I I - Costin Borc · Web viewA decentralized market has been set up for long and medium term...

165

1

Transcript of I I - Costin Borc · Web viewA decentralized market has been set up for long and medium term...

1

CONTENTS

Page.

I. ENERGY OVERVIEW OF ROMANIA; PRESENT AND FUTURE …………. 1II. SECURING OF ENERGY RESOURCES ………………………………………. 8III. ENERGY MARKET MODEL IN ROMANIA …………………………………….. 12IV. ENERGY POLICY IN ROMANIA ………………………………………………... 16

IV.1 Competitive energy sustains a competitive economy ………………. 16IV.2 Role of the Regulatory bodies and of the market operators ……… 19IV. 3 Investment and privatization …………………………………………….. 27IV.4 Pricing policy and social protection ……………………………………. 35

V. ENVIRONMENT …………………………………………………………………… 47VI. RESTRUCTURING OF THE POWER GENERATION SECTOR AND THE MARKET

OPERATION……………………………………….………………………………… 49 VI.1 Energy development program for the period 2003 – 2015 .… 52

VI.2 Power plans closure program ………………………………. 53 VI.3 Nuclear safety ……………………………………………………………. 53 VII.4 Electrification program ………………………………………………… 57VII. REGIONAL ELECTRICITY MARKET …………………………………………... 60

APPENDIX 1 - Primary energy balance for Romania for the period 2003-2015

- Macroeconomics and energy indicators for the period 2003-2015i. Basic scenario

ii. Alternative scenario- Structure of the domestic primary energy consumption

- Installed power demand; load curves for the period 2004-2015- Installed power structure in the period 2003 – 2015: basic scenario

- Gross electricity production structure in the period 2003-2015 – basic scenario

- Graphs for installed power structure, gross electricity production structure

- Load duration curves of the net electricity production (three curves)- Graphs of the evolution of the necessary power capacities

- Development program for the generation capacities for the period 2004-2015

- Proposal for the rehabilitation for the new units – installation program

2

- Thermal power units retirement evolution ( starting from existing units as of 01.01.2003

- Fuel consumption for electricity and heat production for the period 2003-2015 + graphs

- Fuel prices

- Electricity average cost - Requirements of investments in electricity sector + graphs

- Ranking order of candidate units according to the levelized costs ( graphs and tables)

- Ranking order of decided units according to the levelized costs

- Estimation of the electricity average cost in the period 2003-2015- Evolution of natural gas internal market opening degree in the perspective

of Romania's EU accession- Evolution of number of the eligible consumers and evolution of natural gas

internal market opening degree- Evolution of domestic market demand, production and import for natural

gas 2003 - 2015- Development of natural gas storage capacities in the period 2000 – 2010

APPENDIX 2- ELECTRICITY ROAD MAP: MARKET STRUCTURE AND REGULATION FOR

THE PERIOD 2003-2015

APPENDIX 3

- GAS ROAD MAP: MARKET STRUCTURE AND REGULATION FOR THE

PERIOD 2003-2015

3

I. ENERGY OVERVIEW OF ROMANIA; PRESENT AND FUTURE

Recognizing that Romania has continued to make progress towards being a

functional market economy, the present road map is focusing on the

remaining steps Romania needs to follow in order to accelerate the alignment

of its policies with the EU “acquis” in the energy field.

This roadmap has been drafted based on the energy policy of the

Romanian Government, by identifying specific task and targets, time table for

their implementation, as well as the needed financial effort and expected

resources to cover.

This Road map covers the power sector and natural gas sector; some other

sub-sectors such as coal/lignite and oil, energy efficiency are dealt only briefly

as supportive sectors (fuel suppliers) for the power sector. For these sectors

separate detailed strategies have been prepared.

The road map is emphasizing issues like:

- Romanian electricity and natural gas demand on short, medium and long

term basis starting with need of promoting the energy saving;

- Market model and structure, improvement of the regulatory and legal

frameworks, and reforms to be implemented in order to respond to the

requirements of the “acquis” and the development of Romania's electricity

and natural gas market capacity to cope with competitive pressure and

market forces within the European Union, by strengthening the competitive

market mechanisms through stable and transparent, methods, rules and

regulations to be implemented by the regulatory and operation bodies. In

these respect key issues to be resolved where identified;

- Progress in public energy enterprise reform, including the completion of

restructuring plans;

- Adjusting the regulatory framework for ensuring security of supply to

ensure compatibility with a market framework;

1

- Reducing the asymmetries in the implementation of the Directives which

can lead to considerable distortions of the internal market;

- Accelerating privatization in the electricity and gas distribution as well as

on the electricity generation side using flexible formulas such as public

private partnership, as well as closure or liquidation of unviable energy

capacities;

- Defining of the needed investments and their expected sources.

THE NEED OF DEVELOPMENT OF THE ENERGY SECTOR

The energy sector represents a strategic infrastructure of the national

economy on which relies the overall development of the country. In the same

time the energy represents a public utility with an important social impact.

The energy policy, is approaching this important sector of the Romanian

National Economy, as a public utility which needs more commercial

mechanisms and competitive environments, where the prices to be formed in

a free competition between a diversity of suppliers and customers, which are

gradually free to purchase their energy, as well as a transparent and stable

market mechanisms surveyed by independent regulating authorities and

market operators.

The basic evaluation of the energy is based on the consumption. The

consumption projections done, as per the Appendix nr .1 here to, are based

on the need of energy:

to sustain the development trend of the country,

as well as on the need of improving the energy efficiency, environment

protection, optimum utilization of the resources.

2

Consequently, the consumption projection done is based on following specific

vectors:

1. GDP evolvement . The Romanian Government policy is to sustain an

accelerated growth of the GDP in view of achieving the strategic objective

of reduction of the economic discrepancy between Romania and EU

countries. Two scenarios of GDP growth, where basically considered for

the period till the year 2015:

GDP growth in % Achieved in the

2000 – 20012002 – 2005 2006 – 2010 2011 – 2015 Average

value2002 - 2015

Base scenario 5.2% 5.1% 6.0% 5.2% 5.46%

Alternative scenario

4.4% 5.5% 4.8% 4.90%

The basic scenario is the one the Government is keen to implement,

based on accelerated development of the economy, where industry

development has a key role, as well as acceleration of the privatization in the

electricity gas and oil sectors, but also accomplishment of the privatization in

other sectors of the national economy.

The alternative scenario has been considered having in view to the

possible negative impact of the trend of the world wide economy on the

Romania market which could slow down some economic processes.

2. Energy intensity.

In the basic scenario as provided in the strategy for energy efficiency, the

overall energy intensity has to be reduced by 30-50% till the year 2015, in a

complex process which involves replacing of the technologies with high

energy consumptions in a structural adjustment of the economy.

The alternative scenario, of 25% is related to the alternative scenario of

the GDP. i.e. a slower development due to some unexpected effects.

3

Energy intensity measured as an amount of primary energy sources per GDP

unit (a ton of oil equivalent to US $ 1,000) is one of the key measures of

energy efficiency and an important component of a national economy, which

has been considered in the energy planning. Energy intensity in Romania

measured by this indicator is as follows:

Energy intensity, in t.o.e. /$ 1,000 of GDP

1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999

Romania:a)b)

1,330,66

1,210,61

1,060,53

1,070,41

1,020,39

0,920,35

0,880,34

0,890,34

0,990,38

0,96 0,83

UE 0,19 0,19 0,19 0,18 0,19 0,18 0,19 0,18 0,17 0,16 0,15For Romania: - Source of information ISPE (Institute for Energetic Studies and Engineering)

a) Final energy consumption/GDP97

b) Final energy consumption/GDP - parity purchase power (ppc)

** - year 1989 has been calculated at the same ppc as in 1990;

- For the years 1998 - 1999 b) indicator has not been calculated due to the lake of ppc

The drop of energy intensity of 3% is mainly due to the structural change of

GPO i.e.:

- drop of industry ration in total GDP form 40,5% in 1990 to 33,2% in 1996

and 25,23% in 2000

- increase of the ratio of services

Specific targets to reduce heat emissions and intensity are included in the

strategy for energy efficiency. Energy intensity is important for this road map

from the point of view of its influence on the determination of the power

demand.

4

In the strategy for energy it is foreseen the following prognosis for energy

intensity:

Energy intensity in the period 2000 – 2015

Indicator MUYear

Scenario2000 2005 2010 2015

Final energy consumption/GDP

t.o.e./103 $

Optimistic - 0.522

0.409

0.334

Optimistic – moderate

- 0.522

0.426

0.352

Medium 0.835

0.533

0.456

0.410

Medium – pessimistic

- 0.547

0.482

0.434

Minimal - 0.557

0.499

0.451

Source: ISPE. The year 1999 has been considered as basic year

3. Population and their increasing energy consumption, by using more house

appliances. It is foreseen the population of Romania to be of 22,2 to 22,3

million inhabitants in the year 2007 and 22,6 million in the year 2015.

Based on the objectives of: GDP growth

Reduction of the energy intensity by 30-50%

Population energy demand

It was determined the following need of energy resources for Romania:

NEED OF PRIMARY ENERGY RESOURCEStoe /1000$ of GDP (tons of oil equivalent)

Achieved 2001

2005 2010 2015 Increase 2015/2001

Reduction of energy intensity

a) 50%b) 40%c) 30%

54.260 54.00057.77058.300

54.70063.80066.900

57.30068.50074.500

300014.20020.200

5

Having in view the Strategy of Energy Efficiency it is considered the

alternative of reduction of energy intensity by 40%, a realistic achievable

target.

Due to a more efficient energy use the average electricity consumption growth is 2.7% / year at a GDP growth of 4-5%/year.

The electricity demand has been projected (see Appendix nr.1) based on this assumptions, ad correspondingly it has been determined the following the gross electricity production chart for the period 2003-2015:

6

GROSS ELECTRICITY PRODUCTION STRUCTURE IN THE 2003-2015 PERIOD

17,04 17,00 17,00 17,20 18,00

5,34 5,34 5,3410,68

16,0213,50 14,00 14,50

15,00

15,004,36 4,60 4,60

4,60

4,60

4,606,70

6,393,80

3,50 3,30

3,00

3,00

6,537,23 7,43

6,70

6,70

8,25

7,00

1,33

1,33

0,930,930,93

0,00

10,00

20,00

30,00

40,00

50,00

60,00

70,00

80,00

2003 2004 2005 2010 2015

Year

Gross

Elec

tricit

y Pr

oducti

on [

TWh]

Thermal power plants onhidrocarbons

Thermal power plants onhard coal

Thermal power plants onlignite

Thermal power plants ofcondensation onhidrocarbons

Thermal power plants ofcondensation on hardcoal

Thermal power plants ofcondensation on lignite

Nuclear power plants

Hydro power plants

56.159.3 60.1

64.9

72.9

7

II. SECURING OF THE ENERGY RESOURCES

The basic criteria, used in the projections done, for the use of the energy resources

was the merit principle (the most efficient cost). Some other subsequent criteria

have been also considers such as:

o security of supply by maximum use of the domestic energy resources

available in the country, but responding to the need of cost efficiency;

o the need of import of energy resources, but in a more diversified structure to

secure a competitive access to the energy resources .

Based on these criteria, the following domestic energy resources where identified

in the strategy:

1. LIGNITE: Availability of domestic lignite reserves for the next 50 to 70 year at a

production rate of 30-35 million tons/year in open pits operations. The mining

strategy provides that the production of lignite is going to be concentrated in the

most cost efficient operations which are the open pits, and the unviable mining

operation (mainly underground) will be closed. The lignite production in Romania is

not subsidized, and represents a competitive source of energy, not influenced by

the market tendency of price increase of other fuels.

2. HARD COAL: Availability of domestic hard coal at a production rate of 3,5 million

tons/year;

Overall consumption of natural gas in Romania in the period 2003 – 2015Year 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

8

Consumption (bill. c.m.)

18.3 18.3 18.4 18.8 19.2 19.6 20 20.4 20.8 21.2 21.6 22 22.4

Domestic sources (bill. c.m.)

12.7 12.5 11.5 10.9 10.4 10.1 9.8 9.5 9.2 8.9 8.6 8.3 8

Import sources (bill. c.m.)

5.6 5.8 6.9 7.9 8.8 9.5 10.2 10.9 11.6 12.3 13 13.7 14.4

Import in yearly consumption (%)

]30.6 31.7 37.5 42 45.8 48.5 51 53.4 55.8 58 60.2 62.3 64.3

3. NATRUAL GAS: Domestic natural gas production will register a sharp decrease

due to limited natural reserves. Consequently the dependency on import will be

increased as follows:Source: National Regulatory Authority in Natural Gas Sector, Bucharest 2003

4. HYDRO POWER: Using the hydropower reserves so that the annual hydro energy

production to increase with 1,5-2,5 GWh by having installed additional power

capacities of about 500-900MW.

5. NUCLEAR ENERGY: Nuclear energy program will be continued by putting into

operation at Cernavoda Nuclear Power Plant unit nr. 2 in 2006 and at a later date

unit nr.3.

6. RENEWABLE ENERGY: Renewable energy sources should be encouraged as

provided in the national program for renewable energy sources; this represents a

local source that can help reduce reliance on import and improves the security of

energy supply, meeting the environment protection criteria. The renewable energy

sources (biomass, hydropower plants, geothermal energy, etc.) represents an

important resource. But the high cost of initial investments represents a limiting

factor in their expansion so that in order to overcome this obstacle a special

incentive program should be enforced including a financial and or financing

component.

9

CONCLUSION

Based on the a.m. (as detailed in the Appendix nr.1 herewith), THE FOLLWING

CONCLUSION CAN BE SUMMARIZED FOR THE YEAR 2015:

The domestic energy resources will be limited at 24-25 million toe/year

By operating, the coal fire plants at slight constant production rate of 30 million

tons of lignite/year and 3,5 million tons of hard cola/year the decline in domestic

energy resources will be partially covered from the nuclear energy and hydro

generation

Even so the need of import of energy resources will increase form 33, 6% in

2001 to 39-40% in 2005 and 49-50% in the year 2015. In this respect the need of

import of natural gas will increase from 18.4 % in 2001 at 64.3 % in the year 2015.

Having in view the trend of increasing this share of imported energy sources, the Energy Strategy of Romania has been based on making strenuous efforts in two key areas: Reduction in specific energy intensity per GDP unit in economy;

Increase of use of renewable energy sources Dealing with transactions that cross the border of one or more countries

which require a degree of harmonization of the approach to tariffs and capacity

allocation.

Along with that, a significant effort should be done to improve the security of supply

of the energy resources from import, by growing the degree of their availability,

through long term consistent international arrangements and agreements, as wells by

diversification of energy sources, using Romania's key geographic location for the

transit of energy resources (natural gas, and oil) located in the Eastern part of the

Romania.

These objectives should be achieved in a functional market where energy

consumption and energy balance can only be streamlined under competitive terms.

10

Endorsing this vision, the Government of Romania, in its Energy Strategy, has

declared the further need of strengthening of the competitive energy market, as a top

priority for the energy sector.

III. ENERGY MARKET MODEL IN ROMANIA

11

The Strategy for Energy Sector and Energy Efficiency in Romania is based on

setting long - term objectives which are reflecting the needs of the National Economy

for:

- secure energy supply and safety

- energy efficiency,

- utilization of renewable energy sources

- environment protection.

In order to respond to the a.m. basic principles, in line with the “aquis” communautaire, the orientation of the energy structure and energy market model is towards a fully competitive market

The competitive market consists on:

- Bilateral, free negotiated contracts between internal producers and eligible

consumers or with other suppliers which will sell electricity to eligible consumers.

Eligibility will be increased step by step till the full opening of the market. On the

open market, eligible consumers, power suppliers and even the distribution

companies, have the opportunity to trade electricity by directly and freely

negotiated or by setting them on the spot market;

- negotiated contracts concluded by producers and self-producers with distribution

and supply companies;

- transaction on day ahead market.- export contracts, directly negotiated by the producer with the outside customers;

- for the network use, Romania has implemented the regulated third party access

both for transmission as well as for distribution, and related tariffs are published.

Both the existing and the new participants on the electricity market are equally

treated on a transparent and non-discriminatory basis, which also includes the

12

regulated access to the transmission and distribution networks. In this respect,

connection to the grids is compulsory public service.

At present the Romanian Wholesale Electricity Market (REM) is structured into two

parts:

A competitive market andA regulated market

The role of the regulated market is to assure correlated transactions between

producers and suppliers of captive consumers, corresponding to the final

consumption of the captive consumers. Prices on this regulated market are

established in order to cover costs and to include reasonable profit. The quantity of

electricity transacted on the regulated electricity market will diminish gradually, in line

with the market opening and the increase of competitive market.

On the regulated market, electricity is traded on regulated contract basis (with

regulated prices and regulated and usually firm quantities). The contracts concluded

on the regulated market are:

- portfolio contracts of main producers (firm quantities and prices established by the

regulator);

- contracts for electricity in cogeneration (quantities and regulated prices);

- long term contracts with regulated contracts, the “must run-must take” contract of

Nuclearelectrica, concluded for the whole output of nuclear power plant.

Considering the length of the contractual arrangements, REM (Romanian

Electricity Market) can be considered as a two-tire market:

13

- The first-tier of the market comprises (i) bilateral (regulated) contracts between

producers and D/S licensees; (ii) bilateral (negotiated) contracts between

producers and suppliers/eligible customers. During 2003-2004 period, the Initial

Contracts and Initial Option Contracts are to be developed, finalized and put in

place, in consultation with all relevant parties. From 2005 this contracts will replace

the actual portfolio contracts, and will have declining regulated quantities

established according to market opening (as of 2007 market will be fully opened)

After full opening of the market regulated energy prices will be applied only for the

consumers which are not exercising their right to go on the open market and will

prefer to stick with regulated tariffs.

- The second-tier the market comprises (i) Day-Ahead transactions which allow

producers, suppliers and D/S licensees to adjust their contractual positions

previously established in the “first-tier” of the market; (ii) Ancillary service

transactions between producers and the System Operator (Transelectrica); and

(iii) Real-time balancing transactions between the System Operator

(Transelectrica) and producers and/or suppliers. During 2003-2004 period, the

Market Operator (OPCOM) will design, pilot test and launch a “Power Exchange”

to accommodate all Day-Ahead transactions. The regulated production of

hydropower will be supplied on a non discrimination basis to all D/S licensees and

Suppliers through the “Power Exchange” (see Chapter VII hereunder). Also,

settlement of physical electricity sale/purchase transactions of the regulated

segment of the “first-tier” market and all transaction in the second-tier market will

be administered through the “Power Exchange”. When the OPCOM “Power

Exchange” will be commercially launched, it will be mandatory for all market

participants to handle short-term transactions through this “Power

Exchange”(2005-2007).

14

Starting with 2007 and onwards, the volumes in the Initial Contracts will be

reduced to a quantity corresponding to the acquisition need of the “Supplier of Last

Resort”. A key part of the rational for introducing a market for “capacity tickets” in

the OPCOM “Power Exchange” is to facilitate market liberalization by enabling D/S

licensees, Suppliers and Producers to adjust the volumes traded in bilateral

contracts while also meeting “Supplier of Last Resort” obligations as well as

stabilizing revenues for Producers.

The number of eligible consumer will increase under a pre-set schedule for opening

of the market reflecting the requirements of the EU Directive on Electricity.

15

IV. ENERGY POLICY IN ROMANIA

The safe, secure access and efficient functioning of the energy sector represents

the basic and vital millstone for the Romanian economy.

This is why a coherent and economically viable strategy for the energy filed, is a

fundamental prerequisite for the attainment of national objectives of a sustainable

growth and eradication of poverty.

IV.1 A COMPETITIVE ENERGY SUSTAINS A COMPETITIVE ECONOMY

For the past decade, radical institutional, regulatory and structural reforms are

being carried out allover the world with the main goal of deregulation that will improve

efficiency and quality of services.

The energy market model approach of Romania is based on the liberalization

(gradual opening) as an integral part of the overall philosophy of liberalization of the

national economy and free movement of goods and services.

The aim is to create such structures and market environment so that to respond

and cope with the increasingly integrated European energy market, where national

markets are step by step losing their traditional borders and are becoming part of a

common European market.

In the last three years, based on these trends, several important steps have been

already taken in Romanian energy sector, by implementation of a deregulation

process, based on the need of setting more market principles and free competition,

as well as by promoting a sustained privatization process.

In this respect the following have been achieved:

o Unbundling of the vertically integrated power companies into autonomous :

Generation, Transmission, Distribution and supply;

16

o Further unbundling of the generation side into: 5 thermal power producers, one

hydro producers, one nuclear producer and 14 cogeneration producers which

where transferred to the local authorities; there also three small IPP separated

in 1988;

o Unbundling of the natural gas sector into autonomous: Production and

Storage (Romgaz), Transmission (Transgaz) and two Distribution companies (Distrigaz North and Ditrigaz South)

o Reduction of the concentration of the natural gas production and import

by authorization and licensing to an increasing number of companies; o The regulated third party access, on a non discrimination bases to the

transmission system both for gas as well as for electricity has been secured by

law, in line with the trend in European Union;

o A decentralized market has been set up for long and medium term bilateral

contracts, supplemented by short term centralized markets initially compulsory

and on medium term becoming voluntary;

o In the year 1999 has been established the National Agency for Regulation for

Electricity (ANRE) and for Gas (ANRGN) in 2000, with the aim of creating

stable and transparent rules encouraging commercial activity and safeguarding

public interests, in accordance with the requirements of the EU Internal

Electricity Market Directive 96/92/EC for the establishment of an independent

regulatory body and of the Directive 98/30/CE of the European Parliament and

of the Council of 22 June 1998 concerning common rules for the internal

market natural gas;

o In the oil sector, necessary commercial frame has been established, and fixed

such as: a) wellhead prices track international prices; b)regulated tariffs for

crude oil transmission; c) consumer prices are set by the market; d) rules

preclude oil pipeline transmission assets and oil production, supply and refining.

17

o Regulatory intervention on certain market participants to ensure that all

customers are supplied with gas, including some groups which may be less attractive as clients (isolated locations, low users,…).

o A defined strategy for privatization and attraction of new investments.

Further actions should be taken in order to improve the specific issues, namely:

o Regulated prices in line with justified economic costs;

o Opening of the market with energy prices to be formed freely based on

competition and negotiation;

o A clear program for opening of the energy market. The opening the market

for energy will continue based on the following schedule:

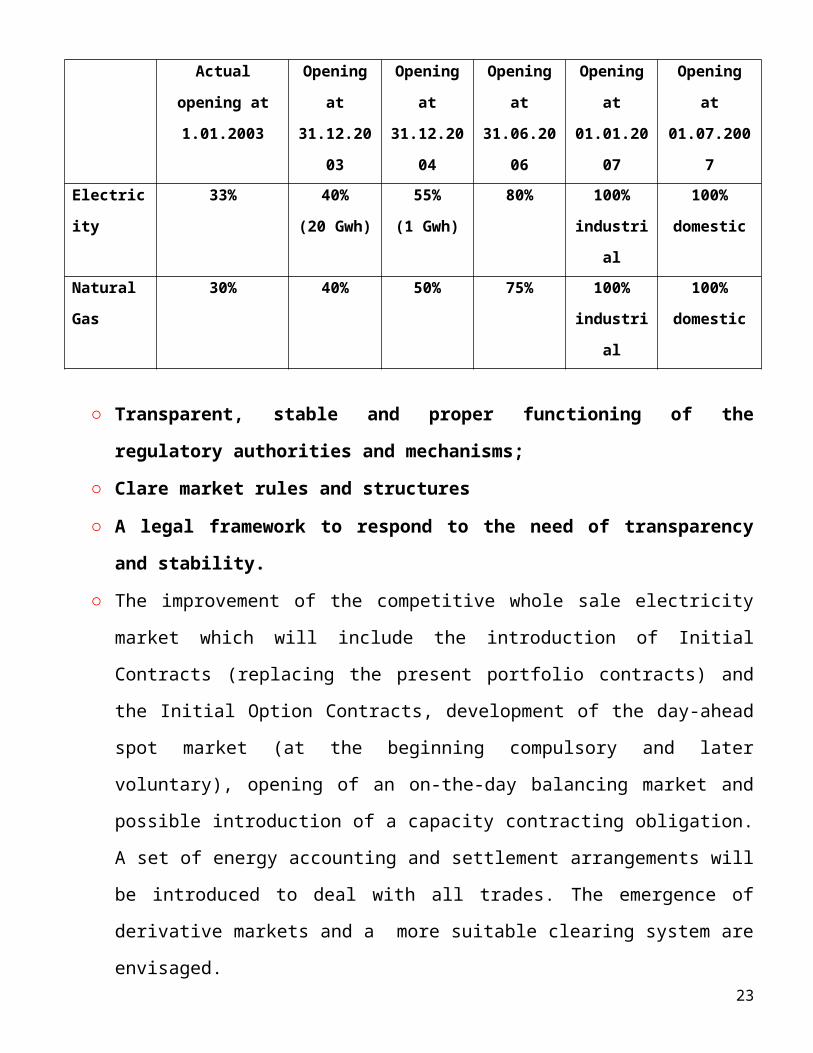

PROGRAM FOR OPENING OF THE MARKETS FOR ELECTRICITY AND NATURAL GAS

Actual opening at 1.01.2003

Opening at

31.12.2003

Opening at

31.12.2004

Opening at

31.06.2006

Opening at

01.01.2007

Opening at01.07.2007

Electricity 33% 40%(20 Gwh)

55%(1 Gwh)

80% 100%industrial

100% domestic

Natural Gas

30% 40% 50% 75% 100%industrial

100% domestic

○ Transparent, stable and proper functioning of the regulatory authorities and mechanisms;

○ Clare market rules and structures

○ A legal framework to respond to the need of transparency and stability.

○ The improvement of the competitive whole sale electricity market which will

include the introduction of Initial Contracts (replacing the present portfolio

contracts) and the Initial Option Contracts, development of the day-ahead spot

market (at the beginning compulsory and later voluntary), opening of an on-the-

day balancing market and possible introduction of a capacity contracting

obligation. A set of energy accounting and settlement arrangements will be 18

introduced to deal with all trades. The emergence of derivative markets and a

more suitable clearing system are envisaged.

○ The improvement of competition by the maintenance or improvement of the

quality of service to customers in terms of security and reliability.

○ The integration of the national power market into a prospective regional market

and a further integration in the Internal Electricity Market of the European Union.

Details of the proposed short, medium and long term transition and integration

schedule are shown in the attached Appendix nr.2 for electricity and Appendix.3 for

natural gas.

IV.2 ROLE OF THE REGULATORY BODIES AND OF THE MARKET OPERATORS

MAIN AREAS TO BE COVERED -By the establishment of a wholesale electricity and natural gas markets, the

captive consumers will continue purchasing energy from supply/distribution

companies that by virtue of their recognized right to monopoly in serving a designated

territory will remain subject to regulatory control.

-Transmission tariffs, as well as the distribution tariffs, are and will remain

regulated.

The transmission service will be provided only by natural monopolies, namely by

electric and gas transmission companies (Transelectrica, Transgaz).

-In the competitive retail market, where eligible customers have the opportunity to

choose their suppliers, the price for energy include a regulated component related to

the cost incurred by the transmission and distribution activities and, for natural gas, by

the underground storage. This component is paid to the relevant transmission and

distribution companies through regulated network access contracts.

- The methods of regulation will also become more complex and the impact of

regulatory decisions more significant at the stage of the forthcoming privatization in

the sector.

This is why the regulatory body both in electricity as well as in gas will continue to play an important role in the development and implementation of

19

the future market model. Detailed functions are shown in the Appendix nr.2 fo electricity and Appendix nr.3 foe gas.

Therefore, putting market structures in place will not diminish the significance and

functions of the regulatory body, but will rather lead to the transformation of their type.

In the market monitoring and dispute resolution the regulatory bodies will play a more

significant role.

The role of the Market Operators both in electricity and gas in the operation of the

wholesale power and gas markets will be reviewed and diversified, to be in line with

the power market liberalization and the increasing competition. This trend makes

necessary the implementation of functional physical and financial power exchange markets, to be operated by Market Operator.

Taking into consideration the proven experience and self-capacity to perform the

power and/or gas exchange functions, the Market Operators will play key role in the

development of the national and regional power trade.

ELECTRICITY MARKET OPERATOR – OPCOM

The electricity market operator OPCOM, is right now in a process of

implementation of new technical and commercial mechanisms for the electricity

market including some financial and commercial instruments, such as the clearing

house, sets of standard contracts to be implemented in the next future period, based

on an international qualified consultancy financed by Phare and World Bank. In the

Appendix nr.1 there is summary chart of all these instruments to be put in place which

will ensure the functionality of OPCOM’s power exchange function for the physical

power market (through two contracts, financed by the European Commission in Phare

2000 program and by the World Bank), as well as for the financial market (by the

Phare 2001 project financed by the European Commission and the Phare 2002

project co-financed by OPCOM and the European Commission).

20

The project developed under the Phare 2000 program is ongoing and consists in

the turnkey supply of an integrated IT system, covering equipment and dedicated

software applications, which will operate as the new IT trading platform for the

Romanian power market. The Phare 2002 program is aimed to implement the

exchange function for the financial power market administration, consisting in the

supply of an integrated IT system dedicated for this function (meaning both hardware

and specific software) and of a simulator of the financial market for training purposes.

These systems will be added with an information module dedicated to the short,

medium and long-term electricity demand forecast. The technical assistance will also

cover OPCOM’s institutional building aimed to ensure the implementation of the

exchange function for the financial power market, as well as the rules, regulations and

specific instruments for this market.

The project financed by the World Bank will be developed on long term, 2003 –

2007. The goal of the project is to provide a comprehensive consultancy and

assistance to OPCOM, in a twinning regime, through rules and regulations design for

the new power market, its testing and the Power Exchange design, pilot testing and

implementation. The consultant will ensure the correlation of the conceptual activities

involved in the design, testing and implementation of the new trading regime of the

Romanian power market. The most important function aimed for the twinning,

according to the new strategic vision to be developed for the Romanian power

market, is to provide technical assistance for the Electricity Market Coordination

Committee in its actions. Through the same project will provided the model for the

physical power market, as well as the updates of the IT system dedicated to the

physical market.

These implementations will allow to set up the Romanian power exchange, which is

aimed to become the regional South-East European market.

21

One of the new instruments will be the Long-Term Contracts (Initial or vesting

contracts)

The Long-Term Contracts (Initial Contracts or Regulated Multi-lateral Contracts)

are concluded between generators and suppliers, with firm quantities and profiled by

trading period.

The contracts will be put in place initially to stabilize electricity sale and purchase

transactions between the distribution companies (eight) and the producers, consistent

with GD 1524/2002 and would last around five years.

The volumes set in these contracts will be reduced each year, to encourage the

market participants to trade bilaterally with each other.

Due to the progressive reduction of the contracted volumes, a new trading

mechanism – the capacity market – will be set up and commissioned.

Prices will be also profiled and subject to quarterly indexation.

Hereunder is the scheme of the operation and place for the initial/vesting contracts.

These arrangements are considered as being the commercial solution able to

provide market stability and at the same time facilitate trading in an increasingly

competitive electricity market.

22

23

ANNEX AOVERVIEW

OPCOM’s projects by the allocation of the main tasks

PHYSICAL MARKET

IT: IT:

Vesting Contracts

Rules, Regulations SIMULATORPOWER EXCHANGE(settlement)

Capacity ContractsRules, Regulations SIMULATOR POWER EXCHANGE

Bilateral ContractsRules, Regulations SIMULATOR POWER EXCHANGE

(settlement)Hydro Regulation

Rules, Regulations SIMULATOR POWER EXCHANGESpot Market Day-Ahead

Rules, Regulations SIMULATOR

POWER EXCHANGE

AdjustmentRules, Regulations SIMULATOR POWER EXCHANGE

Balancing Market

Operated in the Day Ahead by the Market Operator, Horizon I Rules, Regulations SIMULATOR POWER EXCHANGEOperated in Real Time by the System Operator, Horizon II

Rules, Regulations

SIMULATOR

System Operator(DEN)

Phare 2000 – Investment (Alstom)

Including all contracts registration and settlement made for all trades

Twinning based consultancy - World Bank (including supply of the power market simulator and further software updating for the trading and settlement system, in accordance with the market evolution)

POWER MARKET COORDINATION

COMMITTEE

Phare 2002(Clearing implicitly)(With investment preparation under Phare 2001)

24

Ancillary Services

Rules, Regulations SIMULATOR

POWER EXCHANGE

Risks quotation and guarantee mechanisms (including clearing) Rules, Regulations SIMULATOR POWER EXCHANGE

FINANCIAL MARKET

Contracts: futures, options etc.Rules, Regulations PX

Clearing House Rules, Regulations PX

Forecast ModuleRules, Regulations IT

Phare 2002(Implicitly –with investment preparation under Phare 2001)

Phare 2001

LEGEND: - Phare Projects

- World Bank Project

Simulator for the financial market, for training purposes

Phare 2002(With investment preparation under Phare 2001)

25

26

GAS MARKET OPERATOR The role of the Gas Market Operator: The presence of a diversity of consumers (eligible and captive

consumers till full opening of the market, as well as of consumers, voluntarily

not exercising eligibility after full opening if the market) as well as temporary

presence of the mechanism of formation of “basket price”, requires the need

of a Market Operator in the natural gas sector.

Responsibilities:

Supervision of the ratio between purchases and sales, maintaining a non

discriminatory regime for all the players on the Romanian gas market;

Monitoring the interdependence between sources (domestic/import) –

parameters (flows, pressures, underground storage activity,

hourly/daily/seasonal fluctuations, peak demand-gas consumption):

Forecasting of the dynamics of gas demand on the Romanian gas market.

The development of competitive gas market and the possible

establishment of a gas “commercial market operator” (mirroring

developments in the electricity market) are under consideration.

27

To develop the system necessary for the operating and monitoring of gas

market, in order to control the interdependence between sources

(domestic/import) – parameters (flows, pressures, underground storage

activity, hourly/daily/seasonal fluctuations, peak demand-gas

consumption). This design should take into account the potential issues

connected with interoperability of the Romanian gas system with the gas

systems of EU Member States.

A blueprint for the development of the gas market in Romania, together

with a broad strategy for achieving this end.

To design the systems (hardware and software) necessary for the

operation of this developed gas market.

At this moment, it is under preparation the tender of the consultants for the

mentioned project.

It should review the external environment (such as social, legal, cross

border gas exchanges, commercial, economical and regulatory) which

impacts on the operations of TRANSGAZ / D.N.G.N.- O.P. and should review

the current design of gas market. This task requires close consultation with

ANRGN and an open dialog with other Romanian relevant gas market players

to develop a clear view of the present market operation (including a full

understanding of the deficiencies or difficulties in the operation of the present

market).

The output of this project will be a Task report setting out the consultants’

recommendations for the Operator and for the operating/monitoring

mechanisms to be used and their principles, function, proposed activities and

proposed operations to be performed by TRANSGAZ in order to ensure

interoperability with similar gas systems in EU member states.

In the same context , an IT system is necessary to provide and record the

data needed for the operating/monitoring the gas market, and processing it in

order to:

28

Select and analyze from a database (based on information about

supply/demand covering five year period) to estimate current gas demand

with high degree of accuracy; cross-checking against previous statistics

taking into account monthly/daily/hourly evolution of demand, related to

weather forecasted conditions;

Translate the current contractual agreements into an off take schedule to

give the suppliers the information they need to plan their operations;

Cover the whole spectrum of activities needed to match supply to the

projected demand;

Optimize the ratio between the levels of the current domestic production,

calling up the underground storage and the imported gas to cover peak

demand during winter time;

Programming and coordinating of maintenance work (routine or special)

and other activities on the system to ensure that they do not impact on the

security of gas supplies to customers.

The main objective is to develop of the gas market, to comply with the EU

Gas Single Market Directive and the consolidation and strengthening of the

gas market operator.

IV.3. INVESTMENT AND PRIVATIZATION THROUGH PRIVATE CAPTIAL PARTICIPATION AND STRATEGIC INVESTORS

NEED OF INVESTMENTS In order to upgrade the national energy system in Romania large-scale

investments are needed for upgrading, reconstruction, as well as for

expansion of the existing capacities and the construction of green field

capacities.

In despite of the efforts done in the generation sector, this sector is and will

be the mostly intensive investment sector to cover the target for upgrading as

29

well as for the new projects. It is very significant that for more than 5000MW in

the fossil fuel generation, the equipments are very old.

Overall summary picture in the energy sector is the following:

- In the electricity generation based on fossil fuel more than 32% of the

equipments are of more than 30 years of age, and 50% are between 20-30

years old. In this filed only 0, 7% are of less than 10 years old. In the hydro generation 24% of the equipments are of more than 30 years old, 51% of

more than 20 years old and only 13% are of more than 10 years old.

-In the Natural Gas Transmission System, 64% from the total length of

transmission pipelines are older than 25 years. Also, 29% of metering and

regulating stations have an overdue life span.

-The distribution networks operated by the main distribution companies

(S.C. DISTRIGAZ SUD Bucuresti and S.C. DISTRIGAZ NORD Targu Mures)

is in the same difficult situation: 46% of the distribution network is older than

15 years.

STRATEGY APPROACH FOR THE DEVELOPMENT OF THE POWER AND GAS SECTORS

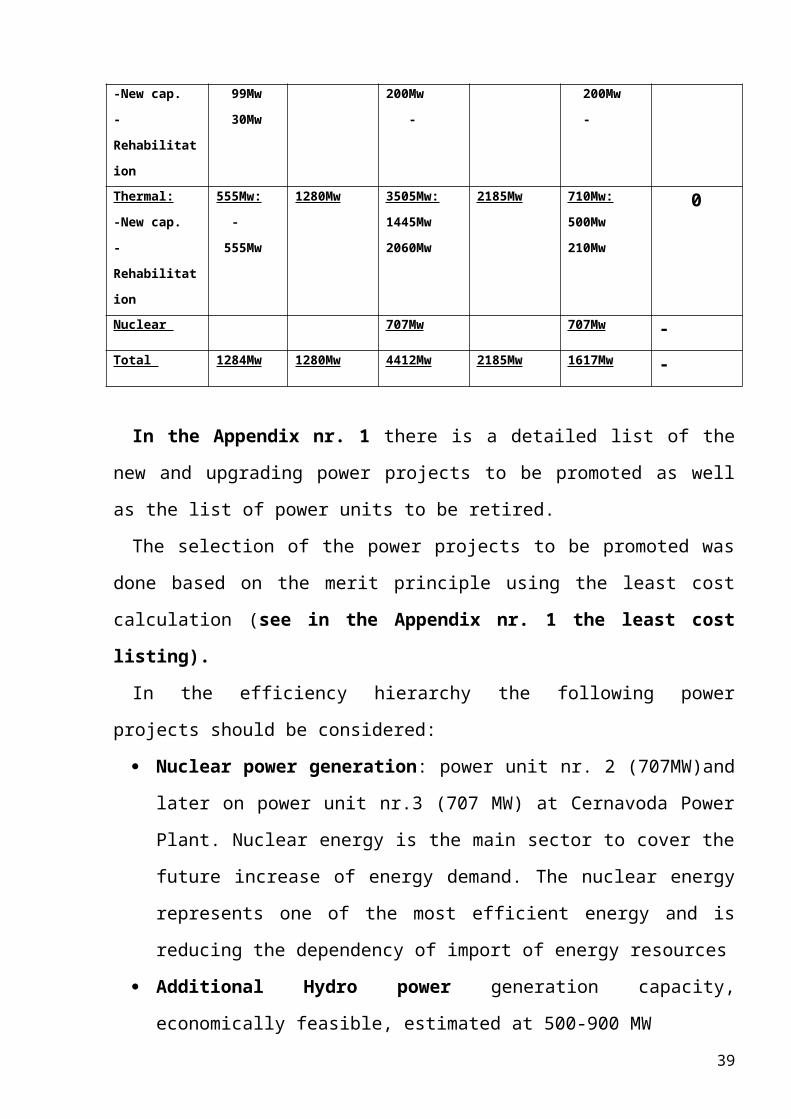

ELECTRICITY In the Appendix nr.1 hereunder, are determined the investments needed in

all power sectors, starting form the need of securing the energy supply.

The new capacities to be built are determined based on the parallel program

of the capacities to be retired,(see details in Appendix nr.1) the overall picture

is as follows:

In MW

30

Sector2003-2005 2006-2010 2011-2015

New capacities

Capacities to be retired

New capacities

Capacities to be retired

New capacities

Capacities to be retired

Hydro:-New cap. -Rehabilitation

129Mw: 99Mw 30Mw

- 200Mw:200Mw -

- 200Mw: 200Mw -

-

Thermal:-New cap. -Rehabilitation

555Mw: - 555Mw

1280Mw 3505Mw:1445Mw2060Mw

2185Mw 710Mw:500Mw210Mw

0

Nuclear 707Mw 707Mw -Total 1284Mw 1280Mw 4412Mw 2185Mw 1617Mw -

In the Appendix nr. 1 there is a detailed list of the new and upgrading

power projects to be promoted as well as the list of power units to be retired.

The selection of the power projects to be promoted was done based on the

merit principle using the least cost calculation (see in the Appendix nr. 1 the least cost listing).

In the efficiency hierarchy the following power projects should be

considered:

Nuclear power generation: power unit nr. 2 (707MW)and later on

power unit nr.3 (707 MW) at Cernavoda Power Plant. Nuclear energy is

the main sector to cover the future increase of energy demand. The

nuclear energy represents one of the most efficient energy and is

reducing the dependency of import of energy resources

Additional Hydro power generation capacity, economically feasible,

estimated at 500-900 MW

Power generation based on lignite and hard coal by rehabilitation of some of the existing power, where the upgrading costs are less

than 50% than for a new capacity and/or built of new units, at the

following locations: Turceni, Rovinari, Isalnita, Deva-Mintia. The

rehabilitation projects could represent 35-45% of the total newly needed

power generation capacity

31

Combined cycle gas turbines. Only 15% of the total power generation

will be secured form natural gas.

Hereunder is a brief presentation of the needed investments effort for the whole energy sector, as well as a tentative definition of investment

sources:

N.B. In the process of determination of the invesmtent sources it has been

firstly considered the private participation to the maximum realistical

expectation possible. Only the difference has been considered to be secured

from state company resources.

In million US$Sector 2003-2005 2006-2010 20111-2015 Total

Total,

out of

which

from:

Investment

sources

Total.

out of

which

from:

Investment

sources

Total,

out of

which

from:

Investment

sources

Private State

owned

comp.

Private State

owned

comp.

Private State

owned

comp.

Thermal

generation

1595 400 1195 1588 800 788 300 200 100 3485

Hydro

generation

450 100 350 500 150 450 660 300 360 1610

Nuclear

generation

480 - 480 1046 400 646 360 100 260 1886

Transmission 491 - 491 234 - 234 341 - 341 1266

Distribution* 628 428 200 727 727 - 885 885 - 2240

Total 3644 928 2716 4095 2077 2018 2764 1485 1261 10485

*Distribution companies will be privatized

The environment investment cost is estimated at 10% of the total investments effort.

The energy sector needs of investments should be fulfilled through the private equity participation to the maximum extend possible and feasible.

32

The ongoing reform and restructuring of the energy field has as main target

to become attractive and convincing for the private investors, so that most of

the necessary capital to flow from the foreign capitals, because of the limited

financial capacity within the country.

It is therefore important to promote an appropriate sequence of

investments, starting with the most viable projects, which could represent a

success story and encourage the investors, as well as a stable, and

transparent legal and regulatory frame work and appropriate market model

and structure. New contracting mechanisms as described in the attached road

map for regulation will be put in place to respond the expectations of the

investors and to limit the practice of long-term power purchase agreements

which should be promoted on a very selective base and only if they will not

break the EU Directives of "stranded cost" or "state aid".

The limited investment capacity of the state companies (direct financing or

sovereign guarantees) will be used in the next years only for those projects

(natural gas and power production and transmission), important for the

national system, but less attractive for foreign investors at this transition stage.

NATURAL GAS It has been also done an estimation of the need of investments in the gas

sector till the year 2010:In million US$

Sector 2003-2005 2006-2010 Total Total, out of which from:

Investment sources Total. out of which from:

Investment sources Private State

owned comp.

Private State owned comp.

For prospecting and drilling works for new wells out of which:-Romgaz-Petrom * -others

626

405191 30

221

191 30

405

405

620

280300 40

340

300 40

280

280

1.246

685491 70

For national transportation network

172 120 52 305 305 - 477

For distribution network *

910 910 - 1260 1260 - 2170

For underground storage

88 40 48 517 200 317 605

Total 1.796 1291 505 2.702 2105 597 4.498* Petrom and the two distribution companies will be privatized

33

The natural gas industry is facing two important targets for having secured

the supply of gas:

o Increase of the underground storage capacity so that during winter time

(high season) to secure necessary pressure and flow into the pipe line.

In this respect important steps where done by doubling the storage

capacity in 2003. Further steps and programs are foreseen so that the

storage capacity to be increased as follows:

Underground storage capacity in billion c.m.

2000 2003 2004 2005 2006 2007 2008 2009 2010

1,3 2,5 3,23 4.05 5.0 5.8 6,3 6,5 6,55

o Diversification of gas supply sources. In this respect there are foreseen

the following actions:

to interconnect the Romanian transportation pipe line network with

European network. The connection pipeline Szeged Arad is actually

under implementation.

to make access of the Caspian and Middle East gas to Europe. A

preliminary agreement has been signed between interested countries

i.e. Turkey, Bulgaria, Romania, Hungary and Austria. Based on this a

feasibility study, partially financed by EU, is conducted, by a

consultant already selected.

PRIVATIZATION The strategy of the Romanian Government is to speed up the path of the

privatization processes in the energy sectors.

The Romania Government strategy is to privatize:

all downstream activities in the electricity i.e. the 8 electricity distribution

companies, as well as in gas i.e. the two gas distribution companies;

power generation activities starting by the most feasible ones.

34

At this stage there are no planes for the privatization of the transmission

companies (TRANSELECTRICA and TRANSGAZ) as well as of the national

gas producer company ROMGAZ. Anyhow there is a strategy for private

access on the new gas fields and there already private companies operating

in new gas production.

The consolidation of the appropriate legal and regulatory environment and

market structures with stable and transparent rules helps and promotes the

privatization process in the energy filed. Therefore the Romanian Government

has set up clear path to be followed as described in the attachments herewith

though that through the reforms and regulation successfully implemented to

offer the investors confidence.

The main goal of the privatization is to get into to the company the

necessary capital and to strengthen the company rather than maximization of

the proceeds, so that to have stronger and more competitive companies after

privatization in gas and power sector, as well as to avoid unnecessary

increase on the tariffs. The privatization strategy should be subordinated to

the long-term objective of attaining competitive prices for energy.

In this view, it is foreseen to use the revenues generated through

privatization in the energy sector for financing of energy projects with a

considerable economic and social impact, as well as for related social costs,

for targeted support for low-income households, and for environmental

investments.

That is why the privatization will be based on the following:

Attraction of the investments necessary for ensuring efficient, secure and

environmentally-friendly energy supply; privatization will be pursued mainly

by attraction of private capital into equity combined with buying of an

additional package of shares of the companies;

Attraction of strategic investors in the utility field which will represent the

guarantee of successful operation based on a up-to-date management

systems;

35

The privatization process in the energy filed will be carried out to respond to

the objectives of:

Well-defined chronological sequence;

Ensuring the transparency of the process, using selected international

consultants;

Building of managerial capacity needed for the operation in a market

environment.

PRIVATIZATION PROGRAM The Romanian Government has approved a privatization program, as

follows:

For the electricity distribution at a rate of 2 distributions/year; this year will

be finalized the privatization of the Electrica Banat and Electrica Doborgea,

and for the year 2004 other two distribution companies are in the

privatization process; it has been signed the contract for selection of the

consultant so that the process is developing as planed.

For the two gas distribution companies, Distrigaz Nord and Distrigaz Sud,

consultancy contract has been signed and the privatization process has

started.

From the year 2000 until present, several private companies in the gas

sector (14 for natural gas distribution and one for underground storage)

have been established. All these companies have applied and obtained the

necessary licenses from ANRGN (see the Appendix 1 referring to

“Participants on natural gas market”).

Also in the gas filed till now were granted:

79 authorizations for initiation the setting up of natural gas

distribution;

51 authorizations for natural gas distribution operation;

40 licenses for natural gas distribution;

1 natural gas dispatching license;

36

42 licenses for natural gas supplying;

2 natural gas storage licenses;

1 natural gas transport license;

1 natural gas transit license.

Privatization of the thermal power generation will start with the most

attractive ones i.e.:

- Turceni, Roivnari plants (lignite based) for which, under USAID

program, consultancy program has been started, funded by

USAID

- Iernut gas power plant

For HIDROELECTRICA, uncompleted projects (21 projects) privatization is

foreseen to be partially finalized this year and next year before the full

opening of the market. There is also foreseen that HIDROELECTRICA will

be unbundled into commercial structures, and to be privatized, preferably

in packages with thermal power plants and their access on the market will

be permitted. Unbundling it is foreseen to be happened even earlier if

market forces will ask for such a decisions.

IV.4.PRICING POLICY AND SOCIAL PROTECTION

PRIECES AND TARIFF POLICYThe price and tariffs policy envisaged will be governed by economic

criteria. i.e. The energy prices (gas and electricity) are fixed:

o for eligible consumers by free negotiation based on competition, following the trend of opening of the market

o for captive consumers, prices are regulated in line with justified economic costs plus a margin pf profit;

o The tariffs for distribution and transmission are regulated in line with justified economic costs plus a margin pf profit;

o Cross subsidies will be abolished. o For the categories of people with social problems (low income), a direct

subsidy mechanism form the budget sources will be introduced.

37

PRICE AND TARIFFS - PAST DEVELOPMENTS

Electricity prices for the final consumers where constantly increased by 3,6% in the period October 2001- march 2002, and as of April 2002 the electricity prices where increased by 14% to cover cost variation due to inflation. In July 2002 the electricity prices where increased by 1,5%. In the period October 2002 January 2003 it has been applied a price adjustment to cover the inflation so that the prices to be constant in US$ at the level had in July 2002. In this frame the prices of Termoelectrica where increased at 39 $/Mw and for heat at 20 $/Gcal as of first of July 2002. The electricity prices at the consumers where differentiated as follows:

o 50,4$/Mwh for captive consumerso 46,7$/Mwh for industrial consumers o 64,1$/Mwh for household consumers

Heat prices (except cogeneration units): starting with September 2002 price regulation is done by the Authority for regulation of the Municipal services (ANRSC), which has been set up by the Government Decision 373/18.04.2002

Natural gas: As of 2002 the price of natural gas has been set up at 82,5$/1000 c.m. (the previous price was 45,12$/1000c.m. for household consumers and 85 $/1000 c.m. for industrial consumers). As of March 2003 the price level ahs been increased to 90 $/a000 c.m. and as of July 2003 at 99 $/1000 c.m. By this, all the costs form the gas producers to the downstream are covered.

FUTURE DEVELOPMENT

Due to need of investment expenditures for setting up new power generation capacities, upgrading the existing capacities including for coping with the environment protection requirements, it expected an increase in the electricity production cost. In the Appendix nr.1 there is a determination chart of the electricity costs for the period till the year 2015. On top of that should be added the financing cost as well as the expected profit of the investor. Depreciation cost (including for environment protection, fuel cost evolvement as per EU projections, labor and other variable cost, but also positive impact of new technologies on the production efficiency have been considered in the production cost projection. Based on this it expected that the cost of energy production to increase in the year 2005 by 10,3% compared to 2003, in the year 2010 by 13,3% compared to 2003, in the year 2015 by 13,8% compared to 2003.

The main features of each period can be summarized as follows: (implementation done in the previous period are no more repeated in the next period, being considered as fully valid).

2003 – 2004

38

For electricity:

The electricity prices for generators will be:

o formed freely based on competition and negotiation between the producers

and eligible customers;

o regulated, for captive consumers, as approved by the Regulatory Authority.

o ANRE will maintain the obligation of Electrica's subsidiaries to take over

the co generated electricity, (corresponding to the heat delivered to

residential consumers) at regulated prices.

o ANRE will transpose or adapt the methodologies of the EU Energy

Regulators Council regarding the cross border tariffication. From 2004 a

CBT (Cross Border Trade) mechanism will be in place in the Balkan

Region, similar to CBT mechanism already in place in Western Europe.

o Having in view the harmonization with the EU Directives, ANRE's

methodology for establishing regulated prices for acquisition of electricity

generated by IPPs and self producers will be extended in order to

purchase the electricity from renewable sources at regulated prices.

Taking into consideration high costs for generating this kind of electricity,

ANRE will study the possibility of subsidizing it by the state/local budget or

will define financial incentive scheme for renewable sources, according to

EU practice of electricity from renewable sources.

Transmission ad distribution tariffs:

Due to nature of these activates i.e. natural monopolies, both the transmission

and the distribution tariffs will be regulated tariffs based on the following

principles, which are giving more stability and transparency to the process:

39

Till the end of 2003, tariffs for transmission and distribution will be

regulated based on justified cost plus profit. By the end of 2003 will be

accomplished the evaluation of the assets of the distribution and

transmission companies' assets will be accomplished.

Based on the evaluation mentioned above, as well as based on a more

representative determination of the historic costs, the implementation of the

ROR (rate of return) mechanism will be done in 2004;

The target is to implement the “price cap” mechanism (CPI-X) index as of

2005.

Tariffs for ancillary services are regulated and are based on the involved

costs as submitted by the generators.

ANRE will determine a mechanism for internalization of the external cost for

environment protection.

The tariffs policy envisages that by the end of the transition period the

monomial end - user’s tariffs to be removed.

National uniform tariffs for captive consumers will be maintained.

Having in view the new structure in the electric electricity sector, for

transmission and distribution services, is intend to include as a new tariff

component, the contracted demand or contracted capacity.

For heat: the residential heat consumers will continue to pay a National

Reference price, which will be adapted in accordance with the gas/fuel oil

price. In parallel, municipalities will develop studies to optimize the heating

solutions for their community.

Low income residential heat consumers will continue to receive subsidies.

40

For natural gas : The domestic gas prices are adjusted in order to cover the production

costs and to provide financial resources for future investments. The

domestic gas prices are fixed:

o for eligible consumers by negotiation

o for captive consumers, domestic gas price is regulated (as

approved by ANRGN)

Transmission, distribution and storage tariffs , are regulated tariffs approved

by ANRGN and ANRM, and than published, and they are based on justified

costs plus profit.

ANRGN is implementing a new pricing and tariffication methodology,

differentiated by consumers’ categories, so that to remove the crossed

subsidies between consumers’ categories and to reflect the effective costs of

natural gas supplied toward each of these categories.

The implementation of this system has started in the year 2001, and is under

further implementation right now, and consists practically of two stages:

In the first stage where elaborated the “Criteria and methods for

establishing regulated prices and tariffs in natural gas sector”, which are the

necessary instruments for ANRGN to start the regulatory activity for prices

applied to the captive consumers.

In the second stage should be differentiate the prices and tariffs for the

consumers, pending on the application of the specific technical solutions for

each type of consumer. In this respect ANRGN has identified two key types

of consumers:

a) those one directly connected to the national transmission system;

b) those connected to the distribution systems.

For these two types of consumers differentiated tariffs are applied, related

to the service used.

41

Based on the a.m. principles, the gas prices ant the tariffs for transmission,

distribution and storage are fixed as follows:

1. Final price of gas to the consumer result from the addition of the

transmission, storage and distribution tariffs, commercial component, to

average weighted price for purchasing of gas, based on the following

formula:

Final price = P average weighted purchasing price + T transmission + + T storage +T distribution + C commercial

The average weighted purchasing price is determined by multiplying the

gas quantities from domestic production and from import with their prices and

after that by dividing the obtained value by total quantity, using the following

formula:

Q internal x P internal + Q import x P importQ internal + Q import

In order to benefit of the domestic gas, all consumers are obliged to pay the

ratio of the imported gas at the import price (or in case of eligible consumers

to buy directly this gas from import). The ratio structure of the domestic and

imported gas is established monthly, by Market Operator.

2. The designing principles for the tariffs for transmission, distribution are: tariff should reflect the cost of service (fix, variable) and investments

plus profit.

At present there are two types of tariffs in force, one for the consumers

connected in distribution systems and another for consumers connected

directly in national transmission system.

The differentiation of the distribution tariffs between categories of

consumers, according to the tariff methodology, will be realized started with

the year 2005.

The tariff methodology will be revised, during the second part of year 2003

first part of 2004 with PHARE assistance

42

3. The storage tariff is determined by allocating the average value of

underground storage service related to a storage cycle at the reserved

average capacity of storage deposit. In the storage tariffs are included

costs for services (fix, variable) and investments plus profit.

The storage tariffs have been established as differentiated service tariffs for

each underground deposit, giving up the system post stamp “storage tariff”.

This has opened the access for eligible consumers to underground storage

systems.

Storage tariff has also a component for reserving capacity, a component

related to injection cycle and one related to extraction cycle for natural gas

from the storage deposit.

4. In order to encourage private producers of gas, by the Government

Decision approved in February 2003, for promoting of the exploration and

production of new domestic gas, establishes that the price for new

domestic gas to be at the level of up to 80% of the imported gas price at

Romanian border.

For the protection of low income residential consumers, the social tariff will be

maintained.

2005-2007

FOR ELECTRICITY:

An increase in real terms for end-users tariffs is estimated due to the

obligation of including environmental costs in the tariff structure

(internalization of externalities), according to the legislation and due to the

necessity of adequate investments for all electricity market participants.

43

The electricity prices: Electricity prices for the consumers exercising the eligible status will be

negotiated.

Despite the totally opening of the market, there will be residential and small

industrial end-users which will prefer to be supplied at regulated prices

through specific mechanisms. For these categories regulated prices will be

maintained. The suppliers selling electricity to these consumers are named

“Suppliers of Last Resort”.

During this period, ANRE will gradually reduce the obligation of the

electricity distribution/supply companies to take over electricity generated

in co-generation power plants, correlated with the results of studies and

programs for rehabilitation, modernization of and investments in systems

supplying heat to residential consumers. If the Directive on the promotion

of the electricity produced in co-generation units (CHP) will be adopted by

EU, a suitable mechanism will be put in place.

Transmission and distribution tariffs:

Due to nature of these activates i.e. natural monopolies, both the

transmission and the distribution tariffs will be regulated tariffs based on the

following principles, which are giving more stability and transparency to the

process:

The tariffication principles will be a the “price-cap” (CPI-X)

mechanism both for distribution and transmission activities.

The social tariff will be maintained, and in parallel a mechanism for direct

budget subsidy system of low income people will be defined and

implemented.

Fore heat: For residential heat consumers it is expected that the results of

the studies aimed to establish the optimal heating solution for each community

to be implemented and in a parallel program for reduction of the subsidies.

44

During this period the residential heat consumers will continue to pay a

National Reference Tariff, but the necessity to maintain it will be reviewed.

For cogeneration will result an obligation to purchase the energy, for which

specific mechanisms should be put in place.

Low income heat consumers will receive direct subsidies.

FOR NATURAL GAS

As of 2007 the market will be fully opened.

The domestic gas prices are fixed:

o for eligible consumers by negotiation

o for captive consumers, and for the consumers not exercising the

eligibility, domestic gas price is regulated (as approved by ANRGN)

Transmission and storage tariffs, are regulated tariffs approved by ANRGN

and ANRM, and than published, and they are based on justified costs plus

profit, and for distribution will be the “price-cap” (CPI-X) mechanism.

Until 2007, is estimated a gradual increase in natural gas end-users’ price

in order to be aligned to the wellhead import price.

In this stage of implementation of the prices and tariffs, ANRGN aims to

further differentiate the distribution tariffs for categories consumers supplied

from distribution systems.

The tariff for transmission services will remain unique at the national level,

“post stamp” type.

45

2008-2015

FOR ELECTRICITY:

The electricity prices: Electricity prices for the consumers exercising the eligible status will

be negotiated.

Despite the totally opening of the market, there will be residential and

small industrial end-users which will prefer to be supplied at regulated

prices through specific mechanisms. For these categories regulated prices

will be maintained. The suppliers selling electricity to these consumers are

named “Suppliers of Last Resort”.

During this period, ANRE will gradually reduce the obligation of the

electricity distribution/supply companies to take over electricity generated

in co-generation power plants, correlated with the results of studies and

programs for rehabilitation, modernization of and investments in systems

supplying heat to residential consumers. If the Directive on the promotion

of the electricity produced in co-generation units (CHP) will be adopted by

EU, a suitable mechanism will be put in place.

Transmission and distribution tariffs:Due to nature of these activates i.e. natural monopolies, both the

transmission and the distribution tariffs will be regulated tariffs based on the

following principles, which are giving more stability and transparency to the

process:

The tariffication principles will be the price-cap (CPI-X) mechanism

both for distribution and transmission activities and for distribution will

be the “price-cap” (CPI-X) mechanism

The social protection for low income consumers will be implemented by a

direct subsidy mechanism form the budget.

46

For heat, pending on the decision to continue the National reference price

system, in the invoice for each consumer will be reflected the cost of heat

based on a regulated price to be approved by the Regulatory Authority.

Low income heat consumers will receive direct subsidies.

For natural gasAs of 2007 the market is fully opened.

The domestic gas prices are fixed:

o -for eligible consumers by negotiation

o -for the consumers not exercising the eligibility, domestic gas price is

regulated (as approved by ANRGN)

Transmission, and storage tariffs are regulated tariffs approved by ANRGN

and ANRM, and than published, and they are based on justified costs plus

profit. In this stage for implementing the tariffs and prices system for

natural gas, ANRGN aims to differentiate the transmission tariff according

to the distance and the transported natural gas volume, and the distribution

tariffs according to the distribution zone covered by the operator.

47

BILL COLLECTION

Improvement of the energy bill collection

In the last two years it was recorded an important improvement of the bill

collection rate. In this respect the Government and the companies have taken

a serious approach by specific measures such:

A firm disconnecting program form power supply for the consumers not

paying the bills not

A clear program for recovery of the overdue, including the rescheduling

of the debts as well as:

the “escrow” accounts where payments for the heat as well state

subsidies are accumulated and than automatically distributed to

the distribution companies

an incentive instrument to pay the bills: such as rescheduling of

the old debts subject of paying the current bills and a forgiving

mechanism for the penalties of late payment in case the

customers follows the payment schedule;

A monthly monitoring program

As a consequence of this measures the collection rate has been significantly

improved: in the last twelve months (June 2002 – June 2003) to 94% for

electricity and to 97% for natural gas.

CONSULTANCY ASSISTANCE

In view of the implementation of these policies it will be needed the support of the EU as well as of international financial institutions, for implementation of the specific tasks with the participation of the specialized consultancy companies.

48

V. ENVIRONMENT

Romania has ratified the UN Framework Convention on Climate Changes.

In accordance with the Kyoto Protocol signed, Romania made the

commitment to reduce anthropogenic emissions of greenhouse gases by 8%

compared to the emissions of 1989 emissions level.

For the implementation of EU Directive 2001/80/Ec, The Romania

Government has prepared a draft of Government Decision for the limitation of

the emissions in the atmosphere coming from big power units i.e. over 50

MW, at the level of the EU Directives (for solid, SO2 and NOX emissions).

These limits are compulsory for any new unit to be implemented.

For the existing units in operation it is foreseen to achieve the required level

of emission in a gradual program so that by the year 2012 to cope with the

level of emission provided in the new regulation, by implementing a very

important investment program.

For the power plants in the structure of Termoelectrica, the total investment

effort for the period 2003 -2015 is estimated at the level of 1,026 billion $, out

of which 28,9% should be spend till the year 2007. The investment for

upgrading of the boilers and electro precipitator (solid emission) represents

8% of the total amount, for upgrading of the burners represents 6%, and for

desulphurization represents 86% of the total amount. EU and Word Bank financial support is needed to help Romania to comply with EU’s standards.

49

The result of the implementation of this program for the plants in the

structure of Termoelectrica is reflected in a significant reduction of the emissions, as

follows:

Emission 1989 2007 2012

SO2t/year 645.546 265.649 56.623

% compared to

1989

100 41% 8.8%

NOXt/year 112.152 62.125 56.386

% compared to

1989

100 55 50

Solidt/year 139.064 16.836 8.836

% compared to

1989

100 12 6

50

VI. RESTRUCTURING OF THE POWER GENERATION SECTOR AND THE MARKET OPERATION

As mentioned above the process of restructuring of the electricity and gas sector has started by: Unbundling of the vertically integrated power companies into autonomous :