How Reps Create Value for Care Givers - HIRA conference/Michael_Marks_PP.pdf · How Reps Create...

52

How Reps Create Value for Care Givers Presenter J. Michael Marks, Managing Partner INDIAN RIVER CONSULTING GROUP www.ircg.com Thursday, June 20, 2013 8:00 AM to Noon Ft. Lauderdale, Florida

Transcript of How Reps Create Value for Care Givers - HIRA conference/Michael_Marks_PP.pdf · How Reps Create...

How Reps Create Value for Care

Givers

Presenter

J. Michael Marks, Managing Partner INDIAN RIVER CONSULTING GROUP

www.ircg.com

Thursday, June 20, 2013

8:00 AM to Noon

Ft. Lauderdale, Florida

WWW.IRCG.COM INDIAN RIVER CONSULTING GROUP

2

Download a PDF of this Presentation

1. Go to www.ircg.com and click on the Client

Downloads tab

2. Enter User Name: HIRA and Password: charlie and

click on the Login button

3. Click on the Presentations folder to open it

4. Navigate to this presentation (it will be the only one in

the folder) and click on the Download button

5. Depending on your browser, a pop up window will

appear where you can select whether to open or save

the file

For Your Convenience

WWW.IRCG.COM INDIAN RIVER CONSULTING GROUP

3

Antitrust Disclaimer

Plan on being deposed in the next 24 months about this meeting

• It is important to be able to enthusiastically tell the whole truth

• If you aren’t deposed- then you can be happy either way

We are NOT going to discuss any specific customers or any specific products or any specific prices or any specific geographical markets, however

• We can speak freely about distributors, in general

• We can speak freely about trading practice alternatives and channel economics

We are not going to make any agreements, either explicit or implied, with any other participant with respect to our future trading practice plans or intentions

• Every firm is free to pursue their own best commercial interests unencumbered by any other participant in this room

WWW.IRCG.COM INDIAN RIVER CONSULTING GROUP

4

About Us

We are a mid size consulting firm founded in 1987 that

provides advisory services for manufacturers and

distributors of products or services in mature, often

complex, B2B markets

Our expertise is in market access which measures how

well resources are aligned with growth opportunities

• Strategy development and execution

• Channel management

• Sales effectiveness and compensation

Well recognized for our industry depth, experience

and practical approach

• Permanent faculty members at UID/Purdue

• Senior NAW Research Fellow & 5 years on HIDA’s board

WWW.IRCG.COM INDIAN RIVER CONSULTING GROUP

5

Agenda

This industry is

rapidly accelerating

to an unsupportable

future and the great

hope is innovation

driven from the

center

Market dominance

requires selling skills

and channel

management skills

for the independent

rep

Healthcare market issues

Channel design principles

Your downstream role

Your upstream role

Innovation trends

WWW.IRCG.COM INDIAN RIVER CONSULTING GROUP

6

The GPO Industry Impact If the only tool that you have is a hammer, then everything looks like a

nail

They are unique to the healthcare industry

• They now extract more value from the supply chain than they add

• They will not go away

• Why do we still have labor unions?

They are having lifecycle issues

• IDNs are regaining strength

• Compliance is a continual battle for them

• As time progresses the incremental value drops (diminishing returns)

• While distributors complain, the transaction complexity is a barrier to entry to distribution firms outside of healthcare

• They are driving hard to get beyond the acute marketplace

WWW.IRCG.COM INDIAN RIVER CONSULTING GROUP

7

Healthcare Has Two Terminal Diseases

Transaction Pricing Myopia (TPM) to the exclusion of market based pricing*

Incremental Plant Loading (IPL)

Symptoms of the combination include:

• Back end rebates, tracking fees, meeting participation fees, regional meeting support fees, meet comp or SPA (Special Pricing Authorizations) discounts, special stock rotations, inventory price protections, consignment inventories with forgiveness, Ship From Stock and Debit transaction costs, free samples and demo equipment, etc.

GM%ƒ(1/Transaction Size)

“5% Greater capacity utilization has an incremental

net profit of 72%”

*The McKinsey quarterly, “The Power of Pricing,” Michael V. Marn, Eric V. Roegner, and Craig C. Zawada, February 2003

WWW.IRCG.COM INDIAN RIVER CONSULTING GROUP

8

The Wal-Mart Disease

Many large, and leading, companies have not created much

shareholder value the last decade

The Wal-Mart disease is focusing on executing the business’s

long-standing success formula better, faster and cheaper —

even though it’s not creating any value for their shareholders

Wal-Mart is now paying dividends so they look more like a

bond than an equity

http://www.business-

strategy-

innovation.com/wordpr

ess/2010/12/walmart-

disease/

What Happens When You Get To The Bottom?

WWW.IRCG.COM INDIAN RIVER CONSULTING GROUP

9

Gray Market Products Our industry’s problems are self inflicted

There are many sources and causes of gray market product

creation* but healthcare issues center around a primary cause:

• When the (Cumulative effects of pushing sales and increasing

incentives to buy) > (Consumption plus channel storage capacity) then

product reemerges as gray market for resale

• For example, acute care groups place a big order to get a great discount

and then resell the excess product to other users or channel partners

(BTW: it also makes it easier to camouflage counterfeit product)

Managing the problem with legal agreements works as well in

healthcare as it does in music downloading

The root cause is the industry myopia with the terminal

diseases- TPM and IPL

Bottom line is that it is not going to change for a while *http://infosciencetoday.org/type/research-type/the-gray-market-as-a-growth-tool-for-small-

high-technology-firms-a-conceptual-framework.html

* Source:

WWW.IRCG.COM INDIAN RIVER CONSULTING GROUP

10

Private Label Is A Catch All Term

Distributors average twice the margin compared to branded products

There are branded products provided by a manufacturer

• Sometimes with many price points and brands

There are generic products provided by a manufacturer

These same products can be provided by a distributor or a group under their name

• There are even suppliers who only do private label production

It is not about the products, it is about the brand promise

WWW.IRCG.COM INDIAN RIVER CONSULTING GROUP

11

Figure 6 % of Contractors Willing to

Use Private Label Products

Trusting Private Label

The

percentage of

surveyed

contractors

who indicated

they were

willing, very

willing, or

already buying

different types

of private label

items

Source: Emerging Trends & Traps in Residential Construction: The NAED Roadmap to

Future Opportunities http://www.naed.org/Education%20and%20Research%20Foundation/Foundation%20Research/Foundation%20Research%20Completed%20Research.html

No

Yes

Maybe

The electrical market is instructive for healthcare because screw ups kill people

WWW.IRCG.COM INDIAN RIVER CONSULTING GROUP

12

Group Activity

Break into groups as instructed

Choose a group leader by determining who has traveled to the most exotic

location

The role of the group leader is to ensure that everyone weighs in with their

own views and that the group stays on track

Consider these statements and questions

1. Share views with respect to the current race to the bottom on pricing

and whether anyone has seen examples of forces that may change the

trend

2. Over the next five years will the role of private label products in this

industry increase or decrease or stay about the same?

3. How does the role of the independent rep change when looking at

private label products?

The purpose is simply to help you clarify your own thinking

WWW.IRCG.COM INDIAN RIVER CONSULTING GROUP

13

Agenda

Healthcare market issues

Channel design principles

Your downstream role

Your upstream role

Innovation trends

The channel is an integral

part of healthcare markets,

customers choose the

distributor before they

choose the brand

“Good enough is now good

enough” The Healthcare mandate on private label

“Products are built in

factories while brands are

built in the mind” Walter Landor

WWW.IRCG.COM INDIAN RIVER CONSULTING GROUP

14

What Is A Marketing Channel?

A channel is an interdependent group of firms who are involved in how a product is used or consumed

Compensation is provided to channel members to reflect the value of services that they provide

• Some are over and under compensated as channels evolve

Many firms confuse products and channels

• The wiener is the product; the bun and condiments are the channel; and all the customer wants is a good lunch

• Even more firms mistakenly assume that the brand is only about the product

WWW.IRCG.COM INDIAN RIVER CONSULTING GROUP

15

Marketing Channel Functions

Marketing channels connect end customers with suppliers by

providing demand creation, logistics, financing and support

services

• Distributors can provide lower cost coverage with their gross margin

basket, they can pull through sales by winning ties when the customer is

indifferent, and they can lower transaction costs independent of order

size

Including distributors, buying groups, agents, reps and brokers

• They survive if they perform activities more cost effectively than those

they buy from (suppliers) and sell to (customers)

Gross margin or commissions compensate them for their value

added

Channel players can be eliminated but channel functions

cannot

WWW.IRCG.COM INDIAN RIVER CONSULTING GROUP

16

Manufacturer

The Channel Story Gather information from multiple sources and look for key drivers and

incorrect assumptions to create actionable choices.

Optimized

Channels Economics Coverage Recommendations

& Action Planning

Channel

Partners Customers

Segmentation

IRCG Channel Analysis Model

We’ve all got cherished beliefs

WWW.IRCG.COM INDIAN RIVER CONSULTING GROUP

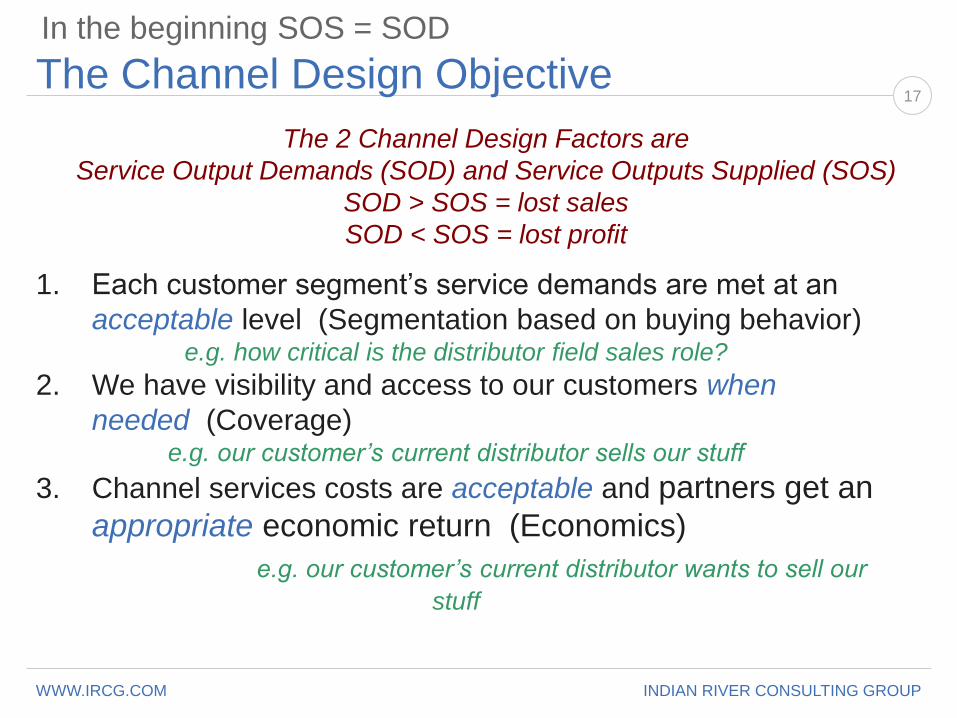

17 The Channel Design Objective

1. Each customer segment’s service demands are met at an

acceptable level (Segmentation based on buying behavior) e.g. how critical is the distributor field sales role?

2. We have visibility and access to our customers when

needed (Coverage) e.g. our customer’s current distributor sells our stuff

3. Channel services costs are acceptable and partners get an

appropriate economic return (Economics)

e.g. our customer’s current distributor wants to sell our

stuff

The 2 Channel Design Factors are

Service Output Demands (SOD) and Service Outputs Supplied (SOS)

SOD > SOS = lost sales

SOD < SOS = lost profit

In the beginning SOS = SOD

WWW.IRCG.COM INDIAN RIVER CONSULTING GROUP

18

Distributor Position Defines Their Strategy

Distributor Product Lines Dollar

Share

These products are higher

margin and get pulled

through with the primary

products

Gap

Fillers

Primary Products

50%

30%

~1-5 Top Vendors

20%

Tertiary

Products

Mfr says jump,

disty says “How

high?”

Next 5-10

Everyone

Else

Distributors need and nurture secondary and tertiary products to expand

their share of spend in their customers

ETDBW* always

trumps price and

quality

* Easy To Do Business With

WWW.IRCG.COM INDIAN RIVER CONSULTING GROUP

19

Cost to Serve Considerations

The nature of the business makes direct cost calculations difficult, as channel

partners routinely

• Lose money on individual items to secure an overall profitable order

• Lose money on individual orders to secure an overall profitable customer

• Accept lower margins on high velocity items or strong brands

Manufacturers are often incapable of providing transactional support services for

end users (i.e. “mass customization”)

• Credit risk analysis and customized terms

• Processing millions of small transactions

• Providing highly flexible logistics (e.g. deliveries accepted between 6:00 and 6:15 AM on

Thursdays only)

% of Sales Gross Margin % of Gross Profit % of Sales Effort

Primary Products 60% 8 – 10% 47% 68%

Secondary Products 30% 15 – 25% 37% 30%

Tertiary Products 10% 30% 16% 2%

Where is your product bundle in the distributor product mix?

WWW.IRCG.COM INDIAN RIVER CONSULTING GROUP

20

Group Activity

Break into groups as instructed

Choose a group leader by determining who has the least total tenure in the

healthcare industry

The role of the group leader is to ensure that everyone weighs in with their

own views and that the group stays on track

Consider these statements and questions

Winning the new game for the rep firm requires true analytical expertise far

in excess of that of your principals, the old time sales guy won’t make it

1. Compare notes with each other on your agreement or disagreement

with the statement above

2. What are some best practices where the rep firm uses market data and

insight to educate their principals and help set appropriate

expectations?

The purpose is simply to help you clarify your own thinking

WWW.IRCG.COM INDIAN RIVER CONSULTING GROUP

21

Agenda

Healthcare market issues

Channel design principles

Your downstream role

Your upstream role

Innovation trends

For the manufacturer

employee sales rep, this

position used to be a

source of a company’s

competitive advantage-

but it has devolved into a

two year training course

for most

The independent rep has

become the last

repository of tenured

market knowledge and

insight

WWW.IRCG.COM INDIAN RIVER CONSULTING GROUP

22

Your Mission

Is to gain market dominance for your product bundle offering in

your assigned geography

Selling is, at the base, customer interruption behavior

You and your boss will have a conspiracy of effectiveness

Success requires the efforts of your channel partners who will

always act in their own self interest

You need to reward and punish channel partners and not all

should like you

Your success in this mission is dependent on your talent, your

value offering, and your time investment decision processes

Effective performance requires that upstream and downstream

partners are often equally irritated with you

WWW.IRCG.COM INDIAN RIVER CONSULTING GROUP

23

What You Need to Determine First

What should be the distributors role in your overall market development plan?

• Are they market makers or market servers or both?

• Which distributor locations or reps give you the best return on invested time and money?

Who really determines choosing your brand, end users, distributors, GPOs, or IDNs?

Do you clearly know what is in it for them and know why they “want to play”?

What are the areas of ambiguity between corporate policy (with your principals) with big nationals and favoritism to local operations?

What is your level of autonomy?

WWW.IRCG.COM INDIAN RIVER CONSULTING GROUP

24

Rank Each Distributor Rep*

Characteristic Winners Potentials Losers

Growth Rate Ranking Top 25% 26%-74% Bottom 25%

Help needed from you Little Moderate High

Price whining Little Moderate High

Your time investment Feels good Easy to ignore Demand lots of

help

Your ability to influence

growth

Low

High

No hope

Typical time investment /

Ideal time investment

25% / 10%

10% / 50%

65% / 40%

* Or branch location

WWW.IRCG.COM INDIAN RIVER CONSULTING GROUP

25

The Principle of Calculated Neglect

The distributor’s opinion of your skill and competence changes

based on your view of their ability to help you achieve market

dominance on your products in your assigned geography

• If they are losers, they need to think that you are a loser as well

• One or two annual complaints to your boss is the goal

• Make sure that your boss is expecting the calls first

Your evaluation is by location, or person, not corporate entity

• You always pay public homage to the big national distributors

If you want everyone to think that you are a great rep- then

you are investing time with losers that could get a better return

if invested with winners

• Never forget your mission

WWW.IRCG.COM INDIAN RIVER CONSULTING GROUP

26

This Book Is About Relationship Economics

The law of legitimate cross purposes

• Manufacturers care most about plant utilization and new

product introductions

• Distributors want to maximize customer share of spend,

overall margin mix, and provide mass customization

The law of perpetual change

• Relationships always start in coyote love (with poor or

nonexistent agreements) and become dysfunctional due to

death by a thousand cuts when incremental damage is not

managed

Manufacturing Retail Distribution Service

Fixed cost portion of

revenue High Medium Low Low

Labor portion of fixed

costs Low Medium High High

http://www.naw.org/publications/pubs_item_view.php?pubs_itemid=2

http://www.naw.org/publicat

ions/pubs_item_view.php?p

ubs_itemid=2

WWW.IRCG.COM INDIAN RIVER CONSULTING GROUP

27

This Book Had Several Key Messages

Messages were sent, but not heard

• The constant din of transaction negotiating drowned out significant

messages that led to profound crises, i.e. termination

The manufacturer’s sales rep was the critical link in the

relationship

• Good ones respected confidences, were slightly disobedient, and could

effectively carry messages

• The independent rep is a sovereign external peer and has more power

Distributors could be classed as winners, potentials, and

losers

• Many manufacturers made the mistake of treating the good ones like the

bad ones for the sake of consistency

How did you feel about your time investment choices?

WWW.IRCG.COM INDIAN RIVER CONSULTING GROUP

28

How to Manage the Distributor Only if you are Primary or a large Secondary

1. Annual planning

• Your commitments to them: Fill rates and lead time fluctuations, stock

rotations, technical & business development support

• Their commitments to you: Resale volume and some kind of sales

tracing, inventory levels, competitive intelligence

• Mutual Commitments to each other: Pricing, freight, and terms, customer

creation activities

2. Quarterly reviews

• Milestone measurement, corrective action, intelligence sharing,

concurrent training

3. Customer creation activities

• Competitor displacement, joint calls & promos, no “suck up” visits,

provision of qualified leads

Always Hold Up Your End!

WWW.IRCG.COM INDIAN RIVER CONSULTING GROUP

29

How to Manage the Distributor If you are Tertiary or a small Secondary

Be very easy to do business with (ETDBW) as this trumps price and product performance, hands down

• Internet availability & your home phone

• Don’t overreach your value to them

Provide some channel compensation to the individual instead of the channel partner firm

• Intrinsic (non cash) is also valuable

Develop a pricing strategy that leverages non-recurring investment activities

• Discounts for number of reps with a successful sale or demo or passing knowledge tests (you drive e-learning, not your principals)

Find an internal champion and reward lead “bird-dogging”

• You do demand creation and give the orders to your chosen ones

WWW.IRCG.COM INDIAN RIVER CONSULTING GROUP

30

Your Economic Power Market power is never given, it is taken

You compete for their mindshare against other suppliers by making a case for your features and benefits

• Sometimes this is an issue or a non event

• Alignment means that you win all the ties where the customer doesn’t care about brand, your product is simply bought and doesn’t need to be sold

Most customers have a preferred distributor rep

If the preferred rep protects your position with the customer, then you will support that rep over the other distributor sales reps

• You will not take other competitors into that account

• If competitors go on their own, bad accidents will happen to them

• You will take the loyal distributor rep into new end users that others have screwed up

WWW.IRCG.COM INDIAN RIVER CONSULTING GROUP

31

Do The Math

Any time you accompany a distributor sales rep (market

making pull through) to get only a product reorder (without

presenting products that the end user or contractor currently

doesn’t buy) you are wasting a sales call

• Calls to replenish inventory are market serving only

If you have a short tail (low switching costs) you will never

achieve market dominance for your products because of

• Existing distributor sales rep sabotage via movement to private label or

competing brands

• A competing distributor sales rep visits with a competitor

How do you identify when the two circumstances above occur in your

territory and what can you do about them?

How sticky is a sold customer to competitive encroachment?

WWW.IRCG.COM INDIAN RIVER CONSULTING GROUP

32

Your Specific Task

Know the preferred distributor of every major user of your

products

Your ride-along task is not about selling your stuff, it is about

aligning your support to specific customer-distributor rep pairs

Getting this right creates both high latency (resistance to

change) and channel power (leverage) with your distributor

reps

The dumbest thing that you can do is help a distributor get

business that you already have through another distributor

• Unless you are intentionally punishing the incumbent distributor rep- then

make it very public

WWW.IRCG.COM INDIAN RIVER CONSULTING GROUP

33

Group Activity

Break into groups as instructed

Choose a group leader by determining who has the most spouses,

children, and grandchildren

The role of the group leader is to ensure that everyone weighs in with their

own views and that the group stays on track

Consider these statements and questions

1. Compare views on Mike’s assertion that the principal of calculated

neglect is required to achieve market dominance

2. Without naming local names of distributors (big guys are OK) what are

the tradeoffs between how giant distributors and independent

distributor can help you make a market?

The purpose is simply to help you clarify your own thinking

WWW.IRCG.COM INDIAN RIVER CONSULTING GROUP

34

Agenda

Healthcare market issues

Channel design principles

Your downstream role

Your upstream role

Innovation trends

An independent

manufacturers rep, when

listened to, provides

significant market insight

to their principals

improving their alignment

of resources to real

growth opportunities in

the market

Reps often deliver

messages that are hard

to hear

WWW.IRCG.COM INDIAN RIVER CONSULTING GROUP

35

The Manufacturer Representative Function

The old school is a low and variable cost model providing a manufacturer

with access to a sales force that gets replaced with a direct sales force

when scale is achieved

The new school for manufacturers that understand channel insight is to

replace the direct sales force with rep firms gaining the following

• Significant cost savings in market serving (the bundling effect)

• Clear competence in market making by discrete tasks (2 tier rates)

• True market insight that challenges assumptions rather than simple

obedience (more effective market access)

• Access to distributor mindshare by leveraging the reps product portfolio

capturing channel led business

There is a growing gap between new school and old school rep firms

Old guy deep relationships versus quantified market insight

WWW.IRCG.COM INDIAN RIVER CONSULTING GROUP

36

Oversimplified Bundling Impacts

Situation: a manufacturer with total selling costs of 6% and margins of

30% and a fully loaded employee sales rep cost (W-2, T&E, benefits) of

$100,000 who makes 4 calls each day

Cost/call = $100,000 / (4 calls/day X 250 days/yr.) = $100/call

Sales required to break even = $100 / 30% margin = $333/call

Situation: A manufacturers rep for the above manufacturer where that

manufacturer’s revenue equals 10% of the reps line card on a 5%

commission line where the rep makes $100,000 fully loaded and makes 6

calls day

Cost/call = $100,000 / (6 calls/day X 250 days/yr) = $66/call

Sales required to breakeven = $66 / 5% = $1,320

Smallest customer covered for that mfr. =$1,320 X 10% share = $132

A rep can cover over twice the customer base at 16% lower cost

WWW.IRCG.COM INDIAN RIVER CONSULTING GROUP

37 The Manufacturer Challenge Most manufacturers have a pie splitting strategy

These strategies often just drive short-term, unsustainable results where

companies are merely "renting share” often destroying long-term industry

profitability for everyone involved

A market access category growth strategy examines and

invests on three variables

Category Growth = A (# of customers) x B* (units per user) x C (price per

unit). To grow a category, you can focus on A (by luring new customers into

the category), or B (by convincing existing users to buy additional units) or

C (by increasing prices).

Adjacency analysis is used to define new categories

http://blogs.hbr.org/cs/2013/04/the_rising_tide_lifts_one_boat.html

?utm_source=feedburner&utm_medium=feed&utm_campaign=Fe

ed%3A+harvardbusiness+%28HBR.org%29

Variation in plant utilization is the hidden profit leak

* e.g. Recency, frequency, **BER-age X utilization

** Beyond Economical Repair

WWW.IRCG.COM INDIAN RIVER CONSULTING GROUP

38

How Far Do You Reach For Growth?

We do market access and we

have learned

• It is much better to start with

customers than with what

someone at a principal decides

that they can make (internal view)

Why? Because they offer the

most realistic growth

opportunities for most B2B

manufacturers

• A new category is worth 100X the

revenue of a new product

• Line extensions are a distraction

Customers

Existing New

Pro

ducts

Exis

ting

Hard

2X Harder

Ne

w

2X

Harder

4X Harder

“Hail Mary” (New + New) growth opportunities are

expensive, distracting, and rarely successful (1% for P&G)

WWW.IRCG.COM INDIAN RIVER CONSULTING GROUP

39

Bought Versus Sold

A product is sold when a customer chooses it from competitive alternatives

for the first time

• A sales rep is often, but not always, involved

• Sometimes there is a thoughtful evaluation of price/performance criteria

• With channel led business the customer doesn’t care or their choice is

independent of price/performance criteria (they choose the distributor

first)

If the product is satisfactory it will be purchased again (bought) when the

customer’s requirement reoccurs- generally independent of sales efforts or

investments (interruptions are often irritating)

When the product is repurchased it is bought, not sold, as the market has

been made

• The long tail repurchase rate measures brand power and customer

switching costs

WWW.IRCG.COM INDIAN RIVER CONSULTING GROUP

40

Insight Is All Around You The automatic negotiating response is for customers to want distributors, and distributors to want manufacturers, to think that price is the only thing that matters

In negotiating, you want to buy from the best supplier at the worst supplier’s price

Since healthcare is primarily a channel led business, the manufacturer who wins ties, but loses head to head comparisons, will always have dominant market share

• What is required to capture discretionary distributor energy necessary to win the ties when the customer doesn’t care?

• Why do your principals spend so much time trying to get customers to care?

Examine your current volume and determine how much is bought versus sold (of the sold share how much is winning non-caring ties)

• Allocate your selling costs appropriately

You will make major changes is your resource deployments

WWW.IRCG.COM INDIAN RIVER CONSULTING GROUP

41

Functional Discounting

Functional discounting is about aligning channel compensation (distributor

margin) to your desired channel partner activities

• This reduces discounts for big orders (classic take-away power) to increase the

compensation for desired activities

• Most efforts fail because we are hostage to quarter end load up programs by

looking at invoicing rather than market position (the monkey on cocaine)

Distributor Annual Volume

<300K 101-300K <100K

Base discount 32% 29% 26%

Market data 3% 3% 3%

EDI Ordering 4% 4% 4%

Meeting plan 2% 2% 2%

Total discount 41% 38% 35%

VPA* for Over Plan 5% 5% 5%

*VPA = Volume Purchase Agreement

In healthcare

products, the

higher the ticket

price, the lower

the product

margin

&

The larger the

distributor take

away power, the

better their margin

WWW.IRCG.COM INDIAN RIVER CONSULTING GROUP

42

Distributor Compensation Changes When

They do more of these things

• Order in standard quantities or in truckload quantities

• Provide responsive point of sale reporting

• Price their activity within my guidelines

• Increase the number of market leading users of my product

• Sell the full product offering not just the fast movers

• Stock appropriate product breadth

• Increase their sales (not purchases) of my product

• Increase my revenue share of a given product category

They do less of these things

• Carry competing brands in my core product areas

• Take unauthorized discounts

• Competitively capture business that I already have with another distributor

• Ordering product with rush expediting

Think about market making versus market serving

These are about

market making or

lowering your

cost to serve

them

These are the

opposite

WWW.IRCG.COM INDIAN RIVER CONSULTING GROUP

43

Agenda

Healthcare market issues

Channel design principles

Your downstream role

Your upstream role

Innovation trends

The major driver of

innovation is always an

outsider’s perspective that

examines the status quo

The independent rep is one

of the primary sources

along with consultants and

other service providers

True open innovation

processes are magnets for

external input that

challenges assumptions

WWW.IRCG.COM INDIAN RIVER CONSULTING GROUP

44

The Weak Link in Supply Chain Management

Traditionally, SCM has centered around logistics and buy/sell

transactions. This is why technology is so prevalent in discussions

between partners. But is this really the most critical link? Maybe instead

of operations, distributors and manufacturers should focus on the sales

efficiency and effectiveness of their supply chain.

Supply chain management is a lot like marriage counseling:

most people consider it only because they hope it will fix their

partner

When suppliers talk about “taking costs out of the channel”

they’re usually not referring to their own profit margins

• Likewise, distributors are much more eager to create vendor score cards

than to participate in benchmarking of their own performance

WWW.IRCG.COM INDIAN RIVER CONSULTING GROUP

45

The IRCG Enterprise Model

This approach to sales is very different from the typical annual planning confrontation, where the manufacturer assigns

aggressive targets and pushes the distributor to devote more sales resources

Both parties take an honest look at their combined approach and ask the question, “Would this make sense if we were part of the same company?” • Financials are combined and shared with both executive teams

• A list of dumb stuff is identified and those practices are eliminated as “muda”, or non value added activity

• The other activities are sorted by who can perform them most effectively (this is not a negotiation)

• Roles are reassigned, compensation and incentives are agreed and scorecards are developed

• CFOs are always involved

WWW.IRCG.COM INDIAN RIVER CONSULTING GROUP

46

An Idea for Consideration Demand-driven channels is a term first used in NAW’s 2007

Facing the Forces of Change Study that described products

being pulled down the supply chain by actual customer

demand. As a new term, it captures the essence of a quietly

growing class of competitive activity. Success in these

efforts requires simultaneous adoption of technology, a

higher level of mutual trust and dependence than is typical,

some new analytics, and a clear recognition of some new

responsibilities to trading partners.

http://blogs.hbr.org/cs/2012/07/the_game_b

uyers_play_with_vend.html

Relationship buying and

sourcing has been replaced by

economic buying and sourcing

• Trusted relationships have

migrated to rabbits &

advantaged players

WWW.IRCG.COM INDIAN RIVER CONSULTING GROUP

47

The Whipsaw Effect

From suppliers

From customers

Research by Pembroke Consulting, published by the NAW Institute, 2007

Order from www.nawpubs.org

WWW.IRCG.COM INDIAN RIVER CONSULTING GROUP

48

WAL-MART “QUICK

RESPONSE” SYSTEM

SF BSF B SFB SF B

PUSH / LOAD UP STRATEGY

SF B

PULL THROUGH / JITPS = PRIMARY SUPPLIER B = BUYERS

SF = SALES FORCE DC = DISTRIBUTION CENTER

TRADITIONAL APPROACH

“QR” RESPONSE

DAILY, PAPERLESS, ERROR FREE

PS MFG DISTY WM END USER

PS MFG DC WM END USER (35% LESS)

• Better scale and efficiency from shifting selling and marketing resources

to the end of the supply chain

• Eliminate redundant functions and improve balance of supply and

demand costs

• Reinvest savings to create and capitalize on the power of brand

Quick Response System

This was built

in the

eighties

And the first

application of

two tier rep

commission

rates

WWW.IRCG.COM INDIAN RIVER CONSULTING GROUP

49

Vendor Managed Inventory (VMI)

Auto-replenish agreed SKU’s (Min/Max)

Clear, non sales, rules of engagement

Redeploy upstream sales rep to demand creation activities

FIFO and freight prepays go out the window

CHANNEL INVENTORY

MFR. DISTY CUST

$ 2 MILL $10 MILL $1 MILL

Manufacturer

Production

End Use

Demand

$ 2 MILL/MO $ 2 MILL/MO

What about the drop in sales?

The decision of when to replenish rests with the upstream supplier

WWW.IRCG.COM INDIAN RIVER CONSULTING GROUP

50

What if...

…we covered both ends?

Distributor

Cost reduction opportunity = 10N

where N is the number of channel partners

VMI DMI Manufacturer Customer

When deployed and stable, production

planning is driven by end user

consumption, not forecasts

Demand Driven Channels

WWW.IRCG.COM INDIAN RIVER CONSULTING GROUP

51

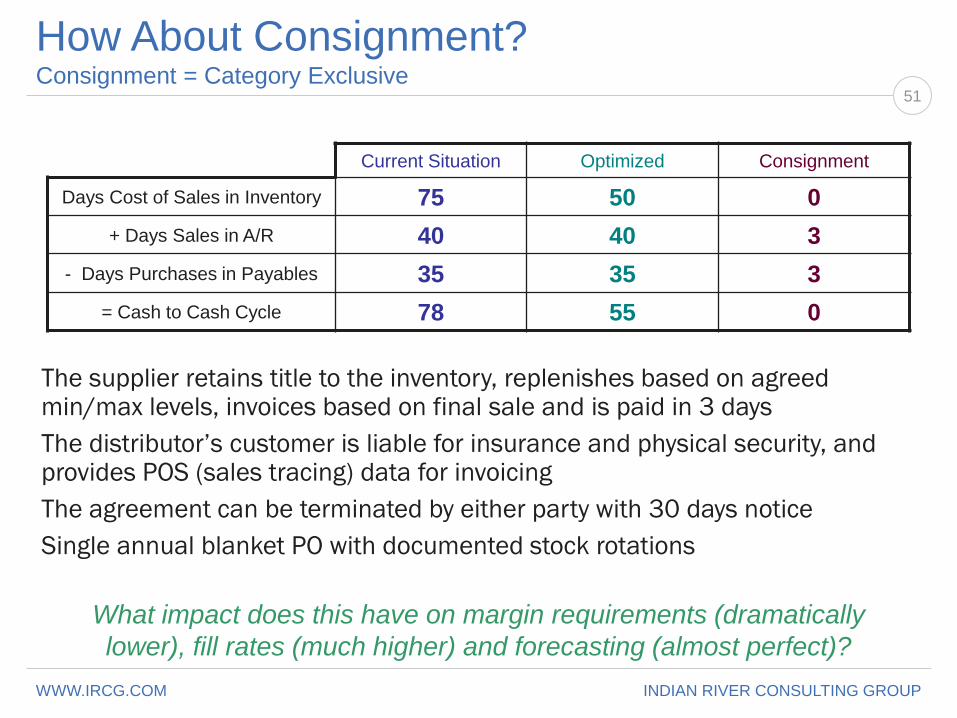

How About Consignment? Consignment = Category Exclusive

Current Situation Optimized Consignment

Days Cost of Sales in Inventory 75 50 0

+ Days Sales in A/R 40 40 3

- Days Purchases in Payables 35 35 3

= Cash to Cash Cycle 78 55 0

The supplier retains title to the inventory, replenishes based on agreed min/max levels, invoices based on final sale and is paid in 3 days

The distributor’s customer is liable for insurance and physical security, and provides POS (sales tracing) data for invoicing

The agreement can be terminated by either party with 30 days notice

Single annual blanket PO with documented stock rotations

What impact does this have on margin requirements (dramatically

lower), fill rates (much higher) and forecasting (almost perfect)?

WWW.IRCG.COM INDIAN RIVER CONSULTING GROUP

52

Group Activity

Break into groups as instructed

Choose a group leader by determining who has had the slowest

commission paying principal in days to pay (please don’t name names)

The role of the group leader is to ensure that everyone weighs in with their

own views and that the group stays on track

Consider these statements and questions

1. Share views with respect to the most valuable learning insight you

have picked up this morning.

2. Based on this session are there any activities that you will do less often

or even stop?

3. Based on this session are there any activities that you will start or do

more in the future?

The purpose is simply to help you clarify your own thinking