Hotels Quarterly Update - htlproperty.com.au · The more notable hotel sales were Helensvale Tavern...

6

P1 Hotels Quarterly Update Quarter 3, 2013 Market Perspectives and Commentaries - Hotel and Leisure Industry RWH QLD UPDATE Yield Perception By Tony Bargwanna Time to Buy in QLD? By Sean Dollar New to the RWH QLD Team Nic Simarro and Harrison Hall N.T & Western QLD Update By Brenton McCarthy Campaign vs Private Treaty By Leon Alaban QLD Property Profile By Christian Tsalikis RWH NSW UPDATE Investor Confidence Returns By Andrew Joliffe The Election & Australian Property Markets By Blake Edwards Gaming Machine Activity in NSW By Nick Maclean Commercial Accommodation Snapshot By Max Cooper Highlights Welcome to the third issue of the Ray White Hotels (RWH) Australia newsletter. Each quarter interviews with Australia’s leading brokers, advisors, valuers and clients will provide you with their current perspectives on topical issues and the latest in market trends. This edition focuses on the future property market and gaming machine trends, predictions post the federal election and recommended selling methods. Ray White Network is the largest residential based agency in Australasia with just under 1000 franchises and over 10,000 employees in 11 countries. They continue to expand throughout Australia, New Zealand, Asia and the Middle East. Ray White Hotels Australia is a member of the Ray White Network and provides specialist sales expertise in Hotel Real Estate. Established in 2010, they have transacted over 75 properties, in excess of $800 million Hotel, Pub, Motel and Leisure assets. Ray White Advisory is wholly owned by Ray White Real Estate Pty Limited and provides specialist Valuation, Strategic Consulting and Research services for Hotel and Leisure property. They offer professional market advice to investors, financers, owners and operators. For further information please contact: Brisbane office Level 7, 123 Eagle Street Brisbane QLD 4000 P: 61 07 3046 4300 Sydney office Level 17/135 King Street Sydney NSW 2000 P: 61 02 8016 3810 www.raywhitehotels.com.au Yield Perception For the first time in 5 years, our property sector may be experi- encing yield compression. Why? Tony Bargwanna, Managing Director, RWH Australia, attributes this to the “drying up” of quality stock/listings at a time when buyer numbers are increasing and banks are providing debt again. “Recent sales including Waterloo Bay Tavern, Mission Beach Hotel Mo- tel & Resort and Helensvale Tavern are good examples whereby there was strong competition for the assets with not a lot of other options for buyers to consider”, Bargwanna reveals. “And with regards to invest- ment stock, in particular ALH and Spirit Hotels tenanted assets, a feeling of “missing the boat” is definitely out there in buyer’s minds”. Currently, RWH have at least six sophisticated investor groups, both institutional and private, searching for this exact asset class. “If I were to be bold enough to nominate some yield ranges for such generic assets like these, I would say quality freehold going concerns with gaming and in need of little capital expenditure in a strong demographic, will achieve 10.5% to 12.5% yield range”, states Bargwanna. “Passive investment product, with Spirit Hotels and/or ALH as a tenant, is categorically sub- 8% now”, he says. Factors that may impact these yields are limited to price point, post code and compliance. Bargwanna believes that although buyers are very educated and conduct thorough due diligence today, they will tighten up their yield expectation for the right asset. Industry reports maintain the commercial property market is in the early stages of a multi- year cyclical upswing with rents set to rise strongly and yields to compress. Tight vacancies, limited capacity expansion and attractive yields will support growing investor interest and are laying the groundwork for a marked increase in valuations as rents rise and yields compress. Moreover, current yields belie the positive fundamentals and are expected to firm, offering further upside to capital values. Despite the strength of the Australian dollar, offshore investor interest in Australian prop- erty remains strong. Favourable pricing and property fundamentals in Australia are in stark contrast to the situation in much of the developed world and will continue to attract foreign capital. However, the outlook is not without risk. Considerable global uncertainties threaten economic and financial market stability and will continue to weigh on investor sentiment and property yields. To finish, Bargwanna also highlights the resurgence of interest in the 3-4 star accommoda- tion market. “Once again I predict yield compression in this sector”, he states, “due to lack of quality product and affordable debt. These two factors are the major contributors to a declining yield”. Tony Bargwanna, Managing Director, RWH Australia RWH is pleased to direct you to their new website. See all the up to date property information from around Australia at www.raywhitehotels.com.au.

Transcript of Hotels Quarterly Update - htlproperty.com.au · The more notable hotel sales were Helensvale Tavern...

P1

Hotels Quarterly UpdateQuarter 3, 2013 Market Perspectives and Commentaries - Hotel and Leisure Industry

RWH QLD UPDATE Yield PerceptionBy Tony BargwannaTime to Buy in QLD?By Sean DollarNew to the RWH QLD Team Nic Simarro and Harrison HallN.T & Western QLD UpdateBy Brenton McCarthyCampaign vs Private TreatyBy Leon AlabanQLD Property ProfileBy Christian Tsalikis

RWH NSW UPDATE Investor Confidence Returns By Andrew JoliffeThe Election & Australian Property MarketsBy Blake EdwardsGaming Machine Activity in NSW By Nick MacleanCommercial Accommodation SnapshotBy Max Cooper

Highlights Welcome to the third issue of the Ray White Hotels (RWH) Australia newsletter.

Each quarter interviews with Australia’s leading brokers, advisors, valuers and clients will provide you with their current perspectives on topical issues and the latest in market trends. This edition focuses on the future property market and gaming machine trends, predictions post the federal election and recommended selling methods.

Ray White Network is the largest residential based agency in Australasia with just under 1000 franchises and over 10,000 employees in 11 countries. They continue to expand throughout Australia, New Zealand, Asia and the Middle East.

Ray White Hotels Australia is a member of the Ray White Network and provides specialist sales expertise in Hotel Real Estate. Established in 2010, they have transacted over 75 properties, in excess of $800 million Hotel, Pub, Motel and Leisure assets.

Ray White Advisory is wholly owned by Ray White Real Estate Pty Limited and provides specialist Valuation, Strategic Consulting and Research services for Hotel and Leisure property. They offer professional market advice to investors, financers, owners and operators.

For further information pleasecontact:Brisbane officeLevel 7, 123 Eagle StreetBrisbane QLD 4000P: 61 07 3046 4300

Sydney officeLevel 17/135 King StreetSydney NSW 2000P: 61 02 8016 3810

www.raywhitehotels.com.au

Yield PerceptionFor the first time in 5 years, our property sector may be experi-encing yield compression. Why?

Tony Bargwanna, Managing Director, RWH Australia, attributes this to the “drying up” of quality stock/listings at a time when buyer numbers are increasing and banks are providing debt again.

“Recent sales including Waterloo Bay Tavern, Mission Beach Hotel Mo-tel & Resort and Helensvale Tavern are good examples whereby there was strong competition for the assets with not a lot of other options for buyers to consider”, Bargwanna reveals. “And with regards to invest-ment stock, in particular ALH and Spirit Hotels tenanted assets, a feeling of “missing the boat” is definitely out there in buyer’s minds”.

Currently, RWH have at least six sophisticated investor groups, both institutional and private, searching for this exact asset class. “If I were to be bold enough to nominate some yield ranges for such generic assets like these, I would say quality freehold going concerns with gaming and in need of little capital expenditure in a strong demographic, will achieve 10.5% to 12.5% yield range”, states Bargwanna.

“Passive investment product, with Spirit Hotels and/or ALH as a tenant, is categorically sub-8% now”, he says. Factors that may impact these yields are limited to price point, post code and compliance. Bargwanna believes that although buyers are very educated and conduct thorough due diligence today, they will tighten up their yield expectation for the right asset.

Industry reports maintain the commercial property market is in the early stages of a multi-year cyclical upswing with rents set to rise strongly and yields to compress. Tight vacancies, limited capacity expansion and attractive yields will support growing investor interest and are laying the groundwork for a marked increase in valuations as rents rise and yields compress. Moreover, current yields belie the positive fundamentals and are expected to firm, offering further upside to capital values.

Despite the strength of the Australian dollar, offshore investor interest in Australian prop-erty remains strong. Favourable pricing and property fundamentals in Australia are in stark contrast to the situation in much of the developed world and will continue to attract foreign capital. However, the outlook is not without risk. Considerable global uncertainties threaten economic and financial market stability and will continue to weigh on investor sentiment and property yields.

To finish, Bargwanna also highlights the resurgence of interest in the 3-4 star accommoda-tion market. “Once again I predict yield compression in this sector”, he states, “due to lack of quality product and affordable debt. These two factors are the major contributors to a declining yield”.

P7

Activity in the HunterThe Hunter Valley is one of the largest regional markets in Australia.

It enjoys a multi-faceted and thriving economy driven by tourism, the wine industry, mining, live entertainment, horse breeding and agriculture. Newcastle, the commercial hub for the region, is the second most populated city in New South Wales accounting for approximately 308,000 of the region’s 620,000 residents.

In 1999, Newcastle experienced a setback with the closure of the BHP steel works after 84 years

in operation. After employing approximately 50,000 people for many decades, the regional economy was forced to diversify as a result of the closure.

The Newcastle and wider Hunter economy has strengthened over the past decade as a result of this diversification and unemployment is at 20 year lows. The Federal Government has shown its commitment to the region with the $1.5 billion infrastructure project, The Hunter Expressway.This 40 kilometre, 4 lane expressway will greatly reduce travel time to the lower and upper Hunter Valley from both Sydney and Newcastle.

With construction due for completion in late 2013, the Hunter Expressway will generate further growth in the area. Significant residential development projects in the Lower Hunter are already under construction with a view to profit from the burgeoning population. Likewise the entertainment, hospitality and leisure industry in the area are likely to benefit from an increase in visitor numbers to the area.

‘Market fundamentals, the diverse economy and projected growth makes Newcastle and the wider Hunter Region an appealing market to those looking to invest in quality hotel and accommodation assets’, believes Nick Maclean, Hotel Sales Executive, Ray White NSW whom specialises in this region.

The Lower Hunter Valleys wineries, golf courses, restaurants, various types of accommodation (from luxury boutique to budget accommodation) and its proximity to Sydney and Newcastle attract approximately 2.3 million tourists to the region annually.

Recent transactions successfully managed by Ray White Hotels include The Honeysuckle Hotel on Newcastle Wharf (sold July 2012) and a 33 Unit Accommodation Development in Pokolbin, in the Lower Hunter Valley’s wine region (sold April 2013).

Currently listed for sale exclusively with Ray White Hotels is The Australia Hotel and Motel, Cessnock. This hotel caters to tourists, transient workers and the growing local residential population.

The Australia is capitalising on the aforementioned market conditions and this is reflected in strong earninings, with an annual turnover of approximately $3.5 million and its multiple revenue streams of accommodation, bar sales, food and poker machines. The Australia Hotel and Motel presents a compelling opportunity for buyers seeking A-Grade hotel assets in this region.

Other recent transactions in the Lower Hunter Valley include the 17 room Peppers Convent which sold for $6 million (November, 2010) and the Crowne Plaza Hunter Valley for $45 million (September, 2012).

Nick Maclean

The Australia Hotel and Motel, Cessnock. Currently exclusively listed for sale with RWH

The Honeysuckle Hotel on Newcastle Harbour. Successfully sold by RWH in July 2012

THE HUNTER VALLEY IS ONE OF THE LARGEST REGIONAL MARKETS IN AUSTRALIA

33 Unit Accommodation Development in Pokolbin, Lower Hunter Valley Wine Country.Successfully sold by RWH April, 2013

Tony Bargwanna, Managing Director, RWH Australia

RWH is pleased to direct you to their new website. See all the up to date property information from around Australia at www.raywhitehotels.com.au.

WELCOME

NEW TO THE RWH QLD TEAM

HARRISON HALL - ANALYST

Harrison Hall joined Ray White Hotels (RWH) in May 2013 as Junior Analyst supporting the RWH Brisbane Team.

One of the new breed of young professionals, Harrison is starting to build his career in real es-tate underpinned by a Bachelor of Property and Sustainable Development with a major in Urban Development and Property Development. His studies give him innovative and practical industry

relevant knowledge which he applies daily in his role.

Harrison’s experience is evolving through his multiple roles in all aspects of sales and property and, most notably, is fueled by his love of the industry and unmatched ambition. He is developing a strong track record for achiev-ing solid results thanks to his respect for clients and his open, hardworking and communicative approach.

“I’m excited about the opportunity RWH has given me”, Harrison says. “To work alongside industry leaders gives me exposure to an extensive knowl-edge pool and allows me the opportunity to be part of a diverse and rapidly expanding team”.

NIC SIMARRO - INVESTMENT SALES EXECUTIVE

After 5 years with Ray White Residential, RWH Australia proudly welcomes Nic Simarro into their sales team as Investment Sales Executive.

Nic has acquired extensive real estate experi-ence across the board, from property manage-ment to leasing to sales and marketing. His ca-reer commenced offshore in NYC with 3 years for a New York Realtor before returning to Australia in 2008. Moving from a smaller agency in 2009 Nic’s career boomed when he was exposed to the opportunities that Ray White offers.

Nic has developed a diverse understanding of the market whether he is talking to an owner occupier or investor. An astute reader of people, Nic is renowned for his ability to monitor and modify marketing campaigns to ensure their success. His most prominent sale, and the fourth larg-est residential sale in 2012, was the renowned heritage listed Brisbane landmark residential dwelling on the cliffs at Kangaroo Point, which sold for $4.3million.

When you ask Nic what he values most about his role in sales he nomi-nates his ability to meet and serve members of his community. “It’s my privilege to assist people with their property needs,”Nic says, “I’m ap-proachable, a good listener and always available for clients”.

Nic’s strength is his dedicated and daily service to vendors as well as his easy going personality mixed with his motivation to achieve the very best outcomes and results for his clients. Known for his dynamism, integrity and client-first ethos, Nic is an excellent professional fit for the RWH sales team.

P2

Time to Buy in Queensland?

After 20+years of high level involvement in the Qld pub and hospitality industry in the finance and banking sectors, Sean Dollar, Director of Sales and Business Development for RWH Australia, believes the current market conditions are as good as they have been since September 2008 for buyers considering a “re-entry” into the market. “The Queensland pub industry in 2013 has definitely turned the corner for the first time post GFC with forward growth opportunities for the sector looking prosperous”, Dollar discloses.

“The low interest rate environment now and in the short and medium term, plus a proactive Qld Government re-ducing the regulatory requirement for hotel businesses are influencing factors contributing to the positive future prospects”, he claims, “And of course, with the federal election around the corner, confidence will return to the market in general.”

Dollar also credits a level of uncertainty has been removed with the Gillard/Wilkie pokie machine war and the price of poker machine au-thorities being at an all time low (and predicted to go up due to lack of future supply).

Fiscal year 2012/2013 saw 26 going concern hotels in Queensland (Qld) change hands, the lowest quantity of sales in Qld for some years. The more notable hotel sales were Helensvale Tavern (Gold Coast), The Waterloo Bay Hotel (Wynnum), the lease of the Envy Hotel (Broadbeach), The Sarina Hotel Motel, Blacks Beach Tavern (Mackay) and the Mission Beach Hotel (North Qld).

Receivership/ mortgagee in possession sales are still trickling through the banking sector but at a reduced rate over the last 6-9 months compared to 3-4 years prior.

“Buyers have returned to the market but remain cautious”, Dollar dis-closes. “We expect this to continue as potential buyers are conduct-ing robust and meaningful due diligence on acquisitions.”

From a sellers prospective its imperative to provide meaningful, ac-curate and up to date financial information when taking your hotel to market. He goes onto say “If buyers are not provided with accurate profit and loss statements broken down on a month by month, de-partment by department basis, they are simply moving onto the next opportunity.”

Dollar supports this professional approach. “Buyers are certainly not paying for “blue sky”, nor are they taking into account or paying for upside”, he says. “Generally buyers are determining value or an ac-quisition price based on the hotels EBITDAR over the last 12 months capped out at a realistic market multiple (yield).”

Liquidity has returned to the market in the last 6-9 months and buyer enquiry level has significantly increased over the same period com-pared to same time last year. Buyer enquiry for freehold investment hotels is also firm driven by low interest rate environment with strength of tenant being the key driver. Pubs with a national tenancy profile are highly sought after.

And so from the sellers perspective, RWH believe the next 6 months provides good opportunities for sellers to take their hotel to market. “There is a noticeable lack of stock (hotels for sale) in the market at present”, Dollar highlights,”and overall (depending on each individual sellers circumstances) our view is that the auction process remains the best sale method in today’s market for sellers to create a competi-tive process for the sale of their asset”.

Why? The auction process gives sellers the opportunity to sell their property for the highest possible price in today’s market (whatever that price may be) and gives a seller “certainty” in terms of a contract being not subject to finance or onerous terms and conditions.

Other sale methods such as Expressions of Interest (EOI’s) and Ten-ders, RWH are finding, over the last 6-12 months, they are not de-livering the same results as auctions. Some sellers are committing their hotel to multiple agents and searching for results in an off market type scenario. Any sale on this basis is difficult to achieve in today’s environment.

“For sellers, its important to pick one sales agent, commit to a formal and professional sales process inclusive of a full marketing campaign, to ensure your hotel is given the best chance to sell for the maximum price in today’s environment, “ Dollar explains.

In the current environment with sellers across the state, Dollar hears consistently “Sean it cost me a lot more than its worth now”, “the fig-ures don’t quite show what it should be making”, “I paid significantly more for the hotel 5 years ago”.

Dollars responds. “Remember buyers are assessing value based pri-marily on the hotels last 12 months profitability, not what may or may not happen in the future”. He says, “The old saying goes, “cost does not necessarily equal value in today’s market... any hotel is worth what an arms length buyer is prepared to pay in today’s market, not what it cost, not what a seller may have paid for it and perhaps not what a valuer valued the hotel at some 6 or 12 months ago.

Sean Dollar

P3

Update on NT and Western QLDAfter recently attending the N.T Hotels Association annual conference in May, Brenton McCarthy, Hotel Sales Executive, N.T and Western Qld came away with a positive future outlook for the N.T tourism sector.

The N.T is showing strong growth in the accom-modation sector, as demand is far outweighing supply. “RWH sees this as an exciting time for

operators wanting to move in and capitalise on the strong growth within the state”, McCarthy highlights. “The demands are being pushed by strong tourism numbers and the growth that continues to come from the resource sector which is boosting the N.T economy”.

Pubs and clubs in the N.T are also showing signs of a strengthen-ing market as trade continues to grow thanks to tourism progress and the gas and mining expansion. “There are whispers of legislation changes with the Territory Gaming Regulations”, McCarthy suggests, “which should see some real results within this sector over the com-ing months”.

Campaign vs Private Treaty?Are you better off selling via campaign (auc-tion, expression of interest, tender) or private treaty (listing with a price)? This is the question Leon Alaban, Director of Investment Sales Queensland RWH Australia puts forward for discussion in this edition.

“All methods of sale have worked effectively for sellers for many years,” says Alaban, “however what we are experiencing in today’s current mar-ket is that taking your property via a campaign process is a far more beneficial sales method for sellers”.

“A sale by public auction is arguably one of the most exciting, effective and rewarding methods of buying and selling a property,” Alaban ex-plains, “But most importantly, the benefits of a Campaign far outweigh those when you list your asset for a price, ie: private treaty”.

Some positives of the auction campaign process are (1) it encourages competitive bidding, which means there is no price barrier and (2) by its very nature an auction creates a sense of urgency where buyers have a definite time frame in which they must act. For the seller, they have (1) the ability to set a reserve price and a settlement date that suits and (2) a written marketing plan with a fully disclosed advertis-ing schedule and pre-agreed appointment times enabling them to ar-range their lives during the lead up period.

“From the buyers perspective, a campaign focuses their actions”, Ala-ban clarifies, “From the sellers perspective, a deadline creates pres-sure and competition which opens up the opportunity to sell their property for the highest possible price in today’s market”. He also mentions that a private treaty generally takes longer to sell compared to an auction campaign (or any type of campaign for that matter) as sellers tend to benefit from a focused commitment from agents when marketing via a campaign.

Alaban also highlights the main point of difference with both an ex-pression of interest and tender campaign when compared to an auc-tion is that these processes provide buyers with flexibility. The flex-ibility (allowing conditions to be imposed) provided to buyers generally provides for a larger group of interested parties expressing their inter-est in the property.

“Whilst the campaign process is far more expensive than a private treaty, due to a commitment of undertaking an advertising campaign, the payback is worth it. Undertaking a campaign to market your as-set shouldn’t be seen as an expense but as an investment!” Alaban explains.

“When sellers undertake a campaign, they are looking for a result. Campaigns are usually a 4-6 week process”, Leon explains, “with the first 4 weeks encompassing an advertising schedule followed by 1-2 weeks for the close date. Our expertise is in developing a strategic marketing and advertising plan with the client, creating the right mes-sage then strategically positioning advertisements in the right market-ing mediums, to target the right market”.

Whilst the digital space and all electronic channels and databases are utilised in the marketing plan, Alaban also sees great value in the print medium. “We are still receiving up to 30% of enquiry through our print advertisements”, he states. “We strategically place the ads, with the right frequency, in the right publications, achieving the awareness for the asset within the right market which stimulates potential buyers call to action”. Refer to Graph 1 below showing the breakdown of enquiry to a recent Marketing Campaign which was met with strong interest.

Alaban finishes with “We consider all of our client’s situations on a case-by-case basis but we are finding campaigns to be producing a far greater outcome for the seller when compared to a Private Treaty”.

RWH Recent Property Marketing Campaign Enquiry Channel Breakdown

The data drawn from this campaign clearly suggests that when selling a property, the external marketing channels (print media and electronic me-dia) are still generating a large percentage of enquiries. From those enquiries there is a large percentage of prospective buyers which are engaging in the process by submitting formal written offers.

Brenton McCarthy

Leon Alaban

Chart 1: Illustrates the amount of enquiries as a percentage generated from each marketing channel.

Chart 2: Illustrates which marketing channel generated formal written offers as a percentage.

QLD Property Profile Q&A with the GM of the Bracken Ridge Tavern

With his recent appointment to Investment Sales, Christian Tsalikis, Cadet Hotel Sales Execu-tive for Ray White Hotels QLD has been active-ly pursuing new property listings. He recently met with his mentor Ben White, General Manager and Director of The Bracken Ridge Tavern, to discuss industry insights and property prospects.

The family owned entertainment precinct, Brack-en Ridge Tavern, is one of the biggest and more popular venues on Brisbane’s northside. Now a

well established brand, they enjoy strong patronage thanks to their ongoing growth and evolution of multiple dining and entertainment offerings including bars, restaurants and function facilities catering to different tastes and budgets. The venue, positioned as “the city experi-ence on the Northside”, proudly offers a diverse range of “entertain-ment experiences” that could once only be found in the city.

With over 100 combined years experience in the hospitality industry, the White family are well respected and truly understand the impor-tance and benefits of re-investing capital into their properties. This is evident in their latest refurbishment, now fully operational. Christian sat down with Ben to talk about these renovations and improvements.

(Christian): What was the motivation behind these latest refur-bishments to the property?

(Ben): “The original bar was 12 years old. It was time to reinvent our product, and the brand, to appeal to our changing market and to maintain our position as one of the leading venues on Brisbane’s Northside. Our core consumer within our catchment area had evolved over the past decade. The socio-demographics of the re-gion had changed significantly due to a large percentage of younger families moving into the area with different attitudes and “wants”. Our growth opportunity was in attracting these new markets and deliver-ing a product and service to appeal to this audience. We researched to find they were seeking a ‘local venue’ that was more sophisticated and social. We know we have to move with the times and continually reinvest in our product and deliver new offerings and experiences to our clientele – existing and new.”

(Christian): Tell us a little bit about the new Sports Bar, Phoenix Bar and Function Facilities and the reasons for the change?

(Ben): “Firstly, we identified a need for a dedicated function space in the region. There is no venue in the area now that can match our stun-ning new function facilities. Having just one bar venue that catered for both a lounge crowd and a sports crowd was becoming too difficult so we separated the two and created a stylish lounge bar/dining venue (Phoenix) and a new sports bar for the sporting and betting enthusiast.

Now there is absolutely something for everyone. In the past it might have been difficult to convince your girlfriend to join you at the pub for the afternoon, but we have created a feel and vibe that is welcoming. Our establishment has a mix of “offerings” where people want to spend their time and easily move between depending on what entertainment experience they are seeking.”

(Christian): Where do the ideas for the venue changes come from?

(Ben): “The whole family contribute. With over 100 combined years of knowledge and experience we all work together to grow the busi-ness. The greatest influence for me has come from personal travel around the world over the past 5 years. I’ve had the opportunity to learn of hospitality market trends-styles and have gained new insights and product knowledge which has been incorporated into our new look venue. I’ve researched Melbourne with its craft beer culture, Syd-ney’s cocktail bar and share platters, the U.S.A and their sports bar atmosphere; and after travelling through France and Italy we’ve now incorporated French champagnes and Italian wines into our menus. My experiences in those countries enabled me to identify the product to offer and to train our staff who in-turn converse with our patrons and customers about the different products. This is just one way in which we try to bring the city experience out to the suburbs, helping to create

a more sophisticated hospitality experience.

(Christian): Have any recent legislative changes impacted your decisions on these works?

(Ben): “There’s always an uncertainty with what legislative changes may or may not be brought in, and you never want to rely on one area of trade to prop up the rest of your business, because overnight the rules and legislation can change and you need to provide yourself with options. Social pressures of having a high volume entertainment venue are frowned upon. We aimed to step away from that, even though it wasn’t a major focus of ours in the past”.

P4

Christian Tsalikis

Why the recent return of investor confidence to the NSW Hotel Market? Andrew Jolliffe, Managing Director NSW, RWH Australia believes inves-tor confidence has returned to the ho-tel market in NSW, and more broadly on a national basis, for a few fundamental reasons.

Firstly hotels are now (and always have) provided very strong cash flow business models. As an asset class, hotels enjoy

little to no trade debtors, meaning the cash flow model is always refreshed and cash payment receipts are regular. “In fact, this par-ticular feature is a patent hedge against unforeseen dips in trade”, Jolliffe goes on to explain, “meaning even latent challenges to rev-enue attraction can be responded to quickly”.

The second interrelated reason is largely due to the compressed nature of the current RBA cash rate, where two important mani-festations exist. Jolliffe outlines, “Investors are now compelled to purchase yield, as distinct from leaving cash in the bank, with ho-tel assets providing this avenue for investment delivering investors double digit yields far in excess of what term deposits can achieve.”

The other indicator is the spread between the cost of capital and the yield at which hotels can be bought has rarely been wider. Jolliffe clarifies, “The comfort level an investor can enjoy regarding

the profit wedge (ie difference between the yield at which a hotel can be purchased and the cost of funding regarding same) is very attractive”.

“In the past month, we have sold in excess of 10 hotels”, he said. “The even spread of the purchaser profile between the experienced hotelier and newcomers to the industry illustrates to us a return of real confidence to a sector which is almost always in vogue, but like all other asset classes, feels the effects of global challenges to the economy”.

Liquidity in debt markets has returned to an extent which promotes the very lubricant required to drive transactional activity, and this is a theme which enjoys great support from all sectors of the invest-ment landscape.

RWH NSW Update

Decisive election result will help Australian property markets recover The general consensus from market experts and analysts is the imminent federal elec-tion is likely to have a positive impact on the property market, provided it delivers a decisive result.

Blake Edwards, Hotel Sales Executive, Ray White Hotels NSW is personally confident that there will be a positive out of the election.

“Confidence is improving already as the election looms”, Edwards outlines, “We are finding sentiment is improving amongst buyers and sellers as the prospect of a new government moves closer.”

Edwards explains the opportunity lies in a clearer leadership profile coming from the election that will then flow through to confidence which then has a flow-on impact on transactions and prices.

“It’s not just the mechanical changes that a new government will bring, but an end to the negativity in the current arrangement that is stifling confidence in business, he says.

Edwards goes on to say that whilst property market activity could slow before the election due to some buyers and sellers “being a bit nervous”, a clear result at the election will be a positive catalyst for the recovery of our industry.

P5

Andrew Jolliffe

Blake Edwards

Gaming Machine Activity in NSWWhen should you consider purchasing or sell-ing gaming machine entitlements / permits asks Nick Maclean, Hotel Sales Executive with Ray White Hotels NSW.

Are you “over-machined” or “under-machined”? Maclean believes pub operators should stop and consider their average earnings per gaming ma-chine to determine their optimum business model.

As at 30 June 2012 there were 23,368 gaming devices within 1,618 pub venues throughout the state of NSW. Current statistics dem-onstrate the average revenue per machine per annum as $71,949, that’s an average of $1,383 per week.

“If your average weekly revenue is considerably exceeding $1,383 you may wish to consider purchasing additional entitlements/per-mits”, Maclean states, “And if your earnings are below this, you may want to consider selling some of your entitlements/permits”.

For example, if a hotel operator has 15 gaming machines with an average weekly gaming revenue of $13,500 ($900 per machine / per week), this hotel may be “over-machined” and the owner should consider selling off surplus entitlements. In this case, two blocks (one block = three entitlements) could potentially be sold off with negligible impact on gaming revenue. In fact, if funds generated from the sale of the entitlements were re-invested in upgrading the gaming room (e.g. adding a smoking solution) or upgrading the hardware, gaming revenue would likely improve despite the lesser number of machines.

If you wish to purchase additional entitlements, clearly this needs to be compliant with the relevant legislation and gaming machine threshold as outlined in your hotel licence. (continued over)

Nick Maclean

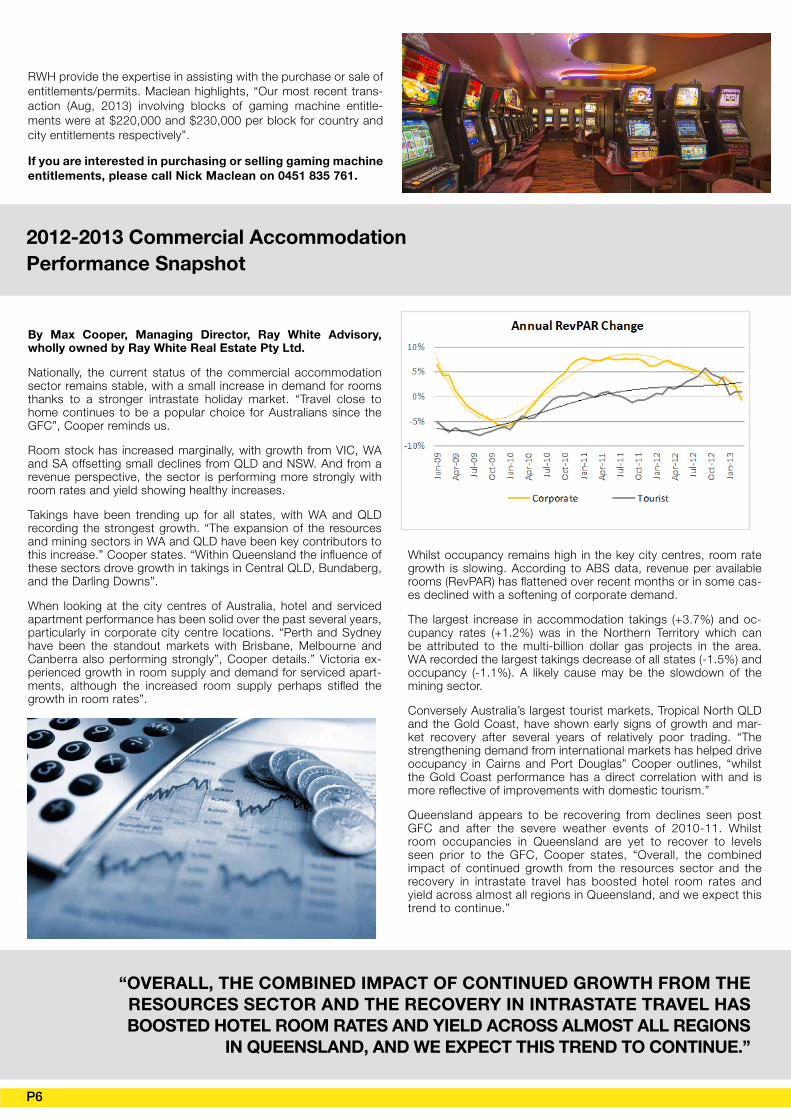

By Max Cooper, Managing Director, Ray White Advisory, wholly owned by Ray White Real Estate Pty Ltd.

Nationally, the current status of the commercial accommodation sector remains stable, with a small increase in demand for rooms thanks to a stronger intrastate holiday market. “Travel close to home continues to be a popular choice for Australians since the GFC”, Cooper reminds us.

Room stock has increased marginally, with growth from VIC, WA and SA offsetting small declines from QLD and NSW. And from a revenue perspective, the sector is performing more strongly with room rates and yield showing healthy increases.

Takings have been trending up for all states, with WA and QLD recording the strongest growth. “The expansion of the resources and mining sectors in WA and QLD have been key contributors to this increase.” Cooper states. “Within Queensland the influence of these sectors drove growth in takings in Central QLD, Bundaberg, and the Darling Downs”.

When looking at the city centres of Australia, hotel and serviced apartment performance has been solid over the past several years, particularly in corporate city centre locations. “Perth and Sydney have been the standout markets with Brisbane, Melbourne and Canberra also performing strongly”, Cooper details.” Victoria ex-perienced growth in room supply and demand for serviced apart-ments, although the increased room supply perhaps stifled the growth in room rates”.

Whilst occupancy remains high in the key city centres, room rate growth is slowing. According to ABS data, revenue per available rooms (RevPAR) has flattened over recent months or in some cas-es declined with a softening of corporate demand.

The largest increase in accommodation takings (+3.7%) and oc-cupancy rates (+1.2%) was in the Northern Territory which can be attributed to the multi-billion dollar gas projects in the area. WA recorded the largest takings decrease of all states (-1.5%) and occupancy (-1.1%). A likely cause may be the slowdown of the mining sector.

Conversely Australia’s largest tourist markets, Tropical North QLD and the Gold Coast, have shown early signs of growth and mar-ket recovery after several years of relatively poor trading. “The strengthening demand from international markets has helped drive occupancy in Cairns and Port Douglas” Cooper outlines, “whilst the Gold Coast performance has a direct correlation with and is more reflective of improvements with domestic tourism.”

Queensland appears to be recovering from declines seen post GFC and after the severe weather events of 2010-11. Whilst room occupancies in Queensland are yet to recover to levels seen prior to the GFC, Cooper states, “Overall, the combined impact of continued growth from the resources sector and the recovery in intrastate travel has boosted hotel room rates and yield across almost all regions in Queensland, and we expect this trend to continue.”

2012-2013 Commercial Accommodation Performance Snapshot

P6

“OVERALL, THE COMBINED IMPACT OF CONTINUED GROWTH FROM THERESOURCES SECTOR AND THE RECOVERY IN INTRASTATE TRAVEL HAS BOOSTED HOTEL ROOM RATES AND YIELD ACROSS ALMOST ALL REGIONS

IN QUEENSLAND, AND WE EXPECT THIS TREND TO CONTINUE.”

RWH provide the expertise in assisting with the purchase or sale of entitlements/permits. Maclean highlights, “Our most recent trans-action (Aug, 2013) involving blocks of gaming machine entitle-ments were at $220,000 and $230,000 per block for country and city entitlements respectively”.

If you are interested in purchasing or selling gaming machine entitlements, please call Nick Maclean on 0451 835 761.