ICFAI Accounts

224

Financial Accounting (MB131) : January 2004 Question Paper Financial Accounting (MB131) : January 2004 Section A : Basic Concepts (30 Marks) • This section consists of questions with serial number 1 - 30. • Answer all questions. • Each question carries one mark. 1. Which of the following represent(s) personal accounts in accounting parlance? a. Sundry creditors b. Bank account c. Outstanding wages d. Prepaid insurance e. All of the above. < Answer > 2. Which of the following methods of valuation of inventory is based on the assumption that costs are charged against revenue in the order in which they occur? a. FIFO method b. LIFO method c. Weighted average method d. Moving average method e. Base stock method. < Answer > 3. Which of the following is not an item of revenue expenditure? a. Interest on deposits accepted b. Annual insurance premium on inventory c. Customs duty paid in connection with the import of equipment d. Repairs and maintenance on machinery e. Expenditure on assets like paper weight and pin cushion. < Answer > 4. Which of the following errors will cause a mismatch in the trial balance?

-

Upload

akhileshwar-singh -

Category

Documents

-

view

214 -

download

19

Transcript of ICFAI Accounts

Financial Accounting (MB131) : January 2004

Question Paper

Financial Accounting (MB131) : January 2004

Section A : Basic Concepts (30 Marks)• This section consists of questions with serial number 1 - 30.• Answer all questions.• Each question carries one mark.1. Which of the following represent(s) personal accounts in accounting parlance?a. Sundry creditorsb. Bank accountc. Outstanding wagesd. Prepaid insurancee. All of the above.< Answer >2. Which of the following methods of valuation of inventory is based on the assumption that costs arecharged against revenue in the order in which they occur?a. FIFO methodb. LIFO methodc. Weighted average methodd. Moving average methode. Base stock method.< Answer >3. Which of the following is not an item of revenue expenditure?a. Interest on deposits acceptedb. Annual insurance premium on inventoryc. Customs duty paid in connection with the import of equipmentd. Repairs and maintenance on machinerye. Expenditure on assets like paper weight and pin cushion.< Answer >4. Which of the following errors will cause a mismatch in the trial balance?a. Errors of complete omissionb. Compensating errorsc. Errors of principled. Recording dual aspects of a transaction more than oncee. Errors of partial omission.< Answer >

5. AB & Co. purchased a machine for Rs.10,00,000 on April 1, 2002. The salvage value of the machine isRs.40,000. The useful life of the machine is 8 years. If the firm intends to depreciate the machinery onstraight-line method, the rate of depreciation will bea. 16%b. 15%c. 14%d. 12.5%e. 12%.< Answer >6. If the purchases day book of a firm is overcast, it willa. Increase gross profit and reduce net profitb. Reduce gross profit and increase net profitc. Reduce gross profit as well as net profitd. Increase gross profit as well as net profite. Reduce gross profit but will not have any impact on net profit.< Answer >7. Which of the following is true when a debtor pays his dues?a. The asset side of the balance sheet will decreaseb. The asset side of the balance sheet will increasec. The liability side of the balance sheet will increased. The liability side of the balance sheet will decrease< Answer >e. There is no change in total assets or total liabilities.8. Withdrawal of goods from stock by the owner of the business for personal use should be recorded bydebitinga. Drawings account and crediting cash accountb. Drawings account and crediting purchases accountc. Capital account and crediting drawings accountd. Purchases account and crediting drawings accounte. Stock account and crediting capital account.< Answer >9. The cost price of a machine is Rs.1,20,000 and the depreciated value of the machine after 3 years willbe Rs.66,000. If the company charges depreciation under straight-line method, the rate of depreciationwill bea. 25%

b. 20%c. 18%d. 15%e. 12%.< Answer >10. Consider the following data pertaining to a firm:The balance as per pass book isa. Rs.20,600 (Dr. balance)b. Rs.18,500 (Dr. balance)c. Rs.18,500 (Cr. balance)d. Rs.15,600 (Dr. balance)e. Rs.20,600 (Cr. balance).Credit balance as per bank column of cash book Rs.13,500Bank interest on overdraft appeared only in the pass book Rs.2,100Cheques deposited but not collected by the bank Rs.5,000< Answer >11. Consider the following data pertaining to a company for the year 2002-2003:The bad debts of the company during the year area. Rs.40,000b. Rs.35,000c. Rs.30,000d. Rs.25,000e. Rs.20,000.Opening balance of sundry debtors Rs. 45,000Credit sales Rs.4,25,000Cash sales Rs. 20,000Cash collected from debtors Rs.4,00,000Closing balance of sundry debtors Rs. 50,000< Answer >12. The opening stock of a company is Rs.40,000 and the closing stock is Rs.50,000. If the purchasesduring the year are Rs.2,00,000 the cost of goods sold will bea. Rs.2,10,000b. Rs.2,00,000c. Rs.1,90,000d. Rs.1,80,000e. Rs.1,50,000.< Answer >13. The balance as per bank statement of a company is Rs.12,500 (Dr.). The

company deposited twocheques worth Rs.8,500, out of which one cheque for Rs.2,800 was dishonoured which was not enteredin the cash book. The credit balance as per cash book isa. Rs.21,000b. Rs.15,300c. Rs.23,800d. Rs. 9,700< Answer >e. Rs. 4,000.14. During the year 2002-03, the profit of a business before charging manager’s commission wasRs.1,89,000. If the manager’s commission is 5% on profit after charging his commission, then the totalamount of commission payable to manager isa. Rs.10,000b. Rs. 9,450c. Rs. 9,000d. Rs. 8,500e. Rs. 9,947.< Answer >15. Which of the following statements is true?a. The losses from the sale of capital assets need not be deducted from the revenue to ascertain netincomeb. Going concern concept requires that always non-monetary assets should be valued and recorded atmarket valuec. According to consistency concept, the results of one accounting period of a business cannot becompared with that of in the pastd. In terms of conservatism concept all probable losses must be considered in computation of incomee. The system of recording transactions based on dual concept is double accounting system.< Answer >16. Which of the following ratios indicates the short-term liquidity of a business?a. Inventory turnover ratiob. Debt-equity ratio

c. Acid test ratiod. Proprietary ratioe. Net profit ratio.< Answer >17. Which of the following should be deducted in the Balance Sheet of a company from the share capital tofind out paid-up capital?a. Calls-in-advanceb. Calls-in-arrearsc. Share forfeitured. Discount on issue of sharese. Share premium.< Answer >18. Which of the following statements is false?a. The forfeited shares should not be issued at a premiumb. At the time of forfeiture of shares, share premium should not be debited with the amount ofpremium already receivedc. Shares can be issued at a discount only after one year from the commencement of businessd. Share premium cannot be utilized to redeem preference sharese. The loss on re-issue of shares cannot be more than the gain on forfeiture of those shares.< Answer >19. Which of the following accounting treatments is/are true in respect of accrued commission appearingon the debit side of a trial balance?a. It is shown on the debit side of the profit and loss accountb. It is shown on the credit side of the profit and loss accountc. It is shown on the liabilities side of the balance sheetd. It is shown on the assets side of the balance sheete. Both (b) and (d) above.< Answer >20. The maximum amount beyond which a company is not allowed to raise funds by issue of shares isa. Issued capitalb. Reserve capitalc. Nominal capitald. Subscribed capitale. Paid-up capital.

< Answer >21. The discount allowed on re-issue of forfeited shares is debited to< Answer >a. Discount on re-issue of shares accountb. Profit and loss accountc. Share premium accountd. Discount on issue of shares accounte. Forfeited shares account.22. The interest on calls in advance is paid for the period from thea. Date of receipt of application money to the date of appropriationb. Date of receipt of allotment money to the date of appropriationc. Date of receipt of advance to the date of appropriationd. Date of appropriation to the date of dividend paymente. Date of appropriation to the date of receipt of final call.< Answer >23. Which of the following items should not appear under the head ‘unsecured loans’ in the Balance Sheetof a company?a. Sinking fundsb. Loans and advances from subsidiariesc. Short term loans and advances from banksd. Loans and advances from otherse. Fixed deposits.< Answer >24. Share premium cannot be used toa. Issue bonus sharesb. Redeem preference sharesc. Write-off preliminary expensesd. Write-off discount on issue of sharese. Provide for premium payable on redemption of debentures.< Answer >25. Rishi Ltd. issued 1,50,000 shares of Rs.100 each at a discount of 10%. Rama, to whom 300 shares wereallotted failed to pay the final call of Rs.30 per share and hence, all his shares were forfeited. At the timeof forfeiture, the amount transferred to share forfeiture account wasa. Rs. 9,000b. Rs.18,000c. Rs.21,000d. Rs.27,000

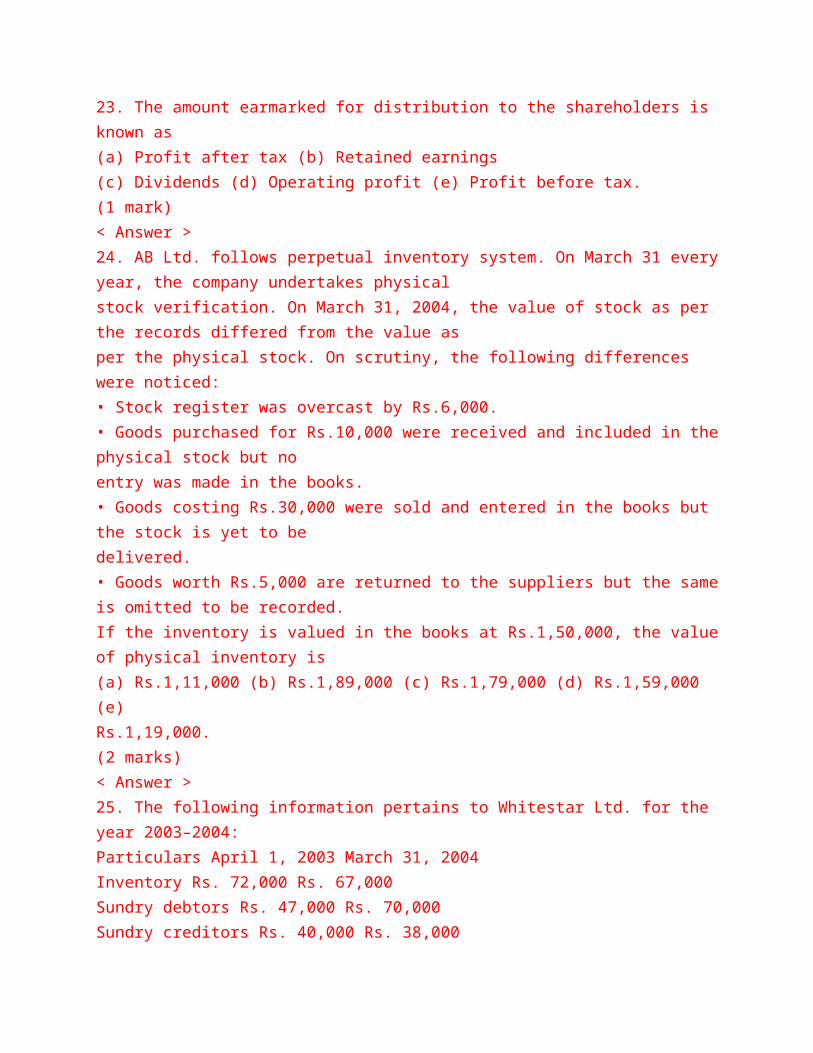

e. Rs.30,000.< Answer >26. Suma Ltd. announced a rights issue of four shares of Rs.100 each at a premium of 160% for every fiveshares held by the existing shareholders. The market value of the share at the time of rights issue isRs.440. The value of right isa. Rs.124b. Rs.352c. Rs. 80d. Rs.110e. Rs.180.< Answer >27. Which of the following statements is true?a. A company will be deemed to be a holding company of another if, it holds more than 50percent of both equity and preference share capitalb. The financial year of the holding company and its subsidiary company must end on the same datec. The share capital of the subsidiary company does not appear in the Consolidated Balance Sheetd. The inter company owing will be shown in the Consolidated Balance Sheete. Minority shareholders of the subsidiary are entitled to proportionate share in capital profits only.< Answer >28. On December 01, 2002 H Ltd. acquired 60% shares in S Ltd. The balance of profit and loss account ofS Ltd. on April 01, 2002 and March 31, 2003 was Rs.90, 000 and Rs.1, 50,000, respectively. The profit isearned evenly throughout the year. The share of capital profit ofH Ltd. in the profits of the subsidiary as on March 31, 2003 isa. Rs. 36,000b. Rs. 60,000c. Rs. 72,000< Answer >d. Rs. 78,000e. Rs.1,30,000.29. On April 01, 2002, Sura Chemicals Ltd. issued 10,000, 18% Debentures of Rs.100 each. The company

reserves the right to redeem its debentures in any year by purchase in open market. Interest ondebentures is payable on September 30, and March 31, every year.• On July 1, 2002, the company purchased 2,000 of its own 18% debentures at Rs.98 cuminterest.• The company cancelled its own 2,000 debentures on March 31, 2003.The profit on cancellation of debentures transferred to Capital reserve isa. Rs. 4,000b. Rs. 9,000c. Rs.36,000d. Rs.13,000e. Rs.27,000.< Answer >30. Consider the following profits pertaining to a company for the last 3 years:The weighted average profit of the company for the purpose of valuation of goodwill isa. Rs.4,50,000b. Rs.4,35,000c. Rs.4,10,000d. Rs.3,85,000e. Rs.3,50,000.Year Profit (Rs.)2000-01 Rs.3,30,0002001-02 Rs.4,20,0002002-03 Rs.4,80,000< Answer >

ANS—

1. Answer : (e)Reason : Personal accounts deal with accounts of individuals like creditors, debtors, banks etc. It shows thebalance due to these individuals or due from them on a particular date and representative personalaccounts represent the amounts due on account of accrual concept

like accrued expenses and prepaidexpenses or accrued incomes and pre-received incomes. By virtue of this, the accounts stated inalternatives (a) sundry creditors, (b) Bank account, (c) outstanding wages and (d) prepaid insurancerepresent personal accounts.< TOP >2. Answer : (a)Reason : The basis for pricing inventory is either cost of production or cost of acquisition. FIFO method ofidentifying inventory is based on the assumption that costs are charged against revenue in the order inwhich they occur. In case of other methods i.e. LIFO (b) method matches the most recent costs incurredwith current revenue, leaving the first cost incurred to be included as inventory. Weighted-Averagemethod (c) assumes that costs are charged against revenue based on an average of the number of unitsacquired at each price level. Moving average method (d) can be used only with a perpetual inventory.The cost per unit is recomputed after every addition to the inventory. The ending inventory is valued atthe last moving average unit cost for the period. Base stock method (e) wherein a minimal level of it isa permanent investment, which is necessary for the normal business activities. Base stock would becarried at historical cost. Thus, FIFO method is the correct answer.< TOP >3. Answer : (c)Reason : Revenue expenditure is incurred for day to day running of the business. Any item of expenditure whichimproves the earning capacity of a business entity or the expenditure incurred till the asset is ready foruse is capital expenditure. From the viewpoint of this, the customs duty paid in connection with theimport of equipment (c) is not revenue expenditure. The expenses mentioned in other alternativesInterest on deposits accepted (a) Annual insurance premium (b) repairs and maintenance (d)Expenditure on assets like paperweight etc. are items of revenue

expenditure.< TOP >4. Answer : (e)Reason : A trial balance in which the total of the debits does not equal to the total of credits due to errorscommitted in the process of accounting. One among the errors is Partial omission of an entry If thedebit or credit aspect of a transaction has been omitted to be recorded, the trial balance will disagree.For example, if a cash sales of Rs.800 is omitted to be recorded in the Sales account then the totaldebits will exceed the total credits by Rs.800. Thus, results in a mismatch in the trial balance. But, incase of errors mentioned in alternatives (a), (b), (c) and (d) the agreeing of trial balance is not affectedas explained hereunder:Omission of the recording of a transaction from the books of accounts: If the withdrawal of goodsworth Rs.1,200 by the proprietor is omitted to be recorded in the books, the trial balance will still agreeas both the debit and the credit aspects have been omitted to be recorded.Compensating errors: These are quite difficult to detect. If a cash discount of Rs.215 allowed to acustomer has been posted to the credit of his account as Rs.251 and a cash sale of Rs.2,851 has beenposted to sales account as Rs.2,815, then the excess credit caused by the first error would be exactlycompensated by the lower credit recorded by the second error and the trial balance will be inagreement.Errors of principle: If the machinery account is debited for an amount of repair charges incurred forthe machinery, the error will not be disclosed by the trial balance. This is because that both machineryaccount and repairs account are debit accounts and it is a question of principle that repair chargesshould not be debited to the machinery account. Hence, the total effect will be the same and hence thetrial balance will tally.

Recording both aspects of a transaction more than once in the books of accounts: If a sale ofRs.3,500 made to PQR Ltd. is entered in the sales book twice, the error will not cause a mismatch in thetotals of the trial balance.< TOP >5. Answer : (e)Reason : Value of machine Rs.10,00,000Less: Salvage value Rs. 40,000Depreciable value Rs. 9,60,000Life of the machine 8 yearsDepreciation = = Rs.1,20,0009,60,0008< TOP >Rate of depreciation = = 12%1, 20,000 10010, 00,000×6. Answer : (c)Reason : If purchase day book is overcast, it shows higher cost of production or goods sold. It reduces grossprofit which in turn reduces net profit. It cannot increase gross profit and net profit. Therefore, (c) is thecorrect answer.< TOP >7. Answer : (e)Reason : If a debtor pays his dues, debtors balance will decrease and cash balance will increase. Thus, thecomposition of assets will change. But there is no change in the total assets or liabilities and hence (e) istrue.< TOP >8. Answer : (b)Reason : If the owner withdraws goods from the business, journal entry will beDrawings account ……… DrTo Purcahses accountOther options, given in a, c, d and e, relating to drawings are not correct.

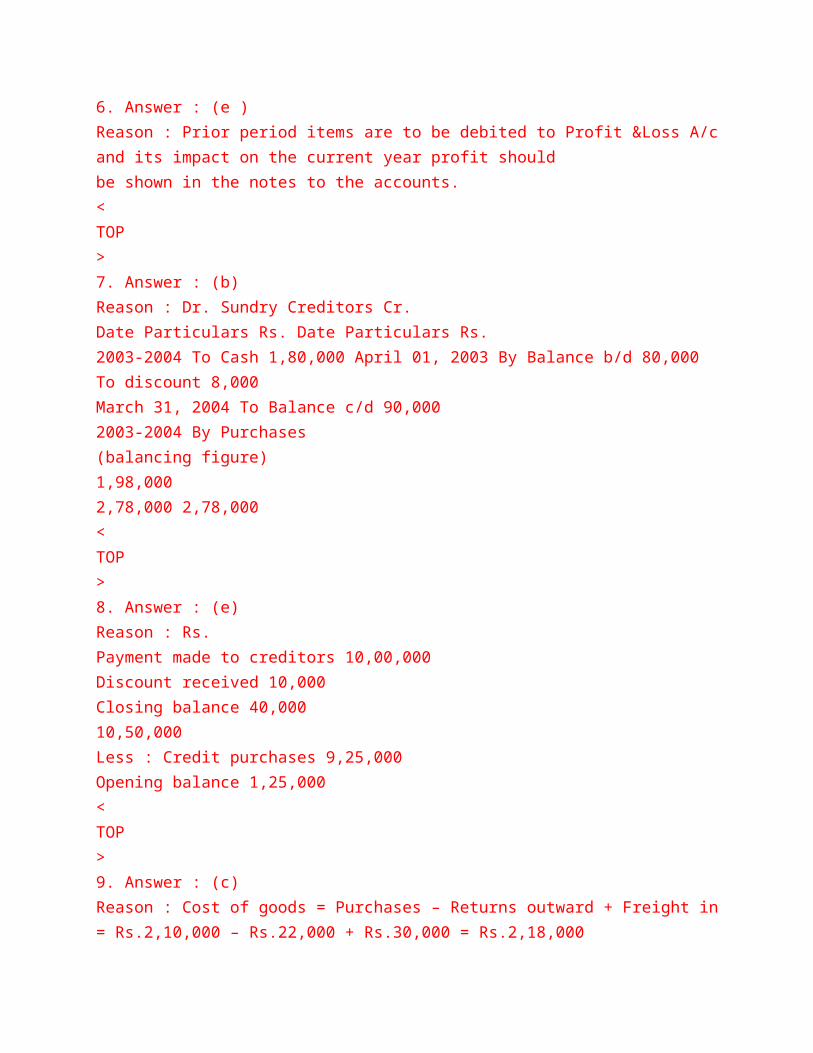

< TOP >9. Answer : (d)Reason : Let the rate of depreciation = xThe depreciated value of machine = Rs.1,20,000 (1 – 3x) = Rs.66,0001 – 3x = = 0.553x = 1 – 0.55 = 0.45x = 0.45 ÷ 3 = 0.15 or 15%.Thus, the rate of depreciation = 15%.AlternativelyCost Price Rs.1,20,000WDV Rs.66,000Total depreciation for 3 years 54,000; Depreciation per year Rs. = Rs.18,000Rate of Depreciation = Rs. = 15%Rs.1,20,000Rs.66,00054,000318, 000 x 1001, 20, 000< TOP >10. Answer : (a)Reason :and the amounts mentioned in other alternatives are not correct.Credit balance as per bank column of cash book Rs.13,500Add: Bank interest on overdraft debited in pass book Rs. 2,100Cheques deposited but not collected by bank Rs. 5,000Debit balance as per pass book Rs.20,600< TOP >11. Answer : (e)Reason :Opening balance of Sundry debtors Rs. 45,000Add: Credit sales Rs.4,25,000Rs.4,70,000Less: Cash collected Rs.4,00,000Rs. 70,000Less: Closing balance of sundrydebtors Rs. 50,000Bad debts Rs. 20,000< TOP >

12. Answer : (c) < TOP >Reason :Opening stock Rs. 40,000Add: Purchases Rs.2,00,000Rs.2,40,000Less: Closing stock Rs. 50,000Cost of goods sold Rs.1,90,00013. Answer : (d)Reason :Particulars Rs.Balance as per banks statement (overdraft) 12,500Less: Cheque returned but not entered in the cash book 2,800Balance as per cash book (overdraft) 9,700< TOP >14. Answer : (c)Reason : Let the profit = 100%Commission = 5%105%Amount of commission payable to manager = Rs.1,89,000 × 105% = Rs.9,0005%< TOP >15. Answer : (d)Reason : The conservatism concept states that the revenues are to be recognized when they are certain and lossesare to be considered when they are probable. Thus, the statement in alternative (d) is true. Thestatements in other alternatives are false since, The losses from the sale of capital assets are to bededucted from revenue to ascertain the net income (a) Going concern pre-supposes that the assets arecategorized into fixed and current and the non-monetary assets are to be recorded at the historical costand not at market value (b) The consistency concept facilitates the comparison of the results of oneaccounting period with that of the past (c) and the system of recording transactions based on dual aspectconcept is double entry system and not the double account system (e). Hence, the correct answer is (d).< TOP >

16. Answer : (c)Reason : Acid test ratio or quick ratio is a liquidity ratio which is an indicator of short term solvency of abusiness. Hence © is the correct answer. The ratios mentioned in other alternatives do not indicate theshort term solvency of a business and are not the correct answers.< TOP >17. Answer : (b)Reason : Called up capital is the amount on the shares which is actually demanded by the company to be paid.However, there may be some shareholders who may make default in the payment. The money due fromthem is called calls-in-arrears. This amount should be deducted from the called up capital to arrive atthe paid-up capital. Thus, (b) is the correct answer.< TOP >18. Answer : (a)Reason : Forfeited shares can be re-issued at a premium. Thus, the statement in alternative (a) is false. Thestatements in other alternatives are true-, if share premium is already received, share premium accountcannot be debited with the amount of premium on forfeiture of shares; Shares can be issued a discount,only after one year from the commencement of business; Share premium can be utilized only specificpurposes as per the provisions of section 78 of the Companies Act and it cannot be utilized to redeempreference shares; The forfeited shares cannot be reissued for a loss more than the gain on those shares.< TOP >19. Answer : (d)Reason : If accrued commission is shown on the debit side list of balances in the trial balance, it indicates that itis already adjusted in the commission received /receivable and it does not require any adjustment in theprofit and loss account. It directly appears as a current asset in the balance sheet. Hence (d) is true< TOP >20. Answer : (c)Reason : The maximum amount beyond which a company is not

allowed to raise funds by issue of shares iscalled nominal capital or authorized capital. The issued capital is that part of the nominal capital issuedto the public and subscribed capital is that part of the issued capital which is subscribed by the public.Paid up capital is the amount which is paid-up by the shareholders. Reserve capital is that capital which< TOP >will be called-up only in case of liquidation. Thus, alternative (c) is the correct answer.21. Answer : (e)Reason : Discount allowed on re-issue of forfeited shares is debited to forfeited shares account. It cannot bedebited to discount on re-issue of shares, since there is no such account maintained, it is not a usualdiscount to be debited to (b) Profit and loss account. The share premium account (c) can be debitedonly for the purposes as per the provisons of the Compnaies Act. The discount on issue of shares (d)can be debited only in the event of issue of shares at a discount originally. Thus, (e) is the correctanswer.< TOP >22. Answer : (c)Reason : The company may receive from the shareholders the amount uncalled on the shares held by them eventhough the amount is not called for. In such a case the company is compelled to pay interest on the callsin advance at prescribed rate from the date of receipt of advance to the date of appropriation i.e. the datewhen the call is made and the advance received is appropriated from calls in advance account to therelevant call account.< TOP >23. Answer : (a)Reason : Sinking fund is created out of profit. It is the part of profit and should be listed under the heading“Reserves and Surplus” and not under “unsecured loans”. Loans and advances from subsidiaries, shortterm loans and advances from banks, loans and advances from others

and fixed deposits are unsecuredloans.< TOP >24. Answer : (b)Reason : Share premium should not be used for redemption of preference shares whereas they can be used toprovide for premium on redemption of preference shares or debentures, to issue bonus shares, to writeoffpreliminary expenses and discount on issue of shares.< TOP >25. Answer : (b)Reason : The shares were issued at a discount of 10% i.e. they were issued for Rs.90 per share.Rama failed to pay the final call of Rs.30. Hence he has paid Rs.60 (Rs.90 – Rs.30).The amount to be credited to shares forfeited account is Rs.60 x 300 shares = Rs.18,000< TOP >26. Answer : (c)Reason : Value of right =Where r = No of rights issuedN = No. of existing sharesM = Market priceS = Issue price of rights= Rs.100 + 160% premium = Rs.100 + Rs.160 = Rs.260∴Value of rights = = Rs.80r (M S)N r − +

4 (440-260)4+5

< TOP >27. Answer : (c)Reason : The share capital of the subsidiary company does not appear in the Consolidated Balance Sheet (c) isthe correct statement and the share capital of the subsidiary company is not shown in the consolidated

balance sheet. and other statements are not true. A company will be deemed to be a holding company ofanother if it holds more than 50 percent of both equity and preference share capital is not true becauseit should hold share only in equity capital and preference share capital will not be considereed fordeciding the cost of control. and (a) is not the correct answer.b. The financial year of the holding company and its subsidiary company must end on the same dateis not the correct answer because it need not be on the same date.d. The inter company owing will be shown in the Consolidated Balance Sheet is incorrect becauseintercompany owing are eliminated in the consolidated balance sheet and hence it is not thecorrect answer.e. Minority of the subsidiary is entitled to proportionate share in capital profits only is incorrectbecause they are entitled for both capital profits and revenue profit and there is no differencebetween the two profits in computation of minority interest. Thus, alternative © is the correctanswer.< TOP >28. Answer : (d)Reason : Profit for the year 2002-2003 = Rs.1,50,000 – Rs.90,000 = Rs.60,000Profit for 8 months (from April 01, 2002 to December 01, 2002)=Share of capital profit of H Ltd. = (90,000 + 40,000) x 60% = Rs.78,000.60,000 8 Rs.40,00012× =< TOP >29. Answer : (d)Reason : The profit on cancellation of debentures transferred to capital reserve is Rs.13,000On purchase of debentures, the journal entry to be made isOn cancellation of the debentures, the journal entry to be made isRs. Rs.Own debentures a/c Dr 1,87,000

Interest on debentures a/c Dr 9,000To Cash a/c 1,96,000Rs. Rs.18% Debentures a/c Dr 2,00,000To Own debentures 1,87,000To Capital Reserve 13,000< TOP >30. Answer: (b)Reason: Weighted average profit∴Weighted average profit = Rs.26,10,000 ÷ 6 = Rs.4,35,000Year 1 Rs.3,30,000 × 1 Rs. 3,30,000Year 2 Rs.4,20,000 × 2 Rs. 8,40,000Year 3 Rs.4,80,000 × 3 Rs.14,40,0006 Rs.26,10,000< TOP >

Financial Accounting (MB131): April 2005

Financial Accounting (MB131): April 2005

• Answer all questions.• Marks are indicated against each question.1. Which of the following is a leverage ratio?(a) Debt-Equity ratio (b) Current ratio ( c) Quick ratio(d) Earning power (e) Inventory turnover ratio.(1 mark)< Answer >2. Amortization of unidentified intangible assets is in terms of(a) Conservatism concept (b) Going concern concept(c) Matching concept (d) Time period concept(e) Business entity concept.(1 mark)< Answer >3. The following Trial Balance pertaining to John Vicky as at March 31, 2005 was prepared by aninexperienced accountant:Trial Balance of John Vicky as at March 31, 2005Particulars Debit (Rs.) Credit (Rs.)Capital (1st April, 2004) 89,000

Drawings 10,000Stock (1st April, 2004) 37,000Purchases 2,31,250Sales 3,94,000Motor vehicles 14,500Cash in hand 1,350Sundry creditors 49,760Sundry debtors 1,39,700Bank overdraft 9,000Administrative expenses 76,360Office equipment 35,000Carriage outward 2,310Returns inward 2,050Provision for bad debts 4,250Returns outward 3,160Discount allowed 2,800Discount received 3,150Total 5,52,320 5,52,320Though the Trial Balance has tallied, it has certain errors which were subsequently rectified. The totalof the corrected Trial Balance as on March 31, 2005 is(a) Rs.5,52,320 (b) Rs.4,64,200 (c) Rs.5,55,510 (d) Rs.5,43,200 (e)Rs.5,03,440.(2 marks)< Answer >4. In contract accounting, the percentage of completion method is an exception to the(a) Matching principle (b) Going concern principle(c) Historical cost principle (d) Business entity principle(e) Revenue recognition principle.(1 mark)< Answer >5. In which of the following areas, will the accounting policies tend to be uniform among the enterprises?(a) Method of providing Depreciation(b) Valuation of Inventories (c) Treatment of Goodwill(d) Treatment of Contingent Liabilities (e) Accounting for Cash.(1 mark)< Answer >2

6. Consider the following data pertaining to Sun Ltd. for the month of March 2005:Particulars Rs.Purchase of goods for resale 2,10,000Freight in 30,000Freight out 25,000Returns outward 22,000Cost of goods available for sale is(a) Rs.1,88,000 (b) Rs.2,10,000 (c) Rs.2,18,000(d) Rs.2,35,000 (e) Rs.2,40,000.(1 mark)< Answer >7. Consider the following information pertaining to Blue Sky Ltd. for the year 2004-2005:Particulars 1st April 2004 31st March 2005Inventory Rs.52,200 Rs.65,800Sundry debtors Rs.37,000 Rs.60,000Total credit sales made during the year were of Rs.6,75,000. The amount of discount allowed to thesundry debtors during the period was Rs.2,800.Cash collected from the sundry debtors during the year was(a) Rs.7,22,000 (b) Rs.6,95,200 (c) Rs.6,75,000(d) Rs.6,49,200 (e) Rs.5,14,200.(2 marks)< Answer >8. On March 31, 2005, the overdraft balance as per the bank pass book of Mr. Suresh was Rs.13,880. Thebalance did not agree with the balance as per cash book. On scrutiny, the following discrepancies arenoticed:• Interest on overdraft for the quarter ended March ’05 is Rs.480 (not recorded in the cash book).• Cheques deposited in the bank, but not cleared aggregate to Rs.1,800.• Cheques issued but not presented are for Rs.2,350.• A cheque for Rs.1,000 which was discounted with the bank earlier was dishonoured. Mr. Sureshwas not aware of the dishonour.The balance as per cash book as on March 31, 2005 is(a) Rs.12,950 (Credit) (b) Rs.14,810 (Credit)(c) Rs.13,810 (Debit) (d) Rs.13,950 (Debit) (e) Rs.12,950 (Debit).

(2 marks)< Answer >9. Carriage inward refers to the cost of transportation for(a) Purchase of materials (b) Sale of products (c) Returns outward(d) Return of unsold goods (e) Newly acquired machinery.(1 mark)< Answer >10. Advance received from customers is an(a) Item of current liability (b) Item of non-current asset(c) Item of contingent liability (d) Item of non-cash transaction(e) Item of inventory.(1 mark)< Answer >11. T.M. & Co. a dealer in shares, purchased shares. This was debited to Investment account. This is a/an(a) Error of commission (b) Error of omission(c) Error of principle (d) Error of compensation(e) Correct recording of transaction (No error).(1 mark)< Answer >12. Consider the following data pertaining to M/s. Ramu Enterprises as on March 31, 2005:Particulars Rs.Credit sales 1,40,000< Answer >3Credit purchases 20,000Cash sales 20,000Cash purchases 70,000Wages paid 5,000Returns inward 3,000Returns outward 2,000Carriage inward 1,000Carriage outward 1,000Gas, water and fuel 2,000Raw materials destroyed by fire 2,000Additional Information:Particulars As on April 01, 2004 As on March 31, 2005Rs. Rs.Inventory 27,000 40,000

Outstanding wages 500 700Gross profit of M/s.Ramu Enterprises for the year ended March 31, 2005 is(a) Rs.73,800 (b) Rs.75,800 (c) Rs.74,800(d) Rs.76,200 (e) Rs.75,200.(2 marks)13. As per the Accounting Standard, which of the following is/are not extra-ordinary item/s to anenterprise?I. Attachment of its property. II. Destruction by fire of factory building.III. Insolvency of a debtor. IV. Factory building collapsed in earthquake.(a) Only (III) above (b) Both (II) and (III) above(c) Both (I) and (IV) above (d) Both (I) and (III) above(e) All (I), (II), (III) and (IV) above.(1 mark)< Answer >14. Which of the following is/are non-current liability(ies)?I. Long term loans. II. Declared dividend.III.Bank overdraft. IV.Sundry creditors. V. Debentures.(a) Only (V) above (b) Only (I) above(c) Both (I) and (V) above (d) (I), (II) and (IV) above(e) (I), (III) and (V) above.(1 mark)< Answer >15. Which of the following transactions does not change the total amount of liabilities in the balance sheet?(a) Purchase of office furniture on credit(b) Payment of bank loan (c) Issue of debentures(d) Acceptance of bills from creditors (e) Issue of preference shares.(1 mark)< Answer >16. Which of the following statements is false?(a) Prepaid expenses are shown on the asset side(b) Income received in advance is shown on the asset side(c) Income earned but not received is shown on the asset side(d) Income accrued but not due is shown on the asset side(e) Outstanding expenses are shown on the liability side.(1 mark)< Answer >17. Which of the following is not true about Fixed Assets?(a) They are acquired for using them in the conduct of business operations

(b) They are not meant for resale to earn profit(c) They can easily be converted into cash(d) Depreciation at specified rates is to be charged on most of the Fixed Assets(e) Their utility is not confined to one accounting period.(1 mark)< Answer >418. Which of the following is not an objective of maintaining books of accounts?(a) Maintaining a permanent, accurate and complete record of business transactions(b) Maintaining records of incomes, expenses and losses in such a way that the net profit or loss forany specified period may be ascertained(c) Increasing the profit or reducing the loss made by the enterprise(d) Maintaining records of assets and liabilities in such a way that the financial position of thebusiness at any point can easily be ascertained(e) Providing required information for legal and tax purposes.(1 mark)< Answer >19. In a manufacturing company, which of the following systems is called a product costing system?(a) Perpetual inventory system (b) Periodic inventory system(c) Accrual system (d) Weighted average system(e) Specific identification system.(1 mark)< Answer >20. Which of the following costs is not directly related to a specific contract?(a) Site labor cost(b) Cost of moving plant and equipment to and from a site(c) Research and Development cost(d) Supervision cost(e) Cost of materials used.(1 mark)< Answer >21. Which of the following methods of valuation of inventory is based on the assumption that costs are

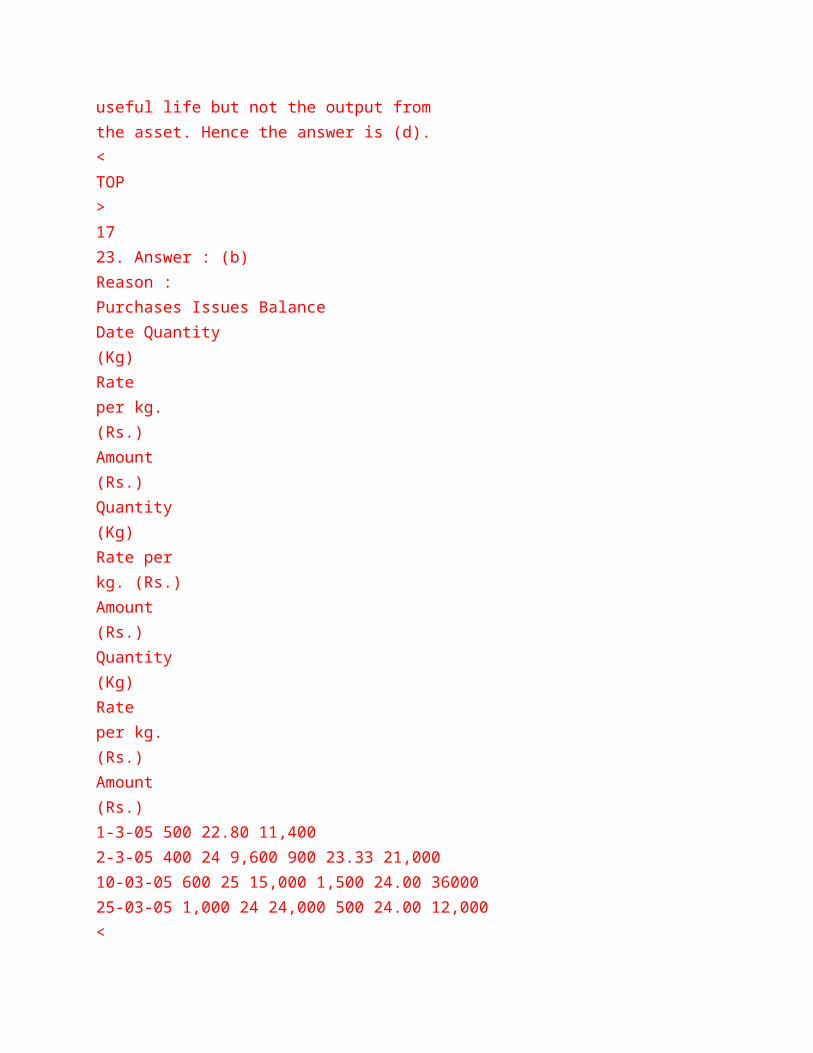

charged against revenue in the order in which they occur?(a) FIFO method (b) LIFO method(c) Weighted average method (d) Moving average method (e) Base stock method.(1 mark)< Answer >22. Which of the following methods of depreciation takes into consideration the output from the asset?(a) Straight line method (b) Written down value method(c) Sum-of-the-years’ digits method (d) Units-of-production method(e) Double declining method.(1 mark)< Answer >23. Consider the following data pertaining to Lairs Ltd. for the month of March 2005:Date Purchases Issues BalanceQuantity (Kg.) Rate (Rs.) Quantity (Kg.) Quantity (Kg.) Rate (Rs.)01-03-2005 500 22.8002-03-2005 400 2410-03-2005 600 2525-03-2005 1,000If the company uses weighted average method for inventory valuation, the value of inventory as onMarch 31, 2005 is(a) Rs.11,967 (b) Rs.12,000 (c) Rs.12,500(d) Rs.11,400 (e) Rs.36,000.(2 marks)< Answer >24. The cost of goods sold does not include(a) Indirect labour (b) Power and light(c) Storage expenses (d) Advertising expenses (e) Excise duty.(1 mark)< Answer >25. Renewal fee for patents is a(a) Capital expenditure (b) Revenue expenditure(c) Deferred revenue expenditure (d) Development expenditure(e) Contingent expenditure.< Answer >5(1 mark)

26. Cost of raw-material is equal to its(a) Purchase price(b) Purchase price plus duties and taxes(c) Purchase price plus duties, taxes and freight inward(d) Purchase price plus duties, taxes and freight inward minus discount(e) Purchase price plus duties, taxes and freight inward minus discount and duty draw back.(1 mark)< Answer >27. Which of the following does not come under fixed assets?(a) Buildings (b) Furniture (c) Long term investment(d) Equipment (e) Machinery.(1 mark)< Answer >28. When goods are sold subject to the approval by the buyer, revenue should be recognized when the(a) Goods have been formally accepted by the buyer(b) Payment has been received from the buyer(c) Buyer has seen the sample and approved the same(d) Goods have been sent to the buyer(e) Goods have been received by the buyer, irrespective of his approval.(1 mark)< Answer >29. For a car manufacturing company, which of the following is not a fixed asset?(a) Land and Building (b) Machinery (c) Office furniture(d) Stock of cars (e) Patents.(1 mark)< Answer >30. Payment of Municipal taxes is a(a) Capital expenditure (b) Revenue expenditure(c) Capital receipt (d) Revenue receipt(e) Development expenditure.(1 mark)< Answer >31. Which of the following expenses is capital in nature?(a) Purchase of a truck (b) Replacement of old tyres and tubes(c) Repairs to furniture (d) Payment of Road tax(e) Payment of insurance premium.(1 mark)

< Answer >32. In a funds flow statement prepared on working capital basis, a short term loan repaid by theorganization(a) Is shown as a source of working capital(b) Is shown as an increase in cash(c) Is shown as a decrease in cash(d) Does not affect the working capital(e) Is not shown either as a source or a use of funds.(1 mark)< Answer >33. In accounting, window-dressing implies(a) Showing the real position of the business(b) Showing a worse position of the business(c) Showing a better position than the true and fair view of the business(d) Making excess provisions for the expenses of the business(e) Showing a true and fair view.(1 mark)< Answer >34. Dinakar operates a garment store in a hired premises at a rent of Rs.1,20,000 per annum. The owner ofthe premises, who has recently completed her fashion-designing course, wishes to purchase the garment< Answer >6the premises, who has recently completed her fashion-designing course, wishes to purchase the garmentstore. The details of the business of Dinakar are as under:• The profit for the year 2004-2005 is Rs.2,30,000.• The capital employed by Dinakar is Rs.20,00,000.• The value of the premises is Rs.4,00,000.If the normal return on capital employed is 12%, the super profit is(a) Rs.58,000 (b) Rs.62,000 (c) Rs.1,10,000(d) Rs.1,20,000 (e) Rs.1,78,000.(3 marks)35. Which of the following are not current assets?(a) Inventories (b) Bills receivable(c) Accounts receivable (d) Prepaid expenses (e) Incomes received in advance.(1 mark)

< Answer >36. Accounting Standard Board was set up by the(a) Government of India(b) Institute of Chartered Accountants of India(c) Institute of Costs and Works Accountants of India(d) Reserve Bank of India(e) Securities and Exchange Board of India.(1 mark)< Answer >37. RSV Ltd. acquires the following assets of BC Ltd. paying a sum of Rs.22,50,000:Particulars Rs.Cash at bank 23,750Cash on hand 12,250Accounts receivable 86,200Other identifiable assets 16,00,000If Accounts Receivable are believed to have a realizable value of Rs.80,000 and other identifiable assetsare estimated to have market value of Rs.18,50,000, the amount of goodwill to be recorded in the booksof RSV Ltd. is(a) Rs.5,34,000 (b) Rs.2,90,200 (c) Rs.2,84,000(d) Rs.5,40,200 (e) Rs.3,20,000.(2 marks)< Answer >38. An inexperienced book-keeper of M/s.Volga & Co. has drawn up the following trial balance of the firmfor the year ended March 31, 2005:Trial Balance as on March 31, 2005Particulars DebitRs.Particulars CreditRs.Provision for doubtful debts 2,000 Capital 45,910Bank overdraft 16,540 Sundry creditors 16,370Sundry debtors 29,830 Discount allowed 7,330Discount received 2,520 General expenses 8,290Drawings 12,000 Returns inward 3,300Office furniture 21,550 Cash sales 60,800Purchases 1,09,230 Credit sales 1,08,020

Rent and rates 3,140Salaries 25,200Opening stock 24,180Provision for depreciation onoffice furniture 3,640Total 2,49,830 Total 2,50,020Subsequently another trial balance was drawn and the residual difference was placed to a suspenseaccount. The amount debited/credited to suspense account was< Answer >7(a) Rs.190 (debit) (b) Rs.530 (credit)(c) Rs.11,750 (debit) (d) Rs.4,170 (debit) (e) Rs.11,750(credit).(2 marks)39. Silver Coats Ltd. invited applications for 1,00,000 equity shares of Rs.10 each at a premium of Rs.2 per share.The entire issue was underwritten by three underwriters in the following percentages:Anil 30%Vimal 40%Sunil 30%The details of marked and unmarked applications received are:Marked applications of Anil 22,000 sharesVimal 24,000 sharesSunil 28,000 sharesUnmarked applications 16,000 sharesThe final liability of Vimal in terms of number of shares is(a) Nil (b) 9,600 (c) 3,200 (d) 16,000 (e) 8,000.(2 marks)< Answer >40. Which of the following error will not be disclosed by a Trial Balance?(a) Posting of one aspect of a transaction twice(b) Omission of recording a transaction(c) Error in balancing of ledger accounts(d) Omission of listing an account balance(e) Overcasting / undercasting of a subsidiary book.(1 mark)< Answer >41. If the forfeited shares are issued at a discount, the amount of discount shall be debited to

(a) Profit and loss account (b) Capital reserve account(c) Share forfeiture account (d) Share premium account(e) Share capital account.(1 mark)< Answer >42. The primary means of communicating comprehensive accounting information to the users is(a) Prospectus (b) Trial balance (c) Bank Reconciliation Statement(d) Financial statements (e) Statement of cash flow.(1 mark)< Answer >43. After preparation of the Profit and Loss Account, the following are extracted from the books ofUniverse Ltd. as on March 31, 2005:Particulars Rs. Particulars Rs.Called-up share capital 5,00,000 Plant and machinery 2,20,000Land and building 4,90,000 Investments 60,000Secured loans 3,00,000 Calls-in-arrear 30,000Term loan from Syndicate Bank 1,00,000 Capital reserve 90,000Sundry creditors 90,000Sundry debtors 1,20,000Profit and loss account(credit balance) 50,000Stock 96,000 Outstanding expenses 500Loans to employees 50,000Provision for doubtful debts 10,000Insurance premium paid inadvance 1,200Interest received in advance 700 Cash 4,000Bank balance (Debit) 40,000 Preliminary expenses 30,000The total of the liabilities side of the balance sheet is(a) Rs.11,01,200 (b) Rs.11,00,200 (c) Rs.11,31,200(d) Rs.11,41,200 (e) Rs.11,01,900.< Answer >8(2 marks)44. The authorized capital of Chand Ltd. is 1,00,000 shares of Rs.10 each. On April 10, 2004, 50,000shares are issued for subscription at a premium of Rs.2 per share. The share money is payable as

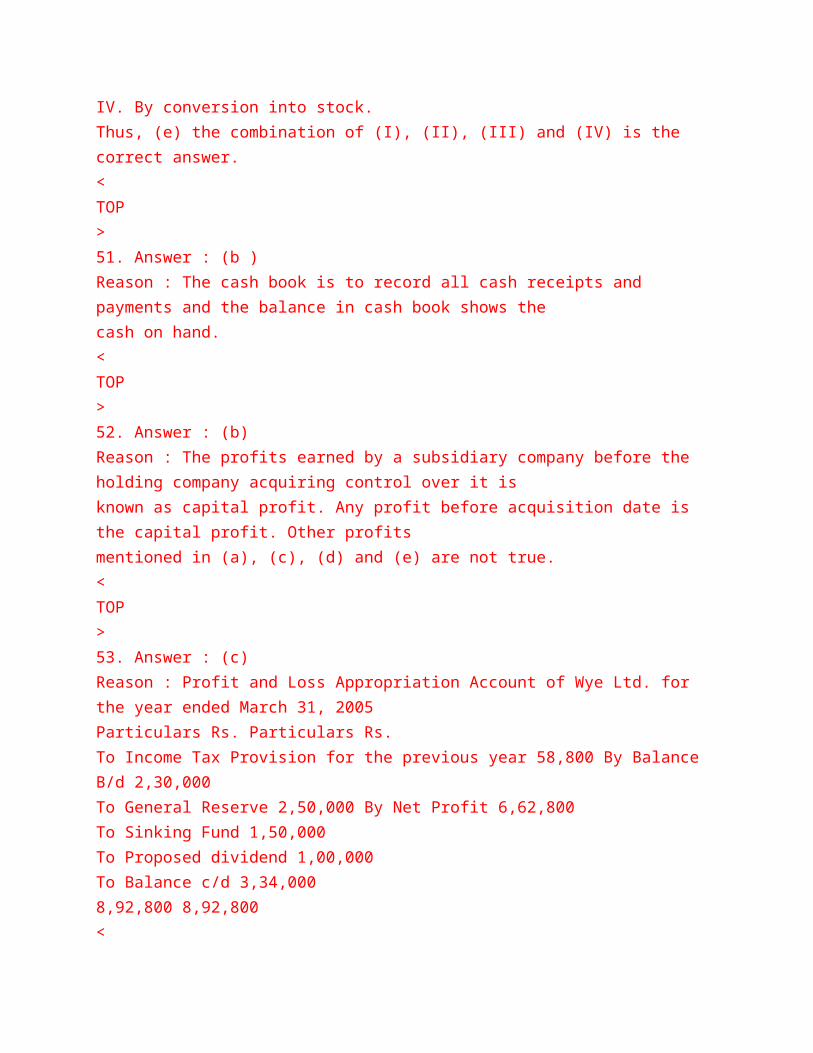

follows:Rs.5 (including the premium of Rs.2) with applicationRs.3 on allotmentRs.2 on first callRs.2 on final call.The subscription list closed on May 11, 2004 and the directors proceeded with allotment on May 18,2004. The shares are fully subscribed and the application money (including the premium) is received infull. The allotment money is received by June 30, 2004, except as regards 500 shares.The first call and the final call money is received by September 30, 2004, and December 31, 2004,respectively, except the final call money on 200 shares which is not received.Assuming that there are no other transactions, the cash balance as on December 31, 2004 is(a) Rs.8,46,100 (b) Rs.6,00,000 (c) Rs.5,96,100(d) Rs.4,96,000 (e) Rs.5,96,000.(2 marks)< Answer >45. Which of the following statement(s) is/are false?I. An equity share always carries the voting right.II. In case of equity shares, the dividend is paid at a fixed rate during the lifetime of the company.III. The share premium received on issue of shares cannot be utilized in writing off the preliminaryexpenses of the company.(a) Only (I) above (b) Only (II) above(c) Both (I) and (II) above (d) Both (I) and (III) above(e) Both (II) and (III) above.(1 mark)< Answer >46. Rights shares are the shares(a) Issued by a newly formed company(b) Legally issued to the public at large(c) Offered to the existing equity shareholders(d) That have a right of redemption(e) That have a right to cumulative dividends.(1 mark)

< Answer >47. A company issued 14% debentures of Rs.10,00,000 at a discount of 10%. The discount on issue ofdebentures will be treated in the account books as(a) Capital expenditure (b) Revenue expenditure(c) Deferred revenue expenditure (d) Capital loss(e) Outstanding expenditure.(1 mark)< Answer >48. The Issued Share Capital of Marval Ltd. is Rs.12,00,000 divided into 1,20,000 shares which wereissued at a premium of 100%. The company offers two shares for every three shares held to its existingshareholders. If the rights issue price is Rs.410 per share and the market value at the time of rights issueis Rs.560 per share, the value of right is(a) Rs.60 (b) Rs.20 (c) Rs.150 (d) Rs.410 (e) Rs.560.(1 mark)< Answer >49. The difference between par value and issue price below the par value of share, is called(a) Share premium (b) Trade discount(c) Commission on issue of shares (d) Discount on issue of shares (e) Cash discount.(1 mark)< Answer >50. Debentures can be redeemedI. At par.II. At a premium.< Answer >9III. At a discount.IV. By conversion into stock.(a) Only (I) above (b) Both (I) and (II) above(c) Both (I) and (III) above (d) (I), (II) and (III) above(e) (I), (II), (III) and (IV) above.(1 mark)51. The balance of cash book signifies(a) Net income (b) Cash in hand (c) Net sales(d) Net purchases (e) Net expenditure.

(1 mark)< Answer >52. The profits earned by a subsidiary company before acquisition by a holding company are known as(a) Revenue profits (b) Capital profits (c) Super profits(d) Average profits (e) Future maintainable profits.(1 mark)< Answer >53. On April 01, 2004, the Profit and Loss Appropriation account of Wye Ltd. had a balance ofRs.2,30,000. During the year 2004-05, the company earned a net profit of Rs.6,62,800 and• The adjustment of income tax provision for the year 2003-04 amounted to Rs.58,800. Thecompany has a policy to transfer every year a sum of Rs.2,50,000 to general reserve.• The sinking fund for redemption of debentures is created on April 01,2002 and the annualinstallment is Rs.1,50,000.• The company declared a dividend of 20% on Equity Share Capital of 5,000 fully paid shares ofRs.100 each issued at Rs.90 each.After effecting the above, the balance in the Profit and Loss Appropriation account of the company ason March 31, 2005 is(a) Rs.3,24,000 (b) Rs.3,92,800 (c) Rs.3,34,000(d) Rs.3,82,800 (e) Rs.4,84,000.(2 marks)< Answer >54. Desktop Publishing Ltd. began its operations on July 01,2004. The following accounts and balanceswere contained in the adjusted trial balance of the company as on March 31, 2005:Equity Share Capital Rs.95,500Declared Dividends Rs.9,550Fees earned Rs.48,200Rent paid Rs.13,200Salaries paid Rs.5,750Income Tax paid Rs.1,100Electricity Rs.3,700

Pre paid rent Rs.1,800Cash on hand Rs.10,600Sundry assets Rs.1,17,650.The amount of profit earned by the company for the year ended March 31, 2005 was(a) Rs.13,100 (b) Rs.24,450 (c) Rs.22,650 (d) Rs.26,250 (e) Rs.16,700.(2 marks)< Answer >55. The Adams Ltd. paid a dividend of Rs.1,20,000 at the end of March 31, 2005. On April 01, 2004, therewas Rs.40,000 of dividends in arrears. The company’s capital structure consists of 5,000 9%,cumulative preference shares of Rs.100 each and 10,000 equity shares of Rs.30 each, both fully paid.How much did Adams Ltd. pay as dividends to its equity shareholders for the year 2004 - 05?(a) Percentage not given-Insufficient data (b) Rs.75,000(c) Rs.45,000 (d) Rs.35,000 (e) Rs.80,000.(2 marks)< Answer >56. The following information is extracted from the books of Sun Pharmacy Ltd.:Purchases made during the year Rs.7,80,000Sales made during the year Rs.13,22,000Opening stock Rs.1,90,000< Answer >10Closing stock Rs.2,17,000• Goods worth Rs.18,000 were distributed as free sample and no entry is made to this effect.• A sale of Rs.28,000 has been credited to purchases account.• Carriage outward amounted to Rs.2,000.Considering the above, gross profit of the company for the year was(a) Rs.5,85,000 (b) Rs.5,87,000 (c) Rs.5,89,000(d) Rs.6,15,000 (e) Rs.6,17,000.(2 marks)57. The system of accounting to be followed by a company(a) Must be the same as of all other companies(b) Can be different from the system followed by other companies(c) Must be disclosed if it is different from the recognized policy

(d) Must be on accrual basis and according to the double entry system of accounting(e) Can be on cash basis of accounting on the approval of the Registrar of Companies.(1 mark)< Answer >58. Pawan Ltd. has been incorporated with an Authorised Capital of Rs.10,00,000 divided into 1,00,000equity shares of Rs.10 each. The company issued 65,000 shares of Rs.10 each to the public forsubscription payable as under:On application Re.1On allotment Rs.2On first call Rs.2On second call Rs.2On final call Rs.3The public has subscribed for 60,000 shares. The directors of the company made first call of Rs.2 pershare to carry on the business of the company. Out of these, one shareholder holding 5,000 sharesfailed to pay the call money of Rs.2 per share.The company made profit of Rs.58,500 during the financial year and the directors declared a dividendof 6% to the shareholders.The amount of capital that is to be considered for paying dividends is(a) Rs.5,00,000 (b) Rs.6,50,000 (c) Rs.3,00,000(d) Rs.6,00,000 (e) Rs.2,90,000.(2 marks)< Answer >59. The following information is taken from the books of Splendid Ltd.:On April 4, 2005 the company issued 7% Debentures having a face value of Rs.12,00,000 at a discountof 2.5%. On April 12, the company further issued 25,000 8% Preference shares of Rs.100 each. OnApril 29, the company redeemed the existing 30,000 6% Preference shares of Rs.100 each at a premiumof 5% together with one month dividend thereon. Bank balance as on March 31, 2005 wasRs.29,25,000.The Bank balance as on April 30, 2005 will be

(a) Rs.32,30,000 (b) Rs.33,15,000 (c) Rs.33,30,000(d) Rs.33,45,000 (e) Rs.34,30,000.(2 marks)< Answer >60. Once the unclaimed dividend is transferred to General Revenue Account of the Central Government,any shareholder entitled to such dividend may claim it from(a) The Reserve Bank of India (b) The Central Government(c) The Company (d) The Registrar of companies(e) Any Scheduled Bank.(1 mark)< Answer >61. The balance in the creditors account of a company as at the beginning of the month of March 2005 wasRs.3,40,000. During the month,• A sum of Rs.1,85,000 was paid to the creditors .• Goods purchased from the suppliers amounted to Rs.2,47,000.< Answer >11• Goods returned to them as defective were of Rs.8,000.• They allowed a sum of Rs.4,800 as cash discount.• A bill for Rs.8,000 accepted by the company in favour of a creditor could not be honoured on thedue date and hence was dishonoured on March 20, 2005.The balance in the creditors account as on March 31, 2005 was(a) Rs.4,02,000 (b) Rs.3,94,200 (c) Rs.3,97,200(d) Rs.4,05,200 (e) Rs.4,50,020.(2 marks)62. The books of Sahara Ltd. revealed the following information:Particulars Rs.Opening inventory 6,00,000Purchases during the year 2004-2005 34,00,000Sales during the year 2004-2005 48,00,000On March 31, 2005, the value of inventory as per physical stock-taking was Rs.3,25,000. Thecompany’s gross profit on sales has remained constant at 25%. The management of the companysuspects that some inventory might have been pilfered by a new employee. What is the estimated costof missing inventory?

(a) Rs.75,000 (b) Rs.25,000 (c) Rs.1,00,000(d) Rs.1,50,000 (e) Rs.2,25,000.(2 marks)< Answer >63. ABC Ltd. maintains the inventory records under perpetual system of inventory. Consider the followingdata pertaining to inventory of ABC Ltd. held for the month of March 2005:Date Particulars Quantity Cost Per unit (Rs.)March 1 Opening inventory 15 4004 Purchases 20 4506 Purchases 10 460If the company sold 32 units on March 24, 2005, closing inventory under FIFO method is(a) Rs.5,200 (b) Rs.5,681 (c) Rs.5,800 (d) Rs.5,850 (e) Rs.5,950.(2 marks)< Answer >64. Consider the following data pertaining to Taurus Ltd.Average Trading Profit Rs.2,58,900Normal Profits Rs.2,23,800Where in the goodwill was valued on the basis of 3 years’ purchase of super profits. Further, it has beenresolved by the company to amortise the goodwill over a period of five years.The journal entry to be passed for amortisation of goodwill every year is(a) Profit and Loss a/c. Dr. Rs.21,060To Goodwill a/c. Rs.21,060(b) Depreciation a/c. Dr. Rs. 7,020To Goodwill a/c. Rs.7,020(c) Goodwill a/c. Dr. Rs.21,060To Profit and Loss a/c. Rs.21,060(d) Profit and Loss a/c. Dr. Rs. 7,020To Goodwill a/c. Rs.7,020(e) General Reserve a/c. Dr. Rs.21,060To Goodwill a/c. Rs.21,060.(2 marks)< Answer >65. Which of the following is false with respect to goodwill?(a) Goodwill though caused by factors which cannot be easily and accurately quantified, must beassigned a value

(b) It is the present value of a firm’s anticipated excess earnings(c) It is the extra saleable value attached to a prosperous business beyond the intrinsic value of netassets< Answer >12(d) It is an identifiable intangible asset(e) It is like any other asset, a store of prospective revenue.(1 mark)66. M/s.Sunder Ltd. issued 80,000 equity shares of Rs.10 each, payable as under:On application Rs.3On allotment Rs.4On first call Rs.2On final call Rs.1The applications received for 1,20,000 shares were dealt with as under:• Applicants of 20,000 shares were allotted in full.• Applicants of 80,000 shares were allotted 60,000 shares pro-rata.• Applications for 20,000 shares were rejected.The amount available for adjustment towards allotment money is(a) Rs.1,20,000 (b) Rs.2,40,000 (c) Rs.60,000(d) Rs.1,80,000 (e) Rs.3,20,000.(2 marks)< Answer >67. Needs Ltd. issued 20,000 equity shares of Rs.100 each at a premium of 20% payable as under:On application Rs.50 (inclusive of premium)On allotment Rs.30On first call Rs.20On second and final call Rs.20Applications were received for 24,000 shares and the company has resolved to reject 4,000 applicationsin full and allot to 20,000 applicants in full. The journal entry passed at the time of receipt ofapplication money is(a) Bank account Dr. Rs.12,00,000To Share application account Rs.12,00,000(b) Share application account Dr. Rs.12,00,000To Share Capital account Rs.12,00,000(c) Bank account Dr. Rs.12,00,000

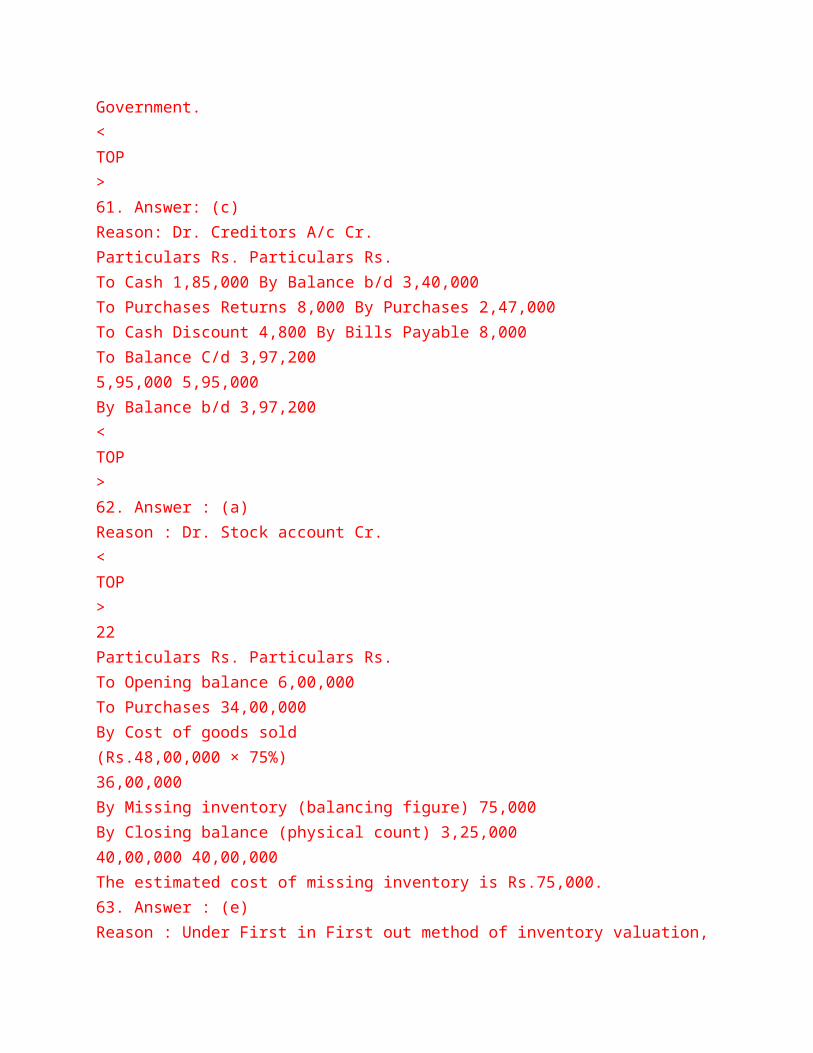

To Share Capital account Rs.12,00,000(d) Bank account Dr. Rs. 6,00,000To Share Capital account Rs. 6,00,000(e) Bank account Dr. Rs.10,00,000To Share Capital account Rs. 6,00,000To Share premium account Rs. 4,00,000.(2 marks)< Answer >68. When redeemable preference shares are due for redemption, the entry passed is(a) Debit Redeemable preference share capital account and Credit Cash account(b) Debit Redeemable preference share capital account and Credit Redeemable Preferenceshareholders account(c) Debit Redeemable Preference shareholders account and Credit Cash account(d) Debit Redeemable Preference shareholders account and Credit Redeemable preference sharecapital account(e) Debit Redeemable preference share capital account and Credit Capital redemption reserveaccount.(1 mark)< Answer >69. Which of the following statements is/are true?I. Discount on issue of debentures can be shown in the books of the accounts even after the life ofthe debentures.II. Capital profits can be used for converting partly paid shares to fully paid-up.III. Bonus issue of shares is not permitted unless the partly paid up shares, if any existing, are madefully paid.< Answer >13fully paid.(a) Only (I) above (b) Only (II) above(c) Both (I) and (II) above (d) Both (I) and (III) above (e) Both (II) and (III) above.

(1 mark)70. Traditionally, human resource is not taken as asset in the Balance Sheet of a business in recognition of,(a) Cost concept (b) Money measurement concept(c) Consistency concept (d) Business entity concept(e) Going concern concept.(1 mark)< Answer >71. A transaction of purchase of stationery of Rs.400 for cash has not been entered in the cashbook. This isan example of(a) Error of partial omission (b) Error of commission(c) Error of principle (d) Compensating error(e) Error of complete omission.(1 mark)< Answer >72. A firm sells goods at a gross margin of 25% on sales. Opening Stock was Rs.40,000 and closing stockwas Rs.30,000. Purchases during the period were Rs.1,10,000. What is the amount of Sales?(a) Rs.1,60,000 (b) Rs.1,20,000 (c) Rs.2,00,000 (d) Rs.1,50,000 (e) Rs.96,000.(2 marks)< Answer >73. Net worth consists ofI. Equity.II. General reserve.III. Capital reserve.IV. Profit and Loss account balance.(a) Only (I) above (b) Both (I) and (IV) above(c) Both (I) and (III) above (d) Both (I) and (II) above(e) All (I), (II), (III) and (IV) above.(1 mark)< Answer >74. Damaged inventory should be valued at(a) Nominal value (b) Market value(c) Net realizable value (d) Cost price or market price, whichever is lower(e) Acquisition cost.(1 mark)< Answer >

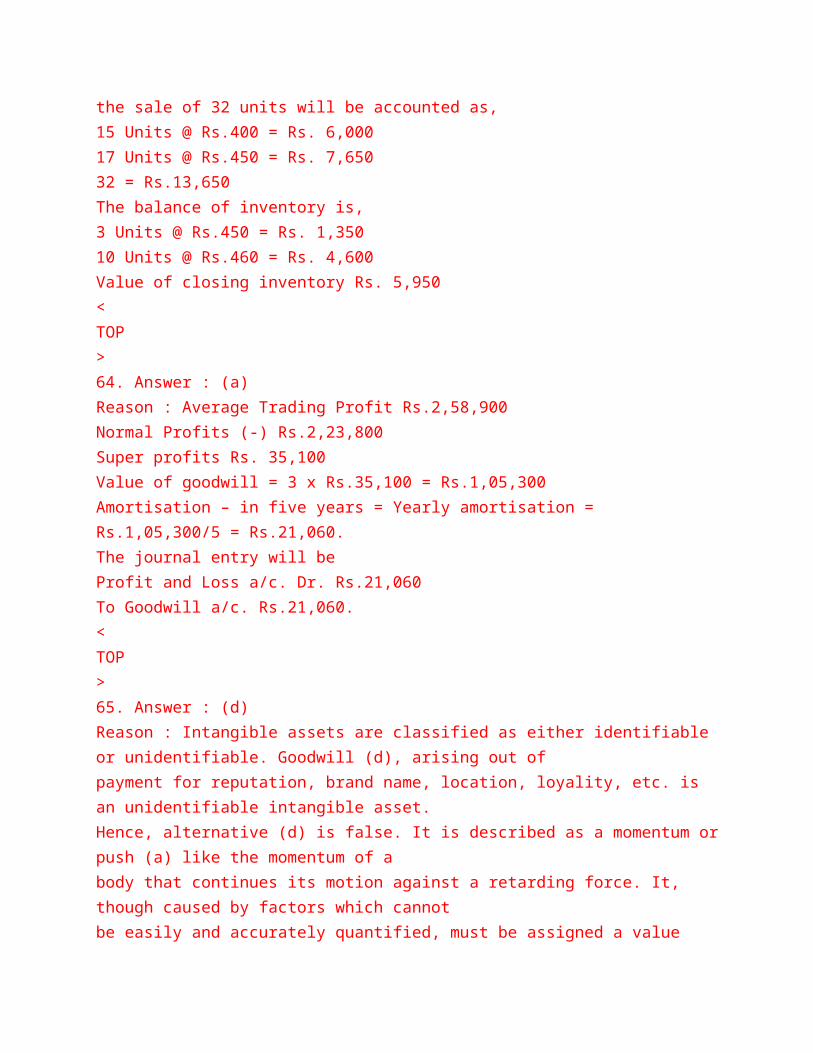

75. Which of the following expenses is not included in the acquisition cost of a plant and equipment?(a) Cost of site preparation(b) Delivery and handling charges(c) Installation costs(d) Professional fees in connection with the equipment(e) Financing costs incurred subsequent to the period after plant and equipment is put to use.(1 mark)< Answer >14

Suggested AnswersFinancial Accounting (MB131): April 20051. Answer : (a)Reason : Debt-Equity ratio is also called as leverage ratio. Thus, alternative (a) is the correct answer.Current ratio (b) and Quick ratio (c) are liquidity ratios and not leverage ratios. Earning power (d)and Inventory turnover ratio (e) are not leverage ratios. Therefore, alternative (a) is the correctanswer.<TOP>2. Answer : (c)Reason : Intangible assets are amortized like tangible fixed assets. If costs benefit more than one accountingperiod, they should be systematically and rationally allocated to all accounting periods. Matchingconcept involves recognizing costs as expenses on the basis of direct association with assets. Thusamortization of intangible assets is the systematic allocation of costs over several periods inrecognition of matching concept. The other concepts do not recognize allocation of costs of fixed

assets. Conservatism concept is not meant to introduce a bias into financial reporting. It is aprudent reaction to uncertainty to try to ensure that inherent risks in business are adequatelyconsidered. Going concern concept (b) assumes that the business entity is assumed to be a goingconcern in the absence of evidence to the contrary. Time Period concept (d) requires accountinginformation to be reported at regular intervals to foster comparability. Business entity conceptexplains that in accounting business is to be considered as a separate entity from the owner. It doesnot speak about amortization.Thus, alternative (c) is the correct answer.<TOP>3. Answer : (a)Reason :Trial Balance of John Vicky as at March 31, 2005Sl.No Heads of AccountDebt Balance(Rs.)Credit Balance(Rs.)1. Capital (1st April, 2004) 89,0002. Drawings 10,0003. Stock (1st April, 2004) 37,0004. Purchases 2,31,2505. Sales 3,94,0006. Motor Vehicles 14,5007. Cash in Hand 1,3508. Sundry Creditors 49,7609. Sundry Debtors 139,70010. Bank Overdraft 9,00011. Administrative over head 76,36012. Office Equipment 35,00013. Carriage Outward 2,31014. Returns Inward 2,05015. Provision for Bad Debts 4,250

16. Returns Outward 3,16017. Discount Allowed 2,80018. Discount Received 3,150TOTAL 5,52,320 5,52,320<TOP>4. Answer : (e)Reason : In contract accounting, there is a reasonable certainty that the project would be completed and thereturn consideration is realized. In fact, return consideration may begin as soon as the work begins.So, revenue may be recognized at work-in-progress. This is the exception to the revenuerecognition principle. Other principles stated in (a), (b), (c) and (d) are not correct. Hence, (e) istrue.<TOP>5. Answer : (e)Reason : Method of providing depreciation ,valuation of inventories, treatment of Goodwill and treatment ofcontingent liabilities differ from enterprise to enterprise<TOP>15contingent liabilities differ from enterprise to enterprise >6. Answer : (c)Reason : Cost of goods = Purchases – Returns outward + Freight in= Rs.2,10,000 – Rs.22,000 + Rs.30,000 = Rs.2,18,000<TOP>7. Answer : (d)Reason :Particulars Rs.Opening balance of sundry debtors 37,000Add : Credit sales 6,75,000

7,12,000Less : Closing balance of Sundry debtors 60,0006,52,000Less : Discount allowed 2,800Cash collected from sundry debtors 6,49,200<TOP>8. Answer : (a)Reason : Bank reconciliation statement as on March 31, 2005:Particulars Rs. Rs.Overdraft as per bank pass book 13,880Less : Interest on overdraft not entered in cash book 480Cheques deposited not cleared 1,800Cheque discounted which was dishonoured 1,0003,28010,600Add : Cheques issued but not presented for payment 2,350Overdraft as per cash book 12,950<TOP>9. Answer : (a)Reason : Carriage inward expense is related to the carrying cost of material purchased. If it is incurred forcarrying new assets, it should be capitalized to the assets value. Carrying cost relating to sale ofproducts, returns outward and return of unsold goods will not be treated as carriage inwardexpenses. Hence, (a) is correct.<TOP>10. Answer : (a)Reason : Advance received from customers is a current liability till the goods are supplied or services arerendered.<TOP>

11. Answer : (c)Reason : Error of principle is the error of treating revenue items as capital and capital items as revenue. Thepurchase of shares by the share broker is to be debited to purchases account and not to investment.It is error of principle. (c) is the correct answer.<TOP>12. Answer : (b)Reason : Books of Ramu EnterprisesDr. Trading Account for the period ending March 31, 2005 Cr.Particulars Rs. Rs. Particulars Rs. Rs.To Opening stock 27,000 By Sales :To Purchases Cash 20,000Cash 70,000 Credit 1,40,000Credit 20,000 1,60,00090,000 (–) Returns inward 3,000 1,57,000(–) Goods lost due to fire 2,000 By Closing stock 40,000(–) Returns outward (–) 2,000 86,000To Wages 5,000(+) Outstanding as onMarch 31, 2005 7005,700(–) Outstanding as onApril 01, 2004 500 5,200To Carriage inward 1,000To Gas, water, fuel 2,000To Gross Profit 75,8001,97,000 1,97,000<TOP>1613. Answer : (a)Reason : Insolvency of a debtor is not an extra-ordinary event. Attachment of property, destruction by fire offactory building, factory building collapsed in earthquake etc. are extra-ordinary items.<

TOP>14. Answer : (c)Reason : The non-current liability is a liability which is not repayable in a period of 12 months or a businesscycle which ever is earlier. Thus, Long-term loans and Debentures are non current liabilities.(c) isthe correct answer.<TOP>15. Answer : (d)Reason : Acceptance of bills drawn by creditors will not result in any change in the amount of liabilities ofbalance sheet, because it will decrease the balance of creditors and increase the balance of billspayable by the same amount. So (d) is correct, other transactions change the total amount ofliabilities of the balance sheet.<TOP>16. Answer : (b)Reason : Income received in advance is a liability and should shown on the liability side and not on assetside. All other statements viz, prepaid expenses shown on asset side, income earned but notreceived shown on asset side, income accrued but not due shown on asset side and outstandingliabilities for expenses shown on liability side are true.<TOP>17. Answer : (c)Reason : Fixed assets cannot easily be converted into cash. They are acquired for using them in the conductof business operations They are not meant for resale to earn profit. Depreciation at specified rates isto be charged on most of the Fixed Assets. Their utility is not confined to one accounting period.

<TOP>18. Answer : (c )Reason : To increase the profit or reduce the loss made by the enterprise is not an object of keepingaccounts. All others are objects of maintaining accounts.<TOP>19. Answer : (a)Reason : In a manufacturing company, the perpetual inventory system is called product costing system. Insuch system, the cost of each product is accumulated as it flows through the production process.<TOP>20. Answer : (c)Reason : Research and Development cost cannot directly be attributed to a specific work. Site labor cost,cost of moving plant and equipment to and from a site , supervision cost and materials used can berelated to specific contract.<TOP>21. Answer : (a)Reason : The basis for pricing inventory is either cost of production or cost of acquisition. FIFO method ofidentifying inventory is based on the assumption that costs are charged against revenue in the orderin which they occur. In case of other methods i.e. LIFO (b) method matches the most recent costsincurred with current revenue, leaving the first cost incurred to be included as inventory. Weighted-Average method (c) assumes that costs are charged against revenue based on an average of thenumber of units acquired at each price level. Moving average method (d) can be used only with a

perpetual inventory. The cost per unit is recomputed after every addition to the inventory. Theending inventory is valued at the last moving average unit cost for the period. Base stock method(e) wherein a minimal level of it is a permanent investment, which is necessary for the normalbusiness activities. Base stock would be carried at historical cost. Thus, FIFO method is the correctanswer.<TOP>22. Answer : (d)Reason : The depreciation rate according to units-of-production method is applied to the number of unitsproduced during an accounting period. Hence, it is related to the usage of the asset. Straight linemethod, written down value method, sum-of-the-years’ digits method and double declining methodtakes into consideration the cost of the asset, salvage value and useful life but not the output fromthe asset. Hence the answer is (d).<TOP>1723. Answer : (b)Reason :Purchases Issues BalanceDate Quantity(Kg)Rateper kg.(Rs.)Amount(Rs.)Quantity(Kg)Rate perkg. (Rs.)

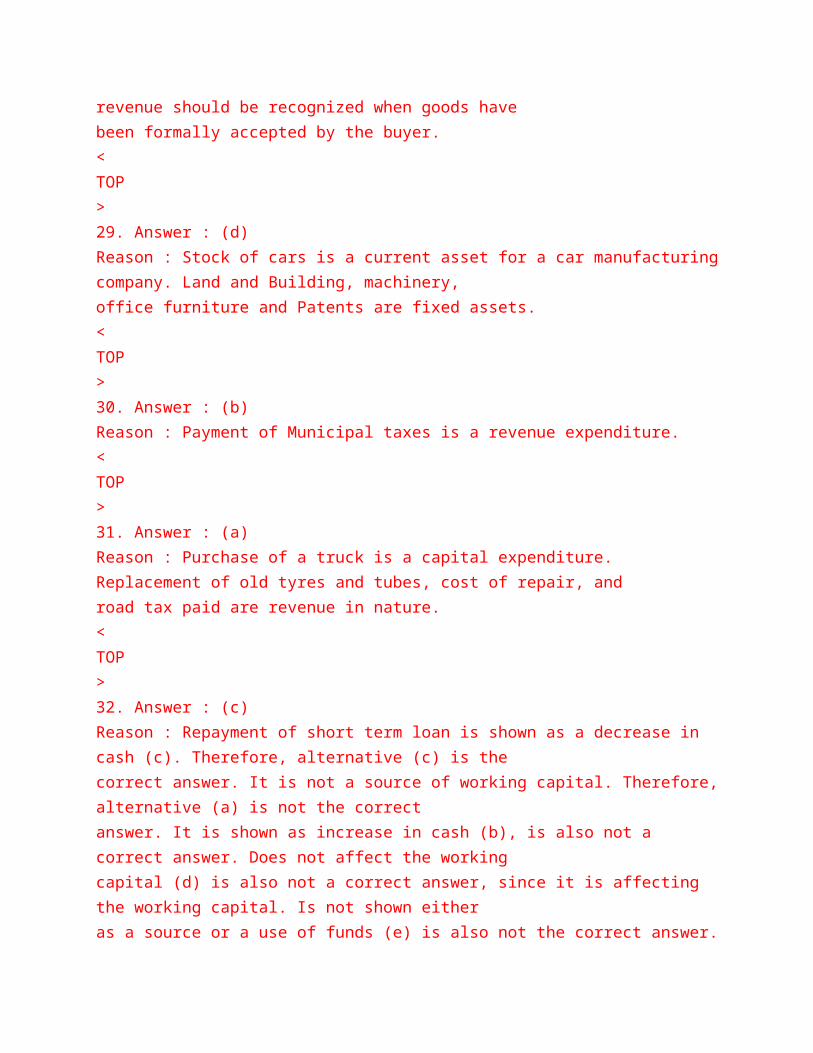

Amount(Rs.)Quantity(Kg)Rateper kg.(Rs.)Amount(Rs.)1-3-05 500 22.80 11,4002-3-05 400 24 9,600 900 23.33 21,00010-03-05 600 25 15,000 1,500 24.00 3600025-03-05 1,000 24 24,000 500 24.00 12,000<TOP>24. Answer: (d)Reason: Both direct and indirect labour as well as power and light form part of the manufacturing cost.Advertising expenses come under selling and distribution cost and hence not a manufacturing costto be included in the cost of goods sold.<TOP>25. Answer : (b)Reason : Although patent is a capital expenditure, renewal fee paid for patent is treated as revenueexpenditure.<TOP>26. Answer : (e)Reason : Cost of purchase of raw-material is purchase price plus duties and taxes plus freight inward minusdiscount and duty draw back.<TOP>27. Answer : (c)

Reason : Long term investment is not a fixed asset. Buildings, Furniture, Equipment and Machinery arefixed assets which also referred to as property.<TOP>28. Answer : (a)Reason : When goods are sold subject to approval by buyer, revenue should be recognized when goods havebeen formally accepted by the buyer.<TOP>29. Answer : (d)Reason : Stock of cars is a current asset for a car manufacturing company. Land and Building, machinery,office furniture and Patents are fixed assets.<TOP>30. Answer : (b)Reason : Payment of Municipal taxes is a revenue expenditure.<TOP>31. Answer : (a)Reason : Purchase of a truck is a capital expenditure. Replacement of old tyres and tubes, cost of repair, androad tax paid are revenue in nature.<TOP>32. Answer : (c)Reason : Repayment of short term loan is shown as a decrease in cash (c). Therefore, alternative (c) is thecorrect answer. It is not a source of working capital. Therefore, alternative (a) is not the correctanswer. It is shown as increase in cash (b), is also not a correct answer. Does not affect the workingcapital (d) is also not a correct answer, since it is affecting the working

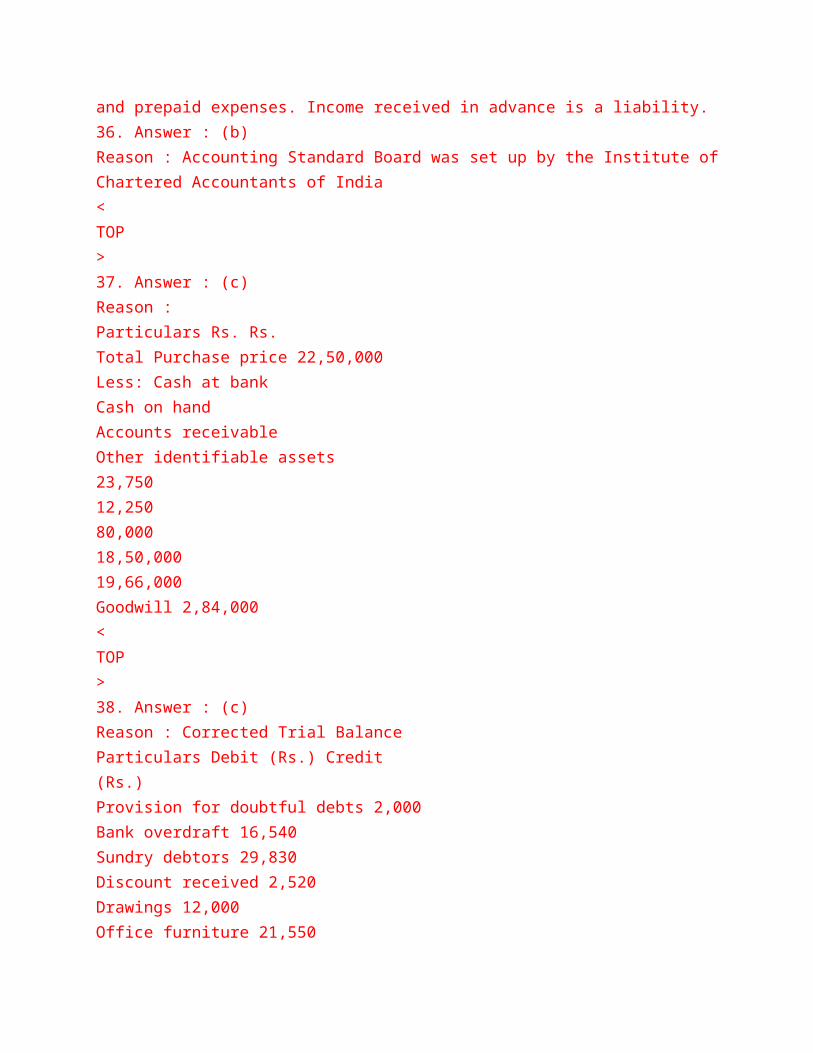

capital. Is not shown eitheras a source or a use of funds (e) is also not the correct answer. Therefore, alternative (c) is thecorrect answer.<TOP>33. Answer : (c)Reason : Window-dressing implies showing a better position than the true and fair view of accounts.<TOP>34. Answer : (b)Reason :Rs.Profit for the year 2004-2005 2,30,000Add: Rent (not relevant if the owner of the premises operates the business) 1,20,000Adjusted maintainable profits 3,50,000Capital employed by Dinakar 20,00,000Add: Value of premises 4,00,000Total capital employed 24,00,000Normal profit (12% of Rs.24,00,000) 2,88,000Super profits (Rs.3,50,000 – Rs.2,88,000) 62,000<TOP>35. Answer : (e)Reason : Current assets include cash and cash equivalents, inventories, accounts receivable, bills receivable,and prepaid expenses. Income received in advance is a liability.<TOP>18and prepaid expenses. Income received in advance is a liability.36. Answer : (b)Reason : Accounting Standard Board was set up by the Institute of Chartered Accountants of India

<TOP>37. Answer : (c)Reason :Particulars Rs. Rs.Total Purchase price 22,50,000Less: Cash at bankCash on handAccounts receivableOther identifiable assets23,75012,25080,00018,50,00019,66,000Goodwill 2,84,000<TOP>38. Answer : (c)Reason : Corrected Trial BalanceParticulars Debit (Rs.) Credit(Rs.)Provision for doubtful debts 2,000Bank overdraft 16,540Sundry debtors 29,830Discount received 2,520Drawings 12,000Office furniture 21,550Purchases 1,09,230Rent and rates 3,140Salaries 25,200Opening stock 24,180Provision for depreciation on furniture 3,640Capital 45,910Sundry creditors 16,370Discount allowed 7,330General expenses 8,290Returns inward 3,300

Cash sales 60,800Credit sales 1,08,020Total 2,44,050 2,55,800Suspense (Debit) Rs.2,55,800 – Rs.2,44,050 = Rs.11,750.<TOP>39. Answer : (e)Reason : (No. of shares)Particulars Anil Vimal Sunil TotalLiability 30,000 40,000 30,000 1,00,000Less: Unmarked applications in theratio of 3:4:34,800 6,400 4,800 16,00025,200 33,600 25,200 84,000Less: Marked (Stamped) applications 22,000 24,000 28,000 74,0003,200 9,600 (2,800) 10,000Less: Division of Sunil’s surplus(in the ratio of 3:4) 1,200 1,600 2,800 –Final liability of each underwriter 2,000 8,000 Nil 10,000<TOP>40. Answer : (b )Reason : Since a transaction altogether has been omitted both debit and credit aspects have not beenrecorded. Hence the trial balance cannot disclose the existence of the above error.<TOP>41. Answer : (c)Reason : If a company reissues the forfeited shares at a discount, that discount amount will be debited toforfeited share account.<TOP>19According to the Companies Act, the company cannot debit share capital

account, profit and lossaccount, capital redemption reserve account and capital reserve account for the amount of discountallowed on reissue of forfeited shares.42. Answer : (d)Reason : The users of accounting information of a company are investors, bankers, creditors, shareholders,management, employees, customers, government and regulatory agencies who are interested in theaffairs of a company. The means of communicating information are financial statements; (d) i.e.profit and loss account and balance sheet. These are the means through which inferences like ratioanalysis are drawn. Prospectus (a) is the document inviting the public to subscribe to its securitiesand there may be certain accounting statistics, which are useful to the users. But it is notcomprehensive. Hence it is false. Trial balance (b) is a summary of all ledger accounts prepared ina tabular form from which no useful inference can be drawn. Hence, it is not the correct answer.Bank reconciliation statement (c) is a statement prepared by a business only in the event ofdifference between balance as per bank statement and bank column of cashbook, which has norelevance to the users. Hence, it is false. Statement of cash flow (e) is the statement depictinginflow and outflow of cash irrespective of nature of source and relevance of period. It is more orless of receipts and payments account of non-profit organization which has no significance to theusers and it is false.<TOP>43. Answer : (a)Reason : Balance Sheet of Universe Ltd. as on March 31, 2005Liabilities Rs. Assets Rs.Share capital 5,00,000 Land & building 4,90,000Less calls in arrears 30,000 4,70,000 Plant and machinery 2,20,000

Capital reserve 90,000 Investments 60,000P & L A/c 50,000 Sundry debtors 1,20,000Secured loans 3,00,000Less provision fordoubtful debts 10,0001,10,000Term Loan from Bank 1,00,000 Stock 96,000Sundry creditors 90,000 Loans to employees 50,000Outstanding expenses 500 Cash 4,000Interest received in advance 700 Bank 40,000Insurance premium paid inadvance1,200Preliminary expenses 30,00011,01,200 11,01,200<TOP>44. Answer : (c)Reason : In the books of the CompanyCash Book (Bank Column only)Date Particulars Rs. Date Particulars Rs.2004May 11To Share Application A/c (Beingapplication money received on 50,000shares @ Rs.5 each includingpremium of Rs.2 per share)2,50,000 2004Dec 31ByBalancec/d5,96,100June 30 To Share Allotment A/c(Being allotment money received on49,500 shares @ Rs.3 each)1,48,500Sept. 30 To Share First Call A/c(Being First call money received on

49,500 shares @ Rs.2 each)99,000Dec. 31 To Share Final Call A/c(Being Final Call money received on49,300 shares @ Rs.2 each)98,6005,96,100<TOP>45. Answer : (e)Reason : The equity shareholders get the dividend, depending on the income the company made and there isno fixed amount and the share premium received on issue of shares can be utilized in writing offthe preliminary expenses of the company. Hence, alternative II and III are not correct and theanswer is (e).<TOP>2046. Answer : (c)Reason : Rights shares are the shares that are offered to the existing equity shareholders (c). These are notissued by a newly formed company (a) They are not the shares issued to the public at large. Theyare issued only to the existing shareholders. (b). It does not indicate the right of redemption ofshares issue (d). These are not the shares with cumulative dividend right.<TOP>47. Answer : (d)Reason : The discount on issue of debentures is a capital loss which will be written off over a period of time.(d) is the correct answer.<TOP>

48. Answer : (a)Reason : Value of right =r(M S)N r − +

Where r = No of rights issuedN = No of old sharesM = Market priceS = Issue price of rights∴ Value of rights =2(Rs.560 Rs.410)3 2 − + = Rs.60

<TOP>49. Answer : (d)Reason : When share is issued at less than par value, the difference is debited to an appropriately titleddiscount account, which is a contra equity share account. The discount account is not an expenseaccount nor does it appear on the income statement.<TOP>50. Answer : (e)Reason : Debentures can be redeemedI. At parII. At a premiumIII. At a discountIV. By conversion into stock.Thus, (e) the combination of (I), (II), (III) and (IV) is the correct answer.<TOP>51. Answer : (b )Reason : The cash book is to record all cash receipts and payments and the balance in cash book shows the

cash on hand.<TOP>52. Answer : (b)Reason : The profits earned by a subsidiary company before the holding company acquiring control over it isknown as capital profit. Any profit before acquisition date is the capital profit. Other profitsmentioned in (a), (c), (d) and (e) are not true.<TOP>53. Answer : (c)Reason : Profit and Loss Appropriation Account of Wye Ltd. for the year ended March 31, 2005Particulars Rs. Particulars Rs.To Income Tax Provision for the previous year 58,800 By Balance B/d 2,30,000To General Reserve 2,50,000 By Net Profit 6,62,800To Sinking Fund 1,50,000To Proposed dividend 1,00,000To Balance c/d 3,34,0008,92,800 8,92,800<TOP>54. Answer : (b)Reason: Net income is equal to revenues minus expenses. In this case, revenues equal Rs.48,200 andexpenses equal Rs.23,750 (Rs.13,200 + Rs.5,750 + Rs.1,100 + Rs.3,700). Net income is Rs.24,450(Rs.48,200 – Rs.23,750).<TOP>55. Answer : (d)Reason: Of the Rs.1,20,000 paid, Rs.40,000 was paid toward dividends in arrears and Rs.80,000 was paidtoward dividends for 2004-05. Of the Rs.80,000, Rs.45,000 was paid to

preference stockholders<TOP>21toward dividends for 2004-05. Of the Rs.80,000, Rs.45,000 was paid to preference stockholders(5,000 shares x Rs.100 per share x .09), leaving Rs.35,000 to be paid to common stockholders(Rs.80,000 – Rs.45,000).56. Answer : (b)Reason :Trading Account for the year endedDr CrParticulars Amount(Rs)Amount(Rs)Particulars Amount(Rs)Amount(Rs)1,90,0007,90,0005,87,00013,50,0002,17,000To Opening StockTo PurchasesLess: Distribution offree samplesAdd: Sale wronglycredited to purchasesTo Gross Profit7,80,00018,0007,62,00028,00015,67,000By Sales

Add: Amountwrongly creditedto purchasesBy Closing Stock13,22,00028,00015,67,000<TOP>57. Answer : (d)Reason : A company’s system of accounting for maintaining books of accounts must be on the accrual basisand according to the double entry system of accounting. The systems in other alternatives are nosystems at all or not recognized under the Act. Thus, alternative (d) is the correct answer.<TOP>58. Answer : (e)Reason : Called up capital The directors of the company called Rs.5 per share on 60,000 shares =Rs.3,00,000Less calls in arrear on 5,000 shares at the rate of Rs.2 = 10,000Paid-up capital to be considered for dividends = Rs.2,90,000Thus, (e) is the correct answer.<TOP>59. Answer : (e)Reason : Balance as on 31st March 2005 Rs.29,25,000Issue of debentures 12,000 Rs.12,00,000Less: discount 2.5% Rs. 30,000 Rs.11,70,000Issued preference shares 25,000 R s.25,00,000Rs.65,95,000Less: Redemption of 30,000 6% preference shares Rs.30,00,000Premium on redemption Rs. 1,50,000Dividend for one month R s. 15,000 Rs.31,65,000Balance as on 30 th April 2005 Rs.34,30,000

<TOP>60. Answer : (b)Reason : Once the unclaimed dividend is transferred to General Revenue a/c of the Central Government, anyshareholder entitled can claim such dividend from the Central Government.<TOP>61. Answer: (c)Reason: Dr. Creditors A/c Cr.Particulars Rs. Particulars Rs.To Cash 1,85,000 By Balance b/d 3,40,000To Purchases Returns 8,000 By Purchases 2,47,000To Cash Discount 4,800 By Bills Payable 8,000To Balance C/d 3,97,2005,95,000 5,95,000By Balance b/d 3,97,200<TOP>62. Answer : (a)Reason : Dr. Stock account Cr.<TOP>22Particulars Rs. Particulars Rs.To Opening balance 6,00,000To Purchases 34,00,000By Cost of goods sold(Rs.48,00,000 × 75%)36,00,000By Missing inventory (balancing figure) 75,000By Closing balance (physical count) 3,25,00040,00,000 40,00,000The estimated cost of missing inventory is Rs.75,000.63. Answer : (e)Reason : Under First in First out method of inventory valuation, the sale of

32 units will be accounted as,15 Units @ Rs.400 = Rs. 6,00017 Units @ Rs.450 = Rs. 7,65032 = Rs.13,650The balance of inventory is,3 Units @ Rs.450 = Rs. 1,35010 Units @ Rs.460 = Rs. 4,600Value of closing inventory Rs. 5,950<TOP>64. Answer : (a)Reason : Average Trading Profit Rs.2,58,900Normal Profits (-) Rs.2,23,800Super profits Rs. 35,100Value of goodwill = 3 x Rs.35,100 = Rs.1,05,300Amortisation – in five years = Yearly amortisation = Rs.1,05,300/5 = Rs.21,060.The journal entry will beProfit and Loss a/c. Dr. Rs.21,060To Goodwill a/c. Rs.21,060.<TOP>65. Answer : (d)Reason : Intangible assets are classified as either identifiable or unidentifiable. Goodwill (d), arising out ofpayment for reputation, brand name, location, loyality, etc. is an unidentifiable intangible asset.Hence, alternative (d) is false. It is described as a momentum or push (a) like the momentum of abody that continues its motion against a retarding force. It, though caused by factors which cannotbe easily and accurately quantified, must be assigned a value (a). It is a payment for somethingwhich places the payer in the position being able to earn more than he would be able to do by hisown unaided efforts (b). It is the difference between the value of a business as a whole and theaggregate of the fair value of its net assets (c). The basic characteristic of

an asset is said to haveproductivity. Since the goodwill helps in extra earnings, it is said to be a store of prospectiverevenue (e). Thus, alternatives (a), (b), and (e) are true.<TOP>66. Answer : (c)Reason :No of sharesAppliedNo ofSharesallottedAmountpaidAmount adjustedtowardsapplicationAmountavailableAmountrefundedRs. Rs. Rs. Rs.20,000 20,000 60,000 60,000 - -80,000 60,000 2,40,000 1,80,000 60,000 -20,000 - 60,000 - - 60,000<TOP>67. Answer : (a)Reason : The journal entry passed at the time of receipt of application money isBank account Dr. Rs.12,00,000To Share application account Rs.12,00,000<TOP>68. Answer : (b)Reason : When redeemable preference shares are due for redemption, the