How Asia-Pacific States can secure Competitive Advantage ... · PDF fileE-mail: [email protected]...

23

Contact: Mr. Robert David Borthwick Axiata Group Berhad Tel: +603 2263 8979 Fax: +603 2263 8980 E-mail: [email protected] ASIA-PACIFIC TELECOMMUNITY 12 th APT Policy and Regulatory Forum Document: PRF-12/INP-18(R1) 21-23 May, 2012 – Bangkok, Thailand 21 May 2012 How Asia-Pacific States can secure Competitive Advantage through Regulating for New and Emerging Communications Developments Prepared by Mr. Robert David Borthwick

Transcript of How Asia-Pacific States can secure Competitive Advantage ... · PDF fileE-mail: [email protected]...

Contact: Mr. Robert David Borthwick

Axiata Group Berhad

Tel: +603 2263 8979

Fax: +603 2263 8980

E-mail: [email protected]

ASIA-PACIFIC TELECOMMUNITY

12th

APT Policy and Regulatory Forum

Document:

PRF-12/INP-18(R1)

21-23 May, 2012 – Bangkok, Thailand 21 May 2012

How Asia-Pacific States can secure Competitive Advantage through

Regulating for New and Emerging Communications Developments

Prepared by

Mr. Robert David Borthwick

How Asia-Pacific States can secure Competitive Advantage through Regulating for New and Emerging Communications Developments Axiata

21 May 2012

Rob Borthwick

Vice President, Group Regulatory Affairs, Axiata Group Berhad

company confidential

2 company confidential

2

Agenda

1. About Axiata

2. Current background – Macro Economic and Sector Prospects

3. Long Term View – Opportunities for Sustainable Growth and Increasing Prosperity

4. Enabling Regulatory Environment for New and Emerging Communications Developments

Axiata Group Regulatory / APT PRF May 2012 3

About Axiata: Owned and based in Asia.

Investing in communications networks and services regionally.

Idea, India

Ownership: 19.1%

Market position: #3

Re-branded and

expanded TMI

Regional Reach in South

and South East Asia

Portfolio of Developed

and Emerging Market

Assets

More than 180 million

Mobile Subscribers

With the broader purpose

of Advancing Asia

Dialog, Sri Lanka

Ownership: 85.0%

Market position: #1

XL, Indonesia

Ownership: 66.7%

Market position: #3

Hello, Cambodia

Ownership: 100.0%

Market position: #5

M1, Singapore

Ownership: 29.4%

Market position: #3

Celcom, Malaysia

Ownership: 100.0%

Market position: #2

Robi, Bangladesh

Ownership: 70.0%

Market position: #3

4 company confidential

4

Agenda

1. About Axiata

2. Current background – Macroeconomic and Sector Prospects

3. Long Term View – Opportunities for Sustainable Growth and Increasing Prosperity

4. Enabling Regulatory Environment for New and Emerging Communications Developments

Axiata Group Regulatory / APT PRF May 2012 5

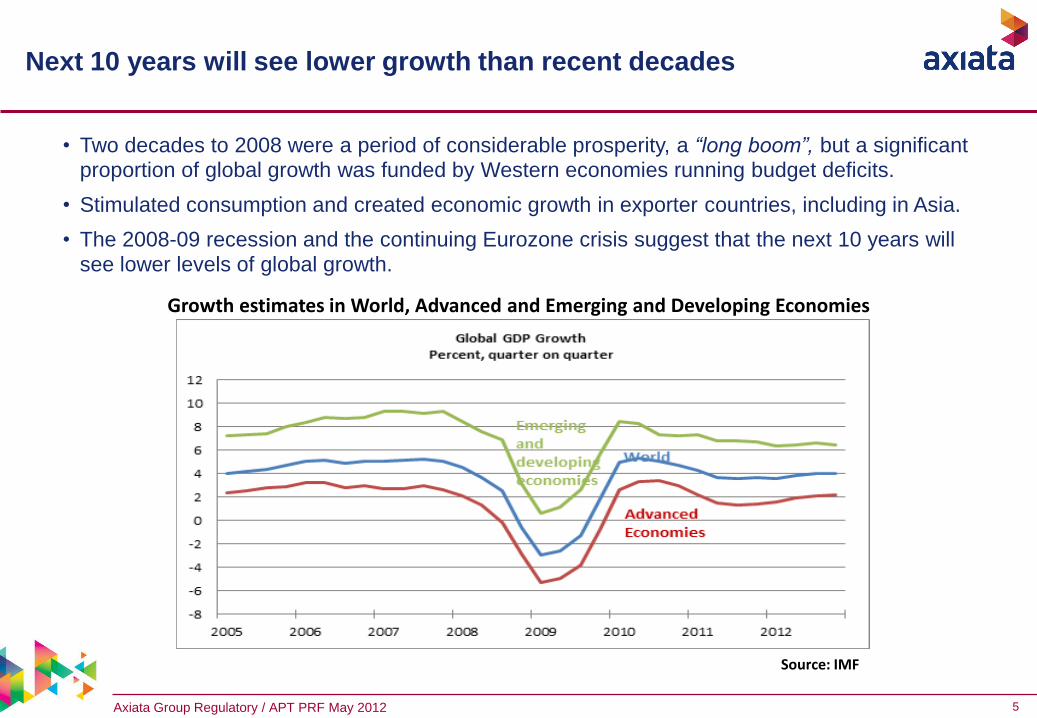

Next 10 years will see lower growth than recent decades

• Two decades to 2008 were a period of considerable prosperity, a “long boom”, but a significant proportion of global growth was funded by Western economies running budget deficits.

• Stimulated consumption and created economic growth in exporter countries, including in Asia.

• The 2008-09 recession and the continuing Eurozone crisis suggest that the next 10 years will

see lower levels of global growth.

Growth estimates in World, Advanced and Emerging and Developing Economies

Source: IMF

Axiata Group Regulatory / APT PRF May 2012 6

Core macroeconomic forecasts presume current Eurozone crisis is

progressively resolved.

• Most likely scenario for SE and South Asia is modestly slower economic growth during 2012-2017.

Asian countries will continue to grow, but at some 2-3% p.a. lower levels than during the period

before 2008-09. If other World regions stabilize, then higher growth may resume.

• But whether this happens is far from certain and it is more useful to consider different scenarios:

1. Stronger economic growth returns during 2013-14. From 2015-2017 growth returns to “long

boom” levels. How lucky do we feel? Not very < 10%

2. Lower economic growth during 2012-2017. Asian countries continue to grow, but at 2-3% p.a.

lower than prior to 2008-09. Most likely 50 to 60%

3. Major EU-led global economic downturn costs 2-3%p.a. more growth during 2012-2017.

Becoming more likely 30 to 40%

• Even in previously high-performing nations of SE and South Asia there is a significant risk of low

growth or even recession as a consequence of international economic failure.

• In particular, if there are significant national departures from the Eurozone, beyond the likely imminent

departure of Greece, and if these are “disorderly”, expect a global downturn.

Axiata Group Regulatory / APT PRF May 2012 7

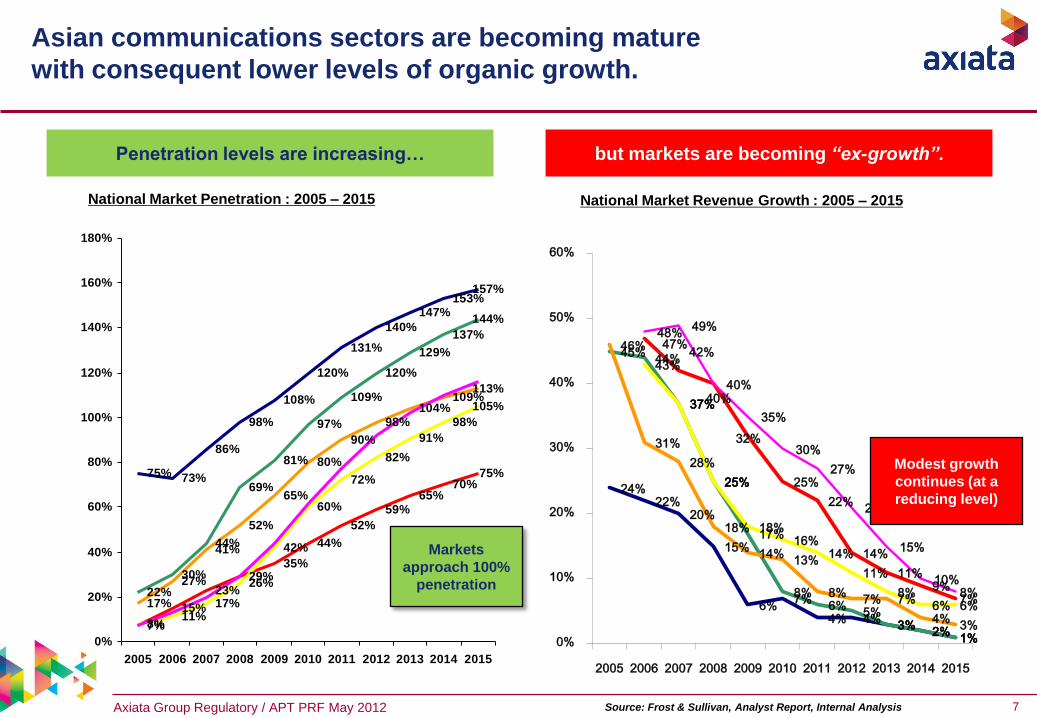

Asian communications sectors are becoming mature

with consequent lower levels of organic growth.

but markets are becoming “ex-growth”. Penetration levels are increasing…

National Market Penetration : 2005 – 2015 National Market Revenue Growth : 2005 – 2015

Source: Frost & Sullivan, Analyst Report, Internal Analysis

75% 73%

86%

98%

108%

120%

131%

140%

147%153%

157%

22%

30%

44%

69%

81%

97%

109%

120%

129%

137%

144%

17%

27%

41%

52%

65%

80%

90%

98%104%

109%113%

7%

15%

23%29%

35%

44%

52%

59%65%

70%75%

8%11%

17%

26%

42%

60%

72%

82%

91%

98%

105%

0%

20%

40%

60%

80%

100%

120%

140%

160%

180%

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

24% 22%

20%

15%

6% 7%

4% 4% 3% 2% 1%

45% 44%

37%

25%

17%

8% 6% 5%

3% 2% 1%

46%

31%

28%

18%

14% 13%

8% 7% 7%

4% 3%

47% 42%

40%

32%

25%

22%

14%

11% 9%

7%

43%

37%

25%

18% 16%

14%

11%

8% 6% 6%

48% 49%

40%

35%

30%

27%

21%

15%

10% 8%

0%

10%

20%

30%

40%

50%

60%

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Markets

approach 100%

penetration

Modest growth

continues (at a

reducing level)

Axiata Group Regulatory / APT PRF May 2012 8

Against this background communications providers

face the need to address new competitive dimensions. …

1995 2000 2010

Voice coverage

(quality)

VAS content

(product range)

Broadband

(video speed)

?

• Enterprise

Applications

• Advertising

• Information

brokering

• Transactions/

Payments

• M2M

• OTT plays

2005

Voice is key Voice is commodity.

Data is key Data is commodity. Content

and applications are key.

Data will become ubiquitous, competition will be more heterogeneous

including and beyond regulated communications services sector.

Voice and SMS

(price)

2015+

Axiata Group Regulatory / APT PRF May 2012 9

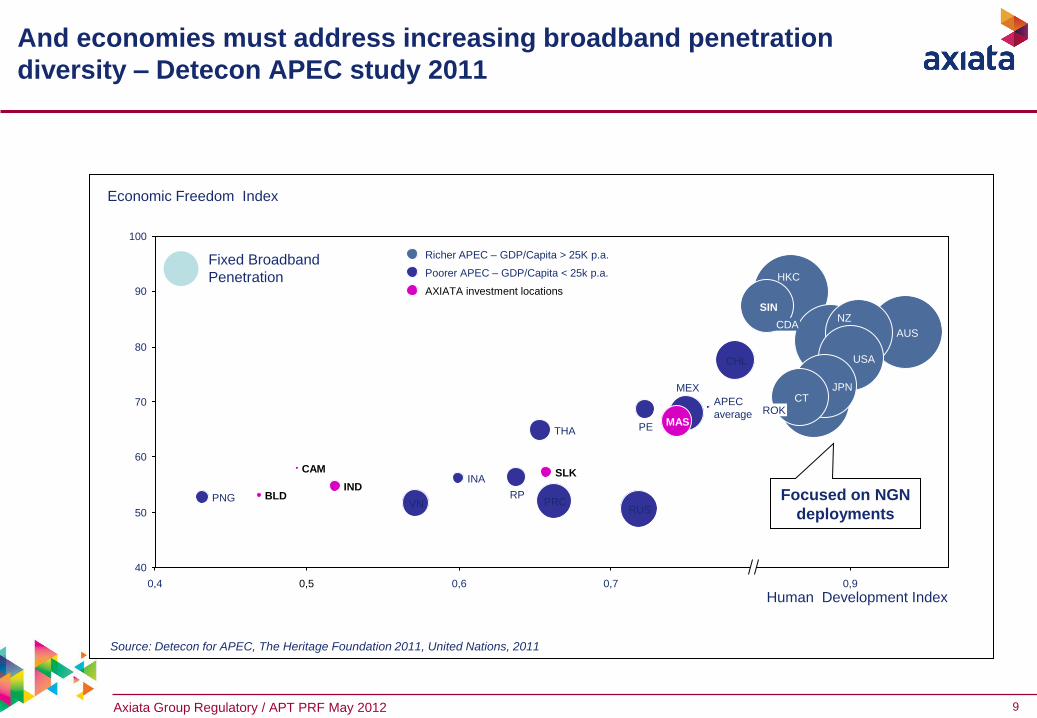

And economies must address increasing broadband penetration

diversity – Detecon APEC study 2011

100

90

60

50

40

0,9 0,7 0,6 0,5 0,4

80

70

CAM

BLD IND

SLK

APEC

average

VN

CT

USA

THA

SIN

RUS

RP

ROK

PRC PNG

PE

NZ

MEX

MAS

JPN

INA

HKC

CHL

AUS CDA

Human Development Index

Economic Freedom Index

Fixed Broadband

Penetration

Source: Detecon for APEC, The Heritage Foundation 2011, United Nations, 2011

Focused on NGN

deployments

Richer APEC – GDP/Capita > 25K p.a.

AXIATA investment locations

Poorer APEC – GDP/Capita < 25k p.a.

10 company confidential

10

Agenda

1. About Axiata

2. Current background – Macroeconomic and Sector Prospects

3. Long Term View – Opportunities for Sustainable Growth and Increasing Prosperity

4. Enabling Regulatory Environment for New and Emerging Communications Developments

Axiata Group Regulatory / APT PRF May 2012 11

Sustainable growth and increasing prosperity in Asia-Pacific

More-constrained communications market: 2010 – 2020

Critical success factors: Which will provide:

A. Sustaining effective competition

B. Access to substantially increased spectrum

resources with different characteristics

C. Consistent, open technologically-neutral

regulatory approach to networks and

services

D. Overall financial relationship between sector

and national economy.

Appropriate market incentives

Data ubiquity with high capacity at low cost

Right level of regulation of different activities which is

“investment-grade” and enables new technology

Public position is the basis for investment decisions by

private actors.

Expanding communications market: 1990 – 2010

Critical success factors: Which provided:

A. Liberalization / introduction of competition

B. Provision of resources to allow competition

to be effective (spectrum, ability to build

networks)

C. Complemented by global mobile technology

development.

New entry and appropriate market incentives

Raw material for the growing industry

Dynamic efficiency which has substantially reduced

costs, increased customer numbers and service range.

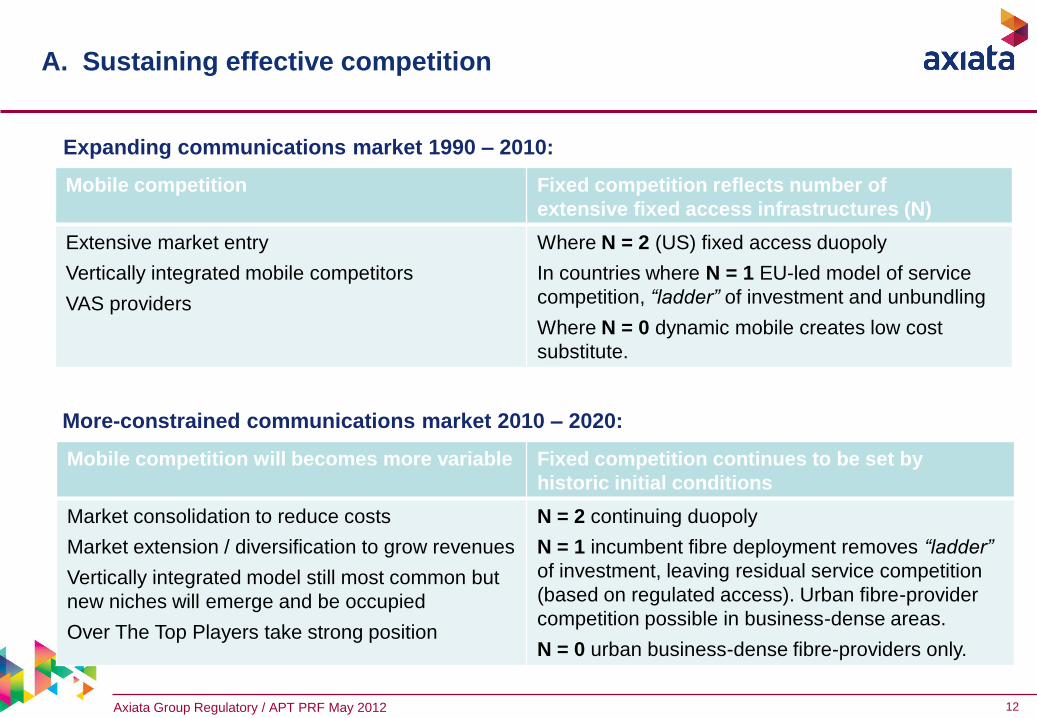

Axiata Group Regulatory / APT PRF May 2012 12

A. Sustaining effective competition

More-constrained communications market 2010 – 2020:

Expanding communications market 1990 – 2010:

Mobile competition Fixed competition reflects number of

extensive fixed access infrastructures (N)

Extensive market entry

Vertically integrated mobile competitors

VAS providers

Where N = 2 (US) fixed access duopoly

In countries where N = 1 EU-led model of service

competition, “ladder” of investment and unbundling

Where N = 0 dynamic mobile creates low cost

substitute.

Mobile competition will becomes more variable Fixed competition continues to be set by

historic initial conditions

Market consolidation to reduce costs

Market extension / diversification to grow revenues

Vertically integrated model still most common but

new niches will emerge and be occupied

Over The Top Players take strong position

N = 2 continuing duopoly

N = 1 incumbent fibre deployment removes “ladder”

of investment, leaving residual service competition

(based on regulated access). Urban fibre-provider

competition possible in business-dense areas.

N = 0 urban business-dense fibre-providers only.

Axiata Group Regulatory / APT PRF May 2012 13

B. Access to substantially increased spectrum resources

with different characteristics

Source: APEC broadband survey, Detecon analysis, data not available for fields with “-”

APEC economies

Spectrum

liberalization

tech. neutral

Spectrum

refarming

framework

Status

4G license

Status

Digital

dividend

Ratio mobile to

fixed line

subscriptions

mobile BB

penetration /

100 inhabitants

Canada - - - - 1.4 :1 33.7

Chinese Taipei planned planned completed planned 1.8 :1 57.0

Republic of Korea - - completed planned 1.9 :1 84.2

United States yes yes completed completed 2.0 : 1 53.8

China - - - - 2.4 : 1 2.0

New Zealand yes yes completed planned 2.5 : 1 47.1

Australia - yes planned planned 2.7 : 1 88.8

Japan - - completed planned 2.7 : 1 88.1

Hong Kong, China yes yes completed not started 2.9 : 1 66.8

Singapore yes - planned - 3.6 : 1 92.7

Mexico - - - - 4.3 : 1 9.0

Chile - - - - 4.6 : 1 7.3

Indonesia - - - - 4.7 : 1 9.6

Brunei Darussalam - - - - 5.1 : 1 55.2

Russia - - - - 5.1 : 1 9.5

Viet Nam yes yes not started planned 5.6 : 1 6.0

Malaysia yes yes planned planned 7.0 : 1 31.4

Peru yes planned planned planned 8.3 : 1 2.0

Thailand yes planned - planned 9.2 : 1 1.4

Philippines - - - - 13.6 : 1 13.5

Papua New Guinea - - - - 15.0 : 1 0.0

The four major levers of effective spectrum

management are spectrum availability,

spectrum assignment, license conditions and

spectrum liberalization and refarming.

Right set of license conditions are

imperative to increase geographic coverage

e.g. first coverage of all white spots, then

move to urban deployment

The digital dividend will have a massive

effect on rapidly increasing broadband

penetration and coverage in emerging

economies. So far, only the US has released

the digital dividend spectrum

Poorer APEC economies can benefit

most from spectrum liberalization and

refarming to promote mobile broadband

deployment.

Spectrum liberalization important to

accommodate for converging markets

Axiata Group Regulatory / APT PRF May 2012 14

But this potentially indicates an area of competitive concern

Expect competitive advantage to accrue to regions which maximize creation of

harmonized broadband spectrum and countries which use created spectrum efficiently

While Asia–Pacific is not homogeneous, competitor regions’ may be able to complement more

widely deployed fixed infrastructure with production of larger amounts of harmonized

spectrum – increasing their aggregate data capacity advantage at low cost.

Region Rhetoric Structure Recent examples

US “digital infrastructure will be a key source of competitive

advantage in the knowledge economy. There is no

policy more important for digital infrastructure than

assuring that scarce spectrum is efficiently allocated.”

- Larry Summers, June 28, 2010

FCC

Rules allowing single channel

sharing by broadcasters.

Proposed FCC auction 1755 –

1780 MHz band for commercial

wireless services.

EU “intelligent and coherent use of radio spectrum will be

the backbone of an Internet explosion […] Get it wrong

and it will be a bottleneck, which will hold back

development of the sector, undermine potential job

creation, and mean we risk losing our competitive edge”

- Neelie Kroes, 14th June 2011

EC Radio-

Spectrum

Policy

Committee

RSPG argues the case for new

broadband in 700 MHz is

"irresistible". Will table second

digital dividend proposal at

European RSPG June meeting.

15 company confidential

15

Agenda

1. About Axiata

2. Current background – Macroeconomic and Sector Prospects

3. Long Term View – Opportunities for Sustainable Growth and Increasing Prosperity

4. Enabling Regulatory Environment for New and Emerging Communications Developments

Axiata Group Regulatory / APT PRF May 2012 16

C. Consistent, open regulatory approach to communications

Communications license

• Single, simple set of rules for commercial operation of communications networks and services

• Without service or technology distinctions

• Communications providers determine level and boundary of their operations on a commercial basis.

Spectrum permission

• Simple description of spectrum which is being made available to a provider

• Or which is unlicensed

• With terms which deal only with spectrum-related issues, e.g. period of allocation, payment terms, management of interference.

• Again without service or technology distinctions

VAS provider code

• A code which is managed by the NRA / Value Added Services-(VAS) regulator

• With terms which deals only with VAS provision: consumer protection, transparency, pricing etc.

• VAS providers must register and be in good standing to offer services and to contract with communications licensees.

National legislation dealing consistently with horizontal concerns: customer

identification, privacy, unsolicited communications etc.

Axiata Group Regulatory / APT PRF May 2012 17

D. Financial flows between sector and economy – a key, if largely

unacknowledged, producer of future “digital divides”

General tax load on

communications is

low / reflective of

other sectors

General tax load on

communications is

medium / somewhat

above other sectors

General tax load on

communications is

high / substantially

above other sectors

Spectrum is

allocated

administratively.

Some APT countries

here

Spectrum is

allocated through

objective market-

based process.

EU

US

Australia / NZ

Some APT member

countries here

Spectrum is

allocated through

market-based

process but with

high reserve

prices.

Some APT member

countries here

Axiata Group Regulatory / APT PRF May 2012 18

Bridging the Digital Divide

APEC Member Governments think that Universal Service provision and national PPPs

are among the top measures for promoting rural broadband.

6.0

6.0

Universal Access

and Service Fund

4.0 3.0 2.5 3.5

Regional PPPs 3.3

Mobile regulatory

intervention (e.g. licensing) 4.0

Fixed regulatory

intervention (e.g. ULL, BSA) 4.0

National PPPs 5.1

Universal Service

Obligation 5.8

financial intervention

(e.g. tax incentives) 2.7

4.5 5.5 5.0

average ranking (1=min; 6=max) Detecon for APEC from: CT, HKC, MAS, NZ, PE, TH, VN

Question: “Please rank the following measures according to their importance for promoting rural

broadband access”

Axiata Group Regulatory / APT PRF May 2012 19

Historic performance depends on Critical Success Factors

Universal Access Service Fund performance has been marginal

57

74 73

86

98

108

120

129

17 17 17 17 16 16 15 15

5 7

13

20

30

45

63

75

4 4 4 3 3 3 3 3 0

20

40

60

80

100

120

140

2004 2005 2006 2007 2008 2009 2010 2011

Country A - mobile Country A - fixed

Country B - mobile Country B - fixed

57

74 73

86

98

108

120

129

5 7

13

20

30

45

63

75

0 0 0 0.3 0.5 0.7 0.98 1.3 0

20

40

60

80

100

120

140

2004 2005 2006 2007 2008 2009 2010 2011

Country A Country B Country C

What constrains UAS performance? i/ Tax-led vs. Objective-led; ii/ institutional factors

favour state-owned operators; iii/ communal solutions vulnerable to market provision.

20

Thank You Rob Borthwick

VP, Group Regulatory Affairs, Axiata Group Berhad

Email: [email protected]

Mobile: +60 19 382 2003

www.axiata.com

Axiata Group Berhad

20

Axiata Group Regulatory / APT PRF May 2012 21

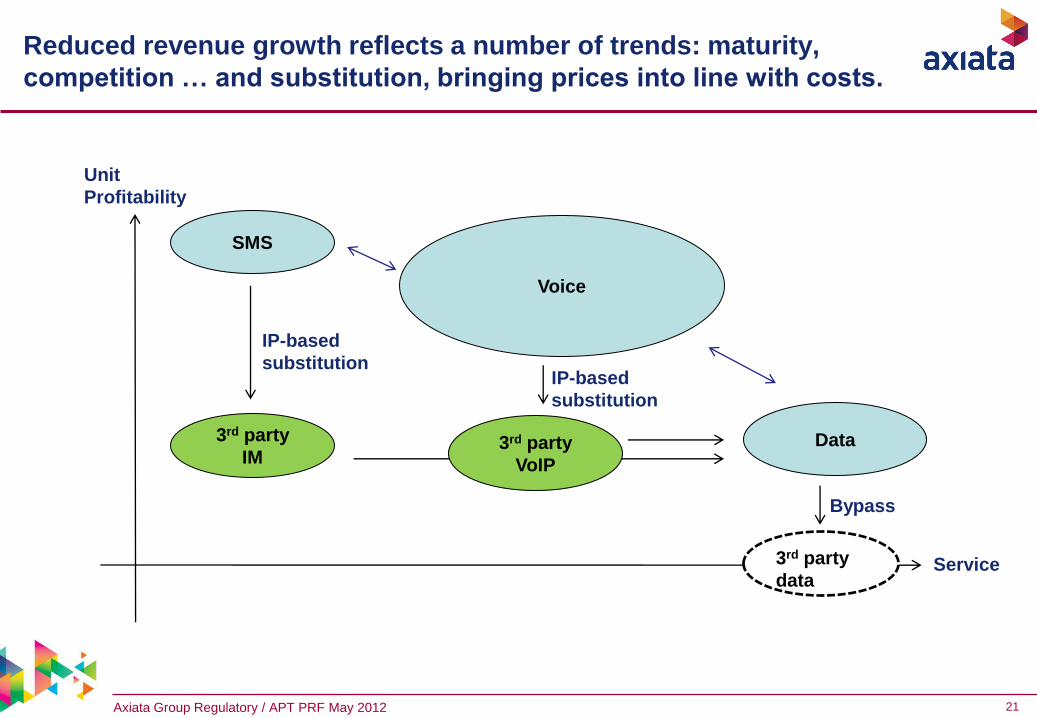

Reduced revenue growth reflects a number of trends: maturity,

competition … and substitution, bringing prices into line with costs.

SMS

Voice

Data

Unit

Profitability

Service

3rd party

IM 3rd party

VoIP

IP-based

substitution

3rd party

data

Bypass

IP-based

substitution

Axiata Group Regulatory / APT PRF May 2012 22

Addressing the Digital Divide through action in fixed Two concepts: the ladder of investment through infrastructure based competition while

the PPP approach promotes service based competition.

PPP approach supports service competition.

Applied, for example, in Singapore.

Regulatory focus on bitstream or resale of fixed

incumbent services facilitates service competition.

Inve

stm

en

t re

turn

Ris

k le

ve

l

high

low Investment cost

Product differentiation high low

Fiber ULL

Sup Loop

Full ULL

Line sharing

Bitstream

Resale

Self build

Infrastructure

Duct Access

Infrastructure

competition

Service competition

Network

competition

Ladder of investment approach in fixed Public Private Partnership approach

Pri

va

te s

ec

tor

ris

k

high

low Private sector

participation high low

Government

Design/Build

Design/Build/Maintain

Design/Build/Operate

Build/Operate/Transfer

Build/Own/Operate

Full privatization

Ladder of investment approach aims to stimulate

(fixed) infrastructure competition.

Applied, for example, in Hong Kong.

Continuing regulatory intervention is necessary to

overcome inherent tensions between fixed

incumbent and entrants in this approach.

UASF, USO,

grants, tax

exemptions