ issued share capital as at the Offer Document LPD. Save for the foregoing, the Offeror has not received any irrevocable undertakings from any Holder to accept or reject the Offer and/or acceptances of the Offer from any Holder. As at the LPD, there is no announcement made by Kenanga IB, on behalf of the Offeror of any acceptance of the Offer Shares.

4. DIRECTORS’ VIEWS

4.1 Rationale of the Offer The Directors have noted the rationale for the Offer as set out in Section 3 of the Offer Document: (a) the Offer is a mandatory obligation pursuant to the Rules as the SPA has become

unconditional. The Offeror’s shareholding in Ideal Jacobs will increase from 0.53% to approximately 92.91% of the total number of issued Shares following the Acquisition; and

(b) the Offeror’s aim to increase its shareholding in Ideal Jacobs is to gain statutory control

in Ideal Jacobs as it recognises the long-term prospects of Ideal Jacobs. Through the Offeror’s controlling interest in Ideal Jacobs, the Joint Ultimate Offerors will have the ability to determine Ideal Jacobs’ strategic direction and flexibility to effect the necessary changes in view of its new core businesses. The Offeror will endeavour to grow Ideal Jacobs’ businesses by, among others, exploring synergies with the WBGSB group of companies.

9

PART A – LETTER FROM THE BOARD (Cont’d)

10

The Directors also take note that the rationale of the Offer is in line with the rationale of the Proposals, for which the Directors have recommended the Ideal Jacobs’ shareholders vote in favour at the extraordinary general meeting held on 29 January 2018. As such, the Directors are of the view that the Offeror’s plans of gaining statutory control of Ideal Jacobs is in the best interests of the New IJ Group moving forward.

4.2 Future plans for Ideal Jacobs and its subsidiaries and their employees The Directors have noted the following intentions of the Offeror in respect of the future plans and employees of the IJ Group as stated in Section 5 of the Offer Document, where the Offeror: (a) does not intend to continue with its existing manufacturing, fabrication and trading