HINDUSTAN INKS & RESINS LTD Silvassa project. Becomes only the third in the world to produce Alkali...

54

Analyst Meet - 23 January 04 HINDUSTAN INKS & RESINS LTD

Transcript of HINDUSTAN INKS & RESINS LTD Silvassa project. Becomes only the third in the world to produce Alkali...

Analyst Meet - 23 January 04

HINDUSTAN INKS & RESINS LTD

“ World Without Inks ”

“ World With Inks ”

1. Milestones & Highlights

2. Understanding Inks

3. Hindustan Inks – Making a Mark on the World

4. The Inks Market

5. Challenges

6. Financial Performance

7. People Behind Hindustan Inks

Analyst Meet-January 2004

Except for the historical information contained herein, statements in this presentation and the subsequent discussions, which include words or phrases such as

“will”, “aim”, “will likely result”, “would”, “believe”, “may”, “expect”, “will

continue”, “anticipate”, “estimate”, “intend”, “plan”, “contemplate”, “seek to”, “future”, “objective”, “goal”, “likely”, “project”, “should”, “potential”, “will

pursue” and similar expressions or variations of such expressions may constitute

"forward-looking statements“ not limited to expected future business and financial performance of HIRL. These forward-looking statements are based on Managements

current expectations and are inherently subject to uncertainties & changes in

circumstances and involve a number of risks, uncertainties and other factors that could cause actual results to differ materially from those suggested by the forward-

looking statements. These risks and uncertainties include, but are not limited to our

ability to successfully implement our strategy, our growth and expansion plans, our provisioning policies, technological changes, investment and business income, cash

flow projections, our exposure to market risks as well as other risks. Investors are

advised to form their own judgments and conclusions before any investment related decision. HIRL does not undertake any obligation to update forward-looking

statements to reflect actual results or any change in events, conditions, assumptions

or other factors.`

Disclaimer

Journey towards Excellence

Ink operations begin as small family unit.

Initial success in Inks Business.

HIRL becomes National Company.

Develops Pigments and Flush Technology.

Milestones…

1986

1992

1994

1996

1998

Initial capital employed Rs.200,000.

Starts a small Ag. Chem intermediate unit – Mitsu. Maiden IPO of Rs.20 Mio. Sales cross Rs.100 Mio.

Diversifies into General inks. Daman plant commences operation.Commences International Business in Ag.Chem.

Group sales cross Rs.1000 Mio, exports USD 5 Mio.

Implements SAP/R3.Launches Deltamethrin – 2nd in the World.Ink sales cross Rs.1000 Mio, group sales cross Rs.3000 Mio

Emerges as Market Leader in India.

Launches Micro inks. Recruits key people.

Micro inks gets initial success. Monthly sales cross $2 Mio.

Micro bags R R DONNELLY contract in the USA.

Micro inks becomes 12th biggest company in USA.

Milestones…1999

2000

2001

2002

2003

Mitsu emerges as biggest exporter of Agrochemicals.Mitsu profits exceed Rs.1000 Mio in a year.Sells 51% stake in Mitsu to HOECHST AGREVO for total $100 Mio.

Completes Silvassa project.

Becomes only the third in the world to produce Alkali Blue.

Commissions fully integrated single stream seamless plant – the biggest and only one of its kind in the World.

Further 23% stake of Bilag sold to AVENTIS for $50 Mio. Ink Exports cross Rs.2000 Mio.

HIRL emerges in the top 15 Global Ink cos.Successful entry in around 50+ Countries spread across all Continents.

Key HighlightsØ 15th Largest ink company in the World.

Ø Largest Ink co. in India , 12th Largest in USA.

Ø One of the fastest growing Ink cos. in the World.

Ø Among the fastest growing cos in India – CAGR of sales exceeds 45%

in 10 years.

Ø Biggest and only fully backward integrated , seamless ink

manufacturing plant in the World.Ø Only the third producer in the world in last 50 years to develop

Alkali Blue and the second largest in the world.

Ø Presence in more than 50 countries in all continents including a

manufacturing facility in USA.

Ø International business grown from $1 Mio. to $100 Mio. in 3years.

Ø International revenues exceed 50% of total revenues.

Understanding InksUnderstanding Inks

Printing Ink… A Primer

PRINTING INK …

Ø Is a performance chemical and requires total solution support.

Ø Is at the end of the chemical value chain.

Ø Has to perform on large variety and variation of substrates like plastic, paper, HDPE, metals, BOPP, polyesters, bonded paper, coated paper etc.

Ø Has to perform on various printing machines having different speeds and other characteristics.

Ø Requires adaptation to various climatic conditions.

Ø Has a long product life cycle.

Chemical Products/

Intermediates

Pigments ResinsSolvents

/ Oils Additives

VarnishesFlushes

PrinterPress/End Customer

Ink cost

< 5-7 % of

Printing

CostPacking Materials

BOPP, Polyesters, BondedPaper, Coated Paper

4B Acid, Bon Acid, Carbon Black, CPC, IPA, Soya Oil, Linseed Oil,

Aniline, Phenol, ONCB,

More than 500 Raw Materials

Value ChainNatural

ProductsRosins, Oil & Petrochemicals,

Sulphur, Salts, Copper, Linseed/Soya etc..

Key Characteristics

Though ink constitutes < 5-7 % of the cost for the printers

- The most visible part of the end product.

- No branding or differentiation is possible without ink.

- The cost driver, since it determines the press

performance, consumption of other materials like paper,

fountain solution, rollers etc.

Robust Ink

Dispersion Fast setting & reduced set off. Less wastage / costs

Transfer of ink related to speed of printing machineViscosity

Yield Value Structure of ink’s ability to withstand for long runs For high tech speed machine.

Stickiness of inkTack

Strength Tinting property of pigment

Print Density Color depth of ink film transferred on the substrate

Reflection from the printGloss

Set off Setting property of the ink

Rub Resistance Abrasion resistance of inks film

Setting property of the inkPress Stability

Flow Controlled & continuous flow of inks. Ink/water balance

Water up take Water intake of the ink.

PROPERTIES MEASURES

Ink Quality Drivers…

Critical Success Factors

Ø Continuous product development and design.

INKS is therefore a TOTAL SOLUTION BUSINESS to customers backed by high quality and real time service

Ø Accuracy & high quality.

Ø Reach and distribution.

Ø Real time- 24x7 - technical service & support.

Ø Productivity.

Ø Relationship driven.

Ø Cost.

Ø Long term research focus.

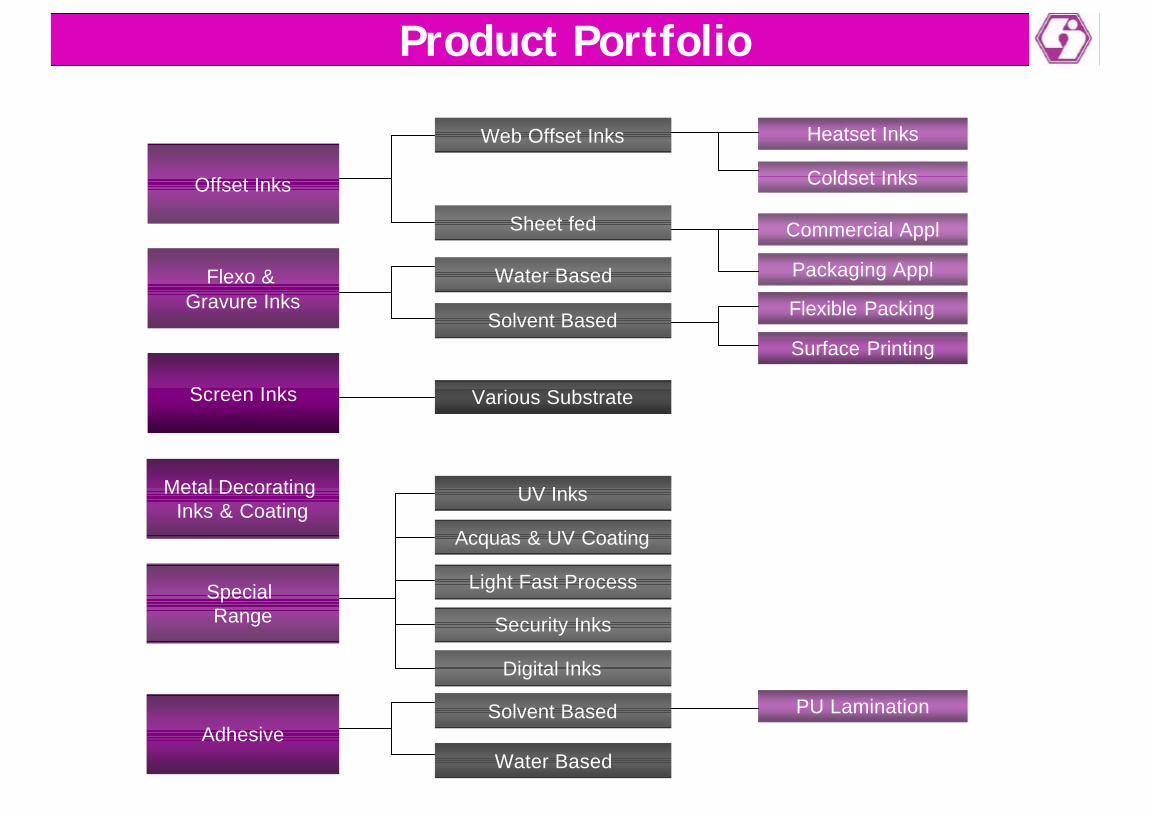

Offset Inks

Flexo & Gravure Inks

Screen Inks

Metal Decorating Inks & Coating

Special Range

Magazines & Books, News Papers, Yellow Pages,

Brochures, Calendars

Printing FMCG & Industrial Pkgon Substrates like Bottles,

Cans, Wrappers, LDP, BOPP& Flexible Pkg

Visiting Cards, Letter Heads, HDPE/PP bottles

Substrates like, Metal, AluminumFoils etc

Products & Applications

CD, DVD, Currency, Credit Card,Digital Printing, etc

Making our mark on the worldMaking our mark on the world

Offset Inks

Flexo & Gravure Inks

Adhesive

Screen Inks

Metal Decorating Inks & Coating

Special Range

Web Offset Inks

Sheet fed

Water Based

Solvent Based

Solvent Based

Water Based

Various Substrate

UV Inks

Acquas & UV Coating

Light Fast Process

Security Inks

Digital Inks

Coldset Inks

Heatset Inks

Commercial Appl

Packaging Appl

PU Lamination

Flexible Packing

Surface Printing

Product Portfolio

Quality drivers at Hindustan Inks

Ø Unique and unmatched technical expertise in Process Chemistry.

Ø Strong Research & Development with focus on new products and applications.

Ø In-house Design, Technology and Unique Process Flow.

Ø Full Vertical Integration and Seamless Process.

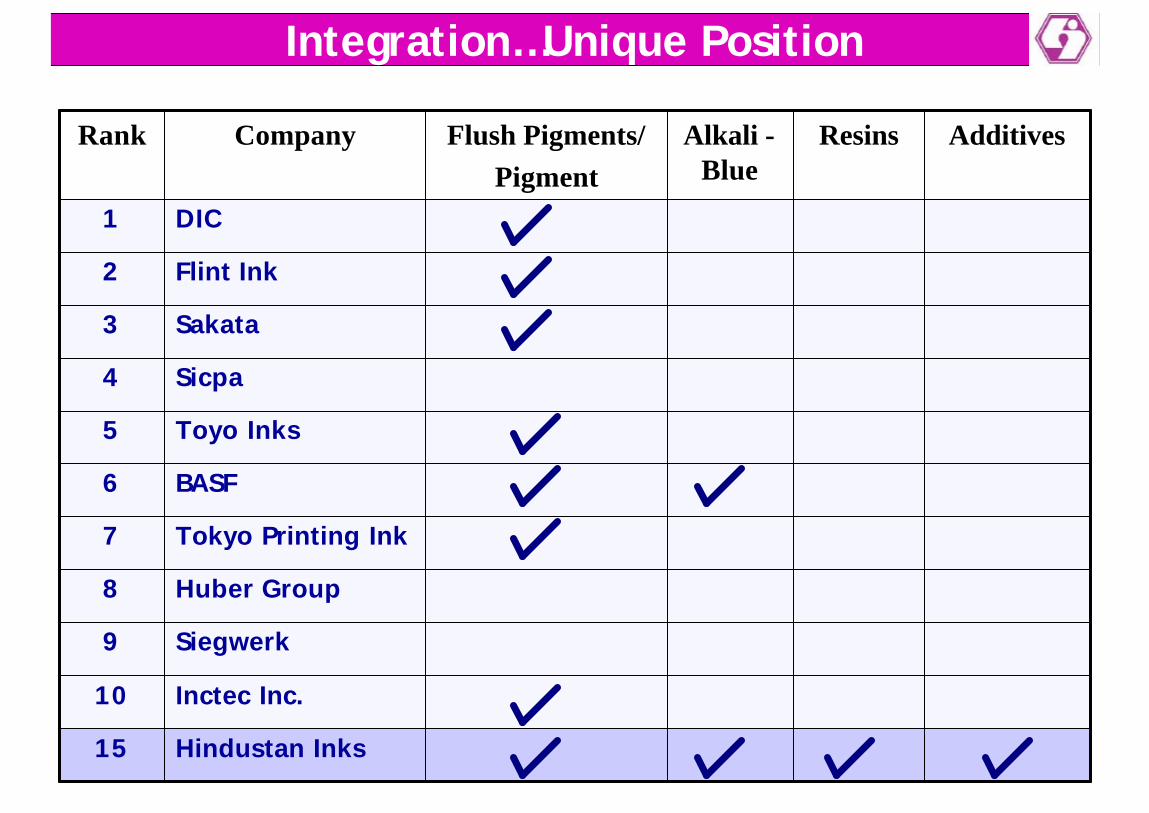

Integration…Key to Quality

Ø Hindustan inks has the only fully integrated plant in the world.

Ø Full control on all critical parameters ensures unmatched

product quality.

Ø High levels of customization possible thus satisfying varying

needs of clients.

Ø Enables rapid turnaround time for faster than normal customer

acquisition.

Ø Provides cost leadership.

Flush Pigments/Pigment

Alkali -Blue

Resins AdditivesCompanyRank

Hindustan Inks 15

Inctec Inc.10

Siegwerk9

Huber Group8

Tokyo Printing Ink7

BASF6

Toyo Inks5

Sicpa4

Sakata3

Flint Ink2

DIC1

Integration…Unique Position

Production Capacities

40000Pigments & Flushed Colors

3000Wire Enamels

Adhesives

Resins

Printing Inks

CLASS OF GOODS

7800

45000

180000

M.T. Per Annum

M.T. Per Annum

CLASS OF GOODS

65000 Finishing Plant for paste inks

U. S. A.INDIA

Ø Current capacity utilization is about 35% and capable of generating revenue in excess of USD 450 Million at full capacity.

Ø Consolidated fixed cost including interest, depreciation is about INR 1850 Million (FY 2003).

Ø Sales growth will lead to significant expansion in margin post the inflexion point.

Markets

Global Ink Market

28%

24%7%

35%

6%Asia

Europe

Latin America

North America

Others

Global Market – USD 15 bnNorth America- USD 5 bnIndian Market – USD 200 mn.

The Global MarketØ Growth at 2 – 3 % in last decade

Approx. Market Share (%)Sales US$ MillionsCompanyRank

1.5145Hindustan Inks 15

3341Inctec Inc.10

3344Siegwerk Druckfarben9

3383Huber Group8

3429Tokyo Printing Ink7

4617BASF6

4662Toyo Inks5

5685Sicpa4

5781Sakata3

111600Flint Ink2

263850DIC / SUN1

Source : Ink World Magazine

Ø Eight countries – US, JAPAN, GERMANY, UK, FRANCE, ITALY, SPAIN and CHINA account for 80% of global market.

Ø Top 10 companies control more than 65% of the global market.

Present Across 50 Countries In The World.

Our Presence across the Globe

India 43%

Africa & Middle East 2%

USA 38%

Asia Pacific 6%

Europe 9%

Latin America 2%

US Market

Ø Growing at 3 – 4% during the last decade.

Ø Volume declined in last two years; market leaders have witnessed

negative growth.

Ø Top 10 companies account for 75% of the market.

157MICRO INKS 12

2110Sicpa5

2125Color Converting4

5250INX International3

18900Flint Ink2

552750Sun Chemicals1

Apprx Market Share (%)

Sales US$ MnCompanyRank

Source : Ink World Magazine April 2003

Our Presence in USA

Micro Inks (Office & Mfg Facility)Ware HouseSales RepresentativesTSR

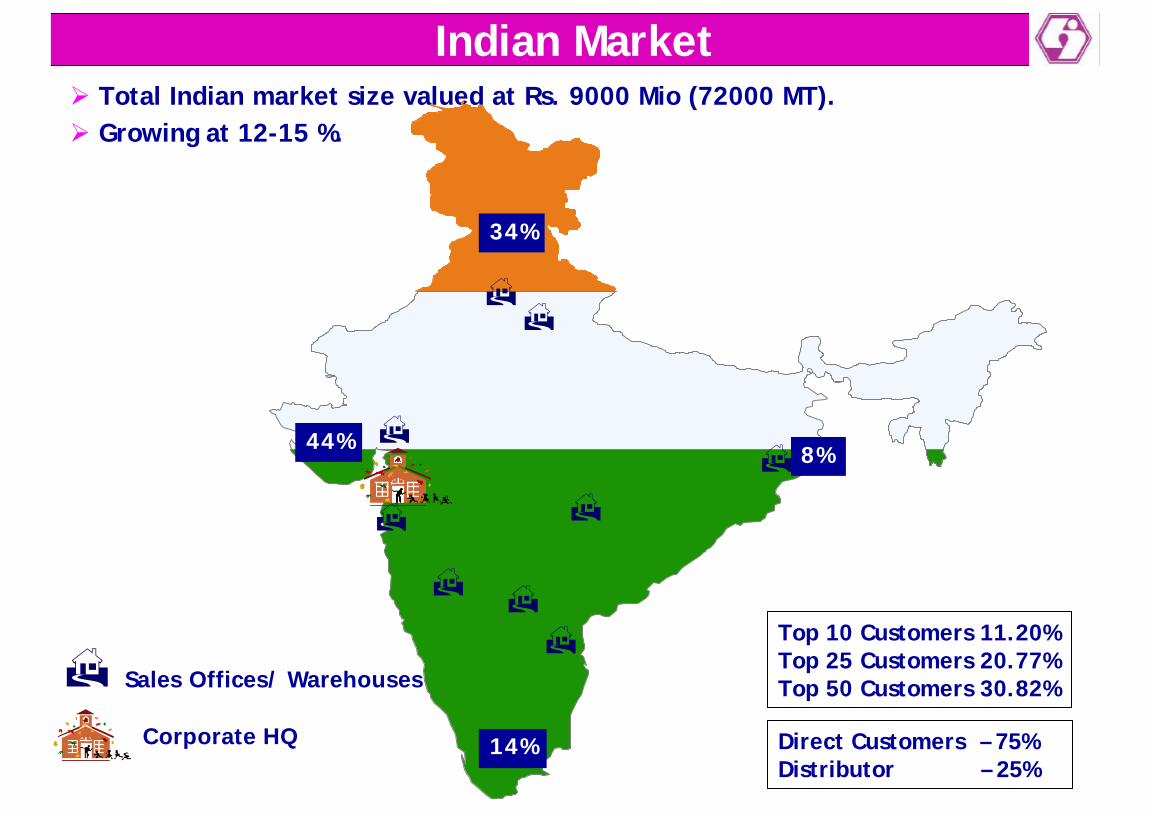

Indian MarketØ Total Indian market size valued at Rs. 9000 Mio (72000 MT).

Top 10 Customers 11.20%Top 25 Customers 20.77%Top 50 Customers 30.82%

Direct Customers – 75%Distributor – 25%

14%Corporate HQ

H Sales Offices/ Warehouses

HH

H H

H

H

HH

H

44%

34%

8%

Ø Growing at 12-15 %.

ChallengesChallenges

Image and Acceptability / Reach & Distribution- Initially less known in the international markets

- Over coming Customer Bias towards – India, Quality Issue, Distance issues etc.

- Service customers across the world.

+ Increasing corporate brand awareness

+ Tying up with local distributors and companies.

+ Private label sales/ OEM strategy

+ Create superior product performance.

Challenges

Increase people depth

- People strength and depth to service customers

+ CEO, marketing head and a marketing team of 40+ to service US. Further key

recruitments to increase penetration.

+ IBD team expanded from 2 to 12.

+ Continuous strengthening R&D and product chemistry related skills.

+ High focus on Training and HR.

Logistics

- Matching quality and delivery parameters of customers

+ Front-end model in US - to extend this model on a smaller scale to other countries.

+ Tying up with local companies and distributors.

+ Utilise information technology.

Market Related Risks :- Weakness in the US economy and new customer acquisition+ Revenues are diversified across geographies & customers. No concentration in

one market & going forward it will become more broad based.+ Developing superior product performance and providing value to customer.

Financial Risks :- Appreciation of Indian currency against dollar.+ Proactive Treasury Management.+ Started Billing in Euro to some Euro zone customers.+ Global sourcing of Raw Materials providing in natural hedge from exchange

fluctuation.+ Foreign currency loans to part finance long term requirement & export related

working capital.

Leverage :- Debt may go up in absence of sales growth due to economic slow down.+ Highly unlikely. However, Internal Generation & Long Term Fund raising shall

mitigate this risk.+ Tight control on Capital Employed.

Threats

Financial PerformanceFinancial Performance

Net Profit

Operating ProfitSales

POST INVESTMENT IN USA, COMPANY HAS ACHIEVED CONSOLIDATED PROFITS

410

162

331

663 709

0100200300400500600700800

99-0

0

00-0

1

01-0

2

02-0

3

03-0

4(9

Mth

s)

Rs.

Mio

201

(153)

(443)

(188)

118

-500-400-300-200-100

0100200300

Rs.

Mio

99-0

0

00-0

1

01-0

2

02-0

3

03-0

4(9

Mth

s)

Consolidated Financial Performance

0

1000

2000

3000

4000

5000

6000

700099

-00

00-0

1

01-0

2

02-0

3

03-0

4(9

Mon

ths)

Rs.

Mio CAGR – 53

% 6836

2194

3152

5181

6025

823887968485883887418741Capital Employed

559060356065601453375337Loan Funds

264827612420282434043404Networth

(153)15381140203373Cash Profit

(443)(188)(9)55115118PAT

(325)(76)2389181242PBT

71113131713(%)

331663208234339709EBIDTA

446561881626186519545477Sales (Net)

FY 2001-02

FY 2002-03

Q32002-03

Q22003-04

Q3 2003-04

9 months 2003-04

4 %2 %US

189 %1422 %PAT Growth

36 %64 %EBDITA Growth

21 %20 %Total Sales

135 %158 %Non-US

14 %10 %Domestic

Growth YTD (YoY)Growth Q3 (YoY)

Rs. MioConsolidated Key Financials

Sales

HIRL EBIDTA Trend

HIRL Profit Trend

HIRL Financial Performance

0500

1000150020002500300035004000450050005500600065007000

Rs.

Mio

92-93 94-95 96-97 98-99 00-01 02-03 03-04(9Mths)

101 4551039

1751

3843

6286

4256

CAGR – 51%

0

200

400

600

800

1000

1200

1400

Rs.

in M

io

92-93 94-95 96-97 98-99 00-01 02-03 03-04(9Mths)

9106

172324

1135

604

928

CAGR – 62%

050

Rs.

in M

io

100150

200

250300

350400450500

92-93 94-95 96-97 98-99 00-01 02-03 03-04(9Mths)

441

316

8475

5

235

458

CAGR – 57%

786885068597965396819681Capital Employed

380437224315457339533953Loan Funds

406447844282508057285728Networth

692681180225242632Cash Profit

483440116167182458PAT

601552147201248583PBT

232021222222(%)

11221135293307363928EBIDTA

492356391409142416344256Sales (Net)

FY 2001-02

FY 2002-03

Q32002-03

Q22003-04

Q3 2003-04

YTD Dec. 2003-04

44 %57 %PAT Growth

8 %24 %EBIDTA

10 %16 %Net Sales Growth

GROWTH YTD (YoY)Growth Q3 (YoY)

Rs. Mio

HIRL Financials

98

2

92

35

58

4

38

45

11

44

43

18

39

0%10%20%30%40%50%60%70%80%90%

100%

99-00 00-01 01-02 02-03 03-04(9Mths)

Domestic Non-USA USA

Consolidated Revenue by Geography%

Sha

re o

f R

even

ue

1206

19551865

13931518

1626 16521657

1000

1250

1500

1750

2000

Q4(01-0

2)

Q1(02-0

3)

Q2(02-0

3)

Q3(02-0

3)

Q4(02-0

3)

Q1(03-0

4)

Q2(03-0

4)

Q3(03-0

4)

Sale

s

Consolidated Revenue - Quarter wise

Rs Mio

Quarterly Net Sales

0

2

4

6

8

10

12

14

16

18

( USD

Mio

)

0

100

200

300

400

500

600

700

800

900 (R

s M

io)

050

100150

200250300

350400450

(Rs

Mio

)

Domestic Sales US Sales

Non - US SalesQ4

(01-0

2)

Q1(02

-03)

Q2(02

-03)

Q3(02

-03)

Q4(02

-03)

Q1(03

-04)

Q2(03

-04)

Q3(03

-04)

Q4(01

-02)

Q1(02

-03)

Q2(02

-03)

Q3(02

-03)

Q4(02

-03)

Q1(03

-04)

Q2(03

-04)

Q3(03

-04)

Q4(01

-02)

Q1(02

-03)

Q2(02

-03)

Q3(02

-03)

Q4(02

-03)

Q1(03

-04)

Q2(03

-04)

Q3(03

-04)

Quarterly Consolidated EBIDTA % Trend

4

10 1113

9 8

13

17

0

5

10

15

20

25

Q4(

01-0

2)

Q1(

02-0

3)

Q2(

02-0

3)

Q3(

02-0

3)

Q4(

02-0

3)

Q1(

03-0

4)

Q2(

03-0

4)

Q3(

03-0

4)

EB

IDT

A %

Quarterly PAT Trend

(191)

(78)(46)

(9)

(55) (52)

55

115

-200

-150

-100

-50

0

50

100

150(R

s M

io)

Q4(01

-02)

Q1(02

-03)

Q2(02

-03)

Q3(02

-03)

Q4(02

-03)

Q1(03

-04)

Q2(03

-04)

Q3(03

-04)

Sales Vs Capital Employed

820077508238

8796

4465

6188

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

10000

2001-02 2002-03 Est(2003-04)

(Rs.

Mio

)

Capital Employed Sales

“Reach Top 5 in the world within next 5 years.”

Vision & Strategy

ü Increase presence significantly across geographies.ü Become the fastest growing and most profitable

company in the world in printing inks.ü Differentiate products and quality.ü Build image and increase reach and distribution.

ü Use acquisitions/JVs to fuel growth.ü Focus on R&D ,Technology and Product Development.

- New Technologies

- Colorants

- Digital Inks.

Other Inks

Packaging

200420042004News Color/Black

UV/EB Inks/Coatings

Sheetfed Inks

20042004Heat Set Inks

OthersEuropeLatin America

North America

AsiaIndia

Product Universe

Promoters & ManagementPromoters & Management

Mr. ZAKIR BILAKHIAMember of the Executive Board.Drives Research, Technology and Product Strategy

MR. ANJUM BILAKHIAManaging Director Member of the Board of Bilag.Drives Execution, Projects and Operations.

MR. YUNUS BILAKHIAChairman & Founder. Chairman of Bilag- a JV with Bayer, Bilakhia HoldingsDrives Vision and Strategy for the Group.

ABOUT THE PROMOTERS…

MR. YUNUS BILAKHIA, MR. YUNUS BILAKHIA,

CHAIRMAN

MR. ANJUM BILAKHIA, MR. ANJUM BILAKHIA,

MANAGING DIRECTOR.

MR. SHIVRAM ANGNE, MR. SHIVRAM ANGNE,

WHOLETIME DIRECTOR

MR.PRASHANT DESAI MR.PRASHANT DESAI

INTERNATIONAL BUSINESS STRATEGIST

MR. M.L.BHAKTA MR. M.L.BHAKTA

SR. PARTNER OF KANGA & CO.- SOLICITORS

MR. K.K.UNNI MR. K.K.UNNI

EX-VICE CHAIRMAN OF AVENTIS CROPSCIENCE, INDIA

MR. HASMUKH SHAH MR. HASMUKH SHAH

CHAIRMAN OF GUJARAT GAS LTD

EX CHAIRMAN OF IPCL

EX-VICE CHAIRMAN OF GE CAPITAL, INDIA

EX-JOINT SECRETARY TO THE PRIME MINISTER

MR. ANJUM BILAKHIA,MR. ANJUM BILAKHIA,

MANAGING DIRECTORMANAGING DIRECTOR

MR. ZAKIR BILAKHIA, MR. ZAKIR BILAKHIA,

DIRECTOR DIRECTOR –– RESEARCH, TECHNOLOGY & RESEARCH, TECHNOLOGY & PRODUCT STRATEGYPRODUCT STRATEGY

MR. SHIVRAM ANGNE, MR. SHIVRAM ANGNE,

DIRECTOR – QUALITY, SYSTEMS & HR.

MR. SANJAY SHAH, MR. SANJAY SHAH,

DIRECTOR DIRECTOR –– OPERATIONS & SUPPLY OPERATIONS & SUPPLY CHAINCHAIN

MR. RAMAKRISHNA KAMAT, MR. RAMAKRISHNA KAMAT,

DIRECTOR DIRECTOR -- DOMESTIC SALESDOMESTIC SALES

MR. VINAY PANDYA, MR. VINAY PANDYA,

DIRECTOR DIRECTOR –– FINANCE, CORPORATE COMMFINANCE, CORPORATE COMM

MR. SNEHAL SHAH, MR. SNEHAL SHAH,

DIRECTOR DIRECTOR –– INTERNATIONAL BUSINESS INTERNATIONAL BUSINESS DEVLOPMENTDEVLOPMENT

MR. ZAINUL LAKDAWALA, MR. ZAINUL LAKDAWALA,

DIRECTOR DIRECTOR -- TECH SERVICE & R & D (USA)TECH SERVICE & R & D (USA)

Board Of Directors Executive Board

Bilakhia Holdings Pvt. Ltd.USD 239 MIL

Hindustan Inks & Resins LtdUSD 146 MIL

Mitsu Ltd USD 10 MIL

Bilag Industries Ltd JV-Bayer Bilakhias

USD 83 MIL

BILAKHIA GROUP

BHPL holds 26% in Bilag presently.

BILAG TODAY IS….

v Largest generic pyrethroid player in the world.v Global market share exceeding 25% on active ingredient basis.v Manufacturer & largest exporter of agrochemicals.v Most profitable unlisted company in India (Source ET – “15/07/2002 “).v international revenues contribute > 80% to sales.v Present in more than 70 countries including market leadership in china.

v Bilakhias entered AG.Chem business under the name Mitsu.

BILAG

v Progressed from simple one step process to complex Chiral chemistry.

v Specialised in Pyrethroid chemistry and setup global scale mega plants with cost leadership and full vertical integration.

v Moved up the value chain from $1 per Kg product to $400 per Kg.

v Introduced two new products every year.

v Recipient of national R&D and safety awards for several years.

v Entered into a JV with Agrevo (is now Bayer) to form Bilag

v One of the most successful JVs of India.