House of Commons Treasury Committee · Mr Andy Love MP (Labour, Edmonton) ... The OBR explained the...

60

HC 818–I House of Commons Treasury Committee Autumn Statement 2012 Seventh Report of Session 2012–13 Volume I

Transcript of House of Commons Treasury Committee · Mr Andy Love MP (Labour, Edmonton) ... The OBR explained the...

HC 818–I

House of Commons

Treasury Committee

Autumn Statement 2012

Seventh Report of Session 2012–13

Volume I

HC 818–I Published on 29 January 2013

by authority of the House of Commons London: The Stationery Office Limited

£0.00

House of Commons

Treasury Committee

Autumn Statement 2012

Seventh Report of Session 2012–13

Volume I

Report, together with formal minutes

Ordered by the House of Commons to be printed 22 January 2013

The Treasury Committee

The Treasury Committee is appointed by the House of Commons to examine the expenditure, administration, and policy of HM Treasury, HM Revenue and Customs and associated public bodies.

Current membership

Mr Andrew Tyrie MP (Conservative, Chichester) (Chairman) Mark Garnier MP (Conservative, Wyre Forest) Stewart Hosie MP (Scottish National Party, Dundee East) Andrea Leadsom MP (Conservative, South Northamptonshire) Mr Andy Love MP (Labour, Edmonton) John Mann MP (Labour, Bassetlaw) Mr Pat McFadden MP (Labour, Wolverhampton South West) Mr George Mudie MP (Labour, Leeds East) Mr Brooks Newmark MP (Conservative, Braintree) Jesse Norman MP (Conservative, Hereford and South Herefordshire) Teresa Pearce MP (Labour, Erith and Thamesmead) David Ruffley MP, (Conservative, Bury St Edmunds) John Thurso MP (Liberal Democrat, Caithness, Sutherland, and Easter Ross)

Powers

The Committee is one of the departmental select committees, the powers of which are set out in House of Commons Standing Orders, principally in SO No 152. These are available on the Internet via www.parliament.uk.

Publication

The Reports and evidence of the Committee are published by The Stationery Office by Order of the House. All publications of the Committee (including press notices) are on the Internet at www.parliament.uk/treascom. The Reports of the Committee, the formal minutes relating to that report, oral evidence taken and some or all written evidence are available in printed volume(s). Additional written evidence may be published on the internet only.

Committee staff

The current staff of the Committee are Chris Stanton (Clerk), Lydia Menzies (Second Clerk), Jay Sheth and Adam Wales (Senior Economists), Hansen Lu, Matthew Manning (on secondment from the FSA) and Duncan Richmond (on secondment from the NAO) (Committee Specialists), Steven Price (Senior Committee Assistant), Jo Cunningham and Lisa Stead (Committee Assistants) and James Abbott (Media Officer).

Contacts

All correspondence should be addressed to the Clerk of the Treasury Committee, House of Commons, 7 Millbank, London SW1P 3JA. The telephone number for general enquiries is 020 7219 5769; the Committee’s email address is [email protected]

Autumn Statement 2012 1

Contents

Report Page

1 Introduction 3 Our inquiry 3 Timing and content of the Autumn Statement 3 Budget 2013 timing 4

2 Macroeconomy 5 Overall GDP forecast 5

Forecasting 7 Business lending 9

Business lending and the impact of the Funding for Lending Scheme 9 Banks’ balance sheet transparency and forbearance 12 ‘Zombie’ companies 14 A bad bank? 16 Conclusions on bank lending 17

Output gap 17 OBR’s change in method 18 A persistently large output gap 19

Monetary policy 21 The effectiveness of Quantitative Easing 21 Monetary policy framework 24

3 The public finances 26 Changes announced in the Autumn Statement 26 Performance against the fiscal targets 26

The fiscal mandate 26 The supplementary target 27

Credit rating 28 UK cost of borrowing 29 Asset Purchase Facility transfer 30

4 Policy decisions 33 Reliance on big ticket items 33

Sale of the 4G spectrum 34 Swiss tax repatriation 36 Departmental cuts 37 Fuel Duty 38

5 Other issues 40 Measures to encourage growth 40 Reforming PFI 41 Distributional analysis 44

Estimated effect of benefit announcements 45

Conclusions and recommendations 49

2 Autumn Statement 2012

Formal Minutes 53

Witnesses 54

List of printed written evidence 54

List of Reports from the Committee during the current Parliament 55

Autumn Statement 2012 3

1 Introduction

Our inquiry

1. The Autumn Statement was delivered by the Chancellor on Wednesday 5 December 2012, and the Economic and fiscal outlook was published by the Office for Budget Responsibility (OBR) on the same day. The Treasury Committee took evidence from six panels of witnesses during the three meetings we held, as follows:

11 December: Office for Budget Responsibility

Robert Chote, Chairman, Graham Parker, Member, and Professor Stephen Nickell, Member, Budget Responsibility Committee.

12 December: Experts and interested parties

First panel: Simon Hayes, Barclays; Paul Mortimer-Lee, BNP Paribas, and Simon Wells, HSBC;

Second panel: Professor Philip Booth, Institute of Economic Affairs, and Lee Hopley, EEF;

Third panel: Paul Johnson and Carl Emmerson, Institute for Fiscal Studies;

Fourth Panel: Mark Hellowell, University of Edinburgh (Specialist Adviser) and Professor Dieter Helm, University of Oxford.

13 December: HM Treasury

Rt Hon George Osborne MP, Chancellor of the Exchequer and James Bowler, Director, Strategy, Planning and Budget.

We have also made use of oral evidence taken from the National Institute of Economic and Social Research on 13 November, and from the Bank of England Monetary Policy Committee on 27 November. The Committee is very grateful to all those who gave their time to provide oral and written evidence to us, in some cases at short notice.

Timing and content of the Autumn Statement

2. The Budget this year was on 21 March 2012. The Autumn Statement was nearly nine months later, and only just over three months before the next Budget, which the Chancellor has announced will be on 20 March 2013. This has had the consequence, the Institute for Fiscal Studies (IFS) said, that the more important economic forecast and statement is the Autumn Statement, not the Budget.1 There were, furthermore, many fiscal announcements in this year’s Autumn Statement that would be more usual in a Budget. Whilst it is recognised that an Autumn Statement is useful to appraise the effectiveness (or otherwise) of measures announced in the spring Budget, and the general state of public finances and the wider economy, the Autumn Statement has taken on the role of

1 Q 190

4 Autumn Statement 2012

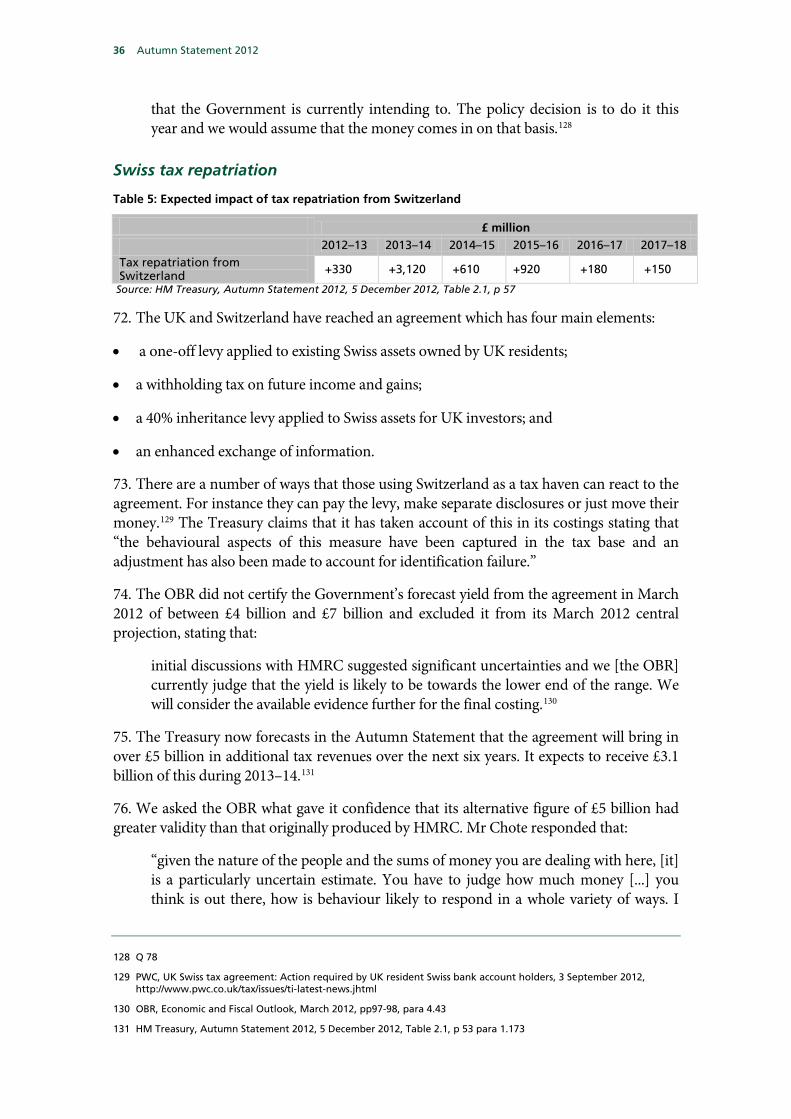

being a second, full, Budget. The implications are that business and the economy needs to react to two periods, not one, of potential uncertainty and change. A return to a position of one Budget in the spring, and an updating statement in the autumn, would be desirable.

Budget 2013 timing

3. As already noted, the Budget will be on Wednesday 20 March, allowing some days for the House to debate the Budget before it rises for the Easter adjournment on Tuesday 26 March. The timings are similar to last year and will require the Treasury Committee to hear oral evidence on the Budget rapidly before the House rises.

4. Last year the Finance Bill was published in the Easter adjournment, on 29 March, and the Second Reading was on the first day the House sat after the adjournment, on Monday 16 April. This timing prevented the Treasury Committee agreeing or publishing its Report in time for Second Reading of the Finance Bill as its practice had been. The Committee agreed its Report on Tuesday 17 April and published it the following day, the first day of the Committee of the Whole House on the Finance Bill.

5. In our Budget 2012 Report we described the timings set by the Government as “highly unsatisfactory”. We recognised that the new pattern of Prorogation and State Opening in April/May risked making the timing of the stages of future Finance Bills tighter than in the recent past, and so recommended that:

the Treasury and the Business Managers work together to plan the timings of future Budgets and Finance Bills so that the House has longer between publication of the Bill and Second Reading and, particularly, between Second Reading and Committee of the Whole House. This may require the Budget to be somewhat earlier in future.2

The Government response to this recommendation was a general one which did not address our particular concern: “The Government is committed to ensuring there is adequate time for Parliament to scrutinise the finance bill”.3

6. The timing of the Budget in 2013 is equivalent to that in 2012. Bearing in mind the vague response of the Government to the serious concerns we raised in 2012, there remains the risk that the Government might schedule the Second Reading of the Finance Bill, and perhaps also the Committee of the Whole House stage, for the week of 15 April 2013. This would be wholly unacceptable and would fail to give the House the time to consider the Bill and the conclusions of the Treasury Committee. We reiterate our recommendation that Treasury and business managers ensure that the House has a longer period than in 2012 between the publication of the Finance Bill and its Second Reading and, particularly, between Second Reading and Committee of the Whole House. We believe this to be an important issue of principle going to the heart of Treasury Ministers’ accountability to Parliament.

2 Thirtieth Report of Session 2010–12, Budget 2012, HC 1910, para 2

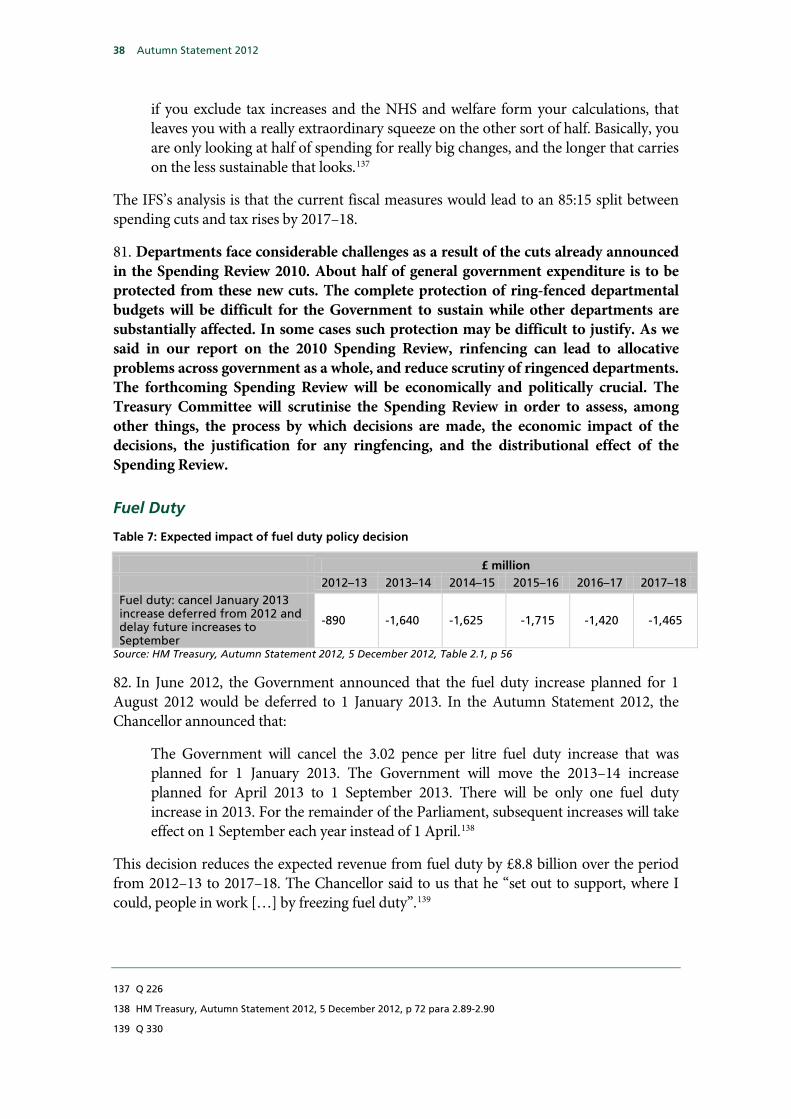

3 Second Special Report of Session 2012–13, HC 422

Autumn Statement 2012 5

2 Macroeconomy

Overall GDP forecast

7. According to the Office for Budget Responsibility (OBR), the outlook for the UK economy had deteriorated since their March 2012 forecast. As Table 1 shows, the OBR has reduced its forecast for real GDP growth in every year from 2012 to 2016. The OBR explained the most recent forecast as follows:

The economy has performed less strongly this year than we expected at the time of our last forecast in March, primarily reflecting the weakness of net exports. Looking forward, the recovery still lacks momentum. We now expect a small fall in GDP in the fourth quarter of this year, followed by a gradual pick-up next year. GDP is forecast to fall by 0.1 per cent in 2012 and then to grow by 1.2 per cent in 2013.

We are more pessimistic about the economy’s medium term growth prospects than we were in March. We expect weak productivity to constrain nominal earnings growth for longer, with a slower fall in inflation delaying the pick-up in real incomes. The outlook for the world economy and UK exports has deteriorated and we expect the difficulties of the euro area to depress confidence and put upward pressure on bank funding costs for longer. Investment is likely to be restrained by poor credit conditions and uncertainty about demand.4

Table 1: OBR’s real GDP growth forecasts (percent)

March 2012 Economic and Fiscal Outlook

December 2012 Economic and Fiscal Outlook

Change (percentage points)

2012 0.8 -0.1 -0.9

2013 2.0 1.2 -0.8

2014 2.7 2.0 -0.7

2015 3.0 2.3 -0.7

2016 3.0 2.7 -0.4

2017 - 2.8 -

Source: Office for Budget Responsibility, Economic and fiscal outlook press conference slides, December 2012, Slide 5

8. The November 2012 Inflation Report also saw the Bank of England’s Monetary Policy Committee (MPC) change its forecast for GDP growth, placing less weight on the potential for more positive outcomes for the economy.5 Sir Mervyn King, Governor of the Bank of England, explained that:

we have significantly lowered, in our view, the chances of growth being rapid. This is something that I think has been building up in our minds over the past year. It is not

4 Office for Budget Responsibility, Economic and fiscal outlook, December 2012, p 5, paras 1.1-1.2

5 Bank of England, Inflation Report, November 2012, p 40, Charts 5.2-5.3

6 Autumn Statement 2012

a sudden change between August and November. Although we only made the change in these charts in November, I think it was a result of finally realising that, as we had debated among ourselves the prospects for growth and the chances of a very rapid expansion of growth—which you might have expected if this had been a normal cyclical downturn and then recovery—we do not think that the chances of very rapid growth in 2013 and 2014 are very great. So we made what we thought was a realistic change to our judgment about where the balance of risks lies.6

The Governor went on to explain why the MPC had come to that conclusion, emphasising the impact of external factors on the UK’s economic performance:

I think the underlying economic factors that have led us to make this judgment through the year—and it has built up over that period—have been external factors. We have seen two things. One is obviously continuing problems in the euro area. We have also seen a slowdown in the world economy as a whole, particularly in the emerging markets, and our colleagues in the United States are still very nervous about the prospects there. I think the consequences of that, particularly weakness in the euro area, certainly have fed through to higher funding costs for banks, which temporarily we have managed to offset with the Funding for Lending scheme. The underlying problem is one in which there is still a great deal of adjustment to be made in the financial sector and in the economy as a whole, with the need for rebalancing. In this sort of situation, it is very unlikely that we would expect to see a rapid recovery.7

The Chancellor also emphasised to us the eurozone crisis’s impact on the UK economy:

the eurozone crisis has had a huge impact on the British economy and indeed many other Western economies. It is not the only thing that is affecting the British economy, of course, and we still are living with the aftershocks of the financial crisis and we were hit by the oil price increase as well across the world. In terms of attributing a number to it, first of all the OBR’s analysis of the deterioration in the growth forecasts since the Budget is that the weakness in the eurozone is the principal cause, indeed more than accounts for the downgrade of the forecast. There is an interesting observation: if trade to the eurozone had grown as fast as trade to the non-eurozone over the last year, then that would have added 1% to our GDP. But I would stress that the impact of the eurozone crisis is not just on trade, it is also on confidence and it is also on financial intermediation. But there is an illustration of the impact. It is something of course that Britain and other countries have to work with.8

9. The over-optimism, in hindsight, of previous OBR forecasts has been a source of concern. We asked witnesses whether the OBR’s forecasts economic forecasts were reasonable this time. Mr Wells argued that such over optimism had not been the sole preserve of the OBR: “I think it is not just them, and it is not just the UK. If you look at the

6 Oral evidence taken before the Treasury Committee, Bank of England November 2012 Inflation Report, Tuesday 27

November 2012, HC (2012-13) 767, Q 3

7 Oral evidence taken before the Treasury Committee, Bank of England November 2012 Inflation Report, Tuesday 27 November 2012, HC (2012-13) 767, Q 5

8 Q 269

Autumn Statement 2012 7

consensus, the average of economists’ forecasts over the past decade, in the UK and the US we have been too optimistic about growth and inflation consistently for nearly a decade”. 9 We discuss the OBR’s forecasting record further below. On the OBR’s present forecast, Mr Wells argued that:

I do think that their latest set of forecasts for this year and next are much closer to the averages and therefore seem much more reasonable than they did in March. So in that sense, as I said at the beginning, I do believe them. Where I still have some concerns is that if this 10-year trend towards over-optimism doesn’t actually come good this time then their forecasts for the potential growth rate of the economy, and indeed the growth rates further out beyond 2015, will turn out to be too optimistic once again. I think there is clearly a big risk of that. Everyone hopes that the UK growth prospects will pick up, but you are quite right, it is not a given.10

Forecasting

10. Under the Budget Responsibility and National Audit Act 2011, the OBR is required to prepare two fiscal and economic forecasts each financial year.11 The Treasury Committee concluded in its Report on the OBR’s creation that:

One of the ways in which we will judge whether the OBR is a success is whether there is greater public understanding of the purpose and limitations of the forecasting process, and realistic expectations of what it can deliver.

There should, and will certainly, be analysis of the accuracy of OBR forecasts. Their quality and authority can be measured over time, relative to other forecasts. Absolute accuracy is not a useful criterion.12

Underlining the inherent uncertainty in its economic forecasts, the OBR noted in its October 2012 Forecast Evaluation Report that:

Along with many other forecasters, we significantly overestimated economic growth over the past two years. This likely reflected several factors, including the impact of stubborn inflation on real consumer spending, deteriorating export markets on net trade, and impaired credit conditions, euro area anxiety and demand uncertainty on business investment. Fiscal consolidation may also have done more to slow growth than we assumed.13

Mr Robert Chote, Chair of the OBR, accepted that most OBR reports had revised downwards the growth forecast from the previous one.14 Given these errors, Mr Chote explained how he believed that the OBR’s own forecasting record had helped to meet the

9 Q 136

10 Q 136

11 Budget Responsibility and National Audit Act 2011, Section 4

12 Treasury Committee, Fourth Report of session 2010-12, Office for Budget Responsibility, paras 38-39

13 Office for Budget Responsibility, Forecast Evaluation Report, October 2012, p 8

14 Q 40

8 Autumn Statement 2012

Treasury Committee’s expectations that the OBR further the public’s understanding of the limitations of forecasting:

I think the cynical and obvious answer to that is, given the outturns for growth relative to what we said, we have probably done quite a good job in demonstrating the limitations of economic forecasting. The key thing is to underline the uncertainties that are around any forecast and for us to explain that nobody should bet the farm on a particular path being the definite outcome and, therefore, to explain how much it matters to the fiscal targets that we are ultimately here to police if the forecast turns out to be different in any one of a number of ways reflected in our sensitivities and scenarios.15

11. Mr Chote also set out why the OBR needed to undertake its own economic forecasts, rather than simply take the average of outside forecasters:

we need a particular type of economic forecast to produce a bottom-up fiscal forecast that really is not out there to pluck off the shelf. For example, you want something that has a much more detailed breakdown of different categories on the income and expenditure side of GDP than most other forecasters would need for their purposes. You need something that extends over five years, you need to take a view on potential output and the output gap over five years, and many people don’t. The other thing is that you need to be able to take into account the impact that measures will have on the fiscal forecast and that is quite hard to do if you are simply trying to bolt it on to a table you have plucked out of a compilation of independent forecasts.16

12. When we questioned City experts on the forecast record of the OBR, Mr Simon Wells, Chief UK Economist at HSBC, told us “They are doing a great service and being very transparent and very open about what they are saying.”17 He added that “The creation of the OBR was a positive step. It does add a lot of credibility to the forecasts, and we have seen that they are not afraid of marking down their forecasts really quite sharply if that is what they think needs doing.”18 Mr Paul Mortimer-Lee, Global Head, Market Economics, BNP Paribas, suggested that there might be an inbuilt optimism bias to the forecasts of the OBR: “If I was the OBR, I would be quite worried about projecting gross debt over 100% of GDP, because that would probably prompt downgrades from at least some of the agencies.”19 He argued that “what are the costs and benefits of erring on either side? If you take account of the costs and benefits, then the costs of erring on the pessimistic side are rather more serious.”20 He noted, however, that “I am not saying they are doing it on purpose, but subconsciously.”21 Mr Simon Hayes, Chief UK Economist at Barclays, however, had confidence that the OBR was giving its best judgement of the outlook for the economy:

15 Q 1

16 Q 3

17 Q 104

18 Q 105

19 Q 106

20 Q 109

21 Q 112

Autumn Statement 2012 9

I think what has happened over the last couple of years is the Chancellor came up with a debt reduction plan and some fiscal rules. Then in November last year the OBR completely changed its view of the underlying potential capacity of the economy and that had the effect of almost totally eliminating the headroom under the two fiscal rules. If the Chancellor had known that assessment, I think we would have had a different set of fiscal rules, so that took us to the edge of breaching these rules. We have now had the OBR revise down not just its real GDP forecasts quite substantially but also its forecast for the GDP deflator, so the nominal GDP forecast is very much lower as well, and that has led to the breach of the debt rule. I think if you were trying to be kind to the Chancellor, you may have done neither of those things and the fact that they have suggests to me that they are, by and large, reporting things as they see them and that the consequences are something for the Chancellor to deal with.22

13. As we have recommended in the past, the OBR should do more to ensure that there is greater public understanding of the limitations and purpose of forecasting, and more realistic expectations of what forecasting can deliver.

14. The OBR’s forecasts so far have been biased to over-optimism. This would not be a cause for concern but for the fact that the OBR’s forecasts have implications for decisions on public policy. This is because the fiscal mandate is defined with direct reference to a forecast, and because the OBR’s is at present the only official forecast against which the fiscal mandate can be measured.

15. The OBR is required by statute to issue two economic and fiscal forecasts a year. The Chancellor’s own Autumn Statement, however, has now grown to be virtually a second Budget. There are good reasons for having a single substantial annual review of the fiscal and economic state of the country, not least to enable the subsequent presentation to Parliament of proposed tax measures and of Estimates of expenditure. The Treasury should re-establish the annual Budget as the main focus of fiscal and economic policy making.

Business lending

Business lending and the impact of the Funding for Lending Scheme

16. The evidence we received suggested that lending to firms was still not sufficient. Lee Hopley, Chief Economist at the EEF, provided a view on credit conditions:

We have a regular credit condition survey across our membership, and we have seen some small signs of slow improvement in both the availability of new lines of credit and some improvement in the balances on cost of credit, although more companies say that credit is getting more expensive relative to it getting cheaper. So there is still an issue. We are only taking small steps from a very low base. I think there is a lot of other evidence out there that suggests a more worrying trend that small companies in particular are disengaging from the financial sector completely. They have a

22 Q 113

10 Autumn Statement 2012

demand for credit, they have investment plans, but they don’t want to go to their bank or external finance providers to get finance to fund those investment plans.23

Simon Kirby, of NIESR, also argued that “Finance from banks is a particular problem for SMEs at present”, although he also warned that:

Some surveys suggest that this is a significant inhibitor to them for investment, but there are also surveys out there that do not suggest that SMEs are having more than a normal inability to raise finance from banks. There is a mixed element to the story.24

17. One of the responses by the Government and the Bank of England to weakness in business lending has been the creation of the Funding for Lending Scheme (FLS). The OBR described it as follows:

The Funding for Lending Scheme (FLS) was launched by the Bank of England and the Government in July 2012. It is designed to encourage banks and building societies to expand their lending to households and private non-financial corporates, by providing funds at cheaper rates than those prevailing in current markets. Both the quantity and the price of these funds are linked to the amount of lending that banks do. The lower cost of FLS funds should then be passed on to real economy customers in lower borrowing costs.25

18. On 3 December 2012, the Bank of England published the first set of data on the FLS.26 Since we completed our hearings, the Bank of England has published the following update on progress with the FLS:

Participation in the Scheme is widespread. Thirty-five banking groups, comprising just over 80% of the stock of FLS eligible loans, had signed up by 3 December 2012. That translates into an initial entitlement of around £68 billion of funding. It was too early for the Scheme to affect net lending in 2012 Q3. And total real economy net lending was close to zero in that quarter. There was net lending of £7.6 billion, however, by those participating groups with positive net lending. That means that the total borrowing allowance increased to around £76 billion as of 3 December 2012, which demonstrates the incentives built into the Scheme. The borrowing allowance will continue to increase by one pound for every pound of additional net lending by banks expanding their loan books. By the end of September 2012, eight weeks into the Scheme, just over £4 billion in funding had been drawn from the FLS, and more has been drawn since.27

Lee Hopley, Chief Economist at the EEF, when asked what impact the FLS was having, responded:

23 Q 172

24 Oral evidence to the Treasury Committee, National institute of Economic and Social Research quarterly review, October 2012, taken on 13 November 2013, HC (2012-13) 750, Q 32

25 Office for Budget Responsibility, Economic and Fiscal outlook, December 2012, p57, Box 3.4

26 Bank of England, Funding for Lending Scheme – Usage and lending data, 3 December 2012, www.bankofengland.co.uk

27 Bank of England, The Funding for Lending Scheme by Rohan Churm, Amar Radia, Jeremy, Sylaja Srinivasan and Richard Whisker, Quarterly Bulletin, 2012 Q4, p 315

Autumn Statement 2012 11

I think it is very difficult to say at the moment. They don’t disaggregate the data into household and business lending. We would assume that it would probably take a little bit longer to feed through into business lending. SME lending is more complex than the mortgage market. We are, however, hopeful that the banks will promote the different schemes available and that perhaps Government might even be a bit more vocal about the fact that lower costs of funding should feed through into small-business lending.28

However, she warned that a delay in seeing any results was to be expected:

I think we would like to see more concrete signs of this having fed through towards the middle of next year. Going back to the National Loan Guarantee Scheme, which had a relatively short lifespan as it was, relatively quickly we were picking up anecdotal evidence that companies were benefiting from various offers from different finance providers through that scheme. We would like to be picking up the same kind of evidence as we move into the beginning of next year.29

The potential delay in the results from the FLS was also highlighted by a recent Quarterly Bulletin article, which stated that it was “probable that it will take longer for the effects from the FLS to feed through to certain types of corporate lending because many corporate loans are tailored to the customer, and so are less standardised than mortgage loans.”30

19. The Chancellor appeared pleased with the progress of the FLS so far, noting that according to the OBR, the Scheme “is adding to GDP, it is bringing down the bank funding costs and we have published in the Green Book, if you look at the unsecured bond spreads, the impact that the FLS announcement has had, so that was a joint scheme between the Treasury and the Bank of England, and I think it has been working well.”31

20. One note of concern has, however, been expressed about the FLS. Both NIESR and the OBR have suggested that the banks using the FLS may favour certain types of lending over others. NIESR has said that:

It is noticeable that the Bank of England does not report any suggestions by banks that the FLS will stimulate lending to non-financial corporations. The FLS does not prescribe how banks should target any increase in their gross lending; rather it is designed to stimulate gross lending to the real economy in general. With mortgage lending attracting a lower risk weighting than lending to the corporate sector, it is entirely consistent for the banking sector to utilise a source of cheaper funding to increase their least risky lending.32

The OBR also came to a similar conclusion:

28 Q 175

29 Q 176

30 Bank of England, The Funding for Lending Scheme by Rohan Churm, Amar Radia, Jeremy, Sylaja Srinivasan and Richard Whisker, Quarterly Bulletin, 2012 Q4, p315

31 Q 294

32 NIESR, National Institute Economic Review, Prospects for The UK Economy, by Simon Kirby and Katerina Lisenkova, October 2012, pp F43

12 Autumn Statement 2012

FLS could prompt relaxation of non-price, quantity constraints: recent announcements suggest lower loan-to-value (LTV) limits may be one direct consequence. However, given longer-term pressures on capital, banks may be wary of taking on more risk; under the FLS, credit risk stays with the banks. This may particularly constrain new lending to SMEs, compared to relatively low-risk residential mortgages, and we expect most additional, FLS-related lending to go households, primarily as mortgages.33

However, the most recent Bank of England Credit Condition’s survey noted that:

Overall credit availability to the corporate sector was reported to have increased significantly in Q4, the first reported rise in availability for a year. This was reflected in a significant increase in availability for medium-sized firms, an increase in availability for large firms, and a slight increase for small firms. Lenders commented that the Funding for Lending Scheme had been important in increasing credit availability to the corporate sector, consistent with reports of an easing in wholesale funding conditions pushing up slightly on credit availability. In contrast to the easing in credit availability, loan tenors had been reduced.34

21. It is early days for the Funding for Lending Scheme, and it is too soon to consider its impact on business lending. We are concerned, however, by reports that there may be a bias in the effect of the Scheme that favours lending for mortgages rather than lending to SMEs. The Bank of England and the Treasury should assess whether this is the case and report their findings and any proposed action to the Treasury Committee.

Banks’ balance sheet transparency and forbearance

22. In March 2012, a report by Deloitte noted that:

One of the most striking differences between the 1990s recession and the present Financial Crisis has been the way that banks, building societies and other lenders have dealt with customers facing financial difficulties. This time round, lenders have made greater use of forbearance strategies, granting concessions to customers, both consumer and corporate, in actual or apparent distress to avoid, where possible, the pain of collecting on the debt.35

Such concessions, or forbearance, by the banks to their customers may not always be benign. The Governor of the Bank of England described the potential problem of forbearance as:

[...] Forbearance has two dimensions. Good forbearance can take place when banks feel, “Look, this company does have a long-run future. Let’s not put it in a difficult position now”. Bad forbearance is where the banks do not insist on repayment, not because they care about the customer but because they are worried about the implications for their own balance sheet, given the account conventions under which banks operate. That is undoubtedly a concern, because the issue is [...] to what extent

33 Office for Budget Responsibility, Economic and Fiscal outlook, December 2012, p 57, box 3.4

34 Bank of England, Credit Conditions Survey: Survey results, 2012 Q 4, 3 January 2013, p 5

35 Deloitte, Loan forbearance: No such thing as a free lunch, March 2012

Autumn Statement 2012 13

are the balance sheets giving an accurate representation of the underlying position of the banks?36

Bad forbearance, as defined by the Governor above, is undertaken to favour the bank, which does not want to record the potential loss, rather than the customer (who of course still benefits from that forbearance). It is difficult for outside observers to identify whether forbearance is for good or bad reasons. Since this can raise questions about the true health of a bank’s balance sheet, it may also be one of the factors affecting the level of investment in banks. Dr Armstrong of NIESR argued that:

It is very difficult for outsiders to understand the quality of the assets that are on bank balance sheets. That is why they trade at half the price-book ratio. That was not just an accident of what happened in the external environment. That was our own creation over the last two decades or so, and it was about the way we approached finance. I would not like to portray it as something that is just unlucky. It is something that you have to deal with, and we are doing so, very slowly.37

23. Bad forbearance may also be a potential reason for the present weakness in productivity. Ben Broadbent, an external member of the Monetary Policy Committee of the Bank of England, explained “I have believed for some time that there is a connection between the problems in the financial system and the slowness both of rebalancing and of productivity growth. The difficulty of judging the risks on banks’ balance sheets may well therefore be very important for productivity growth.”38 Mr Paul Mortimer-Lee, BNP Paribas, emphasised the problems faced by the financial system, and how they were feeding through into the real economy, comparing the UK to Japan:

[...] almost 50% of loans to corporates is on commercial real estate and 20% of that commercial real estate is subject to some form of forbearance. I really don’t think that we have tackled the potential losses on commercial real estate. I think the banks are aware of that and that is constraining their ability to lend because they know there are losses coming down the road. To quote Mervyn King, “In judging whether the banks are adequately capitalised, we need to ensure that capital ratios do in fact provide an accurate picture of banks’ health. At present there are good reasons to think that they do not”. The Governor of the Bank of England and Andrew Bailey, the Deputy CO elect of the PRA, talked about we have to avoid becoming Japan. These gentlemen seem to think that we are becoming Japan and part of the reason is we have not tackled the problems of the banks for a variety of reasons for a long number of years, and I agree with them. If you look at the UK, the poor performance is not due to too rapid fiscal tightening. It is certainly not due to an overvalued exchange rate. What is it due to? It is due to a shrinkage in lending, particularly to the corporate sector.39

36 Oral evidence taken before the Treasury Committee, Bank of England November 2012 Inflation Report, Tuesday 27

November 2012, HC (2012-13) 767, Q 96

37 Oral evidence taken before the Treasury Committee, National institute of Economic and Social Research quarterly review, October 2012, taken on 13 November 2012, HC (2012-13) 750, Q 66

38 Oral evidence taken before the Treasury Committee, Bank of England November 2012 Inflation Report, Tuesday 27 November 2012, HC (2012-13) 767, Q 94

39 Q 122

14 Autumn Statement 2012

24. This concern about the transparency and soundness of banks’ balance sheets has also been expressed recently by the interim Financial Policy Committee (FPC) of the Bank of England:

Historical experience suggested that slow progress in tackling balance sheet problems could impede the recovery of banking systems— and, in turn, the wider economy—from financial crises. A large legacy of poor lending decisions and the perception that banks may have inadequately provisioned against future losses, including on loans subject to forbearance, could create uncertainty about bank capital adequacy and prospective earnings. This could both undermine investor confidence and inhibit the ability of banks to extend new loans to the real economy.40

The interim FPC’s recommendation was that:

the FSA takes action to ensure that the capital of UK banks and building societies reflects a proper valuation of their assets, a realistic assessment of future conduct costs and prudent calculation of risk weights. Where such action reveals that capital buffers need to be strengthened to absorb losses and sustain credit availability in the event of stress, the FSA should ensure that firms either raise capital or take steps to restructure their business and balance sheets in ways that do not hinder lending to the real economy.41

‘Zombie’ companies

25. In our hearings, we discussed with witnesses how far low interest rates and bank forbearance could be a problem for the economy by creating so called ‘zombie companies’—companies that survive day-to-day owing to low interest rates and bank forbearance, but which may struggle to survive in the future. The November 2012 Inflation Report highlighted the risk that:

Evidence on company liquidations could indicate that forbearance, coupled with the low level of Bank Rate, has allowed businesses that will face lower demand in the longer term to continue trading. And a drop in the number of company births may indicate that banks may have been less willing to lend to new or dynamic companies that have the potential to achieve higher productivity.42

Dr Armstrong, NIESR, compared the UK situation with that in Japan:

The notion of zombie firms goes back to the Japanese recession back in the 1990s, and some very famous papers that were written on the back of that. The most important thing is that not only are these firms kept alive but they prevent new firms

40 Bank of England, Record of the Interim Financial Policy Committee meeting held on 21 November 2012. Publication

date: 4 December 2012, para 8

41 Bank of England, Record of the Interim Financial Policy Committee meeting held on 21 November 2012. Publication date: 4 December 2012, para 19

42 Bank of England, Inflation Report, November 2012, p 33

Autumn Statement 2012 15

coming into the market. It is effectively a subsidy to existing firms. You have not only a static effect but also the ongoing ramifications.43

However, he warned against placing too much weight solely on this explanation. He noted that:

the difficult bit with this zombie idea is that, first, lending rates are not exactly low for SMEs. If the lending rates were low, it would be an easy story to tell. Secondly, firms are hiring. If they were not hiring, it would be an easy story to tell as well.44

26. Robert Chote, Chair of the OBR, noted that the slow growth in wages would also be aiding some firms.45 He argued that the problem might be a wider one of the misallocation of capital:

I think it is debatable to what extent it is the zombie firm explanation, i.e. not particularly productive or effective companies living longer than would normally anticipate versus potentially more successful and profitable companies not growing as quickly as they would in ideal circumstances. I think it is not just the zombie story. Ben Broadbent has made this argument in a couple of the speeches that he has done, that you have a misallocation of capital that could show up both in the weak firms and in some potentially strongly contributing firms not being able to contribute as much as we would like.46

The Chancellor also argued that the problem should be seen as a wider one of capital mismatch:

I think there is no doubt that the recovery from a financial crisis, the likes of which we have not seen in this country in any of our lifetimes, is having all sorts of impacts out there in the economy. One of them, which is one of the things the OBR examines, is what happens on credit intermediation and whether it is preventing strong firms expanding because they get cannot get a loan, and also because of the very low interest rates allowing so-called zombie companies to continue. The only question I would raise is it is quite difficult sometimes to tell the difference between a zombie and a good company that is just having a difficult period because the economy is weaker than anyone hoped. I am absolutely clear that trying to clear up the credit intermediation channels and get the bank system functioning normally is probably the most important or certainly one of the most important tasks I face. But I do think this whole area is one that is worthy of greater consideration. I think we should all, including the Treasury, be doing more work on how the recovery from the financial crisis has taken longer than people had hoped and what is the impact on company and household balance sheets.47

43 Oral evidence to the Treasury Committee, National institute of Economic and Social Research quarterly review,

October 2012, taken on 13 November 2013, HC (2012-13) 750, Q 39

44 Oral evidence to the Treasury Committee, National institute of Economic and Social Research quarterly review, October 2012, taken on 13 November 2013, HC (2012-13) 750, Q 39

45 Q 22

46 Q 22

47 Q 291

16 Autumn Statement 2012

However, the Chancellor was not persuaded by the need for some firms to be shut to allow their resources to be used by other firms, so called ‘creative destruction’. He argued:

One of the things that we should welcome over the last couple of years, difficult as this period has been, has been the relatively strong performance of the job market and the fact that yesterday we had another fall in unemployment, another increase in employment. So those who advocate the sort of short, sharp shock that would lead to a load of companies closing and a lot of people being put out of work are not people that I would myself agree with. I don’t think that is what the British economy needs at the moment.48

The Governor of the Bank of England also warned that:

I do not like the phrase “zombie companies”. [...] the problem with the phrase “zombie companies” is that when we had downturns in the 1980s and 1990s, we were really worried that companies that did have a viable long-run future were being forced out of business because interest rates had gone up and they couldn’t get enough finance from the banks to tide them over their difficult circumstances. Now we seem to be worried about companies that ought to be forced out of business not being forced out of business because interest rates are too low.49

A bad bank?

27. Given the importance of bank lending to the real economy, and especially small firms, we explored a more radical solution to the problem loans on banks’ balance sheets: a so-called ‘bad bank’. A recent research note by BNP Paribas outlined what such a bank could achieve:

An approach we feel the UK should have had, and probably should still explore in more detail, is the creation of a ‘bad/run-off bank’ institution that could absorb problematic assets across the sector. This would allow smaller, more focussed (and better capitalised) institutions to lend to business where profitable opportunities exist. The bad bank could hold impaired assets and those targeted for disposal for much longer than a private-sector institution, thereby also limiting some of the downward pressure on asset prices from disposals.50

Mr Mortimer-Lee, of BNP Paribas, argued for such a solution:

It is not a bank; it is a management company. It looks just to manage those loans and it lets the residual good bank get on with looking for the opportunities for the future. In the UK we did exactly the opposite of this formula when with Lloyds we put the bad bank in with the good bank instead of taking the bad bank out and leaving a good bank.51

48 Q 292

49 Oral evidence taken before the Treasury Committee, Bank of England November 2012 Inflation Report, Tuesday 27 November 2012, HC (2012-13) 767, Q 94

50 BNP Paribas, UK: Capital offence, 18 October 2012

51 Q 125

Autumn Statement 2012 17

The Chancellor, however, noted that there was already a bad bank on the Government’s balance sheet, holding some of the assets of Bradford and Bingley and Northern Rock.52 He was sceptical of the case for a new ‘bad bank’:

Although there is a superficial—and I don’t mean that in a pejorative way—attractiveness to the bad bank/good bank idea, that is not the route that was pursued in 2008–09 when RBS was part-nationalised, and it was not the route pursued when HBOS was taken over by Lloyds. So I think the question four or five years later is do you go back into these banks, which have done a lot to shrink their bad assets and are continuing to do so, disrupt everything and try and rip out of RBS the bad assets, try and value them—which would take a long time, and the experience that the previous Government had of valuing assets with the Asset Protection Facility was not a particularly happy one—in order to achieve some gain in the future that you might have created this bad bank and taken these bad assets off RBS’ balance sheet, or indeed, the old HBOS assets. I think it is very, very disruptive and I am not sure the gains outweigh the disruption.53

Conclusions on bank lending

28. Exceptionally accommodative monetary policy and bank forbearance both provide support to companies at present and will have helped many companies to survive, supporting employment. But their effect will not be costless over the long-term. Some companies may remain trading when a more prudent examination of their business plan would suggest that they should not. Loans given to such companies may act to hamper banks’ ability to lend to new firms with better prospects.

29. The supply of corporate lending by the banks remains of significant concern, especially for smaller firms. We have heard evidence that the weakness of corporate lending may be hindering some firms from expanding.

Output gap

30. One of the key forecasts made by the OBR is that of the output gap. The output gap is defined as the difference between the potential output of the economy and the actual level of activity within the economy. When the output gap is negative, there is less activity than potential. The output gap is unobservable since the potential output of the economy is unmeasurable. It is simply an estimate based on the judgement of economists and is inherently extremely imprecise. Yet the output gap is used as a primary tool in assessing the success of the fiscal policy. The size of the output gap determines how much of the fiscal deficit at any given time is cyclical and how much structural: in other words, how much will disappear automatically, as the recovery boosts revenues and reduces spending, and how much will be left when economic activity has returned to its full potential. The narrower the output gap, the larger the proportion of the deficit that is structural and the less room for manoeuvre the Government will have against its fiscal mandate, which is set in structural terms (see paragraph 43). The output gap can also be used to assist with the assessment of the potential for inflationary pressure on prices if demand cannot be met at a

52 Q 293

53 Q 293

18 Autumn Statement 2012

given level of capacity. Chart 1 shows the forecast for the output gap, in comparison to that provided by the OBR in March 2012.

Chart 1: The output gap

Source: Office for Budget Responsibility, Economic and fiscal outlook December 2012, Chart 3.8, page 49

OBR’s change in method

31. Since the output gap is unobservable, estimating its current position and forecasting its future evolution is also inherently uncertain. In its December 2012 Economic and Fiscal Outlook forecasts, the OBR decided to use a different method for estimating the size of the output gap. Mr Chote explained why the OBR had decided to change from the forecast method used in March 2012:

Every time we come to do a forecast we look at the key judgments that we have to make and make the best central judgment that we can on the basis of the evidence we had. As you will recall, at your last gathering you were urging us to look at different ways of estimating the output gap, to come up with a richer picture than relying too heavily just on one method, looking at business surveys. We have looked at the method on business surveys, we have compared that to what that would imply if you were looking at a production function estimate of this, and we have concluded that it makes more sense to assume that the output gap is slightly larger now than a mechanistic application of that methodology was at the time. That makes 0.4% of GDP difference to the output gap, less than 0.3% of GDP difference to the structural budget deficit, and it is more than outweighed by the other fact going in the direction.54

However, Mr Mortimer-Lee disapproved of the change of method, and the consequential forecast by the OBR:

54 Q 48

Autumn Statement 2012 19

I do not like the fact that the OBR’s model said one thing and they decided to do something completely different. I do not like and I do not believe in the forecast of the sudden magical acceleration of productivity that means that the output gap stays wide despite growth picking up. To me it is just far too convenient for the Government finances.55

Mr Wells accepted that the OBR was entitled to change its method for estimating the output gap, though he questioned its judgement in certain respects:

The OBR have a usual set of models that on this occasion would have pointed to the output gap actually narrowing since March. In fact, they decided it was nearly a percentage point wider. But that is their judgment. I think you should always override a model if you don’t think what it is saying is sensible. But, yet again, I think it is the fact that they should have revised the potential growth rate down further and then the cyclically-adjusted fiscal position would have looked worse. They have applied that judgment, and at the moment it is impossible to know who is right. Certainly it would make things harder if they had assumed more of the recent weakness was due to potential rather than cyclical factors.56

Against the charge that the OBR had changed its methodology to appease the Chancellor, Mr Chote defended the OBR’s forecast as follows:

We have made an adjustment that says that the output gap is probably a little bit wider this year than our methodology would normally suggest but that is more than outweighed by a judgment move going in the opposite direction, which is that we think potential GDP is going to grow more slowly between now and the target date. So the judgments that we have made, rather than simply applying new data, make the Chancellor’s job more difficult and not less.57

A persistently large output gap

32. As Chart 1 shows, the OBR now forecasts a persistently large output gap. Mr Chote provided the following explanation as to why the OBR had made this forecast:

One is [this] story, a big output gap at the end. Ours is certainly larger than you would normally expect. It would be smaller than those people who say that we are overestimating the hit to supply from the financial crisis and so on, so there will be people further out in that particular direction. The other alternative is that you assume that economic growth is going to be a lot stronger over the next five years than we anticipate, which would close the output gap. Most people out there are not assuming that economic growth is going to be dramatically stronger than we assume, even those people who aren’t, like us, constrained to assume current policy and could therefore assume that there might be additional monetary or fiscal stimulus. The third possibility is that you believe that the financial crisis has dealt an even bigger hit to the supply potential of the economy than we are assuming but, as we have

55 Q 141

56 Q 103

57 Q 32

20 Autumn Statement 2012

discussed already, people are finding it hard enough to explain the hit to supply that most people think there is at the moment so adding even more to that would intensify that puzzle. The fourth possibility is that it is not the financial crisis per se that has hit the supply potential of the economy but that the trend growth in GDP was weaker prior to the crisis and people were consistently overestimating the potential growth of the GDP before it kicked off.58

Such a persistently large output gap may damage potential output. Mr Wells noted that:

Normally, economic theory would suggest that the longer a period of slow growth persists, the bigger the permanent damage to supply capacity. It is true that the UK labour market has been relatively resilient, with the result that productivity has hardly grown over the past few years. This suggests the loss of skills in the workforce may be more limited than history would suggest. But still, the OBR is once again assuming that all is well because in a few years we will be back to a world of low inflation and high growth.59

Mr Chote also acknowledged that the potential for damage from the persistently large output gap was “one of the reasons why [the OBR] have assumed that trend GDP growth does not recover right back to the long-term rate that you have seen over the past 50 years over that horizon.”60 This risk of potential degradation in potential supply was also referred to in the December minutes of the Monetary Policy Committee:

For one member, the case for undertaking additional asset purchases at this meeting was nonetheless strong. On balance, the near-term outlook for growth seemed a little weaker. Although inflation had risen again, and seemed unlikely to fall very substantially below the 2% target in the medium term, the degree of slack in the economy, and the likely response of supply capacity to increased demand, meant that it would be possible to achieve higher output growth without causing any material inflationary pressure. That would help to avoid potentially lasting destruction of productive capacity and increases in unemployment.61

33. The forecast of a persistently large output gap by the OBR should also have implications for monetary policy, as Mr Wells argued:

Given that the independent OBR now thinks there is considerably more slack in the economy than it did previously, it may also see a much stronger case for the independent MPC to apply more monetary stimulus. The bigger the output gap, the more scope there should be for monetary policy to boost demand without stoking inflationary pressure. [The OBR’s December 2012] forecasts therefore very much put the ball back in the BoE’s court to drive the recovery. Whether or not the MPC sees things the same way remains to be seen. Our reading of recent minutes lead us to

58 Q 41

59 HSBC, Saved by the cycle?, by Simon Wells, 5 December 2012

60 Q 55

61 Bank of England, Minutes of the Monetary Policy Committee meeting held on 5 and 6 December 2012. Published on 19 December 2012, para 30

Autumn Statement 2012 21

suspect it doesn’t. We could be heading for a blame game in policy, testing central bank independence further.62

Monetary policy

The effectiveness of Quantitative Easing

34. On 5 March 2009, the MPC voted for bank rate to fall by 0.5pp to 0.5%.63 Unwilling to lower interest rates further, the monetary policy tool most recently used by the MPC to stimulate demand has been purchases of assets, primarily gilts, financed by the issuance of central bank reserves: so called “quantitative easing” (QE). In November 2012, the minutes of the Monetary Policy Committee noted that “While views differed over the exact impact of the MPC’s asset purchases, the Committee agreed that demand and output would have been significantly weaker in their absence.”64 When asked how he thought QE had affected the economy, the Governor of the Bank of England replied that:

I would look at this simply through what has happened to the figures for broad money. In the absence of what we have done, I would have expected a contraction in broad money, and that would have taken us into very serious territory. I think that contractions of a significant size in the broad money stock are what led to the great depression in the United States in the 1930s, what has led to the equivalent in Greece today and would have threatened us—and indeed other countries—had we not expanded our balance sheet in the way that we did. I think other central banks have taken the same view, because the balance sheets of central banks have broadly expanded by roughly the same amount and using very similar types of instruments.65

Paul Fisher, Executive Director for Markets at the Bank of England, also argued that:

[...] in the two years in which we have done the most QE, 2009 and 2012, you have had record issuance of sterling corporate bonds. That is what you would expect, because as we take gilts out of the market, investors have to go and buy something else, and the demand for corporate bonds goes up. So you can see a very similar sort of impact in 2012 to what you had in 2009. Also, having been to the States, the evidence I have had there from market contacts is that QE, if anything, seems to be working more strongly now there than it did in the earlier phase through similar sorts of portfolio balance challenge.66

35. The November minutes of the MPC also discussed the likely effectiveness of additional asset purchases:

There remained considerable further scope for asset purchases to lower long-term yields on government and corporate debt and support other asset prices. Indeed, it

62 HSBC, Saved by the cycle?, by Simon Wells, 5 December 2012

63 Bank of England, Historical MPC voting spreadsheet, www.bankofengland.co.uk

64 Bank of England, Minutes of the Monetary Policy Committee, 7 and 8 November, published 21 November, para 36

65 Oral evidence taken before the Treasury Committee, Bank of England November 2012 Inflation Report, Tuesday 27 November 2012, HC (2012-13) 767, Q 25

66 Oral evidence taken before the Treasury Committee, Bank of England November 2012 Inflation Report, Tuesday 27 November 2012, HC (2012-13) 767, Q 25

22 Autumn Statement 2012

was possible that the impact of past asset purchases on asset prices had recently become greater. As market expectations of the likely duration of asset purchase programmes by central banks around the world had increased, so too had the incentives to amend investment strategies and reallocate portfolios towards riskier assets, such as corporate bonds and equities. But there was a question over the magnitude of the impact of lower yields and higher asset prices on the broader economy at the current juncture. It was not that asset purchases had become a fundamentally less effective policy tool, but rather it highlighted that the impact of any monetary policy instrument depended on the prevailing state of the economy. At the present time, it was possible that elevated uncertainty and a desire to reduce leverage meant that real activity was less responsive to lower borrowing costs than normal. But this situation could easily reverse, and with it the traction that lower yields could have in stimulating demand and output.67

When we asked the Governor whether he believed future rounds of QE would be as effective, he said:

What I would say is that it is a proposition that is not to do with asset purchases as such, but is to do with any aspect of monetary policy that we might engage in. The purpose of monetary policy in part is to persuade people to spend today what they might otherwise have spent tomorrow. You bring spending from the future to today. The longer time goes on, tomorrow turns into today, and by now has become yesterday. This means that you have a hole to fill that you have created, which you had hoped you wouldn’t need to fill because by now the economy would have picked up, and it hasn’t. I think it is not asset purchases as such that are less effective. We are still injecting more broad money into the economy. It is about the ability to persuade people to spend more today when they know that in the long run—which cannot be deferred indefinitely—they will have to adjust to a new equilibrium.68

36. Our City experts were sure QE had reduced in effectiveness. Mr Hayes, Barlcays, told us that:

I think it has lost a lot of traction. I thought that was true over a year ago when they did QE2 in October last year, and I think it is probably even more the case now. This is not particularly to do with its capacity to keep Government bond yields low, for which I think it still is an important factor, but the extent to which that feeds through into actual spending by consumers and firms is very difficult to design indeed. If the Bank of England announces another £50 billion of QE, I would not rush away and significantly revise our growth and inflation forecasts because of that.69

Mr Wells, HSBC, when asked whether the Bank should undertake another analysis on how well QE was working, replied that “I think it becomes harder and harder, because as quantitative easing comes into market expectations the market tends to react in advance. Therefore, on the day of the announcement it is largely in the price, so the sort of event

67 Bank of England, Minutes of the Monetary Policy Committee, 7 and 8 November, published 21 November, para 36

68 Oral evidence taken before the Treasury Committee, Bank of England November 2012 Inflation Report, Tuesday 27 November 2012, HC (2012-13) 767, Q 25

69 Q 129

Autumn Statement 2012 23

study that they did in the past I think becomes little bit more irrelevant”. On the effectiveness of QE, he agreed with Mr Hayes, and argued that:

is another £50 billion of gilt purchases from the Bank of England going to suddenly drive us to growth? I think that is very unlikely. Quantitative easing was a great response, an unprecedented response to an unprecedented policy outlook in 2009. It did its job. It avoided a depression, it avoided deflation, but we can’t expect more and more money creation from the Bank of England just to fine-tune the economy and drive growth.70

Mr Mortimer-Lee, BNP Paribas, believed that the current QE policy was subject to diminishing returns.71 He advocated a different sort of quantitative easing:

I think, to be honest, we have the wrong sort of QE. In the US when the Fed buys treasuries and lowers the Government bond yield it has a significant effect on the ability of the corporate sector to borrow because a lot of the intermediation is not through banks, it is through the bond market. In the UK that is exactly the opposite. The banks are the main sort of intermediation, and really the Bank of England has made the Government’s job a lot easier. It may initially have helped the economy, but in the recent rounds it clearly has not helped the private sector’s availability to credit. I would love to see them switch to buying, as the Fed has been doing. The most recent round of QE is to buy mortgage-backed securities, and I think the Bank of England should do exactly the same thing, because our problem is credit availability. The Bank could buy packages of corporate loans, but, to be honest, there is a danger of them being given lemons by the banks because there is an asymmetric information problem. With mortgages it is a much more homogenous asset. If the Bank were to take on mortgage-backed securities, that would allow the banks more room, given their capital constraints, to lend to businesses. I think that would be much more helpful than QE in gilts.72

37. NIESR also believed that there was a case for the Bank of England to widen its purchases beyond gilts:

If a further expansion of the Bank’s balance sheet were to occur in the short term, then it would surely be because the MPC feels that lending to the real economy remains impaired. Rather than just purchase gilts in an attempt to flatten the yield curve, purchases would be more effective in raising nominal spending if they were of private sector paper (see Barrell and Holland, 2010).73

Bill Winters, who conducted a review on behalf of the Bank of England into its framework for providing liquidity to the banking system, set out possible additional monetary tools:

At present, the MPC uses only the two tools of Bank Rate and asset purchases to meet its inflation target. It is, however, possible that at some time in future the MPC

70 Q 130

71 Q 134

72 Q 134

73 NIESR, National Institute Economic Review, Prospects for The UK Economy, by Simon Kirby and Katerina Lisenkova, October 2012, p F44

24 Autumn Statement 2012

might wish the Bank to use other types of market operations to enable it to meet its objective, either if it thought the current tools were impaired for some reason, or because it thought some other tool would be more effective. A range of options are theoretically possible including: other types of asset purchases; setting Bank Rate below zero; tiered remuneration on reserves; and using long-term repos to influence longer term rates. Although the operational details would need to be worked out at the time, it appears that the SMF framework itself is sufficiently flexible to accommodate such additional policy measures.74

The Monetary Policy Committee itself discussed the possible use of other tools in May 2012, shortly before the Funding for Lending scheme and the Extended Collateral Term Repo Facility were announced:

Other complementary policy measures that the authorities might take could be better suited to mitigating these problems than asset purchases on their own, and some members expressed a wish for the MPC to consider additional policy tools. In this context, the Governor informed the Committee that initial discussions were underway with the Treasury on possible measures to ease banks’ funding costs and enhance their ability to lend.75

38. The evidence received suggests that quantitative easing was an appropriate response at the start of the financial crisis. As time goes on, its effectiveness may be diminishing. Some, including members of the MPC, have argued that the Bank of England should consider pursuing alternative forms of monetary easing. The Treasury Committee will be holding a detailed inquiry into quantitative easing in the coming months.

Monetary policy framework

39. The United Kingdom operates a monetary policy regime centred on an inflation target of 2% as measured by the Consumer Price Index, implemented by the independent the Bank of England. In a recent speech in Toronto, Dr Mark Carney, the Governor of the Bank of Canada and the Government’s choice as the next Governor of the Bank of England, discussed potential reforms to monetary policy frameworks. In particular, he noted that:

when policy rates are stuck at the zero lower bound, there could be a more favourable case for NGDP [Nominal GDP] targeting. The exceptional nature of the situation, and the magnitude of the gaps involved, could make such a policy more credible and easier to understand.76

40. While the decisions on, and implementation of, monetary policy are undertaken by the Bank of England, the remit is decided by the Chancellor of the Exchequer. Given the Chancellor’s announcement that Dr Carney would replace Sir Mervyn King as Governor

74 Bank of England, Review of the Bank of England’s framework for providing liquidity to the banking system, Report

by Bill Winters, Presented to the Court of the Bank of England October 2012, pp45-46, para 144

75 Bank of England, Minutes of the Monetary Policy Committee meeting 6 and 7 June 2012, para 31

76 Bank of Canada, Remarks - Mark Carney, Governor of the Bank of Canada, Presented to: CFA Society Toronto, Toronto, Ontario, Canada, 11 December 2012

Autumn Statement 2012 25

of the Bank of England in 2013, we discussed with the Chancellor the potential for a change in the monetary policy remit in the United Kingdom. He said that:

[...] we have an inflation targeting regime that has served this country well and has provided stability. There is a debate about the future of monetary policy, not in the UK exclusively, but in many, many countries. You saw yesterday the Federal Reserve take action on indicating the future path for monetary policy and linking it to the unemployment rate, so there is a lot of innovative stuff happening around the world. In the UK, we have the Funding for Lending scheme, which in itself has been very innovative, and other countries have looked at it closely. So there is a debate going on. I am glad that the future Central Bank Governor of the United Kingdom is part of that debate. Of course any decisions about the framework are decisions for the Government”.77

He added “I have no plans to change the framework”.78

41. As part of our hearing on 7 February 2013 with the new Governor of the Bank of England, we will examine whether Dr Carney considers that the current monetary policy of the Bank of England remains the most appropriate. We would welcome written evidence on this from others prior to that hearing.

77 Q 274

78 Q 277

26 Autumn Statement 2012

3 The public finances

Changes announced in the Autumn Statement

42. The impact of measures announced in the Autumn Statement is summarised below. The Government estimates the fiscal impact to be savings of £3.97 billion in 2012–13, with an increase in spending over receipts of £910 million in 2013–14. Over the forecast period, the net impact is a saving of £6.47 billion.

Table 2: Overall fiscal impact of Autumn Statement measures

£ million

2012–13 2013–14 2014–15 2015–16 2016–17 2017–18

Total tax policy decisions -870 +180 -2,385 -905 +295 +305

Total spending policy decisions +4,840 -1,090 +1,465 - - +4,635

TOTAL POLICY DECISIONS +3,970 -910 -920 -905 +295 +4,940 Source: HM Treasury, Autumn Statement 2012, 5 December 2012, Table 1, p 9

Performance against the fiscal targets

The fiscal mandate

43. The OBR is responsible for assessing the Government’s performance against the fiscal mandate and the supplementary target:

The Charter for Budget Responsibility defines the fiscal mandate as “a forward-looking target to achieve cyclically-adjusted current balance by the end of the rolling, five-year forecast period”. This means that total public sector receipts need to at least equal total public sector spending (minus spending on net investment) in five years time, after adjusting for the impact of any remaining spare capacity in the economy. For the purposes of this forecast and the spring 2013 EFO [Economic and fiscal outlook], the five-year horizon ends in 2017-18.

The Charter says that the supplementary target requires “public sector net debt as a percentage of GDP to be falling at a fixed date of 2015–16, ensuring the public finances are restored to a sustainable path.” The target refers to public sector net debt (PSND) excluding the temporary effects of financial interventions.79

44. The OBR stated in its December 2012 Economic and fiscal outlook that there was a greater than 50 per cent chance of the Government meeting the fiscal mandate, albeit by virtue of extending austerity measures a further year into 2016–17. The cyclically-adjusted current budget was forecast to be in surplus by 0.9 per cent of GDP in 2017–18—the current target year for the purposes of the mandate—and by 0.4 per cent in 2016–17.80

79 Office for Budget Responsibility, Economic and fiscal outlook, December 2012, p 173

80 Office for Budget Responsibility, Economic and fiscal outlook, December 2012, p 18

Autumn Statement 2012 27

The supplementary target

45. The OBR forecast that the Government is unlikely to meet its supplementary target. Public sector net debt (PSND) is forecast to rise by 1 per cent of GDP in 2015–16 and then fall by 0.8 per cent in 2017–18, thereby missing the target by one year. The OBR had forecast that the target would be met in its March 2012 EFO, but has since revised down nominal GDP growth, revised upwards net borrowing and factored in the effect of reclassifying Bradford and Bingley and Northern Rock Asset Management as public sector liabilities. The effects of these revisions are offset to a degree by the transfer to the Treasury of the surplus balance in the Bank of England’s Asset Purchase Facility (APF).81

46. The Government has chosen not to implement further cuts in order to meet the supplementary target. The Chancellor effectively acknowledged that doing so could harm the economy. He stated that:

one of the central judgments of this Autumn Statement was not to chase the debt target, in other words, to accept that we had missed the debt target, and had we chased the debt target, that would have required significant cuts or tax rises over the next couple of years.82

[…]

[…] faced with this choice—hit the target and potentially damage the economy in doing so, or miss the target and help the economy—I decided to help the economy.83

The Autumn Statement says that:

At this time of rising debt, the Government will restore debt to a sustainable, downward path and will retain the existing supplementary debt target. As set out in the June Budget 2012, the Government will set a new target once the exceptional rise in debt has been addressed.84

47. Mr Mortimer-Lee stated that the existence of a fiscal framework was in principle valuable but that:

[t]he fiscal framework should be a guide to action and should constrain the Government’s ability to come up with policies that suit the short term but not the long term. The rule helps to achieve that but it is not set in stone. We don’t fall off the end of the earth if we go past it.85

48. The Government is forecast to meet the rolling fiscal mandate by cutting non-investment spending as a share of GDP for a further year, but not the supplementary target. It has decided not to propose further spending cuts or tax rises in order to meet the latter. The possible failure to meet the supplementary target raises the question of the continuing credibility of that target. Successive governments have committed

81 Office for Budget Responsibility, Economic and fiscal outlook, December 2012, p 18

82 Q 290

83 Q 311

84 HM Treasury, Autumn Statement 2012, 5 December 2012, p 31

85 Q 141

28 Autumn Statement 2012

themselves to, but then failed to meet, their fiscal targets. For a fiscal target to be credible, it must be durable, and therefore not subject to frequent revision as circumstances change. It must also be capable of accommodating conditions different from those at the time the target was first formulated. Nor should a fiscal target be open to manipulation. It is not the case, though, that a target is valuable only so long as it is met. A target can remain credible, and so constrain a government’s choices, even if it is not being met, so long as the political commitment that created it continues to inform policy decisions.

49. The supplementary target remains in place for the moment. The Government has said that it will set a new target, but its timetable is vague: it will do so “once the exceptional rise in debt has been addressed”. When the Government does decide to create a new fiscal framework, it should do so only after full public consultation. The Committee will return to this issue.

Credit rating

50. We questioned witnesses on the likelihood and impact of a downgrade of the UK’s AAA credit rating. Mr Hayes and Professor Booth both thought that a downgrade was likely.86 Mr Hayes, when asked if there would be a downgrade in 2013, replied:

I think it is quite likely. There are two reviews coming up that we know of. Early in the year, probably January, Moody’s is looking to revisit this, and in March I think Fitch are looking to review also. In particular as I understand it with Fitch, we are on negative outlook, and on their criteria that implies more than a 50% chance of a downgrade. That was instigated in February this year, I think, since when things have got worse. So it seems to me that things are moving clearly in that direction,87

51. As to the potential impact of such a downgrade, both Professor Booth and Mr Johnson stated that the rating agencies based their decisions on the same information available to the broader market and that therefore any expectations of a downgrade would already be priced into the cost of UK debt.88 Mr Hayes noted that France did not appear to have suffered material rises in borrowing costs following the downgrades of its sovereign debt. Mr Hayes stated that “the likelihood of a leap in bond yields from a rating downgrade is negligible.”89