HYDROGEN ENGINE CENTER, INC. (Nevada)

28

1 ANNUAL FINACIAL REPORT Pursuant to Rule 15c2-11(a)(5) For For HYDROGEN ENGINE CENTER, INC. (Nevada) 1548 Brickell Ave.3 rd Floor Miami, FL 33129 (305)781-3300 www.hectina.net [email protected] For the Year Ended December 31, 2020 Dated: September 26, 2021 Further data to comply with the Basic Disclosure Guidelines Federal securities laws, such as Rules 10b-5 and 15c2-11 of the Securities Exchange Act of 1934 (“Exchange Act”) as well as Rule 144 of the Securities Act of 1933 (“Securities Act”), and state Blue Sky laws, require issuers to provide adequate current information to the public markets. With a view to encouraging compliance with these laws, OTC Markets Group has created these OTC Pink Basic Disclosure Guidelines. We use the basic disclosure information provided by OTC Pink companies under these guidelines to designate the appropriate tier in the OTC Pink marketplace: Current, Limited or No Information. OTC Markets Group may require companies with securities designated as “Caveat Emptor” to make additional disclosures in order to qualify for OTC Pink Current Information tier.

Transcript of HYDROGEN ENGINE CENTER, INC. (Nevada)

1

ANNUAL FINACIAL REPORT Pursuant to Rule 15c2-11(a)(5) For

For

HYDROGEN ENGINE CENTER, INC. (Nevada)

1548 Brickell Ave.3rd Floor Miami, FL 33129 (305)781-3300

www.hectina.net [email protected]

For the Year Ended December 31, 2020

Dated: September 26, 2021

Further data to comply with the Basic Disclosure Guidelines

Federal securities laws, such as Rules 10b-5 and 15c2-11 of the Securities Exchange Act of 1934 (“Exchange Act”) as well as Rule 144 of the Securities Act of 1933 (“Securities Act”), and state Blue Sky laws, require issuers to provide adequate current information to the public markets. With a view to encouraging compliance with these laws, OTC Markets Group has created these OTC Pink Basic Disclosure Guidelines. We use the basic disclosure information provided by OTC Pink companies under these guidelines to designate the appropriate tier in the OTC Pink marketplace: Current, Limited or No Information. OTC Markets Group may require companies with securities designated as “Caveat Emptor” to make additional disclosures in order to qualify for OTC Pink Current Information tier.

2

HYDROGEN ENGINE CENTER, INC. (Nevada)

Table of Content

Item 1. Name and address of the issuer

Item 2. Security Information

Item 3. Issuance History

Item 4. Financial Statements

Item 5. Issuer’s Business, Products and Services

Item 6. Issuer’s Facilities

Item 7. Company Insiders (Officers, Directors, and Control Persons)

Item 8. Legal/Disciplinary History

Item 9. Third Party Providers

Item 10. Issuer Certification

3

HYDROGEN ENGINE CENTER, INC. (Nevada)

ANNUAL REPORT

FOR THE YEAR ENDED DECEMBER 31, 2020 All information contained in this report has been compiled to comply with the disclosure requirements of Rule 15c2-11(a)(5) promulgated under the Securities and Exchange Act of 1934, as amended (the "Exchange Act"). The bullet points contained herein conform to the sequential format set forth in the Rule. No dealer, salesperson or other person has been authorized to give any information or make any representations in connection with the Issuer that are not contained herein. Any representations not contained herein should not be relied upon as having been made or authorized by the Issuer. The transmission of this information does not imply that the information contained herein is correct as of any date after the date of this Report. As of the current reporting date, the number of shares outstanding of our Common Stock:

53,018,563

As of the prior reporting date, the number of outstanding shares of our Common Stock:

53,018,563

As of the fiscal 2020 end date, the number of outstanding shares of our Common Stock was:

53,018,563

Indicate by check mark whether the Company is a shell company (as defined in Rule 405 under the Securities Act of 1933 and Rule 12b-2 under the Exchange Act of 1934):

Yes: ☐ No: ☒

Indicate by check mark whether the company’s shell status has changed since the previous reporting period:

Yes: ☐ No: ☒

Indicate by check mark whether a Change in Control of the company has occurred over this reporting period:

Yes: ☐ No: ☒

Item 1. Name and address of the issuer

Hydrogen Engine Center 548 Brickell Ave.3rd Floor Miami, FL 33129

4

State in which the issuer and each of its predecessors (if any) has been incorporated or registered within the last five years. Please also include the issuer’s current standing in its state of incorporation (e.g., active, default, inactive):

Active

Describe any trading suspension orders issued by the SEC concerning the issuer or its predecessors since inception:

None List any stock split, stock dividend, recapitalization, merger, acquisition, spin-off, or reorganization either currently anticipated or that occurred within the past 12 months:

None The address(es) of the issuer’s principal executive office:

1548 Brickell Ave.3rd Floor Miami, FL 33129 The address(es) of the issuer’s principal place of business:

Check box if principal executive office and principal place of business are the same address: ☒

Has the issuer or any of its predecessors been in bankruptcy, receivership, or any similar proceeding in the past five years?

Yes: ☐ No: ☒ Security Information Trading symbol: HYEG Exact title and class of securities outstanding: HYDROGEN ENGINE CENTER Inc (Nevada) CUSIP: 448876102

Par or stated value: 0,001

Total shares authorized: 100,000,000 as of date: 07/01/2021 Total shares outstanding: 53,018,563 as of date: 07/01/2021 Number of shares in the Public Float1: 11,228,669 as of date: 07/01/2021 Total number of shareholders of record: 214 as of date: 07/01/2021

5

All additional class(es) of publicly traded securities (if any): Trading symbol: HYEG Exact title and class of securities outstanding: Common CUSIP: 448876102 Par or stated value: 0,001 Total shares authorized: 100,000,000 as of date: 07/01/2021 Total shares outstanding: 53,018,563 as of date: 07/01/2021 Transfer Agent Interstate Transfer Company, 1671 Rycroft PL, Suite C, Salt Lake City UT, 84124 (phone number: (801) 414-3928), is registered under the Exchange Act. Due to health issues of our Transfer Agent HEC has planned to hire a new transfer Agent Restrictions on Transfer of Securities: A majority of the "HEC" shares (41,789,894) have not been registered under the U.S. Securities Act of 1933, as amended (the "Securities Act"), and the shares will be "restricted securities" under Rule 144 promulgated under the Securities Act ("Rule 144"). Under applicable rules, this restriction may not be lifted for holders of Restricted Shares until HEC has filed all periodic reports required to be filed with the Securities and Exchange Commission Exchange Commission ("SEC") during the 12 months prior to the date of resale by the shareholder. The Transfer Agent has been registered under the Exchange Act Yes: ☒ No ☐ Issuance History A. Changes to the Number of Outstanding Shares

Check this box to indicate there were no changes to the number of outstanding shares within the past two completed fiscal years and any subsequent periods: ☒

B. Debt Securities, Including Promissory and Convertible Notes

Check this box if there are no outstanding promissory, convertible notes or debt arrangements: ☒ ITEM 4. Financial Statements A. The following financial statements were prepared in accordance with:

☒ U.S. GAAP ☐ IFRS

B. The financial statements for this reporting period were prepared by (name of individual):

Name: Pedro Blach Title: CEO Relationship to Issuer: CEO

6

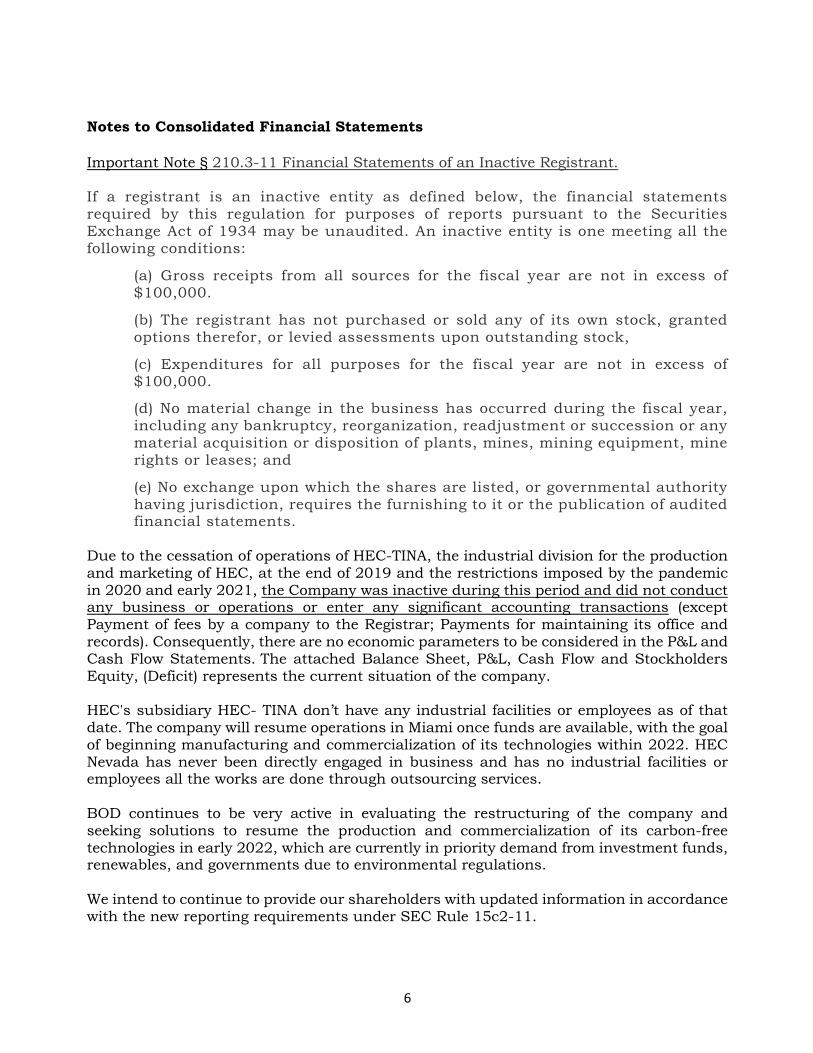

Notes to Consolidated Financial Statements

Important Note § 210.3-11 Financial Statements of an Inactive Registrant. If a registrant is an inactive entity as defined below, the financial statements required by this regulation for purposes of reports pursuant to the Securities Exchange Act of 1934 may be unaudited. An inactive entity is one meeting all the following conditions:

(a) Gross receipts from all sources for the fiscal year are not in excess of $100,000.

(b) The registrant has not purchased or sold any of its own stock, granted options therefor, or levied assessments upon outstanding stock,

(c) Expenditures for all purposes for the fiscal year are not in excess of $100,000.

(d) No material change in the business has occurred during the fiscal year, including any bankruptcy, reorganization, readjustment or succession or any material acquisition or disposition of plants, mines, mining equipment, mine rights or leases; and

(e) No exchange upon which the shares are listed, or governmental authority having jurisdiction, requires the furnishing to it or the publication of audited financial statements.

Due to the cessation of operations of HEC-TINA, the industrial division for the production and marketing of HEC, at the end of 2019 and the restrictions imposed by the pandemic in 2020 and early 2021, the Company was inactive during this period and did not conduct any business or operations or enter any significant accounting transactions (except Payment of fees by a company to the Registrar; Payments for maintaining its office and records). Consequently, there are no economic parameters to be considered in the P&L and Cash Flow Statements. The attached Balance Sheet, P&L, Cash Flow and Stockholders Equity, (Deficit) represents the current situation of the company. HEC's subsidiary HEC- TINA don’t have any industrial facilities or employees as of that date. The company will resume operations in Miami once funds are available, with the goal of beginning manufacturing and commercialization of its technologies within 2022. HEC Nevada has never been directly engaged in business and has no industrial facilities or employees all the works are done through outsourcing services. BOD continues to be very active in evaluating the restructuring of the company and seeking solutions to resume the production and commercialization of its carbon-free technologies in early 2022, which are currently in priority demand from investment funds, renewables, and governments due to environmental regulations. We intend to continue to provide our shareholders with updated information in accordance with the new reporting requirements under SEC Rule 15c2-11.

7

Note 1 Principles of Consolidation - The consolidated financial statements include the accounts of Hydrogen Engine Center, Inc. (Nevada) and its wholly owned subsidiary HEC-TINA, Inc. All significant intercompany balances and transactions have been eliminated in consolidation.

Note 2 Revenue and Expense Recognition – Hydrogen Engine Center, Inc. and Subsidiaries (The “Company”) recognize revenues and expenses for both financial reporting and income tax reporting purposes in accordance with the accrual method of accounting. For custom manufactured items, any customer deposits are reflected in the balance sheet and costs related to the manufacturing are included in work in process inventory. Once the item is completed and shipped, deposits and corresponding work in process costs are recognized in the statement of income.

Note 3 Cash and Cash Equivalents – For purposes of the consolidated statement of cash flows, the Company considers all highly liquid debt instruments purchased with a maturity of three months or less to be cash equivalents. The company has no cash equivalents at the consolidated balance sheet date.

Note 4 Inventories – Inventory consists mainly of parts, components, and work in progress on fully equipped modular units, engines, and generator sets. Capitalized costs associated with work in progress inventory include parts and components used, direct labor and outside services. Due to the very limited amount of production work performed, the Company did not capitalize fixed production overhead items into work in progress. Inventory is recorded at the lower of cost or market under the first-in, first-out (FIFO) method.

Note 5 Property and Equipment – Property and equipment are recorded at cost less accumulated depreciation. The Company has a capitalization policy which requires capitalization of items with a cost of $2,000 or greater and an estimated useful life of three years or more. Items that do not meet that criterion are expensed. Depreciation for financial reporting purposes is computed using the straight-line method and for tax reporting purposes is computed using straight-line and accelerated methods. Repairs and maintenance costs are expensed unless the repair significantly extends the useful life of the asset it is related to. In such cases, the repair cost will be capitalized and depreciated over the extended useful life.

The Company has been building hydrogen fueled engines since 2003. In 2004 the Company added engine controls and then combined these two technologies to build generator sets. Hydrogen Engine Center (HEC) was developed with the objective of producing distributive power, for industrial clients, fueled by alternative fuels, such as hydrogen, natural gas, anhydrous ammonia, methanol, propane, syn-gas, landfill gas and other alternative fuels.

Note 6 Income Taxes – Income taxes are provided for the tax effects of transactions reported in the consolidated financial statements and consist of taxes currently due plus deferred taxes related primarily to differences between the basis of property and equipment, inventories, investments, intangibles, and deferred compensation for financial and income tax reporting. The deferred tax assets and liabilities represent the future tax return consequences of those differences, which will either be taxable or deductible when the assets and liabilities are recovered or settled. Deferred taxes also are recognized for

8

operating losses that are available to offset future taxable income and tax credits that are available to offset future federal income taxes. Current and deferred income taxes are presented for each individual entity in the consolidated statement of earnings and are based upon actual income or loss generated by those entities and the temporary timing differences that are unique to each. In accordance with current accounting standards, tax years 2010, 2011, 2012, 2013, 2014, 2015 ,2016,2017, 2018 and 2019 are currently open for examination from Federal and state taxing authorities.

Due to continuing operating losses, there is no current provision for income taxes recorded in the financial statements.

The Company has cumulative Federal net operating loss carryforwards of approximately $17,800,000 as of September 30, 2019, which are used to offset future taxable income. Federal net operating losses may be carried forward twenty years from the year they were incurred. Unused losses expire after the carryforward period. The Company’s net operating losses on September 30, 2017, expire beginning in 2023 through 2037. The Company has a Federal general business credit carryforward of $178,154. Internal Revenue Code allows the unused portion of the credit to be carried forward for twenty years. This credit will begin expiring in 2025.

Management assesses the available positive and negative evidence to estimate whether sufficient future taxable income will be generated to permit use of existing deferred tax assets. A significant piece of objective negative evidence evaluated was the cumulative loss incurred over the company’s history. Based on this analysis, management believes that it is more likely than not that the company will not be able to utilize all of its deferred tax assets. Therefore, a full valuation allowance against deferred tax assets has been set up.

Uncertain tax positions must be recorded in accordance with ASC 740 based on a two-step process in which management determines it is more likely than not that the tax position will be sustained based on the technical merits of the position. Then, for tax position that meet the more likely than not threshold, the company must recognize the largest amount of tax benefit that is more than 50% likely to be realized upon ultimate settlement with tax authorities. Management has evaluated all tax positions and determined there are no uncertain tax positions taken.

Note 7 Earnings (loss) per Share

Earnings (loss) per common share have been computed based on dividing net earnings (loss) by the weighted-average number of shares of common stock outstanding. Diluted earnings (loss) per common share, which would include the effect of vested stock options have not been presented since the vested shares would be anti-dilutive in a situation where the Company is generating a loss. Earnings (loss) per common share are presented on the consolidated statement of earnings (loss).

Note 8 Use of Estimates - In preparing the consolidated financial statements, management is required to make estimates and assumptions that affect the reported amounts of assets and liabilities as of the statement of condition dates and revenues and expenses for the periods shown. Actual results could differ from the estimates and assumptions used in the consolidated financial statements. Material estimates that are particularly susceptible to significant change in the near term relate to the determination

9

of the allowance for loan losses, the valuation of foreclosed real estate, and deferred tax assets.

Note 9 Shipping and Handling – Common carrier cost for products received are included in cost of goods sold. The Company provides its own truck fleet for the delivery of product to customers. These costs are included in operating expenses. Freight cost is billed to the customer for products delivered.

Note 10 Accounts Receivable – Payment terms on accounts receivable are ordinarily net ten days from invoice. The Company performs credit evaluations on customers and typically does not require collateral from its customers. Advanced deposits for custom projects may be required depending on the customer. An allowance for doubtful accounts is based upon an analysis of aged accounts receivable for current collectability and historical trends. Management periodically reviews this allowance and adjustments are made as necessary. Accounts deemed uncollectible are charged off against income in the period when that determination is made. Currently, the Company does not have any accounts receivable as of August 30, 2021, and, therefore, has not established an allowance for doubtful accounts.

Note 11 Employee Stock Compensation Plan - Generally accepted accounting principles in the United States of America Codification Section 718 requires an entity to measure the cost of employee services received in exchange for an award of equity instruments based on a grant-date fair value of the award (with limited exceptions). That cost will be recognized over the period which an employee is required to provide service in exchange for the award – the requisite service period.

The Company has determined the estimated fair value of stock options at grant date using the Black-Scholes option- pricing model based on market data as of February 21, 2019, the expected dividend yield of 0.0% and expected volatility ranges from 80.34% - 223.06% were used to model the values. The risk-free rate of return ranges from 0.17% - 1.98%, which was based on the yield of a U.S. Treasury note with a term of ten years. The expected life of the stock options ranges from 5.50 - 6.50 years depending upon vesting period.

The Company maintains stock-based benefit plans under which certain employees and directors are eligible to receive restricted stock grants or options. Under the 2015 Stock-Based Benefit Plan, the maximum number of 8,000,000 shares may be issued through the exercise of stock options. The exercise price of each option equals the market price of the Company’s stock on the date of grant and an option’s maximum contractual term is ten years.

Note 12 Research and Development Costs – The Company incurs costs associated with research and development activities related to the design and building of a hydrogen fuel engine. Research and development costs are expensed in the period they are incurred.

NOTE 13 – Recent Accounting Pronouncements

In February 2016, FASB issued ASU 2016-02, Leases (Topic 842). The new standard requires lessees to apply a dual approach, classifying leases as either finance or operating leases based on the principle of whether the lease is effectively a financed purchase by the lessee. This classification will determine whether lease expense is recognized based on an

10

effective interest method or on a straight-line basis over the term of the lease. A lessee is also required to record a right-of-use asset and a lease liability for all leases with a term of greater than 12 months regardless of their classification. Leases with a term of 12 months or less will be accounted for similar to existing guidance for operating leases. The new guidance will be effective for annual reporting periods beginning after December 15, 2018, including interim periods within that reporting period and is applied retrospectively. Early adoption is permitted. We are currently in the process of assessing the impact the adoption of this guidance will have on the Company’s consolidated financial statements.

In May 2014, the FASB issued ASU No. 2014-09, “Revenue from Contracts with Customers” (Topic 606) (ASU 2014-09), which supersedes the revenue recognition requirements in ASC Topic 605, “Revenue Recognition”, and most industry- specific guidance. ASU 2014-09 is based on the principle that revenue is recognized to depict the transfer of goods or services to customers in an amount that reflects the consideration to which the entity expects to be entitled in exchange for those goods or services. ASU 2014-09 also requires additional disclosure about the nature, amount, timing and uncertainty of revenue and cash flows arising from customer contracts, including significant judgments and changes in judgments and assets recognized from costs incurred to obtain or fulfill a contract. The amendments in ASU 2014-09 will be applied using one of two retrospective methods.

Subsequently, the FASB has issued the following standards related to ASU 2014-09: ASU No. 2016-08, Revenue from Contracts with Customers (Topic 606): Principal versus Agent Considerations (ASU 2016-08); ASU No. 2016-10, Revenue from Contracts with Customers (Topic 606): Identifying Performance Obligations and Licensing (ASU 2016-10); and ASU No. 2016-12, Revenue from Contracts with Customers (Topic 606): Narrow-Scope Improvements and Practical Expedients (ASU 2016-12). The Company must adopt ASU 2016-08, ASU 2016-10 and ASU 2016-12 with ASU 2014-09 (collectively, the new revenue standards). The effective date will be the first quarter of our fiscal year ended March 31, 2018. We have not determined the potential effects on our consolidated financial statements.

In March 2016, the FASB issued ASU No. 2016-09, Compensation – Stock Compensation (Topic 718): Improvements to Employee Share-Based Payment Accounting (ASU 2016-09), which simplified certain aspects of the accounting for share- based payment transactions, including income taxes, classification of awards and classification on the statement of cash flows. ASU 2016-09 will be effective for the Company beginning in its first quarter of 2018. The Company is currently evaluating the impact of adopting ASU 2016-09 on its consolidated financial statements.

In January 2016, the FASB issued ASU No. 2016-01, Financial Instruments – Overall (Subtopic 825-10): Recognition and Measurement of Financial Assets and Financial Liabilities (ASU 2016-01), which updates certain aspects of recognition, measurement, presentation, and disclosure of financial instruments. ASU 2016-01 will be effective for the Company beginning in its first quarter of 2019. The Company does not believe the adoption of ASU 2016-01 will have a material impact on its consolidated financial statements.

In June 2016, the FASB issued ASU No. 2016-13, Financial Instruments – Credit Losses (Topic 326): Measurement of Credit Losses on Financial Instruments (ASU 2016-13), which modifies the measurement of expected credit losses of certain financial instruments. ASU

11

2016-13 will be effective for the Company beginning in its first quarter of 2021 and early adoption is permitted. The Company does not believe the adoption of ASU 2016-13 will have a material impact on its consolidated financial statements.

There are several other new accounting pronouncements issued or proposed by the FASB. Each of these pronouncements, as applicable, has been or will be adopted by the Company. Management does not believe any of these accounting pronouncements has had or will have a material impact on the Company’s consolidated financial position or operating results.

NOTE 14 – ADDITIONAL PAID IN CAPITAL

Additional paid in capital on September 30, Common Stock transactions is $ 22,551,410

NOTE 15 – GOING CONCERN

We have not achieved profitability in any quarter since our formation and we will continue to incur net losses until we can produce sufficient revenue to cover our costs. As of August 30, 2021, we had an accumulated deficit of approximately $24.2 million. We anticipate that we will continue to incur losses until we can produce and sell our products on a large- scale and cost-effective basis. Our losses resulted from costs incurred in connection with our research and development expenses and from general and administrative costs associated with our operations. We cannot guarantee when we will operate profitably, if ever.

To achieve profitability, among other factors, management must successfully execute our planned path to profitability. If we are unable to successfully take these steps, we may never operate profitably, and, even if we do achieve profitability, we may be unable to sustain or increase our profitability in the future. We do not have enough cash to fund our operations to profitability and if we are unable to secure additional capital, we may be required to seek strategic alternatives, including but not limited to a potential business combination or a sale of our company or our business, or reduce and/or cease our operations.

To continue operations through the fourth quarter of 2021, management is exploring a variety of opportunities to obtain additional capital, we are in advanced conversations with investors and a potential private placement. There is no assurance that we will be able to raise the necessary capital or that the capital, if available, will be available on terms that will be acceptable to us.

If adequate funds are not available or are not available on acceptable terms, our ability to retake our operations, take advantage of opportunities, develop products and technologies, and otherwise respond to competitive pressures could be significantly delayed or limited, if we are not able to obtain the needed financing in a timely fashion, our ability to achieve profitability will be materially impaired.

12

Balance Sheet

2020 2019Assets

Current Assets CashInventories 281.409 310.000

Total Currenet assets 281.409 310.000

Other Assets Intangible assets, net of amortizacion 199.500 199.500Total Other Assets 199.500 199.500

Total Assets $480.909 $509.500

LIABILITIES and Stockholders´s Equity (Deficit)

Current LiabilitiesAccrued liabilities Parroll taxes 6.050 6.050Accrued officers wages 25.000 25.000Payroll taxes 6.000 6.000Tenneesse Unemployemnte Tax 384 384Tenneesse Excise Tax 3.800 3.800Nevada Silver Fume Copr annual taxes 1.900 1.900IRS (Est.) 10.148 10.148

Oursourcig invoices payable Baker , Donelson 53.942 53.942Craine , Thompson & Jones 5.900 5.900David Brown Law 1.574 1.574Rodefer Moss 12.034 12.034

Total current liabilities $126.732 $126.732

Stockholders´ Equity Common Stock ,$0,001 par value 100,000,000 Shares auhorized

53,018,563 issued and outstanding 53.018 53.018Additional paid in Capital 22.669.528 22.669.528Accumulated other comprehensive incomeRetained deficit -23.076.723 -23.105.314Total Stockholders´ Equity 354.177 382.768Total Liabilities and Stockholders´ equity $480.909 $509.500

13

STOCK. HOLDERS´ EQUITY (Deficit)

Stock Holders´s equity (Deficit)

Common Stock Additional Paid-in Capital Accumulated Retainer Deficit Total Stockholders´other compresnsive Income (net )

Balance at December 31, 2019 53.018$ 22.669.528$ 0 $ (23,076,723) 382.768$ Net Loss $ (28,591)Other comprensive incomeBalance at December 31, 2020 53.018$ 22.669.528$ 0 $ (23,105,314) 354.177$

14

P&L

Income Statment P&L 2020

Revenues

RevenuesRevenues MPMRevenues ICEH2

Total Revenues 0

Depretiation and amortization 0

Costs of Goods Sold ("COGS")COGS MPMCOGS ICEH2

Total Costs of Goods Sold 0

Gross profit before feesGross profit margin before fees (%)

Gross profit after feesGross profit margin after fees (%)

Sales , Marketing and Commecialization Outsourcing Marketing and AdvertisingStands and POS ActivitiesInternet Marketing & AdvertisingDistributors' Commissions and FeesOther Sales, Marketing and Commercial CostsTravel & EntertainmentMarketing & Sales Dept. PersonnelAdministration Personnel

Total Sales, Marketing and Commercial expenses 0

TechnologyResearch, Development & InnovationOther IT costs

Total Technology 0

General & AdministrationTop ManagementFinance & AdministrationLogisticsLegal & ComplianceOffice rentCommunicationsAudit, External CounselOther General & Administration Costs

Total General & Administration 0

15

Cash Flow

Consolidated Statements of Cash Flows 2020Cash flows from operating activities:

Net loss 0Adjustments to reconcile net loss to net cash

used in operating activities: 0Depreciation and amortization 0Gain on sale of fixed assets 0Stock option compensation 0Non cash expenses exchanged for paid in capital 0Interest income 0Decrease (increase) in: Inventory 0

Increase (decrease) in:

Accounts payable 0

Accrued liabilities 0

Accrued officers' wages 0

Accrued interest 0

Net cash used in operating activities 0

Cash flows from investing activities: Interest income

Proceeds from sale of fixed assets 0

Interest income 0

Net cash provided by investing activities

Cash flows from financing activities: 0Net (decrease) increase in borrowings and capital leases 0Issuance of common stock 0Increase in additional paid in capital 0

Net cash provided by financing activities

Net increase (decrease) in cash 0Cash at beginning of year

Cash at end of year 0

16

Issuer’s Business, Products and Services HEC Nevada, have one fully owned subsidiary, HEC-TINA Inc., a Nevada Corporation (“HEC-TINA”). HEC have spent the last 10 years developing technology related to green technologies. We currently have 3 main patents pending or granted, with more in the planning stage. Our intent is to capitalize on this technology as soon possible by transitioning the Company from more of a R&D phase to one of manufacturing, marketing, and sales. HEC is in advanced negotiations with TINA ENERGY SYSTEMS S.L. (TINA), its majority shareholder, for a $4,6 million financing of HEC through a company stock offering expected to close before the end of October 2021. Forecasted Use of Funds from the TINA equity investment

HEC is on track to relocate its headquarters to Miami, Florida and plans to build new state-of-the-art environmentally friendly industrial facilities in Miami. TINA has provided HEC and its subsidiaries with its proprietary hydrogen technologies and technical support since 2015. The new TINA carbon-free, state-of-the-art, proprietary key technologies include:

1. Unique technology of Self-pressurized PEM Stack with direct gases output pressures from 200 to 300 bars. Stack plates are made with especial titanium alloys which have treated with a unique Plasma chemical treatment technology avoiding oxidation and embrittlement which improves reliability of operation and extends operative life.

2. Mini Plants with new generation catalyst in development by TINA scientific team for Haber-Bosch process which improves and reduce cost for the distributed production of Green Fertilizers with "Renewables + Nitrogen + Hydrogen".

3. New catalysts for the synthesis / decomposition of photoinduced electrocatalytic and

thermocatalytic ammonia, It is planned with polyoxometalate catalysts substituted with metals (M- POM, M = Fe, Ru, V, etc.) on carbon and C3N4.

HEC - Use of Equity Funds 2021 2022 2023Equity Investment $770.000 $1.430.000 $2.200.000

Legal closing transaction $45.000Legal & CPA & Audit years 2019 and 2020 K-10 Files to SEC $100.000 $50.000Yearly Legal & CPA & Audit K-8 and K-10 years 2021 K-10 Files to SEC $50.000 $150.000 $150.000Administrative Operation Cost offices in USA (leasing & utilities) $24.000 $48.000 $48.000Payroll Administrative USA $23.400 $46.800 $48.000Regularization All debts $110.000 $10.000New WEB , Promotion and Marketing $20.000 $40.000 $40.000Industrial Leasing facilities $14.000 $70.000 $80.000Works and equipment Industrial $250.000 $300.000Managemnet and Technical personel $30.000 $240.000 $320.000Rebuilt a DEMO improved MPM outside industrial Plant ( from Teneessee) $25.000 $50.000 $50.000Build DEMO NH3 plant outside of the industrial Plant $150.000 $200.000Miscelaneus & Sundry $40.000 $40.000 $40.000

Total $481.400 $1.144.800 $1.276.000Operating Cash Available in account 288.600 € 285.200 € 924.000 €

17

4. Carbon- free mobile mini-Plug & Play power plants to electrify 24/7/365 remote areas

without access to a power grid operating with "Renewables + Hydrogen + Genset ICEH2". 5. GENSETS with ICE fueled by Hydrogen including Plasma chemical treatment of some

components of ICE engines to operate with Hydrogen avoiding oxidation and embrittlement which improves reliability of operation and extends operative life.

6. Hydrogen Filling Stations, equipped with TINA Electrolyzers

HEC will manufacture and commercialize several of its proprietary technologies in collaboration with TINA. Regarding the carbon-free plug & play mobile power plants (MPM), which are describe in our video submitted to OYC information, we will resume our earlier discussions with the authorities in Sarawak, Malaysia, which were interrupted due to the pandemic. Our first approach is to refresh our previously discussed proposals for the economic master plan of the Penan, a nomadic indigenous people comprising some 120 Penan villages, most of which are in the Baram areas.

It includes about 10-11 Rural Economic Hubs based on HEC TINA's technology demonstrator configuration with a system of at least 1 MW per day. It includes about 10-11 Rural Economic Hubs based on the technology demonstrator configuration of HEC TINA with a system of at least 1 MW per day. The macro planning for the Penan Economic Master Plan includes a total of about 25 MW Day.

The extended commitment is a proposal to establish all Sarawak Rural Economic Hubs an extended facility to the rural collection centers in the State of Sarawak. We have not yet started the macro assessments pending the initial commitments from the earlier phases, ie: Prelim REH (Rural

TINA System Hardware

18

Economic Hub), 2 major Penan villages including the Penan "capital" village, and a handful of agro-fisheries including integrated farms associated with REH.

World Bank highlighted those mini grids investments in Africa and Asean will grow from $5 billion in 2020 to $220 Billion by 2030 Forward-looking statements This discussion contains forward-looking statements that involve risks and uncertainties. In some cases, you can identify forward-looking statements by words such as “estimate", "project", "intend", "forecast", “plan”, “expect”, "anticipate", "believe", “goal”, "will", "could", "would", “may", or the negative of such terms and other compatible terminology. You should not place undue reliance on these forward-looking statements, which speak only as of the date made. Our actual results will depend upon a number of factors beyond our control and could differ materially from those anticipated in the forward-looking statements. Some of these factors are discussed below and elsewhere in this form. We assume no obligation to update the forward-looking statements after the date hereof whether because of new information or events, changed circumstances or otherwise, except as required by law. Risks and uncertainties

The discussion and analysis contained in this Report should be read in conjunction with the other financial information and consolidated financial statements and related notes included elsewhere in this Report. We have financed operations since inception primarily through equity and debt financings. We are a development stage enterprise and, as such, our continued existence is dependent upon our ability to resolve our liquidity problems, principally by obtaining additional debt or equity financing. We have yet to generate a positive internal cash flow, and until meaningful sales of our products begin, we are dependent upon debt and equity funding. We intend to aggressively pursue sales of our turnkey Power Modules. We believe that we are ideally positioned to take advantage of the tremendous growth projected for local power systems and for greenhouse gas reduction. Our systems can make power available in remote areas 24/7/365 for our customers. Management believes that the actions presently being taken to further implement its

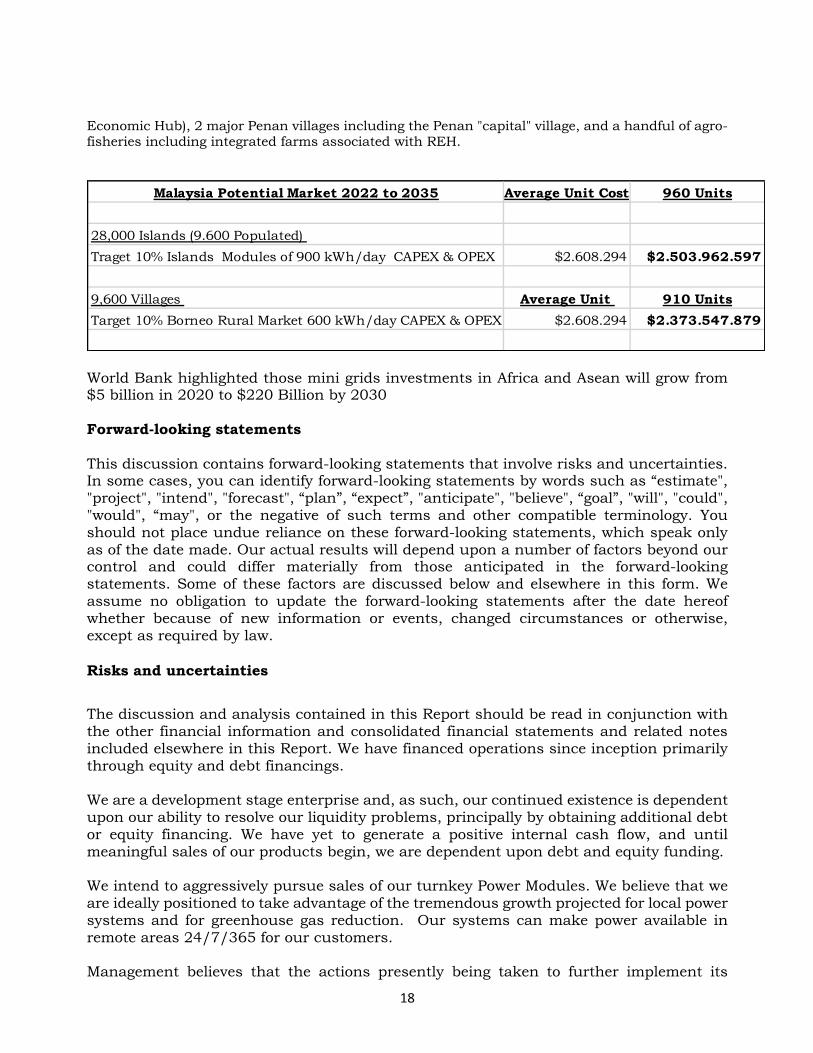

Malaysia Potential Market 2022 to 2035 Average Unit Cost 960 Units

28,000 Islands (9.600 Populated) Traget 10% Islands Modules of 900 kWh/day CAPEX & OPEX $2.608.294 $2.503.962.597

9,600 Villages Average Unit 910 Units

Target 10% Borneo Rural Market 600 kWh/day CAPEX & OPEX $2.608.294 $2.373.547.879

19

business plan and generate revenues provide the opportunity for the Company to continue as a going concern. While the Company believes in the viability of its strategy to generate revenues and in its ability to raise additional funds. The ability of the Company to continue as a going concern is dependent upon the Company’s ability to further implement its business plan and generate revenues. The financial statements do not include any adjustments that might be necessary if the Company is unable to continue.

The Company is subject to risks from, among other things, competition associated with the industry in general, other risks associated with financing, liquidity requirements, rapidly changing customer requirements and technologies and limited operating history. Although there are several companies developing and/or marketing Electrolyzers and hydrogen engines, we are not aware at this date of any significant production of our type of technology. We believe that the competition is targeting production for hydrogen-fueled vehicles. This is a different customer requirement than the distributed energy system we are pursuing. Most of the competitors are targeting larger hydrogen generation systems and are powering them with utility power. Hydrogen filling stations are an example of this. Other competitors and potential competitors involved in the manufacturer of Electrolyzers mainly include Proton Nel-Giner, Hydrogenics, ITM-Power. In the Fuel cell field companies such as Ballard, Plug Power, Fuel Cell Energy, SFC Energy, Intelligent Energy, should be also considered competitors. Fuel cells may be perceived to be competition to our Gensets equipped with ICE fueled by Hydrogen, but we believe they are not at this time. Fuel cells cannot be currently manufactured in sufficient quantity to compete with hydrogen and other alternative fuel internal combustion engines. Also, fuel cells are more expensive than the hydrogen internal combustion engines

The production of green hydrogen by electrolysis of water and renewable energy.

There are two types of commercial Electrolyzers, the alkaline and the Proton Exchange Membrane (PEM), both have their applications: the alkaline one for large productions and the PEM for low- medium productions. In the market, these Electrolyzers are classified according to the kW power they need to produce 1 m3 Hydrogen Gas.

Real numbers: Production of 1.00 Kg of H2 99,99% needs an average of 57 kW electric energy, the kg of H2 have 33 kW of calorific power. Supply 1.00 kg of H2 to a PEMFC deliveries 18 kW and to an ICEH2 deliver 12 kW

20

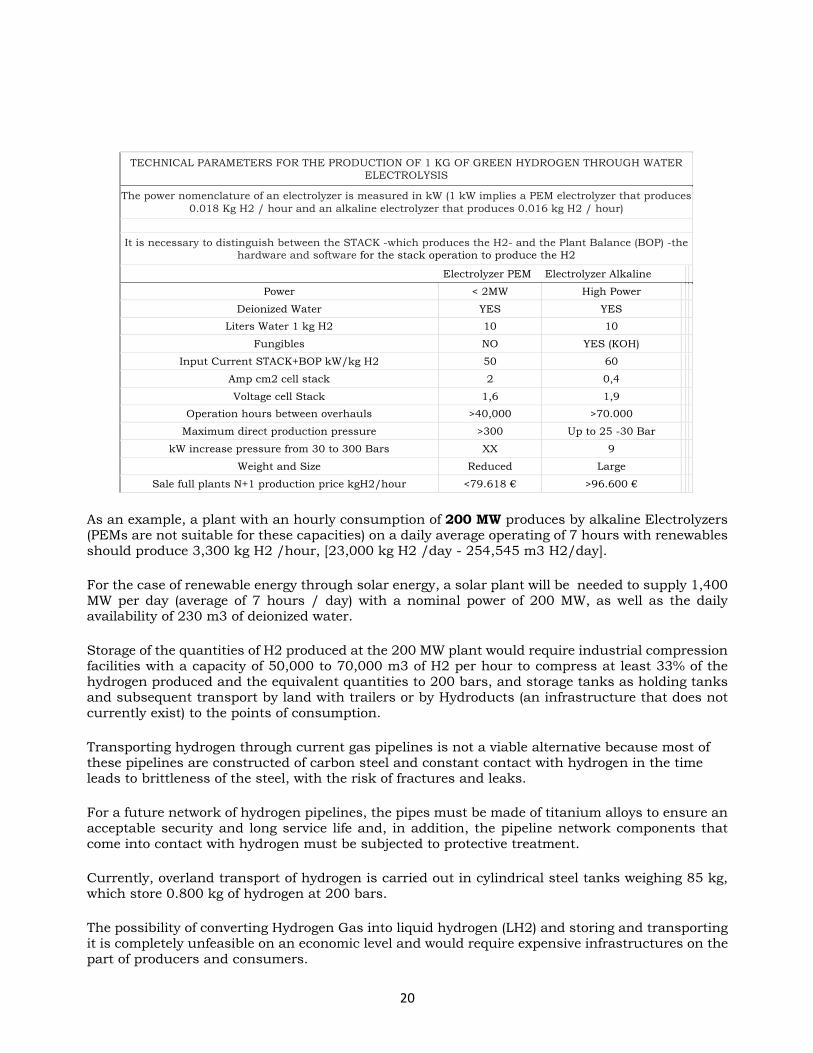

TECHNICAL PARAMETERS FOR THE PRODUCTION OF 1 KG OF GREEN HYDROGEN THROUGH WATER ELECTROLYSIS

The power nomenclature of an electrolyzer is measured in kW (1 kW implies a PEM electrolyzer that produces 0.018 Kg H2 / hour and an alkaline electrolyzer that produces 0.016 kg H2 / hour)

It is necessary to distinguish between the STACK -which produces the H2- and the Plant Balance (BOP) -the hardware and software for the stack operation to produce the H2

Electrolyzer PEM Electrolyzer Alkaline

Power < 2MW High Power

Deionized Water YES YES

Liters Water 1 kg H2 10 10

Fungibles NO YES (KOH)

Input Current STACK+BOP kW/kg H2 50 60

Amp cm2 cell stack 2 0,4

Voltage cell Stack 1,6 1,9

Operation hours between overhauls >40,000 >70.000

Maximum direct production pressure >300 Up to 25 -30 Bar

kW increase pressure from 30 to 300 Bars XX 9

Weight and Size Reduced Large

Sale full plants N+1 production price kgH2/hour <79.618 € >96.600 €

As an example, a plant with an hourly consumption of 200 MW produces by alkaline Electrolyzers (PEMs are not suitable for these capacities) on a daily average operating of 7 hours with renewables should produce 3,300 kg H2 /hour, [23,000 kg H2 /day - 254,545 m3 H2/day].

For the case of renewable energy through solar energy, a solar plant will be needed to supply 1,400 MW per day (average of 7 hours / day) with a nominal power of 200 MW, as well as the daily availability of 230 m3 of deionized water.

Storage of the quantities of H2 produced at the 200 MW plant would require industrial compression facilities with a capacity of 50,000 to 70,000 m3 of H2 per hour to compress at least 33% of the hydrogen produced and the equivalent quantities to 200 bars, and storage tanks as holding tanks and subsequent transport by land with trailers or by Hydroducts (an infrastructure that does not currently exist) to the points of consumption.

Transporting hydrogen through current gas pipelines is not a viable alternative because most of these pipelines are constructed of carbon steel and constant contact with hydrogen in the time leads to brittleness of the steel, with the risk of fractures and leaks.

For a future network of hydrogen pipelines, the pipes must be made of titanium alloys to ensure an acceptable security and long service life and, in addition, the pipeline network components that come into contact with hydrogen must be subjected to protective treatment.

Currently, overland transport of hydrogen is carried out in cylindrical steel tanks weighing 85 kg, which store 0.800 kg of hydrogen at 200 bars.

The possibility of converting Hydrogen Gas into liquid hydrogen (LH2) and storing and transporting it is completely unfeasible on an economic level and would require expensive infrastructures on the part of producers and consumers.

21

TINA strategy of decentralized production and commercialization of green hydrogen

HEC has attended numerous hydrogen related trade shows and conferences around the world over the last 20 years and has maintained contacts with executives of various manufacturers (Plug Power, Giner, Proton, Toyota, Quantum, etc.). Based on his experience in hydrogen, he knows that with current technologies, the production and commercialization of commercially viable Green Hydrogen is about production in distributed systems for the small-medium production and use of hydrogen in situ by the consumer.

Many existing and potential competitors have greater financial resources, larger market share, and larger production and technology research capability, which may enable them to establish a stronger competitive position than we have, in part through greater marketing opportunities. However, we believe our lead in technology is an asset in that it will take a large investment in time and money to duplicate what we have already achieved. There can be no assurance that potential competitors of the Company, which may have greater financial, research and development, sales and marketing and personnel resources than the Company, are not currently developing, or will not in the future develop products and processes that are equally or more effective and/or economical as the products developed by the Company or which would otherwise render the Company’s products obsolete.

The Company may be forced to change the nature of its business because of competitive factors. Given the potential of hydrogen derived energy in general, it is anticipated that the market will become increasingly competitive over the coming years.

Recent events do point to the increased likelihood of a global downturn in world economies, and one cannot imagine that any one sector can remain completely unaffected. On the other hand, HEC solutions are targeted at lowering costs and increasing competitiveness and these are objectives, which in difficult times can be perhaps delayed – but not eliminated.

The Company’s business may be affected by the general risks associated with all companies in the energy industry. The prices received for the Company’s goods and products depend on numerous factors, many of which are beyond its control and the exact effect of which cannot be accurately predicted. Such factors include general economic and political activities, including the extent of government regulation and taxation.

The Company believes that its future success will greatly depend on the expertise services of certain key executives and technical personnel. The Company cannot guarantee the retention of such key executives and technical personnel. As a result, the Company’s business, its results of operations and financial condition may be adversely affected.

The Company’s ability to implement its business strategy may be adversely affected by factors the Company cannot currently foresee, such as unanticipated costs and expenses, interruptions to or delays in production, reduced demand for the Company’s products and technology. All these factors may necessitate changes to the business strategy described in this document.

The Company needs to strengthen its capacity to deliver systems and furthermore, it must be able to continue to invest in R&D. Should such funds not be available for an extended period, HEC will be weakened but we expect it will still be able to reach profitability but at a slower rate.

The Company faces several industrial risks such as a dispute with its workforce and dependence on key suppliers, both of which may lead to a deterioration in financial performance. Like any high-tech Company that relies on technology for its competitive advantage, the company is potentially vulnerable to intellectual property (IP) theft. However, in HEC case, its nature is very specialized, and not residing in any one person’s knowledge. Furthermore, very important and critical elements

22

of the HEC IP should be patent protected. HEC is therefore protected as most – if not more – against such theft risk.

While the Company believes that there continues to be viable markets for its products, there can be no assurance that the Company’s products will prove to be more successful than competing products in the future. If the Company’s products do not gain further market acceptance, further expenditure on marketing and development may be required to make them commercially viable.

The Company intends to continue to expand internationally and therefore its results could be affected significantly by currency fluctuations. Other risks from international business activities include complying with regulatory requirements and standards, tariffs and other trade barriers, reliance on third parties to distribute products and potentially adverse tax consequences

There can be no guarantee that orders will be received for the Company’s products in the anticipated volumes or within the time frames envisioned by the Company. The placing of orders for the Company’s products could be materially delayed by circumstances such as customer evaluations or integration of the Company’s products taking longer than anticipated. The Company must also ensure that production capacity is always sufficient to match the level of orders. Failure to do so could lead to the financial impact of inefficient production, missed sales opportunities and late delivery to customers.

Principal Suppliers We outsource manufactured parts and bring them into our production facility as components ready for the assembly line. We then assemble all components to produce our products. We purchase parts for our devices from several different industrial suppliers. The parts are sourced from destinations located all over the world. The parts are tested for quality and then assembled into engines and tested at our facility. There are risks and uncertainties with respect to the supply of certain component parts that could impact availability in sufficient quantities to meet our needs. If, for any reason, a manufacturer is unable or refuses to manufacture our component parts, our business, financial condition, and results of operations would be materially and adversely affected. Dependence on One or Few Major Customers We do not anticipate dependence on one or a few major customers currently. Intellectual Property and Patent Protection HEC is built on the vision of carbon-free energy independence through the development and commercialization of clean solutions for today’s energy needs. We have been working to expand our intellectual property portfolio and developing technologies to allow fuel generation, engines and gensets to generate and use clean power where needed. We believe that our developing technologies have the potential to revolutionize our world by removing the political and environmental problems generated by our ever-increasing appetite for energy sources. We have several patents pending and several potential patents in the development stage. We also rely on trade secrets, common law trademark rights and trademark registrations. We intend to protect our intellectual property via non-disclosure agreements, license agreements and limited information distribution.

23

Cost of Compliance with Environmental Laws We outsource all manufactured parts and bring them into our production facility as components ready for the assembly line. We then assemble all components to produce our products. The assembly process uses no hazardous materials, nor do they create any hazardous waste. We have written our procedures to meet or current environmental and fire code laws. Any changes in the laws at the state or federal level could require us to modify our procedures to comply with future environmental regulations. We are currently exploring a variety of other opportunities to obtain additional capital through a private placement. There is no assurance that we will be able to raise the necessary capital or that the capital, if available, will be available on terms that will be acceptable to us.

If adequate funds are not available or are not available on acceptable terms, our ability to fund our operations, take advantage of opportunities, develop products and technologies, and otherwise respond to competitive pressures could be significantly delayed or limited, and we may need to downsize or halt our operations. If we are not able to obtain the needed financing in a timely fashion, our ability to achieve profitability will be materially impaired.

We have a limited operating history and have not recorded an operating profit since our inception. The potential for us to generate profits depends on many factors, including the following: • timely receipt of required financing beyond our initial expectations; • successful pursuit of our research and development efforts; • protection of our intellectual property; • quality and reliability of our products. • ability to attract and retain a qualified work force • size and timing of future customer orders, milestone achievement, product delivery and customer acceptance. • success in maintaining and enhancing existing strategic relationships and developing new strategic relationships with potential customers. • actions taken by competitors, including suppliers of traditional engines, hydrogen fuel cells and new product introductions and pricing changes; and • reliability of our suppliers. We cannot assure you that we will achieve success as to any of the foregoing factors or realize profitability in the immediate future or at any time. Our future success depends in part on our ability to retain key employees. We currently do not carry "key man" insurance on our executives; however, we are considering the purchase of such insurance. It would be difficult for us to replace any one of these individuals. In addition, as we grow, we will need to hire additional key personnel.

24

Our products may contain design faults. Though we believe it unlikely, the technologies we have developed and are developing, and the products we produce in our new facility, could contain undetected design faults despite our careful design and testing. We may not discover these faults or errors until after our customers have used a product. Any such faults or errors may cause delays in product introduction and shipments, require design modifications, or harm customer relationships, any of which could adversely affect our business and competitive position. We understand that customer service is an important part of our mission, and we feel poised to address any issues that may arise. If we are unable to successfully address any such issues, our results of operation could be materially and adversely affected. Acceptance of hydrogen as an alternative fuel will affect our ability to achieve commercial application of our products and technologies. With proper precaution, we believe that hydrogen could be as safe as any other fuel. The main benefit of hydrogen as a fuel is that it produces little or no pollution or greenhouse gases when it is used in an internal combustion engine. The development of a market for our technologies may be impacted by many factors, including: • consumer perception of the safety of hydrogen and willingness to use engines powered by

hydrogen. • adverse regulatory developments, including the adoption of onerous regulations regarding

hydrogen use or storage. • barriers to entry created by existing energy providers; and • the emergence of new competitive technologies and products. Certain government regulations concerning electrical and hydrogen generation, delivery and storage of fuels and other related matters may negatively impact our business. Our business is subject to and affected by federal, state, local, and foreign laws and regulations. These may include state and local ordinances relating to public safety, electrical and hydrogen production, delivery and refueling infrastructure, hydrogen storage, and related matters. We do not know the extent to which any such regulations may impact our business or our customers’ businesses. Any new regulation may increase costs and could reduce our potential to be profitable. We believe that we carry a reasonable amount of insurance. However, there can be no assurance that our existing insurance coverage would be adequate in term and scope to protect us against material financial effects in the event of a successful claim. We could be subject to claims in connection with the products that we sell. There can be no assurance that we would have sufficient resources to satisfy any liability resulting from any such claim, or that we would be able to have our customers indemnify or insure us against any such liability. There can be no assurance that our insurance coverage would be adequate in term and scope to protect us against material financial effects in the event of a successful claim. If we fail to keep up with changes affecting our technology and the markets that we will ultimately serve, we will become less competitive and future financial performance would be adversely affected. In order to remain competitive and serve our potential customers effectively, we must respond on a timely and cost-efficient basis to the need for new technology, as well as changes in technology,

25

industry standards and procedures, and customer preferences. We need to continuously develop new technology, products, and services to address new technological developments. In some cases, changes may be significant, and the cost of implementation may be substantial. We cannot assure you that we will be able to adapt to any changes in the future or that we will have the financial resources to keep up with changes in the marketplace. Also, the cost of adapting our technology, products, and services may have a material and adverse effect on our operating results. We do not anticipate paying dividends in the foreseeable future. This could make our stock less attractive to potential investors. Any future payment of cash dividends will be at the discretion of our board of directors after considering many factors, including our operating results, financial condition, and capital requirements. Corporations that pay dividends may be viewed as a better investment than corporations that do not. The authorization and issuance of blank–check preferred stock may prevent or discourage a change in our management.

The Company’s Articles of Incorporation authorize the issuance of up to 100,000,000 shares of Common Stock, par value $0.001 per share, par value $0.001 per share. It may be difficult for a third party to acquire us, and this could depress our stock price. Nevada corporate law includes provisions that could delay, defer, or prevent a change in control of our Company or our management. These provisions could discourage information contests and make it more difficult for stockholders to elect directors and take other corporate actions. As a result, these provisions could limit the price that investors are willing to pay in the future for shares of our common stock. For example: • Without prior stockholder approval, the board of directors has the authority to issue one or more

classes of preferred stock with rights senior to those of common stock and to determine the rights, privileges, and preferences of that preferred stock; and

• There is no cumulative voting in the election of directors; and Inherent Limitations Over Internal Controls Our internal control over financial reporting is designed to provide reasonable assurance regarding the reliability of financial reporting and the preparation of financial statements for external purposes in accordance with generally accepted accounting principles. Our internal control financial reporting includes those policies and procedures that:

(i) pertain to the maintenance of records that, in reasonable detail, accurately and fairly reflect the transactions and disposition of our assets;

(ii) provide reasonable assurance that transactions are recorded as necessary to permit

preparation of financial statements in accordance with generally accepted accounting principles, and that our receipts and expenditures are being made only in accordance with authorizations of our management and directors; and

(iii) provide reasonable assurance regarding prevention or timely detection of

unauthorized acquisition, use, or disposition of our assets that could have a material effect on the financial statements.

Our auditors have not performed an audit of our internal controls over the 2020 financial reporting. Management do not expect that our internal controls will prevent or detect all errors and all fraud.

26

A control system, no matter how well designed and operated, can provide only reasonable, not absolute, assurance that the objectives of the control system are met. Further, the design of a control system must reflect the fact that there are resource constraints, and the benefits of controls must be considered relative to their costs. Because of the inherent limitations in all control systems, no evaluation of internal controls can provide absolute assurance that all control issues and instances of fraud, if any, have been detected. Also, any evaluation of the effectiveness of controls in future periods are subject to the risk that those internal controls may become inadequate because of changes in business conditions, or that the degree of compliance with the policies or procedures may deteriorate.

Contingencies

If the assessment of a contingency indicates it is probable that a material loss has been incurred and the amount of the liability can be estimated, then the estimated liability would be accrued in the Company’s financial statements. If the assessment indicates that a potential material loss contingency is not probable but is reasonably possible, or is probable but cannot be estimated, then the nature of the contingent liability, together with an estimate of the range of possible loss if determinable and material would be disclosed. Loss contingencies considered to be remote by management are generally not disclosed unless they involve guarantees, in which case the guarantee would be disclosed.

Issuer’s Facilities Presently HEC (Nevada) don’t have Industrial facilities Company Insiders (Officers, Directors, and Control Persons) The following table sets forth the securities and beneficial ownership for each class of stock of the Company for each person known to be the beneficial owner of more than ten percent (10%) of the Company as of August 30, 2021. Except described below, the security ownership of each of the above beneficial owners is also the owner of the same number of shares.

Title of Class

Name and Address of Beneficial Owner

Amount and Nature of Beneficial Ownership

Percent of Class4

Common Theodore G. Hollinger 215 Appian Way Greeneville TN 37745

13,206,772 (1) 24.90%

Common TINA Energy Systems C/Alcalá nº59-5 Madrid 28014 Spain

18,317,463 (2) 34,54%

Common Pedro Blach Apart. 13A Devonshire St Cable Beach New Providence Bahamas

2,000,000 (3) 3.77%

(1) Includes 38,505 shares held by Mr. Hollinger’s wife.

(2), (3) Mr. Blach is an affiliate of TINA Energy Systems. The combined holdings of Mr. Blach and TINA Energy Systems, including the exercisable options and the agreement to purchase shares as described above, 20,317,463 total shares, or 38,31%.

27

(4) Applicable percentages of ownership are based on 53,018,000 shares of Common Stock outstanding as of June 30, 2021. For each shareholder holding exercisable options (or options exercisable within 60 days), or under an agreement to purchase shares, the percentage of ownership has been calculated assuming that such options have been exercised and such shares have been purchased.

Presently we don’t have Outstanding warrants Third Party Providers

Legal Counsel Baker, Donelson, Bearman, Caldwell & Berkowitz, PC 265 Brookview Centre Way, Suite 600 Knoxville, TN 37919 Direct: 865.549.7125 Fax: 865.633.7125 E-mail: [email protected] www.bakerdonelson.com Accountants Craine, Thompson & Jones, P.C. 225 W First North St Morristown, TN 37814 423-586-7650 www.ctandj.net Auditors Rodefer Moss & Co, PLLC 608 Mabry Hood Road I Knoxville, TN 37932 865.684.1956 Direct 865.583.0091 Office http:/www.rodefermoss.com

Investor Relations Kim Tilson Greeneville, TN 37745 Phone: (423) 278-2952 E-mail: [email protected]

28

Issuer Certification Pedro Blach certifies that: 1.- I read the disclosure report of Hydrogen Engine Center Inc (Nevada) 2. to my knowledge, this disclosure statement does not contain any untrue statement of a material fact or omit to state a material fact necessary to make the statements made, considering the circumstances under which such statements were made, not misleading with respect to the period covered by this disclosure statement; and 3. to the best of my knowledge, the financial statements, and other financial information included or referred to in this Disclosure Statement present fairly in all material respects the financial condition, results of operations of the Issuer as of, and for, the periods covered by this Disclosure Statement. 27 September 2021

Signature

Pedro Blach