Highlights - TD Canada Trust · Highlights • Record cash EPS ... Total Revenues $163 $249 $243...

22

1 BANK ANK F FINANCIAL INANCIAL G GROUP ROUP THIRD THIRD Q QUARTER UARTER 1999 1999 Dan Dan Marinangeli Marinangeli Highlights • Record cash EPS of $0.66 excluding gain on sale of TD Waterhouse - up 38% from last year and 14% from last quarter (accrual EPS $0.64 - up 39% from last year) • Cash ROE 21.4% excluding gain on Waterhouse (accrual ROE 18.9%) • Transacted $US 1.0B IPO for TD Waterhouse - the largest internet related IPO in NYSE history. Resulted in gain of $CDN 1.082 Billion • Increased Tier 1 and Total Capital ratios to 8.7% and 12.1% respectively • Reduced expected full year PCL by $100MM to $300MM including $100MM special general provision 2

Transcript of Highlights - TD Canada Trust · Highlights • Record cash EPS ... Total Revenues $163 $249 $243...

1

BBANKANK F FINANCIALINANCIAL G GROUPROUP

THIRDTHIRD Q QUARTERUARTER 1999 1999

Dan Dan MarinangeliMarinangeli

Highlights

• Record cash EPS of $0.66 excluding gain on sale of TDWaterhouse - up 38% from last year and 14% from lastquarter (accrual EPS $0.64 - up 39% from last year)

• Cash ROE 21.4% excluding gain on Waterhouse (accrualROE 18.9%)

• Transacted $US 1.0B IPO for TD Waterhouse - the largestinternet related IPO in NYSE history. Resulted in gain of$CDN 1.082 Billion

• Increased Tier 1 and Total Capital ratios to 8.7% and12.1% respectively

• Reduced expected full year PCL by $100MM to $300MMincluding $100MM special general provision

2

2

ROE Cash Basis*

10

15

20

25

Q1/97

Q2/97

Q3/97

Q4/97

Q1/98

Q2/98

Q3/98

Q4/98

Q1/99

Q2/99

Q3/99

Cash Basis ROEAccrual Basis ROE

* Cash basis measurement is based on excluding goodwill effect from both earnings and capital. Data adjusted to exclude extraordinary items.

%

Fiscal 1998 = 17.4%

Fiscal 1997 = 19.0%

3

Cash EPS Growth

Base = Q1/98

5060708090

100110120130140150

Q1 98 Q2 98 Q3 98 Q4 98 Q1 99 Q2 99 Q3 99

TD 4 Peer Average

4

*

*Q3/99 peer average based on adjusted consensus analyst estimates

3

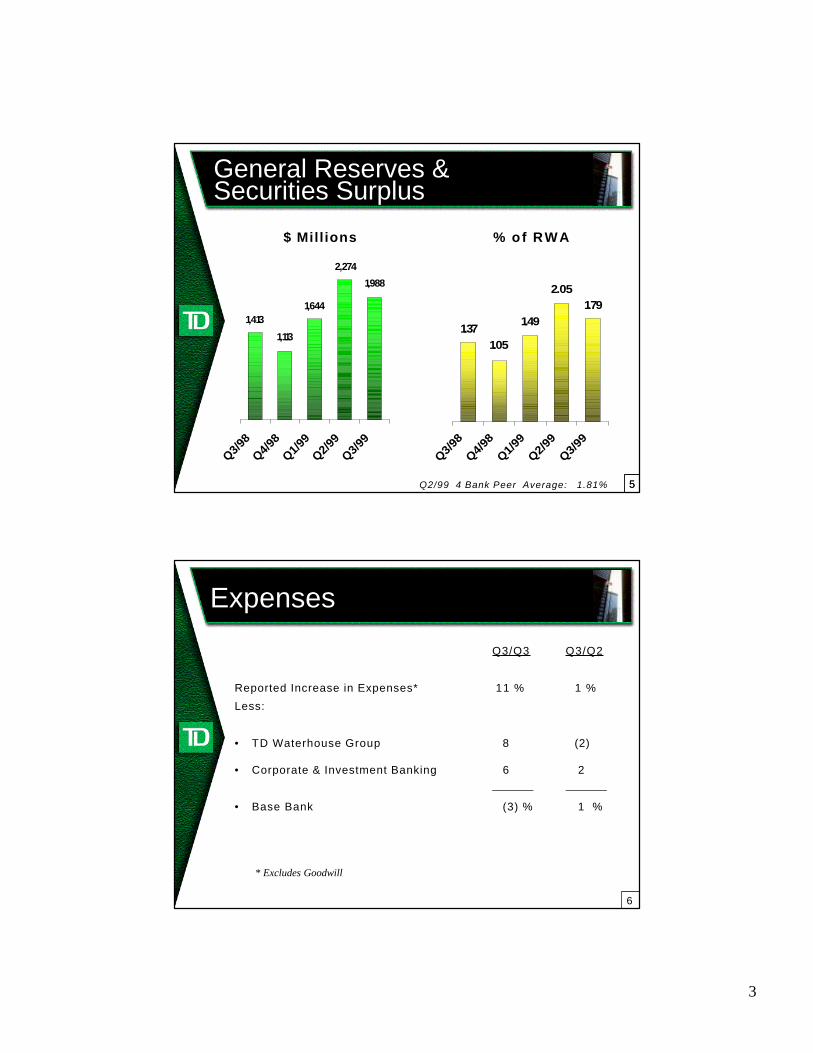

General Reserves &Securities Surplus

1.792.05

1.49

1.051.37

Q3/98

Q4/98

Q1/99

Q2/99

Q3/99

% of RWA

1,988

2,274

1,644

1,113

1,413

Q3/98

Q4/98

Q1/99

Q2/99

Q3/99

$ Mill ions

Q2/99 4 Bank Peer Average: 1.81% 55

Expenses

Q3/Q3 Q3/Q2

Reported Increase in Expenses* 11 % 1 %

Less:

• TD Waterhouse Group 8 (2)

• Corporate & Investment Banking 6 2

• Base Bank (3) % 1 %

* Excludes Goodwill

6

4

12

3

THREE GROWTH STRATEGIES

Invest in wealthmanagementbusinesses

Reposition retailbanking network

Focus corporate andinvestment banking

businesses

Wealth Management Segment vsTD Waterhouse Group

Wealth Management Segment - TD Bank comprised of:

• TD Waterhouse - global discount brokerage

• TD Investments - investment management

• Mutual Funds - Canadian fund operations

Wealth Management/Discount Brokerage segment resultsdiffer from the public company TD Waterhouse Groupresults because:

• $CDN versus $US

• Minority interest of 11.5%

• Goodwill adjustments

• U.S. GAAP accounting for option expense

• Knight/Trimark shares not owned by TD Waterhouse Group

8

5

Wealth Management

$1,485

$298$403* $403*

$471

Q3/98 Q2/99 Q3/99

Revenue$ Millions

$93

$52* $37

$1,130

$48*

Q3/98 Q2/99 Q3/99

Net Income$ Millions

* Excludes gains, restated for transfer of Private Client business to P&C9

0

100

200

300

400

500

Q3/98 Q4/98 Q1/99 Q2/99* Q3/99

Fund Services

TD Investments

Mutual Funds

TD Waterhouse:Other

TD Waterhouse:Canada

TD Waterhouse:USA

Wealth ManagementRevenue by Component

$ Millions

*Excludes gains10

6

0

50

100

150

200

250

Q2/97

Q3/97

Q4/97

Q1/98

Q2/98

Q3/98

Q4/98

Q1/99

Q2/99

Q3/99

TD Investments

Mutual Funds

TD Waterhouse:Other

TD Waterhouse:Canada

TD Waterhouse:USA

$ Billions

Wealth ManagementAssets Under Administration

11

April 30April 30 July 31July 31 ChangeChangeJuly 31July 31

19981998 19991999 Yr/YrYr/Yr

($US Millions)

Commission/Fees $106 $177 $155 47%

Other Revenue 57 72 88 53%

Total Revenues $163 $249 $243 49%

Total Expenses 136 194 194 43%

Net Income $ 13 $ 30 $ 26 104%

EPS (Diluted) $0.04 $0.09 $0.08 94%

TD Waterhouse Group

12

7

TD Waterhouse Group

Active Accounts (000) 1,485 1,884 2,066 39%

New accounts (000) 125 253 169 35%

Trades/day (000) 58 118 109 86%

Online penetration 45% 59% 64% 43%

Customer Assets($B) $74 $106 $113 51%

April 30April 30 July 31July 31 ChangeChangeJuly 31July 31

19981998 19991999 Yr/YrYr/Yr

13

($US)

Mutual Funds - Canada

$4

$6

$8

$10

$12

$14

$16

$18

Q3/97

Q1/98

Q3/98

Q1/99

Q3/99

4%

5%

6%

Canada Waterhouse Cdn M.F. Industry Mkt. Share to June/99

$ BillionsWAF: 1.12% 1.16% 1.19% 1.17% 1.13% 1.14% 1.12% 1.12%WAF: 1.12% 1.16% 1.19% 1.17% 1.13% 1.14% 1.12% 1.12%

14

8

12

3

THREE GROWTH STRATEGIES

Reposition retailbanking network

Invest in wealthmanagementbusinesses

Focus corporate andinvestment banking

businesses

$794 $779$819

Q3/98 Q2/99 Q3/99

Revenue$ Millions

$139

$101$104

Q3/98 Q2/99 Q3/99

Net Income$ Millions

Personal & Commercial Bank

* Restated to include transfer of Private Client group16

9

Personal and CommercialBanking Margin

2.50%

3.00%

3.50%

4.00%

Q3 98 Q4 98 Q1 99 Q2 99 Q3 99

17

Residential Mortgages

$ Billions

$24

$27

$30

$33

$36

$39

Q3/97 Q1/98 Q3/98 Q1/99 Q3/9913%

14%

15%

Volume Cdn. Bank Mkt. Share to June/99

Insured mortgages

Q3/99: 74 %

Q3/98: 73 %

Note: Data includes securitized mortgages.

8% year over year growth

18

10

$6

$8

$10

$12

$14

$16

Q3/97 Q1/98 Q3/98 Q1/99 Q3/99

10%

11%

12%

13%

Volume Cdn. Bank Mkt. Share to June/99

$ Billions

Note: Data includes securitized loans.

9% year over year growth

Personal Loans & Cards(Canadian Currency)

19

Personal Deposits(Canadian Currency)

$36

$37

$38

$39

$40

$41

$42

Q3/97 Q1/98 Q3/98 Q1/99 Q3/9912%

13%

14%

Volume Cdn. Bank Mkt. Share to June/99

$ Billions 7% year over year growth

20

11

Electronic Banking

15%

30%

45%

Q1 97 Q3 97 Q1 98 Q3 98 Q1 99 Q3 9910

10.5

11

11.5

12

12.5

13

Web & Telephone BankingCounter Transactions (MM's)

Web and telephone banking customers as a % penetrationof TD households vs number of counter transactions

40% penetration and 1.7MM customers (181M web and 1.5MM telephone)21

12

3

THREE GROWTH STRATEGIES

Reposition retailbanking network

Invest in wealthmanagementbusinesses

Focus corporate andinvestment banking

businesses

12

$573

$744$623

$544*

Q3/98 Q2/99 Q3/99

$ Millions

Corporate & InvestmentBanking: Revenue

*Excludes special gains

23

$163

$258

$192

$150*

Q3/98 Q2/99 Q3/99

Net Income$ Millions

20%

16%

26%

15%*

Q3/98 Q2/99 Q3/99

ROE%

* Excludes special gains

Corporate & InvestmentBanking

24

13

Capital Allocated

1996 1997 1998 1999 YTD

Other Personal & Commercial Banking

Wealth Management Corporate & Investment Banking

Retail 45%

Wholesale

55%

Retail50%*

Wholesale

50%

Goal(2001)

40%

60%

*Other Capital included in Retail

25

BBANKANK F FINANCIALINANCIAL G GROUPROUP

Q3 1999Q3 1999Risk ManagementRisk Management

Tom SpencerTom Spencer

14

Strong Asset Quality

0.00

0.20

0.40

0.60

0.80

1.00

1994 1995 1996 1997 1998 Q1/99 Q2/99 Q3/99

TD 4 Bank Peer

%

Ratio of PCL to Loans & BAs

Notes: Excludes special general provisions and reverse repos.

10 bps*

27*1999 full year estimate for PCL to loans and BA’s at July 31/99 20 bps

General Reserves &Net Impaired Loans

0.18

0.39

0.610.67 0.67 0.68

1996 1997 1998 Q1 99 Q2 99 Q3 991996 1997 1998 Q1 99 Q2 99 Q3 99

$ Millions

Q2 99 4 Bank Peer Average: 0.61%

Net Impaired Loans $(411)million

$636

General Reservesas a % of RWA

$402

$159

$744 $740 $749

28

15

$0

$250

$500

$750

$1,000

$1,250

$1,500

1993 1994 1995 1996 1997 1998 Q2/99Q3/990%

1%

2%

3%

4%

$ Millions

BUSINESS & GOVERNMENT

As a % of Loans & BA’s

Net Impaired Loans(before General Reserves)

61 bps

29

Asian ExposureGross Outstanding Loans and other Credit Exposures

Millions of Canadian DollarsJuly 31, 1999

Country

China *Hong KongIndonesiaMalaysiaPhilippinesSingaporeSouth KoreaTaiwanThailandSub-total

Japan

Total

Sovereign

8

14166

188

2,553

$2,741

Banks

64 36 26 4 3 168 70 30 401

68

$469

Commercial& Industrial

55 166 45 46 7 547 8 874

1,397

$2,271

Total

65 100 195

49 63 341 617 38 1,468

4,140

$5,608

Mark toMarket

1 1 3

5

122

$127* We have no exposure to International Trusts and Investment Corporations.

TotalApr./99

55 94 230 2 65 61 141 728 36 1,412

3,514

$4,926

30

16

Latin American ExposureGross Outstanding Loans and other Credit Exposures

Millions of Canadian DollarsJuly 31, 1999

Country

ArgentinaBrazilChileColombiaMexicoPeruAll Other

Total

Banks

153 122 133 129 327 17 23

$904

Commercial& Industrial

223 28 160 15 131 67

$624

Mark toMarket

$0

Total

376 150 293 144 458 17 90

$1,528

TotalApr./99

491 85 309 150 403 30 43

$1,512

31

BBANKANK F FINANCIALINANCIAL G GROUPROUP

Q3 1999Q3 1999

Bob KellyBob KellyVice Chair, Retail BankingVice Chair, Retail Banking

An overview of TD WaterhouseAn overview of TD WaterhouseNational BankNational Bank

17

TD WaterhouseNational Bank

• TD’s original purchase of Waterhouse

included a national US banking license.

• Original purpose of the bank was to house

“Investor’s Money Market” accounts.

• NOW : a fully functional electronic bank

available to both US and Canadian

customers.

BackgroundBackground

33

TD WaterhouseNational Bank

• Sell Banking services to 1.9 million TD

Waterhouse U.S. investing customers.

• Provide cross-border electronic banking

services to Canadian customers.

• Integrate banking/brokerage services on

both sides of the border.

• Identify profitable customer segments to

build further banking presence in U.S.

StrategyStrategy

34

18

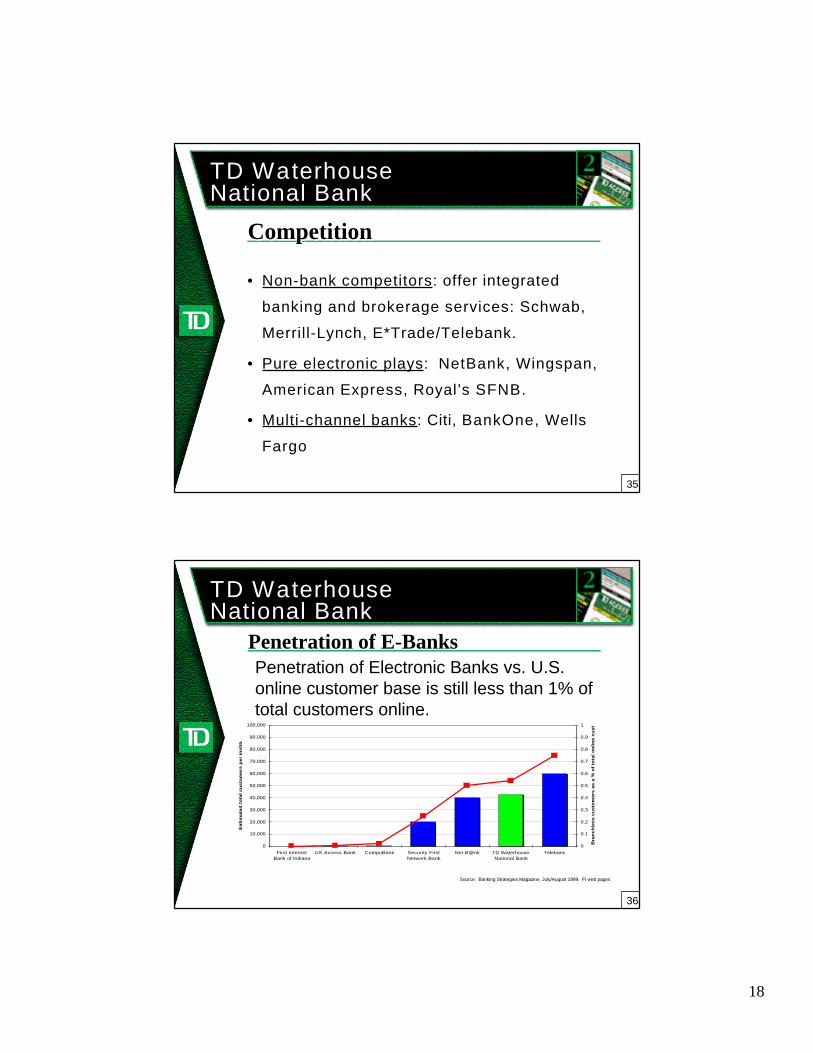

TD WaterhouseNational Bank

• Non-bank competitors: offer integrated

banking and brokerage services: Schwab,

Merrill-Lynch, E*Trade/Telebank.

• Pure electronic plays: NetBank, Wingspan,

American Express, Royal’s SFNB.

• Multi-channel banks: Citi, BankOne, Wells

Fargo

CompetitionCompetition

35

TD WaterhouseNational Bank

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

100,000

First InternetBank of Indiana

US Access Bank CompuBank Security FirstNetwork Bank

Net.B@nk TD WaterhouseNational Bank

Telebanc

Ea

tim

ate

d t

ota

l c

us

tom

ers

pe

r in

sti

tuti

on

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1

Bra

nc

hle

ss

cu

sto

me

rs a

s a

% o

f to

tal

on

lin

e c

us

tom

ers

Penetration of E-Banks Penetration of E-Banks Penetration of Electronic Banks vs. U.S.online customer base is still less than 1% oftotal customers online.

Source: Banking Strategies Magazine, July/August 1999, FI web pages

36

19

TD WaterhouseNational Bank

• Growing TD Waterhouse customer base, of

which 837,000 are now on-line.

• Integration of Bank and Broker on both

sides of the border

• TDW branch network.

• TD Waterhouse brand

• Canadian E-Banking know-how.

Competitive Advantages:Competitive Advantages:

37

TD WaterhouseNational Bank

0

500

1,000

1,500

2,000

ac

co

un

ts (

00

0)

1996 1997 1998 q3/99

TWE accounts (US)

TWE accounts online(US)

WNB accounts

The opportunity is signficantThe opportunity is signficantTWE Customer Accounts showing penetrationof Online and Banking accounts. TD WNBaccounts represent 5% of target population.

38

20

TD WaterhouseNational Bank

• A Complete product suite:

• Credit cards

• ATM/Check cards

• checking accounts

• secured and unsecured lines of credit

• mortgages.

What we have built to date:What we have built to date:

39

TD WaterhouseNational Bank

• Fully functional phone support (based in Canada),

• Web Banking offering transactions, product

applications and bill payment,

• Marketing Web site with l inks to TWE Web Broker

and to TD.

• Funds transfer between TD and WNB.

• Coming this month: funds transfer on the Web

between Bank and Broker in the US.

• Partnership with TWE Branch network.

A complete set of Channels:A complete set of Channels:

40

21

TD WaterhouseNational Bank

• Sept. launch in conjunction with TD Waterhouse.

• More complete banking product suite,

incorporating the “Open Finance” model: a

commitment to provide“best of breed” banking

offers from other providers.

• Continued integration between bank and

brokerage, US and Canada.

• Loyalty Plan.

• Identify new profitable customer segments.

Next Steps:Next Steps:

41

Forward Looking Statements

42

This document may contain forward-looking statements, includingstatements regarding the business and anticipated financialperformance of TD. These statements are subject to a number ofrisks and uncertainties that may cause actual results to differmaterially from those contemplated by the forward-lookingstatements. Some of the factors that could cause such differencesinclude legislative or regulatory developments, competition,technological change, global capital market activity, interest rates,inflation and general economic conditions in geographic areas whereTD operates. Also, additional risk factors relating to the pendingacquisition of CT Financial Services Inc. are described in TD'sReport on Form 6-K, filed with the U.S. Securities and ExchangeCommission on August 3, 1999 and TD's Material Change Report,filed with the Ontario Securities Commission on August 3, 1999.

22

BBANKANK F FINANCIALINANCIAL G GROUPROUP

THIRDTHIRD Q QUARTERUARTER 1999 1999