How Originators can Improve Their Understanding of...

51

How Originators can Improve Their Understanding of Generic Competition THOMSON REUTERS HEALTHCARE AND SCIENCE API INTELLIGENCE David Harding CPHI Worldwide 12 October 2009

-

Upload

trinhnguyet -

Category

Documents

-

view

219 -

download

0

Transcript of How Originators can Improve Their Understanding of...

How Originators can Improve Their Understanding of Generic CompetitionTHOMSON REUTERS HEALTHCARE AND SCIENCEAPI INTELLIGENCE

David Harding

CPHI Worldwide12 October 2009

Agenda

• Why API intelligence?

• Trends in the World Generic Market and API Industry

• Generic API development as early warning intelligence

• Examining the generic development process and timing

• The API Intelligence team at Thomson Reuters

• Case studies

Why API Intelligence?

For generic competition, there has to be generic finished product

For generic finished product there has to be generic API

If you want to understand generic competition, you have to

understand generic API manufacturing

Trends in the World Generic Market and API

Industry

4

Generics: a $100bn+ global market

Total World Pharmaceutical Sales: $600bn

US, Canada: $57bn

Latin America: $19bn

Western Europe

$17bn

Rest of World: $9bn

Eastern Europe & Russia: $5bn

Source: TS Research, IMS Health, VOI PharmaHandbook

Japan: $5bn

China: $3bn

Generics: Growth fastest in BRIC countries

US, Canada2%

Latin America: 15%

Western Europe2%

Rest of World10%

Eastern Europe & Russia12%

Source: VOI PharmaHandbook

Japan2%

China: 15%

2008 Final ANDA Approvals by Country

Source: FDA, Newport Premium™

Total ANDA Approvals by Indian Generics

0

20

40

60

80

100

120

140

160

180

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

# A

ND

As

0

5

10

15

20

25

30

# H

old

ers Tentative

Final

Holders

Source: Newport Premium™

Top 10 Companies by Number of Final ANDA Approvals: 1999 – 2008

Source: Newport Premium™

Group Country Number

Teva Pharmaceutical Industries Ltd Israel 364

Mylan Laboratories Inc USA 185

Novartis AG Switzerland 166

Apotex Inc Canada 158

Boehringer Ingelheim KG Germany 137

Watson Pharmaceuticals Inc USA 111

Actavis Group Hf Iceland 108

Daiichi Sankyo Co Ltd Japan 90

Fresenius AG Germany 85

Sun Pharmaceutical Industries Ltd India 78

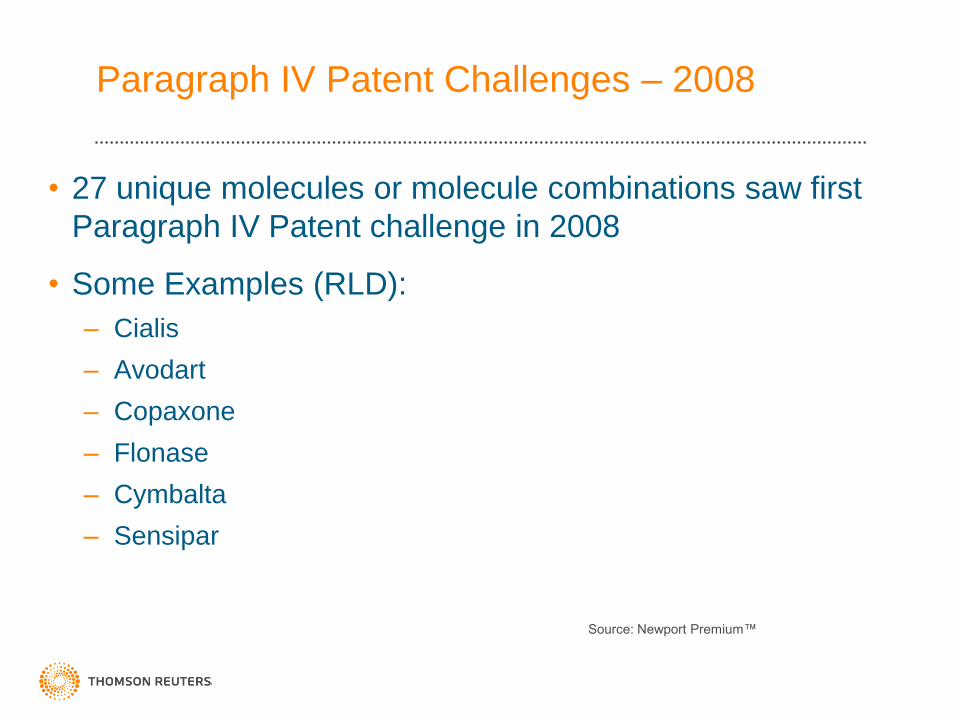

Paragraph IV Patent Challenges – 2008

• 27 unique molecules or molecule combinations saw first

Paragraph IV Patent challenge in 2008

• Some Examples (RLD):

– Cialis

– Avodart

– Copaxone

– Flonase

– Cymbalta

– Sensipar

Source: Newport Premium™

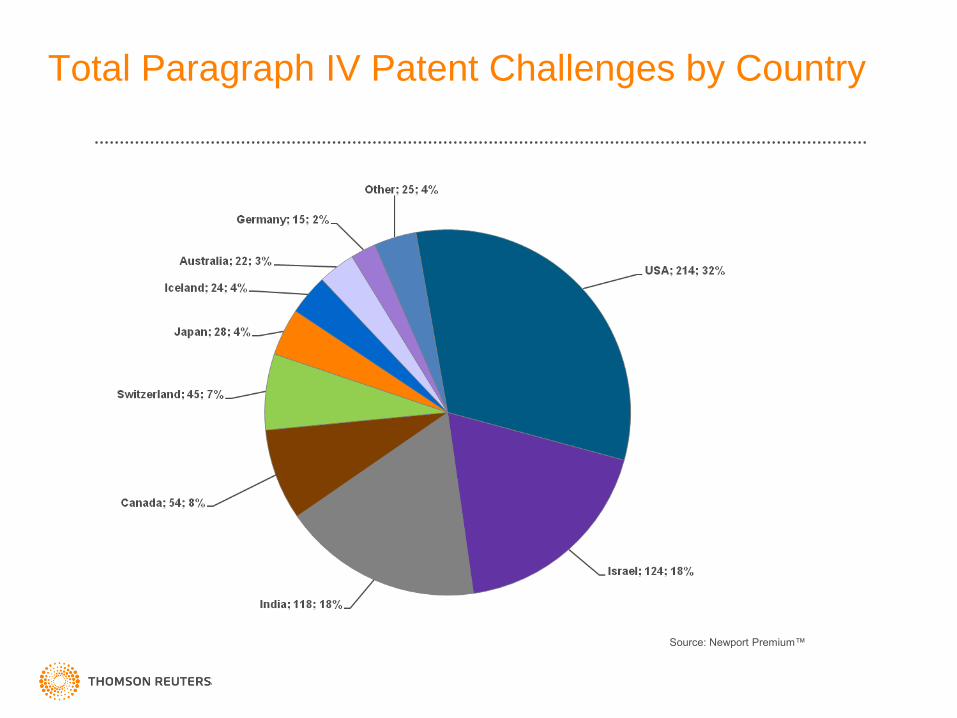

Total Paragraph IV Patent Challenges by Country

Source: Newport Premium™

Top 10 Companies by Number of Paragraph IV Patent Challenges

Source: Newport Premium™

Group Country Number

Teva Pharmaceutical Industries Ltd Israel 136

Mylan Laboratories Inc USA 66

Novartis AG Switzerland 63

Apotex Inc Canada 53

Sun Pharmaceutical Industries Ltd India 38

Dr Reddy's Group India 36

Watson Pharmaceuticals Inc USA 32

Daiichi Sankyo Co Ltd Japan 30

Actavis Group Hf Iceland 26

Par Pharmaceutical Companies Inc USA 24

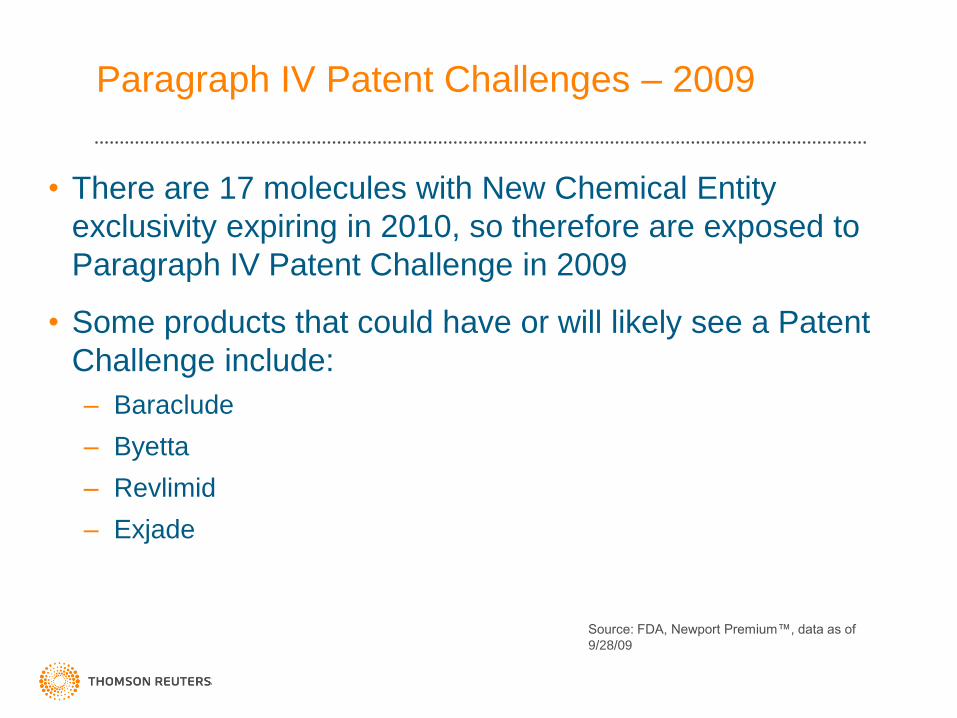

Paragraph IV Patent Challenges – 2009

• There are 17 molecules with New Chemical Entity

exclusivity expiring in 2010, so therefore are exposed to

Paragraph IV Patent Challenge in 2009

• Some products that could have or will likely see a Patent

Challenge include:

– Baraclude

– Byetta

– Revlimid

– Exjade

Source: FDA, Newport Premium™, data as of

9/28/09

Strong forces continue to drive generics

• Near universal encouragement of brand to generic substitution

• Continued price pressures (especially in EU and US)

• Too few products expiring for too many companies

• Emerging possibilities for biogenerics

• Rapid pace of mergers and acquisitions

• Patent challenges key to health of generic pipelines

• Low-cost, high-quality Indian FD production

• Emergent low-cost, high-quality Chinese API production

• Licensing deals now key to sustaining growth

• Early access to viable source of API is still key

World generic API manufacturer landscape

15Source: TS Research

Experience in

supplying regulated

markets

US DMF Filings by Indian, Chinese and Rest of World API Manufacturers: 1998 – 2008

Source: Newport Premium™

Number of US FDA Inspections : 2001 – 2009*

Source: Newport Premium™; * = data as of 9/28/09

Of the ~340 experienced manufacturers…

• Half are vertically integrated into finished dose

• 50 have a presence in the US generic market

• 60% are headquartered in the US, India, China or Italy

18Source: TS Research

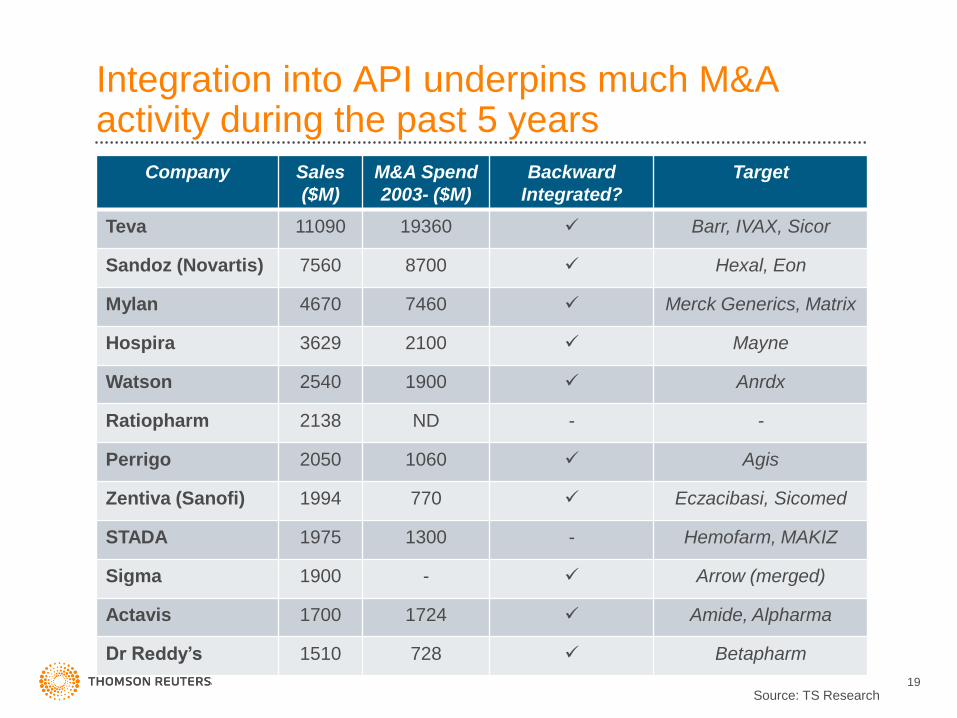

Integration into API underpins much M&A activity during the past 5 years

Company Sales

($M)

M&A Spend

2003- ($M)

Backward

Integrated?

Target

Teva 11090 19360 Barr, IVAX, Sicor

Sandoz (Novartis) 7560 8700 Hexal, Eon

Mylan 4670 7460 Merck Generics, Matrix

Hospira 3629 2100 Mayne

Watson 2540 1900 Anrdx

Ratiopharm 2138 ND - -

Perrigo 2050 1060 Agis

Zentiva (Sanofi) 1994 770 Eczacibasi, Sicomed

STADA 1975 1300 - Hemofarm, MAKIZ

Sigma 1900 - Arrow (merged)

Actavis 1700 1724 Amide, Alpharma

Dr Reddy’s 1510 728 Betapharm

19Source: TS Research

The Generic Development Process

20

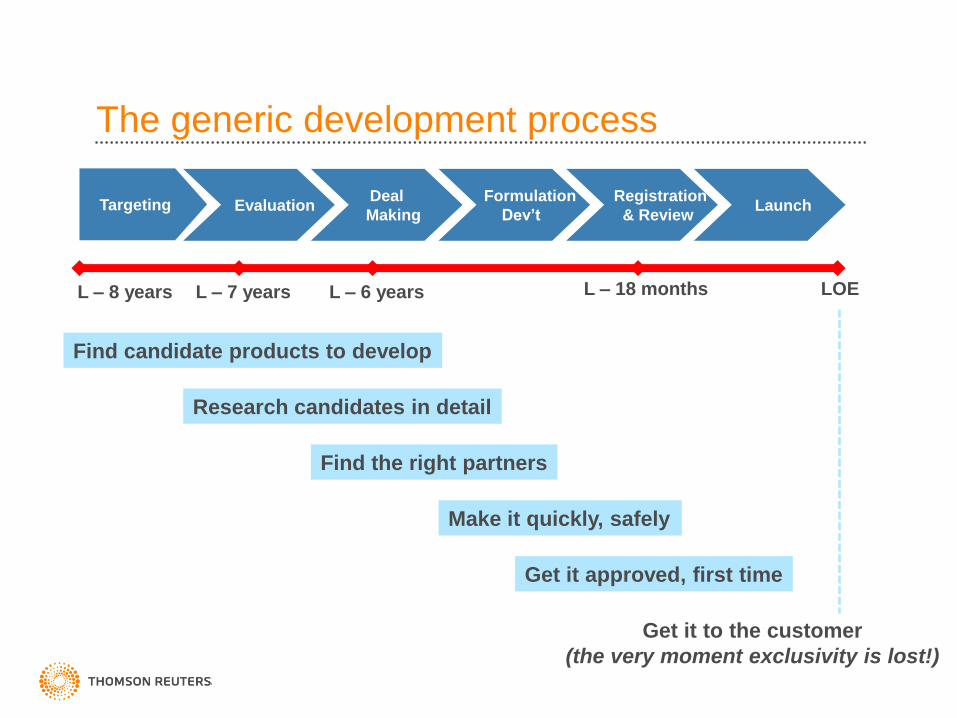

The generic development process

Targeting EvaluationDeal

Making

Formulation

Dev’t

Registration

& ReviewLaunch

Find candidate products to develop

Research candidates in detail

Find the right partners

Make it quickly, safely

Get it approved, first time

Get it to the customer

(the very moment exclusivity is lost!)

LOEL – 18 monthsL – 8 years L – 7 years L – 6 years

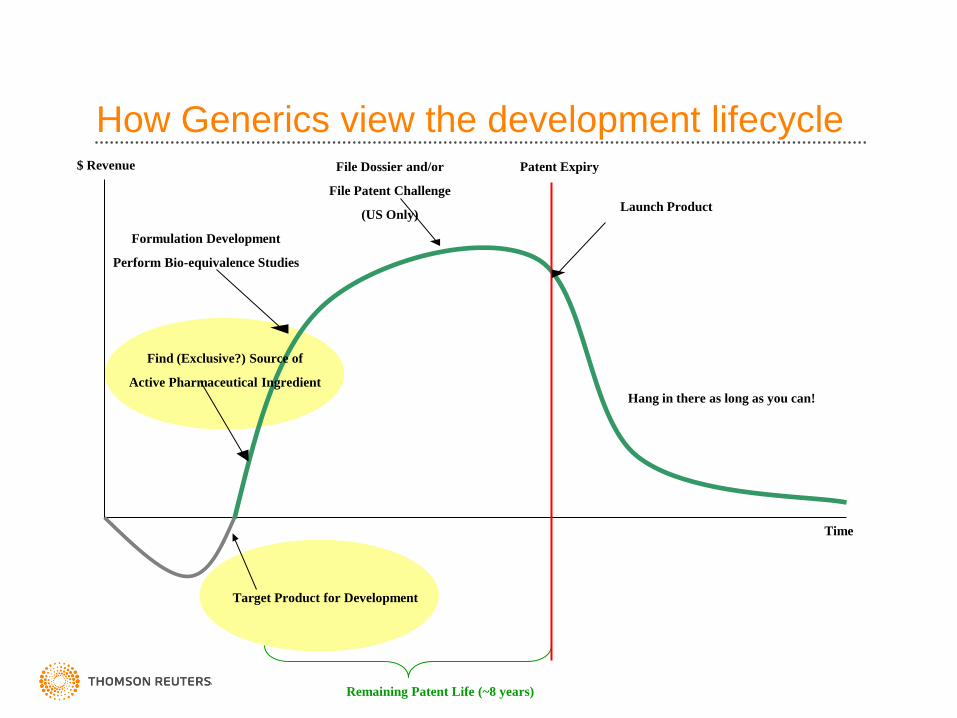

How Generics view the development lifecycle

Target Product for Development

$ Revenue

Remaining Patent Life (~8 years)

Time

Patent Expiry

Find (Exclusive?) Source of

Active Pharmaceutical Ingredient

Formulation Development

Perform Bio-equivalence Studies

File Dossier and/or

File Patent Challenge

(US Only)Launch Product

Hang in there as long as you can!

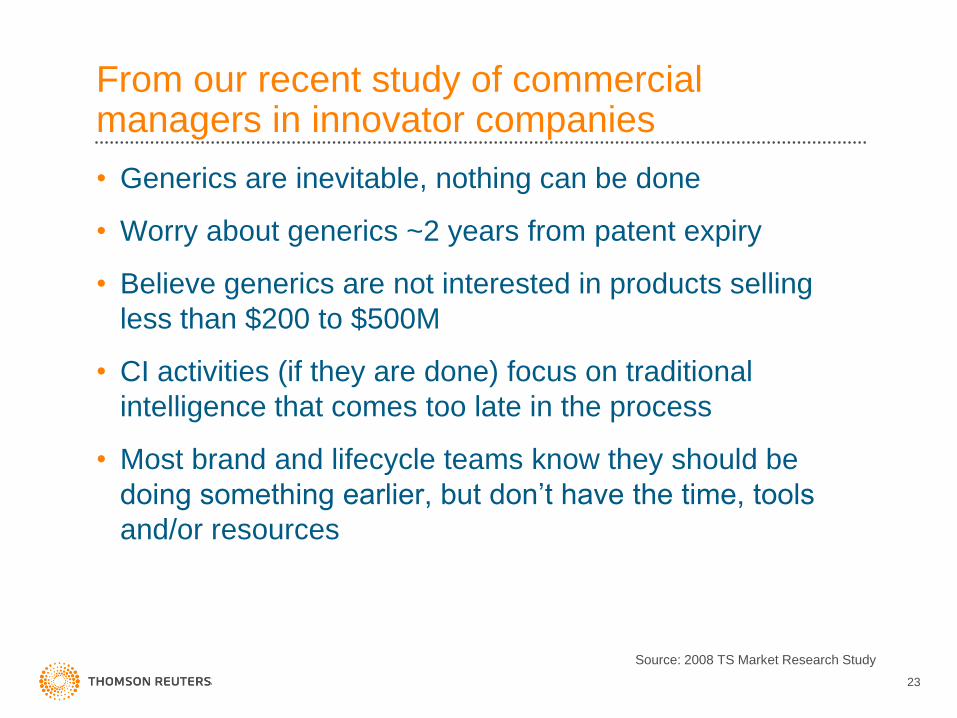

From our recent study of commercial managers in innovator companies

• Generics are inevitable, nothing can be done

• Worry about generics ~2 years from patent expiry

• Believe generics are not interested in products selling

less than $200 to $500M

• CI activities (if they are done) focus on traditional

intelligence that comes too late in the process

• Most brand and lifecycle teams know they should be

doing something earlier, but don’t have the time, tools

and/or resources

23

Source: 2008 TS Market Research Study

Innovator’s view of the development lifecycle?

Product promotion

Product Improvement

Phase IV Studies

$ Revenue

Patent Life (20 Years)

Time

Patent Expiry

End of life

Launch

Start worrying

about generics?

Why API Intelligence?

• Generics often start targeting products 8 to 10 years before

patent expiry

– Many start targeting well before commercial launch by

innovators

• API always comes before the finished product (dose form)

– Without API, there can be no generic

– API often precedes dose development by 3+ years

• API has to be available in sufficient quantities and with

sufficient quality for regulated market needs

• The number, capabilities and track record of API

manufacturers is highly indicative of future (FD) competition

• Works for all types of product (traditional or biological)

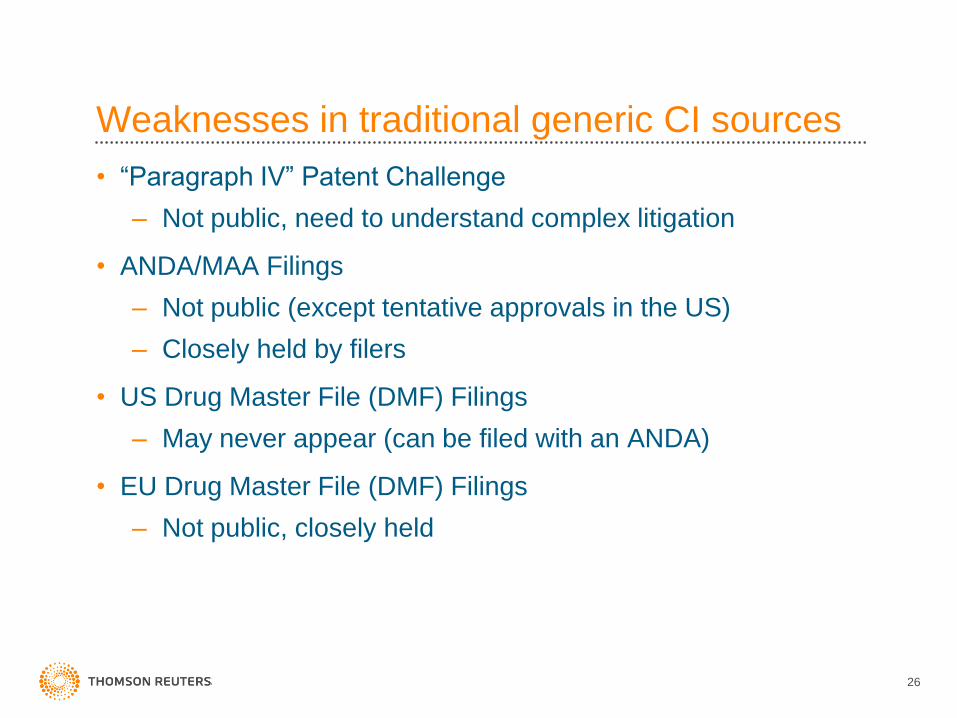

Weaknesses in traditional generic CI sources

• “Paragraph IV” Patent Challenge

– Not public, need to understand complex litigation

• ANDA/MAA Filings

– Not public (except tentative approvals in the US)

– Closely held by filers

• US Drug Master File (DMF) Filings

– May never appear (can be filed with an ANDA)

• EU Drug Master File (DMF) Filings

– Not public, closely held

26

About Thomson Reuters API Intelligence

• Founded in 1990 as Newport Strategies

• Part of Thomson Reuters Scientific since 2004

• A team of research analysts devoted to collecting, validating,

and analyzing information about API manufacturing

• Unique primary research using an extensive global network of

industry experts

• Team based in Portland, Maine, USA

Our research process

• Many daily conversations with manufacturers, agents,

traders, consultants and experts worldwide to determine

– Which company?

– Is making what active ingredient?

– At which factory?

– What stage of development have they reached?

• Validation requires multiple confirmations (independent of the

original source)

• Historical accuracy and reliability of each source tracked

• Researchers therapeutically aligned

• All work conducted according to a strict confidentiality

protocol

Case Example: ABILIFY® (aripiprazole)

29

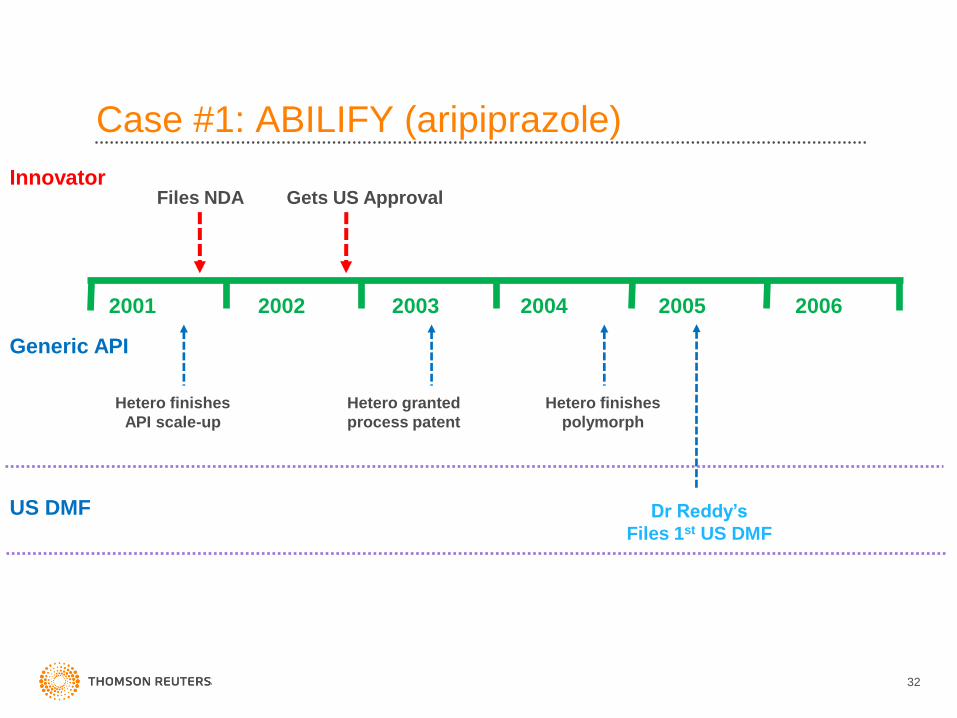

Case #1: ABILIFY (aripiprazole)

200620052004200320022001

Files NDA Gets US ApprovalInnovator

Case #1: ABILIFY (aripiprazole)

31

Hetero finishes

API scale-up

Hetero granted

process patent

Hetero finishes

polymorph

Files NDA Gets US ApprovalInnovator

Generic API

At least 10 other

manufacturers ready

200620052004200320022001

Case #1: ABILIFY (aripiprazole)

32

Hetero finishes

API scale-up

Hetero granted

process patent

Hetero finishes

polymorph

Dr Reddy’s

Files 1st US DMF

Files NDA Gets US ApprovalInnovator

Generic API

US DMF

200620052004200320022001

Case #1: ABILIFY (aripiprazole)

33

Hetero finishes

API scale-up

Hetero granted

process patent

Hetero finishes

polymorph

Dr Reddy’s

Files 1st US DMF

Files NDA Gets US ApprovalInnovator

Generic API

US DMF

200620052004200320022001

Patent Challenge Patent

Challenges

(at least 6)

At least 10 other

manufacturers ready

Case #1: ABILIFY (aripiprazole)

34

Hetero finishes

API scale-up

Hetero granted

process patent

Hetero finishes

polymorph

Dr Reddy’s

Files 1st US DMF

Files NDA Gets US ApprovalInnovator

Generic API

US DMF

200620052004200320022001

Patent Challenge Patent

Challenges

(at least 6)

Begins Litigation

(7 cases)

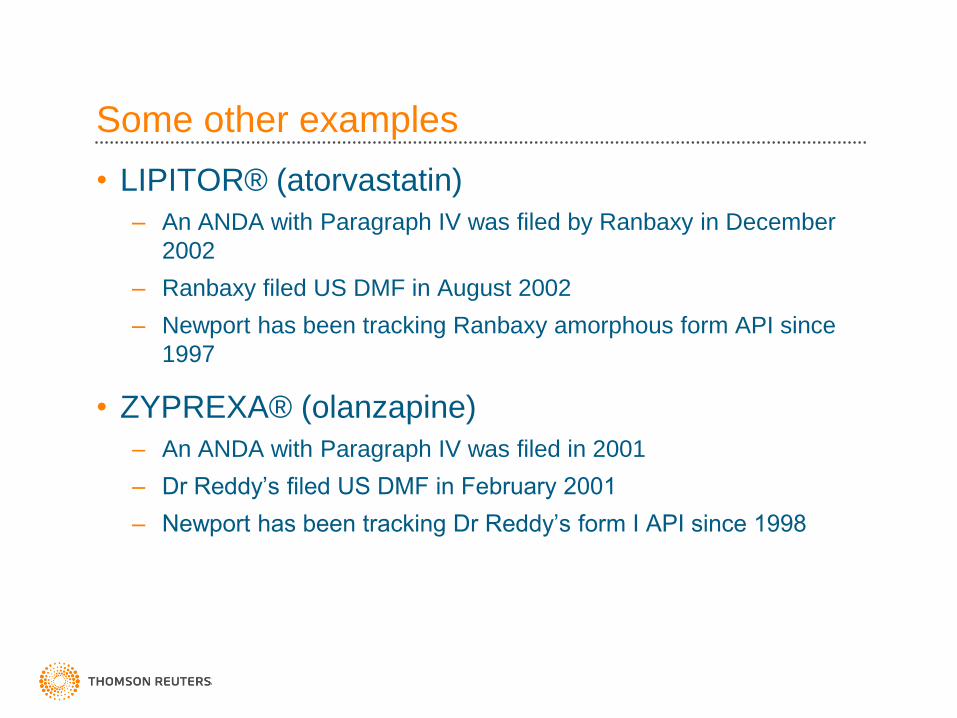

Some other examples

• LIPITOR® (atorvastatin)

– An ANDA with Paragraph IV was filed by Ranbaxy in December

2002

– Ranbaxy filed US DMF in August 2002

– Newport has been tracking Ranbaxy amorphous form API since

1997

• ZYPREXA® (olanzapine)

– An ANDA with Paragraph IV was filed in 2001

– Dr Reddy’s filed US DMF in February 2001

– Newport has been tracking Dr Reddy’s form I API since 1998

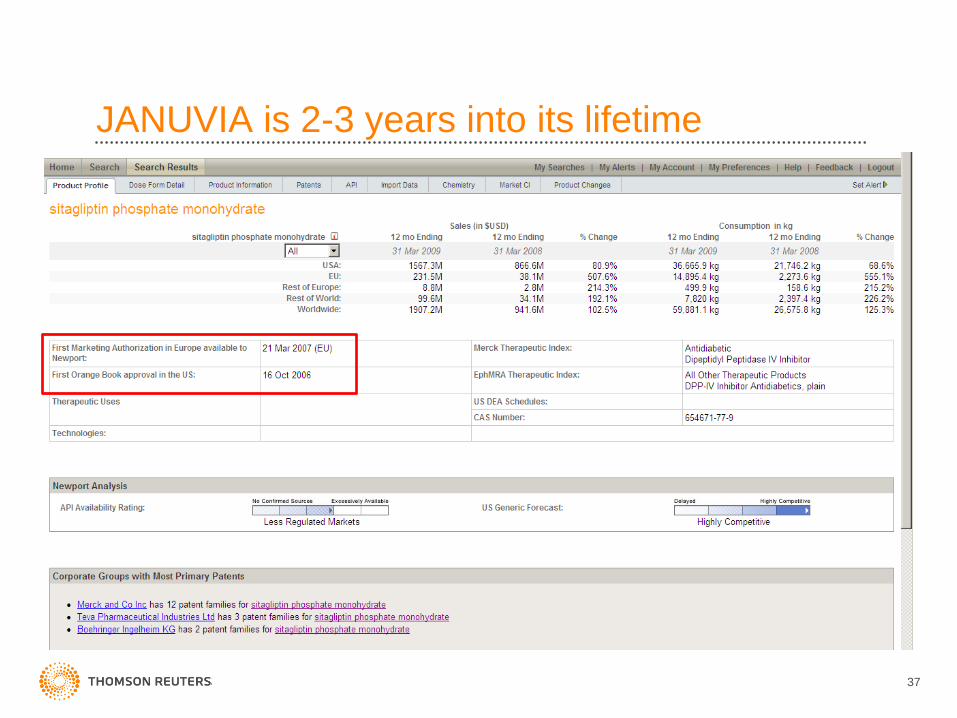

Looking at Merck’s JANUVIA™

JANUVIA is 2-3 years into its lifetime

37

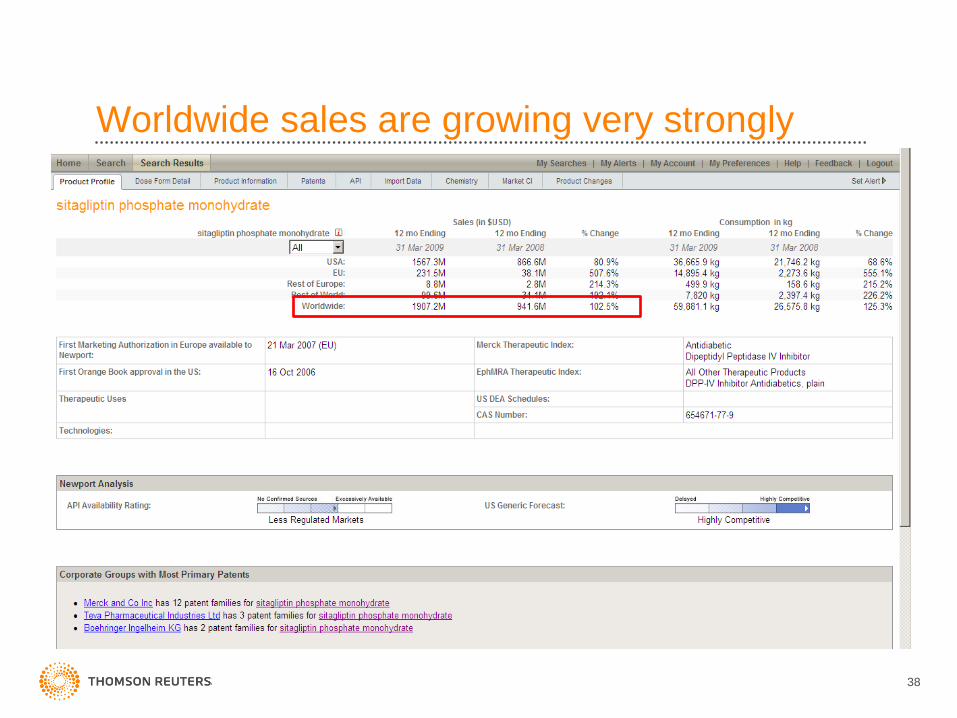

Worldwide sales are growing very strongly

38

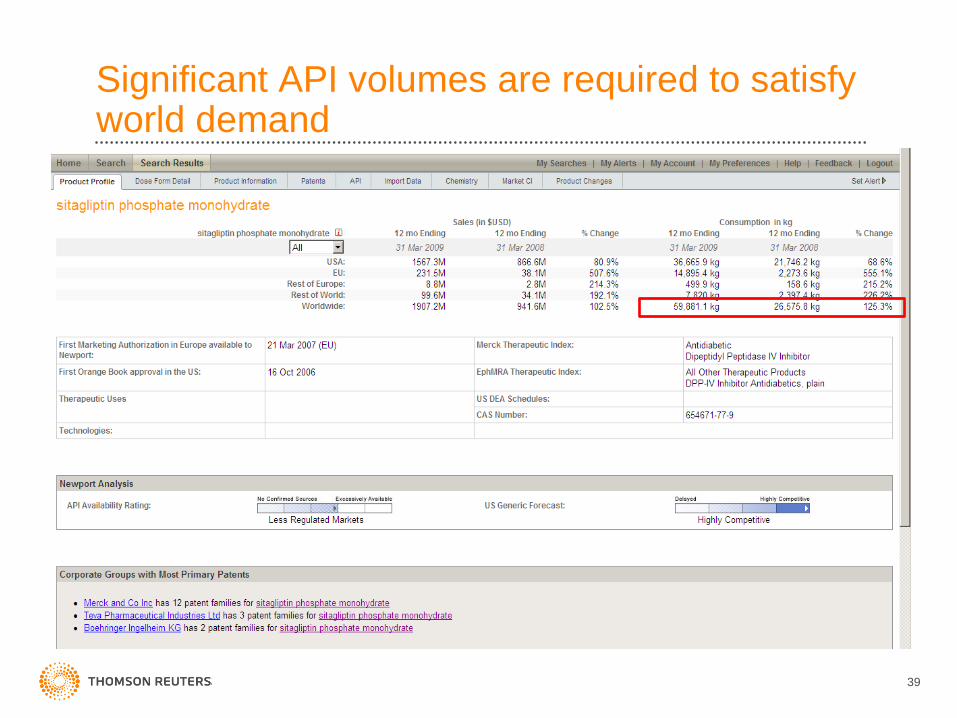

Significant API volumes are required to satisfy world demand

39

We already see significant generic API activity

40

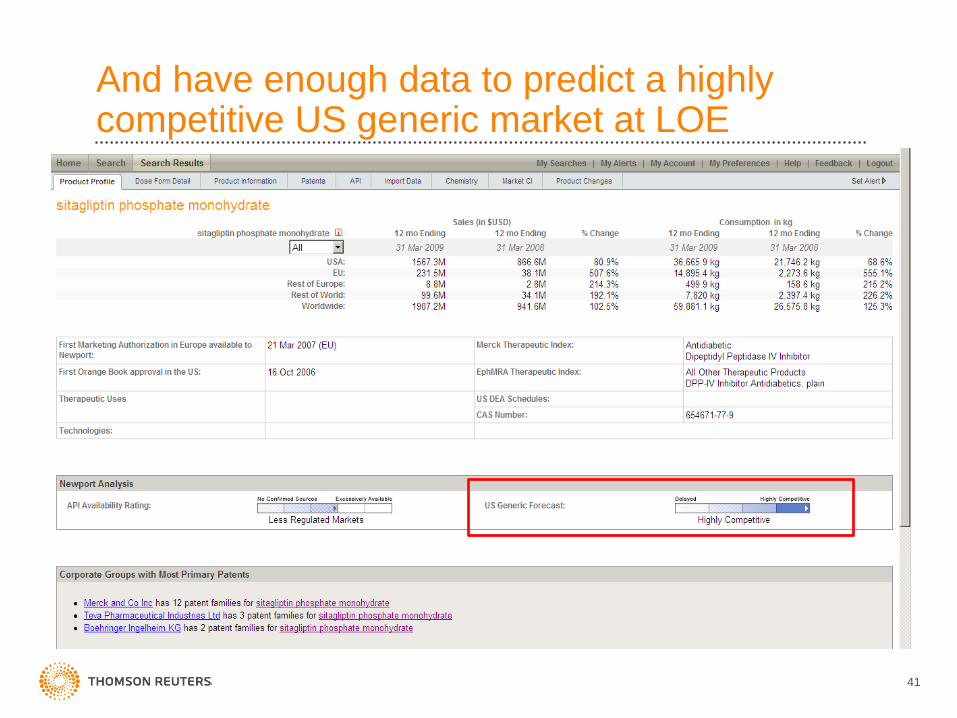

And have enough data to predict a highly competitive US generic market at LOE

41

JANUVIA is currently protected by an NCE exclusivity in the US

42

There is the possibility of patent challenges in October 2010 but we estimate LOE in 2022

43

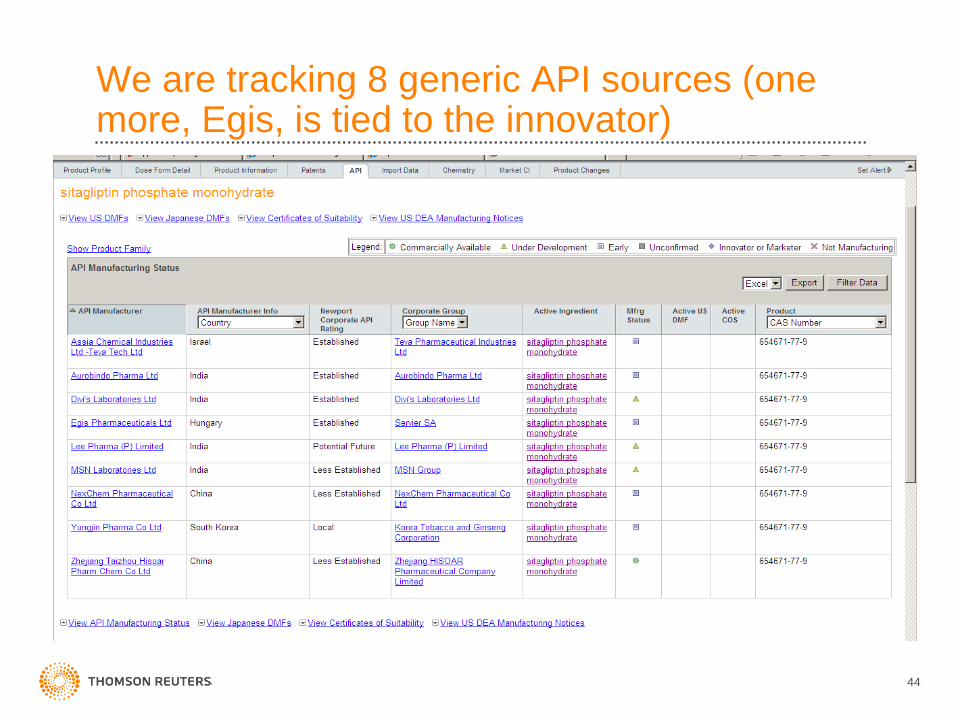

We are tracking 8 generic API sources (one more, Egis, is tied to the innovator)

44

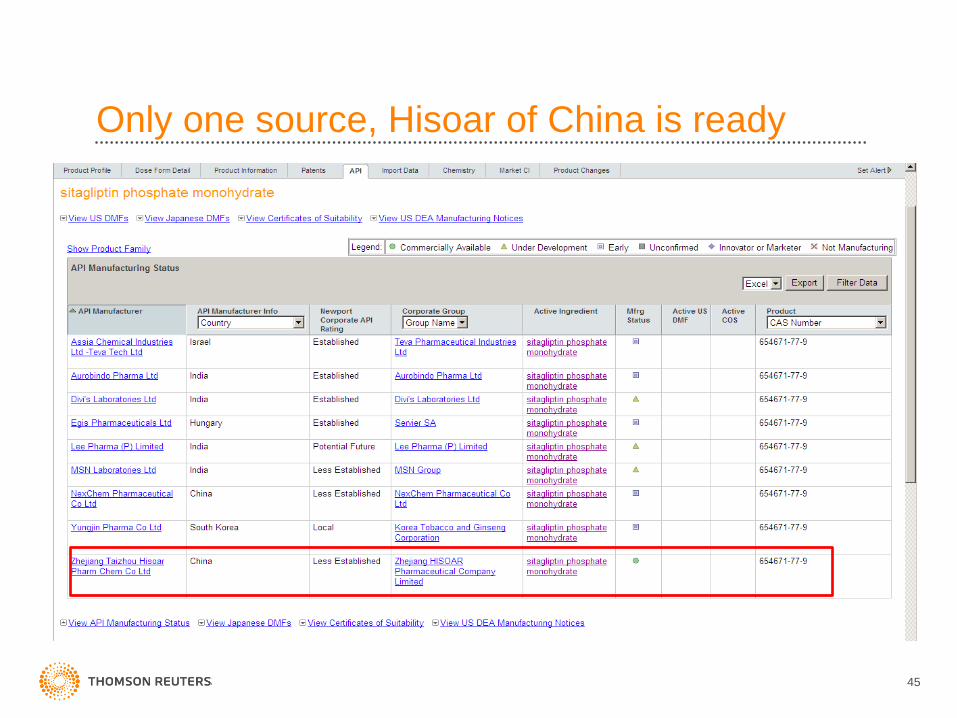

Only one source, Hisoar of China is ready

45

Hisoar is rated Less Established, making them a likely viable source for regulated markets

46

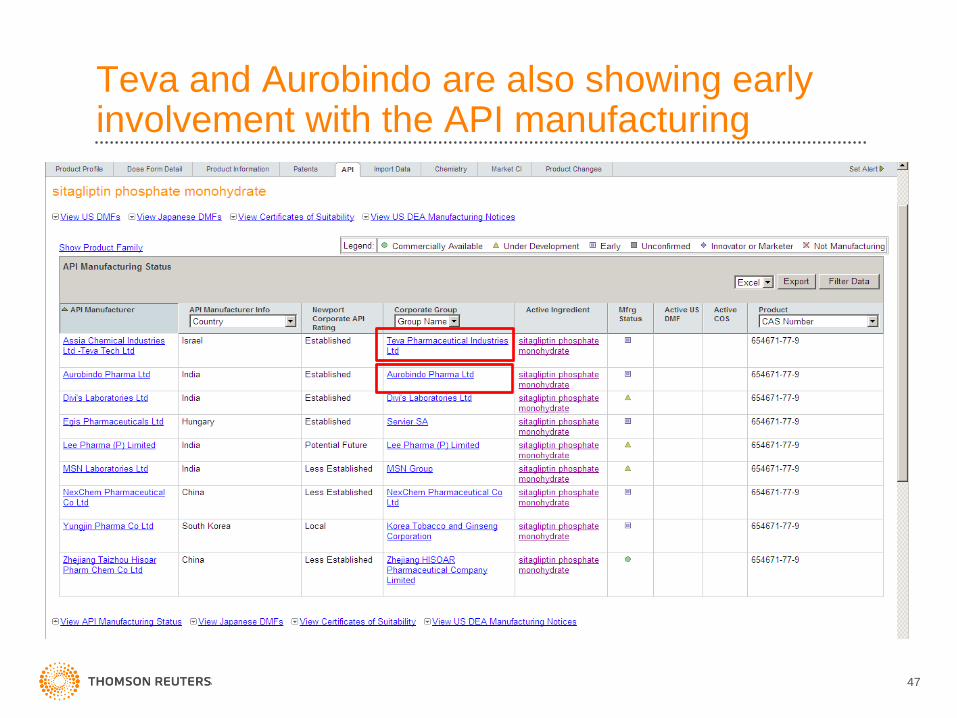

Teva and Aurobindo are also showing early involvement with the API manufacturing

47

There are no DMF or COS filings yet

48

Both Teva and Aurobindo are both vertically integrated, with histories of Paragraph IV activity

49

Earliest generic activity was picked up in mid-2008

50

Thank You!

David Harding

Newport Product Specialist

Thomson Reuters Healthcare & Science

+1 207 871 9700 x27

www.thomsonreuters.com/business_units/scientific/pharma/generics

COME VISIT US AT CPHI WORLDWIDE BOOTH 6F38