Highlights for May 2021 Exams

39

CA Final Audit – Highlights for May 2021 Exams 1 Highlights for May 2021 Exams

Transcript of Highlights for May 2021 Exams

CA Final Audit – Highlights for May 2021 Exams

1

Highlights for

May 2021 Exams

CA Final Audit – Highlights for May 2021 Exams

2

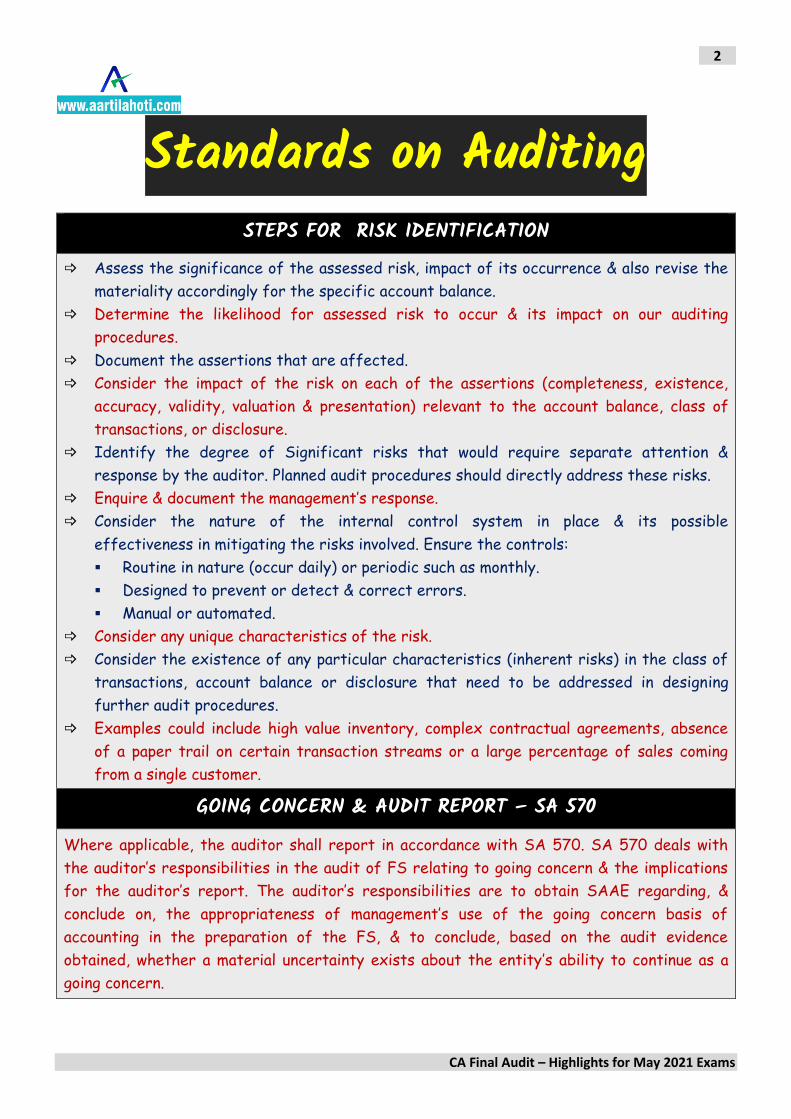

Standards on Auditing

STEPS FOR RISK IDENTIFICATION Assess the significance of the assessed risk, impact of its occurrence & also revise the

materiality accordingly for the specific account balance.

Determine the likelihood for assessed risk to occur & its impact on our auditing

procedures.

Document the assertions that are affected.

Consider the impact of the risk on each of the assertions (completeness, existence,

accuracy, validity, valuation & presentation) relevant to the account balance, class of

transactions, or disclosure.

Identify the degree of Significant risks that would require separate attention &

response by the auditor. Planned audit procedures should directly address these risks.

Enquire & document the management’s response.

Consider the nature of the internal control system in place & its possible

effectiveness in mitigating the risks involved. Ensure the controls:

▪ Routine in nature (occur daily) or periodic such as monthly.

▪ Designed to prevent or detect & correct errors.

▪ Manual or automated.

Consider any unique characteristics of the risk.

Consider the existence of any particular characteristics (inherent risks) in the class of

transactions, account balance or disclosure that need to be addressed in designing

further audit procedures.

Examples could include high value inventory, complex contractual agreements, absence

of a paper trail on certain transaction streams or a large percentage of sales coming

from a single customer.

GOING CONCERN & AUDIT REPORT – SA 570

Where applicable, the auditor shall report in accordance with SA 570. SA 570 deals with

the auditor’s responsibilities in the audit of FS relating to going concern & the implications

for the auditor’s report. The auditor’s responsibilities are to obtain SAAE regarding, &

conclude on, the appropriateness of management’s use of the going concern basis of

accounting in the preparation of the FS, & to conclude, based on the audit evidence

obtained, whether a material uncertainty exists about the entity’s ability to continue as a

going concern.

CA Final Audit – Highlights for May 2021 Exams

3

RELATIONSHIP BETWEEN EMPHASIS OF MATTER PARAGRAPHS & KEY AUDIT MATTERS IN THE AUDITOR’S REPORT

KEY AUDIT MATTER EMPHASIS OF MATTER Key audit matters - Those matters that, in

the auditor’s professional judgment, were of

most significance in the audit of the FS of

the current period. Key audit matters are

selected from matters communicated with

those charged with governance. [SA 701]

Emphasis of Matter paragraph - A paragraph

included in the auditor’s report that refers

to a matter appropriately presented or

disclosed in the FS that, in the auditor’s

judgment, is of such importance that it is

fundamental to users’ understanding of the

FS. [SA 706]

Matters that are determined to be key audit

matters in accordance with SA 701 may also

be, in the auditor’s judgment, fundamental to

users’ understanding of the FS. In such

cases, in communicating the matter as a key

audit matter in accordance with SA 701, the

auditor may wish to highlight or draw

further attention to its relative importance.

Communicating key audit matters provides

additional information to intended users of

the FS to assist them in understanding those

matters that, in the auditor’s professional

judgment, were of most significance in the

audit & may also assist them in understanding

A widespread use of Emphasis of Matter

paragraphs may diminish the effectiveness

of the auditor’s communication about such

matters.

Use of Emphasis of Matter paragraphs is not

a substitute for a description of individual

key audit matters where SA 701 is

applicable.

There may be a matter that is not

determined to be a key audit matter in

accordance with SA 701 (i.e., because it did

not require significant auditor attention), but

which, in the auditor’s judgment, is

fundamental to users’ understanding of the

CA Final Audit – Highlights for May 2021 Exams

4

the entity & areas of significant management

judgment in the audited FS.

FS (e.g., a subsequent event). If the auditor

considers it necessary to draw users’

attention to such a matter, the matter is

included in an Emphasis of Matter paragraph

in the auditor’s report in accordance with

this SA.

The communication of key audit matters in

the auditor’s report may also provide

intended users a basis to further engage

with management & those charged with

governance about certain matters relating to

the entity, the audited FS, or the audit that

was performed.

The auditor may do so by presenting the

matter more prominently than other matters

in the Key Audit Matters section (e.g., as the

first matter) or by including additional

information in the description of the key

audit matter to indicate the importance of

the matter to users’ understanding of the

FS.

Professional Ethics OVERVIEW OF THE CODE OF ETHICS

Part 1 Complying with the Code, Fundamental Principles & Conceptual Framework, which includes the fundamental principles & the conceptual framework & is applicable to all professional accountants.

Part 2 Professional Accountants in Service, which sets out additional material that applies to professional accountants in service when performing professional activities. Professional accountants in service include professional accountants employed, engaged or contracted in an executive or non-executive capacity in, for example:

Commerce, industry or service. The public sector. Education. The not-for-profit sector. Regulatory or professional bodies.

It is also applicable to individuals who are professional accountants in public practice when performing professional activities pursuant to their relationship with the firm as an employee.

Part 3 Professional Accountants in Public Practice, which sets out additional material that applies to professional accountants in public practice when providing professional services.

Independence Standards, which sets out additional material that applies to professional accountants in public practice when providing assurance services, as follows:

CA Final Audit – Highlights for May 2021 Exams

5

Part 4A Independence for Audit & Review Engagements, which applies when performing audit or review engagements.

Part 4B Independence for Assurance Engagements Other than Audit & Review Engagements, which applies when performing assurance engagements that are not audit or review engagements.

THREATS, EVALUATION OF THREATS & SAFEGUARDS

THREATS TO INDEPENDENCE

SELF-INTEREST THREATS SELF-REVIEW THREATS ADVOCACY THREATS FAMILIARITY THREATS INTIMIDATION THREATS

EVALUATION OF THREATS

Acceptable level The conditions, policies & procedures described above might impact the evaluation of whether a threat to compliance with the fundamental principles is at an acceptable level.

An acceptable level is a level at which a professional accountant using the reasonable & informed third party test would likely conclude that the accountant complies with the fundamental principles.

Reasonable & Informed Third Party (RITP)

The reasonable & informed third party test is a consideration by the professional accountant about whether the same conclusions would likely be reached by another party.

Such consideration is made from the perspective of a reasonable & informed third party, who weighs all the relevant facts & circumstances that the accountant knows, or could reasonably be expected to know, at the time the conclusions are made.

The reasonable & informed third party does not need to be an accountant but would possess the relevant knowledge & experience to understand & evaluate the appropriateness of the accountant’s conclusions in an impartial manner.

MEMBERS WHO ARE DEEMED TO BE IN PRACTICE [SECTION 2(2)] The expression “other services” include “Management consultancy & other services”.

The expression Management Consultancy & Other Services shall not include the function of statutory or periodical audit, tax (both direct taxes & indirect taxes) representation or advice concerning tax matters or acting as liquidator, trustee, executor, administrator, arbitrator or receiver, but shall include the following:

Financial management planning & financial policy determination* Capital structure planning & advice regarding raising finance*

CA Final Audit – Highlights for May 2021 Exams

6

Working capital management* Preparing project reports & feasibility studies*

* (Consideration of “tax implications” while rendering the above services will be considered as part of “Management Consultancy & other services”.)

Acting as Registered Valuer under the Companies Act, 2013 read with the Companies (Registered Valuers & Valuation) Rules, 2017.

Acting as Insolvency Professional in terms of Insolvency & Bankruptcy Code, 2016

Administrative Services. Administrative Services involve assisting clients with their routine or

mechanical tasks within the normal course of operations. Such services require little to no

professional judgment & are clerical in nature. Examples of administrative services include –

(a) Word processing services.

(b) Preparing administrative or statutory forms for client approval.

(c) Submitting such forms as instructed by the client.

(d) Monitoring statutory filing dates, & advising an audit client of those dates.

For example, the functions of a GST practitioner as specified under Rule 83(8) of Central Goods & Services Tax Rules, 2017 –

furnish the details of outward & inward supplies

furnish monthly, quarterly, annual or final return

making deposit for credit into the electronic cash ledger

file a claim for refund

file an application for amendment or cancellation of registration

furnish information for generation of e-way bill

furnish details of challan in form GST ITC-04

file an application for amendment or cancellation of enrollment under rule 58 &

file an intimation to pay tax under the composition scheme or withdraw from the said scheme.

MEMBER IN PRACTICE PROHIBITED FROM USING A DESIGNATION OTHER THAN CHARTERED ACCOUNTANT [SECTION 7]

Directors of Companies, Members of political parties, position in clubs, etc.

The members of the Institute who are also Directors in Companies, members of Political parties or CAs Cells in the political parties, holding different positions in clubs or other organisations are not permitted to mention these positions as these would be violative of the provisions of Section 7 of the Act.

Members who are also Cost Accountants

Though a member cannot designate himself as a Cost Accountant, he can use the letters A.C.M.A (Associate) or F.C.M.A (Fellow) after his name, when he is a member

of that Institute.

Permission to mention qualifications of

The members are permitted to mention membership of a foreign Institute of Accountancy, which has been recognized by the Council through a Memorandum of

Understanding (MoU)/Mutual Recognition Agreement (MRA) with the said Institute.

CA Final Audit – Highlights for May 2021 Exams

7

certain Institutions CS/CMA Members of the Institute in practice who are otherwise eligible may also practice as

Company Secretaries &/or Cost Accountants. Such members shall, however, not use designation/s of the aforesaid Institute/s simultaneously with the designation “Chartered Accountant”.

MAINTENANCE OF BRANCH OFFICES (SECTION 27) Separate Charge If a CA in practice or a Firm of CAs has more than one office in India, each one

of such offices should be in the SEPARATE CHARGE OF A MEMBER OF THE INSTITUTE.

Active Association The requirement of Section 27 in regard to a member being in charge of an

office of a CA in practice or a firm of such CAs shall be satisfied only if the

member is actively associated with such office.

Such association shall be deemed to exist if the member resides in the place

where the office is situated for a period of not less than 182 days in a year or if

he attends the said office for a period of not less than 182 days in a year or in

such other circumstances as, in the opinion of the Executive Committee,

establish such active association.

CLAUSES OF ETHICS

CLAUSE (2) OF PART 1 OF FIRST SCHEDULE

Fee Payable to State Government

The Institute came across certain Circulars/Orders issued by the Registrars of various State Co-operative Societies wherein it has been mentioned that certain amount of audit fee is payable to the concerned SG & the auditor has to deposit a percentage of his audit fee in the state Treasury by a prescribed challan within a prescribed time of the receipt of Audit fee.

The Council decided that as such there is no bar in the Code of Ethics to accept such assignment wherein a percentage of professional fee is deducted by the Government to meet the administrative & other expenditure.

CLAUSE (3) OF PART 1 OF FIRST SCHEDULE

REFERRAL FEES AMONGST MEMBERS

It is not prohibited for a member in practice to charge Referral Fees, being the fees obtained by a member in practice from another member in practice in relation to referring a client to him.

CLAUSE (6) OF PART 1 OF FIRST SCHEDULE

Advertisements & notes in the press

A member is permitted to issue a classified advertisement in the journal/ newsletter of the Institute intended to give information for sharing professional work on assignment basis or for seeking partnership or salaried employment of an accountancy nature, provided it only contains the accountant’s name, address or

CA Final Audit – Highlights for May 2021 Exams

8

telephone no., fax no., e-mail address & address(es) of Social Networking sites of members. However, mere factual position of experience & area of specialization, relevant to seek response to the advertisement, are permissible.

Publication of Books, Articles or Presentation

It is not permissible for a member to mention in a book or an article published by him, or a presentation made by him, any professional attainment(s), whether of the member or the firm of CAs, with which he is associated.

However, he may indicate in a book, article or presentation the designation “CA” as well as the name of the firm.

Advertisement for Silver, Golden, Platinum or Centenary celebrations

It is not permitted to advertise the events organised by a Firm of CAs. However, considering the need of interpersonal socialization/relationship of the

members through such get together occasions, the advertisement for Silver, Golden, Diamond, Platinum or Centenary celebrations of the CAs Firms may be published in newspaper or newsletter.

Sponsoring Activities

A member in practice or a Firm of CAs is not permitted to sponsor an event. However, such member or Firm may sponsor an event conducted by a Programme Organizing Unit (PoU) of the ICAI, provided such event has the prior approval of Continuing Professional Education (CPE) Directorate of the ICAI.

Members sponsoring activities relating to Corporate Social Responsibility may mention their individual name with the prefix “CA”. However, the mention of Firm name or CA Logo is not permitted.

Sharing Firm Profile with prospective Client

It is not permitted to share Firm profile with a prospective Client unless it is in response to a proposed client’s specific query, & otherwise not prohibited to be used by the client.

Television or Movie Credits

While sharing name of the member or Firm of CAs for inclusion in Television or Movie Credits, it must be taken care of that exhibition of name is not made differently as compared to other entries in the credits.

Soliciting professional work by making roving enquiries

It is not permissible for a member to address letters, emails or circulars specifically to persons who are likely to require services of a CA since it would tantamount to advertisement.

Members &/or firms who publish advertisements under Box numbers

Members/Firms are prohibited from inserting advertisements for soliciting clients or professional work under box numbers in the newspapers. This practice is in violation of this clause.

Educational While the videos of educational nature may be uploaded on the internet by members, no reference should be made to the CAs Firm wherein the member is a

CA Final Audit – Highlights for May 2021 Exams

9

Videos partner/ proprietor. Further, it should not contain any contact details or website address.

Guidelines for posting the particulars on Website

1. Not to issue any circular or any other advertisement or any other material of any kind whatsoever by virtue of which they solicit people to visit their Website. CA can mention website address on professional stationery & email.

2. Display of Passport Style photograph is permitted.

3. Can provide link of its page on Social Networking site. However, the members should not solicit people to visit or like their respective page(s) on such social Networking site.

4. Can provide on line advice to their clients who specifically request for the advice whether free of charge or on payment.

ONLINE THIRD PARTY PLATFORMS

A number of non-CAs’ firms, corporates including banks, finance Companies & newspapers have set up their own Websites providing advisory services on taxation & other areas where CAs are rendering professional service.

Some of such Websites may request CAs or CAs’ firms to provide consultation & advice through their Websites. No other service, besides consultancy & advice can be rendered through such websites.

This would be permitted subject to the condition that on the Website, contact address of the CA concerned is not provided nor such Website will contain any material which advertises professional achievements or status of such CA except making a statement that they are CAs.

The name of CAs’ firm with suffix “Chartered Accountants” would not be permitted.

PUBLICATION OF NAME OR FIRM NAME BY CAS IN THE TELEPHONE OR OTHER DIRECTORIES PUBLISHED BY TELEPHONE AUTHORITIES OR

PRIVATE BODIES

The CAs & CAs Firms may have entries made in a Telephone Directory (in printed & electronic form) either by making a special request or by means of an additional payment. The Council has also considered the question of permitting entries in respect of CAs & their firms under specified groups in telephone/trade directories subject to the following additional restrictions: -

The entry should not appear in any other section/category except that of ‘Chartered Accountants’.

The member/firm should belong to the town/city in respect of which the directory is being published.

The order of the entries should not be in any manner other than alphabetical.

The entry should not be made in a differential or prominent manner giving the impression of publicity/advertisement.

The entries should not be restricted & should be open to all the CAs/firms of CAs in the particular city/town in respect whereof the directory is published.

The members can also include their names in trade/social directories.

APPLICATION BASED SERVICE PROVIDER AGGREGATORS

It is not permissible for members to list themselves with online application based service provider Aggregators, wherein other categories like businessmen, technicians, maintenance workers, event organizers etc. are also listed.

CA Final Audit – Highlights for May 2021 Exams

10

SPECIALISED DIRECTORIES FOR LIMITED CIRCULATION

The name, description & address of member (or firm) may appear in any directory or list of members of a particular body in which the names are listed alphabetically. For a specialised directory or a publication such as a “Who’s Who” (including those compiled on purely local basis), a member should use his discretion in supplying information, bearing in mind the nature & purpose of the publications.

In addition to his name, description & address & those of his firm, a member may give where appropriate, directorships held & reasonable personal details & may state his outside interests. He should not, however, give the names of any of his clients.

CLAUSE (7) OF PART (I) OF FIRST SCHEDULE Insolvency Professional/Registered Valuer

A member empanelled as Insolvency Professional or Registered Valuer can mention “Insolvency Professional” or “Registered Valuer” respectively on his visiting card & letter head.

Permission to mention qualifications of certain Institutions

The members are permitted to mention a title on their visiting cards to indicate membership of a foreign Institute of Accountancy, which has been recognised by the Council e.g. South African Institute of Chartered Accountants (SAICA), Institute of Certified Public Accountants (CPA Ireland) & Institute of Chartered Accountants in England & Wales (ICAEW).

Date of setting-up practice

The date of setting up the practice by a member or the date of establishment of the firm on the letter heads & other professional documents etc. should not be mentioned.

Reports & Certificates

The reports & certificates issued by a CA bring him to the notice of the public in a greater or lesser degree.

The members may however note that they should use letterhead of their Firm for issuing reports & certificates.

Appearance of Chartered Accountants on Electronic Media (including Internet)

Members may appear on television, films & Internet & agree to broadcast in the Radio or give lectures at forums & may give their names & describe themselves as CAs.

Special qualifications or specialised knowledge directly relevant to the subject matter of the programme may also be given. Firm name may also be mentioned, however, any exaggerated claim or any kind of comparison is not permissible. What he may say or write must not be promotional of him or his firm but must be an objective professional view of the topic under consideration.

Writing Articles or Letters to the Press

Members writing articles or letters to the Press on subjects connected with the profession may give their names & use the description CAs.

Size of Sign Board

With regard to the size of sign board for his office that a member can put up, it is a matter in which the members should exercise their own discretion & good taste while keeping in mind the appropriate visibility & illumination (limited to the sake

CA Final Audit – Highlights for May 2021 Exams

11

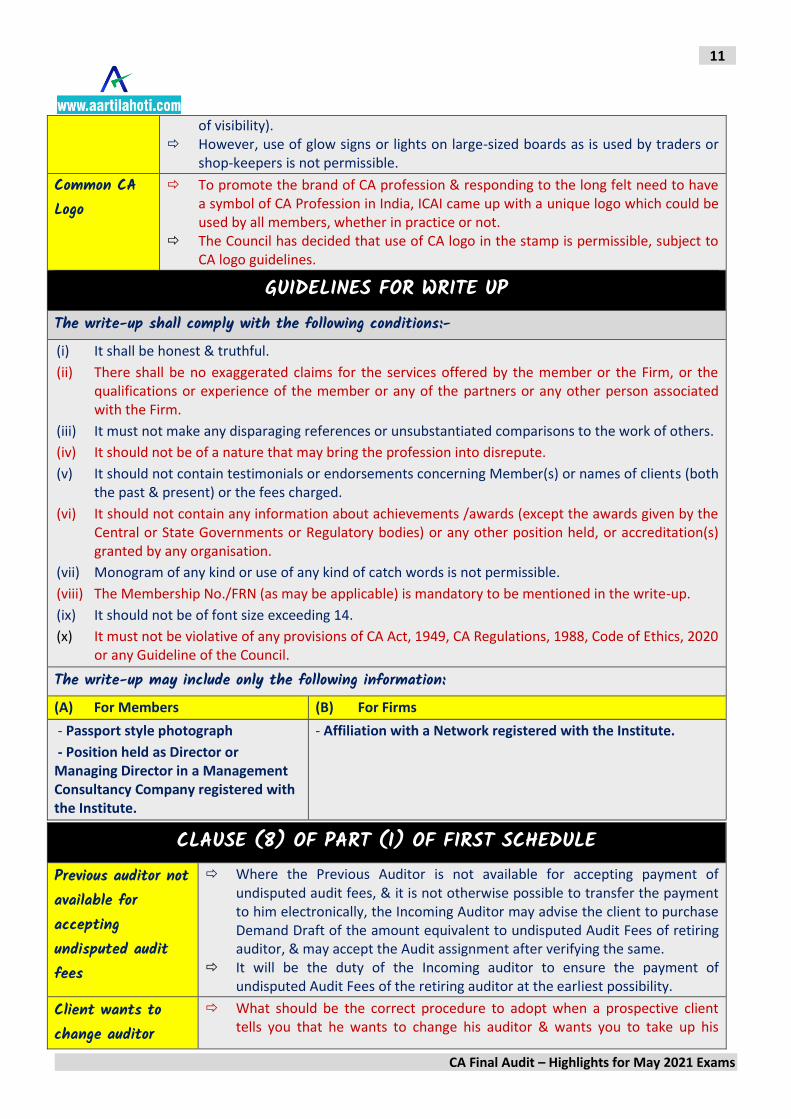

of visibility). However, use of glow signs or lights on large-sized boards as is used by traders or

shop-keepers is not permissible.

Common CA Logo

To promote the brand of CA profession & responding to the long felt need to have a symbol of CA Profession in India, ICAI came up with a unique logo which could be used by all members, whether in practice or not.

The Council has decided that use of CA logo in the stamp is permissible, subject to CA logo guidelines.

GUIDELINES FOR WRITE UP

The write-up shall comply with the following conditions:- (i) It shall be honest & truthful.

(ii) There shall be no exaggerated claims for the services offered by the member or the Firm, or the qualifications or experience of the member or any of the partners or any other person associated with the Firm.

(iii) It must not make any disparaging references or unsubstantiated comparisons to the work of others.

(iv) It should not be of a nature that may bring the profession into disrepute.

(v) It should not contain testimonials or endorsements concerning Member(s) or names of clients (both the past & present) or the fees charged.

(vi) It should not contain any information about achievements /awards (except the awards given by the Central or State Governments or Regulatory bodies) or any other position held, or accreditation(s) granted by any organisation.

(vii) Monogram of any kind or use of any kind of catch words is not permissible.

(viii) The Membership No./FRN (as may be applicable) is mandatory to be mentioned in the write-up.

(ix) It should not be of font size exceeding 14.

(x) It must not be violative of any provisions of CA Act, 1949, CA Regulations, 1988, Code of Ethics, 2020 or any Guideline of the Council.

The write-up may include only the following information: (A) For Members (B) For Firms

- Passport style photograph

- Position held as Director or Managing Director in a Management Consultancy Company registered with the Institute.

- Affiliation with a Network registered with the Institute.

CLAUSE (8) OF PART (I) OF FIRST SCHEDULE

Previous auditor not available for accepting undisputed audit fees

Where the Previous Auditor is not available for accepting payment of undisputed audit fees, & it is not otherwise possible to transfer the payment to him electronically, the Incoming Auditor may advise the client to purchase Demand Draft of the amount equivalent to undisputed Audit Fees of retiring auditor, & may accept the Audit assignment after verifying the same.

It will be the duty of the Incoming auditor to ensure the payment of undisputed Audit Fees of the retiring auditor at the earliest possibility.

Client wants to change auditor

What should be the correct procedure to adopt when a prospective client tells you that he wants to change his auditor & wants you to take up his

CA Final Audit – Highlights for May 2021 Exams

12

work? There being two persons involved, the Company & the old auditor, the

former should be asked whether the retiring auditor had been informed of the intention to change. If the answer is in the affirmative, then a communication should be addressed to the retiring auditor.

If, however, it is learnt that the old auditor has not been informed, & the client is not willing to make the first move, it would be necessary to ask him the reason for the proposed change. If there is no valid reason for a change, it would be healthy practice not to accept the audit. If he decides to accept the audit, he should address a communication to the retiring auditor.

Incoming auditor to ascertain circumstances for change in auditor

The object of the incoming auditor, in communicating with the retiring auditor is to ascertain from him whether there are any circumstances which warrant him not to accept the appointment.

Positive Evidence of Delivery

Members should therefore communicate with a retiring auditor in such a manner as to retain in their hands positive evidence of the delivery of the communication to the addressee.

In the opinion of the Council, the following would in the normal course provide such evidence:-

Communication by a letter sent through “Registered Acknowledgement due”, or

By hand against a written acknowledgement, or Acknowledgement of the communication from retiring auditor’s vide email

address registered with the Institute or his last known official email address, or

Unique Identification Number (UDIN) generated on UDIN portal.

Premises found Locked

The communication received back by the Incoming Auditor with “Office found Locked” written on the Acknowledgement Due shall be deemed as having been delivered to the retiring auditor.

Firm not found at the given Registered address

If the Communication sent by the Incoming auditor is received back with remarks "No such office exists at this address”, & the address of communication is the same as registered with the Institute on the date of dispatch, the letter will be deemed to be delivered, unless the retiring auditor proves that it was not really served & that he was not responsible for such non-service.

As a matter of professional courtesy & professional obligation it is necessary for the new auditor appointed to act jointly with the earlier auditor & to communicate with such earlier auditor.

Special Audit under Income Tax Act, 1961

It would be a healthy practice if a Tax Auditor appointed for conducting special audit under the Income Tax Act, 1961 communicates with the member who has conducted the Statutory Audit.

Communication required for all kinds of audit

The requirement for communicating with the previous auditor being a CA in practice would apply to all types of Audit viz., Statutory Audit, Tax Audit, GST Audit, Internal Audit, Concurrent Audit or any other kind of audit.

CA Final Audit – Highlights for May 2021 Exams

13

Communication in case of Assignments done by other professionals

A Communication is mandatorily required for all types of Audit/Report where the previous auditor is a CA.

In case of assignments done by other professionals not being CAs, it would also be a healthy practice to communicate.

Lack of time in acceptance of Government Audits

In the case of audit of government Companies/ banks or their branches, in case the time schedule given for the assignment is such that there is no time to wait for the reply from the outgoing auditor, the incoming auditor may give a conditional acceptance of the appointment & commence the work which needs to be attended to immediately after he has sent the communication to the previous auditor in accordance with this clause.

CLAUSE (10) OF PART (I) OF FIRST SCHEDULE

EXCEPTIONS Fee should not be regarded as being contingent if fixed by a Court or other public authority.

Regulation 192 – Exemption from clause (10)

a) any other service or audit as may be decided by the Council. [Following activities have been decided by the Council under “h” above :-(i) Acting as Insolvency Professional;(ii) Non-Assurance Services to Non-Audit Clients ]

`

CLAUSE (11) OF PART (I) OF FIRST SCHEDULE

SERVICES THAT CAN BE OFFERED (REGULATION 190A) PERMISSION TO BE GRANTED SPECIFICALLY: Members of the Institute in practice may engage in the following categories of business or occupations, after obtaining the specific & prior approval of the Council in each case: -

a Office of managing director or a whole-time director of a body corporate within the meaning of the Companies Act, 2013 provided that the member and/or any of his relatives do not hold substantial interest in such concern.

a Interest in family business concerns (including such interest devolving on the members as a result of inheritance /succession /partition of the family business) or concerns in which interest has been acquired as a result of relationships & in the management of which no active part is taken.

a Member in practice in a HUF doing business: “A member of the Institute can acquire interest in family business in any of the following manner:

- as a proprietary firm

- as a partnership firm

- in the name & style of Hindu Undivided Family as its Karta or a member.

a It would be necessary for the members to provide evidence that interest in the family business concern devolved on him as a result of inheritance/succession/partition of the family business.

a It is also necessary for the member to show that he was not actively engaged in carrying on the said business & that the family business concern in question was not created by himself.

a To establish his case, the member should furnish a declaration in the prescribed format & the documents evidencing above for consideration to the concerned Decentralized Office.”

CLAUSE (12) OF PART (I) OF FIRST SCHEDULE

CA Final Audit – Highlights for May 2021 Exams

14

Routine Documents

The Council has clarified that the power to sign routine documents on which a professional opinion or authentication is not required to be expressed may be delegated in the following instances & such delegation will not attract provisions of this clause:

(i) Issue of audit queries during the course of audit.

(ii) Asking for information or issue of questionnaire.

(iii) Letter forwarding draft observations/FS.

(iv) Initiating & stamping of vouchers & of schedules prepared for the purpose of audit.

(v) Acknowledging & carrying on routine correspondence with clients.

(vi) Issue of memorandum of cash verification & other physical verification or recording the results thereof in the books of the clients.

(vii) Issuing acknowledgements for records produced. Raising of bills & issuing acknowledgements for money receipts.

(viii) Attending to routine matters in tax practice, subject to provisions of Section 288 of Income Tax Act.

(ix) Any other matter incidental to the office administration & routine work involved in practice of accountancy.

CLAUSE (4) OF PART (I) OF SECOND SCHEDULE

Requirements of Clause applicable to all Attest Functions

The requirements of Clause (4) are equally applicable while performing all types of attest functions by the members. e.g., Tax Audit, GST Audit, Concurrent Audit of Banks, Concurrent Audit of Borrowers of Financial institutions, Audit of non-corporate borrowers of Banks & Financial Institutions, Audit of Stock Exchange, Brokers, etc.

Tax Consultant An accountant is expected to be no less independent in the discharge of his duties as a tax consultant or as a financial adviser than as auditor. In fact, it is necessary that he should bear the same degree of integrity & independence of mind in all spheres of his work.

Statutory auditor not to be the Internal Auditor simultaneously

An Auditor appointed by an entity under the Companies Act or any other statute shall not be the Internal Auditor of the same entity.

Internal auditor not to be the Tax auditor simultaneously

An Internal Auditor of an assessee, whether working with the organization or an independently practicing CA irrespective of being an individual CA or a firm of CAs cannot be appointed as its Tax Auditor.

Internal Auditor not to be the GST Auditor simultaneously

The Internal Auditor of an entity cannot undertake GST Audit of the same entity.

Cooling off period after completion

A member shall not accept the assignment of audit of a Company for a period of 2 years from the date of completion of his tenure as Director, or resignation as Director

CA Final Audit – Highlights for May 2021 Exams

15

of tenure as Director

of the said Company.

Members to satisfy whether appointment is as per the statute

A member should satisfy himself before accepting an appointment as an auditor of an entity that his appointment is in accordance with the statute governing the entity. In case the entity is constituted under a trust deed/instrument, the member should satisfy whether his appointment is valid according to the instrument constituting the entity & rules & regulations made thereunder.

In case the appointment is to be authorised by the regulatory authorities such as in the case of co-operative societies, trusts etc. then the member must satisfy whether such regulatory authorities have authorised the managing committee of the society/trust for appointment of the auditors.

In a case where any entity is being managed by a Managing Committee or Board of Trustees or Board of Governors by whatever name called he should ensure that his appointment is duly made by a resolution passed of such Managing Committee or Board of Trustees or Board of Governors.

Even in case of partnership or sole proprietary concerns, the member must ensure that a letter of appointment/engagement is given by the firm/sole proprietor before he accepts the appointment/ engagement.

CLAUSE (9) OF PART (I) OF SECOND SCHEDULE

Generally Accepted Audit Procedures

What constitutes "generally accepted audit procedure” would depend upon the facts & circumstances of each case, but guidance is available in general terms from the various pronouncements of the Institute is issued by way of Engagement & Quality Control Standards, Statements, General Clarifications, Guidance Notes Technical Guides, Practice Manuals, Studies & Other Papers.

Audit of Listed Companies

Pursuant to SEBI Notification, Statutory Audit of Listed Companies under the Companies Act, 2013 shall be done by only those auditors who have subjected themselves to the Peer Review process of the Institute, & hold a valid certificate issued by the Peer Review Board of the ICAI.

FRN & Membership No.

The members are required to mention the Membership number & Firm registration number to all reports issued pursuant to any attestation engagements, including certificates, issued by them as proprietor of/partner in the said firm.

Unique Document Identification Number (UDIN)

The members may note that UDIN is mandatory from 1st July, 2019 on all Corporate/ Non- Corporate Audit, Attest & Assurance Functions. Thus, a member of the Institute in practice shall generate Unique Document Identification Number (UDIN) for all kinds of the certification, GST & Tax Audit Reports & other Audit, Assurance & Attestation functions undertaken/signed by him.

Statutory Functions & Duties

An auditor of a company is appointed by the shareholders to perform certain statutory functions & duties & it is expected of him that he will in fact, perform these functions & duties. The failure to perform a statutory duty in the manner required is not excused merely by giving a qualification or reservation in auditor's report.

COUNCIL GUIDELINES

CA Final Audit – Highlights for May 2021 Exams

16

CHAPTER VII – APPOINTMENT OF AN AUDITOR IN CASE OF NON-PAYMENT OF UNDISPUTED FEES

a A member in practice shall not accept the appointment as auditor of entity; if undisputed audit fees of another CA for statutory audit have not been paid. Above notification does not apply to sick units.

a The provision for audit fee in accounts signed by both - the auditee & the auditor along with other expenses, if any, incurred by the auditor in connection with the audit, shall be considered as “undisputed audit fees”.

a "Sick Unit” shall mean a unit registered for not less than 5 years, which has at the end of any financial year accumulated losses equal to or exceeding its entire net worth.

CHAPTER VIII – SPECIFIED NUMBER OF AUDIT ASSIGNMENTS

A member of the Institute in practice shall not hold at any time appointment of more than the “specified number of audit assignments” of Companies under Section 141 of the Companies Act 2013.

For the above purpose, the “specified number of audit assignments” means -

a in the case of a CA in practice or a proprietary firm of CA, 30 audit assignments whether in respect of private Companies or other Companies, with the exception of one person Companies & dormant companies.

a in the case of CAs in practice, 30 audit assignments per partner in the firm, whether in respect of private Companies or other Companies, with the exception of One person Companies & dormant companies.

CHAPTER X – APPOINTMENT OF AN AUDITOR WHEN HE IS INDEBTED TO A CONCERN

A member of the Institute in practice or a partner of a firm in practice or a firm or a relative of such member or partner shall not accept appointment as auditor of a concern while indebted to the concern or given any guarantee or provided any security in connection with the indebtedness of any third person to the concern, for limits fixed in the statute & in other cases for amount exceeding ' 100,000/-.

CHAPTER XI – DIRECTIONS IN CASE OF UNJUSTIFIED REMOVAL OF AUDITORS

A member of the Institute in practice shall follow the direction given, by the Council or an appropriate Committee or on behalf of any of them, to him being the incoming auditor(s) not to accept the appointment as auditor(s), in the case of unjustified removal of the earlier auditor(s).

CHAPTER XIII – GUIDELINES ON TENDERS

a A member of the Institute in practice shall not respond to any tender issued by an organization or user of professional services in areas of services which are exclusively reserved for CAs, such as audit & attestation services.

a However, such restriction shall not be applicable where minimum fee of the assignment is prescribed in the tender document itself or where the areas are open to other professionals along with the CAs.

CHAPTER XIV – UNIQUE DOCUMENT IDENTIFICATION NUMBER (UDIN) GUIDELINES

CA Final Audit – Highlights for May 2021 Exams

17

a Whereas, to curb the malpractice of false certification/attestation by the unauthorized persons & to eradicate the practice of bogus certificates & to save various regulators, banks, stakeholders etc. from being misled, the Council of the Institute decided to implement an innovative concept to generate Unique Document Identification Number (UDIN) mandatorily for all kinds of the certificates/GST & Tax Audit Reports & other attest function in phased manner, for which members of the ICAI were notified through the various announcements published on the website of ICAI www.icai.org at the relevant times.

a A member of the Institute in practice shall generate Unique Document Identification Number (UDIN) for all kinds of the certification, GST & Tax Audit Reports & other Audit, Assurance & Attestation functions undertaken/signed by him which made mandatory from the following dates through announcements published on the website of the ICAI www.icai.org at the relevant time: - ▪ For all Certificates w.e.f. 1st February, 2019. ▪ For all GST & Tax Audit Reports w.e.f. 1st April, 2019. ▪ For all other Audit, Assurance & Attestation functions w.e.f. 1st July, 2019.

CHAPTER XVI – LOGO GUIDELINES

a The logo consists of letter ‘CA’ with a tick mark inside a rounded rectangle with white background. a The letters CA have been put in blue, the corporate colour which not only stands out on the

background but also denotes creativity, innovativeness, knowledge, integrity, trust, truth, stability & depth.

a The upside down tick mark typically used by CAs, has been used to symbolize the wisdom & value of the professional.

a The green colour in the tick mark signifies growth, prosperity, harmony & freshness. a Members are encouraged to use the new logo, as published here as it is. a Do not change the design & colours, including the white background. a Refrain from rotating or tilting the logo.

CHAPTER XVII – GUIDELINES FOR CORPORATE FORM OF PRACTICE

a The Council decided to allow members in practice to hold the office of Managing Director, Whole-time Director or Manager of a body corporate within the meaning of the Companies Act provided that the body corporate is engaged exclusively in rendering Management Consultancy & Other Services permitted by the Council in pursuant to Section 2(2)(iv) of the CA Act, 1949 & complies with the conditions(s) as specified by the Council from time to time in this regard.

a The members can retain full time Certificate of Practice besides being the Managing Director, Whole-time Director or Manager of such Management Consultancy Company. There will be no restriction on

CA Final Audit – Highlights for May 2021 Exams

18

the quantum of the equity holding of the members, either individually and/ or along with the relatives, in such Company. Such members shall be regarded as being in full- time practice & therefore can continue to do attest function either in individual capacity or in Proprietorship/Partnership firm in which capacity they practice & wherein they are also entitled to train articled/audit assistants.

a The name of the Management Consultancy Company is required to be approved by the Institute & such Company has to be registered with the Institute.

a It may be clarified that no audit practice can be done in Corporate Form. The consultancy practice hitherto done in Individual or Firm Status alone is now intended to be permitted in Corporate Form also.

a Ethical Compliance: (i) Once the Management Consultancy Company is Registered with the Institute, it will be necessary for such a Company to comply with the following requirements: -

a If the individual practitioner/sole-proprietorship firm/partnership firm is the statutory auditor of an entity then the Management Consultancy Company should not accept the internal audit or book-keeping or such other professional assignments, which are prohibited for the statutory auditor firm.

a The Notification in respect of ceiling on Non-audit fees is applicable in relation to a Management Consultancy Company.

a The Management Consultancy Company shall comply with clauses (6) & (7) of Part-I of the First Schedule.

Company Audit CEILING ON NUMBER OF AUDITS

a It has been mentioned earlier that before appointment is given to any auditor, the company must obtain a certificate from him to the effect that the appointment, if made, will not result in an excess holding of company audit by the auditor concerned over the limit laid down in Sec 141(3)(g) of the Companies Act, 2013 which prescribes that a person shall not be eligible for appointment as an auditor if he is in full time employment elsewhere or a person or a partner of a firm holding appointment as its auditor, if such person or partner is at the date of such appointment or reappointment, already holding appointment as auditor of more than 20 companies other than one person companies, dormant companies, small companies & private companies having paid- up share capital less than ` 100 crore (private company which has not committed a default in filing its FS u/s 137 of the said Act or annual return u/s 92 of the said Act with the Registrar).

SECTION 143(3)(i) a Clause (i) of Sub-Section (3) of Sec143 shall not apply to a private company:-(i) which is a one person

company or a small company; or (ii) which has turnover less than rupees 50 crores as per latest audited financial statement & which has aggregate borrowings from banks or financial institutions or anybody corporate at any point of time during the financial year less than rupees 25 crores)

MANAGERIAL REMUNERATION a The auditor of the company shall, in his report u/s 143, make a statement as to whether the

CA Final Audit – Highlights for May 2021 Exams

19

remuneration paid by the company to its directors is in accordance with the provisions of this section, whether remuneration paid to any director is in excess of the limit laid down under this section & give such other details as may be prescribed” (as per section 197(16) of the Companies Act, 2013)

a The aforesaid reporting requirement for auditors of public companies needs to be covered in auditor’s report under the Section “Report on Other Legal & Regulatory Requirements”.

CONSTITUTION OF NFRA a According to Sec 132 of the Act, the Central Government may, by notification, constitute a National

Financial Reporting Authority (NFRA) to provide for matters relating to accounting & auditing

standards for adoption by companies or class of companies under the Act. The NFRA shall perform its

functions through such divisions as may be prescribed.

a Every auditor referred to in Rule 3 shall file a return with the NFRA on or before 30th November every year in Form NFRA-2”

a Punishment in case of non-compliance – If a company or any officer of a company or an auditor or any other person contravenes any of the provisions of NFRA Rules, the company & every officer of the company who is in default or the auditor or such other person shall be punishable as per the provisions of Sec 450 of the Act.

a Further, as per Sec 132(4) of the Companies Act, 2013 as amended by the Companies Amendment Act, 2019, National Financial Reporting Authority, where professional or other misconduct is proved, have the power to make order for:

(A) imposing penalty of—

i) not less than one lakh rupees, but which may extend to five times of the fees received, in case of individuals; &

ii) not less than five lakh rupees, but which may extend to ten times of the fees received, in case of firms;

(B) debarring the member or the firm from:

i) being appointed as an auditor or internal auditor or undertaking any audit in respect of financial statements or internal audit of the functions & activities of any company or body corporate; or

ii) performing any valuation as provided u/s 247, for a minimum period of 6 months or such higher period not exceeding 10 years as may be determined by the NFRA.

PAYMENT OF DIVIDENDS a As per Accounting Standards (AS) 4 - Contingencies & Events Occurring After the Balance Sheet Date

& Ind AS 10- Events after the Reporting Period, if dividends are declared after the balance sheet date but before the FS are approved for issue, the dividends are not recognised as a liability at the balance sheet date because no obligation exists at that time unless a statute requires otherwise. Such dividends are disclosed in the notes.

AUDIT PROCEDURE FOR PAYMENT OF DIVIDEND a If dividends are declared after the balance sheet date but before the FS are approved for issue, check

that the dividends have not been recognised as a liability as per Accounting Standard (AS) 4 - Contingencies & Events Occurring After the Balance Sheet Date & Ind AS 10- Events after the Reporting Period, but whether a disclosure of the same has been made in the notes.

CA Final Audit – Highlights for May 2021 Exams

20

Audit Committee & Corporate Governance

VERIFICATION REGARDING COMPOSITION OF BOARD a The auditor shall ensure that the Chairperson of the board of the top 500 listed entities is - (a) a non-

executive director; (b) not related to the Managing Director or the Chief Executive Officer as per the definition of the term “relative” defined under the Companies Act, 2013.

OBLIGATIONS WITH RESPECT TO EMPLOYEES, INCLUDING SENIOR MANAGEMENT, KEY MANAGERIAL PERSONS, DIRECTORS & PROMOTERS

a The Board shall meet at least 4 times a year, with a maximum time gap of 120 days between any two meetings.

a The quorum for every meeting of the board of directors of the top 2,000 listed entities shall be 1/3 of its total strength or 3 directors, whichever is higher, including at least 1 independent director. The participation of the directors by video conferencing or by other audio-visual means shall also be counted for the purposes of such quorum.

a The top 2,000 entities shall be determined on the basis of market capitalisation, as at the end of the immediate previous financial year. For the purpose of above-mentioned provision, the count for the number of listed entities on which a person is a director/independent director shall be only those whose equity shares are listed on a stock exchange.

a The independent directors of the listed entity shall hold at least one meeting in a year, without the presence of non-independent directors & members of the management & all the independent directors shall strive to be present at such meeting.

INFORMATION TO SHAREHOLDERS a The listed entity shall send the soft copy of the full annual report to the shareholders who have

registered their email address(es) or hard copies of the salient features of all the documents, as prescribed in Sec 136 of the Companies Act, 2013 or rules made thereunder (unless the full annual has been specifically requested) where the email address has not been registered, not less than 21 days before the annual general meeting.

DISCLOSURE OF EVENTS OR INFORMATION a Every listed entity shall make disclosures of any events or information which, in the opinion of the

board of directors of the listed company, is material. a Board of directors of the listed entity shall authorize one or more Key Managerial Personnel for the

purpose of determining materiality of an event or information & for the purpose of making disclosures to stock exchange(s) under this regulation & the contact details of such personnel shall be also disclosed to the stock exchange(s) & as well as on the listed entity`s website.

a Such disclosures shall be hosted on the website of the listed entity for a minimum period of 5 years & thereafter as per the archival policy of the listed entity, as disclosed on its website.

CA Final Audit – Highlights for May 2021 Exams

21

Audit of Consolidated Financial Statements

AUDIT CONSIDERATIONS a While considering the observations (for instance modification & /or emphasis of matter in accordance

with SA 705/706) of the component auditor in his report on the standalone FS, the principles of SA

600 needs to be considered. ICAI issued an announcement dated May 25, 2017 which amended

paragraph 17 of Guidance Note & states that while considering the observations (for instance

modification & /or emphasis of matter/other matter in accordance with SA 705/706) of the

component auditor in his report on the standalone FS, the parent auditor should comply with the

requirements of SA 600, “Using the Work of Another Auditor”.

a Therefore, the concept of materiality would be considered while considering the observations of

the component auditor.

Audit under Fiscal Laws

TAX AUDIT APPLICABILITY OF TAX AUDIT

Sec 44AB provides for the compulsory audit of accounts of certain persons carrying on business or profession. Sec 44AB reads as under:

“Audit of accounts of certain persons carrying on business or profession”. Every person –

(a) carrying on business shall, if his total sales, turnover or gross receipts, as the case may be, in business exceed or exceeds Rs. 1 crore in any previous year.

(b) carrying on profession shall, if his gross receipts, in profession exceed Rs. 50 lakhs in any previous year,

With effect from assessment year 2020-21, the threshold limit, for a person carrying on business, has been increased from ` 1 crore to `5 crores in case when cash receipts & payments made during the year does not exceed 5% of total receipt or payment, as the case may be. In other words, 95% or more of the business transactions should be done through banking channels.

ADDITIONS TO FORM 3CD Clause 8A of The new clause inserted in part A of the form 3CD requires the assessee to state whether

CA Final Audit – Highlights for May 2021 Exams

22

Form 3CD the assessee has opted for taxation under any of the sections 115BA, 115BAA & 115BAB.

It may be noted that all the above sections i.e.115BA, 115BAA & 115BAB are applicable to the company assesses only.

The reply to the above clause can either be a “yes” or “no”. If the assessee has not opted for any concessional rates as provided under the sections 115BA, 115BAA & 115BAB, of the Act, then, the tax auditor is not required to take any further steps & no further audit procedure is required to be followed. The answer to such question as per the clause in such case can be given as “No” only.

However, if the assessee informs that it has opted for the concessional rate of taxation as per the provisions of sections 115BA, 115BAA & 115BAB of the Act, then the audit approach is required to be modified.

Clause 18 of Form 3CD

Particulars of depreciation allowable as per the Income-tax Act, 1961 in respect of each asset or block of assets, as the case may be, in the following form:-

(a) Description of asset/block of assets. (b) Rate of depreciation. (c) Actual cost or written down value, as the case may be.

(ca) Adjustment made to the written down value u/s 115BAA (for assessment year 2020-21 only)

(cb) Adjusted written down value

(d) Additions/deductions during the year with dates; in the case of any addition of an asset, date put to use; including adjustments on account of –

i) Central Value Added Tax credits claimed & allowed under the Central Excise Rules, 1944, in respect of assets acquired on or after 1st March, 1994,

ii) Change in rate of exchange of currency, & iii) Subsidy or grant or reimbursement, by whatever name called.

(e) Depreciation allowable.

(f) Written down value at the end of the year.

Clause 32a of Form 3CD

Details of brought forward loss or depreciation allowance, in the following manner, to the extent available:

1 Sl. No.

2 Assessment Year

3 Nature of loss/allowance (in rupees)

4 Amount as returned (in rupees)

5 All losses/allowances not allowed u/s 115BAA*

6 Amount as adjusted by withdrawal of additional depreciation on account of opting for taxation u/s 115BAA*

7 Amount as assessed (give reference to relevant order)

8 Remarks

This clause requires information in respect of brought forwarded losses & unabsorbed depreciation, which can be verified from the previous return & the assessment orders.

The above brought forwarded losses/allowance, not allowed u/s 115BAA, are to be listed out assessment year wise & section wise as per the return (& where assessed, as per the assessment order) are to be reported under this clause. A reporting format is prescribed for the sake of standardization.

*Note: All losses/ allowances not allowed u/s 115BAA & Amount as adjusted by

CA Final Audit – Highlights for May 2021 Exams

23

withdrawal of additional depreciation on account of opting for taxation u/s 115BAA* is required to be filled in for assessment year 2020-21 only.

SIGNATURE & STAMP/SEAL OF THE SIGNATORY While issuing the tax audit report u/s 44AB of the Income Tax Act 1961, the Auditor should generate appropriate UDIN (Unique Document Identification Number) & refer the same in its report.

GST AUDIT 1. AUDIT BY PROFESSIONALS

Audit of Accounts [Section 35(5) Read alongwith Section 44(2) & Rule 80]

✓ Every registered person must get his accounts audited by a Chartered Accountant or a Cost Accountant if his aggregate turnover during a FY exceeds ` 2 crores.

✓ Such registered person is required to furnish electronically through the common portal alongwith Annual Return a copy of:

Audited annual accounts

A Reconciliation Statement, duly certified, in prescribed FORM GSTR-9C.

Multiple Branches

Where a taxpayer has multiple branches registered under GST in different States/ Union Territories, the total aggregate turnover of all such branches is considered while calculating the threshold limit.

So, if the cumulative turnover of all the branches exceed threshold limit, then the GST audit is applicable to each of these branches, irrespective of whether the turnover of a particular branch is less than the threshold.

Same PAN If a registered person is liable to get his accounts audited u/s 35, all the registrations obtained under the same PAN will also be liable for such audit, regardless of the turnover in each State in which the other registrations have been obtained.

QUALIFICATION OF GST AUDITOR & ELIGIBILITY

Only a Chartered Accountant or a Cost Accountant can perform GST audit under section 35(5). Points to note:

No GST Audit of Government subject to CAG Audit: It may be noted that the section 35(5) shall not apply to any department of the Central Government or a State Government or a local authority, whose books of account are subject to audit by the Comptroller & Auditor- General of India or an auditor appointed for auditing the accounts of local authorities under any law for the time being in force.

OIDAR & Foreign Airlines not liable for GST Audit: Further, persons supplying Online Information & Data Base Access or Retrieval Services from a place outside India to a person in India & persons who are foreign company which is an airline company shall not be required to furnish reconciliation statement in FORM GSTR-9C.

However, the foreign airline company is required to submit a statement of receipts & payments for the FY in respect of its Indian business operations, duly authenticated by a practicing chartered accountant in India or a firm or a Limited Liability Partnership of practicing chartered accountants in India for each GSTIN by the 30th September, of the year succeeding the FY.

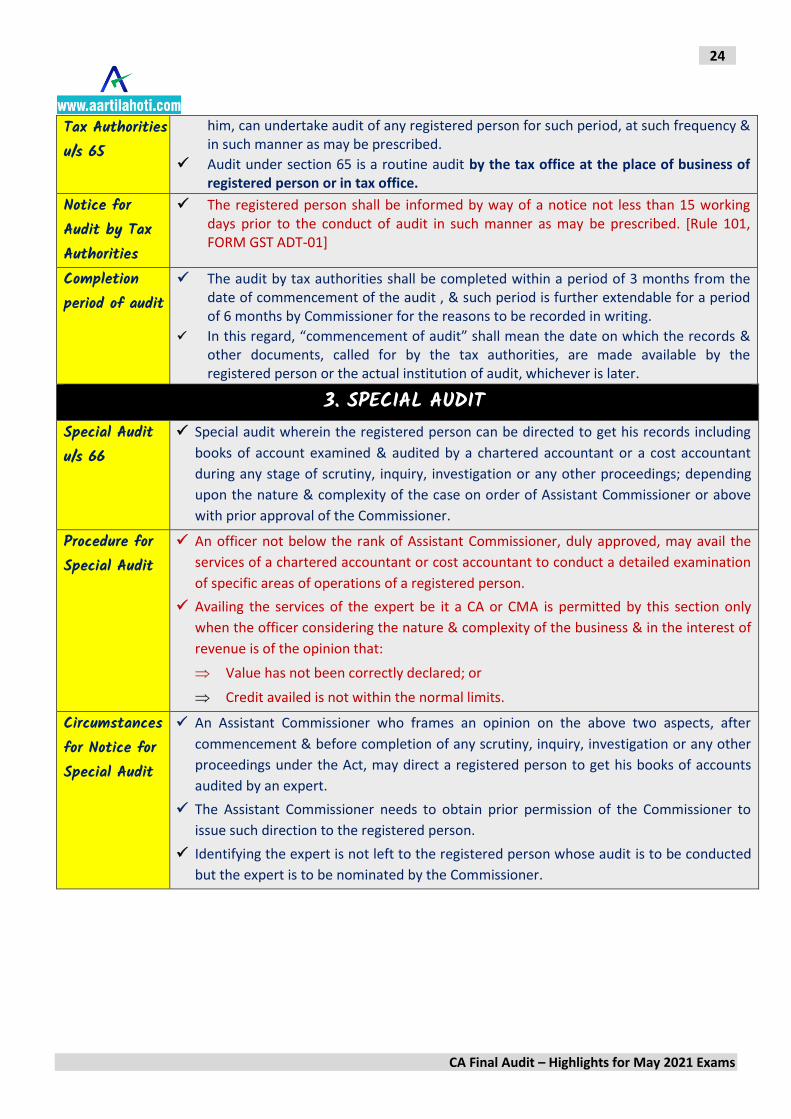

2. GENERAL AUDIT Audit by the ✓ In case of audit by the tax authorities the Commissioner or any officer authorised by

CA Final Audit – Highlights for May 2021 Exams

24

Tax Authorities u/s 65

him, can undertake audit of any registered person for such period, at such frequency & in such manner as may be prescribed.

✓ Audit under section 65 is a routine audit by the tax office at the place of business of registered person or in tax office.

Notice for Audit by Tax Authorities

✓ The registered person shall be informed by way of a notice not less than 15 working days prior to the conduct of audit in such manner as may be prescribed. [Rule 101, FORM GST ADT-01]

Completion period of audit

✓ The audit by tax authorities shall be completed within a period of 3 months from the date of commencement of the audit , & such period is further extendable for a period of 6 months by Commissioner for the reasons to be recorded in writing.

✓ In this regard, “commencement of audit” shall mean the date on which the records & other documents, called for by the tax authorities, are made available by the registered person or the actual institution of audit, whichever is later.

3. SPECIAL AUDIT Special Audit u/s 66

✓ Special audit wherein the registered person can be directed to get his records including

books of account examined & audited by a chartered accountant or a cost accountant

during any stage of scrutiny, inquiry, investigation or any other proceedings; depending

upon the nature & complexity of the case on order of Assistant Commissioner or above

with prior approval of the Commissioner.

Procedure for Special Audit

✓ An officer not below the rank of Assistant Commissioner, duly approved, may avail the

services of a chartered accountant or cost accountant to conduct a detailed examination

of specific areas of operations of a registered person.

✓ Availing the services of the expert be it a CA or CMA is permitted by this section only

when the officer considering the nature & complexity of the business & in the interest of

revenue is of the opinion that:

Value has not been correctly declared; or

Credit availed is not within the normal limits.

Circumstances for Notice for Special Audit

✓ An Assistant Commissioner who frames an opinion on the above two aspects, after

commencement & before completion of any scrutiny, inquiry, investigation or any other

proceedings under the Act, may direct a registered person to get his books of accounts

audited by an expert.

✓ The Assistant Commissioner needs to obtain prior permission of the Commissioner to

issue such direction to the registered person.

✓ Identifying the expert is not left to the registered person whose audit is to be conducted

but the expert is to be nominated by the Commissioner.

CA Final Audit – Highlights for May 2021 Exams

25

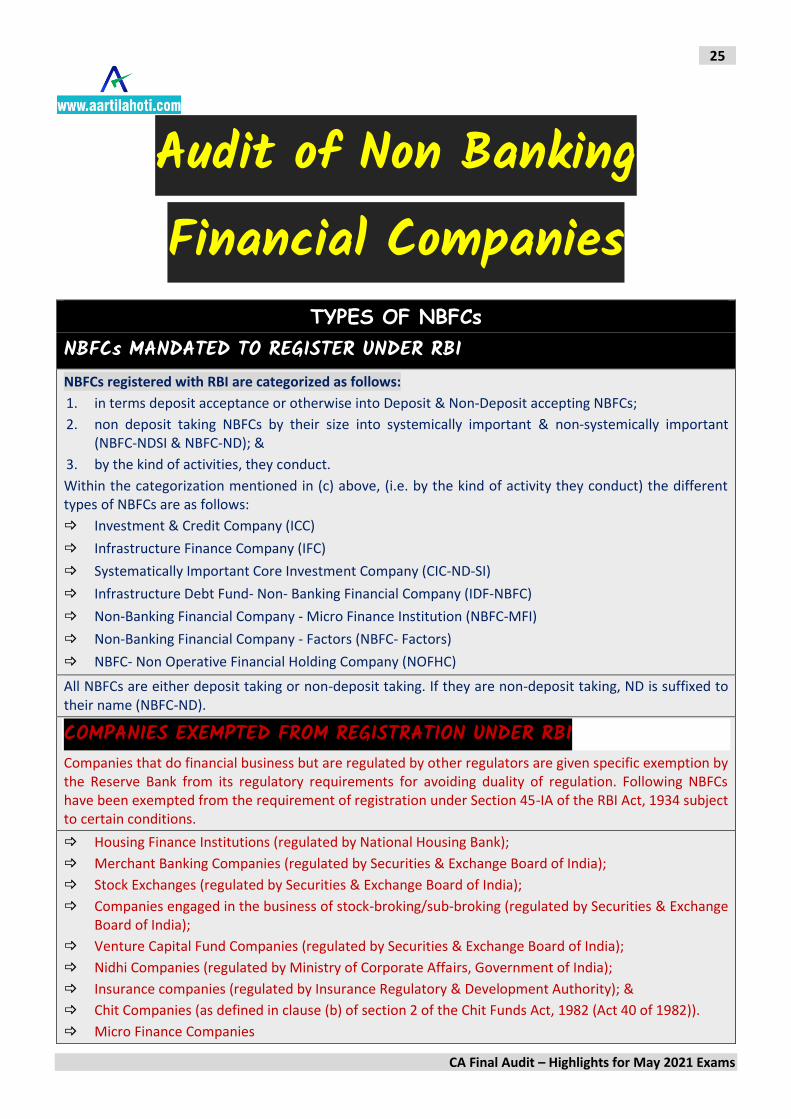

Audit of Non Banking Financial Companies

TYPES OF NBFCs

NBFCs MANDATED TO REGISTER UNDER RBI NBFCs registered with RBI are categorized as follows:

1. in terms deposit acceptance or otherwise into Deposit & Non-Deposit accepting NBFCs;

2. non deposit taking NBFCs by their size into systemically important & non-systemically important (NBFC-NDSI & NBFC-ND); &

3. by the kind of activities, they conduct.

Within the categorization mentioned in (c) above, (i.e. by the kind of activity they conduct) the different types of NBFCs are as follows:

Investment & Credit Company (ICC)

Infrastructure Finance Company (IFC)

Systematically Important Core Investment Company (CIC-ND-SI)

Infrastructure Debt Fund- Non- Banking Financial Company (IDF-NBFC)

Non-Banking Financial Company - Micro Finance Institution (NBFC-MFI)

Non-Banking Financial Company - Factors (NBFC- Factors)

NBFC- Non Operative Financial Holding Company (NOFHC)

All NBFCs are either deposit taking or non-deposit taking. If they are non-deposit taking, ND is suffixed to their name (NBFC-ND).

COMPANIES EXEMPTED FROM REGISTRATION UNDER RBI Companies that do financial business but are regulated by other regulators are given specific exemption by the Reserve Bank from its regulatory requirements for avoiding duality of regulation. Following NBFCs have been exempted from the requirement of registration under Section 45-IA of the RBI Act, 1934 subject to certain conditions.

Housing Finance Institutions (regulated by National Housing Bank);

Merchant Banking Companies (regulated by Securities & Exchange Board of India);

Stock Exchanges (regulated by Securities & Exchange Board of India);

Companies engaged in the business of stock-broking/sub-broking (regulated by Securities & Exchange Board of India);

Venture Capital Fund Companies (regulated by Securities & Exchange Board of India);

Nidhi Companies (regulated by Ministry of Corporate Affairs, Government of India);

Insurance companies (regulated by Insurance Regulatory & Development Authority); &

Chit Companies (as defined in clause (b) of section 2 of the Chit Funds Act, 1982 (Act 40 of 1982)).

Micro Finance Companies

CA Final Audit – Highlights for May 2021 Exams

26

Securitisation & Reconstruction Companies

Mutual Benefit Companies

Mortgage Guarantee Companies

Core Investment Companies i.e. a NBFC being a Core Investment Company referred to in the Core Investment Companies (Reserve Bank) Directions, 2016, which is not a Systemically Important Core Investment Company, as defined in subparagraph (xxv) of paragraph 3 of the Core Investment Companies (Reserve Bank) Directions, 2016.

Alternative Investment Fund (AIF) Companies

DIFFERENCES BETWEEN DIVISION II (IND- AS- OTHER THAN NBFCS) & DIVISION III (IND- AS- NBFCS) OF SCHEDULE III

The presentation requirements under Division III for NBFCs are similar to Division II (Non NBFC) to a large extent except for the following:

(a) NBFCs have been allowed to present the items of the balance sheet in order of their liquidity which is not allowed to companies required to follow Division II. Additionally, NBFCs are required to classify items of the balance sheet into financial & non-financial whereas other companies are required to classify the items into current & non-current.

(b) An NBFC is required to separately disclose by way of a note any item of ‘other income’ or ‘other expenditure’ which exceeds 1 per cent of the total income e. Division II, on the other hand, requires disclosure for any item of income or expenditure which exceeds 1 per cent of the revenue from operations or ` 10 lakhs, whichever is higher.

(c) NBFCs are required to separately disclose under ‘receivables’, the debts due from any Limited Liability Partnership (LLP) in which its director is a partner or member.

(d) NBFCs are also required to disclose items comprising ‘revenue from operations’ & ‘other comprehensive income’ on the face of the Statement of profit & loss instead of showing those only as part of the notes.

(e) Separate disclosure of trade receivable which have significant increase in credit risk & credit impaired.

(f) The conditions or restrictions for distribution attached to statutory reserves have to be separately disclose in the notes as stipulated by the relevant statute.

Peer Review & Quality Review

TECHNICAL, ETHICAL & PROFESSIONAL STANDARDS a Accounting Standards issued by ICAI that are applicable for entities other than companies under the

Companies Act, 2013; a Accounting Standards prescribed u/s 133 of the Companies Act; 2013 by the CG based on the

recommendation of ICAI & in consultation with the National Financial Reporting Authority (NFRA) & notified as Accounting Standards Rules 2006, as amended from to time;

a Indian Accounting Standards prescribed u/s 133 of the Companies Act 2013 by the CG based on the recommendation of ICAI & in consultation with NFRA & notified as Companies (Indian Accounting

CA Final Audit – Highlights for May 2021 Exams

27

Standards) Rules, 2015, as amended from time to time; a Standards :

Standards issued by the ICAI including-

Engagement standards

Statements Guidance notes

Standards on Internal Audit. Guidelines/ Notifications/Directions/Announcements/Pronouncements/Profe

ssional Standards issued from time to time by the Council or any of its Committees.

a Framework for the preparation & presentation of FS, Preface to the Standards on Quality Control, Auditing, Review, Other Assurance & Related Services & Framework for Assurance engagements;

a Provisions of the relevant statutes &/or rules or regulations which are applicable in the context of the specific engagements being reviewed including instructions, guidelines, notifications, directions issued by regulatory bodies as covered in the scope of assurance engagements.

APPLICABILITY OF PEER REVIEW 1. Every Practice Unit including its branches, based on their category as determined below will be

subject to Peer Review in accordance with this Statement.

Level I:

A Practice Unit which has undertaken any of the under-mentioned assurance services in the period under review shall be treated a Level I entity:

Central Statutory Audit of Public Sector Banks, Private Sector Banks, Foreign Banks, Cooperative Banks & Public Financial Institutions;

Central Statutory Audit of Central or State Public Sector Undertakings & Central Cooperative Societies based on criteria such as turnover or paid up capital etc. as may be decided by the Board;

Central Statutory Audit of Insurance Companies;

Statutory Audit of asset management companies or mutual funds;

Statutory Audit of enterprises whose equity or debt securities are listed in India or abroad;

Statutory audit of any body corporate including trusts which are covered under public interest entities.

Statutory Audit of Entities which have raised funds from public or banks or financial institutions of over Rs. 50 Crores during the period under Review;

Statutory Audit of Entities which have raised donations &/or contributions over Rs. 50 Crores during the period under Review;

Statutory Audit of entities having net worth of more than Rs. 250 Crores at any time during the period under Review.

Statutory Audit of entities which have been funded by Central &/or State Government(s) schemes of over Rs. 50 Cores during the period under Review.

Statutory Audit of NBFCs as may be defined by the Board.

Central Statutory Audit of Regional Rural Banks.

Statutory Audit of parent, subsidiary, associate, & joint venture of the above entities.

Level II:

A Practice Unit which has undertaken any of the under-mentioned assurance services in the period under review shall be treated as Level II entity:

Statutory/Internal/Concurrent/Systems/Tax audit &/or Departmental Review of Branches/Offices of – ▪ Public Sector undertaking

CA Final Audit – Highlights for May 2021 Exams

28

▪ Public Sector or Private Sector &/or Foreign Banks ▪ Insurance Companies ▪ Co-operative Banks ▪ Regional Rural Banks

Statutory Audit of NBFCs as may be defined by the Board.

Statutory Audit of entities having Net Worth of over Rs. 5 Crores or an annual turnover of more than Rs. 50 Crores during the period under Review.

UDIN`s generated by the Practice Units more than the specified number determined by the Board from time to time.

Statutory Audit of entities which have raised funds from public or banks or financial institutions of more than Rs. 25 Crores but less than Rs. 50 Crores during the period under review.

Any other Practice Unit providing assurance or other services not covered under (i) (ii), (iii), (iv) & (v) hereinabove.

2. Special case review

The Board, based on specific information received from Secretary, ICAI or any other Committee of the Institute including Disciplinary directorate or any other Regulator, which in the opinion of the Board requires a special review of the Practice Unit, may conduct a special review of the Practice Unit.

Any Practice Unit not selected for Peer Review, may suo moto apply to the Board for the conduct of its Peer Review. The Board shall act upon the same within 30 days from the date of receipt of such request.

An auditee (Client) may request the Board for the conduct of Peer Review of its auditor (Practice Unit). The Board shall act upon the same within 30 days from the date of receipt of such request.

PERIODICITY OF PEER REVIEW The periodicity of peer review will be –

a Level I Practice Units – Once in 3 years. a Level II Practice Units – Once in 4 years.

However, if the Board so decides or otherwise at the request of the Practice Unit, the Peer Review for a Practice Unit can be conducted at shorter intervals.

ELIGIBILITY TO BE A REVIEWER 1. A Peer Reviewer shall: -

(a) Shall be a member in practice with at least 10 years of experience for Level I entities & 7 years of experience for Level II entities.

(b) In case a member has moved from industry to practice & is currently in practice he should have at least 15 years of experience in industry & at least 5 years` experience in practice for Level I entities & an experience of at least 10 years in industry & at least 3 years` experience in practice, for Level II entities.

(c) Should have undergone the requisite training & cleared the requisite test for Peer Review as prescribed by the Board.

(d) Should have conducted audit of Level I Entities for at least 7 years or got his entity audited for at least 7 years which should be a Level I entity to be eligible for conducting Peer Review of Level I Entities.

2. A Reviewer shall not accept any professional assignment from the Practice Unit for a period 2 years from the date of appointment. Further, he should not have accepted any professional assignment from the Practice Unit for a period of 2 years before the date of appointment as reviewer of that Practice Unit.

CA Final Audit – Highlights for May 2021 Exams

29

OBLIGATIONS OF THE PRACTICE UNIT Any Practice Unit, in addition to the prescribed information to be furnished including the questionnaire, statements & such other particulars as the Board may deem fit, shall comply with the following.

i. Produce to the Reviewer or allow access to, any record, document or prescribed register maintained by the Practice Unit.

ii. Provide to the Reviewer such explanation or further particulars/ information, as the Reviewer shall specify.

iii. Provide to the Reviewer all assistance in connection with Peer Review; iv. Where any information or matter relevant to a Practice Unit is recorded otherwise than in a legible

form, the Practice Unit shall provide & present to the Reviewer a reproduction of any such information or matter, or of the relevant part of it in a legible form, with a translation in English or Hindi, if the matter is in any other language, & if such translation is requested for by the Reviewer.

OBLIGATIONS OF THE PEER REVIEWER (i) The Reviewer shall not take any extracts of the Practice Units clients` file or records examined by him

while conducting Peer Review, as a part of his working papers. (ii) The Reviewer shall complete the Review within the prescribed time frame.

DIFFERENCE BETWEEN PEER REVIEW & QUALITY REVIEW PEER REVIEW a Peer review is a review of the systems & procedures of an audit firm. a Although sample audit files are inspected by the peer reviewer, it is done for the purpose of testing

the effectiveness of the systems & procedures. a The intention is to not to find faults but to help the firm develop effective systems. a It is a kind of mentoring process. a Peer review is a part of the activities of ICAI aimed at improving the quality of service.

QUALITY REVIEW a In contrast, a quality review is supposed to act as a deterrent.

a Quality Review Board (QRB) is constituted by the CG & is independent of ICAI.

a As per Sec 28A of the CA Act, the CG has the authority to constitute a QRB.

a QRB carries out supervisory & disciplinary functions.

a A quality review normally pertains to one particular audit conducted by an audit firm.

a The main objective quality review is to find errors or inadequacies, if any, committed by the auditor

while conducting the audit.

a Serious errors detected in quality review lead to disciplinary action against the member.

QUALITY REVIEW IMPORTANT AREAS AS PER QUALITY REVIEW REPORT IN ACCORDANCE

WITH SQC-1 ARE a Whether the audit firm establishes & implements policies & procedure on all the element of system

of quality control. a Whether the engagement quality control reviewer review at an appropriate time for the planning of

an audit, significant audit judgement, & expressions of an audit opinion.

CA Final Audit – Highlights for May 2021 Exams

30

a Whether the audit firm assigns as the person responsible for the monitoring of the system of quality control a person with appropriate experience for the role, vest the assigned person with sufficient & appropriate authority.

a Whether the audit firm obtain, at least annually, a confirmation letter concerning compliance with policies & procedure for the maintenance of independence from all person required to maintain independence.

a Whether the audit firm perform the independence confirmation procedure set forth in its internal rules before acceptance & continuance of an audit engagement, & when issuing the auditor`s report appropriately confirms that there was no change in the status of independence.