HospitalsDecember 04, 2019 - ICICI Direct

65

ICICI Securities – Retail Equity Research Sector Report Hospitals December 10, 2019 Opportunities beckon in hospitals space… In the last three to four years, with many frontline large cap pharma companies being hampered by structural US related & other issues, we have seen growing investors’ preference for healthcare services providers. At the same time, as many as four hospitals and three diagnostic companies got listed on the bourses, thus providing a much larger basket for investors. Some peculiar factors responsible for growing interest in the hospitals space are: 1) waning high capex episodes of private hospitals after the 2008-18 capex cycle, 2) shifting focus towards assets light model for most hospital players, 3) improving financial matrix, 4) government’s endeavour to bring private players on board in the wake holistic view of universal and affordable healthcare (themes like NHP 2017 and Ayushman Bharat), 5) India’s emergence as the destination for medical tourism and 6) the underserved situation of Indian hospitals compared to the growing needs and demographic changes well documented by new and existing players. Taking into account all the headwinds and tailwinds, we believe the sector is yet to witness the fullest realisation of its potential as scepticism about the capital intensiveness is yet to wane. Apollo Hospitals Enterprise Ltd. (Apollo), the sector leader by far, remains a preferred bet from the sector with a calibrated improvement in margins and return ratios on the back of effective utilisation of both existing and new hospitals. In the Indian multispecialty category, we like Apollo due to 1) one of the best integrated business models in the healthcare space with strong management pedigree, 2) ability to balance between expansion and profitability, 3) near completion of the long capex cycle and a determined focus on improvement in margins and return ratios. Similarly, we also prefer Narayana Hrudayalaya Ltd. (Narayana) on account of 1) asset-right model and affordability philosophy, 2) ability to adapt to the requirement where affordability does not work, 3) moderation of capex and focus on return ratios and 4) traction from HCCI Cayman. Among others, we have a BUY rating on Aster DM healthcare (Aster), which is the only hospital chain having higher outside India presence, on the back of 1) significant presence in the Gulf Cooperation Council (GCC) (Middle East) region with a strong pedigree and return ratios, 2) calibrated approach in India growth, 3) unique ecosystem banking on GCC presence and India expansion besides labour arbitrage. We have a HOLD rating on Healthcare Global Enterprises (HCG) as we believe the positives 1) comprehensive cancer treatment network with strong pedigree, 2) overall potential of cancer as a treatment category, 3) established presence in IVF treatment are getting mitigated by concerns on account of weak leverage and return ratios. Similarly, we have a HOLD rating on Shalby Ltd (Shalby) as positive aspects 1) brand loyalty in joint replacement, 2) calibrated expansion in other procedures and geographies to de-risk and 3) leverage free balance sheet are slightly undone by asset concentration risk. Lastly, we keep Fortis Healthcare (Fortis) Under Review due to the pending litigation in some aspects. Key Financial Summary Company CMP TP Rating M Cap (|) (|) (| cr) FY19 FY20E FY21E FY22E FY19 FY20E FY21E FY22E FY19 FY20E FY21E FY22E FY19 FY20E FY21E FY22E Apollo Hospitals 1466 1,800 Buy 20401 17.0 25.3 43.7 68.1 22.2 14.0 11.4 9.5 8.8 11.4 14.8 17.5 1.1 0.9 0.7 0.4 Narayana Hrudalaya 304 360 Buy 6213 2.9 7.2 9.8 13.3 24.1 15.7 13.5 11.1 7.7 12.0 13.9 16.5 0.8 0.7 0.5 0.3 Aster DM Healthcare 154 210 Buy 7786 6.6 5.0 8.9 13.5 11.9 8.7 7.2 5.8 8.3 8.4 10.3 12.3 0.9 0.9 0.7 0.5 Healthcare Global 101 110 Hold 898 -2.8 -11.0 -7.9 -4.0 13.8 15.5 12.5 9.6 3.0 1.2 2.5 4.3 1.4 3.6 4.2 4.5 Shalby Limited 103 110 Hold 1109 2.9 4.4 5.4 6.8 13.5 10.8 9.0 7.6 6.8 7.9 9.1 10.5 0.1 0.1 0.1 0.1 EPS (|) EV/EBITDA(x) RoCE (%) Debt/Equity (x) Source: ICICI Direct Research; Company Apollo Hospitals -- Maintain BUY TP -- | 1800 (existing hospitals at 13x FY22E EV/EBITDA, new hospitals and pharmacies at 1.5x FY22E EV/sales) Narayana – Maintain BUY –TP | 360 (mature hospitals and Cayman Islands at 8x FY22E EV/EBITDA, new hospitals at 1.5x FY22E EV/sales and other business at 1.5x FY22E EV/sales) Aster DM – Initiate with BUY -- TP | 210 (Mature hospitals (GCC & India) at 8x FY22E EV/EBITDA, new hospitals(GCC & India), clinics and pharmacies at 1x FY22E EV/sales) HCG– Initiate with HOLD -- TP | 110 (hospitals and Milan at 10x FY22E EV/EBITDA) Shalby Ltd – Initiate with HOLD -- TP | 110 (more than six years hospitals 8x of FY22E EV/EBITDA, less than six years hospitals at 1x FY22E EV/sales) Maintain Under review on Fortis Research Analyst Siddhant Khandekar [email protected] Mitesh Shah, CFA [email protected] Sudarshan Agarwal [email protected]

Transcript of HospitalsDecember 04, 2019 - ICICI Direct

ICIC

I S

ecurit

ies –

Retail E

quit

y R

esearch

Sector R

eport

Hospitals

December 10, 2019

Opportunities beckon in hospitals space…

In the last three to four years, with many frontline large cap pharma

companies being hampered by structural US related & other issues, we have

seen growing investors’ preference for healthcare services providers. At the

same time, as many as four hospitals and three diagnostic companies got

listed on the bourses, thus providing a much larger basket for investors.

Some peculiar factors responsible for growing interest in the hospitals space

are: 1) waning high capex episodes of private hospitals after the 2008-18

capex cycle, 2) shifting focus towards assets light model for most hospital

players, 3) improving financial matrix, 4) government’s endeavour to bring

private players on board in the wake holistic view of universal and affordable

healthcare (themes like NHP 2017 and Ayushman Bharat), 5) India’s

emergence as the destination for medical tourism and 6) the underserved

situation of Indian hospitals compared to the growing needs and

demographic changes well documented by new and existing players.

Taking into account all the headwinds and tailwinds, we believe the sector

is yet to witness the fullest realisation of its potential as scepticism about the

capital intensiveness is yet to wane. Apollo Hospitals Enterprise Ltd.

(Apollo), the sector leader by far, remains a preferred bet from the sector

with a calibrated improvement in margins and return ratios on the back of

effective utilisation of both existing and new hospitals. In the Indian

multispecialty category, we like Apollo due to 1) one of the best integrated

business models in the healthcare space with strong management pedigree,

2) ability to balance between expansion and profitability, 3) near completion

of the long capex cycle and a determined focus on improvement in margins

and return ratios. Similarly, we also prefer Narayana Hrudayalaya Ltd.

(Narayana) on account of 1) asset-right model and affordability philosophy,

2) ability to adapt to the requirement where affordability does not work, 3)

moderation of capex and focus on return ratios and 4) traction from HCCI

Cayman.

Among others, we have a BUY rating on Aster DM healthcare (Aster), which

is the only hospital chain having higher outside India presence, on the back

of 1) significant presence in the Gulf Cooperation Council (GCC) (Middle

East) region with a strong pedigree and return ratios, 2) calibrated approach

in India growth, 3) unique ecosystem banking on GCC presence and India

expansion besides labour arbitrage. We have a HOLD rating on Healthcare

Global Enterprises (HCG) as we believe the positives 1) comprehensive

cancer treatment network with strong pedigree, 2) overall potential of cancer

as a treatment category, 3) established presence in IVF treatment are getting

mitigated by concerns on account of weak leverage and return ratios.

Similarly, we have a HOLD rating on Shalby Ltd (Shalby) as positive aspects

1) brand loyalty in joint replacement, 2) calibrated expansion in other

procedures and geographies to de-risk and 3) leverage free balance sheet

are slightly undone by asset concentration risk. Lastly, we keep Fortis

Healthcare (Fortis) Under Review due to the pending litigation in some

aspects.

Key Financial Summary

Company CMP TP Rating M Cap

(|) (|) (| cr) FY19 FY20E FY21E FY22E FY19 FY20E FY21E FY22E FY19 FY20E FY21E FY22E FY19 FY20E FY21E FY22E

Apollo Hospitals 1466 1,800 Buy 20401 17.0 25.3 43.7 68.1 22.2 14.0 11.4 9.5 8.8 11.4 14.8 17.5 1.1 0.9 0.7 0.4

Narayana Hrudalaya 304 360 Buy 6213 2.9 7.2 9.8 13.3 24.1 15.7 13.5 11.1 7.7 12.0 13.9 16.5 0.8 0.7 0.5 0.3

Aster DM Healthcare 154 210 Buy 7786 6.6 5.0 8.9 13.5 11.9 8.7 7.2 5.8 8.3 8.4 10.3 12.3 0.9 0.9 0.7 0.5

Healthcare Global 101 110 Hold 898 -2.8 -11.0 -7.9 -4.0 13.8 15.5 12.5 9.6 3.0 1.2 2.5 4.3 1.4 3.6 4.2 4.5

Shalby Limited 103 110 Hold 1109 2.9 4.4 5.4 6.8 13.5 10.8 9.0 7.6 6.8 7.9 9.1 10.5 0.1 0.1 0.1 0.1

EPS (|) EV/EBITDA(x) RoCE (%) Debt/Equity (x)

Source: ICICI Direct Research; Company

Apollo Hospitals -- Maintain

BUY TP -- | 1800 (existing

hospitals at 13x FY22E

EV/EBITDA, new hospitals and

pharmacies at 1.5x FY22E

EV/sales)

Narayana – Maintain BUY –TP

| 360 (mature hospitals and

Cayman Islands at 8x FY22E

EV/EBITDA, new hospitals at

1.5x FY22E EV/sales and other

business at 1.5x FY22E

EV/sales)

Aster DM – Initiate with BUY --

TP | 210 (Mature hospitals

(GCC & India) at 8x FY22E

EV/EBITDA, new

hospitals(GCC & India), clinics

and pharmacies at 1x FY22E

EV/sales)

HCG– Initiate with HOLD -- TP

| 110 (hospitals and Milan at

10x FY22E EV/EBITDA)

Shalby Ltd – Initiate with HOLD

-- TP | 110 (more than six

years hospitals 8x of FY22E

EV/EBITDA, less than six years

hospitals at 1x FY22E EV/sales)

Maintain Under review on

Fortis

Research Analyst

Siddhant Khandekar

Mitesh Shah, CFA

Sudarshan Agarwal

ICICI Securities | Retail Research 2

ICICI Direct Research Sector Report | Hospitals

Indian healthcare not just about Pharma…

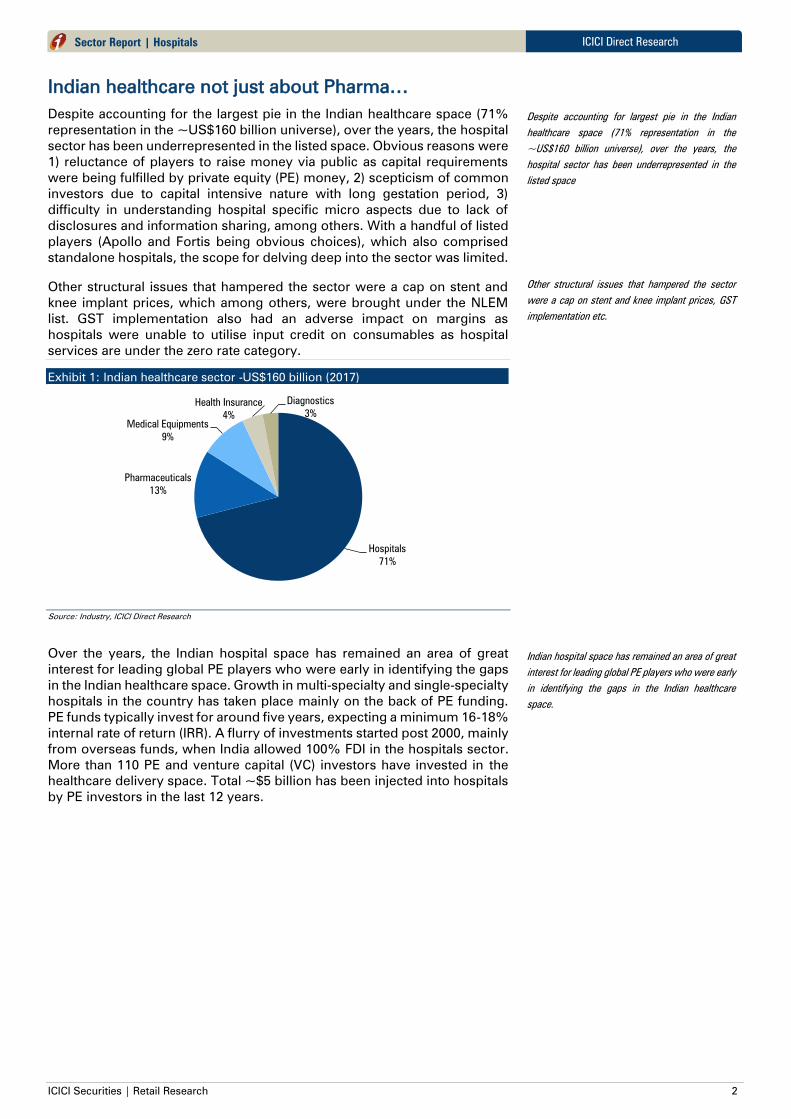

Despite accounting for the largest pie in the Indian healthcare space (71%

representation in the ~US$160 billion universe), over the years, the hospital

sector has been underrepresented in the listed space. Obvious reasons were

1) reluctance of players to raise money via public as capital requirements

were being fulfilled by private equity (PE) money, 2) scepticism of common

investors due to capital intensive nature with long gestation period, 3)

difficulty in understanding hospital specific micro aspects due to lack of

disclosures and information sharing, among others. With a handful of listed

players (Apollo and Fortis being obvious choices), which also comprised

standalone hospitals, the scope for delving deep into the sector was limited.

Other structural issues that hampered the sector were a cap on stent and

knee implant prices, which among others, were brought under the NLEM

list. GST implementation also had an adverse impact on margins as

hospitals were unable to utilise input credit on consumables as hospital

services are under the zero rate category.

Exhibit 1: Indian healthcare sector -US$160 billion (2017)

Source: Industry, ICICI Direct Research

Over the years, the Indian hospital space has remained an area of great

interest for leading global PE players who were early in identifying the gaps

in the Indian healthcare space. Growth in multi-specialty and single-specialty

hospitals in the country has taken place mainly on the back of PE funding.

PE funds typically invest for around five years, expecting a minimum 16-18%

internal rate of return (IRR). A flurry of investments started post 2000, mainly

from overseas funds, when India allowed 100% FDI in the hospitals sector.

More than 110 PE and venture capital (VC) investors have invested in the

healthcare delivery space. Total ~$5 billion has been injected into hospitals

by PE investors in the last 12 years.

Hospitals

71%

Pharmaceuticals

13%

Medical Equipments

9%

Health Insurance

4%

Diagnostics

3%

Despite accounting for largest pie in the Indian

healthcare space (71% representation in the

~US$160 billion universe), over the years, the

hospital sector has been underrepresented in the

listed space

Other structural issues that hampered the sector

were a cap on stent and knee implant prices, GST

implementation etc.

Indian hospital space has remained an area of great

interest for leading global PE players who were early

in identifying the gaps in the Indian healthcare

space.

ICICI Securities | Retail Research 3

ICICI Direct Research

Sector Report | Hospitals

Exhibit 2: Key PE deals in healthcare segment (above US$50 million)

Company US$ mn Key investors Date

Radiant Life Care 200 KKR July ’17

Condis Healthcare 200 India Value Fund Mar ’17

Manipal Health Enterprises 171 Temasek Mar ’17

Max Healthcare Institute 75 IFC May ’17

Vijaya Diagnostic Centre 63.5 Kedaara Capital Dec ’16

Apollo Health & Lifestyle 68 IFC May ’16

Care Hospitals 221 Abraaj Group Jan ’16

Cloud Nine 60.5 India Value Fund Dec ’15

Metropolis Healthcare 127.5 Carlyle Sep ’15

Metropolis Healthcare* 90 KKR Apr ’15

Sutures India 60 TPG Growth Feb ’15

Manipal Health Enterprises 150 TPG Capital Jan ’15

Medanta Medicity 113.5 Temasek Jan ’15

Aster DM Healthcare 60 India Value Fund, Olympus Capital May ’14

Source: Bloomberg, ICICI Direct Research

Perception is changing, courtesy availability of options

with stock specific peculiarities and improving (albeit

slowly) industry dynamics…

Cut to 2017-19, with many frontline large cap pharma companies being

hampered by structural US related and other issues, we have seen growing

investors’ preference for hospitals. During the same time, as many as four

hospitals got listed on the bourses, thus providing a much larger basket for

investors.

Some crucial factors supplementing the growing interest in the hospitals

space are 1) waning high-capex episodes of private hospitals after the 2008-

18 capex cycle, 2) shift towards assets light model, 3) government’s

endeavour to bring private players on board in the wake of the holistic view

of universal and affordable healthcare (themes such as NHP 2017 and

Ayushman Bharat), 4) India’s emergence as the destination for medical

tourism and lastly, 5) the legacy argument of the underserved situation of

Indian hospitals compared to other developed and developing economies

well documented by new and existing players.

Waning capex and focus on assets light model

Multi-specialty healthcare is a highly capital intensive business on account

of the real estate involved in setting up facilities as well as the money

required for medical equipment and hiring of skilled staff. It takes at least

one and a half to three years for green-field projects to reach operational

break-even.

What is also driving investors’ interest is the shift (albeit slowly) from capital

intensive to asset-light model with minimal locking of the capital. Preference

is also shifting towards hospital chains from standalone hospitals as the

former provides a better return profile on the back of a portfolio of hospitals.

With many frontline large cap pharma companies

being hampered by structural US related and other

issues, we have seen growing investors’ preference

for hospitals and diagnostic players

Crucial factors supplementing the growing interest

in the hospitals space are: 1) waning high-capex

episodes, 2) shift towards asset light model, 3)

government’s endeavour to bring private players on

board (themes such as NHP 2017 and Ayushman

Bharat), 4) medical tourism and 5) the underserved

situation of Indian hospitals

Multi-specialty healthcare is a highly capital

intensive business

Shift (albeit slowly) from capital intensive to asset-

light model with minimal locking of the capital is also

driving interest.

ICICI Securities | Retail Research 4

ICICI Direct Research Sector Report | Hospitals

Exhibit 3: Industry dynamics (select pack)

(| crore) FY16 FY17 FY18 FY19 FY20E FY21E FY22E

Revenue 13,953.0 16,088.2 18,452.8 21,878.1 25,269.8 28,302.8 31,562.5

EBITDA 1,447.4 1,465.8 1,810.7 2,409.1 3,511.6 4,132.4 4,790.8

Depreciation 638.4 789.9 851.0 957.6 1,490.4 1,572.1 1,651.5

Other income 68.6 93.0 121.4 102.4 127.8 168.1 201.8

Capex 1,885.3 2,254.5 2,007.7 1,984.9 3,833.4 1,055.0 960.0

Gross FA 9,953.7 11,653.6 13,839.4 15,601.7 19,575.1 20,855.1 22,015.1

Capital employed 13,857.2 15,564.7 17,683.7 19,272.8 22,827.3 22,874.3 23,394.6

Asset Turnover(x) 1.4 1.4 1.3 1.4 1.3 1.4 1.4

ROCE (%) 6.3% 4.9% 6.1% 8.1% 9.4% 11.9% 14.3%

Source: Company, ICICI Direct Research

Besides National Health Protection (NHP) and Pradhan Mantri Jan Arogya

Yojana (PMJAY), the government’s decision to accord industry status has

paved the way for private players to expand in Tier II and Tier III cities as the

government has proposed to provide viability gap funding (VGF) of up to

40% of total cost and will also provide gap funding of up to 50% of tax on

capital cost.

Government initiatives

We see serious government endeavour to narrow down the healthcare gaps

with concentrated efforts. Although it is early days (NHP – 2017; Ayushman

Bharat 2018) with lots of unconnected dots, we believe private hospitals can

look at increasing volumes to improve financials. Although most of the

managements remain sceptical about the scheme (main bone of contention

is the low procedural rates quoted in the scheme), the government has

indicated its intention to consider these issues. Note that these kinds of

nationwide health schemes take years to become feasible for all

stakeholders [a case in point is National Health Service (NHS) of UK].

Exhibit 4: Total healthcare expenditure (as % of GDP) (India includes private sector)

Source: *CY15 data, Crisil; WHO database; ICICI Direct Research

NHP 2017- Government recognition for private sector capability

National Health Policy (NHP) 2017 has effectively charted out three clear

objectives - progressively achieve universal health coverage, reinforce trust

in public healthcare system and complement the growth of the private

healthcare sector with public health goal. The roadmap to involve the private

sector to address the shortcomings of government driven health deliveries

is by far the most important outcome of the new policy. It does acknowledge

the extremely poor spending by the state and inability to cover the entire

spectrum of healthcare needs through increased public investment, which

6

9

5

4

3

4 4

10

17

6

0

2

4

6

8

10

12

14

16

18

Russia Brazil China India Indonesia Malaysia Thailand UK US Vietnam

Besides NHP and PMJAY, the government’s

decision to accord industry status has paved the

way for private players to expand in Tier II and Tier

III cities

We see serious government endeavour to narrow

down the healthcare gaps with concentrated efforts,

although it is early days (NHP – 2017; Ayushman

Bharat 2018)

NHP 2017 has effectively charted out three clear

objectives - progressively achieve universal health

coverage, reinforce trust in public healthcare system

and complement the growth of the private

healthcare sector with public health goal

Guided reduction in capex by

almost all listed players

ICICI Securities | Retail Research 5

ICICI Direct Research Sector Report | Hospitals

has led to a rise in the out-of-pocket expenditure and consequent

impoverishment. It advocates a shift from a primary focus on garnering

additional financial resources from the private sector or subsidising it, to an

approach in which there is a well-defined service delivery partnership

between the government, as purchaser, and private sector, as a provider.

Exhibit 5: Out of pocket healthcare spend as percentage of total healthcare

expenditure

Source: Crisil; WHO Database; ICICI Direct Research

The policy explains the need for coordination with private sector enterprises

by giving statistical instances. The private sector accounts for 90% of all

hospitals (up from 8% in 1947), 60% of all beds, and 80-85% of all doctors.

Over 70% of an ailing population in rural areas and almost 80% in urban

areas utilise private facilities. As much as 75% of outpatient (OPD) care is

exclusively private while more than 55% of inpatient (IPD) care is sought

from private hospitals in India.

Exhibit 6: Share in total health market

Source: Company; ICICI Direct Research

Ayushman Bharat

Under the National Health Policy 2017, Ayushman Bharat - Pradhan Mantri

Jan Arogya Yojana (AB-PMJAY) was launched on September 23, 2018 as

the secondary/tertiary care arm of Ayushman Bharat. The programme,

devised to prevent impoverishment due to catastrophic health expenses,

aims to provide annual health insurance of | 5 lakh/family to over 10.74 crore

families (~50 crore individuals) listed as per “deprivation” in the socio-

economic caste census.

28

1115

65

3236

50

43

12

0

20

40

60

80

Brazil US UK India China Malaysia Indonesia Vietnam Thailand

Private Hospitals

80%

Public Hospitals

20%

Ayushman Bharat scheme aims to provide annual

health insurance of | 5 lakh per family to over 10.74

crore families (~50 crore individuals) listed as per

“deprivation” in the socio-economic caste census

ICICI Securities | Retail Research 6

ICICI Direct Research Sector Report | Hospitals

Exhibit 7: Average cost of treatment (|) in large hospitals & insurance schemes

Source: Crisil; IRDAI, Ayushman Bharat; ICICI Direct Research

The scheme has been implemented in 32 states and UTs. Two states that

are yet to adopt the PMJAY are Odisha and Telangana. West Bengal enrolled

in the scheme but opted out later. PM-JAY has also provided flexibility to

states/UTs to choose their own Ayushman implementation model.

• 17 states/UT are implementing via trust mode,

• nine states/UTs via insurance mode and

• six states/UTs using the mixed mode

Exhibit 8: PMJAY progress

Sep-18 Oct-18 Nov-18 Dec-18 Jun-19 Sep-19

Hospitals empanelled (nos) 13741 14778 15104 16134 15839 18236

Beneficiaries admitted (nos) 25407 144924 386924 685807 3152505 4640000

eCards issued (nos) 42352 339613 1116154 4038450 40185659 103000000

Hospitalisation benefits availed (| Cr) 41.6 225.2 531.3 912.1 3078 7500

Progress of Ayushman Bharat (cumulative)

Source: Ayushman Bharat website, ICICI Direct research

Recently, the government has also increased allocation to AB to | 6,400

crore under the healthcare budget for FY20. As per the PMJAY website (till

September 22, 19) 18,000+ hospitals have already been empanelled, more

than ~4.6 million beneficiaries have availed treatment and more than 10.3

crore e-cards have been issued under AB-PMJAY. The procedure charges

(some private players allege that the quoted procedure charges are even

lower than CGHS, GIPSA rates and lower than marginal costs) and

implementation of the scheme still entail unresolved issues. However,

officials of the scheme are looking at these aspects with continuous

discussion involving hospitals, industry groups & service providers and are

open to revising rates. The officials expect | 8000 crore allocation towards

PMJAY in the forthcoming Union Budget to shore up the financials further.

155,142

140,244

136,562

96,164

84,335

70,702

44,281

28,453

16,108

8,885

4,825

- 20,000 40,000 60,000 80,000 100,000 120,000 140,000 160,000 180,000

Max Healthcare

Fortis Healthcare

Apollo Hospitals

Narayana Health

Shalby

HCG

Individual schemes

Corporate schemes

Ayushman Bharat

State schemes

RSBY

Ayushman Bharat scheme has been implemented in

32 states & UTs

Total 18,000+ hospitals have already been

empanelled under PMJAY Yojana. More than ~4.6

million beneficiaries have availed treatment while

more than 10.3 crore e-cards have been issued

under AB-PMJAY

ICICI Securities | Retail Research 7

ICICI Direct Research Sector Report | Hospitals

Exhibit 9: Management quotes on Ayushman Bharat

Source: ICICI Direct Research, Company

Medical tourism- Another key focus area

Another important factor is the growing medical tourism concept, which can

be the X-factor for assets in metros and Tier 1 cities as companies keep on

adding tertiary and quaternary care hospitals. The government’s steps such

as visa on arrival and medical visa have made the modalities of admitting

foreign patients a lot easier.

Over the years, India has grown to become a top notch destination for

medical value travel because it scores high over a range of factors that

determine the overall quality of care. From quality of therapy, range of

procedural and treatment options, infrastructure and skilled manpower to

perform any medical procedure with zero waiting time and lastly availability

of generic drugs, the list of benefits of travelling for medical treatment in

India are many. This is especially for costly and delicate surgeries like

bypass, kidney and liver transplant, hip replacement, dental services,

cosmetic surgery and bariatric surgery. Indian hospitals are offering

standard services at comparatively low costs. Statistics reveal that treatment

of major surgeries in India costs ~20% of that in developed countries.

Accredited hospitals with huge capacity and gamut of specialty offerings –

Over the years, Indian hospitals have realised the importance of facility

accreditation and accordingly worked towards achieving the benchmark.

Globally, the Joint Commission International (JCI) is considered a major

benchmark by medical tourists. Currently, India has 39 JCI accredited

hospitals. However, the number is still less compared to other countries

(UAE 215; China 102; Thailand 69). Still, with growing awareness and quest

to move into specialty and super specialty, the accreditation number is set

to increase. Similarly, most accredited hospitals have huge capacity (bed

count 200+) while average capacity utilisation is still low at ~50%. Similarly,

most of these hospitals are tertiary/quaternary care multispecialty or single-

super specialty hospitals.

Venugopalan Kesavan (Narayana

Hrudayalaya Q2FY20 earnings call)

Ayushman Bharat is not really a game changer. However, it is good for covering the bottom 10-15% of general ward

beds and on a marginal cost basis, you can justify doing certain procedures. However, by and large, Ayushman

procedures are margin depletive while the government does not pay you anywhere close to what the true cost is nor

do you get paid on time. Game changer is a strong word but it is an indication of the way things are moving forward.

Depending on their budget allocation, the government will start to become more of a payer for large segments of the

population

Suneeta Reddy (Apollo Hospitals

Q2FY20 earnings call)

Of the 256 procedures with a revised base, some are really good to work with. We are having a dialogue with the

government to allow the private sector to do that. I think the pricing there is quite beneficial on a marginal costing

basis. It should work and we are only doing it in Tier 3 hospitals and some of our Tier 2 ones. Going forward, we

hope the government gives out more of the tertiary care work

Nishita Shukla (Shalby Hospitals

Q2FY20 earnings call)

Ayushman payment cycle is supposed to be around 45 days. However, the usual trend is to receive the money in 80-

90 days

Shanay Shah (Shalby Hospitals

Q2FY20 earnings call)

From a marginal costing perspective, sometimes it makes sense to take up schemes. Hence, to that extent, we take

up schemes. Compared to our schedule of charges, Ayushman Bharat rates are very low and the payment is very

much delayed. However, from a new hospital/doctor perspective with comparatively less work, they get to perform a

lot of procedures because of some of these state & central schemes

Growing medical tourism concept that can be the X-

factor for assets located in metros and Tier 1 cities

Over the years, India has grown to become a top

notch destination for medical value travel because it

scores high over a range of factors that determines

the overall quality of care

Currently, India has 39 JCI accredited hospitals.

However, the number is still less compared to other

countries (UAE 215; China 102; Thailand 69)

ICICI Securities | Retail Research 8

ICICI Direct Research Sector Report | Hospitals

Exhibit 10: Joint Commission International (JCI) accredited hospitals

Source: JCI website; ICICI Direct Research

Fast track action – negligible waiting period - Quick and immediate attention

to surgeries and all interventions is another advantage in India. Getting an

appointment for bypass surgery or a planned angioplasty in certain

countries takes almost one to three months. There is almost zero waiting

time in India for any procedure, be it heart surgery, kidney care, cancer

treatment, knee/hip/joint replacements, dental, cosmetic surgeries, weight

loss surgery, etc.

Use of state-of-the art technologies and procedures - Most recognised

hospitals have invested heavily in supportive technology and operative

techniques. Recent advancements in robotic surgeries, radiation surgery or

radio therapies with cyber knife options, intensity modulated radiation

therapy IMRT/image guided radiation therapy (IGRT), transplant support

systems, advanced neuro and spinal options are all available in India.

Quality services at reasonable prices - Healthcare costs in India are

extremely competitive compared to those in developed countries and other

Asian countries. Procedures such as hip and knee replacement, face lift and

gastric bypass are far more affordable in India, including the cost of travel

and accommodation, compared to the US. Moreover, these cosmetic

procedures are not covered by most insurance providers in Western

countries. India has many hospitals for open-heart surgery and paediatric

heart surgeries, which are equipped with the latest equipment that are at par

with these western countries. With healthcare costs soaring in these

countries, the relatively low cost of surgery and critical care in India make it

an attractive destination for medical tourism. India also attracts medical

tourists from other developing nations due to the lack of advanced medical

facilities in many of these countries.

Exhibit 11: Country wise cost of aliments (US$ ‘000s)

Source: Company, ICICI Direct Research

215

102

69

39

20

0

50

100

150

200

250

UAE China Thailand India Singapore

UAE China Thailand India Singapore

Treatment US Korea Singapore Thailand India

Hip Replacement 50.0 14.1 12.0 7.9 7.0

Knee Replacement 50.0 19.8 13.0 12.3 6.2

Heart Bypass 144.0 28.9 18.5 15.1 5.2

Angiopiasty 57.0 15.2 13.0 3.8 3.3

Heart Valve Replacement 170.0 43.5 12.5 21.2 5.5

Dental Implant 2.8 4.2 1.5 3.6 1.0

Quick and immediate attention to surgeries and all

interventions another advantage in India

Most recognised hospitals In India have invested

heavily in supportive technology and operative

techniques

Healthcare costs in India are extremely competitive

compared to those in developed countries as well as

other Asian countries

ICICI Securities | Retail Research 9

ICICI Direct Research Sector Report | Hospitals

Exhibit 12: Number of medical tourists (in lakh)

Source: Crisil, Ministry of Tourism

Facilitation for medical visa - The government has introduced e-visas for

patients seeking prolonged treatment in recognised healthcare centres.

Applicants from nearly 160 countries are eligible for e-tourist visas and can

send online applications for medical visas with scanned copies of medical

prescriptions from a government-accredited hospital of his/her country. The

biometric details of applicants are taken on arrival. The short-term medical

visa is valid for 30 days from the date of arrival, after which the home

department of individual states can extend it by up to a year, provided the

application is based on a medical certificate backed by documented advice

from a hospital in India. The government has also introduced medical visa

and medical attendant visa as separate categories of visa to facilitate entry

of medical tourists in India. The visa relaxation follows the Tourism

Ministry’s efforts to bring India at par with competing nations like Thailand,

Malaysia and Singapore, which offer visa on arrival.

Exhibit 13: Indian medical tourism originating countries

Source: *CY17 data, Crisil; Ministry of tourism; ICICI Direct Research

Favourable macroeconomic factors

Ever since the government opened up healthcare to the private sector in the

1980s, India has seen exponential growth in corporate hospitals. Several

family-owned and doctors managed private hospitals, with a portfolio

approach emerged between 1980 and 2015. Intense competition and

reverse drain of expatriate and highly trained doctors enabled these chains

to venture into specialties & super-specialties. These hospitals also received

government support in the nature of tax and other breaks. Conducive

policies for encouraging FDI, tax benefits, favourable government policies

coupled with promising growth prospects have helped the industry fulfil the

capital requirements via scores of private equity and venture capital deals.

The Government of India has introduced e-visas for

patients seeking prolonged treatment in recognised

healthcare centres

Significant infrastructural gaps persist in the Indian

hospital industry. The bed availability in India in

terms of estimated beds was at 12 per 10,000,

significantly lower than the WHO guideline of 30

beds per 10,000 population

ICICI Securities | Retail Research 10

ICICI Direct Research Sector Report | Hospitals

Significant infrastructural gaps persist in the Indian hospital industry. The

bed availability in India in terms of estimated beds was at 12 per 10,000,

which was significantly lower than the WHO guideline of 30 beds per 10,000

population. Demand-supply mismatch with a combination of

macroeconomic factors, including changing demographics, increasing

affluence of the Indian population, greater health awareness, rising incomes,

changes in the disease profile (towards lifestyle-related ailments) and rising

penetration of health insurance are likely to lead to an increase in demand

for quality healthcare services. Apart from this, increasing trend of medical

tourism for low cost of surgery and critical care in India are expected to be

a key growth driver for healthcare delivery in India.

Exhibit 14: Hospital bed density (per ‘0000 population)

Source: Crisil Research; World Bank; ICICI Direct Research (~2 million more beds are required to be at par with global median)

Exhibit 15: Density of medical professionals in India

Source: Crisil, WHO World Health Statistics 2018, ICICI Direct Research

Exhibit 16: Insurance penetration in India

Source: Crisil, IRDAI

82

42

28 29

22 21

26

19

12

0

10

20

30

40

50

60

70

80

90

Russia China UK US Brazil Thailand Vietnam Malaysia India

(Estimated)

40

28 26

19 1815

8 85

8784

98

74

23

41

21

14

23

0

20

40

60

80

100

120

Russia UK US Brazil China Malaysia India Vietnam Thailand

Doctors (per '0000 population) Nurses (per '0000 population)

Significant infrastructural gaps persist in the Indian

hospital industry. The bed availability in India in

terms of estimated beds was at 12 per 10,000,

which was significantly lower than the WHO

guideline of 30 beds per 10,000 population.

ICICI Securities | Retail Research 11

ICICI Direct Research Sector Report | Hospitals

Positive structural changes notwithstanding, we

follow stock specific approach…

Taking into account all the headwinds and tailwinds, we believe the sector

is yet to witness the realisation of its fullest potential as scepticism about the

capital intensiveness is yet to wane. Apollo, the sector leader by far, remains

a preferred bet from the sector with a calibrated improvement in margins

and return ratios on the back of effective utilisation of both existing and new

hospitals. In the Indian multispecialty category, we like Apollo due to 1) one

of the best integrated business models in the healthcare space with strong

management pedigree, 2) ability to balance between expansion and

profitability, 3) near completion of the long capex cycle and a determined

focus on improvement in margins and return ratios.

Similarly, we also prefer Narayana on account of 1) asset-right model and

affordability philosophy, 2) ability to adapt to the requirement where

affordability does not work, 3) moderation on capex and focus on return

ratios and 4) traction from HCCI Cayman. Among others, we have a BUY

rating on Aster, which is the only hospital chain with a higher outside India

presence, on the back of 1) a significant presence in the GCC (Middle-East)

region with strong pedigree and return ratios, 2) calibrated approach in India

growth, 3) unique ecosystem banking on GCC presence and India expansion

besides labour advantage. We have a HOLD rating on HCG as we believe

the positives 1) comprehensive cancer treatment network with strong

pedigree, 2) overall potential for cancer as a treatment category, 3)

established presence in IVF treatment are getting mitigated by concerns on

in the form of subdued leverage and return ratios. Similarly, we have a HOLD

rating on Shalby as positive aspects 1) brand loyalty in joint replacement, 2)

calibrated expansion in other procedures and geographies to de-risk and 3)

leverage free balance sheet are slightly undone by asset concentration risk.

We keep Fortis Healthcare Under Review due to pending litigation in some

aspects.

We like Apollo Hospitals due to 1) one of the best

integrated business models with strong

management pedigree, 2) ability to balance between

expansion and profitability, 3) near completion of the

long capex cycle

We also like Narayana on account of 1) asset-right

model and affordability philosophy, 2) ability to

adapt to the requirement where affordability does

not work, 3) moderation of capex and focus on return

ratios and 4) traction from HCCI Cayman

We have a BUY rating on Aster DM on the back of

1) significant presence in GCC (Middle-East) region

with strong pedigree and return ratios, 2) calibrated

approach to India growth and 3) unique ecosystem

banking on GCC presence and India

We have a HOLD rating on Healthcare Global (HCG)

as we believe the positives 1) comprehensive

cancer treatment network with strong pedigree, 2)

overall potential for cancer as a treatment category,

3) established presence in IVF treatment are getting

mitigated by concerns on the fronts of subdued

leverage and return ratios

Similarly, we have a HOLD rating on Shalby as

positive aspects 1) brand loyalty in joint

replacement, 2) calibrated expansion in other

procedures and geographies to de-risk and 3)

leverage free balance sheet are slightly undone by

asset concentration risk.

We keep Fortis Healthcare Under Review due to the

pending litigations on some aspects

ICICI Securities | Retail Research 12

ICICI Direct Research

Sector Report | Hospitals

Exhibit 17: Operating matrix compendium

Operational Highlights

(Q2FY19)

Apollo

Hospitals

(Healthcare

delivery)

Narayana HCG Aster DM Shalby

Fortis

(Hospital

segment)

Max India

(Hospital

segment)

No. of healthcare facilities 70 50 24 25 11 24 14

Beds capacity (no.) 9373 7162 2031 4794 2012 NA NA

Operational Beds (no.) 7450 6323 ~1870 3515 1200 3663 2385

Bed occupancy Rate (%) 68% ~59% 43% 63% 48% 72% 75%

ARPOB (| per day) 36,982 26,301 32,769 56,400 29,399 42,192 49,607

ARPOB (| crore p.a) 1.3 1.0 1.2 2.1 1.1 1.5 1.8

ALOS (days) 3.9 3.5 2.0 3.0 4.3 3.2 3.5

Countries IndiaIndia

Cayman Islands

India

Kenya

GCC

India

India

Africa

India India

Presence

Madurai, Karur,

Karaikudi,

Trichy, Nellore,

Hyderabad,

Karimnagar,

Vizag, Kakinada,

Bangalore,

Mysore,

Jayanagar,

Malleswaram,

Bhubaneswar,

Bilaspur, Nashik

& Navi Mumbai

Jammu, Delhi

NCR, Jaipur,

Ahmedabad,

Mumbai,

Shimoga, Bellary,

Bengaluru,

Mysore, Rajpur,

Jamshedpur,

Durgapur, Kolkata,

Guwahati

Bhavnagar,

Rajkot,

Ahmedabad,

Chennai, Jaipur,

Kolkata, Ranchi,

Cuttack,

Vishakapatnam,

Ongole,

Vijaywada,

Nagpur, Borivali,

Nasik, Delhi

NCR,

Ahmedabad,

Baroda,

Gulbarga,

Bangalore, Hubli,

Shimoga

India - Guntur,

Vijaywada,

Ongole,

Bengaluru,

Kozhikode,

Kottakkal,

Kochi,

Wayanad,

Kannur,

Kolhapur,

Hyderabad

GCC - Riyadh,

Muscat,

Sohar, Ibri,

Doha, Dubai,

Sharjah

India - Vapi,

Jabalpur,

Indore,

Mumbai,

Jaipur,

Ahmedabad,

Surat &

Mohali

Africa - Kenya,

Tanzania,

Ethiopia,

Sudan,

Rwanda

Amritsar,

Ludhiana,

Mohali,

Chandigarh,

Delhi NCR,

Dehradun,

Jaipur,

Bangalore,

Chennai,

Kolkata,

Mumbai, Navi

Mumbai

Kangra

Saket,

Patparganj,

Vaishali,

Shalimar Bagh,

Mohali,

Bathinda,

Dehradun, Delhi

NCR, Gurugram,

Noida,Greater

Noida,

Pitampura

Financial highlights (FY19

Consolidated)

Apollo

Hospitals

Narayana HCG Aster DM Shalby Fortis Max India*

Revenues (| crore) 9617.44 2860.92 976.03 7962.71 460.95 4578.04 2921.00

EBITDA (| crore) 1064.64 287.881 111.57 862.8 82.17 -0.48 242.00

EBITDA margin (%) 11.07 10.06 11.43 10.84 17.83 -0.01 8.28

Total Assets(| crore) 7948.62 2214.85 1247.23 7091.54 873.98 11951.27 NA

CMP (as on 9th December'19) 1466.35 304.00 101.35 154.10 102.70 138.50 76.85

Market Cap (| crore) 20400.62 6212.57 898.37 7785.55 1109.26 10456.17 2064.69

Total Debt (| crore) 3673.06 813.47 657.90 2788.44 70.82 2010.27 NA

Cash (| crore) 346.96 100.72 20.87 341.14 74.61 855.85 NA

EV (| crore) 23726.72 6925.31 1535.40 10232.85 1105.47 11610.59 NA

EV/Sales (x) 2.47 2.42 1.57 1.29 2.40 2.54 NA

EV/EBITDA (x) 22.29 24.06 13.76 11.86 13.45 NA NA

Asset Turnover (x) 1.54 1.20 0.90 1.57 0.60 0.50 1.32

Equity (| crore) 69.56 202.80 87.92 505.23 108.01 754.95 53.72

ROE (%) 7.08 5.49 -5.20 10.37 4.06 -4.53 -3.07

ROCE (%) 8.83 7.72 2.99 8.33 6.80 2.49 NA

Source: ICICI Direct Research, Company; Narayana Bed Occupancy - FY19, Apollo’s operational data is for owned hospitals, * Max India Financials are relating to the Healthcare segment.

ICIC

I S

ecurit

ies –

Retail E

quit

y R

esearch

Com

pany U

pdate

CMP: | 1466 Target: | 1800 (23%) Target Period: 12 months

Apollo Hospitals (APOHOS)

BUY

December 10, 2019

Best integrated model in healthcare space…

Apollo Hospitals has one of the best integrated business models in the

healthcare space with a strong management pedigree. It has a presence

across the value chain of hospitals, pharmacies and recently entered retail

healthcare business like Apollo Clinics, Apollo Sugar, White Dental, Apollo

Day Surgery centres, Apollo Cradle and Diagnostic segment through its

subsidiary Apollo Health & Lifestyle Ltd. In hospital segment, the company

owns 70 hospitals with total bed capacity of 10262 beds. In case of

pharmacies, which are basically drug stores chain selling prescription, OTC

and private label products, the company owns 3607 stores as on H1FY20.

Healthcare expansion moderate; focus on asset sweating

Rapid expansion and maturity of older hospitals has kept the overall growth

tempo at 12-14% per annum. However, constant addition is likely to put

some pressure on EBITDA margins and return ratios in the short to medium

term. Similarly, existing hospital margins are being compressed due to 1)

regulation on stent/implants pricing, 2) negative GST impact and 3) higher

guarantee fees to the doctors. However, in the past, the company has

demonstrated its ability to balance between expansion and profitability. We

expect healthcare sales to grow at a CAGR of 12.5% in FY19-22E to | 7324.6

crore mainly due to strong growth at new hospitals and AHLL.

Pharmacy business EBITDA continues to improve

The pharmacy business (40% of FY19 revenues) has grown at ~22% CAGR

in the last five years on the back of consistent addition of new pharmacies

and timely closure of non-performing pharmacies. FY19 margins were at

5.2%. We expect the pharmacy business to grow at ~15% CAGR in FY19-

22E to | 5129 crore mainly on the back of new addition and improvement in

realisation owing to ramp up in private label contribution.

Valuation & Outlook

The company continues to deliver a healthy set of numbers on the revenues

and cost fronts. The overall narrative is panning out on expected lines with

sustained margin expansion and improvement in RoCE, as guided by the

management at the beginning of the last fiscal. The management has

reiterated a similar strategy, going ahead, with more focus on consolidation

of the existing hospitals and making new hospitals profitable. The company

has one of the best integrated business models in the healthcare space with

a strong management pedigree. The management has reiterated plans for

phased promoters pledge reduction. We value the stock on an SOTP basis

by valuing the healthcare business (existing hospitals & JV) at 13x FY22E

EV/EBITDA, healthcare business (new hospitals and JVs) and pharmacy

business at 1.5x FY22E EV/sales. We have a target price of | 1800.

Key Financial Summary

FY19 FY20E FY21E FY22E CAGR (FY19-22E) %

Net Sales 9617.4 11175.6 12625.2 14232.4 14.0

EBITDA 1064.6 1640.5 1968.5 2285.2 29.0

EBITDA margins (%) 11.1 14.7 15.6 16.1

PAT 236.0 351.4 608.4 948.1 59.0

EPS (|) 17.0 25.3 43.7 68.1

PE (x) 86.4 58.1 33.5 21.5

P/BV (x) 6.1 5.6 5.0 4.2

RoE (%) 7.1 9.7 14.9 19.6

RoCE (%) 8.8 11.4 14.8 17.5

Source: ICICI Direct Research; Company

Particulars

Particular Amount

Market Capitalisation | 20401 crore

Debt (FY19) | 3673 crore

Cash (FY19) | 347 crore

EV | 23727 crore

52 week H/L (|) 1580/1083

Equity capital | 69.6 crore

Face value | 5

Price Performance Graph

Research Analyst

Siddhant Khandekar

Mitesh Shah, CFA

Sudarshan Agarwal

0

2000

4000

6000

8000

10000

12000

0

200

400

600

800

1000

1200

1400

1600

1800

Dec-16

Jun-17

Dec-17

Jun-18

Dec-18

Jun-19

Dec-19

Apollo(L.H.S) NSE500(R.H.S)

ICICI Securities | Retail Research 14

ICICI Direct Research Company Update | Apollo Hospitals

Company Background

Established in 1983, the company is one of the few listed players in the

healthcare space. It derives revenues from two broader segments in the

standalone accounts - 1) healthcare services i.e. hospitals and 2) standalone

pharmacies. In the consolidated accounts, other reporting segments are – 1)

hospital revenues from JVs/subsidiaries and associates, 2) Apollo-Munich

Health insurance JV, 3) Apollo Health & Lifestyle Ltd, which is the retail

healthcare business of Apollo Hospitals.

Apollo owns 70 hospitals with a total bed capacity of 10167 beds. Of these

70 hospitals, 44 are owned by the company (including JVs, subsidiaries and

associates) while five are managed by the company with 934 beds while 11

are day care/short surgical stay centres with 267 beds and 11 cradles with

283 beds.

In case of managed hospitals, the company charges 5-6% management fees

for third party hospitals for project management and consultancy covering

all facets of development and operation of a hospital, including market

research, technical design, arranging finance, hiring manpower and running

the facility.

The healthcare segment has been divided into four clusters- 1) Tamil Nadu

Region (Chennai and others), 2) Andhra Pradesh, Telangana region

(Hyderabad, others) 3) Karnataka Region (Bangalore, others) and 3) others

that include hospitals in Bhubaneswar, Bilaspur, Nashik and Navi Mumbai.

In June 2015, the company acquired a 51% stake in Assam Hospitals Ltd,

which runs a 220 bed hospital in Guwahati.

Apollo Healthcare and Lifestyle Ltd (AHLL) subsidiary covers the retail

healthcare business of the Apollo group, comprising Apollo Clinics, Apollo

Sugar, White Dental, Apollo Day Surgery centres and Apollo Cradle. AHLL

reported | 459 crore of sales in FY18.

Apollo Sugar Clinics is a one stop shop for diabetics and offer packages to

better manage diabetes through a combination of prescriptions, dietary,

exercise regimens and other lifestyle changes apart from management of

diabetes related complications. Sanofi has 20% stake in Apollo Sugar Clinics

business. The company has 30 Apollo Sugar Clinics.

Apollo Day Surgery centres focus on planned surgeries done in a day/short

stay basis. The company has 12 centres as of FY18.

Apollo Cradle denotes lifestyle birthing centres. It launched the first Apollo

Cradle in Delhi a decade ago and currently has three centres in the network,

and plans to add five more centres - two in Hyderabad, two in Delhi and one

in Bengaluru.

In FY15, AHLL acquired 11 day and short stay surgery centres (over 350

beds) from Nova Specialty Hospitals with a presence in eight cities across

India. This acquisition provides APL an opportunity to provide quality

healthcare delivery closer to home and also entry in new markets such as

Mumbai, Jaipur and Kanpur.

In case of standalone pharmacies, which are basically drug stores chain

selling prescription, OTC and private label FMCG products, the company

owns 2742 stores in FY17. In FY15, the company acquired Hyderabad-based

Hetero Med Solutions Ltd (HMSL). HMSL has ~320 stores across Telangana,

Andhra Pradesh and Tamil Nadu.

The Apollo board has decided to segregate the front-end retail pharmacy

business carried out in the standalone pharmacy segment into a separate

company Apollo Pharmacies (APL) as part of the proposed reorganisation.

APL to focus on- 1) Building a growth platform for the standalone

pharmacies business to get to a medium-term target of over 5000 pharmacy

outlets over five years with a goal of over | 10,000 crore sales and 30% RoCE

for the stand-alone pharmacy business in five years, 2) enabling foray into

digital commerce as part of Apollo’s omni-channel strategy to provide

consumers increased convenience and ability to choose between online and

ICICI Securities | Retail Research 15

ICICI Direct Research

Company Update | Apollo Hospitals

physical stores, 3) Enhancing the private label business further from the

current 6 + % levels to over 12% in five years through a combination of both

broadening and deepening the product portfolio.

APL will become a wholly owned subsidiary of Apollo Medicals Pvt Ltd

(AMPL). The entire shareholding of AMPL will be held by Apollo and certain

identified investors. Apollo will hold 25.5% of the total share capital of AMPL

with other investors collectively holding the remaining share capital of

AMPL. Specifically, Jhelum Investment Fund 1 will hold 19.9%, Hemendra

Kothari will hold 9.9 % while Enam Securities Pvt Ltd will hold 44.7% of the

total share capital of AMPL.

Apollo shall have the right to acquire the shares of AMPL from investors in

compliance with the regulatory framework. Apollo will be the exclusive

supplier for APL under a long-term supplier agreement while Apollo will

enter into a brand licencing agreement with APL to licence the “Apollo

Pharmacy” brand to the frontend stores and online pharmacy operations.

The proposed reorganisation is not expected to have a material impact on

the financials of Apollo as the backend business related to the standalone

pharmacies, which represents ~85% of the business economics, will

continue to be held by Apollo. The structure is likely to take Apollo one step

closer to a potential unlocking of value in the standalone pharmacy segment.

For the purposes of effectuating the restructuring, Apollo will transfer the

business of the front-end retail pharmacy business carried out in the

standalone pharmacy segment to APL by way of slump sale under a scheme

of arrangement with such transfer being effective from April 1, 2019. The

slump sale has been decided at | 527.8 crore.

ICICI Securities | Retail Research 16

ICICI Direct Research Company Update | Apollo Hospitals

Exhibit 1: Revenues to grow at CAGR of 14% over FY19-22E

Source: ICICI Direct Research, Company

Exhibit 2: Hospitals to grow at CAGR of 12% over FY19-22E

Source: ICICI Direct Research, Company

Exhibit 3: Pharmacy to grow at CAGR of 15% over FY19-22E

Source: ICICI Direct Research, Company

Exhibit 4: AHLL to grow at CAGR of 21% over FY19-22E

Source: ICICI Direct Research, Company

Exhibit 5: EBITDA & margins trend

Source: ICICI Direct Research, Company

Exhibit 6: RoE & RoCE trend

Source: ICICI Direct Research, Company

5178.5

6214.7

7254.9

8243.5

9617.4

11175.6

12625.2

14232.4

0.0

2000.0

4000.0

6000.0

8000.0

10000.0

12000.0

14000.0

16000.0

FY15 FY16 FY17 FY18 FY19 FY20E FY21E FY22E

(|

crore)

Revenues

CAGR 16.7%

CAGR 14.0%

3221.4

3703.34085.1

4515.6

5142.1

5837.1

6543.1

7324.6

0.0

2000.0

4000.0

6000.0

8000.0

FY15 FY16 FY17 FY18 FY19 FY20E FY21E FY22E

(|

crore)

Healthcare Services

CAGR 12.4%

CAGR 12.5%

1772.6

2322.0

2785.2

3268.9

3886.0

4592.2

5206.5

5857.0

0.0

1000.0

2000.0

3000.0

4000.0

5000.0

6000.0

7000.0

FY15 FY16 FY17 FY18 FY19 FY20E FY21E FY22E

(|

crore)

Pharmacy

CAGR 21.7%

CAGR 14.7%

111.0

189.4

385.4458.9

588.8

729.7

875.6

1050.8

0.0

200.0

400.0

600.0

800.0

1000.0

1200.0

FY15 FY16 FY17 FY18 FY19 FY20E FY21E FY22E

(|

crore)

AHLL

CAGR 51.8%

CAGR 21.3%

734.7 687.8 728.6793.2

1064.6

1640.5

1968.5

2285.2

14.2

11.110.0

9.6

11.1

14.715.6

16.1

0.0

4.0

8.0

12.0

16.0

20.0

0.0

500.0

1000.0

1500.0

2000.0

2500.0

FY15 FY16 FY17 FY18 FY19 FY20E FY21E FY22E

(%

)

(|

crore)

EBITDA EBITDA Margins (%)

9.9

6.6 6.1 6.2

8.8

11.4

14.8

17.5

10.4

5.36.0 3.6

7.1

9.7 14.9

19.6

0.0

5.0

10.0

15.0

20.0

25.0

FY15 FY16 FY17 FY18 FY19 FY20E FY21E FY22E

(%

)

RoCE (%) RoNW (%)

ICICI Securities | Retail Research 17

ICICI Direct Research

Company Update | Apollo Hospitals

Exhibit 7: One-year forward EV/EBITDA

Source: ICICI Direct Research, Bloomberg

Exhibit 8: Valuation

Particulers Valuation Matrix Multiple (x) EV (| cr)

Healthcare (Existing Hospitals & JV) EV/EBITDA 13.0 16,329

Healthcare (New Hospitals) EV/Sales 1.5 3,039

Pharmacy EV/Sales 1.5 7,468

Others EV/Sales 1.0 1,428

Net Debt FY21E (| cr) 3,269.7

Targeted MCap (| cr) 24,995

No of shares (cr) 13.9

Per Share Value (|) 1,800

Source: ICICI Direct Research, Bloomberg

Exhibit 9: Summary

Revenues Growth EPS Growth P/E EV/EBITDA RoNW RoCE

(| crore) (%) (|) (%) (x) (X) (%) (%)

FY19 9617 16.7 17.0 100.6 22.2 2.5 8.8 10.1

FY20E 11176 16.2 25.3 48.8 14.0 2.1 11.4 12.5

FY21E 12625 13.0 43.7 73.2 11.4 1.8 14.8 15.5

FY22E 14232 12.7 68.1 55.8 9.5 1.5 17.5 18.2

Source: ICICI Direct Research, Bloomberg

0

5000

10000

15000

20000

25000

30000

35000

40000D

ec-16

Jun-17

Dec-17

Jun-18

Dec-18

Jun-19

Dec-19

(|

crore)

EV 20.9x 16.2x 13.8x 10.2x 7.8x

ICICI Securities | Retail Research 18

ICICI Direct Research

Company Update | Apollo Hospitals

Financial Summary

Exhibit 10: Profit & Loss (| crore)

(Year-end March) FY19 FY20E FY21E FY22E

Revenues 9,617.4 11,175.6 12,625.2 14,232.4

Growth (%) 16.7 16.2 13.0 12.7

Raw Material Expenses 4,660.9 5,395.8 6,095.6 6,871.6

Employee Expenses 1,598.2 1,852.8 2,093.1 2,359.6

Other expenditure 2,293.7 2,286.5 2,467.9 2,716.0

Total Operating Expenditure 8,552.8 9,535.1 10,656.6 11,947.2

EBITDA 1,064.6 1,640.5 1,968.5 2,285.2

Growth (%) 34.2 54.1 20.0 16.1

Depreciation 395.5 593.4 625.8 658.2

Interest 327.0 528.8 418.9 355.9

Other Income 31.4 59.5 101.0 113.9

PBT 373.5 577.7 1,024.8 1,384.9

Total Tax 173.4 218.2 358.7 346.2

MI & Profit from Associates 35.9 -8.2 -57.7 -90.7

Adjusted PAT 236.0 351.4 608.4 948.1

Growth (%) 100.6 48.8 73.2 55.8

EPS (Adjusted) 17.0 25.3 43.7 68.1

Source: ICICI Direct Research

Exhibit 11: Cash Flow Statement (| crore)

(Year-end March) FY19 FY20E FY21E FY22E

Profit/(Loss) after taxation 200.2 351.4 608.4 948.1

Add: Depreciation & Amortization 395.5 593.4 625.8 658.2

Working Capital Changes -45.8 -139.7 -129.5 -144.1

CF from operating activities 549.9 805.1 1,104.7 1,462.2

Change in Capex -672.0 -1,973.4 -260.0 -260.0

(Inc)/dec in Investments -103.6 0.0 -300.0 -300.0

Others -177.5 12.0 62.9 96.1

CF from investing activities -953.2 -1,961.4 -497.1 -463.9

Issue of Equity 0.0 0.0 0.0 0.0

Inc/(dec) in loan funds 234.7 1,481.2 -500.0 -700.0

Dividend paid & dividend tax -83.7 -72.4 -125.4 -195.4

Others -365.5 0.0 0.0 0.0

CF from financing activities -214.5 1,408.8 -625.4 -895.4

Net Cash flow -617.8 252.5 -17.8 102.9

Opening Cash 417.2 347.0 599.5 581.7

Closing Cash -200.5 599.5 581.7 684.6

Free Cash Flow -122.1 -1,168.3 844.7 1,202.2

Source: ICICI Direct Research

Exhibit 12: Balance Sheet (| crore)

(Year-end March) FY19 FY20E FY21E FY22E

Equity Capital 69.6 69.6 69.6 69.6

Reserve and Surplus 3,263.9 3,542.8 4,025.8 4,778.5

Total Shareholders funds 3,333.5 3,612.4 4,095.4 4,848.0

Total Debt 3,673.1 3,250.3 2,750.3 2,050.3

Lease Liabilities 0 1904 1904 1904

Deferred Tax Liability 314.9 321.2 327.6 334.1

Minority Interest 135.5 146.8 209.2 304.9

Long term provisions 11.4 11.7 11.9 12.1

Other Non Current Liabilities 480.3 489.9 499.7 509.7

Total Liabilities 7,948.6 9,736.3 9,798.1 9,963.2

Gross Block - Fixed Assets 6,252.9 8,426.3 8,886.3 9,346.3

Accumulated Depreciation 1,624.0 2,217.5 2,843.3 3,501.5

Net Block 4,628.9 6,208.8 6,043.0 5,844.8

Capital WIP 821.8 621.8 421.8 221.8

Goodwill on Consolidation 346.2 346.2 346.2 346.2

Total Fixed Assets 5,796.8 7,176.8 6,811.0 6,412.7

Investments 468.2 468.2 768.2 1,068.2

Inventory 584.8 679.5 767.7 865.4

Debtors 1,023.2 1,189.0 1,343.2 1,514.2

Loans & Advances, & other CA 456.4 645.6 332.1 294.9

Cash 347.0 599.5 581.7 684.6

Total Current Assets 2,212.9 2,731.1 2,960.9 3,337.9

Creditors 713.1 828.7 936.1 1,055.3

Provisions & Other CL 393.0 410.6 426.2 474.9

Total Current Liabilities 1,234.5 1,360.4 1,478.5 1,608.6

Net Current Assets 978.4 1,370.7 1,482.4 1,729.3

Long term loans & advances 687.8 701.5 715.6 729.9

Deferred Tax Assets 17.4 19.1 21.0 23.1

Application of Funds 7,948.6 9,736.3 9,798.1 9,963.2

Source: ICICI Direct Research

Exhibit 13: Key Ratios (| crore)

(Year-end March) FY19 FY20E FY21E FY22E

Per share data (|)

Adjusted EPS 17.0 25.3 43.7 68.1

BV per share 239.6 259.7 294.4 348.5

Dividend per share 6.9 5.2 9.0 14.0

Cash Per Share 24.9 43.1 41.8 49.2

Operating Ratios (%)

Gross Profit Margins 51.5 51.7 51.7 51.7

EBITDA margins 11.1 14.7 15.6 16.1

Net Profit margins 2.5 3.1 4.8 6.7

Inventory days 22.2 22.2 22.2 22.2

Debtor days 38.8 38.8 38.8 38.8

Creditor days 27.1 27.1 27.1 27.1

Asset Turnover 1.5 1.3 1.4 1.5

EBITDA Conversion Rate 51.7 49.1 56.1 64.0

Return Ratios (%)

RoE 7.1 9.7 14.9 19.6

RoCE 8.8 11.4 14.8 17.5

RoIC 10.1 12.5 15.5 18.2

Valuation Ratios (x)

P/E 86.4 58.1 33.5 21.5

EV / EBITDA 22.2 14.0 11.4 9.5

EV / Net Sales 2.5 2.1 1.8 1.5

Market Cap / Sales 2.1 1.8 1.6 1.4

Price to Book Value 6.1 5.6 5.0 4.2

Solvency Ratios

Debt / EBITDA 3.5 2.0 1.4 0.9

Debt / Equity 1.1 0.9 0.7 0.4

Net Debt / Equity 1.1 0.9 0.6 0.4

Current Ratio 1.5 1.6 1.6 1.6

Source: ICICI Direct Research

ICIC

I S

ecurit

ies –

Retail E

quit

y R

esearch

Com

pany U

pdate

CMP: | 304 Target: | 360 (18%) Target Period: 12 months

Narayana Hrudayalaya (NARHRU)

BUY

December 10, 2019

Stellar numbers; vital parameters continue to improve

Incorporated by renowned cardiac surgeon Dr Devi Prasad Shetty in 2000,

Narayana Hrudayalaya (Narayana) operates as a chain of multispecialty

hospitals. Started predominantly in Karnataka and Eastern India, the

company is growing its footsteps in western and northern India as well. We

reiterate our BUY recommendation on the stock as we believe it is well

poised to thrive in the domestic healthcare delivery (hospitals) space on the

back of its asset right business model with focus on quality and affordability.

Blended model of affordable + high-quality services

The company has a legacy model based on affordability over the years. Due

to strict control over costs and capital, the company was making reasonable

profits. However, as it looks to scale up in other regions, where the

consideration for quality has more weight than affordability, the model is

likely to be modified from ‘’affordable’’ to a mix of affordable + quality at

premium. Cases in point are the recent acquisition of Gurugram Hospital and

buying out of partner in the Cayman Islands hospital internationally where

acquisition costs were optically higher.

‘’Asset right model’’ to improve return ratios

Under this model, the company engages with partners who invest in land

and building while it takes care of medical equipment and hospital

management on a revenue share basis. However, the management has

maintained a flexible approach in this regard. Thus, it also owns some

hospitals where the opportunity is right. Due to this focus on balance sheet

and likely improvement in average realisation per operating bed (ARPOB) by

optimising the case mix, we expect an improvement in RoCE from 7.7% to

16.5% in FY19-22E.

Valuations & Outlook

A persistent improvement in occupancy rate across all segments coupled

with substantial seasonality impact propelled both revenue growth, margins

in H1. The new hospitals (SRCC, Gurugram, Dharamshila) continue to see a

reduction in losses as the ramp-up in these assets is slowly but surely

improving. The management reiterated a significant moderation in capex.

On the M&A front, this should improve return ratios gradually. The

improvement, sustainability of these vital prints hold key as the focus now

shifts to improvement in operating leverage. This was clearly visible in H1

performance. The improvement in numbers over the last few quarters is also

on the back of a judicious case mix identification (more focus on transplants

as well as non-invasive procedures). We continue to believe in the long term

prospects of the company on the back of asset-right model and affordability

philosophy. We arrive at an SOTP target price of | 360 by valuing the

matured hospitals and Cayman Islands at 8x of FY22E EV/EBITDA, new

hospitals at 1.5x FY22E EV/sales and other business at 1x FY22E EV/sales.

Key Financial Summary

(| Crore) FY19 FY20E FY21E FY22E CAGR FY19-22E %

Revenues 2860.9 3226.2 3488.7 3808.0 10.0

EBITDA 287.9 444.8 503.3 585.0 26.7

EBITDA Margins (%) 10.1 13.8 14.4 15.4

Adjusted PAT 59.3 146.3 199.8 272.3 66.2

EPS (|) 2.9 7.2 9.8 13.3

PE (x) 104.7 42.5 31.1 22.8

EV to EBITDA (x) 24.1 15.7 13.5 11.1

Price to book (x) 5.7 5.2 4.5 3.8

RoE (%) 5.5 12.2 14.5 16.7

RoCE (%) 7.7 12.0 13.9 16.5

Source: ICICI Direct Research; Company

Particulars

Particular Amount

Market Capitalisation | 6213 crore

Debt (FY19) | 813 crore

Cash (FY19) | 101 crore

EV | 6925 crore

52 week H/L (|) 319/181

Equity capital | 204.4 crore

Face value | 10

Price Performance Graph

Research Analyst

Siddhant Khandekar

Mitesh Shah, CFA

Sudarshan Agarwal

0

2000

4000

6000

8000

10000

12000

0

100

200

300

400

Dec-16

Jun-17

Dec-17

Jun-18

Dec-18

Jun-19

Dec-19

Narayana(L.H.S) NSE500(R.H.S)

ICICI Securities | Retail Research 20

ICICI Direct Research Company Update | Narayana Hrudayalaya

Company Background

Narayana was incorporated by renowned cardiac surgeon Dr Devi Prasad

Shetty in 2000. It was started as a predominant cardiac care hospitals group

initially. Gradually, it also diversified into other specialties although cardiac

still remains a mainstream specialty followed by renal (kidney care).

Narayana network comprises 24 hospitals (including three managed

hospitals), seven heart centres, 19 primary care facilities (including clinics

and information centres) a multi-speciality hospital in Cayman Islands by

entering into agreement with the Government of Cayman Islands. The

company has 6283 operational beds and the potential to reach a capacity of

up to 7155 beds. Region wise, southern (mainly Karnataka) and eastern

(mainly Kolkata) regions together account for 81% of the operating revenues

(FY18).

Cluster wise bifurcation

Karnataka cluster – Comprises seven hospitals including four in Bengaluru

and a hospital each in Mysore, Bellary and Shimoga totalling 2213

operational beds. The company also manages six heart centres totalling 322

operating beds.

Eastern cluster - Comprises nine hospitals including hospitals in the greater

Kolkata area encompassing Howrah, Barasat and the Eastern Metropolitan

Bypass, a multispecialty hospital in Jamshedpur, Jharkhand, a

superspeciality hospital in Guwahati, Assam and a hospital in Durgapur,

West Bengal totalling 2105 operational beds. The company also manages a

heart centre in Durgapur, West Bengal, totalling 49 operational beds.

Western and northern clusters - Comprises five hospitals - Jaipur

(Rajasthan), Palanpur (Gujarat), Ahmedabad (Gujarat), paediatric hospital in

Mumbai (Maharashtra), Raipur (Chhattisgarh), Jammu and Delhi totalling

1474 current operational beds. The company acquired a multispecialty

hospital has commissioned in Q4FY18.

Health City Cayman Islands (HCCI) - Narayana had set up a multi-speciality

hospital in Cayman Islands by entering into an agreement with the

Government of Cayman Islands on April 7, 2010. Health City Cayman Islands

(HCCI) is a joint venture between Narayana and Ascension Health Ventures

LLC, a US based trust. This 106 bedded hospital was commissioned in April

2014 and earned JCI, US accreditation in May, 2015 (JCI is the international

arm of The Joint Commission, the leading health care accreditor in the US).

Narayana had initially entered into the JV with 28.6% stake in the hospital

and then bought back the rest of the 71.4% stake from Ascension Health for

a cash consideration of US$32 million in 2017 (implied EV of US$70 million

for 105 beds). Now, it is the step down subsidiary of Narayana Health. HCCI

primarily targets North American patients (Cayman Islands is 430 miles

south of Miami, near Caribbean islands) and provides high-quality,

affordable health care. For FY19, HCCI revenues was at US$54.5 million with

EBITDA at US$9.5 million (EBITDA margin of 17.4%). For FY19, the hospital

was running at ~32% occupancy rate.

As of FY19, it has 16690 employees, which included 3644 doctors.

ICICI Securities | Retail Research 21

ICICI Direct Research Company Update | Narayana Hrudayalaya

Exhibit 1: Revenues to grow at CAGR of 10% over FY19-22E

Source: ICICI Direct Research, Company

Exhibit 2: EBITDA & EBITDA margins trend

Source: ICICI Direct Research, Company

Exhibit 3: Net profit to grow at 66% CAGR over FY19-22E

Source: ICICI Direct Research, Company

Exhibit 4: RoE & RoCE trend

Source: ICICI Direct Research, Company

1363.9

1613.9

1878.2

2281.4

2862.8

3226.2

3488.7

3808.0

0

500

1000

1500

2000

2500

3000

3500

4000

FY15 FY16 FY17 FY18 FY19 FY20E FY21E FY22E

(|

crore)

Revenues

CAGR 20.4%

CAGR 10.0%

123.7

174.6

228.9212.6

287.9

444.8

503.3

585.0

9.1

10.8

12.2

9.310.1

13.814.4

15.4

0

2

4

6

8

10

12

14

16

18

0

100

200

300

400

500

600

700

FY15 FY16 FY17 FY18 FY19 FY20E FY21E FY22E

(%

)

(|

crore)

EBITDA EBITDA Margins (%)

-5.8

32.2

84.4

51.2 59.3

146.3

199.8

272.3

-50

0

50

100

150

200

250

300

FY15 FY16 FY17 FY18 FY19 FY20E FY21E FY22E

(|

crore)

Net Profit

5.9

8.8

12.5

6.3

7.7

12.0

13.9

16.5

-0.8

3.7

8.8

4.9

5.5

12.2

14.5

16.7

-2

0

2

4

6

8

10

12

14

16

18

FY15 FY16 FY17 FY18 FY19 FY20E FY21E FY22E

(%

)

RoCE (%) RoE (%)

ICICI Securities | Retail Research 22

ICICI Direct Research Company Update | Narayana Hrudayalaya

Exhibit 5: Valuation

Particulers Valuation Matrix Multiple (x) Enterprise value (| cr)

Hospital (Matured) EV/EBITDA 8.0 5749.8

Cayman EV/EBITDA 8.0 1102.6

Hospital (New) EV/Sales 1.5 563.5

Other Business EV/Sales 1.0 187.2

Net Debt FY22E (| cr) 285.0

EV (| cr) 7318.1

No of shares (cr) 20.4

Per Share Value (|) 360.0

Source: Company

Exhibit 6: One-year forward EV/EBITDA

Source: Bloomberg, ICICI Direct Research

Exhibit 7: Valuation

Revenues Growth Adj. EPS Growth P/E EV/EBITDA RoE RoCE

(| crore) (%) (|) (%) (x) (X) (%) (%)

FY19 2860.9 77.3% 2.9 0.8 104.7 24.1 5.5 7.7

FY20E 3226.2 12.8% 7.2 146.6% 42.5 15.7 12.2 12.0

FY21E 3488.7 8.1% 9.8 36.6% 31.1 13.5 14.5 13.9

FY22E 3808.0 9.2% 13.3 36.3% 22.8 11.1 16.7 16.5

Source: ICICI Direct Research, Company

-2000

0

2000

4000

6000

8000

10000

12000

14000

16000

Dec-16

Mar-17

Jun-17

Sep-17

Dec-17

Mar-18

Jun-18

Sep-18

Dec-18

Mar-19

Jun-19

Sep-19

Dec-19

(|

crore)

Narayana 29.4x 27.4x 23.3x 11.1x 2.9x

ICICI Securities | Retail Research 23

ICICI Direct Research Company Update | Narayana Hrudayalaya

Financial Summary

Exhibit 8: Profit & Loss (| crore)

(Year-end March) FY19 FY20E FY21E FY22E

Revenues 2,860.9 3,226.2 3,488.7 3,808.0

Growth (%) 25.4 12.8 8.1 9.2

Raw Material Expenses 687.5 774.5 837.5 914.2

Employee Expenses 624.1 696.6 753.2 822.2

Other Manufacturing Expenses 1,261.5 1,310.3 1,394.6 1,486.6

Total Operating Expenditure 2,573.0 2,781.3 2,985.4 3,223.0

EBITDA 287.9 444.8 503.3 585.0

Growth (%) 35.4 54.5 13.2 16.2

Interest 71.4 87.3 68.0 48.6

Depreciation 137.4 170.2 179.1 188.1

Other Income 16.7 14.5 10.5 15.2

PBT before Exceptional Items 95.8 201.8 266.8 363.6

Less: Forex & Exceptional Items 0.0 0.0 0.0 0.0

PBT 95.8 201.8 266.8 363.6

Total Tax 34.1 53.5 67.0 91.3

PAT before MI 61.7 148.3 199.8 272.3

Minority Interest 0.0 0.0 0.0 0.0

PAT 59.3 146.3 199.8 272.3

Adjusted PAT 59.3 146.3 199.8 272.3

Growth (%) 16.0 146.6 36.6 36.3

EPS 2.9 7.2 9.8 13.3

EPS (Adjusted) 2.9 7.2 9.8 13.3

Source: ICICI Direct Research

Exhibit 9: Cash Flow Statement (| crore)

(Year-end March) FY19 FY20E FY21E FY22E

Profit/(Loss) after taxation 39.4 146.3 199.8 272.3

Add: Depreciation & Amortization 137.4 170.2 179.1 188.1

Net Increase in Current Assets -7.8 -52.1 -40.5 -48.3

Net Increase in Current Liabilities 16.1 51.2 40.3 47.9

Others 93.5 87.3 68.0 48.6

CF from operating activities 278.6 402.9 446.6 508.6

(Inc)/dec in Fixed Assets -149.5 -345.7 -200.0 -150.0

(Inc)/dec in Investments -10.0 0.0 0.0 0.0

Others -26.4 12.2 13.4 14.8

CF from investing activities -185.9 -333.4 -186.6 -135.2

Inc / (Dec) in Equity Capital 0.4 0.0 0.0 0.0

Inc / (Dec) in Debt 27.6 87.3 -200.0 -200.0

Dividend & Dividend Tax 0.0 -23.8 -23.8 -23.8

Others -55.3 -87.3 -68.0 -48.6

CF from financing activities -27.3 -23.8 -291.7 -272.3