Health Insurance Exchange and ACA -...

54

Health Insurance Exchange and the ACA Presented by: West Virginia Offices of the Insurance Commissioner

Transcript of Health Insurance Exchange and ACA -...

Health Insurance Exchange gand the ACA

Presented by: West Virginia Offices of the Insurance Commissioner

STATE WORK ON EXCHANGESTATE WORK ON EXCHANGE• Need to work with multiple state and federal agenciesstate and federal agencies

• Need to work with multiple stakeholders

• Need to implement in conjunction with other reformsreforms

• Limited Resources

• Limited Guidance

• Limited Time

WORK TO DATE OVERVIEWWORK TO DATE OVERVIEW• Coordination with other

states• Discussions with NAIC and

HHSstates• Review of other

exchanges (past and present)

HHS

• Discussions with constituent state agenciespresent)

• Technical Assistance from national think tanks/ experts

constituent state agencies

• Discussions with stakeholdersexperts

• Stakeholder Engagement• NAIC Exchange Subgroup

• Plans to be at table when HHS develops rules

member • Planning Exchange Grant

RECENT WORKRECENT WORK• Submitted PEG Grant• NAIC Exchange

• Presented to independent agents• NAIC Exchange

Subgroup Meeting• NGA Meeting in VT

independent agents, medical association, GOHELP, and at WV g

• Contributing to NASHP exchange discussions

• Submitted SHAP Budget

Health Summit• WV plans for Request f C t• Submitted SHAP Budget

• Discussions with CHIP/ DHHR regarding

for Comment• Met with key legislators• Further research on

g geligibility • Further research on

technical infrastructure

SHAP and FED HEALTH REFORM

PLANNING EXCHANGE GRANTPLANNING EXCHANGE GRANT• Submitted Late AugustA d E t d b S t b 30• Award Expected by September 30

• Technical Assistance from Dr. Gruber of MIT and Jon KingsdaleJon Kingsdale

• Shared plans with several stakeholder groups• Fairly aggressive work planFairly aggressive work plan• Leverage with SHAP and draw down next round of OCIIO exchange grants for big ticket g g gprocurements

PEG OBJECTIVESPEG OBJECTIVES•Consumer Survey •Project Facilitation • Industry Survey•Actuarial and Economic

Contract

•Exchange Strategic PlanAssessment/ Model

•Policy Model and

•Education and Outreach Plan

Planning Assessment •Technological Infrastructure Plan

•Business Plan

STAFF DEVELOPMENTSTAFF DEVELOPMENTCurrent Staff New Staff

•Health Policy•Rates and Forms

•Health Insurance Attorney•Education/ Outreach S

•Consumer Service

• Information Technology

Spec.•Procurement/Financial Officergy

• Legal• Finance

Officer•Health Policy Researcher• Insurance Program Spec.Finance

•ExecutiveInsurance Program Spec.

•Office Secretary

REQUEST FOR COMMENTREQUEST FOR COMMENT•Released Early August•Contributing to NAIC and •Due October 4th

•HHS outlined several

NGA Submission

•Reached out to other categories of questions

•Question whether states

state agencies

•May submit WV state

are yet positioned to address exchange RFC

agency comments as whole or go through NAIC/NGA • State Issuer Comments?NAIC/NGA

STAKEHOLDER STRATEGYSTAKEHOLDER STRATEGY• Launch stakeholder •Continue to be available

f i / meetings around state by mid/late October

for presentations/ discussions

•Engage Legislature •After statewide stakeholder meeting develop community of

•Engage Legislature•Engage carriers in regulator/issuer only develop community of

interest groups to focus on specific exchange issues

g / ymeetings

•Plans to set up project b i

specific exchange issuesmanagement website

INSURANCE EXCHANGE CONCEPTO i i t i k t• Organizes private insurance market

• Provides platform for carrier plans

• Expands size of risk pool

• Streamlines administration for carriersStreamlines administration for carriers

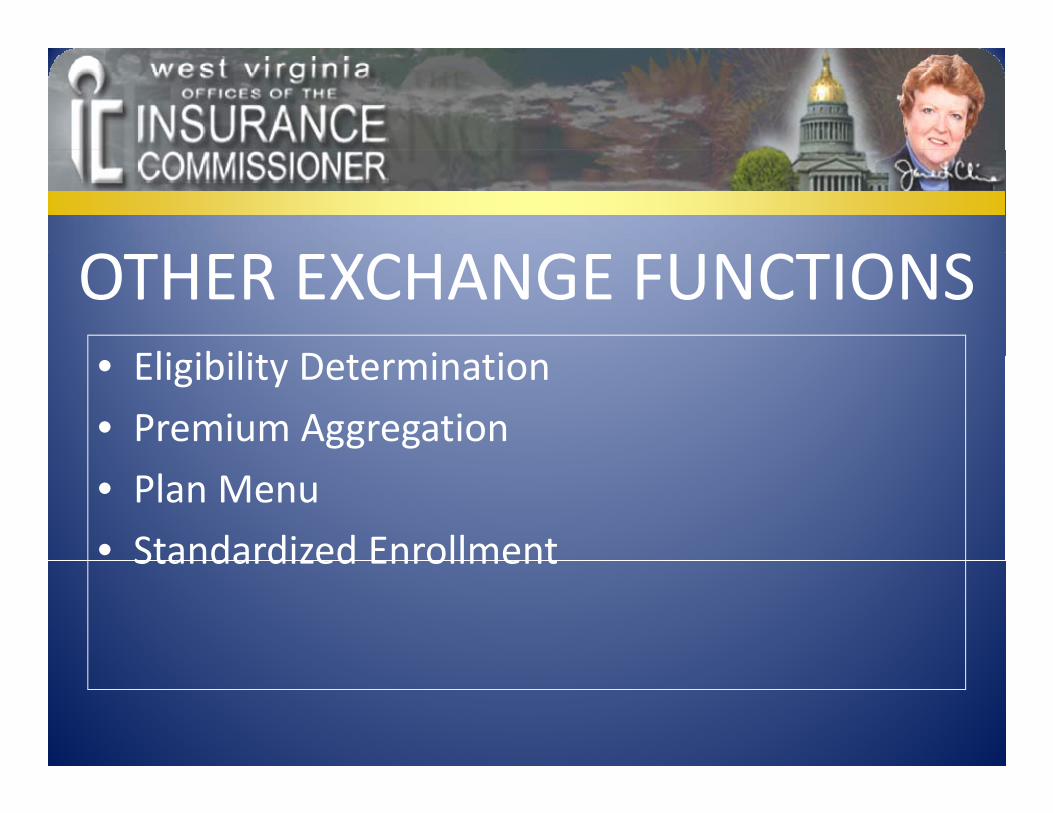

OTHER EXCHANGE FUNCTIONSEli ibilit D t i ti• Eligibility Determination

• Premium Aggregation

• Plan Menu

• Standardized EnrollmentStandardized Enrollment

ANCILLARY EXCHANGE FUNCTIONS

S ifi t d F d l E l

HISTORY OF EXCHANGES• Specific trade or professional groups

• Federal Employees Health Benefits Program (FEHBP)

• State operated small group exchange

Program (FEHBP)

• Medicare Advantagegroup exchange • Medicare Advantage

HISTORY OF EXCHANGES

HISTORY OF EXCHANGESHISTORY OF EXCHANGES

Nuts and Bolts

MASSACHUSETTS CONNECTORTakeaway for WVNuts and Bolts

• Flagship of statewide exchange effort

Takeaway for WV

• MA is to WV as apples are to oranges but WV can learng

• Resulted from bipartisan health reform efforts in 2006

g

• Engage stakeholders

• Make exchange available • Two exchanges:

– Commonwealth Care

– Commonwealth Choice

through various means

• Strongly consider enrollment designated periodsdesignated periods

HISTORY OF EXCHANGESHISTORY OF EXCHANGES

Nuts and Bolts

UTAH EXCHANGETakeaway for WVNuts and Bolts

• Driven by state health reform legislation in 2008 d 2009

Takeaway for WV

• Test exchange before launch

• Keep it simpleand 2009• Still testing system • Initial focus on small group

Keep it simple

• Employer chooses default plan for employeesInitial focus on small group

• Much smaller scope than MA exchangeH il li t b k

• Need to develop All Payer Database

• Premium Aggregator• Heavily reliant on brokers • Premium Aggregator

ACA EXCHANGE TIMELINEACA EXCHANGE TIMELINETimeline

• September 2010 through January 2015‐ HHS grant awards

• January 1, 2013‐ HHS must know state’s exchange plan

• January 1, 2014‐ State must implement exchange

h• January 2015‐ Exchange must be self‐sustaining

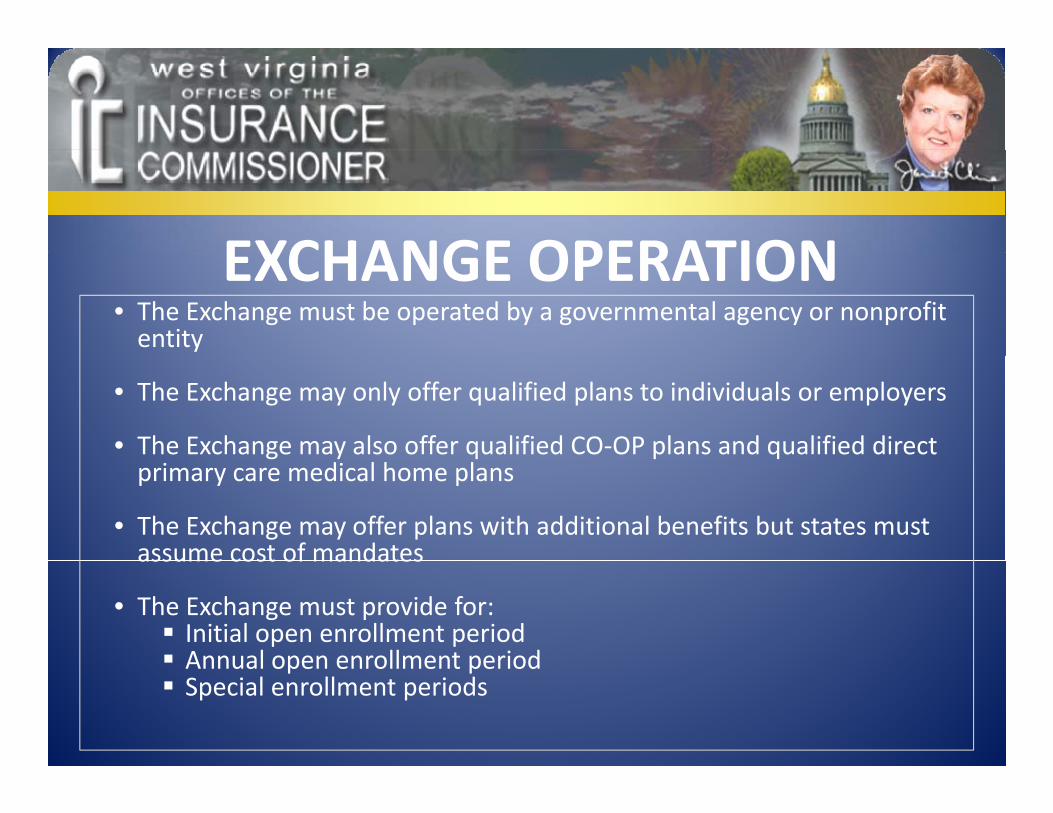

EXCHANGE OPERATIONEXCHANGE OPERATION• The Exchange must be operated by a governmental agency or nonprofit entity

• The Exchange may only offer qualified plans to individuals or employers

• The Exchange may also offer qualified CO‐OP plans and qualified direct g y q p qprimary care medical home plans

• The Exchange may offer plans with additional benefits but states must assume cost of mandatesassume cost of mandates

• The Exchange must provide for: Initial open enrollment period Annual open enrollment periodAnnual open enrollment period Special enrollment periods

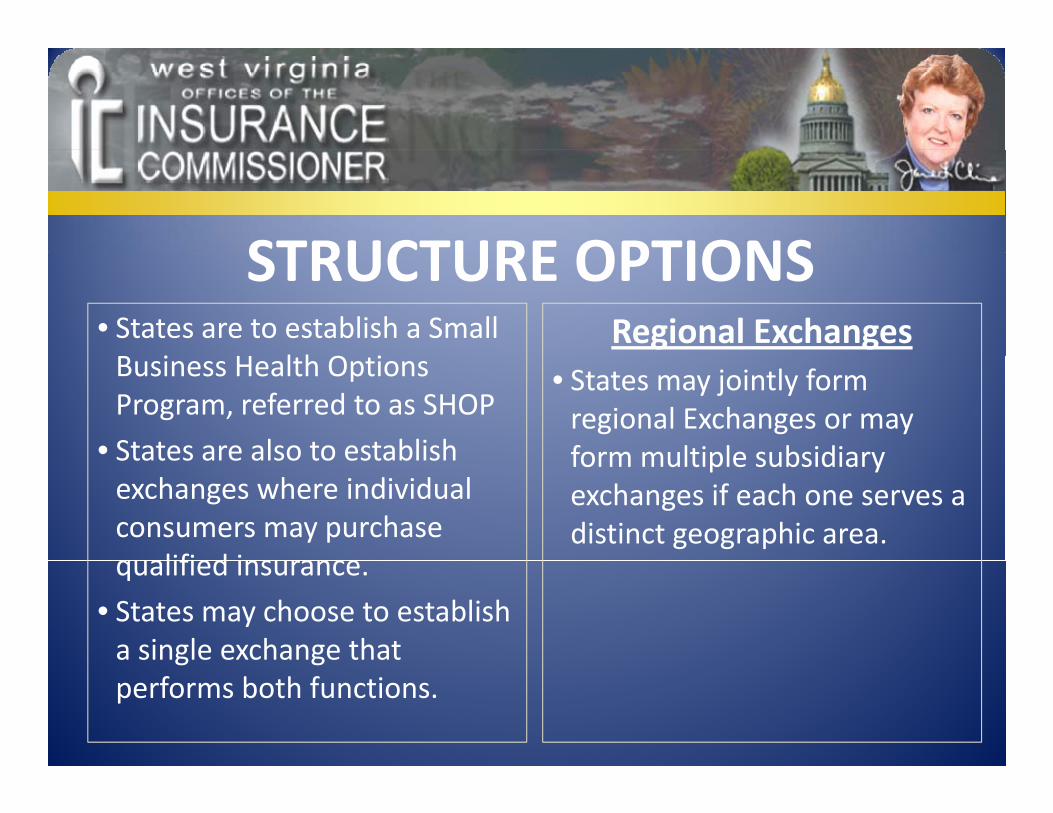

STRUCTURE OPTIONSSTRUCTURE OPTIONSRegional Exchanges• States are to establish a Small

i l h i • States may jointly form regional Exchanges or may form multiple subsidiary

Business Health Options Program, referred to as SHOP

• States are also to establish form multiple subsidiary exchanges if each one serves a distinct geographic area.

States are also to establish exchanges where individual consumers may purchase qualified insurancequalified insurance.

• States may choose to establish a single exchange that g gperforms both functions.

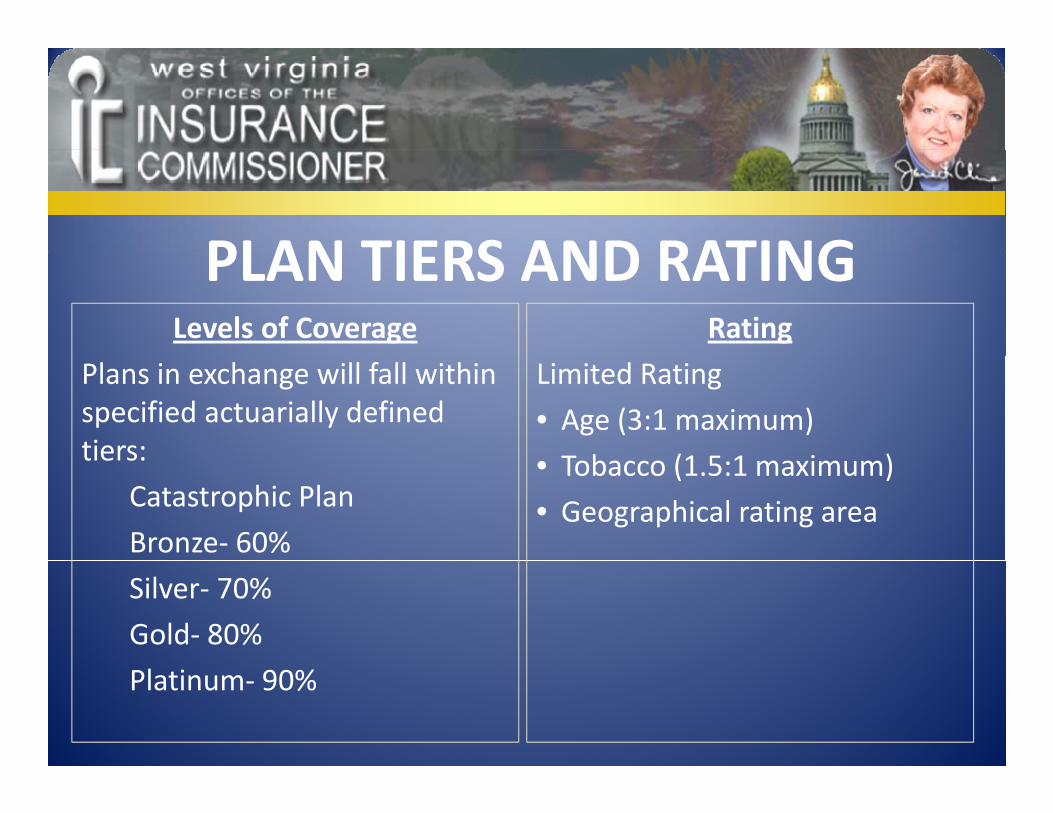

PLAN TIERS AND RATINGPLAN TIERS AND RATINGLevels of Coverage Rating

Plans in exchange will fall within specified actuarially defined tiers:

Limited Rating

• Age (3:1 maximum)

T b (1 5 1 i )tiers:

Catastrophic Plan

Bronze‐ 60%

• Tobacco (1.5:1 maximum)

• Geographical rating area

Silver‐ 70%

Gold‐ 80%

Platinum‐ 90%

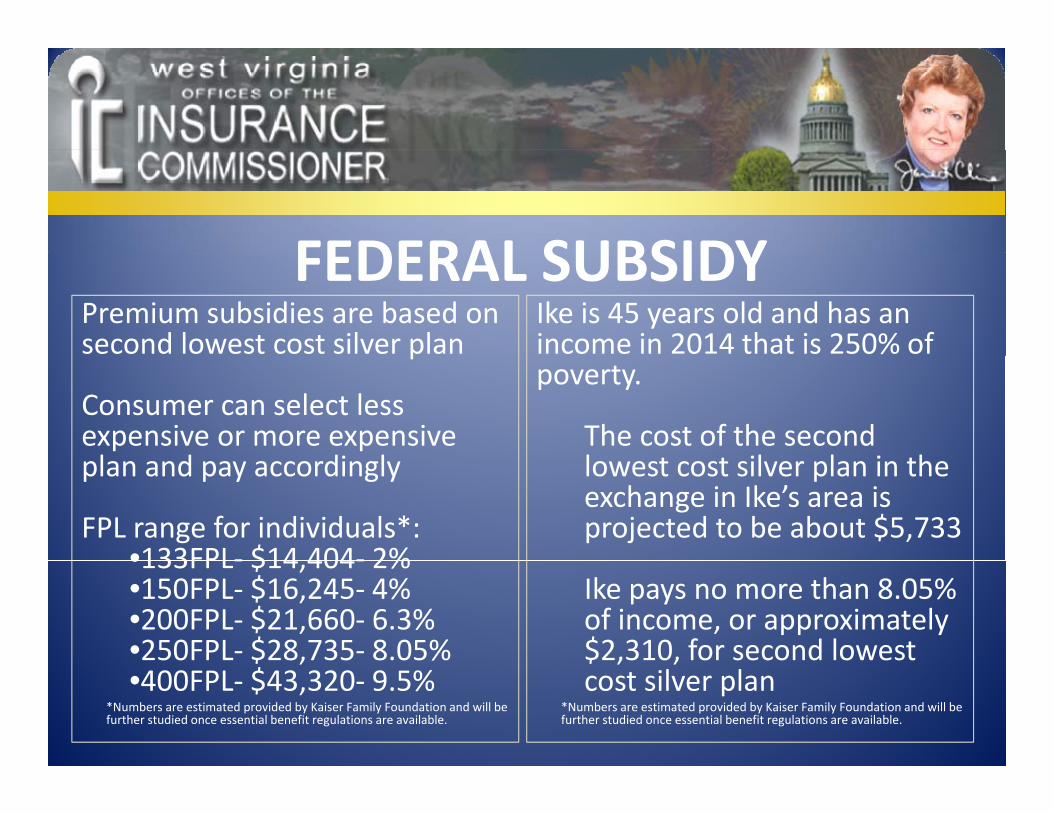

FEDERAL SUBSIDYFEDERAL SUBSIDYPremium subsidies are based on second lowest cost silver plan

Ike is 45 years old and has an income in 2014 that is 250% of p

Consumer can select less expensive or more expensive l d di l

poverty.

The cost of the second l t t il l i thplan and pay accordingly

FPL range for individuals*:•133FPL‐ $14 404‐ 2%

lowest cost silver plan in the exchange in Ike’s area is projected to be about $5,733

•133FPL‐ $14,404‐ 2%•150FPL‐ $16,245‐ 4%•200FPL‐ $21,660‐ 6.3%•250FPL‐ $28,735‐ 8.05%

Ike pays no more than 8.05% of income, or approximately $2,310, for second lowest $ ,

•400FPL‐ $43,320‐ 9.5%*Numbers are estimated provided by Kaiser Family Foundation and will be further studied once essential benefit regulations are available.

$ , ,cost silver plan

*Numbers are estimated provided by Kaiser Family Foundation and will be further studied once essential benefit regulations are available.

SHOP EXCHANGESSHOP EXCHANGES

• Small Group defined as 1‐100 employees

• State may elect to define as

• Employees given choice of carrier

• Employer chooses coverageState may elect to define as 1‐50 until January 1, 2016

• State may elect to combine non gro p and small gro p

Employer chooses coverage level

• Employees choose from carriers offering at that le elnon‐group and small group

marketscarriers offering at that level

• Employees individually rated

PLAN COST SHARINGPLAN COST SHARINGCost Sharing and Deductibles Cost Sharing

• Cost‐sharing under a health plan may not exceed the cost‐sharing for the bronze plan

• There will be additional cost‐sharing subsidies for eligible individuals and families withsharing for the bronze plan

• Deductibles for plans in the small group market are limited

individuals and families with income up to 250% of the federal poverty level.

small group market are limited to $2,000 individual/$4,000 family, indexed to average premium growth.

CONSUMER CHOICECONSUMER CHOICEConsumer Choice in ExchangeConsumer Choice of Insurance

• Individuals may choose any

plan in exchange

• To be eligible for federal subsidy (those between 133‐400 FPL) consumers must use

• Employers will designate tier of

400 FPL) consumers must use exchange

plans for which employees are

eligible

• Only lawful residents may purchase coverage in exchange

PLANS AVAILABLEPLANS AVAILABLEQualified Health Plans

• Provide, at minimum, defined benefits package

C i t• Carrier must:

• be licensed and in good standing; g;

• offer at least one silver and one gold plan;

• charge same premium for plan in and out of exchange

EXCHANGE BENEFITSEXCHANGE BENEFITSACA BenefitsACA Benefits

• Prescription drugs• Rehab services and devices

• Ambulatory patient servicesE i • Laboratory services

• Preventive and wellness

• Emergency services• Hospitalization• Maternity and newborn • Chronic disease

management• Pediatric services oral

• Maternity and newborn care

• Behavioral health services • Pediatric services‐ oral, vision

Behavioral health services

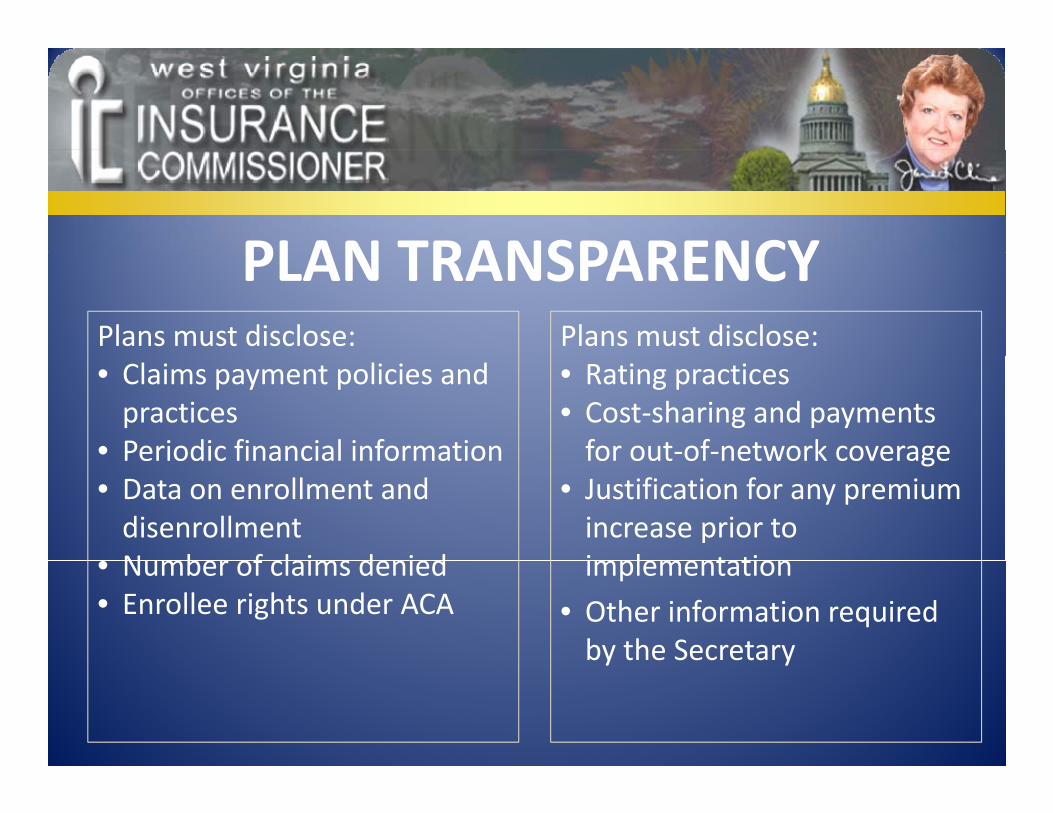

PLAN TRANSPARENCYPLAN TRANSPARENCYPlans must disclose: Plans must disclose:• Claims payment policies and practices

• Periodic financial information

• Rating practices• Cost‐sharing and payments for out‐of‐network coveragePeriodic financial information

• Data on enrollment and disenrollment

• N mber of claims denied

for out of network coverage• Justification for any premium increase prior to implementation• Number of claims denied

• Enrollee rights under ACAimplementation

• Other information required by the Secretaryy y

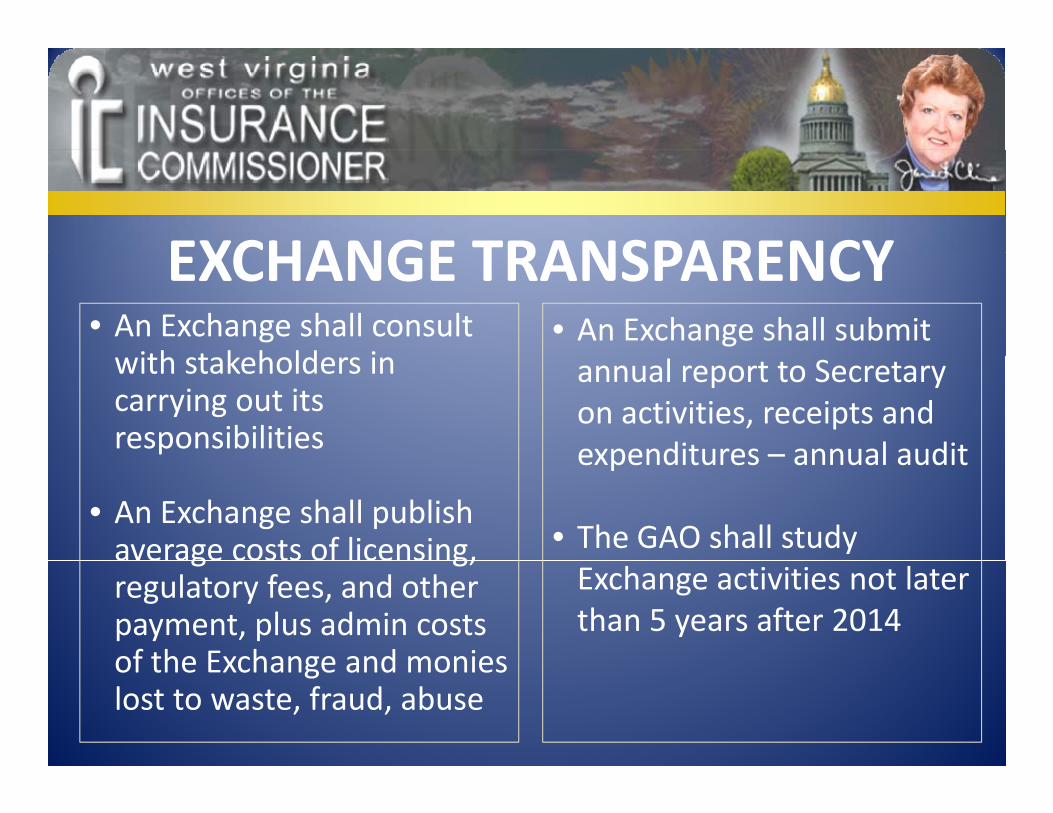

EXCHANGE TRANSPARENCYEXCHANGE TRANSPARENCY• An Exchange shall submit • An Exchange shall consult

ith t k h ld i annual report to Secretary on activities, receipts and expenditures – annual audit

with stakeholders in carrying out its responsibilities expenditures annual audit

• The GAO shall study • An Exchange shall publish average costs of licensing,

Exchange activities not later than 5 years after 2014

a e age costs o ce s g,regulatory fees, and other payment, plus admin costs of the Exchange and moniesof the Exchange and monies lost to waste, fraud, abuse

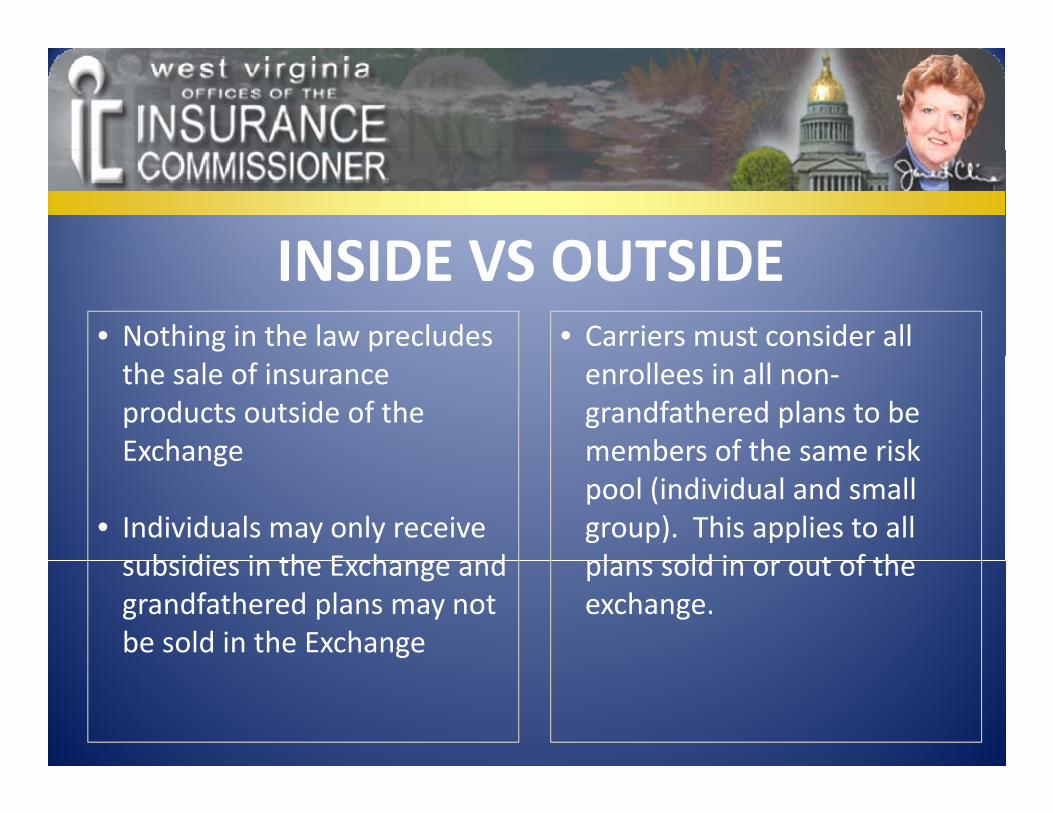

INSIDE VS OUTSIDEINSIDE VS OUTSIDE • Nothing in the law precludes • Carriers must consider all the sale of insurance products outside of the Exchange

enrollees in all non‐grandfathered plans to be members of the same riskExchange

• Individuals may only receive s bsidies in the E change and

members of the same risk pool (individual and small group). This applies to all plans sold in or o t of thesubsidies in the Exchange and

grandfathered plans may not be sold in the Exchange

plans sold in or out of the exchange.

ADDRESSING RISKADDRESSING RISK• Transitional Reinsurance • Temporary Risk Corridors Program Secretary and NAIC to establish a mandatory

Secretary to establish risk corridors for 2014‐2016

establish a mandatory reinsurance program for 2014‐2016 Ins rers and TPAs m st

• Risk Adjustment Each state will operate risk adj stment based on Insurers and TPAs must

contribute Total contributions to be

risk adjustment based on criteria developed by the Secretary in consultation

based on estimates of the NAIC

with states

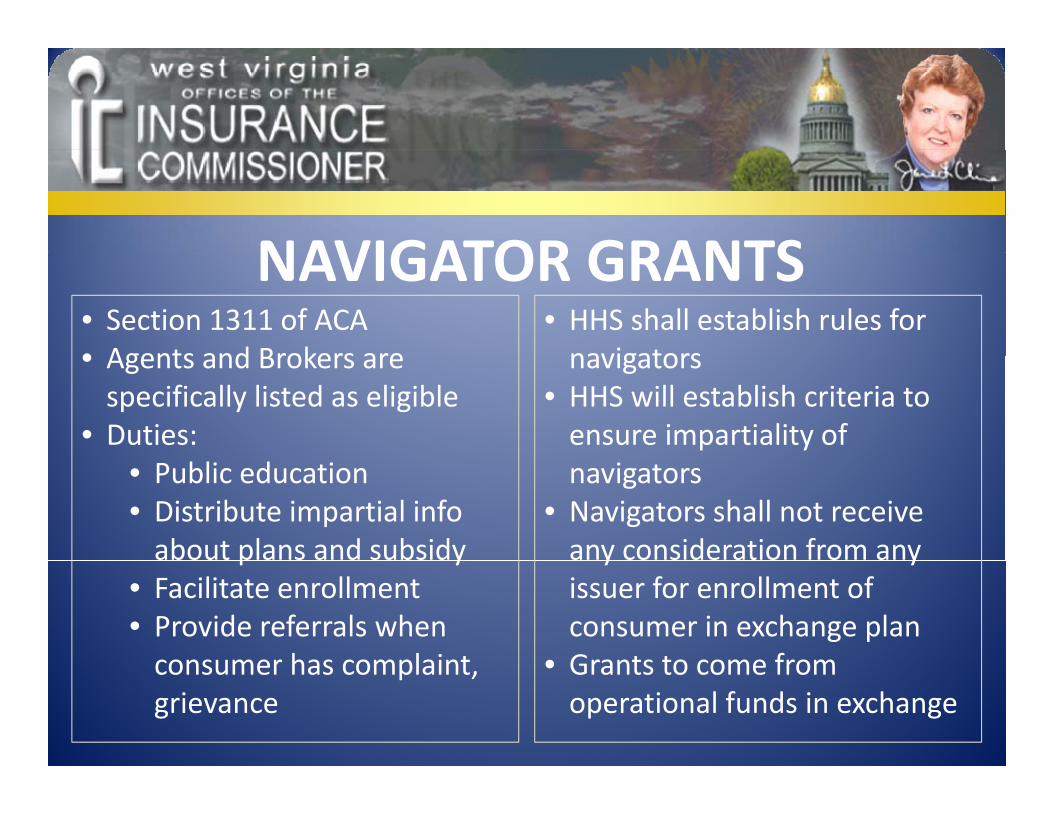

NAVIGATOR GRANTSNAVIGATOR GRANTS• HHS shall establish rules for navigators

• Section 1311 of ACA• Agents and Brokers are navigators

• HHS will establish criteria to ensure impartiality of

• Agents and Brokers are specifically listed as eligible

• Duties:navigators

• Navigators shall not receive any consideration from any

• Public education• Distribute impartial info about plans and subsidy y y

issuer for enrollment of consumer in exchange plan

• Grants to come from

p y• Facilitate enrollment• Provide referrals when consumer has complaint • Grants to come from

operational funds in exchangeconsumer has complaint, grievance

PRODUCERS and EXCHANGEPRODUCERS and EXCHANGESection 1312 of ACA

• HHS Secretary shall establish procedures under which a state may allow agents or brokers

T ll i di id l d l i lifi d h lth• To enroll individuals and employers in any qualified health

plans in exchange

T i i di id l i l i f i di• To assist individuals in applying for premium tax credits and cost‐sharing reductions in exchange

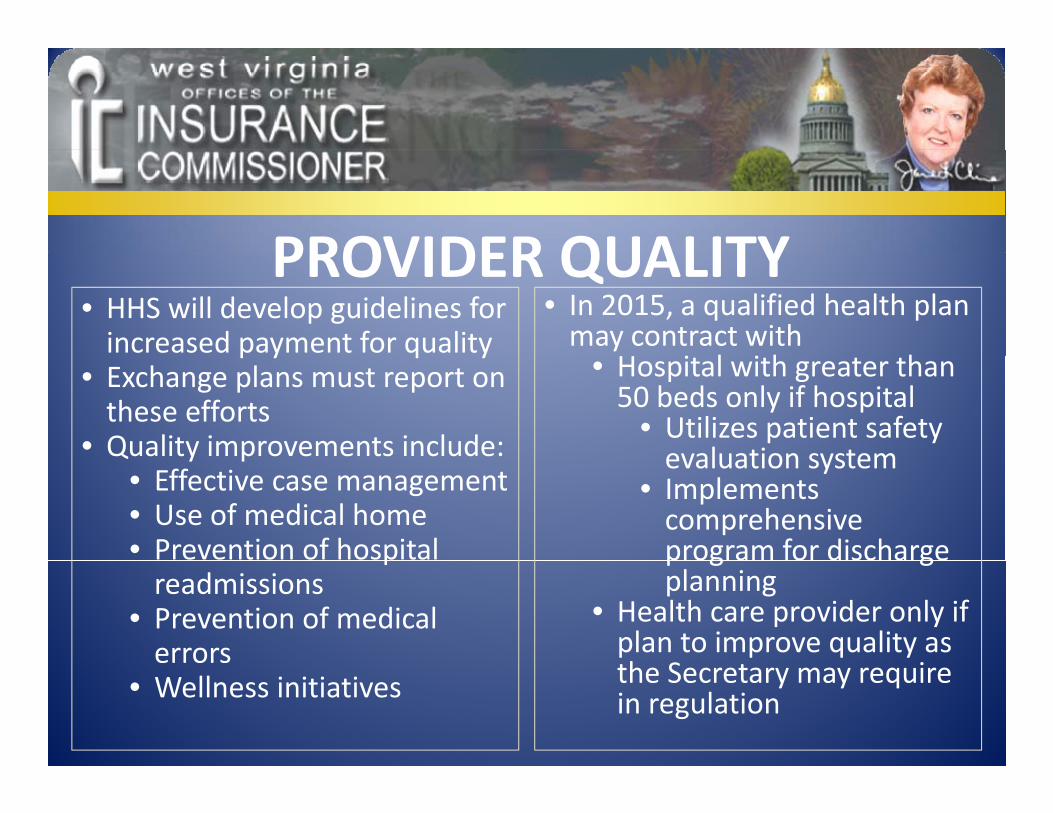

PROVIDER QUALITYPROVIDER QUALITY• HHS will develop guidelines for increased payment for quality

• In 2015, a qualified health plan may contract with

l h hp y q y

• Exchange plans must report on these efforts

• Quality improvements include:

• Hospital with greater than 50 beds only if hospital

• Utilizes patient safety evaluation systemQ y p

• Effective case management• Use of medical home• Prevention of hospital

evaluation system• Implements comprehensive program for discharge p

readmissions• Prevention of medical errors

p g gplanning

• Health care provider only if plan to improve quality as h S i• Wellness initiatives the Secretary may require in regulation

OTHER EXCHANGE FUNCTIONSOTHER EXCHANGE FUNCTIONS• Operate toll free consumer h li

• Implement procedures for ifi i ifi ihotline

• Use a standard format for presenting coverage options

certification, recertification and decertification of health planspresenting coverage options

• Certify mandate exemptions

• Establish a navigator program

p• Assign a rating to each plan• Make available a premium calculator

for education and outreach

• Inform consumers of eligibility for federal subsidy Medicaid

calculator• Transfer to the Treasury a list of exempt individuals and

l li ibl ffor federal subsidy, Medicaid, CHIP

employees eligible for tax credit

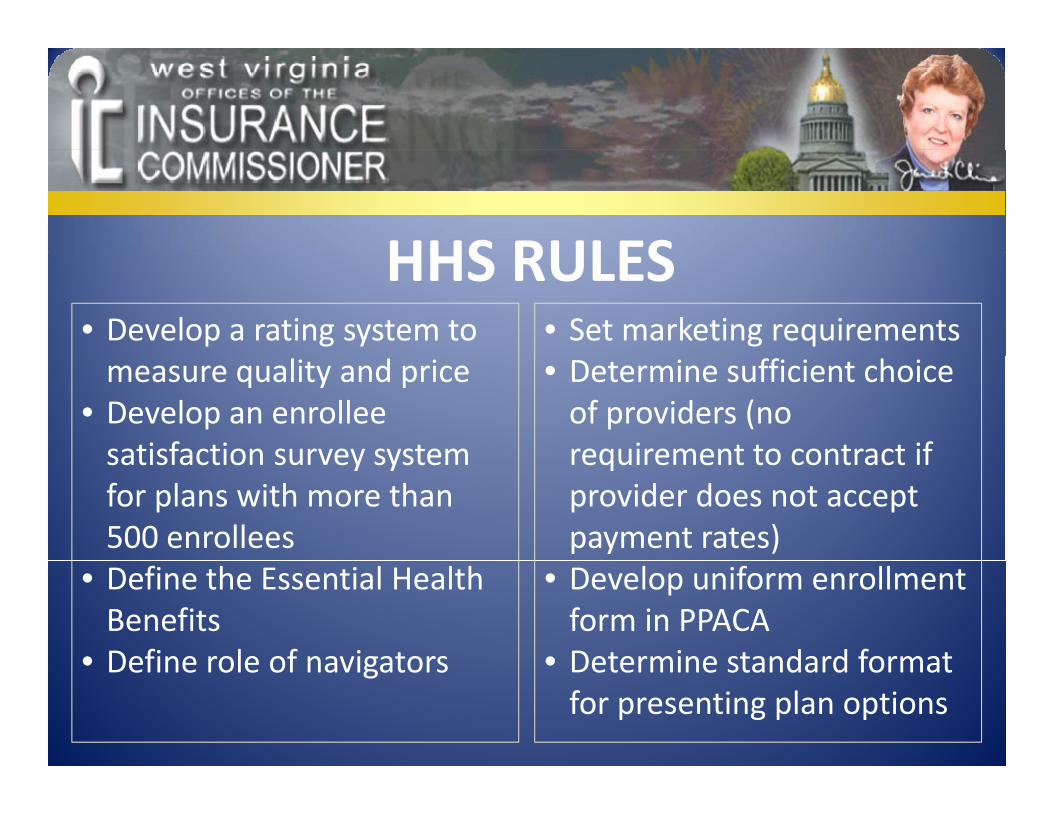

HHS RULESHHS RULES• Develop a rating system to • Set marketing requirementsmeasure quality and price

• Develop an enrollee satisfaction survey system

• Determine sufficient choice of providers (no requirement to contract ifsatisfaction survey system

for plans with more than 500 enrollees

requirement to contract if provider does not accept payment rates)

• Define the Essential Health Benefits

• Define role of navigators

• Develop uniform enrollment form in PPACA

• Determine standard format• Define role of navigators • Determine standard format for presenting plan options

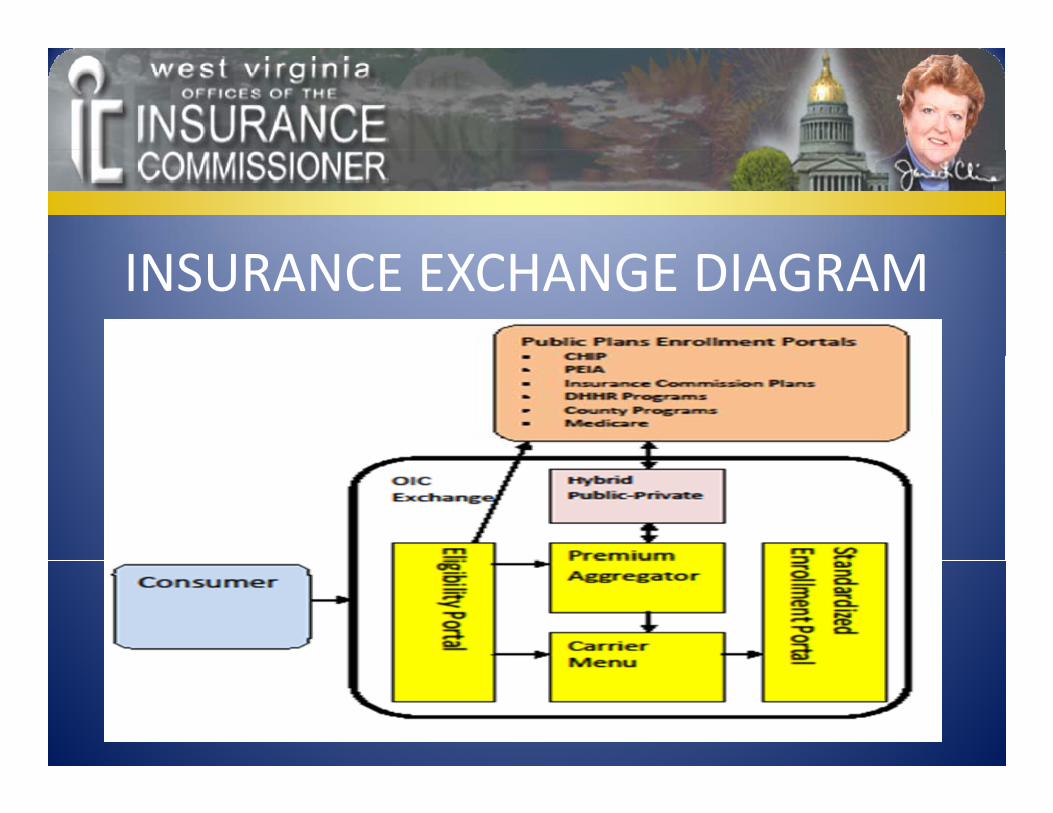

WV CONNECT KEY CONCEPTSWV CONNECT KEY CONCEPTSKey Functions

•Eligibility Portal•Premium Aggregator•Carrier Menu• Standardized Enrollment PortalPortal

•Premium Collection and RemittanceRemittance

•Coverage Assistance Tool

ELIGIBILITY PORTALELIGIBILITY PORTALKey Functions

• Short Questionnaire• Assess public plan

li ibiliteligibility• Assess employer contributioncontribution

• Assess third part contribution

• Assess federal subsidy

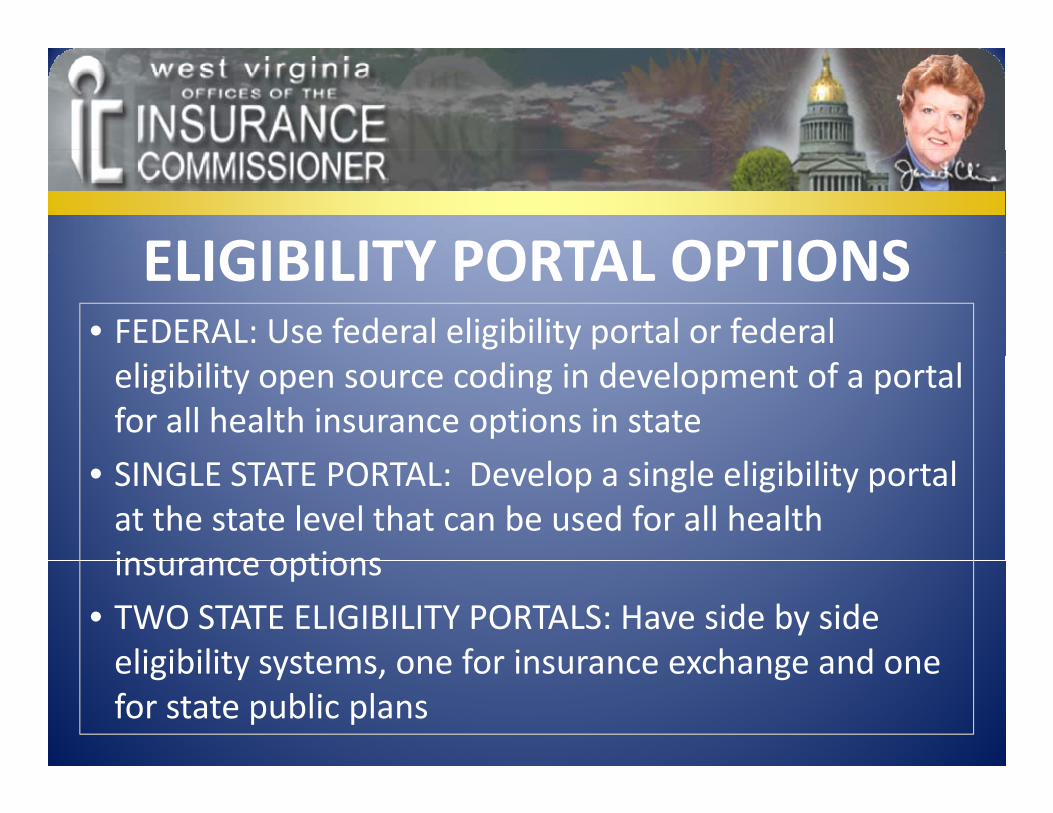

ELIGIBILITY PORTAL OPTIONSELIGIBILITY PORTAL OPTIONS• FEDERAL: Use federal eligibility portal or federal eligibility open source coding in development of a portal for all health insurance options in state

• SINGLE STATE PORTAL: Develop a single eligibility portal at the state level that can be used for all health insurance optionsinsurance options

• TWO STATE ELIGIBILITY PORTALS: Have side by side eligibility systems one for insurance exchange and oneeligibility systems, one for insurance exchange and one for state public plans

PREMIUM AGGREGATORPREMIUM AGGREGATORKey Functions

• Adds accounts contributing to premium

l f f l b• Simplifies federal subsidy and employer contribution

• Allows for multiple account• Allows for multiple account sources

• Simplifies consumerSimplifies consumer budgeting considerations

CARRIER MENUCARRIER MENUKey Functions

• Allows consumer to compare and contrast plans

• Gives consumer option to get more information on specific plans and carriersspecific plans and carriers

• Allows consumer to order and rank plans based on various metrics

ENROLLMENT PORTALENROLLMENT PORTALKey Functions

• Simplifies system for purchasing coverage

• Streamlines and digitizes system for purchasing coverage

PREMIUM COLLECTIONPREMIUM COLLECTION Key Functions

• Collect from accounts for carrier

• Ease administrative burden on consumerburden on consumer and carrier

• Economy of scale• Economy of scale

COVERAGE ASSISTANCE TOOLCOVERAGE ASSISTANCE TOOL Key Functions

A i t i• Assist consumers in determining best plan for their situation

• Would have to be optional and carry disclaimer

• Decision tree logic would have to be carefully developed and regularlydeveloped and regularly updated

OTHER WV EXCHANGE CONCEPTSOTHER WV EXCHANGE CONCEPTS• Portability of Coverage• Employer Exchange Kit•Health Coverage Matrix• Cost Compare Providers• Review Carrier Complaints

• Link to regional exchange/ cross border coverage options • Review Carrier Complaints

• Review Provider Quality• Consumer Assistance

p•Multi state vendor agreements

Consumer Assistance• Agent Portal• Stakeholder Surveys

•Multi Exchange Access Points

•Market Risk Adjuster• Exchange service tracking

Market Risk Adjuster• Exchange Tutorials

INSURANCE EXCHANGE DIAGRAM

CORE AGENT ISSUESCORE AGENT ISSUES• Producer education on ACA

• Agent compensation methodology

R l f i• Role of navigators

• Agent case management portal g g p

ROLE OF AGENTROLE OF AGENT• We need agent input

• Agents have a role in exchange

ACA l f h ll b l• ACA presents a lot of challenges but also a lot of opportunity

• Agent portal would give agents access to exchange for consumersexchange for consumers

NAIC AND AGENTSWorkgroup Resolutiong p

• Taskforce created to work on the role of the producer in exchange

Resolution

• Importance of information provided to consumers

producer in exchange• Taskforce will address

concern about reduction

• Importance of educated and certified producers

of compensation for agents

• Taskforce gives resolution

• Resolves that role of producer should be protected• Taskforce gives resolution

a processprotected

EXCHANGE & OTHER STATE EFFORTSEXCHANGE & OTHER STATE EFFORTSInterconnected Issues

•All Payer Claims Database

•Master Client Index

•Public Plan Eligibility• Insurance Reforms

•Quality Improvement Initiatives

ALL PAYER DATABASEClaims Data Sourcesi

ALL PAYER DATABASEAPD Functions

• Private Insurance Carriers

• Public Insurance

• Risk Adjustment

• Public policymaking• Public Insurance Providers

• ERISA Plans via TPAs

• Consumer tool

• Comprehensive data

• Public Health Encounter Data

component

• Fraud tool• Medicare • Consumer Budgeting

MASTER CLIENT INDEXCoverage/Services

MASTER CLIENT INDEXMCI Functions

• Private Insurance Carriers

• Public policymaking

• Case worker tool• All DHHR Programs and Services

l

• Consumer tool

• Comprehensive data • ERISA Plans via TPAs

• Medicarecomponent

TO LINK OR NOT TO LINK• DHHR’s public interface

for RAPIDS

TO LINK OR NOT TO LINK • System needs

d dfor RAPIDS

• Gives enrollment options for Medicaid, CHIP, and social services

expanded anyway• Cost and Effectiveness

i l O i fsocial services• Discussions with DHHR

and CHIP underway

• Potential Options for linkage

KEY DECISION POINTSKEY DECISION POINTS• GovernanceR l f V i S

• Regulation of the O id M k• Roles of Various State

Agencies• Additional Functions of

Outside Market• Multi‐State Exchange• Mandated Benefits

the Exchange• Additional Information for Consumers

• Funding of Operations• Combine Individual and Small Group

• Role of Agent, Navigators, Consultants

• Negotiate plan

p• Parameters on bringing in Large groups

• Negotiate ProviderNegotiate plan premiums

Negotiate Provider Prices

Questions?

Contact our Health Policy Program Manager y g g

Jeremiah Samples

WV Offices of the Insurance CommissionerWV Offices of the Insurance Commissioner

Charleston, WV 25301

(304) 558‐6279 ext. 1131

11/2/2010

![03 15 ACA and Insurance[1]](https://static.fdocuments.in/doc/165x107/577d20761a28ab4e1e92f341/03-15-aca-and-insurance1.jpg)