HIH Case Study on Asset Risk - iaisweb.org · HIH Case Study on Asset Risk ... plex project) and...

43

HIH Case Study on Asset Risk Round 3 5 November 2000 A Core Curriculum for Insurance Supervisors

Transcript of HIH Case Study on Asset Risk - iaisweb.org · HIH Case Study on Asset Risk ... plex project) and...

�

HIH Case Studyon Asset Risk

Round 35 November 2000

A Core Curriculum for Insurance Supervisors

Copyright © 2006 International Association of Insurance Supervisors (IAIS).All rights reserved.

The material in this module is copyrighted. It may be used for training by competent organiza-tions with permission. Please contact the IAIS to seek permission.

Author Jeffrey Carmichael is chief executive officer of Promontory Australasia. Until recently a full-time consultant, he was previously chairman of the Australian Prudential Regulation Au-thority. His career also includes senior positions with the Reserve Bank of Australia, seven years as professor of finance at Bond University, and appointment to a number of government and private sector boards and inquiries, including the Wallis Inquiry into the Australian financial system. He has published in a number of the world’s top economics and finance journals, in-cluding the American Economic Review and Journal of Finance.

�

HIH Case Study on Asset Risk(Round 3)

Attached is a memorandum containing an updated comprehensive assessment of the HIH group prepared by your second in command, who has taken over responsibility for HIH from the desk officer.

Your task for this round is to:

• Assess the information provided• Determine what further actions and requests should be taken at this time with

respect to HIH • Assess the case for taking enforcement action against the company• Review, and revise if necessary, your action plan for going forward.

Insurance Superv�s�on Core Curr�culum

2

MEMORANDUM FOR GENERAL MANAGERHIH INSURANCE LIMITED

5 November 2000

Matters with respect to HIH have begun to move rapidly. Ray Williams’ resignation as CEO on 13 October was an important step towards improving governance within HIH. However, the expeditious appointment of a suitable replacement will be critical.

I have been concerned that HIH’s responses have been excessively slow, notwith-standing repeated follow-ups from our desk officer, and notwithstanding Williams’ departure. The media campaign also continues to be negative and HIH’s share price continues to drift downwards. While this may be due to factors other than asset quality and valuations, this remains an area of concern.

Given my suspicion that HIH had been sidestepping us, I have taken over carriage of HIH from the desk officer and have conducted a comprehensive review of all the information we have available at this time. On balance, while HIH is still a high-risk company, there are some positive signs.

I have organized a meeting for us with the desk officer for HIH for tomorrow morning to discuss what, if any, action should be taken at this stage and to update our action plan for supervisory review of asset risk in HIH. You may wish to invite other members of the senior management team if you think the issues are sufficiently pressing.

Attached for your reference are:

• Attachment 1 – Another letter from HIH responding to some of the issues raised after the Asset Risk visit in July.

• Attachment 2 – My review of what we know about HIH at this stage.• Attachment 3 - An update on the terms of the Convertible and Converting Note

Issues.• Attachment 4 – An update on the impact on future income tax benefits.• Attachment 5 – A progress report on the valuation of investments.• Attachment 6 – An update on the impact of goodwill.• Attachment 7 – Further details on the Allianz transaction.• Attachment 8 – Another recent media story about HIH.

Senior Manager

HIH Case Study on Asset R�sk (Round 3)

3

Attachment 1

HIH

26 October 2000General ManagerDiversified Institutions DivisionAustralian Prudential Regulation AuthorityG.P.O. Box 9836Sydney, NSW 2001

Dear GM,

Credit Risk Management Visit

This is a follow-up letter to my earlier letter of 15 September. It seems to us that APRA’s major concern is that, although the current guidelines were approved after the FAI ac-quisition, many breaches occur with respect to certain investments (which are mainly within FAI) and the guidelines have not been amended accordingly. In response I would like to set out the following background information which might assist with your con-sideration.

• The investment guidelines have been compiled on a conservative basis in line with the policy that business risk should not be compounded by investment risk.

• To retain their character, these guidelines have not been changed to any substan-tial extent to accommodate breaches caused by the mainly FAI investments.

• Breaches are brought to the attention of the Investment Committee (a com-mittee of Board) at its quarterly meetings, and therefore the underlying invest-ments are monitored regularly.

• In a majority of cases, it is HIH’s intention to dispose of those investments that cause frequent departures from the guidelines. Investments outside of the guidelines (“non-core investments”) are not what HIH intends to hold in the long term in its portfolio.

• Due to the nature of the market for some of the non-core investments (espe-cially those in the property sector), disposal may only be effected over a lengthy period of time in order to realize their intrinsic values.

As noted in my previous letter, many of the FAI assets have been problematic for us due to:

• Lack of a documentation trail within FAI.

Insurance Superv�s�on Core Curr�culum

�

• Loss of staff continuity as all key FAI accounting/investment staff left shortly after completion of the FAI acquisition.

• The complex structure of some of the unlisted investments which are subject to legal obligations of one form or another.

Although it may not be apparent to an external party, substantial time and effort have indeed been expended by HIH staff to identify, analyze and evaluate risk profiles of the current investment portfolio especially the segment that is considered to be of a non-core nature. We are committed to properly documenting risk exposures but are subject to the constraint of available staff resources.

Our response to the specific issues that you raised are set out in the attachment to this letter. We wish to assure you that we welcome any constructive comments that you may care to bring to our attention.

Yours sincerelyD FoderaChief Operating Officer

HIH Case Study on Asset R�sk (Round 3)

5

Annex 1

Please refer to the background information in the body of the letter. A group of execu-tives comprising Terry Cassidy, Dominic Fodera, John Ballhausen and Bill Howard is ultimately responsible for the risk management of the investment portfolio.

The legal ownership status of the St Moritz Hotel is clear as is demonstrated by the fact that HIH is due to receive in early November the first installment (US$65 million) of its sale proceeds.

The HIH America consolidation entry recorded was to credit investment in subsid-iaries and debit paid-in capital in the US general ledger. The initial incorrect entry and the subsequent correction have no effect on current, past, or future earnings or share-holders’ funds of the group.

Insurance Superv�s�on Core Curr�culum

�

Annex 2: Policy Exceptions and Shortcomings

Insofar as the $100 million fund is concerned, we shall review the guideline wording to ensure clarity. The intention is that historical investment cost of this fund is not to exceed $100 million, but growth in market value beyond $100 million is permissible. We disagree with the view that the Investment Committee is involved in stock selection. The Investment Committee has acted, and will continue to act, as the body that oversees the investment function of HIH.

There were incorrect classifications in the March return to APRA which have been discussed between relevant officers of our respective organizations.

We concur with your recommendation that investment guidelines be applied to our Hong Kong and New Zealand operations, and that the guidelines be expanded to ex-panded to capture hybrid instruments.

The margins prescribed in mandates given to external managers are applicable to 3 years rolling periods. We accept your advice and shall include an additional column in our investment report showing the relevant margin applicable to each manager.

Independent and reputable valuers are consistently engaged to carry our property valuations. Your recommendation will be put before the Investment Committee for its consideration for adoption.

It was the Investment Committee’s decision in late 1999 early 2000 to increase ex-posure to equities through increasing risk levels rather than increasing the size of funds under management. The increased risk was applied to the internal fund. This approach was considered acceptable given the risk levels employed by the other equity managers engaged by HIH. The Investment Department closely monitored all positions within the portfolio and provided regular reporting on the portfolio to the Investment Com-mittee.

HIH Case Study on Asset R�sk (Round 3)

�

Annex 3: Inter-company Investments

Steps have been taken to ensure that similar errors will not recur. This matter has been discussed between relevant officers of our respective organizations.

Insurance Superv�s�on Core Curr�culum

�

Annex 4: Loan Exposures

Substantial time and effort has been expended by relevant staff to analyze the loan book so that appropriate action may be taken when and where appropriate. However we do accept that more effort is required to record the result of the analyses in a proper docu-ment format.

An evaluation of the quantum of potential defaults was carried out for the purpose of the 30 June 2000 financial report. A provision was made in the accounts in accor-dance therewith.

We believe this matter has been discussed between relevant officers of our respective or-ganizations. We agree with your suggestion, which has been implemented, that treasury be assigned the task of managing the funds flow between all entities, be they internal or external.

We shall carry out an update review of the Emu Brewery development (which is a com-plex project) and shall then commission independent valuations where required.

HIH Case Study on Asset R�sk (Round 3)

�

Attachment 2

Memorandum

HIH Asset Risk—Current Assessment as at 31 October 2000

1. Current position – Summary

• HIH is a company under considerable stress. We rate it as high risk and have done so for some time.

• HIH remains profitable and is taking action to cement its position.• A series of recently announced transactions, particularly the relationship with

Allianz, the resolution of the US business, the progress of the asset realization program on schedule (particularly the St Moritz Hotel in New York and the Emu Brewery sites in Western Australia) are positive for the company but have been poorly communicated to the market.

• The company is looking for a new CEO.• The company is on credit watch with ratings agencies.• APRA is conducting weekly meetings with the Chief Operating Officer.

• We have investigated the profit outlook for the company and find it to be rea-sonably promising subject to the caveat that the plans in place need to be carried through.

• The company has greater flexibility to deal with its issues than it did just one month ago as a result of recent transactions and a change of management.

• The critical risks for the company remain, in particular, the prospect of a down-grade in credit rating (see table below), the lack of a change in sentiment, the appointment of a CEO without credibility, and the failure to execute the current transactions.

• The appointment of the new CEO is critical for the company. In particular, this offers the opportunity for a further change of management attitude (we have already seen some) and a change in the public and market sentiment.

Over the last month, since we intervened on the need for the company to consider its future seriously, we have seen the response turn in favour of our recommendations. In particular, we have provided impetus to settle the uncertainty surrounding the CEO, and have encouraged (and seen) improvement of focus on more robust risk assess-

Insurance Superv�s�on Core Curr�culum

�0

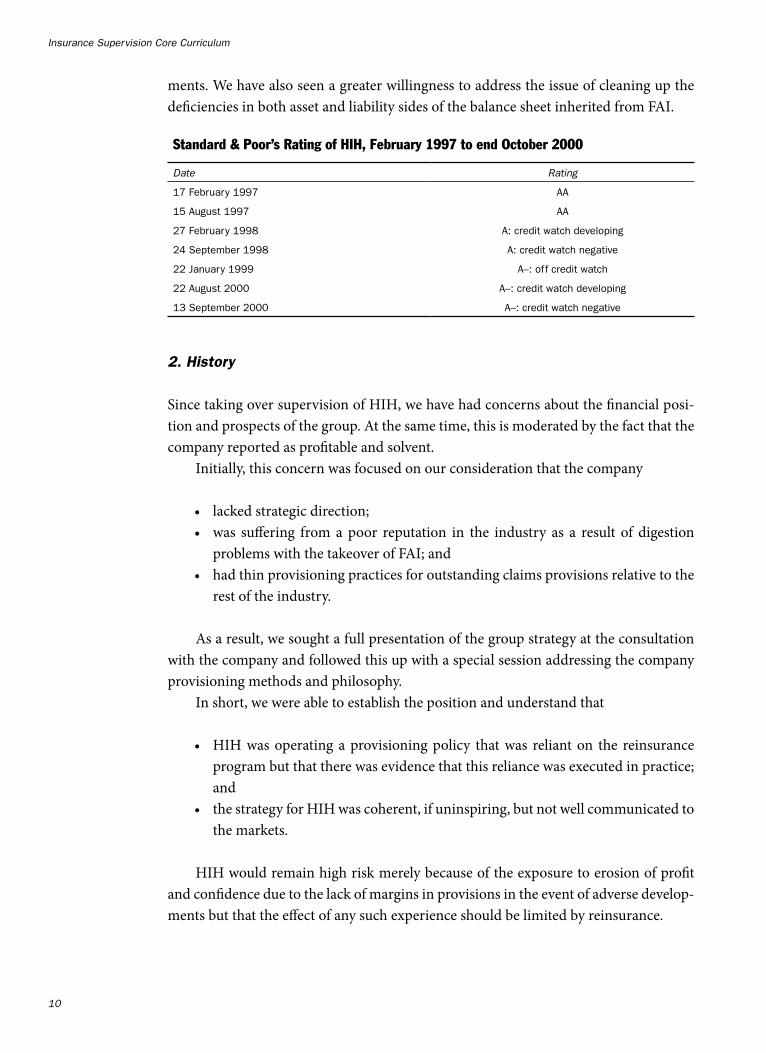

ments. We have also seen a greater willingness to address the issue of cleaning up the deficiencies in both asset and liability sides of the balance sheet inherited from FAI.

2. History

Since taking over supervision of HIH, we have had concerns about the financial posi-tion and prospects of the group. At the same time, this is moderated by the fact that the company reported as profitable and solvent.

Initially, this concern was focused on our consideration that the company

• lacked strategic direction;• was suffering from a poor reputation in the industry as a result of digestion

problems with the takeover of FAI; and• had thin provisioning practices for outstanding claims provisions relative to the

rest of the industry.

As a result, we sought a full presentation of the group strategy at the consultation with the company and followed this up with a special session addressing the company provisioning methods and philosophy.

In short, we were able to establish the position and understand that

• HIH was operating a provisioning policy that was reliant on the reinsurance program but that there was evidence that this reliance was executed in practice; and

• the strategy for HIH was coherent, if uninspiring, but not well communicated to the markets.

HIH would remain high risk merely because of the exposure to erosion of profit and confidence due to the lack of margins in provisions in the event of adverse develop-ments but that the effect of any such experience should be limited by reinsurance.

Standard & Poor’s Rating of HIH, February 1997 to end October 2000

Date Rat�ng

17 February 1997 AA

15 August 1997 AA

27 February 1998 A: credit watch developing

24 September 1998 A: credit watch negative

22 January 1999 A–: off credit watch

22 August 2000 A–: credit watch developing

13 September 2000 A–: credit watch negative

HIH Case Study on Asset R�sk (Round 3)

��

3. Announcement of 13 September

The announcement on 13 September 2000 followed a suspension from trading of HIH shares on the ASX from the morning of 11 September. The key points were:

• The establishment of a joint venture with Allianz• The announcement of profit• Some comments on APRA’s reform papers and the internal review at HIH that

the papers “inspired”.

We have concluded that the Allianz deal is positive for future policyholders and that this is an imperative that leads directly to our support for its approval.

4. Investment Risk Visit

We conducted an investment risk visit to HIH in July. The visit raised a number of detailed issues as to the valuation of assets, in particular those inherited from FAI, al-though the magnitudes were low, as might have been expected given the nature of ex-ception reporting.

We asked for substantial additional information that was slow in coming forward. Eventually, HIH were able to locate the information we needed. This highlighted to them that they had a substantial issue in the management of assets inherited from FAI. Since the request, management have indicated to us that they have identified other asset issues that they are pursuing.

Our conclusion is that HIH have discovered that the absence of proper records at FAI has left them exposed to asset risk which can only be rectified with a far closer scrutiny that has been applied in the past.

5. Profit

Having established the Allianz joint venture, we were keen to pursue the question of whether or not the company would have a suitable remaining business mix capable of generating a profit outlook.

In addition, we were particularly keen to investigate the reasons for the FAI de-terioration reported in the results for the year ended 2000. In particular, if our under-standing of the provisioning policy were to be sustained then a loss of such magnitude should have fallen to the reinsurers—something that clearly did not happen.

Insurance Superv�s�on Core Curr�culum

�2

We have conducted two visits to the company to establish a view as to its expected prof-itability and to validate the robustness of their projections. The company has reported as follows.

HIH Case Study on Asset R�sk (Round 3)

�3

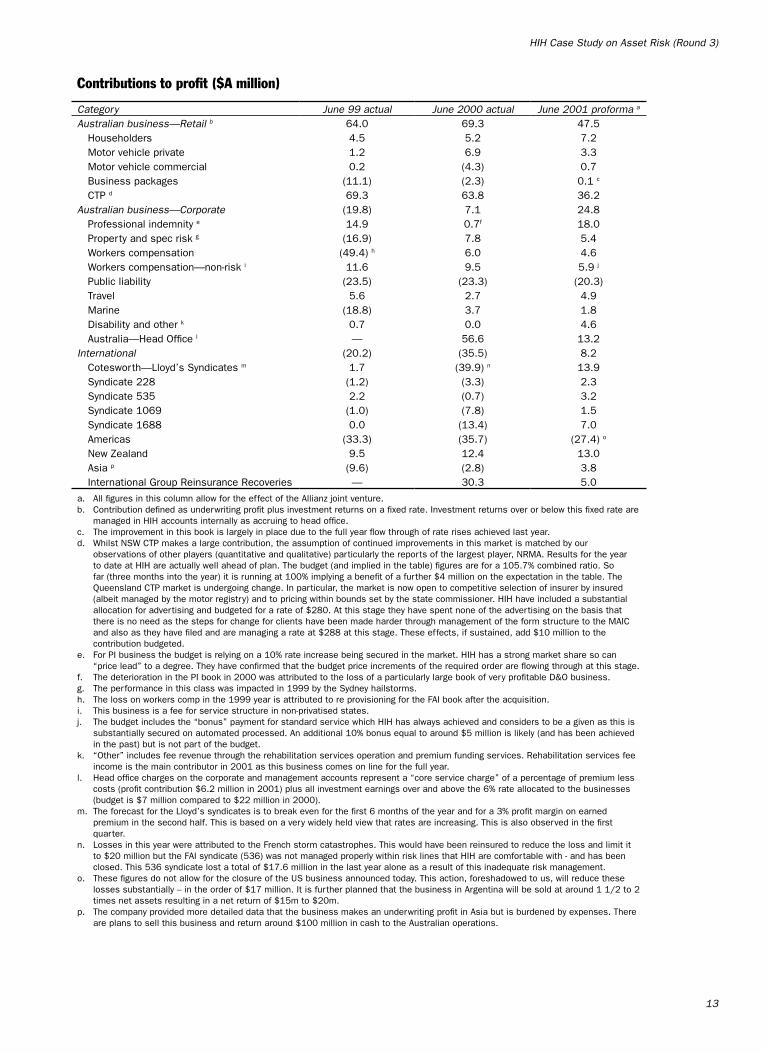

Contributions to profit ($A million)

Category June �� actual June 2000 actual June 200� proforma a

Austral�an bus�ness—Reta�l b 64.0 69.3 47.5Householders 4.5 5.2 7.2Motor vehicle private 1.2 6.9 3.3Motor vehicle commercial 0.2 (4.3) 0.7Business packages (11.1) (2.3) 0.1 c

CTP d 69.3 63.8 36.2Austral�an bus�ness—Corporate (19.8) 7.1 24.8

Professional indemnity e 14.9 0.7f 18.0Property and spec risk g (16.9) 7.8 5.4Workers compensation (49.4) h 6.0 4.6Workers compensation—non-risk i 11.6 9.5 5.9 j

Public liability (23.5) (23.3) (20.3)Travel 5.6 2.7 4.9Marine (18.8) 3.7 1.8Disability and other k 0.7 0.0 4.6Australia—Head Office l — 56.6 13.2

Internat�onal (20.2) (35.5) 8.2Cotesworth—Lloyd’s Syndicates m 1.7 (39.9) n 13.9Syndicate 228 (1.2) (3.3) 2.3Syndicate 535 2.2 (0.7) 3.2Syndicate 1069 (1.0) (7.8) 1.5Syndicate 1688 0.0 (13.4) 7.0Americas (33.3) (35.7) (27.4) o

New Zealand 9.5 12.4 13.0Asia p (9.6) (2.8) 3.8International Group Reinsurance Recoveries — 30.3 5.0

a. All figures in this column allow for the effect of the Allianz joint venture.b. Contribution defined as underwriting profit plus investment returns on a fixed rate. Investment returns over or below this fixed rate are

managed in HIH accounts internally as accruing to head office.c. The improvement in this book is largely in place due to the full year flow through of rate rises achieved last year.d. Whilst NSW CTP makes a large contribution, the assumption of continued improvements in this market is matched by our

observations of other players (quantitative and qualitative) particularly the reports of the largest player, NRMA. Results for the year to date at HIH are actually well ahead of plan. The budget (and implied in the table) figures are for a 105.7% combined ratio. So far (three months into the year) it is running at 100% implying a benefit of a further $4 million on the expectation in the table. The Queensland CTP market is undergoing change. In particular, the market is now open to competitive selection of insurer by insured (albeit managed by the motor registry) and to pricing within bounds set by the state commissioner. HIH have included a substantial allocation for advertising and budgeted for a rate of $280. At this stage they have spent none of the advertising on the basis that there is no need as the steps for change for clients have been made harder through management of the form structure to the MAIC and also as they have filed and are managing a rate at $288 at this stage. These effects, if sustained, add $10 million to the contribution budgeted.

e. For PI business the budget is relying on a 10% rate increase being secured in the market. HIH has a strong market share so can “price lead” to a degree. They have confirmed that the budget price increments of the required order are flowing through at this stage.

f. The deterioration in the PI book in 2000 was attributed to the loss of a particularly large book of very profitable D&O business.g. The performance in this class was impacted in 1999 by the Sydney hailstorms.h. The loss on workers comp in the 1999 year is attributed to re provisioning for the FAI book after the acquisition.i. This business is a fee for service structure in non-privatised states.j. The budget includes the “bonus” payment for standard service which HIH has always achieved and considers to be a given as this is

substantially secured on automated processed. An additional 10% bonus equal to around $5 million is likely (and has been achieved in the past) but is not part of the budget.

k. “Other” includes fee revenue through the rehabilitation services operation and premium funding services. Rehabilitation services fee income is the main contributor in 2001 as this business comes on line for the full year.

l. Head office charges on the corporate and management accounts represent a “core service charge” of a percentage of premium less costs (profit contribution $6.2 million in 2001) plus all investment earnings over and above the 6% rate allocated to the businesses (budget is $7 million compared to $22 million in 2000).

m. The forecast for the Lloyd’s syndicates is to break even for the first 6 months of the year and for a 3% profit margin on earned premium in the second half. This is based on a very widely held view that rates are increasing. This is also observed in the first quarter.

n. Losses in this year were attributed to the French storm catastrophes. This would have been reinsured to reduce the loss and limit it to $20 million but the FAI syndicate (536) was not managed properly within risk lines that HIH are comfortable with - and has been closed. This 536 syndicate lost a total of $17.6 million in the last year alone as a result of this inadequate risk management.

o. These figures do not allow for the closure of the US business announced today. This action, foreshadowed to us, will reduce these losses substantially – in the order of $17 million. It is further planned that the business in Argentina will be sold at around 1 1/2 to 2 times net assets resulting in a net return of $15m to $20m.

p. The company provided more detailed data that the business makes an underwriting profit in Asia but is burdened by expenses. There are plans to sell this business and return around $100 million in cash to the Australian operations.

Insurance Superv�s�on Core Curr�culum

��

We have also examined the outlook for the company to 2006. The company has provided figures that support a profit expectation. The volatility of insurance markets suggests that this result is useful but not certain.

5.2 O ur C OnClus iOns

• All figures allow for the reduced share of business profit arising from the joint venture with Allianz.

• Public liability remains problematic although they are seeing 30% rate increases flowing through. The concern remains in claims inflation. The company is working on improvements but has not budgeted on these flowing through in the 2001 year.

• Several liabilities arose beyond the expectations as the company discovered that the reinsurance protection it thought that it had in place under the older business lines acquired from FAI (including Lloyd’s business) was not up to scratch.

• The company is well placed to secure a profit on all remaining business lines in its report at June 2001 (contrasted with a myriad of profits and losses resulting in a small profit overall in 2000).

5.3 T he FAi DeTeriOrATiOn

We have also verified the sources of the poor profit result in the year ended June 2000.We now understand that the result reflects the combined effects of:

• the discovery that FAI reinsurance arrangements were not correctly reported by FAI systems – this has now been subject to a manual reconstruction of records. ($30 million);

• the need to provision for claims that FAI had marked as closed or had under provisioned—this reflected the fact that FAI would close inactive files, even if there were no reasons to suggest that the case would not reopen—in one ex-ample a letter from a solicitor was the first that HIH knew of a matter that they are now provisioning $26 million for;

• the discovery that much of the FAI business was poorly reinsured and implied substantial exposures to single events without protection.

It is now considered by HIH management that the situation has been put on a far sounder footing.

HIH Case Study on Asset R�sk (Round 3)

�5

5.4 O ur C OnClus iOns

• Clearly, and similarly to our finding in terms of asset quality, the FAI inheritance has been the source of the problems for HIH.

• FAI has resulted in a great deal of pain being taken to P&L to put the business on a more secure provisioning footing.

• Whilst further “surprises” can not be fully ruled out at this stage, efforts taken to date suggest future impacts should be much more manageable.

6. Letters of Credit

The company has issued a number of letters of credit as a normal part of its business. The magnitude of these exposures has become a concern to APRA after action taken by the company at the encouragement of their auditor to discuss these with us.

It should be noted that the substantial part of the exposure is related to UK and US business where these letters of credit are a requirement on companies to operate in these markets (so the issue is broader to the whole of the industry where it operates overseas).

It is clear, however, that our discussions with the company on the matter has led management to agree that there needs to be a full audit of the exposures and more ac-tive management of the risks involved.

Work is progressing.

7. Market Sentiment

The company has been the subject of an ongoing campaign in the press let by Mr Mark Westfield in the Australian. The rest of the press has been a little more balanced but the pressure of sentiment has grown since the announcements of the poor profit result.

We note that there is speculation as to the source of information provided to Mr Westfield. Company insiders have some suspicion that the campaign is supported by Mr Adler, a Director of HIH and the former CEO of FAI. It has been suggested in the press that Mr Adler should be a candidate for the vacant CEO position. Clearly, given the fact that the challenges for HIH have arisen largely from FAI then this would be a concerning outcome for us.

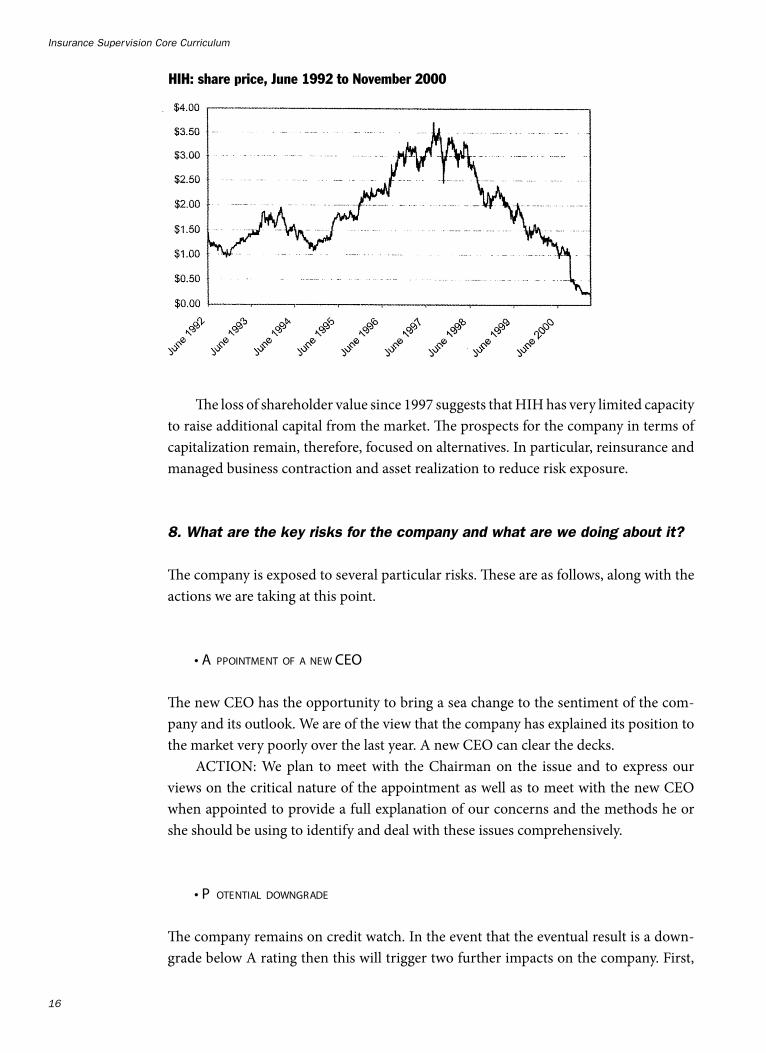

The share price performance for HIH over the last 5 years is shown below. The company has seen a deteriorating situation since the FAI acquisition.

Insurance Superv�s�on Core Curr�culum

��

The loss of shareholder value since 1997 suggests that HIH has very limited capacity to raise additional capital from the market. The prospects for the company in terms of capitalization remain, therefore, focused on alternatives. In particular, reinsurance and managed business contraction and asset realization to reduce risk exposure.

8. What are the key risks for the company and what are we doing about it?

The company is exposed to several particular risks. These are as follows, along with the actions we are taking at this point.

• A ppOinTmenT OF A new CeO

The new CEO has the opportunity to bring a sea change to the sentiment of the com-pany and its outlook. We are of the view that the company has explained its position to the market very poorly over the last year. A new CEO can clear the decks.

ACTION: We plan to meet with the Chairman on the issue and to express our views on the critical nature of the appointment as well as to meet with the new CEO when appointed to provide a full explanation of our concerns and the methods he or she should be using to identify and deal with these issues comprehensively.

• p OTenTiAl DOwngrADe

The company remains on credit watch. In the event that the eventual result is a down-grade below A rating then this will trigger two further impacts on the company. First,

HIH: share price, June 1992 to November 2000

HIH Case Study on Asset R�sk (Round 3)

��

Allianz will have an option to walk away from the joint venture should such a down-grade occur before the end of December 2000. Second, a reasonable amount of the remaining business will not renew as some brokers have a policy of not recommending a company with a rating less than A.

There is some scope for judgement as to what the prospects for this would be. Prima facie, it would seem that such a downgrade is inevitable. If, however, the ratings agencies factor in the cash payments from Allianz ($200 million on 1 January 2001), the Emu Brewery and St Moritz asset sales ($49 million and $65 million respectively, both due in November 2000) and the potential sales of Asian and US lines then there is scope to be optimistic.

ACTION: We have requested that management analysis be completed on liquidity, profit and capital on a scenario testing basis to consider the ratings downgrade. It will, we expect, show that the company would shrink further but remain profitable.

• F urTher DeTeriOrATiOn OF bus ines s res ulTs

There is a risk that further FAI asset or liability deterioration will become apparent. However, we consider that these issues are most likely to be less severe in magnitude given the efforts taken to date to uncover issues as far as possible.

ACTION: The company and the auditor will be completing a further review of re-cords. We will also monitor developments on a monthly basis to check that emergence is in line with our view that only small issues should be uncovered from here on.

• l iquiDiTy mAnAgemenT

The company is to provide us with a management analysis of liquidity over the next five years including the workout of the large and problematic assets.

ACTION: The company has agreed with our request that this analysis should in-clude stress testing and we have recommended several scenarios. The results of the liquidity analysis are to be discussed next week with the company.

• T he COmpleTiOn OF The TrAns ACTiOns CurrenTly AnnOunCeD, in pArTiCulAr The J V wiTh AlliAnz.

The company is to provide us with a more detailed analysis of the impact of the JV on liquidity and on the residual insurance company, as well as a strategy in the event that the deal falls through. There are still some features of the transaction that require a better understanding on our part, e.g. the role of the trust account.

Insurance Superv�s�on Core Curr�culum

��

ACTION: The company has agreed with our request. The details should be pro-vided within a few weeks.

Senior Manager

HIH Case Study on Asset R�sk (Round 3)

��

Attachment 3

Memorandum

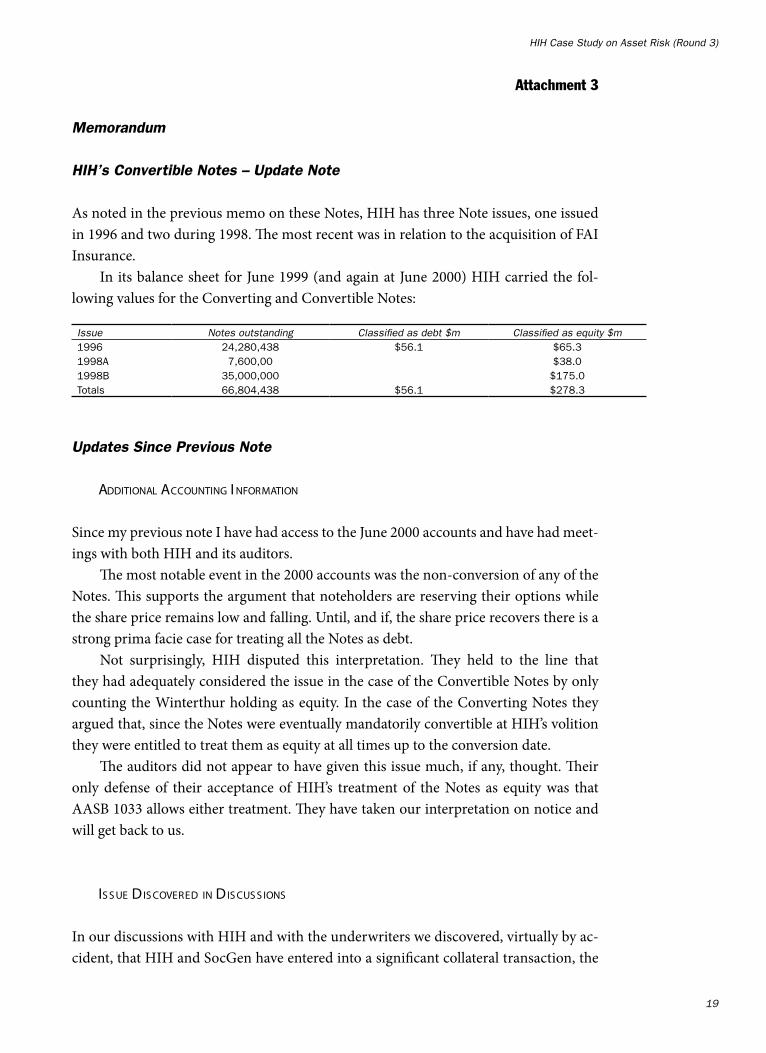

HIH’s Convertible Notes – Update Note

As noted in the previous memo on these Notes, HIH has three Note issues, one issued in 1996 and two during 1998. The most recent was in relation to the acquisition of FAI Insurance.

In its balance sheet for June 1999 (and again at June 2000) HIH carried the fol-lowing values for the Converting and Convertible Notes:

Updates Since Previous Note

ADDiTiOnAl ACCOunTing i nFOrmATiOn

Since my previous note I have had access to the June 2000 accounts and have had meet-ings with both HIH and its auditors.

The most notable event in the 2000 accounts was the non-conversion of any of the Notes. This supports the argument that noteholders are reserving their options while the share price remains low and falling. Until, and if, the share price recovers there is a strong prima facie case for treating all the Notes as debt.

Not surprisingly, HIH disputed this interpretation. They held to the line that they had adequately considered the issue in the case of the Convertible Notes by only counting the Winterthur holding as equity. In the case of the Converting Notes they argued that, since the Notes were eventually mandatorily convertible at HIH’s volition they were entitled to treat them as equity at all times up to the conversion date.

The auditors did not appear to have given this issue much, if any, thought. Their only defense of their acceptance of HIH’s treatment of the Notes as equity was that AASB 1033 allows either treatment. They have taken our interpretation on notice and will get back to us.

is s ue Dis COVereD in Dis Cus s iOns

In our discussions with HIH and with the underwriters we discovered, virtually by ac-cident, that HIH and SocGen have entered into a significant collateral transaction, the

Issue Notes outstand�ng Class�fied as debt $m Class�fied as equ�ty $m1996 24,280,438 $56.1 $65.31998A 7,600,00 $38.01998B 35,000,000 $175.0Totals 66,804,438 $56.1 $278.3

Insurance Superv�s�on Core Curr�culum

20

effect of which appears to be quite complicated. It does not appear to have been fully understood by the HIH board and was not disclosed in the prospectus for the notes.

SocGen was a joint underwriter with Macquarie Equities of the converting note issue following the acquisition of FAI. It also received a $35 million priority allocation of the notes.

From the outset, SocGen’s proposal appears to have included the idea of a collateral transaction between HIH and SocGen called the total return swap (the swap). As part of the swap, a collateral deposit was to be paid by HIH to SocGen of $35 million, equal to the amount of the priority allocation underwritten by SocGen. The collateral deposit entitled HIH to receive interest at a rate higher than the deposit market rate. It was also designed to “secure HIH’s obligations under the swap”. The deposit served to protect SocGen in the event that the notes declined in value, in which event SocGen had the right to sell the notes and apply the deposit to indemnify itself against any loss which it thereby suffered.

Key terms of the swap include the following:

• HIH can withdraw the deposit at any time on 30 days written notice; • on the giving of a withdrawal notice SocGen can sell the converting notes that it

has underwritten; • any profit on sale of the notes is to be HIH’s; but • in the event of a loss, SocGen has a right of set-off against the deposit to recover

any loss on the transaction—the trigger point for this set-off to be activated is if HIH’s share price falls below $1.00 for five consecutive trading days.

HIH receives interest on the notes less a margin payable to SocGen. The amount involved is $35 million. It appears that SocGen required HIH to agree to the swap at the same time that HIH and SocGen agreed the underwriting agreement in respect of the converting notes.

I asked for a copy of the due diligence committee reports prepared for the HIH Board in the period leading up to the acquisition of FAI and the finalization of the pro-spectus for the issue of the notes. None of these makes any reference to the swap. Thus the question of disclosure in the prospectus never seems to have been addressed. Senior staff at HIH assured me nonetheless that the Board was fully aware of the swap. I note that ASIC granted HIH exemption from compliance with the requirements of s.1022 for a full prospectus for the issue of the converting notes. Consequently HIH is-sued a short-form prospectus under s.1022AA of the Corporations Law on 26 October 1998. The prospectus did not mention the swap or its effect. A declaration was made in the prospectus pursuant to s.1008A of the Law that the statements in the prospectus were true and not misleading.

In view of the swap transaction I wonder whether this matter should be referred to ASIC for possible action.

Senior Manager

HIH Case Study on Asset R�sk (Round 3)

2�

Attachment 4

Memorandum

HIH’s Future Income Tax Benefits—Update Note

As noted in the previous memo on FITB, in the 30 June 1999 financial report for HIH, an amount of $145.2 million was recorded in respect of FITB for timing differences and $27.2 million for tax losses. As mentioned, the financial report does not disclose a provision for tax or for deferred income tax.

Since that memo we have met with HIH’s auditors and followed up with HIH. We have used the information in the whistleblower document as a guide for our discus-sions, focusing mainly on recoverability.

In my meeting with the auditors they produced a spreadsheet prepared by HIH with respect to FITB. The spreadsheet recorded that:

• The FITB balance attributable to tax losses disclosed in the 30 June 1999 fi-nancial report for the HIH consolidated entity ($27.2 million) was a net figure which had been arrived at by offsetting the consolidated entity’s provision for deferred income tax ($113.6 million) against the consolidated entity’s gross bal-ance of FITB attributable to tax losses ($140.8 million).

• The FITB balance attributable to timing differences disclosed in the 30 June 1999 financial report for the HIH consolidated entity ($145.2 million) was also a net figure which had been arrived at by offsetting the consolidated entity’s provision for income tax ($60.0 million) against the consolidated entity’s gross balance of FITB attributable to timing differences ($205.2 million).

From what we have seen, the audit work papers created in the conduct of the 1999 audit by the auditors with respect to taxation were directed only at the risk associated with the taxation calculations. The audit work papers did not deal with the risk of FITB not being recoverable.

These findings raised the following issues/concerns about the accounts and the auditors:

1. Whether the manner in which the balances of provision for deferred income tax were offset against FITB attributable to tax losses as at 30 June 1999 was a con-travention of AASB 1020 and, if so, whether the auditors ought to have qualified their audit report in that respect. AASB 1020 states clearly that:

A future income tax benefit brought to account by one company in a group of

companies shall not be offset against a provision for deferred income tax brought

Insurance Superv�s�on Core Curr�culum

22

to account by another company in the group of companies, when drawing up group accounts.

2. Whether the manner in which the balance of the provision for income tax was offset against the balance of FITB attributable to timing differences as at 30 June 1999 was an inappropriate accounting treatment and if so, whether auditors ought to have qualified their audit report in that respect.

3. Whether the auditors even obtained sufficient appropriate audit evidence with respect to the recognition of FITB as an asset as at 30 June 1999.

Further investigations provided the following information:

VAliDiTy OF neTTing in The 1999 A CCOunTs

First, with respect to the offsetting of income tax balances described above, an analysis on a company-by-company basis suggests that provisions for deferred income tax to-taling $32.5 million were able to be legitimately offset validly against FITB attributable to tax losses. This means that a provision for deferred income tax provision of $81.5 mil-lion should have remained which, in the absence of appropriate audit evidence, should not have been offset against the balance of FITB attributable to tax losses.

Second, following advice from our own internal accounting standards experts, the offsetting of $60 million of FITB attributable to timing differences against the provision for income tax was an inappropriate accounting treatment because realization of the FITB would only occur in future periods, whereas the provision for income tax was a current liability which could not be reduced by the reversal of timing differences in the future.

With respect to the offsetting, the auditors argued that HIH had presented the con-solidated data to them as having already been netted in accordance with AASB 1020.

reCOgniTiOn OF neT FiTb As An As s eT in The 1999 A CCOunTs

Not surprisingly, the auditors defended their decision to recognize the net FITB figures as assets (leaving aside the issue of whether or not they were netted correctly under AASB 1020). They argued that they believed HIH would make future profits, such that prior period losses would be recoverable. They argued that the cause of the past losses had ceased because a large proportion of the difference between reserves booked in De-cember 1997 and June 1999 related to FAI and were not ongoing operational problems that will continue to generate losses. They pointed out that HIH’s reported loss in 1999 was only small, and only after bringing to account an abnormal item and an extraordi-

HIH Case Study on Asset R�sk (Round 3)

23

nary item of $50 million each. Thus they argued that HIH’s underlying operating results indicated that it was operating profitably.

reCOgniTiOn OF neT FiTb As An As s eT in The 2000 A CCOunTs

Our discussion about the accounts for June 2000 followed along similar lines. My inves-tigations of their files suggested that:

• The FITB balance attributable to tax losses disclosed in the 30 June 2000 finan-cial report for the HIH consolidated entity ($137.2 million) was a net figure which had been arrived at by offsetting the consolidated entity’s provision for deferred income tax ($131.3 million) and a portion of the consolidated entity’s provision for income tax ($40.6 million) against the consolidated entity’s gross balance of FITB attributable to tax losses ($309.1 million).

• The FITB balance attributable to timing differences disclosed in the 30 June 2000 financial report for the HIH consolidated entity ($91.2 million) was a net figure which had been arrived at by offsetting a portion of the consolidated en-tity’s provision for income tax ($56.1 million) against the consolidated entity’s gross balance of FITB attributable to timing differences ($147.3 million).

The same issues raised above with respect to the 1999 accounts arise again in the context of the 2000 accounts.

Unlike the situation in 1999, however, the auditors in 2000 appear to have explicitly considered the recognition of FITB and, in doing so, concluded that there was a residual audit risk in that respect. Indeed, the recognition of FITB in the 30 June 2000 financial report appears to have been a significant issue throughout the 2000 audit.

The recoverability of FITB was raised as an issue at the audit committee meetings on 12 September 2000 and 12 October 2000. At the meeting on 12 October 2000, it was resolved that the financial report would disclose the expected recovery period for tax losses (five years). The management representation letter to the auditors states that “The directors are virtually certain that all future income tax benefits relating to tax losses included in the financial report will be recovered in a period of not more than 5 years.” The auditors appear to have relied on this representation to continue to accept the rec-ognition of FITB as an asset—even though they had reservations. In short, they passed responsibility for the decision to HIH.

The audit work appears to be well short of acceptable standards. There is no evi-dence that they sought to corroborate the management representations as required by AUS 520. They relied on unsubstantiated assertions about future earnings. They made no efforts to analyze the FITB on a company-by-company basis. There is no evidence that they considered the impact of the Allianz deal on the recoverability of FITB.

Insurance Superv�s�on Core Curr�culum

2�

There is some evidence of these analyses having been done within HIH but there is no evidence demonstrating that these matters were resolved to the level of virtual certainty required by AASB 1020.

On the basis of the evidence I conclude that none of the amounts of net FITB rec-ognized as assets in the 2000 accounts should have been so recognized.

VAliDiTy OF neTTing in The 2000 A CCOunTs

Again, the company-by-company analysis suggests that of the provisions for deferred income tax totaling $131.3 million offset against FITB attributable to tax losses, only $68.7 million was legitimately allowable under AASB 1020.

As with the 1999 accounts, on the basis of the evidence, it is my opinion neither the $40.6 million of income tax provisions offset against FITB attributable to tax losses, nor the $56.1 million offset against FITB for timing differences should have been allowed.

Senior Manager

HIH Case Study on Asset R�sk (Round 3)

25

Attachment 5

Memorandum

Valuation of Investments—Progress Report

You asked us to look at the valuation methodology of a range of assets held by HIH. In the time available we have only had time to explore a few of these in detail. To maximize our effectiveness we focused on those assets that offered the quickest resolution. Our findings are summarized below.

Deferred Information Technology Costs

Given that this asset was highlighted by the whistleblower document we pursued it as one of our first priorities. Deferred IT costs increased from $30 m in 1997 to $63 m in 1999, to $88 m in 2000. Our investigation revealed only one issue of contention.

In the conduct of the audit for June 2000, an amount of $11.7 million was identified and described in the following terms in the audit work papers:

“These costs relate to information processing performed by the divisions due to system failures. The contractor costs/salaries/rent allocations have been determined by each division. These costs relate to processing only and not IT development i.e. there are no IT Technical staff costs included in these numbers. Information processing relates to backlogs generated by system down time, reprocessing due to data corruption and additional financial assistance to reconcile financial information.”

Following this notation the auditors initially recorded their view that the amount of $11.7 million should be expensed in the profit and loss account.

This initial view was revised following the Allianz transaction and the costs were not expensed. The motivation appears to have been that the accounting treatment of the Allianz deal involved writing part of the cash and receivables against deferred IT Costs.

However, recoverability is not the issue here. The $11.7 m should have been treated as an expense in the June 2000 accounts. The amount is material and the likelihood of recovering the costs in January is no justification for an incorrect accounting treat-ment.

Insurance Superv�s�on Core Curr�culum

2�

Investments in Associates

We sampled one associate company only out of some 16 or so – Home Security Inter-national (HSI). Following the acquisition of FAI, HIH inherited a 36 per cent share-holding in a company incorporated in Delaware and floated on the US stock market known as Home Security International (HSI). HSI conducted a home security business in Australia via its wholly owned subsidiary FAI Home Security Pty Ltd (FAIHS). For various periods of time up until the float of HSI in July 1997 FAIHS was part of the FAI group. After that time it was not. It used the name “FAI” under a licence agreement with the FAI Insurance Group. HIH’s relationship with this company appears to be complex and complicated by conflicts of interest. However, the only issue that we cover below is the valuation of shares in HIS in the June 1999 accounts.

As at 30 June 1999 FAI held an investment in HSI of 2 150 000 shares. Those shares were valued in the financial statements at $28 584 378, on the basis of a “third party” offer price (from the CEO of HSI Brad Cooper) of US$8.80. The market price of the shares at the time, however, was US$5.63, being some $10.3 million below the value recognized in the financial statements.

The auditors proposed an adjustment to the carrying value of this asset of $10 million. However, the audit committee accepted management’s valuation of the asset which was based upon a letter of offer dated 12 January 1999 from Cooper to Rodney Adler (CEO of FAI and later a Board member of HIH). That offer was no longer current when the 1999 financial statements were prepared. It came from a person who was the chairman and chief executive of HSI and could not have been taken as a market price which another willing buyer might have paid.

In my view it was quite inappropriate to value the shares in HSI at the price Cooper had offered in January. The auditor’s proposed adjustment to this value should have been made, but was not. The investment was therefore overstated by $10.3 m.

We are currently investigating some significant payments made to HIS by HIH over the past year. The evidence to hand so far indicates that the overstatement of the value of HIS in the 2000 accounts may be significantly greater than in 1999.

Marketable Investments

We have reviewed the portfolio of marketable investments and, while I believe that many of them are inappropriate to the business of insurance there is no evidence that the value of any of these investments have been misstated in the annual accounts or in APRA returns. The problems that can arise from inappropriate investments are illus-trated by HIH’s history with its investment in One.Tel, a dot.com company inherited from FAI.

As at 31 December 1998 FAI owned 9.8 million One.Tel shares. This holding had an historical cost of $1.2 million and a market value of $58.7 million at that time. Fol-

HIH Case Study on Asset R�sk (Round 3)

2�

lowing the takeover and before 30 June 1999, One.Tel made a bonus issue pursuant to which HIH received 39.6 million additional shares in One.Tel. During the same period HIH sold One.Tel shares valued at $49.3 million. Taking into account a decline in One.Tel’s share price during this period, HIH booked a total gain in respect of its One.Tel shareholding of $34.2 million for the six months to 30 June 1999. HIH sold further One.Tel shares in the six months to 31 December 1999, at which date it held 25 million One.Tel shares. Realized and unrealized gains in respect of that holding were $56.4 million as at 31 December 1999. However a substantial decline in One.Tel’s share price in early 2000 eliminated most of the unrealized gains recorded as at 31 December 1999 so that realized and unrealized gains as at 30 June 2000 were reduced to $25.4 million. A fur-ther decline in One.Tel’s share price in recent weeks has meant that HIH’s remaining shareholding in One.Tel has lost virtually all its value.

Non-Marketable Investments

The extent of assets held at “Directors’ valuations” is abnormally high for a company of this type. As at June 2000 of the $1.75 billion of non-current investments, roughly $1.2 billion of this was in assets held at Director’s valuations. This included a property port-folio of $613 million, investments in unlisted companies unlisted bonds and loans.

Assets acquired in the take-over of FAI were a particular focus for our investiga-tions. We checked a number of external valuations undertaken by HIH of a number of the larger “non-core” FAI assets as at 30 June 1999. These indicated that they were not materially under or over-valued at the date of the takeover. They included the St Moritz Hotel, the Emu Brewery site and OCAL.

We were also given access to a paper prepared by HIH’s internal actuary, in which he reviewed a number of transactions undertaken and accounting treatments adopted by FAI prior to the takeover.

The report noted that at the time of the FAI acquisition there were a number of commercial loans in the FAI portfolio which were in default or in arrears. Further-more, inadequate provisions had been made for them in the accounts of FAI. The report described FAI’s loan approach as high-risk, not prudentially managed, poorly docu-mented and without adequate follow-up. These findings were consistent with those of our Asset Risk team. Sadly, those poor practices appear to be still in operation.

The report noted that the FAI commercial loans which were in default at July 1999 totaled $56.1 million. As a result it concluded that a further $33.65 million of provisions were required. A number of these loans were analyzed in the report. Many were made to companies which had been liquidated years earlier or which were no longer on the ASIC register of companies and which, in the internal auditor’s view, ought to have been written off at the time of the FAI acquisition.

Insurance Superv�s�on Core Curr�culum

2�

The report also analyzed loans which were recorded in the FAI general ledger but not in its commercial loans accounting system. These totaled $33.3 million, of which loans approximating $7 million were in default but had not been provided for.

Elsewhere in the report there were many references to FAI loans, investments and other transactions which the internal auditor considered to be suspicious, undesirable or insecure for various reasons. No allowances for bad or doubtful FAI debts arising out of these transactions appear to have been made in HIH’s calculations of the goodwill on the acquisition of FAI.

We will continue investigating.

Senior Manager

HIH Case Study on Asset R�sk (Round 3)

2�

Attachment 6

Memorandum

Accounting for Goodwill—Update Note

As noted in the earlier memo on goodwill, for the financial year ending 31 December 1996, goodwill was recorded in the financial records of HIH at $48.8 m. By 31 De-cember 1997 it had increased to $67.2 m and by 30 June1999 to $346.5m. The source of the 1999 increase was the premium over NTA paid for FAI.

In the June 2000 accounts goodwill had increased further to $475.3 m as a result of a further write-up of goodwill related to FAI (an additional $163 m).

Since that earlier note we have met with both HIH and their auditors and have seen most of the primary documentation supporting the recognition of goodwill as well as the various audit committee papers. We used the comments in the whistleblower docu-ment as a guide to our line of questioning. A summary of our findings follows.

Goodwill on acquisition of FAI by HIH – Treatment in the 1999 Accounts

As mentioned in the previous memo, the recognition of $275 m of goodwill on the purchase of FAI appeared to have arisen as a result of write-downs that occurred subse-quent to the purchase. We investigated these write-downs with HIH.

A paper entitled “FAI acquisition” prepared by HIH management set out a calcula-tion of goodwill on acquisition of $275 m on the basis of a cost of acquisition of $300 m and adjusted net assets at acquisition of $25 m. Net assets at acquisition were derived by making a number of adjustments to the $224 m reported net assets of FAI as at 30 June 1998. A summary of the adjustments set out in the paper is as follows:

• $67 m reduction in net assets, being in respect of FAI’s trading loss for the six months ended 31 December 1998;

• $20 m reduction in net assets, being for redundancy costs and representing “the expected total payout for 400 FAI and HIH staff retrenched as part of the merger process”;

• $35 m reduction in net assets, being for computer write-offs/other expenses on the basis that it was “necessary to recognize a significant write-down of com-puter related assets and associated IT costs” with other costs said to include “dead rent, relocation, staff transition and training programs”;

• $74 m reduction in net assets relating to “claims provisions”. This item resulted from a “review of claims provisions subsequent to December 1998” which “identified a further deterioration” in the workers compensation, professional indemnity/public liability, inwards and Queensland CTP portfolios;

Insurance Superv�s�on Core Curr�culum

30

• $12 m reduction in net assets relating to “Hannover”;• $20 m reduction in net assets relating to the GCR and NI reinsurance con-

tracts; • $23 m reduction in net assets described as “actuarial adjustment”; • $40 m reduction in net assets in respect of “reinsurance exposures”; • $20 m reduction in net assets relating to the fair value at acquisition of Oceanic

Coal; and• $112 m increase in net assets, being the income tax effect of the above items.

The “FAI acquisition” paper also set out the following:

• The justification for the goodwill value was based on expected returns from the acquisition. The strategic reasons for purchasing FAI were two fold: it pro-vided HIH with critical mass in the Australian market which has been con-solidating rapidly (through such mergers as NRMA/SGIO and AMP/GIO); and it strengthened HIH’s presence in key markets of personal lines and CTP. FAI had established strong brand awareness for its personal lines, a telephone sales operation, FAI Direct, to sell its products, a distribution channel HIH was yet to fully develop. No goodwill value was attributed to FAI’s commercial lines of business or its overseas operations.

• The make up of the adjustments to net assets may vary as the extent of the claim provisions deterioration and value of strategic assets becomes more certain. It may even be necessary to further increase the goodwill in the next financial year.

• For HIH to be able to justify the carrying value of the goodwill, the two strategic businesses, FAI Direct and CTP must produce sufficient returns to support the carrying value of the goodwill. HIH management believes this is achievable due to a lower cost structure, represented through savings in reinsurance costs due to the purchasing power of the combined HIH/FAI book and the lower over-head structure of a larger group.

• Budget forecasts for these two businesses put after-tax earnings for 1999/2000 at $37.9 m after tax. Using an earnings multiple of 12 (based on the average PE multiple for HIH), this produced a value for FAI to HIH of $455 m. On this basis they concluded that there was reasonable evidence to support the recover-ability of the FAI goodwill.

Treatment in the 2000 Accounts

In the course of the year ending 30 June 2000, several adjustments were made to the calculation of net assets of FAI at acquisition such that the amount of goodwill at cost

HIH Case Study on Asset R�sk (Round 3)

3�

recognized with respect to the acquisition of FAI increased from $275 m at 30 June 1999 to $438 m at 30 June 2000. This overall increase of $163 m implied that FAI actually had a deficiency of net assets of $138 m at acquisition (as compared with assessed net assets of $224 m in the 1998 FAI accounts and $25 m as assessed by HIH after the acquisition roughly a year later).

A further paper entitled “Goodwill on FAI acquisition” prepared by HIH manage-ment set out a summary of the relevant adjustments which I will not repeat here (the details are available if you wish to see them).

At the audit committee meeting on 12 September 2000, the auditors presented a summary of the audit issues for the financial year ending 30 June 2000. The presentation highlighted the carrying value of goodwill and noted that the goodwill had increased from $346 m as at June 1999 to $475 m and that FAI represented $405 m of this.

Goodwill Issues Arising from the 1999 Accounts

The principal question in relation to the amount of goodwill booked at 30 June 1999 was not so much the adjustments which were made, but the assessment of the carrying value of the goodwill based on recoverability.

The auditors claimed that their assessment of recoverability was based on the profit forecasts made by HIH and that they had no reason to dispute them. The budgeted profitability presented to the auditors by HIH supported the commercial purpose of the acquisition and was consistent with HIH’s primary objective for the acquisition of FAI, including the personal lines and distribution platform and the expected synergies to be derived from combining the two businesses.

Given that the auditors made no critical assessment of the budgeted earnings of the selected FAI businesses, in my view they did not obtain sufficient appropriate audit evidence with respect to the carrying value of goodwill arising in respect of the acquisi-tion of FAI as at 30 June 1999 as required by the auditing standards AUS 502. The point is moot, however, since:

• HIH subsequently derived a goodwill figure of at least $275 m through the sale to Allianz (see below).

• The budgeted profits of the core businesses that had driven the acquisition ($37.9 m) indicated that profits were likely to be significantly in excess of the future amortization charge of $13.7 m that would result from booking that goodwill amount.

In summary, the 1999 recognition of goodwill appears to have been largely an ex-ercise of “fitting the numbers to the desired outcome”; that is, as holes were discovered in FAI’s balance sheet they were simply added to goodwill rather than written off. The company’s work was bottom-line driven and the auditor’s work was not sufficiently crit-

Insurance Superv�s�on Core Curr�culum

32

ical. However, the subsequent sale to Allianz appears to have justified the figure ex post and so there is no point disputing the figures further.

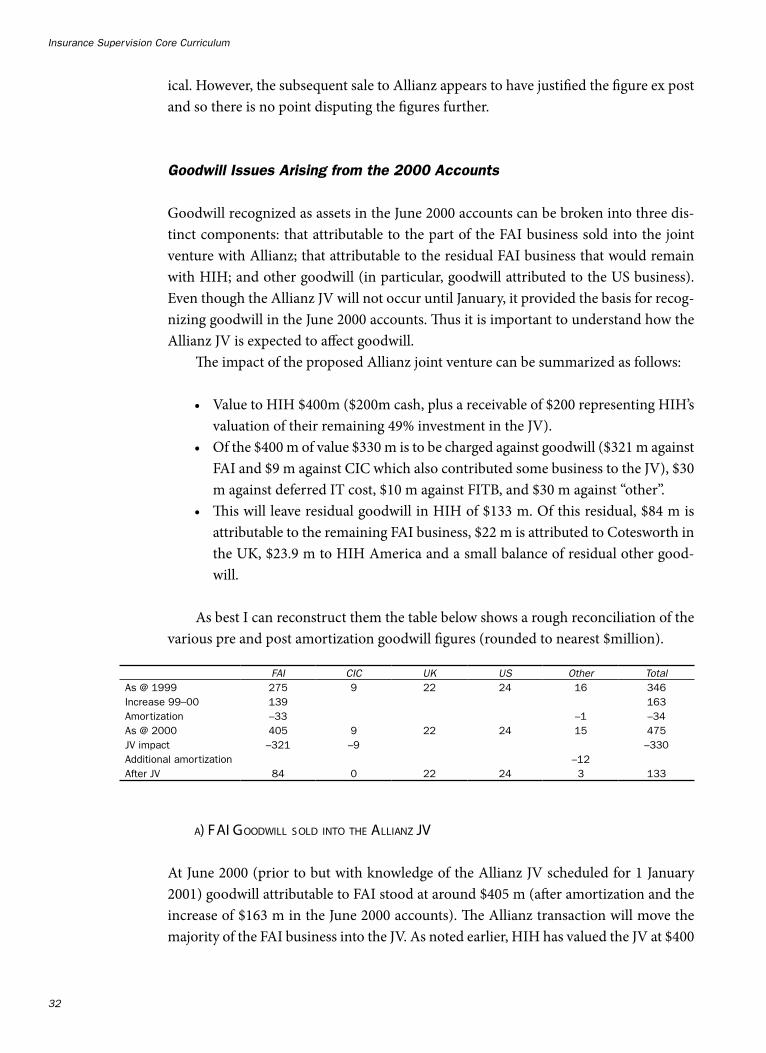

Goodwill Issues Arising from the 2000 Accounts

Goodwill recognized as assets in the June 2000 accounts can be broken into three dis-tinct components: that attributable to the part of the FAI business sold into the joint venture with Allianz; that attributable to the residual FAI business that would remain with HIH; and other goodwill (in particular, goodwill attributed to the US business). Even though the Allianz JV will not occur until January, it provided the basis for recog-nizing goodwill in the June 2000 accounts. Thus it is important to understand how the Allianz JV is expected to affect goodwill.

The impact of the proposed Allianz joint venture can be summarized as follows:

• Value to HIH $400m ($200m cash, plus a receivable of $200 representing HIH’s valuation of their remaining 49% investment in the JV).

• Of the $400 m of value $330 m is to be charged against goodwill ($321 m against FAI and $9 m against CIC which also contributed some business to the JV), $30 m against deferred IT cost, $10 m against FITB, and $30 m against “other”.

• This will leave residual goodwill in HIH of $133 m. Of this residual, $84 m is attributable to the remaining FAI business, $22 m is attributed to Cotesworth in the UK, $23.9 m to HIH America and a small balance of residual other good-will.

As best I can reconstruct them the table below shows a rough reconciliation of the various pre and post amortization goodwill figures (rounded to nearest $million).

A) FAi gOODwill s OlD inTO The AlliAnz JV

At June 2000 (prior to but with knowledge of the Allianz JV scheduled for 1 January 2001) goodwill attributable to FAI stood at around $405 m (after amortization and the increase of $163 m in the June 2000 accounts). The Allianz transaction will move the majority of the FAI business into the JV. As noted earlier, HIH has valued the JV at $400

FAI CIC UK US Other TotalAs @ 1999 275 9 22 24 16 346Increase 99–00 139 163Amortization –33 –1 –34As @ 2000 405 9 22 24 15 475JV impact –321 –9 –330Additional amortization –12After JV 84 0 22 24 3 133

HIH Case Study on Asset R�sk (Round 3)

33

m (cash and receivables) and intends to write $321 of this value against goodwill from the FAI acquisition.

The valuation of the goodwill sold into the JV at $321 m appears on the surface to be reasonable, provided the valuation of the JV at $400 m can be sustained. The auditors accepted that figure without much analysis. They based their assessment on the charac-teristics of the deal as follows.

• The Allianz joint venture transaction (JV) involves no transfers of physical as-sets or liabilities.

• Under the JV HIH will contribute business with a premium income of approxi-mately $1 billion (virtually all of the old FAI retail business) and Allianz would contribute similar business with a premium income of $400 m. HIH will retain a 49% share in a business with a total premium income of $1.4 billion.

• Since Allianz was to pay HIH $200 m for the excess premiums that it was con-tributing, with an option to purchase the other half for between $125 m and $500 m, the implicit “value” of the total (FAI) business should be somewhere between $325 m and $700 m. The figure of $400 m chosen by HIH does not seem inappropriate.

• Since no assets or liabilities will be transferred, the value of $400 m put on the total business should largely represent goodwill.

Thus, in their opinion, value was determined by a market transaction, and they did not need to rely on forecasts of recoverability.

I see no reason to dispute this assessment provided our own analysis of the JV does not produce a materially different assessment of value.

b) r es iDuAl FAi gOODwill

The residual FAI goodwill effectively arises because of the increased recognition of $163 m of goodwill attributable to FAI in the 2000 accounts. This has come under intense criticism by the market and the media. It conveys the impression that HIH artificially used the Allianz joint venture to justify writing up goodwill to mask an otherwise disap-pointing profit outcome.

The justification for the write-up relies on AASB 1013, clause 7.1, which states that:

Where it becomes known, subsequent to acquisition, that assets or liabilities existed at the date of acquisition but were not recognized, an adjustment must be made in respect of those assets and liabilities and, where relevant, in respect of the amount of goodwill or discount on acquisition. A similar adjustment must also be made where

Insurance Superv�s�on Core Curr�culum

3�

assets and liabilities which were unidentifiable at acquisition subsequently become identifiable.

A substantial proportion of the increase in the carrying value of goodwill at cost between 30 June 1999 and 30 June 2000 was attributable to what the auditors described as “additional pre-acquisition claims deterioration that had been identified as a result of management or actuarial reviews”. They concluded that this accounting treatment was in accordance with clause 7.1 and further stated that given the large parts of FAI’s business that went into run-off shortly after acquisition by HIH, the identification of deterioration as having been “pre-acquisition” was relatively simple.

The auditors argued that, once it is established that the liabilities existed but were not recognized or capable of identification at the date of acquisition and that the good-will balance was considered to be recoverable, then the additional excess of cost over the cost of acquisition represented by these additional liabilities was required to be ac-counted for as goodwill.

Our internal accounting experts have a different opinion. They argue that once assets and liabilities have been measured at their fair values at the date of acquisition, any subsequent re-assessment of the fair values should not be adjusted against goodwill but instead should be recognized immediately in the profit and loss statement as an expense.

Unfortunately, AASB 1013 is unclear and is applied differently by different accoun-tants.

The critical issue is therefore whether or not the residual FAI goodwill of $84 m can reasonably be assessed as recoverable from the profits from that residual business.

In assessing recoverability the auditors relied on a set of forecasts prepared by HIH. These had the appearance of working backwards from the desired result to the needed forecasts in that they contained an unexplained mixture of past actual and forecast budget figures—whichever was the more favourable.

Notwithstanding their reliance on HIH’s forecasts documents created by the audit firm at or about the time of completion of the 2000 audit raised concerns as to HIH’s ability to achieve income and cash flow forecasts and limitations of the budgetary pro-cess. These included:

• An internal report dated 24 October 2000 (eight days after the signing of the audit report in respect of the HIH 2000 accounts) which assessed HIH’s ability to achieve income and cash flow forecasts as “very poor”. This assessment had been downgraded from “poor” in the previous report dated 29 August 2000.

• A management letter prepared by the auditors to HIH after completion of the 30 June 2000 audit, which noted that “in each year of the past 6 years HIH has missed its budgeted result by a significant margin and has had to rely on major reinsurance and other transactions to recover the position. This approach is not

HIH Case Study on Asset R�sk (Round 3)

35

sustainable and some fundamental reforms are required to address the limita-tions of the current budgeting process.”

It was clear to us that the auditors held and expressed the view that HIH’s budgets were systematically unreliable and did not provide adequate support for the goodwill booked.

The reality is that by far the best parts of the FAI business will be sold into the JV. The FAI businesses not sold to Allianz contributed core earnings losses of approxi-

mately $22 m in the year ending 30 June 2000. If the businesses which contributed to that loss were in run-off and their liabilities had been sufficiently provided for, that fact would not preclude the recognition of goodwill in respect of the remaining businesses. However, that was not the case; HIH had not withdrawn from those lines of business.

In view of the lack of substantiation and the obvious reservations of the auditors I believe that the $84 m of goodwill attributed to the residual FAI business in the June 2000 accounts is highly unlikely to be recoverable and should be written off.

C) us g OODwill

The whistleblower document raises questions about any goodwill attributable to the US business. In view of the losses sustained in that business we were inclined to agree that a strong justification would be needed to sustain the June 2000 figure of $23.9 m (unamortized – around $20 m amortized).The minutes of a meeting of the audit committee held on 12 September 2000 recorded that:

Mr Fodera (HIH) tabled an analysis of the goodwill account ($133.2 m) after the Allianz transaction. There was discussion as to whether the goodwill associated with the purchase of the US operations should be written off. It was concluded that the US goodwill figure could be substantiated on budgeted future profits, especially once claims inflation reduced to more normal levels. Amongst other options, a sale of the US operations was being contemplated. However no firm commitment had been made.

At a subsequent meeting of the audit committee on 12 October the auditors pre-pared a memorandum for the files which made the following comments in respect of US goodwill:

We advised the Committee that we had identified a number of material adjustments and had used the general reserve of $40m to absorb the adjustments. Hence no gen-eral provisions now exist. We also advised that we had also offset a write down in US

Insurance Superv�s�on Core Curr�culum

3�

goodwill of $20m against a further write up of the FAI goodwill as we could find no support for the carrying value of the US goodwill.

At best, this suggests that the auditors will write down the US goodwill figure in the next set of accounts (worryingly, they appear to be content to write up residual FAI goodwill to avoid having any net impact on P&L). At worst it suggests that they thought the adjustment had been made in the June 2000 accounts but failed to follow up to en-sure that the changes were made. In either case it is sub-standard work by the auditors.On the basis that the US operations have been making consistent losses, there is no sustainable basis for maintaining US goodwill—a proposition that appears to have been accepted by the auditors. It follows that the amount of the goodwill attributable to the US operations ($23.9 m as at June 2000) ought to have been written off.

Senior Manager

HIH Case Study on Asset R�sk (Round 3)

3�

Attachment 7

Memorandum

The Allianz Transaction—Danger Signs

The key elements of the Allianz transaction were detailed in the note following the an-nouncement of HIH’s June 2000 financial results. In very brief terms:

• Each company is to transfer its personal lines and compulsory third party insur-ance products into the joint venture, with Allianz also transferring some com-mercial lines.

• HIH will transfer $l billion of premium business into the JV on renewal and Al-lianz will do likewise with $400 million of similar business.

• The business will operate as an agency and risks will be underwritten by HIH group companies and Allianz on a 49%, 51% coinsured basis.

• Allianz will pay HIH $200 million initially so as to “provide for the imbalance of premium contributed”.

• Allianz will have an option to buy out the remaining 49% at the end of five years for an amount based on an independent market valuation of the business, but subject to a guaranteed minimum of $125 million.

• At any time in the period before the five years expires, HIH has the option to “put” its 49% share to Allianz subject to the $125 million floor valuation.

Apparent Attraction for HIH

The joint-venture proposal appears attractive to HIH. It should provide the group with restructure that should resolve a number of concerns that had arisen during 2000. The biggest of these is the high proportion of intangibles in the group’s balance sheet. Our proposed reforms to insurance licensing regulations would effectively require HIH to convert a significant amount of these intangible assets into tangible assets. The Allianz joint venture offers HIH that opportunity. It would also provide HIH with a $200 mil-lion cash injection, that being the sum payable by Allianz “up front” for the purchase of HIH’s retail lines.

Two Concerns

While the transaction appears superficially attractive, a closer investigation of the docu-mentation reveals that the transaction may have a profound negative impact on HIH: first, there are serious doubts in our mind about the viability of the residual business in

Insurance Superv�s�on Core Curr�culum

3�

HIH; second, the transaction has a hidden element that has received no public airing and which could adversely affect HIH’s cash flow position. It is not clear to us that HIH is aware of this possibility.

One of the attractions of the JV to HIH is the access that it supposedly gives the company to cash, through the up-front payment of $200m from Allianz. Under the terms of the agreement HIH will retain responsibility for liabilities arising out of busi-ness written prior to the commencement of the joint venture. The agreement also re-quires the creation of a claims provision trust into which HIH must place high-quality assets equal to its claims liabilities under in-force policies. These assets amount to ap-proximately $500 million. A quick review of HIH’s balance sheet suggests that meeting this requirement will need all of the $200m it will receive in cash.

To compound matters HIH will not have access to any of the premium income from the JV for some time. Premium income to which HIH is entitled will be paid into the claims provision trust fund with the release of the money from the fund to occur at quarterly intervals and only if there is sufficient money over required provisions. For the March and September quarters, the required provisions are to be determined within sixty days after the end of the period to enable an actuarial valuation to be undertaken. This means that for the first three months of 2001, all of HIH’s cash flow from premium income earned from the joint-venture business is to be withheld. No release of funds will be made until after the actuarial valuation has been completed. This means HIH cannot reasonably expect distributions from the trust until late May 2001 at the ear-liest.

It was exacerbated by the fact that HIH did not have assets worth $500 million to contribute to the claims provision trust as required. As a result, the $200 million in sale proceeds which otherwise would have been received from Allianz was required to be placed into the trust and was not available to meet the pressing cash flow needs of HIH. An amendment agreement was executed in November to provide for direct payment of the $200 million into the trust.

Thus HIH will not only have its most liquid assets tied up in the trust, it will be cut off from its main premium income flow—approximately $1 billion a year—until the completion of the first actuarial assessment, which could be five months or more after the start of the joint venture.

We have asked HIH to provide us with their cash flow modeling, including some severe scenario tests to see whether there is any prospect of their surviving the start-up period of the JV. I am not optimistic on what I have seen to date.

Further, while it may seem somewhat problematic in view of the potentially dam-aging liquidity problems that HIH may face under the JV, we have also begun analyzing the residual company and its prospects. We are by no means sanguine. Our analysts are looking at the claims experience of the residual company and whether the asset base is adequate to support it.

Senior Manager

HIH Case Study on Asset R�sk (Round 3)

3�

Attachment 8

MEDIA CLIPPINGS

The Aus TrAliAn, T hurs DAy 5 O CTOber 2000 www. news. COm. Au

Adler’s HIH loss-sell a sure sign that Williams must goMark WestfieldINSIDER

HIH Insurance director Rodney Adler’s sell-down of his holding in the troubled general insurer at a loss is adding to the pressures on the group’s long-time managing director, Ray Williams, to step down.

Williams has resisted calls for his resignation despite the continuing slide in the share price and a management paralysis which appears to have gripped HIH.

Adler bought HIH shares aggressively in the high 90c range in June, pushing the stock through $1, after HIH gave a weak and unconvincing statement on capital ad-equacy and earnings outlook.

The statement was revealed as irrelevant and perhaps misleading by the group’s woeful result for 2000 of $18.4 million, or about $40 million below market expectations, accompanied by the sale of 51 per cent of its household, car and compulsory third party business to Germany’s Allianz.