HATHERSAGE ROAD, MANCHESTER - Savillspdf.savills.com/documents/Victoria Point Manchester.pdf1...

11

1 HATHERSAGE ROAD, MANCHESTER A RARE OPPORTUNITY TO ACQUIRE A PURPOSE BUILT RESIDENTIAL PROPERTY, CURRENTLY IN USE AS STUDENT ACCOMMODATION, COMPRISING 561 BEDS OVER 6 BLOCKS

-

Upload

hoanghuong -

Category

Documents

-

view

224 -

download

4

Transcript of HATHERSAGE ROAD, MANCHESTER - Savillspdf.savills.com/documents/Victoria Point Manchester.pdf1...

1

HATHERSAGE ROAD, MANCHESTER

A RARE OPPORTUNITY TO ACQUIRE A PURPOSE BUILT RESIDENTIAL PROPERTY, CURRENTLY IN USE AS STUDENT

ACCOMMODATION, COMPRISING 561 BEDS OVER 6 BLOCKS

2

KEY INVESTMENT CONSIDERATIONS

> 561 beds laid out over six blocks as 2, 3 or 4 bed apartments

> Very significant site area of 3.53 acres

> The average 2016-17 rent is £108 per week which is at the affordable end of the sector. Comparable properties indicate far higher rents than those passing at Victoria Point

> Strong occupancy track record with sustained year on year rental growth achieved

> Real potential to refurbish blocks and to provide significant on site amenities.

> Victoria Point is well located for all 3 main universities and the central teaching hospital. There are a total of 77,125 full time students in Manchester

> Strong residential underlying value, both from a PRS and a VP perspective

> Pricing demonstrates a below replacement cost level

> The student market is currently insulated against significant further pipeline delivery given challenges around securing planning permission in Manchester

> We are instructed to seek offers in excess of £29,000,000 (Twenty Nine Million Pounds) for the virtual freehold interest, which reflects a net initial yield of 6.10% (£51,700 per bed) based on purchasers costs of 2.8% allowing for Multiple Dwelling Relief

3

PR

INC

ESS

RD

UPPER BROO

K ST

UPPER BROO

K ST

ANSON RD

ASHTON OLD RD

HYDE RD

PLYMOUTH GROVE

W

ILM

SLO

W R

D

DICKENSON RD

A34

A34

A57

A6

MANCHESTERCITY CENTRE

PLATT FIELDSPARK

ALEXANDRAPARK

BIRCHFIELDSPARK

HULME

ARDWICK

MOSS SIDE

A57(M)

A57(M)

A635

MOSS LANE EAST OXFORD PL DAISYBANK RD

OXFO

RD RD

B5219

A5103

CH

OR

LTON

RD

B5218

HATHERSAGE ROAD

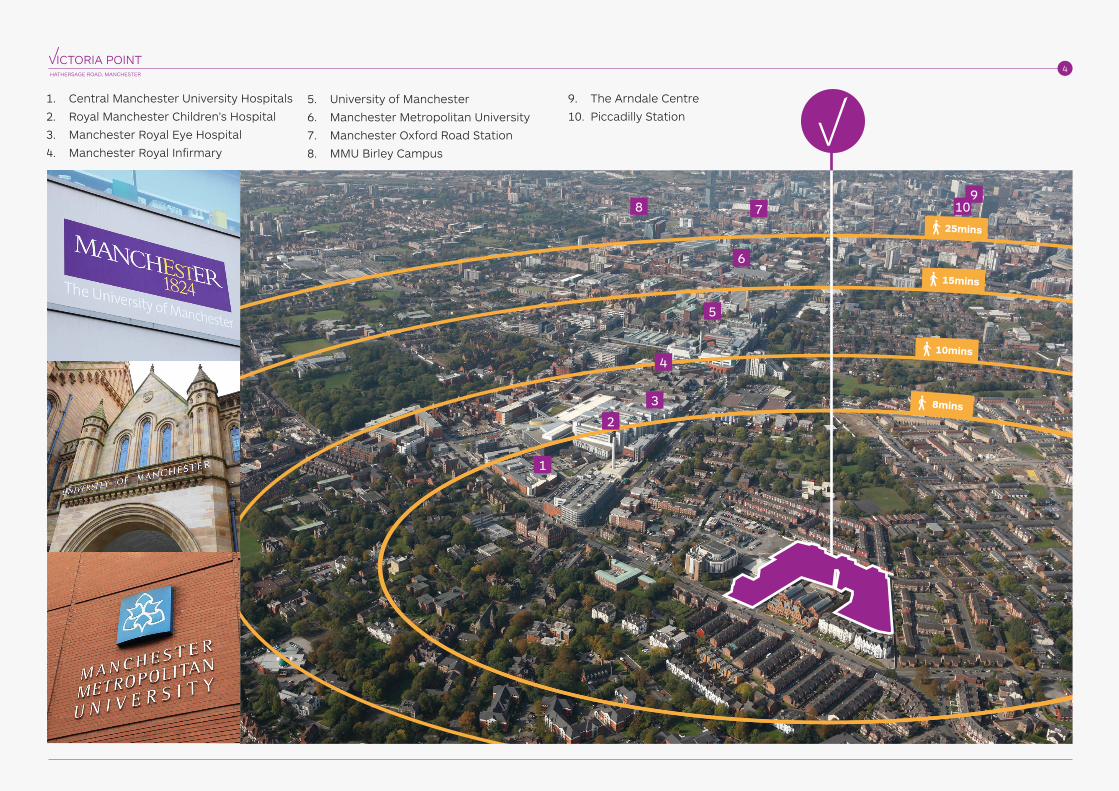

LOCATION & SITUATION

Manchester is the educational and cultural capital of the North West and widely viewed as the UK’s largest financial hub outside of London.

Manchester has been a longstanding major educational destination and is home to three significant higher education providers; The University of Manchester (UoM), Manchester Metropolitan University (MMU) and the University of Salford. These institutions attract close to 76,345 full-time students in total, which make it the largest student accommodation market in the UK outside of London.

Victoria Point is in Victoria Park, a mile to the South of Manchester City Centre and next to the ‘Knowledge Quarter’ or Oxford Road corridor which connects Manchester University, Manchester Metropolitan University and Manchester Royal Infirmary and Eye Hospital.

Not to Scale - for Idenification purposes only

4

1. Central Manchester University Hospitals

2. Royal Manchester Children’s Hospital

3. Manchester Royal Eye Hospital

4. Manchester Royal Infirmary

5. University of Manchester

6. Manchester Metropolitan University

7. Manchester Oxford Road Station

8. MMU Birley Campus

9. The Arndale Centre

10. Piccadilly Station

8mins

10mins

1

3

789

5

6

15mins

25mins

4

10

2

55

HIGHER EDUCATION IN MANCHESTER

The city benefits from a number higher education institutions and has the highest student population in the UK outside of London. The immediate institutions to Victoria Point are UoM and MMU who together attract over 60,755 students, albeit the University of Salford and The Royal Northern College of Music are also within easy access.

HESA (2013/14) Undergraduates Postgraduates

HE provider Full-Time Part-Time Full-Time Part-Time Total HE students

University of Manchester

25,795 685 7,975 3,465 37,920

Manchester Metropolitan University

24,640 1,995 2,345 3,185 32,165

University of Salford

13,580 1,325 2,010 1,565 18,480

The Royal Northern College of Music

585 - 195 10 790

Total 64,600 4,005 12,525 8,225 89,355

University of Manchester

The UoM is a Russell Group member with the UK’s largest full-time student population, 33,770 in 2013/14 – over three times the national average. Furthermore, the proportion of postgraduate students, 24% (7,975), is significantly higher than the UK average of 18% reflecting the institution’s research intensive nature.

The University of Manchester is ranked 28th by The Times Good University Guide 2016 and 33rd by the QS World University Rankings 2015-16. The University has 7.8 applicants per place.

The University’s main campus is located on Oxford Road south of the City Centre and is the largest single site university in the UK with the biggest student community in the UK. The University is aiming to raise its profile to be “one of the leading universities in the world by 2020”. The 2020 Vision has led to the University investing £1 billion between 2012 and 2022 on student, staff and research facilities as well its public spaces.

Manchester Metropolitan University

MMU is the largest campus-based undergraduate University in the UK. MMU’s full-time student population totalled 26,985 in 2013/14 with the make-up largely undergraduate in its composition (91%).

Manchester Metropolitan University is ranked 77th by The Times Good University Guide 2016 and has 7.4 applicants per place.

It has been engaged in a £350m investment programme over the past decade, which has rationalised its number of campuses from seven to two – in Crewe and its main campus in Manchester City Centre.

Manchester total full-time student population (HESA 2013-14)

77,125

66

Employment growth in Manchester has been faster than in any large UK city, with job creation being relatively broad-based across sectors. More professional services jobs have been created in the North West than Greater London over the last 12 months, many of them in the Greater Manchester. Indeed, 57,000 jobs have been created in central Manchester since 2011 – more than double the rate of growth in either the North West or the UK as a whole.

Oxford Economics project that the resident population of Manchester and Salford will rise by 65,000 people over the next decade. There has been an undersupply of new homes in the city in the recent past with just 4,500 net additional dwellings per year in Greater Manchester between 2010 and 2015. This is less than half the 9,654 new homes that should be provided every year according to the districts that make up Greater Manchester.

The imbalance between supply and demand against a backdrop of an improving economy is underpinning residential values. This is driven not only by owner occupiers but by the expansion of the private rented sector (PRS), particularly among students and young professionals. The number of households renting privately in central Manchester and Salford rose by 436% between 2001 and 2011 and now represents 63% of households in the city centre.

Manchester has become a focus for investors in PRS including Private Companies, UK and European Institutions, Private Equity and the HCA as well as overseas capital from Middle East, China and US.

Rising demand in the city centre mean that the private rented sector is becoming increasingly congested and those not able to afford the increasing prices are moving to areas such as Victoria Park.

THE PRIVATE RENTED SECTOR MARKET

of full-time students have access to purpose built accommodation.

35%The planning pipeline consists of just 2,695 beds at present, 2,313 of which are to be delivered as part of the University of Manchester’s redevelopment of the Owens Park accommodation

2,695

Existing

Very little new purpose-built student accommodation has been delivered in Manchester over the last few years meaning that the city’s current stock is generally of inferior quality to other large university cities. Furthermore, this has led to a large supply/demand imbalance with only 35% of full-time students having access to purpose built accommodation.

Pipeline

The planning environment in Manchester for student accommodation is extremely challenging, with a moratorium on new developments unless they concern sites within 500m of a university campus and have the support of the university. Such sites are exceedingly rare.

The planning pipeline consists of just 2,695 beds at present, 2,313 of which are to be delivered as part of the University of Manchester’s redevelopment of the Owens Park accommodation. Taking into account the number of beds to be demolished, this development will result in a net uplift of just 137 beds. The universities are becoming increasingly undersupplied as their numbers increase but developments are not coming through. This insulates the value of standing stock, and investor appetite is very strong for well-located schemes of scale.

MANCHESTER STUDENT ACCOMMODATION MARKET

57,000 jobs have been created in central Manchester since 2011 – more than double the rate of growth in either the North West or the UK as a whole

57,000The number of households renting privately in central Manchester and Salford rose by 436% between 2001 and 2011 and now represents 63% of households in the city centre.

436%

7

DESCRIPTION

The Property comprises six blocks set in landscaped gardens on a total site area of 1.43ha (3.53 acres). It was built in 2009.

The property provides a total of 561 beds within 193 apartments. The accommodation blocks range from three to five storeys. In addition, there are 184 car parking spaces and 5 of the blocks have secure parking provided in the basement.

The accommodation is set out in two, three and four bedroom apartments along with nine three bedroom duplexes. There are also a range of room grades and sizes including Classic, Classic Plus, Premium, Premium Plus and Deluxe.

The apartments are all finished to a very high standard, with large well equipped modern kitchens and fully tiled bathrooms.

The property has a management suite on site. It also has CCTV, bike storage and on-site laundry facilities.

8

PLANNING

The six blocks have planning consent for ‘residential units’, and they have been let to students since 2009. Victoria Point was originally designed as private rented accommodation and therefore could easily be converted back to residential use with minimal expense.

9

ACCOMMODATION

Block 2 3 4 3 Total Apartments

Total Beds

Beds Beds Beds Duplex

1 0 22 8 0 30 98

2 6 23 1 0 30 85

3 6 23 1 0 30 85

4 7 22 1 0 30 84

5 11 34 2 0 47 132

6 3 12 2 9 26 77

TOTAL 33 136 15 9 193 561

44.2m

45.4m

Chy

D

HATHERSAGE ROAD

VAX RO

AD

a Victoria Point

31

19

39

29

Public Baths

2

17

28

Offices

42

41

1

1

1

2

7

3

26

6

5

49

El Sub Sta

Edbrook Walk

UPPER WEST GROVE

BRANDISH C

LOSE

HOLKER CLOSE

KESWIC

K CLO

SE

VE

15

31

11

19

25

5

2

19

9

219

2

11 11a

26

1

14

1 38

7

26

7

15

1

El Sub Sta

1

2

3

4

37

Victoria Point, 6 Hathersage Rd, Manchester M13 0FT

Ordnance Survey © Crown Copyright 2016. All rights reserved. Licence number 100022432. Plotted Scale - 1:1563

NOTE:- Reproduced from the Ordnance Survey Map with the permission of the Controller of H.M. Stationery Office. © Crown copyright licence number 100024244 Savills (UK) Limited. NOTE:- Published for the purposes of identification only and although believed to be correct accuracy is not guaranteed.

1010

FORECAST 2016-17 INCOME

Bedroom Type Beds Average Contract Length (weeks)

2016-17 Rent Per Week

Total Gross Rent

Classic 47 44 99 £204,732

Classic* 93 44 102 £417,384

Premium 80 44 106 £373,120

Premium* 92 44 110 £445,280

Deluxe 70 44 112 £344,960

Deluxe* 101 44 116 £515,504

Classic Plus 48 44 105 £221,760

Premium Plus 30 44 115 £151,800

561 £2,674,540

Other Income:

Holiday Income - 12.5% occupancy on available rooms for 7 weeks £50,000

Application Fee £39,425

Car parking, laundry and miscellaneous £30,000

Total Gross Income £2,793,965

Occupancy Void at 1.5% -£40,118

Operating and Management Costs at £1,675 per bed per annum -£939,675

Total Net Student Income £1,814,172

* denotes uplift in rents following early booking season

The vendor will offer a purchaser a gross rent guarantee based on the forecast 2016-17 income of £2,753,847. This amount includes all ‘Other Income’ and allows for a 1.5% occupancy void. Details of this structure are available on request.

Information on the 2015-16 income and current letting performance for the forthcoming 2016-17 academic year can be made available on request.

Given the scale and configuration of the property, it is assumed that the management and operating cost will be approximately £1,675 per bed per annum. The vendor currently manages the property at a considerably lower cost of £1,425 per bed per annum. They will continue to manage the property until the start of the 2016-17 year.

11

ASSET MANAGEMENT

As a result of the strong location, the quality of the accommodation and the high level of student demand, average rental growth has been strong over recent years.

Value add opportunities include:

> Increasing the letting period beyond the current 44 week period. Competing schemes are securing 48 week and 51 week lettings at similar, and in some cases higher, weekly rental levels

> Capitalise on current low rents and rental growth potential with selective refurbishment

> Use underutilised courtyards and basement carpark areas for additional resident’s amenities such as gym, study rooms, cinema room, common room.

> Potential lease and nominations agreements with the major institutions , particularly UoM which is located nearby

> Potential lease and nominations agreement with the NHS.

TENURE

Long leasehold interest for 999 years commencing on the 19th March 2007 without any provision for the payment of ground rent.

VAT

The property is not elected for VAT and VAT will not be payable on the purchase price.

CAPITAL ALLOWANCES

There are no remaining unclaimed capital allowances.

DATA ROOM

For further information access to a data room is available on request.

Important Notice

Savills, their clients and any joint agents give notice that:

1. They are not authorised to make or give any representations or warranties in relation to the property either here or elsewhere, either on their own behalf or on behalf of their client or otherwise. They assume no responsibility for any statement that may be made in these particulars. These particulars do not form part of any offer or contract and must not be relied upon as statements or representations of fact.

2. Any areas, measurements or distances are approximate. The text, photographs and plans are for guidance only and are not necessarily comprehensive. It should not be assumed that the property has all necessary planning, building regulation or other consents and Savills have not tested any services, equipment or facilities. Purchasers must satisfy themselves by inspection or otherwise.

Designed and Produced by Savills Marketing: 020 7499 8644

February 2016

CONTACTS

For further information please contact:

Savills Student Investment

James Hanmer James Snaith [email protected] [email protected] 020 7016 3711 020 7016 3762

Camilla Bird [email protected] 020 7075 2887

Savills Residential Investment

George Hepburne Scott [email protected] 020 7016 3761

PROPOSAL

We are instructed to seek offers in excess of £29,000,000 (Twenty Nine Million Pounds) for the virtual freehold interest, which reflects a net initial yield of 6.10% (£51,700 per bed) based on purchasers costs of 2.8% allowing for Multiple Dwelling Relief.