IB 1006 Islamic REITS Prof. Dr. Saiful Azhar Rosly International Center for Education in Islamic...

87

IB 1006 Islamic REITS Prof. Dr. Saiful Azhar Rosly International Center for Education in Islamic Finance (INCEIF)

-

Upload

james-fowler -

Category

Documents

-

view

222 -

download

0

Transcript of IB 1006 Islamic REITS Prof. Dr. Saiful Azhar Rosly International Center for Education in Islamic...

IB 1006 Islamic REITS

Prof. Dr. Saiful Azhar RoslyInternational Center for Education in Islamic Finance (INCEIF)

IslamicFinancialSystem

IndirectFinancial

Market

DirectFinancial

Market

Islamic Bond

Market

IslamicEquityMarket

FinanceCompanies

CommercialBanks

UnitTrusts

Takaful

IslamicFinancialMarket

Islamic Financial SystemDefinition: Quranic rules and Regulations (Divine values) that govern the flow of funds from thesurplus spending unit (SSU) to thedeficit spending unit (DSU).

DeficitSector

SurplusSector

IslamicMoney Market

CAPITAL MARKET

Islamic REITS

Merchant banks

LIMITED RESOURCESUNLIMITED

DESIRES

SCARCITY

PROBLEM OF CHOICE

KNOWLEDGE

BASIC ECONOMIC PROBLEMS

P1: What to produce? How much?

P2: How to produce?

P3: How to reward factor inputs?

P4: How to control inflation and unemployment? P5: How to attain positive growth?

Scarcity requiresman to be efficientin utilizing resources

We cannot afford towaste resources under scarcity

Inefficiency due tomisallocation of resourcescan create1. Poverty2. Inflation3. Unemployment4. Negative growth

REVELATION• Quran•Hadiths

REASON/DEDUCTION(Istiqra’)

SENSES/INDUCTION (Istinbat)

ISLAMICECONOMICS

Human Behaviour Choice &

Action

Based onNon-Observable

Foundations(DIVINE)

Based onObservableFoundations(SCIENCE)

IslamicWorldview

Concept of

GodDinMan

SocietyUniverse

Prophethood

RukunIman

RukunIslam

Fard ‘Ayn(Obligatory knowledge)

Reason

Facts

Dunya (World)Scarcity

Alam Barzakh(Life in the Grave)

Mother’s Womb(Alam Rahim)

PrimordialStage (Alam Ruh)

Hereafter(Akhirah)

The Muslim Mindset

Stagesof Existencefrom Islamic perspective

ISLAMIC REITS: OBJECTIVES Shariah aspects – Equity Objective

- Observing the Purpose of Shariah (Maqasid Al-Shariah)- Application of Islamic Contracts- 20% cap on non-Shariah permissible trades

Operational (Tabi’) aspects – Efficiency Objective-Yield- Management Fees-Tax -Business strategies such as investment, operating, acquisition and capital management strategies - to improve yield-Marketing-Risk

Principles of Islamic Finance

1. Shari’ Principles – Equity objective e.g. Halal & HaramDOING THE RIGHT THING

2. Tabi’ Principles – Efficiency objective

DOING IT RIGHT

Islamic Financial System is based on Divine Values

These Divine values are put together under 5 basic principles

SHARIAH PRINCIPLES IN FINANCIAL TRANSACTIONS

Principle #1 : Prohibition of riba Principle #2: Application of al-bay’ (trade

and commerce) Principle #3: Avoidance of gharar

(ambiguities) in contractual agreements

Principle #4: Prohibition of maisir (gambling) Principle #5: Disengagement from production of

impure commodities.

SHARIAH – Divine Values

SHARIAH OF ISLAM

AQIDAH (FAITH)Rukn Iman

Belief in God, the Angels, the Prophets, the Holy Books,

and Predestination

AKHLAK (ETHICS AND MORALITYKnowledge of Conducts

Virtues and Vices

MAN AMONG MANCriminal Law, family LawLaws of Contract, etc.

MUAMALAT(INTERACTIONS)

GOD AND MAN Rukn Islam

SHARIAH

Purpose of Shariah: PROTECTION OF PUBLIC INTEREST

1. Preservation of benefits – The Permissible (Halal)

2. Prevention of harm – The Prohibited (Haram)

SHARIAH PRINCIPLE #1

Prohibition of interest as ribaNo contractual guarantee(s) on investments

“They say: Trade is like riba” (Qalu Innamal bay’u mith lurriba)

“ The Quran says: Allah has allowed al-bay’ but prohibits riba”(waahalallah ul bay’ wa haramu riba)

(Al-Baqarah :275-278)

SHARIAH PRINCIPLE #2

Application ofAl-Bay’Profit creation with equivalent counter-value (‘iwad)

eg. no risk no gain

risk = ‘iwadgain = profit

Principle Components of ‘iwad

1. Risk-taking(Al-Ghorm bil Ghonm)

2. Value-addition

3. Liability(Al-Kharaj Bil Daman)

SHARIAH PRINCIPLE #3

Elimination of uncertainties/ambiguities (gharar) in contractual agreements

SHARIAH PRINCIPLE #4

Prohibition of Gambling (Maisir)i.e earning via game of chance

Gambling

Lotteries Casinos Insurance Commodity Trading Futures Options

MAISIR: Game of Chance

Excessive risk Earnings arising from mere chance (aleotary) and not

by way of knowledge, skills and value-addition The probability of winning is very remote Zero-sum game

One party wins and the other losses Aleotary – outcome arising from pure chance alone Making bets with an expectation to win Bets and winnings are hugely disproportionate

SHARIAH PRINCIPLE #5

Avoiding impure commodities.

Islamic Finance Principles No profit can be created without risk-taking. Islamic financial transactions are based on valid

contracts The Purpose of the Shariah (Maqasid al-Shariah) is

strictly observed:

Purpose of Shariah: PROTECTION OF PUBLIC INTEREST1. Preservation of benefits – The Permissible

(Halal)2. Prevention of harm – The Prohibited (Haram)

Islamic Finance Corporate Finance

Sukuks, Islamic Private Debt Securities, Islamic REITS, Islamic Unit Trusts

Consumer FinanceMurabahah, Ijara

Enterprise Finance – Small & Medium Sized EnterprisesMudaraba, Musyarakah

Microfinance Public Finance

‘Allah has allowed trading and commerce (al-bay’) but prohibits riba” (Quran: Al-Baqarah 275)

Islamic Banking = Trading & Commerce

“Allah has allowed AL-BAY’ but prohibits RIBA”AL-BAY’(TRADE & COMMERCE)

Contract of ExchangeUqud al-buyu’

Forward Sale

Al-Bay

Al-Mudharabah(Trustee Partnership)

Contract of Profit-SharingUqud al-Istiraq

Contract SaleExchange Goods for Money

Salam

Al-Shirka(General Partnership)

Contract of SaleExchange Services for Money

Istisna’

IjarahWakalahKafalah

Al-MurabahahCredit sale

Spot Sale with mark-up(Al-Murabahah)

Bay’al-musawaammahBay Wadhiah, Mutlak

Deferred SaleBay’ Muajjal

Bai-Bithaman Ajil

Principle of Contract (‘Aqd) in Al-Bay

Pillars of Contract (AQD)

Agents of Contract - rational Objective of Contract – transfer of

ownership Price – stated on the spot Subject matter - halal Offer & Acceptance

Productive Elements in Al-Bay

Multi-dimentional view of Al-Bay

RISK(al-ghorm bil ghonm)

EFFORT

RESPONSIBILITYAl-kharaj bil daman

IWAD AQAD

Al-Bay and Its Derivatives

Al-Bay and Its Derivatives

Ijarah

Murabahah

Wakalah, kafala

Partnership

Industry Updates

Islamic REIT

Al-Hadharah Boustead REIT

AL-AQAR KPJ REIT - MALAYSIA

AXIS REIT - MALAYSIA

Islamic REITS: Basic Issues Objective Structure Regulatory Regime General Benefits Investors Comparison with Alternative Investment Fees and Charges Performance Indicators

Objective of an Islamic REITS To provide unit holders with a stable distributions per

unit with the potential for sustainable long-term growth of such distributions.

How?

By optimizing the performance and enhancing the overall quality of a large and geographically diversified portfolio of Shariah-Compliant real estate assets through various permissible investments and business strategies.

Fund Manager / Distributor

Name of Fund

Country Size(USDm)

Type Investor Advisor Description

Guidance Financial Group

Guidance Fixed Income Fund

USA 200 Residential Freddie Mac

real estate finance assets. The securities will

be issued and guaranteed by the Federal

Home Loan Mortgage Corporation (‘Freddie

Mac’). The fund will hold securities that are

backed by Shariah-compliant

Shamil Bank China Realty Fund

China 150 Commercial CITIC International Assets Management Co. Ltd. (CITICIAM)

Shamil Bank Bahrain entered into an MoU with prominent Chinese financial institutions, CITICIAM to set up and launch USD150m closed-end China Realty Fund.

ISLAMIC REAL ESTATE FUNDS

Fund Manager / Distributor

Name of Fund

Country Size(USDm)

Type Investor Advisor Description

Kuwait Finance House

Baitak Asia Real Estate Fund

South Asia 600 Commercial, Residential

Pacific Star Group A USD600m Islamic real estate fund. The Baitak Asia Real Estate Fund will invest in residential and commercial sites in Asian countries. This will be the first real estate deal in Asia for Kuwait Finance House.

Kuwait Finance House

Islamic European Real Estate Fund

Europe 486 Commercial, Residential

Equity Estates BV The fund intends to invest Euro 400m in European property concentrating on high yielding office, logistics and light industrial properties in the Benelux, France and Germany.

Dubai Islamic Bank (DIB); Cheung Kong Group

Al Islamic Far Eastern Real Estate Fund

Far East 450 Commercial, Retail, Residential

ARA Asset Management

The new fund will be managed by ARA Asset Management and jointly promoted by DIB and Cheung Kong Group. The Islamic-compliant investment vehicle has set aside USD450m to invest in commercial, retail and residential projects in major Asian cities.

ISLAMIC REAL ESTATE FUNDS

Sources: World Bank Organization, FTSE, EPRA

REITs Market around the World……Top 15 World Real Estate market

• United States has the largest real estate market in the world. The estimated size of the US market is approximately US$5 trillion.

• Japan ranks second with around US$2 trillion, followed by the four major European economies. The German market is approximately US$1.1 trillion, with the UK just behind at approximately US$1 trillion.

• France is close to US$800 billion. Italy is approximately US$660 billion. Canada comes in at just under the US$400 billion mark.

• The top 15 countries comprise around 88% of the total global real estate market. Interestingly, the top five countries hold 68% of the total. The next ten countries add 20% and the remaining 34 countries make up the final 12%. No OIC member countries. But Islamic REITS can be structured under Conventional legislation in non-Muslim countries.

Structure and Organization

Islamic REITS

TYPICAL REITS RELATIONS

Unitholders

Trustee

Invest in authorisedinvestment

ManagementCompany

REIT

Distribution and Possible capital gains

Islamic REITS Tripartite agreement between three

parties:

1. The Manager2. The Trustee3. Unitholders

Tripartite relationship is governed by a Deed registered with the Regulator (e.g Securities Commission –Malaysia)

DEED A Deed is a legal instrument used to grant a right. The trust deed is a legally binding agreement

between the manager, trustee and unit holders. The agreement usually spells out clearly how the unit trust scheme is to be administered. The contents usually include:-

Valuing and the pricing of units; Keeping of proper accounts and records; Collection and distribution of income; Rights of unit holders; Duties and responsibilities of the manager; Duties and responsibilities of the trustees; and Protection of unit holders’ interest.

Shariah Aspects

Islamic REITS

SHARIAH ASPECTS: LEGALITY The SC I-REITS Guidelines discussed four

matters for I-REITS, viz.: rental of real estate by I-REITS for

business purposes with a permissibility benchmark of 20%;

investment, deposit and financing for I-REITS;

takaful schemes to insure real estate; and forward sales or purchases of currency for

risk management.

ISLAMIC REITS: Legality

20% Permissibility Benchmark Benchmarking is based on rental space rather than

volumes of sales the non-permissible business can generate.

Nature of all non-permissible businesses is that it is highly profitable.1. casino & lottery outlets – game of chance always favour the operator2. liqour stores – addiction i.e captured market4. interest-bearing banks- small cap but

able to raise high volumes of deposits to make loans.

Islamic Benchmark : [Space/Sales] ratio and [Space/Sales].

sales $100m

sales$200m

Islamic Contracts in REITS: WAKALAH Model Unitholders and Management Company(MC)

Wakalah – Fee-basedUnitholders appoint MC to invest funds in properties.MC earns fees.

Unitholders and TrusteeWakalah – Fee-BasedUnitholders appoint Trustee to serve as a custodian for all the assets of the Islamic REIT.Trustee earns fees.

The Wakalah principles are incorporated in the Deed of Islamic Reits.

Nature of work undertaken by Management Company (Wakil) Managing the Properties effectively Maintaining net property income Maximizing the return and performance of each

Properties and their growth via enhancement of properties

Raising the profile of Properties Acquiring property assets with good yield and

growth potential for both locally and abroad that meet the Manager’s investment criteria

Employing optimum capital structure.

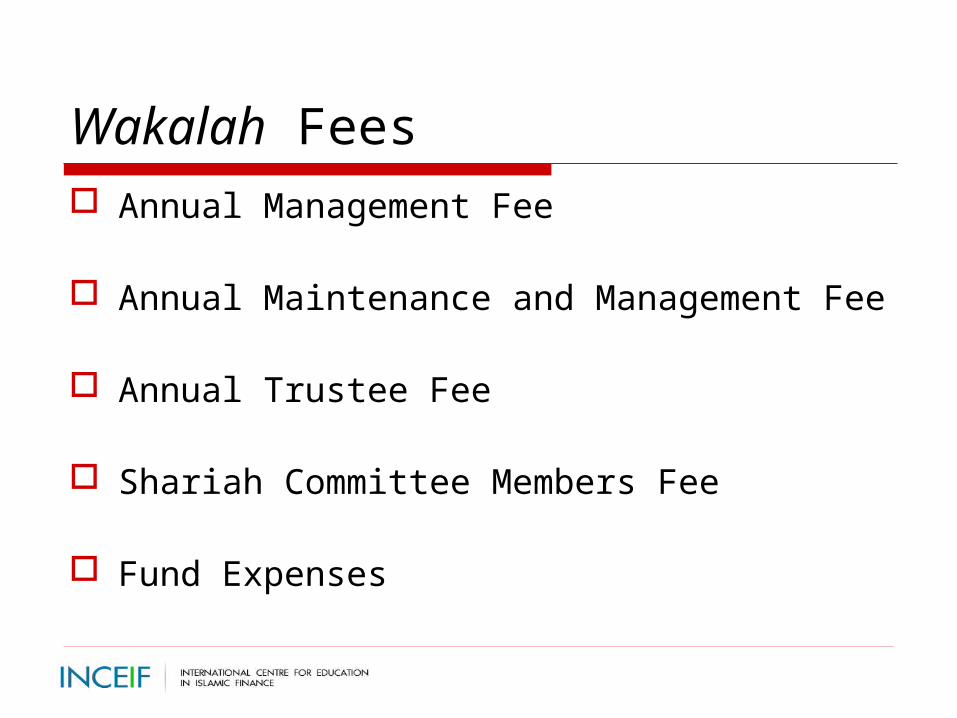

Wakalah Fees Annual Management Fee

Annual Maintenance and Management Fee

Annual Trustee Fee

Shariah Committee Members Fee

Fund Expenses

Management Expense Ratio (MER) Management Expense (ME) = Annual management

fee + Annual management and maintenance fee + Annual Trustee fee + Shariah fee + Fund expenses

MER = [(ME + Non-Recoverable Expenses) / (Average Value of a REIT calculated on a daily basis)] x 100

Shariah-compliant MER? up to?

To protect investors from high loading charges by Islamic Reits management companies.

Wakalah Model. Management Company (ie Wakil) does not bear

potential of loss (ie. risk) of investment. Management Company is entrusted to invest the REIT

Fund in return for a Fee (ujrah). Potential loss of investment is borned by Unitholders. Management Company receives fee payment (ie fees)

eventhough Unitholders are suffering capital losses. Nominal fees (ie absolute amount) may fall when net

asset value of REIT declined. Percentage fee remained unchanged.

Risk-Return Principle

Juristic Principle (Al-Qawaid Fiqiah) - “Al-Ghorm Bil Ghonm”No Pain No Gain

Financial period/years ending 31 December

Total rental amount per annum (RM’ mil)

Total rental amount per month (RM’ mil)

2006* 35.48 (US$10.13m) Approx. 2.96 (US$0.84m)

2007 35.70 Approx. 2.98

2008 36.43 Approx. 3.04

2009 36.96 Approx. 3.08

Al-’AQAR KPJ REIT RENTAL AMOUNTThe rental amount for the financial period ending 31 December 2006 and three (3) full financial years ending 31 December 2007, 31 December 2008 and 31 December 2009 are as follows:

Note * The rental rate is approximately 7.38% of the gross market value of the Properties.

RETURN

RISKS faced by Unitholders

Investment by Unitholders is based on Risk-Return Principle “ al-Ghornm bil Ghonm” where:

1. Original investment not guaranteed2. Income may rise or fall3. May not receive any income at all.

Types of Risk in Islamic REIT

Organizational and Operational Risk Risk relating to investment in real

estate Risk relating to Properties Shariah non-compliance risk Risk relating to an investments in the

units

Alternative to REIT Wakalah Model

Unitholders and Management Company (MC)Al-MudarabahProfit-Sharing

MC “fees” = portion of rental income. Unitholders and Trustee

WakalahTo ensure MC adheres strictly to the provisions of the Deed.

Typical REIT structure

Unitholders

Trustee (holds properties for the Benefit of

unitholders)

Property assets

REIT manager

REIT

Purchase assets Net property income

Investment in REIT Distributions

Acts on behalf of unitholders

Trustee’s fees

Managementfee

Management services

Al-’Aqar KPJ Islamic Reits Oversubscribed by 4.13 times Islamic Reits drew 5,115 non-Muslim

and non-Bumiputra investors. Open up at RM0.99, a premium of

4.2%, or 4 sen, over its retail offer price of RM0.95

30,810 units done at the opening bell Closed at 3.5 sen up at RM0.985 Al-’Aqar REIT raised RM177.25 million

Al-’Aqar KPJ REIT Structure - MALAYSIA

Unitholders*

Trustee (Amanah Raya

Berhad)

REIT properties, comprising 6 hospitals

Manager (Damansara REIT

Managers Sdn. Bhd.)

Al-’Aqar KPJ REIT

Ownership of properties Net property income

Holding of units

Distributions

Acts on behalf of unitholders

Trustee’s feesManagementservices

Management fees

Note * where KPJ will indirectly own 47.06% of the units

Hospital tenants

Maintenance manager for the properties

(Healthcare Technical Services Sdn. Bhd.)

Shariah Committee Members

Advise the Al-’Aqar KPJ REIT on Shariah-related matters

Rental payments

RentMaintenance and management

services

Maintenance and management

fees

Al-’Aqar KPJ REIT First Islamic Real Estate Investment Trust

(I-REIT) Comprises of six hospitals building worth

RM461.24m or USD$131.9m Manager: Damansara REIT Managers Pte. Lead adviser: AmMerchant Bank Pte. Trustee: Amanah Raya Pte. Units holdings:

KPJ : 160 million unitsInstitutional investors: 165 million unitsRetail investors: 15 million units

Al-’Aqar KPJ REIT: Fees and Expenses Annual management Fee Maintenance and management fees Annual trustee fee Shariah Committee Members fee Others

Auditors feesValuation feesRelevant professional feesProfit payments and expenses in respect of Islamic financing facilityPrinting, posting, general and operating expenses for the administration of the fund.

Al-Aqar KPJ Islamic REIT World’s first Islamic REIT IPO

The world’s first Islamic real estate investment trust (I-REIT) – Al Aqar KPJ REIT IPO – was launched with AmMerchant Bank appointed as the advisor, managing underwriter and sole placement agent.

Under the IPO, a total of 340 million units were issued and of these, KPJ Healthcare would hold 160 million units (47%), while 165 million units would be issued to institutional investors at US$0.27 (RM1) per unit and 15 million units to the public at US$0.26 (RM0.95) each. About US$49 million (RM180 million) was expected to be raised from the IPO.

Al-Hadharah Boustead REIT

Al-HADHARAH BOUSTED REITS

Unitholders*

Plantation Asets

Boustead REIT Manager

Al-Hadharah Boustead

Ownership of properties(Vested inTrustees)

Rental Income

Acts on behalf of unitholders

Trustee’s feesManagementservices

Management fees

Plantation AdviserIBFIMShariah Advisor

Boustead PropertiesAnd Other Vendors

Advise the Al-Hadharah REIT on Shariah-related matters Monitoring the

Plantation Assets

CIMB Trustee

Letting ofAsset for rentalTo be paid bytenantsSale of Assets

Distribution in the form ofDividends and other distributions

Investment in REITS

Bousted Al-Hadharah Islamic REITS

Vendor sells assets to SPV (Al-Hadarah REITS).

SPV leases back the assets to the Vendor.

Vendor pays fixed rentals for 30 years Rentals passed to Unitholders as

income. Unitholders – no fixed income and

capital protection.

CONTRACTS: SPA & Ijarah

Sale and Purchase Agreement: The sale and purchase agreements between the Vendors and the Trustee, on behalf of Al-Hadharah Bousted REIT, in relation to the sale and purchase of the Plantation Assets

CONTRACTS Ijarah Arrangements: The arrangements

by al-Hadharah Bousted REITS (AHBR)where the Trustee on behalf of AHBR as lanlord agrees to let the Plantation Assets to the Vendors as tenants for a period of three years which are renewable four times up to twelve years and thereafter renewable for up to an additional fifteen years comprising five additional terms of not more than threee years each, save and except for the tenancy of the Malay Reserved Land which are not automatically renewable.

Islamic REITS Structure

The FUND – Islamic REITS The Unit Holder Manager The Trustee Shariah Committee/Shariah Adviser The Property Assets Authorized Investments

Regulatory Framework

Islamic REITS

REITS DEFINED Securities Commission REITs

Guidelines: “ a trust investment vehicle that invests or

proposes to invest at least 50% of its total assets in real estate. An investment in real estate may be by way of direct ownership or a shareholding in a single-purpose company whose principle assets comprise real estate.”

REITS DEFINED

Invests at least 50% of its total assets in real estates

Trusts – passive income vehicle Distributes dividends to unit-holders Governed by a constitution Cannot reinvest income as retained

earnings Dividends are tax deductible

REITS DEFINED

Has a management company Has a trustee company Employs a property manager

REITs in Asia - Qualification and Legislations

Singapore Australia Japan Malaysia Hong Kong Thailand South Korea

Taiwan

Dividend yield

At least 90% of taxable earnings

100% of taxable earnings

At least 90%

No requirement

At least 90% after-tax-income

At least 90% of net profit

At least 90% of taxable earnings

Income must be distributed within 6 months ofFYE

Tax pass through

Yes Yes Yes Yes for local residents only

No Yes No yes

Property transfer taxes

Stamp duty waived for 5 years to 2010

None Reduced tax rates

Stamp duty waived

None Reduced property transfer rate

property transfer rate

None

Tax incentives for investors

Yes Nil Nil Nil 25% withholding tax on dividend

Nil Nil Nil Yes – 6% withholding tax on dividend

Gearing cap Max 35% of total assets unless REIT or all borrowings rated min A

No restriction, market average 38%

No restriction, market average 25-45%

35% of asset, unless approved by SC

Max 35% of gross asset value

Borrowing not permitted

Borrowing not permitted

No stated, but regulations prefers less than 35% of gross asset value

Investment restrictions

At least 70% in real estate

None At least 75% in real estate

At least 75% in real estate

<10% of asset in non-income producing properties

At least 75% in real estate

At least 70-90% in real estate

At least 75% in real estate

Development

Max 20% Yes Yes, if >50% of assets are income producing

No No Properties at least 80% constructed

K REIT- yesCR REIT-No

No

Geographical restrictions

No No No No Local only Local only No Local only, approval needed for foreign

Source: DIFC, Khalid Yousef,2006

REITs in the US…………..Qualification and legislations

• REITs were formed in 1960 – Congress passed legislation providing small investors access to income producing properties (The Real Estate Investment Trust Act of 1960).

• Benefit of REIT structure – entity does not pay corporate taxes as at least 90% of income distributed to shareholders annually.

• To qualify as REIT status, a company must meet and maintain certain provisions.

• Publicly traded REITs are SEC-registrants and subjected various regulatory requirements.

Provisions toQualify as REITs

No more than 50% of shares can be held by 5 or fewer

Have a minimum of 100 shareholders

Minimum 75% of income derived from properties/mortgages

Minimum 75% of total asset invested in ‘properties investment’*

Not more than 20% of assets can consist of shares in TRS**

* Investment includes mortgage loans and shares in other REITs

** TRS = Taxable REITs Subsidiary was formed by REITs to involve in taxable ancillary businesses such as advising clients

Conventional REITS Islamic REITS

1. Permissibility Not established Permissible (Halal)

2.Rental purpose No restrictions Business purposes only

3.Insurance No restrictions Takaful only

4. Activities on No restrictions Permissible activities only.

property Must not include:

- financial activities based on

riba (interest)

- gambling & gaming

- conventional insurance

- entertainment activities that

are not permissible according

to shariah laws

- manufacturing &/ sale of

tobacco-based products or

related products

- stock-broking or share trading

in shariah non-compliant

Securities

- hotels and resorts

- In incidences of mixture, for

example supermarkets, a

benchmark of 20% is allowed

for non-permissible goods of

trade

5. Financing No restrictions Funds must be shariah-

compliant

OPERATIONAL ASPECTS

Islamic REITS

Performance Indicators

Management Expense Ratio (MER) Total Returns Average Annual Returns Distribution Yield Net Asset Value (NAV)

Authorized Investments At least 75% of al-aqar KPJ REIT total assets

shall be investment in Shariah-compliant real estate, single purpose companies which are Shariah compliant, real-estate related assets or liquid assets which are Shariah compliant;

The remaining 25% of al-aqar KPJ may be invested in other Shariah-compliant assets (ie Shariah compliant real estate related assets, Shariah compliant non-real estate related assets such as Islamic asset-backed securities)

Performance Indicators

Management Expense Ratio (MER) Total Returns Average Annual Returns Distribution Yield Net Asset Value

Valuation of REITs…………how are REIT Unit pricedREITS in Japan, US and Singapore are trading at a premium of 70 - 230 bps

compared to the government bonds

3.9

7.1

5.4

3.2

4.2

3.6

1.3

7.3

4.6

4.9

0 1 2 3 4 5 6 7 8

Average Malaysian REIT Yield

Malaysian 10 yr Gov bond

Australian LPT

Australian 10 yr Gov bond

Singapore REITs

Singapore 10 yr Gov bond

US REIT

US 10 yr Gov bond

Japan REITs

Japan 10 yr Gov bond

Yield (%)

Premiumof 230 bps

Premium of 140

bps

Premium of 170

bps

Premiumof 70 bps

Premium of 340

bps

Source: Bloomberg, CIMB

Notes:1. Average 12 month gross dividend yield of Berjaya Sports, Hap Seng Consolidated, Hong Leong bank, Shell Refining, Nestle,

Tanjong PLC, United Plantation and YTL Power2. Kuala Lumpur Stock Exchange Composite Index dividend yield3. Kuala Lumpur Property Index dividend yield

1.53

4.11

5.20

3.27

4.54

200bps

36bps

of 133bps

of 200bps

of 320bps

Investing in REITs…why are REITs attractive to investors?

Income stability

Quality realestate

Capital stability & growth

Liquidity & valuation

• REITs is typically distribute >90% of net cash flow• Income is underpinned by legally enforceable lease

agreements• Low leverage• Little or no development risk

• REIT unit price is much lower than those of general equities• Long-term unit price capital growth potential is driven by

increase in rental earnings and also by capital appreciation of the underlying properties

• Provide institutional investors with an alternative to direct real estate investment with increased flexibility

• Provide retail investors with an opportunity to invest in high-value institutional quality real estates assets that would otherwise not be possible

• Packaging illiquid real estate into liquid listed securities that offer diversification, transparency, expert management and regular research coverage

• Institutions receive daily ‘mark to market’ value of their investment

• Low transaction costs in buying/selling REIT units vs trading underlying assets

• Individuals can ‘redeem’ small investment quickly by selling the units in the open market and with little cot

• REITs allow institutional funds to make incremental investments in lumpy real estate as and when new investment funds are received

Investing in REITs…. (cont’d)

ExpertManagement

Diversification

Defensive

• Diversification by types of properties, tenants and locations

• Benefit from experienced, professional real estate managers

• Additional scrutiny by the trustee

• Consistent yield-based investment has defensive asset class characteristics

• Income-generating investment grade property is a ‘safe haven’ during uncertain times

Transparency

• Subject to stringent corporate governance and disclosure requirements

• Government regulates on payout ratios, gearing, allowable investment, etc.

Source: JPMorgan, 2005

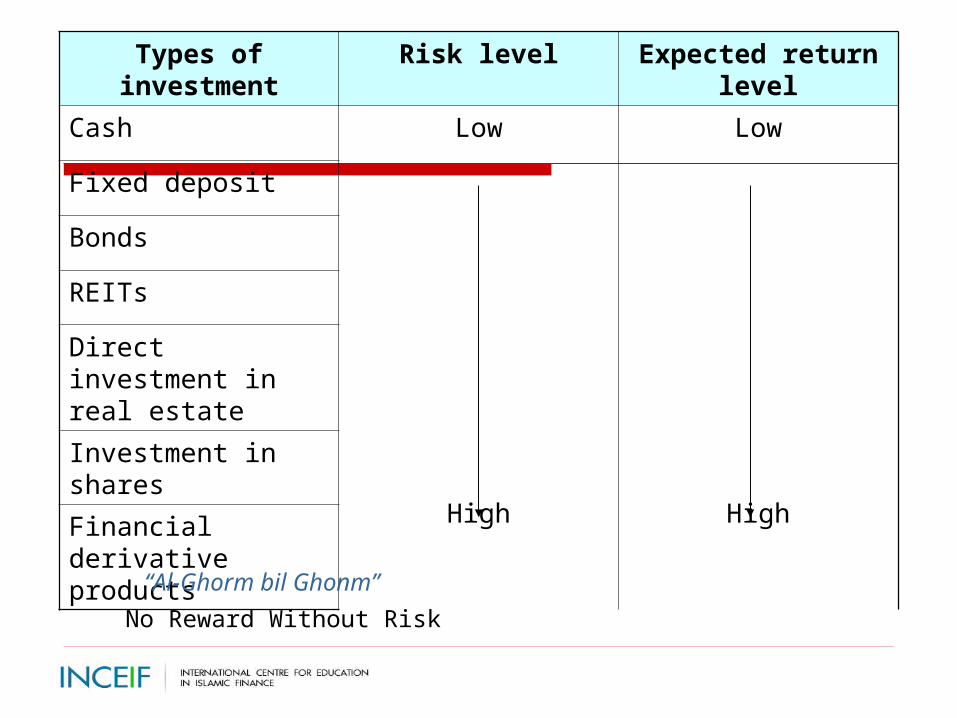

Types of investment Risk level Expected return level

Cash Low

High

Low

High

Fixed deposit

Bonds

REITs

Direct investment in real estate

Investment in shares

Financial derivative products

“Al-Ghorm bil Ghonm”

No Reward Without Risk

REIT developments in other Asian markets

IndiaIndia

REITs are yet to be established in India, however the Securities and Exchange Board of India (SEBI) has been finalizing a framework for Real Estate Mutual Funds (REMFs)

The Association of Mutual Funds of India (AMFI) issued a report to SEBI regarding the launch of real estate investment schemes in 2002

Regulators have been cautious on approving REMFs due to fears or them causing excess speculation in the real estate market

ThailandThailand

Formal REIT guidelines are still yet to be legislated. However, framework exists and guidelines are in place for Property funds by the Office of the Securities and Exchange Commission (SEC)

Under the current regime, only a licensed mutual fund management company is eligible for the establishment and management of all types of mutual funds including property funds

Lack of available assets remains a limitation. Underlying residential market has been strong and has been pushing property development stocks higher

PhilippinesPhilippines

No specific REIT regulation exists. However, the Special Purpose Vehicles (SPV) Act of 2002 has provided for the creation of Asset Management Companies (AMCs). SPCVs could include the function of REITs

IndonesiaIndonesia

While REITs have not been established in Indonesia, the Indonesian Bank Restructuring Agency (IRBA) has been considering setting REITs up

Property companies currently provide investors with exposure to listed real estate

ChinaChina

PRC Trust Laws, introduced in October 2001, provide guidance on recognition of trusts in China

However detailed implementation rules are yet to be released. Land laws and ownership structures in place are capable of providing a sufficient legal framework for REITs, however, the current unit trust structure prohibits investment in real estate

Some private syndicated deals have occurred in China and there is an expectation of the market developing further

As Chinese property companies are launched, modern REIT structures are likely develop in tandem on an accelerated basis

41

Wassalam

Thank You