HealthCare Reform Exec Brief - Companies Under 250 Employees

48

Executive Brief Understanding the Impact of Health Care Reform on Your Business in 2015

-

Upload

paul-e-kilzer -

Category

Healthcare

-

view

29 -

download

0

Transcript of HealthCare Reform Exec Brief - Companies Under 250 Employees

Executive BriefUnderstanding the Impact ofHealth Care Reform on Your Business in 2015

<50 50-99 >100

<50 50-99 >100

Company Size

<50 50-99 >100

Elevated

High

Severe

Levels of Risk

AgendaGeneral Overview of Health Care Reform (HCR)

Critical Decisions and Considerations for 2015• Individual Mandate• Employer Shared Responsibility (Play or Pay)• Reporting• Cost Drivers• State Marketplaces

HCR Action Items

Your Business Strategy

insperity.com | 866.210.7415

2

Complexity Compliance Cost

More complexity in workforce management

Increased compliance

burdens

Rising costsfor businesses

General Overview of HCRProvisions 2010 - 2018

Impact to Your Business

• Insurer Mandates• Access to Affordable, Quality Coverage• Taxes, Penalties, Fees and Credits• Reporting and Administration

insperity.com | 866.210.7415

3

Critical Decisions and Considerations for 2015

Individual Mandate

Employer Shared Responsibility (Play or Pay)

Reporting

Cost Drivers

State Marketplaces

insperity.com | 866.210.7415

4

What is it?

Individual Mandate

• Effective January 2014, all individuals must purchase qualifying health coverage

• Limited exceptions apply• Penalties for failure to comply collected through individual’s federal

income tax return

2014

2015

Penalty is $95/adult and $47.50/child (up to $285/family) per yearOR 1% of annual household income, whichever is greater.

Penalty is $325/adult and $162.50/chile (up to $975/family) peryear OR 2% of annual household income, whichever is greater.

Penalty is capped at the national average cost of bronze-level coverage in the state marketplaces. For 2015, that average cost is $207/month for an individual, up from $204/month in 2014.

<50 50-99 >100

ComplexityComplianceCost

insperity.com | 866.210.7415

5

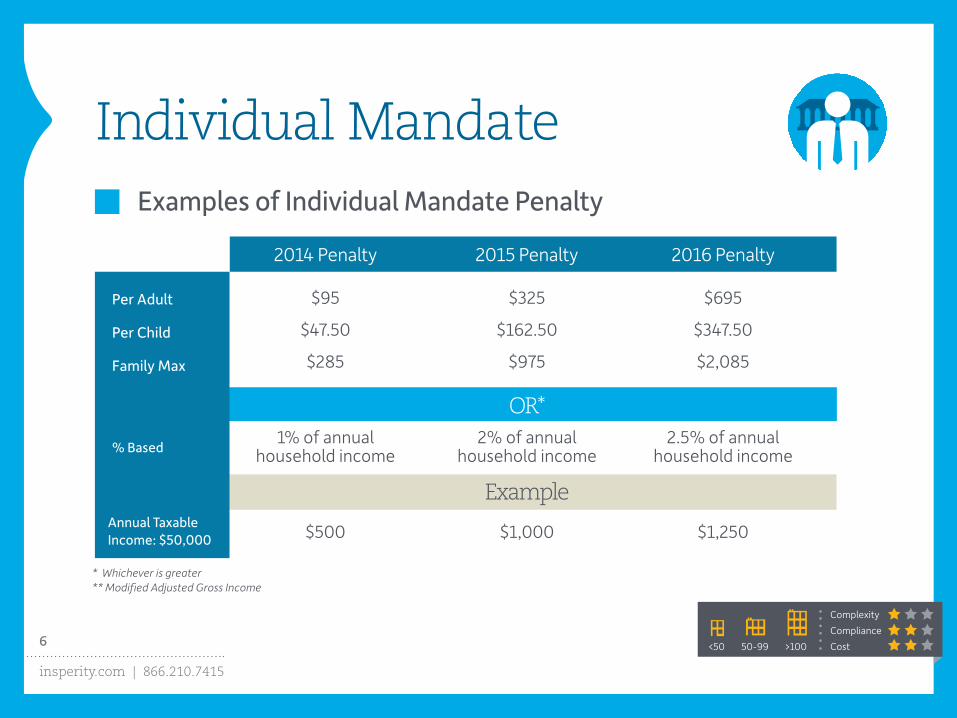

Examples of Individual Mandate Penalty

<50 50-99 >100

ComplexityComplianceCost

2014 Penalty 2015 Penalty 2016 Penalty

% Based

Per Adult

Per Child

Family Max

$95

$47.50

$285

1% of annual household income

$500

2% of annual household income

$1,000

2.5% of annual household income

$1,250

$325

$162.50

$975

$695

$347.50

$2,085

* Whichever is greater** Modified Adjusted Gross Income

OR*

ExampleAnnual Taxable Income: $50,000

Individual Mandate

insperity.com | 866.210.7415

6

2014 IRS Form 1040

<50 50-99 >100

ComplexityComplianceCost

Individual Mandate

insperity.com | 866.210.7415

7

Example of Potential Impact to Your BusinessThe individual mandate may increase participation of employees not enrolled in your plan today

Company ABC HCR Impact

• 40 FTEs*• Offers coverage• 75% participation• 10 FTEs currently not enrolled• $5,000 contribution per employee

A. 10 FTEs (currently not enrolled) enroll because of individual mandate

B. Employer’s cost of offering coverage increases

C. 10 x $5,000 = $50,000

*Full-time employees

<50 50-99 >100

ComplexityComplianceCost

Individual Mandate

insperity.com | 866.210.7415

8

Critical Considerations• Are you prepared to answer employees’ questions?

• Will the penalty change your employees’ behavior?

• Will more employees (and their spouses and dependents) enroll in your health insurance offering?

• What is the impact to your total health care cost?

<50 50-99 >100

ComplexityComplianceCost

Individual Mandate

insperity.com | 866.210.7415

9

Critical Decisions and Considerations for 2015

Individual Mandate

Employer Shared Responsibility (Play or Pay)

Reporting

Cost Drivers

State Marketplaces

insperity.com | 866.210.7415

10

Employer Shared Responsibility (Play or Pay)

Beginning Jan. 1, 2015, employers with 50 or more FTEs (including full-time equivalent employees, or FTEQs) in the prior calendar year* must comply with Play or Pay rules • Called Applicable Large Employers (ALEs)

Applies to employers with 50-99 FTEs in 2014 who: 1. Maintain employee count and total labor hours as of 2/9/2014 through

12/31/2014 – unless necessary for legitimate business reasons, and 2. Maintain approximate health coverage and employer contribution levels

offered as of 2/9/2014 through end of 2015 plan year

Transition Relief from Play or Pay Available for 2015 Only

<50 50-99 >100

ComplexityComplianceCost

*For 2015 only, a period of 6 consecutive months can be used to determine ALE status.

insperity.com | 866.210.7415

11

Employer Shared Responsibility (Play or Pay)

ALEs must offer qualifying coverage to FTEs and dependents (children) or face possible penalties

Under 50 FTEs Rules do not apply Rules do not apply

Offer coverage to ≥95% of FTEs50-99 FTEsRules may apply; Determine eligibility

for Transition Relief (TR);If TR not available, offer coverage

to ≥70% of FTEs

100+ FTEs Offer coverage to ≥70% of FTEs Offer coverage to ≥95% of FTEs

# of FTEs(including equivalents)

2016 and beyond2015

<50 50-99 >100

ComplexityComplianceCost

insperity.com | 866.210.7415

12

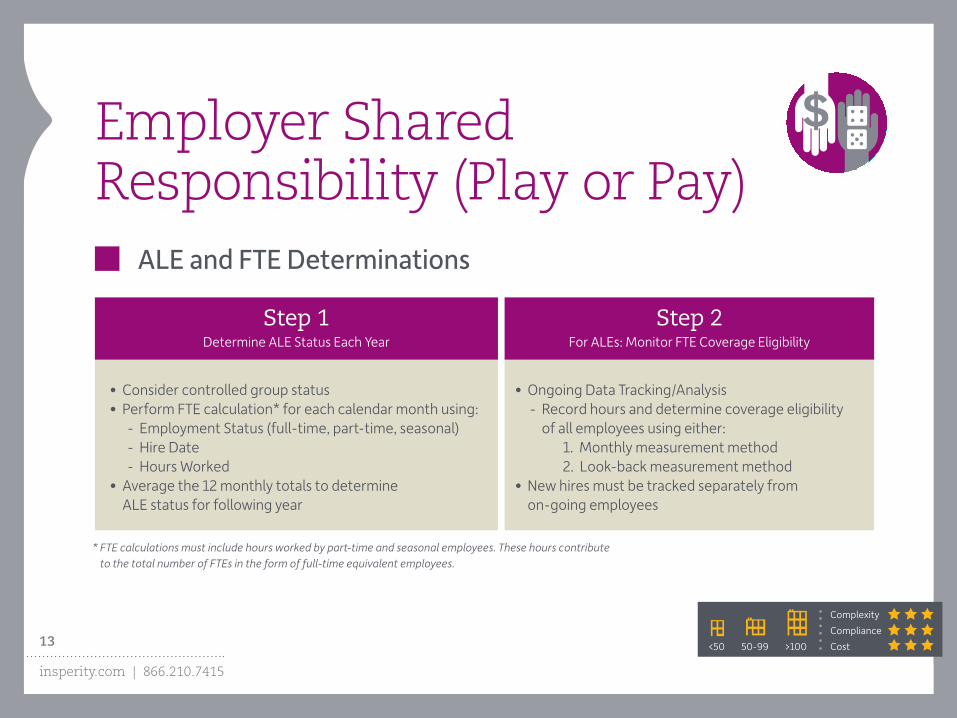

ALE and FTE Determinations

Step 1Determine ALE Status Each Year

Step 2For ALEs: Monitor FTE Coverage Eligibility

• Consider controlled group status• Perform FTE calculation* for each calendar month using: - Employment Status (full-time, part-time, seasonal) - Hire Date - Hours Worked• Average the 12 monthly totals to determine

ALE status for following year

• Ongoing Data Tracking/Analysis - Record hours and determine coverage eligibility

of all employees using either: 1. Monthly measurement method 2. Look-back measurement method• New hires must be tracked separately from

on-going employees

* FTE calculations must include hours worked by part-time and seasonal employees. These hours contribute to the total number of FTEs in the form of full-time equivalent employees.

<50 50-99 >100

ComplexityComplianceCost

Employer Shared Responsibility (Play or Pay)

insperity.com | 866.210.7415

13

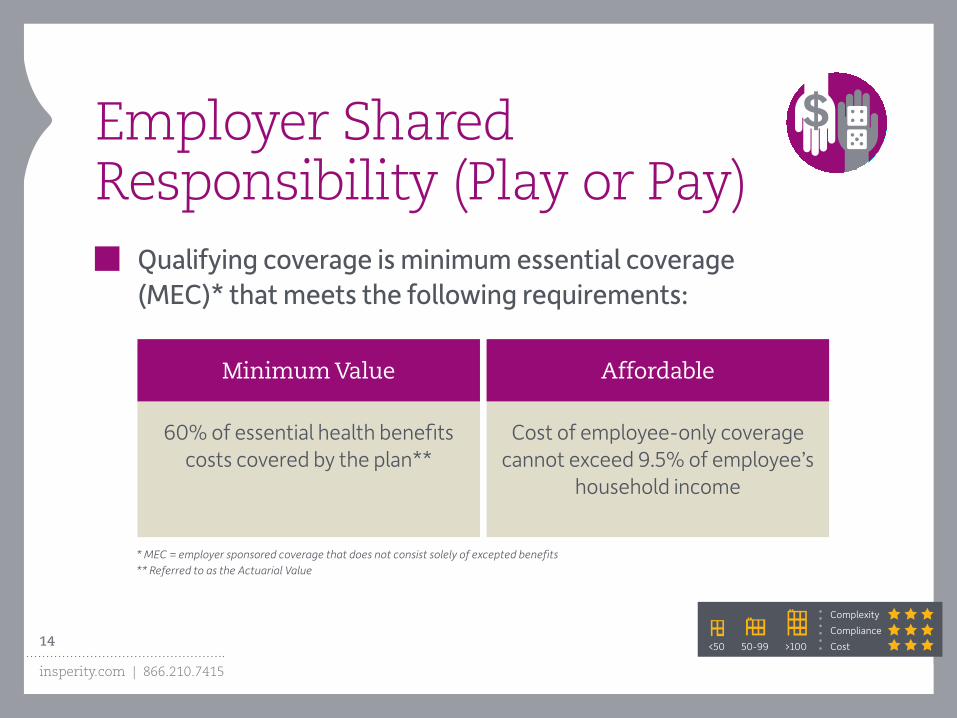

Qualifying coverage is minimum essential coverage (MEC)* that meets the following requirements:

Minimum Value Affordable

60% of essential health benefits costs covered by the plan**

Cost of employee-only coverage cannot exceed 9.5% of employee’s

household income

* MEC = employer sponsored coverage that does not consist solely of excepted benefits** Referred to as the Actuarial Value

<50 50-99 >100

ComplexityComplianceCost

Employer Shared Responsibility (Play or Pay)

insperity.com | 866.210.7415

14

Examples of Potential Impact in 2015

* Penalty could increase to $2,080 based on inflation adjustment clause of ACA. IRS has not yet confirmed this adjusted figure.

** For 2015, less the first 80 FTEs if ALE had 100+ FTEs in 2014*** Offers to <95% FTEs for 2016 and beyond

<50 50-99 >100

ComplexityComplianceCost

Employer Shared Responsibility (Play or Pay)

Company ABC HCR Impact

• 100 FTEs (including FTEQs)

• ≠ MEC, or• Offers MEC to <70% FTEs***

A. 1 FTE goes to state marketplaceB. 1 FTE receives premium tax creditC. Penalty on employer is triggeredD. (100 – 80) x $2,000 = $40,000

Not Offering MEC to at least 70% FTEs. Penalty: $2,000* for all FTEs (less first 80)** if any FTE receives a premium tax credit for state marketplace coverage

insperity.com | 866.210.7415

15

Examples of Potential Impact in 2015

* Penalty could increase to $3,120 based upon inflation adjustment clause of ACA. IRS has not yet confirmed this adjusted figure.

<50 50-99 >100

ComplexityComplianceCost

Employer Shared Responsibility (Play or Pay)

Company ABC HCR Impact

• 100 FTEs (including FTEQs)• Offers Coverage ≠ Minimum Value ≠ Affordable

A. 10 FTEs go to state marketplaceB. 5 FTEs get premium tax creditsC. Penalty on employer is triggeredD. 5 x $3,000 = $15,000

Offering Coverage ≠ Minimum Value or Affordable. Penalty: $3,000* for each FTE who receives a premium tax credit for state marketplace coverage (or the penalty for not offering MEC, whichever is less)

insperity.com | 866.210.7415

16

Employer Shared Responsibility (Play or Pay)

<50 50-99 >100

ComplexityComplianceCost

Critical Considerations• Are you an ALE for 2015 based upon the number of FTEs you had in 2014?

If so, are you measuring hours worked by employees to determine health insurance eligibility?

• Does your business qualify for Transition Relief to defer the possibility of Play or Pay penalties until 2016?

• If you offer health insurance, does it meet the minimum value and affordability requirements?

• What is your exposure to Play or Pay penalties? For instance, do you think any of your full-time employees will receive a premium tax credit (subsidy) for state marketplace coverage? (See Slide 39)

• Have you implemented a compliance strategy?

insperity.com | 866.210.7415

17

Critical Decisions and Considerations for 2015

Individual Mandate

Employer Shared Responsibility (Play or Pay)

Reporting

Cost Drivers

State Marketplaces

insperity.com | 866.210.7415

18

ALE members must report annually on the MEC offered to FTEs (those working an average of 30 or more hours per week) for purposes of Play or Pay penalty assessments. IRS can also levy fines for non-compliance with Reporting rules.

Reporting

• Process mirrors the W-2/W-3 reporting process for wages - First employee benefit statements (Form 1095-C) to be distributed

to all full-time employees by Jan. 31, 2016 - First employer transmittal form (Form 1094-C) to be filed along with

statement copies with IRS by February 28, 2016 (or March 31 if filed electronically for 250 or more forms)

<50 50-99 >100

ComplexityComplianceCost

insperity.com | 866.210.7415

19

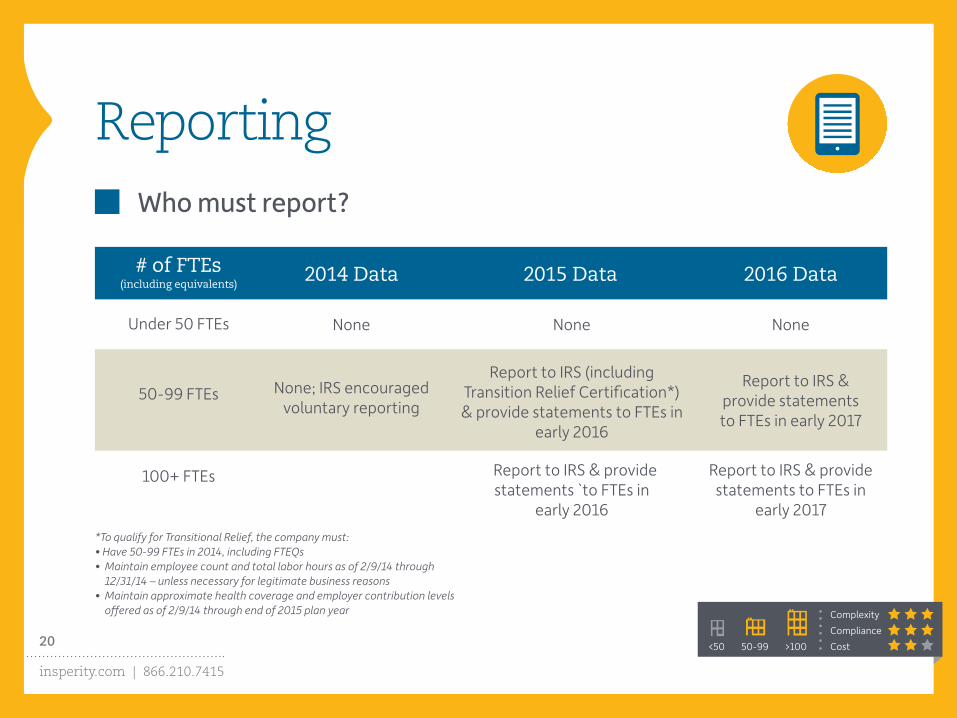

Who must report?

<50 50-99 >100

ComplexityComplianceCost

Under 50 FTEs None None None

50-99 FTEs None; IRS encouraged voluntary reporting

Report to IRS & provide statements `to FTEs in

early 2016

Report to IRS & provide statements to FTEs in

early 2017

Report to IRS (including Transition Relief Certification*) & provide statements to FTEs in

early 2016

Report to IRS & provide statements to FTEs in early 2017

100+ FTEs

# of FTEs(including equivalents)

2016 Data2014 Data 2015 Data

*To qualify for Transitional Relief, the company must:• Have 50-99 FTEs in 2014, including FTEQs• Maintain employee count and total labor hours as of 2/9/14 through

12/31/14 – unless necessary for legitimate business reasons• Maintain approximate health coverage and employer contribution levels

offered as of 2/9/14 through end of 2015 plan year

Reporting

insperity.com | 866.210.7415

20

Current Status: First ALE reports due to IRS in early 2016 to report 2015 calendar-year data.

• Draft forms and instructions issued by IRS in late August 2014 inviting public comment; forms finalized in February 2015

• Data collection and storage at the individual employee level must begin with the 2015 calendar year. For example:

- Eligibility data - Offers of coverage - Months of coverage, including dependent information - Employee-only tier cost of least expensive plan offered

<50 50-99 >100

ComplexityComplianceCost

Reporting

insperity.com | 866.210.7415

21

ALE Employee Statement: IRS Form 1095-C

<50 50-99 >100

ComplexityComplianceCost

18 unique indicator codes will be used on lines 14 and 16. A few examples include:1B-MEC providing MV offered to EE only 1D-MEC providing MV offered to EE & spouse (but not children)1F-MEC not providing MV offered 1H-No offer of coverage

Reporting

insperity.com | 866.210.7415

22

ALE Transmittal: IRS Form 1094-C

<50 50-99 >100

ComplexityComplianceCost

Reporting

insperity.com | 866.210.7415

23

ALE Transmittal: IRS Form 1094-C (continued)

<50 50-99 >100

ComplexityComplianceCost

Use Part II to indicate controlled group status and to attest to eligibility for the Play or Pay Transition Relief for ALEs with 50-99 FTEs in 2014 (Line 22(C))

Reporting

insperity.com | 866.210.7415

24

ALE Transmittal: IRS Form 1094-C (continued)

<50 50-99 >100

ComplexityComplianceCost

Reporting

insperity.com | 866.210.7415

25

ALE Transmittal: IRS Form 1094-C (continued)

<50 50-99 >100

ComplexityComplianceCost

Reporting

insperity.com | 866.210.7415

26

<50 50-99 >100

ComplexityComplianceCost

• W-2 reporting on cost of employer-sponsored coverage for small employers*• Evidence of compliance with state/local requirements• RS Play or Pay penalty determination notices or appeals• Sharing of employee data to verify subsidy eligibility

Potential Reporting

What else is coming?It is widely expected that some form of reporting will be required of ALL employers in order to facilitate operation of state marketplaces and enforcement of HCR regulations.

* Already required for businesses issuing 250 or more Form W-2s

Reporting

insperity.com | 866.210.7415

27

<50 50-99 >100

ComplexityComplianceCost

Payroll

IRS HHS DOL CMS States

Benefits

Your Business

HR Systems

Business

Agencies

Example of Potential Impact to Your BusinessData for required reporting and compliance is typically housed in multiple systems which must then be compiled and organized for reporting to various government agencies.

Reporting

insperity.com | 866.210.7415

28

<50 50-99 >100

ComplexityComplianceCost

Critical Considerations

• Is your business an Applicable Large Employer for 2015 and thus required to prepare and distribute HCR tax forms in early 2016?

• Are you prepared to comply with existing or future reporting requirements?

• Are your payroll processing, benefits administration and HR services managed by multiple systems and/or vendors?

• How will you coordinate the tracking of necessary information on a timely basis?

Reporting

insperity.com | 866.210.7415

29

Critical Decisions and Considerations for 2015

Individual Mandate

Employer Shared Responsibility (Play or Pay)

Reporting

Cost Drivers

State Marketplaces

insperity.com | 866.210.7415

30

<50 50-99 >100

ComplexityComplianceCost

Insurer Excise Tax

Transitional Reinsurance Fee

Patient Centered Outcomes Research Institute Fee

Pharmaceutical Manufacturer Excise Tax

Medical Device Sales Tax

$63 per covered life per year

$2 per covered life per year

$4 per covered life per year

$2 per covered life per year

$44 per covered life per year

$2.08 per covered life per year

$4 per covered life per year

$2 per covered life per year

2.3% of premiums for fully insured plans

2.3% of premiums for fully insured plans

Examples and Estimated Impact of Taxes and Fees

20152014

Cost DriversWhat are they?Taxes and fees on insurers/health care industry are estimated to increase costs for businesses by 3.5% to 4%, or $400 per employee per year.

insperity.com | 866.210.7415

31

<50 50-99 >100

ComplexityComplianceCost

• Rating bands compressed to 3:1 – premium costs between old and young are compressed

• Guaranteed issue and renewability – no one can be denied coverage• Cannot increase rates or deny coverage for pre-existing conditions• Underwriting criteria limited to age, family size (coverage tier), geography and tobacco use

• Essential health benefits (EHB) must be included• Out-of-pocket maximums shift costs to insurer• Elimination of annual benefit limits on EHB increases carriers’ liability• Maximum 90-day wait period for extending benefits coverage

Adjusted Community Rating

Underwriting Restrictions

Plan Design Mandates

Cost Drivers: Employers <50 FTEs

What are they?Taxes and fees on insurers/health care industry are estimated to increase costs for businesses by 3.5% to 4%, or $400 per employee per year.

NOTE: Many provider networks being narrowed to offset increased coverage costs.

insperity.com | 866.210.7415

32

<50 50-99 >100

ComplexityComplianceCost

$$$

$

Cost Drivers: Employers <50 FTEs

Adjusted Community Rating

Impact on Small Group Health Insurance Costs

Younger Older

Current State 3:1 Ratio

Prior State 8:1 Ratio*

insperity.com | 866.210.7415

33

<50 50-99 >100

ComplexityComplianceCost

Cost Drivers: Employers <50 FTEs

Limited Underwriting Criteria

Before 2014 Now

• Family size (Coverage tier)*• Age• Gender• Geographic area• Occupation• Industry• Tobacco use• Weight• Health status• Claims history• And more...

• Family size (Coverage tier)*• Age• Geographic area• Tobacco use

* Indicates who is covered by policy (e.g., individual, individual plus spouse, individual plus children, etc.)

insperity.com | 866.210.7415

34

<50 50-99 >100

ComplexityComplianceCost

Cost Drivers: Employers <50 FTEs

Deadline Extensions

• The federal government will allow some noncompliant small group health plans to renew through Oct. 1, 2016.

• State insurance commissioners will decide whether to honor the extension and for what period of time.

• Affected provisions include: - Adjusted community rating - Limited underwriting criteria - Guaranteed issue

- Pre-existing conditions for adults- Essential health benefits- Out-of-pocket maximums

insperity.com | 866.210.7415

35

<50 50-99 >100

ComplexityComplianceCost

• Rating bands compressed to 3:1 – premium costs between old and young are compressed*

• Guaranteed issue and renewability – no one can be denied coverage• Cannot increase rates or deny coverage for pre-existing conditions• Underwriting criteria limited to age, family size (coverage tier), geography and tobacco use*

• Essential health benefits (EHB) must be included*• Out-of-pocket maximums shift costs to insurer• Elimination of annual benefit limits on EHB increases carriers’ liability• Maximum 90-day wait period for extending benefits coverage

Adjusted Community Rating

Underwriting Restrictions

Plan Design Mandates

Cost Drivers: Employers 50-99 and 100+ FTEs

What are they?

* These restrictions and mandates will apply to businesses with ≤100 employees in 2016.

insperity.com | 866.210.7415

36

<50 50-99 >100

ComplexityComplianceCost

Cost Drivers: Critical Considerations

• Will new small group regulations increase your costs?

• What impact will taxes and fees have on your cost structure?

• Can you modify your plan designs to offset expected cost increases?

• Should you adjust employee contributions to offset higher costs?

• Can you adjust your product or service prices to cover expected increases in expenses?

insperity.com | 866.210.7415

37

Critical Decisions and Considerations for 2015

Individual Mandate

Employer Shared Responsibility (Play or Pay)

Reporting

Cost Drivers

State Marketplaces

insperity.com | 866.210.7415

38

<50 50-99 >100

ComplexityComplianceCost

State MarketplacesWhat are they?

• State marketplaces were established for individuals and small businesses to view, compare and purchase health insurance

• Subsidies for individuals are available on a sliding scale for those earning between 100% and 400% of federal poverty level (FPL)

- $46,680 for individual, $95,400 for family of four (2014 FPL) - Primarily available for coverage obtained through marketplaces - Unavailable to FTEs if employer offers qualified coverage

• Small Business Health Options Program (SHOP) - Businesses with 50 or fewer FTEs are eligible - Limited access and product choices in 2015

insperity.com | 866.210.7415

39

<50 50-99 >100

ComplexityComplianceCost

State MarketplacesImpact to Your Business

• Employers relying on state marketplaces for employee medical coverage may be disadvantaged against competitors who attract and retain top talent through a comprehensive benefits strategy

• Since October 2013, employers must distribute a “Notice of Exchanges and Subsidies” to all new hires within 14 days of their start date

• State marketplaces may not provide a consistent health insurance solution for employees across multiple states

• State marketplace products may be limited to medical, dental and Rx only, requiring you to seek other solutions for ancillary insurance products (e.g., vision, life, disability, etc.)

insperity.com | 866.210.7415

40

<50 50-99 >100

ComplexityComplianceCost

State MarketplacesCritical Considerations

• Are you distributing the marketplace notice to your new hires within 14 days of their start date?

• Are you prepared to answer your employees’ questions on the state marketplaces?

• Are you aware that some of your employees could incur greater costs by purchasing coverage through state marketplaces?

• Are your employees prepared to purchase insurance on their own?

insperity.com | 866.210.7415

41

Your Company is ResponsibleTo Do<50 FTEs* 50-99 FTEs* 100+ FTEs*

2015 HCR Action ItemsTo Do

Are you distributing the marketplace notice to your new hires within 14 days of their start date?

Expect market reforms to continue to impact cost of group health insurance.

Ensure group health plan design meets HCR coverage requirements (e.g., no pre-existing condition exclusions, must include essential health benefits coverage with no annual dollar limits).

Make sure the waiting period for your group health coverage eligibility does not exceed 90 days from employee’s date of hire (except where state law may be more restrictive).

Issue “Notice of Exchanges and Subsidies” to all new hires within 14 days of their start date.**

insperity.com | 866.210.7415

42

2015 HCR Action Items

Your Company is ResponsibleTo Do<50 FTEs* 50-99 FTEs* 100+ FTEs*

Ensure that incongruent compliance regulations are being followed if you have employees working in different states.

Provide an informed and reliable resource to answer employee questions about various aspects of the new healthcare laws (e.g., individual mandate penalties, marketplace subsidies, mandatory coverage levels).

Secure an authoritative and reliable information resource to keep your business well informed about rapidly evolving rules and regulations.

Make sure your Health Flexible Spending Account (FSA) annual employee contribution maximum does not exceed $2,500.***

Make sure you are withholding the additional 0.9% Medicare Tax on high wage employees (different thresholds may apply depending upon employee filing status).***

insperity.com | 866.210.7415

43

2015 HCR Action Items

Your Company is ResponsibleTo Do<50 FTEs* 50-99 FTEs* 100+ FTEs*

Provide employees with a standard “Summary of Benefits and Coverage” that explains their coverage and costs.***

Return or reinvest any Medical Loss Ratio Rebates paid by insurance carrier.***

Include HCR reporting and compliance costs when you determine your 2015 and 2016 budgets.

If not already completed, build your data tracking and analysis systems for 2015 reporting requirements, including new IRS report for ALEs.

Track FTE information for determination of your 2016 Applicable Large Employer (ALE) status, by calendar month throughout 2015. Catch up on your 2015 ALE status if not already completed.

Track hours worked and measure all employees to meet coverage eligibility requirements.

insperity.com | 866.210.7415

44

2015 HCR Action Items

Your Company is ResponsibleTo Do<50 FTEs* 50-99 FTEs* 100+ FTEs*

Prepare for additional IRS reporting requirements that become effective in 2015.

Determine if you qualify for 2015 Transitional Relief from Play or Pay penalties.

Decide if you will Play or Pay in 2015 by offering qualified coverage that meets minimum value and affordability requirements to at least 70% of your FTEs in 2015 or risk paying a penalty.

Determine your plan’s measurement, administration and stability periods for eligibility and coverage.

Report the aggregate cost of employer-provided group health plan coverage on employee W-2s if you issue 250 or more forms annually, beginning with 2012 form W-2.***

*FTEs: Full-time employees, including full-time equivalent employees (FTEQs)**For businesses covered by the Fair Labor Standards Act (FLSA)***Required by Health Care Reform prior to 2015

insperity.com | 866.210.7415

45

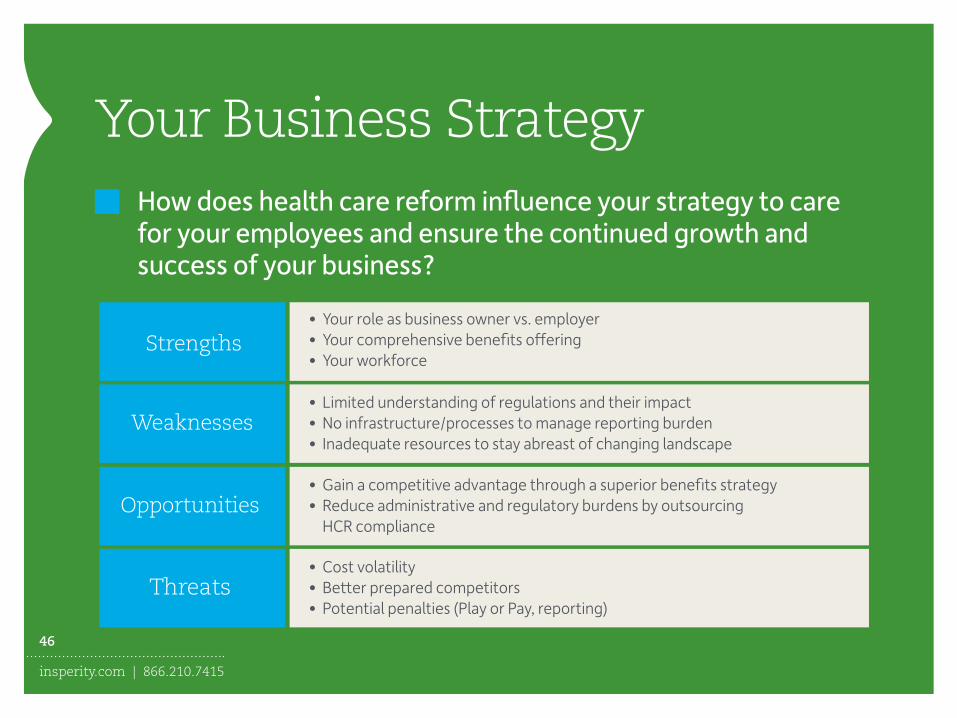

Your Business StrategyHow does health care reform influence your strategy to care for your employees and ensure the continued growth and success of your business?

Strengths

Weaknesses

Opportunities

Threats

• Your role as business owner vs. employer• Your comprehensive benefits offering• Your workforce

• Limited understanding of regulations and their impact• No infrastructure/processes to manage reporting burden• Inadequate resources to stay abreast of changing landscape

• Gain a competitive advantage through a superior benefits strategy• Reduce administrative and regulatory burdens by outsourcing

HCR compliance

• Cost volatility• Better prepared competitors• Potential penalties (Play or Pay, reporting)

insperity.com | 866.210.7415

46

Why InsperityInsperity offers solutions that address the challenges of health care reform. Here’s how we can help your business:

Complexity Compliance Cost

Reduce administrative burdens through a dedicated service

team and best-in-class IT infrastructure

in workforce management

Minimize risk of fines and penalties through continuous monitoring of changing federal and

state regulations

Stabilize health care costs through our

fully insured health plan and its

low-cost structure

For more than 28 years, Insperity has provided large company benefits and employment administration to America’s best small and midsize businesses.

insperity.com | 866.210.7415

47

Legal Notice

Your Company is ResponsibleTo Do<50 FTEs* 50-99 FTEs* 100+ FTEs*

The information provided in this communication is for educational and informational purposes only, and is not legal advice.

IRS Circular 230 Disclaimer: To ensure compliance with requirements imposed by the IRS, we inform you that any U.S. federal tax advice contained in this communication (including any attachments) is not intended or written to be used, and cannot be used, for the purpose of (i) avoiding penalties under the Internal Revenue Code or (ii) promoting, marketing or recommending to another party any transaction or matter addressed herein. You should seek advice based on your particular circumstances from an independent tax advisor with respect to any federal tax transaction or matter addressed herein.

82-896 | HCR-P0215-231insperity.com | 866.210.7415

48