Housing stress: How, Where, Who and Why - Home | … Housing Stress.pdf · Housing stress: How,...

28

Housing stress: How, Where, Who and Why Robert Tanton National Centre for Social and Economic Modelling

-

Upload

nguyenmien -

Category

Documents

-

view

215 -

download

0

Transcript of Housing stress: How, Where, Who and Why - Home | … Housing Stress.pdf · Housing stress: How,...

Housing stress: How, Where, Who and Why

Robert TantonNational Centre for Social and Economic Modelling

Housing Stress: How, Where, Who and Why?

How – to measure housing stress and different variantsWhere – is housing stressWho – is most likely to suffer housing stressWhy – are so many suffering housing stress todayDiscussion, implications

Housing stress: How

Traditionally 30% of income spent on housing costs (’30 rule’)Cut out top 60% of income to cut out middle to high income earners (’30/40 rule’)Cut out bottom 10% to remove odd incomes (’30/10-40 rule’)

Why 30%?

Housing stress is a broad measure• It is best looked at over time• It is only one part of a bigger picture

– General Social Survey – had to borrow– Fujitsu Consulting - mortgage arrears ‘stress-o-meter’

30% rule was used by banks• In the ‘good old days’, couldn’t get a loan unless could afford to pay

30% of income on mortgage

Used by real estate agents• Can’t get rental property if rent was more than 30% of income

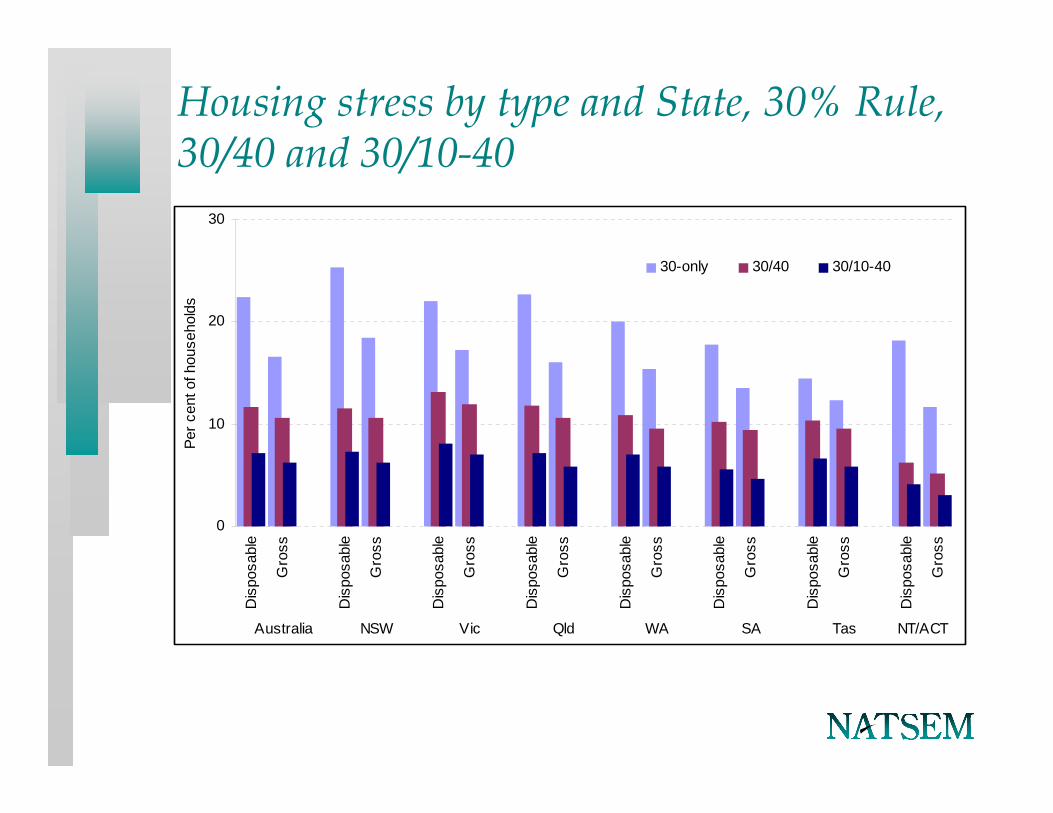

Housing stress by type and State, 30% Rule, 30/40 and 30/10-40

0

10

20

30

Dis

posa

ble

Gro

ss

Dis

posa

ble

Gro

ss

Dis

posa

ble

Gro

ss

Dis

posa

ble

Gro

ss

Dis

posa

ble

Gro

ss

Dis

posa

ble

Gro

ss

Dis

posa

ble

Gro

ss

Dis

posa

ble

Gro

ss

Australia NSW Vic Qld WA SA Tas NT/ACT

Per c

ent o

f hou

seho

lds

30-only 30/40 30/10-40

Alternatives to 30% Housing Stress measure – Reserve Bank

Reserve Bank - % dwellings accessible to persons aged 25 – 39 years based on assumptions about bank lending behaviour (30% repayment to gross income ratio, 10% deposit)• Affordability worse over last 10 years

Alternatives to 30% Housing Stress measure – Urban Development Institute of Australia

UDIA/Matusik Measure – Unnafordable when a household spending 30% of average income for area on repayments could purchase less than 15% of houses in area• In NSW, most areas had detached houses affordable in 2001,

Unaffordable or Seriously constrained in 2006• State average gone from Affordable to Seriously Constrained• For WA, State average gone from Affordable in 2001 to

Unaffordable in 2006

Alternatives to 30% - Fujitsu ‘stress-o-meter’

Propensity to default * number of defaults+ Forced sales+ Average arrears months * Affordability * Reprioritised spending70,000 households experiencing ‘severe stress’, hot spots in Sydney, Melbourne and Perth.

Alternatives to 30% Housing Stress measure

All but one measure uses 30% of income somewhere in calculationAll measures giving similar results – increasing over last 10 years, particularly bad in NSW30% measure is probably easiest for public to understand

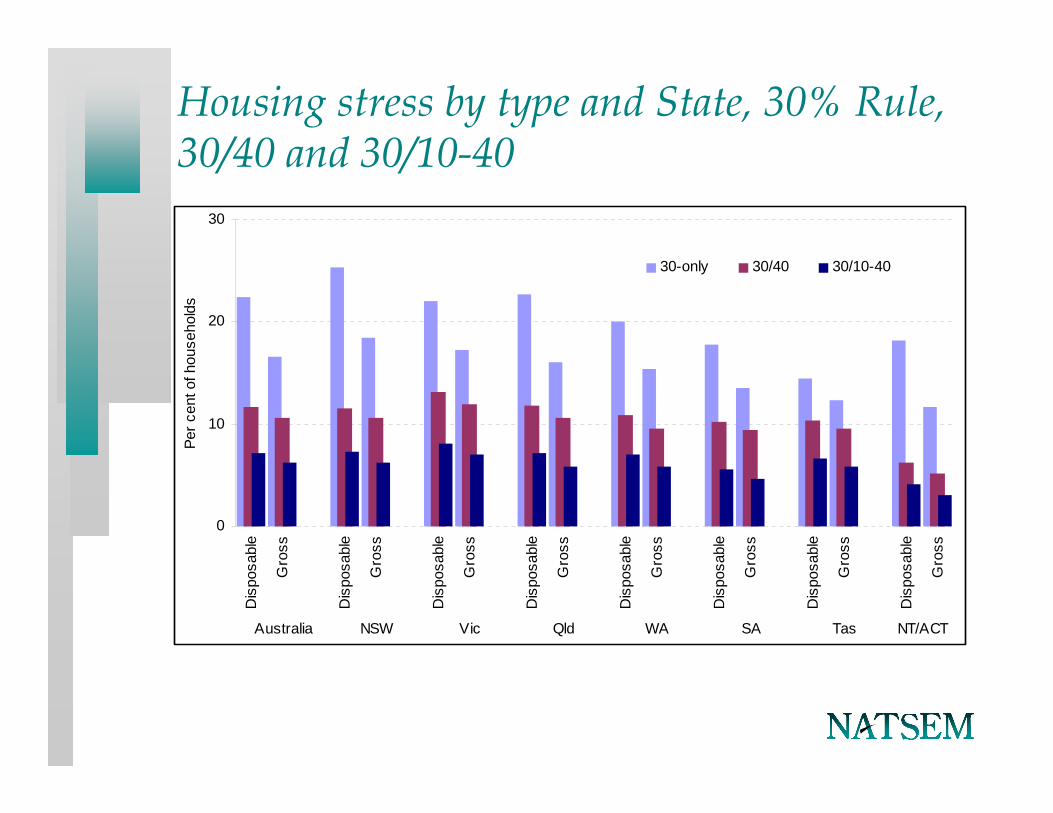

Housing stress by type and State, 30% Rule, 30/40 and 30/10-40

0

10

20

30

Dis

posa

ble

Gro

ss

Dis

posa

ble

Gro

ss

Dis

posa

ble

Gro

ss

Dis

posa

ble

Gro

ss

Dis

posa

ble

Gro

ss

Dis

posa

ble

Gro

ss

Dis

posa

ble

Gro

ss

Dis

posa

ble

Gro

ss

Australia NSW Vic Qld WA SA Tas NT/ACT

Per c

ent o

f hou

seho

lds

30-only 30/40 30/10-40

Housing stress: How

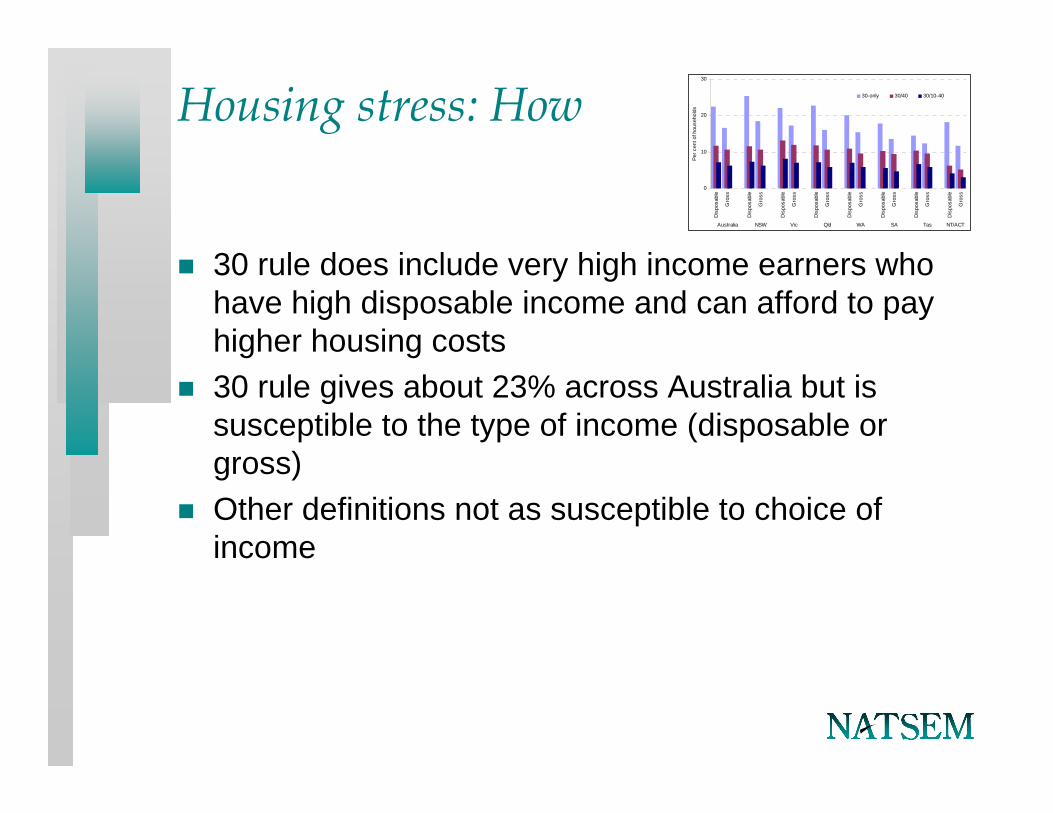

30 rule does include very high income earners who have high disposable income and can afford to pay higher housing costs30 rule gives about 23% across Australia but is susceptible to the type of income (disposable or gross)Other definitions not as susceptible to choice of income

0

10

20

30

Dis

posa

ble

Gro

ss

Dis

posa

ble

Gro

ss

Dis

posa

ble

Gro

ss

Dis

posa

ble

Gro

ss

Dis

posa

ble

Gro

ss

Dis

posa

ble

Gro

ss

Dis

posa

ble

Gro

ss

Dis

posa

ble

Gro

ss

Australia NSW Vic Qld WA SA Tas NT/ACT

Per c

ent o

f hou

seho

lds

30-only 30/40 30/10-40

Housing Stress: How

30/40 rule• Cuts out top 60% of income earners• This is those earning more than $50,000 (Australia) for couple family

with 1 child

Choice of income (disposable/gross) has little effect

0

10

20

30

Dis

posa

ble

Gro

ss

Dis

posa

ble

Gro

ss

Dis

posa

ble

Gro

ss

Dis

posa

ble

Gro

ss

Dis

posa

ble

Gro

ss

Dis

posa

ble

Gro

ss

Dis

posa

ble

Gro

ss

Dis

posa

ble

Gro

ss

Australia NSW Vic Qld WA SA Tas NT/ACT

Per c

ent o

f hou

seho

lds

30-only 30/40 30/10-40

Housing Stress: How

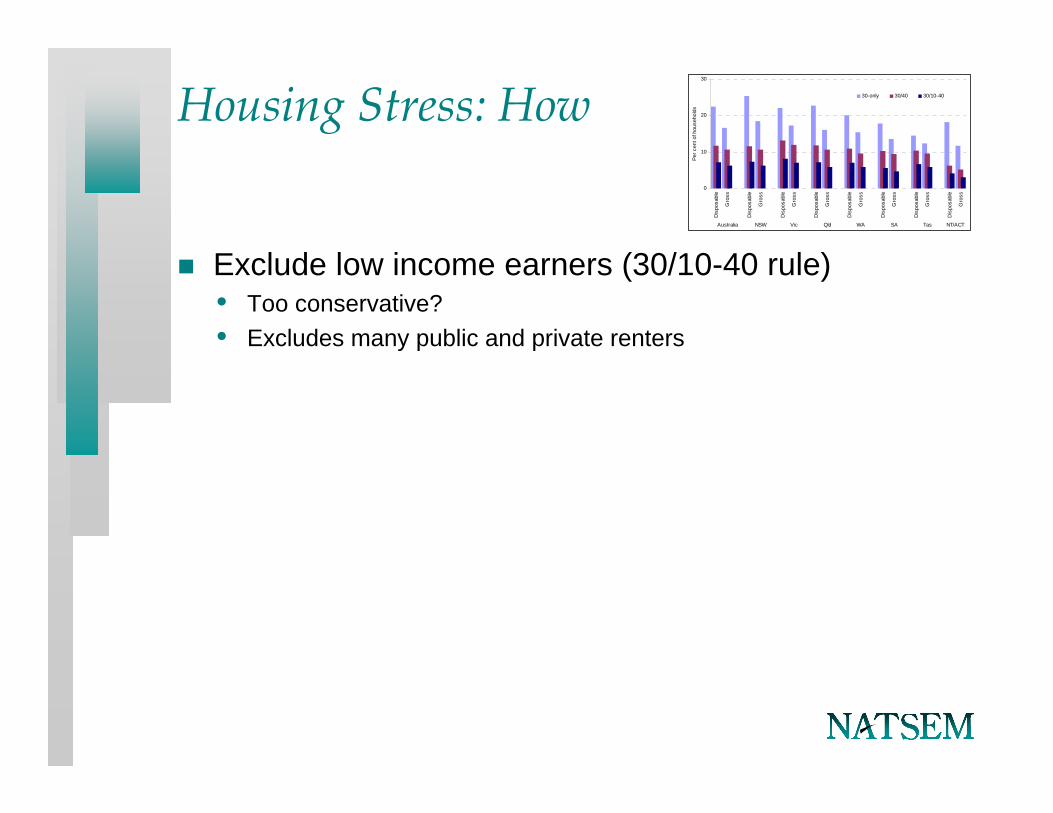

Exclude low income earners (30/10-40 rule)• Too conservative?• Excludes many public and private renters

0

10

20

30

Dis

posa

ble

Gro

ss

Dis

posa

ble

Gro

ss

Dis

posa

ble

Gro

ss

Dis

posa

ble

Gro

ss

Dis

posa

ble

Gro

ss

Dis

posa

ble

Gro

ss

Dis

posa

ble

Gro

ss

Dis

posa

ble

Gro

ss

Australia NSW Vic Qld WA SA Tas NT/ACT

Per c

ent o

f hou

seho

lds

30-only 30/40 30/10-40

Housing Stress by Tenure type

0

10

20

30

40

Dis

posa

ble

Gro

ss

Dis

posa

ble

Gro

ss

Dis

posa

ble

Gro

ss

Dis

posa

ble

Gro

ss

Renter private Purchaser Renter public Ow ner

Per c

ent o

f hou

seho

lds

30-only 30/40 30/10-40

Housing stress: How

NATSEM tends towards 30/40 rule if data allowsSometimes the data doesn’t allow it

Housing stress: Where?Housing stress by State using the 30/40 rule

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

NSW Vic Qld SA

WA Tas

ACT/NT

Austra

lia

State

% in

hou

sing

stre

ss

Capital CityRest of StateState

Housing stress: Who?

30/40 rule• Labour force status• Family Type• Age

Housing Stress: Who?Housing Stress by labour force status

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

45.0

50.0

Employed fulltime

Employedpart time

Unemployed Not in labourforce

Australia

Labour force status

% in

hou

sing

stre

ss

Housing stress by family typeHousing stress by family type

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

Couplewith nochildren

Couplewith

children

Sole parent Single Others Australia

Family type

% in

hou

sing

stre

ss

Housing stress by Age of household reference person

Housing Stress by age of household reference person

0

5

10

15

20

25

15 to

20 ye

ars

21 to

29 ye

ars30

to 39

years

40 to

49 ye

ars50

to 59

years

60 to

69 ye

ars70

+yea

rsAus

tralia

Age of reference person

% in

hou

sing

str

ess

Housing stress: Who?

So far, used 30/40 ruleWhen looking at income, need to use 30 only rule, used in AMP reportAlso some other interesting splits from AMP report• Over time• Recent buyers

Housing stress (30 only) over time

21.3

18.1

20.0

15.116.9

8.5

19.0

25.4

22.0 22.7

17.8

20.1

14.5

11.5

20.922.5

0

5

10

15

20

25

30

NSW VIC QLD SA WA TAS NT ACT AUS

%H

H s

pend

ing

mor

e th

an 3

0% o

f inc

ome

on h

ousi

ng 1995-96 2005-06

Housing stress (30 only) by incomeHousing stress by income

0

5

10

15

20

25

30

35

0 to 0.5 median(poverty)

0.5 median tomedian

Median to 1.5median

Above 1.5 median(high incomehouseholds)

Income class

% in

hou

sing

str

ess

Housing stress (30 rule) by recent purchasers Housing stress for new home owners and old

0

10

20

30

40

50

60

70

Bought in thepast 3 years asthe first home

Bought in thepast 3 years butnot as the first

home

Bought more than3 years ago andnow fully owned

Bought more than3 years ago and

still payingmortgage

Type of purchase

% in

hou

sing

str

ess

Housing stress: Why?

House prices have increased 5 fold in the last 20 years, where incomes have doubled

100

200

300

400

500

600

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

Averge earning index

House price index

`

What has caused this huge increase in house prices?

Lots of complex interactions• Supply/Demand, particularly in capital cities

– Demographics• Government fees and charges• Interest rates

Means isn’t one simple solution• Land release• Banks lending less

Discussion/Implications

Housing stress is hitting people in Australia disproportionately• Low income• Unemployed• Sole parent families• First home buyers• Younger

Young and first home buyers have a long term potentialOthers are marginal groups in society also suffering other problems (stress, mental health, physical health)

Implications

Need to think about longer term• Easier ways to pass on housing wealth to younger generations• Those who are in housing stress are the marginalised – how can we

help them?– Housing assistance– Public housing