Heavy Oil Latin America Congress HOLA Markets and ... n Dr... · PDF file213 CPE-1 META...

19

Heavy Oil Latin America Congress HOLA Markets and Investment Commercial potential of heavy oil reserves in Colombia Armando Zamora Director General Bogotá, August 2011

Transcript of Heavy Oil Latin America Congress HOLA Markets and ... n Dr... · PDF file213 CPE-1 META...

Heavy Oil Latin America CongressHOLA

Markets and Investment

Commercial potential of heavy oil reserves in Colombia

Armando ZamoraDirector General

Bogotá, August 2011

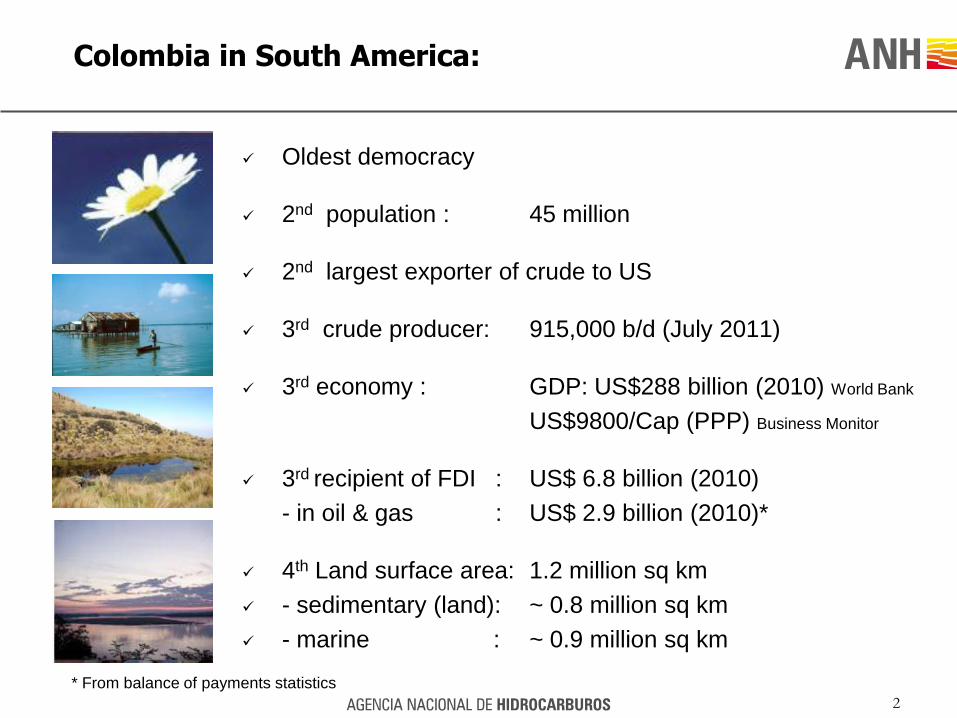

Colombia in South America:

Oldest democracy

2nd population : 45 million

2nd largest exporter of crude to US

3rd crude producer: 915,000 b/d (July 2011)

3rd economy : GDP: US$288 billion (2010) World Bank

US$9800/Cap (PPP) Business Monitor

3rd recipient of FDI : US$ 6.8 billion (2010)

- in oil & gas : US$ 2.9 billion (2010)*

4th Land surface area: 1.2 million sq km

- sedimentary (land): ~ 0.8 million sq km

- marine : ~ 0.9 million sq km

2

* From balance of payments statistics

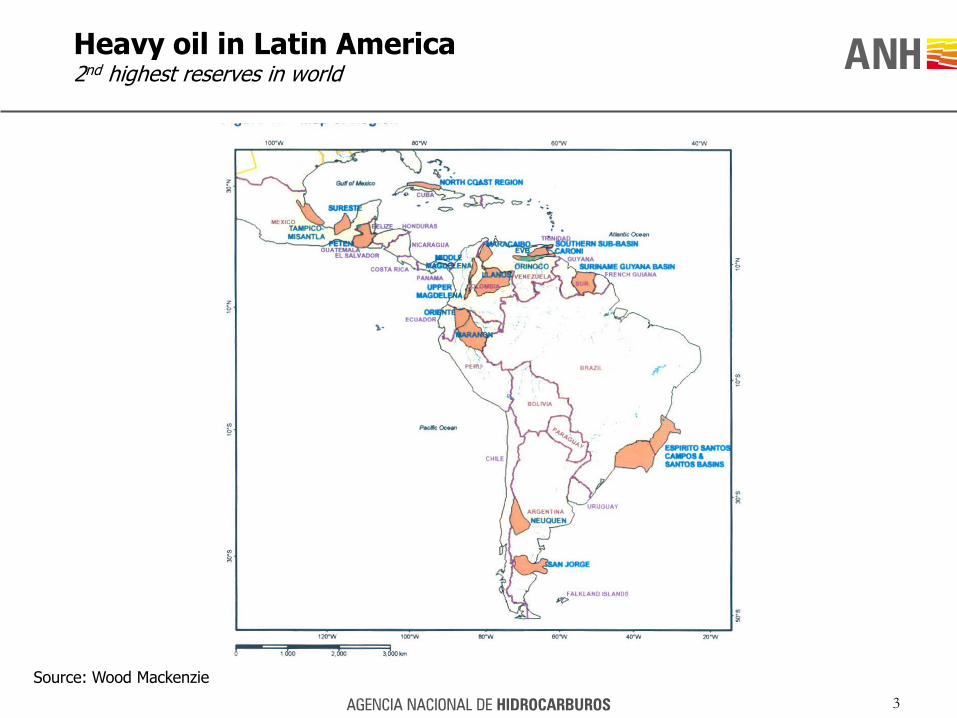

Heavy oil in Latin America2nd highest reserves in world

3

Source: Wood Mackenzie

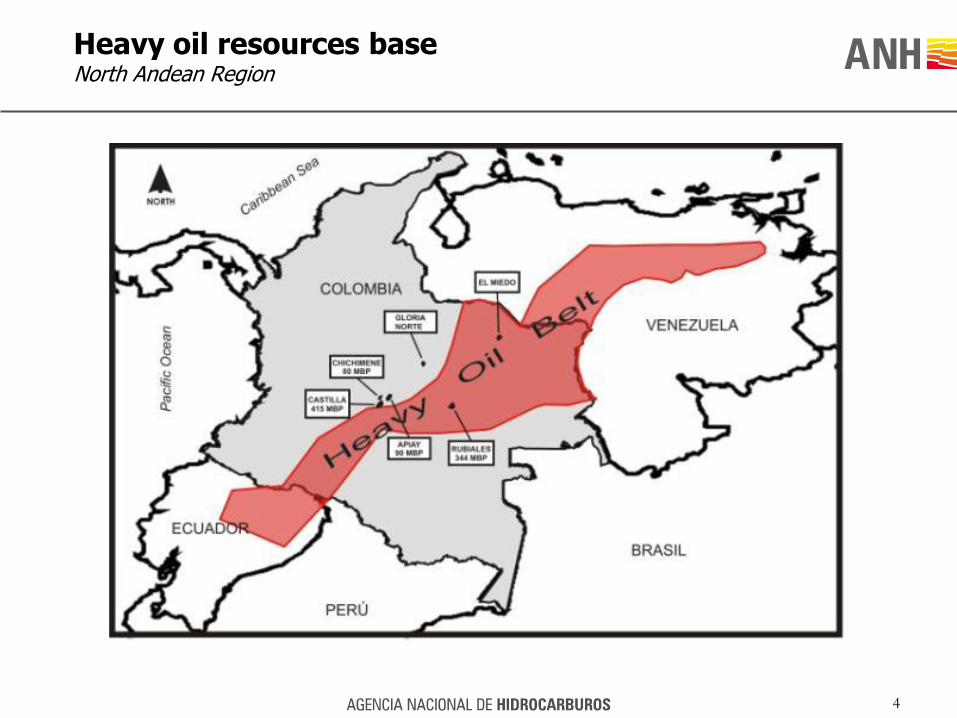

Heavy oil resources baseNorth Andean Region

4

Regional background

5

ESCUDO DE

GUAYANA

BOGOTA

LAGO DE MARACAIBO

BARINAS APURE

87,000 Km2

2,000 MM BBLS

55,000 km2

34,800 MM BBLS

220,000 Km2

4,000 MM BBLS

Sources: Plan de Negocio 2004-2009 PDVSA.- Colombianet, Ecopetrol

RESERVES

50,000 Km2

21,600 MM BBLS

10,000 MM BBLS pesados

FAJA DEL ORINOCO

LLANOS ORIENTALES

Wells and shows in Llanos basin

6

Source: * PROYECTO DE CRUDOS PESADOS 2006. LANDMARK, HALLIBURTON. - ACIPET.

RIO CASANARE

RIO ARAUCA

N

Villavicencio

Yopal

Arauca

Oil show

Oil and Gas show

Gas show

Well

Llanos Basin

ANH Special Area

River

The map ilustrates the 41 exploratory wells drilled in the exploratory area of

the ANH with hydrocarbon shows.

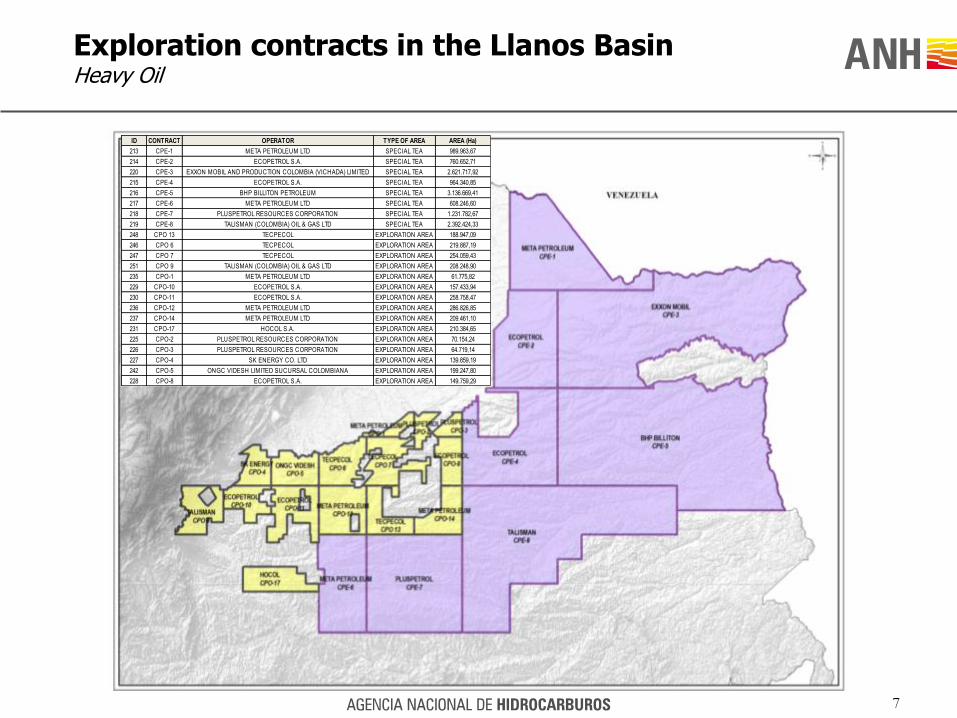

ID CONTRACT OPERATOR TYPE OF AREA AREA (Ha)

213 CPE-1 META PETROLEUM LTD SPECIAL TEA 989.963,67

214 CPE-2 ECOPETROL S.A. SPECIAL TEA 760.652,71

220 CPE-3 EXXON MOBIL AND PRODUCTION COLOMBIA (VICHADA) LIMITED SPECIAL TEA 2.621.717,92

215 CPE-4 ECOPETROL S.A. SPECIAL TEA 964.340,85

216 CPE-5 BHP BILLITON PETROLEUM SPECIAL TEA 3.136.669,41

217 CPE-6 META PETROLEUM LTD SPECIAL TEA 608.246,60

218 CPE-7 PLUSPETROL RESOURCES CORPORATION SPECIAL TEA 1.231.782,67

219 CPE-8 TALISMAN (COLOMBIA) OIL & GAS LTD SPECIAL TEA 2.392.424,33

248 CPO 13 TECPECOL EXPLORATION AREA 188.947,09

246 CPO 6 TECPECOL EXPLORATION AREA 219.887,19

247 CPO 7 TECPECOL EXPLORATION AREA 254.059,43

251 CPO 9 TALISMAN (COLOMBIA) OIL & GAS LTD EXPLORATION AREA 208.248,90

235 CPO-1 META PETROLEUM LTD EXPLORATION AREA 61.775,82

229 CPO-10 ECOPETROL S.A. EXPLORATION AREA 157.433,94

230 CPO-11 ECOPETROL S.A. EXPLORATION AREA 258.758,47

236 CPO-12 META PETROLEUM LTD EXPLORATION AREA 286.826,85

237 CPO-14 META PETROLEUM LTD EXPLORATION AREA 209.461,10

231 CPO-17 HOCOL S.A. EXPLORATION AREA 210.384,65

225 CPO-2 PLUSPETROL RESOURCES CORPORATION EXPLORATION AREA 70.154,24

226 CPO-3 PLUSPETROL RESOURCES CORPORATION EXPLORATION AREA 64.719,14

227 CPO-4 SK ENERGY CO. LTD EXPLORATION AREA 139.859,19

242 CPO-5 ONGC VIDESH LIMITED SUCURSAL COLOMBIANA EXPLORATION AREA 199.247,80

228 CPO-8 ECOPETROL S.A. EXPLORATION AREA 149.759,29

Exploration contracts in the Llanos BasinHeavy Oil

7

E&P Discoveries

Light Oil

Medium Oil

Heavy Oil

8

Risked STOIIP

The P50 STOIIP with an average geological risk of 15%Is around 124.000 MMBBLS

9

Yet-to-find recoverable oil reservesColombia

10

Sources: National University (Colombia), Halliburton (heavy oil)

0

20

40

60

80

100

120

140

High Medium Low

Bn bls

Heavy Oil

-

500.000

1.000.000

1.500.000

2.000.000

2002 2004 2006 2008 2010 2012 2014 2016 2018 2020 2022 2024

bopd

Heavy Oil Other

Heavy oil share of expected future productionBase case scenario (P50)

11

Projection

Source: ANH analysis

50%54%

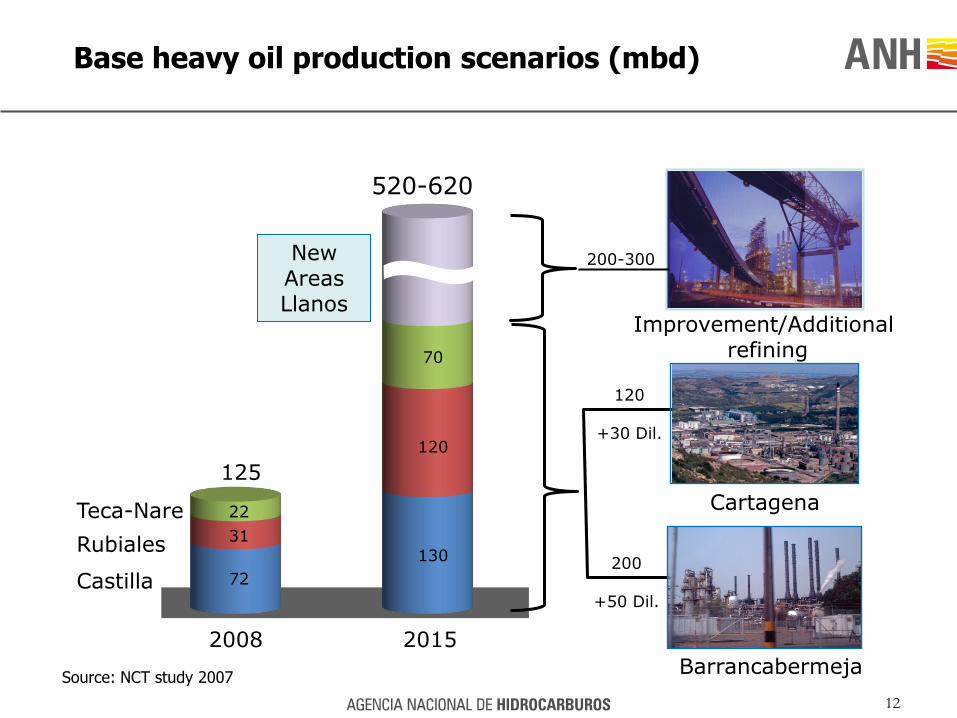

Base heavy oil production scenarios (mbd)

12

72

2008 2015

31

22

130

120

70

125

Castilla

Rubiales

Teca-Nare

New Areas Llanos

Barrancabermeja

Cartagena

120

+30 Dil.

200

+50 Dil.

Improvement/Additionalrefining

200-300

520-620

Source: NCT study 2007

13

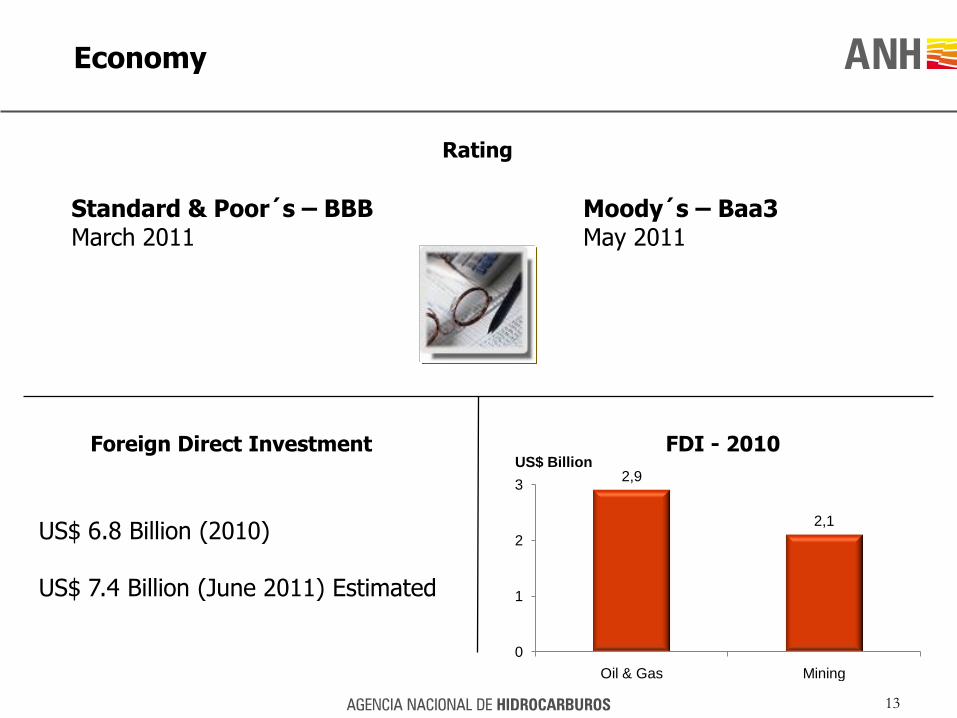

Economy

Rating

Standard & Poor´s – BBBMarch 2011

US$ 6.8 Billion (2010)

US$ 7.4 Billion (June 2011) Estimated

Foreign Direct Investment FDI - 2010

2,9

2,1

0

1

2

3

Oil & Gas Mining

US$ Billion

Moody´s – Baa3May 2011

Source: Banco de la República

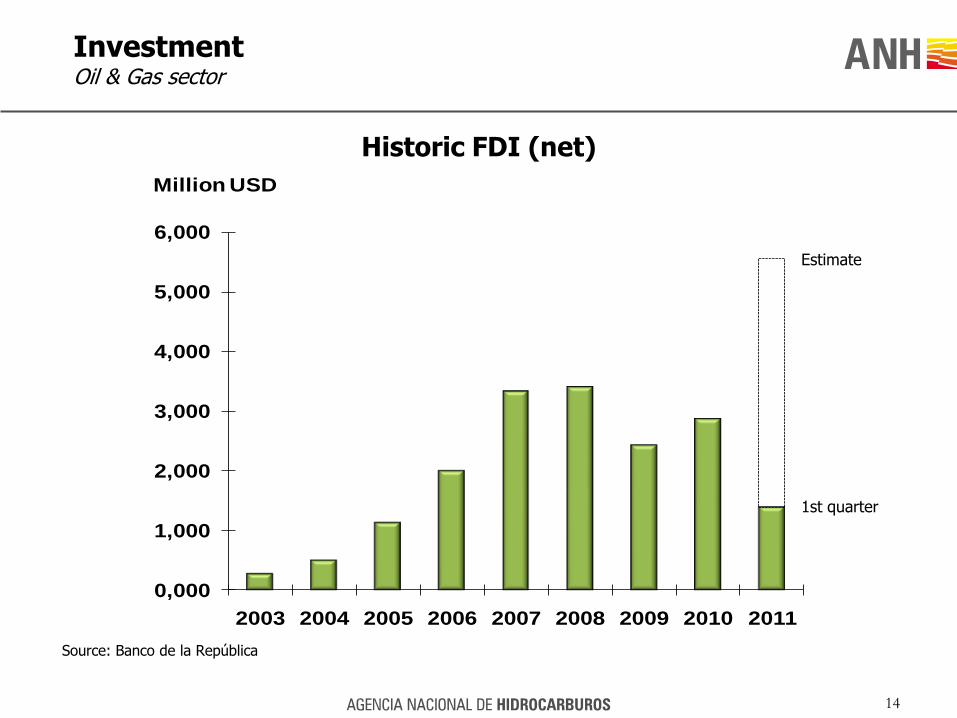

InvestmentOil & Gas sector

Historic FDI (net)

14

1st quarter

0,000

1,000

2,000

3,000

4,000

5,000

6,000

2003 2004 2005 2006 2007 2008 2009 2010 2011

Million USD

Estimate

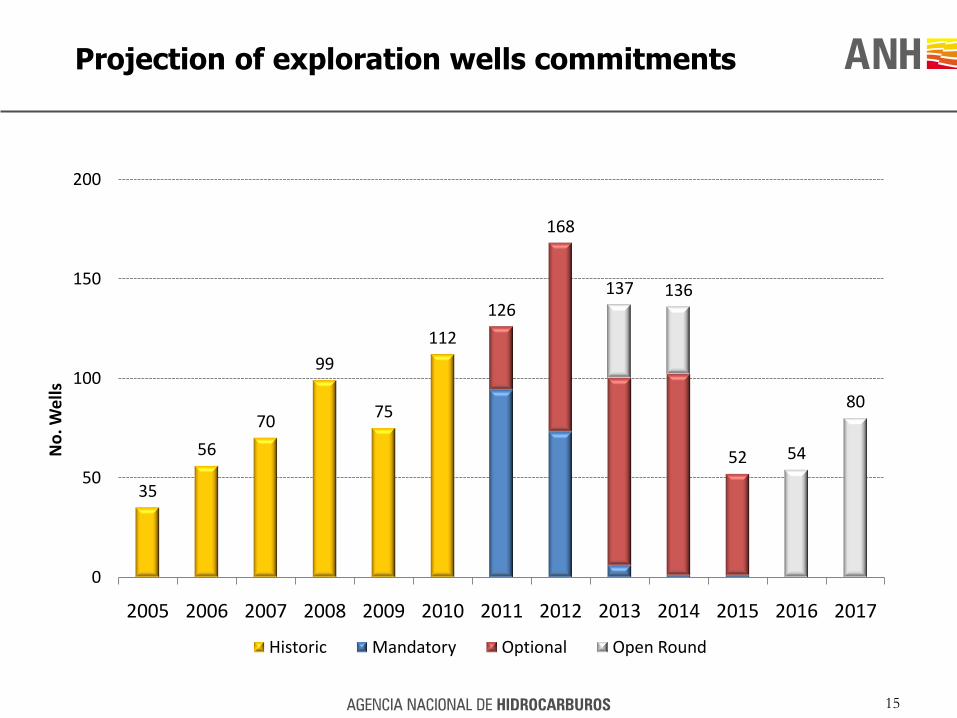

Projection of exploration wells commitments

15

35

56

70

99

75

112

126

168

137 136

52 54

80

0

50

100

150

200

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

No

. We

lls

Historic Mandatory Optional Open Round

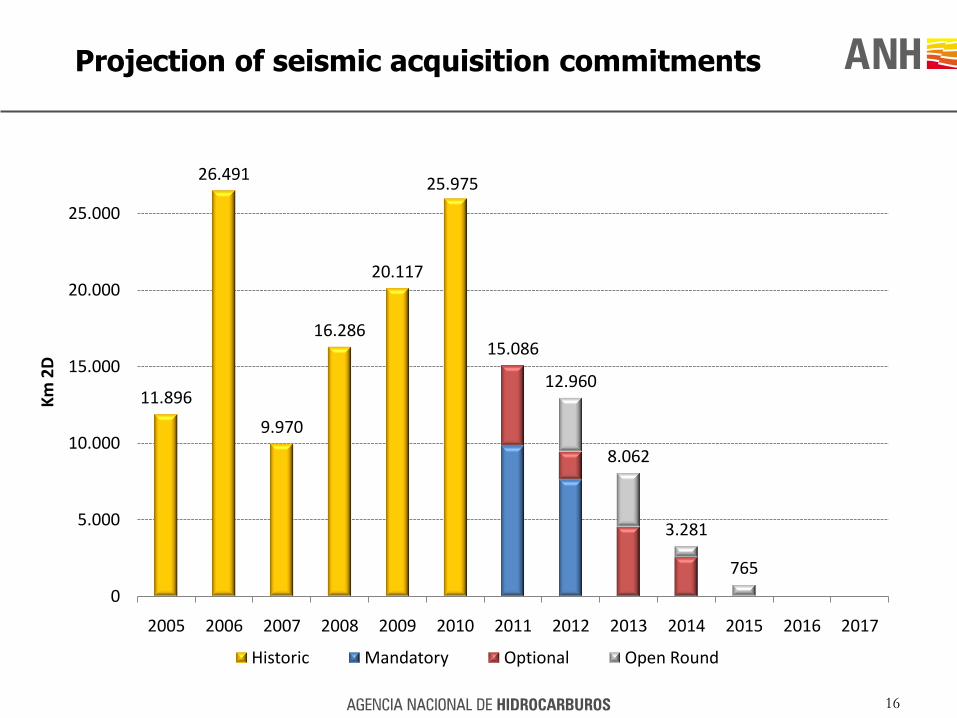

Projection of seismic acquisition commitments

16

11.896

26.491

9.970

16.286

20.117

25.975

15.086

12.960

8.062

3.281

765

0

5.000

10.000

15.000

20.000

25.000

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Km

2D

Historic Mandatory Optional Open Round

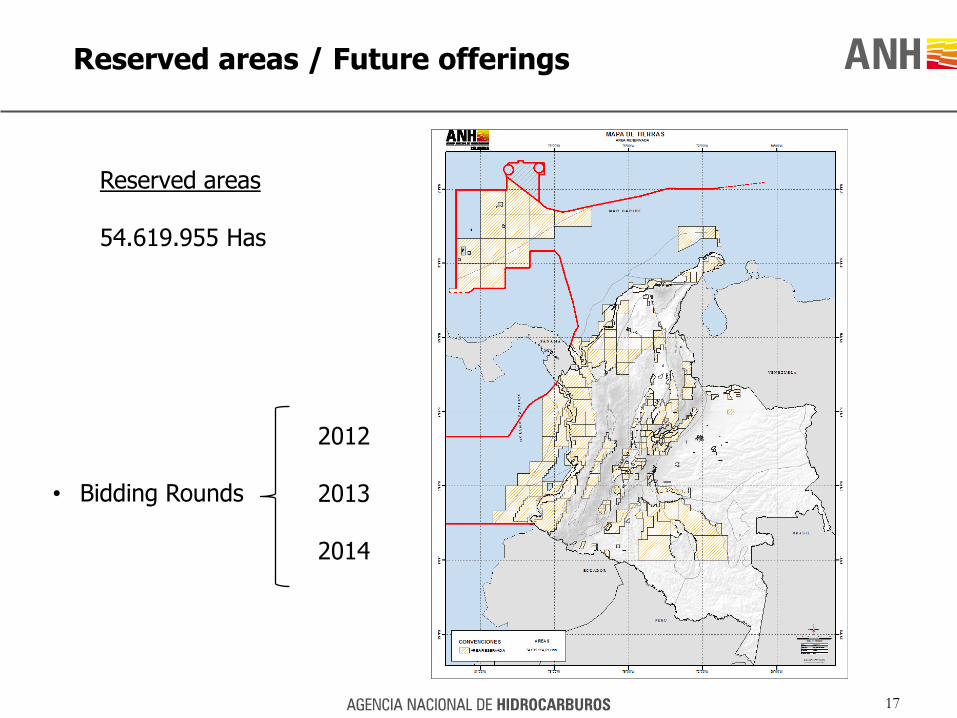

Reserved areas / Future offerings

17

Reserved areas

54.619.955 Has

• Bidding Rounds

2012

2013

2014

Challenges

• Community relations

• Environmental permits

• Transport infrastructure

• Security

• Industry image

• Technology / services / Man power

18

Thank you!

www.anh.gov.co

19