HSIL Ltd - Result Update

5

Wealth Research, Unicon Financial Intermediaries. Pvt Ltd. Email: [email protected] LONG TERM INVESTMENT CALL BUY 27 July 2011 Company Report | Q1FY12 Result Update Q1FY12 Result Highlights HSIL announced its Q1FY12 results and reported a very strong performance. Its revenues increased to INR 3280 mn, an increase of 41.5% as compared to Q1FY11. The EBITDA posted by the company was INR 627 mn, an increase of 55.5% YoY. EBIDTA margins increased by 180 basis points to 20.4% The Profit before Tax (PBT) increased to INR 417 mn, a rise of 130% as compared to the first quarter of the previous financial year. The Profit after Tax (PAT) showed a robust growth of 111% to INR 285 mn. The PAT margins increased substantially by 309 basis points to 9.36% Cash profits showed strong growth of 32% to INR 410 mn. The two divisions of the company i.e. the Building Products division and the Container Glass division recorded robust sales growing by 29% and 53% YoY. The company has reported outstanding results for Q1FY12 beating most forecasted estimates. Both divisions of the company i.e. the Building Products division and the Container Glass division have performed well both on absolute as well as margin parameters. Currently, all plants of the company are running at full capacity. The sanitary ware division is running at 116% capacity and the Container glass division is running at 100% capacity. The Building Products division recorded 29% growth in revenue and a 10% growth in volume for this quarter. The Container Glass division recorded a 53% growth of which 31% was due to volume growth and 22% was due to realization and product mix growth. Outlook and Valuation The management of the company has focused on certain key parameters, which resulted in a stellar performance for this quarter. The efficiency of the plants has been improved. The company has launched new designs across product segments. There has been a focus on premium products and segments, which have higher profit margins. The company has expanded its distribution network and has ~1550 distributors and ~12,000 retailers. . The management is confident of achieving more than 30% growth in both sales and profits for the entire year. For FY12, the management has given revenue guidance of ~INR 15000 mn and EBIDTA estimates between ~INR 2900-3000 mn. Industry Building Products & Container Glass CMP (INR) 219 Target (INR) 265 52 week High/Low (INR) 229.80/106 Market Cap (INR Mn) 14450 3M Avg. Daily Volumes (‘000) 166.8 Company PE (FY12e) 10.5x Shareholding Pattern (%) Stock Performance Performance (%) 1 Month 3 Months 1 Year HSIL 24.3 38.9 83.4 NIFTY 1.9 -5.0 2.9

-

Upload

seema-gusain -

Category

Documents

-

view

222 -

download

0

Transcript of HSIL Ltd - Result Update

8/6/2019 HSIL Ltd - Result Update

http://slidepdf.com/reader/full/hsil-ltd-result-update 1/4Wealth Research, Unicon Financial Intermediaries. Pvt Ltd.

Email: [email protected]

ONG TERM INVESTMENT CALL

BUY27 July 2011

Company Report | Q1FY12 Result Update

Q1FY12 Result Highlights

HSIL announced its Q1FY12 results and reported a very strong

performance. Its revenues increased to INR 3280 mn, an increase of 41.5%

as compared to Q1FY11. The EBITDA posted by the company was INR

627 mn, an increase of 55.5% YoY. EBIDTA margins increased by 180

basis points to 20.4%

The Profit before Tax (PBT) increased to INR 417 mn, a rise of 130% as

compared to the first quarter of the previous financial year. The Profit

after Tax (PAT) showed a robust growth of 111% to INR 285 mn. The

PAT margins increased substantially by 309 basis points to 9.36% Cash

profits showed strong growth of 32% to INR 410 mn.

The two divisions of the company i.e. the Building Products division and

the Container Glass division recorded robust sales growing by 29% and

53% YoY.

The company has reported outstanding results for Q1FY12 beating most

forecasted estimates. Both divisions of the company i.e. the Building

Products division and the Container Glass division have performed well

both on absolute as well as margin parameters. Currently, all plants of

the company are running at full capacity. The sanitary ware division is

running at 116% capacity and the Container glass division is running at100% capacity.

The Building Products division recorded 29% growth in revenue and a

10% growth in volume for this quarter. The Container Glass division

recorded a 53% growth of which 31% was due to volume growth and

22% was due to realization and product mix growth.

Outlook and Valuation

The management of the company has focused on certain key parameters,

which resulted in a stellar performance for this quarter. The efficiency ofthe plants has been improved. The company has launched new designs

across product segments. There has been a focus on premium products

and segments, which have higher profit margins. The company has

expanded its distribution network and has ~1550 distributors and ~12,000

retailers. .

The management is confident of achieving more than 30% growth in both

sales and profits for the entire year. For FY12, the management has given

revenue guidance of ~INR 15000 mn and EBIDTA estimates between

~INR 2900-3000 mn.

IndustryBuilding Products

& Container GlassCMP (INR) 219

Target (INR) 265

52 week High/Low (INR) 229.80/106

Market Cap (INR Mn) 14450

3M Avg. Daily Volumes

(‘000)166.8

Company PE (FY12e) 10.5x

Shareholding Pattern (%)

Stock Performance

Performance (%)

1 Month 3 Months 1 Year

HSIL 24.3 38.9 83.4

NIFTY 1.9 -5.0 2.9

8/6/2019 HSIL Ltd - Result Update

http://slidepdf.com/reader/full/hsil-ltd-result-update 2/4Wealth Research, Unicon Financial Intermediaries. Pvt Ltd.

Email: [email protected]

In future, HSIL plans to focus on Brass Chrome Plated Bath Fittings (Faucets)

segment with a target to become the second largest player in the faucet market in

India, having an estimated size of ~INR 30000 mn. After the acquisition of the

faucets division of Havells India at Bhiwadi, Rajasthan, the company is now

running it at 100% capacity. It has discontinued Crab Tree brand and markets it

under the Vanilla brand. It currently manufactures 3 lac pieces per annum, and

capacity is expected to increase to 5 lac pieces per annum once the expansion is

complete in September 2011. The faucets division contributed 17% of the Building

Products revenue last year.

It has acquired a 100% stake in Garden Polymers Pvt Ltd (turnover of INR 1050

mn). The company manufactures PET bottles, caps and closures with two plants

strategically located at Dharwad, Karnataka and Selaqui, Uttrakhand. This

company should grow at 20 to 25%

For FY2011-2012 the company has planned capex of INR 6500 mn, which is

expected to be completed as per projected schedule. This capex has been spread

over 2.5 years, with INR 1600 mn having already been invested, it is projected that

INR 2000 mn will be invested this year; the remaining amount will be invested

during the next 18-24 month time-frame. The company is looking to have a presence

in every city having a population of over 25,000 people.

At current market price of INR 219, the stock is trading at a P/E of 10.5x for FY12

est. earnings. Looking at the robust performance by the company in the first quarter

and given the expansion plans in place and management capabilities to drive the

business, we re-rate and recommend a “BUY” on the stock with a price target of

INR265.

8/6/2019 HSIL Ltd - Result Update

http://slidepdf.com/reader/full/hsil-ltd-result-update 3/4Wealth Research, Unicon Financial Intermediaries. Pvt Ltd.

Email: [email protected]

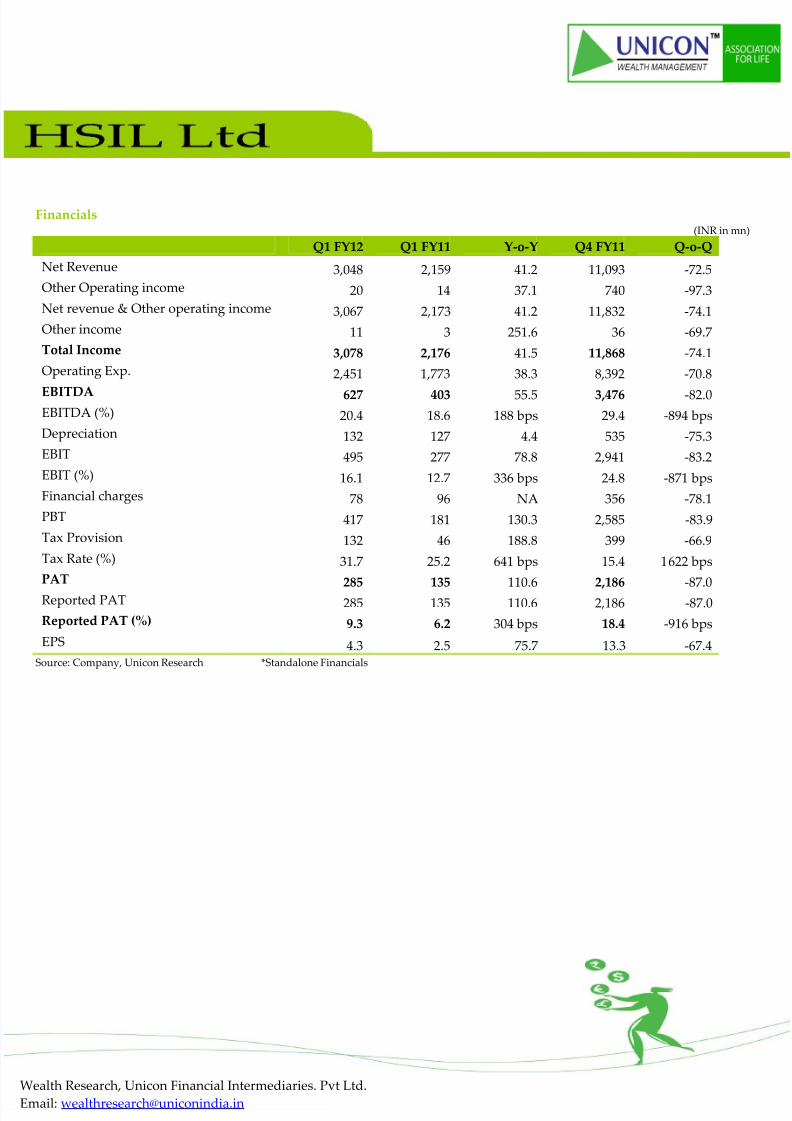

Financials(INR in mn)

Q1 FY12 Q1 FY11 Y-o-Y Q4 FY11 Q-o-Q

Net Revenue 3,048 2,159 41.2 11,093 -72.5

Other Operating income 20 14 37.1 740 -97.3

Net revenue & Other operating income 3,067 2,173 41.2 11,832 -74.1

Other income 11 3 251.6 36 -69.7

Total Income 3,078 2,176 41.5 11,868 -74.1

Operating Exp. 2,451 1,773 38.3 8,392 -70.8

EBITDA 627 403 55.5 3,476 -82.0EBITDA (%) 20.4 18.6 188 bps 29.4 -894 bps

Depreciation 132 127 4.4 535 -75.3

EBIT 495 277 78.8 2,941 -83.2

EBIT (%) 16.1 12.7 336 bps 24.8 -871 bps

Financial charges 78 96 NA 356 -78.1

PBT 417 181 130.3 2,585 -83.9

Tax Provision 132 46 188.8 399 -66.9

Tax Rate (%) 31.7 25.2 641 bps 15.4 1622 bps

PAT285 135 110.6 2,186 -87.0Reported PAT 285 135 110.6 2,186 -87.0

Reported PAT (%) 9.3 6.2 304 bps 18.4 -916 bps

EPS 4.3 2.5 75.7 13.3 -67.4Source: Company, Unicon Research *Standalone Financials

8/6/2019 HSIL Ltd - Result Update

http://slidepdf.com/reader/full/hsil-ltd-result-update 4/4Wealth Research, Unicon Financial Intermediaries. Pvt Ltd.

Email: wealthresearch@uniconindia in

Unicon Investment Ranking Methodology Rating Buy Accumulate Hold Reduce Sell

Return Range >= 20% 10% to 20% -10% to 10% -10% to -20% <= -20%

Disclaimer

This document has been issued by Unicon Financial Intermediaries Pvt. Ltd. (“UNICON”) for the information of its customers only. UNICON is governed by

the Securities and Exchange Board of India. This document is not for public distribution and has been furnished to you solely for your information and mustnot be reproduced or redistributed to any other person. Persons into whose possession this document may come are required to observe these restrictions. The

information and opinions contained herein have been compiled or arrived at based upon information obtained in good faith from public sources believed to

be reliable. Such information has not been independently verified and no guarantee, representation or warranty, express or implied is made as to its accuracy,

completeness or correctness. All such information and opinions are subject to change without notice. This document has been produced independently of any

company or companies mentioned herein, and forward looking statements; opinions and expectations contained herein are subject to change without notice.

This document is for information purposes only and is provided on an “as is” basis. Descriptions of any company or companies or their securities mentioned

herein are not intended to be complete and this document is not, and should not be construed as an offer, or solicitation of an offer, to buy or sell or subscribe

to any securities or other financial instruments. We are not soliciting any action based on this document. UNICON, its associate and group companies its

directors or employees do not take any responsibility, financial or otherwise, of the losses or the damages sustained due to the investments made or any action

taken on basis of this document, including but not restricted to, fluctuation in the prices of the shares and bonds, reduction in the dividend or income, etc. This

document is not directed to or intended for display, downloading, printing, reproducing or for distribution to or use by any person or entity who is a citizen

or resident or located in any locality, state, country or other jurisdiction where such distribution, publication, reproduction, availability or use would be

contrary to law or regulation or would subject UNICON or its associates or group companies to any registration or licensing requirement within such

jurisdiction. If this document is inadvertently sent or has reached any individual in such country, the same may be ignored and brought to the attention of thesender. This document may not be reproduced, distributed or published for any purpose without prior written approval of UNICON. This document is for

the general information and does not take into account the particular investment objectives, financial situation or needs of any individual customer, and it

does not constitute a personalised recommendation of any particular security or investment strategy. Before acting on any advice or recommendation in this

document, a customer should consider whether i t is suitable given the customer’s particular circumstances and, if necessary, seek professional advice. Certain

transactions, including those involving futures, options, and high yield securities, give rise to substantial risk and are not suitable for all investors. UNICON,

its associates or group companies do not represent or endorse the accuracy or reliability of any of the information or content of the document and reliance

upon it is at your own risk.

UNICON, its associates or group companies, expressly disclaims any and all warranties, express or implied, including without limitation warranties of

merchantability and fitness for a particular purpose with respect to the document and any information in it. UNICON, its associates or group companies, shall

not be liable for any direct, indirect, incidental, punitive or consequential damages of any kind with respect to the document. No part of this publication may

be reproduced, stored in a retrieval system, or transmitted, on any form or by any means, electronic, mechanical, photocopying, recording, or otherwise,

without the prior written permission of Unicon Financial Intermediaries Pvt. Ltd.

Address:

Wealth Management

Unicon Financial Intermediaries Pvt. Ltd.

2nd Floor, VILCO Center, 8 Subhash Road,

Vile Parle (E), Mumbai 400 057

Ph: 022-3390 1234

Email: [email protected]

![Financial Result Updates [Company Update]](https://static.fdocuments.in/doc/165x107/577c78191a28abe0548eb963/financial-result-updates-company-update.jpg)