Hong Kong Retail Sector - Credit Suisse

26

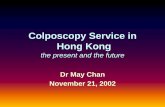

DISCLOSURE APPENDIX CONTAINS ANALYST CERTIFICATIONS AND THE STATUS OF NON-US ANALYSTS. U.S. Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision. 04 January 2012 Asia Pacific/Hong Kong Equity Research Retailing Hong Kong Retail Sector SECTOR REVIEW Rental cycle is catching up Figure 1: Rental cycle started catching retail cycle in September -20 -10 0 10 20 30 40 50 60 1Q02 4Q02 3Q03 2Q04 1Q05 4Q05 3Q06 2Q07 1Q08 4Q08 3Q09 2Q10 1Q11 1Q12 Overall prime Premium prime High-street Retail sales growth (%) Source: Jones Lang LaSalle, CEIC, Credit Suisse estimates ■ Rental pressure kicked in since September 2011. Given the typical Hong Kong retail lease structure of three-year fixed terms, the retail cycle normally runs ahead of the rental cycle by 9-12 months. While overall Hong Kong retail sales growth started decelerating in September 2011, the speed of rental rate growth shows no sign of decelerating. That said, rental pressure is building up. ■ The catch-up could be significant. Retail sales growth has been outpacing rental rate growth since 1Q09; this rarely happened over the previous ten years, suggesting that landlords underestimated the growth potential. Hence, we expect lots of catching up by rental rates and this explains the significant rental hikes recorded, particularly in tourist districts. Historically, rental rate growth has outpaced retail sales growth, and we believe this cycle is no exception. Thus, existing earnings forecasts could be optimistic, and rental pressure may force some retailers to scale down store expansion plans, triggering even more downward earnings estimate revisions. ■ Cautious on mid- to high-end apparel retailers. We studied the financial track record of 22 Hong Kong retail companies for the past 11 years and found that mid- to high-end apparel retailers in general have the highest rental expenses-to-turnover ratio, making them more vulnerable to rental hike pressure. Among them, Bauhaus (0483.HK), I.T (0999.HK), Moiselle (0130.HK) and Veeko (1173.HK) have rental expenses that exceeded 20% of their turnover in 2010. On the other hand, cosmetic retailers have shown the most resilient sales growth during economic downturns. Research Analysts Gabriel Chan, CFA 852 2101 6523 [email protected] Isis Wong 852 2101 7109 [email protected]

Transcript of Hong Kong Retail Sector - Credit Suisse

DISCLOSURE APPENDIX CONTAINS ANALYST CERTIFICATIONS AND THE STATUS OF NON-US ANALYSTS. U.S. Disclosure: Credit Suisse does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the Firm may have a conflict of interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

04 January 2012Asia Pacific/Hong Kong

Equity ResearchRetailing

Hong Kong Retail Sector SECTOR REVIEW

Rental cycle is catching up Figure 1: Rental cycle started catching retail cycle in September

-20

-10

0

10

20

30

40

50

60

1Q02 4Q02 3Q03 2Q04 1Q05 4Q05 3Q06 2Q07 1Q08 4Q08 3Q09 2Q10 1Q11 1Q12

Overall prime Premium prime High-street Retail sales growth

(%)

Source: Jones Lang LaSalle, CEIC, Credit Suisse estimates

■ Rental pressure kicked in since September 2011. Given the typical Hong Kong retail lease structure of three-year fixed terms, the retail cycle normally runs ahead of the rental cycle by 9-12 months. While overall Hong Kong retail sales growth started decelerating in September 2011, the speed of rental rate growth shows no sign of decelerating. That said, rental pressure is building up.

■ The catch-up could be significant. Retail sales growth has been outpacing rental rate growth since 1Q09; this rarely happened over the previous ten years, suggesting that landlords underestimated the growth potential. Hence, we expect lots of catching up by rental rates and this explains the significant rental hikes recorded, particularly in tourist districts. Historically, rental rate growth has outpaced retail sales growth, and we believe this cycle is no exception. Thus, existing earnings forecasts could be optimistic, and rental pressure may force some retailers to scale down store expansion plans, triggering even more downward earnings estimate revisions.

■ Cautious on mid- to high-end apparel retailers. We studied the financial track record of 22 Hong Kong retail companies for the past 11 years and found that mid- to high-end apparel retailers in general have the highest rental expenses-to-turnover ratio, making them more vulnerable to rental hike pressure. Among them, Bauhaus (0483.HK), I.T (0999.HK), Moiselle (0130.HK) and Veeko (1173.HK) have rental expenses that exceeded 20% of their turnover in 2010. On the other hand, cosmetic retailers have shown the most resilient sales growth during economic downturns.

Research Analysts Gabriel Chan, CFA

852 2101 6523 [email protected]

Isis Wong 852 2101 7109

04 January 2012

Hong Kong Retail Sector 2

Focus charts Figure 2: Retail sales versus retail rental growth Figure 3: Weakening consumer confidence in China

-2 0

-1 0

0

1 0

2 0

3 0

4 0

5 0

6 0

1Q 0 2 1 Q 0 3 1 Q 0 4 1 Q 0 5 1 Q 0 6 1 Q 0 7 1 Q 0 8 1 Q 0 9 1 Q 1 0 1 Q 1 1 1 Q 12

O ve ra ll p rim e P re m iu m p rim eH ig h -st re e t R e t a il sa le s g ro wt h

(% )

9092949698

100102104106108110

Jan-09 Jul-09 Jan-10 Jul-10 Jan-11 Jul-11

China consumer confidence index

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

Figure 4: Increasing contribution from mainland visitors Figure 5: Apparel & accessories retailers have the highest rental expense-to-turnover ratio

0

1 0 ,0 0 0

2 0 ,0 0 0

3 0 ,0 0 0

4 0 ,0 0 0

5 0 ,0 0 0

6 0 ,0 0 0

7 0 ,0 0 0

2 0 0 0 2 0 0 1 2 0 0 2 2 0 0 3 2 0 0 4 2 0 0 5 2 0 0 6 2 0 0 7 2 0 0 8 2 0 0 9 2 0 1 00

5

10

15

20

25

Ch in e s e vis ito rs' sh o p p in g s p e n d in g (H K $ m n ) - L H SCo n tr ib u t io n to H K re ta il s a le s

(H K $ m n ) (% )

C A G R = 2 2 .3 %

0

5

10

15

20

25

Apparel &accessories

Hard luxury Cosmetic F&B Others

2010 rental expense to turnover ratio

(%)

Source: Company data, Credit Suisse estimates Source: Company data, Credit Suisse estimates

Figure 6: HOLT® analysis—rental expense as a percentage of gross cash flow

Figure 7: HOLT analysis—price potential to HOLT’s best warranted prices

0

10

20

30

40

50

60

70

80

90

280 5 92 483 130 1 13 999 709 9 84 647 5 2 6 53 341 178 8 87 398 573 1 16 738 590

R ental exp ense as % of gr oss cash flo w

M ed ian = 57.4%

(%)

-120

-100

-80

-60

-40

-20

0

20

113 590 116 999 398 483 887 653 738 709 573 178 341 647 592 984 52 130 280

Potential to HOLT's best warranted price (%)

Median = 39.0%

(%)

Source: Company data, Credit Suisse HOLT Source: Company data, Credit Suisse estimates

04 January 2012

Hong Kong Retail Sector 3

Rental cycle is catching up Rental pressure kicked in since September 2011 Given the typical Hong Kong retail lease structure of three-year fixed terms, the retail cycle normally runs ahead of the rental cycle by 9-12 months, as landlords refer to current sales performance as benchmarks for setting new rental rates. While overall Hong Kong retail sales growth started decelerating in September 2011, the speed of rental rate growth shows no sign of decelerating. That said, rental pressure is building up.

Note that we expect Hong Kong retail sales to grow about 15% YoY in 2012, compared to about 24-25% YoY in 2011. The deceleration, in our view, will be driven by: (1) weakening consumer sentiment in both Hong Kong and China; (2) higher-based comparison; (3) slower Rmb appreciation; (4) slower GDP growth (both in real and nominal terms) in China; and (5) continuous down-trading by locals.

Note that retail sales growth has been outpacing rental rate growth since 1Q09, which rarely happened over the past ten years, suggesting that landlords had underestimated the growth potential. Hence, we expect lots of catching up by the rental rate and this explains the significant rental hikes recorded, particularly in popular tourist districts. Historically, the rental rate growth has outpaced retail sales growth, and we believe this cycle is no exception.

We are cautious on mid- to high-end apparel retailers With increasing pressure from rental costs, we believe existing earnings forecasts for Hong Kong retailers could be optimistic. Furthermore, the high rental cost may eventually force some retailers to scale down their store expansion plans, which could trigger even more downward earnings estimate revisions and result in some valuation de-rating.

We studied the financial track record of 22 Hong Kong retail companies for the past 11 years and found that mid- to high-end apparel retailers in general have the highest rental expense-to-revenue ratios, making them more vulnerable to rental hike pressure. Among them, Bauhaus (0483.HK, HK$1.85, not rated), I.T (0999.HK, HK$4.27, not rated), Moiselle (0130.HK, HK$2.06, not rated) and Veeko (1173.HK, HK$0.23, not rated) have rental expenses that exceeded 20% of their turnover in 2010.

While the hard luxury segment has historically been more cyclical in terms of sales performance, we believe this cycle is different due to the much increased revenue contribution from mainland Chinese shoppers in Hong Kong who take advantage of lower retail prices here due to the absence of VAT, consumption tax and import duties. Besides, hard luxury retailers normally have a very low rental-to-turnover ratio of less than 5%, making them less vulnerable to rental pressure. We reiterate Luk Fook (0590.HK, HK$27.70, OUTPERFORM [V], TP HK$37.80) as our top pick in the Hong Kong retail sector.

On the other hand, cosmetics retailers such as Sa Sa (0178.HK, HK$4.36, NEUTRAL [V], TP HK$5.00) and Bonjour (0653.HK, HK$1.23, not rated) have shown the most resilient sales growth during economic downturns. However, we observe severe competition for rental spaces in key tourist districts, resulting in significant increases in rental costs. Thus, we remain cautious on cosmetic retailers’ margins.

Besides pressure from rental hikes (F&B is one of the few sub-segments whose revenue growth has been outpaced by rental rate hikes since the end of the global financial crisis in 2008-09), food inflation has also been catching up quickly. The margin pressure is particularly severe for fast food chains, such as Café de Coral (0341.HK, HK$17.82, not rated) and Fairwood (0052.HK, HK$10.10, not rated), on the back of the minimum wage law imposed since May 2011.

The rental cycle normally lags the retail cycle by 9-12 months

We expect Hong Kong retail sales growth to slow to around 15% YoY in 2012E

Rental growth normally outpaces retail sales growth

Earnings forecasts and valuations are at risk

Mid- to high-end apparel retailers have the highest rental cost-to-revenue ratios

Stiff price differential between Hong Kong and China may help support the sales growth of luxury retailers

Cosmetic retailers have been most resilient in terms of sales growth

F&B is likely to remain under margin pressure

04 January 2012

Hong Kong Retail Sector 4

Valuation summary Figure 8: Valuation comparison—Hong Kong retailers Mkt Credit Pot. P/E EV/EBITDA cap Price Suisse TP up/down (x) (x) Company Ticker (US$ mn) (l.c.) rating (l.c.) (%) CY11E CY12E CY13E CY11E CY12E CY13EApparels and accessories BOSSINI INT'L 0592.HK 123 0.59 Not rated n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a.Giordano Intl. 0709.HK 1,106 5.65 Not rated n.a. n.a. 11.7 10.3 9.3 7.1 6.1 5.4Bauhaus Int'l 0483.HK 86 1.85 Not rated n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a.I.T 0999.HK 671 4.27 Not rated n.a. n.a. 11.0 9.2 7.5 6.8 5.5 4.3Joyce Boutique 0647.HK 155 0.74 Not rated n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a.Le Saunda Hldgs 0738.HK 221 2.69 Not rated n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a.Moiselle Int'l 0130.HK 75 2.06 Not rated n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a.Veeko Intl 1173.HK 63 0.23 Not rated n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a.Dickson 0113.HK 189 3.95 Not rated n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a.Hard luxury CHOW SANG SANG 0116.HK 1,527 17.52 Not rated n.a. n.a. 11.0 9.1 7.7 8.6 7.2 6.1Emp Wat & Jew 0887.HK 856 0.99 Not rated n.a. n.a. 11.5 8.9 7.0 8.0 6.2 4.8King Fook Hldgs 0280.HK 65 1.16 Not rated n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a.Luk Fook 0590.HK 1,934 27.70 OUTPERFORM 37.80 36.5 11.6 9.8 8.2 8.9 7.1 5.7Oriental Watch 0398.HK 259 3.53 Not rated n.a. n.a. 7.0 5.8 5.0 n.a. 3.3 2.7Milan Station 1150.HK 116 1.34 Not rated n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a.Cosmetics BONJOUR Hldg 0653.HK 476 1.23 Not rated n.a. n.a. 13.1 10.5 8.4 10.9 8.9 7.5Sa Sa International Holding 0178.HK 1,580 4.36 NEUTRAL 5.00 14.7 20.3 16.2 13.7 14.3 11.2 9.2Food & beverage Fairwood Hold 0052.HK 162 10.10 Not rated n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a.Cafe De Coral 0341.HK 1,299 17.82 Not rated n.a. n.a. 21.1 19.0 16.6 10.7 9.2 7.7Tao Heung 0573.HK 401 3.06 Not rated n.a. n.a. n.a. n.a. n.a. n.a. n.a. n.a.Others Aeon stores 0984.HK 599 17.90 Not rated n.a. n.a. 14.7 12.4 11.0 3.7 2.5 1.6CRA 0831.HK 304 3.22 Not rated n.a. n.a. 15.3 12.9 10.7 7.3 5.9 4.7 12.3 10.3 8.7 7.8 6.4 5.3

Source: Company data, I/B/E/S estimates for Not Rated stocks, Credit Suisse estimates

04 January 2012

Hong Kong Retail Sector 5

Rental cycle is catching up Retail sales momentum started weakening in September 2011 Hong Kong retail sales growth momentum started weakening in September 2011, with growth decelerating from 29% in July and August to 24% in September, and further decelerating to 23.1% in October.

We expect the deceleration to continue to be driven by the following factors:

(1) weakening consumer sentiment in both Hong Kong and China: Both reached their lowest levels since early 2009 in the latest survey.

Figure 9: China consumer confidence index Figure 10: Hong Kong consumer confidence index

9092949698

100102104106108

110

Jan-09 Jul-09 Jan-10 Jul-10 Jan-11 Jul-11

China consumer confidence index

60

70

80

90

100

Mar-09 Sep-09 Mar-10 Sep-10 Mar-11 Sep-11

Hong Kong consumer confidecne index

Source: CEIC Source: CEIC

(2) Higher-based comparison: Retail sales growth accelerated from about 20% in 2010 to 24-25% in 2011.

Figure 11: Hong Kong retail sales growth trend

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

Jan-09 Apr-09 Jul-09 Oct-09 Jan-10 Apr-10 Jul-10 Oct-10 Jan-11 Apr-11 Jul-11 Oct-11-20

-10

0

10

20

30

40

Total retail sales - LHS YoY % chg - RHS

(HK$ mn) (%)

Source: CEIC, Credit Suisse estimates

04 January 2012

Hong Kong Retail Sector 6

(3) Slower Rmb appreciation: This reduces the price attractiveness of consumer products in Hong Kong as it narrows the price gap. For more information, please refer to our previous report, A bargain for luxury products, published on 8 August 2011.

Figure 12: Rmb non-deliverable forward price

6.20

6.30

6.40

6.50

6.60

6.70

Jan-11 Feb-11 Mar-11 Apr-11 May-11 Jun-11 Jul-11 Aug-11 Sep-11 Oct-11 Nov-11 Dec-11 Jan-12

1M 3M 12M

(RMB/US$)

Source: Bloomberg

Note that mainland Chinese visitors to Hong Kong have been the most important driver of retail sales growth. Over the past ten years, retail spending by mainland visitors increased at a 22.3% CAGR between 2000 and 2010. And their contribution to the Hong Kong retail sales also increased from 5% to 23% during the same period.

Figure 13: Mainland Chinese visitors’ contribution to Hong Kong retail sales

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 20100

5

10

15

20

25

Chinese visitors' shopping spending (HK$ mn) - LHS Contribution to HK retail sales

(HK$ mn) (%)

CAGR = 22.3%

Source: CEIC, Credit Suisse estimates

(4) Slower GDP growth (both in real and nominal terms) in China: Credit Suisse economists have recently revised down China’s 2012 GDP growth rate projection from 8.2% to 8.0%.

(5) Continuous down-trading by locals: Despite the robust retail sales growth registered, Hong Kong locals have been spending less in the past two years; the following chart shows Hong Kong retail sales excluding visitors’ spending.

04 January 2012

Hong Kong Retail Sector 7

Figure 14: Retail sales contributed by Hong Kong locals

0

50,000

100,000

150,000

200,000

250,000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Retail sales excluding tourists' spending

(HK$ mn)

2000-2010 CAGR = 1.9%

Source: CEIC, Credit Suisse estimates

While we do not have a quantitative model for the overall retail sales growth projection, we believe the slowing trend will continue to mid-teen levels in 2012E, converging back to the long-term CAGR of about 10%.

Figure 15: Hong Kong retail sales trend, 2004-10

0

50,000

100,000

150,000

200,000

250,000

300,000

2004 2005 2006 2007 2008 2009 2010

Retail sales exclud ing tourists' spending Mainland China visitors Other tourists

(HK$ mn)

2004-2010 CAGR = 9.7%

Source: CEIC

Retail rental rate hike is accelerating Despite the retail sales growth momentum starting to weaken in September, retail rental rate hikes continue to accelerate. Based on data from Jones Lang LaSalle, retail rental growth has been accelerating since 1Q09, and at a even faster rate over the past two quarters.

Note that such rental hike acceleration is registered across the board in overall prime, premium prime and high-street level. But among the three sub-segments, high-street retail rental normally shows the highest volatility, i.e., it rises and drops more than other segments during a cycle.

Retail rental growth has been accelerating since 1Q09

04 January 2012

Hong Kong Retail Sector 8

Figure 16: Retail sales versus retail rental growth

-20

-10

0

10

20

30

40

50

60

1Q02 4Q02 3Q03 2Q04 1Q05 4Q05 3Q06 2Q07 1Q08 4Q08 3Q09 2Q10 1Q11 4Q11

Overall prime Premium prime High-street Retail sales growth

(%)

Source: Jones Lang LaSalle, CEIC, Credit Suisse estimates

Retail sales cycle normally runs ahead of rental cycle by 9-12 months

In Hong Kong, retail leases normally have a term length of three years, with a fixed monthly rental rate during the lease period (and sometimes have a pre-set rental rate increase for the next rental renewal). When landlords enter into new rental agreements with retailers, they normally use the latest retail sales trend to set the new rental rate. From the retailers’ perspective, every year, they have about a third of rental agreements that are subject to renewal. Thus, it is typical that the retail sales cycle is running ahead of the rental rate cycle by 9-12 months.

Rental rate growth has historically surpassed retail sales growth

On the other band, in the past ten years, retail sales growth has underperformed the retail rental growth rate, particularly when retail sales momentum starts to slow.

However, the past two years marks an interesting period in which retail sales growth has consistently been faster than retail rental growth, suggesting that landlords have underestimated retail sales growth significantly; therefore, we expect rental rate growth to catch up and eventually surpass retail sales growth, like in previous cycles.

We believe retail rentals will be further stimulated by the influx of foreign brands setting up their flagship stores in Hong Kong. A few most eye-catching examples include Abercrombie & Fitch’s (ANF, $48.84, not rated) and Gap’s (GPS, $18.55, not rated) new flagship stores in Central, Hong Kong, with monthly rentals of HK$7 mn and HK$3.2 mn, respectively.

On the other hand, robust jewellery and luxury watches sales have also driven rental rates in major tourist districts, such as Causeway Bay and Tsimshatsui (TST) significantly. The highest rental increase we recognised was registered in October, with Chow Sang Sang (0116.HK, HK$17.52, not rated), one of the leading jewellery retailers, replacing Bonjour (0653.HK, HK$1.23, not rated), a cosmetic retail chain, in a 400 sq ft shop in TST, and the monthly rental rate increasing 525% from HK$0.4 mn per month to HK$2.5 mn per month.

The following table shows the list of rental agreements registered since late August. Note that the majority of them have rental rate increases of more than 100%, compared to the previous lease agreements. With the overall retail sales level estimated to be 48% higher in 2012 compared to 2011, margin pressure from rental rate hikes is definitely kicking in.

The rental cycle normally lags behind the retail cycle by 9-12 months

Landlords have been underestimating retail sales growth over the past two years

Incoming foreign brands are driving up rental rates as well

04 January 2012

Hong K

ong Retail S

ector 9

Figure 17: Recently registered rental agreement Date Size Current lease agreement New lease agreement % chg.registered Location District (sq. ft) Lessee Rent

(HK$/month)Rent

(HK$/sq. ft) Lessee Rent

(HK$/month)Rent

(HK$/sq. ft)(rent/sq. ft)

22-Aug-11 J & K, 39-47 Lee Garden Road Causeway Bay 3,150 Fashion/Eyewear retailer

600,000 190 Luk Fook 1,500,000 476 150

2-Sep-11 41 Queen's Road Central 1,250 Bonjour 600,000 480 Seed 850,000 680 422-Sep-11 23-25 Lee Garden Road Causeway Bay 1,400 Bonjour 580,000 414 Swatch 2,300,000 1,643 2976-Sep-11 G-1/F, 28 Hankow Rd Tsim Sha Tsui 18,300 HMV 1,200,000 103 CSL/Bauhaus 2,500,000 137 327-Sep-11 Shop no. 3-7, 2-4 Hysan Road Causeway Bay 1,446 n.a. 250,000 173 Foreign chained

fashion retailer 500,000 346 100

12-Sep-11 G-1/f, Airland Center Mong Kok 15,000 Sa Sa/ Café De Coral

700,000 47 Lowry Farm 1,200,000 80 71

12-Sep-11 Argyle Street Mong Kok 2,000 Crocodile Shirt 980,000 490 Crocodile Shirt 1,800,000 900 8412-Sep-11 Sino Plaza Mong Kok 4,000 n.a. n.a 200 TSL/Wing Guang Jew 2,200,000 550 17514-Sep-11 G-2/f, MPM Mong Kok 15,000 Bonjour 600,000 53 GAP 3,200,000 213 30019-Sep-11 G/f, Park Lane HK Causeway Bay 3,000 Fashion retailer 650,000 217 King Fook Jewellery 1,200,000 400 8520-Sep-11 Unit B, G/f Melbourne Center,

33-33A Qeen's Road Central n.a. Tong Ren Tang 800,000 n.a. Tong Ren Tang 1,200,000 n.a. 50

20-Sep-11 G/f, 18 Queen's Road Central n.a. Standard Chartered Bank

1,500,000 n.a. Emperor Watch & Jew. 3,000,000 n.a. 100

20-Sep-11 G/F, 76 Percival Street Causeway Bay 600 RADO 640,000 1,067 RADO 1,330,000 2,217 10821-Sep-11 B-1/f, Lee Theatre Plaza Causeway Bay 30,000 California/Esprit 1,150,000 38 UNIQLO 2,300,000 77 10023-Sep-11 Shop C, 52 Yun Ping Road Causeway Bay 300 Lo Hang Ka 120,000 400 Citychain 250,000 833 10823-Sep-11 Shop A&B, 52 Yun Ping Road Causeway Bay 1,000 Longines 330,000 330 Longines 700,000 700 11223-Sep-11 G/f, 47 Haiphong Road Tsim Sha Tsui 1,500 Millie's 355,000 237 Crocs 710,000 473 10028-Sep-11 Shop 2, MPM Mong Kok 900 Hui Lau Shan 250,000 278 Crocs 580,000 644 13230-Sep-11 G/f, 68 Percival Street Causeway Bay 1,000 CSL 1010 295,000 295 CSL 1010 500,000 500 6930-Sep-11 G/-2/f, 108 Johnston Road Wanchai 4,819 Physical Fitness 150,000 31 Sa Sa 350,000 73 13330-Sep-11 1-2/f, 35- 37 Haiphong Road, Tsim Sha Tsui 3,600 沙嗲王 (Satay

King) 250,000 69 Sa Sa 500,000 139 100

4-Oct-11 2W-2X, Sai Yeong Choi Street South

Mong Kok 2,045 Sa Sa 700,000 342 Dai Lei Café 850,000 416 21

7-Oct-11 53 Carnavon Mans Tsim Sha Tsui 400 Bonjour 400,000 1,000 Chow Sang Sang 2,500,000 6,250 52511-Oct-11 G-1/f, 14 Kai Chiu Road Causeway Bay 3,000 Sa Sa 900,000 300 Chow Sang Sang 2,200,000 733 14411-Oct-11 G/f, Century Square, 1-13

D'Aguilar Street Central 1,000 Telecom shop 500,000 500 Watch retailer 650,000 650 30

13-Oct-11 Unit A, G/f Melbourne Center, 33-33A Qeen's Road

Central 1,300 Staccato 650,000 500 Pandora 1,600,000 1,231 146

14-Oct-11 No. 4-6, G/f, China Hong Kong City

Tsim Sha Tsui 15,000 Esprit 2,000,000 133 Emperor Watch & Jew. 3,500,000 233 75

26-Oct-11 16 Canton Road Tsim Sha Tsui 800 Swarovski 850,000 1,063 Swarovski 1,700,000 2,125 10027-Oct-11 Unit A,B, G-2/f, Soundwill Plaza,

Russell Street Causeway Bay 5,200 Nokia 1,850,000 356 Burberry 6,500,000 1,250 251

27-Oct-11 86-96 Canton Road Tsim Sha Tsui 4,200 Sa Sa 1,590,000 556 Asia Comm 6,300,000 1,500 1703-Nov-11 10 Kai Chiu Road Causeway Bay 1,500 Sa Sa 1,000,000 667 VIP Station 1,800,000 1,200 80

04 January 2012

Hong K

ong Retail S

ector 10

Figure 17: Recently registered rental agreement (cont’d) Date Size Current lease agreement New lease agreement % chg.registered Location District (sq. ft) Lessee Rent

(HK$/month)Rent

(HK$/sq. ft) Lessee Rent

(HK$/month)Rent

(HK$/sq. ft)(rent/sq. ft)

3-Nov-11 G-1/f, 18 D'Aguilar Street Central 2,000 Coffee shop 250,000 125 G2000 500,000 250 1004-Nov-11 G/f, 54-64B Nathan Road Tsim Sha Tsui 844 Pharmacy n.a. n.a. Pharmacy 600,000 711 n.a.4-Nov-11 15-17 Lee Garden Road Causeway Bay 1,500 Westwood 400,000 267 Sa Sa 1,000,000 667 15016-Nov-11 38-40 Haiphong Road Tsim Sha Tsui 2,300 Bonjour 680,000 296 Bonjour 1,140,000 496 6817-Nov-11 3-4/f, Entertainment Building Central 17,000 King Group 629,630 37 HMV 1,700,000 100 17022-Nov-11 Shop 38. G/f, 83-96 Nathan

Road Tsim Sha Tsui 500 Bird nest shop 253,000 506 Pharmacy 500,000 1,000 98

23-Nov-11 G/f, Island Beverly Center, 1 Great George Street

Causeway Bay 530 The Body Shop 500,000 943 The Body Shop 850,000 1,604 70

23-Nov-11 G/f, Honest Motors Building, Leighton Road

Causeway Bay 4,809 Quicksilver 290,000 60 I.T. 500,000 104 72

23-Nov-11 Shop 3-7, G/f, 2-4 Leighton Road Causeway Bay 1,700 n.a. 250,000 147 Replay 520,000 306 10824-Nov-11 Shop 76A, Fa Yuen Street Mong Kok n.a. Nike 2,015,000 n.a. Nike 2,490,000 n.a. 2429-Nov-11 Unit F, G/f, 601 Nathan Road Mong Kok 2,760 Mi-Ne Sushi 398,000 144 Jewellery retailer 900,000 326 12629-Nov-11 G/f, 717 Nathan Road Mong Kok 1,200 Jewellery retailer 235,000 196 Luk Fook 475,000 396 10229-Nov-11 Unit A, 701 Nathan Road Mong Kok 883 幸福珠寶 (Hang

Fook Jewellery) n.a. n.a. Luk Fook 350,000 396 n.a.

30-Nov-11 Unit F, G-1/f, Soundwill Plaza, Russell Street

Causeway Bay 6,952 Sa Sa 2,500,000 360 Omega 5,000,000 719 100

1-Dec-11 Unit G-J, Hong Kong Mansion, 1A-1L Yee Wo Street

Causeway Bay 5,520 King Fook 2,000,000 362 Sa Sa 3,000,000 543 50

Source: Company data, Credit Suisse estimates

04 January 2012

Hong Kong Retail Sector 11

We are cautious on mid- to high-end apparel retailers Earnings and valuations are at risk With increasing pressure from rental costs, we believe existing earnings forecasts for Hong Kong retailers could be optimistic. We have already seen some retailers reporting slower operating margin improvement in their latest half-yearly results, and the trend could continue with slower sales growth and higher operating costs.

Furthermore, the higher rental cost may eventually force some retailers to scale down their store expansion plans, which would trigger even more downward earnings estimate revisions, and result in some valuation de-rating.

What we learn from history? We studied the financial track record of 22 Hong Kong retail companies, under four different categories (namely apparel, hard luxury, cosmetic, F&B and others) for the past 11 years as well as the respective segment growth trend since 2002. The key findings from our study include:

(1) Among all sub-segments, the ‘apparels & accessories’ segment has the highest rental expenses-to-revenue ratio, followed by ‘food & beverages’, ‘cosmetics’, ‘others’ and ‘hard luxury’ segments.

(2) Both the ‘apparel & accessories’ and ‘hard luxury’ segments have recorded consistent rises in rental expense-to-revenue ratios.

(3) The ‘cosmetics’ segment has been the most resilient in terms of retail sales growth, while the ‘hard-luxury’ segment has been the most volatile. On the other hand, the ‘food & beverage’ segment has consistently underperformed other sub-segments.

(4) Among the sub-segments, ‘apparel & accessories’ and ‘hard luxury’ sales growth is still outpacing that of rental rate growth. On the other hand, rental rate growth started catching up with retail sales growth for the ‘cosmetic’ segment in 3Q11, while ‘food & beverage” sales revenue growth has been outpaced by rental rate growth since 1Q10.

04 January 2012

Hong Kong Retail Sector 12

Figure 18: Rental expense as a percentage of revenue Company Ticker 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010Apparels & accessories Bossini 0592.HK 14.0% 15.4% 16.6% 16.6% 15.0% 14.1% 16.0% 17.0% 16.9% 17.1% 16.3%Giordano 0709.HK 12.6% 13.3% 14.2% 15.1% 15.5% 16.0% 17.6% 16.4% 19.2% 20.2% 18.8%Bauhaus 0483.HK 17.1% 19.2% 18.9% 18.7% 18.8% 20.3% 23.2% 25.4% 25.4%I.T 0999.HK 17.5% 17.4% 16.8% 17.2% 18.0% 17.9% 18.5% 20.6% 20.1%Joyce Boutique 0647.HK 22.8% 23.1% 18.0% 17.5% 19.3% 17.8% 20.9% 21.5% 20.4% 18.2%Le Saunda 0738.HK 12.7% 12.7% 15.4% 10.9% 8.4% 9.4% 9.8% 10.3% 8.9% 6.7% 5.2%Moiselle 0130.HK 21.3% 25.6% 26.4% 24.2% 22.9% 25.2% 26.8% 30.4% 34.4% 33.2%Veeko 1173.HK 22.1% 25.8% 27.3% 26.3% 25.7% 25.4% 26.9% 25.5% 23.5% 23.9% 23.7%Dickson Concepts 0113.HK 9.1% 11.1% 11.8% 13.3% 13.3% 14.3% 16.5% 16.9% 17.6% 18.5% 18.6%Average 14.1% 17.5% 18.8% 18.1% 17.3% 17.5% 18.5% 19.1% 20.0% 20.8% 20.0%Median 12.7% 15.4% 17.1% 17.4% 16.8% 17.2% 17.8% 17.9% 19.2% 20.4% 18.8%Hard luxury Chow Sang Sang 0116.HK 2.1% 2.1% 2.0% 1.5% 1.4% 2.2% 4.2% 4.7% 2.2% 3.1% 2.8%Emperor Watch 0887.HK 2.5% 2.9% 3.1% 5.3% 8.0% 6.7%King Fook 0280.HK 3.6% 4.3% 5.0% 6.3% 6.0% 5.9% 5.5% 5.5% 5.7% 7.3% 8.4%Luk Fook 0590.HK 1.2% 1.1% 1.0% 1.4% 3.3% 3.6% 4.1% 3.7% 3.9% 4.0% 3.5%Oriental Watch 0398.HK 0.6% 0.6% 0.6% 0.6% 0.6% 0.8% 1.1% 1.5% 2.4% 3.5% 3.5%Milan station 1150.HK 6.0% 5.8% 5.9%Average 1.9% 2.0% 2.1% 2.4% 2.8% 3.0% 3.6% 3.7% 4.2% 5.3% 5.3%Median 1.6% 1.6% 1.5% 1.5% 2.3% 2.5% 4.1% 3.7% 4.6% 5.7% 5.9%Cosmetics Bonjour 0653.HK 9.8% 10.4% 10.4% 9.9% 9.6% 13.6% 14.9% 13.5% 11.6% 10.7% 10.7%Sa Sa 0178.HK 10.6% 9.8% 8.5% 8.4% 9.3% 9.6% 9.6% 9.7% 9.7%Average 9.8% 10.4% 10.5% 9.8% 9.0% 11.0% 12.1% 11.5% 10.6% 10.2% 10.2%Median 9.8% 10.4% 10.5% 9.8% 9.0% 11.0% 12.1% 11.5% 10.6% 10.2% 10.2%Food & Beverage Fairwood 0052.HK 18.3% 19.1% 19.2% 18.4% 16.9% 15.8% 14.6% 14.1% 14.3% 14.8% 14.7%Café de Coral 0341.HK 11.3% 10.9% 11.2% 11.3% 11.0% 10.7% 10.8% 11.1% 11.1% 11.0% 11.2%Tao Heung 0573.HK 6.3% 6.4% 6.8% 6.6% 7.1% 7.5% 7.4%Average 14.8% 15.0% 15.2% 14.8% 11.4% 11.0% 10.7% 10.6% 10.8% 11.1% 11.1%Median 14.8% 15.0% 15.2% 14.8% 11.0% 10.7% 10.8% 11.1% 11.1% 11.0% 11.2%Others Aeon stores 0984.HK 8.7% 8.9% 9.2% 8.2% 9.2% 9.8% 10.6% 10.2% 9.7% 11.1% 10.2%CRA 0831.HK 6.7% 6.7% 6.7% 6.8% 7.1% 7.6% 8.0% 8.6% 8.9% 9.3% 9.1%Average 7.7% 7.8% 7.9% 7.5% 8.1% 8.7% 9.3% 9.4% 9.3% 10.2% 9.7%Median 7.7% 7.8% 7.9% 7.5% 8.1% 8.7% 9.3% 9.4% 9.3% 10.2% 9.7%Overall average 9.5% 11.6% 12.9% 12.5% 11.8% 11.7% 12.3% 12.6% 12.6% 13.3% 12.6%Overall median 9.5% 11.0% 11.8% 11.3% 10.3% 10.7% 10.8% 11.1% 10.4% 10.8% 10.7%

Source: Company data, Credit Suisse estimates

04 January 2012

Hong Kong Retail Sector 13

Figure 19: YoY revenue growth Ticker 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010Apparels & accessories Bossini 0592.HK 16.9% 3.3% 6.2% 7.4% 12.0% 15.6% 2.5% -6.4% -0.2% 8.5%Giordano 0709.HK 1.4% 3.1% -5.5% 18.1% 10.2% -0.9% 13.2% -4.8% -10.1% 11.8%Bauhaus 0483.HK 8.1% 12.6% 15.9% 24.1% 18.1% 21.1% 16.6% 12.0%I.T 0999.HK 10.1% 25.5% 26.5% 17.8% 29.8% 34.8% 12.9% 25.2%Joyce Boutique 0647.HK 31.7% -38.7% 5.2% 9.0% 17.2% 15.2% 7.9% 14.0% 6.4% 8.4%Le Saunda 0738.HK -4.7% -6.8% 39.2% 25.4% 17.3% 10.5% 8.2% 15.1% 10.8% 28.6%Moiselle 0130.HK 11.6% 11.2% 10.4% 22.0% 8.3% 14.4% 13.4% 2.4% 5.6%Veeko 1173.HK 11.4% 9.1% 12.9% 6.9% 14.1% 13.1% 12.4% 13.8% 6.6% 15.8%Dickson Concepts 0113.HK -20.5% 4.9% 4.8% 6.9% 3.9% -0.2% 18.3% 15.6% 0.3% -5.5%Average 6.0% -1.9% 10.2% 13.6% 15.5% 11.5% 13.8% 13.0% 5.1% 12.3%Median 6.4% 3.3% 8.1% 10.4% 15.9% 13.1% 13.2% 14.0% 6.4% 11.8%Hard luxury Chow Sang Sang 0116.HK 0.0% 2.8% 31.4% 10.9% -17.9% 21.2% 12.8% 25.5% -4.2% 23.7%Emperor Watch 0887.HK 68.1% 44.0% 18.0% 45.8% 52.4%King Fook 0280.HK -13.5% -18.4% -19.2% 8.8% 13.3% 19.6% 21.1% 15.1% -5.7% 9.9%Luk Fook 0590.HK -6.6% -6.3% 1.4% 12.9% 18.6% 15.1% 29.0% 18.1% 22.8% 40.5%Oriental Watch 0398.HK 5.3% 8.2% 7.7% 1.2% 6.2% 6.9% 24.6% 4.1% -4.0% 25.0%Milan Station 1150.HK 19.4% 19.5%Average -3.7% -3.4% 5.3% 8.4% 5.1% 26.2% 26.3% 16.2% 12.4% 29.1%Median -3.3% -1.8% 4.5% 9.8% 9.8% 19.6% 24.6% 18.0% -4.0% 25.0%Cosmetics Bonjour 0653.HK 45.2% 36.0% 26.9% 33.0% 5.8% 6.2% 10.2% 14.2% 23.4% 24.4%Sa Sa 0178.HK 8.7% 6.8% 8.9% 17.0% 20.1% 10.2% 6.8% 18.0% 12.5% 15.4%Average 26.9% 21.4% 17.9% 25.0% 12.9% 8.2% 8.5% 16.1% 18.0% 19.9%Median 26.9% 21.4% 17.9% 25.0% 12.9% 8.2% 8.5% 16.1% 18.0% 19.9%Food & beverage Fairwood 0052.HK -7.8% -7.8% -3.9% 4.5% 13.9% 18.9% 21.3% 14.3% 3.2% 6.6%Café de Coral 0341.HK 4.8% 2.2% 1.2% 5.9% 12.0% 13.1% 12.2% 9.9% 7.9% 5.7%Tao Heung 0573.HK 21.2% 14.3% 32.4% 17.2% 6.8% 12.5%Average -1.5% -2.8% -1.4% 5.2% 15.7% 15.4% 22.0% 13.8% 6.0% 8.3%Median -1.5% -2.8% -1.4% 5.2% 13.9% 14.3% 21.3% 14.3% 6.8% 6.6%Others Aeon stores 0984.HK 8.6% 6.9% 14.8% 5.5% -17.5% 9.4% 11.0% 12.9% 9.8% 3.5%CRA 8052.HK 14.4% 6.8% 9.5% 13.8% 14.9% 11.8% 30.7% 13.9% 0.8% 6.7%Average 11.5% 6.9% 12.1% 9.7% -1.3% 10.6% 20.9% 13.4% 5.3% 5.1%Median 11.5% 6.9% 12.1% 9.7% -1.3% 10.6% 20.9% 13.4% 5.3% 5.1%Overall average 6.0% 1.4% 9.0% 12.4% 11.5% 15.2% 18.1% 14.2% 8.4% 16.9%Overall median 5.0% 3.3% 8.1% 10.4% 14.0% 13.1% 14.4% 14.3% 6.7% 12.5%

Source: Company data, Credit Suisse estimates

04 January 2012

Hong Kong Retail Sector 14

Figure 20: Retail sales growth trend among different segments

-40

-20

0

20

40

60

80

1Q02 4Q02 3Q03 2Q04 1Q05 4Q05 3Q06 2Q07 1Q08 4Q08 3Q09 2Q10 1Q11 4Q11

Overall Apparel Hard luxury Cosmetic & medicine F&B

(%)

Source: CEIC, Credit Suisse estimates

Figure 21: Apparel sales vs rental rate growth Figure 22: Hard luxury sales vs rental rate growth

-30

-20

-10

0

10

20

30

40

50

60

1Q02 1Q03 1Q04 1Q05 1Q06 1Q07 1Q08 1Q09 1Q10 1Q11 1Q12

Overall pr ime Premium primeHigh-street Reta il sales growth - Apparel

(%)

-40

-20

0

20

40

60

80

1Q02 1Q03 1Q04 1Q05 1Q06 1Q07 1Q08 1Q09 1Q10 1Q11 1Q12

Overall prime Premium primeHigh-street Retail sales growth - hard luxury

(%)

Source: CEIC, Jones Lang LaSalle, Credit Suisse estimates Source: CEIC, Jones Lang LaSalle, Credit Suisse estimates

04 January 2012

Hong Kong Retail Sector 15

Figure 23: Cosmetic sales vs rental rate growth Figure 24: F&B sales vs rental rate growth

-20

-10

0

10

20

30

40

50

60

1Q02 1Q03 1Q04 1Q05 1Q06 1Q07 1Q08 1Q09 1Q10 1Q11 1Q12

Overall prime Premium primeHigh-street Retail sa les growth - cosmetic

(%)

-20

-10

0

10

20

30

40

50

60

1Q02 4Q02 3Q03 2Q04 1Q05 4Q05 3Q06 2Q07 1Q08 4Q08 3Q09 2Q10 1Q11 4Q11

Overall prime Premium prime High-street Retail sales growth - F&B

(%)

Source: CEIC, Jones Lang LaSalle, Credit Suisse estimates Source: CEIC, Jones Lang LaSalle, Credit Suisse estimates

Mid- to high-end apparel retailers seem most vulnerable Based on the above, among all sub-segments, we found that mid- to high-end apparel retailers are the most vulnerable to the catching up of the rental cycle, on the back of their highest rental expense-to-turnover ratio, as well as relatively high revenue growth cyclicality. Bauhaus (0483.HK, HK$1.85, not rated), I.T (0999.HK, HK$4.27, not rated), Moiselle (0130.HK, HK$2.06, not rated) and Veeko (1173.HK, HK$0.23, not rated) all have rental expense that exceeded 20% of their turnover in 2010.

And for those companies that had disclosed rental expenses in their latest half-yearly results, all, except I.T, had recorded rises in rental expense-to-turnover ratios. In the case of I.T, we believe it is partly because of its aggressive store openings; it opened nine additional shops in Hong Kong during the period, and some of them are located in new shopping malls and thus, have a relatively lower-than-advantage rental rate.

Figure 25: Rental expense-to-turnover ratio—select mid- to high-end apparel retailers

0

5

10

15

20

25

30

35

Giordano Bauhaus I.T Joyce Boutique Le Saunda

CY2010 Latest half-year

(%)

Source: Company data, Credit Suisse estimates

Mid- to high-end apparel retailers have the highest rental cost-to-revenue ratios

04 January 2012

Hong Kong Retail Sector 16

Hard luxury segment may see less impact compared to the previous cycle While the hard luxury segment has historically been more cyclical in terms of sales performance, with believe this cycle is different due to the much-increased revenue contribution from mainland Chinese shoppers in Hong Kong, who take advantage of lower retail prices here due to the absence of VAT, consumption tax and import duties (for further details, please refer to our 08 August 2011 report, A bargain for luxury products).

As mentioned above, Hong Kong locals have been on a down-trading mode for more than two years, but the hard luxury segment’s contribution to overall retail sales in Hong Kong has been increasing, accounting for 22.2% of total retail sales in Hong Kong in the first ten months of 2011; in our view, the growth is largely, if not all, driven by the visiting mainland Chinese shoppers.

Figure 26: Hard luxury’s contribution to total retail sales in Hong Kong

0

5

10

15

20

25

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 10m11

(%)

Source: CEIC, Credit Suisse estimates

Besides, hard luxury retailers normally have a very low rental-to-turnover ratio of less than 5%, which makes them less vulnerable to rental pressure. We reiterate Luk Fook (0590.HK, HK$27.70, OUTPERFORM [V], TP HK$37.80) as our top pick in the Hong Kong retail sector. Furthermore, the company also has the most potential share price upside, among all the Hong Kong retailers discussed in this report, based on our HOLT analysis. We discuss this in more detail in a later section.

Stiff price differential between Hong Kong and China may help support sales growth of luxury retailers

04 January 2012

Hong Kong Retail Sector 17

Figure 27: Hard luxury segment has the lowest rental expense to turnover ratio

0

5

10

15

20

25

Apparel & accessories Hard luxury Cosmetic F&B Others

2010 rental expense to turnover ratio

(%)

Source: Company data, Credit Suisse estimates

Cosmetics segment looks most resilient On the other hand, cosmetics retailers such as Sa Sa (0178.HK, HK$4.36, NEUTRAL [V], TP HK$5.00) and Bonjour (0653.HK, HK$1.23, not rated) have shown the most resilient sales growth during economic downturns. In our view, it could be because cosmetics are considered more ‘essential’ than ‘luxury’ consumption by female consumers, and during economic downturns, they would rather cut spending on clothing than cosmetics.

However, cosmetics are subject to a high consumption tax rate in China, making the price differential steep between Hong Kong and the mainland. Besides, a wider product variety, better product quality and higher certainty of product genuineness also make Hong Kong a better place to buy cosmetics.

However, we notice severe competition for rental spaces (not only among cosmetics retailers, but hard luxury retailers and newly entered foreign brands as well) in key tourist districts, and this results in a significant increase in rental costs.

In the past three months, based on our channel checks, Sa Sa signed four new rental agreements with rental rates 50-150% higher than the previous one. While Bonjour only recorded one new rental agreement during the period, with a rental rate 68% higher than the previous one, it was replaced by other retailers in five other locations, with the new rental rates being 42-300% higher than what it paid previously.

Given their aggressive store expansions in their latest fiscal half-year (both Sa Sa and Bonjour opened six additional stores in Hong Kong), we remain cautious on cosmetics retailers’ margins.

Cosmetic retails have been most resilient in terms of sales growth

04 January 2012

Hong Kong Retail Sector 18

Figure 28: Recently recorded new rental agreement which involved cosmetic retailers Current Rent New Rent Date recorded District lessee (HK$/mo) (HK$/sq. ft) lessee (HK$/mo) (HK$/sq. ft) % chg.2-Sep-11 Central Bonjour 600,000 480 Seed 850,000 680 422-Sep-11 Causeway Bay Bonjour 580,000 414 Swatch 2,300,000 1,643 29712-Sep-11 Mong Kok Sa Sa/ Café De Coral 700,000 47 Lowry Farm 1,200,000 80 7114-Sep-11 Mong Kok Bonjour 600,000 53 GAP 3,200,000 213 30030-Sep-11 Wanchai Physical Fitness 150,000 31 Sa Sa 350,000 73 13330-Sep-11 Tsim Sha Tsui 沙嗲王 (Satay King) 250,000 69 Sa Sa 500,000 139 10011-Oct-11 Causeway Bay Sa Sa 900,000 300 Chow Sang Sang 2,200,000 733 14427-Oct-11 Tsim Sha Tsui Sa Sa 1,590,000 556 Asia Comm 6,300,000 1,500 1703-Nov-11 Causeway Bay Sa Sa 1,000,000 667 VIP Station 1,800,000 1,200 804-Nov-11 Causeway Bay Westwood 400,000 267 Sa Sa 1,000,000 667 15016-Nov-11 Tsim Sha Tsui Bonjour 680,000 296 Bonjour 1,140,000 496 6822-Nov-11 Causeway Bay Bonjour 580,000 414 Watch/Jewellery Shop 2,320,000 1,657 30030-Nov-11 Causeway Bay Sa Sa 2,500,000 360 Omega 5,000,000 719 1001-Dec-11 Causeway Bay King Fook 2,000,000 362 Sa Sa 3,000,000 543 50

Source: Company data, Credit Suisse estimates

F&B retailers remain under pressure Besides pressure from rental hikes (F&B is one of the few sub-segments whose revenue growth has been outpaced by rental rate hikes since the end of the global financial crisis in 2008-09), food inflation has also been catching up. The margin pressure is particularly severe for fast food chains, such as Café de Coral (0341.HK, HK$17.82, not rated) and Fairwood (0052.HK, HK$10.10, not rated), on the back of the minimum wage law imposed since May 2011, putting additional pressure on F&B retailers’ margins.

Figure 29: Food inflation versus growth in restaurant receipts

-2

-1

0

1

2

3

4

5

6

7

Jan-09 Apr-09 Jul-09 Oct-09 Jan-10 Apr-10 Jul-10 Oct-10 Jan-11 Apr-11 Jul -11 Oct-11

Food inflation YoY % chg in restaurant receipt

(%)

Source: CEIC, Credit Suisse estimates

HOLT’s view on the Hong Kong retail sector Below is the analysis produced by our HOLT® consumer analyst, Jane Tai. In summary, she believes Hong Kong retailers are priced for peak level returns and robust growth; thus potential upside is only warranted if asset growth surprises on the upside. Among the 19 companies studied, only Luk Fook (0590.HK, HK$27.70, OUTPERFORM [V], TP HK$37.80) and Dickson Concepts (0113.HK, HK$3.95, not rated) show positive upside to HOLT’s best warranted prices.

F&B is likely to remain under margin pressure

04 January 2012

Hong K

ong Retail Sector

19

Figure 30: HOLT’s analysis

1CLARITY IS CONFIDENCE HOLT

HK retailing sector: Priced for peak level returns and robust growth

Performance: HK retailers have achieved fairly stable high single digit CFROI® in the past 6 years with a small dip in 2008. IBES consensus estimates suggest further improvement in economic returns to around 11% for 2011 on a more optimistic consumer spending outlook.

What is in the price? Assuming 2011 consensus can be maintained by 2015, the sector will need to achieve 13% CAGR p.a. to justify the current valuation. Expectations appear fair on account of increasing tourist arrivals, particularly those from Mainland China. Upside is only warranted if asset growth surprises, as last seen in 2010.

10.9%

Source: HOLT Macrostation includes 14 HK retail companies.

Aggregate CFROI & asset growth

13%

Source: Company data, Credit Suisse HOLT

04 January 2012

Hong Kong Retail Sector 20

Figure 31: HOLT analysis—CFROI

0

2

4

6

8

10

12

14

16

18

590 653 178 738 116 573 647 887 999 709 341 398 483 984 52 113 592 130 280

CFROI (%)

(%)

Median = 7.5%

Source: Company data, Credit Suisse HOLT

Figure 32: HOLT analysis—asset efficiency (sales/inflation adj. gross investment)

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

590 116 398 653 887 178 573 984 738 592 999 647 280 341 483 709 52 113 130

Asset efficiency

Median = 0.65

Source: Company data, Credit Suisse HOLT

04 January 2012

Hong Kong Retail Sector 21

Figure 33: HOLT analysis—adjusted operating margin

0

10

20

30

40

50

60

130 483 999 709 647 113 52 341 592 178 653 738 573 984 887 590 280 116 398

Adj. operating margin (%)

(%)

Median = 23.7%

Source: Company data, Credit Suisse HOLT

Figure 34: HOLT analysis—rental expense as % of gross cash flow

0

10

20

30

40

50

60

70

80

90

280 592 483 130 113 999 709 984 647 52 653 341 178 887 398 573 116 738 590

Rental expense as % of gross cash flow

Median = 57.4%

(%)

Source: Company data, Credit Suisse HOLT

04 January 2012

Hong Kong Retail Sector 22

Figure 35: HOLT analysis—sales/capitalised operating leases

0

1

2

3

4

5

6

116 590 398 887 573 738 178 653 280 999 984 592 341 647 483 709 113 52 130

Sales/ cap ita lized operating leases

Median = 1.1

Source: Company data, Credit Suisse HOLT

Figure 36: HOLT analysis—potential to HOLT's best warranted prices

-120

-100

-80

-60

-40

-20

0

20

113 590 116 999 398 483 887 653 738 709 573 178 341 647 592 984 52 130 280

Potentia l to HOLT's best warranted price (%)

Median = 39.0%

(%)

Source: Company data, Credit Suisse HOLT

Companies Mentioned (Price as of 03 Jan 12) Abercrombie & Fitch Co. (ANF, $48.84, NOT RATED) Aeon Stores (Hong Kong) Company Ltd (0984.HK, HK$17.90, NOT RATED) Bauhaus Int'l (0483.HK, HK$1.85, NOT RATED) Bonjour (0653.HK, HK$1.23, NOT RATED) Bossini Int'l (0592.HK, HK$0.59, NOT RATED) Cafe De Coral Holdings Ltd (0341.HK, HK$17.82, NOT RATED) Chow Sang Sang (0116.HK, HK$17.52, NOT RATED) CRA (0831.HK, HK$3.22, NOT RATED) Dickson Concepts (0113.HK, HK$3.95, NOT RATED) Emperor Watch & Jel. (0887.HK, HK$0.99, NOT RATED) Fairwood (0052.HK, HK$10.10, NOT RATED) Gap, Inc. (GPS, $18.55, NOT RATED) Giordano Intl. (0709.HK, HK$5.65, NOT RATED) I.T (0999.HK, HK$4.27, NOT RATED) Joyce Boutique (0647.HK, HK$0.74, NOT RATED)

04 January 2012

Hong Kong Retail Sector 23

King Fook (0280.HK, HK$1.16, NOT RATED) Le Saunda (0738.HK, HK$2.69, NOT RATED) Luk Fook Holdings International (0590.HK, HK$27.70, OUTPERFORM [V], TP HK$37.80) Milan Station (1150.HK, HK$1.34, NOT RATED) Moiselle (0130.HK, HK$2.06, NOT RATED) Oriental Watch (0398.HK, HK$3.53, NOT RATED) Sa Sa International Holding (0178.HK, HK$4.36, NEUTRAL [V], TP HK$5.00) Tao Heung (0573.HK, HK$3.06, NOT RATED) Veeko (1173.HK, HK$0.23, NOT RATED)

Disclosure Appendix Important Global Disclosures Gabriel Chan, CFA & Isis Wong each certify, with respect to the companies or securities that he or she analyzes, that (1) the views expressed in this report accurately reflect his or her personal views about all of the subject companies and securities and (2) no part of his or her compensation was, is or will be directly or indirectly related to the specific recommendations or views expressed in this report. See the Companies Mentioned section for full company names. 3-Year Price, Target Price and Rating Change History Chart for 0590.HK 0590.HK Closing

Price Target

Price

Initiation/ Date (HK$) (HK$) Rating Assumption 5-Jan-11 26.95 33.8 O X 21-Apr-11 29 35 30-Jun-11 37.75 45 2-Aug-11 43.7 51.75 27-Sep-11 25.3 35 29-Nov-11 30.15 37.8

34 35

45

52

3538

5-Jan-11

O

1

11

21

31

41

51

3-Jan-

09

3-Mar-

09

3-May-

09

3-Jul-09

3-Sep-09

3-Nov-09

3-Jan-10

3-Mar-10

3-May-

10

3-Jul-1

0

3-Sep

-10

3-Nov-

10

3-Jan-

11

3-Mar-

11

3-May-

11

3-Jul-11

3-Sep-

11

3-Nov-

11

Closing Pr ice Target Price Initiation/Assumption Rating

HK$

O=Outperform; N=Neutral; U=Underperform; R=Restricted; NR=Not Rated; NC=Not Covered

3-Year Price, Target Price and Rating Change History Chart for 0178.HK 0178.HK Closing

Price Target

Price

Initiation/ Date (HK$) (HK$) Rating Assumption 26-Jun-09 1.445 1.615 30-Nov-09 2.44 2.61 25-Jun-10 3.07 3.55 12-Oct-10 3.11 4.05 X 2-Dec-10 4.885 5.5 8-Sep-11 5.26 5 N 2

3

44

65

12-Oct-10

N

0

1

2

3

4

5

6

7

8

3-Jan-

09

3-Mar-

09

3-May-

09

3-Jul-09

3-Sep-09

3-Nov-09

3-Jan-10

3-Mar-10

3-May-

10

3-Jul-1

0

3-Sep

-10

3-Nov-

10

3-Jan-

11

3-Mar-

11

3-May-

11

3-Jul-11

3-Sep-

11

3-Nov-

11

Closing Pr ice Target Price Initiation/Assumption Rating

HK$

O=Outperform; N=Neutral; U=Underperform; R=Restricted; NR=Not Rated; NC=Not Covered

The analyst(s) responsible for preparing this research report received compensation that is based upon various factors including Credit Suisse's total revenues, a portion of which are generated by Credit Suisse's investment banking activities. Analysts’ stock ratings are defined as follows: Outperform (O): The stock’s total return is expected to outperform the relevant benchmark* by at least 10-15% (or more, depending on perceived risk) over the next 12 months. Neutral (N): The stock’s total return is expected to be in line with the relevant benchmark* (range of ±10-15%) over the next 12 months. Underperform (U): The stock’s total return is expected to underperform the relevant benchmark* by 10-15% or more over the next 12 months. *Relevant benchmark by region: As of 29th May 2009, Australia, New Zealand, U.S. and Canadian ratings are based on (1) a stock’s absolute total return potential to its current share price and (2) the relative attractiveness of a stock’s total return potential within an analyst’s coverage universe**, with Outperforms representing the most attractive, Neutrals the less attractive, and Underperforms the least attractive investment opportunities. Some U.S. and Canadian ratings may fall outside the absolute total return ranges defined above, depending on market conditions and industry

04 January 2012

Hong Kong Retail Sector 24

factors. For Latin American, Japanese, and non-Japan Asia stocks, ratings are based on a stock’s total return relative to the average total return of the relevant country or regional benchmark; for European stocks, ratings are based on a stock’s total return relative to the analyst's coverage universe**. For Australian and New Zealand stocks, 12-month rolling yield is incorporated in the absolute total return calculation and a 15% and a 7.5% threshold replace the 10-15% level in the Outperform and Underperform stock rating definitions, respectively. The 15% and 7.5% thresholds replace the +10-15% and -10-15% levels in the Neutral stock rating definition, respectively. **An analyst's coverage universe consists of all companies covered by the analyst within the relevant sector. Restricted (R): In certain circumstances, Credit Suisse policy and/or applicable law and regulations preclude certain types of communications, including an investment recommendation, during the course of Credit Suisse's engagement in an investment banking transaction and in certain other circumstances. Volatility Indicator [V]: A stock is defined as volatile if the stock price has moved up or down by 20% or more in a month in at least 8 of the past 24 months or the analyst expects significant volatility going forward.

Analysts’ coverage universe weightings are distinct from analysts’ stock ratings and are based on the expected performance of an analyst’s coverage universe* versus the relevant broad market benchmark**: Overweight: Industry expected to outperform the relevant broad market benchmark over the next 12 months. Market Weight: Industry expected to perform in-line with the relevant broad market benchmark over the next 12 months. Underweight: Industry expected to underperform the relevant broad market benchmark over the next 12 months. *An analyst’s coverage universe consists of all companies covered by the analyst within the relevant sector. **The broad market benchmark is based on the expected return of the local market index (e.g., the S&P 500 in the U.S.) over the next 12 months. Credit Suisse’s distribution of stock ratings (and banking clients) is:

Global Ratings Distribution Outperform/Buy* 47% (61% banking clients) Neutral/Hold* 40% (57% banking clients) Underperform/Sell* 10% (51% banking clients) Restricted 2%

*For purposes of the NYSE and NASD ratings distribution disclosure requirements, our stock ratings of Outperform, Neutral, and Underperform most closely correspond to Buy, Hold, and Sell, respectively; however, the meanings are not the same, as our stock ratings are determined on a relative basis. (Please refer to definitions above.) An investor's decision to buy or sell a security should be based on investment objectives, current holdings, and other individual factors.

Credit Suisse’s policy is to update research reports as it deems appropriate, based on developments with the subject company, the sector or the market that may have a material impact on the research views or opinions stated herein. Credit Suisse's policy is only to publish investment research that is impartial, independent, clear, fair and not misleading. For more detail please refer to Credit Suisse's Policies for Managing Conflicts of Interest in connection with Investment Research: http://www.csfb.com/research-and-analytics/disclaimer/managing_conflicts_disclaimer.html Credit Suisse does not provide any tax advice. Any statement herein regarding any US federal tax is not intended or written to be used, and cannot be used, by any taxpayer for the purposes of avoiding any penalties. See the Companies Mentioned section for full company names. Price Target: (12 months) for (0590.HK) Method: Our TP of HK$37.80 for Luk Fook is based on 13x FY3/13 P/E (price-to-earnings ratio). Our valuation target also implies 10% discount to other China focused high-end retailers. In our view, as over 60% of Luk Fook's operating profits are directly or indirectly coming from China, its valuation gap should continue to narrow. Risks: Risks to our HK$37.80 target price includes 1) sharp decline in precious metals or gem prices, 2) higher-than-expected increase in rental costs, and 3) failure to uphold product control and monitor sales through franchisees. Price Target: (12 months) for (0178.HK) Method: Our HK$5.00 target price for Sa Sa is based on 0.80x price/earnings growth (PEG) or 18x FY3/13 P/E. Risks: Risks to our HK$5.00 target price for Sa Sa of include: 1) a slowdown in domestic consumption, 2) bad tourist arrival figures from China at Hong Kong, 3) execution of its China retail expansion plans, and 4) whether continued roll-out of its in-house brands is successful Please refer to the firm's disclosure website at www.credit-suisse.com/researchdisclosures for the definitions of abbreviations typically used in the target price method and risk sections.

See the Companies Mentioned section for full company names. Credit Suisse expects to receive or intends to seek investment banking related compensation from the subject company (0178.HK) within the next 3 months. Important Regional Disclosures Singapore recipients should contact a Singapore financial adviser for any matters arising from this research report. The analyst(s) involved in the preparation of this report have not visited the material operations of the subject company (0590.HK, 0178.HK) within the past 12 months. Restrictions on certain Canadian securities are indicated by the following abbreviations: NVS--Non-Voting shares; RVS--Restricted Voting Shares; SVS--Subordinate Voting Shares.

04 January 2012

Hong Kong Retail Sector 25

Individuals receiving this report from a Canadian investment dealer that is not affiliated with Credit Suisse should be advised that this report may not contain regulatory disclosures the non-affiliated Canadian investment dealer would be required to make if this were its own report. For Credit Suisse Securities (Canada), Inc.'s policies and procedures regarding the dissemination of equity research, please visit http://www.csfb.com/legal_terms/canada_research_policy.shtml. As of the date of this report, Credit Suisse acts as a market maker or liquidity provider in the equities securities that are the subject of this report. Principal is not guaranteed in the case of equities because equity prices are variable. Commission is the commission rate or the amount agreed with a customer when setting up an account or at anytime after that. Taiwanese Disclosures: Reports written by Taiwan-based analysts on non-Taiwan listed companies are not considered recommendations to buy or sell securities under Taiwan Stock Exchange Operational Regulations Governing Securities Firms Recommending Trades in Securities to Customers. To the extent this is a report authored in whole or in part by a non-U.S. analyst and is made available in the U.S., the following are important disclosures regarding any non-U.S. analyst contributors: The non-U.S. research analysts listed below (if any) are not registered/qualified as research analysts with FINRA. The non-U.S. research analysts listed below may not be associated persons of CSSU and therefore may not be subject to the NASD Rule 2711 and NYSE Rule 472 restrictions on communications with a subject company, public appearances and trading securities held by a research analyst account. • Gabriel Chan, CFA, non-U.S. analyst, is a research analyst employed by Credit Suisse (Hong Kong) Limited. • Isis Wong, non-U.S. analyst, is a research analyst employed by Credit Suisse (Hong Kong) Limited. For Credit Suisse disclosure information on other companies mentioned in this report, please visit the website at www.credit-suisse.com/researchdisclosures or call +1 (877) 291-2683. Disclaimers continue on next page.

04 January 2012Asia Pacific/Hong Kong

Equity Research

CS0583

This report is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation or which would subject Credit Suisse AG, the Swiss bank, or its subsidiaries or its affiliates (“CS”) to any registration or licensing requirement within such jurisdiction. All material presented in this report, unless specifically indicated otherwise, is under copyright to CS. None of the material, nor its content, nor any copy of it, may be altered in any way, transmitted to, copied or distributed to any other party, without the prior express written permission of CS. All trademarks, service marks and logos used in this report are trademarks or service marks or registered trademarks or service marks of CS or its affiliates. The information, tools and material presented in this report are provided to you for information purposes only and are not to be used or considered as an offer or the solicitation of an offer to sell or to buy or subscribe for securities or other financial instruments. CS may not have taken any steps to ensure that the securities referred to in this report are suitable for any particular investor. CS will not treat recipients as its customers by virtue of their receiving the report. The investments or services contained or referred to in this report may not be suitable for you and it is recommended that you consult an independent investment advisor if you are in doubt about such investments or investment services. Nothing in this report constitutes investment, legal, accounting or tax advice or a representation that any investment or strategy is suitable or appropriate to your individual circumstances or otherwise constitutes a personal recommendation to you. CS does not offer advice on the tax consequences of investment and you are advised to contact an independent tax adviser. Please note in particular that the bases and levels of taxation may change. CS believes the information and opinions in the Disclosure Appendix of this report are accurate and complete. Information and opinions presented in the other sections of the report were obtained or derived from sources CS believes are reliable, but CS makes no representations as to their accuracy or completeness. Additional information is available upon request. CS accepts no liability for loss arising from the use of the material presented in this report, except that this exclusion of liability does not apply to the extent that liability arises under specific statutes or regulations applicable to CS. This report is not to be relied upon in substitution for the exercise of independent judgment. CS may have issued, and may in the future issue, a trading call regarding this security. Trading calls are short term trading opportunities based on market events and catalysts, while stock ratings reflect investment recommendations based on expected total return over a 12-month period as defined in the disclosure section. Because trading calls and stock ratings reflect different assumptions and analytical methods, trading calls may differ directionally from the stock rating. In addition, CS may have issued, and may in the future issue, other reports that are inconsistent with, and reach different conclusions from, the information presented in this report. Those reports reflect the different assumptions, views and analytical methods of the analysts who prepared them and CS is under no obligation to ensure that such other reports are brought to the attention of any recipient of this report. CS is involved in many businesses that relate to companies mentioned in this report. These businesses include specialized trading, risk arbitrage, market making, and other proprietary trading. Past performance should not be taken as an indication or guarantee of future performance, and no representation or warranty, express or implied, is made regarding future performance. Information, opinions and estimates contained in this report reflect a judgement at its original date of publication by CS and are subject to change without notice. The price, value of and income from any of the securities or financial instruments mentioned in this report can fall as well as rise. The value of securities and financial instruments is subject to exchange rate fluctuation that may have a positive or adverse effect on the price or income of such securities or financial instruments. Investors in securities such as ADR’s, the values of which are influenced by currency volatility, effectively assume this risk. Structured securities are complex instruments, typically involve a high degree of risk and are intended for sale only to sophisticated investors who are capable of understanding and assuming the risks involved. The market value of any structured security may be affected by changes in economic, financial and political factors (including, but not limited to, spot and forward interest and exchange rates), time to maturity, market conditions and volatility, and the credit quality of any issuer or reference issuer. Any investor interested in purchasing a structured product should conduct their own investigation and analysis of the product and consult with their own professional advisers as to the risks involved in making such a purchase. Some investments discussed in this report have a high level of volatility. High volatility investments may experience sudden and large falls in their value causing losses when that investment is realised. Those losses may equal your original investment. Indeed, in the case of some investments the potential losses may exceed the amount of initial investment, in such circumstances you may be required to pay more money to support those losses. Income yields from investments may fluctuate and, in consequence, initial capital paid to make the investment may be used as part of that income yield. Some investments may not be readily realisable and it may be difficult to sell or realise those investments, similarly it may prove difficult for you to obtain reliable information about the value, or risks, to which such an investment is exposed. This report may provide the addresses of, or contain hyperlinks to, websites. Except to the extent to which the report refers to website material of CS, CS has not reviewed the linked site and takes no responsibility for the content contained therein. Such address or hyperlink (including addresses or hyperlinks to CS’s own website material) is provided solely for your convenience and information and the content of the linked site does not in any way form part of this document. Accessing such website or following such link through this report or CS’s website shall be at your own risk. This report is issued and distributed in Europe (except Switzerland) by Credit Suisse Securities (Europe) Limited, One Cabot Square, London E14 4QJ, England, which is regulated in the United Kingdom by The Financial Services Authority (“FSA”). This report is being distributed in Germany by Credit Suisse Securities (Europe) Limited Niederlassung Frankfurt am Main regulated by the Bundesanstalt fuer Finanzdienstleistungsaufsicht ("BaFin"). This report is being distributed in the United States by Credit Suisse Securities (USA) LLC ; in Switzerland by Credit Suisse AG; in Canada by Credit Suisse Securities (Canada), Inc.; in Brazil by Banco de Investimentos Credit Suisse (Brasil) S.A. or its affiliates; in Mexico by Banco Credit Suisse (México), S.A. (transactions related to the securities mentioned in this report will only be effected in compliance with applicable regulation); in Japan by Credit Suisse Securities (Japan) Limited, Financial Instrument Firm, Director-General of Kanto Local Finance Bureau (Kinsho) No. 66, a member of Japan Securities Dealers Association, The Financial Futures Association of Japan, Japan Securities Investment Advisers Association, Type II Financial Instruments Firms Association; elsewhere in Asia/Pacific by whichever of the following is the appropriately authorised entity in the relevant jurisdiction: Credit Suisse (Hong Kong) Limited, Credit Suisse Equities (Australia) Limited , Credit Suisse Securities (Thailand) Limited, Credit Suisse Securities (Malaysia) Sdn Bhd, Credit Suisse AG, Singapore Branch, Credit Suisse Securities (India) Private Limited regulated by the Securities and Exchange Board of India (registration Nos. INB230970637; INF230970637; INB010970631; INF010970631), having registered address at 9th Floor, Ceejay House,Dr.A.B. Road, Worli, Mumbai - 18, India, T- +91-22 6777 3777, Credit Suisse Securities (Europe) Limited, Seoul Branch, Credit Suisse AG, Taipei Securities Branch, PT Credit Suisse Securities Indonesia, Credit Suisse Securities (Philippines ) Inc., and elsewhere in the world by the relevant authorised affiliate of the above. Research on Taiwanese securities produced by Credit Suisse AG, Taipei Securities Branch has been prepared by a registered Senior Business Person. Research provided to residents of Malaysia is authorised by the Head of Research for Credit Suisse Securities (Malaysia) Sdn. Bhd., to whom they should direct any queries on +603 2723 2020. In jurisdictions where CS is not already registered or licensed to trade in securities, transactions will only be effected in accordance with applicable securities legislation, which will vary from jurisdiction to jurisdiction and may require that the trade be made in accordance with applicable exemptions from registration or licensing requirements. Non-U.S. customers wishing to effect a transaction should contact a CS entity in their local jurisdiction unless governing law permits otherwise. U.S. customers wishing to effect a transaction should do so only by contacting a representative at Credit Suisse Securities (USA) LLC in the U.S. Please note that this report was originally prepared and issued by CS for distribution to their market professional and institutional investor customers. Recipients who are not market professional or institutional investor customers of CS should seek the advice of their independent financial advisor prior to taking any investment decision based on this report or for any necessary explanation of its contents. This research may relate to investments or services of a person outside of the UK or to other matters which are not regulated by the FSA or in respect of which the protections of the FSA for private customers and/or the UK compensation scheme may not be available, and further details as to where this may be the case are available upon request in respect of this report. Any Nielsen Media Research material contained in this report represents Nielsen Media Research's estimates and does not represent facts. NMR has neither reviewed nor approved this report and/or any of the statements made herein. If this report is being distributed by a financial institution other than Credit Suisse AG, or its affiliates, that financial institution is solely responsible for distribution. Clients of that institution should contact that institution to effect a transaction in the securities mentioned in this report or require further information. This report does not constitute investment advice by Credit Suisse to the clients of the distributing financial institution, and neither Credit Suisse AG, its affiliates, and their respective officers, directors and employees accept any liability whatsoever for any direct or consequential loss arising from their use of this report or its content. Copyright 2012 CREDIT SUISSE AG and/or its affiliates. All rights reserved.

CREDIT SUISSE (Hong Kong) Limited Asia/Pacific: +852 2101-6000