HARTFORD COUNTY COMMERCIAL REAL ESTATE MARKET NOVEMBER 2009 Veterans Day Presented by: Andrews &...

24

HARTFORD COUNTY COMMERCIAL REAL ESTATE MARKET NOVEMBER 2009 Veterans Day Presented by: Andrews & Galvin Appraisal Services, LLC 16 Spring Lane, Farmington, CT [email protected] 860-677-5522

-

Upload

dangelo-lockyer -

Category

Documents

-

view

214 -

download

1

Transcript of HARTFORD COUNTY COMMERCIAL REAL ESTATE MARKET NOVEMBER 2009 Veterans Day Presented by: Andrews &...

HARTFORD COUNTY COMMERCIAL REAL ESTATE MARKET

NOVEMBER 2009Veterans Day

Presented by:Andrews & Galvin Appraisal Services, LLC

16 Spring Lane, Farmington, [email protected]

860-677-5522

REAL ESTATE MARKET PRESENTATION OVEVIEWHartford County – Fall 2009

What Just Happened – Where are we Now? Market Real Estate Segments Review of Trends

Hartford County Map

Last Years Theme - What Segment of the Coaster Do You Operate In?

IM STICKING WITH THE COASTERSReality Is All Hartford Market Segments Are

Heading in the Same Direction Fall 2009

For Some It Seem More Like This!

So Where Are We Now?

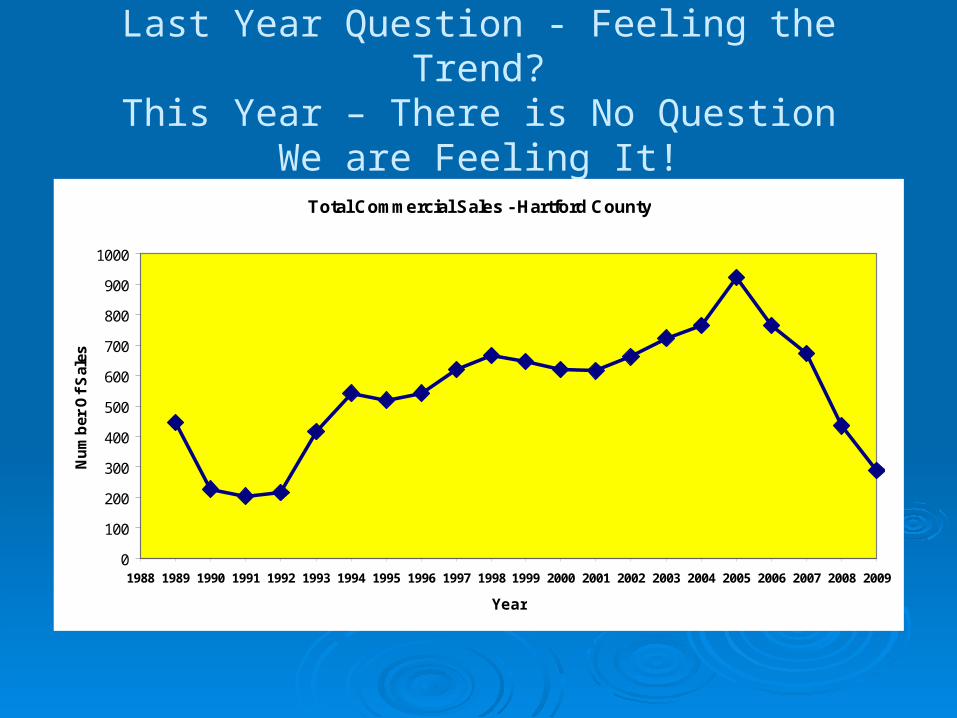

Last Year Question - Feeling the Trend?This Year – There is No Question

We are Feeling It!

Total Commercial Sales - Hartford County

0

100

200

300

400

500

600

700

800

900

1000

1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Year

Nu

mb

er O

f S

ales

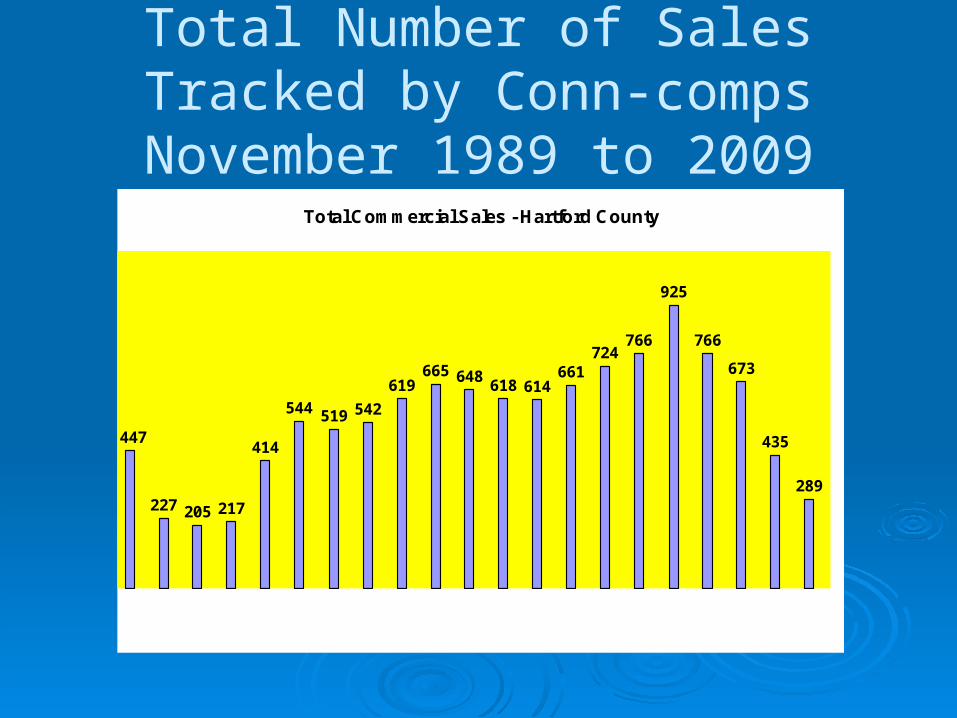

Total Number of SalesTracked by Conn-compsNovember 1989 to 2009

Total Commercial Sales - Hartford County

447

227 205 217

414

544 519 542

619665 648

618 614661

724766

925

766

673

435

289

November 1989 to November 2009

Results of Phone Surveys

Last Year – Uncertainty over Financial Markets and Some Over President Elect

Changes in Financial Markets We Understand - Liquidity

Since Presidential Elect – External Changes Causing Uncertainty Most Do Not Understand – Automotive, Unemployment, Housing, Health Care, War …

Too Many Changes Too Fast

Consequently – Hartford Commercial Real Estate Market is Nearly On Hold – lack of liquidity - Resulting in Large Disconnect Between Market Participants

So What Are the Uncertainties?

Stimulus Package-Residual Impact of Clunkers

Automobile Market Here in Hartford – More Vacant Space

Obsolete Space – Vacant Auto dealerships -

Less Used Car Inventory–low end?

Les Cars to Repair – Less Demand for Automotive Garages

Less Demand For Auto Parts – Increase in Vacant Retail Space

Starting to See Foreclosures in This market segment - 1099

Defense – Middle East UTC – Renewed Headquarters

Lease in Gold Building – but closing some operations

Several Manufactures Pulling Back Work from Smaller Job Shops

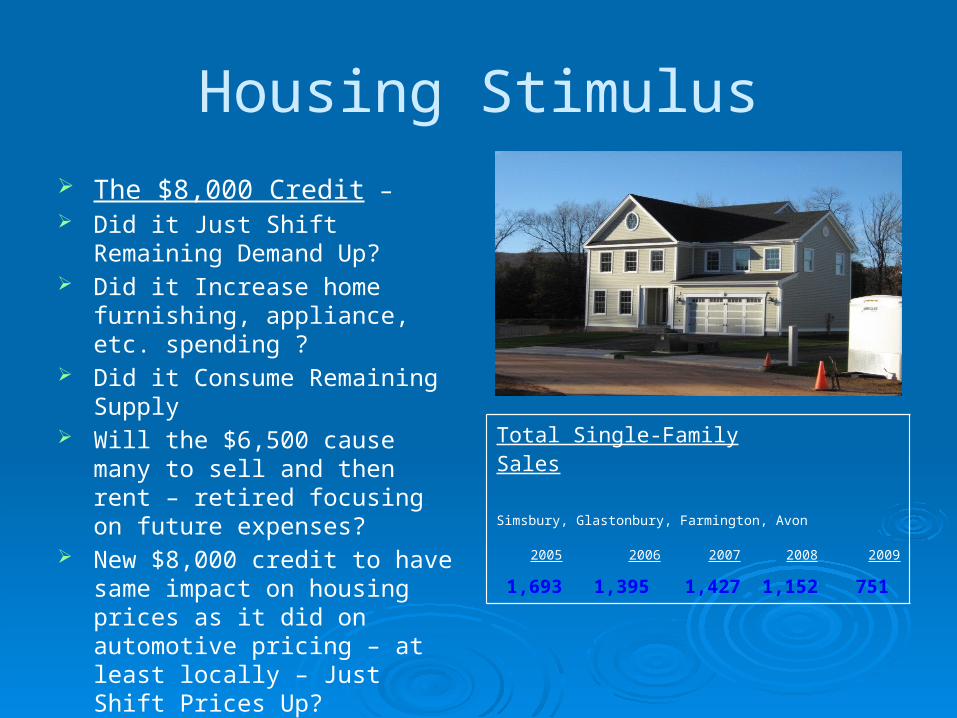

Housing Stimulus The $8,000 Credit – Did it Just Shift Remaining

Demand Up? Did it Increase home furnishing,

appliance, etc. spending ? Did it Consume Remaining Supply Will the $6,500 cause many to sell

and then rent – retired focusing on future expenses?

New $8,000 credit to have same impact on housing prices as it did on automotive pricing – at least locally – Just Shift Prices Up?

Did Help New Residential Projects

Total Single-Family Sales

Simsbury, Glastonbury, Farmington, Avon

2005 2006 2007 2008 2009

1,693 1,395 1,427 1,152 751

Health Care Reform Creates Uncertainty in the

Hartford Real Estate Market Will it Change Future Demand for

Office Space by Insurance Users? Employment Base – Location

Quotient – Will it Change? What About B and C Office Near

Hospitals and Suburbs? Retail Base – Will it Decline? Municipalities–Tax Base Change? Medical Space Demands

Change? Hospitals Repositioning

So – Market is Nearly Stagnant – definitely Slowed Down

Lets Look at some Sales Activity Starting with Industrial, Office, Apartments & Retail

Review of Lender Survey & Positive Trends

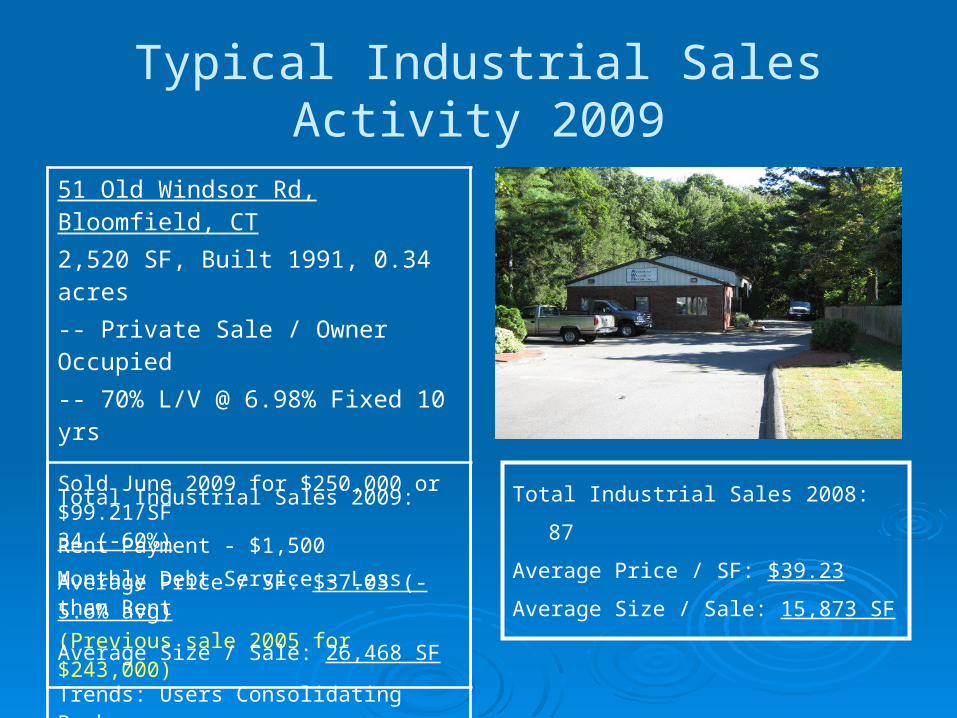

Typical Industrial Sales Activity 2009

51 Old Windsor Rd, Bloomfield, CT2,520 SF, Built 1991, 0.34 acres-- Private Sale / Owner Occupied-- 70% L/V @ 6.98% Fixed 10 yrs

Sold June 2009 for $250,000 or $99.21/SFRent Payment - $1,500Monthly Debt Service – Less than Rent(Previous sale 2005 for $243,000)

Total Industrial Sales 2009: 34 (-60%)

Average Price / SF: $37.03 (-5.6% avg)

Average Size / Sale: 26,468 SF

Trends: Users Consolidating Back

Total Industrial Sales 2008: 87

Average Price / SF: $39.23

Average Size / Sale: 15,873 SF

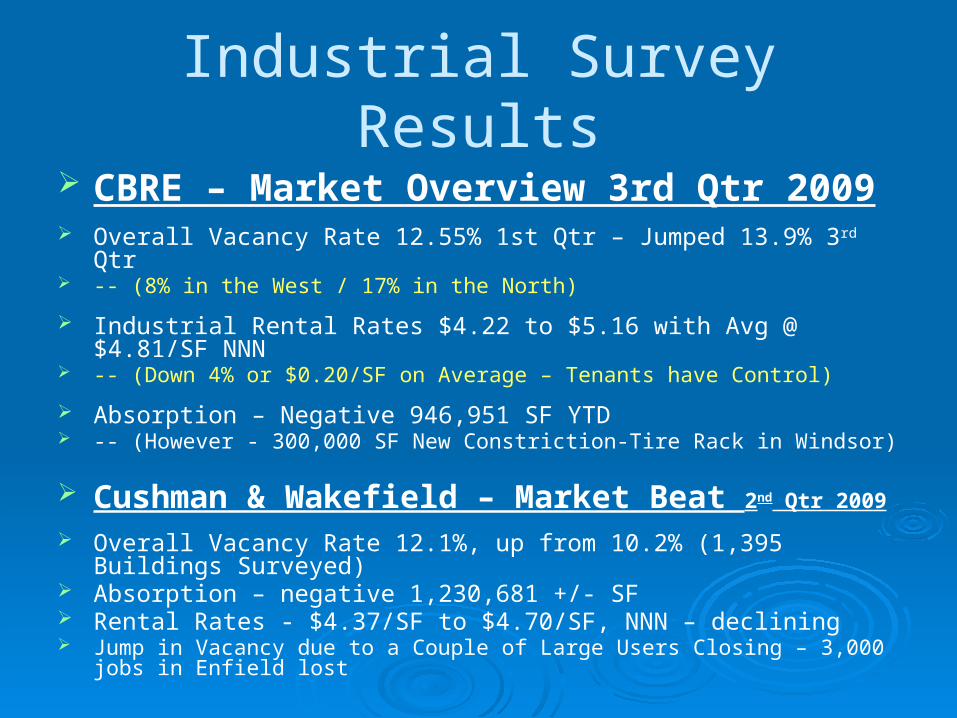

Industrial Survey Results CBRE – Market Overview 3rd Qtr 2009 Overall Vacancy Rate 12.55% 1st Qtr – Jumped 13.9% 3rd Qtr -- (8% in the West / 17% in the North)

Industrial Rental Rates $4.22 to $5.16 with Avg @ $4.81/SF NNN -- (Down 4% or $0.20/SF on Average – Tenants have Control)

Absorption – Negative 946,951 SF YTD -- (However - 300,000 SF New Constriction-Tire Rack in Windsor)

Cushman & Wakefield – Market Beat 2nd Qtr 2009

Overall Vacancy Rate 12.1%, up from 10.2% (1,395 Buildings Surveyed) Absorption – negative 1,230,681 +/- SF Rental Rates - $4.37/SF to $4.70/SF, NNN – declining Jump in Vacancy due to a Couple of Large Users Closing – 3,000 jobs in Enfield lost

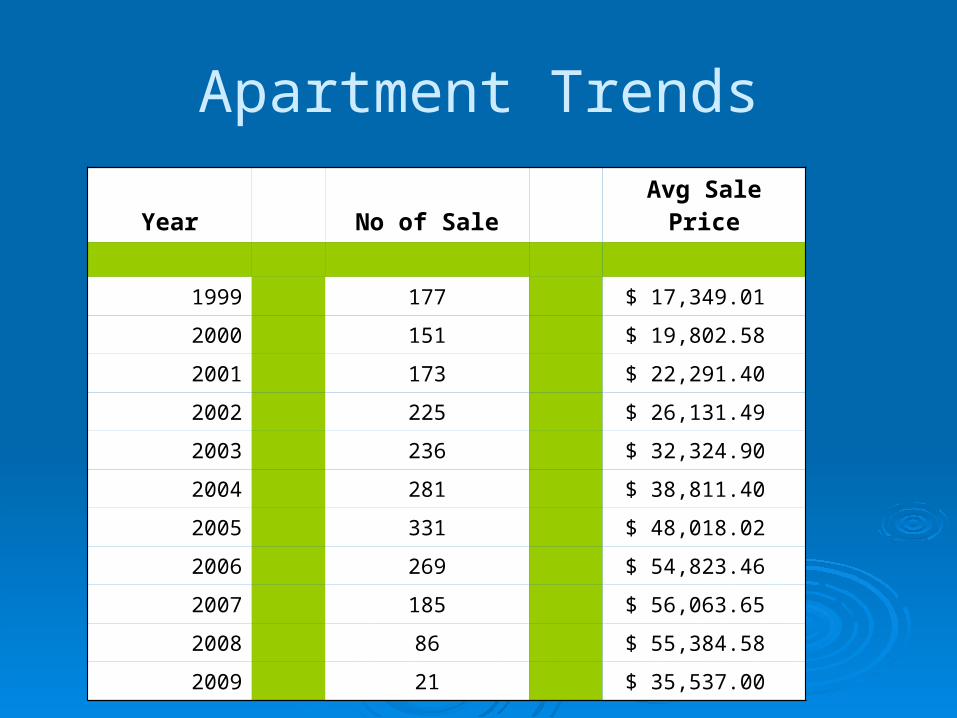

Apartment Trends

Year No of Sale Avg Sale Price

1999 177 $ 17,349.01

2000 151 $ 19,802.58

2001 173 $ 22,291.40

2002 225 $ 26,131.49

2003 236 $ 32,324.90

2004 281 $ 38,811.40

2005 331 $ 48,018.02

2006 269 $ 54,823.46

2007 185 $ 56,063.65

2008 86 $ 55,384.58

2009 21 $ 35,537.00

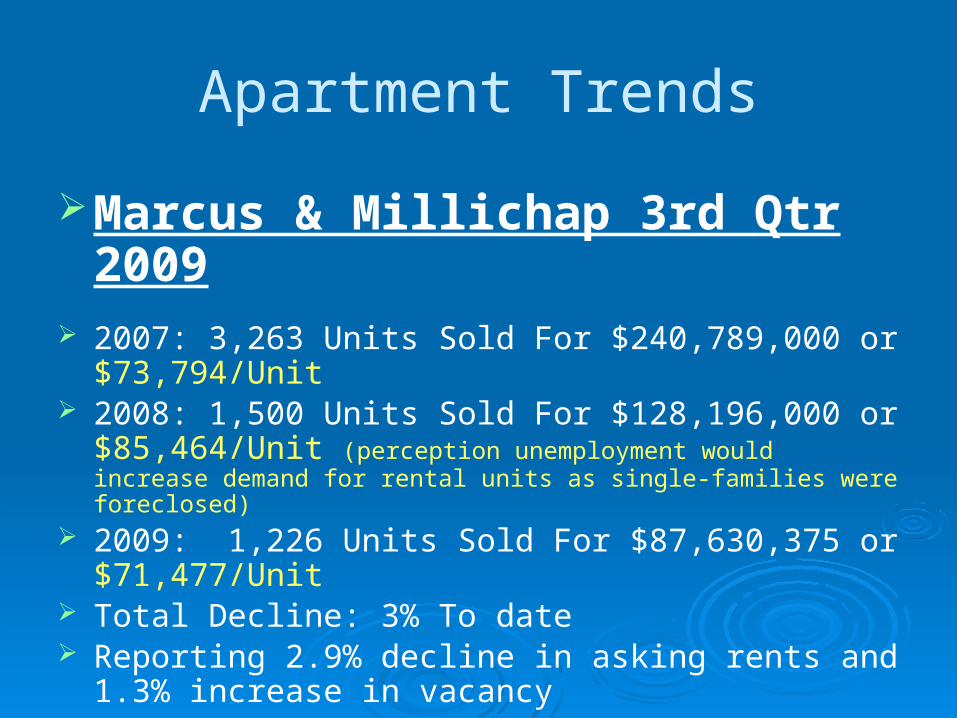

Apartment Trends

Marcus & Millichap 3rd Qtr 2009 2007: 3,263 Units Sold For $240,789,000 or

$73,794/Unit 2008: 1,500 Units Sold For $128,196,000 or

$85,464/Unit (perception unemployment would increase demand for rental units as single-families were foreclosed)

2009: 1,226 Units Sold For $87,630,375 or $71,477/Unit Total Decline: 3% To date Reporting 2.9% decline in asking rents and 1.3%

increase in vacancy

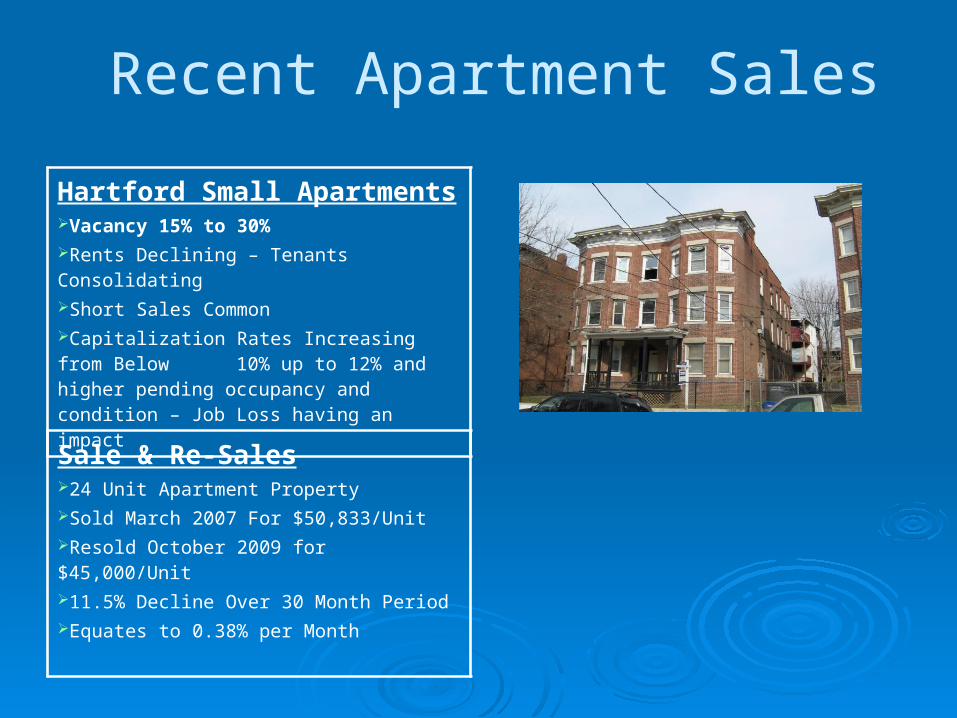

Recent Apartment Sales

Hartford Small ApartmentsVacancy 15% to 30%Rents Declining – Tenants ConsolidatingShort Sales CommonCapitalization Rates Increasing from Below 10% up to 12% and higher pending occupancy and condition – Job Loss having an impact

Sale & Re-Sales24 Unit Apartment Property Sold March 2007 For $50,833/UnitResold October 2009 for $45,000/Unit11.5% Decline Over 30 Month PeriodEquates to 0.38% per Month

Hartford County Office MarketOne Large Office Building Sale 2009The Exchange – 270 Farmington AvFarmington – Sold Sept 2009$14,250,000 or $56.92/SF260,000 SF on 15 Acres80% Occupancy / 10.53% OAR(Previously Sold Dec 1997 for $42.83/SF- 2.7% Increase in Value Per Year)

Typical Office Building Sale1 Old Mill Lane, Simsbury Sold Jan 09$542,000 - $149.12/SF – Owner Occupied3,856 SF on 0.67 Acres

Vacancy: 19.6% - Avg Rent $19.14/SFLeasing Activity: Several Large Leases Absorption: – Neg. 9,978 per CBRE- Neg. 88,975 SF - Cushman & Wakefield

Hartford County Retail Market Few Large Retail Sales 825-875 Queen St, Southington Sold August 2009 for $16,500,000 171,989 SF built 1969 on 17.6 Acres 97% Occupied / 10.45% OAR All Cash Deal – Bob’s Discount,

Fashion Bug, Outback, Ruby Tuesday, Radio Shack, TJ Maxx, Bed, Bath & Beyond, Golden Nails, plus others

Couple Smaller Retail Sales 7 Mill Pond Drive, Granby sold June 2009 $2,000,000 or $181.52/SF – Built 2004 11,018 SF Building on 1.89 Acres Previous sale May 2005 for $170.45/SF 2009 OER: 9.75% 2005 OER: 8.25%

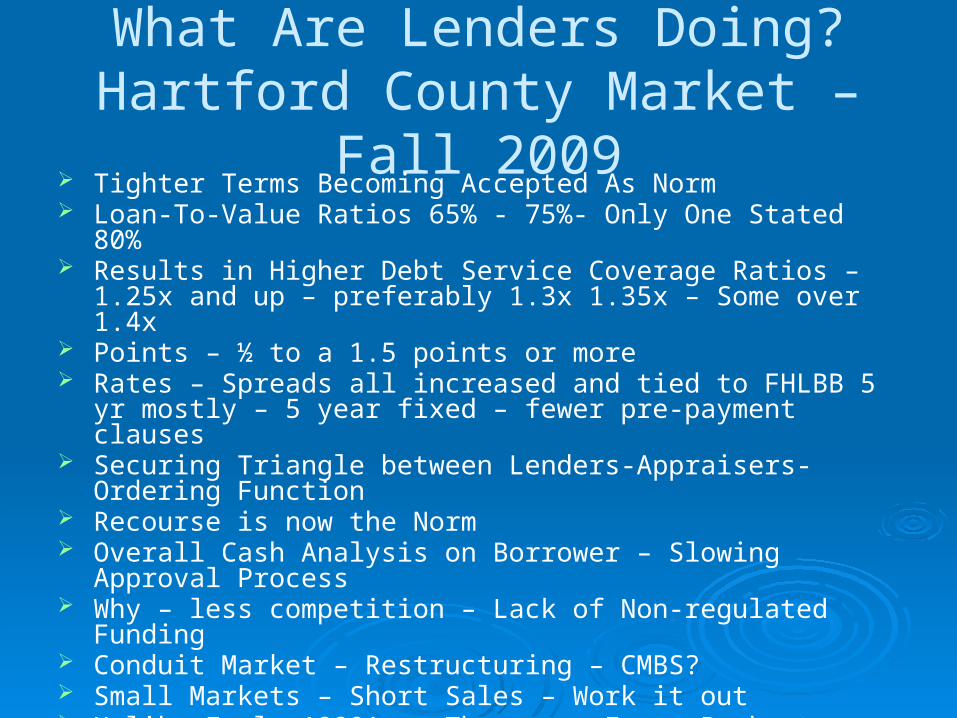

What Are Lenders Doing?Hartford County Market – Fall 2009 Tighter Terms Becoming Accepted As Norm Loan-To-Value Ratios 65% - 75%- Only One Stated 80% Results in Higher Debt Service Coverage Ratios – 1.25x and up –

preferably 1.3x 1.35x – Some over 1.4x Points – ½ to a 1.5 points or more Rates – Spreads all increased and tied to FHLBB 5 yr mostly – 5

year fixed – fewer pre-payment clauses Securing Triangle between Lenders-Appraisers-Ordering Function Recourse is now the Norm Overall Cash Analysis on Borrower – Slowing Approval Process Why – less competition – Lack of Non-regulated Funding Conduit Market – Restructuring – CMBS? Small Markets – Short Sales – Work it out Unlike Early 1990’s – There are Fewer Banks to Take Property Back Regulations – OK to have Performing Loans With LTV of 100% +

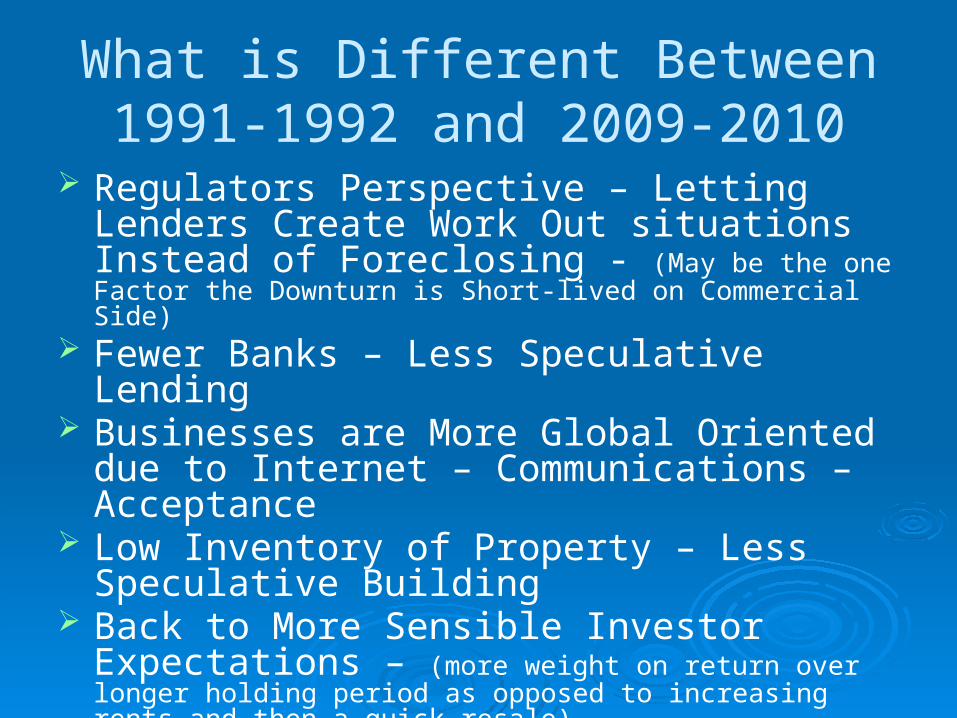

What is Different Between1991-1992 and 2009-2010

Regulators Perspective – Letting Lenders Create Work Out situations Instead of Foreclosing - (May be the one Factor the Downturn is Short-lived on Commercial Side)

Fewer Banks – Less Speculative Lending Businesses are More Global Oriented due to

Internet – Communications – Acceptance Low Inventory of Property – Less Speculative

Building Back to More Sensible Investor Expectations –

(more weight on return over longer holding period as opposed to increasing rents and then a quick resale)

Thank you …& Think Positive

Andrews & Galvin Appraisal Services, LLC

16 Spring Lane, Farmington, [email protected]

860-677-5522

![ur,«]» 1'&Jy'~'~D - Farmington Libraries · DISTRICT: 5 NR: ACTUAL POTENTIAL STATE OF CONNECTICUT CONNECTICUT HISTORICAL COMMISSION 59 South Prospect Street. Hartford, Connecticut](https://static.fdocuments.in/doc/165x107/5d1b8fb788c993dc468d0c52/ur-1jyd-farmington-district-5-nr-actual-potential-state-of-connecticut.jpg)