Howard Rye Institute_November 21 2015-2-2

52

Federal Reserve Bank of Boston Union of Minority Neighborhoods Howard Rye Institute Anthony Poore Ana Patricia Muñoz Kaili Mauricio Robert Clifford November 21, 2015 “The views expressed here do not necessarily represent those of the Federal Reserve Bank of Boston or the Federal Reserve System”

-

Upload

horace-small -

Category

Documents

-

view

60 -

download

0

Transcript of Howard Rye Institute_November 21 2015-2-2

Federal Reserve Bank of Boston

Union of M

inority Neighborhoods

How

ard Rye Institute A

nthony Poore A

na Patricia Muñoz

Kaili Mauricio

Robert Clifford

Novem

ber 21, 2015

“The views expressed here do not necessarily represent those of the Federal Reserve Bank of Boston or the Federal Reserve System

”

Federal Reserve Bank of Boston REG

ION

AL &

CO

MM

UN

ITY OU

TREACH

2

�M

ission �

The Federal Reserve Bank of Boston promotes econom

ic grow

th in lower-incom

e comm

unities by convening stakeholders, conducting research, and identifying approaches that w

ork.

�Focal A

reas �

Smaller Industrial C

ities – Working C

ities Challenge

�H

ousehold Financial Stability – Children’s Savings

Accounts

�W

orkforce Developm

ent - Fintech Internship Program

Ana Patricia M

uñoz Regional and C

omm

unity Outreach D

epartment, Federal Reserve Bank of Boston

The views expressed here do not necessarily represent those of the Federal Reserve Bank of Boston or the Federal Reserve System

.

3

THE C

OLO

R O

F WEA

LTH IN

BOSTO

N

ww

w.bostonfed.org/color-of-w

ealth

4

Kenneth Galbraith

“Societies never really become

effectively concerned with social

problems until they learn to m

easure them

”

Importance of w

ealth

�W

ealth allows fam

ilies to make investm

ents in education, and business creation, and to cover expenses in case of m

edical emergencies or job loss.

�A

sset poverty is shown to be m

ore persistent than income poverty.

�N

et worth is the econom

ic indicator in which w

hites and comm

unities of color are m

ost disparate

�A

true poverty-reduction policy should provide incentives for the poor to accum

ulate assets. (Wolf and C

aner 2004).

�Sem

inal work by Sherraden (1991) and O

liver and Shapiro (1995) underscored the im

portance of implem

enting policies that help reduce the w

ealth gap

5

Importance of w

ealth

Inflow: incom

e

Stock: wealth

Outflow

: expenditure

Measuring w

ealth (net worth)

ASSETS LIA

BILITIES (DEBTS)

Savings accounts C

hecking accounts Retirem

ent accounts Bonds Stocks H

ome

Vehicle Business equity

Mortgages

Auto loans

Credit card debt

Medical debt

Student loans

Wealth (net w

orth) = assets - liabilities

Measuring w

ealth: widening racial

wealth gap at the national level

8

79,650

110,500

7,546 6,314

9,925 7,683

0

20,000

40,000

60,000

80,000

100,000

20002011

Med

ian N

et Wo

rth o

f U.S. H

ou

seho

lds, 2

00

0 an

d 2

01

1

White, not Hispanic

BlackHispanic

X11 X8

X18 X14

Source: U.S. C

ensus Bureau, Survey of Income and Program

Participation. Note: Blacks include H

ispanics.

U.S. dollars

Measuring w

ealth

�Tw

o shortcomings of these surveys:

�They don’t provide enough inform

ation by race and ethnicity.

�M

ost surveys provide data only at the national level.

�To address these lim

itations, we partnered w

ith the Ford Foundation and D

uke University's C

onsortium on Social

Equity to bring the National A

sset Scorecard for C

omm

unities of Color (N

ASC

C) to the Boston M

etropolitan A

rea

9

The NA

SCC

project is funded by the Ford Foundation and the Federal Reserve Bank of Boston (for the Boston data). W

illiam D

arity, Jr. (Duke U

niversity) and Darrick H

amilton (The N

ew School) serve as prim

ary investigators. NA

SCC

-Boston project m

anager is Ana Patricia M

uñoz.

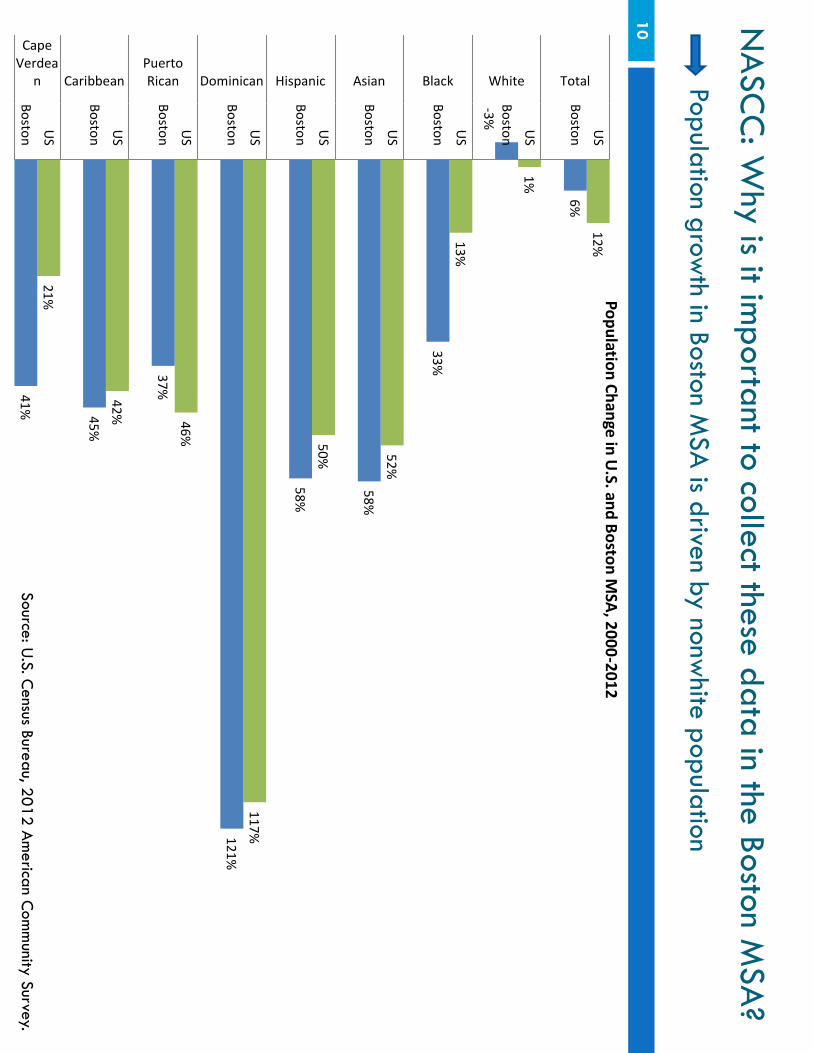

NA

SCC

: Why is it im

portant to collect these data in the Boston MSA

? Population grow

th in Boston MSA

is driven by nonwhite population

10

12%

6%

1%

-3%

13%

33%

52%

58%

50%

58%

117% 121%

46%

37% 42%

45%

21%

41%

US

BostonUS

BostonUS

BostonUS

BostonUS

BostonUS

BostonUS

BostonUS

BostonUS

Boston

TotalWhiteBlackAsianHispanicDominicanPuertoRicanCaribbean

CapeVerdea

n

Po

pu

lation

Ch

ange in

U.S. an

d B

osto

n M

SA, 2

00

0-2

01

2

Source: U.S. Census Bureau, 2012 A

merican C

omm

unity Survey.

11 The Color of W

ealth in Boston: Summ

ary of findings

Source: Muñoz, A

na Patricia, Marlene Kim

, Mariko C

hang, Regine Jackson, Darrick H

amilton, and W

illiam D

arity. (2015). The color of wealth in Boston.

Com

munity D

evelopment D

iscussion Paper, Federal Reserve Bank of Boston, Duke U

niversity, The New

School. ww

w.bostonfed.org/color-of-w

ealth

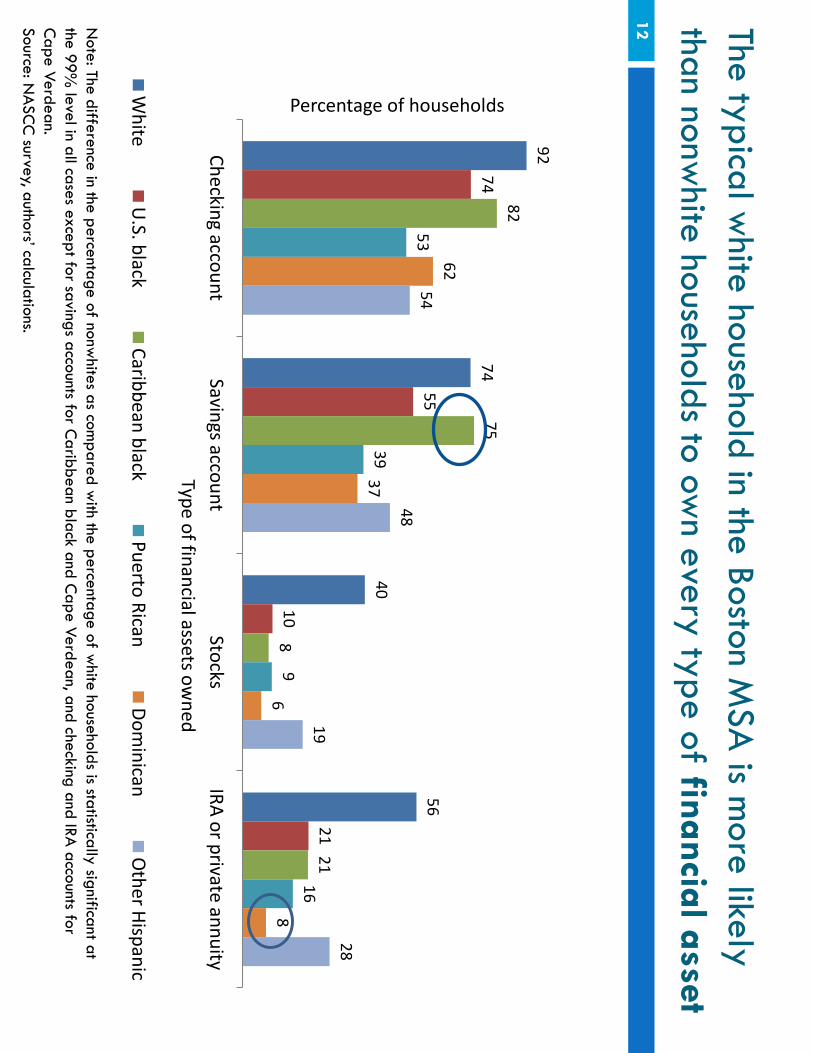

The typical white household in the Boston M

SA is m

ore likely than nonw

hite households to own every type of financial asset

12

92

74

40

56

74

55

10

21

82 75

8

21

53

39

9 16

62

37

6 8

54 48

19 28

Checking accountSavings account

StocksIRA or private annuity

Percentage of households

Type of financial assets owned

White

U.S. black

Caribbean blackPuerto Rican

Dominican

Other Hispanic

Note: The difference in the percentage of nonw

hites as compared w

ith the percentage of white households is statistically significant at

the 99% level in all cases except for savings accounts for C

aribbean black and Cape Verdean, and checking and IRA

accounts for C

ape Verdean. Source: N

ASC

C survey, authors’ calculations.

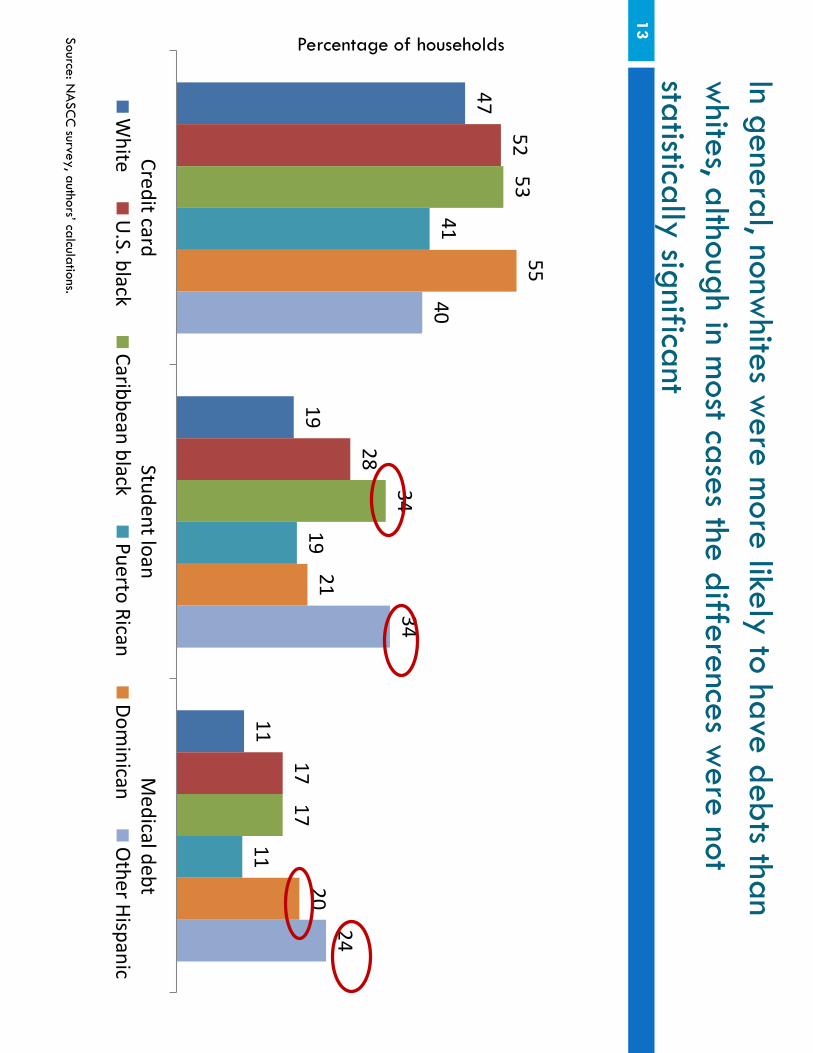

In general, nonwhites w

ere more likely to have debts than

whites, although in m

ost cases the differences were not

statistically significant 13

47

19

11

52

28

17

53

34

17

41

19

11

55

21 20

40 34

24

Credit cardStudent loan

Medical debt

White

U.S. black

Caribbean blackPuerto Rican

Dominican

Other Hispanic

Percentage of households

Source: NA

SCC

survey, authors’ calculations.

The white households in the Boston M

SA are m

ore likely than nonw

hite households to own every type of tangible asset

14

79 84

34

51 49

84

21

61

17

69

34

77

HouseVehicle

Percentage of households

Type

of tan

gible

asset

White

U.S. black

Caribbean blackPuerto Rican

Dominican

Other Hispanic

Note: The difference in the percentage of nonw

hites as compared w

ith the percentage of white households is statistically significant at

the 99% level in all the cases for hom

eownership. A

s for vehicle ownership the difference is statistically significant for U.S. blacks,

Puerto Ricans, and Dom

inicans. Source: N

ASC

C survey, authors’ calculations.

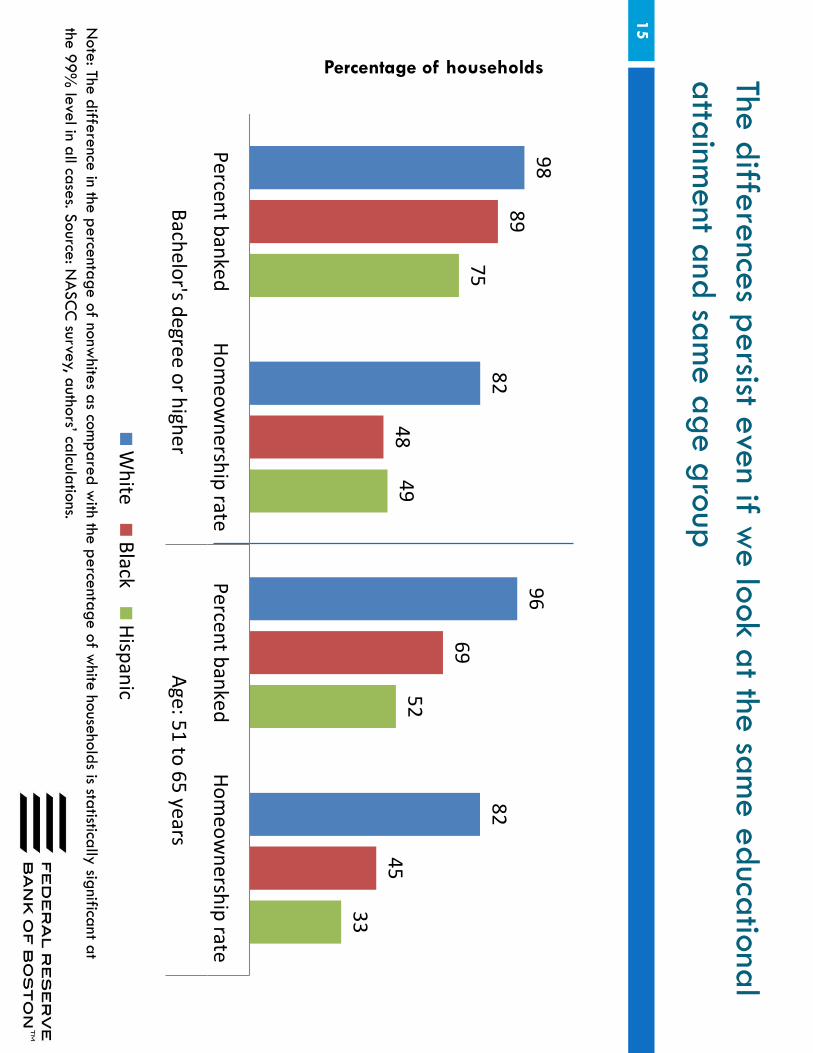

The differences persist even if we look at the sam

e educational attainm

ent and same age group

15

Percentage of households

Note: The difference in the percentage of nonw

hites as compared w

ith the percentage of white households is statistically significant at

the 99% level in all cases. Source: N

ASC

C survey, authors’ calculations.

98

82

96

82 89

48

69

45

75

49 52

33

Percent bankedHom

eownership rate

Percent bankedHom

eownership rate

Bachelor's degree or higherAge: 51 to 65 years

White

BlackHispanic

Percentage of banked households, homeow

nership and vehicle ownership

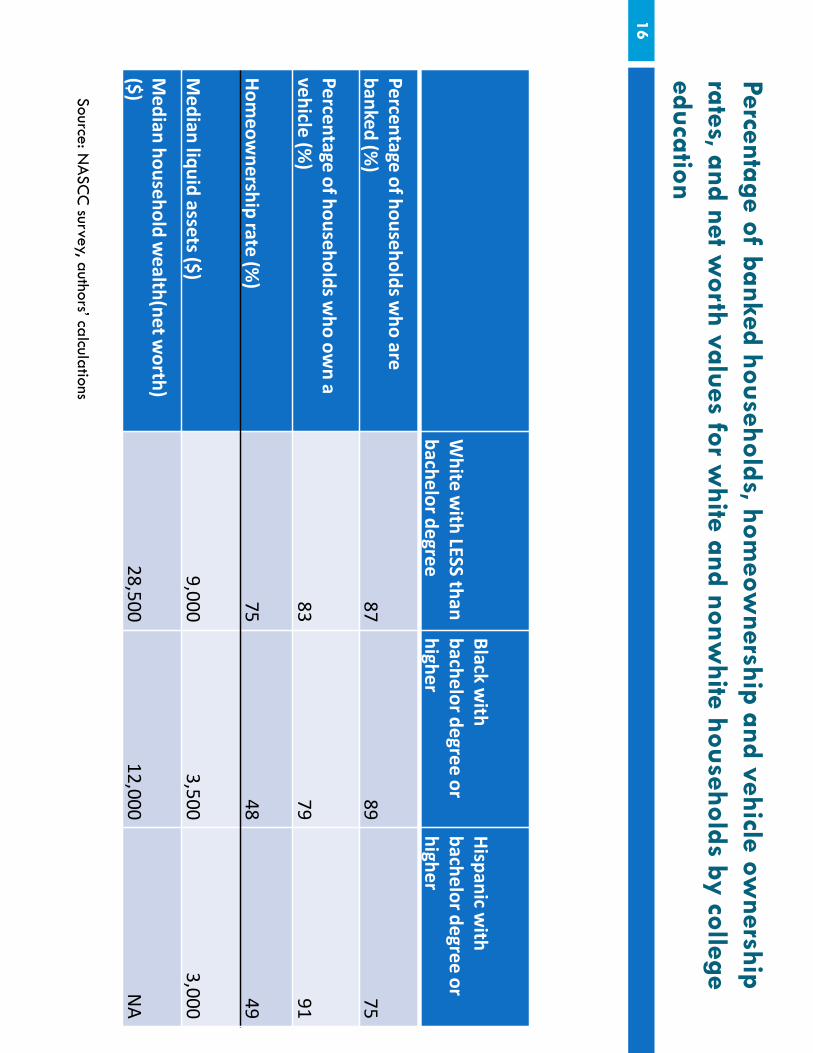

rates, and net worth values for w

hite and nonwhite households by college

education 16

W

hite

with

LESS than

b

ache

lor d

egre

e

Black w

ith

bach

elo

r de

gree

or

high

er

Hisp

anic w

ith

bach

elo

r de

gree

or

high

er

Pe

rcen

tage o

f ho

use

ho

lds w

ho

are

ban

ked

(%)

87 89

75

Pe

rcen

tage o

f ho

use

ho

lds w

ho

ow

n a

veh

icle (%

) 83

79 91

Ho

me

ow

nersh

ip rate

(%)

75 48

49

Me

dian

liqu

id assets ($

) 9,000

3,500 3,000

Me

dian

ho

use

ho

ld w

ealth

(net w

orth

) ($

) 28,500

12,000 N

A

Source: NA

SCC

survey, authors’ calculations

Median value of liquid assets (in dollars)

17

25,000

670

3,500

150

20

150

700

White

U.S. black

Caribbean black

Cape V

erdean

Puerto Rican

Dom

inican

Other H

ispanic

Note: Liquid assets, w

hich can quickly be converted into cash, include money in savings and checking accounts, stocks, m

oney m

arket funds, and government bonds. The category excludes cash on hand.

Source: NA

SCC

survey, authors’ calculations

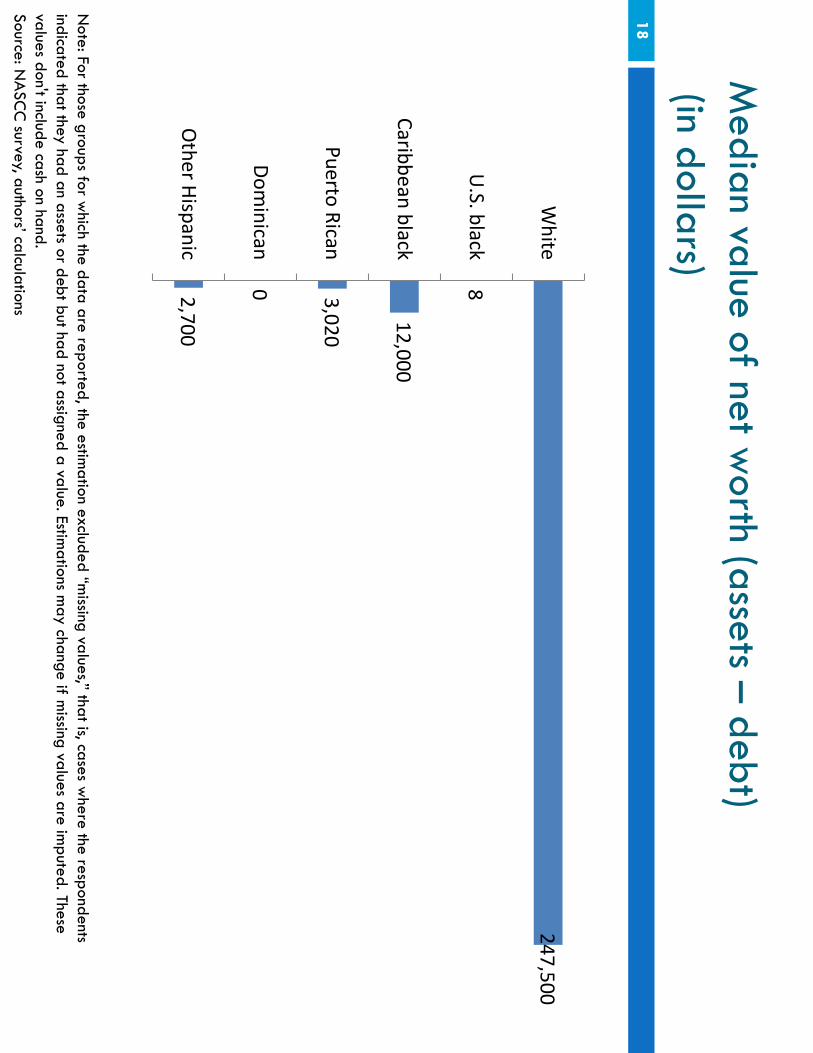

Median value of net w

orth (assets – debt) (in dollars)

18

Note: For those groups for w

hich the data are reported, the estimation excluded “m

issing values,” that is, cases where the respondents

indicated that they had an assets or debt but had not assigned a value. Estimations m

ay change if missing values are im

puted. These values don't include cash on hand. Source: N

ASC

C survey, authors’ calculations

247,500

8

12,000

3,020

0 2,700

White

U.S. black

Caribbean black

Puerto Rican

Dominican

Other Hispanic

Other variables of interest

U

se o

f payd

ay le

nd

ing

Re

spo

nd

en

t or fam

ily h

as be

en

in jail

Sen

ds re

mittan

ces

regu

larly

White

1.2 8.7

2.6 U.S. black

4.0 21.2**

8

Caribbean black 1.4

3.1 26.6***

Cape Verdean 1.0

7.8 16.6**

Puerto Rican 2.5

12.9 6

Dominican

8.7** 7.4

32.3*** O

ther Latino 6.4*

8.7 17**

NEC

5.5 16.6

17.3

Source: NA

SCC

-Boston. Notes: Black, w

hite and Asian are non-H

ispanic.

Financial Resources in Kinship and Social

Netw

orks 20

Source: Tatjana Meschede et. al. (2015), “Financial Resources in Kinship and Social N

etworks: Flow

and Relationship to Household W

ealth by Race and Ethnicity am

ong Boston Residents”, Boston Fed Com

munity developm

ent discussion paper

Percentage of Respondents Receiving Large Financial Gift/Inheritance and Sending

Money in Support of Fam

ily Mem

bers by Race/Ethnicity

Some takeaw

ays 21

�Racial w

ealth gap much w

ider that income w

ealth gap

�Im

portance of looking at both sides of the balance sheet: assets and debts

�W

ealth is transmitted intergenerationally

�N

onwhite groups in the study have very little to rely on in case of an em

ergency

�The staggering disparities should urge us to find policies that can help narrow

the w

ealth gap

�Policy solutions are com

plex and need to use a multifaceted approach.

�Such policies should consider the w

ide diversity among nonw

hite populations and be targeted or adapted accordingly

�Som

e solutions will have to be driven at the national level. W

hat can be done locally?

�Education alone w

on’t close the racial wealth gap

�Im

portance of collecting data on assets and debts at the local level, including disaggregated inform

ation for nonwhite groups.

The views expressed here do not necessarily represent those of the

Federal Reserve Bank of Boston or the Federal Reserve System

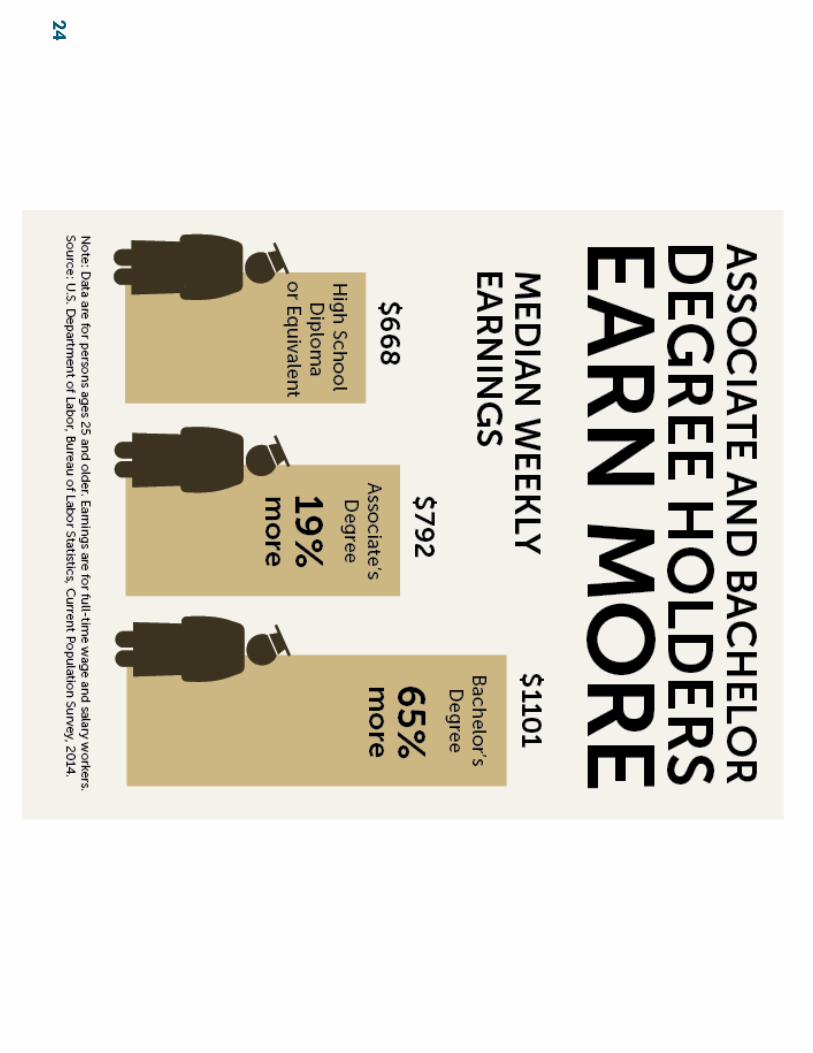

The Cost of Post-Secondary Education and Student D

ebt in New

England

Kaili Mauricio - Regional and C

omm

unity Outreach D

epartment, Federal Reserve Bank of Boston

Robert C

lifford -Research Departm

ent, Federal Reserve Bank of Boston

23

Less than 9th

Grade

Incomplete

High

School

High

School or Equivalent

Some

College

Associate's C

ollege G

raduate

United States

4.0%

8.1%

24.1%

23.3%

8.5%

22.5%

9.5%

New

England 2.4%

5.6%

22.8%

19.5%

7.3%

28.0%

14.5%

Massachusetts

2.5%

5.1%

19.9%

17.7%

6.5%

30.9%

17.4%

Connecticut

2.8%

6.2%

24.0%

20.3%

6.9%

25.3%

14.6%

Vermont

1.0%

5.6%

28.6%

19.2%

8.4%

27.4%

9.8%

New

H

ampshire

1.4%

5.6%

25.7%

21.4%

9.4%

26.8%

9.7%

Rhode Island 3.6%

7.1%

22.9%

22.2%

8.5%

24.9%

10.8%

Maine

1.0%

5.0%

30.1%

24.4%

9.5%

22.8%

7.1%

Educational attainment by state

and region, ages 25-34

Source: U

.S. C

ensus Bureau. (2009-2013). 2013 A

merican C

omm

unity Survey 5-Y

ear E

stimates. R

etrieved fromhttp://factfinder2.census.gov

24

25

26

Story Time!

27

�Tw

o siblings �

Story of averages and medians

�O

ne does well goes to a m

ore selective school �

The other takes a different path but still goes to school after graduating high school.

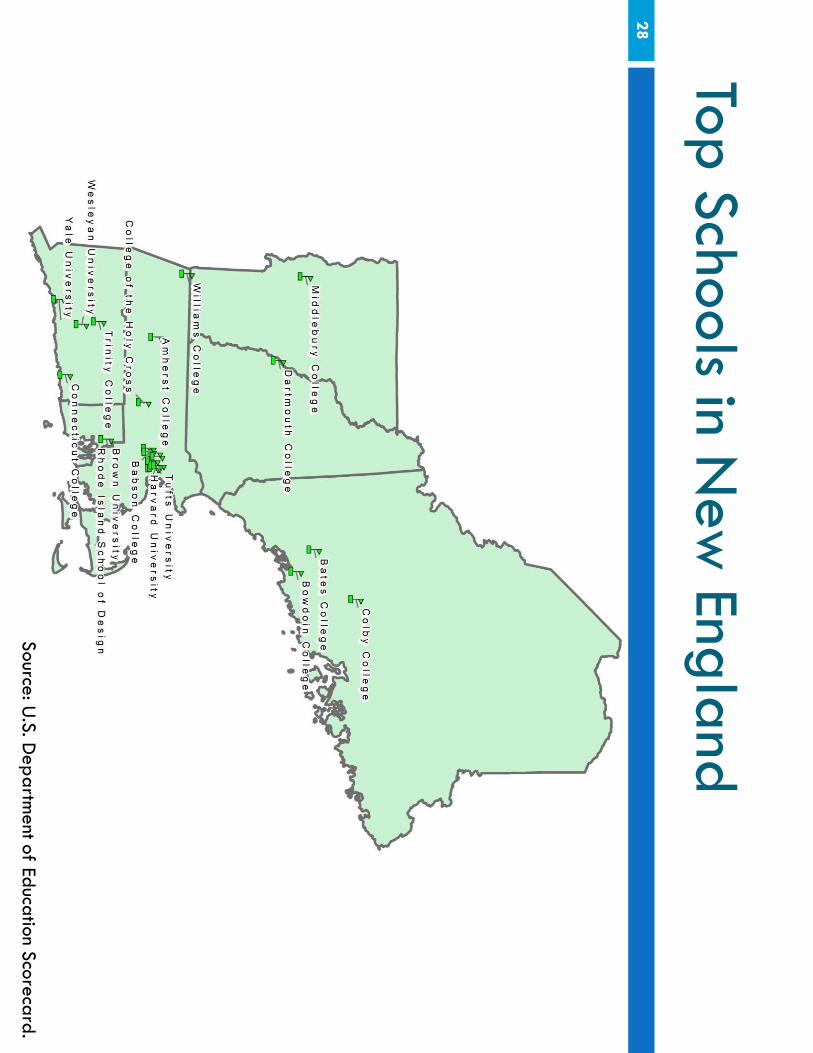

Top Schools in New

England 28

Source: U.S. D

epartment of Education Scorecard.

First Sibling Expectations 29

Source: Authors calculation from

U.S. Departm

ent of Education Scorecard. *2013 Cost

Sarah (Se

lective

Scho

ol)

Cost

$43,062*

Graduating D

ebt $19,038

Withdraw

Debt

$18,507 2

-year / 3

-year d

efault

rates

1.5% / 1.7%

Not w

orking 2 years out 7.4%

Earnings 2 years out $58,001

Earnings 6 years out $71,249

Two-year For Profit Schools in N

ew

England 30

Source: U.S. D

epartment of Education Scorecard.

Expectations? 31

Source: Authors calculation from

U.S. Departm

ent of Education Scorecard.*2013 costs

Sarah (Se

lective

Scho

ol)

Julie

t (2

-Year Fo

r-pro

fit)

Cost

$43,062* $27,920*

Graduating D

ebt $19,038

$13,162

Withdraw

Debt

$18,507 $7,249

2-ye

ar / 3-ye

ar defau

lt rate

s 1.5%

/ 1.7%

11.4% / 17.1%

N

ot working 2 years

out 7.4%

19.1%

Earnings 2 years out $58,001

$33,015

Earnings 6 years out $71,249

$36,048

Student loans are an investment in hum

an capital 32

�Loans enable a large portion of the population enrolled in college to attend higher education institutions.

�Student loans are an investm

ent in the acquisition of skills and credentials in exchange for future earnings.

�W

hile the return to obtaining a post-secondary education is persistent, borrow

ers need to make

complicated assum

ptions about costs and benefits w

hen deciding whether, w

hen, and where to attend.

The wage prem

ium for post-secondary

education is persistent and increases over-time

33

$0

$20,000

$40,000

$60,000

$80,000

$100,000

$120,000

25-2930-34

35-3940-44

45-4950-54

55-5960-64

65+

Master's D

egree or above

Bachelor's Degree

Associate's D

egree

Some C

ollege, no degree

High School

Less than High School

Source: Authors calculation using the U

.S. Census Bureau, 2013 A

merican C

omm

unity Survey. N

ote: Sample is restricted to those 25+

and employed.

Average W

age and Salary Income in N

ew England by A

ge and Education, 2013

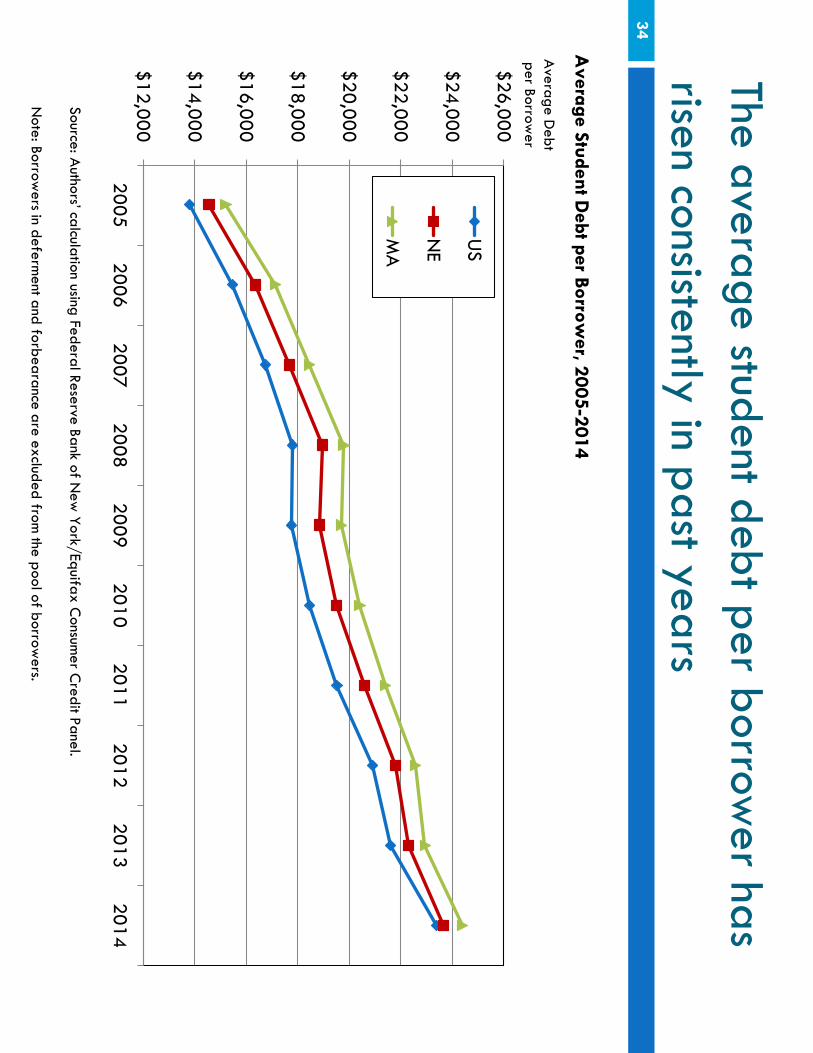

The average student debt per borrower has

risen consistently in past years 34

$12,000

$14,000

$16,000

$18,000

$20,000

$22,000

$24,000

$26,000

20052006

20072008

20092010

20112012

20132014

US

NE

MA

Source: Authors’ calculation using Federal Reserve Bank of N

ew York/Equifax C

onsumer C

redit Panel. N

ote: Borrowers in deferm

ent and forbearance are excluded from the pool of borrow

ers.

Average Student D

ebt per Borrower, 2005-2014

Average D

ebt per Borrow

er

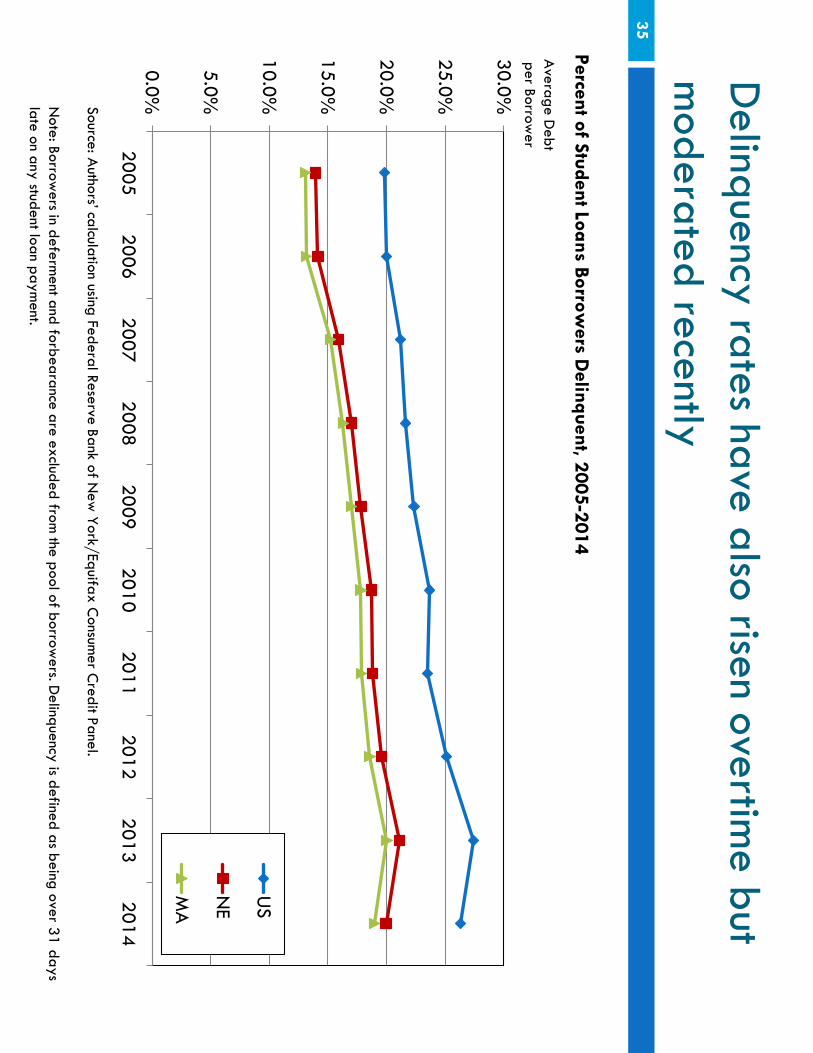

Delinquency rates have also risen overtim

e but m

oderated recently 35

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

20052006

20072008

20092010

20112012

20132014

US

NE

MA

Source: Authors’ calculation using Federal Reserve Bank of N

ew York/Equifax C

onsumer C

redit Panel. N

ote: Borrowers in deferm

ent and forbearance are excluded from the pool of borrow

ers. Delinquency is defined as being over 31 days

late on any student loan payment.

Percent of Student Loans Borrowers D

elinquent, 2005-2014

Average D

ebt per Borrow

er

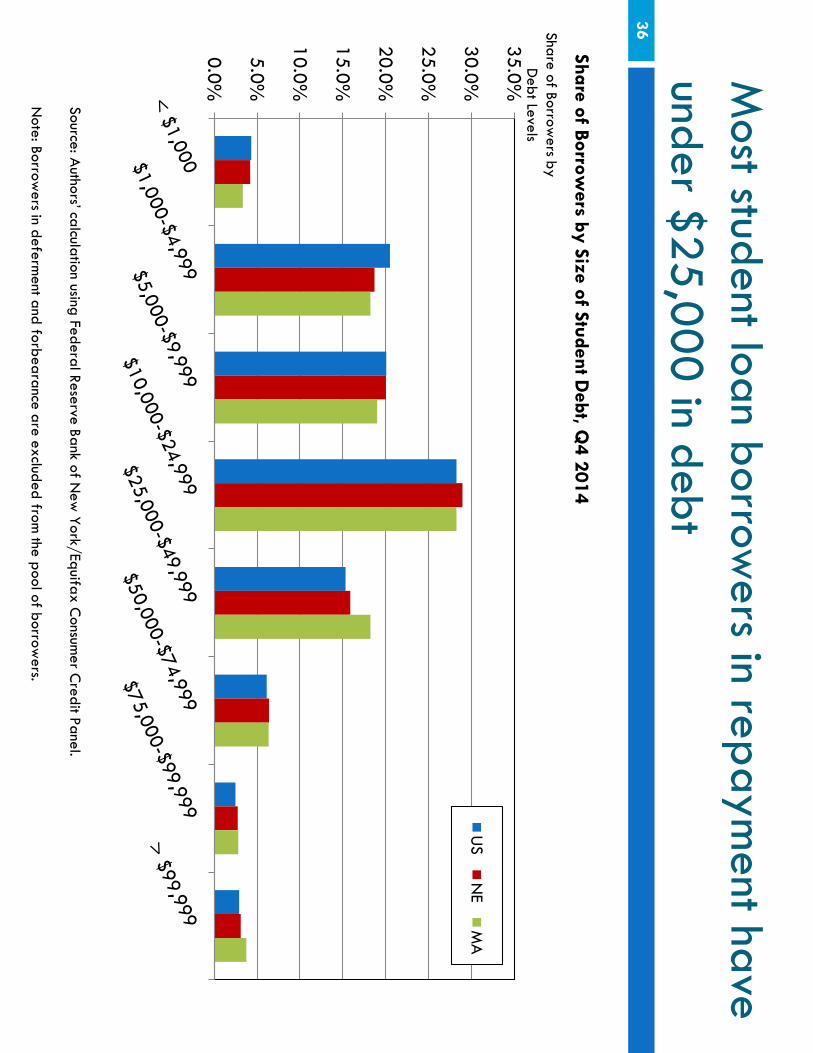

Most student loan borrow

ers in repayment have

under $25,000 in debt 36

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

US

NE

MA

Source: Authors’ calculation using Federal Reserve Bank of N

ew York/Equifax C

onsumer C

redit Panel. N

ote: Borrowers in deferm

ent and forbearance are excluded from the pool of borrow

ers.

Share of Borrowers by Size of Student D

ebt, Q4 2014

Share of Borrowers by

Debt Levels

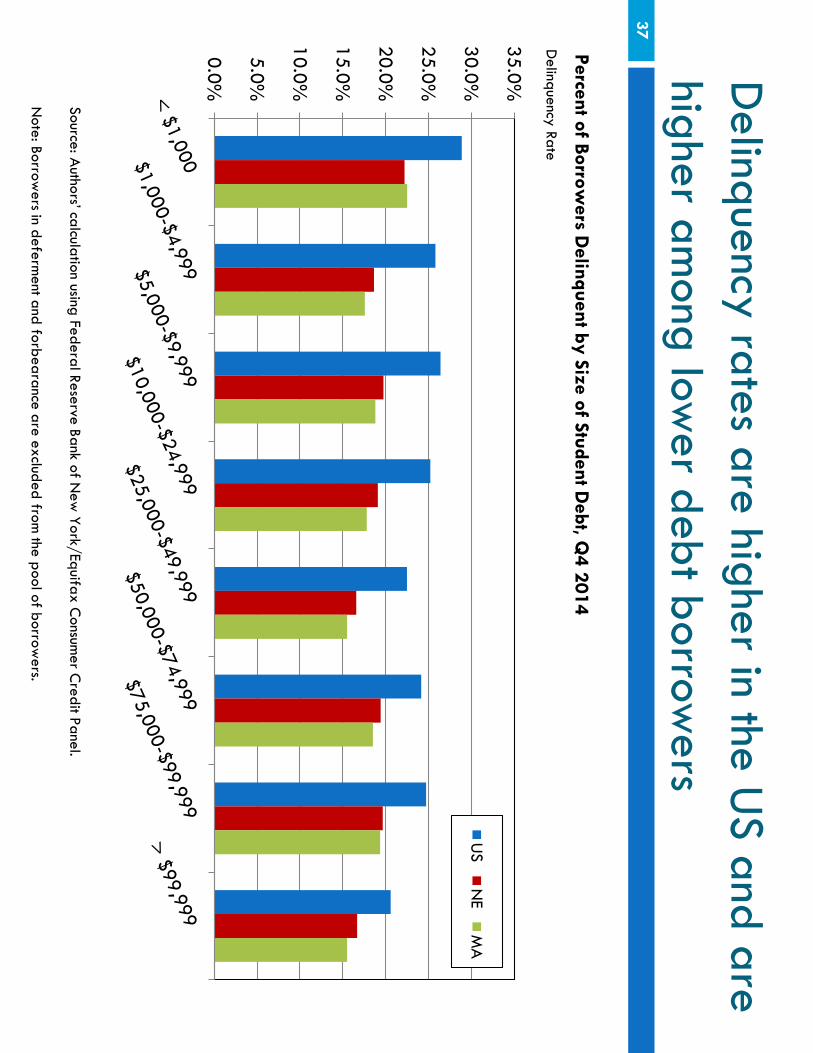

Delinquency rates are higher in the U

S and are higher am

ong lower debt borrow

ers 37

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

US

NE

MA

Source: Authors’ calculation using Federal Reserve Bank of N

ew York/Equifax C

onsumer C

redit Panel. N

ote: Borrowers in deferm

ent and forbearance are excluded from the pool of borrow

ers.

Percent of Borrowers D

elinquent by Size of Student Debt, Q

4 2014 D

elinquency Rate

Federal Reserve Bank of Boston

Com

plementary Solutions

to Student Debt &

Their Im

plications for M

assachusetts

What are C

hildren’s Savings Accounts (C

SAs)

�Long-term

asset-building accounts established for children, as early as birth, and allow

ed to grow over their lifetim

e.

�Tw

o Product Models

�A

deposit-only savings account offered by traditional lender. (K2C M

odel, San Francisco)

�A

529 savings plan (named for the relevant section of the federal tax code) is a state-

sponsored, tax-preferred savings plan for qualified post-secondary education expenses. (H

arold Alfond, M

aine)

�Either m

odel can provide savings matches or other incentives to encourage positive

savings behaviors – particularly those of lower incom

e – to save.

39

Major D

evelopments in the C

SA Field

40

Source: Center for Enterprise D

evelopment (C

FED)

Why D

o We C

are?

9C

SAs have the potential to expand econom

ic and educational opportunities for low

- and moderate incom

e families &

children.

9C

SAs support the interest of States in increasing the percentage of

its population with college degrees, certificates and credentials

(Lumina Foundation G

oal 2025). 9

Massachusetts G

oal: 60% by 2020

College A

ttainment am

ong Adults A

ges 25-64 : 51.5%

9C

SAs represent a long term

investment in our citizenry w

hile helping address and alleviate N

ew England’s/M

assachusetts middle skills

gap by addressing secondary education affordability. 9

CSA’s encourage and leverage, fam

ily, public and private capital resources.

41

Principles of Effective CSA

Design

42

�

Allow

universal, automatic child enrollm

ent. �

Carry a national footprint and equitable am

ong different jurisdictions.

�A

llow identification and engagem

ent with accounts, including

parent and child deposits, in-person and via electronic interface. �

Restrict accounts to asset-building purposes, but not strictly to higher education.

�Be adm

inistratively efficient in all essential operations, including disbursem

ent, and sustainable at scale, with tolerably low

adm

inistrative costs and integration into existing policy systems.

�A

dequately protect consumers, w

ith publicly provided accounts or private accounts w

ith substantial regulatory oversight

Moving Tow

ard a Policy Agenda for Im

proving Children's Savings A

ccount Delivery System

s W

illiam Elliott III, M

elinda K. Lewis, A

nthony Poore, and Brian Clarke, C

omm

unity Developm

ent Issue Brief, No. 1, 2015

New

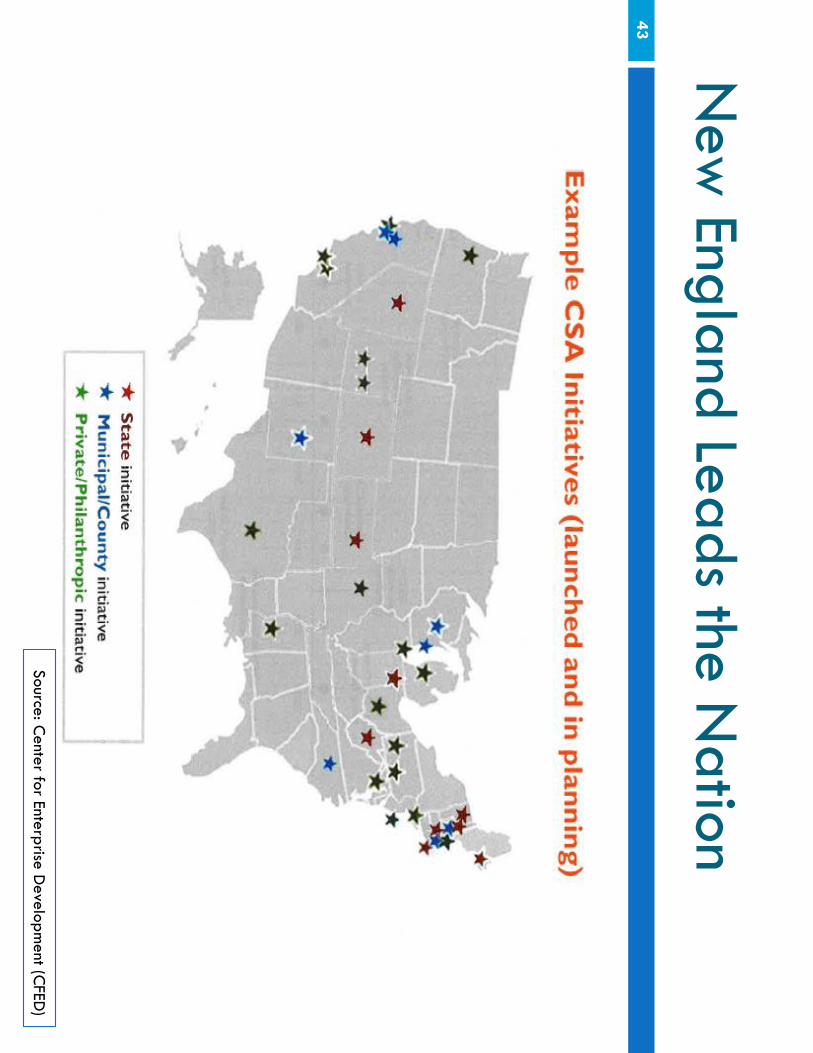

England Leads the Nation

43

Source: Center for Enterprise D

evelopment (C

FED)

New

England Leads the Nation

New

England Leads the Nation

45

New

England Leads the Nation

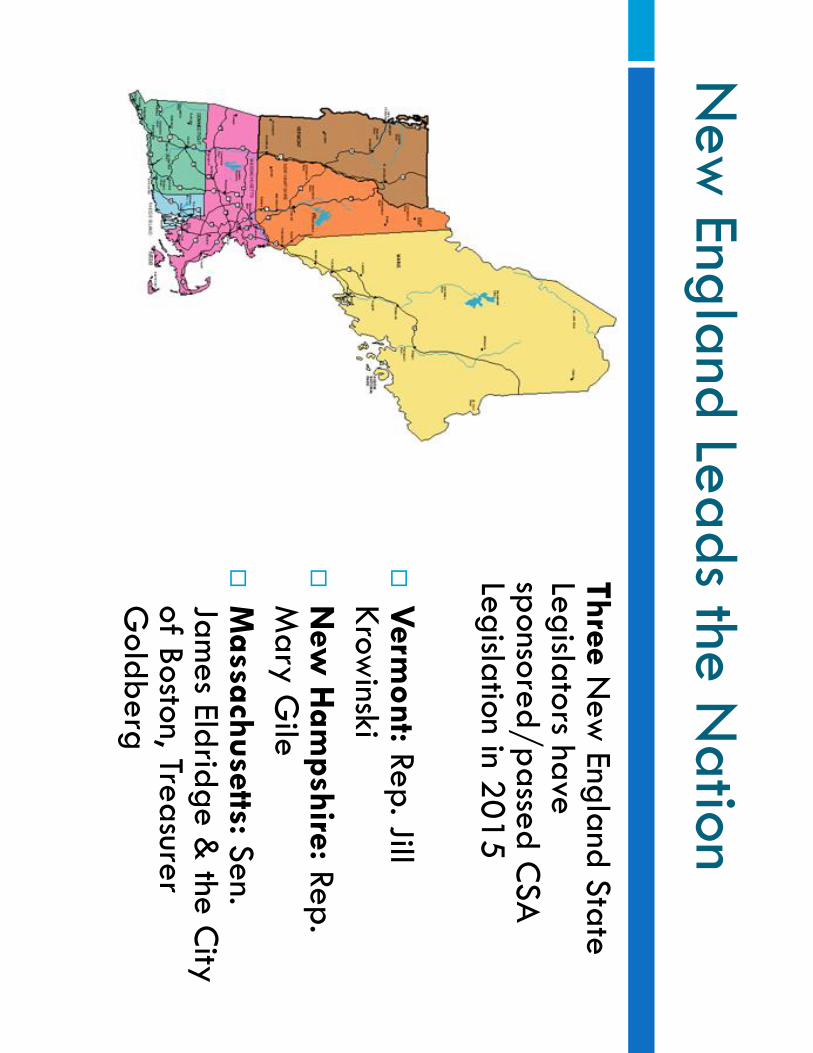

Three New

England State Legislators have sponsored/passed C

SA

Legislation in 2015 �

Verm

ont: Rep. Jill Krow

inski �

New

Ham

pshire: Rep. M

ary Gile

�M

assachusetts: Sen. Jam

es Eldridge & the C

ity of Boston, Treasurer G

oldberg 46

CSA

s Continue to G

ain Mom

entum

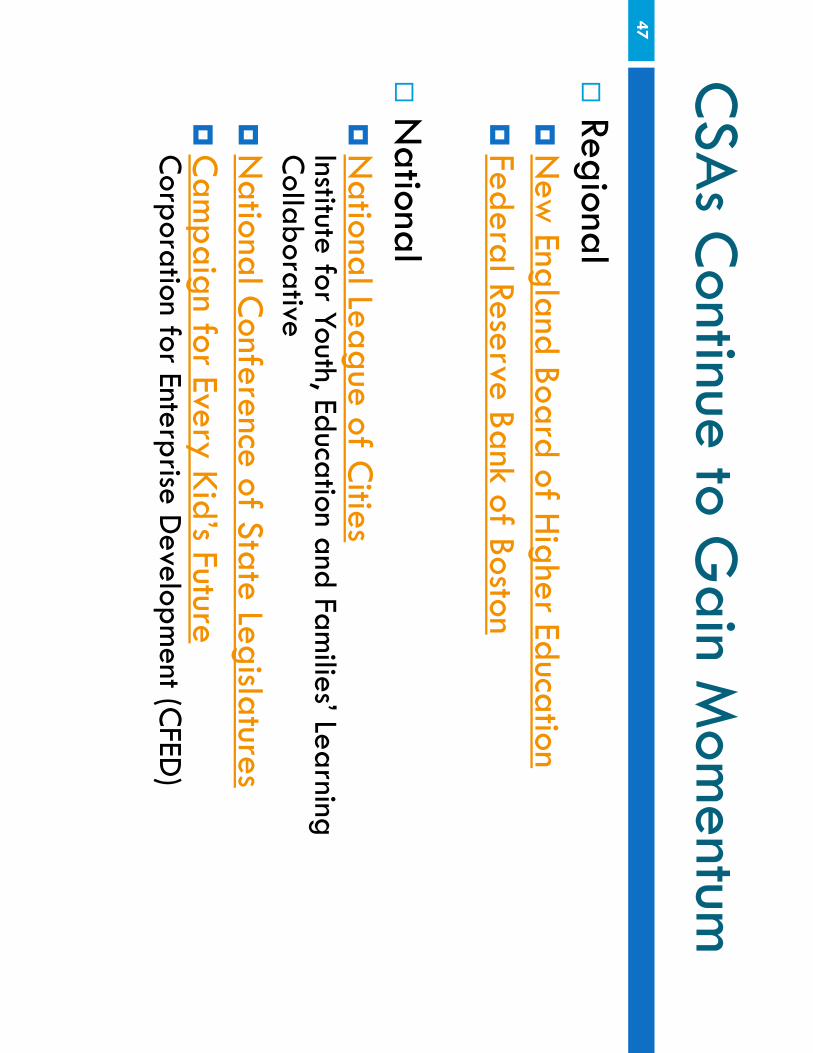

47

�Regional �

New

England Board of Higher Education

�Federal Reserve Bank of Boston

�

National �

National League of C

ities Institute for Youth, Education and Fam

ilies’ Learning C

ollaborative �

National C

onference of State Legislatures �

Cam

paign for Every Kid’s Future C

orporation for Enterprise Developm

ent (CFED

)

So What’s H

appening in Massachusetts ?

48

�C

omm

unity Based Efforts �

Inversant (formally know

n as Fuel Education)

�M

unicipal Efforts �

City of Boston - Fall 2016

�C

omm

onwealth (Sen. Eldridge &

Rep. Sannicandro) �

S664/ H.1067: A

n Act to create a college savings program

for every child born in M

assachusetts that would create a

college savings account for every child born in the state.

�M

A State Treasurer D

eborah Goldberg

�Pilot Program

: Fall 2015

What D

oes Early Research Suggest: A

ssets, Empow

erment &

Opportunity

College Readiness

�H

igher student and parental college expectations.

�W

eak but positive effects on reading & m

ath.

�H

igher high school GPA

�C

ollege Bound Identity

College A

ccess

�Even college savings of less than $500 increase college entry for low

and moderate incom

e students.

�3X

s more likely to enroll in college than w

ith no savings account.

�C

ollege Savers Identity

49

Elliot, W. and Lew

is (2013). Are student loans w

idening the wealth gap in A

merica? It’s a question of equity. Law

rence, KS: A

ssets & Education Initiative (A

EDI).

What D

oes Early Research Suggest: A

ssets, Empow

erment &

Opportunity

College C

ompletion

�Even college savings of less than $500 increase college com

pletion for low and m

oderate income students.

�4X

s more likely to graduate college than w

ith no savings account.

Young adult graduates who had savings as adolescents:

�2X

s more likely to ow

n savings accounts (banked/unbanked)

�2xs m

ore likely to own credit cards

�4xs m

ore likely to own stocks

50

Elliot, W. and Lew

is (2013). Are student loans w

idening the wealth gap in A

merica? It’s a question of equity. Law

rence, KS: A

ssets & Education Initiative (A

EDI).

What A

re Some O

ther Com

plementary Solutions

to Student Debt?

51

�Scholarship &

Mentoring A

pproaches �

Tennessee Promise

�O

regon Promise

�Loan Repaym

ent Assistance

�A

drian College: A

drian Plus Program

�Yale Law

School: Career O

ptions Assistance Program

�A

sset Based Approaches

�M

atched Savings Programs/IDA

s �

Children’s Savings A

ccounts

52

Anthony Poore

Deputy D

irector, R&C

O

ww

w.bostonfed.org/com

mdev/childrens-savings-accounts