IBIS Global Plastic Product

30

www.ibisworld.com | www.ibisworld.com.au | www.ibisworld.co.uk | www.ibisworld.com.cn IBISWorld Industry Report Global Plastic Product & Packaging Manufacturing February 2014 About This Industry ................................. 2 Industry Definition .........................................2 Main Activities ...............................................2 Similar Industries ..........................................2 Additional Resources ....................................3 Industry Performance .............................. 4 Executive Summary ......................................4 Key External Drivers .....................................4 Current Performance ....................................5 Industry Outlook............................................7 Industry Life Cycle ........................................9 Products & Markets ................................. 10 Supply Chain ................................................10 Products & Services .....................................11 Demand Determinants ..................................13 Major Markets ...............................................13 International Trade........................................15 Business Locations .......................................16 Competitive Landscape ........................... 17 Market Share Concentration ........................ 17 Key Success Factors ................................... 17 Cost Structure Benchmarks ......................... 18 Basis of Competition .................................... 20 Barriers to Entry ........................................... 21 Industry Globalization .................................. 22 Major Companies .................................... 23 Other Players ............................................... 23 Operating Conditions .............................. 25 Capital Intensity ........................................... 25 Technology & Systems ................................ 25 Revenue Volatility ........................................ 26 Regulation & Policy ...................................... 26 Industry Assistance ...................................... 27 Key Statistics ........................................... 28 Industry Data................................................ 28 Annual Change ............................................ 28 Key Ratios.................................................... 29 Jargon .......................................................... 29 Global Plastic Product & Packaging Manufacturing

-

Upload

nathan-yeh -

Category

Documents

-

view

15 -

download

2

description

IBIS World Study on the Global Plastic Product Industry in 2013.

Transcript of IBIS Global Plastic Product

CONTENTS

Error! No text of specified style in document.

February 2014

www.ibisworld.com | www.ibisworld.com.au | www.ibisworld.co.uk | www.ibisworld.com.cn

IBISWorld Industry Report

Global Plastic Product & Packaging Manufacturing

February 2014

About This Industry ................................. 2 Industry Definition ......................................... 2 Main Activities ............................................... 2 Similar Industries .......................................... 2 Additional Resources .................................... 3

Industry Performance .............................. 4 Executive Summary ...................................... 4 Key External Drivers ..................................... 4 Current Performance .................................... 5 Industry Outlook............................................ 7 Industry Life Cycle ........................................ 9

Products & Markets ................................. 10 Supply Chain ................................................ 10 Products & Services ..................................... 11 Demand Determinants .................................. 13 Major Markets ............................................... 13 International Trade........................................ 15 Business Locations ....................................... 16

Competitive Landscape ........................... 17

Market Share Concentration ........................ 17 Key Success Factors ................................... 17 Cost Structure Benchmarks ......................... 18 Basis of Competition .................................... 20 Barriers to Entry ........................................... 21 Industry Globalization .................................. 22

Major Companies .................................... 23 Other Players ............................................... 23

Operating Conditions .............................. 25 Capital Intensity ........................................... 25 Technology & Systems ................................ 25 Revenue Volatility ........................................ 26 Regulation & Policy ...................................... 26 Industry Assistance ...................................... 27

Key Statistics ........................................... 28 Industry Data ................................................ 28 Annual Change ............................................ 28 Key Ratios .................................................... 29 Jargon .......................................................... 29

Global Plastic Product & Packaging Manufacturing

WWW.IBISWORLD.COM Global Plastic Product & Packaging Manufacturing February 2014 2

About This Industry

Industry Definition

Enterprises in this industry manufacture a variety of plastic goods, including plastic building materials, products used to package food and beverages and plastic products used to manufacture furniture and other durable goods. Companies that manufacture foam products, such as those used in automotive manufacturing and insulation for housing, are also included in this industry.

Main Activities

The primary activities of this industry are:

Manufacturing foam used in furniture, construction, transportation and electrical goods

Manufacturing of foam packaging products

Manufacturing plastic containers and packaging products

Manufacturing plastic pipes, plates, shapes and sheets, including plastic bags

Manufacturing plastic used in furniture, construction, transportation and electrical goods The major products and services in this industry are:

Plastic used in furniture, construction, transportation, electrical

Plastic pipes, plates, shapes and sheets, including plastic bags

Plastic containers and packaging products

Foam used in furniture, construction, transportation and electrical

Foam packaging products

Other

Similar Industries

C2111-GL - Global Glass and Glass Products Manufacturing This industry manufactures glass and glass products.

WWW.IBISWORLD.COM Global Plastic Product & Packaging Manufacturing February 2014 3

Additional Resources

For additional information on this industry: www.cpia.ca Canadian Plastics Industry Association www.plasticseurope.org PlasticsEurope www.plasticsindustry.org The Plastics Industry Trade Association www.chinaplasonline.com Chinaplas www.euromap.org EUROMAP

WWW.IBISWORLD.COM Global Plastic Product & Packaging Manufacturing February 2014 4

Industry Performance

Executive Summary

Over the past five years, consumers of have increased their consumption of plastic. Plastic products have increasingly substituted materials such as wood, paper, metals and glass in many applications. Plastic is often more price-competitive, while also offering better performance characteristics. As a recyclable material, plastic also provides environmental benefits, such as waste reduction and energy savings. This trend has boded well for global plastic product manufacturers, with revenue expected to grow 1.7% in 2014 to $830.5 billion, capping annualized growth of 2.8% in the five years to 2014. This increase has been underpinned by recovery from recessionary lows, and revenue growth is expected to continue moving forward. The next five years are expected to be prosperous for the industry thanks to continuing improvements in demand for plastic. However, input price volatility and concerns about a slowdown in rapidly developing Asian economies, notably China, will threaten the industry over the next five years. Despite challenges, industry revenue is expected to grow at an annualized rate of 2.1% from 2014 to 2019 to reach $920.9 billion. Global demand for construction remains a key revenue driver for the industry. Over the past five years, this sector exhibited massive growth due to the economic recovery in developed countries and the speedy industrialization of economies like India and China. Over the next five years, the construction sector is expected to grow moderately, boosting industry revenue. As global construction markets continue to strengthen, IBISWorld anticipates industry operators to benefit from the plastic products they produce for construction projects. A wide variety of manufacturing industries use plastic products, including those involved in food and beverages, household chemicals, pharmaceuticals, personal care, automobiles, furniture and household appliances. Because food is less discretionary for consumers, operators that cater to the food and beverage market likely outperformed the rest of the industry during the financial crisis. Additionally, the packaging segment of the industry likely performed relatively well against other industry products due to the inelastic nature of demand for packaging products.

Key External Drivers

The key sensitivities affecting the performance of the Global Plastic Product & Packaging Manufacturing industry include: Downstream Demand - Manufacturing Plastic products are often sold as inputs to manufacturers of intermediate and final goods. These customers form a large part of the industry's revenue base, and therefore have a significant effect on the industry's performance. In addition, industry products are also used to package downstream manufactured goods. Downstream demand from manufacturing is expected to increase during 2014. Downstream Demand- Motor Vehicle and Part Manufacturing Plastic products are used to manufacture automobiles and vehicle component parts. As demand and vehicle production increase, automotive manufacturers will increase their use of plastic products, resulting in greater revenue for the industry. Demand from motor vehicle and related parts manufacturers is expected to increase in 2014. Global consumer spending Many of the items this industry produces are either sold to households or used as inputs for products that are subsequently sold to households. Therefore, an increase in global consumer spending results in additional revenue. Global consumer spending is expected to increase during 2014.

WWW.IBISWORLD.COM Global Plastic Product & Packaging Manufacturing February 2014 5

Global value of construction The level of construction activity affects demand for plastic products used in the building process. Plastic products are used for insulation purposes and are found in plumbing systems and other parts of a building, such as light switches and power plugs. Thus, as residential and nonresidential construction activity increases, so does demand for plastic products. The global value of construction is expected to increase during 2014, representing a potential opportunity for the industry. World price of crude oil This industry's largest costs are associated with inputs and raw materials, such as crude oil. In times of high demand, higher oil prices can generally be passed down to customers in the form of higher prices. Conversely, during periods of weak demand, higher oil prices can adversely affect profitability. Although the world price of crude oil is expected to decline in 2014, prices have historically shown a great deal of volatility. As such, oil prices remain a threat to the industry.

Current Performance

From food producers to car manufacturers, this industry supplies plastic products to a wide range of sectors. The industry manufactures plastic containers for food, beverages, household chemicals and personal care products. It also manufactures plastic components for motor vehicles, buildings (e.g. plumbing fixtures and pipes), furniture and household appliances. Consequently, demand for each of these downstream products affects demand for plastic. In the five years to 2014, demand for plastic recovered from the shocks of the global financial crisis. Industry revenue fell in 2009 as construction activity and motor vehicle manufacturing activity contracted in Europe and North America and consumer sentiment plummeted worldwide, but the industry has recovered strongly from this decline. Innovation and cost cutting The main material used to produce plastic products is plastic resin, a petroleum-based product. For this reason, fluctuations in global crude oil prices lead to changes in the input costs for plastic manufacturers. Crude oil prices are generally volatile, but an overall trend of increasing costs per barrel has prevailed over the five years to 2014, with oil prices growing at an annualized rate of 10.1% over the period. With competition being mostly price-based, companies have struggled to develop more affordable and environmentally friendly products. For example, manufacturers were able to reduce the weight of polyethylene terephthalate (PET) bottles by 30.0% by using fewer raw materials in the manufacturing process. This method has also been used in other product segments and will become more widespread as stronger and lighter plastics are developed. In addition, manufacturers have improved their production capabilities worldwide by adopting labor-saving machinery, such as in-line socketing machines; in effect, operators have increased productivity and decreased wage costs. Many larger companies have also developed manufacturing operations in regions such as Southeast Asia to take advantage of greater labor resources at more affordable rates. The growing level of manufacturing in this part of the world has aided improved technical proficiency, allowing more complex items to be manufactured at far lower costs and relieving some of the pressure on profit margins that persisted during the recession. As a result of manufacturers moving production to cost-saving areas, employment numbers have increased faster than wage costs. Industry labor is expected to expand at an average annual rate of 3.1% over the five years to 2014 to 4.1 million people. However, the average wage has declined at an annualized rate of 0.8% since 2009. Furthermore, as the costs of operation continue to decline, IBISWorld expects the number of industry establishments to expand at an annualized rate of 3.6% in the five years to 2014 to reach an estimated 139,488. Fluctuating demand Overall, demand for plastics has grown consistently in the five years to 2014, especially from the automotive sector, with consumers and manufacturers increasingly seeking lower cost and more

WWW.IBISWORLD.COM Global Plastic Product & Packaging Manufacturing February 2014 6

environmentally friendly, fuel-efficient cars. Plastics have become a common substitute for many metals in this sector, providing a lightweight alternative that provides a similar level of protection. Additionally, consumer preferences have been shifting toward smaller single-serving food packages, which has fueled demand for plastic packaging. Electrical products, computers, consumer goods, motor vehicle manufacturing and packaging industries worldwide are major consumers of plastic products. China, a major force in each of these sectors, is a large market for the Plastic Product and Packaging Manufacturing industry. For example, in 2012, China experienced an oversupply of plastics due to excessive domestic production and slower-than-expected demand for plastic product exports. Revenue and profitability Industry revenue growth has been strong throughout most of the period from 2009 to 2014. Besides a sharp 11.2% decline in 2009 in response to the global economic crisis, industry revenue has grown every year over the past five years at an annualized rate of 2.8% to $830.5 billion, including a 1.7% jump in 2014. The industry has especially benefited from rapidly recovering demand from downstream industries. While Asia has increasingly played a key role in this industry's success, the recovering housing and automobile markets in the United States have also driven demand for plastic products. Industry profitability has rebounded strongly after collapsing to 2.4% of revenue during 2009. Currently, industry profitability, measured by earnings before interest and taxes, is expected to be 4.5% of industry revenue. Fluctuating world oil prices, which impact not only the cost of plastic resin, but also transportation costs, have spurred many manufacturers to set up operations close to key buying industries. In the five years to 2014, the world price of crude oil is expected to rise at an annualized rate of 10.1%. As companies continue to innovate, develop product lines and set up manufacturing operations in low-cost areas of the world, such as South East Asia, IBISWorld expects that operators will continue to pass along rising input costs to consumers.

WWW.IBISWORLD.COM Global Plastic Product & Packaging Manufacturing February 2014 7

Industry Outlook

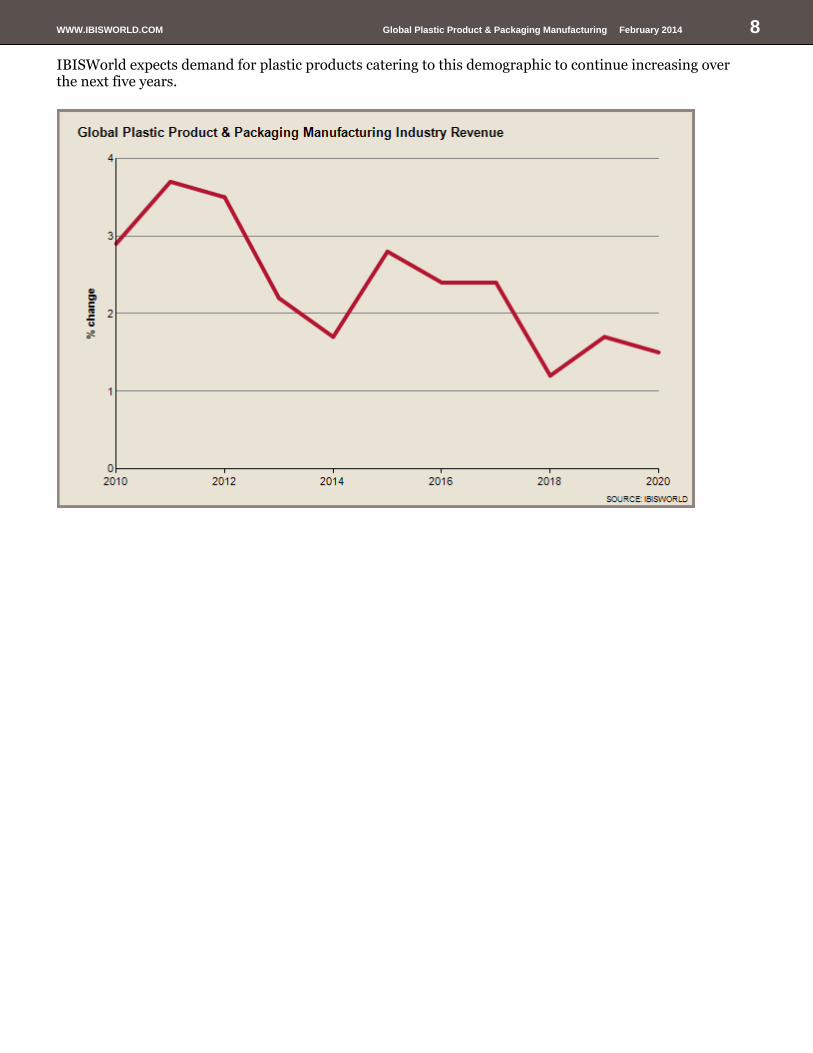

The Global Plastic Product and Packaging Manufacturing industry is expected to fare well over the next five years. IBISWorld anticipates that revenue will grow at an annualized rate of 2.1% through 2019 to $920.9 billion. Much of this growth will likely result from product development and entry into new markets, driven by a growing demand and preference for plastics as opposed to substitute materials. The versatility of plastic when compared with materials like glass, wood, metal or paper is one of the major advantages plastic manufacturers have over their competition. Profit and demand IBISWorld expects profit margin growth to be constrained in the five years to 2019, exhibiting a slight rise from 4.5% of revenue in 2014 to 4.7% in 2019. World crude oil prices, which affect the price of plastic resin inputs, are expected to continue growing at an annualized rate of 3.7% over the next five years. Rising oil prices will also negatively impact transportation costs. Manufacturers will likely not be able to pass all the additional costs on to consumers and will therefore absorb a portion of the cost increase. In addition, an oversupply of plastic in Asia will challenge operators' ability to raise product prices. Furthermore, growing wage costs in previously low-cost countries, such as China, may further limit profit margin growth. Consequently, wages are expected to rise at an annualized rate of 2.3% to $84.1 billion in the five years to 2019. However, as manufacturing capabilities become more advanced, the industry will be able to produce higher-quality items. Technological advances and reducing the weight of plastic materials, as well as the quantity of materials used to produce industry items, will help to protect profit margins from the threat of rising input costs. Greater demand for plastic products will encourage companies around the world to invest more in research and development. Manufacturers will strive to create products that can enter new markets and compete against products traditionally dominated by goods manufactured using substitute materials. Product innovation will continue to be a key feature of the industry, and obtaining patents will remain an important form of competition for operators. IBISWorld expects the number of industry enterprises to grow at an annualized rate of 2.3% in the five years to 2019 to reach 150,909 as new companies innovate products and develop patents. Employment opportunities Stronger global demand for plastics will encourage continued demand for low-cost labor and sustained growth in employment and enterprise numbers. Much of the industry's workforce over the next five years is forecast to expand in regions such as Southeast Asia, where labor costs are significantly lower than those in more developed regions. Many larger operators will follow the trend by moving the bulk of their manufacturing facilities into low-cost countries, leaving more specialized divisions, such as research and development and corporate headquarters, in developed nations. Key demand drivers The recyclability of plastic products gives the industry yet another competitive advantage, with environmental issues expected to remain a primary concern for governments around the world. The global climate change debate has prompted governments to act, as public awareness of environmental issues has increased, placing greater emphasis on increasing production efficiency, reducing energy consumption and expanding recyclability. Recycling plastic requires half the energy of burning plastic, and 70.0% less energy is needed to produce plastic products made from recycled plastics. Industry research and development over the next five years is expected to focus on creating cost-effective, environmentally friendly plastic products. Such products would appeal to environmentally conscious consumers while also reducing manufacturing costs as technology continues to improve. A greater number of people are living alone, particularly in developed countries, such as the United States, Japan and many the United Kingdom; to serve this consumer segment, operators have introduced more single-serving food and beverage packages. As a result, food and beverage producers are increasing their demand for foam and plastic packaging products. At the same time, industry operator Graham Packaging Company notes there is a trend toward concentrated fabric care products, which use smaller packages.

WWW.IBISWORLD.COM Global Plastic Product & Packaging Manufacturing February 2014 8

IBISWorld expects demand for plastic products catering to this demographic to continue increasing over the next five years.

WWW.IBISWORLD.COM Global Plastic Product & Packaging Manufacturing February 2014 9

Industry Life Cycle

This industry is in the mature stage of its life cycle. Life Cycle Stage

Plastic is gaining market share over substitute goods, such as glass and aluminum

Technological innovation is improving and expanding the industry's product range

The industry's contribution to the global economy will lag global GDP growth in the 10 years to 2019

The number of establishments will increase

The Global Plastic Product and Packaging Manufacturing industry is operating in the mature stage of the life cycle. In the 10 years to 2019, the industry is expected to grow less than the overall global economy. IBISWorld estimates that industry value added will grow at an annualized rate of 2.9% from 2009 to 2019, slower than the expected world GDP growth of 5.9% over the same period. The financial crisis saw global aggregate demand fall drastically in the early portion of the past five years. This industry was deeply affected because its consumer base is so diverse and widespread. Falling household expenditure saw demand for plastic products used in the packaging of food and beverages decline, as well as plastic used to produce furniture and household durable goods. Much the same, the use of plastic in automobile manufacturing fell as car producers around the globe saw demand for vehicles fall. In response, they decreased their production volumes, and consequently, their demand for plastic goods. However, other indicators suggest that the industry is moving into a growth stage of its life cycle. The industry's products are continuing to penetrate new markets traditionally dominated by products made of traditional materials, such as wood, glass and metals. Allowing for this to occur are technological advancements that enable manufacturers to produce plastic products that can be sold to the market at a lower price than competing goods, without compromising quality and performance. Because plastics are such versatile materials, this trend is likely to continue, and may result in the industry's move into the growth stage of its life cycle over the next five years. Linked to this technological change is a key feature of this industry: companies often work with customers in product development. Industry operators note the importance of product innovation and often conduct research and development activities. Companies in this industry compete on the basis of price, quality, new product introductions and economies of scale. For example, industry manufacturer Illinois Tool Works states in its annual report that it has seen growth due to the development of new products, broadening the applications of existing products and from the development of new manufacturing processes. As another example, Saudi Basic Industries Corporation cites its work with a customer to develop a new resin that is comprised of up to 25.0% post-consumer recycled content from used water bottles.

WWW.IBISWORLD.COM Global Plastic Product & Packaging Manufacturing February 2014 10

Products & Markets

Supply Chain

Key Buying Industries A-GL - Global Agriculture, Hunting, Forestry and Fishing Farmers purchase plastic and foam products in packaging of fresh foods such as meat, fruit and vegetables, fish and dairy products. C-GL - Global Manufacturing Downstream manufacturing industries use plastic packaging as well as intermediate plastic products which are integrated into the final consumer good production. E-GL - Global Construction Foam and plastic goods are used in the construction of housing and real estate, i.e. plastic pipes and insulation foam. F-GL - Global Wholesale and Retail Trade Wholesalers and retailers use plastic products in securing products during shipments and for packaging purposes. G-GL - Global Hotels and Restaurants Disposable plastic food containers and other plastic packaged products are used by restaurants and other hospitality industries. Key Selling Industries C1912-GL - Global Petrochemicals Manufacturing This industry supplies plastic product manufacturers with chemicals used as inputs in the production process. C1931-GL - Global Resin and Synthetic Rubber Manufacturing Resins are used in the production of plastic product and are purchased from this industry. F4311-GL - Global Wholesale Trade Wholesalers supply the industry with machinery as well as some inputs that are not purchased directly from other manufacturers.

WWW.IBISWORLD.COM Global Plastic Product & Packaging Manufacturing February 2014 11

Products & Services

Foam packaging products 1.9%

Foam used in furniture, construction, transportation and electrical

9.6%

Other 0.8%

Plastic containers and packaging products 14.0%

Plastic pipes, plates, shapes and sheets, including plastic bags

32.5%

Plastic used in furniture, construction, transportation, electrical

41.2%

The industry produces a wide variety of plastic products, which are mainly used by downstream manufacturers, wholesalers and construction companies. The largest product group is plastic products used in furniture, construction, transportation, electrical and consumer goods. These items are mainly intermediate manufactured goods, which are integrated into other consumer. Demand for these products is dependent on construction activity and the level of manufactured output. As such, during the global downturn, this product group experienced a sharper fall in revenue compared with the rest of the industry, given the slowdown in construction in most developed nations. Plastic pipes, plates, shapes and sheets, plastic bags and film are the next largest product group, accounting for 32.5% of revenue. These products are used in a variety of applications, including construction, manufacturing, supermarkets and grocery stores. Demand is dependent on activity in these downstream industries. During the global recession, demand from supermarkets and grocery stores was considerably more stable compared with construction and manufacturing. Therefore, sales of plastic bags outperformed the rest of the industry, particularly in developing nations where economic growth remained positive and consumerism continues to grow. Plastic containers and packaging products account for 14% of revenue, increasing from 11.5% in 2009. This product segment has become more significant over the past five years due to strong manufacturing activity in emerging economies and growing demand for packaging with changes in household formation and population demographics. Single person households are on the rise, necessitating smaller food portions and greater packaging as other consumables are packaged to target this growing market. Also, technological developments in plastic packaging have made this product group more environmentally friendly, which has increased its appeal among buyers. According to industry operators, there are two main segments in the plastic container industry: conventional plastic containers, which include containers for drink and are manufactured in large numbers; and custom containers, which are tailor-made to have unique characteristics, such as heat resistance or air tightness. Graham Packaging Company is an example of a company that focuses on the custom plastic packaging for food, beverage, household, personal care and automotive lubricants. It states that plastic containers are one of the fastest growing segments in rigid packaging. Smaller product groups include foam packaging and foam used in furniture, transportation, electrical and consumer goods. Similarly with plastic products, foam used in construction and some manufacturing has experienced a sharper decline during the economic downturn compared with packaging, due to its reliance on construction activity. Other products include polyester based products, garbage bins and all other plastic products, demand for which has grown in line with the rest of the industry over the past five years.

WWW.IBISWORLD.COM Global Plastic Product & Packaging Manufacturing February 2014 12

WWW.IBISWORLD.COM Global Plastic Product & Packaging Manufacturing February 2014 13

Demand Determinants

Plastic products have a wide variety of applications, from packaging of foods and beverages to insulation used in housing construction. Furthermore, this industry's manufacturers produce plastic products that are, in many cases, used as inputs in the production process of intermediate and final goods. For example, plastic bottles are used to package beverages, while plastic pipes are used in construction when installing utilities' infrastructure, among other things. Because of these features and their far-reaching applications a number of factors affect the demand for plastic products, most importantly, price. Plastic products are fairly simple, easy to replicate, homogeneous products that are also highly substitutable with paper, glass and aluminum products, depending on their application. In packaging, plastic bags are highly substitutable with paper bags, while plastic bottles can easily be replaced by glass bottles or aluminum cans. For this reason, it is vital that plastic products are competitively priced. Although facing tough competition from substitutes, manufacturers also face strong price competition between one another as consumers are happy to switch to cheaper suppliers of plastic products given that their perceptions are that the goods are of a similar look, standard and quality. Their use in the manufacture of intermediate and final goods also affects demand, determined by the demand exhibited in downstream markets for the intermediate and final goods themselves. Manufactured plastic goods are used in the production of automobiles. Foam products form parts of the seating, interiors of the doors, boot, floor and roof of the car (among others), while plastic products are used to in the dashboard, lights, the engine and many other interior and exterior component parts. As such, when the demand for automobiles falls, as it had during the Global Financial Crisis recently experienced, the demand for plastic products also falls, as automobile manufacturers reduce their production and therefore the plastic product they require/demand. Other factors affecting the demand for the industry's products are less industry specific and are of a broad and macroeconomic scale. For instance, an increase in the unemployment rate can adversely affect consumer spending, and it can also negatively affect the household sector's ability to attain mortgage finance. This tends to translate into less construction of new housing taking place. Thus, the demand for plastic products falls as plastic used in packaging of consumer goods, furniture, automobiles and that used in construction declines with consumption falling. Likewise, interest rates, household debt and aggregate demand can all have similar effects on the Global Plastic Product and Packaging Manufacturing industry.

Major Markets

Packaging 40.1%

Other 26.9%

Building and construction 20.4%

Motor vehicle and transport manufacturing 7.0%

Electrical equipment and components 5.6%

WWW.IBISWORLD.COM Global Plastic Product & Packaging Manufacturing February 2014 14

Packaging At 40.1% of industry revenue, this market includes a number of manufacturing and food and beverage industries that use industry packaging products as part of a final product. These products include items such as bottles, containers, plastic bags, film and foam used in the packaging of other items. The durability of plastics and their ability to hold wet, dry, hot and cold products has seen the use of plastics in packaging increase significantly in recent years. Producing plastic packaging is also beneficial for manufacturers, as products are often generic and required in large numbers. Growing amounts of consumption in China, India and other developing countries also drives demand for plastic packaging. Building and construction Accounting for 20.4% of industry revenue, the construction industry is also a major market for plastic products, such as pipes, floor and wall coverings and insulation. Demand for these products, however, is dependent on the level of construction activity across the globe. During the financial slowdown in 2008 and 2009, construction in many of the world's major economies drastically slowed down, this lead to a major fall in revenue for firms producing these types of products. Thankfully for the industry, construction activity is beginning to pick up again in developed countries, such as the United States. Motor vehicle and transportation Plastics for use in the manufacturing of motor vehicles are also a significant market of this industry, comprising 7.0% of all industry demand in 2014. The constant development of lighter and stronger plastics has seen automotive companies increase their reliance on plastics over traditional metals, as consumers, particularly those in developed economies, search for a more environmentally friendly motor vehicles. Ever increasing world oil and fuel prices has also driven the greater use of plastics in motor vehicles, due to their lighter weight and therefore greater fuel efficiency. The global economic crisis also took a toll on this sector of the industry, as many consumers put off non-essential vehicle purchases until the outlook was more stable and positive. Electrical Equipment and components Plastics are also used extensively in the manufacture of electrical equipment and components. Comprising 5.6% of total industry demand in 2014, plastics are a popular choice in many electrical items because of their light weight and resistance to electrical shock when compared to alternative materials, such as metal. Other Accounting for an estimated 26.9% of industry revenue in 2014, other market segments include sports and leisure industries, agricultural applications and other durable goods manufacturing industries. Because this market encompasses a broad selection of different industries, demand has been fairly stable over the past five years. However, since much of this market is dependent on the level of disposable income in any particular economy, demand from these buyers suffered a setback throughout the recession.

WWW.IBISWORLD.COM Global Plastic Product & Packaging Manufacturing February 2014 15

International Trade

Exports in this industry are low and steady. Imports in this industry are low and steady.

As a global industry, international trade data is not recorded within the key statistics section of this report. Furthermore, global trade of industry products is limited, due to the fact that many plastic products are low-value, high-volume goods, which are not cost-effective to ship overseas. Nonetheless, international trade does occur within country-specific industries that produce similar goods. As one example, exports within the US Plastic Bottle Manufacturing industry (IBISWorld report 32616), are estimated to account for 5.4% of that industry's revenue. Similarly, imports of plastic bottles into the United States are low, accounting for an estimated 6.9% of US demand. The largest export destinations for US plastic bottle manufacturers are Canada and Mexico, which benefit from their shared borders with the United States, and from favorable trade conditions via the North American Free Trade Agreement. The bulk of imported plastic bottles into the United States come from Canada, as well as China, which continues to lure manufacturers seeking lower labor and production costs.

WWW.IBISWORLD.COM Global Plastic Product & Packaging Manufacturing February 2014 16

Business Locations

Region %

North America 28.7

Europe 28.5

North Asia 25.5

Africa & Middle East 5.2

South America 4.5

India & Central Asia 3.7

South East Asia 2.7

Oceania 1.2

Historically, North America and Europe have been the largest plastic product manufacturing regions of the world. This is not surprising given the productivity of the regions, which generally results in high levels of consumption expenditure. However, over the past 10 to 15 years, these two regions have lost some of their share of the global market. Strong competition from emerging economies, mainly China, has resulted in more and more companies closing shop in the US, Europe and Canada. At the same time, major global companies from the Western world have ramped up foreign investment in China and other developing nations, taking advantage of cheap production costs associated with labor and raw materials. This has led to the growing dominance of North Asia in the industry, as well most other manufacturing industries. North Asia accounts for 25.5% of total revenue. China is the largest producer in the region, doubling its production capacity over the past ten years. Japan is also a strong player, although much like the US and Europe, its manufacturing output is declining. Oceania is the only other region in the world, which has lost its share of revenue over the past five years, with domestic manufacturing companies unable to compete with cheaper, imported goods flooding their domestic markets. The rest of the world's regions are considered to be developing and are growing in dominance in the global manufacture of plastic products, slowly taking away the market share of more developed Western economies. Over the next five years, it is likely that developing economies such as Bangladesh and Cambodia will play an increasing role in global plastics manufacturing.

WWW.IBISWORLD.COM Global Plastic Product & Packaging Manufacturing February 2014 17

Competitive Landscape

Market Share Concentration

Industry concentration is low.

The Global Plastic Product and Packaging industry has a fragmented structure, resulting in a low level of market share concentration. The three largest players are estimated to account for a mere 4.0% of revenue in 2014. The industry's low concentration is primarily due to the fact there are more than 134,000 enterprises operating within the industry, each manufacturing a certain type of product that caters to a specific and limited customer base. As such, an enterprise's ability to generate revenue and dominate the market is limited by the range of products manufactured and its global reach. Additionally, the range of products that are produced from plastics is extremely broad, making it extremely difficult a company to increase its market share. As such, very few firms have the scope to be able to produce on such a large and diverse scale.

Key Success Factors

The key success factors in the Global Plastic Product & Packaging Manufacturing industry are: Economies of scale The development of large-scale production facilities allows firms to minimize per unit costs of production. Having the ability to produce on a large scale also gives them the ability to attract large customers and contracts. Effective quality control Producing high-quality goods on a consistent basis can attract new customers and help increase sales as quality of the products manufactured is a key competitive feature of this industry. Output is sold under contract - incorporate long-term sales contracts Negotiating long-term supply contracts with customers ensures a more consistent revenue stream and allows firms to plan their expenditures on a long term basis. Undertaking technical research and development Use of plastic and its applications continues to develop, as such firms must have the right R&D programs in place to keep up with the changing nature of the industry and the products offered to the market. Supply contracts in place for key inputs Inputs contribute a large proportion to cost in this industry, therefore manufacturers must ensure they have contracts in place that minimize the price paid for inputs as it directly affects their profit margins. Effective cost controls Profit margins are a key concern, as such firms must have effective cost controls in place that ensure costs are minimized by monitoring inventory levels, costs associated with sales and production capacity.

WWW.IBISWORLD.COM Global Plastic Product & Packaging Manufacturing February 2014 18

Cost Structure Benchmarks

Purchases 70.6%

Wages 9.0%

Rent & Utilities 4.7%

Depreciation 3.3%

Marketing 0.5%

Other 7.4%

Profit 4.5%

Profit The industry's profit margin is still recovering from a significant decline in 2009, when profit fell to 2.4% of industry revenue. Currently, industry profit margins are estimated to account for 4.5% of revenue. Some of the larger industry companies have padded their margins by offshoring manufacturing operations to more cost-effective corners of the world, such as China. As demand for plastics around the world grows, profit figures should continue to benefit as manufacturing systems become more automated and the reliance on labor decreases. IBISWorld expects profit to grow marginally in the five years to 2019. Purchases The largest cost this industry incurs is for inputs, such as plastic resins and recycled feedstock. IBISWorld estimates that purchases will account for 70.6% of total industry revenue in 2014. Producers are generally price takers as prices of inputs are determined by the global market. Affecting prices of plastic resins are demand and supply considerations, and more importantly, the price of oil. Oil feedstock is used as an input in the manufacture of plastic resins. Because oil prices can fluctuate considerably over time, so too can the price of plastic resins, affecting the cost of inputs for manufacturers. As a result of fluctuating input prices, producers typically negotiate long-term contracts with their suppliers that contain price escalation clauses. In this way, industry manufacturers are able to maintain some control over input costs. Despite a forecasted dip in crude oil prices, world oil prices are expected to continue climbing over the long term future, placing some pressure on industry profitability. Labor and depreciation Wages, which currently account for an estimated 9.0% of industry revenue, are another significant expense for industry manufacturers, and are affected by the amount of labor the industry employs and the availability of unskilled labor. In this regard, developing countries in South East Asia and South America have a competitive advantage compared to the developed regions of the world. This is due to the fact that there is an abundance of cheap labor in these regions that can be employed quickly to meet demand. In general, this industry's manufacturing processes do not require any highly-skilled labor functions or special education requirements. Wages have displayed a downward trend over the past five years, and this trend is set to stability, with wages growing marginally in the five years to 2019.

WWW.IBISWORLD.COM Global Plastic Product & Packaging Manufacturing February 2014 19

Being a highly capital intensive industry, manufacturers of plastic products invest heavily in machinery and equipment in order to achieve optimal productive efficiency. In this way, greater levels of automation can be achieved that reduce handling costs and those related with product defects and labor. As such, depreciation costs are significant, amounting to 3.3% of industry revenue in 2014. Other Rent and utilities are expected to consume 4.7% of industry revenue in 2014, reflecting costs associated with leasing manufacturing facilities and electricity. Although a small share, marketing and advertising costs are expected to account for 0.5% of industry revenue. Other costs, not including rent, utilities and advertising are expected to total 7.4% of industry revenue and include research and development initiatives, insurance premiums and administrative expenses.

WWW.IBISWORLD.COM Global Plastic Product & Packaging Manufacturing February 2014 20

Basis of Competition

Competition is high and increasing. Competition in this industry is principally based on price. In this industry, large customers can be in a strong position when negotiating price, which shows that price is a significant competitive factor. In recent years, industry players reported an erosion of margins because they could not pass on, in full, the increase that had occurred in raw materials and transport costs. Another significant competitive factor is the quality of the products produced and the reliability of delivery times. Downstream users of plastic products seek to work with manufacturers who are able to produce high quality goods that they are then able to transport reliably and seamlessly to their end markets with minimal disruptions and delays. Manufacturers who have the technology to innovate new products are at a competitive advantage to their rivals. One example of this has been the extension of shelf life of wine packaged in plastic bottles. As such, those companies that are able to access such technology and produce bottles with such features are at a competitive advantage to their peers. Furthermore, with environmental issues being so topical and businesses looking to improve their social responsibility by reducing their global footprint in terms of the impact they have on the environment, recyclability of the products has become crucial. Social trends and the demand emanating from the market have seen preferences shift towards plastic products, because of their recyclability qualities. Besides the competition faced within the industry from producers of plastic products, competition exists from producers of substitute products. Plastic product is used in many applications, for a wide variety of purposes. Having said this, in many of their uses, they are substitutable with comparable paper, wood, glass and metal based products. The way the industry's various consumer groups, whether households, or manufacturers in downstream industries decide between which of these products they use is based on comparisons between the relative price, weight, performance, safety, recyclability, presentation and versatility of each of these.

WWW.IBISWORLD.COM Global Plastic Product & Packaging Manufacturing February 2014 21

Barriers to Entry

Barriers to entry are high and steady.

Barriers to Entry checklist Level/Impact Industry Competition High

Industry Concentration Low

Life Cycle Stage Mature

Capital Intensity High

Technology Change Medium

Regulation and Policy Light

Industry Assistance Low

SOURCE: IBISWORLD

Barriers to entry for this industry are high. Existing large players can negotiate lower prices for raw materials (principally plastic resins), which represent a large percentage of total industry costs. This enables them to offer their products to their customers at a more affordable price than new or entering competitors which do not have such bargaining power. Because of this, new entrants may find it difficult to compete as price is a key competitive factor used in attracting customers, with demand for plastic products being highly price elastic. Apart from price pressures, significant investments are required in acquiring plant and equipment for the manufacturing process to take place. Larger operators can fund state-of-the-art machinery and are more able to maximize utilization of this equipment which brings down the per unit cost of production. Enabling them, once more, to minimize their costs and under cut prices of their competitors' products. Significant costs are required in research and development expenditures or technology transfer agreements, in order to expand market opportunities to compete and achieve growth. Often joint ventures or strategic alliances between the large global operators occur which may assist to reduce this barrier. Existing operators are able to enter into long term contracts with their customers, who form the demand for the industry's products that exists in the marketplace. As such, new entrants do not only face the difficulties associated with attracting customers away from existing players, but also need to have the ability to negotiate their own contracts with customers as these contracts elapse. This means that timing is crucial and that the offer they give their customers in contract negotiations has to be of better value than that offered by their competitors. This can be quite difficult to achieve. Vertically integrated operators that have been servicing their consumer markets for long periods of time often have a better understanding of their customers, their needs and the general trend of the industry. This may also reduce opportunities for new entrants.

WWW.IBISWORLD.COM Global Plastic Product & Packaging Manufacturing February 2014 22

Industry Globalization

The level of globalization is low and steady.

The Global Plastic Product and Packaging Manufacturing industry exhibits a low level of globalization, as the nature of the industry and the products themselves necessitates operations to be fairly localized. One of the main reasons for this is that plastic products are generic and bulky goods that are used in the production of a wide variety of intermediate and final products. It is inefficient, for example, to produce the plastic components for a car in Europe, ship those parts to the car manufacturer in Asia and then ship the final product back to Europe to be sold. This forces manufacturers to set up operations close to major buying markets to minimize transport costs and deliver goods in a timely manner. Key buying industries will also, when presented with the choice between a manufacturer of plastics in the same country or city or a manufacturer on the other side of an ocean, choose the closer option if the prices are similar. Furthermore, because plastic products have far reaching applications, most countries around the world have developed their own plastic manufacturing industries to serve as the primary source of plastic goods. This has led to the industry's low market share concentration, with no one company able to hold a major market dominance. There are a number of industry players with establishments and operations in multiple countries; however, they typically account for a very small share of total industry revenue.

WWW.IBISWORLD.COM Global Plastic Product & Packaging Manufacturing February 2014 23

Major Companies

There are no major players in this industry

Other Players

With the industry being so fragmented, there is no single large player dominating the market for manufactured plastic products globally. However, IBISWorld has identified three of the largest players operating in Africa, the Middle East, Oceania and North America that have significant control of their respective domestic markets, as well as a significant global presence. Although they represent the largest operators in the industry, from a global perspective, they form only a small share of the total market, accounting for between 0.4% and 1.0% of total revenue. Saudi Basic Industries Corporation Estimated market share: 1.0% Saudi Basic Industrial Corporation (SABIC) is one of the world's largest industrial chemical companies. The company is owned by the government of Saudi Arabia and operates through the following segments: chemicals, performance chemicals, innovative plastics, polymers, fertilizers, metals and technology and innovation. Most relevant to the industry are the innovative plastics and polymers segments. The innovative plastic operations' products include thermoplastic resins, film and sheet products, specialty compounds and coatings for various downstream markets including the automotive manufacturers, aircraft, construction and healthcare industries. The polymers segment produces polyethylene and polypropylene. The company states that it focuses on innovation and invests in new polymer technologies. It invested in expanding its manufacturing operations globally. In 2009, the innovative plastics segment introduced its European STAMAX product line to the North American market, with manufacturing operations in Michigan. The company also expanded resin compounding production in China and India during the past five years. In 2013, SABIC is estimated to have posted $8.0 billion in industry-relevant revenue, giving it a market share of 1.0%. Amcor Limited Estimated market share: 0.6% Amcor, a publicly listed Australian company, is one of the largest packaging companies in the world with operations in 43 countries. As of 2013, its main markets are Western Europe (37.0% of revenue); North America (28.0%); Australia and New Zealand (18.0%); and emerging markets (17.0%). The company was established in the 1860s as Australian Paper Manufacturers, focusing its operations on paper production. In the 1970s and 1980s the company added a range of diverse packaging interests to its traditional papermaking activities, including plastic. In 1986, the company became Amcor Ltd. The company acquired four of Alcan's packaging businesses from Rio Tinto in 2010. These companies include Alcan Packaging Global Pharmaceutical, Alcan Packaging Food Europe, Alcan Packaging Food Asia and Alcan Packaging Global Tobacco. The company also acquired Ball Plastic Packaging America in 2010, which has five plants in the United States. The company operates through four main segments: flexibles, rigid plastics, Australasia and packaging distribution and investment. The flexibles division provides packaging for fresh food, processed food and

WWW.IBISWORLD.COM Global Plastic Product & Packaging Manufacturing February 2014 24

tobacco, through three divisions: flexibles Europe and Americas, flexibles Asia Pacific and global tobacco packaging. The rigid plastics division produces PET containers, used in markets such as food, beverage, pharmaceutical, personal care and household chemicals. According to the group's annual report, the Australasia and packaging distribution is not relevant to this industry as it includes products other than plastic (such as fiber, glass and aluminum). IBISWorld estimates that Amcor generated $4.8 billion in industry-relevant revenue in 2013, giving it a market share of 0.6%. Illinois Tool Works Incorporated Estimated market share: 0.4% Illinois Tool Works Inc. (ITW) was established in 1912 and incorporated in 1915. The company is a worldwide manufacturer of highly engineered products and specialty systems, with 840 operating facilities in 57 countries. The company operates through the following divisions: transportation, industrial packaging, food equipment, power systems and electronics, construction products, polymers and fluids, decorative surfaces and other. The segments most relevant to the industry include the industrial packaging, transportation and other segments. The industrial packaging segment produces steel and plastic strapping and plastic stretch film. The transportation segment produces metal and plastic components, fasteners and assemblies for automobiles. The other segment produces a wide range of products included in this industry, such as plastic bags, plastic packaging for food storage and plastic fasteners for appliances and furniture. In 2013, the company's industry-relevant revenue is estimated to have generated $3.2 billion, giving it a 0.4% market share.

WWW.IBISWORLD.COM Global Plastic Product & Packaging Manufacturing February 2014 25

Operating Conditions

Capital Intensity

The level of capital intensity is high.

There is a heavy reliance on large-scale extrusion machines in manufacturing plastic products

In minimizing per unit costs of production, investment in the latest and most efficient machinery and equipment is necessitated

This industry has a high level of capital intensity. For every dollar spent on wages, companies operating within this industry will allocate an estimated $0.37 on machinery, equipment and other capital expenses. Depreciation, which provides an indication of the level of capital investment, will account for 3.3% of industry revenue in 2014. In comparison, wages will account for an estimated 9.0% of industry revenue. Consequently, the level of capital investment required in this industry is significant. The largest cost this industry incurs is that paid for raw materials, principally resin. In order to produce the final product, manufacturers rely heavily upon large-scale extrusion machines capable of large volume production runs. As such, a relatively low level of labor input is necessitated in the manufacturing process. Contributing further to the high investment requirements is the need to have access to the most efficient extrusion machinery and equipment available, which allow for large production volumes so as to reduce both variable and fixed per unit costs of production. This need arises from the highly competitive market that manufacturers operate in globally. For example, polyethylene terephthalate (PET) container manufacturer Constar states that the ability to compete in the industry is based on flexibility and having economies of scale. The company states that in some cases an entire manufacturing line may be restricted to the requirement of a single customer.

Technology & Systems

The level of technology change is medium.

Technological development in the industry is estimated to be at a medium level, with varying levels of advancements in different parts of the world. The US, the EU and Japan have a highly developed technological base in all industries, and they have the majority of patents. Developed nations have increased their investment in the latest machinery and equipment over the past 10 to 15 years, with significant assistance having been extended from foreign investors. This has led to a solid improvement in productivity in these regions, however they are still behind the developed world, on average. Machine technology used to produce plastic pipe and shapings has improved in recent years. The production capacity of extruders has been boosted by the creation of high output twin screw extruders, improved dye and calibrator designs, water tanks with greater cooling capacity, pullers with greater pulling force, and faster, more accurate saws and cutters. Cooling is the most significant factor limiting line speed and higher output. Recently a new technology involving nitrogen gas cooling of plastic extrusion has been developed. Other research and development conducted within the industry is focused upon expanding the use of recycled materials, improving product performance (e.g. increased strength, reduced wall thickness, increased diameters) and expanding product applications (e.g. high-pressure applications). These developments are allowing plastic product manufacturers to enter new markets and find new uses for their products that are able to compete with products made from substitute materials such as paper, glass, wood and metals, which have traditionally dominated those specific product markets.

WWW.IBISWORLD.COM Global Plastic Product & Packaging Manufacturing February 2014 26

Revenue Volatility

Industry revenue volatility is medium.

In the five years to 2014, the Global Plastic Product and Packaging Manufacturing industry has exhibited a moderate level of revenue volatility. This industry produces plastic products that have a wide array of applications, including: food and beverage packaging; automotive parts and components; construction, including insulation and piping; and furniture manufacturing, among others. For this reason, the revenue volatility of the Global Manufacture of Plastics Products industry is closely aligned with the downstream demand for products that use the products the industry's participants manufacture. Demand for soft drinks and drinks packaged in plastic bottles tend to be seasonal. This translates into volatility in the revenue generated as different weather conditions throughout the various parts of the world influence the demand for drinks and therefore the demand for plastic bottles. Similarly, demand for vehicles can be affected by macroeconomic variables such as unemployment and more directly through tax incentives, for instance. As demand for vehicles fluctuates so too does the demand for foam and plastic products that are used in seating, steering wheel, dashboard and other interior and exterior car components. From a cost-price perspective, the price of inputs that manufacturers pay to produce their products affects the price they charge for the final product they sell to their customers. Resultantly, as prices of inputs rise, the added costs are passed onto consumers through higher prices being charged. This generally sees the demand for plastic products fall, as consumers shift preferences towards relatively cheaper substitute products such as those manufactured from paper board, aluminum and glass, depending on their purpose. This affects the amount of revenue that is generated and, in turn, affects volatility.

Regulation & Policy

The level of regulation is light and the trend is increasing. The level of industry regulation varies across regions. Globally regulation is at a low level, despite the fact that it is moderate in more developed economies, because emerging nations generally lag in environmental regulation. Environmental awareness and associated laws and regulation increase with higher socio-economic standards in regions, as businesses can afford to invest in new machinery and in making their facilities compliant. This is one of the reasons for cheaper plastic products from countries such as China, where regulation is weaker and therefore costs of production are lower. Over time however, regulation is expected to increase in emerging economies as well, as governments aim to reduce pollutants emitted by the production facilities and greenhouse gases. The United States Regulation in the United States is considered to be moderate. Most plastic composites manufacturing operations generate some emissions of hazardous air pollutants (HAPs) during the application and curing of thermoset resins. The manufacturing of composite products with polyester and vinylester resins and gel coats in particular can release significant amounts of the HAP styrene. These emissions are regulated by state and federal air pollution control requirements and most manufacturing facilities are required to obtain a registration or permit. Although plastic manufacturing equipment makers design their equipment and manufacturing process to comply with these standards, the regulations have nonetheless increased the price of the equipment as well as the cost of production. The higher costs associated with these environmental regulations are one of the reasons that companies are now looking to manufacture in countries with fewer environmental regulations, such as China. Recycling legislation, which has also been enacted in several states, requires that a certain specified minimum percentage of recycled plastic be included in certain new plastic containers. Since the price of recycled resin is currently lower than the price for virgin resin, it is unclear how these regulations will affect the cost of production. Depending on the plastic product being produced, these regulations could pose a problem for manufacturers due to the higher level of impurities present in recycled plastic.

WWW.IBISWORLD.COM Global Plastic Product & Packaging Manufacturing February 2014 27

Industry Assistance

The level of industry assistance is low and the trend of industry assistance is steady. There are no specific tariffs for this industry.

Industry assistance is generally in the form of import tariffs, government subsidies or grants, as well as memberships with associations which can influence the industry. It is common for countries to impose tariffs on imported plastic products in order to protect the domestic industry; however, over time this practice is becoming increasingly frowned upon as free-trade agreements among trading partners expand. North America, as the largest plastic product manufacturing region in the world, sees the countries within it trading freely between themselves, imposing some tariffs on imports from other origins. In the US, imports of plastic products made from polypropylene and polyethylene are subject to a 3.1% tariff if they are derived from countries which have normal trade relations with the US (NTR countries). This is most countries in the world, with the exception of a few. In addition, imports of polyethylene terephthalate (PET) products are currently subject to a 7.1% tariff. Imports of both high-density polyethylene (HDPE) and low-density polyethylene (LDPE) products are also subject to a 6.8% tariff. Therefore, some protection exists, however it is lower compared to 20 years ago. Government subsidies and grants to manufacturers are not very common in the Western world but do occur globally. Emerging economies such as China have subsidies for nearly all businesses that are export oriented, and hence reduce their production costs. There are no major industry specific subsidies for plastic product manufacturers in China, while all other subsides for export oriented businesses still apply.

WWW.IBISWORLD.COM Global Plastic Product & Packaging Manufacturing February 2014 28

Key Statistics

Industry Data

Revenue ($m)

IVA ($m)

Establish-ments Enterprises

Employ-ment

Exports ($m)

Imports ($m)

Wages ($m)

World Price of Crude

Oil ($US per barrel)

2005 688,866.9 111,490.8 103,727 100,104 3,318,632 - - 65,336.8 53.4

2006 724,318.1 114,172.7 110,278 106,356 3,513,464 - - 69,989.3 64.3

2007 775,432.1 122,907.5 118,386 114,931 3,645,619 - - 74,055.3 71.1

2008 812,530.7 131,585.9 126,171 123,581 3,841,595 - - 77,958.9 97.0

2009 722,958.9 117,075.4 116,704 114,175 3,522,694 - - 72,251.9 61.8

2010 743,905.0 110,012.6 121,241 117,480 3,648,352 - - 66,122.2 79.6

2011 771,749.6 128,760.3 125,060 121,067 3,765,474 - - 68,563.9 104.0

2012 798,897.6 130,551.4 130,681 126,470 3,912,594 - - 71,433.0 105.0

2013 816,807.9 135,204.1 133,989 129,620 3,995,755 - - 73,126.7 104.1

2014 830,471.0 139,825.6 139,488 134,918 4,101,959 - - 75,048.9 100.2

2015 853,899.0 143,128.0 143,088 138,278 4,198,232 - - 77,093.2 101.0

2016 874,340.6 145,469.4 146,443 141,691 4,308,204 - - 79,262.4 105.0

2017 894,957.5 151,174.0 148,641 143,673 4,385,535 - - 80,961.3 110.5

2018 905,876.0 152,473.6 152,573 147,461 4,466,361 - - 82,451.3 114.9

2019 920,913.5 155,811.7 156,197 150,909 4,552,286 - - 84,130.9 120.0

Annual Change

Revenue (%)

IVA (%)

Establish-ments

(%) Enterprises

(%)

Employ-ment (%)

Exports (%)

Imports (%)

Wages (%)

World Price of Crude Oil

(%)

2006 5.1 2.4 6.3 6.2 5.9 N/C N/C 7.1 20.4

2007 7.1 7.7 7.4 8.1 3.8 N/C N/C 5.8 10.6

2008 4.8 7.1 6.6 7.5 5.4 N/C N/C 5.3 36.4

2009 -11.0 -11.0 -7.5 -7.6 -8.3 N/C N/C -7.3 -36.3

2010 2.9 -6.0 3.9 2.9 3.6 N/C N/C -8.5 28.8

2011 3.7 17.0 3.1 3.1 3.2 N/C N/C 3.7 30.7

2012 3.5 1.4 4.5 4.5 3.9 N/C N/C 4.2 1.0

2013 2.2 3.6 2.5 2.5 2.1 N/C N/C 2.4 -0.9

2014 1.7 3.4 4.1 4.1 2.7 N/C N/C 2.6 -3.7

2015 2.8 2.4 2.6 2.5 2.3 N/C N/C 2.7 0.8

2016 2.4 1.6 2.3 2.5 2.6 N/C N/C 2.8 4.0

2017 2.4 3.9 1.5 1.4 1.8 N/C N/C 2.1 5.2

2018 1.2 0.9 2.6 2.6 1.8 N/C N/C 1.8 4.0

2019 1.7 2.2 2.4 2.3 1.9 N/C N/C 2.0 4.4

WWW.IBISWORLD.COM Global Plastic Product & Packaging Manufacturing February 2014 29

Key Ratios

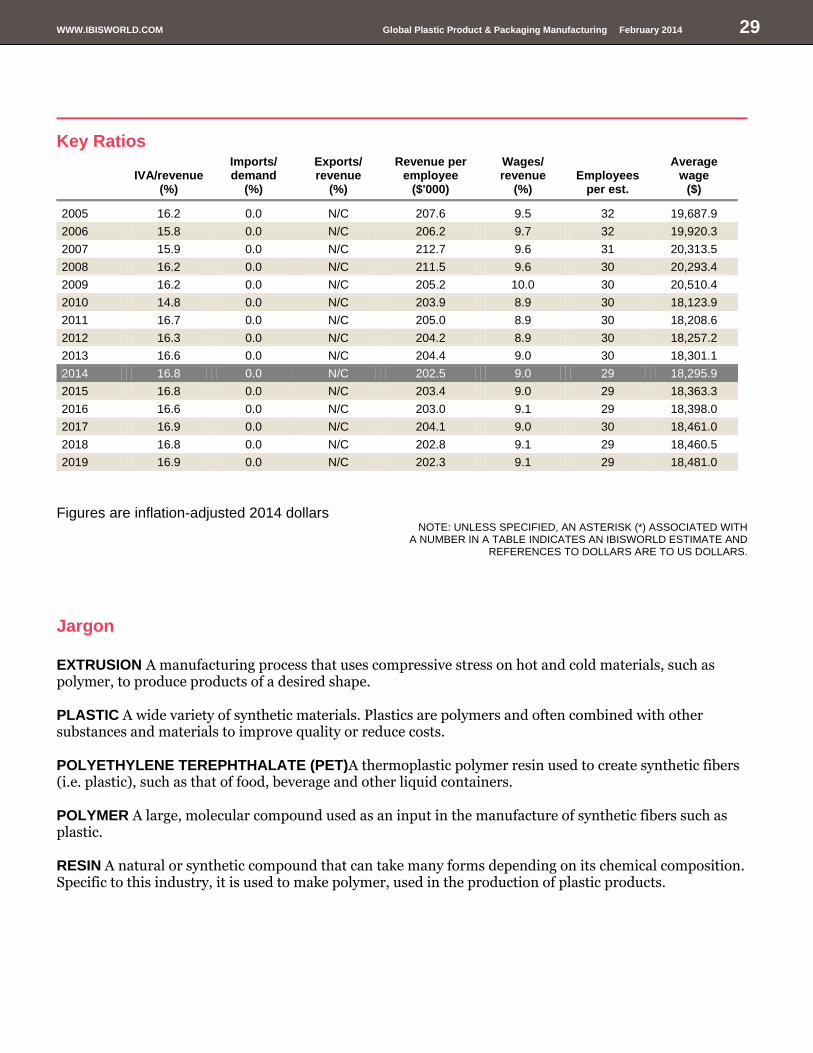

IVA/revenue (%)

Imports/ demand

(%)

Exports/ revenue

(%)

Revenue per employee

($'000)

Wages/ revenue

(%) Employees

per est.

Average wage

($)

2005 16.2 0.0 N/C 207.6 9.5 32 19,687.9

2006 15.8 0.0 N/C 206.2 9.7 32 19,920.3

2007 15.9 0.0 N/C 212.7 9.6 31 20,313.5

2008 16.2 0.0 N/C 211.5 9.6 30 20,293.4

2009 16.2 0.0 N/C 205.2 10.0 30 20,510.4

2010 14.8 0.0 N/C 203.9 8.9 30 18,123.9

2011 16.7 0.0 N/C 205.0 8.9 30 18,208.6

2012 16.3 0.0 N/C 204.2 8.9 30 18,257.2

2013 16.6 0.0 N/C 204.4 9.0 30 18,301.1

2014 16.8 0.0 N/C 202.5 9.0 29 18,295.9

2015 16.8 0.0 N/C 203.4 9.0 29 18,363.3

2016 16.6 0.0 N/C 203.0 9.1 29 18,398.0

2017 16.9 0.0 N/C 204.1 9.0 30 18,461.0

2018 16.8 0.0 N/C 202.8 9.1 29 18,460.5

2019 16.9 0.0 N/C 202.3 9.1 29 18,481.0

Figures are inflation-adjusted 2014 dollars

NOTE: UNLESS SPECIFIED, AN ASTERISK (*) ASSOCIATED WITH A NUMBER IN A TABLE INDICATES AN IBISWORLD ESTIMATE AND

REFERENCES TO DOLLARS ARE TO US DOLLARS.

Jargon

EXTRUSION A manufacturing process that uses compressive stress on hot and cold materials, such as polymer, to produce products of a desired shape. PLASTIC A wide variety of synthetic materials. Plastics are polymers and often combined with other substances and materials to improve quality or reduce costs. POLYETHYLENE TEREPHTHALATE (PET)A thermoplastic polymer resin used to create synthetic fibers (i.e. plastic), such as that of food, beverage and other liquid containers. POLYMER A large, molecular compound used as an input in the manufacture of synthetic fibers such as plastic. RESIN A natural or synthetic compound that can take many forms depending on its chemical composition. Specific to this industry, it is used to make polymer, used in the production of plastic products.

WWW.IBISWORLD.COM Global Plastic Product & Packaging Manufacturing February 2014 30

Disclaimer This product has been supplied by IBISWorld Inc. (“IBISWorld”) solely for use by its authorized licensees strictly in accordance with their license agreements with IBISWorld. IBISWorld makes no representation to any person with regard to the completeness or accuracy of the data or information contained herein, and it accepts no responsibility and disclaims all liability (save for liability which cannot be lawfully disclaimed) for loss or damage whatsoever suffered or incurred by any other person resulting from the use of, or reliance upon, the data or information contained herein. Copyright in this publication is owned by IBISWorld Inc. The publication is sold on the basis that the purchaser agrees not to copy the material contained within it for other than the purchasers own purposes. In the event that the purchaser uses or quotes from the material in this publication – in papers, reports or opinions prepared for any other person – it is agreed that it will be sourced to IBISWorld Inc.

www.ibisworld.com | www.ibisworld.com.au | www.ibisworld.co.uk | www.ibisworld.com.cn

IBISWorld's reports are more than just numbers. They combine data and analysis to answer the questions that successful businesses ask.

Who is IBISWorld? We are strategists, analysts, researchers and marketers. We provide answers to information-hungry, time-poor businesses. Our goal is to provide real-world answers that matter to your business. When tough strategic, budget, sales and marketing decisions need to be made, our suite of industry, economy and risk reports give you thoroughly researched answers quickly. IBISWorld Membership IBISWorld offers tailored membership packages to meet your needs.