Harry waters next gen may 2013

14

Challenges in Delivering Infrastructure Harry Waters Agrivert Limited 16 th May, 2013

Transcript of Harry waters next gen may 2013

Challenges in Delivering Infrastructure

Harry WatersAgrivert Limited

16th May, 2013

Agenda

• Introduction to Agrivert

• Our credentials (why we successfully deliver)

• The AD challenge

Agrivert

• Operating for 18 years

• Started in sewage sludge

• Expanded into organic wastes

• Sites in Oxfordshire, Hertfordshire and Northumbria

• Treating food waste for 22 local authorities

• Market leader in Anaerobic Digestion

Agrivert Services

• Design

• Build

• Operate

• Finance

• Food waste treatment

• Green waste treatment

• Biofertiliser recycling

Agrivert’s Experience in Sector

• Anaerobic Digestion

• IVC

• Composting

• Water treatment

Recent Agrivert Projects

• Apr 2013- West London AD plant -50kpa

• Jan 2013 - Wallingford AD plant – 50ktpa

• Jan 2012 - Howden AD plant feed systems

• Sep 2011 - Hendon dewatering plant

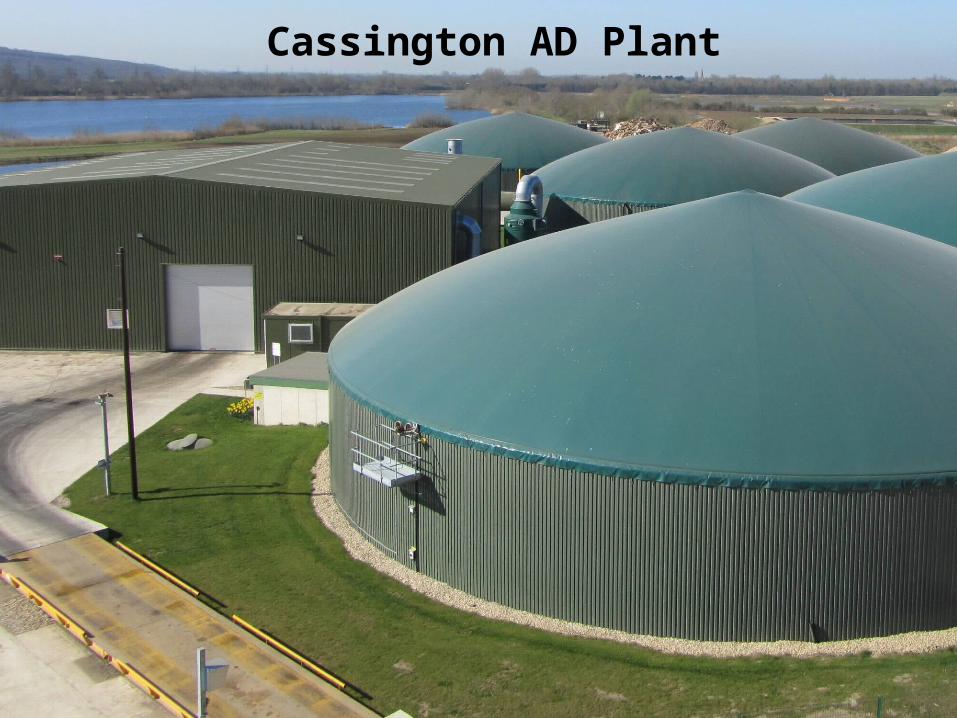

• Sep 2010 - Cassington AD plant - 50ktpa

• Jan 2010 - Ardley IVC Facility - 35ktpa

• Apr 2010 - South Mimms IVC Facility - 50ktpa

Cassington AD Plant

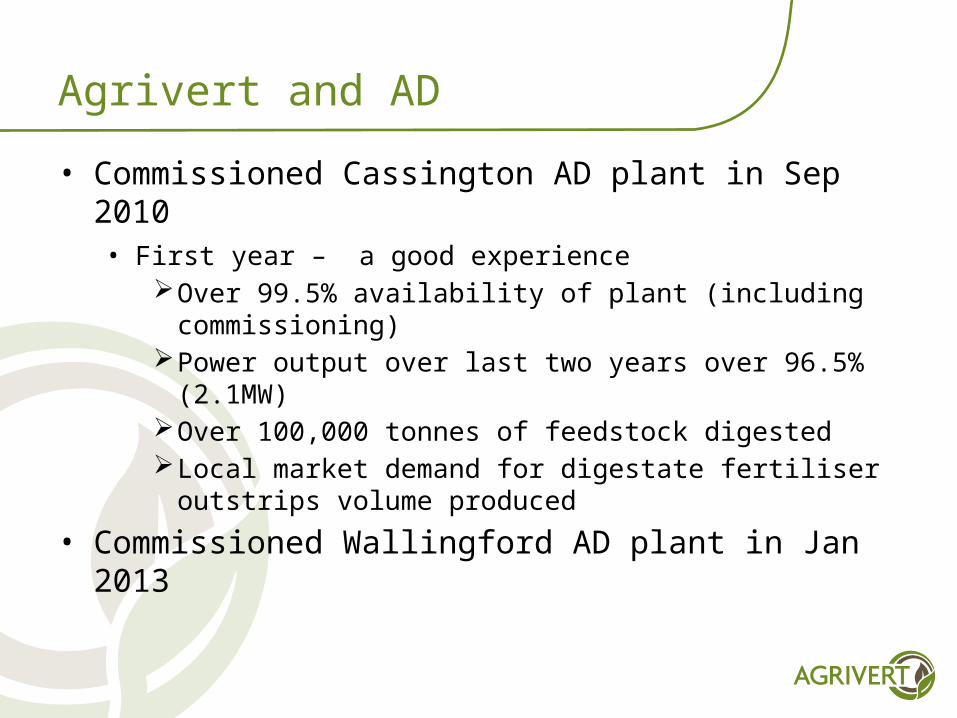

Agrivert and AD

• Commissioned Cassington AD plant in Sep 2010 • First year – a good experience

Over 99.5% availability of plant (including commissioning)Power output over last two years over 96.5% (2.1MW)Over 100,000 tonnes of feedstock digestedLocal market demand for digestate fertiliser outstrips volume

produced

• Commissioned Wallingford AD plant in Jan 2013

The Challenge

Despite successful experience in the sector, we struggled to secure finance on our third plant which :-

• Had planning permission granted• Had waste secured on long term contracts• Was based on successful proven technology• Had a successful operating track record• Had a very profitable reference plant• Had a proven construction delivery record

Why?

Bank Experience

• Some banks have lost money abroad because of changing government policy or rapidly changing feedstock markets

• Not all UK experiences have been good, with some plants failing to live up to power expectations (only 55% power output UK ave 2012)

• Sudden changes in other renewables policies (PV) has added risk to plant income

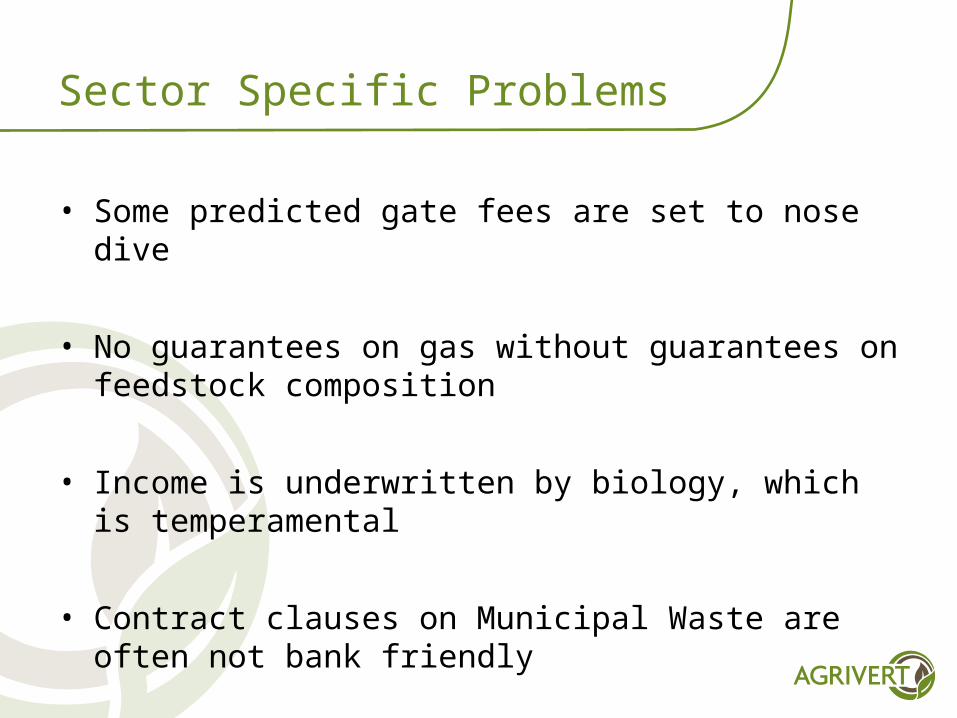

Sector Specific Problems

• Some predicted gate fees are set to nose dive

• No guarantees on gas without guarantees on feedstock composition

• Income is underwritten by biology, which is temperamental

• Contract clauses on Municipal Waste are often not bank friendly

Uncertainty

• Still uncertainty on ROCs, FITs and RHIs

• End of Waste not yet defined

• Will utility companies be allowed to enter market?

• How will dewatered digestate be treated when considering recycling?

• Permitting requirements still evolving

Conclusion

• AD should be an attractive investment opportunity

• Money is in short supply

• Blend of Historic, Sector Specific and Policy Risk make AD unattractive to project finance

• Planning, permitting, technology barriers are dwarfed by financing challenge