11.the determinants of banks’ capital ratio in developing countries

Journal of Development EconomicsŽ .Vol. 59 1999 337–364

Hot money, accounting labels and thepermanence of capital flows to developing

countries: an empirical investigation

Lucio Sarno a, Mark P. Taylor a,b,)

a Oxford UniÕersity, Oxford, UKb Centre for Economic Policy Research, London, UK

Received 1 August 1996; accepted 1 September 1998

Abstract

Using maximum likelihood Kalman filtering techniques and non-parametric varianceratio statistics, we gauge the relative importance of permanent and temporary componentsof capital flows to Latin American and Asian developing countries over the period

Ž .1988–1997, for the broad categories of flows in the capital account: equity flows EF ,Ž . Ž . Ž .bond flows BF , official flows OF , commercial bank credit BC , and foreign directŽ .investment FDI . We find relatively low permanent components in EF, BF and OF, while

commercial BC flows appear to contain quite large permanent components and FDI flowsare almost entirely permanent. These results have a natural interpretation and clear policyimplications. q 1999 Elsevier Science B.V. All rights reserved.

JEL classification: E44; F20; F34

Keywords: Capital flows; Persistence; Kalman filter; Developing countries; Capital account

1. Introduction

This paper examines the permanence of capital flows to Latin American andAsian developing countries over the period 1988–1997. The 1990s saw a very

) Corresponding author. Department of Economics, Oxford University, St. Cross Building, ManorRoad, Oxford OXI 3UL, UK. Tel.: q44-1865-276643; Fax: q44-1865-281282; E-mail:[email protected]

0304-3878r99r$ - see front matter q 1999 Elsevier Science B.V. All rights reserved.Ž .PII: S0304-3878 99 00016-4

( )L. Sarno, M.P. TaylorrJournal of DeÕelopment Economics 59 1999 337–364338

sharp expansion of net and gross capital flows to developing countries from theŽ . 1developed world World Bank, 1997 . Once it is accepted that a surge in capital

inflows to a developing country may require compensatory policies to offset anyŽ .adverse effects on the recipient economy see, e.g., World Bank, 1997, Chap. 4 ,

then gauging the degree of permanence of any particular capital flow becomescrucial for appropriate policy design. 2 This is particularly important since it isnow increasingly recognised that accounting labels such as ‘short-term’ or ‘long-

Ž .term’ may be an unreliable guide as to the degree of ‘hotness’ temporariness orŽ . Ž . 3‘coolness’ permanence of a capital flow Claessens et al., 1995 .

Another important feature of the recent trend in capital flows to developingcountries is that priÕate capital flows are increasingly a crucial source offinancing of large current account imbalances, significantly dwarfing official

Ž . Ž .flows OF in terms of relative importance. Bruno 1993 , for example, estimatesthat, in the early 1990s, close to half of all aggregate external financing ofdeveloping economies came from private sources and went to private destinations,

Ž .and the World Bank, 1997, p. 9 estimates that private capital flows are now fivetimes the size of OF. The 1990s also saw a considerable broadening in thecomposition of private capital flows to developing countries relative to the 1980s.

Ž .Foreign direct investment FDI now represents the most important component ofŽ .private capital flows, followed by portfolio equity and bond flows, which were

virtually negligible until the late 1980s. On the other hand, commercial bank creditŽ .BC flows, which accounted for over 65% of all private flows in the late 1970sand early 1980s, declined very significantly in terms of relative importance during

Ž .the 1990s World Bank, 1997 . These trends in the pattern of capital flows raiseimportant issues concerning the factors which determine them, how these flowsaffect and are expected to affect the economic performance of developing coun-tries, and how permanent or temporary they are expected to be.

The present paper contributes to the literature on this topical and importantresearch in that we measure the relative size and statistical significance of thepermanent and temporary components of various categories of capital flows to a

1 For a comprehensive review of some recent prospects and developments concerning capital flowsto developing countries, see PriÕate Capital Flows to DeÕeloping Countries: The Road to Financial

Ž .Integration World Bank, 1997 , World InÕestment Report: Transnational, Market Structure andŽ . Ž .Competition Policy United Nations, 1997 , Trends in DeÕeloping Economies World Bank, 1995 ,

Ž .International Capital Markets: DeÕelopments, Prospects, and Policy Issues IMF, 1994, pp. 83–91 ,Ž .PriÕate Market Financing for DeÕeloping Countries IMF, 1995 . Important, slightly earlier studies

Ž . Ž .include Goldstein et al. 1991 and Montiel 1993 .2 Ž . Ž .See, e.g., Corbo and Hernandez 1993, 1996 , Kiguel and Caprio 1993 , Agenor and Montiel

Ž . Ž . Ž . Ž .1996 , Fernandez-Arias and Montiel 1996 , World Bank 1997 , and Razin et al. 1998 .3 The importance of determining the degree of permanence of capital inflows in determining

Ž . Ž . Ž .appropriate policy responses is also stressed by Gooptu 1993 , Nunnenkamp 1993 , Reisen 1993 ,Ž . Ž . Ž .Corbo and Hernandez 1993, 1996 , Claessens et al. 1995 , Hernandez and Rudolph 1995 , and

Ž .Dooley et al. 1996 .

( )L. Sarno, M.P. TaylorrJournal of DeÕelopment Economics 59 1999 337–364 339

large group of Latin American and Asian developing countries during the sampleperiod 1988–1997, distinguishing between the broad categories of flows in the

Ž . Ž .capital account—equity flows EF , bond flows BF , OF, commercial BC, andŽ . 4FDI see Section 2 .

The remainder of the paper is set out as follows. In Section 2, we provide abrief overview of some of the issues raised by the recent increase in internationalcapital flows to developing countries, discuss the relevance of their degree ofpermanence from the policy-making point of view, and establish our priors as tothe expected time series properties of the various capital account items. In Section3, we discuss the data set used and, in Section 4, we describe the estimationtechniques employed in order to model capital flows to developing countries andmeasure their permanence. In Section 5, we report and discuss the empiricalresults. Section 6 concludes.

2. International capital flows, ‘hot money’ and macroeconomic policy

A standard treatment of the desirability of capital flows to developing countriesmight stress the comparative advantage aspect of such transactions, with the gainsfrom capital flows mirroring the gains from trade in goods and services: recipientcountries receive funds for investment which would not normally be available

Žfrom domestic sources, while investing countries receive a higher return adjusted. 5for risk than would be available in the developed world. Equivalently, capital

flows represent intertemporal trade in goods and services, since developingcountry capital account surpluses now are the obverse of current account deficitswhich represent an excess of domestic investment over domestic saving and whichshould be reversed in the future. Arguments for the free flow of capital may thenbe seen as underpinned by arguments for the gains from intertemporal trade.

ŽA number of authors—including those of the recent World Bank report World.Bank, 1997 —have, however, stressed the point that capital inflows to developing

countries may also have deleterious side effects on the recipient economies whichmay require offsetting action by the recipient economy authorities. Given this, the

4 The focus of our analysis is thus less on isolating the underlying determinants of capital flows—anŽ . Ž .issue addressed in papers such as Chuhan et al. 1993, 1998 , Fernandez-Arias 1996 , Taylor and

Ž . Ž .Sarno 1997 and Agenor 1998 —and more on measuring the characteristics of the flows themselves,Žin particular, the relative size of their temporary and permanent components see, e.g., Claessens et al.,

.1995 .5 The rates of return available on various categories of capital rose significantly in many developing

Žcountries during the late 1980s relative to those available in major industrialized economies Calvo et.al., 1993, 1996; Chuhan et al., 1993, 1998; Frankel and Okongwu, 1996 . Credit ratings and secondary

market prices of sovereign debt, reflecting the opportunities and risks of investing in the country, areŽalso likely to be important factors in determining capital flows e.g., Bekaert, 1995; Tesar and Werner,

. Ž1995 ; those indicators also experienced a rising trend in the late 1980s e.g., Mathieson and.Rojas-Suarez, 1992; Chuhan et al., 1993, 1998; Reisen and Fischer, 1993 .

( )L. Sarno, M.P. TaylorrJournal of DeÕelopment Economics 59 1999 337–364340

importance of gauging the degree of permanence of any particular category ofcapital flow becomes clear. On the one hand, the authorities may wish to weighthe costs of designing and implementing a particular macroeconomic policy inorder to offset the harmful side-effects of a particular capital inflow, against theperceived permanence of that flow. On the other hand, the authorities may wish toinsulate the economy against the possible sudden reversal of capital flows whichare deemed to have large temporary, reversible components. The recent World

Ž .Bank report World Bank, 1997 echoes the concerns of many writers on thissubject when it calls for the appropriate design of macroeconomic policies inresponse to capital inflows. 6

Ž . Ž .Corbo and Hernandez 1993, 1996 and Kiguel and Caprio 1993 , for example,describe a number of cases of policy responses adopted by developing countries inresponse to the increase of ‘hot money’ inflows. These include exchange ratepolicies, fiscal policy, sterilization policies or changes in reserve requirements.

Ž .Fernandez-Arias and Montiel 1996 summarize a number of arguments to justifywhy large temporary portfolio flows may not be desirable and may potentiallyperversely affect developing countries unless proper policies designed to neutralize

Ž .them are adopted. The World Bank 1997 , among others, have argued, forexample, that strong surges in portfolio inflows to developing countries maygenerate asset market bubbles—an observation which seems to have been borne

Ž .out by the recent East Asian crisis see, e.g., Krugman, 1998 .On this argument, then, gauging the degree of permanence of capital flows to

developing countries is extremely important, since their reversibility can poten-tially generate high adjustment costs arising from resource reallocation, sunk costsand other hysteresis effects, or other market imperfections, and the countryconcerned should, moreover, try to avoid a long and difficult adjustment processon the basis of capital flows which may be reversed later. 7

Ž .In an influential paper Claessens et al., 1995 , using balance of paymentscapital account data for a range of developing countries, show that the accountinglabels ‘short-term’ and ‘long-term’ as traditionally applied to capital flows do notprovide any reliable indication as to the degree of persistence or ‘coolness’ of the

6 Ž .See also Kaminsky and Reinhart 1998a for an empirical investigation of the extent to which pastfinancial crises share common characteristics in Latin America, Asia, Europe and the Middle East, aswell as an examination of the recent crises in Asia and Latin America in order to determine the extentto which the considerable regional differences of the past have eroded over time. Kaminsky and

Ž .Reinhart 1998b also analyze the link between banking and currency crises for a number of countries,providing evidence that problems in the banking sector typically precede a currency crisis; the currencycrisis deepens the banking crisis, activating a vicious spiral; financial liberalization often precedes abanking crisis; and these episodes may be explained by common macroeconomic causes, typicallywhen a country enters a recession following a prolonged boom in economic activity that is usuallyfueled by credit, large capital inflows and domestic currency overvaluation.

7 Ž .As noted by Corbo and Hernandez 1993 : ‘‘Reversing an initial adjustment could be quite costlyif there are irreversible costs involved . . . This is particularly relevant in the case of hot money.’’

( )L. Sarno, M.P. TaylorrJournal of DeÕelopment Economics 59 1999 337–364 341

flows. They argue, moreover, that relying on the accounting label rather than theactual time series properties of capital flows for policy purposes may generatepotentially disastrous results. 8 Thus, the importance of investigating the timeseries properties of capital flows to developing countries—the focus of theresearch reported in this paper—becomes clear.

Capital flows to developing countries may be classified into four broadcategories: private portfolio flows—which may be further sub-divided into BF and

Ž .EF i.e., developing country company share purchase flows; commercial banklending from developed to developing countries; FDI, whereby a firm largelyowned by residents in a developed country acquires or expands a factory orsubsidiary firm located in a developing country; and OF, representing loans frominternational agencies such as the World Bank and the International MonetaryFund, as well from developed country governments. Before analysing the timeseries properties of these various categories of flows and, in particular, theirdegree of persistence, it is useful to set out one’s prior expectations concerning thedegree of permanence or persistence on might expect for each of them.

In forming a prior for the degree of permanence of flows of FDI, one mustdistinguish between the degree of reversibility of the flows and of the actualphysical investment itself. There is an important literature on the sunk costs nature

Ž .of much physical investment see, e.g., Dixit and Pindyck, 1994 . Granting thatphysical investment in a developing country may be largely irreversible, however,does not imply that the flows of funds for such investment are themselvesirreversible. To give a simple example, once a firm has invested in plant andmachinery in a country, then it is very hard or indeed impossible to reverse thatinvestment. On the other hand, if the investment is one-off, then the resulting timeseries for FDI investment flows will appear to be temporary—only occurring overa short period while the plant and machinery are being built and installed and thenceasing. One might argue, however, that where a firm has made a directinvestment in a country, then it will almost certainly have thoroughly examinedthe underlying economic fundamentals and is less likely to be influenced byfinancial market inefficiencies such as herding effects, so that FDI flows might beexpected to be more permanent than portfolio flows. Also, although the irre-versible nature of much physical investment is not the same as the irreversibilityor otherwise of the FDI flows themselves, there may be some link between the twoin that once a firm has made a commitment to a particular country through FDI,then the less likely it is to decide suddenly to start investing in alternativelocations elsewhere. Moreover, there are likely to be important signalling effects

8 Ž .Dooley 1995 , for example, argues that the 1982 debt crisis was in part generated by theimprudence of private investors induced by capital flows to developing countries in the 1970s which,although labeled as private, should really have been considered as official in that a general governmen-tal guarantee underlay them.

( )L. Sarno, M.P. TaylorrJournal of DeÕelopment Economics 59 1999 337–364342

in FDI in the sense that once a firm makes a largely irreversible investment in aparticular country, this commitment signals to other firms a belief that that country

Žis safe to invest in in terms of market access andror its governance and.institutions , thus, encouraging further FDI. Of the various categories of inflows,

therefore, FDI may perhaps be expected to have a large permanent component.Ž .Portfolio flows i.e., EF and BF , on the other hand, might be expected to be

significantly more volatile then FDI flows and—with increasing deregulation anddecreasing transactions costs—more sensitive to movements in short-term differ-entials in rates of return. Also, given that emerging markets are still underweighted

Ž .in foreign investors’ portfolios World Bank, 1997 and that foreign investors arestill relatively unfamiliar with emerging markets, these markets may be quitesusceptible to cyclical conditions in major industrialized countries and more prone

Žto investor herding behavior than industrial countries’ financial markets World. 9Bank, 1997 .

A priori, then, we might expect portfolio—bond and equity—flows and FDIflows to define the most volatile or temporary and least volatile or permanentcapital-account items respectively. The remaining category of private capitalflows, commercial BC—the least important fraction of private capital flows todeveloping countries in the 1990s in terms of relative size—one might expect tohave an important persistent component. In particular, because of the illiquidity ofcommercial loans to developing countries once they are made, one might expectcommercial banks to look more closely at the underlying economic fundamentalsbefore committing funds and therefore to be less prone to sudden changes of heart.Moreover, once funds are committed in this way, it may seriously jeopardise abank’s chances of recovering its investment if lending is suddenly withdrawn.Hence, the permanent component in commercial BC time series may reasonablybe expected to be relatively large and perhaps to dominate the transitory compo-nent, albeit to a lesser extent than for FDI flows.

It is perhaps a little harder to form strong priors concerning the degree ofpermanence of OF to developing countries. Although OF have been considerably

Ždwarfed by private capital flows to developing countries in the 1990s World.Bank, 1997, p. 9 , they still remain of some importance for various low-income

developing countries. More generally, OF continue to play a valuable complemen-tary role to private capital flows for a number of reasons, such as sustainingimprovements in the policy and institutional framework, and acting as a catalyst

9 Indeed, portfolio EF to developing countries may be expected to be sensitive to the degree ofopenness of the country considered, and in particular to the rules concerning the repatriation of capital

Ž .and income Goldstein et al., 1991; Papaioannu and Duke, 1993; Williamson, 1993 . The InternationalFinance differentiates between countries which give foreign investors free and unrestricted repatriationof capital and income from equity investment, and countries, defined ‘relatively open’, which applysome restrictions on the repatriation of capital and income, and still other countries, defined ‘relativelyclosed’, which apply very strict restrictions to the way in which capital may be repatriated.

( )L. Sarno, M.P. TaylorrJournal of DeÕelopment Economics 59 1999 337–364 343

for private flows in countries with increasingly sound macroeconomic policiesŽ .World Bank, 1997, pp. 66–71 . Given that OF are largely under the control ofinternational agencies and national governments, one might perhaps expect themto be more persistent than private portfolio flows. On the other hand, a developingcountry may have recourse to OF in order to compensate for reversals in othercategories of the capital account, and to that extent OF may be largely picking upthe residual effects of those other flows. Overall, therefore, general priors for thepermanence of OF are hard to determine.

We now turn to a discussion of the data employed in our empirical analysis ofhow far these priors are satisfied.

3. Data

We employ a data base on the various categories of US capital flows to nineAsian and nine Latin American countries from the beginning of 1988 through tothe end of 1997. The nine Asian countries considered are China, India, Indonesia,Korea, Malaysia, Pakistan, Philippines, Taiwan and Thailand. The nine LatinAmerican countries considered are Argentina, Brazil, Chile, Colombia, Ecuador,

10 Ž .Jamaica, Mexico, Uruguay and Venezuela. For US portfolio equity and bondflows and OF to these countries, the frequency of our data base is monthly. Thesetime series were constructed using the International Capital Reports of the USTreasury Department. 11 Following a number of studies, we use net EF and grossBF to developing countries, which cover a substantial share of portfolio flows tothose countries, 12 since even if in principle we are concerned with modelling netcapital flows, it seems preferable to use gross measures for BF in order to abstractfrom the effect of sterilization policy actions and other types of reserve operations

10 Ž .These are the same countries considered by Chuhan et al. 1993, 1998 and Taylor and SarnoŽ .1997 .

11 Quarterly data are published in the US Treasury Bulletin, while monthly data are now availablefrom the website of the US Treasury Department. Most of these data are collected by the Treasury fromfinancial intermediaries in the US through the International Capital Form S reports. Hence, the data donot include direct dealings of US investors with foreign intermediaries as these transactions bypass thesystem. Note also that the data on bonds cover transactions of foreign securities in the US from and todeveloping countries; transactions in bonds not issued by the developing country concerned nor by US

Žparties are expected to be quite insignificant see Chuhan et al., 1993, 1998, pp. 446–451; Tesar and.Werner, 1994; Taylor and Sarno, 1997 .

12 Net capital flows arise when savings and investment are unbalanced across countries, and thereforea transfer of real resources is generated through a trade or current account imbalance. Gross capitalflows, on the other hand, need not involve any transfer of real resources, since they may be offsettingacross countries. Nevertheless, they allow individuals and firms to adjust the composition of theirfinancial portfolios and are therefore important in improving the liquidity and diversification ofportfolios.

( )L. Sarno, M.P. TaylorrJournal of DeÕelopment Economics 59 1999 337–364344

Žby the monetary authorities see, e.g., Chuhan et al., 1993; Taylor and Sarno,.1997 .

Quarterly data on US commercial BC flows to the same developing countriesŽwere taken from the US Treasury Bulletin Capital Movements Section, Table

.CM-II-2 which presents claims on foreigners reported by US banks and otherdepository institutions, brokers, and dealers. 13 Also, quarterly data for FDI tothose developing countries were taken from the diskette US Direct InÕestmentAbroad of the US Department of Commerce. 14

The sample period runs from 1988M1 to 1997M12 for EF, BF and OF, andfrom 1988Q1 to 1997Q4 for the series on BC and FDI, therefore, providing uswith a 10-year observation period during which both inflows and outflows haveoccurred before and after the Mexican crisis, and spanning until a few years afterthe ending of the downturn in US interest rates.

4. Estimation techniques

4.1. UnobserÕed components

The persistence of capital flows can be examined by employing the unobservedŽ .components model suggested by Harvey 1981, 1989 . The essential idea is to

break the time series down into unobserved permanent and temporary componentsusing maximum likelihood estimation. Consider a panel data set of N countrieswith capital flows of a certain category for the ith country at time t genericallydenoted f . The unobserved components model may be written. 15

i t

f sm qn qe is1, . . . , N ; ts1, . . . ,T 1Ž .i t i t i t i t

where f may be any of the capital-account items discussed in Sections 2 and 3,i t

m is a trend component, the irregular component ´ is approximately normallyi t i t

independently distributed with zero mean and constant variance and n representsi tŽ .a first-order autoregressive, AR 1 component:

n sr n qj 2Ž .i t n i ty1 i ti

where j is approximately normally independently distributed with zero mean andi t

13 In fact, data on bank claims held for their own account are collected monthly. However,information on claims held for their domestic customers as well as foreign currency claims is collectedonly on a quarterly basis and, therefore, relatively reliable and comprehensive data on BC are onlyavailable on a quarterly basis.

14 These data are also published in the SurÕey of Current Business of the US Department ofCommerce.

15 A possible extension of the model would be to consider one or more cyclical components. Weneglect this possibility because, in our empirical analysis, the inclusion of a cycle in the model was notfound to improve the goodness of fit on the basis of the prediction error variance and the AIC.

( )L. Sarno, M.P. TaylorrJournal of DeÕelopment Economics 59 1999 337–364 345

constant variance, and the autoregressive coefficient is constrained to be less thanunity in absolute value in order to ensure stationarity of the component. 16

The stochastic trend component is modelled as:

m sm qb qh 3Ž .i t i ty1 i ty1 i t

and

b sr b qz 4Ž .i t b i ty1 i ti

where b represents the slope or gradient of the trend component m and ri t i t b i

represents the damping factor, while each of the disturbances h and z isi t i t

approximately normally independently distributed with zero mean and constantvariance.

The irregular component ´ , the level disturbance h and the slope disturbancei t i t

z are mutually uncorrelated. The slope component may be treated as fixed ratheri t

than stochastic and also excluded from the trend specification when this isappropriate.

Ž .Intuitively, Eq. 1 expresses the capital flow as the sum of a permanentŽ . Ž .component m , a purely temporary, zero persistence component ´ and ai t i t

Ž .more slowly decaying temporary component n . In addition, the drift in thei tŽ .random walk component b may itself vary over time. Thus, the modeli t

separates out the persistent and temporary components of the data in a verygeneral, comprehensive fashion. 17

The statistical treatment of the unobserved components model outlined above isŽ .conveniently handled by writing it in state space form SSF involving a measure-Ž .ment equation relating the unobserved components the state vector to an

observed series, together with a transition equation governing the evolution of the

16 Ž .The need to impose stationarity on the AR 1 process arises because of the risk of it beingconfounded with the random-walk component in the trend specification, in which case the modeleffectively be unidentified.

17 Ž .Note that the structural time series model outlined above also nests an I 2 process for f . Ini tŽ .particular, ignoring the AR 1 component and dropping the country subscript i for ease of exposition,

the first difference of f , D f , may be written as:t t

D f s b qh qe yet ty1 t t ty1

Ž .Since b s r b qz , if s s0 or r s0, then D f is the sum of an MA 1 process and aty1 b ty2 ty1 z b tŽ . Ž . Ž .white noise process, so that f ; I 1 : f ;ARIMA 0,1,1 Granger and Morris, 1976 . If s /0,t t z

Ž . 2 Ž . Ž .however: a if r s1 then D f is the sum of a white noise process, an MA 1 and an MA 2 sob tŽ . Ž . Ž . Ž . < < Ž .f ; I 2 : f ;ARIMA 0,2,2 ibid. ; b if r -1, then D f is the sum of a stationary AR 1 , ant t b tŽ . Ž . Ž . Ž .MA 1 and white noise so f ; I 1 : f ;ARIMA 1,1,2 ibid. . Nevertheless, the finding—discussedt t

in Section 5—that the stochastic slope is not found to be statistically significantly different from zeroat conventional nominal levels of significance clearly implies that all the series modelled in this paperare first-difference stationary, which also accords with the evidence, reported below, from executingunit root tests. This taxonomy also illustrates how the structural time series model may be viewed as ameans of interpreting low-order ARIMA processes in terms of permanent and temporary components.

( )L. Sarno, M.P. TaylorrJournal of DeÕelopment Economics 59 1999 337–364346

Ž . Ž .state vector. The SSF corresponding to the model outlined in Eqs. 1 – 4 may bewritten as:

mi t

f s 1 0 1 qe 5Ž . Ž .bi t i ti t� 0n i t

1 1 0 hm m i ti t i ty1 1 0 00 r 0b zs q 6i Ž .b b 0 1 0 i ti t i ty1 ž /� 0 � 0 � 0� 00 0 r 0 0 1n n jni t i ty1 i ti

Ž .where Eq. 5 represents the measurement equation, which shows how an observedŽ .series is related to the state vector, whereas Eq. 6 is the transition equation,

Ž .describing the dynamic evolution of the state vector. The SSF given by Eqs. 5Ž .and 6 may itself be written—dropping the country subscript for clarity—in a

more compact form, using obvious notation, as:

f szX x qe ts1, . . . ,T 7Ž .t t r

x sM x qR k ts1, . . . ,T 8Ž .t ty1 r

where:

e ; IN 0,s 2 9Ž . Ž .t

k ; IN 0,s 2 Q 10Ž . Ž .t

X Ž . Ž .z is a known 3=1 vector, M and R are fixed matrices of order 3=3 , and QŽ . Ž .is also a fixed 3=3 matrix. The 3=1 vector x is the unobservable statet

vector.Given knowledge of the parameters of the SSF, the Kalman filter provides us

Žwith optimal estimates of x , using either information up to time ty1 thet. Ž .prediction equations , information up to time t the updating equations , or the fullŽ . Ž . 18sample information the smoothing equations Kalman, 1960a,b .

Suppose we have an optimal estimator of x using all information up to timety1

ty1, and denote this X . Then, the prediction equation providing us with thety1

optimal predictor of x using information up to time ty1, denoted X is:t t < ty1

X sM X 11Ž .t < ty1 ty1

and the covariance matrix of X can be shown to be given by:t < ty1

P sMP MX qRQRX 12Ž .t < ty1 ty1

Ž . Ž .where P is the covariance matrix of X . Eqs. 11 and 12 describe thety1 t < ty1

prediction equations of the Kalman filter.

18 Ž . Ž . Ž .See Harvey 1989 or Cuthbertson et al. 1992 Chap. 7 for an accessible introduction to theKalman filter.

( )L. Sarno, M.P. TaylorrJournal of DeÕelopment Economics 59 1999 337–364 347

The updating equations, which update these predictions on the basis of informa-Ž . Ž .tion at time t, are given by Eqs. 13 and 14 :

X sX qP z f yzX X rg 13Ž .Ž .t t < ty1 t < ty1 t t < ty1 t

P sP yP z zX P rg 14Ž .t t < ty1 t < ty1 t < ty1 t

where g szX P zq1. 19t t < ty1

Given a finite sequence of observations f , the only state vector estimatort

which uses all the available information is X . The smoothing equations, given byTŽ . Ž .Eqs. 15 and 16 , describe optimal, full-sample information estimators:

X sX qPU X yM X 15Ž .Ž .t <T t t tq1 <T t

P sP yPU P yP PUX 16Ž .Ž .t <T t t tq1 <T tq1 < t T

U Ž . Ž .where P sP MrP , X sX and P sP . Eqs. 11 – 16 describe thet t tq1 < t T <T T T <T TŽ .Kalman filter recursions Kalman, 1960a,b .

The state space parameters can in practice be estimated by maximum likelihoodŽ .methods Harvey, 1989; Cuthbertson et al., 1992 . A natural by-product of the

Kalman filter recursions is a sequence of one-step-ahead prediction errors, u ,t

defined by:

u s f yzX X 17Ž .t t t < ty1

Ž .Using a result due to Schweppe 1965 , the likelihood function for the sample,Ž .Ł P , can be derived and expressed in terms of the innovations u and theirt

variances, g :tT y2 T 2T T 1 s ut2£sy ln2py lns y ln g y 18Ž .Ý Ýt2 2 2 2 gtts1 ts1

The likelihood function obtained can then be maximized with respect to the20 Žparameters using numerical optimisation procedures e.g., Cuthbertson et al.,

.1992, Chap. 2 . In our empirical work, we employ the Broyden–Fletcher–Gold-

19 Ž X . Ž .The term f y z X in Eq. 13 is the prediction error. This innovation contains all the new< ty1t tŽ .information in f and is used to update x via the Kalman gain, which is the 3=1 vectort t

Ž .P z r g which essentially decides what weight to assign to the innovation.t < ty1 t20 2 Ž .The scale factor s may always be concentrated out of Eq. 18 by substituting:

T 21 ut2s sˆ ÝT gtts1

so that the maximization of the likelihood function becomes equivalent to minimizing the function:T

2FsT lns q ln gˆ Ý tts1

Concentrating s 2 out of the likelihood function reduces the dimension of the search involved in thenumerical optimisation procedure.

( )L. Sarno, M.P. TaylorrJournal of DeÕelopment Economics 59 1999 337–364348

Ž .farb–Shanno quasi-Newton algorithm Harvey, 1981 , based on three convergencecriteria—changes in the likelihood kernel, the gradient and the parameters.

The estimated variance parameters indicate the relative contribution of eachcomponent in the state vector to explaining the total variation in the time seriesunder consideration. In some sense, therefore, the estimated variances allowus—by providing information on the size of the nonstationary and the stationarycomponents in the series—to quantify the degree of persistence of the series inquestion. If a large and statistically significant proportion of the variation in flowsis attributed to the stochastic level, for example, then one may expect that a largepart of the capital flows will remain in the country concerned for an indeterminateperiod of time. By contrast, if a large portion of the variation in the time series isexplained by movements in the temporary components, then the capital flowsunder consideration may be regarded as characterized by low persistence, indicat-ing a higher degree of potential reversibility. 21

When the maximum likelihood estimate of the variance of an element of theŽ 2 .state vector i.e., s or one of the diagonal elements of Q is zero, the model can

be re-estimated making the corresponding component deterministic. Also, standardtests of the significance of the component itself can be carried out: if thecomponent concerned is not found to be statistically significantly different fromzero, the model may be simplified by eliminating the component from the SSFaltogether.

In choosing the most appropriate model for each country and label flow, werelied not only on standard measures such as the coefficient of determination: thefit of alternative models was also compared on the basis of the Akaike information

Ž . Ž . Ž .criterion AIC , equal to log PEV q2 mrT , where PEV is the steady-stateŽ .prediction error variance Harvey, 1989, pp. 263–270 , m represents the number

of parameters to be estimated plus the number of nonstationary components, and Tis the number of observations. 22

4.2. Variance ratio tests

The other measure of persistence we employ in this paper is a simpleŽ .non-parametric test, due originally to Cochrane 1988 , generally referred to as the

Ž .variance ratio test, z k :

1 Var f y fŽ .i t i tykz k s 19Ž . Ž .

k Var f y fŽ .i t i ty1

21 Ž .While the irregular component is totally temporary, the AR 1 component displays some degree ofpositive persistence determined by the size of the damping factor, albeit still mean reverting.

22 Although the PEV is, in general, the basic measure of goodness of fit, when a choice has to bemade among alternative models with different numbers of hyperparameters, it is more appropriate to

Ž .compare them on the basis of the AIC or alternative information criteria Harvey, 1989 .

( )L. Sarno, M.P. TaylorrJournal of DeÕelopment Economics 59 1999 337–364 349

where k is a positive integer and Var stands for variance. At one extreme, ifmovements in the series in question are entirely permanent, then the ratio in Eq.Ž .19 should be equal to unity. If capital flows exhibit mean reversion, however,

Ž .then the ratio z k should be in the range between zero and unity, with a valueclose to zero indicating a high temporary component.

Ž .Cochrane 1988 shows that the Bartlett estimator provides appropriate standardŽ . 23errors for z k . In small samples, however, both the variance ratios and the

Bartlett standard errors may be biased upwards and the asymptotic standard errorsmay not be a satisfactory approximation of the actual standard errors. Thus, in ourempirical work, we adopt the two corrections for small-sample bias suggested byŽ .Cochrane, 1988, pp. 907–910 . First, we use the sample mean of the firstdifferences to estimate the drift term at all k rather than estimate a different driftterm at each k from the mean of the k-differences. Second, we adopt a degrees of

Ž .freedom correction, Tr Tyky1 , where T is the number of observations.

5. Empirical results 24

5.1. Unit root tests

As a preliminary exercise, we computed simple augmented Dickey–Fuller unitroot tests statistics for each of the five US capital flows examined to Latin

ŽAmerica and Asia, both in levels and first differences not reported but available.on request . In every case, we could not reject, at standard significance levels, the

null hypothesis that there is a unit root in each of the time series when expressedin levels, while we were always able to reject the hypothesis of nonstationarity ofthe series in first differences. This therefore provides prima facie evidence of apermanent component in each of the capital flow series. We next employedKalman filtering techniques to evaluate the relative size of the permanent andtemporary components.

5.2. Kalman filter results

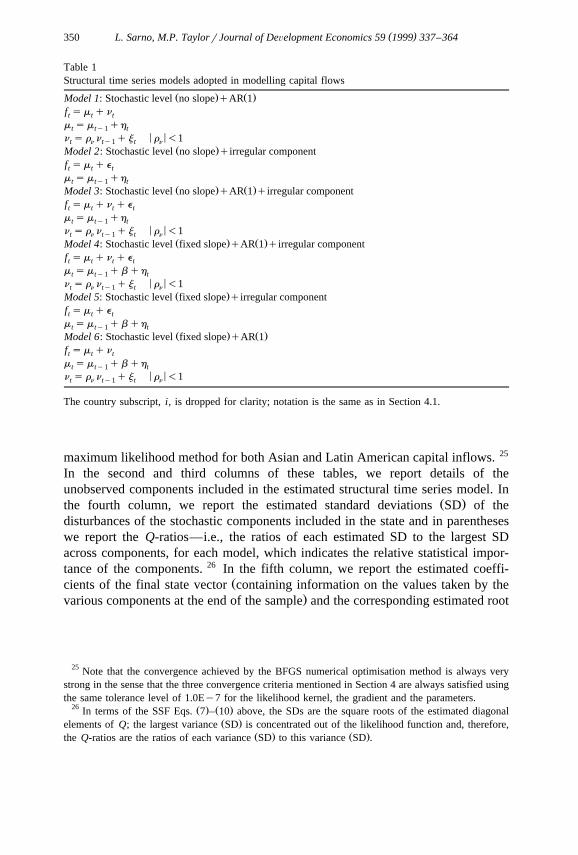

In Table 1, we classify the various model specifications which were selected forcapital flows to developing countries on the basis of the goodness of fit criteriadiscussed in Section 4.1. In Tables 2–6, we report the results of estimating themost appropriate structural time series model in SSF by the Kalman filter

23 Ž .0.5 Ž .Thus, the standard error is consistently estimated as 4kr3T Var f .i tyk24 Throughout our discussion of the empirical results, we employ a nominal significance level of 5%

unless explicitly stated otherwise, so that expressions such as ‘statistically significant’, for example,should be read as ‘statistically significantly different from zero at the 5% nominal level of significance’.

( )L. Sarno, M.P. TaylorrJournal of DeÕelopment Economics 59 1999 337–364350

Table 1Structural time series models adopted in modelling capital flows

Ž . Ž .Model 1: Stochastic level no slope qAR 1f sm qnt t t

m sm qht ty1 t< <n s r n qj r -1t n ty1 t n

Ž .Model 2: Stochastic level no slope qirregular componentf sm qet t t

m sm qht ty1 tŽ . Ž .Model 3: Stochastic level no slope qAR 1 qirregular component

f sm qn qet t t t

m sm qht ty1 t< <n s r n qj r -1t n ty1 t n

Ž . Ž .Model 4: Stochastic level fixed slope qAR 1 qirregular componentf sm qn qet t t t

m sm q b qht ty1 t< <n s r n qj r -1t n ty1 t n

Ž .Model 5: Stochastic level fixed slope qirregular componentf sm qet t t

m sm q b qht ty1 tŽ . Ž .Model 6: Stochastic level fixed slope qAR 1

f sm qnt t t

m sm q b qht ty1 t< <n s r n qj r -1t n ty1 t n

The country subscript, i, is dropped for clarity; notation is the same as in Section 4.1.

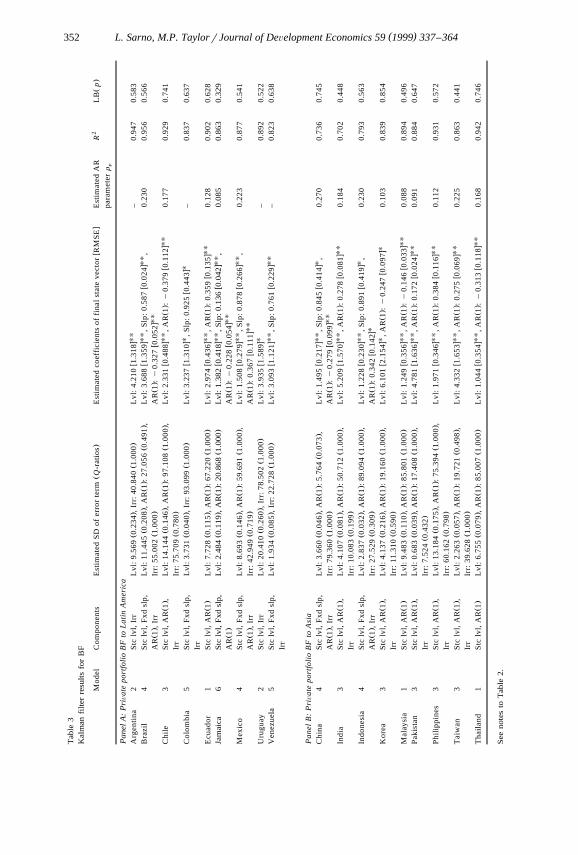

maximum likelihood method for both Asian and Latin American capital inflows. 25

In the second and third columns of these tables, we report details of theunobserved components included in the estimated structural time series model. In

Ž .the fourth column, we report the estimated standard deviations SD of thedisturbances of the stochastic components included in the state and in parentheseswe report the Q-ratios—i.e., the ratios of each estimated SD to the largest SDacross components, for each model, which indicates the relative statistical impor-tance of the components. 26 In the fifth column, we report the estimated coeffi-

Žcients of the final state vector containing information on the values taken by the.various components at the end of the sample and the corresponding estimated root

25 Note that the convergence achieved by the BFGS numerical optimisation method is always verystrong in the sense that the three convergence criteria mentioned in Section 4 are always satisfied usingthe same tolerance level of 1.0Ey7 for the likelihood kernel, the gradient and the parameters.

26 Ž . Ž .In terms of the SSF Eqs. 7 – 10 above, the SDs are the square roots of the estimated diagonalŽ .elements of Q; the largest variance SD is concentrated out of the likelihood function and, therefore,

Ž . Ž .the Q-ratios are the ratios of each variance SD to this variance SD .

( )L. Sarno, M.P. TaylorrJournal of DeÕelopment Economics 59 1999 337–364 351

Tab

le2

Kal

man

filt

erre

sult

sfo

rE

F

2Ž

.w

xŽ

.M

odel

Com

pone

nts

Est

imat

edS

Dof

erro

rte

rmQ

-rat

ios

Est

imat

edco

effi

cien

tsof

fina

lst

ate

vect

orR

MS

EE

stim

ated

AR

RL

Bp

para

met

err

n

Pan

elA

:P

riÕat

epo

rtfo

lio

EF

toL

atin

Am

eric

aU

UU

UŽ.

Ž.

Ž.

Ž.

wx

Ž.

wx

Arg

enti

na1

Stc

lvl,

AR

1L

vl:

18.6

780.

194

,A

R1

:96

.464

1.00

0L

vl:

y1.

747

0.47

7,

AR

1:

0.15

50.

030

0.11

60.

862

0.54

7U

UU

UŽ.

Ž.

Ž.

Ž.

wx

Ž.

wx

Bra

zil

1S

tclv

l,A

R1

Lvl

:1.

124

0.07

1,

AR

1:

15.8

641.

000

Lvl

:1.

532

0.46

7,

AR

1:

0.26

10.

035

0.22

20.

902

0.43

7U

UŽ

.Ž

.w

xC

hile

2S

tclv

l,Ir

rL

vl:

10.7

360.

281

,Ir

r:38

.243

1.00

0L

vl:

1.71

40.

384

–0.

847

0.48

3U

UU

UŽ.

Ž.

Ž.

Ž.

wx

Ž.

wx

Col

ombi

a1

Stc

lvl,

AR

1L

vl:

2.51

60.

095

,A

R1

:26

.494

1.00

0L

vl:

4.15

61.

272

,A

R1

:0.

156

0.02

90.

018

0.89

20.

764

UU

UU

Ž.

Ž.

Ž.

Ž.

wx

Ž.

wx

Ecu

ador

3S

tclv

l,A

R1

,Ir

rL

vl:

6.26

10.

143

,A

R1

:43

.760

1.00

0,

Lvl

:y

2.22

30.

798

,A

R1

:y

0.16

40.

032

0.09

60.

804

0.34

0Ž

.Ir

r:36

.940

0.84

4U

UU

Ž.

Ž.

Ž.

Ž.

wx

Ž.

wx

Jam

aica

1S

tclv

l,A

R1

Lvl

:3.

471

0.05

1,

AR

1:

67.8

701.

000

Lvl

:y

3.35

91.

413

,A

R1

:0.

341

0.13

00.

238

0.93

20.

943

Ž.

Ž.

Ž.

Ž.

wxU

Ž.

wxU

UM

exic

o1

Stc

lvl,

AR

1L

vl:

2.54

50.

088

,A

R1

:28

.953

1.00

0L

vl:

y2.

912

1.28

5,

AR

1:

0.36

20.

102

0.22

40.

893

0.43

9U

UU

Ž.

Ž.

Ž.

Ž.

wx

Ž.

wx

Uru

guay

3S

tclv

l,A

R1

,Ir

rL

vl:

2.84

50.

119

,A

R1

:23

.799

1.00

0,

Lvl

:y

2.83

50.

898

,A

R1

:y

0.11

70.

031

0.04

80.

856

0.56

2Ž

.Ir

r:19

.091

0.80

2U

UU

UŽ.

Ž.

Ž.

Ž.

wx

Ž.

wx

Ven

ezue

la1

Stc

lvl,

AR

1L

vl:

12.1

030.

255

,A

R1

:47

.428

1.00

0L

vl:

y1.

872

0.66

4,

AR

1:

0.12

70.

019

0.26

80.

822

0.74

3

Pan

elB

:P

riÕat

epo

rtfo

lio

EF

toA

sia

UU

UU

Ž.

Ž.

Ž.

wx

wx

Chi

na4

Stc

lvl,

Fxd

slp,

Lvl

:4.

577

0.09

1,

AR

1:

50.0

091.

000

,L

vl:

4.96

30.

924

,S

lp:

0.30

70.

043

,0.

214

0.83

80.

503

UU

Ž.

Ž.

Ž.

wx

AR

1,

Irr

Irr:

0.98

50.

020

AR

1:

y0.

456

0.17

1U

UU

UŽ

.Ž.

Ž.

wx

wx

Indi

a4

Stc

lvl,

Fxd

slp,

Lvl

:1.

839

0.07

2,

AR

1:

25.6

501.

000

,L

vl:

6.00

21.

602

,S

lp:

0.60

10.

202

,0.

075

0.94

80.

683

UU

Ž.

Ž.

Ž.

wx

AR

1,

Irr

Irr:

19.8

450.

774

AR

1:

0.19

80.

048

UU

UU

Ž.

Ž.

Ž.

Ž.

wx

Ž.

wx

Indo

nesi

a1

Stc

lvl,

AR

1L

vl:

3.87

30.

065

,A

R1

:59

.686

1.00

0L

vl:

3.93

81.

150

,A

R1

:y

0.24

30.

045

0.05

90.

920

0.39

4Ž

.Ž.

Ž.

wxU

Uw

xUU

Kor

ea4

Stc

lvl,

Fxd

slp,

Lvl

:5.

071

0.05

5,

AR

1:

92.7

401.

000

,L

vl:

1.78

60.

247

,S

lp:

0.77

80.

241

,0.

120

0.80

30.

756

UU

Ž.

Ž.

Ž.

wx

AR

1,

Irr

Irr:

39.9

570.

431

AR

1:

0.33

90.

025

UŽ

.Ž

.w

xM

alay

sia

2S

tclv

l,Ir

rL

vl:

10.9

710.

181

,Ir

r:60

.653

1.00

0L

vl:

y4.

241

1.65

7–

0.79

20.

748

UŽ

.Ž

.w

xP

akis

tan

2S

tclv

l,Ir

rL

vl:

8.95

10.

223

,Ir

r:40

.044

1.00

0L

vl:

y3.

118

1.22

9–

0.83

70.

672

UU

Ž.

Ž.

wx

Phi

lipp

ines

2S

tclv

l,Ir

rL

vl:

2.99

70.

107

,Ir

r:27

.944

1.00

0L

vl:

1.25

00.

190

–0.

765

0.54

7U

UU

UŽ.

Ž.

Ž.

Ž.

wx

Ž.

wx

Tai

wan

1S

tclv

l,A

R1

Lvl

:2.

420

0.05

0,

AR

1:

47.9

581.

000

Lvl

:y

4.49

81.

466

,A

R1

:0.

395

0.14

60.

264

0.82

90.

482

UU

Ž.

Ž.

wx

Tha

ilan

d2

Stc

lvl,

Irr

Lvl

:3.

134

0.09

1,

Irr:

34.5

811.

000

Lvl

:3.

969

1.26

7–

0.80

10.

636

Ž.

The

Q-r

atio

isth

era

tio

ofth

est

anda

rdde

viat

ion

SD

ofea

chco

mpo

nent

toth

ela

rges

tS

Dac

ross

com

pone

nts

for

each

mod

el,

and

isre

port

edin

pare

nthe

ses

inth

efo

urth

colu

mn;

inth

efi

fth

Ž.

UŽU

U.

Ž.

Ž.

colu

mn,

we

repo

rtth

ees

tim

ated

root

mea

nsq

uare

erro

rsR

MS

Ein

squa

rebr

acke

ts,

whi

lein

dica

tes

stat

isti

cal

sign

ific

ance

ofth

eco

mpo

nent

conc

erne

dat

the

5%1%

leve

l.L

Bp

isth

e2Ž

.p-

valu

efr

omex

ecut

ing

Lju

ng–

Box

test

stat

isti

csfo

rab

senc

eof

resi

dual

seri

alco

rrel

atio

nw

hich

,un

der

the

null

,ar

edi

stri

bute

das

xp

whe

rep

sp

yp

and

pan

dp

deno

teth

enu

mbe

rof

12

12

Ž.

lags

s12

and

the

num

ber

ofpa

ram

eter

sin

the

stat

e,re

spec

tive

ly.

Oth

erab

brev

iati

ons

used

are:

stc

for

stoc

hast

ic,

lvl

for

leve

l,fx

dfo

rfi

xed,

slp

for

slop

e,ir

rfo

rir

regu

lar.

( )L. Sarno, M.P. TaylorrJournal of DeÕelopment Economics 59 1999 337–364352

Tab

le3

Kal

man

filt

erre

sult

sfo

rB

F

2Ž

.w

xŽ

.M

odel

Com

pone

nts

Est

imat

edS

Dof

erro

rte

rmQ

-rat

ios

Est

imat

edco

effi

cien

tsof

fina

lst

ate

vect

orR

MS

EE

stim

ated

AR

RL

Bp

para

met

err

n

Pan

elA

:P

riÕat

epo

rtfo

lio

BF

toL

atin

Am

eric

aU

UŽ

.Ž

.w

xA

rgen

tina

2S

tclv

l,Ir

rL

vl:

9.56

90.

234

,Ir

r:40

.840

1.00

0L

vl:

4.21

01.

318

–0.

947

0.58

3U

UU

UŽ

.Ž.

Ž.

wx

wx

Bra

zil

4S

tclv

l,F

xdsl

p,L

vl:

11.4

450.

208

,A

R1

:27

.056

0.49

1,

Lvl

:3.

688

1.35

9,

Slp

:0.

587

0.02

4,

0.23

00.

956

0.56

6U

UŽ.

Ž.

Ž.

wx

AR

1,

Irr

Irr:

55.0

021.

000

AR

1:

y0.

327

0.05

2U

UU

UŽ.

Ž.

Ž.

Ž.

wx

Ž.

wx

Chi

le3

Stc

lvl,

AR

1,

Lvl

:14

.144

0.14

6,

AR

1:

97.1

081.

000

,L

vl:

2.33

10.

488

,A

R1

:y

0.37

90.

112

0.17

70.

929

0.74

1Ž

.Ir

rIr

r:75

.709

0.78

0U

UŽ

.Ž

.w

xw

xC

olom

bia

5S

tclv

l,F

xdsl

p,L

vl:

3.73

10.

040

,Ir

r:93

.099

1.00

0L

vl:

3.23

71.

310

,S

lp:

0.92

50.

443

–0.

837

0.63

7Ir

rU

UU

UŽ.

Ž.

Ž.

Ž.

wx

Ž.

wx

Ecu

ador

1S

tclv

l,A

R1

Lvl

:7.

728

0.11

5,

AR

1:

67.2

201.

000

Lvl

:2.

974

0.43

6,

AR

1:

0.35

90.

135

0.12

80.

902

0.62

8Ž

.Ž.

Ž.

wxU

Uw

xUU

Jam

aica

6S

tclv

l,F

xdsl

p,L

vl:

2.48

40.

119

,A

R1

:20

.868

1.00

0L

vl:

1.38

20.

418

,S

lp:

0.13

60.

042

,0.

085

0.86

30.

329

UU

Ž.

Ž.

wx

AR

1A

R1

:y

0.22

80.

054

UU

UU

Ž.

Ž.

Ž.

wx

wx

Mex

ico

4S

tclv

l,F

xdsl

p,L

vl:

8.69

30.

146

,A

R1

:59

.691

1.00

0,

Lvl

:1.

508

0.27

9,

Slp

:0.

878

0.26

6,

0.22

30.

877

0.54

1U

UŽ.

Ž.

Ž.

wx

AR

1,

Irr

Irr:

42.9

490.

719

AR

1:

0.36

70.

111

UŽ

.Ž

.w

xU

rugu

ay2

Stc

lvl,

Irr

Lvl

:20

.410

0.26

0,

Irr:

78.5

021.

000

Lvl

:3.

935

1.58

9–

0.89

20.

522

UU

UU

Ž.

Ž.

wx

wx

Ven

ezue

la5

Stc

lvl,

Fxd

slp,

Lvl

:1.

934

0.08

5,

Irr:

22.7

281.

000

Lvl

:3.

093

1.12

1,

Slp

:0.

761

0.22

9–

0.82

30.

638

Irr

Pan

elB

:P

riÕ

ate

port

foli

oB

Fto

Asi

aU

UU

Ž.

Ž.

Ž.

wx

wx

Chi

na4

Stc

lvl,

Fxd

slp,

Lvl

:3.

660

0.04

6,

AR

1:

5.76

40.

073

,L

vl:

1.49

50.

217

,S

lp:

0.84

50.

414

,0.

270

0.73

60.

745

UU

Ž.

Ž.

Ž.

wx

AR

1,

Irr

Irr:

79.3

601.

000

AR

1:

y0.

279

0.09

9U

UU

UŽ.

Ž.

Ž.

Ž.

wx

Ž.

wx

Indi

a3

Stc

lvl,

AR

1,

Lvl

:4.

107

0.08

1,

AR

1:

50.7

121.

000

,L

vl:

5.20

91.

570

,A

R1

:0.

278

0.08

10.

184

0.70

20.

448

Ž.

Irr

Irr:

10.0

830.

199

UU

UŽ

.Ž.

Ž.

wx

wx

Indo

nesi

a4

Stc

lvl,

Fxd

slp,

Lvl

:2.

837

0.03

2,

AR

1:

89.0

941.

000

,L

vl:

1.22

80.

230

,S

lp:

0.89

10.

419

,0.

230

0.79

30.

563

UŽ.

Ž.

Ž.

wx

AR

1,

Irr

Irr:

27.5

290.

309

AR

1:

0.34

20.

142

UU

Ž.

Ž.

Ž.

Ž.

wx

Ž.

wx

Kor

ea3

Stc

lvl,

AR

1,

Lvl

:4.

137

0.21

6,

AR

1:

19.1

601.

000

,L

vl:

6.10

12.

154

,A

R1

:y

0.24

70.

097

0.10

30.

839

0.85

4Ž

.Ir

rIr

r:11

.310

0.59

0U

UU

UŽ.

Ž.

Ž.

Ž.

wx

Ž.

wx

Mal

aysi

a1

Stc

lvl,

AR

1L

vl:

9.48

30.

110

,A

R1

:85

.801

1.00

0L

vl:

1.24

90.

356

,A

R1

:y

0.14

60.

033

0.08

80.

894

0.49

6U

UU

UŽ.

Ž.

Ž.

Ž.

wx

Ž.

wx

Pak

ista

n3

Stc

lvl,

AR

1,

Lvl

:0.

683

0.03

9,

AR

1:

17.4

081.

000

,L

vl:

4.78

11.

636

,A

R1

:0.

172

0.02

40.

091

0.88

40.

647

Ž.

Irr

Irr:

7.52

40.

432

UU

UU

Ž.

Ž.

Ž.

Ž.

wx

Ž.

wx

Phi

lipp

ines

3S

tclv

l,A

R1

,L

vl:

13.1

840.

175

,A

R1

:75

.394

1.00

0,

Lvl

:1.

971

0.34

6,

AR

1:

0.38

40.

116

0.11

20.

931

0.57

2Ž

.Ir

rIr

r:60

.162

0.79

8U

UU

UŽ.

Ž.

Ž.

Ž.

wx

Ž.

wx

Tai

wan

3S

tclv

l,A

R1

,L

vl:

2.26

30.

057

,A

R1

:19

.721

0.49

8,

Lvl

:4.

332

1.65

3,

AR

1:

0.27

50.

069

0.22

50.

863

0.44

1Ž

.Ir

rIr

r:39

.628

1.00

0U

UU

UŽ.

Ž.

Ž.

Ž.

wx

Ž.

wx

Tha

ilan

d1

Stc

lvl,

AR

1L

vl:

6.75

50.

079

,A

R1

:85

.007

1.00

0L

vl:

1.04

40.

354

,A

R1

:y

0.31

30.

118

0.16

80.

942

0.74

6

See

note

sto

Tab

le2.

( )L. Sarno, M.P. TaylorrJournal of DeÕelopment Economics 59 1999 337–364 353

Tab

le4

Kal

man

filt

erre

sult

sfo

rO

F

2Ž

.w

xŽ

.M

odel

Com

pone

nts

Est

imat

edS

Dof

erro

rte

rmQ

-rat

ios

Est

imat

edco

effi

cien

tsof

fina

lst

ate

vect

orR

MS

EE

stim

ated

AR

RL

Bp

para

met

err

n

Pan

elA

:O

Fto

Lat

inA

mer

ica

UU

UU

Ž.

Ž.

Ž.

Ž.

wx

wx

Arg

enti

na4

Stc

lvl,

Fxd

Slp

,L

vl:

11.2

480.

123

,A

R1

:91

.706

1.00

0,

Irr:

69.1

340.

754

Lvl

:2.

848

0.37

9,

Slp

:0.

553

0.11

3,

0.08

90.

765

0.34

9U

UŽ.

Ž.

wx

AR

1,

Irr

AR

1:

0.21

20.

044

UU

UU

Ž.

Ž.

Ž.

Ž.

Ž.

wx

Ž.

wx

Bra

zil

3S

tclv

l,A

R1

,Ir

rL

vl:

35.1

200.

438

,A

R1

:21

.647

0.27

0,

Irr:

80.2

081.

000

Lvl

:1.

798

0.37

8,

AR

1:

y0.

745

0.23

60.

549

0.80

20.

428

UU

UŽ.

Ž.

Ž.

Ž.

Ž.

wx

Ž.

wx

Chi

le3

Stc

lvl,

AR

1,

Irr

Lvl

:6.

149

0.07

0,

AR

1:

88.5

321.

000

,Ir

r:80

.441

0.90

9L

vl:

1.21

40.

483

,A

R1

:0.

910

0.25

50.

765

0.82

10.

471

UU

UU

Ž.

Ž.

Ž.

Ž.

wx

wx

Col

ombi

a4

Stc

lvl,

Fxd

Slp

,L

vl:

15.1

600.

186

,A

R1

:81

.647

1.00

0,

Irr:

54.3

950.

666

Lvl

:4.

441

1.57

8,

Slp

:0.

874

0.31

6,

0.30

10.

793

0.47

8U

UŽ.

Ž.

wx

AR

1,

Irr

AR

1:

y0.

531

0.16

5U

UU

UŽ.

Ž.

Ž.

Ž.

Ž.

wx

Ž.

wx

Ecu

ador

3S

tclv

l,A

R1

,Ir

rL

vl:

12.8

100.

315

,A

R1

:33

.351

0.82

1,

Irr:

40.6

341.

000

Lvl

:1.

236

0.30

1,

AR

1:

0.75

00.

127

0.55

20.

772

0.50

1Ž.

Ž.

Ž.

Ž.

Ž.

wxU

UŽ.

wxU

UJa

mai

ca3

Stc

lvl,

AR

1,

Irr

Lvl

:29

.541

0.46

3,

AR

1:

13.9

110.

218

,Ir

r:63

.860

1.00

0L

vl:

2.55

20.

391

,A

R1

:y

0.81

10.

295

0.77

90.

915

0.26

7U

UU

Ž.

Ž.

Ž.

Ž.

Ž.

wx

Ž.

wx

Mex

ico

3S

tclv

l,A

R1

,Ir

rL

vl:

17.4

230.

553

,A

R1

:18

.227

0.57

8,

Irr:

31.5

081.

000

Lvl

:1.

906

0.75

7,

AR

1:

0.55

30.

160

0.37

40.

837

0.65

2U

UU

UŽ.

Ž.

Ž.

Ž.

Ž.

wx

Ž.

wx

Uru

guay

3S

tclv

l,A

R1

,Ir

rL

vl:

6.65

70.

175

,A

R1

:38

.014

1.00

0,

Irr:

32.8

530.

864

Lvl

:4.

531

1.26

3,

AR

1:

y0.

248

0.03

20.

100

0.72

50.

205

UU

UŽ.

Ž.

Ž.

Ž.

Ž.

wx

Ž.

wx

Ven

ezue

la3

Stc

lvl,

AR

1,

Irr

Lvl

:54

.921

0.60

2,

AR

1:

82.9

070.

909

,Ir

r:91

.185

1.00

0L

vl:

3.37

91.

396

,A

R1

:0.

103

0.03

20.

071

0.79

20.

667

Pan

elB

:O

Fto

Asi

aU

UU

UŽ

.Ž.

Ž.

Ž.

wx

wx

Chi

na4

Stc

lvl,

Fxd

Slp

,L

vl:

12.4

960.

199

,A

R1

:62

.712

1.00

0,

Irr:

36.0

480.

575

Lvl

:3.

090

0.45

9,

Slp

:0.

645

0.12

7,

0.38

50.

736

0.32

8U

Ž.

Ž.

wx

AR

1,

Irr

AR

1:

0.49

10.

125

UU

UU

Ž.

Ž.

Ž.

Ž.

wx

Ž.

wx

Indi

a1

Stc

lvl,

AR

1L

vl:

18.1

410.

410

,A

R1

:44

.243

1.00

0L

vl:

1.68

80.

204

,A

R1

:0.

499

0.10

40.

328

0.79

20.

394

Ž.

Ž.

Ž.

Ž.

wxU

UŽ.

wxU

UIn

done

sia

2S

tclv

l,Ir

rL

vl:

11.7

080.

605

,Ir

r:19

.351

1.00

0,

AR

1:

5.28

30.

273

Lvl

:1.

090

0.29

6,

AR

1:

0.56

10.

137

0.23

60.

934

0.64

0U

UU

UŽ.

Ž.

Ž.

Ž.

wx

Ž.

wx

Kor

ea1

Stc

lvl,

AR

1L

vl:

10.0

950.

302

,A

R1

:33

.460

1.00

0L

vl:

1.62

60.

482

,A

R1

:0.

555

0.16

50.

147

0.87

40.

374

UU

UŽ.

Ž.

Ž.

Ž.

Ž.

wx

Ž.

wx

Mal

aysi

a3

Stc

lvl,

AR

1,

Irr

Lvl

:11

.708

0.27

7,

AR

1:

42.2

901.

000

,Ir

r:38

.466

0.91

0L

vl:

3.73

91.

642

,A

R1

:0.

908

0.28

70.

605

0.87

70.

547

UU

UU

Ž.

Ž.

Ž.

Ž.

Ž.

wx

Ž.

wx

Pak

ista

n3

Stc

lvl,

AR

1,

Irr

Lvl

:8.

512

0.09

4,

AR

1:

15.1

020.

168

,Ir

r:90

.089

1.00

0L

vl:

1.17

60.

433

,A

R1

:y

0.32

90.

119

0.10

70.

736

0.74

3U

UU

Ž.

Ž.

Ž.

Ž.

Ž.

wx

Ž.

wx

Phi

lipp

ines

3S

tclv

l,A

R1

,Ir

rL

vl:

21.6

690.

375

,A

R1

:53

.182

0.92

0,

Irr:

57.8

331.

000

Lvl

:3.

171

1.27

7,

AR

1:

0.79

60.

189

0.56

00.

883

0.91

2U

UU

UŽ.

Ž.

Ž.

Ž.

wx

Ž.

wx

Tai

wan

1S

tclv

l,A

R1

Lvl

:29

.545

0.30

0,

AR

1:

98.4

481.

000

Lvl

:1.

682

0.55

3,

AR

1:

0.38

20.

076

0.20

80.

832

0.43

5Ž.

Ž.

Ž.

Ž.

Ž.

wxU

UŽ.

wxU

UT

hail

and

3S

tclv

l,A

R1

,Ir

rL

vl:

6.20

40.

246

,A

R1

:25

.250

1.00

0,

Irr:

17.1

920.

681

Lvl

:2.

922

0.65

8,

AR

1:

0.57

30.

194

0.42

60.

821

0.63

1

See

note

sto

Tab

le2.

( )L. Sarno, M.P. TaylorrJournal of DeÕelopment Economics 59 1999 337–364354

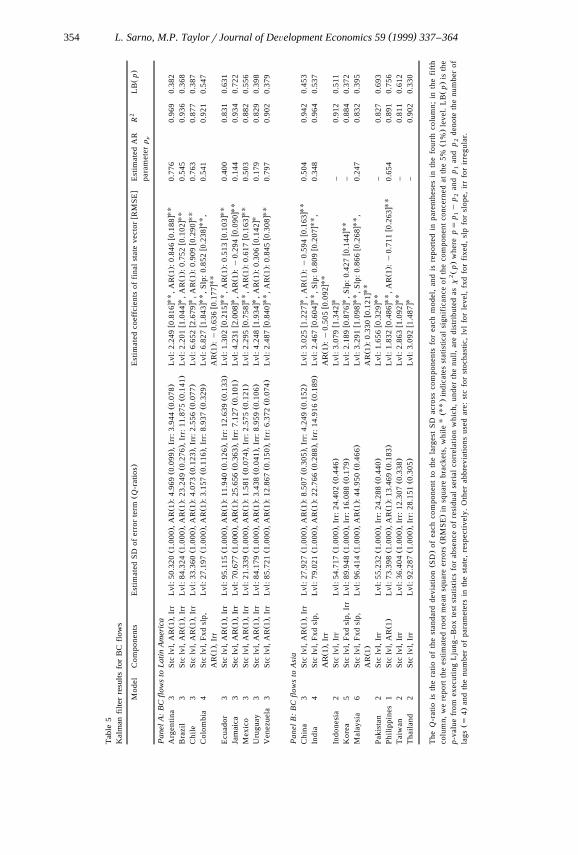

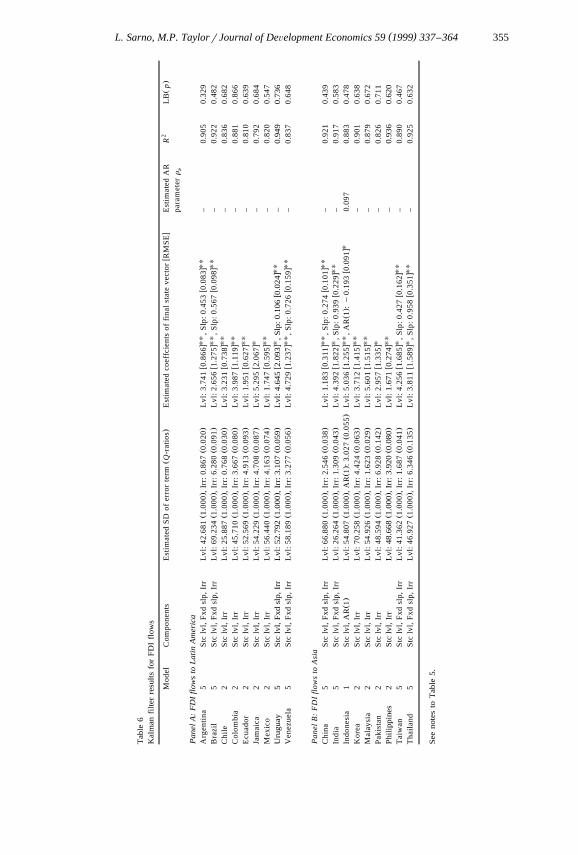

Tab

le5

Kal

man

filt

erre

sult

sfo

rB

Cfl

ows

2Ž

.w

xŽ

.M

odel

Com

pone

nts

Est

imat

edS

Dof

erro

rte

rmQ

-rat

ios

Est

imat

edco

effc

ient

sof

fina

lst

ate

vect

orR

MS

EE

stim

ated

AR

RL

Bp

para

met

err

n

Pan

elA

:B

Cfl

ows

toL

atin

Am

eric

aU

UU

UŽ.

Ž.

Ž.

Ž.

Ž.

wx

Ž.

wx

Arg

enti

na3

Stc

lvl,

AR

1,

Irr

Lvl

:50

.320

1.00

0,

AR

1:

4.96

90.

099

,Ir

r:3.

944

0.07

8L

vl:

2.24

90.

816

,A

R1

:0.

846

0.18

80.

776

0.96

90.

382

UU

UŽ.

Ž.

Ž.

Ž.

Ž.

wx

Ž.

wx

Bra

zil

3S

tclv

l,A

R1

,Ir

rL

vl:

84.3

241.

000

,A

R1

:23

.249

0.27

6,

Irr:

11.8

750.

141

Lvl

:2.

201

1.04

4,

AR

1:

0.75

20.

102

0.54

50.

936

0.36

8U

UU

Ž.

Ž.

Ž.

Ž.

Ž.

wx

Ž.

wx

Chi

le3

Stc

lvl,

AR

1,

Irr

Lvl

:33

.360

1.00

0,

AR

1:

4.07

30.

123

,Ir

r:2.

556

0.07

7L

vl:

6.65

22.

679

,A

R1

:0.

909

0.29

00.

763

0.87

70.

387

UU

UU

Ž.

Ž.

Ž.

Ž.

wx

wx

Col

ombi

a4

Stc

lvl,

Fxd

slp,

Lvl

:27

.197

1.00

0,

AR

1:

3.15

70.

116

,Ir

r:8.

937

0.32

9L

vl:

6.82

71.

843

,S

lp:

0.85

20.

238

,0.

541

0.92

10.

547

UU

Ž.

Ž.

wx

AR

1,

Irr

AR

1:

y0.

636

0.17

7U

UU

UŽ.

Ž.

Ž.

Ž.

Ž.

wx

Ž.

wx

Ecu

ador

3S

tclv

l,A

R1

,Ir

rL

vl:

95.1

151.

000

,A

R1

:11

.940

0.12

6,

Irr:

12.6

390.

133

Lvl

:1.

302

0.21

5,

AR

1:

0.51

30.

103

0.40

00.

831

0.63

1Ž.

Ž.

Ž.

Ž.

Ž.

wxU

Ž.

wxU

UJa

mai

ca3

Stc

lvl,

AR

1,

Irr

Lvl

:70

.677

1.00

0,

AR

1:

25.6

560.

363

,Ir

r:7.

127

0.10

1L

vl:

4.23

12.

008

,A

R1

:y

0.29

40.

090

0.14

40.

934

0.72

2U

UU

UŽ.

Ž.

Ž.

Ž.

Ž.

wx

Ž.

wx

Mex

ico

3S

tclv

l,A

R1

,Ir

rL

vl:

21.3

391.

000

,A

R1

:1.

581

0.07

4,

Irr:

2.57

50.

121

Lvl

:2.

295

0.75

8,

AR

1:

0.61

70.

163

0.50

30.

882

0.55

6U

UŽ.

Ž.

Ž.

Ž.

Ž.

wx

Ž.

wx

Uru

guay

3S

tclv

l,A

R1

,Ir

rL

vl:

84.1

791.

000

,A

R1

:3.

438

0.04

1,

Irr:

8.95

90.

106

Lvl

:4.

248

1.93

4,

AR

1:

0.30

60.

142

0.17

90.

829

0.39

8U

UU

UŽ.

Ž.

Ž.

Ž.

Ž.

wx

Ž.

wx

Ven

ezue

la3

Stc

lvl,

AR

1,

Irr

Lvl

:85

.721

1.00

0,

AR

1:

12.8

670.

150

,Ir

r:6.

372

0.07

4L

vl:

2.48

70.

840

,A

R1

:0.

845

0.30

80.

797

0.90

20.

379

Pan

elB

:B

Cfl

ows

toA

sia

UU

UŽ.

Ž.

Ž.

Ž.

Ž.

wx

Ž.

wx

Chi

na3

Stc

lvl,

AR

1,

Irr

Lvl

:27

.927

1.00

0,

AR

1:

8.50

70.

305

,Ir

r:4.

249

0.15

2L

vl:

3.02

51.

227

,A

R1

:y

0.59

40.

163

0.50

40.

942

0.45

3U

UU

UŽ

.Ž.

Ž.

Ž.

wx

wx

Indi

a4

Stc

lvl,

Fxd

slp,

Lvl

:79

.021

1.00

0,

AR

1:

22.7

660.

288

,Ir

r:14

.916

0.18

9L

vl:

2.46

70.

604

,S

lp:

0.80

90.

207

,0.

348

0.96

40.

537

Ž.

Ž.

wxU

UA

R1

,Ir

rA

R1

:y

0.50

50.

092

UŽ

.Ž

.w

xIn

done

sia

2S

tclv

l,Ir

rL

vl:

54.7

171.

000

,Ir

r:24

.402

0.44

6L

vl:

3.07

91.

342

–0.

912

0.51

1U

UU

Ž.

Ž.

wx

wx

Kor

ea5

Stc

lvl,

Fxd

slp,

Irr

Lvl

:89

.948

1.00

0,

Irr:

16.0

880.

179

Lvl

:2.

189

0.87

6,

Slp

:0.

427

0.14

4–

0.88

40.

372

UU

UU

Ž.

Ž.

Ž.

wx

wx

Mal

aysi

a6

Stc

lvl,

Fxd

slp,

Lvl

:96

.414

1.00

0,

AR

1:

44.9

500.

466

Lvl

:3.

291

1.09

8,

Slp

:0.

866

0.26

8,

0.24

70.

832

0.39

5U

UŽ.

Ž.

wx

AR

1A

R1

:0.

330

0.12

1U

UŽ

.Ž

.w

xP

akis

tan

2S

tclv

l,Ir

rL

vl:

55.2

321.

000

,Ir

r:24

.288

0.44

0L

vl:

1.65

60.

329

–0.

827

0.69

3U

UU

UŽ.

Ž.

Ž.

Ž.

wx

Ž.

wx

Phi

lipp

ines

1S

tclv

l,A

R1

Lvl

:73

.398

1.00

0,

AR

1:

13.4

690.

183

Lvl

:1.

832

0.48

6,

AR

1:

y0.

711

0.26

30.

654

0.89

10.

756

UU

Ž.

Ž.

wx

Tai

wan

2S

tclv

l,Ir

rL

vl:

36.4

041.

000

,Ir

r:12

.307

0.33

8L

vl:

2.86

31.

092

–0.

811

0.61

2U

Ž.

Ž.

wx

Tha

ilan

d2

Stc

lvl,

Irr

Lvl

:92

.287

1.00

0,

Irr:

28.1

510.

305

Lvl

:3.

092

1.48

7–

0.90

20.

330

Ž.

The

Q-r

atio

isth

era

tio

ofth

est

anda

rdde