Home Depot Situation Analysis 5471644 -...

36

Situation Analysis: Home Depot Samantha Dintsch Rebecca Harris Camille Harvey Natalie Townsend Mary Carlie Vaughn Natalie White

Transcript of Home Depot Situation Analysis 5471644 -...

Situation Analysis: Home Depot

Samantha Dintsch

Rebecca Harris

Camille Harvey

Natalie Townsend

Mary Carlie Vaughn

Natalie White

2

Introduction 1

Industry Overview 4-8

Client Profile: The Home Depot 9-11

Competitor Analysis: Lowe’s

Comparative Analysis

12

13

Secondary Competitor Analysis: Sears and WalMart 14

Consumer Analysis 15

Quantitative Research

Qualitative Research

Marketing/Communications Recommendations

Appendix I: Survey

Appendix II: Qualitative Guide

Reference List

16-19

20-

T a b l e O f C o n t e n t s

3

I n t r o d u c t i o n

A s the largest home improvement store in the United States, The Home Depot has made a name for itself in the home im-provement industry. With the recent decline in the home im-

provement industry and increased competition from Lowe’s, The Home Depot must innovate in order to maintain its place in the market. By analyzing the home improvement market and competition within the market, The Home Depot can gain insight into industry trends and market its brand accordingly. The following report will explore the home improvement industry as a whole, The Home Depot and its competitors, and the consumer base.

B y highlighting valuable information about the home improvement industry, the industry overview pro-vides the information necessary to begin researching

The Home Depot. The Industry Overview also illustrates how The Home Depot compares to its competitors. Key points in the Indus-try Overview are the history of the industry, industry size, advertising expenditures, growth Industry Overview are The Home Depot’s primary and secondary competitors, social and cultural trends, the effect of the economic environment on the industry, regulatory and legal issues, and new developments within the home improvement industry. Following the Industry Overview is the Client Profile and Competitor Analysis. This section is very important because it not only provides information about The Home Depot’s history, sales, and marketing mix, but it also provides the same information about The Home Depot’s primary com-petitor, Lowe’s.

T he final section of the situation analysis is the Consumer Analy-sis. In order for The Home Depot’s marketing efforts to be suc-cessful it must be aware of its target market. This section ana-

lyzes consumer trends in the home improvement industry, highlighting the demographics and psychographics that comprise the overall target

market.

B y looking at all the different aspects of the home improvement industry, we can better recognize The Home Depot’s role within the industry. Knowing the details of the industry is cru-

cial to implementing the correct marketing strategy in order to main-tain The Home Depot’s place in the market.

T o gain further information about females atti-tudes and beliefs of The Home Depot, our group designed and conducted a survey. We hand dis-

tributed the survey in locations such as The Home Depot, Lowe’s, WalMart, Sears, Bed, Bath and Beyond. The ulti-mate goal of this survey was to discover information on the following research objectives: To measure the target

market's current, past (last 12 months) or future (next 12 months) home improvement projects or plans, to assess the target market's attitudes and beliefs about home improvement retailers, to assess the target mar-ket's attitudes and beliefs about The Home Depot, to assess the target market’s attitudes and beliefs about Lowe’s in comparison to your cli-ent, to measure the target market's The Home Depot usage, and to iden-tify if there are consumer behavioral differences in age, gender, income, etc.

A fter the survey was conducted there was still some lack of in-formation and gaps in fully understanding the home improve-ment consumers. Therefore we conducted six personal inter-

views to fill in those gaps, gain further consumer insight and attitudes towards The Home Depot. These personal interviews allowed more flexibility and probing than the survey. These interview questions di-rectly addressed the needed information to conclude the findings from the quantitative research.

4

T he home improvement industry be-gan primarily with many local hard-ware stores, such as Lowe’s North

Wilkesboro Hardware Store. Lucious S. Lowe opened this small store in North Carolina in 1921. After his death, his son, Jim Lowe and war veteran friend, Carl Buchan, took over the business. They expanded the business and created the first official Lowe’s Home Improvement store in 1946 in North Caro-lina.1 The home improvement industry boomed after World War II. In 1949, Arthur Levitt and sons created the first modern sub-division in Long Island. War veterans pur-

chased the homes and since they all looked alike, the homeowners sought out hardware stores to buy items that would create indi-viduality. A U.S. census showed that home re-pair/improvement boomed from 1982 to 1992. Overall, Lowe’s dominated the industry until the 1980s.2 Due to the popularity of the industry, Bernie Marcus and Arthur Blank founded The Home Depot in 1978 . They opened their first store in Atlanta, Georgia in 1979. In 1980, The Home Depot introduced the first “Do It Yourself” workshop. This cre-ated a phenomenon within the home im-provement industry.

Now, the home improvement indus-try is one of the most thriving industries in The United States.3 The Home Depot and Lowe’s have even expanded their locations to Canada and in 2006 The Home Depot ac-quired a twelve store chain in China. The suc-cess of the home improvement industry is based largely on the boom that was gener-ated by WWII veterans and the first subdivi-sion that was created from the post-war ef-forts.2 Ever since this boom, The Home De-pot and Lowe’s have been the two main play-ers that comprise the Home Improvement Industry.

H i s t o r y

1921

North Wilkesboro-Hardware Store

opened

1946

First Lowe’s Home Im-provement Store opened in

North Carolina

1949

First Subdivision cre-ated by Arthur Levitt

1978

Home Depot was founded

1979

First Home Depot opened in GA

1980

Home Depot offered first Do-It-Yourself

program

1961

Lowe’s went public on NASDAQ

1981

Home Depot went public on NASDAQ

2006

Home Depot acquired stores in China

2007

Lowe’s opened first store in

Canada

Ind

ustry

Ove

rvie

wIn

du

stry

Ove

rvie

w

Figure : 1

Source: HomeDepot.com

5

A s shown in Graph 1, the sales in the home improvement industry are steadily increasing. Since

2000, its revenues increased from $176 bil-lion to $306 billion in 2007.4 The Home Depot is the largest home retail center con-trolling 42-46% of the market. The primary competitor for The Home Depot is Lowe’s because it sells the same products as The Home Depot and also appeals to the same target market. Lowe’s controls the second

largest portion of the market with 27-30%.5 One secondary competitor for The Home Depot is Wal-Mart because it offers a variety of home improvement products such as: paint, tools, and hardware for a low price. Sears is also a secondary com-petitor because it offers tools along with appliances and electronics that could be purchased at The Home Depot. The Home Depot spent

more than $1.1 million on adver-tising in 2005 and 2006. Spending less than The Home Depot, Lowe’s invested $778 thousand in adver-tising in 2005 and $838 thousand in 2006. When combined, these two companies make up almost 80% of the home improvement retail mar-ket. Graph 2 reveals the overall trend of advertis-

ing expenditures among the home improve-ment industry.6

Advertising Spending

0

200

400

600

800

1,000

1,200

2006 2005Year

Ad

ve

rtis

ein

g d

oll

ars

sp

en

t (t

ho

usa

nd

s)

Graph: 2 Source: Leading National Advertisers

Graph: 1 Source: NHRA

I n d u s t r y S i z e

Total Retail Sales by Home Improvement Retailers

0

50

100

150

200

250

300

350

2000 2001 2002 2003 2004 2005 2006 2007

Year

Sa

les

(in

bil

lio

ns)

Ind

ustr

y O

ve

rvie

wIn

du

str

y O

ve

rvie

w

“Longer terms, trends underlying the home

improvement industry remain favorable for

continued sales and market share growth.”

-Arthur Blank 9

6

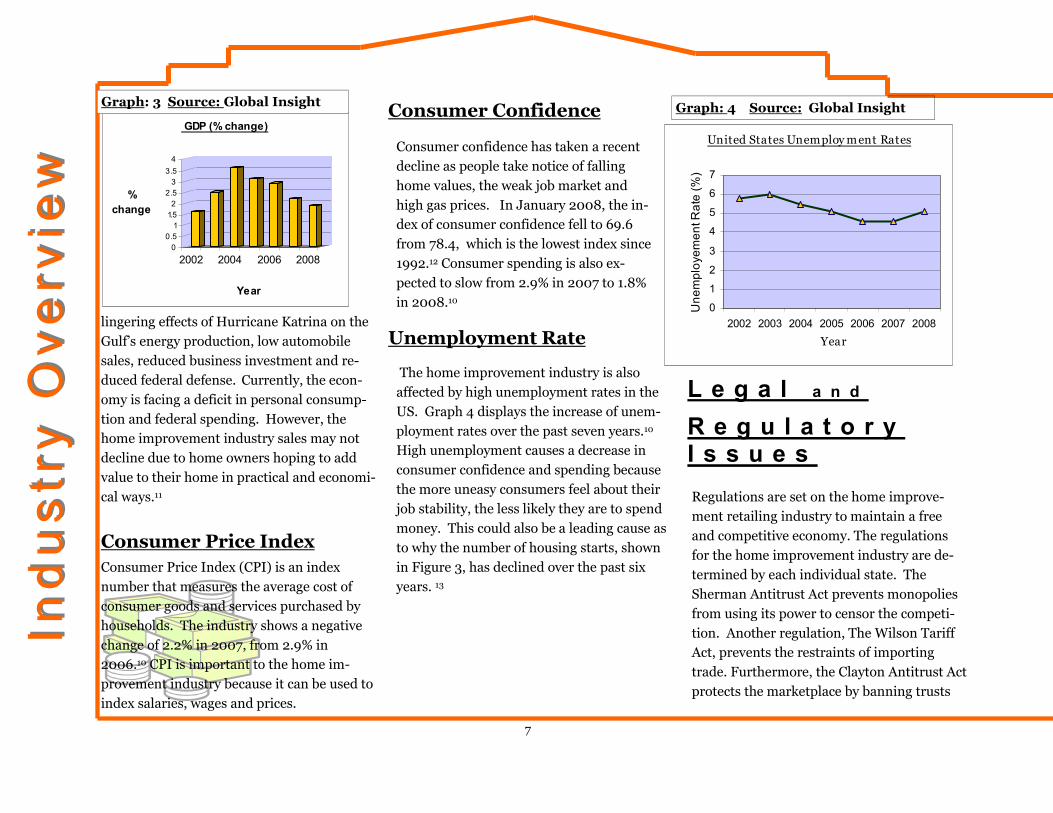

According to the North American Retail Hardware Association’s annual report, the home improvement industry is mature.4 At this mature stage, the industry is well established , sales volumes have peaked, costs are very low, competition is increasing, and stores strive to differ from the competition with the products offered. It still shows a positive growth as demonstrated by retail sales, fea-tured in Graph 1.

According to Figure 2, quarterly income statements from the larg-est market shareholders in the industry, The Home Depot and Lowe’s, show the most money is spent on home improvement dur-ing the second and third quarters. Statements report that during the second quarter, The Home Depot was most profitable and earned $21,585 million in profit. It was the least profitable in the fourth quarter with sales of $18,961 million. Lowe’s was most prof-itable in the third quarter with sales of $14,166 million while its lowest sales, $10,405 million, occurred in the first quarter.7

The growth potential for the home improvement industry is neu-tral. The housing market has been on a decline for nearly two years and is not predicted to show any improvement through 2008. Al-though the housing market is low, there is still hope for the home improvement industry due to the fact that home ownership has re-

mained healthy. Since ownership has remained positive and home-owners view their homes as investments and therefore spend more on improvement than renters do, this should continue to drive market growth. According to market research firm Global Insight, the total home improvement products market in the U.S. was esti-mated to have declined to $308.9 billion in 2007, from $312.9 bil-lion in 2006. However, it is projected to advance to $394.1 billion by 2012, a 5.0% compound annual growth rate. 8

Graph 3 shows that the real domestic growth product (GDP) de-creased 2.9% in 2006 to 2.2% in 2007, which leads economists to believe that the GDP will fall another 1.9% in 2008.10 Some of the factors that may account for the decline in GDP could be: the ever

S e a s o n a l i t y

S t a g e i n P r o d u c t L i f e C y c l e In

du

stry

Ove

rvie

wIn

du

stry

Ove

rvie

w

Quarter Lowe’s The Home Depot

1. Ending Jan 07 Quarter

$10,405 $20,265

2. Ending Apr 07 Quarter

$12,172 $21,585

3. Ending Jul 07 Quarter

$14,166 $19,144

4. Ending Oct 07 Quarter

$11,566 $18,961

Quarterly Income Statements: Home Depot and Lowe’s (millions)

G r o w t h & P o t e n t i a l F o r e c a s t

Figure: 2 Source: hoovers.com

T h e E c o n o m y GDP Decline

7

lingering effects of Hurricane Katrina on the Gulf’s energy production, low automobile sales, reduced business investment and re-duced federal defense. Currently, the econ-omy is facing a deficit in personal consump-tion and federal spending. However, the home improvement industry sales may not decline due to home owners hoping to add value to their home in practical and economi-cal ways.11

Consumer Price Index (CPI) is an index number that measures the average cost of consumer goods and services purchased by households. The industry shows a negative change of 2.2% in 2007, from 2.9% in 2006.10 CPI is important to the home im-provement industry because it can be used to index salaries, wages and prices.

Consumer confidence has taken a recent decline as people take notice of falling home values, the weak job market and high gas prices. In January 2008, the in-dex of consumer confidence fell to 69.6 from 78.4, which is the lowest index since 1992.12 Consumer spending is also ex-pected to slow from 2.9% in 2007 to 1.8% in 2008.10

The home improvement industry is also affected by high unemployment rates in the US. Graph 4 displays the increase of unem-ployment rates over the past seven years.10 High unemployment causes a decrease in consumer confidence and spending because the more uneasy consumers feel about their job stability, the less likely they are to spend money. This could also be a leading cause as to why the number of housing starts, shown in Figure 3, has declined over the past six years. 13

Regulations are set on the home improve-ment retailing industry to maintain a free and competitive economy. The regulations for the home improvement industry are de-termined by each individual state. The Sherman Antitrust Act prevents monopolies from using its power to censor the competi-tion. Another regulation, The Wilson Tariff Act, prevents the restraints of importing trade. Furthermore, the Clayton Antitrust Act protects the marketplace by banning trusts

00.5

11.52

2.53

3.5

4

% change

2002 2004 2006 2008

Year

GDP (% change)

Consumer Price Index

Unemployment Rate

Ind

ustr

y O

ve

rvie

wIn

du

str

y O

ve

rvie

w

L e g a l a n d

R e g u l a t o r y I s s u e s

Consumer Confidence United States Unemploy m ent Rates

0

1

2

3

4

5

6

7

2002 2003 2004 2005 2006 2007 2008

Year

Une

mpl

oyem

ent R

ate

(%)

Graph: 3 Source: Global Insight Graph: 4 Source: Global Insight

8

board of directors, fixed prices, etc. to con-trol the supply and price of products to gain a monopoly. These regulations are put in place to ensure that the general public is provided with the best prices, quality and to maintain competition between busi-nesses.14 Since the highest complaint in the industry among consumers is home im-provement fraud, The Federal Trade Com-mission, the National Association of Home Builders Remodelors™ Council and the National Association of Consumer Agency Administrators have created a kit called “Home Improvement: Tools You Can Use,” which lists several tips for hiring a contrac-tor and avoiding home improvement fraud.15

The main factor in how consumers make their home improvement purchasing deci-sions is based on their level of income and the allocated budget for home improve-ment products and projects. The larger the budget, the more choices consumers have regarding the durability and finish of the products they choose. Therefore, the amount of money that consumers have to spend on their purchases not only increases demand for improvement products but will also affect the range of products offered.11

The main two customers in the industry are:

• Do-It –Yourself

• Do-It-For-Me

These are social considerations for the in-dustry to remember in order to provide the best customer service and products. 16

The Do-It-Yourself Market (DIY) is a large customer group in the home improvement industry where consumers purchases sup-plies and complete their own projects. This is a driving trend for the industry that ac-counts for approximately 40% of the total market. To increase spending among DIY consumers, home improvement retailers have started to provide in store customer assistance and websites specifically for DIY projects.16

Housing Market (number of housing starts in thousands of units per year)

2002 2003 2004 2005 2006 2007

2 ,20 0

1 ,9 00

1 ,70 0

1 ,50 0

1 ,300

1 ,100

Ind

ustry

Ove

rvie

wIn

du

stry

Ove

rvie

w

Figure: 3

Source: Standard and Poors

S o c i e t a l & C u l t u r a l i s -s u e s

Do-It-Yourself

9

T he Do-It-For-Me

Market (DIFM) is

a large home im-

provement industry group in

which consumers purchase

supplies and hire a third-

party to complete the project

for them. This market is pre-

dicted to increase with the

retirement of many baby boomers, which

should lead to continuous home improvement

spending.16

A s America’s baby boomer popula-

tion gets older, they are increas-

ing their spending. Baby boomers

are responsible for more than half of all

home improvement expenditures, today.

They are expected to increase their spend-

ing on home improvement projects after

their kids have moved out. Within the home

improvement industry, they are expected to

influence the do-it-for me service category.

Additionally, this popula-

tion is likely to drive an

increase in existing home

sales as many of them ei-

ther look to downsize or

acquire a second vacation

or retirement home. These

scenarios should have a positive im-

pact on the home improvement in-

dustry.11

O ver the last few years, buying

environment ally friendly prod-

ucts for the home has become an

increasingly important consideration for

homeowners looking to make "green" im-

provements to their living space. Consum-

ers feel the need to add environmentally

friendly, “green,” products and practices to

their homes in order to make it healthier

and more comfortable. The industry’s main

stores, The Home Depot and

Lowe’s, have added “green” prod-

ucts such as flooring, lighting, pan-

eling, materials such as paint and

varnish, appliances, heating and

cooling systems, and electronics.

As the

world adjusts to

“going green,”

the Home Im-

provement In-

dustry is adjust-

ing to provide

environmen-

tally friendly products and options for the

consumer. 20, 27

S o c i e t a l & C u l t u r a l i s s u e s

Ind

us

try

Ov

erv

iew

Ind

us

try

Ov

erv

iew

Baby Boomers Green Movement

Do-It-For Me

10

H i s t o r y

Clie

nt P

rofile

Clie

nt P

rofile

1990: Surpassed Lowe’s as top home

improvement industry seller

1978: Corporation founded by Marcus

and Banks

1980: First how-to product training seminars began

2000: Launched

online store

1986: Had 56 operating stores and reached $1 billion in sales

2005: Launched “Rebuilding Hope

and Homes” for Katrina victims

2006: Extended stores to China

Figure: 4 Source: HomeDepot.com 1984: Had 19 operating stores and

sales of $256 million

1981: Company went public on

NASDAQ

H ome Depot was founded on June 22, 1978 in Atlanta Georgia. It was started by two entre-

preneurs, pictured in Figure 5, Bernie Marcus and Ar-thur Blank. Marcus and Blank found them-selves without jobs after the change in management at the Handy Dan home center chain. Marcus and Blank decided to open their own home improvement store. From the begin-ning, the employees at Home Depot recog-nized the importance of customer service.

The em-ployees had vast knowledge of all their prod-

ucts and even offered “how to” clinics to consumers.

By 1984, the company was operating 19 stores and reported

sales of $256 million, a 118% increase from 1983. In

1986, The Home Depot’s sales reached the $1 billion mark, and the com-pany was operating 50 retail outlets. Home Depot surpassed Lowe’s in sales in 1989 to

become the largest home-repair chain in the US.17

“Bernie and I picked our-selves up, and we mapped

out Home Depot on a napkin in our favorite coffee shop.”

-Arthur Blank 18

Figure: 5

Source: referenceforbusiness.com

11

The revenues for The Home Depot are rising slowly but steadily. From 2002 to 2007, the sales have increased from $55 million a year to more than $90 million a year. As shown by Graph 5, sales beginning to level off is an indication that The Home Depot is in the mature stage of the product life cycle.19

The ad expenditures for The Home Depot have increased from $1,109 million in 2005 to $1,118 million in 2006, shown in Graph 2, page 4. Although The Home Depot has a solid consumer base, advertising is important so it doesn’t lose sales to the competitors. The increase in money spent on advertising corresponds to the increase in the revenues for The Home Depot. 6

Figure 6 indicates that television dominated the media allocation for The Home Depot in 2006. Outdoor advertising held the lowest part of the media allocation. The Home Depot shows its advertisements on

television to reach the largest number of its target audience.6

The share of voice shows where the advertising dollars are best being spent. The share of voice is the total percentage of advertising that The Home Depot possesses within the home improvement industry. Figure 8 shows that in 2005 The Home Depot held 71% of the market share, then dropped down to 57% in 2006. 6

The Home Depot reports that one key to its success is treating people well. The company executes this important principle within the com-pany by urging associates to be creative, express their ideas, take risks, acknowledging and rewarding good performances, and teaching its em-ployees in order to grow. Most importantly, the company wants custom-ers to feel as if they are number one when they enter any of The

Share of Voice

Positioning

Media Allocation

The Home Depot - 2006 Media Allocation (Percentage)

7%

21%

50%

21%

0%

1%

Magazines

Newspapers

Television

Radio

Outdoor

Internet

Sales C

lie

nt

Pro

file

Cli

en

t P

rofi

le Graph: 5 Source: Standard and Poor’s

Figure: 6 Source: Ad Age

Revenues for the Fiscal Year Ending January

020,00040,00060,00080,000

100,000

2002 2003 2004 2005 2006 2007

Year

Sales (in millions )

Advertising Expenditures

12

C

lien

t Pro

fileC

lien

t Pro

file

Home Depot stores. The Home Depot strives to provide excellent cus-tomer service by providing customers with information that will maxi-mize all of the benefits of products purchased. Its eight core values are giving back, excellent customer service, creating shareholder value, en-trepreneurial spirit, taking care of their people, respect for all people, doing the right thing, and building strong relationships.21

The Home Depot announced in April 2007 that it would offer more environmentally friendly products. There were more than 2,500 prod-ucts included in this announcement ranging from front-loading wash-ing machines to water efficient toilets, to programmable thermostats. The Home Depot’s slogan for Eco Options is “Improve your Home. And the Environment.”22

Since females will most likely remodel, The Home Depot has targeted them by making the interior of its store softer, adding more kitchen lay-outs, and an assortment of appliances.33

Much of The Home Depot’s advertising is about showing the feeling of satisfaction homeowners get from home improvement. The ad to the right shows a young woman being convinced that it is possible for her to retile her floors, despite her doubting hus-band. The Home Depot’s ads show the power of the brand and how associates can help regular people accomplish great things in their home.

There are several links available on the company’s homepage that offer addi-

tional advice and services aimed at the dif-ferent target audiences that shop at The Home Depot. It offers a link that is tar-geted at DIY consumers. This link has online workshops that the DIY consumer

can view from the privacy of their own home. There is also a link, shown to the left, providing information, maps, and pictures of the philanthropic work that The Home Depots has been doing with Habitat for Humanity in the rebuilding of homes after Hurri-cane Katrina. The Home Depot also has a com-plete website, shown above, dedicated to the NASCAR sponsorship it has with Tony Stewart’s

number 20 racing team.

Recently, for the Home Depot, there has been a Public Relations offen-sive to help protect the environment. This campaign is aimed at all con-sumers to become actively interested in environmental issues and sup-port environmental causes. The need for this Public Relations cam-paign is due to the world population expanding and the depletion of natural resources.20

Creative Strategy

New Developments

Share of Voice

Year Brand To-tal

Maga-zine

News-paper

TV Ra-dio

Out-door

Inter-net

‘06 57% 51% 54% 51%

70% 77% 27%

43% 49% 46% 49%

30% 23% 73%

‘05 71% 70% 53% 53%

67% 53% 23%

29% 30% 67% 67%

53% 67% 77%

Figure: 8 Source:Leading National Advertisers

13

Lowe’s is the primary competitor for the

Home Depot because they are the closest

competitor in terms of net sales, share of

voice, number of stores in the United States.

Lowe’s Home Improvement stores began with

Lucious S. Lowe. He opened North Wilkes-

boro Hardware Store in North Carolina in

1921. in 1946, Lowe and his sons expanded

the business and opened the first Lowe’s.

Lowe’s held the number one spot in the Home

Improvement Industry until 1978 , and they

are now second to The Home Depot. They

have over 1,500 operating stores within the

US. 1

Since 2002, Lowe’s has consistently increased

its amount of sales every year. Graph 7 shows

the exact amounts of increase from 2002 to

2006. 23

Lowe’s allocates the majority of its advertising

expenditures on the medium of television.

The second largest advertising expense is

newspapers. Internet is the only medium on

which Lowe’s spends more advertising dollars

compared to Home Depot.6

Lowe’s advertising expenditures are less than

The Home Depot. In 2006, Lowe’s increased

their advertising expense to $835.thousand,

but The Home Depot still spent $279.6 thou-

sand more. Graph 8 gives a visual representa-

tion of the numbers above.6

Lowe’s promotes a warm, family friendly im-

age and gives a feeling of connection through

their slogan, “Lets build something together.”

Lowe’s is invested in the well being of the

communities they service. Lowe’s Charitable

and Educational Foundation recently an-

nounced their donation of $500,000 to the

YMCA in Toronto.24 Their contributions fo-

cus on education, community renovation, and

the construction of safe and affordable hous-

ing. To ensure the satisfaction of customers,

Lowe’s web page provides information on in-

stallation, credit options, and protection

plans. 25

• December 10, 2007: Opened first three

stores in Canada. Three more to open by

first of February 2008.

•Earned Environmental Excellence Award

from the EPA’s SmartWay Transport Part-

nership through their attempts to lower

green house gas emissions by decreasing car-

bon dioxide emissions on the highway.26,27

Co

mp

eti

tor

Co

mp

eti

tor

An

aly

sis

An

aly

sis

Lowe's Net Sales 2002-2006

0

10

20

30

40

50

2002

2003

2004

2005

2006

Year

Amount of Net Sales

(billions)

Net Sales

% Change

Sales

Media Allocation

History

Advertising Expenditures

Advertising Expenditures

0.00200.00400.00600.00800.00

1,000.001,200.00

2005 2006

Year of Expenditure

Amount of Money

spent (thousand)

The HomeDepotLow e's

Creative Strategy

Positioning

New Developments

Graph: 7 Source: Shareholder.com

Graph: 8 Source: Ad Advantage

14

T he Home Depot and Lowe’s are the major companies that comprise the Home Improvement Industry. Fig-

ure 9 demonstrate the differences between the two companies. As depicted in the table, Home Depot has more weekly visits from customers, larger sales, more stores, stores in more countries, more employees, and is ranked higher in the FORTUNE 500 List than Lowe’s.

Co

mp

ara

tive

An

aly

sis

Co

mp

ara

tive

An

aly

sis

Figure 9 Source: The Home Depot, Lowe’s. Hoovers.com The Home Depot Lowe’s

Photo

Year Founded 1978 1946

Number of weekly visits

22+ million 14 million

Slogan You can do it. We can help.

Let’s Build Something Together

2006 Sales $90.8 billion $46.9 billion

2006 number of stores

2,074 1,385

Stores outside of US

Canada, Puerto Rico, US Virgin Islands,

Mexico, China

Canada

Number of prod-ucts available

40,000 in store 40,000 in store

Number of employ-ees

364,000 215,000

Number of stores opening in 2008

55 120

FORTUNE® 500 List

Ranked #17 Ranked #45

DIY Workshops Of-fered

Yes Yes

15

We have identified Sears and WalMart as

secondary competitors because they each

pose a threat to Home Depot’s sales by tar-

geting a similar market and having similar

services or products.

Sears, Roebuck and Co. is the leader of the

U.S home appliance market. It is also a leader

in retail sales for tools, lawn and garden

equipment, and home electronics. Sears’

stores carry top names like Kenmore, Crafts-

man, and Die Hard; brands that can not be

found at other retailers.28 Known for its ex-

tensive service and repair plans, Sears pro-

vides the country with the largest product

repair service. Sears rivals Home Depot for

sales based upon their vast appliance selec-

tion, top brand names, home service and re-

pairs. Although Sears’ product selection ex-

tends beyond home appliances, their com-

mitment to service, protection, and installa-

tion services place them in the arena of home

improvement retail and therefore make them

an indirect competitor of The Home Depot.29

WalMart grossed $348,650 million this past

year.30 WalMart is competition for The

Home Depot because they provide hardware

tools and home appliances amongst their

broad selection of products. With an empha-

sis on customer service, WalMart offers

paint, gardening supplies, and tools at a low

price. Known as one of the original “super-

centers,” consumers view WalMart as their

one stop shop for groceries, beauty supplies,

electronics, and hardware materials.31 The

convenience of finding everything in one lo-

cation is attracting busy consumers more and

more. As a result of the totality of WalMart

shopping centers, Home Improvement cen-

ters like The Home Depot might be less ap-

pealing to consumers in need of small home

repairs or tool purchases.

Simmons Market Research Bureau (SMRB) is

a syndicated research company that gathers

and displays information from many differ-

ent sources to assist companies in how to bet-

ter understand its target consumers. This

information for The Home Depot has been

categorized into different demographics,

psychographics and geographics. With these

facts, the SMRB has divided the sample into

DIY consumers versus DIFM consumers, ex-

penditures on home improvement and re-

modeling in the past versus remodeling in the

future. The samples represent those 21 and

older.

Men and women are most likely to spend

$251-$999 on home improvements. As age

increases, the money spent on home im-

provement also increases. Caucasians and

African Americans are most likely to spend

$251-$999 on home improvements. As to be

expected, as the household income increases

so does the likelihood of people spending

more money on home improvements.

Secondary Competitors

Consumer Analysis

Total Expenditures

16

Females (106) are above average and held

52% of the sample to have remodeled in the

past 12 months. More than average males

(104) held 51% of the sample in planning to

remodel in the next 12 months, furthermore

men have more influence in the purchase of

remodeling products at 55%.32 Ages 35-44

are most likely to have completed a project

in the last 12 months with 27% and 31% are

also most likely to remodel in the next 12

months. Caucasians, held 86% of the sam-

ple, are most likely to have remodeled in the

past and 85% plan to remodel in the future;

while all other races have below average

index numbers to complete any project.

People who attended college for less than 1-

3 years held 30% of the sample to have re-

modeled in the past 12 months and held

31% in planning to remodel in the future.

People with and income of $150,000-

$249,000 had the highest percentage for

planning to remodel, making them most

likely to remodel. Overall, the Midwest is

the most likely to have completed projects

in the past or to complete projects in the

future.35

Females (109), people ages 45-65 (140 and

132), college graduates, and the Northeast-

ern region (124) are most likely to be DIFM

customers. Males (103), people ages 25-44

(126 and 130), those who attended college

for less than 1-3 years, and the Midwestern

region (above 100) are most likely to be DIY

customers. Households with an income

$60,000-$99,999 are most likely to be DIY

customers. Consequently, households with

incomes above $250,000 are most likely to

be DIFM customers.36

According to the interpretation of the Sim-

mon’s Market Research Bureau, The Home

Depot should focus on white females, ages

35-54, with an income above $60, 000 from

the Midwest region. With this target mar-

ket, the Census Bureau predicts that The

Home Depot will market to a white popula-

tion of 239,746,254, a female population of

151,886,332, an age population of roughly

84,082,929 (the ages used were 25-44 in

order to estimate this population), and a

regional population of 66,388,795.

DIY vs. DIFM

Target Market

Home Remodeling: Last 12 months vs. Plan in the next 12 months

17

T o gain further information about females’ attitudes and beliefs about The Home Depot, our group designed and conducted a survey. The ultimate goal of the this survey was to discover information on the following research objectives:

• To assess the target market's attitudes/beliefs about home improvement retailers.

• To assess the target market's attitudes/beliefs about The Home Depot.

• To assess the target market’s attitudes/beliefs about Lowe’s in comparison to The Home Depot.

• To measure the target market's The Home Depot usage.

• To identify if there are age, gender, income, etc. variable differences for the above categories.

Qu

an

tita

tiv

e R

es

ea

rch

Qu

an

tita

tiv

e R

es

ea

rch

Research Objectives

W e went to different retail locations where we handed out our survey for respondents to com-plete. The sample for the survey was all adults 21

years and older who had completed a home improvement pro-ject in the last 12 months, who were currently involved in a home improvement project or planned to complete a home improvement project within the next 12 months. The sample size for the survey was 97. The data collection method is shown to the right in Figure 10. With our chosen survey method, self-administered intercept, we reduced bias by not going online or using a telephone method . Therefore, non-respondent error was reduced because self administered inter-cept is more personal and evoked better participation. Also, we clearly identified ourselves as students to reduce auspices bias. Overall, the only bias that could have resulted from our survey would have been interviewer bias because ultimately our presence could have influenced some respondents.

Name Location How survey con-ducted

# of surveys completed Methods

Sam Sears Self-administered intercept

15

Rebecca Target Self-administered intercept

15

Camille Lowe’s Self-administered intercept

15

Natalie T. WalMart Self-administered intercept

15

Mary Carlie Home Depot Self-administered intercept

15

Natalie W. Bed, Bath and Beyond

Self-administered intercept

15

Proposed Design Survey

T he method that we used was self administered intercept. Figure 11, to the right on page 17, shows which questions in our survey answered certain research objectives. Our proposed survey con-sisted of 28 variables.

Figure 10

18

Efforts to Reduce Survey Design Bias

I n order to assure the most accurate information possible, we took the following precautions in de-signing our survey.

1. We did not assume that the respondents partici-pated in home improvement projects because we asked screening questions at the beginning to verify that they were 21 or older and met the criteria to give their opin-ions on the home improvement industry. We also screened by asking if those who participated in the sur-vey had experience with The Home Depot.

2. To made sure not to combine two questions, we eliminated the word “and” in order to prevent confu-sion.

3. We kept questions short and the survey brief to maintain the respondent’s attention.

4. We used clear, understandable language.

5. Demographic and sensitive questions were kept until the end, with the exception of screening questions, to ensure greater coopera-tion throughout the survey.

6. We placed demographic questions at the end, along with fairly broad choice options to ensure more accurate responses to personal questions, such as age and income.

7. Filter questions were used to save the respondent from confusion and eliminate irrelevant questions.

8. We did not use leading questions that suggested any answer as right or wrong.

9. We provided extensive instructions on how to complete the survey to enhance accurate data collection.

10. We provided mutually exclusive/non over-lapping ranges to reduce confusion.

11. We grouped like scales to simplify the survey.

12. We provided all possible response choices by using the tried and true Likert scale with five available options and provided blanks labeled “other” when necessary .

Research Objective Survey Question Number(s)

To measure the target market’s current, past (last 12 months) or future (next 12 months) home improve-ment projects or plans.

2

To assess the target market’s attitudes/beliefs about home improvement retailers.

3, 4, 17

To assess the target market’s attitudes/beliefs about The Home Depot.

7, 8, 11

To assess the target market’s attitudes/beliefs about Lowe’s in comparison to your client.

12, 13, 14, 15, 16

To measure the target market’s The Home Depot us-age.

5, 6, 9, 10

To identify if there are age, gender, income, etc. vari-able differences for the above measures.

1, 18, 19, 20

Figure 11

Qu

an

titativ

e R

es

ea

rch

Qu

an

titativ

e R

es

ea

rch

19

Q

ua

nti

tati

ve

Re

se

arc

hQ

ua

nti

tati

ve

Re

se

arc

h

Results and Discussion

The majority of respondents (81%) (79/97) either agreed (47%) (46/97) or strongly agreed (34%) (33/97) that home improve-ment retailers provide them with the mate-rials needed to complete home improve-ment projects. However, there were no re-spondents that disagreed with this state-ment and 19% (18/97) remained neutral in their response.

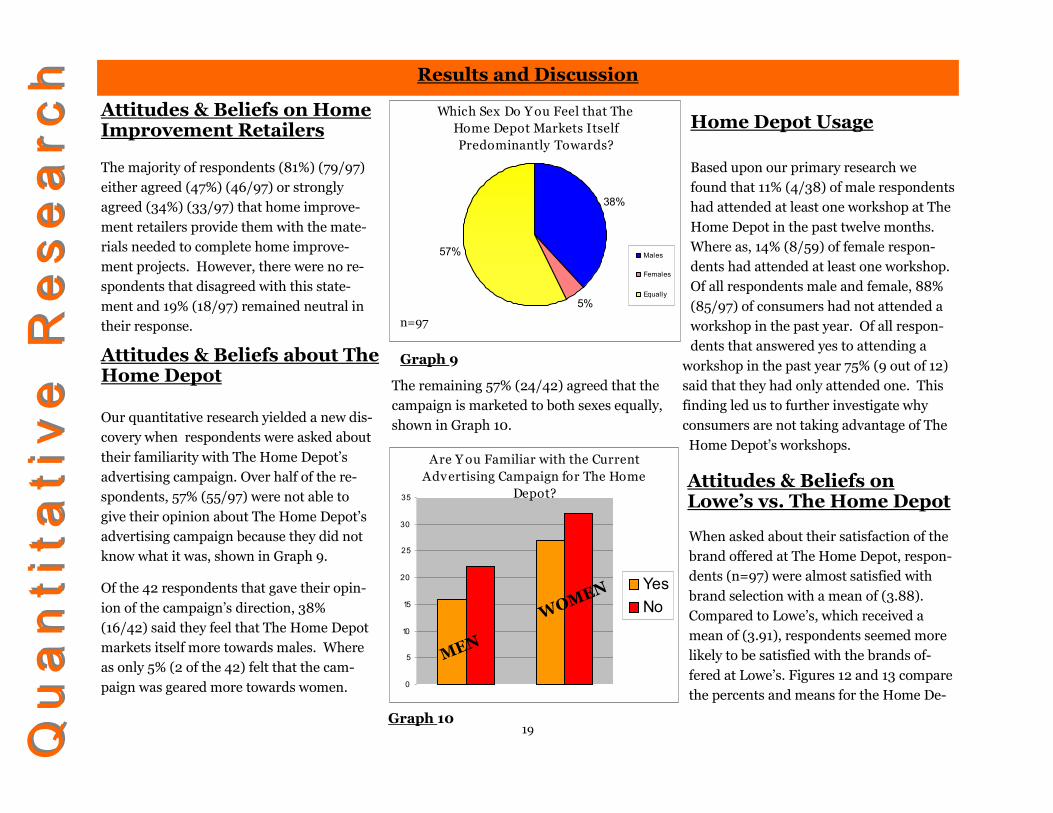

Our quantitative research yielded a new dis-covery when respondents were asked about their familiarity with The Home Depot’s advertising campaign. Over half of the re-spondents, 57% (55/97) were not able to give their opinion about The Home Depot’s advertising campaign because they did not know what it was, shown in Graph 9.

Of the 42 respondents that gave their opin-ion of the campaign’s direction, 38% (16/42) said they feel that The Home Depot markets itself more towards males. Where as only 5% (2 of the 42) felt that the cam-paign was geared more towards women.

The remaining 57% (24/42) agreed that the campaign is marketed to both sexes equally, shown in Graph 10.

Based upon our primary research we found that 11% (4/38) of male respondents had attended at least one workshop at The Home Depot in the past twelve months. Where as, 14% (8/59) of female respon-dents had attended at least one workshop. Of all respondents male and female, 88% (85/97) of consumers had not attended a workshop in the past year. Of all respon-dents that answered yes to attending a

workshop in the past year 75% (9 out of 12) said that they had only attended one. This finding led us to further investigate why consumers are not taking advantage of The Home Depot’s workshops.

When asked about their satisfaction of the brand offered at The Home Depot, respon-dents (n=97) were almost satisfied with brand selection with a mean of (3.88). Compared to Lowe’s, which received a mean of (3.91), respondents seemed more likely to be satisfied with the brands of-fered at Lowe’s. Figures 12 and 13 compare the percents and means for the Home De-

Attitudes & Beliefs on Home Improvement Retailers

Attitudes & Beliefs about The Home Depot

Home Depot Usage Which Sex Do Y ou Feel that The

Home Depot Markets Itself Predominantly Towards?

38%

5%

57% Males

Females

Equally

Are Y ou Familiar with the Current Advertising Campaign for The Home

Depot?

0

5

10

15

20

25

30

35

YesNo

MEN

WOMEN

Attitudes & Beliefs on Lowe’s vs. The Home Depot

Graph 9

Graph 10

n=97

20

Qu

an

titativ

e R

es

ea

rch

Qu

an

titativ

e R

es

ea

rch

Lowe’s. In terms of cleanliness and layout, The Home Depot once again received a slightly lower mean. On average, respon-dents said they were almost satisfied with the layout (mean of 3.82) and almost satis-fied with the cleanliness of The Home De-pot (3.81). Respondents on average were much closer to being satisfied with the lay-out of Lowe’s (3.97). However, Lowe’s scored a mean of (4.02) in store cleanliness, which was considerably higher than the mean for The Home Depot. These results showed us that on average consumers are less satisfied with the overall appearance and environment of The Home Depot.

There was a significant difference in gender and respondents that had visited a Lowe’s store. Significantly more females (12%) (7/59) than males (0%), had not visited a

Lowe’s home improvement center in the past twelve months (Chi Square= 4.859,d.f.1; Sig=.028).

Attribute 1 2 3 4 5 Mean

Convenience of location

0 11.1% 29% 33% 27% 3.76

Cleanliness of store

0 0% 22% 93% 7% 4.02

Customer ser-vice

0 4% 28% 50% 18% 3.81

Products of-fered

0 1% 24% 50% 24% 3.98

Brands offered 0 2% 28% 47% 23% 3.91

Pricing of products

0 8% 31% 50% 11% 3.64

Attributes 1 2 3 4 5 Mean

Convenience of location

3% 8% 20% 45% 24% 3.78

Cleanliness of store

1% 7% 22% 50% 21% 3.81

Customer ser-vice

0 8% 29% 41% 22% 3.76

Products of-fered

0 3% 19% 52% 27% 4.02

Brands offered 0 3% 25% 54% 19% 3.88

Pricing of products

0 7% 34% 49% 10% 3.62

Percent and Means for The Home Depot Percent and Means for Lowe’s

*On a scale from 1 to 5, 1 being Very Dissatisfied to 5 being Very Satisfied

Variable Differences

Significant Differences between Men and Women

Percentages

Measure Men Women Chi-Square Value

Significance

Respondents who have visited a Lowe’s store.

100% 88% 4.859 .028

Figure 12 Figure 13

21

C

on

su

me

r In

sig

hts

Co

ns

um

er

Ins

igh

ts Purpose

Methods

Figure 13

W e used structured personal interviews to gain further insight into consumer behavior. The reason we used the personal interview was be-

cause it is a private, face to face conversation. This gave us the opportunity to tailor questions to specific respondents. We felt that this was the best suited technique for our re-search because it allowed us to probe open-ended ques-tions that explored our objectives, and allowed the respon-dent to provide the interviewer with more personal and thorough answers.

We addressed our objectives through personal interviews that each group member conduct.ed, shown in Figure 13. Each group member personally interviewed a man or woman who met the general requirements to participate in our research. We located willing participants outside of a Knoxville location of The Home Depot. We asked those subjects who agreed to participate in our research pre-pared interview questions. The interviews were conducted on April 10, 2008.

T he purpose of using qualitative research was to collect and provide insights and explanations directly from the respondents, shown in Figure 14. Using qualitative research helped the researcher understand the data from quantitative research and gain a more in depth perspective of the consumer’s attitudes, motivations and feelings in their responses. The purpose of our qualitative

research was to gain insight into the following objectives:

• To determine why consumers did not take advantage of DIY workshops at The Home Depot.

• To determine why consumers were less than satisfied with the brands offered at The Home Depot.

• To determine why many consumers do not have knowledge of The Home Depot’s advertising campaigns.

• To determine why consumers were less satisfied with the cleanliness and layout of The Home Depot when compared to Lowe’s.

Name Location How interview conducted

# of interviews completed

Sam The Home Depot Self-administered intercept

1

Rebecca The Home Depot Self-administered intercept

1

Camille The Home Depot Self-administered intercept

1

Natalie T. The Home Depot Self-administered intercept

1

Mary Carlie The Home Depot Self-administered intercept

1

Natalie W. The Home Depot Self-administered intercept

1

22

C

on

su

me

r Ins

igh

tsC

on

su

me

r Ins

igh

ts

Survey Design

Methods used to Reduce Survey Design Bias

O verall, there were general limitations in our conducted qualitative research. Small sample size prevented population generalizations and interpretations of the

data were more subjective than quantitative data. This directly correlated to the personal interview technique because the inter-views were sensitive interviewer bias, problems with data analy-sis, and overall generalization. To overcome limitations, each group member was aware of possible interview bias and ques-tions were prepared and practiced extensively, prior to the inter-views. Group members were also aware that the data is subjec-tive and may not represent The Home Depot consumers as a whole. To avoid any incorrect generalizations, additional inter-views could have been conducted if it seemed that responses were skewed in any particular interviews.

To analyze the results we met as a group and compared each member’s findings. We took those findings and applied them to our previously stated objectives. Additionally, we went back to our quantitative research and compared it to our qualitative re-search and determined how representative of the population our respondents were.

Research Objectives Survey Question Number(s)

To determine why con-sumers did not take ad-vantage of DIY workshops at The Home Depot.

5, 6, 7

To determine why con-sumers were less than sat-isfied with the brands of-fered at The Home Depot.

18, 19, 20, 25

To determine why many consumers did not have knowledge of The Home Depot’s advertising cam-paigns.

13, 14, 15, 16, 17

To determine why con-sumers were less satisfied with the cleanliness and layout of The Home Depot when compared to Lowe’s.

8, 9, 10, 11, 21, 22, 23

Figure 14

23

C

on

su

me

r In

sig

hts

Co

ns

um

er

Ins

igh

ts

F rom our quantitative research we discovered 4 main themes to fur-ther examine in our qualitative

research. The themes identi-fied were: (1) To determine why consumers do not take advantage of DIY workshops at The Home Depot. (2) To determine why consumers are less than satisfied with the brands and products offered at The Home Depot. (3) To determine why many consumers have no knowledge of The Home Depot’s advertising cam-paign. (4) To determine why consumers are less than satisfied with the cleanliness and layout of The Home Depot. Direct quotes taken from personal interviews conducted are used to further elaborate and Figure 15 shows a profile of the re-spondents.

O ur respon-dents wanted

DIY workshops to be offered at different times of the day.

Many people are too busy to attend the workshops that are held on the weekends. “Workshops seem to only be offered on

Saturdays, when I am working on projects at home.” (Male, 56) This would allow a more diverse group of people to at-tend; such as parents who have children in school, people who work on the weekends, or peo-ple who cannot attend until

after work. Most respondents agree that television is the best way to reach them and that advertisements for DIY work-shops should be created to raise aware-ness and provide information to increase attendance.

A lthough our primary research suggested that respondents pre-ferred Lowe’s brands over those

of The Home Depot, our in-depth interviews revealed that those who frequent The Home De-pot are actually quite satisfied with the brand selections offered. One

respondent voiced this opinion by saying, “Home Depot was the only place that I was able to find a certain grout cleaner. It was so wonderful that I told all my friends about it!” (Female, 50)

Also when questioned about eco-friendly products and brands, respondents said that going green did affect their purchase choices and will continue to affect them in the future as they become more environ-mentally aware.

A ll respondents agreed that cleanliness was very important to them in terms of creating a

positive shopping experience. General cleanliness was mentioned as an issue; however the overwhelming consensus from our respondents was that The Home

DIY Workshops

“Workshops seem to only be of-

fered on Saturdays, when I am

working on projects at home.”

-Male, 56

Brand Offering

“I can’t recall a Home Depot ad off the top of my head, but I remember seeing that Lowe’s one with the bear during the championship basketball game.”

-Male, 36

Cleanliness and Layout

24

C

on

su

me

r Ins

igh

tsC

on

su

me

r Ins

igh

ts

Depot had a “warehouse” feel to it that negatively influenced the perception of how clean the store was. “The warehouse atmosphere appears cluttered and rugged, I wouldn’t say it is unclean, how-ever.” (Female, 50)

This quote showed that Lowe’s has a more effective advertising campaign that cre-ates top of the mind awareness with its consumers.

M uch like the survey respon-dents from our primary re-search, questionnaire partici-

pants were not aware of The Home De-pot’s advertising campaign. Question-naire responses varied, however, a com-mon theme was that The Home Depot’s

advertisements are simply not memora-ble. A 36 year old male said, “I can’t recall a Home Depot ad off the top of my head, but I remember seeing that Lowe’s one with the bear during the championship basketball game.”

Knowledge of The Home Depot’s Advertisement

“The warehouse atmosphere appears

cluttered and rugged, I wouldn’t say it

is unclean, however”.

-Female, 50

Personal Interview Respondents

Interviewer Respondent

Sam Dintsh Male, 36

Rebecca Harris Male, 56

Camille Harvey Female, 50

Natalie Townsend Female, 32

Mary Carlie Vaughn Male, 45

Natalie White Female, 38

25

M a r k e t i n g R e c o m m e n d a t i o n sM a r k e t i n g R e c o m m e n d a t i o n s

E ven though many of the interview-ees were not familiar with The Home Depot’s advertising cam-

paign, the respondents that were familiar with the campaign stated that the advertise-ments were targeted specifically towards males. Therefore, The Home Depot needs to

develop more female friendly advertise-ments to gain a larger female consumer population. The cam-paign should show the advantages that Home Depot offers for fe-males and be shown

through female dominated media. This me-dia would include print ads in Women's Day and First, television ads on Oxygen, con-tinuing sponsoring shows on TLC and Life-time, and on the internet.

A finding within our research shows the overwhelming lack of partici-pation in the Do-It-Yourself work-

shops. Hardly any males or females had ever participated in the workshops that The Home Depot offers. Home Depot boasts the slogan of "You Can Do It, We Can Help," therefore, their DIY workshops should be in popular demand and utilized by more consumers. Therefore, an overall change needs to be made beginning with new activities that are gender specific. This could be achieved by splitting the month up and organizing female activities (for example: gardening tips, simple home re-pairs, crafting, projects and workshops for kids ) on two weekends and the other two weekends for male activities (for example: building tips, plumbing tips, lawn care and home repairs). These DIY workshops should also be better advertised through local radio, newspa-pers., and television.

A s our quantitative findings show, many of the respondents had con-cerns about the layout and cleanli-

ness of The Home Depot. The survey con-cluded that overall Lowe's had a better lay-out and was thought to be a cleaner store . Therefore, small adjustment s should be made to the store layout in order to provide

customers with a more efficient and easier way to find prod-ucts . Also, cleanliness seems like a store specific characteris-tic, every store in every location should uphold the Home Depot name and image. Therefore, each store should be held ac-countable for maintaining a respectable and clean store ap-pearance. A simple statement

to store managers readdressing the cleanli-ness and encouraging the standards of a Home Depot store should help address the cleanliness issue.

t o T h e H o m e D e p o tt o T h e H o m e D e p o t Create A New Female Focused Advertising Campaign

Create New DIY Workshop Activities

Re-vamp Store and Maintain Clean Store Environment

26

A huge problem for one of our per-sonal interviewees was that The Home Depot did not stand behind

their products. One respondent went into further detail about not being able to attain a broken part for a kitchen faucet and do to the lack of employee help and product avail-ability she had to buy a completely new fau-

cet, which cost her more than she planned on spending. Therefore, The Home Depot needs to stand behind the brands they offer, have extra parts to fix and maintain these products and develop proper customer ser-vice relations in order to make customers happy in any situation.

A ccording to our personal inter-views , not many customers are familiar with the eco-friendly

products and brands offered by The Home Depot but do share interests in “Going Green.” Since, the "Go Green" Movement is gaining momentum across the United States being a part of this movement would gain credibility among those who are switching over to a more "green" lifestyle. Also, offering these products and brands is one way to stand out from the other home improvement competitors, mainly Lowe's. Therefore, The Home Depot should address the topic of global warming and products offered to "Go Green". One way to launch this specific idea would be to have a highly publicized Earth Day Sale, putting eco-friendly products on clearance and con-tinue their Arbor day sales in order to pro-mote more planting.

Overall, The Home Depot should focus on better advertisement distribution to make the general public more aware of their cor-poration. On top of a female focused cam-paign, The Home Depot’s general campaign should reach a larger audience and the ad-vertisements should be more memorable to its audience.

Develop Better Customer Relations

Focus on More Eco-friendly Products and Advertisements

Create More Memorable Advertisements to a Larger Audience

27

A

ppen

dix

1: S

urve

yA

ppen

dix

1: S

urve

y

Hom

e Im

prov

emen

t Ind

ustry

Opi

nion

Sur

vey

This survey is being conducted by an advertising research class at the University of Ten-

nessee. Your participation will help us to better understand the attitudes and opinions of

consumers in the home improvement industry.

Please read the following questions and respond by circling the corresponding answer as

it pertains to you.

Are

you

21

or o

lder

?

Yes

N

o

Hav

e yo

u co

mpl

eted

a h

ome

impr

ovem

ent p

roje

ct in

Y

es

No

the

past

12

mon

ths,

are

you

cur

rent

ly in

volv

ed in

a h

ome

impr

ovem

ent p

roje

ct, o

r do

you

pla

n on

sta

rtin

g a

hom

e

impr

ovem

ent p

roje

ct in

the

next

12

mon

ths?

If y

ou

an

swer

ed “

No

” to

on

e o

r b

oth

of

the

abo

ve q

ues

tio

ns,

th

is c

on

clu

des

yo

ur

elig

ibil

ity

for

com

ple

tin

g th

is s

urv

ey.

Th

ank

yo

u f

or

you

r ti

me

and

par

tici

pat

ion

. If

you

an

swer

ed

“Yes

” to

bo

th o

f th

ese

qu

esti

on

s, p

leas

e m

ove

fo

rwar

d t

o q

ues

tio

n 1

an

d c

om

ple

te t

he

sur-

vey.

On

a s

cale

of

1-5

wit

h 1

bei

ng

stro

ngl

y d

isag

ree

and

5 b

ein

g st

ron

gly

agre

e,

p

leas

e n

ote

yo

ur

per

son

al o

pin

ion

s to

war

ds

the

foll

ow

ing

stat

emen

ts.

1.

Hom

e im

prov

emen

t ret

aile

rs in

gen

eral

pro

vide

nec

essa

ry m

ater

ials

to c

ompl

ete

hom

e im

prov

emen

t pro

-je

cts.

Str

ongl

y D

isag

ree

1 2

3 4

5 St

rong

ly A

gree

2.

The

dec

line

in th

e ec

onom

y ha

s af

fect

ed y

our

hom

e im

prov

emen

t pur

chas

ing

b

ehav

ior.

Stro

ngly

Dis

agre

e 1

2 3

4 5

Stro

ngly

Agr

ee

3.

Hav

e yo

u ev

er v

isit

ed a

Hom

e D

epot

sto

re?

Y

es

N

o

If y

es, c

on

tin

ue

to q

ues

tio

n 4

If

no

, sk

ip t

o q

ues

tio

n 1

2.

28

.4.

How

man

y ti

mes

in th

e pa

st tw

elve

mon

th h

ave

you

visi

ted

The

Hom

e D

epot

?

(P

leas

e ch

eck

on

e b

ox

on

ly)

0

1-3

4-6

7-10

1

1 or

mor

e

5.

Bas

ed o

n a

sati

sfac

tion

sca

le o

f 1-5

, 1 b

eing

ver

y un

sati

sfie

d an

d 5

bein

g ve

ry s

atis

fied

, how

wou

ld y

ou r

ate

Th

e H

om

e D

epo

t in

the

follo

win

g ca

tego

ries

bas

ed u

pon

your

per

sona

l exp

erie

nce?

Ver

y U

nsat

isfi

ed

V

ery

Sati

sfie

d

Con

veni

ence

of L

ocat

ion

1

2

3

4

5

Cle

anlin

ess

of S

tore

1

2

3

4

5

Cus

tom

er S

ervi

ce

1

2

3

4

5

Pro

duct

Off

erin

g

1

2

3

4

5

Bra

nd O

ffer

ing

1

2

3

4

5

Pri

cing

of P

rodu

cts

1

2

3

4

5

6.

The

layo

ut o

f a H

ome

Dep

ot s

tore

allo

ws

me

to e

asily

find

the

prod

ucts

I n

eed.

Stro

ngly

Dis

agre

e 1

2 3

4 5

Stro

ngly

Agr

ee

7.

Hav

e yo

u ev

er a

tten

ded

a w

orks

hop

at T

he H

ome

Dep

ot?

Yes

No

If y

ou

an

swer

ed “

Yes

” to

qu

esti

on

7 p

leas

e m

ove

on

to

qu

esti

on

8. I

f yo

u a

nsw

ered

“N

o”

ple

ase

skip

to

qu

esti

on

9.

8. H

ow m

any

wor

ksho

ps h

ave

you

atte

nded

at T

he H

ome

Dep

ot?

(P

leas

e ch

eck

on

e b

ox

on

ly)

0

1

2

3

4 o

r m

ore

9. O

n a

scal

e of

1 to

10

, wit

h 10

bei

ng th

e hi

ghes

t, h

ow w

ould

you

rat

e yo

ur o

vera

ll ex

peri

ence

wit

h T

he H

ome

Dep

ot?

(Ple

ase

circ

le c

orr

esp

on

din

g n

um

ber

)

1

2

3

4

5

6

7

8

9

1

0

10.

Hav

e yo

u ev

er v

isit

ed a

Low

e’s

stor

e?

Y

es

N

o

If

you

an

swer

ed “

Yes

,” c

on

tin

ue

to q

ues

tio

n 1

1. I

f “N

o,”

sk

ip t

o q

ues

tio

n 1

5.

11.

How

man

y ti

mes

in th

e pa

st tw

elve

mon

th h

ave

you

visi

ted

Low

e’s?

0 1

-3

4

-6

7

-10

11

or m

ore

29

A

ppen

dix

1: S

urve

yA

ppen

dix

1: S

urve

y

12.

Onc

e ag

ain,

bas

ed o

n a

sati

sfac

tion

sca

le o

f 1-5

wit

h 1

bein

g ve

ry u

nsat

isfi

ed a

nd 5

bei

ng v

ery

sati

sfie

d, h

ow

wou

ld y

ou r

ate

the

follo

win

g as

pect

s of

Lo

we’

s?

Ver

y U

nsat

isfi

ed

V

ery

Sati

sfie

d

Con

veni

ence

of L

ocat

ion

1

2

3

4

5

Cle

anlin

ess

of S

tore

1

2

3

4

5

Cus

tom

er S

ervi

ce

1

2

3

4

5

Pro

duct

Off

erin

g

1

2

3

4

5

Bra

nd O

ffer

ing

1

2

3

4

5

Pri

cing

of P

rodu

cts

1

2

3

4

5

13.

The

layo

ut o

f Low

e’s

allo

ws

me

to e

asily

find

the

prod

ucts

I n

eed.

St

rong

ly D

isag

ree

1 2

3 4

5 St

rong

ly A

gree

14.

On

a sc

ale

of 1

to 1

0, w

ith

10 b

eing

the

high

est,

how

wou

ld y

ou r

ate

your

ov

eral

l exp

erie

nce

wit

h Lo

we’

s?

(Ple

ase

circ

le c

orr

esp

on

din

g n

um

ber

)

1

2

3

4

5

6

7

8

9

10

15.

If y

ou w

ere

to c

hoos

e on

e of

the

follo

win

g re

taile

rs to

mee

t you

r ho

me

impr

ovem

ent n

eeds

inst

ead

of T

he

Hom

e D

epot

whi

ch w

ould

it b

e? (

If o

ther

, ple

ase

pro

vid

e th

e re

tail

er)

W

alm

art

L

owe’

s

S

ears

Oth

er_

__

__

__

__

__

16.

Are

you

fam

iliar

wit

h th

e cu

rren

t adv

erti

sing

cam

paig

n fo

r T

he H

ome

Dep

ot?

□

Yes

□N

o

If y

ou

an

swer

ed y

es t

o t

he

abo

ve q

ues

tio

n, p

leas

e co

nti

nu

e to

on

to

qu

esti

on

17.

If

you

an

-sw

ered

no

to

qu

esti

on

16

, ple

ase

skip

to

qu

esti

on

18

.

17.

Do

you

feel

that

The

Hom

e D

epot

mar

kets

itse

lf m

ore

tow

ards

:

□ M

ales

□ F

emal

es

□ B

oth

sexe

s fa

irly

the

sam

e

Ple

ase

read

all

th

e an

swer

ch

oic

e fo

r q

ues

tio

n 1

8 b

efo

re a

nsw

erin

g, t

hen

ch

eck

th

e co

rre-

spo

nd

ing

bo

x, i

f o

ther

, ple

ase

exp

lain

.

30

18.

Whi

ch o

f the

follo

win

g be

st d

escr

ibes

you

r liv

ing

situ

atio

n?

□ I o

wn

my

resi

den

cy.

□

I ren

t my

resi

den

cy.

19.

Ple

ase

circ

le y

our

gend

er.

M

ale

Fe

mal

e

20.

Ple

ase

chec

k th

e bo

x co

rres

pond

ing

to y

our

age

rang

e.

21-

34

35

-49

50

-64

65 o

r gr

eate

r

21.

Wha

t is

your

mar

ital

sta

tus?

□

Sing

le

□

Mar

ried

□D

ivor

ced

22.

Ple

ase

chec

k th

e re

gion

of t

he U

nite

d St

ates

that

bes

t rep

rese

nts

your

cu

rren

t res

iden

cy?

□ N

orth

east

□ S

outh

east

□ M

idw

est

□ S

outh

wes

t

□ W

est

□ I

do

not l

ive

in th

e U

nite

d St

ates

.

23.

Ple

ase

chec

k yo

ur a

nnua

l inc

ome

□ U

nder

$24

,999

□ $

25,0

00

-$49

,999

□ $

50,0

00

-$74

,999

□ $

75,0

00

-$99

,999

_ $

100

,00

0 o

r gr

eate

r

Tha

nk

you

for

com

plet

ing

this

sur

vey.

You

r in

form

atio

n w

ill b

e us

ed fo

r re

sear

ch p

urpo

ses

only

and

will

rem

ain

conf

iden

tial

.

31

Th

e H

om

e D

epo

t In

terv

iew

Gu

ide

Inte

rvie

wer

Nam

e _

__

__

__

__

__

__

__

__

__

__

__

__

__

__

__

__

__

__

__

__

__

__

__

__

Bac

kgro

und

Info

rmat

ion

on I

nter

view

ee:

Age

__

__

__

__

__

__

__

__

__

__

__

__

__

__

Rac

e/E

thni

city

__

__

__

__

__

__

__

__

__

__

__

__

Gen

der

__

__

__

__

__

__

__

__

__

__

__

__

_

L

ocat

ion

of I

nter

view

__

__

__

__

__

__

__

__

__

_

Th

ank

s ag

ain

fo

r ag

reei

ng

to p

arti

cip

ate

in t

his

per

son

al i

nte

rvie

w. W

e w

ill

star

t w

ith

so

me

bas

ic

qu

esti

on

s ab

ou

t yo

ur

Ho

me

Dep

ot

exp

erie

nce

.

1. W

hy d

id y

ou c

hoos

e to

vis

it T

he H

ome

Dep

ot to

day?

2. D

escr

ibe

wha

t a u

sual

trip

to T

he H

ome

Dep

ot w

ould

ent

ail.

3. A

bout

how

muc

h ti

me

wou

ld y

ou u

sual

ly s

pend

at a

Hom

e D

epot

loca

tion

?

4. H

ow m

any

tim

es h

ave

you

visi

ted

a H

ome

Dep

ot lo

cati

on w

ithi

n th

e pa

st m

onth

?

5. A

re y

ou a

war

e th

at T

he H

ome

Dep

ot o

ffer

s D

IY w

orks

hops

?

6. H

ave

you

ever

par

tici

pate

d in

a D

IY w

orks

hop

at T

he H

ome

Dep

ot?

If n

o, w

hy?

If y

es, d

id y

ou fi

nd it

hel

pful

?

Whe

ther

you

att

ende

d or

not

how

did

you

find

out

abo

ut D

IY w

orks

hops

?

7. W

hat w

ould

mot

ivat

e yo

u to

att

end

a D

IY w

orks

hop?

8.

How

eas

y is

it fo

r yo

u to

find

the

prod

ucts

you

cam

e to

look

for?

App

endi

x 2:

Qua

litat

ive

Gui

deA

ppen

dix

2: Q

ualit

ativ

e G

uide

32

9. H

ow o

ften

do

you

have

to a

sk fo

r he

lp fi

ndin

g a

prod

uct?

10.

How

fam

iliar

are

you

wit

h th

e la

yout

of T

he H

ome

Dep

ot?

11.

Wha

t do

you

like

abou

t the

layo

ut o

f The

Hom

e D

epot

?

12.

How

do

you

feel

abo

ut th

e si

ze o

f The

Hom

e D

epot

? (T

oo la

rge,

too

smal

l)

13.

Are

you

fam

iliar

wit

h T

he H

ome

Dep

ot’s

adv

erti

sing

cam

paig

n? I

f no,

why

not

?

14.

Wha

t’s th

e la

st H

ome

Dep

ot a

dver

tise

men

t you

saw

?

15.

Wha

t eff

ect d

id s

eein

g th

at a

dver

tise

men

t hav

e on

you

?

16.

Do

you

feel

like

The

Hom

e D

epot

’s a

dver

tisi

ng c

ampa

ign

is d

irec

ted

tow

ards

you

?

17.

Whi

ch m

edia

cha

nnel

wou

ld b

est r

each

you

for

The

Hom

e Im

prov

emen

t adv

erti

sem

ents

? (r

adio

, tel

evis

ion,

mag

azin

es, n

ewsp