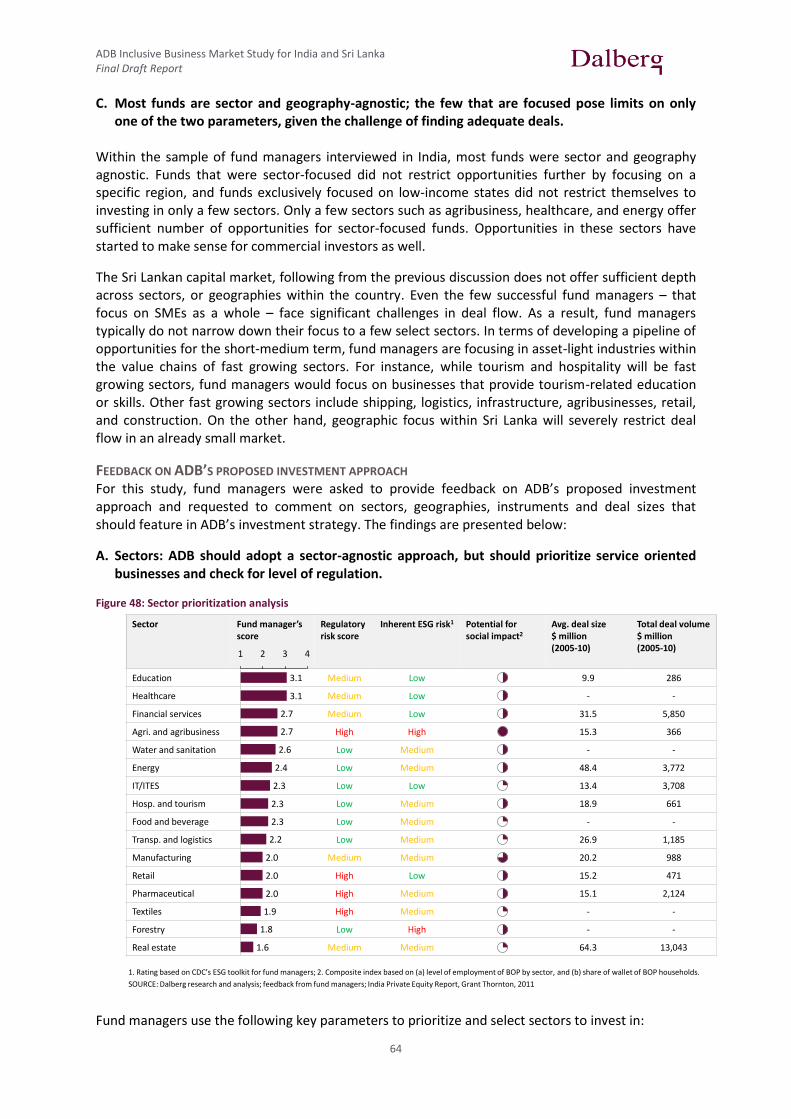

I NCLUSIVE BUSINESS MA RKET STUDY FOR INDIA AND SRI...

81

INCLUSIVE BUSINESS MARKET STUDY FOR INDIA AND SRI LANKA DRAFT FINAL REPORT OCTOBER 30, 2012

Transcript of I NCLUSIVE BUSINESS MA RKET STUDY FOR INDIA AND SRI...

INCLUSIVE BUSINESS MARKET STUDY

FOR INDIA AND SRI LANKA

DRAFT FINAL REPORT

OCTOBER 30, 2012

ADB Inclusive Business Market Study for India and Sri Lanka Final Draft Report

1

List of abbreviations used

ADB Asian Development Bank

BOP Base of the pyramid

BMGF Bill & Melinda Gates Foundation

DFI Development finance institution

DFID Department for International Development

ESG Environmental, Social and Governance (criteria for investment)

FDI Foreign direct investment

FMO Netherlands Development Finance Company

GDP Gross domestic product

GDP (PPP) Gross domestic product at purchasing power parity

HDI Human development index

IB Inclusive business

IFC International Finance Corporation

IPO Initial public offering

IRR Internal rate of return

JICA Japan International Cooperation Agency

KfW Kreditanstalt für Wiederaufbau, a German government-owned development bank

LIS Low-income states

LP Limited partner

MPI Multidimensional poverty index

NORFUND Norwegian Government’s Investment Fund for Developing Countries

NSDC National Skill Development Corporation

PE Private equity

R & D Research and development

SIDA Swedish International Development Cooperation Agency

SIDBI Small Industries Development Bank of India

SME Small and medium enterprises

Swedfund Swedish Government’s Investment Fund for Developing Countries

TA Technical assistance

VC Venture capital

ADB Inclusive Business Market Study for India and Sri Lanka Final Draft Report

2

TABLE OF CONTENTS

Table of Contents .......................................................................................................................... 2

1. Identifying and Supporting Inclusive Businesses ..................................................................... 4

1.1. ADB’s definition of inclusive business ................................................................................. 4

1.2. Potential strategies for scaling-up inclusive businesses...................................................... 5

1.3. About ADB’s Inclusive Business Initiative ............................................................................ 6

2. Findings and Recommendations ............................................................................................. 7

2.1. Background and methodology ............................................................................................ 7

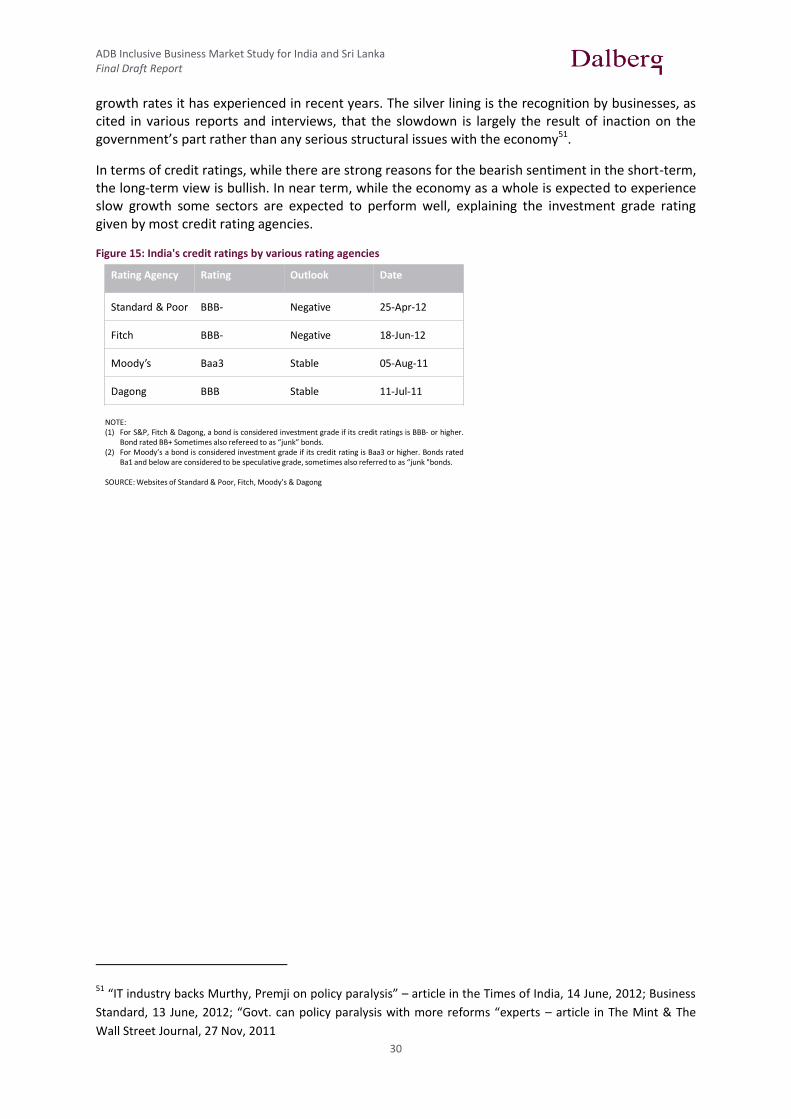

2.2. Findings................................................................................................................................ 8

2.3. Recommendations............................................................................................................. 14

3. Macroeconomic assessment of India .................................................................................... 15

3.1. Overview of performance on economic and social indicators .......................................... 15

3.2. Key Inclusive Business Sectors and Government Initiatives ............................................. 19

3.3. Key trends shaping the economy ...................................................................................... 24

3.4. Size of the market at the base of the pyramid .................................................................. 28

3.5. Climate for enterprise and investment ............................................................................. 29

4. Macroeconomic assessment of Sri Lanka .............................................................................. 31

4.1. Overview of performance on economic and social indicators .......................................... 31

4.2. Key trends shaping the economy ...................................................................................... 35

4.3. Size of the market at the base of the pyramid .................................................................. 37

4.4. Climate for enterprise and investment ............................................................................. 38

5. Inclusive business mapping .................................................................................................. 39

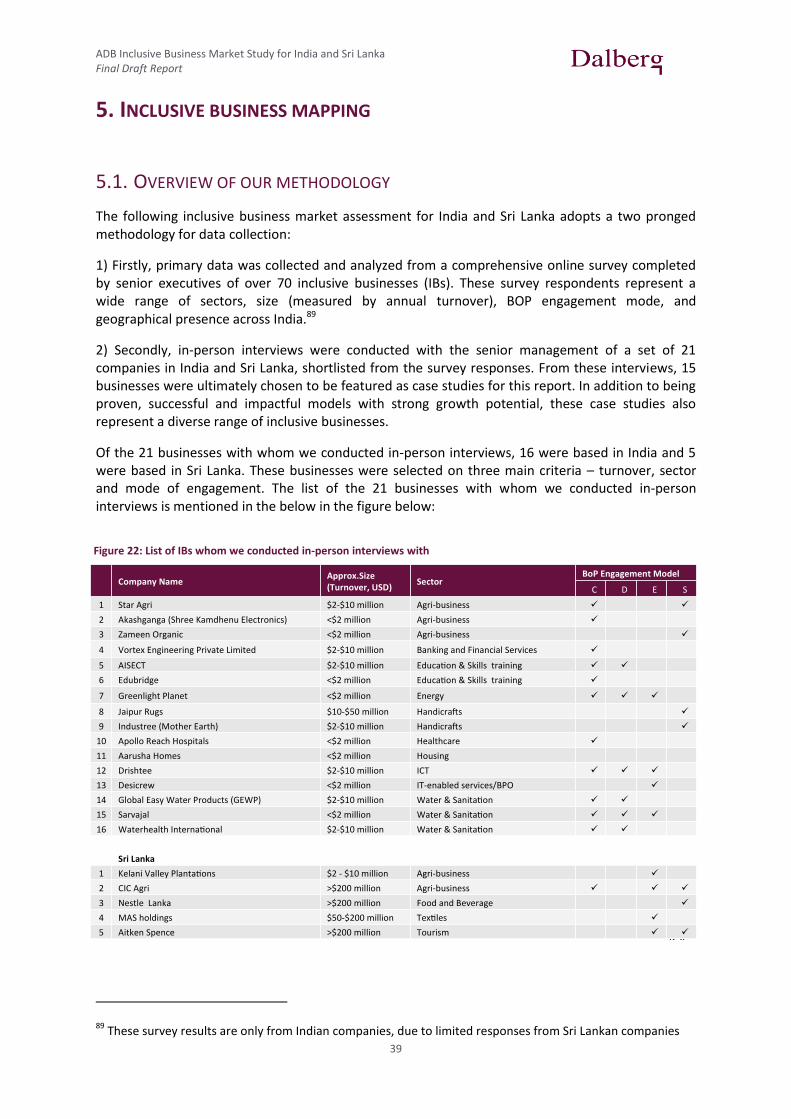

5.1. Overview of our methodology .......................................................................................... 39

5.2. Analysis of findings ............................................................................................................ 41

5.3. Funding needs of Inclusive Businesses .............................................................................. 53

5.4. Implications for ADB .......................................................................................................... 57

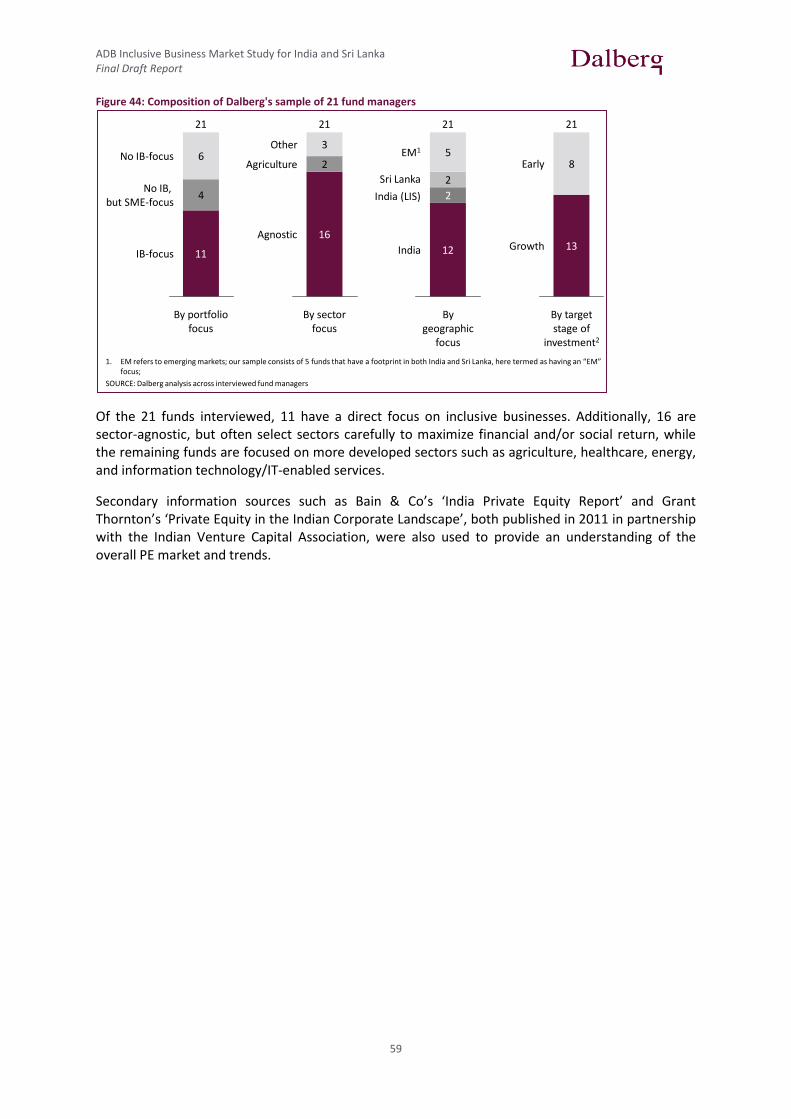

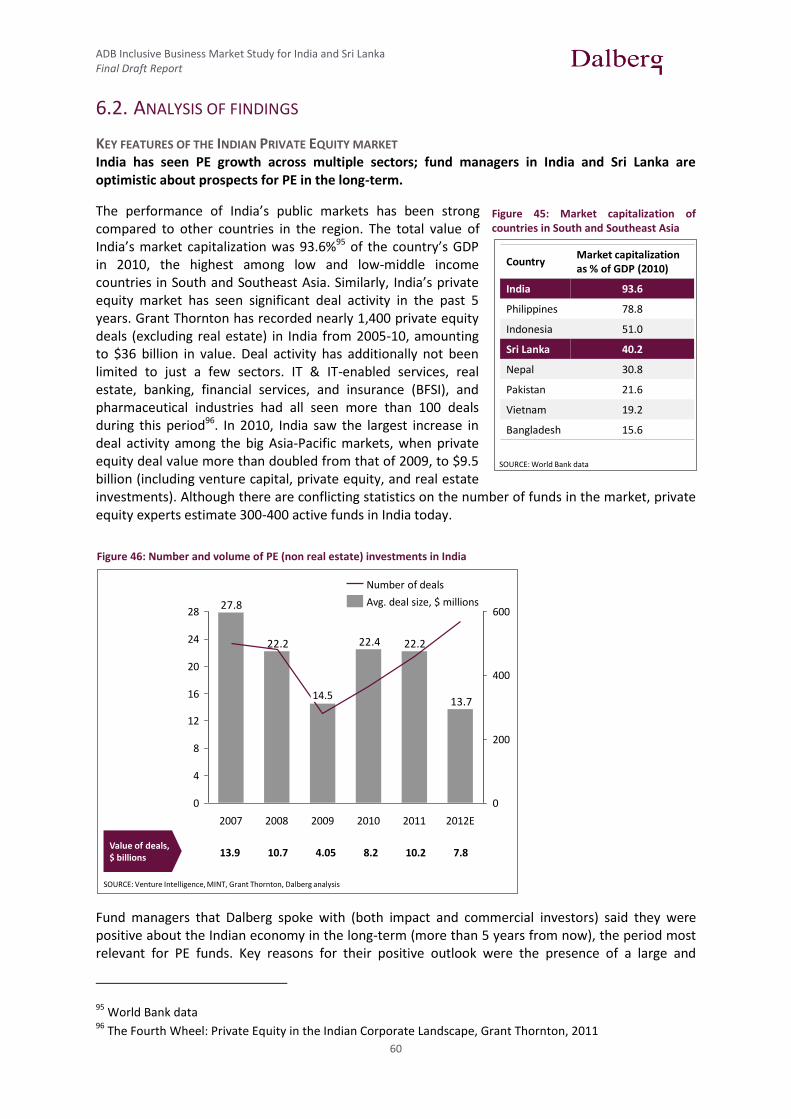

6. PE markets assessment ........................................................................................................ 58

6.1. Overview of our methodology .......................................................................................... 58

6.2. Analysis of findings ............................................................................................................ 60

7. Donor mapping.................................................................................................................... 69

7.1. Overview of our methodology .......................................................................................... 69

7.2. Analysis of findings ............................................................................................................ 70

8. Highlights from the Inclusive Business Forum and Roundtable Discussions ............................ 74

8.1. Objectives .......................................................................................................................... 74

8.2. Participation ...................................................................................................................... 74

8.3. Highlights ........................................................................................................................... 74

9. Bibliography ........................................................................................................................ 79

ADB Inclusive Business Market Study for India and Sri Lanka Final Draft Report

3

List of Figures

Figure 1: Classification of business models ............................................................................................. 4 Figure 2: Potential strategies for scaling up inclusive business activities ............................................... 5 Figure 3: Framework to organize insights collected in the study ........................................................... 7 Figure 4: Total and equity-only FDI inflows into India .......................................................................... 15 Figure 5: Gross domestic product (GDP) at PPP ................................................................................... 15 Figure 6: Historic and planned sector growth rates ............................................................................. 16 Figure 7: Contribution of sectors to GDP and labour force employment ............................................. 17 Figure 8: Percentage of India's population in 9 poorest states ............................................................ 18 Figure 9: Half of the households in India do not have access to basic sanitation facilities ................. 21 Figure 10: Projections for India's working age population ................................................................... 25 Figure 11: Distribution of urban and rural population ......................................................................... 25 Figure 12: Increase in the number of urban towns .............................................................................. 26 Figure 11: Annual household consumer expenditure in India (1987-2010) ......................................... 27 Figure 14: Market size of India's BOP ................................................................................................... 28 Figure 15: India's credit ratings by various rating agencies .................................................................. 30 Figure 16: Gross domestic product of South and Southeast Asian countries ...................................... 31 Figure 17: Weighted contribution to GDP growth rate by sectors ....................................................... 32 Figure 18: Composition of FDI inflows .................................................................................................. 33 Figure 19: Age profile of Sri Lanka’s population ................................................................................... 35 Figure 20: Unemployment in Sri Lanka by education level and age group .......................................... 36 Figure 21: Segmentation of market at the base of the pyramid .......................................................... 37 Figure 22: List of IBs whom we conducted in-person interviews with ................................................. 39 Figure 23: Distribution of survey respondents ..................................................................................... 40 Figure 24: Primary BOP engagement mode of survey respondents ..................................................... 41 Figure 25: Additional BOP modes of engagement ................................................................................ 42 Figure 26: Consumer model strategies ................................................................................................. 42 Figure 27: Distributor model strategies ................................................................................................ 43 Figure 28: Supplier model strategies .................................................................................................... 44 Figure 29: Employee model strategies.................................................................................................. 44 Figure 30: Benefits to company of being inclusive ............................................................................... 45 Figure 31: Benefits to the BOP of inclusive businesses ........................................................................ 46 Figure 32: Level of social impact measurement ................................................................................... 47 Figure 33: Geographical spread of IB operations ................................................................................. 48 Figure 34: Perceptions of operating in low-income states ................................................................... 49 Figure 35: Critical growth factors .......................................................................................................... 49 Figure 36: Key risk factors ..................................................................................................................... 50 Figure 37: Equity received to date ........................................................................................................ 53 Figure 38: Debt received to date .......................................................................................................... 53 Figure 39: Credit guarantees received to date ..................................................................................... 54 Figure 40: Required investment size, by sector .................................................................................... 54 Figure 41: Investment size by geography and mode of engagement ................................................... 55 Figure 42: Ideal grant-funded investments .......................................................................................... 55 Figure 43: List of fund managers interviewed ...................................................................................... 58 Figure 44: Composition of Dalberg's sample of 21 fund managers ...................................................... 59 Figure 45: Market capitalization of countries in South and Southeast Asia ......................................... 60 Figure 46: Number and volume of PE (non real estate) investments in India ...................................... 60 Figure 47: Responses to the question: "What is your general outlook for India's economy?" ............ 61 Figure 48: Sector prioritization analysis ................................................................................................ 64 Figure 49: Illustrative approaches of major investors deploying equity/debt to IBs in India............... 70 Figure 50: Exposure of major investors deploying equity/debt to priority sectors in South Asia ........ 71 Figure 51: Participation at the three inclusive business events in India & Sri Lanka ............................ 74

ADB Inclusive Business Market Study for India and Sri Lanka Final Draft Report

4

1. IDENTIFYING AND SUPPORTING INCLUSIVE BUSINESSES

1.1. ADB’S DEFINITION OF INCLUSIVE BUSINESS

The ADB defines Inclusive Businesses (IBs) as those profit making companies that bring systemic impact in scale to the poor and vulnerable people under the $3 international poverty line (i.e. about 60% percent of developing Asia’s population). These Inclusive Businesses are focused on making a reasonable profit (an IRR of 10-20%) while contributing to systemic impact on the lives of the poor. This can occur in a number of ways – specifically including the poor as suppliers, consumers, employees, and distributors.

As described in Figure 1 below, Inclusive Businesses differ from social enterprises and corporate social responsibility activities in their realized profit making motive/ability to offer market returns, as well as the scale of positive externalities generated. This results in their needing larger investments than social enterprises. Many IBs, particularly those that have attained scale in operations, deliver market returns or above market returns on par with commercial businesses enabling them to access a large spectrum of commercially-oriented funding sources including stock markets.

However, the number of standalone IBs in Asia that have attained that level of scale is very low. There are very few examples of companies like Jain Irrigation Systems Limited, the world’s second largest irrigation company in the world with a customer base of 1.2 million farmers across developing countries, which are listed on the Bombay Stock Exchange. There are many more enterprises that are still in the ‘social enterprise’ category, the bulk of which are relatively small in size. In India, the ADB found 150 social enterprises of which 90% had annual revenues of USD 500,000 or less1. Again, while there are a number of examples of established commercial business houses like Unilever and Nestle expanding their businesses in ways that are inclusive2 in Asia, there is limited understanding of the kind of external support that might help scale these initiatives or inspire other established commercial businesses, especially those that aren’t multinationals.

Therefore, in addition to finding ways to help existing IBs expand, ADB’s Inclusive Business initiative must to understand how to support the growth of social enterprises into inclusive businesses and how to promote greater inclusivity among commercial or traditional businesses.

Figure 1: Classification of business models

1 India Social Enterprise Landscape Report, ADB, 2012 2 Unilever has pioneered a direct-to-home distribution model in India for which they engage over 45,000 women from base-of-pyramid populations as distributors for the products, significantly enhancing their monthly income. Nestle’s milk district model wherein dairy farmers are now provided with continuous training, technology and skill development touches farmers in 30 countries globally.

Market returns

Business

Below market

Social enterprise

Above market returns

Low HighPositive externalities 1

Inclusive Business

1 Improvement in human development indicators Source: Dalberg analysis

ADB Inclusive Business Market Study for India and Sri Lanka Final Draft Report

5

1.2. POTENTIAL STRATEGIES FOR SCALING-UP INCLUSIVE BUSINESSES

Inclusive business activities can be promoted by supporting and scaling-up inclusive businesses, social enterprises and inclusive operations of corporate firms. The ADB, in its role as the anchor DFI for Asia, is most suited to addressing gaps in terms of finances required to scale IB activities. Dalberg’s team has identified a broad set of potential strategies for ADB to follow in supporting growth of IB activities. These potential strategies vary by type of organization - Inclusive Businesses, Social Enterprises and traditional businesses.

Figure 2: Potential strategies for scaling up inclusive business activities

a) Potential strategies to support existing Inclusive Businesses

Address equity requirements as many businesses may still be years away from an IPO and/or may be operating in markets with limited private equity activity

Provide concessional debt to finance working capital requirements that tend to be sizeable in businesses that have attained a certain scale

Offer technical assistance to help companies strengthen areas that are typically under-invested in, but those that generate long-term benefits such as R&D or training

b) Potential strategies to support social enterprises scale-up to become inclusive businesses

Address ‘early growth’ equity requirements beyond the scope of seed and social venture capital, i.e. look to supplement the efforts of existing impact investors

Address debt requirements of equity investees of existing impact investors so that equity goes further, especially where access to formal debt sources is restricted

Offer technical assistance /grant support to help companies invest in areas that are typically under-invested due to long-term, ‘public good’ nature of returns

c) Potential strategies to make commercial businesses more inclusive

Offer concessional debt to account for higher risk and value of social benefit created by firms wishing to expand inclusive operations

Offer a credit guarantee facility to select sectors or sub-sectors that deliver high impact

The bank must adopt a tailored approach that’s appropriate to the needs of the local businesses in each of the geographies in which is seeks to support IBs. The main focus of this report is the

BusinessInclusive Business

Below market

Social enterprise

Above market returns

Low HighPositive externalities 1

1 Improvement in human development indicatorsSource; Dalberg analysis

ADB Inclusive Business Market Study for India and Sri Lanka Final Draft Report

6

approach the ADB should adopt to grow IB activity in India and Sri Lanka with a particular focus on whether and how a dedicated IB PE fund could be relevant and effective.

1.3. ABOUT ADB’S INCLUSIVE BUSINESS INITIATIVE

First approved in 2008 and refined in 2010, ADB engaged in an initiative to stimulate IB in Asia and the Pacific. An initial technical assistance (TA) project aimed to develop inclusive business ventures in 6 (later broadened to 10) target Asian countries (Bangladesh, India, Indonesia, Pakistan, the Philippines and Viet Nam; later to include Cambodia, Lao PDR, Sri Lanka, and Thailand) and prepare them for project financing through the development of national/sub-regional private equity funds. The project is co-implemented, and leveraged where appropriate, with the Netherlands' Development Organization SNV and the networks and assets of the World Business Council for Sustainable Development (WBCSD). The Ford Foundation is supporting the work in Indonesia.

The initiative aims to:

• perform market studies in 10 Asian countries with the results to be discussed in country investment roundtables and regional inclusive businesses fora;

• develop an impact assessment tool for possible ADB investments;

• build up the first inclusive businesses investment fund for the Mekong region;

• work on the creation of a technical assistance facility (2013-2016) together with other donors who support inclusive business activities in Asia.

• promote further knowledge exchange with development partners, including IDB, World Business Council for Sustainable development, SIDA, DFID, Ford Foundation, KfW, and development institutions in Japan, among others.

ADB Inclusive Business Market Study for India and Sri Lanka Final Draft Report

7

2. FINDINGS AND RECOMMENDATIONS

2.1. BACKGROUND AND METHODOLOGY

In May 2012, the ADB commissioned Dalberg Global Development Advisors to undertake a study on the Inclusive Business3 Market in India and Sri Lanka as part of a larger project titled “Promoting Inclusive Growth through Business Development at the Base of the Pyramid”.

The objective of the market study was to assess the feasibility of setting up an inclusive business (IB) private equity fund in India and Sri Lanka. Dalberg’s analysis focused on answering the following key questions:

(1) Relevance. Is PE funding relevant for the growth of IBs in India and Sri Lanka? (2) Strategy. What should ADB’s investment strategy be? (3) Operationalisation. How should ADB’s fund be operationalised?

These key areas of analysis - relevance, strategy and operationalisation – were then broken down into sub-questions as described in the table below:

Figure 3: Framework to organize insights collected in the study

Dalberg’s approach had four distinct parts:

A. Assessment of macroeconomic and microeconomic conditions in India and Sri Lanka B. Mapping of inclusive businesses operating in India and Sri Lanka through an online survey of

130 businesses, and interviews with 20 potential investees for ADB C. Assessment of strength of capital markets in both countries through interviews with 21 fund

managers with exposure to inclusive businesses D. Mapping of potential co-investors (donors) in ADB’s fund through interviews with 11

agencies including family foundations, banks, DFI-funded investors and bilateral aid agencies

3 As defined by ADB, the Base of the Pyramid (BOP) is defined as individuals earning $3-$4 per day, per capita,

or less. Inclusive businesses are enterprises that engage the BOP in their core business operations as either:

consumers, distributors, suppliers or employees

7

Our analysis is presented along 3 topics:(1) Relevance of ADB’s potential IB fund, (2) investment strategy and (3) fund operationalisation

Key questions addressed in our study

Relevance

a. Are macroeconomic conditions conducive for IB growth?

b. Are macroeconomic and business conditions favorable for VC/PE investment?

c. Is there demand from inclusive businesses to seek out VC/PE investment?

Strategy

a. What size of enterprise and investment should the fund target?

b. Which sectors should the fund prioritize?

c. Should geography be a factor, and if so, where should the fund focus?

d. Which financial instruments should the fund deploy?

e. Should mode of engagement be an investment criterion?

f. Which company-specific parameters should influence investment decisions?

Operationalisation

a. How should ADB engage existing PE funds investing in IBs?

b. Who should ADB target to raise funds from?

c. What are some other key considerations to set the IB fund up for success?

METHODOLOGY

ADB Inclusive Business Market Study for India and Sri Lanka Final Draft Report

8

The detailed methodology adopted within each of these work streams is described in the relevant sections of the report.

2.2. FINDINGS

This section presents our findings in detail, organized by the three broad questions outlined at the start of this chapter: Relevance, Strategy, and Operationalisation.

RELEVANCE Private equity funding is relevant for the growth of small and medium IBs in both India and Sri Lanka, however diverse conditions warrant a differentiated approach to investment in both countries. In India the need for equity is being met to some extent by the existing investment community including impact investors, whereas in Sri Lanka the nascent venture capital and private equity market implies a scarcity of equity and the need for intervention. Debt requirement for growth stage businesses in both countries is very large and not being addressed due to the stringent collateral requirements of banks in India and the challenges of accessing debt at reasonable terms in Sri Lanka.

In order to assess relevance of an ADB intervention to support Inclusive Businesses in India and Sri Lanka, Dalberg’s team looked at both demand and supply factors. On the demand-side, we examined whether macroeconomic conditions support the growth of IBs and whether IBs look to PE firms to support their growth. On the supply-side, we looked at whether macroeconomic conditions and capital markets support PE investment.

In India, the growth of private business is supported by the country’s positive long-term economic prospects driven by favourable demographics and consumption growth. The segment of the private sector expected to grow the fastest is the collection of approximately 12 million ‘small and medium enterprises’ (SMEs) that employ over 30 million people. Within this large set, there are thousands of inclusive businesses that engage members of India’s vast BOP population (>1 billion) and need growth financing in the range of $1-10 million. Impact investors are particularly optimistic about the growth of enterprises that provide access to basic services like energy, water, education and health as India’s massive BOP population suffers deprivation across multiple development parameters4. On whether IBs are turning to PE funds for support, we found that among the SMEs that qualify as inclusive businesses, at least 75-100 business are receiving equity support from designated impact investors5 in India. This figure does not include those whose equity needs are being met by pure commercial funds.

Most of the IBs we spoke with, expressed a greater need for support in securing debt to meet their working capital requirements. The larger need for debt is supported by a recent IFC-sponsored publication that found that the addressable gap in debt financing for the Micro, Small and Medium Enterprise sector in India stood at $58 billion while the gap for equity stood at $38 billion6. The same study found that it is the collateral requirements of commercial banks, which account for 80% of existing lending to the MSME sector, that are the key barrier to debt. Almost all banks insist on

4 India’s 2011 HDI rank was 134th of187 countries and MPI for the same year stood at 0.283 putting it at 76

th of

209 countries in 2011 5 There are over 15 impact investors in India with more than $750 million in committed capital

6 Micro, Small and Medium Enterprise Finance Market in India, International Finance Corporation, 2012

ADB Inclusive Business Market Study for India and Sri Lanka Final Draft Report

9

immovable collateral to hedge against risk of default. The study found that the typical collateral to credit ratio is estimated between 125% and 170%. Even though a credit guarantee facility has been instituted to support collateral-free debt up to INR 10 million ($ 0.2 million) by institutions like the Small Industries Development Bank of India (SIDBI), this facility remains underutilized at less than 5% of the overall debt to the sector. While collateral-free debt is growing gradually, collateralized debt continues to account for 95%-98% of MSME credit.

On the equity front, while there are at least 15-20 dedicated impact investors investing in IBs in India, with more than $750 million in committed capital, there is definitely scope to deploy more funds. For the VC/PE community (supply-side), India‘s most attractive features are the size of its stock market, IPO issuing activity and expected economic growth. PE market statistics show that the number of deals is increasing, indicative of more opportunities for PE investment. While an unclear regulatory environment and inadequate infrastructure do pose challenges to doing business in the country, we feel that these will dissipate over a 10-year period. Thus, the conditions are suitable for making equity investments in IBs in India.

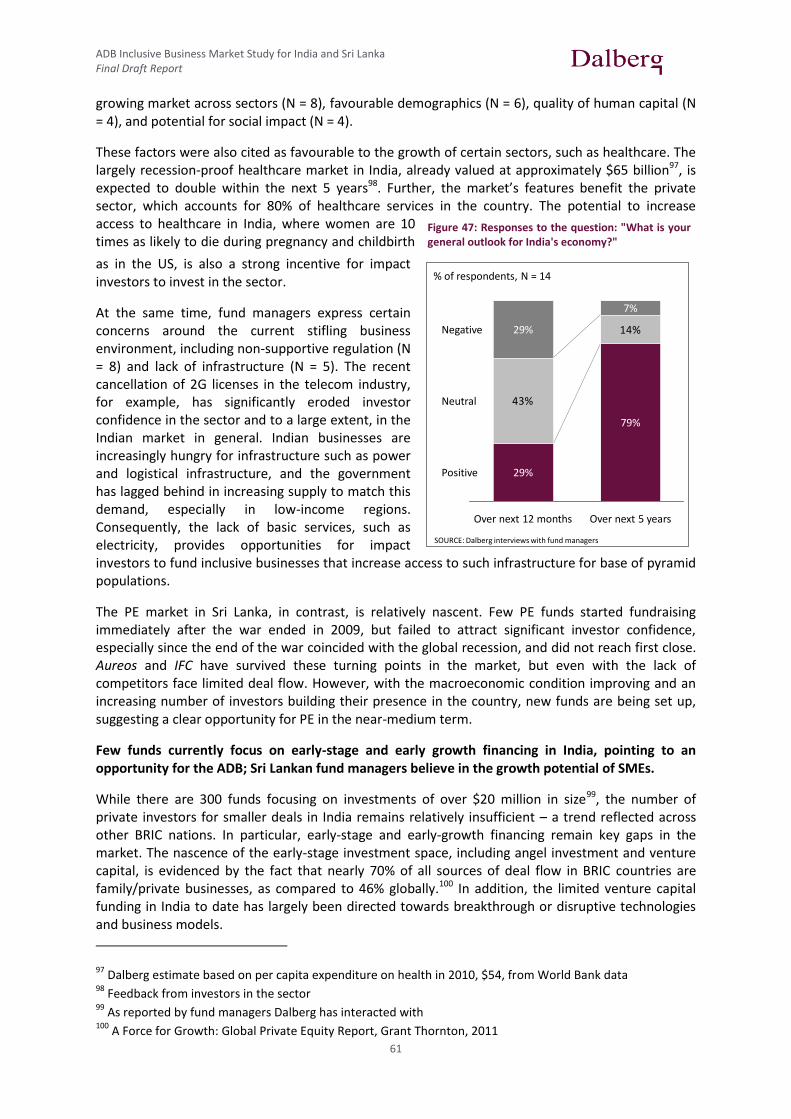

In Sri Lanka, conditions warrant a different, more measured approach. Sri Lanka’s economy has grown at more than 8% since 2009, when its 26-year long civil war ended. The government has initiated a number of measures to stimulate the growth of businesses in sectors like tourism where the target is to attract 1.5 million tourists by 2016 from 850,000 in 2011. The results of these efforts are beginning to show – from 2011 to 2012 the country jumped nine places in the Doing Business Rankings and is ranked 89th of 183 countries, which is second best (behind Maldives) in the South Asia region.

Fund managers (there are two active PE funds at present bringing in foreign investments) expect investment opportunities to emerge in the SME sector, especially in services and manufacturing companies catering to the needs of larger firms in inherently inclusive sectors like tourism, agri-business and renewable energy. These businesses are expected to engage hundreds of BOP members as employees and suppliers addressing Sri Lanka’s problems of a high youth unemployment rate (20%). Consumer-oriented IBs are less relevant in Sri Lanka due to the relatively small BOP population (<2% of India’s at 12 million people) and the high level of access to basic services contributing to Sri Lanka’s low multi-dimensional poverty score of 0.021 compared to India 0.283.

It must also be kept in mind that PE is a relatively new asset class in Sri Lanka. The total number of investible opportunities ready to absorb PE funds is said to be in the range of 100-150. This number is hard to verify as accessing opportunities in Sri Lanka is entirely dependent on proprietary networks, unlike in India where the PE market is highly intermediated. Many IBs we spoke with expressed a preference for concessionary debt over equity given the prevailing high interest rates. A lot of groundwork will need to be done to convince business owners to sell their stake. Exit options must also be thoroughly explored before investment. The corpus of money raised by IPOs on the Colombo Stock Exchange increased nearly fivefold from 2010 to 2011, but the LKR 19.2 billion ($165 million) raised by the 13 listings in 2011, is small in absolute terms. Overall market capitalization as a percentage of GDP continues to remain very low at 40.2% of GDP, compared to other nations like India (93.6%), Philippines (78.8%) and Indonesia (51%).

It is clear that in Sri Lanka, while the need for debt on concessionary terms is large, there is a strong case for equity support from development banks for small and medium-sized inclusive businesses, especially those that engage the BOP as suppliers and employees. While the Sri Lankan PE market presents risks associated with a nascent market, we believe these risks can be effectively managed by taking a measured approach to investment. ADB should set aside a limited amount to invest through an experienced fund manager with the expectation of making 1-2 IB investments a year initially.

ADB Inclusive Business Market Study for India and Sri Lanka Final Draft Report

10

STRATEGY

Our findings in response to the question of what the fund’s strategy should be are divided into six parts:

a) Instruments and returns expectation b) Target size of IBs’ investment requirement c) Sector focus d) Geographic focus e) Mode of engagement f) Other criteria for investment

a) Instruments and returns expectations

ADB should observe financial discipline across all instruments that it deploys; reasonable net financial return expectations provide an opportunity to service the large need for non-equity instruments.

In our assessment, ADB’s expectation of net financial returns in the range of 10-12% can be met by observing discipline across the instruments deployed by the fund. This implies that expected returns on equity and debt should be no less than market rate (typically in excess of 20% for equity and 14% for debt, gross).

A strategy that is focused solely on equity will not address the large underserved need for debt for working capital, which is currently a critical barrier to growth of inclusive businesses, largely for want of collateral/security. ADB’s reasonable overall returns expectations and impact-orientation provide an important opportunity to address this issue by focusing on increasing access to debt for IBs. This could be achieved by setting-up a debt financing facility where loans are provided to investees of existing impact investors. An additional intervention to increase debt could be a credit guarantee scheme, targeted at IBs that are keen to access debt from the commercial banking sector. Interventions on the debt side may be considered timely as a number of impact-oriented PE funds are currently contemplating launching Non-Banking Finance Companies to provide debt to businesses. ADB could consider collaborating with a few SME, LIS and IB-focused PE funds to extend debt to their investee companies.

A technical assistance (TA) or grant facility is another important mechanism to supporting capacity-building in IBs. Pre-investment support could be offered through collaborating with existing incubators in areas such as legal and IP support, accounting, MIS, etc. Post-investment support could target areas such as training and awareness generation that also result in the creation of public goods. In Sri Lanka, an ADB TA facility could look at supporting capital market development and reforming the tea estates sector.

b) Target size of IBs’ investment requirement

In terms of equity, the gap in the market is between $2-10 million; debt financing to meet working capital requirements is a large need across a wide range of asset-light businesses and requires further analysis on the size of debt offerings that should be priority

Stakeholders across various categories – IBs, fund managers and donors – have echoed the view that ADB’s fund should focus on supporting the growth of small and medium-scale IBs that roughly correspond to the Indian government’s small and medium industry classification, i.e. firms with less than $2 million invested in plant and machinery. The largest unmet need in these firms is the need for debt for working capital. These firms have limited access to external sources of debt finance as

ADB Inclusive Business Market Study for India and Sri Lanka Final Draft Report

11

banks practice collateral-based lending and a large number of these firms are unable to comply with these requirements.

Larger firms, on the other hand, have several alternate financing options, including commercial PE (there are over 300 PE funds in India, majority of whom invest upwards of $10 million per deal); commercial bank loans, corporate debt and the stock market.

In equity, very few equity investors provide support in the $1-10 million range required for early growth financing. While USD $1-10 million is seen as a relevant range to support inclusive businesses, investors expect a higher proportion of deals to be below $5 million given the nascent stage of development of most IBs in India and Sri Lanka today. This, along with the focus on low-income states and impact investments, would have implications on the selection of fund managers that ADB would collaborate with to make available its debt financing facility.

c) Sector focus

ADB should adopt a sector agnostic approach, but prioritize sectors that are currently presenting strong opportunities for social impact, such as rural livelihood (agri-businesses, tourism, handicrafts), education, healthcare, water, sanitation and energy.

Though the overall market for PE deals in India is substantial (460 deals in 2011), very few sectors, barring large infrastructure, real estate, finance and telecom, see sufficient annual deal flow to warrant exclusive focus. Highly inclusive sectors like agriculture saw fewer than 4 deals per year between 2005 and 20107. The relative lack of depth in any specific sector has resulted in very few sector-specific PE funds - over 80% of the 300+ PE funds active in India today are sector-agnostic. Given the newness of the asset class in Sri Lanka, adopting a sector-agnostic approach is perceived by many as the only feasible approach.

Acknowledging the constraints imposed by the stage of PE market development, we recommend that ADB work with funds that are sector-agnostic in their approach with a light focus on sectors that deliver high financial and social returns, in addition to being relatively asset-light and free of risks such as over-regulation and ESG concerns. Based on Dalberg’s analysis of these factors and risks, inclusive businesses that impact rural livelihoods like agri-businesses, handicrafts, tourism etc. and those in education, healthcare, water, sanitation, and energy appear to be the most attractive.

d) Geographic focus

ADB should largely adopt a geography-agnostic approach, but may consider channelling part of its debt financing facility through existing low-income states (LIS) focused funds.

Low deal flow is a key reason cited by many impact-oriented investors as the key reason for maintaining a pan-India investment approach instead of focusing exclusively on India’s low-income states in the north and east. India’s high and growing incidence of urban poverty (298 million BOP live in urban areas that typically fall in high-income states) and the pan-India growth plans of majority (more than 75%) of IBs that responded to our survey, are additional arguments in favour of a geography-agnostic approach in planning for its debt financing facility. There are, at present, only two funds in India which invest exclusively in low-income states. Both were launched in 2012 with support from DFIs and DFI-funded investors like DFID, CDC and IFC and their performance is yet to be assessed.

7 Grant Thornton India PE Report 2011

ADB Inclusive Business Market Study for India and Sri Lanka Final Draft Report

12

In Sri Lanka too, investors are wary of exclusively focusing on post-conflict provinces in the north & north-east and under-developed eastern and southern provinces. The higher operational costs, in terms of personnel and time to source deals from these regions, was also cited as a disincentive.

While uncertainty concerning deal quality and deal flow can be mitigated with an agnostic approach, the argument still remains that under-developed regions deserve special attention. We recommend that ADB collaborate with a few existing low-income states-focused SME funds to extend its debt facility to IBs operating in low-income states.

e) Mode of engagement with the BOP

The ADB should remain open to supporting businesses that engage the BOP in a variety of ways

Mode of engaging the BOP refers to the way in which businesses interface with the poor – as consumers, distributors, employees or suppliers. The analysis reveals that successful IBs tend to utilize more than one mode of engagement, sometimes even three or four. In the Indian context, all modes of engagement are relevant and have high potential for social impact and financial returns. The relatively small size of the BOP in Sri Lanka and high level of human development reduce the relevance of pursuing consumer-oriented models in Sri Lanka. Overall, our recommendation is that the ADB should support innovative businesses that engage the BOP in a variety of ways.

f) Other criteria for investment

The ADB should focus on businesses that are asset-light, service-oriented and are deploying technology to facilitate growth.

Across the board, fund managers have said they prefer to make equity investments in businesses that are asset light, service oriented and enabled by technology.

Capital intensive sectors such as microfinance and housing are not favoured by investors with limited funds. Service orientation, i.e. the addition of a layer of service on top of a product is also seen to play a big role in the success of inclusive businesses many of which are selling novel products, such as solar lanterns, milk chillers, phone-based medical counselling, etc. to first-time buyers.

In the Indian context, technologies like smart cards and mobile-based payments and information systems are helping to drive scale especially for models that require extensive rural reach. Company innovation and access to technology was cited as the top two critical factors for growth by majority of inclusive businesses surveyed as part of this study.

OPERATIONALIZATION

ADB should collaborate with a few, existing impact-focused funds managed by experienced fund managers.

India has several funds targeting IBs, many of which have fund managers with deep experience in investing for both impact and financial returns. Feedback from fund managers suggests that they would consider collaborating with the ADB where ADB provides debt to the funds’ investee companies.

ADB Inclusive Business Market Study for India and Sri Lanka Final Draft Report

13

This feedback was corroborated by feedback from other donors and investors, majority of whom have taken a fund-of-funds approach. CDC and IFC, two of the largest DFI-supported PE investors, have only recently invested in impact-oriented SME funds8 where managers are still in the process of fund raising. Considering the large unaddressed need for debt, a number of PE funds are considering setting-up of Non-Banking Financing Companies to provide debt to companies to meet their working capital needs. These funds are an attractive option for ADB to collaborate with as their managers have completed the due diligence process, have local networks and experience, critical elements for a debt financing facility.

We recommend, therefore, that ADB support the scale-up IBs in India by setting-up a debt financing facility and route its debt through a few established funds that are impact focused. These may be a mix of funds that are focused on SMEs and/or LIS. The funds would independently select the companies they choose to make an equity investment in. The ADB could, through a separate debt facility, offer debt to select investees that fall under ADB’s classification of inclusive business. We believe this approach could help ADB achieve the desired outcome of supporting the scaling-up of IBs and serving an unmet need, without the costs and risks associated with having to identify offer and monitor debt to companies entirely independently.

In Sri Lanka, in addition to setting-up a debt facility, the ADB could make equity investments into IBs by partnering with the existing PE funds. Deal sourcing in Sri Lanka is largely non-intermediated and most under-the-radar opportunities can be accessed only by experienced fund managers. This would place ADB in a unique position in Sri Lanka in both, the IB debt financing and equity investing space.

Potential Fund Manager Partners for ADB

Our recommendation to the ADB would be to consider fund managers to partner with based on 5 criteria – 1) the stage in which they invest into companies; 2) their exposure to low income states; 3) their development mandate; 4) their experience in making $1-$10 million investments with a preference towards $1-$5 million; and 5) their familiarity with social impact reporting metrics.

Based on our interviews with nearly 21 fund managers in India and Sri Lanka, we recommend the following fund managers for the ADB to consider partnering with:

a) Pragati India Fund (India) b) Aavishkaar (India) c) Small Enterprises Assistance Fund (India) d) SIDBI-Venture Capital (India) e) Aureos South Asia (India & Sri Lanka) f) LR Global (Sri Lanka)

More details on the above-mentioned fund managers may be found in the annexure to this report.

8 CDC and IFC have invested in Pragati, a low-income-states focused SME fund; IFC has invested in LR Global,

an SME-focused fund in Sri Lanka

ADB Inclusive Business Market Study for India and Sri Lanka Final Draft Report

14

2.3. RECOMMENDATIONS

In light of these findings, Dalberg advises ADB to adopt a three-pronged strategy to support the development of inclusive business in India and Sri Lanka.:

I. First, given the larger, unaddressed need for collateral-free debt financing, ADB should set up a debt-financing facility to support growth of existing IBs in India and Sri Lanka.

Given the diversity observed in existing IBs, the debt-financing facility should be geography agnostic, though the ADB may consider channelling part of its debt financing facility through existing low-income states (LIS)-focused funds

ADB should adopt a sector agnostic approach, though priority may be given to addressing needs of IBs operating in high impact sectors such as rural livelihoods ( e.g. agri-business, tourism, handicrafts), water, sanitation, education, healthcare and energy

Mode of engagement with BOP should not be a major criterion for offering debt

Focus should be on innovative, high-growth models that are asset-light, service oriented and enabled by technology

The financing facility should work in collaboration with a selection of existing fund managers with experience of making investments in social enterprises and inclusive businesses in the sub $10 million deal size category (but not necessarily including angel investors)

In addition to offering debt to companies, the facility could also provide credit guarantees for inclusive businesses in India & Si Lanka that have challenges providing collateral acceptable to the banking system. Defining the exact size, rules and distribution was not part of the scope of this study and needs to be further explored.

II. Second, ADB should establish a Technical Assistance facility to support pre-investment and post-investment capacity building in IBs.

Pre-investment support could be provided through existing incubation centres that provide support in areas such as legal, IP support, accounting, MIS, etc.

Post-investment support could be targeted at areas such as training and awareness generation, that also result in the creation of public goods

In Sri Lanka, the ADB TA facility could support capital market development and reforming the tea estates sector

III. Third, in Sri Lanka, the ADB should consider offering equity to inclusive businesses either

directly or through an existing fund with a mandate to support inclusive business.

We also recommend further analysis to understand the role ADB can play in offering debt to help inclusive businesses in India and Sri Lanka achieve scale.

ADB Inclusive Business Market Study for India and Sri Lanka Final Draft Report

15

3. MACROECONOMIC ASSESSMENT OF INDIA

A number of secondary data sources were used to conduct an assessment of macroeconomic conditions in India. These sources include government census reports, economic publications and surveys, data published by international organizations such as the ADB, UN, World Bank and CIA, and other key BOP-focused reports including The Next 4 Billion.

3.1. OVERVIEW OF PERFORMANCE ON ECONOMIC AND SOCIAL INDICATORS

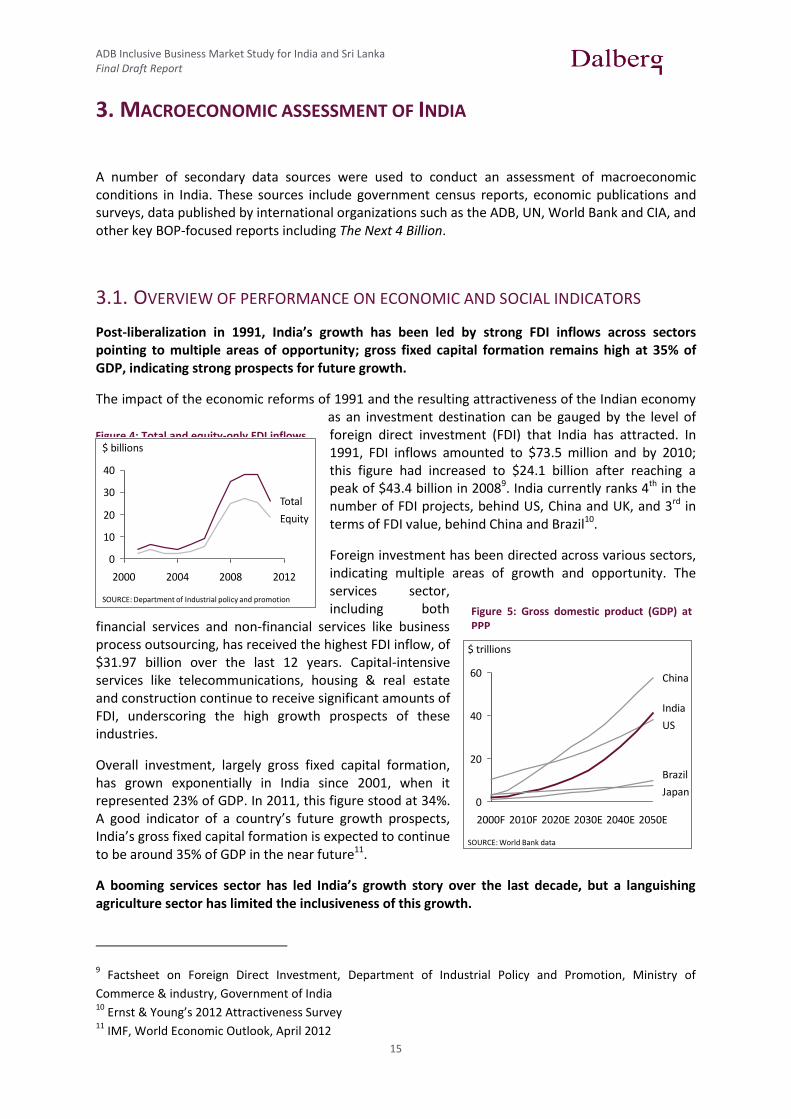

Post-liberalization in 1991, India’s growth has been led by strong FDI inflows across sectors pointing to multiple areas of opportunity; gross fixed capital formation remains high at 35% of GDP, indicating strong prospects for future growth.

The impact of the economic reforms of 1991 and the resulting attractiveness of the Indian economy as an investment destination can be gauged by the level of foreign direct investment (FDI) that India has attracted. In 1991, FDI inflows amounted to $73.5 million and by 2010; this figure had increased to $24.1 billion after reaching a peak of $43.4 billion in 20089. India currently ranks 4th in the number of FDI projects, behind US, China and UK, and 3rd in terms of FDI value, behind China and Brazil10.

Foreign investment has been directed across various sectors, indicating multiple areas of growth and opportunity. The services sector, including both

financial services and non-financial services like business process outsourcing, has received the highest FDI inflow, of $31.97 billion over the last 12 years. Capital-intensive services like telecommunications, housing & real estate and construction continue to receive significant amounts of FDI, underscoring the high growth prospects of these industries.

Overall investment, largely gross fixed capital formation, has grown exponentially in India since 2001, when it represented 23% of GDP. In 2011, this figure stood at 34%. A good indicator of a country’s future growth prospects, India’s gross fixed capital formation is expected to continue to be around 35% of GDP in the near future11.

A booming services sector has led India’s growth story over the last decade, but a languishing agriculture sector has limited the inclusiveness of this growth.

9 Factsheet on Foreign Direct Investment, Department of Industrial Policy and Promotion, Ministry of

Commerce & industry, Government of India 10

Ernst & Young’s 2012 Attractiveness Survey 11

IMF, World Economic Outlook, April 2012

Figure 4: Total and equity-only FDI inflows into India

2

Foreign Direct Investment (FDI) growth and top sectors

SOURCE: Department of Industrial policy and promotion

Sectors attracting highest equity inflows in 2011-12Figures in USD (billions)

Power

Computer software& hardware

2011-2012

18

26%

17%

12%

12%

11%

9%

9%

4%

Service sector

Drugs & pharmaceutical

Construction activities

Others

Telecommunication

Metallugical industry

2012

40

2000

30

20

10

2008

0

2004

Equity

Total

$ billions

Figure 5: Gross domestic product (GDP) at PPP

3

3. Gross Domestic Product at PPP

SOURCE: World Bank data

$ trillions

Brazil

Japan

India

China

US

2020E 2030E2010F2000F

40

60

0

20

2040E 2050E

ADB Inclusive Business Market Study for India and Sri Lanka Final Draft Report

16

Over the last decade, India’s GDP has been growing at an average of around 8% per annum, making it one of the fastest growing major economies in the world. At a total size of $1.45 trillion, the Indian economy is the 11th largest by nominal GDP and at a total size of $4.82 trillion (PPP), the 3rd largest by Purchasing Power Parity (PPP) behind the US and China. Multiple forecasts predict this trend continuing to accelerate, and by 2020 India’s GDP in PPP terms is expected to rise to $8.01 trillion12.

While India’s economy as a whole has been growingly rapidly, the key economic sectors of agriculture, industry and services have been growing unevenly. Data from past five-year plans, 9th Plan (1997-2002), 10th Plan (2002-2007) and 11th Plan (2007-2012) point to the fact that the agriculture and allied services sector, which employs over 50% of the country’s population, has grown significantly slower (less than 3.5% annually) than the services sector (approx. 7.5% annually). This has significantly limited the inclusiveness of India’s growth.

Figure 6: Historic and planned sector growth rates

The sections below describe the trends and issues across these key sectors:

AGRICULTURE AND ALLIED SERVICES

The agricultural sector, comprising of activities such as crop farming, horticulture, animal husbandry and fisheries, provides livelihood to roughly half of India’s population, and is a high-impact sector in the context of inclusive growth. Its contribution to India’s GDP, however, has reduced from 29.3% in 1990-91 to 18% in 2011-201213. In the most recent 11th plan period (2007-12), agriculture grew by only 3.2%, as compared to the target of 4%. Furthermore, within that period, the sector stagnated at 0.1% growth for two consecutive years between 2008 and 2010.

12 World Bank, PWC Report and Dalberg analysis

13 CIA World Factbook, Planning Commission of India

4

3. Historic and planned sector growth rates

% growth rates9th plan(‘97-’02)

10th plan(‘02-’07)

11th plan(‘07-’12)

12th plan(‘12-’17)

Low Growth Estimate *

High Growth Estimate*

Agriculture, Forestry and Fishing 2.5 2.3 3.2 4.0 4.2

Industry 4.3 9.4 7.4 9.6 10.9

Mining & quarrying 4.0 6.0 4.7 8.0 8.5

Manufacturing 3.3 9.3 7.7 9.8 11.5

Elect., gas & water 4.8 6.8 6.4 8.5 9.0

Construction 7.1 11.8 7.8 10.0 11.0

Services 7.9 9.3 10.0 10.0 10.0

Trade, hotels & restaurants 7.5 9.6 7.0 11.0 11.2

Transport, storage, and communication 8.9 13.8 12.5 11.0 11.2

Banking and financial services 8.0 9.9 10.7 10.0 10.5

Community, social & personal services 7.7 5.3 9.4 8.0 8.0

GDP 5.5 7.8 8.2 9.0 9.5

* Low growth target - 9% target ; high growth target -9.5%Note: Classification of sub-sectors into industry & services is done according to planning commission of India’s method

SOURCE: Faster, Sustainable and More Inclusive Growth – An Approach to the Twelfth Five Year Plan 2012-2017; Planning Commission-2011, Government of India

ADB Inclusive Business Market Study for India and Sri Lanka Final Draft Report

17

Under-investment in critical infrastructure, inefficient land-use patterns and seasonal uncertainties are to be blamed

for the sector’s poor performance. In the 12th 5-year plan (2012-2017), the government plans to achieve growth rates over 4% by focusing on non-farm activities, such as post-harvest operations, rural supply chain management, and warehousing, which can all contribute significantly towards the expansion of employment and income opportunities.

INDUSTRY

Though industry has grown faster than agriculture (a 7.4% growth rate14 during the recent plan period), growth has still been below expectations (10-11%). Within that period, the growth of the sector, which includes mining

and quarrying, manufacturing and energy, dropped from 12.2% in 2006-2007 to 3.9% in 2011-2012. Furthermore, its contribution to India’s GDP decreased from 28.7% to 26%15. In addition to contributing heavily to overall GDP growth, a growing industrial sector is essential for absorbing surplus labour from the agricultural sector.

Growth in industry has been impeded by challenges in land acquisition and poor energy and water infrastructure. In more recent times (2011-12), the high interest rates imposed by the central bank to combat inflation have been blamed for the slow growth of industrial output, as measured by India’s Index of Industrial Production.

SERVICES

The services sector in India has grown sharply over the past decade and continues to do so. Services comprise of financial services, information technology and information technology-enabled services (IT and ITES), tourism and hospitality, health, education and construction. Combined contribution of all service-oriented industries to India’s GDP has grown from 54% in 2006-07 to 59% in 2011-12. The services sector is currently growing at a healthy 10% annually.

This growth in the service sector has been led primarily by private enterprises, aided by India’s large pool of workers, both skilled and unskilled. The sector’s activities have resulted in massive job creation, and it has become a catalyst of urbanization and urban migration. The construction industry alone provides direct/ indirect employment to 35 million people and is expected to employ 92 million people by 2022.

India’s limited inclusiveness of growth is reflected in its significant economic inequality and poor performance on human development indicators.

Despite emerging as one of the world’s largest economies, India’s per capita income still places it in the low-middle income bracket, as per World Bank’s definition of country lending groups. At $3,694 (PPP), India’s per-capita income places it at the 129th place in the world; just below Iraq16.

In 2004-05, the average per capita income of India’s bottom quintile by income was $176 (INR 9,305) but $1,997 (INR 105,845) for the top quintile, an eleven-fold difference in income levels. As per the

14 Planning Commission, 2011

15 Exim Bank of India report

16 IMF, World Economic Outlook, April 2012

5

3. Contribution of sectors to GDP and labor force employment

SOURCE: CIA Factbook

26%

14%

Services

Industry

Agriculture

Labour force by sector

(2009)

488 million

Sectoral contribution

to GDP(2011)

$ 1.8 trillion

18%

56%

52%

34%

Figure 7: Contribution of sectors to GDP and labour force employment

: asdasd

ADB Inclusive Business Market Study for India and Sri Lanka Final Draft Report

18

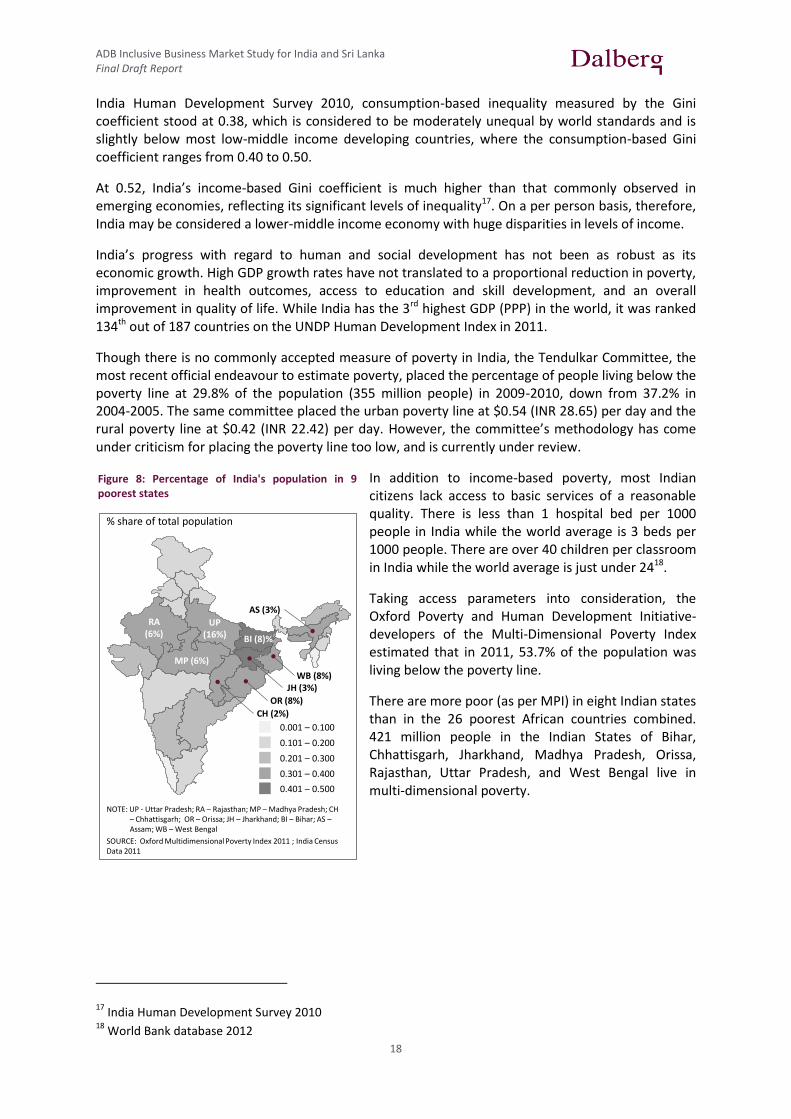

India Human Development Survey 2010, consumption-based inequality measured by the Gini coefficient stood at 0.38, which is considered to be moderately unequal by world standards and is slightly below most low-middle income developing countries, where the consumption-based Gini coefficient ranges from 0.40 to 0.50.

At 0.52, India’s income-based Gini coefficient is much higher than that commonly observed in emerging economies, reflecting its significant levels of inequality17. On a per person basis, therefore, India may be considered a lower-middle income economy with huge disparities in levels of income.

India’s progress with regard to human and social development has not been as robust as its economic growth. High GDP growth rates have not translated to a proportional reduction in poverty, improvement in health outcomes, access to education and skill development, and an overall improvement in quality of life. While India has the 3rd highest GDP (PPP) in the world, it was ranked 134th out of 187 countries on the UNDP Human Development Index in 2011.

Though there is no commonly accepted measure of poverty in India, the Tendulkar Committee, the most recent official endeavour to estimate poverty, placed the percentage of people living below the poverty line at 29.8% of the population (355 million people) in 2009-2010, down from 37.2% in 2004-2005. The same committee placed the urban poverty line at $0.54 (INR 28.65) per day and the rural poverty line at $0.42 (INR 22.42) per day. However, the committee’s methodology has come under criticism for placing the poverty line too low, and is currently under review.

In addition to income-based poverty, most Indian citizens lack access to basic services of a reasonable quality. There is less than 1 hospital bed per 1000 people in India while the world average is 3 beds per 1000 people. There are over 40 children per classroom in India while the world average is just under 2418.

Taking access parameters into consideration, the Oxford Poverty and Human Development Initiative- developers of the Multi-Dimensional Poverty Index estimated that in 2011, 53.7% of the population was living below the poverty line.

There are more poor (as per MPI) in eight Indian states than in the 26 poorest African countries combined. 421 million people in the Indian States of Bihar, Chhattisgarh, Jharkhand, Madhya Pradesh, Orissa, Rajasthan, Uttar Pradesh, and West Bengal live in multi-dimensional poverty.

17 India Human Development Survey 2010

18 World Bank database 2012

Figure 8: Percentage of India's population in 9 poorest states

6

3. Multi-dimensional poverty index (MPI) mapping of Indian States

NOTE: UP - Uttar Pradesh; RA – Rajasthan; MP – Madhya Pradesh; CH – Chhattisgarh; OR – Orissa; JH – Jharkhand; BI – Bihar; AS –Assam; WB – West Bengal

SOURCE: Oxford Multidimensional Poverty Index 2011 ; India Census Data 2011

% share of total population

0.301 – 0.400

0.201 – 0.300

0.101 – 0.200

0.001 – 0.100

0.401 – 0.500

RA (6%)

MP (6%)

UP (16%) BI (8)%

OR (8%)

WB (8%)JH (3%)

CH (2%)

AS (3%)

ADB Inclusive Business Market Study for India and Sri Lanka Final Draft Report

19

3.2. KEY INCLUSIVE BUSINESS SECTORS AND GOVERNMENT INITIATIVES

Agriculture

More than half the population of India is dependent on agriculture as a source of employment and livelihood. The long-term growth in agriculture has been just around 2%, which is just above the population growth rate. Agriculture’s declining share in the country’s economy is putting huge pressure on food security and consequently on food prices. Given the fact that this is a hugely important sector from an employment, food security and overall impact perspective, a lot needs to be done to stimulate growth.

India had record food grain production of over 250 million tonnes in 2011-2012 but the saddening irony is that there are millions in India that are either malnourished or go hungry. The Global Hunger Index released by the International Food Policy Research Institute ranks India 66th among 88 vulnerable countries and as per the government’s estimates 42% of children in India are malnourished. India’s food grain stockpile is roughly around 75 million tonnes, which is roughly two and a half times the stipulated maximum food buffer. However, our warehousing capacity is just 63 million tonnes. As per the government’s own estimate, 6 million tonnes of food grain rotted in its granaries due to poor storage last year. A report by the commissioner appointed by the Supreme Court of India put the figure at 13 million tonnes. While the government debates the Food Security Bill, 57% of the subsidized food does not reach the intended poor due to systemic leakages in the public distribution network19. To add to the woes, tons of food grains rot every year in open fields for want of proper storage facilities. Revamping the entire procurement, distribution, transport and storage ecosystem is required to meaningfully address these issues.

“Ensuring an increase in private investment” is the government’s focus for in this sector over the next five years. Other recommendations that are yet to be implemented are liberalizing agri-procurement, streamlining norms for private investment in agricultural supply chains and revisiting the Minimum Support Price norms.

Key government initiatives:

18% hike in the budgetary allocation to agriculture in the 2012-2013 budget, from $3.2 billion (INR 17,123 crore) in 2011-2012 to $3.8 billion (INR 20,208 crore) in 2012-2013.

Agricultural credit was also increased by $18.8 billion (INR 1,00,000 crore) over the previous year to $108.5 billion (INR 5,75,000 crore).

Focus areas in the 12th five-year plan:

Frame policies that trigger domestic demand recovery

Ensure rapid rise in private investment

Remove bottlenecks in agriculture, energy, transport, coal, power and national highway

Address malnutrition

Health

The hospital and diagnostic center segment in medical care in India has attracted FDI to the tune of $1.2 billion between 2000 and 2012, while the drugs $ pharmaceuticals and medical and surgical appliances industries received investments worth $9.2 billion and $514 million respectively. The

19 UID and PDS in India; Unique Identification Authority of India, Planning Commission, Government of India

ADB Inclusive Business Market Study for India and Sri Lanka Final Draft Report

20

government has taken some progressive measures to encourage private participation in the healthcare industry to bridge the vast demand-supply gap.

Key government initiatives20:

The government plans to increase health expenditure to 2.5% of GDP by the end of the 12th five-year plan, from the current 1.4%.

It has allowed 100% FDI for health and medical services under the automatic rule.

Allocation of funds to the National Rural Health Mission was increased from $3.59 billion in 2011-2012 to $4.13 billion in 2012-2013.

Education

The education sector holds a huge promise for private sector participation. Roughly 45% of the population is under the age of 19 years, meaning that over 500 million people are in need of primary, secondary and higher education. The government has committed $11 billion to this sector towards primary and secondary education in 2012-2013. However, the government is not well positioned to cater to the demand for quality education given restrictions on pay scales for teachers in government-run institutes and inability to expand schooling infrastructure at the required pace.

Between 2008 and 2012, the K12 education sector (Kindergarten to 12th grade) grew 14% from a market size of $20 billion to $34 billion, while higher education grew 12% from $6.5 billion in 2008 to $10.3 billion in 201221. Vocational training institutes, which have a huge relevance for the BOP segment, have a market size of approximately $4 billion, up from $1.6 billion in 2008. Overall, the education sector has a market size of $50 billion per annum with more than 45 million students and an investment requirement of approximately $100 billion by 2014.

Key government initiatives22:

In the 11th five-year plan (2007-2012) the allocation of funds towards technical and higher education was increased nine-fold to $18.8 billion from $2.1 Billion in the 10th five-year plan

100% FDI in education allowed through the automatic route23

National Skill Development Corporation has approved public-private partnership projects that are expected to train 62 million people in 10 years

The National Skill Development Fund has been allocated $ 0.19 billion for 2012-2013.

The government proposes to set-up a separate Credit Guarantee Fund to improve the flow of institutional credit for skill development

Water & Sanitation

By, India’s goal is to halve the proportion of people without sustainable access to improved water sources by 2015. As per available government statistics India had already met this target by 2008 by reducing the percentage of households without access to improved water sources from 32% in 1993 to 9% through a massive program of expanding bore well and hand pump construction under

20 IBEF, March 2012 Update: Ministry of Commerce and CII Initiative,

http://www.ibef.org/artdispview.aspx?art_id=31258&cat_id=119&in=29; DIPP 21

India Brand Equity Foundation (IBEF): Ministry of Commerce and CII initiative 22

IBEF, March 2012 Update: Ministry of Commerce and CII Initiative, http://www.ibef.org/artdispview.aspx?art_id=31278&cat_id=1057&in=76 23

Press release on “Foreign Universities and Educational Institutions”, 4 May, 2012: Press Information Bureau, Government of India

ADB Inclusive Business Market Study for India and Sri Lanka Final Draft Report

21

schemes such as the Accelerated Rural Water Supply Program However, drinking water experts fear that many habitations will ‘slip’ back with the drying up and contamination of ground water, the source for 85% of rural water supply. Supply of ‘safe drinking water’ will be a major focus for the government in the coming years as awareness of the health impacts of unsafe water spreads. Purification of water is also an area where the private sector has a key role to play, especially in the provision of appropriate technologies.

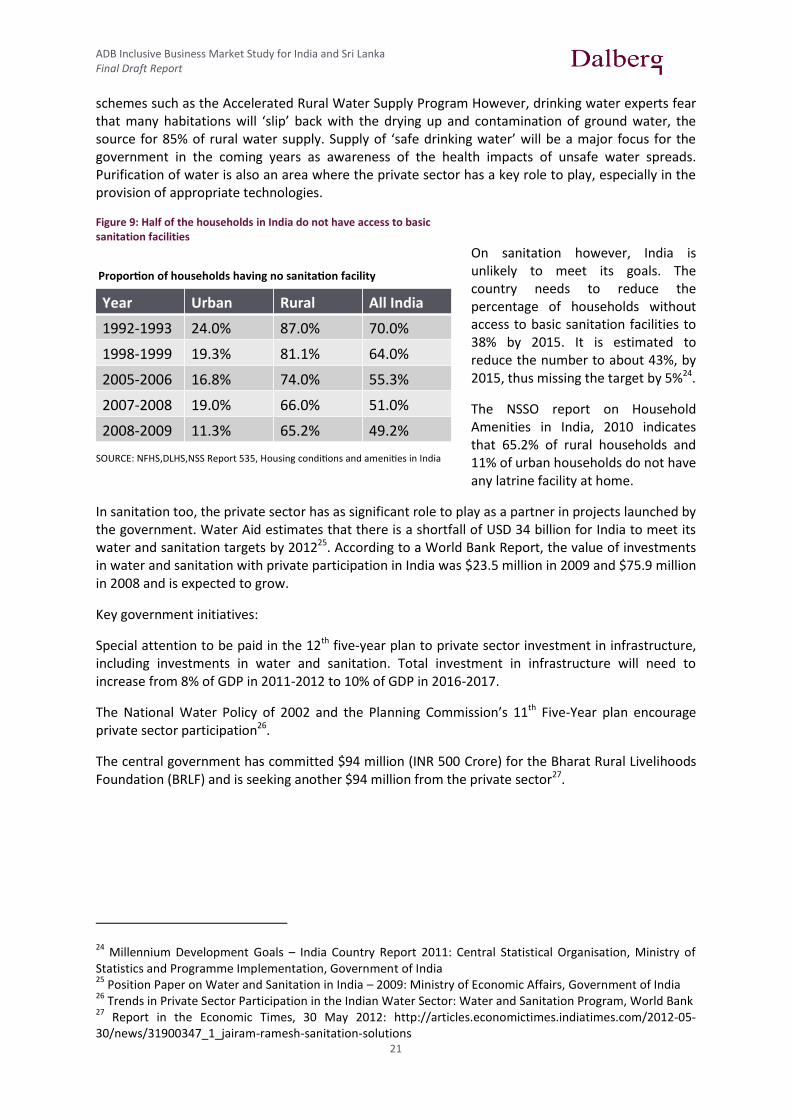

Figure 9: Half of the households in India do not have access to basic sanitation facilities

On sanitation however, India is unlikely to meet its goals. The country needs to reduce the percentage of households without access to basic sanitation facilities to 38% by 2015. It is estimated to reduce the number to about 43%, by 2015, thus missing the target by 5%24.

The NSSO report on Household Amenities in India, 2010 indicates that 65.2% of rural households and 11% of urban households do not have any latrine facility at home.

In sanitation too, the private sector has as significant role to play as a partner in projects launched by the government. Water Aid estimates that there is a shortfall of USD 34 billion for India to meet its water and sanitation targets by 201225. According to a World Bank Report, the value of investments in water and sanitation with private participation in India was $23.5 million in 2009 and $75.9 million in 2008 and is expected to grow.

Key government initiatives:

Special attention to be paid in the 12th five-year plan to private sector investment in infrastructure, including investments in water and sanitation. Total investment in infrastructure will need to increase from 8% of GDP in 2011-2012 to 10% of GDP in 2016-2017.

The National Water Policy of 2002 and the Planning Commission’s 11th Five-Year plan encourage private sector participation26.

The central government has committed $94 million (INR 500 Crore) for the Bharat Rural Livelihoods Foundation (BRLF) and is seeking another $94 million from the private sector27.

24 Millennium Development Goals – India Country Report 2011: Central Statistical Organisation, Ministry of

Statistics and Programme Implementation, Government of India 25

Position Paper on Water and Sanitation in India – 2009: Ministry of Economic Affairs, Government of India 26

Trends in Private Sector Participation in the Indian Water Sector: Water and Sanitation Program, World Bank 27

Report in the Economic Times, 30 May 2012: http://articles.economictimes.indiatimes.com/2012-05-30/news/31900347_1_jairam-ramesh-sanitation-solutions

15

Year Urban Rural AllIndia

1992-1993 24.0% 87.0% 70.0%

1998-1999 19.3% 81.1% 64.0%

2005-2006 16.8% 74.0% 55.3%

2007-2008 19.0% 66.0% 51.0%

2008-2009 11.3% 65.2% 49.2%

Propor onofhouseholdshavingnosanita onfacility

SOURCE:NFHS,DLHS,NSSReport535,Housingcondi onsandameni esinIndia

ADB Inclusive Business Market Study for India and Sri Lanka Final Draft Report

22

Energy

The energy requirements in a rapidly growing economy like India are growing at an accelerated rate. Access to clean and affordable energy is one of the primary requirements for everyone, especially the poor at the base of the pyramid.

Most rural households and indeed a significant of urban poor still use kerosene for lighting and largely free fuels like firewood or dung for cooking. These are not only harmful to their health but also contribute to environmental degradation. Besides, the time that is wasted in collecting firewood can be utilized for other productive activities.

The private sector is playing an active role in reaching out to this large market by providing clean energy solutions in cooking and lighting. Solar lighting, solar cookers, biomass gassifier systems etc. are some of the products being offered by the private sector to addressing needs of this large market.

The World Resources Institute, per a report published in 2004-05, estimated that the opportunity in the clean energy market in the rural BoP segment in India was $2.11 billion per year, including $ 2.04 billion for decentralized renewable energy services and $70.1 million for energy products per year. The solar lantern market for supplying basic lighting to the rural BoP alone was estimated to be worth $18 million. The energy-efficient cook stove market was estimated to be worth roughly $24 million per year.

Key government initiatives28:

The Rajiv Gandhi Grameen Vidyutikaran Yojana (RGGVY) was devised to remedy the issue of access to power in rural habitations, especially to households living below the poverty line.

Distribution of solar lanterns at subsidized rates

The Bachat Lamp Yojana (BLY) provides compact fluorescent lamps (CFLs) to households at the cost of incandescent lamps. Currently, 20 million CFLs have been distributed under the BYL.

Tourism

Tourism, along with hospitality, contributes approximately $33 billion, or around 6% of the GDP. The tourism sector in India is one of the largest service industry employment sectors in the country providing 9% of the total employment opportunity in India. The sector is estimated to create 78 jobs per million rupees (approx. $19,000) of investment as compared to 45 jobs per million rupees in the manufacturing sector. The sector is also more inclusive in that it provides jobs to a wide spectrum of job seekers from the unskilled to the highly specialized; jobs are spread across the country; and there is a large percentage of women employment in this sector. The Travel and Tourism Competitiveness Report by the World Economic Forum has ranked India at the 6th place in tourism and hospitality. According to the World Travel and Tourism Council, India is poised to be one of the top tourism destinations in the world till about 2018. The tourism industry in India is expected to grow at close to 9% per annum, making it the 2nd fastest growing tourism market in the world.

Besides providing large-scale employment, the tourism industry also has indirect contribution to the GDP providing a multiplier effect affecting several other associated sectors and industries. According to the Department of Industrial Policy and Promotion, the tourism sector attracted FDI worth $2.8 billion (INR 14,771 crore) between April 2000 and January 2012. Foreign tourism arrivals

28 Planning Commission of India

ADB Inclusive Business Market Study for India and Sri Lanka Final Draft Report

23

in the country have gone up from 3.9 million in 2005, to 5.4 million in 2010 and 6.9 million in the last year29.

Key government initiatives30:

FDI of up to 100% is permissible in the sector through the automatic route.

In 2011-2012, the Ministry of Tourism provided employment to 33,000 youth in tourism. In 2012-2013, they plan to increase this number to 100,000.

It is recommended that the National Tourism Policy form an integral part of the poverty reduction strategy during the 12th five-year plan.

29 IBEF, July 2012; Ministry of Tourism; Department of Industrial Policy and Promotion

30 IBEF, Planning Commission of India

ADB Inclusive Business Market Study for India and Sri Lanka Final Draft Report

24

3.3. KEY TRENDS SHAPING THE ECONOMY

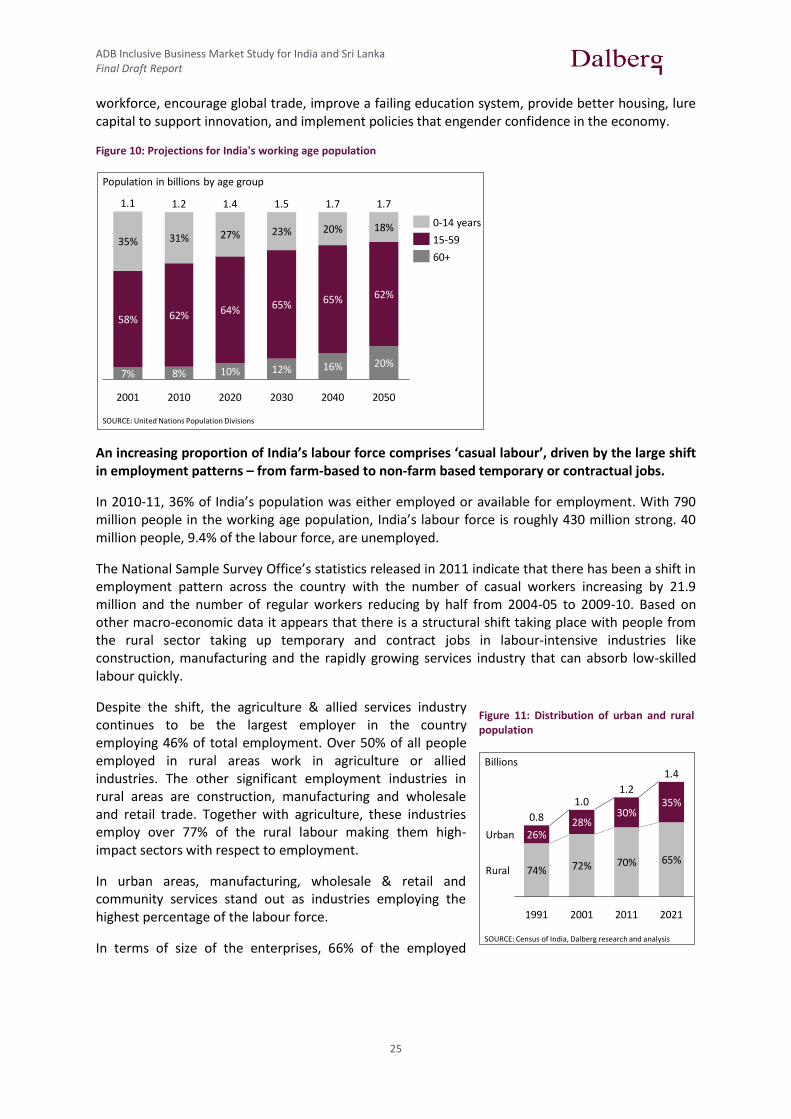

India could take advantage of its favourable age demographics and develop a competitive advantage in possessing 25% of the world’s workforce; demographics in low-income states are particularly well positioned to drive growth.

OECD estimates that in 2020, India will have a population of 1.3 billion people31, surpassing China to become the most populous nation in the world. Against the backdrop of new economic opportunities, India’s teeming millions, once seen as a major burden, are being seen as assets to propel the country onto a higher growth trajectory.

According to the IMF, a substantial proportion of growth that India experienced since the 1980’s can be attributed to the country’s age structure and age demographics32. Currently 54% of India’s 1.2 billion people are under the age of 25 and 63.5% of India’s population, roughly around 760 million people, falls in the working-age bracket of 15 to 59 years33. Further, 300 million people will enter the labour market by 2025, providing 25% of the world’s workers34. The continuing demographic dividend is estimated to add roughly 2 percentage points to India’s per capita GDP growth every year.

There are multiple implications of millions of young people entering the workforce. According to David Bloom - the demographer who first coined the term ‘demographic dividend’ - young, unencumbered workers are seen to spur entrepreneurship and innovation, enabling significant gains in productivity, savings, and capital inflows.

Additionally, India will be experiencing an increase in the number of working age people just when other large countries see the average age of their populations decline, opening up opportunities for the export of workers from India to the rest of the world. In 2020, the average age in India will be only 29 years, compared with 37 in China and the United States, 45 in Western Europe, and 48 in Japan35.

Demographics are also believed to have played a role in influencing the growth rates of Indian states. Authors of the IMF working paper feel that some of India’s economically strong states have already reaped a demographic dividend over the last couple of decades. Per their analysis, the states of Karnataka, Tamil Nadu and Gujarat can attribute between 2.4 and 3 percent of their annual per capital GDP growth rate in the 1980’s to a favourable age distribution.

According to the authors, the 9 economically weaker states36 in the country, home to more than half the population, may have just entered the sweet spot in terms of the age structure of their populations to start experiencing a demographic dividend. Bihar, a traditionally low-growth state, has been the fastest growing state for the last two years with its GDP expanding by 14.8% and 13.1% in 2010-11 and 2011-12 respectively. A percentage of this growth could be attributed to favourable demographics.

The value of India’s demographic dividend will depend in great measure on whether the public and private sector have the political will and foresight not only to create jobs but also to train the new

31 OECD Factbook, 2011-12

32 The Demographic Dividend: Evidence from Indian States, IMF, 2011

33 Report on Employment and Unemployment, Labour Bureau of India, 2010

34 The Financial Times

35 ‘India’s Demographic Moment’, Nandan Nilekani, 2009

36 The nine states include Uttar Pradesh, Rajasthan, Madhya Pradesh, Chhattisgarh, Orissa, Jharkhand, Bihar,

Assam & West Bengal

ADB Inclusive Business Market Study for India and Sri Lanka Final Draft Report

25