Hancock Agricultural Investment Group Farmland...

6

Over the past 18 months, members of HAIG have spent, on a combined basis, almost 12 months in Australia, looking at properties, meeting with leading agricul- tural experts, talking with local property managers and becoming fully immersed in Australian agricultural markets.This on-site due diligence has confirmed the decision to invest in Australia. Australia’s Farm Economy Australia has one of the largest farm economies in the world. Agriculture plays an important role in the overall Australian economy,accounting for approxi- mately 4 percent of the country’s gross national product, according to the Australian Bureau of Agriculture and Resource Economics (ABARE). Approximately 4 percent of the Australian population is involved in agriculture in some manner. According to ABARE: •There are more than 115,000 farms in Australia encompassing 1.1 billion acres; •Australian farmland is valued at close to $60 billion; and •Farm output accounts for almost 20 percent of total Australian exports. Australian per capita production of agricul- tural commodities is one of the highest in the world,and 16 percent higher than the U.S. per capita production.* Overall,the Australian farm economy is large and efficient. In addition to its size and efficiency, there are a number of features that make Australian agriculture attractive to investors. Climatic Diversity Australia’s climate varies from tropical in the far north to temperate in Tasmania. In between there are desert and Farmland Investor Farmland Investor Hancock Agricultural Investment Group Volume 8, Number 1 Summer 2000 Continued on page 2 The Case for Institutional Investment in Australian Farmland hase II of the Hancock Agricultural Investment Group’s international initiative looked at a short list of countries from a statistical standpoint to determine their attractiveness for institutional farmland investment. On paper, Australia appeared attractive. After detailed on-site due diligence, would the conclusion be the same? P The Case for Institutional Investment in Australian Farmland . . . . . . . . . . . . . . . . . . 1 Prospective Investors Tour Aussie Properties . . . . . . . . . . . . . . . . . . . . . . . . . 2 Investing in Australian Agriculture: HAIG’s Process . . . . . . . . . . . . . . . . . . . . . 4 New Research Associate Joins HAIG . . . . . 5 Contents

Transcript of Hancock Agricultural Investment Group Farmland...

Over the past 18 months, members of

HAIG have spent, on a combined basis,

almost 12 months in Australia, looking at

properties, meeting with leading agricul-

tural experts, talking with local property

managers and becoming fully immersed

in Australian agricultural markets.This

on-site due diligence has confirmed the

decision to invest in Australia.

Australia’s Farm Economy

Australia has one of the largest

farm economies in the world.

Agriculture plays an important

role in the overall Australian

economy, accounting for approxi-

mately 4 percent of the country’s

gross national product, according

to the Australian Bureau of Agriculture

and Resource Economics (ABARE).

Approximately 4 percent of the

Australian population is involved in

agriculture in some manner.

According to ABARE:•There are more than 115,000 farms

in Australia encompassing 1.1

billion acres;

•Australian farmland is valued at

close to $60 billion; and

•Farm output accounts for almost 20

percent of total Australian exports.

Australian per capita production of agricul-

tural commodities is one of the highest in the

world,and 16 percent higher than the U.S.

per capita production.* Overall,the Australian

farm economy is large and efficient.

In addition to its size and efficiency,

there are a number of features that make

Australian agriculture attractive to investors.

Climatic Diversity

Australia’s climate varies from tropical

in the far north to temperate in Tasmania.

In between there are desert and

Farmland InvestorFarmland InvestorH a n c o c k A g r i c u l t u r a l I n v e s t m e n t G r o u p

Volume 8, Number 1Summer 2000

Continued on page 2

The Case for Institutional Investmentin Australian Farmland

hase II of the Hancock Agricultural Investment Group’s

international initiative looked at a short list of countries from a

statistical standpoint to determine their attractiveness for institutional

farmland investment. On paper, Australia appeared attractive. After

detailed on-site due diligence, would the conclusion be the same?

P

The Case for Institutional Investment in

Australian Farmland . . . . . . . . . . . . . . . . . .1

Prospective Investors Tour Aussie

Properties . . . . . . . . . . . . . . . . . . . . . . . . . 2

Investing in Australian Agriculture:

HAIG’s Process . . . . . . . . . . . . . . . . . . . . . 4

New Research Associate Joins HAIG . . . . . 5

Contents

2

At the end of March, members of HAIG and

its Australian farm management firm, Rural

Funds Management (RFM), hosted a tour of

Australian farm properties. Prospective

investors from both Australia and the U.S.

toured cotton, citrus, wine grape and

macadamia nut properties located in New

South Wales and Queensland. The tour

included visits to the Suncoast Gold

macadamia nut processing plant and the

Casella Winery.

Prospective Investors Tour Aussie Properties

Mediterranean climates as well.HAIG

expects to invest most assets in the

Mediterranean climate zones in New

South Wales,Victoria and South Australia.

This climate typically has hot,dry

summers and cool,moist winters, very

favorable conditions for the production

of wine grapes, almonds and citrus fruit.

Commodities grown in this climate zone

require irrigation for consistent produc-

tion, and tend to be found along rivers in

the Murray-Darling River Basin. In the

northeastern section of New South

Wales and the southeastern section of

Queensland, the sub-tropical climate is

the native environment for macadamia

nuts. Further north, the tropical climate

in Queensland and the Northern

Territory provides good growing condi-

tions for mangoes, avocados and other

tropical fruit.

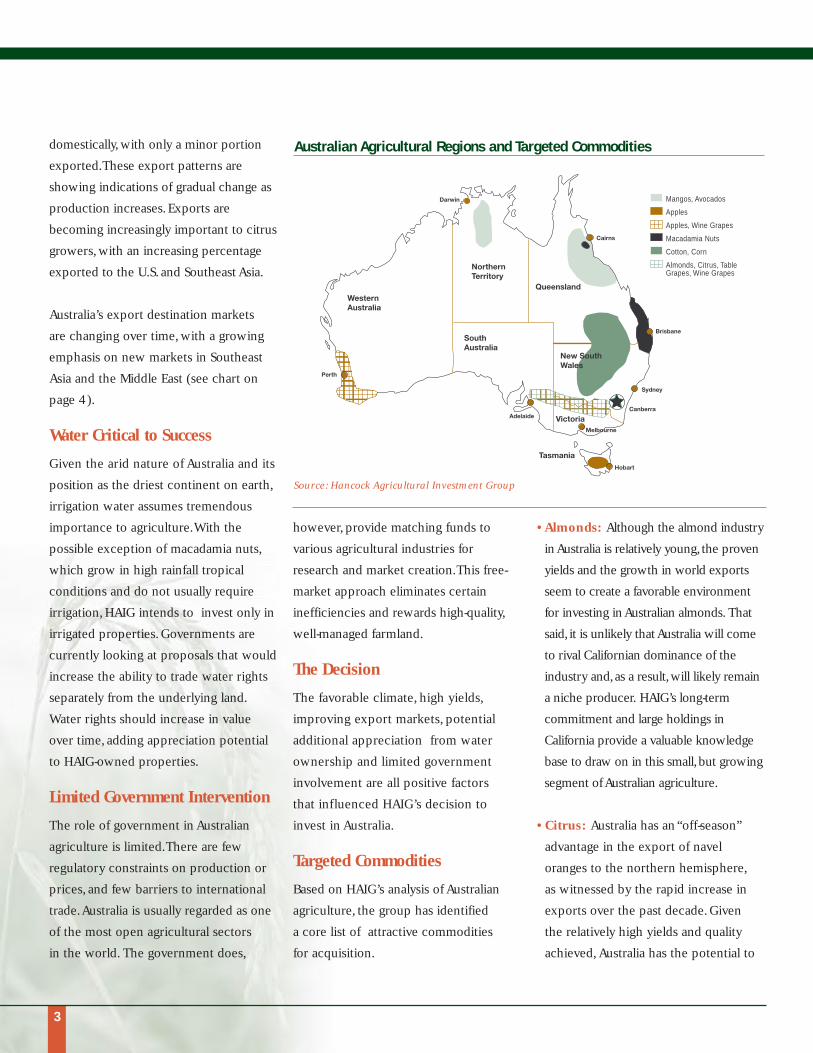

The accompanying map on page 3

illustrates the regions under

consideration for investment by HAIG.

Technology Drives YieldAdvantages*

Australian yields are typically high by

international standards. Production

technology is world-class, partly a

result of limited labor availability.

Yields in Australia average over 100

percent of the world average for all the

crops under consideratiozn for HAIG

investment, and Australia’s cotton, grape

and almond yields are about 200

percent above the average for the rest

of the world.

Export Growth Continues

Exports are very important to the

Australian agricultural industry,with

over 50 percent of production exported

each year.The primary markets are in

Asia,North America and the European

Union.Cotton exports typically go to

Southeast Asian nations,while wine and

macadamia nuts are exported to the

United States and Europe. Almond and

corn production is usually consumed

“The favorable climate, high

yields, improving export

markets, potential additional

appreciation from water owner-

ship and limited government

involvement are all positive

factors that influenced HAIG’s

decision to invest in Australia.”

Wine grape nursery in Victoria, Australia.

Continued from front page

3

domestically,with only a minor portion

exported.These export patterns are

showing indications of gradual change as

production increases.Exports are

becoming increasingly important to citrus

growers,with an increasing percentage

exported to the U.S. and Southeast Asia.

Australia’s export destination markets

are changing over time, with a growing

emphasis on new markets in Southeast

Asia and the Middle East (see chart on

page 4).

Water Critical to Success

Given the arid nature of Australia and its

position as the driest continent on earth,

irrigation water assumes tremendous

importance to agriculture.With the

possible exception of macadamia nuts,

which grow in high rainfall tropical

conditions and do not usually require

irrigation, HAIG intends to invest only in

irrigated properties. Governments are

currently looking at proposals that would

increase the ability to trade water rights

separately from the underlying land.

Water rights should increase in value

over time, adding appreciation potential

to HAIG-owned properties.

Limited Government Intervention

The role of government in Australian

agriculture is limited.There are few

regulatory constraints on production or

prices, and few barriers to international

trade.Australia is usually regarded as one

of the most open agricultural sectors

in the world. The government does,

however, provide matching funds to

various agricultural industries for

research and market creation.This free-

market approach eliminates certain

inefficiencies and rewards high-quality,

well-managed farmland.

The Decision

The favorable climate, high yields,

improving export markets, potential

additional appreciation from water

ownership and limited government

involvement are all positive factors

that influenced HAIG’s decision to

invest in Australia.

Targeted Commodities

Based on HAIG’s analysis of Australian

agriculture, the group has identified

a core list of attractive commodities

for acquisition.

•Almonds: Although the almond industry

in Australia is relatively young,the proven

yields and the growth in world exports

seem to create a favorable environment

for investing in Australian almonds. That

said, it is unlikely that Australia will come

to rival Californian dominance of the

industry and,as a result,will likely remain

a niche producer. HAIG’s long-term

commitment and large holdings in

California provide a valuable knowledge

base to draw on in this small,but growing

segment of Australian agriculture.

•Citrus: Australia has an “off-season”

advantage in the export of navel

oranges to the northern hemisphere,

as witnessed by the rapid increase in

exports over the past decade. Given

the relatively high yields and quality

achieved, Australia has the potential to

NorthernTerritory

Queensland

South Australia

Western Australia

Brisbane

Sydney

Canberra

Tasmania

VictoriaMelbourne

Adelaide

Darwin

New South Wales

Mangos, Avocados

Apples

Apples, Wine Grapes

Macadamia Nuts

Cotton, Corn

Almonds, Citrus, Table Grapes, Wine Grapes

Perth

Hobart

Cairns

Australian Agricultural Regions and Targeted Commodities

Source: Hancock Agricultural Investment Group

develop a long-term competitive

advantage in navel orange production.

•Corn: Australia is an efficient producer

of corn on irrigated farms, although not

a large one. As long as Australian

producers can grow corn for the same

or lower price than the cost of shipped

competing corn, there should be a

reasonable market for Australian corn.

The major market for Australian corn is

likely to remain the domestic market,

with only minor exports.

•Cotton: Australian yields and increased

exports demonstrate the efficiency of

Australian cotton production. Global

demand has trended upward over the

past twenty years, which benefits

Australian cotton producers with a

long-term competitive advantage in

irrigated cotton.

A key attraction of cotton is the ability

to forward sell at set prices significant

portions of production.This, coupled

with the relative stability of yields in

irrigated cotton due to best manage-

ment practices, helps to dampen

income variation.

•Macadamia nuts: Macadamia

nut trees are native to Australia.

Australia is the world’s largest

producer of macadamia nuts.

Australian macadamia farms are

typically larger and more efficient

than their counterparts elsewhere.

Yields are some of the highest in the

world, and the industry maintains a

strong commitment to improving

quality and marketing.

•Wine grapes: Australia has seen

remarkable growth in wine exports

over the past decade, driven by

reliable quality and price.The

Australian industry appears

committed to increasing wine

quality and growing markets,

“Australia is usually

regarded as one of the

most open agricultural

sectors in the world.”

Other28%

MiddleEast5%

SE Asia11% Japan

23%

Americas14%

Europe15%

China4%

Other30%

MiddleEast8%

SE Asia16%

Japan18%

Americas11%

Europe12%

China5%

Source: Australian Bureau of Agriculture and Resource Economics, Balance of Payment Method

Australian Agricultural Export Destinations

4

Dr. Shaffer has conducted a number of research studies for the Hancock Agricultural Investment Group, coveringeverything from the effects of El Niño on HAIG propertyperformance to the international investment opportunitiesdescribed in this and the previous issue of Farmland Investor.This international initiative has been his primary responsibilityfor the last 18 months, culminating in HAIG’s decision to begininvesting in Australian agriculture. In order to see this project to its completion,Dr. Shaffer was recently promoted to Director of International Operations and hasrelocated to Melbourne, Victoria to oversee HAIG’s Australian operations.

For details on HAIG’s new Research Associate, please refer to Jean P. Zwickert’sbiography on the back page.

Continued on page 5

1 9 9 1 / 9 2 1 9 9 8 / 9 9

5

important attributes in an environ-

ment of increasing production. Given

the rapid increase in Australian wine

production, however, potential

oversupply is a concern. HAIG intends

to grow grapes under contracts with

established wineries and does not

plan to develop or buy vineyards

based on speculative markets.Winery

delivery contracts typically have floor

prices and quality guidelines,

mitigating grower price risk.

ConclusionAgriculture is an important compo-

nent of the Australian economy,

accounting for almost 20 percent

of Australian exports.With global

growth rebounding and Australia’s

proximity to rapidly growing

Asian economies, Australian

farmers should be well positioned

to benefit from their technological

innovations, their water use

efficiency and their commitment

to improving quality and yields

through research.These unique

advantages, combined with the

scale and efficiency of Australian

agriculture, suggest that Australian

farmland is an appropriate invest-

ment option for institutional

investors.

* Source: Food and Agricultural Organization

of the United Nations (FAO)

Continued from page 4

Step 1) Analyze broad economic,political and agricul-

tural criteria to generate a “short list”of potential

international investment opportunities.

Step 2) Study more detailed statistics for each country

on this list so the countries could be ranked by

their attractiveness for potential investment.

The final ranking was as follows:

• Australia • New Zealand

• Spain • Chile

• Argentina

Step 3) Conduct on-site due diligence to reach a final

decision on the investment potential of the

leading countries.

The article in the previous issue of Farmland Investor,

available on the HAIG website www.haig.jhancock.com,

described the first two steps in the process.The article

beginning on page one of this issue describes HAIG’s

findings and conclusions after a detailed study of the

potential opportunities in Australian agriculture.

Investing in Australian Agriculture:HAIG’s Process

n the last Farmland Investor, Dr. Matt Shaffer,

Hancock Agricultural Investment Group Research

Director, described the study HAIG conducted to review

global agricultural investment opportunities. The study

followed a three-step process:

I

Jean P. Zwickert, CFA

joined the Hancock Agricultural

Investment Group in May as a

Research Associate. He has

assumed the research responsi-

bilities of Dr. Matt Shaffer, Ph.D.,

who is now Director

of International Operations

based in Melbourne, Victoria,

Australia. In this role, Jean is

responsible for commodity-

specific and global agricultural

market research and analysis,

as well as price forecast devel-

opment and reporting. Prior

to joining HAIG, Jean was

a business consultant in

John Hancock’s Investment

Accounting Group. He holds

a B.S. in Agri-business from

l’Ecole Supérieure d’Agriculture

in Angers, France and an

M.S. in Agri-

business

from Illinois

State University in Bloomington,

Illinois. He is a CFA charter-

holder and a member of the

Association for Investment

Management and Research

and the Boston Security

Analysts Society.

New Research Associate Joins HAIG

Hancock Natural Resource Group99 High Street26th FloorBoston, MA 02110-2320

Farmland Investor is published by John HancockFinancial Services, Inc.,Boston, MA, for the institu-tional investment community.It is distributed with the under-standing that John Hancock isnot rendering legal,accountingor other professional services.

For further information onany of the topics covered inFarmland Investor, contact JulieKoeninger, CFA, editor andPortfolio Manager at (617) 747-1620, or JamesMcBride, Senior Vice President -Business Development at (617)747-1625 or visit our website athttp://haig.jhancock.com.

First Class MailU.S. Postage

PAIDBoston, MA

Permit No. 11

HancockAgriculturalInvestmentGroup

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

![Brent 2014 Farmland Preservation, Agricultural …web.isanet.org/Web/Conferences/FLACSO-ISA BuenosAires...[Draft only—please do not cite] of farmland (Sokolow, 2002). This paper](https://static.fdocuments.in/doc/165x107/5e9245094b453964605e083c/brent-2014-farmland-preservation-agricultural-web-buenosaires-draft-onlyaplease.jpg)