How to Prevent Failure of Financial Institutions?

14

1 Financial System The financial system is a set of organized institutional set-up through which surplus units transfer their funds to deficit units. Define a financial system fair narrowly, to consist of a set of markets, individuals and institutions, which trade in those markets and the supervisory bodies responsible for their regulation. The end-users of the system are people and firms whose desire is to lend and to borrow. A financial system is a system that to channels funds from lenders to borrowers, to create liquidity and money, to provide a payments mechanism, to provide financial services such as insurance & pensions and to offers portfolio adjustment facilities. In Finance, the financial system is the system that allows the transfer of money between savers and borrowers. It comprises a set of complex and closely interconnected financial institutions, markets, instruments, services, practices and transactions. An economy’s financial system exists to organize the settlement of payments, to raise and allocate finance and to manage the risks associated with financing and exchange. So, the government sector and the corporate sector are the users of financial surplus of household sector and that the financial sector performs this vital function of intermediation. Empirical evidence shows that the growth of financial markets and development of the economy are complementary to each other. A developed financial system is one that has a secure and efficient payment system, security market and financial intermediaries that arrange financing and derivative markets & financial institutions that provide access to risk management instruments. Thus, A financial system consists of a set of organized markets and institutions together with regulators of those markets and institutions. Their main function is to channel funds between end users of the system: from lenders (‘surplus units’) to borrowers (‘deficit units’). In addition, a financial system provides payments facilities, a variety of services such as insurance, pensions and foreign exchange, together with facilities, which allow people to adjust their existing wealth portfolios. STRUCTURE OF FINANCIAL SYSTEM IN BANGLADESH Background of financial system in Bangladesh: The financial system in Bangladesh includes Bangladesh Bank (the Central Bank), scheduled banks, non-bank financial institutions, Microfinance institutions (MFIs), insurance companies, co-operative banks, credit rating agencies and stock exchange. Among scheduled banks there are 4 Nationalised commercial banks (NCBs), 4 state owned specialized banks (SBs), 30 domestic private commercial banks (PCBs), 9 foreign commercial banks (FCBs) and 31 non-bank financial institutions (NBFIs) as of December 2006 after that total number of institutions are increasing rapidly. However, Rupali Bank, an NCB is being sold to a foreign buyer, and once this transaction is completed, the country will have only 3 NCBs., which are being corporative. Over and above the institutions cited above, four development financial institutions namely 1)House Building Financial Corporation(HBFC) 2) Palli Karma Sahayak Foundation(PKSF) 3) Samabay Bank 4) Grameen Bank

-

Upload

bijoy-salahuddin -

Category

Documents

-

view

14 -

download

2

description

How to Prevent Failure of Financial Institutions?

Transcript of How to Prevent Failure of Financial Institutions?

1

Financial System

The financial system is a set of organized institutional set-up through which surplus units

transfer their funds to deficit units. Define a financial system fair narrowly, to consist of a set

of markets, individuals and institutions, which trade in those markets and the supervisory

bodies responsible for their regulation. The end-users of the system are people and firms

whose desire is to lend and to borrow. A financial system is a system that to channels funds

from lenders to borrowers, to create liquidity and money, to provide a payments mechanism,

to provide financial services such as insurance & pensions and to offers portfolio adjustment

facilities. In Finance, the financial system is the system that allows the transfer of money

between savers and borrowers. It comprises a set of complex and closely interconnected

financial institutions, markets, instruments, services, practices and transactions. An

economy’s financial system exists to organize the settlement of payments, to raise and

allocate finance and to manage the risks associated with financing and exchange.

So, the government sector and the corporate sector are the users of financial surplus of

household sector and that the financial sector performs this vital function of intermediation.

Empirical evidence shows that the growth of financial markets and development of the

economy are complementary to each other. A developed financial system is one that has a

secure and efficient payment system, security market and financial intermediaries that

arrange financing and derivative markets & financial institutions that provide access to risk

management instruments. Thus, A financial system consists of a set of organized markets and

institutions together with regulators of those markets and institutions. Their main function is

to channel funds between end users of the system: from lenders (‘surplus units’) to borrowers

(‘deficit units’). In addition, a financial system provides payments facilities, a variety of

services such as insurance, pensions and foreign exchange, together with facilities, which

allow people to adjust their existing wealth portfolios.

STRUCTURE OF FINANCIAL SYSTEM IN BANGLADESH

Background of financial system in Bangladesh:

The financial system in Bangladesh includes Bangladesh Bank (the Central Bank), scheduled

banks, non-bank financial institutions, Microfinance institutions (MFIs), insurance

companies, co-operative banks, credit rating agencies and stock exchange. Among scheduled

banks there are

4 Nationalised commercial banks (NCBs),

4 state owned specialized banks (SBs),

30 domestic private commercial banks (PCBs),

9 foreign commercial banks (FCBs) and

31 non-bank financial institutions (NBFIs) as of December 2006 after that total number of

institutions are increasing rapidly. However, Rupali Bank, an NCB is being sold to a foreign

buyer, and once this transaction is completed, the country will have only 3 NCBs., which are

being corporative. Over and above the institutions cited above, four development financial

institutions namely

1)House Building Financial Corporation(HBFC)

2) Palli Karma Sahayak Foundation(PKSF)

3) Samabay Bank

4) Grameen Bank

2

They are operating in Bangladesh, all of which are state owned.

The financial system of Bangladesh is mainly bank dependent. Though in the recent years, a

number of non-banking financial institutions (leasing and merchant banks) have been

established, yet the banking sector still captures the lion share of the financial market.

Financial Institutions/Intermediaries:

An organization which borrows funds from lenders and lends them to borrowers on terms

which are better for both parties than if they dealt directly with each other. Financial

institutions as ‘intermediaries’: As a general rule, financial institutions are all engaged to

some degree in what is called intermediation. Rather obviously ‘intermediation’ means acting

as a go-between for two parties. The parties here are usually called lenders and borrowers or

sometimes-surplus sectors or units, and deficit sectors or units. As a general rule, what

financial intermediaries do is: to create assets for savers and liabilities for borrowers which

are more attractive to each than would be the case if the parties had to deal with each other

directly. There are two general consequences of financial intermediation. The first is that

there will exist more financial assets and liabilities than would be the case if the community

were to rely upon direct lending. The second general consequence of the intervention of

financial institutions is that lending and borrowing have become easier. It is now no longer

necessary for savers to search out borrowers with matching needs. In this sense financial

intermediaries have lowered the ‘transaction costs’ of lending and borrowing.

Banks

Banking is essentially based on the debtor-creditor relationship between the depositors and

the bank on the one hand and between the borrowers and the bank on the other. Interest is

considered to be the price of credit, reflecting the opportunity cost of money. The commercial

banking system dominates Bangladesh's financial sector. Bangladesh Bank is the Central

Bank of Bangladesh and the chief regulatory authority in the sector. The banking system is

composed of four Public commercial banks, five specialized development banks, thirty

private commercial Banks and nine foreign commercial banks. Out of 6562 scheduled bank

branches operating in the country, up to end December 2006 the NCBs operate 3384

branches, of which 2146 are in rural areas and 1238 are in urban areas; SBs have 1354

branches of which 1200 are in rural areas and 154 are in urban areas; PCBs have 1776

branches of which 488 are in rural areas and 1288 are in urban areas; and FCBs have 48

branches exclusively in urban areas. Out of 30 PCBs, 7 have been operating as Islamic banks.

After the year 2006 that total number of branches are increasing rapidly up to 2009.

List of All types of banking sectors are:

1) Central Bank

2) Private Commercial Banks

3) Public Commercial Banks

4) Foreign Commercial Banks

5) Specialized Development Banks

3

Private Commercial Banks

Even with all the provisions at hand, during the interviews many experts opined that there

could be separate agencies to regulate and supervise the private sector banking activities in

Bangladesh. A number of agencies can be set up and each would look into a number aspects

related to private sector banking. Under the current system, the commercial banks and

financial institutions have to report to and are to a certain extent supervised by the Securities

and Exchange Commission, when they register with the stock exchange. Private banks are the

highest growth sector due to the dismal performances of government banks (above). They

tend to offer better service and products.

STRUCTURE OF FINANCIAL SYSTEM IN BANGLADESH

b) Public Commercial Banks:

The Basel Committee on Banking Supervision published guidance in 1999 to assist banking

supervisors in promoting the adoption of sound corporate governance practices by banking

organizations in their countries. This guidance drew from principles of corporate governance

that were published earlier that year by the Organization for Economic Co-operation and

Development (OECD) with the purpose of assisting governments in their efforts to evaluate

and improve their frameworks for corporate governance and to provide guidance for financial

market regulators and participants in financial markets at public commercial banks.

· Sonali Bank Limited

· Janata Bank Limited

· Agrani Bank Limited

· Rupali Bank Limited

c) Private Foreign Commercial Banks:

The state and nature of corporate governance has been studied under five general

headings. Three types of foreign commercial banks or companies were studied: a)

the public corporations - these are mainly private utility companies operated by the

government with a board of director consisting of the people of Bangladesh and

few experts, b) financial institutions like banks which are listed in the Dhaka Stock

Exchange but related with governmental condition about share distribution and c)

non-financial limited companies also listed in the stock exchanges in the country but

related with governmental condition about share distribution.

4

d) Specialized Financial Institutions:

Out of the specialized banks, two (Bangladesh Krishi Bank and Rajshahi Krishi Unnayan

Bank) were created to meet the credit needs of the agricultural sector while the other two (

Bangladesh Shilpa Bank (BSB) & Bangladesh Shilpa Rin Sangtha (BSRS) are for extending

term loans to the industrial sector.

Non-Bank Financial Institutions

Non-Bank Financial institutions in Bangladesh have been playing a significant role in

financial system of the country. This sector has emerged as an increasingly important

segment of the financial system because of the rapidly rising demand for long term financing

and equity type services. NBFIs added differentiation to the bank based financial market of

Bangladesh. The inevitability of the NBFIs has created a new phase to strengthen the

financial system of the country in parallel with the saturated banking industry. Thus, this

sector has become a distinct player in maintaining the sound health of our financial and

economic sectors. NBFIs in Bangladesh play major role in filling gaps in financial

intermediation by providing diversified investment instruments and risk pooling services.

NBFIs have achieved impressive growth in recent years reflecting the importance of financial

innovation and holding the promise of deepening financial intermediation through satisfying

long term financing need.

Backgrounds of NBFIs in Bangladesh

NBFIs were incorporated in Bangladesh under the Company Act, 1912 and were being

regulated by thr provisions contained in Chapter V of the Bangladesh Bank Order. 1972.

Later to remove regulatory deficiency and also to define a wide range of activities to be

covered by the NBFIs, a new statute titled the “Financial Institution Act, 1993’ was enacted

in 1993 by the ‘Financial Institution Regulation, 1994’. NBFIs have been given license and

regulated under the Financial Institution Act 1993. There are 31 NBFIs licensed under this

act. As per the Financial Institution Regulation, 1994, at present minimum paid up capital for

NBFIs is Taka 1.0 billion or 100 Crores. So far, twenty one NBFIs raised capital though

issuing IPO, while three are exempted from the issuance of IPO. Other major sources of

funds of NBFIs are term deposit, credit facility from banks and other NBFIs, call money as

well as bond and securitization. The NBFIs business line is narrow in comparison with banks

in Bangladesh. Now a days the NBFIs are working as multi product financial institutions.

Year 2006 2007 2008 2009 2010 2011 2012

No. of NBFIs 29 29 29 29 29 30 31

Government

owned

1 1 1 1 1 2 3

Joint-venture 8 8 8 8 8 8 10

Private 20 20 20 20 20 20 18

New branches 10 8 8 8 20 53 3

Total branches 64 72 80 88 108 161 164

5

Source: Department of Financial Institutions and Markets, BB

NBFI Sector Performance

Assets: The asset base of the NBFIs increased substantially in 2911 and 2012. Aggregate

industry assets increased to Taka 288.4 billion 2011 from taka 251.5 billion in 2010, showing

a growth of 14.7 percent. The growth rate for 2012 will probably be higher than that of 2011.

By the end of June 2012 taka asset increased to Taka 309.0 billion.

Investment: NBFIs are investing in different sectors of the economy, ut their

investments are mostly concentrated in industrial sector. In June 2012 the different sectors in

which the NBFIs invested were industry (42.6%), real estate (18.5%), trade and commerce

(10.4%), merchant banking (1.4%), agriculture sector (1.3%) and others (17.8%)

Liabilities and equity: The aggregate liability of the industry in 2011 increased to

Taka 235.7 billion from Taka 206.8 billion in 2010 while equity increased to Taka 52.7

billion in 2011 compared to Taka 44.7 billion in 2010 showing an overall increase of 14.0

and 17.9 percent respectively. Total liabilities and equity were Taka 252.2 billion and Taka

56.8 billion respectively at end of June 2012

Deposits: Total deposits of the NBFIs in 2011 rose to Taka 112.6 billion (47.8% of total

liabilities) from Taka 94.4 billion (45.7% of total liabilities) in 2010 showing an overall

increase of 19.3 percent. On 30 June 2012 total deposit stood at Taka 124.2 billion (49.2

percent of total liabilities)

Overall Performance of the NBFIs in terms of CAMELS rating

As of December 2011, out of the 29 NBFIs, the composite CAMEL rating of 2 NBFIs were

“1” or Strong, 16 were “2” or Satisfactory, 10 were “3” or Fair and the rest was “4” or

Marginal. On the other hand, in December 2010, out of the 29 NBFIs, the composite CAMEL

rating of 14 NBFIs were “2” or Satisfactory and the rest of the 15 NBFIs rating were “3” or

Fair. The CAMEL rating of the entire industry improved compared to the previous year

6

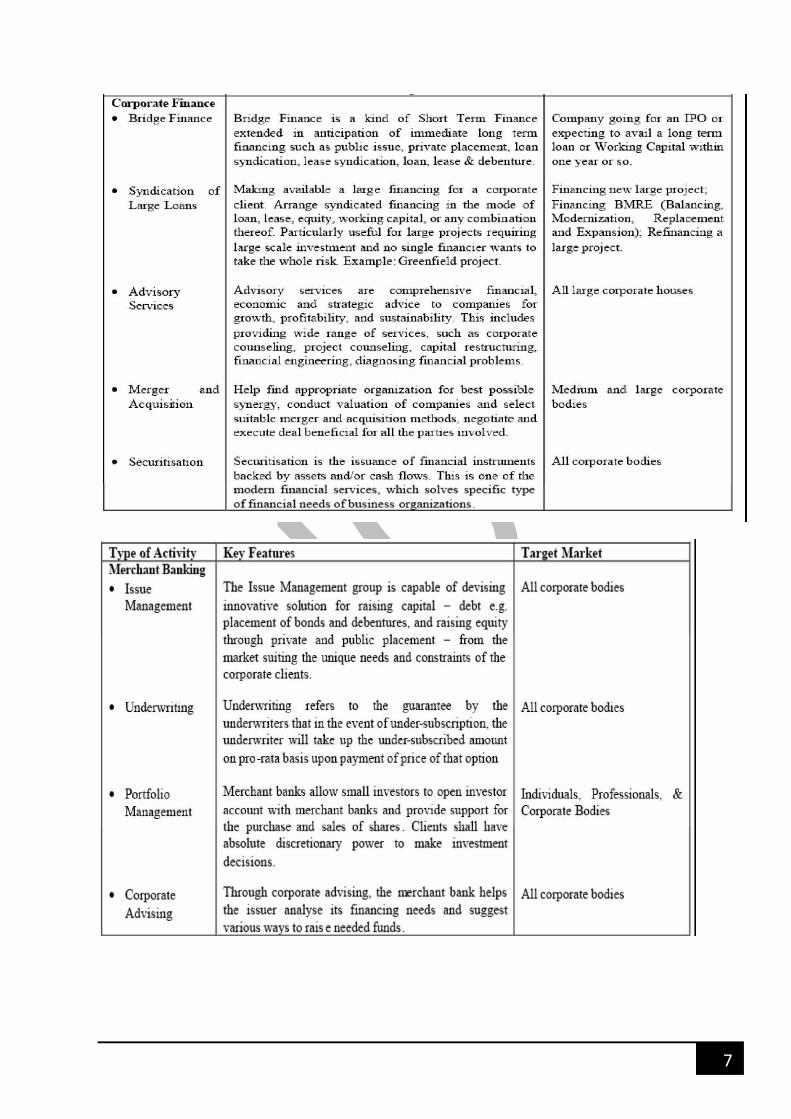

Different products and services

7

8

a) Insurance Companies

The insurance sector is regulated by the Insurance Act, 1938 with regulatory oversight

provided by the Controller of Insurance on authority under the Ministry of Commerce. A

separate Insurance Regulatory Authority is being established. A total of 62 insurance

companies have been operating in Bangladesh, of which 19 provide life insurance and 43 are

in the general insurance field. Among the life insurance companies, except the state owned

Jiban Bima Corporation (GBC) foreign owned American Life Insurance Company (ALlCO),

and the rest of the private. Among the general insurance companies, state-owned Shadharan

Bima Corporation (SBC) is the most active in the insurance sector

b) Security Firms

Financial institutions that underwrite securities and engage in related activities such as

securities brokerage, securities trading and making a market in which securities can trade.

c) Investment Banks

It primarily helps net suppliers of funds transfer funds to net users of funds at a low cost and

with maximum degree of efficiency.

d) Financial Companies

The primary function of finance companies is to make loans to both individuals and business.

Finance companies provide such services as consumer lending, business lending and

mortgage financing.

e) Mutual Funds

Mutual funds are portfolios of different securities such as stocks, bonds, treasuries,

derivatives, etc. Mutual funds pool money of both individual and institutional investors

allowing the funds to achieve: (i) economies of scale by reducing costs and increasing

9

investment returns; (ii) divisibility and diversification; (iii) active management with superior

stock picking and market timing; (iv) reinvestment of dividends, interest and capital gains;

(v) tax-efficiency; and (vi) buying and selling flexibility. There might be varieties of mutual

funds that differ in terms of their investment objectives, underlying portfolios of shares, risks

and returns, fees and expenses, etc.

Mutual funds are professionally managed investment schemes that collect funds from small

investors and invest in stocks, bonds, short term money market instruments, and other

securities. This ensures a diversified portfolio for the investors at much less efforts than

through purchasing individual stocks and bonds. Fund managers who undertake trading of the

pooled money and are responsible for managing the portfolio of holdings usually manage

mutual funds. Generally, mutual funds are organized under the law as companies or business

trusts and managed by separate entities. Mutual funds fall into two categories: open-end

funds and closed-end funds.

f) Pension Funds

Pension funds are analyzed as financial intermediaries using a functional approach to finance,

which encompasses traditional theories of intermediation. Funds fulfill a number of the

functions of the financial system more efficiently than banks or direct holdings. Their growth

complements that of capital markets and they have acted as major catalysts of change in the

financial landscape. Financial efficiency in this functional sense is not the only reason for

growth. It is also a consequence of fiscal incentives and benefits to employers, as well as

growing demand arising from the ageing of the population. Employers, such as companies,

public corporations, and industry or trade groups, typically sponsor pension funds;

accordingly, employers as well as employees typically contribute. Funds may be internally or

externally managed. Returns to members of pension plans backed by such funds may be

purely dependent on the market (defined contribution funds) or may be overlaid by a

guarantee of the rate of return by the sponsor (defined benefit funds).

The Role of Financial Intermediaries

The reasons center around the power of information: how to get quality information at a

reasonable cost. In this context, financial intermediaries perform 5 functions:

1. Pooling the resources of small savers

Many borrowers require large sums, while many savers offers small sums. Without

intermediaries, the borrower for a $100,000 mortgage would have to find 100 people willing

to lend her $1000. That is hardly efficient. Banks, for example, pool many small deposits and

use this to make large loans. Insurance companies collect and invest many small premiums in

order to pay fewer large claims. Mutual funds accept small investment amounts and pool

them to buy large stock and bond portfolios. In each case, the intermediary must attract many

10

savers, so the soundness of the institution must be widely believed. This is accomplished

through federal insurance or credit ratings.

2. Providing safekeeping, accounting, and payments mechanisms

for resources

Again, banks are an obvious example for the safekeeping of money in accounts, the records

of payments, deposits and withdrawals and the use of debit/ATM cards and checks as

payment mechanisms. Financial intermediaries can do all of this much more cheaply than you

or I because the take advantage of economies of scale. All of these services are standardized

and automated on a large scale, so per unit transaction costs are minimized.

3. Providing liquidity

Recall that liquidity refers to how easily and cheaply an asset can be converted to a means of

payment. Financial intermediaries make is easy to transform various assets into a means of

payment through ATMs, checking accounts, debit cards, etc. In doing this, financial

intermediaries must many short term outflows and investments will long term outflows and

investments in order to meet their obligations while profiting from the spread between long

and short term interest rates. Again, economies of scale allow intermediaries to do this at

minimum cost.

4. Diversifying risk

We have seen in chapter 5 how diversification is a powerful tool in minimizing risk for a

given leven of return. Financial intermediaries help investors diversify in ways they would be

unable to do on their own. Mutual funds pool the funds of many investors to purchase and

manage a stock portfolio so that investors achieve stock market diversification for as little at

$1000. If an investor were to purchase stocks directly, such diversification would easily cost

over $15,000. Insurance companies geographically diversify in ways that a Gulf Coast

homeowner cannot. Banks spread depositor funds over many types of loans, so the default of

any one loan does not put depositor funds in jeopardy.

5. Collecting and processing information

Financial intermediaries are experts at collecting and processing information in order to

accurately gauge the risk of various investments and to price them accordingly. Indviduals do

not likely have to tools or know-how to do the same, and certainly could not do so as cheaply

as financial intermediaries (once again, economies of scale are important here). This need to

collect/process information comes from a fundamental asymmetric information problem

inherent in financial markets.

11

Reasons for failure

1) Enforcement actions

Before a banks fails their CAMELS rating moves down a steady slope until the

bank is rated a composite “5” before failure.

2) Capital

Of the 322 US banks that failed from 2008 to 2010, 293 or 91% were

undercapitalized or worse the quarter before they were seized.

3) Material loss review

a) Poor underwriting and credit administration practices.

b) Board and management not implementing adequate risk management

practices.

c) Aggressive growth.

d) Loss on investment securities.

e) Out-of-territory lending or purchases of risky loan participants.

4) Asset Quality

Loans are the largest asset on a bank’s balance sheet, and consequently, they have

the greatest potential to negatively impact a depository institution’s capital if they

go bad. For the failed banks, mostly had loan quality problems before failing.

After loans, securities are the 2nd largest asset on a bank’s balance sheet. In

contrast to loan quality, there are no standardized metrics which regulators use to

assess securities quality. This is mainly due to the fact that investment securities

are more complex. Yet, of the banks without loan quality problems, five failed

banks had investment quality problems leading up to their failures.

All in all, out of all the failed banks from 2008 to 2010, only three banks had

sound loan and investment quality the quarters leading up to failure.

5) Earnings

6) Management

a) Incompetency

b) Dishonesty

7) Higher Competition

Due to higher competition they often attract depositors with higher interest rates

and go for risky investment and loan disbursement with a hope get higher return

for greater profitability. Such higher risk often lead to bank failure.

12

Prevent Bank Failure

Regulations:

1) Restrictive chartering: Limit the number of license to the banks. Since competition

among the banks will led their profit margin down and influence them to take risky

investment and the possibility of failure will rise. Since the market is concentrated and

profit margin is getting lower eventually banks will fail. So limiting the number of the

license will reduce competition in the market and as a result the bank failure will be

reduced.

2) Limit interstate banking( McFadden act 1927)

Limit interstate banking will reduce competing by not competing with so many banks

in the same state which will increase the profit up and will not let the bank broke.

3) Limit competition for deposits

Maximum interest rate or Celling on deposits. It can eliminate the banks from fighting

fiercely for deposit. If there is no celling the banks may attract with higher interest

rate but may fail with making risky investment with a hope to get higher return. Net

interest margin get lower and lower and the bank fail.

4) Glass-Steagall: Keep other institutions out of banking.

5) Limit on the size of loan any one borrower.(Hall Mark)

Not making all the loans to a single borrower because if the borrower get in trouble

the bank will have huge loan losses. If they diversify the loan the risk can be reduced.

6) Capital Requirements:

Capital Adequacy ratio should be >=8%

7) Monitoring (CAMELS Rating)

From the banks side

1) Management:

Due to incompetency the loan officers disburse loan in a small area without

understanding the consequences or risk and can eventually fail and sometimes fraud.

So it is necessary to have fair management practice.

2) Asset quality:

Banks shouldn’t make loan in a highly risky project and shouldn’t invest in risky

investment. This is the one single reason banks fail. Due to incompetence the

managers fail to evaluate properly the project and without considering the project

13

riskiness they disburse loans and eventually incur loss. It’s necessary to diversify the

loan.

3) Liquidity:

Banks must enough liquidity.

4) Sensitivity:

Banks should go for such investment where the banks is highly sensitive to the

changes. If banks have so many long term loans then it’s good to sell some of them if

possible. Or go for hedging.

14

Conclusion:

For a healthy economy a good financial is very necessary. Without a strong financial

system an economy don’t flourish. To have a sound financial system it is necessary to

financial institutions are working properly which can ensure the growth of the

economy. So it’s vital to take all necessary actions to prevent failure of financial

institutions which can lead to a healthy economy.

![Aalborg Universitet Toward Reliable Power …failure, frequency of failure, or in terms of availability [1]. The essence of reliability engineering is to prevent the creation of failures.](https://static.fdocuments.in/doc/165x107/5ea2cb42ce180618a40e75d3/aalborg-universitet-toward-reliable-power-failure-frequency-of-failure-or-in-terms.jpg)