IBP AT MERCK - · PDF fileIBP AT MERCK . 2 Content Who is Merck ? IBP concept Benefits & Key...

23

Didier Dayen Senior Director Global Advanced Planning June 19 th , 2017 Supply Chain Logistics summit - Barcelona IBP AT MERCK

Transcript of IBP AT MERCK - · PDF fileIBP AT MERCK . 2 Content Who is Merck ? IBP concept Benefits & Key...

Didier Dayen Senior Director Global Advanced Planning June 19th, 2017

Supply Chain Logistics summit - Barcelona

IBP AT MERCK

2

Content

Who is Merck ?

IBP concept

Benefits & Key Success Factors

Conclusion

3

Content

Who is Merck ?

IBP concept

Benefits & Key Success Factors

Conclusion

4

WE ARE MERCK – THE ORIGINAL

Who we are - History

Nearly 350 years of experience for patients and customers

Friedrich Jacob Merck purchases the Angel Pharmacy (Engel-Apotheke) in Darmstadt

Emanuel Merck begins production on an industrial scale

In 1887, Merck opened its own office in New York, which gave rise to the subsidiary Merck & Co. three years later. Our U.S. subsidi-ary Merck & Co. is expropriated as a consequence of World War I

1668 1827 1917

Merck – the original holds the global rights to the Merck name and brand. Exceptions are Canada and the United States, where we operate as EMD Serono, MilliporeSigma and EMD Performance Materials.

5

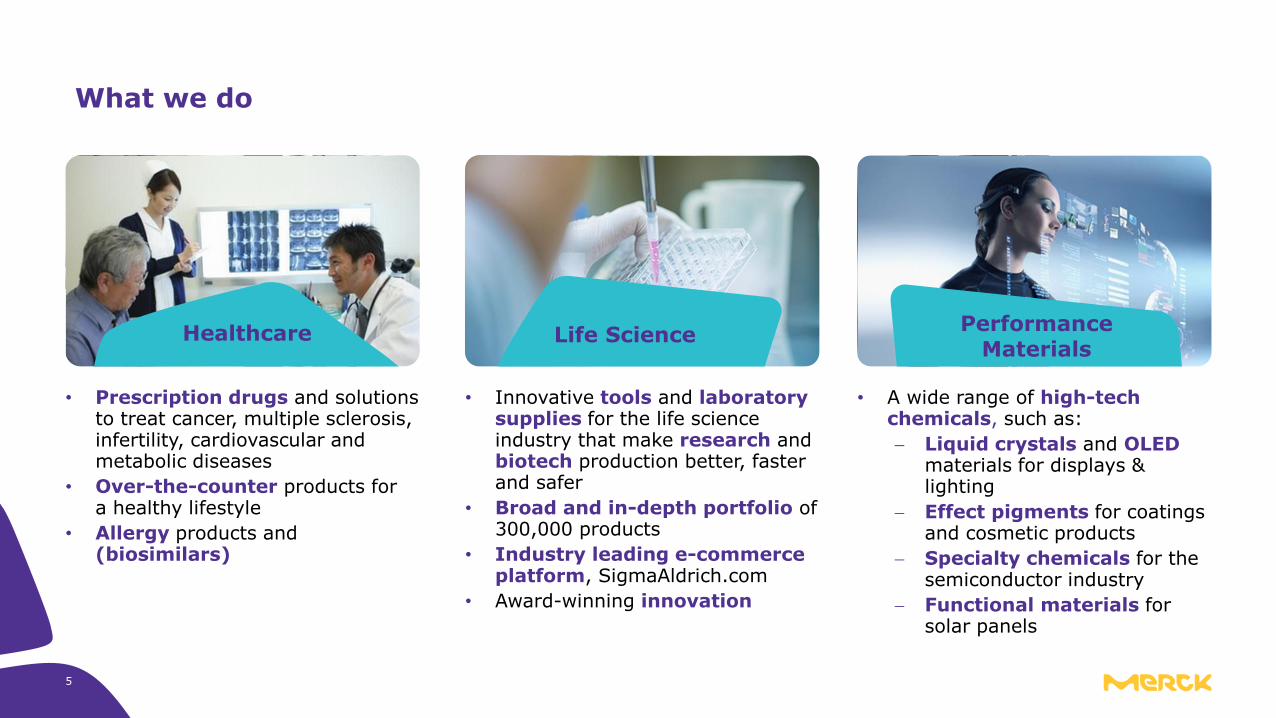

What we do

Life Science Performance

Materials Healthcare

• A wide range of high-tech chemicals, such as:

Liquid crystals and OLED materials for displays & lighting

Effect pigments for coatings and cosmetic products

Specialty chemicals for the semiconductor industry

Functional materials for solar panels

• Innovative tools and laboratory supplies for the life science industry that make research and biotech production better, faster and safer

• Broad and in-depth portfolio of 300,000 products

• Industry leading e-commerce platform, SigmaAldrich.com

• Award-winning innovation

• Prescription drugs and solutions to treat cancer, multiple sclerosis, infertility, cardiovascular and metabolic diseases

• Over-the-counter products for a healthy lifestyle

• Allergy products and (biosimilars)

6

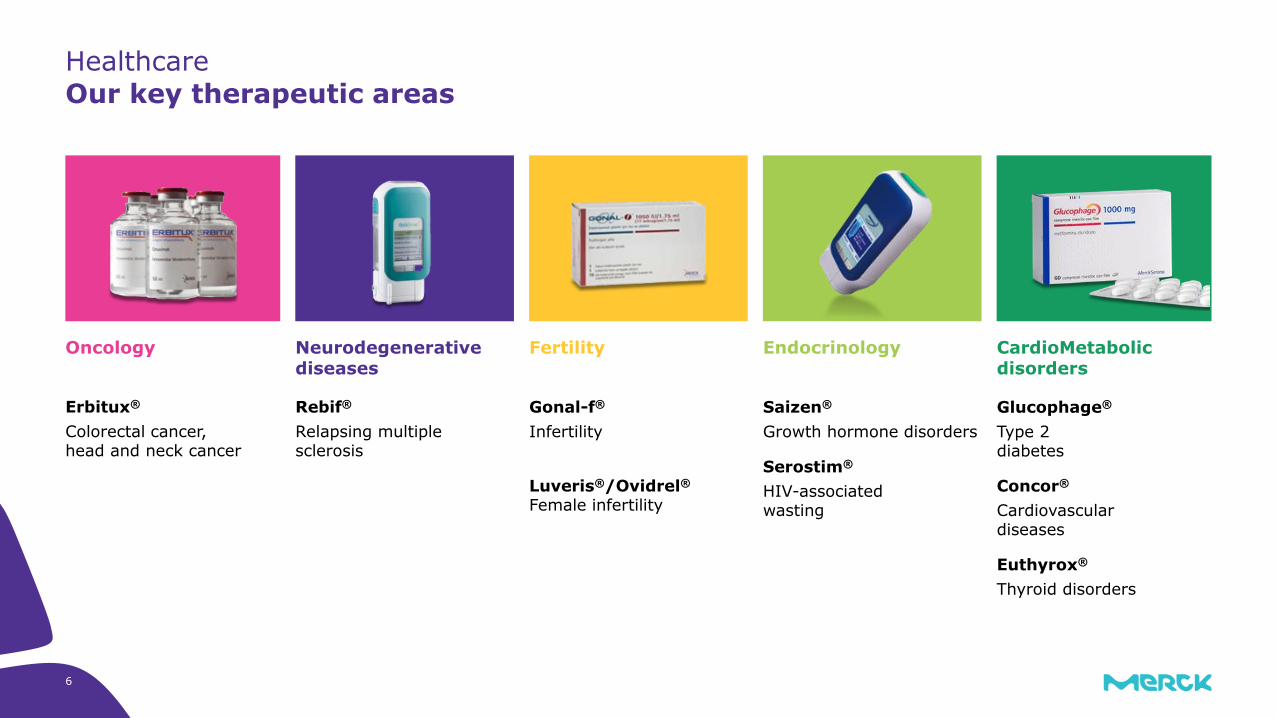

Healthcare

Our key therapeutic areas

Erbitux®

Colorectal cancer, head and neck cancer

Rebif®

Relapsing multiple sclerosis

Gonal-f®

Infertility

Luveris®/Ovidrel®

Female infertility

Saizen®

Growth hormone disorders

Serostim®

HIV-associated wasting

Glucophage®

Type 2 diabetes

Concor®

Cardiovascular diseases

Euthyrox®

Thyroid disorders

Oncology Neurodegenerative diseases

Fertility Endocrinology CardioMetabolic disorders

7

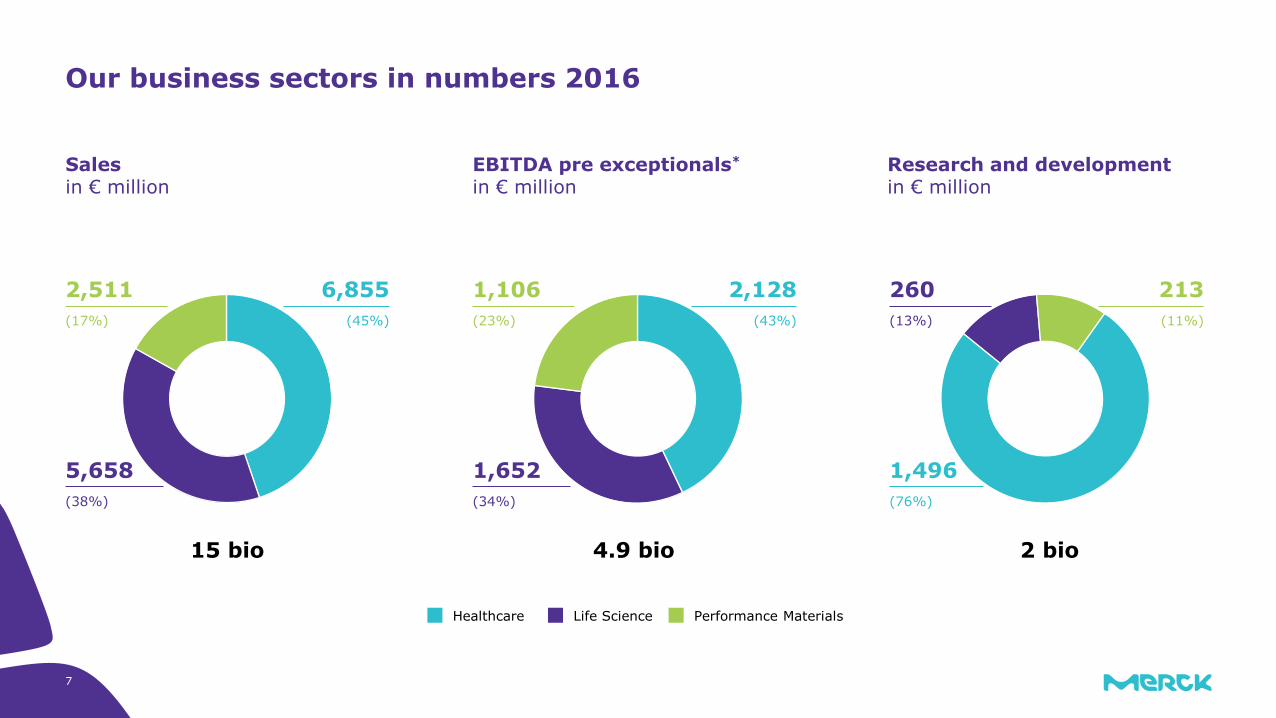

Our business sectors in numbers 2016

Sales in € million

EBITDA pre exceptionals* in € million

Research and development in € million

Healthcare Life Science Performance Materials

2,511

(17%)

6,855

(45%)

5,658

(38%)

1,106

(23%)

2,128

(43%)

1,652

(34%)

260

(13%)

213

(11%)

1,496

(76%)

15 bio 4.9 bio 2 bio

8

We are global

Sales by region 2016 in € million

Employees by region 2016 (as of December 31)

We operate around the world and have a strong presence in growth markets.

129 nationalities are represented at Merck and our employees work at sites in 66 countries around the world.

1,136

(8%)

4,735

(31%)

4,736

(31%)

Europe North America Asia-Pacific (APAC)

3,858

(26%)

4,140

(8.2%)

24,438

(48.5%)

10,754

(21.3%) 10,037

(20.0%)

Latin America

559

(4%)

1,045

(2.0%)

Middle East and Africa (MEA)

50'000 15 bio

MDA Semoy Spittal Mollet Mexico Other

API Subcontractors

Global SNO

From Local Steering To Global Steering

Affiliate 1 Affiliate 2 Affiliate 3 Affiliate 4 Affiliate 5 Affiliate 6

Affiliate 1 Affiliate 2 Affiliate 3 Affiliate 4 Affiliate 5 Affiliate 6

MDA Semoy Spittal Mollet Mexico Other

API Subcontractors

C1

C2 C3 Cn C1

C2 C3 Cn C1

C2 C3 Cn C1

C2 C3 Cn C1

C2 C3 Cn C1

C2 C3 Cn

C1

C2 C3 Cn C1

C2 C3 Cn C1

C2 C3 Cn C1

C2 C3 Cn C1

C2 C3 Cn C1

C2 C3 Cn

9

Global Supply Chain organization

10

Content

Who is Merck ?

IBP concept

Benefits & Key Success Factors

Conclusion

11

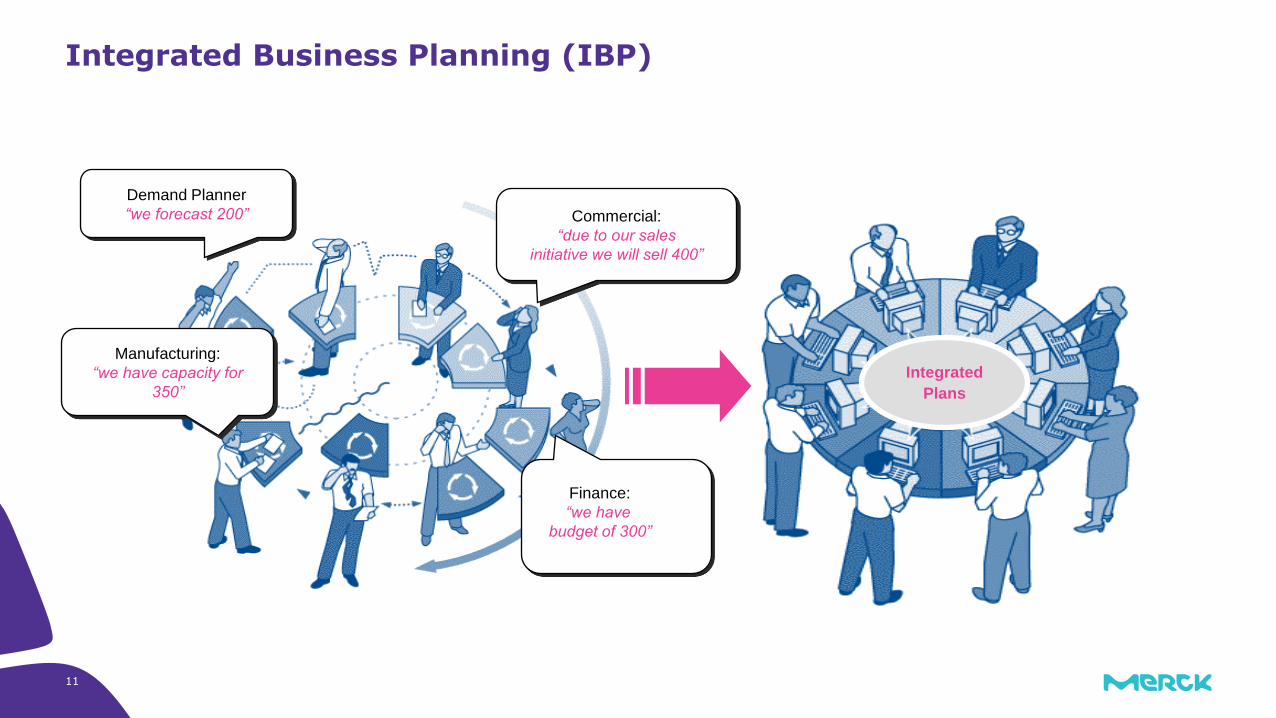

Integrated Business Planning (IBP)

Demand Planner

“we forecast 200” Commercial:

“due to our sales

initiative we will sell 400”

Finance:

“we have

budget of 300”

Integrated

Plans

Manufacturing:

“we have capacity for

350”

One single plan aligned between Commercial, Controlling and Supply Chain

Integrated Business Planning

The IBP main objective is to align different business forecast into one integrated plan providing higher transparency, increased efficiency, better financial forecast (OP, Fn), improved gap identification, better supply chain decision, faster definition of mitigation plan

“The Integrated Business Planning is the evolution of S&OP into a fully integrated management and supply chain collaboration process” – Oliver Wight, White Paper series

12

13

The IBP process is based on a sequence of meetings on local, regional & global levels

14

Constrained Forecast and Best Estimate reflect risks in Unconstrained Forecast

Risks in Unconstrained Forecast

90

70

30

Constrained Forecast

Supply Risk

-10

Unconstrained Forecast

100

80

70

30

Best Estimate Demand Risks &

Opportunities

-20

Unconstrained Forecast

100

Due to e.g. limited capacities, supply chain might not able to completely fulfill the unconstrained forecast

Volumes which potentially cannot be fulfilled are called “Supply Risks” and are deducted from unconstrained forecast

Resulting “Constrained Forecast” is “commitment” from SNO on what they will be able to deliver

70

30

Unconstrained Forecast

Tender Forecast

100

Market Forecast

Forecast by SNO & Commercial based on statistical forecast, historical demand and market outlook

Complemented with demand from specific tender opportunities

Includes demand with medium to high probability (~60-90%)

Does not include demand with very low probability (~30%)

Unconstrained forecast includes volumes which will materialize with medium probability

Volumes which potentially might not materialize are called “Demand Risks & Opportunities” and are deducted from the unconstrained forecast

Resulting “Best Estimate” is “commitment” from Commercial on what they will be able to sell

Starting Point / Baseline: Unconstrained Forecast

Demand Risk Reflection: Best Estimate

Supply Risk Reflection: Constrained Forecast

Consensus Forecast equals minimum of Constrained Forecast and Best Estimate

Breathing space: Our weapon against political forecast

8090

100

Supply Constraint Constrained Forecast

-10

Best Estimate Demand Risks

-20

Unconstrained Forecast

Consensus Forecast

80

Financial Planning

Un/Constrained forecast: “What do we plan for”

Consensus forecast: “What can we commit to”

Breathing space: difference versus the financial commitment (Consensus Fcst) and the forecast used for production (Uncon. or Constrained Fcst)

Gap (<X%) allows development of business beyond current financial commitments

Consensus Forecast

equals minimum of

Constrained Forecast

and Best Estimate

(conservative view)

Maintained in JDA

Maintained in JDA

Calculated in JDA

Maintained in JDA

Calculated in JDA

“Breathing Space”

Calculated in JDA

Financial outlook (monthly) & Financial Forecast (quarterly): F1, F2, F3, OP

Full transparency on forecast and Demand risks / Supply constraints in JDA

Production Planning

15

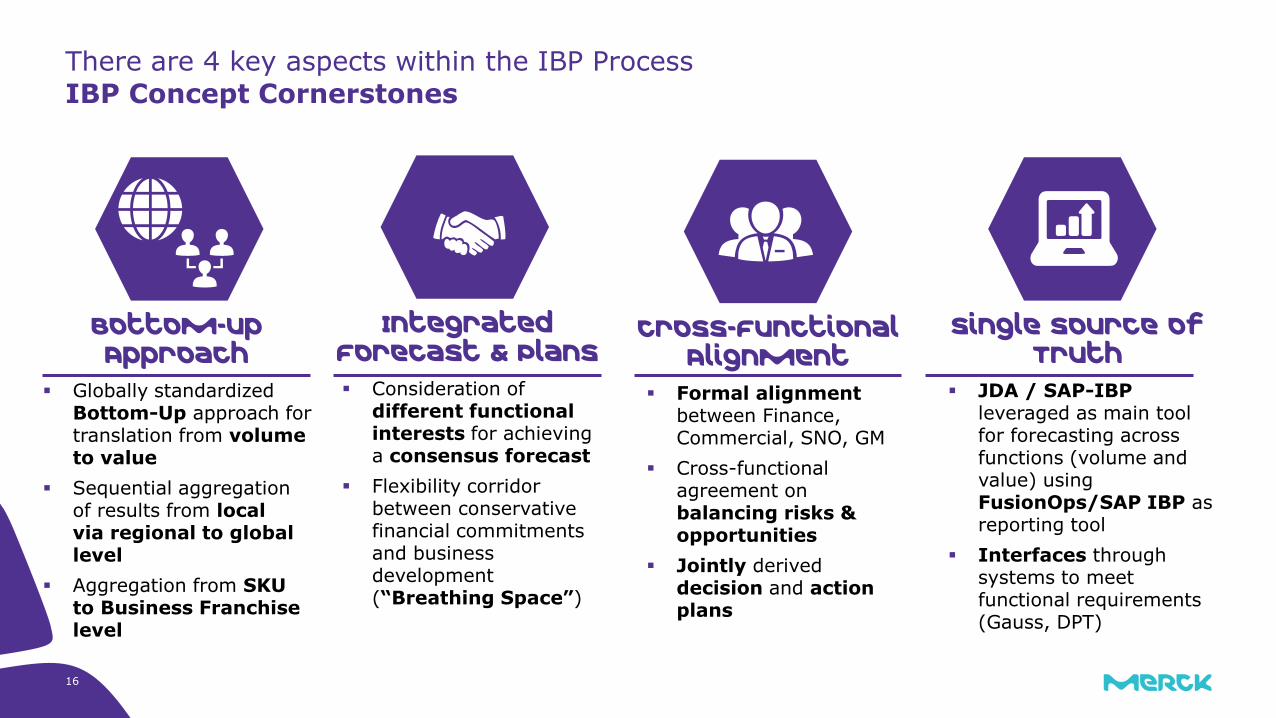

There are 4 key aspects within the IBP Process

IBP Concept Cornerstones

Globally standardized Bottom-Up approach for translation from volume to value

Sequential aggregation of results from local via regional to global level

Aggregation from SKU to Business Franchise level

Formal alignment between Finance, Commercial, SNO, GM

Cross-functional agreement on balancing risks & opportunities

Jointly derived decision and action plans

Consideration of different functional interests for achieving a consensus forecast

Flexibility corridor between conservative financial commitments and business development (“Breathing Space”)

JDA / SAP-IBP leveraged as main tool for forecasting across functions (volume and value) using FusionOps/SAP IBP as reporting tool

Interfaces through systems to meet functional requirements (Gauss, DPT)

Bottom-Up Approach

Cross-Functional Alignment

Integrated Forecast & Plans

Single Source of Truth

16

17

JDA/SAP is leveraged as master tools across functions

Technical Realization of IBP (high-level)

Controlling BW

Actuals in value and quantity

OP 2016

Input

Master tool

JDA leveraged as main tool

Interfaces between JDA and controlling systems

IBP Executive Dashboard available to all functions at local, regional and global levels

Controlling BW Output

F1/F2/F3 Operational Plan 2017

18

Content

Who is Merck ?

IBP concept

Benefits & Key Success Factors

Conclusion

19

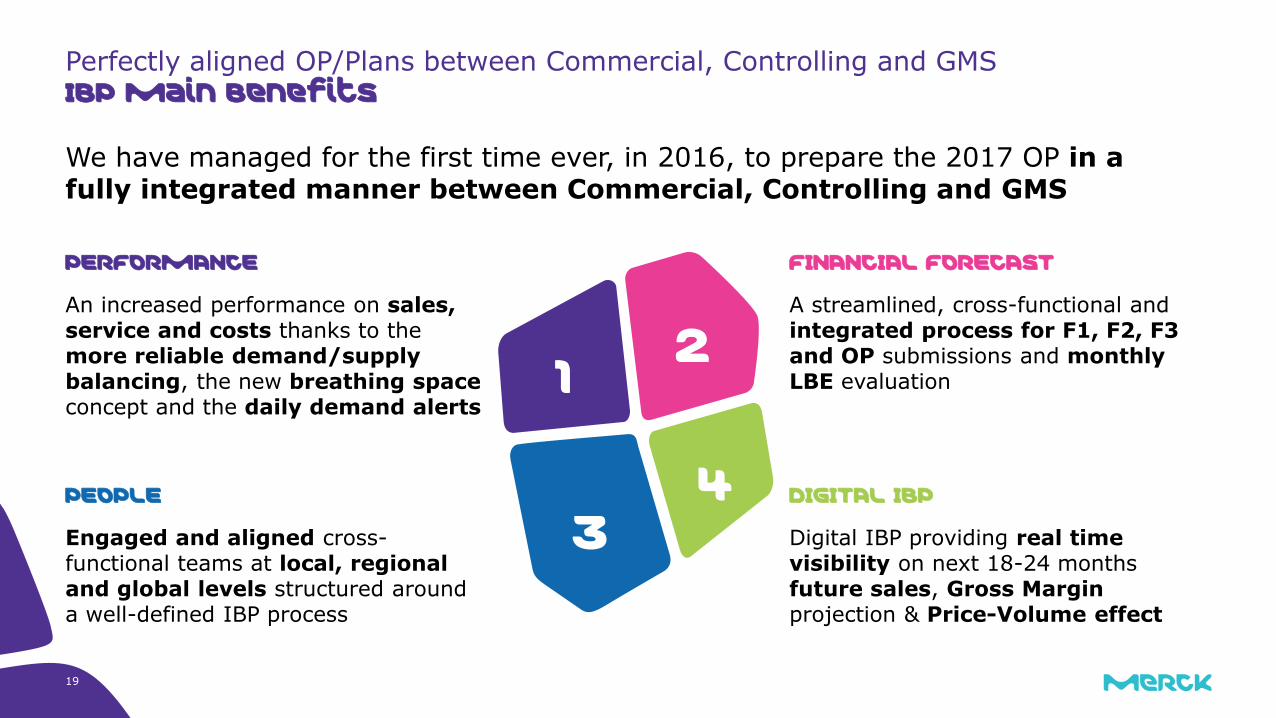

Perfectly aligned OP/Plans between Commercial, Controlling and GMS IBP main Benefits

We have managed for the first time ever, in 2016, to prepare the 2017 OP in a fully integrated manner between Commercial, Controlling and GMS

PEOPLE

Engaged and aligned cross-functional teams at local, regional and global levels structured around a well-defined IBP process

FINANCIAL FORECAST

A streamlined, cross-functional and integrated process for F1, F2, F3 and OP submissions and monthly LBE evaluation

DIGITAL IBP

Digital IBP providing real time visibility on next 18-24 months future sales, Gross Margin projection & Price-Volume effect

1 2

3 4

PERFORMANCE

An increased performance on sales, service and costs thanks to the more reliable demand/supply balancing, the new breathing space concept and the daily demand alerts

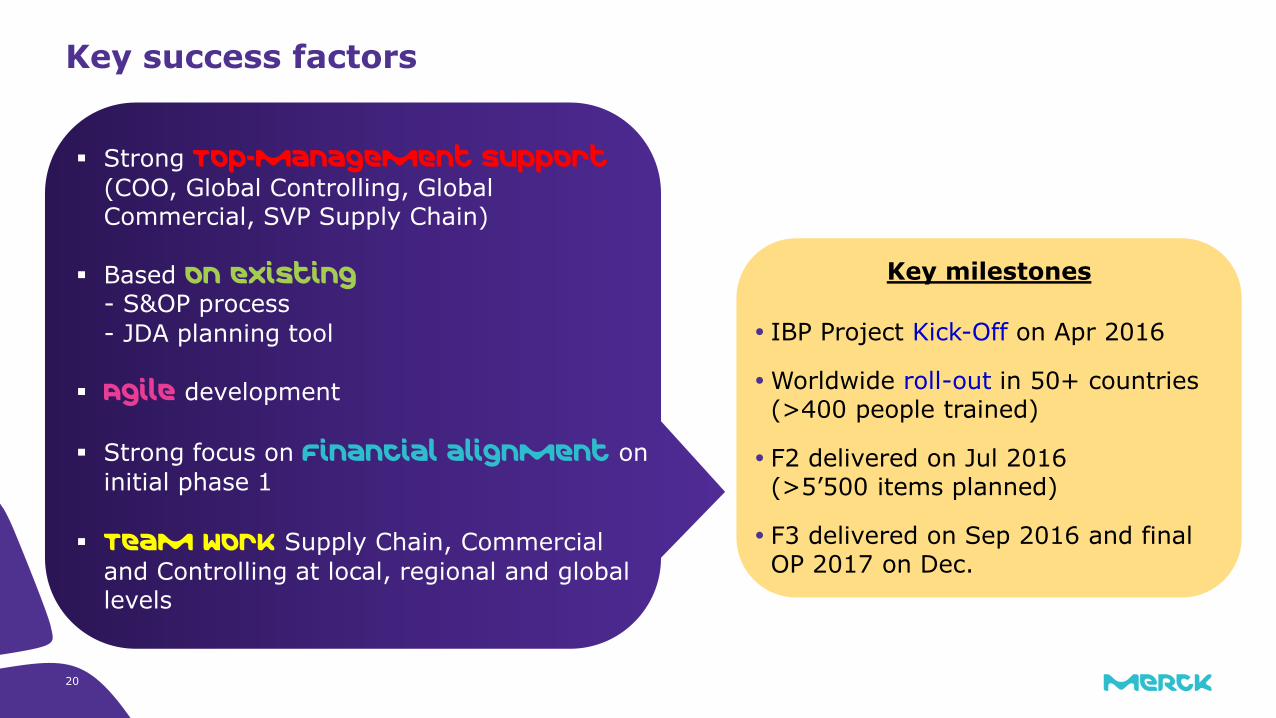

Key success factors

Strong Top-Management support

(COO, Global Controlling, Global Commercial, SVP Supply Chain)

Based on existing - S&OP process - JDA planning tool

Agile development

Strong focus on Financial alignment on

initial phase 1

Team work Supply Chain, Commercial

and Controlling at local, regional and global levels

Key milestones

IBP Project Kick-Off on Apr 2016

Worldwide roll-out in 50+ countries (>400 people trained)

F2 delivered on Jul 2016 (>5’500 items planned)

F3 delivered on Sep 2016 and final OP 2017 on Dec.

20

21

Content

Who is Merck ?

IBP concept

Benefits & Key Success Factors

Conclusion

22

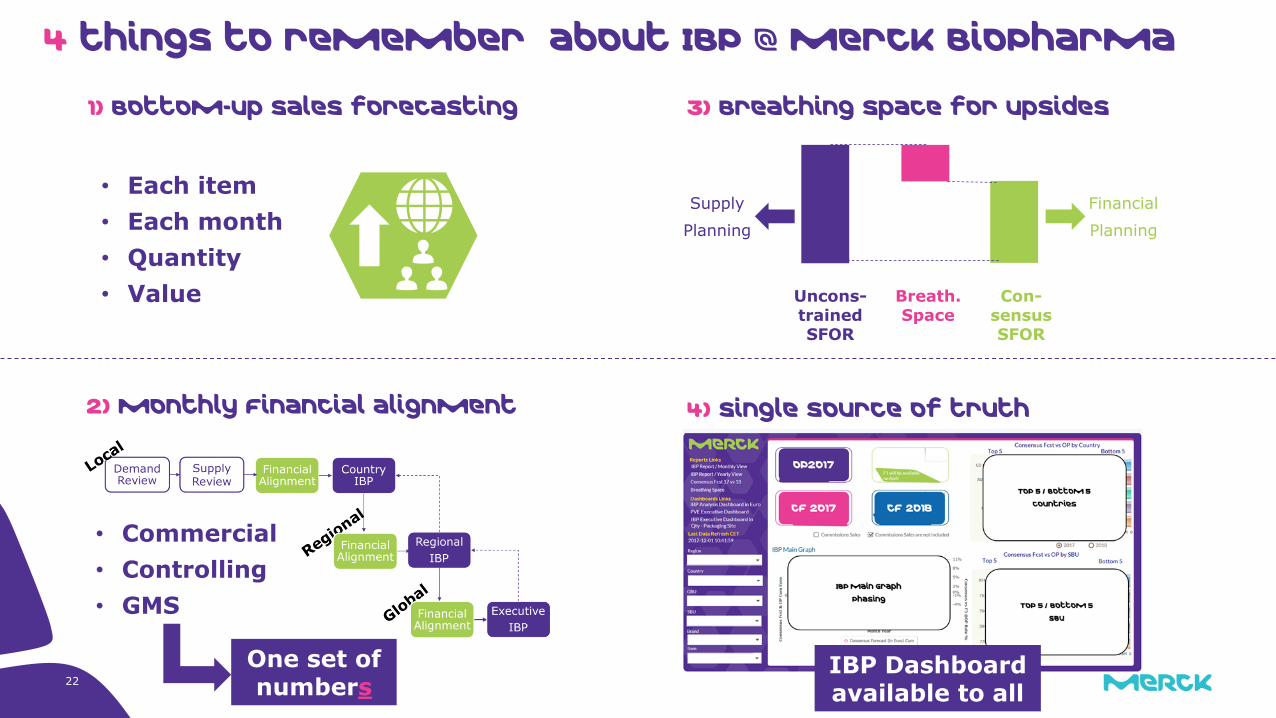

1) Bottom-up sales forecasting

2) Monthly Financial alignment

3) Breathing space for upsides

Supply

Planning

Financial

Planning

4) Single source of truth

• Commercial

• Controlling

• GMS

• Each item

• Each month

• Quantity

• Value Uncons- trained SFOR

Con- sensus SFOR

Breath. Space

4 things to remember about IBP @ Merck BioPharma

IBP Dashboard available to all

One set of numbers

![IBP Southern Luzon3] Southern Luzon.pdf · IBP Southern Luzon Region donates to health offices, BJMPs & frontliners IBP Aurora, Batangas, CalMaNa. Makati, Marinduque, Occidental Mindoro.](https://static.fdocuments.in/doc/165x107/600a54d3b5cfa474cb7da335/ibp-southern-3-southern-luzonpdf-ibp-southern-luzon-region-donates-to-health.jpg)