How Well Do Professionals Forecast Exchange Rates ...inceo/Survey Based Expectations.pdf · How...

36

How Well Do Professionals Forecast Exchange Rates? Evidence from Survey Expectations † Onur Ince * Tanya Molodtsova ** April 28, 2015 Abstract This paper examines rationality and forecasting accuracy of exchange rate survey expectations from two datasets that include 10 major and 40 minor currencies during the recent two decades. Based on the tests of unbiasedness and orthogonality, the forecasts for minor currencies are relatively more rational than the forecasts for major currencies at the short horizon of 3 months, and the forecasts for major currencies are relatively more rational at longer horizons of 12 and 24 months. We evaluate the predictive accuracy and directional accuracy of professional exchange rate forecasts and find that the evidence of forecasting accuracy is stronger at longer than at shorter forecast horizons and for minor currencies than for major currencies. JEL Classifications: C53, F31, F37, F47, G17 † We thank Alan Teck, Tatevik Shekhposyan, Olivier Coibion and participants at the Canadian Economic Association Meetings 2013 and Western Economic Association Meetings 2014 for helpful comments and discussions. * Department of Economics, Appalachian State University, Boone, NC 28608. Tel: +1 (828) 262-4033 Email: [email protected] ** Department of Economics, Appalachian State University, Boone, NC 28608. Tel: +1 (828) 262-2117 Email: [email protected]

Transcript of How Well Do Professionals Forecast Exchange Rates ...inceo/Survey Based Expectations.pdf · How...

How Well Do Professionals Forecast Exchange Rates?

Evidence from Survey Expectations†

Onur Ince*

Tanya Molodtsova**

April 28, 2015

Abstract

This paper examines rationality and forecasting accuracy of exchange rate survey expectations from two datasets that include 10 major and 40 minor currencies during the recent two decades. Based on the tests of unbiasedness and orthogonality, the forecasts for minor currencies are relatively more rational than the forecasts for major currencies at the short horizon of 3 months, and the forecasts for major currencies are relatively more rational at longer horizons of 12 and 24 months. We evaluate the predictive accuracy and directional accuracy of professional exchange rate forecasts and find that the evidence of forecasting accuracy is stronger at longer than at shorter forecast horizons and for minor currencies than for major currencies. JEL Classifications: C53, F31, F37, F47, G17

† We thank Alan Teck, Tatevik Shekhposyan, Olivier Coibion and participants at the Canadian Economic Association Meetings 2013 and Western Economic Association Meetings 2014 for helpful comments and discussions. * Department of Economics, Appalachian State University, Boone, NC 28608. Tel: +1 (828) 262-4033 Email: [email protected] ** Department of Economics, Appalachian State University, Boone, NC 28608. Tel: +1 (828) 262-2117 Email: [email protected]

1. Introduction

Exchange rate expectations play an important role in the literature on exchange rate

determination. Understanding how exchange rate expectations are formed is crucial for academic

analysis of exchange rate behavior, as well as for decision-making of both practitioners and

policymakers. Models of exchange rate determination in open-economy macroeconomics often

rely on assumptions about rationality of exchange rates expectations. It is practically impossible

to test the implications of theoretical exchange rate models, without running into the problem of

joint hypothesis testing in the absence of survey-based expectations. In addition to understanding

exchange rate behavior, the rationality assumption can have serious implications for evaluating

the effectiveness of many government policies. The availability of survey forecasts allows us to

evaluate the rational expectations hypothesis directly.

Although survey-based forecasts of other macroeconomic variables have been studied in

the literature for at least 60 years, research on rationality and accuracy of exchange rate forecasts

goes back only to the late 1980s. Limited data availability on professional exchange rate

forecasts is partially responsible for the short history of research on survey-based exchange rate

forecasts. Following early studies of Dominguez (1986) and Frankel and Froot (1987), many

researchers have studied the nature of exchange rate expectations using survey data. Engel

(1996) and Lewis (1995) summarize the literature on exchange rate expectations assuming

rational expectations. Takaji (1991), Macdonald (2000), and Jongen et al. (2007) summarize the

studies on survey-based exchange rate expectations. Two most commonly examined questions in

the literature on survey-based exchange rate expectations include rationality of the forecasts and

their predictive accuracy. We systematically evaluate these two questions for a sample of 10

major currencies and 40 minor currencies vis-à-vis the U.S. dollar over the last two decades.

Most of the previous studies on exchange rate forecasts, with the exception of Frankel

and Chinn (1993), Chinn and Frankel (1994, 2002), and Frankel and Poonawala (2010), focus

exclusively on major currencies. Conclusions about rationality and predictive accuracy of

exchange rate expectations in the literature on survey-based expectations depend on the sample

size, the set of countries that are considered, and estimation methods. Although the evidence is

mixed, existing studies predominantly find evidence against rationality of expectations and no

evidence of predictability of professional exchange rate forecasts.

1

In this paper, we systematically examine the characteristics of the exchange rate forecasts

for major and minor currencies at 3-, 6-, 12-, and 24-month horizons. We use two most

comprehensive datasets on survey-based expectations, Consensus Economics and FX4Casts. The

former is previously known as The Financial Times Currency Forecaster, and the latter as

Currency Forecasters’ Digest. These datasets contain exchange rate forecasts of 37 and 46

currencies vis-à-vis the U.S. dollar, respectively, with the sample period going back to January

1990 and ending in December 2012. Frankel and Poonawala (2010) consider exchange rate

forecasts for 35 currencies from Currency Forecasters’ Digest, including 15 minor currencies.

We expand the list of minor currencies from 15 to 40, combining both sources of data. The use

of the survey datasets that cover a large number of minor currencies, in addition to 10 major

currencies, over a broad range of forecast horizons during the last two decades allows us to study

systematic empirical regularities that couldn’t be observed so far.

We test the rationality of exchange rate expectations at 3-, 6-, 12-, and 24-month forecast

horizons using the unbiasedness and orthogonality tests. Even when unbiasedness and/or

orthogonality are rejected, exchange rate expectations can be rational under certain conditions.

These conditions include, for example, time-varying exchange rate process, peso problem, non-

linear forecasting model, or asymmetric loss function. In order to examine predictive accuracy of

the forecasts based on the mean squared prediction error (MSPE) comparison, we use Diebold

and Mariano (1995) and West (1996) tests (henceforth, DMW tests). for equal predictability of

survey forecasts relative to a random walk without drift1. In addition to MSPE-based tests, we

use Pesaran and Timmerman (1992) test for nonparametric dependence between the forecasts

and random walk benchmark. The advantage of using the direction of change tests of predictive

accuracy is that they do not impose any restrictions on the functional form of the forecasting

model and allow for learning behavior of exchange rate forecasters.

We find that the evidence of the forecast rationality and accuracy increases with the

horizon. The forecasts for minor currencies tend to be relatively more rational at the short

horizons of 3 and 6 months, while the forecasts for major currencies are relatively more rational

at the longer horizons of 12 and 24 months. The evidence of predictive accuracy is stronger for

minor than for major currencies, and it improves with the forecast horizon for both groups of

1 Since Meese and Rogoff (1983), evaluating exchange rate forecasts relative to the random walk benchmark has become a standard in the literature. We choose a more conservative benchmark of a random walk without drift that is more difficult to beat to reduce the possibility of finding spurious evidence of predictability.

2

countries. While the standard DMW statistics are unable to detect any evidence of predictive

accuracy at shorter forecast horizons for major currencies, the nonparametric tests indicate the

presence of significant dependence between actual and forecasted exchange rate depreciation.

This might suggest that the nature of the relationship is nonlinear, asymmetric, time-varying, or

all of the above.

2. Survey Data

We use the data on professional exchange rate forecasts from two data sources:

Consensus Economics and FX4casts, previously known as The Financial Times Currency

Forecaster and Currency Forecasters’ Digest, respectively. Both datasets contain exchange rate

forecasts for the same 9 major countries (Australia, Canada, Denmark, Japan, New Zealand,

Norway, Sweden, Switzerland, and the U.K.) plus the Euro Area during approximately the same

period between January 1990 and December 2012. In addition to 10 major currencies, Consensus

Economics contains forecasts for 27 minor currencies, and FX4casts reports forecasts for 37

minor currencies. Both data sets combined contain exchange rate forecasts for 40 minor

currencies.

We have excluded some countries with tightly fixed exchange rates. Following Frankel

and Poonawala (2010), we didn’t exclude currencies that have relatively stable exchange rates or

operate under capital controls. Although some of the included currencies operate under de jure

stabilizing arrangement relative to one currency or a basket of currencies, a sufficient amount of

movement is allowed for all of the included currencies. Appendix A and B lists each country’s

de jure exchange rate regime according to the recent IMF classification obtained from the

International Monetary Fund Annual Report on Exchange Arrangements and Exchange

Restrictions 2013. Recent research has shown that de facto exchange rate regime can deviate

from the de facto classification.

The forecasts reported each month are the geometric mean of the respondents' forecasts,

which minimizes the effect of extreme forecasts.2 Unfortunately, individual forecasts of each

respondent are not available. Thus, we couldn’t explore heterogeneity and other characteristics of

individual forecasters.

2 See Timmermann (2005) for an overview of the advantages of combining individual forecasts.

3

Consensus Economics dataset contains 3-, 12-, and 24-month ahead forecasts for 10

major currencies and 27 minor currencies vis-à-vis the U.S. dollar.3 Foreign Exchange

Consensus forecasts are produced as a result of a monthly survey of over 250 professional

currency forecasters.4 The comprehensive country coverage, which goes back to January 1990

for many major and minor countries, makes this dataset appropriate for our purposes. The

number of responders (typically around 30) varies across countries and over time periods. They

include investment banks, large non-financial enterprises, consulting firms, and university

economists. The survey is usually conducted on the second Monday of every month. In addition

to the forecasts of the level of the exchange rate 3-, 12- and 24-month ahead, Consensus

Economics reports the level of the spot exchange rate on the date of the forecast, or a nowcast.

Although Consensus Economics dataset provides a comprehensive coverage of major and

minor currencies and has not been extensively studied in the literature, the respondents include

business firms and academicians, who might not have strong incentives to provide accurate

forecasts. The second dataset that we use mitigates this problem by surveying exclusively

professional forecasters.

In addition to Consensus Economics dataset, we use 3-, 6-, and 12-month ahead forecasts

of 10 major currencies and 37 minor currencies vis-à-vis the U.S. dollar from FX4casts,

previously known as The Financial Times Currency Forecaster and Currency Forecasters’

Digest.5 The data for all major currencies, except New Zealand and the U.K. starts in January

1990, and the forecasts 37 minor currencies start in the early 2000’s. FX4casts puts an emphasis

on reliability of their forecasts by surveying 45 large financial institutions.6 The survey is usually

conducted on the last Friday of the month by email (or fax), with the responses returned during

Friday and the following Monday and Tuesday. In addition to the forecasts of the level of the

exchange rate 3-, 6- and 12-month ahead, FX4casts reports the level of the spot exchange rate on

the date of the forecast for each currency.

3 The list of major and minor currencies in Consensus Economics dataset is provided in Appendix A. 4 We work with mean forecasts for each country, because Consensus Economics forecasts for individual professional forecasters are not available. Total number of survey respondents and the number of respondents are taken from Consensus Economics website: http://www.consensuseconomics.com/forex_major.htm. 5 The list of major and minor currencies in FX4casts dataset is provided in Appendix B. 6 Total number of survey respondents and the number of respondents are taken from FX4casts website: http://www.FX4casts.com

4

3. Summary Statistics

We start by examining the summary statistics for the actual and expected exchange rate

depreciation and forecast errors in both datasets. Tables 1A and 1B provide summary statistics

for actual and expected exchange rate depreciation in Consensus Economics dataset. Table 1C

reports the mean and standard deviation of the forecast error in Consensus Economics dataset. In

all tables, Panel A reports the statistics for 10 major currencies, and Panel B provides the results

for 27 minor currencies. Three main patterns are apparent from examining the data.

First, the absolute value of the mean expected and actual depreciation in Tables 1A and

1B increases with the forecast horizon. Thus, forecasters do not believe that there is the exchange

rates in most countries follow a mean reverting process. This empirical finding is consistent with

the results reported by Dominguez (1986), Frankel and Froot (1987), Macdonald and Torrance

(1990). Both major and minor currencies exhibit increasing mean expected depreciation with the

forecast horizon. However, the number of exceptions from this regularity is larger for major

currencies than for minor currencies. The pattern is violated for Denmark, Japan and Switzerland

at the 12-month horizon, and for New Zealand and the U.K. at the 24 month horizon. Among the

minor currencies, only the Philippines show a declining mean expected depreciation at the 12-

month horizon. Thus, there is more evidence in favor of mean-reverting forecasts for major

currencies than for minor currencies. Comparing expected depreciation and actual depreciation,

the same pattern of increasing mean actual depreciation holds for all major currencies, except

Sweden and the U.K. at the 24 month horizon, and for all minor currencies except Bolivia and

Uruguay at the 24-month horizon and Paraguay at the 12-month horizon.

Second, the standard deviation of expected and actual depreciation in Tables 1A and 1B

increase with the horizon as well. Third, both the mean and standard deviations of the forecast

errors reported in Table 1C increase with the forecast horizon. This empirical result provides

evidence that exchange rate forecasting performance deteriorates as the forecast horizon expands

from 3 to 24 months ahead. The finding is in accord with the results in Dominguez (1986) and

Frankel and Froot (1987) for pooled forecasts of major currencies. It is worth noting that the

mean forecast error declines with the horizon for 2 out of 10 major currencies, and for 8 out of

27 minor currencies.

In order to verify that these patterns are not specific to Consensus Economics dataset, we

examine the summary statistics for a broader set of countries in FX4casts data. This dataset has

5

been used before by Frankel and Chinn (1993), Chinn and Frankel (1994, 2002), and Frankel and

Poonawala (2009) to study a smaller group of currencies over a different sample. Due to data

limitations many of the existing studies rely on pooled forecasts. We estimate individual

equations for each currency in the sample, as the sample is long enough. Since exchange rate

forecasts in this dataset are collected from a group of 45 financial institutions that specialize in

exchange rate forecasting, they can arguably better represent market expectations.

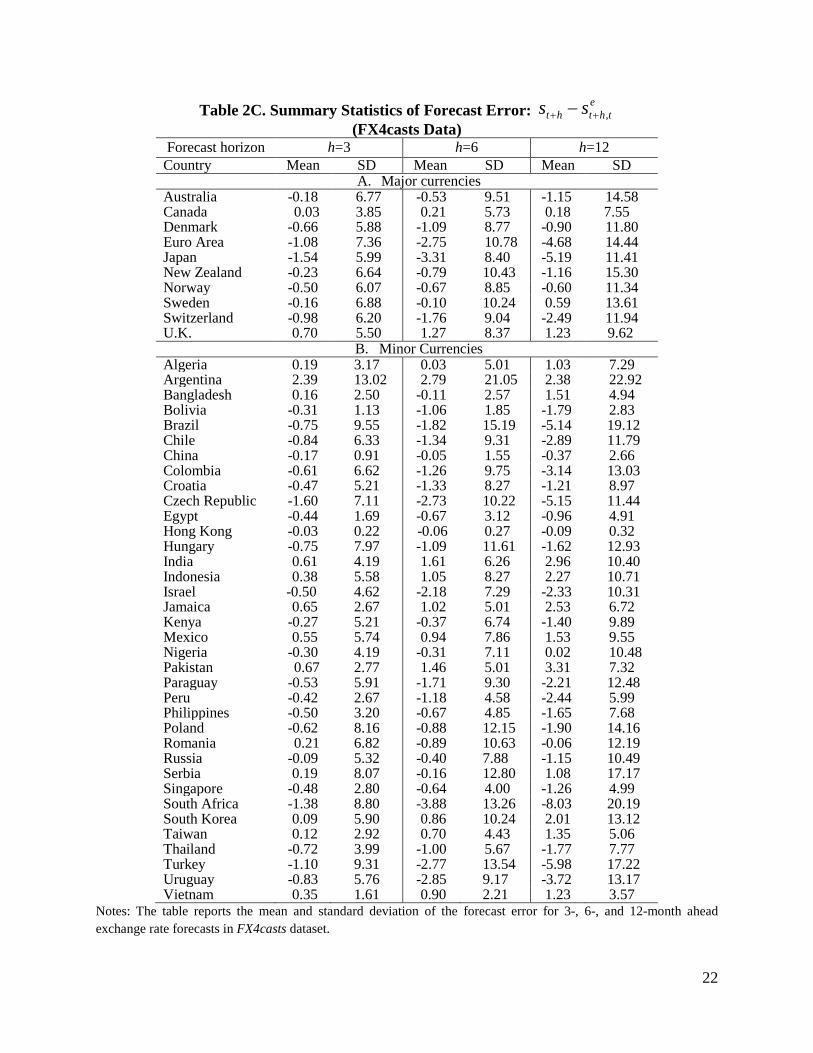

Tables 2A and 2B provide summary statistics for actual and expected exchange rate

depreciation in FX4casts dataset. Table 1C reports the mean and standard deviation of the

forecast error. In all three tables, Panel A reports the statistics for 10 major currencies, and Panel

B provides the results for 36 minor currencies. The same three main patterns are evident from

Tables 2A-2C. There are fewer countries that exhibit a mean reverting behavior in expected

exchange rate depreciation, and relatively more major countries with decreasing mean forecast

error at longer horizon of 6 or 12 month.

4. Rationality of Survey-Based Expectations

The availability of survey-based expectations allows us to test the rationality of exchange

rate expectations explicitly. Since Muth’s (1961) seminal paper, many definitions and tests of

rationality have been proposed. We apply two conventional tests of rationality of survey-based

expectations: tests of unbiasedness and orthogonality of expectations. Unbiasedness tests involve

testing whether the expected exchange rate is an unbiased predictor of the future spot rate.

Orthogonality condition assumes that professional forecasters fully incorporate all information

that is available at the time when the forecast is made. Thus, the forecast error should be

orthogonal to the information in the information set available to forecasters.

4.1 Unbiasedness of Expectations

Unbiasedness of exchange rate expectations can be tested by regressing actual

depreciation on expected depreciation:

htte

thttht ussss +++ +−+=− )( ,βα (1)

where ts is the log of the U.S. dollar nominal exchange rate determined as the domestic price of

foreign currency, so that an increase in ts is a depreciation of the dollar, ethts ,+ is the survey-

based expectation of the spot exchange rate at period t+h made at period t, and htu + is a white

6

noise error term. Testing for unbiasedness of exchange rate expectation involves testing a joint

null hypothesis that 0=α and 1=β in Equation (1). We estimate Equation (1) using OLS for

h=3, 12, and 24 month with Consensus Economics data and for h=3, 6, and 12 months with

FX4casts data.

Table 3 reports the results of estimating Equation (1) with Consensus Economics data for

3-, 12-, and 24-month ahead forecasts. The statistical significance of the estimated coefficients is

determined based on Newey-West standard errors. For each forecast horizon, we report the p-

values for the χ2 statistics for the joint null that 0=α and 1=β . At the 3-month horizon, there is

strong evidence against the unbiasedness hypothesis. The joint null hypothesis of unbiasedness is

rejected for all 10 major currencies, and for 23 out of 27 minor currencies. As the forecast

horizon increases, the bias in the forecasts for major currencies decreases dramatically. At the

12-month horizon, the joint null hypothesis of unbiasedness is rejected for 3 out of 10 major

currencies, and for 14 out of 27 minor currencies. At the 24-month horizon, the joint null

hypothesis of unbiasedness is rejected for all major currencies except the Japanese yen, and for

16 out of 27 minor currencies. Thus, there is more evidence of rationality at the 12- and 24-

month forecast horizon than at the 3-month horizon. The forecasts are relatively more biased for

major currencies than for minor currencies at the short horizon of 3 months, and relatively more

rational for major currencies than for minor currencies at longer horizons of 12 and 24 months.

Table 4 reports the results of estimating Equation (1) with FX4casts data for 3-, 6-, and

12-month ahead forecasts. As with Consensus Economics data, we find strong evidence against

the unbiasedness hypothesis at the 3-month ahead horizon, with the same number of rejections

for major and minor currencies. It is worth noting, however, that although the number of

rejections of the unbiasedness hypothesis is the same, FX4casts dataset contains 36 minor

currencies instead of 27 currencies in Consensus Economics. As the forecast horizon increases to

12 months, the bias in the forecasts decreases by half for major currencies and stays virtually the

same for minor currencies. At the 12-month horizon, the joint null hypothesis of unbiasedness is

rejected for 5 out of 10 major currencies, and for 23 out of 36 minor currencies. Thus, there is

more evidence of rationality at the 12-month forecast horizon than at the 3-month forecast

horizon. The forecasts are relatively more biased for major currencies than for minor currencies

at the short horizon of 3 months, and relatively more rational for major currencies than for minor

7

currencies at the longer horizon of 12 months. There is virtually no difference between the

performance of the forecasts at the 3- and 6-month horizon.

4.2 Orthogonality of Expectations

Orthogonality is another important condition of rationality of exchange rate expectations.

If professional forecasters fully incorporate information that is available to them at the time they

make forecasts, any variable that belongs to their information set should be orthogonal to the

forecast error. The first orthogonality test that we use involves regressing the forecast error on its

lagged value:

hte

httte

ththt ussss +−++ +−+=− )( ,, βα (2)

If the forecast error is orthogonal to past forecast errors, then 0=α and 0=β in equation (2).

The second test for orthogonality involves regressing the forecast error on lagged actual

exchange rate depreciation:

httte

ththt ussss +−++ +−+=− )( 1, βα (3)

If the forecast error is orthogonal to past exchange rate change, then 0=α and 0=β in equation

(3).

Table 5 reports the results of estimating Equation (2) with Consensus Economics data for

3-, 12-, and 24-month ahead forecasts. For each forecast horizon, the table reports the p-values

for the χ2 statistics for the joint test that 0=α and 0=β . At the 3-month horizon, we find

evidence against orthogonality for 5 out of 10 major currencies, and for 17 out of 27 minor

currencies. As the forecast horizon increases, the efficiency of the forecasts initially improves at

the 12-month horizon for both major and minor currencies and then deteriorates back to the same

level. At the 12-month horizon, the joint null hypothesis of orthogonality is rejected for 2 out of

10 major currencies, and for 11 out of 27 minor currencies. At the 24-month horizon, the joint

null hypothesis of orthogonality is rejected for 5 out of 10 major currencies, and for 16 out of 27

minor currencies. Thus, there is more evidence of rationality at the 12-month forecast horizon

than at the 3- or 24-month horizons. The forecasts are relatively less efficient for minor

currencies than for major currencies.

Table 6 reports the results of estimating equation (2) with FX4casts data for 3-, 6, and

12-month ahead forecasts. The findings are different than those obtained with Consensus

Economics data. At the 3-month horizon, we find evidence against orthogonality for 5 out of 10

8

major currencies, and for only 4 out of 36 minor currencies. Thus, minor currencies forecasts are

relatively more rational at the short forecast horizon. As the forecast horizon increases to 6

months, the efficiency of the forecasts improves dramatically for major currencies to 1 rejection

out of 10 and deteriorates for minor currencies to 17 rejections out of 36. At the 12-month

horizon, the joint null hypothesis of orthogonality is rejected for 2 out of 10 major currencies,

and for 21 out of 36 minor currencies. As with the tests of unbiasedness, the forecasts for minor

currencies are relatively more rational at the short horizon of 3 months, while the forecasts for

major currencies are relatively more rational at the longer horizons of 6 and 12 months. There is

virtually no difference between the performance of the forecasts at the 3- and 6-month horizon.

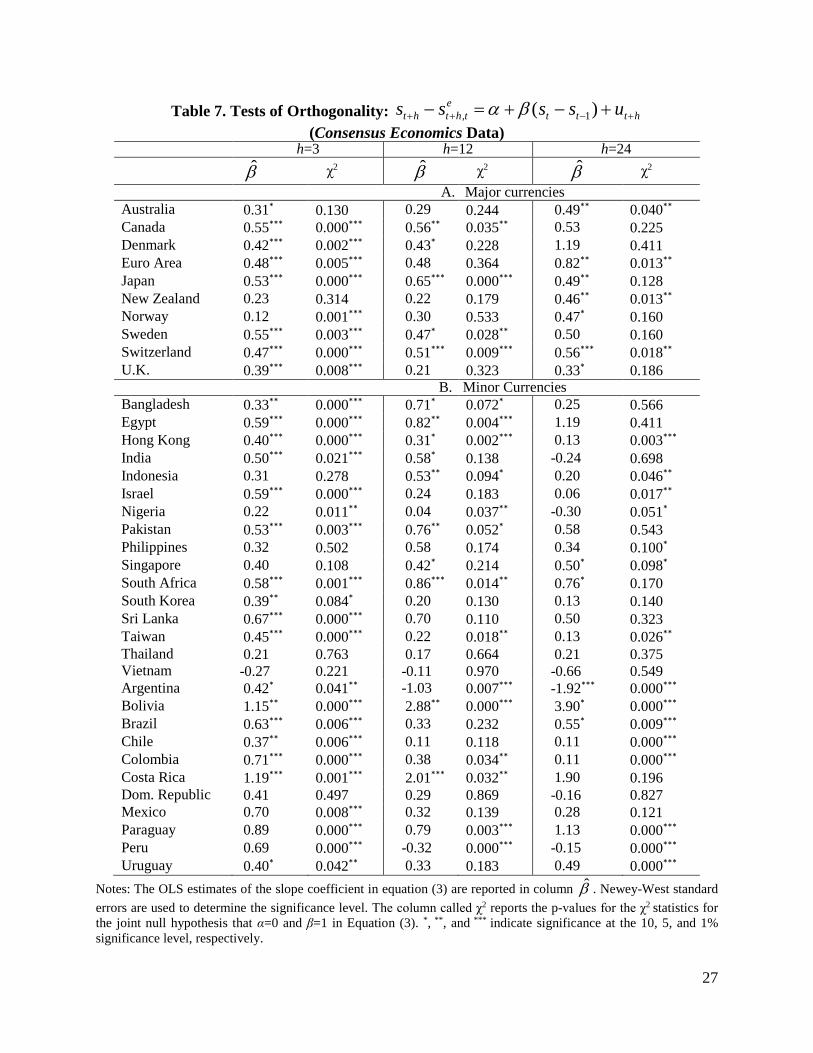

Finally, Table 7 reports the results of estimating equation (3) with Consensus Economics

data for 3-, 12-, and 24-month ahead forecasts. At the 3-month horizon, we find evidence against

orthogonality for 8 out of 10 major currencies, and for 21 out of 27 minor currencies. As the

forecast horizon increases, the efficiency of the forecasts initially improves. At the 12- and 24-

month horizon, the joint null hypothesis of orthogonality is rejected for 4 out of 10 major

currencies, and for 13 and 15 out of 27 minor currencies. Thus, there is more evidence of

rationality at the longer forecast horizon than at the short horizon.

Table 8 reports the results of estimating equation (3) with FX4casts data for 3-, 6, and 12-

month ahead forecasts. At the 3-month horizon, we find evidence against orthogonality for 3 out

of 10 major currencies, and for 6 out of 36 minor currencies. As the forecast horizon increases to

6 months, the efficiency of the forecasts improves to 1 rejection out of 10 for major currencies

and to only 3 rejections out of 36 for minor currencies. At the 12-month horizon, however, the

joint null hypothesis of orthogonality is rejected for 2 out of 10 major currencies, and for 15 out

of 36 minor currencies. As with the tests of unbiasedness, the forecasts for minor currencies are

relatively more rational at the short horizons of 3 and 6 months, while the forecasts for major

currencies are relatively more rational at the longer horizons of 12 months. There is no difference

between the performance of the major currency forecasts at the 6- and 12-month horizons.

5. Predictive Accuracy of Survey-Based Expectations

5.1 Tests Based on the MSPE Comparison

To compare the out-of-sample forecasting ability of the survey forecasts, this study

focuses on the minimum mean-squared prediction error (MSPE) approach, which became

9

dominant in the exchange rate forecasting literature after Meese and Rogoff (1983). The

prediction errors of survey forecasts and driftless random walk model are calculated as:

Survey Forecasts: ,e

t h t h ts s+ +− (4)

Driftless Random Walk: t h ts s+ −

To measure the relative forecast accuracy of the survey forecasts against the driftless

random walk, we use the Diebold-Mariano and West (DMW) test statistics.

Suppose that a martingale difference process and a linear model are given as:

Model 1: tt ey = (5)

Model 2: ttt eXy += β' where 0)(1 =− tt eE

where the dependent variable is the change in the exchange rate. Under the null hypothesis, the

population parameter 0=β and the exchange rate follows a random walk. For simplicity let us

concentrate on one-step-ahead forecasting. Assume that sample size is T, and P is equal to the

number of forecasts. So we have, T=P.

The estimated forecasts for the random walk and the structural model are 0 and 1,et ts + . The

respective forecast errors for the models are 11,1 ++ = tt ye and 2, 1 1 1,ˆ et t t te s s+ + += − . Thus, the sample

MSPE’s of the two models become:

∑

+−=+

−=T

PTttyP

1

21

121σ and 2 1 2

2 1 1,1

ˆ ( )T

et t t

t T PP y sσ −

+ += − +

= −∑ (6)

Diebold and Mariano (1995) and West (1996) construct a t-type statistics which is

assumed to be asymptotically normal and the population MSPE’s are equal under the null.

Defining the following equations,

2,2

2,1 ˆˆˆ

ttt eef −=

∑+−=

+− −==

T

PTttfPf

1

22

211

1 ˆˆˆ σσ (7)

∑+−=

+− −=

T

PTtt ffPV

1

21

1 )ˆ(ˆ

The DMW test statistic is

10

VP

fDMWˆ1−

= (8)

Table 9 reports the ratio of the MSPE’s of survey forecasts to that of the driftless random

walk model and DMW statistics with Consensus Economics data for 3-, 12-, and 24-month ahead

forecasts. At the 3-month horizon, survey forecasts cannot outperform the random walk model.

The MSPE’s for 5 minor currencies are lower than MSPE’s of the driftless random walk,

however the difference is not significant. As the forecast horizon increases, predictive ability of

the survey forecasts improves. At the 12-month horizon, predictability is found for 1 major

currency, and for 8 minor currencies. At the 24-month horizon, survey forecasts outperform the

driftless random walk for 2 out of 10 major currencies, and for 12 out of 27 minor currencies.

Thus, there is more evidence of predictability at the 24-month forecast horizon than at the 3- or

12-month horizons.

Table 10 reports the out-of-sample predictability results with FX4casts data for 3-, 6, and

12-month ahead forecasts. At the 3-month horizon, survey forecasts outperform the driftless

random walk for 6 out of 36 minor currencies. As the forecast horizon increases to 6 months, the

evidence of predictability is found for 5 minor currencies. At the 12-month horizon, however, the

evidence of predictability improves to 13 out of 36 minor currencies.

The results in Tables 9 and 10 show that forecasting ability of the survey forecasts

increases as forecast horizon increases. Also, survey forecasts for minor currencies seem more

accurate compared to major currencies.

5.2 Directional Accuracy

To evaluate the directional accuracy of the survey forecasts, we rely on the non-

parametric test developed by Pesaran and Timmermann (1992) that focuses on the correct

prediction of the direction of change in the variable under consideration. Pesaran and

Timmermann test (PT test, henceforth) is based on the proportion of times that the direction of

change in the exchange rate is correctly forecasted.

Let y be a predictor of y , Pr( 0)y tp y= > , ˆ ˆPr( 0)y tp y= > , and p is the proportion of

times that the sign of y is correctly forecasted. The PT test statistic, nS is

*1/ 2

*

ˆ ˆˆ ˆ ˆ ˆ( ( ) ( ))n

p pSv p v p

−=

− (9)

11

where ˆ ˆ*ˆ (1 )(1 )y y y yp p p p p= + − − , * *1ˆ ˆ ˆ ˆ( ) (1 )v p p pn

= −

2 2ˆ ˆ ˆ ˆ ˆ* 2

1 1 1ˆ ˆ( ) (2 1) (1 ) (2 1) (1 4 (1 )(1 )y y y y y y y y y yv p p p p p p p p p p pn n n

= − − + − − ) + − −

The null hypothesis of the PT test is that y and y distributed independently, and 2nS is

asymptotically distributed as 21χ .

Table 11 presents the ratio of the proportion of survey forecasts that have correct sign and

the PT test statistics with Consensus Economics data for 3-, 12-, and 24-month ahead forecasts.7

At the 3-month horizon, we find evidence against the null of no dependence for 5 out of 10

major currencies, and for 7 out of 27 minor currencies. As the forecast horizon increases to 12

months, the independency is rejected 6 out of 10 for major currencies and 10 out of 27 for minor

currencies. At the 12-month horizon, however, the PT is significant for 5 out of 10 major

currencies, and for 6 out of 27 minor currencies.

The directional accuracy results with FX4casts data for 3-, 6, and 12-month ahead

forecasts are reported in Table 12. The null hypothesis of independency for major currencies is

rejected only for 12-month ahead forecasts for 8 currencies. At the 3-month horizon, PT test is

significant for 8 minor currencies. As the forecast horizon increases to 6 months, the evidence of

dependency is found for 21 minor currencies. At the 12-month horizon, however, the null of

independency is rejected for 24 out of 36 minor currencies. Overall, the results in Tables 11 and

12 show that the dependence of the distributions of actual and forecasted exchange rate

depreciations increases as forecast horizon increases.

5.3 Summary of the Results

We have reported the results of three tests of rationality and two tests of predictive

accuracy for two datasets of professional exchange rate forecasts that contain 37 and 46

currencies each. In order to summarize the results, Table 13 reports the number of significant

statistics for each dataset. Panel A summarizes the results for major currencies, and Panel B

summarizes the results for minor currencies. The first three rows in Panels A and B report the

number of times the joint null hypothesis of unbiasedness or orthogonality can be rejected at the

10% significance level or higher. Two tests for orthogonality include testing for orthogonality of

7 The PT test is not available for some minor currencies because all the forecasts have the same sign, which makes the denominator in equation (9) equal to 0.

12

the forecast errors to lagged forecast errors and lagged actual exchange rate depreciation. Lower

number of rejections indicates stronger evidence of rationality of exchange rate expectations.

The next three rows summarize the results on the predictive accuracy of the forecasts:

the number of MSPE ratios below 1, the number of significant DMW statistics , the number of

proportions of correctly signed forecasts above 0.50, and the number of significant Pesaran and

Timmermann (1992) statistics (at the 10% significance level or higher). The last row in each

panel is the overall number of countries in each group and each dataset. In Panel A, all the cells

have 10 possible rejections. In Panel B, all the cells for Consensus Economics Data have 27

possible rejections, and all the cells for FX4casts data have 36 possible rejections.

6. Conclusions

We re-examine rationality and predictive accuracy of survey-based exchange rate

expectations for 10 major currencies and 40 minor currencies in Consensus Economics and

FX4casts datasets over the last two decades. Using the tests for unbiasedness and orthogonality,

we find the exchange rate forecasts are more rational at the long horizons of 24 and 12 months

than at the 3-month ahead horizon. The forecasts for minor currencies are relatively more

rational than the forecasts for major currencies at the short horizon of 3 months, and the forecasts

for major currencies are relatively more rational at the longer horizons of 12 months and 24

months.

Using the tests based on the MSPE comparison and on the nonparametric dependence

between forecasted and actual depreciation, we find that the predictive accuracy of the forecasts

improves with the forecasts horizon. Although, the evidence of predictive accuracy is week,

survey forecasts for minor currencies seem to be relatively more accurate compared to major

currencies based on the MSPE comparison. Another interesting finding is that while the DMW

tests couldn’t detect any evidence that the forecasts for major currencies perform better than the

random walk at the 3- or 6-month horizons, the direction-of-change PT test indicates the

presence of significant dependence between actual and forecasted depreciation. This might

suggest that the nature of the relationship is nonlinear or asymmetric.

In this paper, we have focused our analysis on examining the characteristics of survey-

based exchange rate expectations over various forecasts horizons for major and minor currencies.

13

In a companion paper, we re-evaluate the uncovered interest rate parity and analyze the implied

risk premium for two groups of countries.

14

References Chinn, Menzie and Jeffrey Frankel, “Patterns in Exchange Rate Forecasts for 25 Currencies,” Journal of Money, Credit and Banking 26(4), 1994, 759-770. ____________, “Survey Data on Exchange Rate Expectations: More Currencies, More Horizons, More Tests,” in W. Allen and D. Dickinson (eds), Monetary Policy, Capital Flows and Financial Market Developments in the Era of Financial Globalisation: Essays in Honour of Max Fry, London:Routledge, 2002, 145-167. Diebold, Francis and Robert Mariano, “Comparing Predictive Accuracy” Journal of Business and Economic Statistics, 1995, 13, pp.253-263

Dominguez, Kathryn M., 1986. "Are Foreign Exchange Forecasts Rational? New Evidence from Survey Data," Economics Letters, 21(3), 277-281. Engel, Charles, “The Forward Discount Anomaly and the Risk Premium: A Survey of Recent Evidence,” Journal of Empirical Finance 3 (2), 1996, 123-192. Frankel, Jeffrey and Kenneth Froot, 1987. "Using Survey Data to Test Standard Propositions Regarding Exchange Rate Expectations," American Economic Review, 77(1), Reprinted in Frankel, On Exchange Rates, MIT Press, 1993.133-153. Frankel, Jeffrey and Jumana Poonawala, 2010, “The Forward Market in Emerging Currencies: Less Biased than in Major Currencies”, Journal of International Money and Finance, 29(3), 585-598. Frankel, Jeffrey and Menzie Chinn,“Exchange Rate Expectations and the Risk Premium: Tests for a Cross-Section of 17 Currencies,” Review of International Economics 1(2), 1993, 136-144. Jongen, Ron, Willem F.C. Verschoor, and Christian C.P. Wolff, 2008. “Foreign Exchange Rate: Survey and Synthesis,” Journal of Economic Surveys, 22(1), 140–165. Lewis, Karen K., “Changing Beliefs and Systematic Rational Forecast Errors with Evidence from Foreign Exchange,” American Economic Review 79(4), 1989, 621-636. Maddala, G.S., 1991. “Survey Data on Expectations: What Have We Learnt?”In M. Nerlove (ed.), Issues in Contemporary Economics: Proceedings of the Ninth World Congress of the International Economic Association, Vol. 2: Macroeconomics and Econometrics. London: Macmillan. 319–344. MacDonald, Ronald, 2000. “Expectations Formation and Risk in Three Financial Markets: Surveying What the Surveys Say,” Journal of Economic Surveys, 14(1), 69–100. Macdonald, Ronald, and Thomas S. Torrance, “Expectations Formation and Risk in Four Foreign Exchange Rate Markets.” Oxford Economic Papers 42(3), 1990, 544-561 Meese, Richard A. and Kenneth Rogoff, “Empirical Exchange Rate Models of the Seventies: Do They Fit Out of Sample?” Journal of International Economics 14, 1983, 3-24 Muth, Richard A., “Rational Expectations and the Theory of Price Movements,” Econometric 29(3), 1961, 315-335

15

Pesaran, M. Hashem, and Alan Timmerman, “A Simple Nonparametric Test of Predictive Performance,” Journal of Business and Economic Statistics 10, 561-565 Takagi, Shinji, 1991. "Exchange Rate Expectations: A Survey of Survey Studies." IMF Staff Papers 38(1), 156-183. Timmermann, Allan, 2006. "Forecast Combinations," Handbook of Economic Forecasting, Elsevier. West, Kenneth D., “Asymptotic Inference about Predictive Ability” Econometrica, 1996, 64, pp.1067-1084

16

Table 1A. Summary Statistics of Actual Depreciation: tht ss −+ (Consensus Economics)

Forecast horizon h=3 h=12 h=24

Country Mean SD Mean SD Mean SD A. Major currencies

Australia -0.26 7.91 -1.01 16.67 -2.13 24.49 Canada -0.20 3.69 -0.91 7.77 -2.35 10.24 Denmark -0.07 5.47 -0.14 10.49 -1.10 14.68 Euro Area -0.25 5.46 -1.39 10.71 -4.84 14.30 Japan -0.67 5.83 -2.76 10.05 -5.39 15.29 New Zealand -0.79 10.12 -3.33 21.05 -7.23 31.96 Norway -0.10 5.79 -0.24 11.21 -1.46 14.05 Sweden 0.18 6.49 0.86 13.29 0.01 17.23 Switzerland -0.50 5.84 -1.93 10.58 -4.71 14.45 U.K. 0.15 4.93 0.54 9.26 0.28 12.31

B. Minor Currencies Bangladesh 1.00 1.81 4.16 3.60 8.03 5.34 Egypt 1.02 3.50 4.23 8.61 8.94 14.55 Hong Kong -0.01 0.21 -0.01 0.32 0.01 0.37 India 0.76 3.63 3.00 8.15 4.90 9.74 Indonesia 1.84 14.20 7.43 31.39 15.08 40.51 Israel 0.10 4.37 -0.22 8.33 -1.38 10.12 Nigeria 1.04 4.21 3.94 8.07 7.58 10.62 Pakistan 1.59 3.19 6.39 7.40 12.35 11.35 Philippines 0.73 5.01 2.95 11.95 6.25 17.31 Singapore -0.39 2.93 -1.54 5.96 -2.89 8.89 South Africa 1.27 7.97 4.75 16.61 8.99 24.23 South Korea 0.51 7.38 2.14 14.70 4.22 19.61 Sri Lanka 1.34 2.35 5.39 5.56 10.06 7.90 Taiwan 0.12 2.92 0.44 6.15 0.89 8.01 Thailand 0.23 6.15 1.04 12.63 2.01 16.73 Vietnam 0.89 1.66 3.70 3.89 7.84 6.01 Argentina 1.67 7.27 3.54 10.40 7.66 11.67 Bolivia 0.13 1.27 0.27 4.47 -0.24 7.67 Brazil -0.17 9.53 -1.94 18.22 -8.59 19.39 Chile -0.51 6.37 -2.78 10.92 -6.91 11.96 Colombia -0.55 6.62 -2.31 12.49 -6.22 14.34 Costa Rica 0.93 2.39 3.80 6.86 7.42 11.14 Dom. Republic 1.99 9.51 8.20 24.72 16.40 30.95 Mexico 0.71 5.50 3.28 9.43 5.83 10.84 Paraguay 0.30 6.77 0.17 15.64 -3.59 18.49 Peru -0.71 2.41 -2.64 4.63 -5.45 4.35 Uruguay 0.91 9.04 3.61 21.95 2.08 27.82

Notes: The table reports the mean and standard deviation of actual depreciation for 3-, 12-, and 24-month ahead exchange rate forecasts in Consensus Economics sample.

17

Table 1B. Summary Statistics of Expected Depreciation: te

tht ss −+ , (Consensus Economics Data)

Forecast horizon h=3 h=12 h=24

Country Mean SD Mean SD Mean SD A. Major currencies

Australia 0.31 2.69 1.17 5.21 2.06 8.49 Canada -0.30 1.52 -1.07 2.55 -1.77 4.05 Denmark 0.23 2.82 -0.23 5.65 -1.86 7.10 Euro Area -0.65 2.35 -2.13 5.04 -2.65 7.59 Japan 0.19 2.55 0.08 5.14 -1.98 6.78 New Zealand -0.14 2.90 0.30 5.92 0.14 10.03 Norway -0.43 2.60 -1.43 5.50 -2.96 6.72 Sweden -1.05 2.84 -3.04 5.88 -5.87 7.24 Switzerland 0.32 2.82 0.15 5.82 -2.24 6.84 U.K. 0.53 1.57 1.00 2.97 0.91 3.68

B. Minor Currencies Bangladesh 1.87 1.42 5.06 2.11 9.03 3.17 Egypt 1.13 1.50 3.81 3.28 6.75 4.41 Hong Kong 0.08 0.19 0.16 0.29 0.20 0.39 India 0.51 1.75 1.59 4.03 4.43 5.72 Indonesia 0.05 3.20 -0.10 5.72 -0.94 7.55 Israel 0.90 1.95 2.03 3.19 4.33 4.30 Nigeria 2.46 2.97 9.09 6.66 21.63 14.60 Pakistan 2.39 1.76 6.56 2.99 11.43 4.57 Philippines 0.43 1.68 0.23 3.00 1.70 3.52 Singapore -0.15 1.37 -1.38 2.18 -3.74 1.72 South Africa 1.02 3.34 4.38 5.19 8.45 7.10 South Korea -0.58 1.85 -2.66 3.72 -5.59 4.86 Sri Lanka 1.73 1.50 5.14 2.44 9.69 3.39 Taiwan -0.55 1.25 -2.02 1.96 -3.98 1.96 Thailand 0.04 1.75 -0.71 2.39 -1.74 2.67 Vietnam 1.19 1.45 3.79 3.10 6.59 4.98 Argentina 2.41 3.51 9.06 10.19 15.71 16.62 Bolivia 1.08 1.12 3.63 2.98 7.49 4.38 Brazil 0.50 3.47 3.98 5.14 8.68 5.76 Chile 0.23 1.70 1.57 2.55 3.49 3.58 Colombia 1.28 2.74 4.67 4.04 9.14 4.64 Costa Rica 1.64 1.27 6.23 2.22 11.69 4.40 Dom. Republic 2.61 3.87 6.68 5.22 10.86 6.39 Mexico 0.25 2.20 2.35 3.22 5.40 3.49 Paraguay 3.00 2.94 7.55 4.18 12.59 4.99 Peru 0.09 1.30 0.82 1.78 2.29 2.20 Uruguay 2.59 3.67 7.17 5.17 12.27 7.49

Notes: The table reports the mean and standard deviation of expected depreciation for 3-, 12-, and 24-month ahead exchange rate forecasts in Consensus Economics dataset.

18

Table 1C. Summary Statistics of Forecast Errors: eththt ss ,++ −

(Consensus Economics Data) Forecast horizon h=3 h=12 h=24

Country Mean SD Mean SD Mean SD A. Major currencies

Australia -0.57 8.54 -2.18 16.84 -3.17 25.34 Canada 0.10 4.08 0.16 7.71 -2.18 10.95 Denmark -0.30 5.86 0.09 11.21 1.63 14.37 Euro Area 0.40 6.09 0.73 11.44 -2.19 13.89 Japan -0.86 6.52 -2.84 11.82 -0.84 15.44 New Zealand -0.65 10.72 -3.63 21.26 -4.90 31.09 Norway 0.32 6.23 1.18 10.91 1.59 14.08 Sweden 1.23 6.82 3.90 12.22 5.35 14.93 Switzerland -0.81 6.42 -2.08 11.70 -1.18 14.62 U.K. -0.38 4.99 -0.41 8.28 -1.11 11.07

B. Minor Currencies Bangladesh -0.87 2.37 -0.90 4.50 -0.99 5.22 Egypt -0.11 3.63 0.42 8.13 2.18 13.56 Hong Kong -0.09 0.24 -0.17 0.33 -0.14 0.32 India 0.25 3.90 1.41 8.73 0.46 10.08 Indonesia 1.79 14.76 7.53 30.96 18.08 41.79 Israel -0.80 4.37 -2.25 7.50 -5.71 8.86 Nigeria -1.43 4.94 -5.15 9.16 -14.05 16.02 Pakistan -0.80 3.61 -0.18 7.62 0.91 11.62 Philippines 0.30 5.19 2.72 12.16 4.55 17.03 Singapore -0.24 3.28 -0.16 6.60 2.27 9.34 South Africa 0.25 9.03 0.36 17.74 0.03 24.67 South Korea 1.09 7.36 4.80 14.31 9.99 21.34 Sri Lanka -0.39 2.71 0.25 5.84 0.37 7.22 Taiwan 0.67 3.18 2.46 6.10 5.11 7.98 Thailand 0.18 6.15 1.75 12.74 4.29 18.24 Vietnam -0.30 1.92 -0.09 4.60 1.25 8.09 Argentina -0.74 5.93 -5.52 14.82 -8.04 21.11 Bolivia -0.95 1.29 -3.36 3.56 -7.72 6.30 Brazil -0.66 10.07 -5.92 18.13 -17.26 20.97 Chile -0.74 6.25 -4.35 10.13 -10.40 10.27 Colombia -1.83 7.19 -6.98 11.69 -15.36 12.67 Costa Rica -0.71 2.95 -2.43 7.24 -4.27 11.27 Dom. Republic -0.62 9.68 1.51 25.18 5.53 33.03 Mexico 0.46 5.79 0.94 9.06 0.43 10.14 Paraguay -3.69 6.92 -7.38 15.03 -16.18 17.59 Peru -0.80 2.99 -3.46 5.28 -7.54 4.97 Uruguay -1.68 8.37 -3.56 20.06 -10.19 25.06

Notes: The table reports the mean and standard deviation of the forecast error for 3-, 12-, and 24-month ahead exchange rate forecasts in Consensus Economics dataset.

19

Table 2A. Summary Statistics of Actual Depreciation: tht ss −+ (FX4casts Data)

Forecast horizon h=3 h=6 h=12 Country Mean SD Mean SD Mean SD

C. Major currencies Australia 0.35 5.95 0.68 8.91 1.29 12.34 Canada -0.20 3.72 -0.38 5.58 -0.71 7.72 Denmark -0.14 5.39 -0.22 7.60 -0.29 10.36 Euro Area -0.28 6.85 -0.60 10.15 -1.00 14.75 Japan -0.65 5.68 -1.42 7.75 -2.68 10.04 New Zealand 0.50 6.22 0.96 9.86 1.76 14.37 Norway -0.16 5.73 -0.27 8.02 -0.33 10.73 Sweden 0.08 6.64 0.20 9.53 0.62 12.94 Switzerland -0.53 5.72 -0.98 7.89 -1.75 10.44 U.K. -0.04 5.13 -0.10 7.59 -0.55 9.43

D. Minor Currencies Algeria 0.31 3.13 0.69 4.61 0.99 6.24 Argentina 3.58 13.91 5.50 21.36 6.81 21.92 Bangladesh 0.93 2.11 1.91 2.93 4.06 4.33 Bolivia -0.31 1.20 -0.67 1.98 -1.53 3.27 Brazil -0.44 9.38 -0.81 14.66 -2.91 18.22 Chile -0.81 6.44 -1.59 9.15 -3.33 11.12 China -0.65 0.98 -1.28 1.67 -2.66 2.85 Colombia -0.56 6.62 -1.09 9.79 -2.74 12.83 Croatia -0.20 5.26 -0.33 7.81 -0.54 9.67 Czech Republic -1.48 6.89 -2.88 10.18 -5.42 12.36 Egypt -0.02 1.68 -0.08 2.59 -0.27 4.00 Hong Kong -0.01 0.21 -0.03 0.26 -0.05 0.29 Hungary -0.58 7.87 -1.06 11.57 -1.71 14.14 India 0.29 4.09 0.58 5.99 0.98 9.56 Indonesia -0.14 5.14 -0.29 7.92 -0.19 10.14 Israel -0.40 4.44 -0.81 6.82 -1.88 8.95 Jamaica 1.18 2.61 2.35 4.27 4.69 6.39 Kenya 0.34 5.13 0.56 7.55 0.84 9.57 Mexico 0.76 5.52 1.65 7.83 3.23 9.80 Nigeria 0.39 4.02 0.92 5.94 2.12 9.08 Pakistan 1.47 2.67 2.96 4.49 5.86 7.21 Paraguay -0.92 5.86 -1.74 9.12 -3.68 11.41 Peru -0.84 2.54 -1.69 3.91 -3.27 4.95 Philippines -0.70 3.18 -1.36 4.75 -2.88 7.08 Poland -0.58 7.99 -1.09 12.22 -2.25 15.33 Romania 0.15 6.78 0.35 10.48 0.51 13.55 Russia 0.07 5.30 0.15 7.86 0.02 10.41 Serbia 1.28 7.82 2.64 12.28 4.82 16.39 Singapore -0.92 2.57 -1.85 3.71 -3.59 4.62 South Africa -0.44 8.50 -1.20 12.15 -2.59 17.63 South Korea -0.38 5.67 -0.75 8.73 -1.12 12.77 Taiwan -0.39 2.76 -0.77 3.91 -1.48 4.61 Thailand -0.83 3.55 -1.63 5.24 -3.22 7.42 Turkey 0.36 7.97 1.04 10.57 1.79 13.57 Uruguay -1.15 5.47 -2.15 8.05 -4.36 10.77 Vietnam 0.81 1.61 1.65 2.21 3.50 3.56

Notes: The table reports the mean and standard deviation of actual depreciation for 3-, 6-, and 12-month ahead exchange rate forecasts in FX4casts dataset.

20

Table 2B. Summary Statistics of Expected Depreciation: te

ht ss −+ (FX4casts Data)

Forecast horizon h=3 h=6 h=12 Country Mean SD Mean SD Mean SD

A. Major currencies Australia 0.35 1.73 1.13 3.13 2.21 4.91 Canada -0.23 1.03 -0.59 1.64 -0.92 2.58 Denmark 0.52 2.13 0.87 4.08 0.61 6.04 Euro Area 0.78 2.73 2.07 4.30 3.49 4.87 Japan 0.89 1.99 1.89 3.47 2.52 4.84 New Zealand 0.70 1.83 1.65 2.87 2.63 4.50 Norway 0.33 2.27 0.37 4.17 0.14 5.89 Sweden 0.24 2.40 0.27 4.32 -0.18 6.42 Switzerland 0.45 2.30 0.78 4.26 0.74 6.46 U.K. -0.74 1.88 -1.37 3.92 -1.64 5.20

B. Minor Currencies Algeria 0.15 0.77 0.21 1.54 0.30 2.85 Argentina 1.23 3.37 2.96 6.54 5.06 5.79 Bangladesh 0.79 1.62 1.83 1.64 2.89 2.92 Bolivia -0.01 0.45 0.05 1.11 0.05 2.03 Brazil 0.28 1.28 0.86 2.92 1.74 4.63 Chile 0.04 1.30 -0.20 2.31 -0.43 3.77 China -0.47 0.50 -1.21 1.02 -2.30 1.93 Colombia 0.06 1.52 0.18 3.61 0.32 4.57 Croatia 0.31 0.98 0.42 1.89 0.82 3.17 Czech Republic 0.15 1.71 -0.07 2.63 -0.07 4.01 Egypt 0.46 0.84 0.77 1.59 0.92 2.79 Hong Kong 0.01 0.08 0.03 0.11 0.04 0.13 Hungary 0.18 1.64 0.10 2.47 0.11 3.92 India -0.33 0.98 -1.06 1.55 -2.06 2.73 Indonesia -0.52 0.99 -1.32 1.52 -2.49 2.25 Israel 0.13 0.99 0.47 1.80 0.90 3.09 Jamaica 0.55 0.76 1.21 1.22 2.25 2.08 Kenya 0.62 1.08 1.23 1.83 2.26 3.50 Mexico 0.19 1.32 0.63 1.97 1.31 3.12 Nigeria 0.71 1.12 1.40 2.02 2.23 3.49 Pakistan 0.86 0.86 1.59 1.47 2.92 2.64 Paraguay -0.36 0.98 -0.72 1.83 -1.26 3.30 Peru -0.45 0.82 -0.81 1.39 -1.06 2.36 Philippines -0.21 0.97 -0.72 1.63 -1.38 2.81 Poland 0.06 1.52 -0.12 2.30 -0.13 3.89 Romania -0.02 1.80 0.37 2.00 0.74 3.40 Russia 0.18 1.19 0.58 2.18 1.16 3.92 Serbia 0.98 1.25 1.99 1.87 3.62 2.84 Singapore -0.44 0.74 -1.20 1.07 -2.34 1.45 South Africa 0.94 2.39 2.65 3.97 5.17 5.77 South Korea -0.48 1.36 -1.62 1.93 -3.11 2.39 Taiwan -0.51 0.75 -1.46 1.31 -2.76 1.79 Thailand -0.12 1.21 -0.66 2.01 -1.54 3.03 Turkey 1.44 3.24 3.68 5.70 7.19 9.84 Uruguay -0.33 1.07 -0.39 2.10 -0.66 3.61 Vietnam 0.46 0.50 0.98 0.82 2.06 1.25

The table reports the mean and standard deviation of expected depreciation for 3-, 6-, and 12-month ahead exchange rate forecasts in FX4casts dataset.

21

Table 2C. Summary Statistics of Forecast Error: eththt ss ,++ −

(FX4casts Data) Forecast horizon h=3 h=6 h=12 Country Mean SD Mean SD Mean SD

A. Major currencies Australia -0.18 6.77 -0.53 9.51 -1.15 14.58 Canada 0.03 3.85 0.21 5.73 0.18 7.55 Denmark -0.66 5.88 -1.09 8.77 -0.90 11.80 Euro Area -1.08 7.36 -2.75 10.78 -4.68 14.44 Japan -1.54 5.99 -3.31 8.40 -5.19 11.41 New Zealand -0.23 6.64 -0.79 10.43 -1.16 15.30 Norway -0.50 6.07 -0.67 8.85 -0.60 11.34 Sweden -0.16 6.88 -0.10 10.24 0.59 13.61 Switzerland -0.98 6.20 -1.76 9.04 -2.49 11.94 U.K. 0.70 5.50 1.27 8.37 1.23 9.62

B. Minor Currencies Algeria 0.19 3.17 0.03 5.01 1.03 7.29 Argentina 2.39 13.02 2.79 21.05 2.38 22.92 Bangladesh 0.16 2.50 -0.11 2.57 1.51 4.94 Bolivia -0.31 1.13 -1.06 1.85 -1.79 2.83 Brazil -0.75 9.55 -1.82 15.19 -5.14 19.12 Chile -0.84 6.33 -1.34 9.31 -2.89 11.79 China -0.17 0.91 -0.05 1.55 -0.37 2.66 Colombia -0.61 6.62 -1.26 9.75 -3.14 13.03 Croatia -0.47 5.21 -1.33 8.27 -1.21 8.97 Czech Republic -1.60 7.11 -2.73 10.22 -5.15 11.44 Egypt -0.44 1.69 -0.67 3.12 -0.96 4.91 Hong Kong -0.03 0.22 -0.06 0.27 -0.09 0.32 Hungary -0.75 7.97 -1.09 11.61 -1.62 12.93 India 0.61 4.19 1.61 6.26 2.96 10.40 Indonesia 0.38 5.58 1.05 8.27 2.27 10.71 Israel -0.50 4.62 -2.18 7.29 -2.33 10.31 Jamaica 0.65 2.67 1.02 5.01 2.53 6.72 Kenya -0.27 5.21 -0.37 6.74 -1.40 9.89 Mexico 0.55 5.74 0.94 7.86 1.53 9.55 Nigeria -0.30 4.19 -0.31 7.11 0.02 10.48 Pakistan 0.67 2.77 1.46 5.01 3.31 7.32 Paraguay -0.53 5.91 -1.71 9.30 -2.21 12.48 Peru -0.42 2.67 -1.18 4.58 -2.44 5.99 Philippines -0.50 3.20 -0.67 4.85 -1.65 7.68 Poland -0.62 8.16 -0.88 12.15 -1.90 14.16 Romania 0.21 6.82 -0.89 10.63 -0.06 12.19 Russia -0.09 5.32 -0.40 7.88 -1.15 10.49 Serbia 0.19 8.07 -0.16 12.80 1.08 17.17 Singapore -0.48 2.80 -0.64 4.00 -1.26 4.99 South Africa -1.38 8.80 -3.88 13.26 -8.03 20.19 South Korea 0.09 5.90 0.86 10.24 2.01 13.12 Taiwan 0.12 2.92 0.70 4.43 1.35 5.06 Thailand -0.72 3.99 -1.00 5.67 -1.77 7.77 Turkey -1.10 9.31 -2.77 13.54 -5.98 17.22 Uruguay -0.83 5.76 -2.85 9.17 -3.72 13.17 Vietnam 0.35 1.61 0.90 2.21 1.23 3.57

Notes: The table reports the mean and standard deviation of the forecast error for 3-, 6-, and 12-month ahead exchange rate forecasts in FX4casts dataset.

22

Table 3. Tests of Unbiasedness: htte

httht ussss +++ +−+=− )(βα (Consensus Economics Data)

h=3 h=12 h=24 β χ2 β χ2 β χ2

A. Major currencies Australia -0.21 0.000*** 0.40 0.281 0.51 0.577 Canada -0.16 0.000*** 0.57 0.756 -0.09 0.011** Denmark 0.22 0.000*** 0.26 0.077* 0.73 0.852 Euro Area -0.15 0.000*** 0.18 0.165 0.60 0.214 Japan -0.16 0.000*** -0.23 0.000*** 0.50 0.577 New Zealand -0.24 0.000*** 0.37 0.354 0.68 0.733 Norway 0.12 0.001*** 0.61 0.517 0.57 0.657 Sweden 0.22 0.000*** 0.89* 0.244 0.96* 0.162 Switzerland 0.05 0.000*** 0.13 0.008*** 0.52 0.577 U.K. 0.38 0.084* 1.47*** 0.670 1.80*** 0.249

B. Minor Currencies Bangladesh -0.09 0.000*** -0.32 0.000*** 0.57 0.014** Egypt 0.28 0.076* 0.87 0.914 1.22 0.869 Hong Kong 0.28*** 0.000*** 0.44*** 0.000*** 0.63*** 0.000*** India 0.17 0.001*** 0.20 0.067* 0.40 0.115 Indonesia -0.30 0.001*** 0.91 0.278 3.07** 0.160 Israel 0.50 0.077* 1.15*** 0.364 1.15*** 0.045** Nigeria 0.12 0.000*** 0.29 0.000*** 0.16 0.000*** Pakistan 0.04 0.000*** 0.32 0.225 0.35 0.235 Philippines 0.18 0.009*** 0.22 0.176 0.90 0.554 Singapore -0.07 0.000*** -0.35 0.000*** 0.24 0.252 South Africa -0.32* 0.000*** -0.22 0.078* 0.75 0.932 South Korea 0.54 0.018** 0.91** 0.124 1.29** 0.164 Sri Lanka 0.10 0.000*** 0.22 0.164 0.95*** 0.969 Taiwan -0.01 0.000*** 0.59 0.013** 2.18*** 0.019** Thailand 0.50 0.219 0.28 0.177 1.65** 0.613 Vietnam 0.28** 0.000*** 0.19 0.000*** -0.09 0.000*** Argentina 1.22*** 0.235 -0.04 0.000*** -0.06 0.000*** Bolivia 0.48*** 0.000*** 0.91*** 0.000*** 1.00*** 0.002*** Brazil 0.06 0.003*** 0.56 0.368 -0.46 0.001*** Chile 0.75*** 0.432 1.78*** 0.052* 1.97*** 0.000*** Colombia -0.03 0.000*** 1.10** 0.013** 1.55** 0.000*** Costa Rica -0.43 0.000*** -0.05 0.247 0.38 0.164 Dom. Republic 0.39* 0.001*** 0.08 0.131 -1.13 0.001*** Mexico 0.15 0.058* 0.83*** 0.595 1.11** 0.980 Paraguay 0.38 0.013** 1.03*** 0.126 1.16*** 0.002*** Peru -0.41 0.000*** -0.51 0.000*** -0.10 0.000*** Uruguay 0.93* 0.237 1.98*** 0.025** 1.80*** 0.000***

Notes: The OLS estimates of the slope coefficient in Equation (1) are reported in column β . Newey-West standard errors are used to determine the significance level. The column called χ2 reports the p-values for the χ2 statistics for the joint null hypothesis that α=0 and β=1 in Equation (1). *, **, and *** indicate significance at the 10, 5, and 1% significance level, respectively.

23

Table 4. Tests of Unbiasedness: htte

httht ussss +++ +−+=− )(βα (FX4casts Data)

h=3 h=6 h=12 β χ2 β χ2 β χ2

A. Major currencies Australia -0.16 0.000*** -0.07 0.003*** 0.08 0.111 Canada 0.05 0.000*** 0.18 0.038** 0.70 0.819 Denmark -0.11 0.000*** -0.07 0.000*** 0.08 0.001*** Euro Area 0.02 0.000*** 0.15 0.000*** 0.70 0.047** Japan 0.05 0.000*** 0.07 0.000*** -0.11 0.000*** New Zealand -0.32 0.000*** -0.22 0.030** -0.20 0.183 Norway 0.11 0.000*** 0.10 0.000*** 0.31 0.024** Sweden 0.21 0.003*** 0.13 0.003*** 0.28 0.147 Switzerland -0.04 0.000*** -0.03 0.000*** 0.12 0.000*** U.K. -0.05 0.000*** 0.10 0.000*** 0.42 0.111

B. Minor Currencies Algeria 0.26 0.267 -0.01 0.054** -0.39 0.000*** Argentina 1.54*** 0.655 0.65 0.093* -0.21 0.007*** Bangladesh 0.17 0.000*** 0.14 0.000*** 0.16 0.000*** Bolivia 0.87*** 0.003*** 0.68** 0.000*** 0.82*** 0.000*** Brazil 0.06 0.298 -0.45 0.108 -0.32 0.083* Chile 0.92** 0.601 0.23 0.085* -0.01 0.094* China 0.74*** 0.016** 0.69*** 0.114 0.63** 0.056* Colombia 0.49 0.440 0.52** 0.124 0.39 0.423 Croatia 0.81 0.811 0.41 0.613 1.11** 0.811 Czech Republic -0.01 0.002*** 0.45 0.307 1.16 0.007*** Egypt 0.48*** 0.006*** 0.21 0.008*** 0.00 0.015** Hong Kong 0.45 0.098* 0.21 0.000*** 0.08 0.000*** Hungary 0.20 0.145 0.43 0.734 1.52*** 0.560 India 0.08 0.017** -0.18 0.000*** -0.54 0.000*** Indonesia -0.51 0.000*** -0.67 0.004*** -0.58 0.004*** Israel -0.30 0.006*** -0.54 0.000*** -1.00* 0.000*** Jamaica 0.34 0.019** 0.25 0.006*** 0.11 0.000*** Kenya 0.16 0.265 0.24 0.298 0.27 0.112 Mexico -0.19 0.012** 0.44 0.423 0.77** 0.644 Nigeria -0.06 0.003*** -0.34 0.000*** -0.51 0.000*** Pakistan 0.08 0.007*** 0.22 0.001*** 0.88 0.029** Paraguay 0.22 0.198 -0.34 0.000*** -0.74* 0.000*** Peru 0.03 0.002*** -0.08 0.003*** -0.49 0.000*** Philippines 0.43 0.123 0.32 0.001*** -0.02 0.000*** Poland -0.11 0.058* 0.65 0.887 1.61** 0.141 Romania 0.43 0.304 1.60** 0.705 1.93*** 0.307 Russia 0.42 0.206 0.48 0.232 0.45 0.188 Serbia 0.45 0.763 0.29 0.560 0.20 0.787 Singapore -0.59** 0.000*** -0.43 0.000*** -0.29** 0.000*** South Africa 0.06 0.013** -0.36 0.000*** -0.87 0.000*** South Korea -0.22 0.000*** -0.34 0.001*** -0.22 0.102 Taiwan -0.30 0.000*** -0.71*** 0.000*** -0.14 0.000*** Thailand -0.62*** 0.000*** -0.07 0.007*** 0.24 0.235 Turkey -0.57*** 0.000*** -0.18 0.000*** -0.05 0.000*** Uruguay -0.93* 0.000*** -1.29** 0.000*** -1.53*** 0.000*** Vietnam 0.51 0.019** 0.38 0.023** 0.47 0.492

Notes: See notes to Table 3.

24

Table 5. Tests of Orthogonality: hte

httte

ththt ussss +−++ +−+=− )( .,, βα (Consensus Economics Data)

h=3 h=12 h=24 β χ2 β χ2 β χ2

A. Major currencies Australia 0.16* 0.074* 0.11 0.459 0.34*** 0.000*** Canada 0.32*** 0.000*** 0.09 0.905 0.28 0.012** Denmark 0.15* 0.154 0.24 0.267 0.12 0.691 Euro Area 0.15 0.254 0.14 0.619 -0.28 0.000*** Japan 0.15** 0.028** 0.30* 0.068 -0.17 0.063* New Zealand 0.15 0.259 0.16 0.162 0.34*** 0.000*** Norway 0.14* 0.252 0.08 0.835 0.20 0.631 Sweden 0.19** 0.006*** 0.09 0.415 -0.06 0.221 Switzerland 0.14* 0.092* 0.26 0.096* 0.25 0.239 U.K. 0.11 0.427 -0.02 0.741 -0.14 0.705

B. Minor Currencies Bangladesh 0.31** 0.000*** 0.26 0.214 -0.63*** 0.000*** Egypt 0.25*** 0.003*** 0.20 0.419 0.07 0.923 Hong Kong 0.39*** 0.000*** 0.21 0.007*** -0.07 0.000*** India 0.24** 0.047** -0.24 0.287 0.10 0.923 Indonesia 0.11 0.419 -0.18** 0.022** -0.10 0.326 Israel 0.27*** 0.004*** -0.20 0.157 -0.25*** 0.003*** Nigeria 0.13 0.000*** 0.01 0.009*** 0.44*** 0.000*** Pakistan 0.24** 0.001*** 0.07 0.878 0.03 0.932 Philippines 0.14 0.733 -0.05 0.527 0.22* 0.085* Singapore 0.11 0.440 0.12 0.670 0.30*** 0.016** South Africa 0.32*** 0.003*** 0.17 0.705 -0.07 0.951 South Korea 0.07 0.336 -0.10 0.110 -0.19 0.399 Sri Lanka 0.33*** 0.000*** -0.07 0.887 0.24 0.538 Taiwan 0.14* 0.042** -0.26*** 0.003*** -0.30*** 0.005*** Thailand 0.06 0.951 -0.17* 0.137 0.01 0.980 Vietnam 0.05 0.162 0.13 0.771 -0.02 0.887 Argentina 0.18 0.115 -0.05 0.502 -0.06 0.811 Bolivia 0.56 0.000*** 0.15 0.000*** 0.02 0.000*** Brazil 0.30*** 0.001*** -0.09 0.020** -0.21 0.001*** Chile 0.10 0.228 -0.38** 0.000*** -0.41*** 0.000*** Colombia 0.26** 0.009*** -0.27 0.003*** -0.31*** 0.000*** Costa Rica 0.61*** 0.000*** 0.12 0.174 0.04 0.118 Dom. Republic 0.49** 0.008*** -0.22 0.432 -0.31*** 0.000*** Mexico 0.17 0.463 -0.25 0.141 -0.54** 0.007*** Paraguay 0.43*** 0.000*** -0.18 0.000*** -0.07 0.000*** Peru 0.35** 0.001*** -0.62*** 0.000*** -0.42** 0.000*** Uruguay 0.13 0.144 -0.10 0.008*** -0.16*** 0.000***

Notes: The OLS estimates of the slope coefficient in equation (2) are reported in column β . Newey-West standard errors are used to determine the significance level. The column called χ2 reports the p-values for the χ2 statistics for the joint null hypothesis that α=0 and β=1 in Equation (2). *, **, and *** indicate significance at the 10, 5, and 1% significance level, respectively.

25

Table 6. Tests of Orthogonality: 3.,, )( +−++ +−+=− te

httte

ththt ussss βα (FX4casts Data)

h=3 h=6 h=12 β χ2 β χ2 β χ2

A. Major currencies Australia 0.18** 0.038** 0.04 0.844 -0.01 0.803 Canada 0.14** 0.078* -0.07 0.698 -0.11 0.835 Denmark 0.08 0.219 0.05 0.726 0.09 0.657 Euro Area 0.11* 0.039** 0.01 0.169 0.18 0.042** Japan -0.01 0.019** 0.01 0.012** 0.24 0.008*** New Zealand -0.28*** 0.026** 0.12 0.684 0.02 0.869 Norway 0.03 0.560 -0.06 0.756 -0.14 0.698 Sweden 0.11 0.375 -0.04 0.951 -0.07 0.869 Switzerland 0.03 0.237 0.04 0.432 0.12 0.249 U.K. 0.11 0.186 -0.13 0.372 -0.06 0.763

B. Minor Currencies Algeria 0.01 0.951 -0.15 0.330 -0.37 0.212 Argentina 0.35 0.031** -0.14*** 0.009*** -0.23*** 0.000*** Bangladesh 0.10 0.787 0.22*** 0.278 0.23* 0.206 Bolivia 0.26 0.131 0.02 0.072* -0.18 0.167 Brazil 0.26** 0.018** -0.15 0.247 -0.29* 0.001*** Chile 0.01 0.638 -0.30 0.000*** -0.44*** 0.000*** China 0.29** 0.073* 0.16 0.670 -0.27* 0.126 Colombia 0.06 0.571 -0.22* 0.087* -0.43*** 0.000*** Croatia 0.07 0.445 -0.36*** 0.000*** -0.49*** 0.000*** Czech Republic 0.09 0.110 -0.33*** 0.001*** -0.47** 0.007*** Egypt 0.03 0.232 0.10 0.756 -0.27** 0.060* Hong Kong -0.16 0.147 -0.21 0.024** -0.31** 0.042** Hungary 0.08 0.477 -0.32*** 0.006*** -0.37** 0.023** India 0.09 0.468 0.26* 0.119 -0.32** 0.080* Indonesia 0.07 0.295 -0.16 0.235 -0.24 0.188 Israel 0.15 0.267 -0.22 0.113 0.49** 0.001*** Jamaica 0.30 0.230 0.02 0.698 -0.26 0.571 Kenya -0.02 0.878 0.30*** 0.004*** -0.47*** 0.008*** Mexico 0.04 0.748 -0.25** 0.033** -0.34* 0.017** Nigeria 0.05 0.664 0.04 0.887 -0.36** 0.000*** Pakistan 0.34 0.239 0.16 0.492 -0.16 0.346 Paraguay 0.16 0.320 -0.30 0.126 -0.51** 0.002*** Peru 0.16 0.244 -0.21 0.131 -0.61*** 0.000*** Philippines 0.02 0.577 0.01 0.607 -0.25 0.058* Poland 0.16 0.326 -0.31*** 0.010*** -0.51** 0.046* Romania 0.15 0.571 -0.28*** 0.019** -0.30** 0.125 Russia 0.07 0.869 -0.22* 0.181 -0.34* 0.000*** Serbia 0.20*** 0.026** -0.19 0.120 -0.44 0.247 Singapore 0.06 0.289 -0.27*** 0.005*** -0.47** 0.000*** South Africa 0.13 0.110 0.14 0.265 0.19 0.330 South Korea 0.10 0.507 -0.04 0.419 -0.23 0.206 Taiwan 0.04 0.923 -0.33*** 0.007*** -0.33 0.326 Thailand 0.10 0.375 -0.03 0.631 -0.18 0.247 Turkey -0.07 0.670 -0.11 0.336 -0.15 0.177 Uruguay 0.08 0.478 -0.16 0.005*** -0.58*** 0.009*** Vietnam -0.21 0.151 0.35* 0.000*** 0.20 0.298

Notes: See notes to Table 5.

26

Table 7. Tests of Orthogonality: httte

ththt ussss +−++ +−+=− )( 1, βα (Consensus Economics Data)

h=3 h=12 h=24 β χ2 β χ2 β χ2

A. Major currencies Australia 0.31* 0.130 0.29 0.244 0.49** 0.040** Canada 0.55*** 0.000*** 0.56** 0.035** 0.53 0.225 Denmark 0.42*** 0.002*** 0.43* 0.228 1.19 0.411 Euro Area 0.48*** 0.005*** 0.48 0.364 0.82** 0.013** Japan 0.53*** 0.000*** 0.65*** 0.000*** 0.49** 0.128 New Zealand 0.23 0.314 0.22 0.179 0.46** 0.013** Norway 0.12 0.001*** 0.30 0.533 0.47* 0.160 Sweden 0.55*** 0.003*** 0.47* 0.028** 0.50 0.160 Switzerland 0.47*** 0.000*** 0.51*** 0.009*** 0.56*** 0.018** U.K. 0.39*** 0.008*** 0.21 0.323 0.33* 0.186

B. Minor Currencies Bangladesh 0.33** 0.000*** 0.71* 0.072* 0.25 0.566 Egypt 0.59*** 0.000*** 0.82** 0.004*** 1.19 0.411 Hong Kong 0.40*** 0.000*** 0.31* 0.002*** 0.13 0.003*** India 0.50*** 0.021*** 0.58* 0.138 -0.24 0.698 Indonesia 0.31 0.278 0.53** 0.094* 0.20 0.046** Israel 0.59*** 0.000*** 0.24 0.183 0.06 0.017** Nigeria 0.22 0.011** 0.04 0.037** -0.30 0.051* Pakistan 0.53*** 0.003*** 0.76** 0.052* 0.58 0.543 Philippines 0.32 0.502 0.58 0.174 0.34 0.100* Singapore 0.40 0.108 0.42* 0.214 0.50* 0.098* South Africa 0.58*** 0.001*** 0.86*** 0.014** 0.76* 0.170 South Korea 0.39** 0.084* 0.20 0.130 0.13 0.140 Sri Lanka 0.67*** 0.000*** 0.70 0.110 0.50 0.323 Taiwan 0.45*** 0.000*** 0.22 0.018** 0.13 0.026** Thailand 0.21 0.763 0.17 0.664 0.21 0.375 Vietnam -0.27 0.221 -0.11 0.970 -0.66 0.549 Argentina 0.42* 0.041** -1.03 0.007*** -1.92*** 0.000*** Bolivia 1.15** 0.000*** 2.88** 0.000*** 3.90* 0.000*** Brazil 0.63*** 0.006*** 0.33 0.232 0.55* 0.009*** Chile 0.37** 0.006*** 0.11 0.118 0.11 0.000*** Colombia 0.71*** 0.000*** 0.38 0.034** 0.11 0.000*** Costa Rica 1.19*** 0.001*** 2.01*** 0.032** 1.90 0.196 Dom. Republic 0.41 0.497 0.29 0.869 -0.16 0.827 Mexico 0.70 0.008*** 0.32 0.139 0.28 0.121 Paraguay 0.89 0.000*** 0.79 0.003*** 1.13 0.000*** Peru 0.69 0.000*** -0.32 0.000*** -0.15 0.000*** Uruguay 0.40* 0.042** 0.33 0.183 0.49 0.000***

Notes: The OLS estimates of the slope coefficient in equation (3) are reported in column β . Newey-West standard errors are used to determine the significance level. The column called χ2 reports the p-values for the χ2 statistics for the joint null hypothesis that α=0 and β=1 in Equation (3). *, **, and *** indicate significance at the 10, 5, and 1% significance level, respectively.

27

Table 8. Tests of Orthogonality: httte

ththt ussss +−++ +−+=− )( 1, βα (FX4casts Data)

h=3 h=6 h=12 β χ2 β χ2 β χ2

A. Major currencies Australia 0.23 0.350 0.28 0.242 0.13 0.852 Canada 0.12 0.543 0.07 0.811 0.01 0.990 Denmark 0.10 0.221 -0.00 0.644 0.01 0.923 Euro Area 0.19** 0.023** 0.14 0.114 0.25 0.181 Japan 0.25** 0.004*** -0.17 0.006*** 0.33 0.009*** New Zealand 0.35** 0.128 0.35 0.275 0.24 0.827 Norway 0.10 0.432 0.05 0.787 -0.17 0.726 Sweden 0.17 0.267 0.03 0.980 -0.07 0.887 Switzerland 0.04 0.188 -0.12 0.259 0.02 0.502 U.K. 0.16 0.089* -0.05 0.487 -0.22 0.387

B. Minor Currencies Algeria -0.05 0.923 -0.05 0.990 -0.63 0.347 Argentina 0.86*** 0.000*** 0.75*** 0.003*** 0.25 0.432 Bangladesh -0.08 0.887 0.20 0.403 -0.39 0.185 Bolivia 0.17 0.088* 0.67 0.025** 0.34 0.026 Brazil 0.32 0.126 0.18 0.449 -0.47* 0.031** Chile 0.07 0.482 0.01 0.719 -0.42** 0.011** China 0.39 0.202 0.38 0.571 0.08 0.844 Colombia 0.02 0.787 0.08 0.549 -0.42 0.043** Croatia 0.10 0.644 -0.04 0.763 -0.71*** 0.000*** Czech Republic 0.14 0.063* 0.03 0.223 -0.43** 0.006*** Egypt 0.09 0.102 -0.05 0.625 -0.69 0.267 Hong Kong -0.16 0.194 -0.11 0.254 -0.13 0.287 Hungary 0.15 0.419 0.04 0.763 -0.47** 0.055* India 0.11 0.512 0.35 0.210 0.31 0.254 Indonesia 0.01 0.878 -0.04 0.712 -0.33 0.357 Israel 0.06 0.771 0.30 0.145 -0.57* 0.097* Jamaica 0.49 0.254 0.63 0.275 0.23 0.159 Kenya 0.19 0.698 -0.08 0.932 -0.70*** 0.008*** Mexico 0.27 0.619 -0.09 0.664 -0.25 0.533 Nigeria 0.26** 0.072* 0.27* 0.121 -0.04 0.980 Pakistan 0.55 0.225 0.92* 0.204 0.49 0.151 Paraguay 0.33** 0.060* -0.10 0.651 -0.67 0.160 Peru 0.01 0.577 0.36 0.482 -0.88* 0.000*** Philippines 0.13 0.399 0.17 0.449 0.05 0.691 Poland 0.28 0.239 0.10 0.748 -0.55** 0.010*** Romania 0.19 0.607 0.16 0.733 -0.51** 0.119 Russia 0.23 0.445 0.19 0.607 -0.34* 0.168 Serbia 0.27** 0.091* 0.20 0.657 -0.69** 0.031** Singapore 0.07 0.361 -0.13 0.619 -0.55** 0.002*** South Africa 0.12 0.273 -0.21 0.387 0.02 0.336 South Korea 0.09 0.914 -0.04 0.657 -0.35 0.055* Taiwan 0.18 0.638 -0.13 0.482 -0.67 0.027** Thailand 0.10 0.387 -0.06 0.577 0.01 0.595 Turkey 0.07 0.670 -0.13 0.391 -0.20 0.391 Uruguay 0.37* 0.087 0.35 0.214 -0.70* 0.051* Vietnam -0.08 0.307 0.52* 0.000*** 0.18 0.468

Notes: See notes to Table 7.

28

Table 9. Tests of Predictive Accuracy: Consensus Economics Data h=3 h=12 h=24

MSPE Ratio

DMW MSPE Ratio

DMW MSPE Ratio

DMW

A. Major currencies Australia 1.169 -4.532 1.033 -0.999 1.011 -0.334 Canada 1.219 -3.377 0.971 0.549 1.073 -1.338 Denmark 1.152 -2.118 1.141 -1.923 0.909 1.183 Euro Area 1.244 -3.192 1.126 -1.445 0.867 1.350* Japan 1.255 -4.730 1.361 -5.886 0.971 0.443 New Zealand 1.119 -3.984 1.024 -0.937 0.966 1.188 Norway 1.156 -2.295 0.958 0.604 0.974 0.319 Sweden 1.142 -1.883 0.928 0.915 0.927 0.733 Switzerland 1.218 -3.014 1.221 -3.394 0.946 0.839 U.K. 1.029 -0.567 0.799 3.353*** 0.784 5.175***

B. Minor Currencies Bangladesh 1.496 -4.435 0.692 4.033*** 0.302 10.430*** Egypt 0.997 0.022 0.720 2.854*** 0.645 5.176*** Hong Kong 1.576 -3.538 1.408 -2.418 0.825 1.120 India 1.112 -1.325 1.036 -0.655 0.855 2.054** Indonesia 1.079 -1.610 0.975 1.206 0.888 4.991*** Israel 1.033 -0.377 0.883 1.669** 1.066 -0.921 Nigeria 1.405 -2.379 1.369 -2.894 2.669 -6.574 Pakistan 1.075 -0.653 0.605 5.387*** 0.481 8.069*** Philippines 1.053 -0.916 1.024 -0.622 0.916 3.129*** Singapore 1.233 -3.649 1.149 -3.100 1.051 -0.878 South Africa 1.255 -4.431 1.054 -1.097 0.861 2.843*** South Korea 1.011 -0.290 1.032 -0.929 1.085 -2.193 Sri Lanka 1.021 -0.198 0.570 7.374*** 0.318 9.955*** Taiwan 1.238 -4.121 1.136 -2.820 1.155 -2.836 Thailand 1.000 -0.005 1.028 -0.984 0.987 0.569 Vietnam 1.061 -0.199 0.731 2.981*** 0.685 5.008*** Argentina 0.642 1.236 2.073 -2.021 2.615 -2.588 Bolivia 1.584 -3.483 1.202 -1.647 1.696 -4.030 Brazil 1.120 -1.656 1.084 -1.435 1.644 -6.575 Chile 0.972 0.621 0.958 0.813 1.122 -2.314 Colombia 1.249 -2.782 1.150 -1.536 1.629 -5.883 Costa Rica 1.397 -1.994 0.948 0.352 0.808 1.339* Dom. Republic 0.996 0.034 0.937 0.944 0.912 1.830** Mexico 1.100 -0.978 0.831 2.878*** 0.677 4.219*** Paraguay 1.204 -1.600 1.148 -1.508 1.615 -4.923 Peru 1.511 -3.023 1.404 -5.493 1.742 -8.176 Uruguay 0.883 0.686 0.838 1.767** 0.941 0.503

Notes: The table reports the ratio of the out-of-sample MSPE’s of survey forecasts to that of the random walk model without drift and the DMW statistics for the test of equal predictability between the two models. The MSPE Ratio below 1 indicates that the MSPE of survey forecasts is lower than that of the random walk. Significant test statistics indicates rejection of the null of no predictability. *, **, and *** indicate significance at the 10, 5, and 1% significance level respectively.

29

Table 10. Tests of Predictive Accuracy: FX4casts Data h=3 h=6 h=12

MSPE Ratio

DMW

MSPE Ratio

DMW

MSPE Ratio

DMW

A. Major currencies Australia 1.108 -3.116 1.136 -3.195 1.129 -2.107 Canada 1.065 -1.816 1.052 -1.391 0.947 1.143 Denmark 1.205 -4.215 1.352 -5.417 1.304 -3.836 Euro Area 1.178 -1.442 1.197 -2.489 1.055 -1.253 Japan 1.171 -3.361 1.315 -4.999 1.457 -6.548 New Zealand 1.134 -2.675 1.116 -2.379 1.123 -2.142 Norway 1.129 -3.190 1.223 -3.942 1.119 -1.798 Sweden 1.077 -1.402 1.153 -2.708 1.111 -1.528 Switzerland 1.195 -3.842 1.343 -5.196 1.327 -4.358 U.K. 1.166 -2.955 1.243 -3.231 1.061 -0.728

B. Minor Currencies Algeria 1.022 -0.408 1.102 -1.381 1.358 -3.823 Argentina 0.849 1.440* 0.926 0.866 1.007 -0.074 Bangladesh 1.178 -0.540 0.868 1.010 0.754 1.857** Bolivia 0.899 1.668** 0.925 1.023 0.861 1.646** Brazil 1.039 -0.923 1.086 -2.284 1.152 -3.074 Chile 0.967 0.989 1.026 -0.541 1.092 -1.505 China 0.628 3.590*** 0.539 3.810*** 0.473 4.606*** Colombia 1.002 -0.064 0.997 0.073 1.042 -0.663 Croatia 0.986 0.393 1.016 -0.338 0.874 1.901** Czech Republic 1.068 -1.650 0.999 0.026 0.864 2.797*** Egypt 1.081 -1.084 1.298 -2.371 1.558 -2.592 Hong Kong 1.027 -0.326 1.154 -1.933 1.255 -2.887 Hungary 1.030 -0.815 1.007 -0.169 0.838 3.423*** India 1.066 -1.834 1.156 -3.576 1.268 -4.890 Indonesia 1.074 -2.248 1.107 -2.372 1.165 -2.669 Israel 1.082 -2.505 1.154 -3.355 1.334 -6.104 Jamaica 0.903 1.531* 0.920 1.522* 0.802 2.637*** Kenya 1.029 -0.636 1.038 -0.636 1.082 -0.900 Mexico 1.070 -1.122 0.978 0.611 0.879 2.588*** Nigeria 1.083 -1.209 1.182 -2.525 1.262 -4.066 Pakistan 0.869 3.080*** 0.808 3.883*** 0.745 4.573*** Paraguay 0.999 0.027 1.037 -0.911 1.117 -2.217 Peru 1.011 -0.284 1.013 -0.229 1.186 -2.110 Philippines 0.988 0.231 0.984 0.262 1.055 -0.746 Poland 1.045 -0.989 0.986 0.389 0.849 3.321*** Romania 1.010 -0.201 0.920 1.723** 0.808 4.285*** Russia 1.008 -0.184 1.006 -0.131 1.028 -0.459 Serbia 0.983 0.421 0.973 0.720 0.956 0.849 Singapore 1.078 -1.269 0.953 0.666 0.773 3.061*** South Africa 1.094 -1.659 1.281 -2.290 1.489 -3.401 South Korea 1.080 -2.180 1.088 -2.193 1.072 -1.591 Taiwan 1.101 -1.879 1.265 -3.113 1.172 -1.467 Thailand 1.237 -3.418 1.104 -1.670 0.969 0.511 Turkey 1.379 -1.869 1.463 -1.519 1.775 -2.518 Uruguay 1.086 -2.377 1.211 -4.169 1.386 -5.257 Vietnam 0.836 2.082** 0.717 3.361*** 0.569 5.453***

Notes: See notes to Table 9.

30

Table 11. Tests of Directional Accuracy: Consensus Economics Data

h=3 h=12 h=24

PCS PT PCS PT PCS PT A. Major currencies

Australia 0.418 0.005*** 0.508 0.778 0.482 0.615 Canada 0.446 0.006*** 0.487 0.543 0.425 0.007*** Denmark 0.502 0.938 0.596 0.003*** 0.596 0.006*** Euro Area 0.461 0.218 0.622 0.004*** 0.639 0.002*** Japan 0.425 0.015** 0.367 0.000*** 0.497 0.325 New Zealand 0.421 0.010*** 0.542 0.171 0.539 0.310 Norway 0.494 0.743 0.588 0.006*** 0.549 0.169 Sweden 0.510 0.949 0.592 0.003*** 0.622 0.000*** Switzerland 0.482 0.590 0.533 0.274 0.508 0.784 U.K. 0.550 0.079* 0.588 0.002*** 0.591 0.000***

B. Minor Currencies Bangladesh 0.650 0.662 0.883 0.621 0.938 - Egypt 0.558 0.439 0.620 0.407 0.616 - Hong Kong 0.517 0.415 0.602 0.000*** 0.694 0.000*** India 0.523 0.642 0.654 0.000*** 0.617 0.413 Indonesia 0.586 0.027** 0.673 0.000*** 0.653 0.000*** Israel 0.477 0.551 0.583 0.002*** 0.550 0.024** Nigeria 0.521 0.599 0.622 0.449 0.701 0.691 Pakistan 0.668 0.171 0.863 - 0.886 - Philippines 0.472 0.233 0.561 0.126 0.585 0.319 Singapore 0.479 0.080* 0.520 0.008*** 0.591 0.800 South Africa 0.513 0.785 0.619 0.753 0.720 0.001*** South Korea 0.505 0.887 0.572 0.045** 0.508 0.774 Sri Lanka 0.743 0.008*** 0.790 0.014** 0.917 0.770 Taiwan 0.484 0.435 0.492 0.712 0.518 - Thailand 0.433 0.016** 0.378 0.000*** 0.549 0.997 Vietnam 0.804 0.022** 0.888 0.453 0.979 - Argentina 0.695 0.115 0.782 0.804 0.822 0.035 Bolivia 0.355 0.760 0.372 0.464 0.393 0.179 Brazil 0.522 0.158 0.450 0.449 0.436 0.160 Chile 0.587 0.014** 0.512 0.073* 0.410 0.031** Colombia 0.464 0.774 0.411 0.347 0.308 0.269 Costa Rica 0.710 0.091* 0.713 0.530 0.709 - Dom. Republic 0.739 0.362 0.853 - 0.855 0.688 Mexico 0.522 0.417 0.628 0.021** 0.667 0.042** Paraguay 0.471 0.550 0.434 0.224 0.274 - Peru 0.406 0.400 0.411 0.893 0.239 0.456 Uruguay 0.464 0.638 0.465 0.559 0.256 -

Notes: The table reports the ratio of the proportion of forecasts that have correct sign and the Pesaran and Timmermann (1992) statistics for the test of directional accuracy of the forecasts. Significant test statistics indicates rejection of the null. *, **, and *** indicate significance at the 10, 5, and 1% significance level respectively.

31

Table 12. Tests of Directional Accuracy: FX4casts Data h=3 h=6 h=12 PCS PT PCS PT PCS PT

A. Major currencies Australia 0.491 0.437 0.533 0.632 0.580 0.066* Canada 0.502 0.736 0.496 0.762 0.576 0.010*** Denmark 0.513 0.562 0.522 0.379 0.561 0.039** Euro Area 0.542 0.183 0.548 0.199 0.602 0.002*** Japan 0.476 0.573 0.456 0.203 0.386 0.037** New Zealand 0.513 0.832 0.565 0.364 0.548 0.587 Norway 0.531 0.315 0.485 0.541 0.625 0.000*** Sweden 0.465 0.197 0.478 0.350 0.568 0.026** Switzerland 0.491 0.858 0.522 0.404 0.530 0.191 U.K. 0.505 0.797 0.493 0.742 0.602 0.000***

B. Minor Currencies Algeria 0.509 0.722 0.534 0.548 0.433 0.145 Argentina 0.598 0.912 0.612 0.346 0.675 0.478 Bangladesh 0.623 0.879 0.670 0.188 0.784 0.933 Bolivia 0.415 0.001*** 0.456 0.083* 0.443 0.070* Brazil 0.462 0.691 0.403 0.145 0.423 0.584 Chile 0.530 0.626 0.558 0.481 0.642 0.010*** China 0.500 0.000*** 0.558 0.000*** 0.691 0.000*** Colombia 0.583 0.090* 0.543 0.706 0.602 0.120 Croatia 0.528 0.452 0.583 0.036** 0.660 0.000*** Czech Republic 0.492 0.740 0.605 0.046** 0.724 0.000*** Egypt 0.708 0.000*** 0.728 0.000*** 0.691 0.000*** Hong Kong 0.045 0.000*** 0.062 0.000*** 0.065 0.000*** Hungary 0.462 0.391 0.496 0.798 0.707 0.000*** India 0.492 0.217 0.457 0.008*** 0.439 0.001*** Indonesia 0.492 0.306 0.465 0.027** 0.472 0.042** Israel 0.415 0.064* 0.388 0.028** 0.227 0.000*** Jamaica 0.654 0.733 0.693 0.067* 0.674 0.056* Kenya 0.575 0.147 0.621 0.003*** 0.567 0.031* Mexico 0.538 0.274 0.581 0.048** 0.618 0.008*** Nigeria 0.509 0.282 0.573 0.055* 0.608 0.015** Pakistan 0.660 0.391 0.709 0.082* 0.825 0.539 Paraguay 0.547 0.795 0.515 0.250 0.474 0.051* Peru 0.619 0.271 0.667 0.709 0.604 0.469 Philippines 0.560 0.471 0.602 0.369 0.598 0.949 Poland 0.485 0.593 0.605 0.039** 0.740 0.000*** Romania 0.585 0.087* 0.573 0.132 0.711 0.000*** Russia 0.538 0.446 0.605 0.008*** 0.618 0.000*** Serbia 0.531 0.330 0.537 0.168 0.596 0.032** Singapore 0.417 0.000*** 0.628 0.000*** 0.740 0.001*** South Africa 0.462 0.407 0.426 0.553 0.463 0.392 South Korea 0.545 0.588 0.543 0.023** 0.650 0.053* Taiwan 0.538 0.147 0.550 0.001*** 0.577 0.048** Thailand 0.439 0.028** 0.481 0.132 0.545 0.761 Turkey 0.379 0.143 0.434 0.130 0.545 0.366 Uruguay 0.547 0.190 0.388 0.000*** 0.433 0.000*** Vietnam 0.726 0.613 0.806 0.083* 0.876 0.717

Notes: See notes to Table 11.

32

Table 13. Summary of the Results

Consensus Economics Data FX4casts Data h=3 h=12 h=24 h=3 h=6 h=12

A. Major Currencies Rationality Tests Unbiasedness Test 10 3 1 10 10 5 Orthogonality Test 1 5 2 5 5 1 2 Orthogonality Test 2 8 4 4 3 1 1 Predictive Accuracy Tests MSPE Ratio<1 0 4 8 0 0 1 DMW Test 0 1 2 0 0 0 PCS>0.5 3 8 7 6 5 9 PT Test 5 6 5 0 0 8 Number of countries 10 10 10 10 10 10

B. Minor Currencies Rationality Tests Unbiasedness Test 23 14 16 23 24 23 Orthogonality Test 1 17 11 16 4 17 21 Orthogonality Test 2 21 13 15 6 3 15 Predictive Accuracy Tests MSPE Ratio<1 5 12 15 11 15 15 DMW Test 0 8 12 6 5 13 PCS>0.50 17 19 20 23 24 26 PT Test 7 10 6 9 21 24 Number of countries 27 27 27 36 36 36

Notes: The first three rows in Panels A and B report the number of significant χ2 statistics (at the 10% significance level or higher) for the joint null of unbiasedness and orthogonality. “Orthogonality Test 1” and “Orthogonality Test 2” denote the tests of orthogonality of the forecast errors to lagged forecast errors and lagged actual exchange rate depreciation, respectively. The last five rows in Panels A and B report the number MSPE ratio less than one, the number of significant DMW statistics, the number of proportions of correctly signed forecasts above 0.50, the number of significant PT statistics (at the 10% significance level or higher), and the overall number of countries in each group and each dataset. In Panel A, all the cells have 10 possible rejections. In Panel B, all the cells for Consensus Economics Data have 27 possible rejections, and all the cells for FX4casts data have 36 possible rejections.

33

Appendix A. List of Countries in Consensus Economics Dataset

Forecast horizon, h = 3, 12

h = 24 Country Exchange Rate

Sample Period N Sample

N