Half year results presentation - Bupa/media/files/site-specific-files/our... · 2017 half year...

33

Half year results presentation 6 months ended 30 June 2017

-

Upload

truongcong -

Category

Documents

-

view

219 -

download

2

Transcript of Half year results presentation - Bupa/media/files/site-specific-files/our... · 2017 half year...

Half year results presentation 6 months ended 30 June 2017

Overview Financial review Outlook & operating priorities Market unit performance

Agenda

2017 half year results presentation

2

Market unit performance

Joy Linton, CFO

Section 2

Financial review

Martin Potkins, Corporate Controller

Gareth Evans, Group Treasurer

Section 3

Evelyn Bourke, Group CEO

1. Overview

2. Market Unit performance

3. Financial review

4. Outlook and operating priorities

5. Questions and Answers

Overview Financial review Outlook & operating priorities Market unit performance

Section 1

Overview

Evelyn Bourke, Group CEO

3

Overview Financial review Outlook & operating priorities Market unit performance

Embedding Bupa’s strategic framework

4

HY 2017 Group highlights

• Using Net Promoter System to improve customer experience

• Focusing on digital transformation and continuous improvement

• Investing in strength and depth in key markets, and in risk management and compliance

Overview Financial review Outlook & operating priorities Market unit performance

Investing in strength and depth for future growth

5

HY 2017 Group highlights

Bupa Arabia stake increased from 26.25% to 34.25%

Operating highlights:

Australian health insurance business remains No.1 provider in highly competitive market Affordability pressures for customers

Intense competition

Challenging and volatile political and economic environments

Operating environment characterised by:

In the UK, completed Oasis Dental Care acquisition; integration on track

Bupa Thailand assets held for sale, with

divestment announced on 25 July 2017.

Growth in revenue, underlying profit and cashflow in H1

New CPO; Appointment of CEO International

Markets announced.

Overview Financial review Outlook & operating priorities Market unit performance

HY 2017 Group highlights

6

(1) The Solvency II capital coverage ratio is an estimated value.

Revenue

£6.1bn +4% CER

Underlying profit before tax

£330.9m +11% CER

Statutory profit before tax

£231.3m +66% AER

Net cash flow from operations

£554.4m +8% AER

Solvency coverage ratio (1)

160% -44% pts

Overview Financial review Outlook & operating priorities Market unit performance

Section 2

Market Unit

performance

Joy Linton, Chief Financial Officer

7

Overview Financial review Outlook & operating priorities Market unit performance

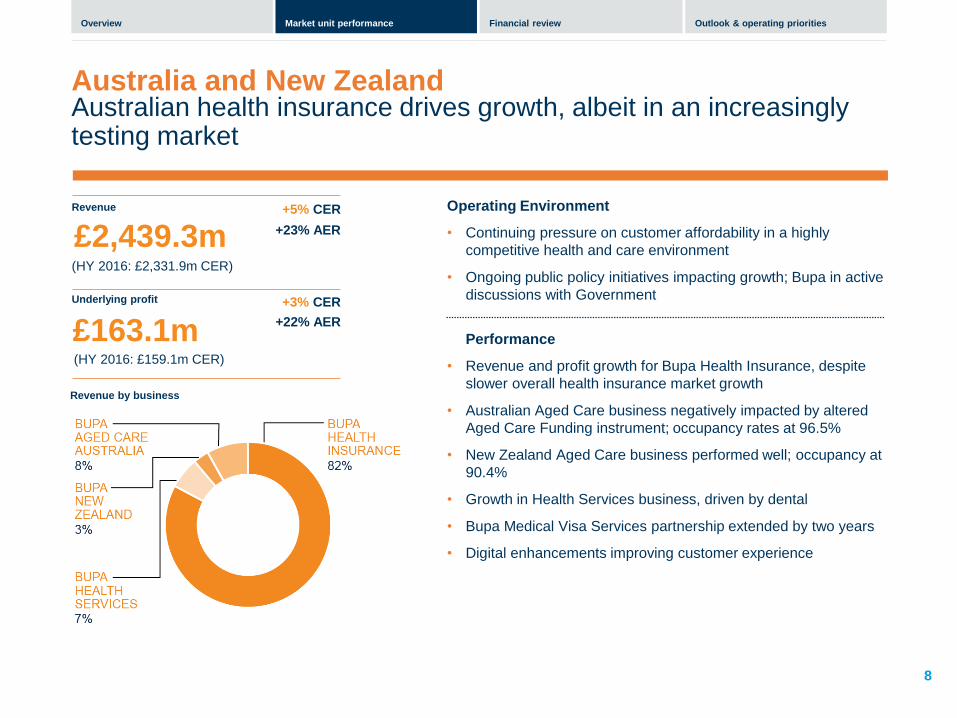

Australian health insurance drives growth, albeit in an increasingly testing market

8

Australia and New Zealand

Revenue

Underlying profit

Revenue by business

(HY 2016: £2,331.9m CER)

£2,439.3m +5% CER

+23% AER

(HY 2016: £159.1m CER)

£163.1m +3% CER

+22% AER

Operating Environment

• Continuing pressure on customer affordability in a highly

competitive health and care environment

• Ongoing public policy initiatives impacting growth; Bupa in active

discussions with Government

Performance

• Revenue and profit growth for Bupa Health Insurance, despite

slower overall health insurance market growth

• Australian Aged Care business negatively impacted by altered

Aged Care Funding instrument; occupancy rates at 96.5%

• New Zealand Aged Care business performed well; occupancy at

90.4%

• Growth in Health Services business, driven by dental

• Bupa Medical Visa Services partnership extended by two years

• Digital enhancements improving customer experience

Overview Financial review Outlook & operating priorities Market unit performance

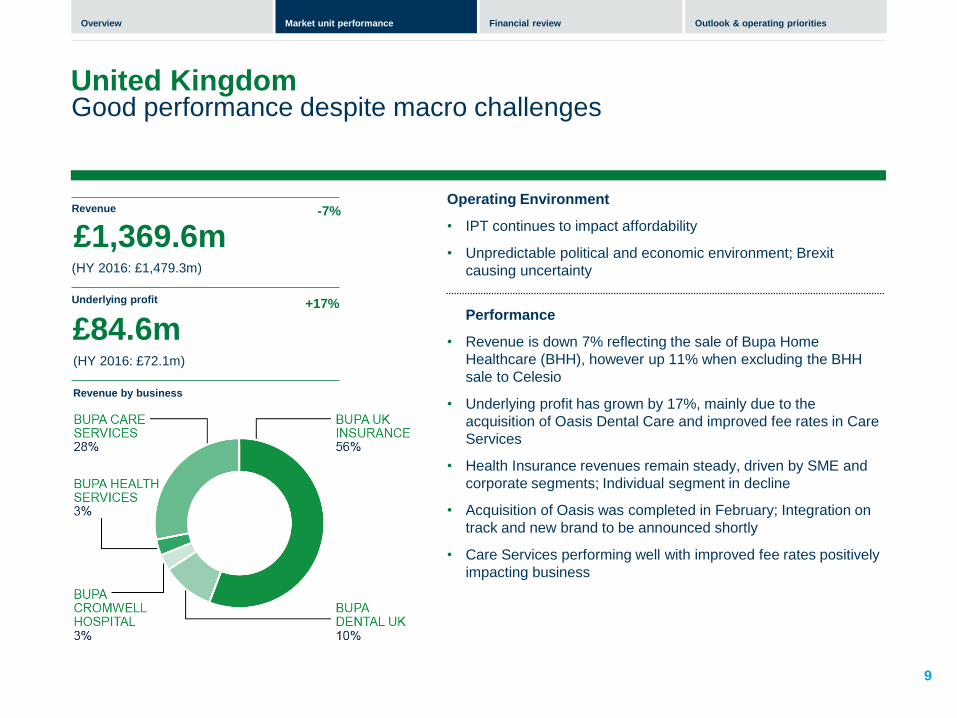

Good performance despite macro challenges

9

United Kingdom

Revenue

Underlying profit

Revenue by business

(HY 2016: £1,479.3m)

£1,369.6m -7%

(HY 2016: £72.1m)

£84.6m +17%

Operating Environment

• IPT continues to impact affordability

• Unpredictable political and economic environment; Brexit

causing uncertainty

Performance

• Revenue is down 7% reflecting the sale of Bupa Home

Healthcare (BHH), however up 11% when excluding the BHH

sale to Celesio

• Underlying profit has grown by 17%, mainly due to the

acquisition of Oasis Dental Care and improved fee rates in Care

Services

• Health Insurance revenues remain steady, driven by SME and

corporate segments; Individual segment in decline

• Acquisition of Oasis was completed in February; Integration on

track and new brand to be announced shortly

• Care Services performing well with improved fee rates positively

impacting business

Overview Financial review Outlook & operating priorities Market unit performance

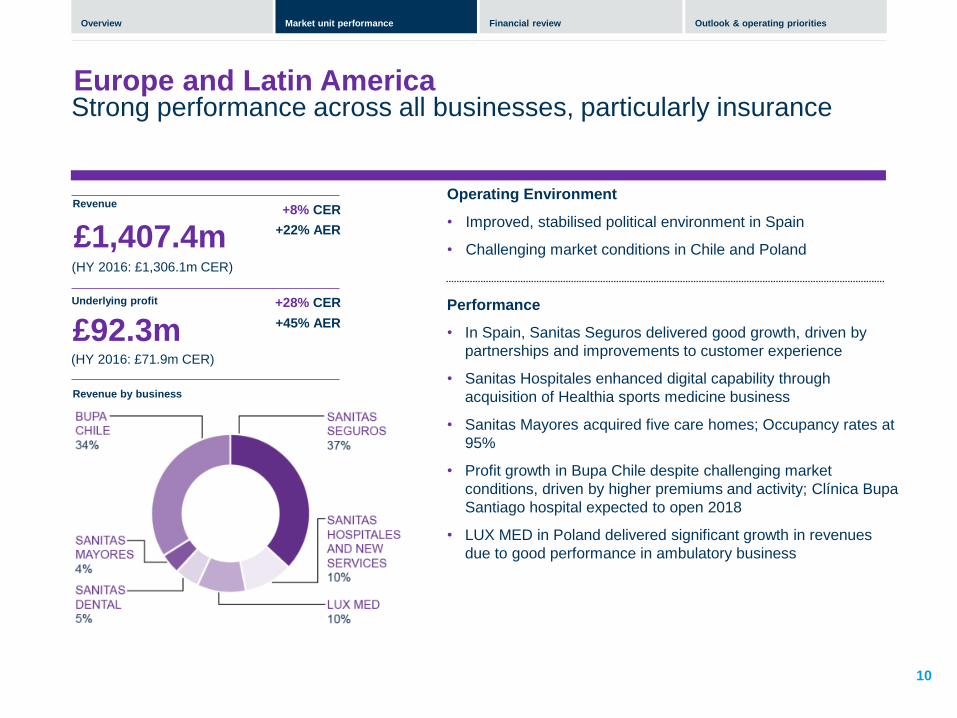

Strong performance across all businesses, particularly insurance

10

Europe and Latin America

Revenue

Underlying profit

Revenue by business

(HY 2016: £1,306.1m CER)

£1,407.4m +8% CER

+22% AER

(HY 2016: £71.9m CER)

£92.3m +28% CER

+45% AER

Operating Environment

• Improved, stabilised political environment in Spain

• Challenging market conditions in Chile and Poland

Performance

• In Spain, Sanitas Seguros delivered good growth, driven by

partnerships and improvements to customer experience

• Sanitas Hospitales enhanced digital capability through

acquisition of Healthia sports medicine business

• Sanitas Mayores acquired five care homes; Occupancy rates at

95%

• Profit growth in Bupa Chile despite challenging market

conditions, driven by higher premiums and activity; Clínica Bupa

Santiago hospital expected to open 2018

• LUX MED in Poland delivered significant growth in revenues

due to good performance in ambulatory business

Overview Financial review Outlook & operating priorities Market unit performance

Growth in revenues but Bupa Global challenges continue to impact profitability

11

International Markets

Revenue(1)

Underlying profit(1)

Revenue by business(2)

(HY 2016: £751.4m CER)

£862.8m +15% CER

+27% AER

(HY 2016: £34.4m CER)

£25.7m -25% CER

-18% AER

Operating Environment

• Less favourable economic conditions in Saudi Arabia

• Intense competition for IPMI

Performance

• Bupa Global customer mix changes and higher loss ratios

• Increased stake in Bupa Arabia to 34.25%; continues to deliver

good customer and revenue growth

• Acquisition of Care Plus in Brazil had positive impact on

performance; integration on track

• Bupa Hong Kong performance on target benefitting from strong

renewals and pricing improvements; Continued expansion of

Quality HealthCare clinics business with three new facilities

• Divestment of Bupa Thailand to Aetna announced 25 July

(1) Revenue of £862.8m does not include the revenues of our equity accounted associates (Max Bupa, India, Bupa Arabia and Highway to

Health, part of Bupa Global North America). Our appropriate share of profit from these businesses is included in underlying profit.

(2) Chart includes 100% of Bupa revenues from all businesses to give a sense of scale

Overview Financial review Outlook & operating priorities Market unit performance

Section 3

Financial review

Martin Potkins, Corporate Controller

Gareth Evans, Group Treasurer

12

Overview Financial review Outlook & operating priorities Market unit performance

Financial highlights

13

HY 2017 Financial overview

Short-term funding refinanced via £300m senior bond

Completion of transactions impacts solvency and funding metrics at the

half year as expected

Solvency capital coverage 160% (1)

Continued strong cash generation

(1) The Solvency II capital coverage ratio is an estimated value.

Overview Financial review Outlook & operating priorities Market unit performance

Group grew revenues by 4% and underlying profit 11% – a good result given local market conditions

14

HY 2017 Financial overview

Revenues

Underlying profit before tax(1)

HY 2017

HY 2016 (CER)

£6.1bn

£5.9bn

• Deepened and strengthened our market positions

aided through a number of key transactions

• Growth in underlying profit is underpinned by good

performances from ELA and the UK, driven by

growth in Sanitas Seguros and the acquisition of

Oasis Dental Care, respectively

HY 2017

HY 2016 (CER)

£330.9m

£298.5m

(1) In order to reflect trading performance in a consistent manner year on year, a number of non-trading items that limit comparability are removed from our statutory profit before tax to arrive at underlying profit. This

distinguishes underlying profit from other constituents of the statutory profit before tax, excluding items relating to business combinations and disposals, fluctuations in foreign exchange, property revaluations and

investment returns on return-seeking assets, along with other one-off items.

+4% at CER

+15% at AER

+11% at CER

+26% at AER

Overview Financial review Outlook & operating priorities Market unit performance

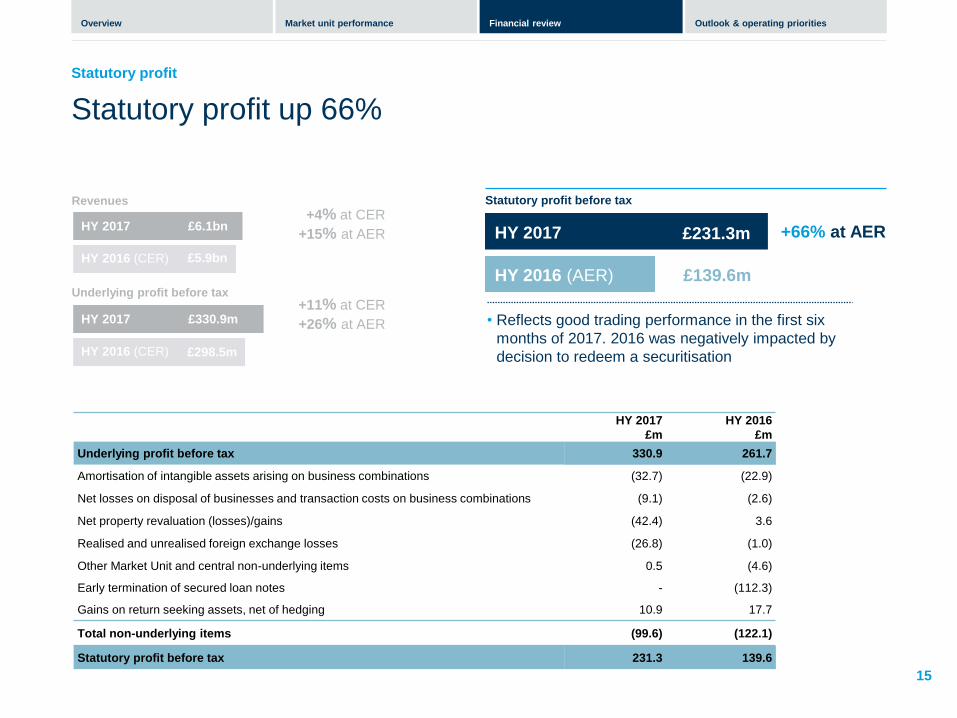

Statutory profit up 66%

15

Statutory profit

Revenues Statutory profit before tax

+4% at CER

+15% at AER HY 2017

HY 2016 (CER)

£6.1bn

£5.9bn

• Reflects good trading performance in the first six

months of 2017. 2016 was negatively impacted by

decision to redeem a securitisation

+66% at AER HY 2017

HY 2016 (AER) £139.6m

Underlying profit before tax

+11% at CER

+26% at AER HY 2017

HY 2016 (CER)

£330.9m

£298.5m

£231.3m

HY 2017

£m

HY 2016

£m

Underlying profit before tax 330.9 261.7

Amortisation of intangible assets arising on business combinations (32.7) (22.9)

Net losses on disposal of businesses and transaction costs on business combinations (9.1) (2.6)

Net property revaluation (losses)/gains (42.4) 3.6

Realised and unrealised foreign exchange losses (26.8) (1.0)

Other Market Unit and central non-underlying items 0.5 (4.6)

Early termination of secured loan notes - (112.3)

Gains on return seeking assets, net of hedging 10.9 17.7

Total non-underlying items (99.6) (122.1)

Statutory profit before tax 231.3 139.6

Overview Financial review Outlook & operating priorities Market unit performance

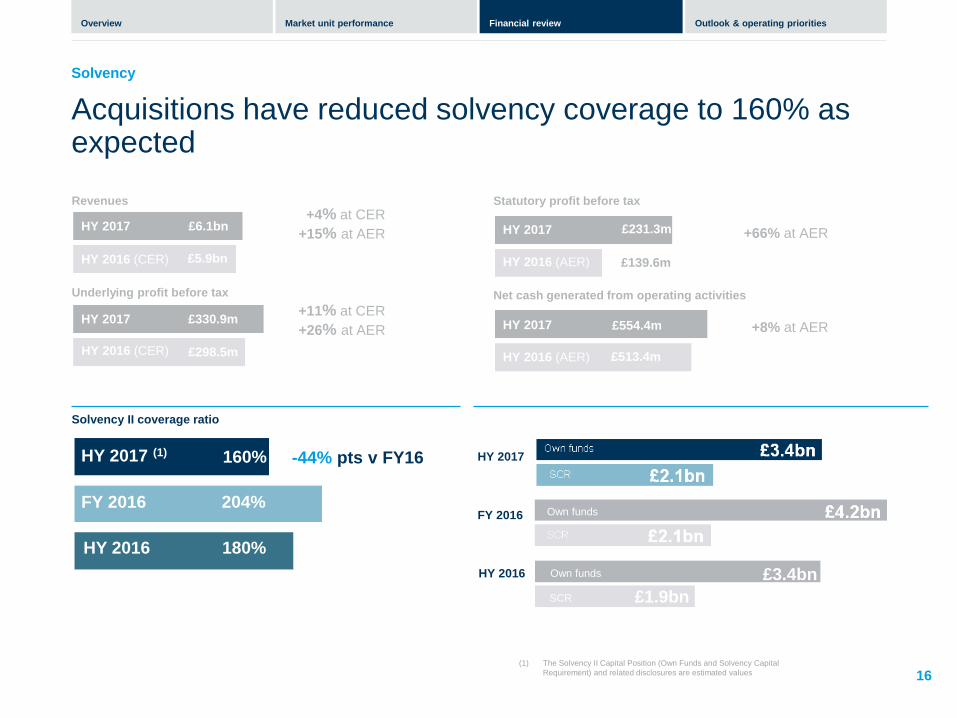

Acquisitions have reduced solvency coverage to 160% as expected

16

Solvency

Revenues

Solvency II coverage ratio

+4% at CER

+15% at AER HY 2017

HY 2016 (CER)

£6.1bn

£5.9bn

-44% pts v FY16

HY 2017 (1)

FY 2016

160%

204%

(1) The Solvency II Capital Position (Own Funds and Solvency Capital

Requirement) and related disclosures are estimated values

Underlying profit before tax

HY 2017

HY 2016 (CER)

£330.9m

£298.5m

Statutory profit before tax

+66% at AER HY 2017

HY 2016 (AER)

£231.3m

£139.6m

Net cash generated from operating activities

+8% at AER HY 2017

HY 2016 (AER)

£554.4m

£513.4m

HY 2016 180%

+11% at CER

+26% at AER

HY 2017

FY 2016

HY 2016 180%

HY 2016 Own funds £3.4bn

SCR £1.9bn

Own funds Own funds

Own funds £3.4bn

SCR £1.9bn

HY 2017 (1)

FY 2016

160%

204%

HY 2016 180%

Overview Financial review Outlook & operating priorities Market unit performance

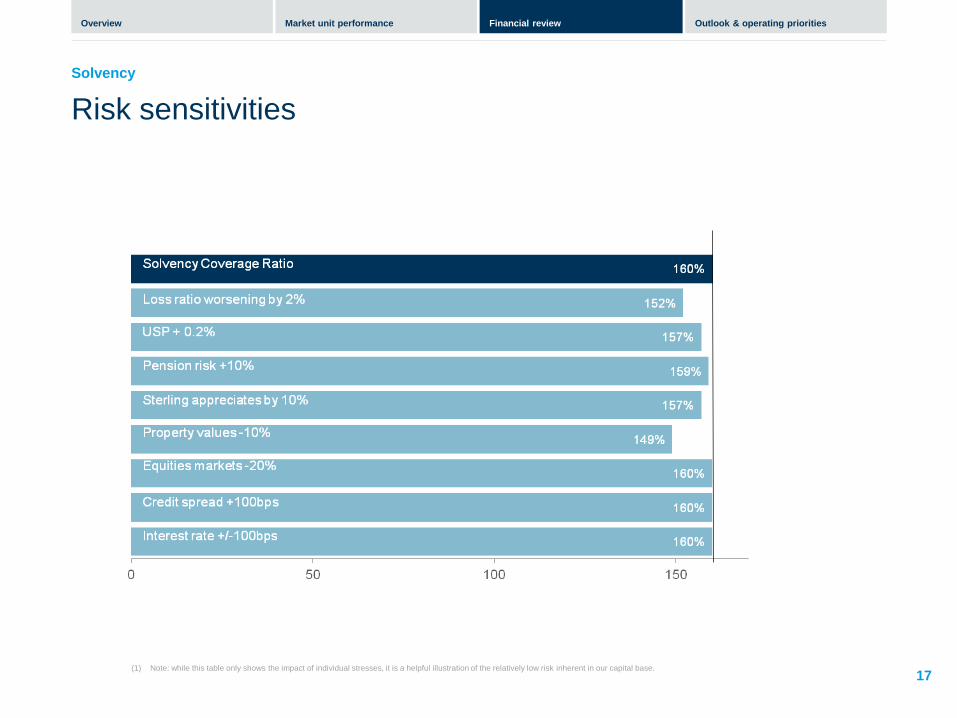

Risk sensitivities

17

Solvency

(1) Note: while this table only shows the impact of individual stresses, it is a helpful illustration of the relatively low risk inherent in our capital base.

Overview Financial review Outlook & operating priorities Market unit performance

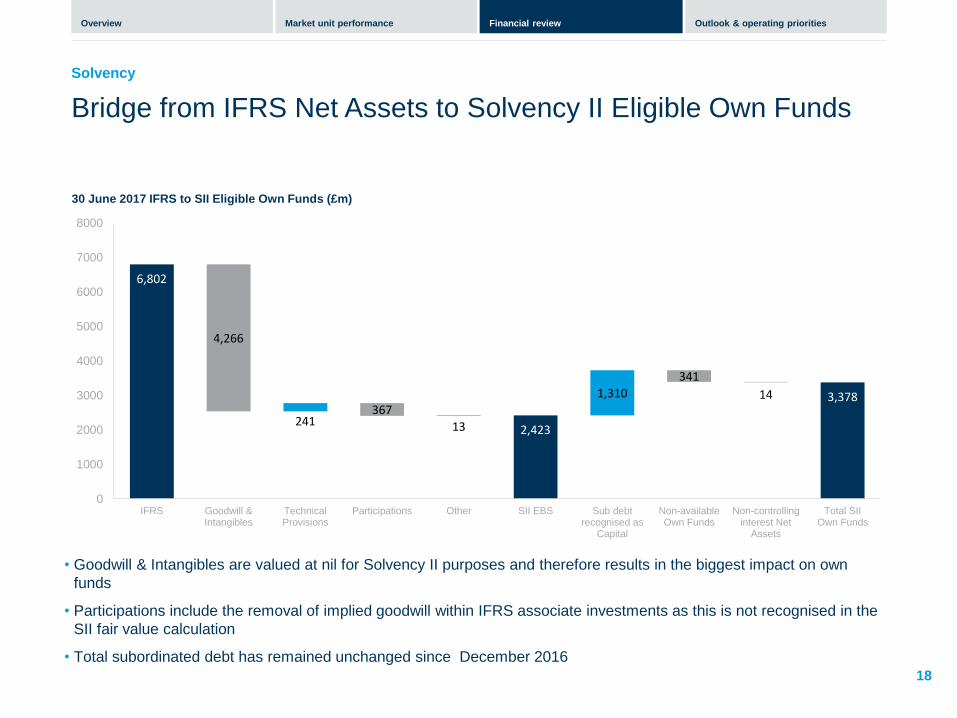

Bridge from IFRS Net Assets to Solvency II Eligible Own Funds

18

Solvency

30 June 2017 IFRS to SII Eligible Own Funds (£m)

• Goodwill & Intangibles are valued at nil for Solvency II purposes and therefore results in the biggest impact on own

funds

• Participations include the removal of implied goodwill within IFRS associate investments as this is not recognised in the

SII fair value calculation

• Total subordinated debt has remained unchanged since December 2016

6,802

2,423

3,378

241 13

1,310

4,266

367

341

14

0

1000

2000

3000

4000

5000

6000

7000

8000

IFRS Goodwill &Intangibles

TechnicalProvisions

Participations Other SII EBS Sub debtrecognised as

Capital

Non-availableOwn Funds

Non-controllinginterest Net

Assets

Total SIIOwn Funds

Overview Financial review Outlook & operating priorities Market unit performance

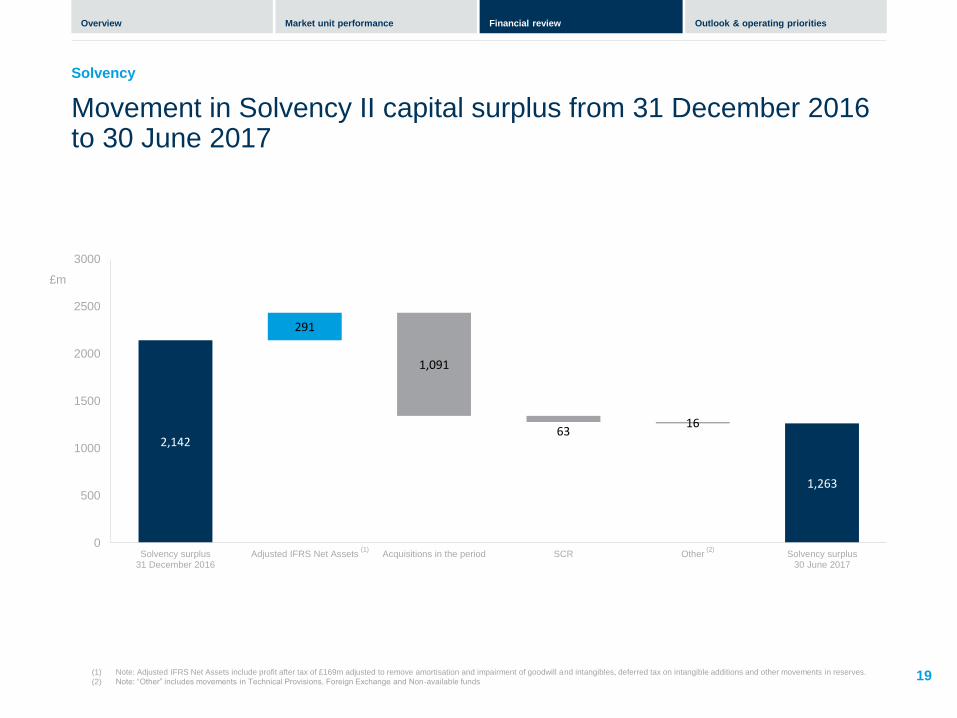

Movement in Solvency II capital surplus from 31 December 2016 to 30 June 2017

19

Solvency

Jun-18

(1) Note: Adjusted IFRS Net Assets include profit after tax of £169m adjusted to remove amortisation and impairment of goodwill and intangibles, deferred tax on intangible additions and other movements in reserves.

(2) Note: “Other” includes movements in Technical Provisions, Foreign Exchange and Non-available funds

2,142

1,263

291

1,091

63 16

0

500

1000

1500

2000

2500

3000

Solvency surplus31 December 2016

Adjusted IFRS Net Assets Acquisitions in the period SCR Other Solvency surplus30 June 2017

(1) (2)

£m

Overview Financial review Outlook & operating priorities Market unit performance

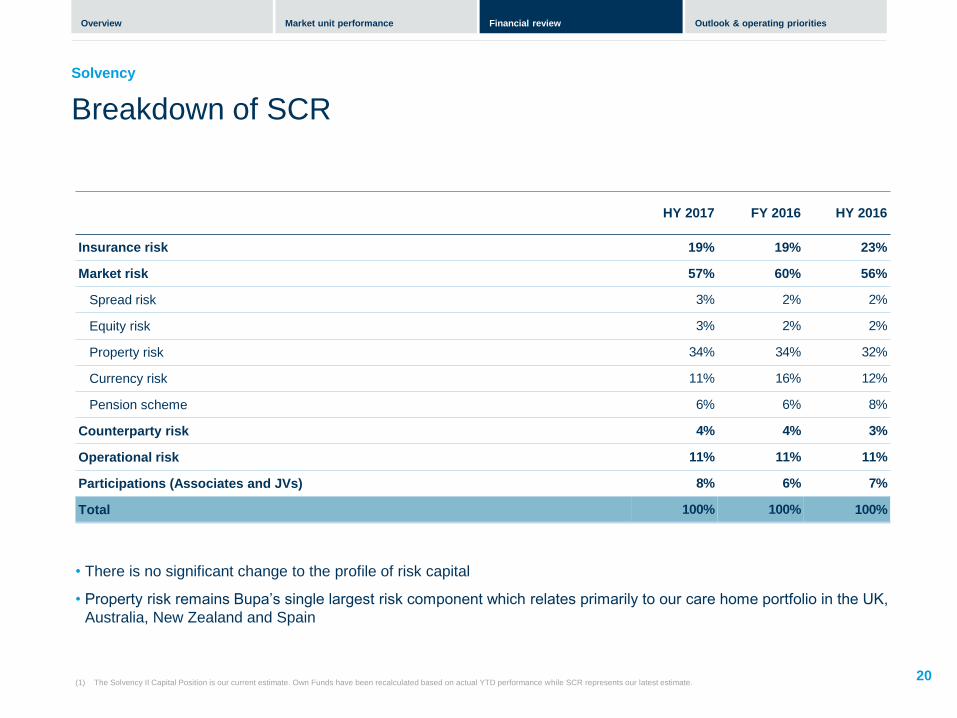

Breakdown of SCR

20

Solvency

(1) The Solvency II Capital Position is our current estimate. Own Funds have been recalculated based on actual YTD performance while SCR represents our latest estimate.

HY 2017 FY 2016 HY 2016

Insurance risk 19% 19% 23%

Market risk 57% 60% 56%

Spread risk 3% 2% 2%

Equity risk 3% 2% 2%

Property risk 34% 34% 32%

Currency risk 11% 16% 12%

Pension scheme 6% 6% 8%

Counterparty risk 4% 4% 3%

Operational risk 11% 11% 11%

Participations (Associates and JVs) 8% 6% 7%

Total 100% 100% 100%

• There is no significant change to the profile of risk capital

• Property risk remains Bupa’s single largest risk component which relates primarily to our care home portfolio in the UK,

Australia, New Zealand and Spain

Overview Financial review Outlook & operating priorities Market unit performance

Cashflow remains strong

21

Cashflow

Revenues

Net cash generated from operating activities

+4% at CER

+15% at AER HY 2017

HY 2016 (CER)

£6.1bn

£5.9bn

HY 2017

HY 2016 (AER)

£554.4m

£513.4m

Underlying profit before tax

HY 2017

HY 2016 (CER)

£330.9m

£298.5m

Statutory profit before tax

+66% at AER HY 2017

HY 2016 (AER)

£231.3m

£139.6m

+8% at AER

+11% at CER

+26% at AER

Overview Financial review Outlook & operating priorities Market unit performance

Increased leverage following acquisitions

22

HY 2017 Financial overview

Revenues

Leverage(1)

+4% at CER

+15% at AER HY 2017

HY 2016 (CER)

£6.1bn

£5.9bn

HY 2017

FY 2016

30.2%

22.6%

Underlying profit before tax

HY 2017

HY 2016 (CER)

£330.9m

£298.5m

Statutory profit before tax

+66% at AER HY 2017

HY 2016 (AER)

£231.3m

£139.6m

Net cash generated from operating activities

+8% at AER HY 2017

HY 2016 (AER)

£554.4m

£513.4m

Solvency II coverage ratio

-44% pts v FY16 HY 2017

FY 2016

160%

204%

(1) Gross debt (including hybrid debt) / gross debt plus equity

+7.6% pts v FY16

HY 2016 24.3%

HY 2016 180%

+11% at CER

+26% at AER

Overview Financial review Outlook & operating priorities Market unit performance

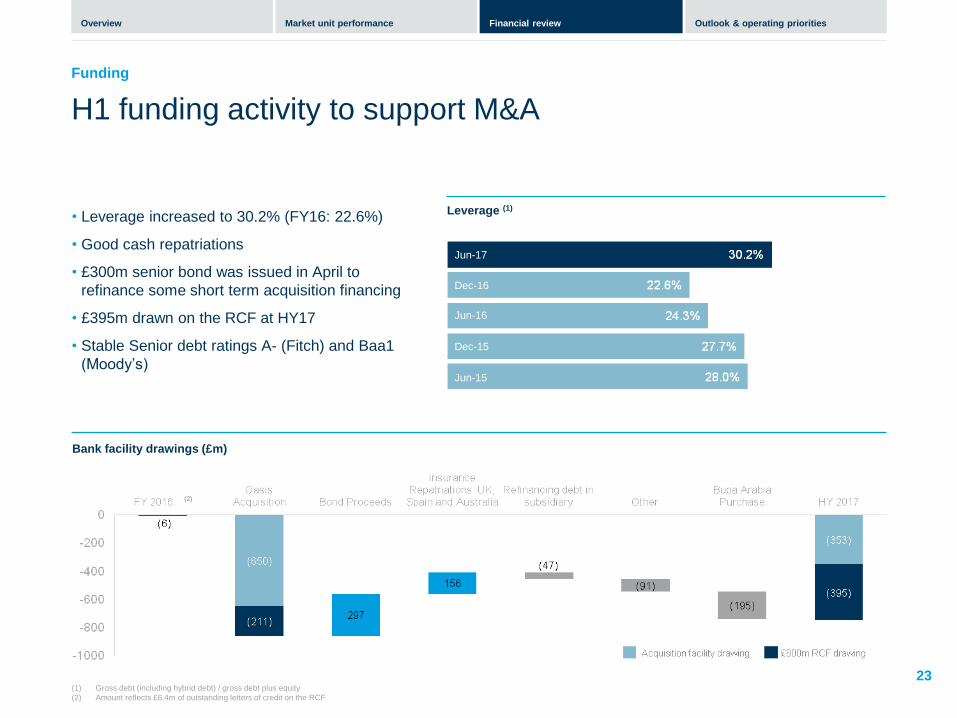

H1 funding activity to support M&A

23

Funding

Leverage (1)

Jun-17

Jun-16

Dec-15

Jun-15

Jun-18

Dec-16

• Leverage increased to 30.2% (FY16: 22.6%)

• Good cash repatriations

• £300m senior bond was issued in April to

refinance some short term acquisition financing

• £395m drawn on the RCF at HY17

• Stable Senior debt ratings A- (Fitch) and Baa1

(Moody’s)

(1) Gross debt (including hybrid debt) / gross debt plus equity

(2) Amount reflects £6.4m of outstanding letters of credit on the RCF

Bank facility drawings (£m)

(2)

Overview Financial review Outlook & operating priorities Market unit performance

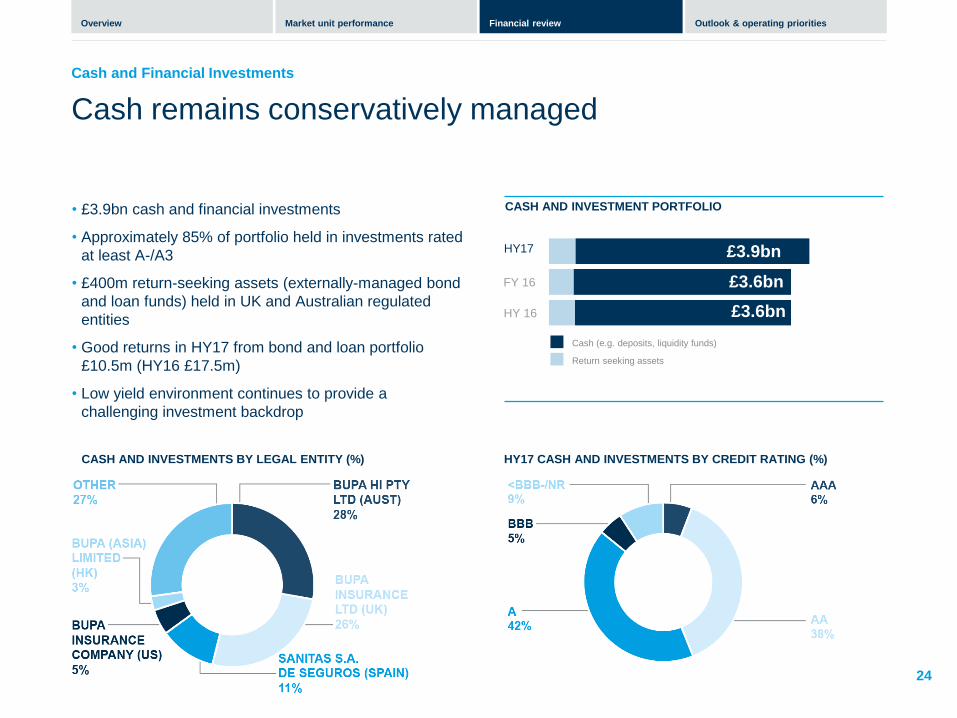

Cash remains conservatively managed

24

Cash and Financial Investments

CASH AND INVESTMENT PORTFOLIO • £3.9bn cash and financial investments

• Approximately 85% of portfolio held in investments rated

at least A-/A3

• £400m return-seeking assets (externally-managed bond

and loan funds) held in UK and Australian regulated

entities

• Good returns in HY17 from bond and loan portfolio

£10.5m (HY16 £17.5m)

• Low yield environment continues to provide a

challenging investment backdrop

HY17

Jun-18

HY17 CASH AND INVESTMENTS BY CREDIT RATING (%)

FY 16

£3.9bn

£3.6bn

Cash (e.g. deposits, liquidity funds)

Return seeking assets

HY 16 £3.6bn

CASH AND INVESTMENTS BY LEGAL ENTITY (%)

Overview Financial review Outlook & operating priorities Market unit performance

Section 4

Outlook and operating priorities Evelyn Bourke, Group CEO

25

Overview Financial review Outlook & operating priorities Market unit performance

Market conditions to remain testing in 2017; we are focused on continuously improving the customer experience

Outlook and operating priorities

Outlook:

Operating priorities:

• Demand for high quality, value-for-money healthcare

expected to remain strong

• Conditions in key markets expected to remain testing for

remainder of 2017

• Continuing to navigate volatile political and economic

environments, including UK withdrawal from EU

• Changing customer standards of personalisation, ease

and choice; high expectations of quality, safety, privacy

and transparency

• Continuously improving the customer experience

• Empowering our people to deliver for our customers

• Investing in the strength and depth of our market leading

businesses

• Disciplined capital management

• Focus on management of risk and compliance, upholding

the high standards our customers and regulators expect

26

Overview Financial review Outlook & operating priorities Market unit performance

Questions and answers

27

Overview Financial review Outlook & operating priorities Market unit performance

Further information

• For further information or to request a follow-up call or meeting, email [email protected]

• All financial results and 2016 SFCRs for Bupa Group and Bupa Insurance Limited available on www.bupa.com/Corporate/our-performance

28

Overview Financial review Outlook & operating priorities Market unit performance

Appendices

29

Overview Financial review Outlook & operating priorities Market unit performance

Organisation structure

30

Market Units

Australia and New Zealand

• Bupa Health Insurance

• Bupa Health Services

• Bupa Aged Care Australia

• Bupa New Zealand

(1) Bupa completed the purchase of Oasis Dental Care on 09 February 2017

(2) Bupa Thailand sold 25 July 2017

Appendix

UK Europe & Latin America

International Markets

• Bupa UK Insurance

• Bupa Care Services

• Bupa Health Services

• Bupa Cromwell Hospital

• Bupa Dental UK (1)

• Sanitas Seguros

• Sanitas Hospitales and

New Services

• Sanitas Dental

• Sanitas Mayores

• LUX MED

• Bupa Chile

• Bupa Global

• Bupa Arabia

• Bupa Hong Kong

• Quality HealthCare

(Hong Kong)

• Max Bupa (India)

• Bupa China

• Bupa Thailand (2)

Overview Financial review Outlook & operating priorities Market unit performance

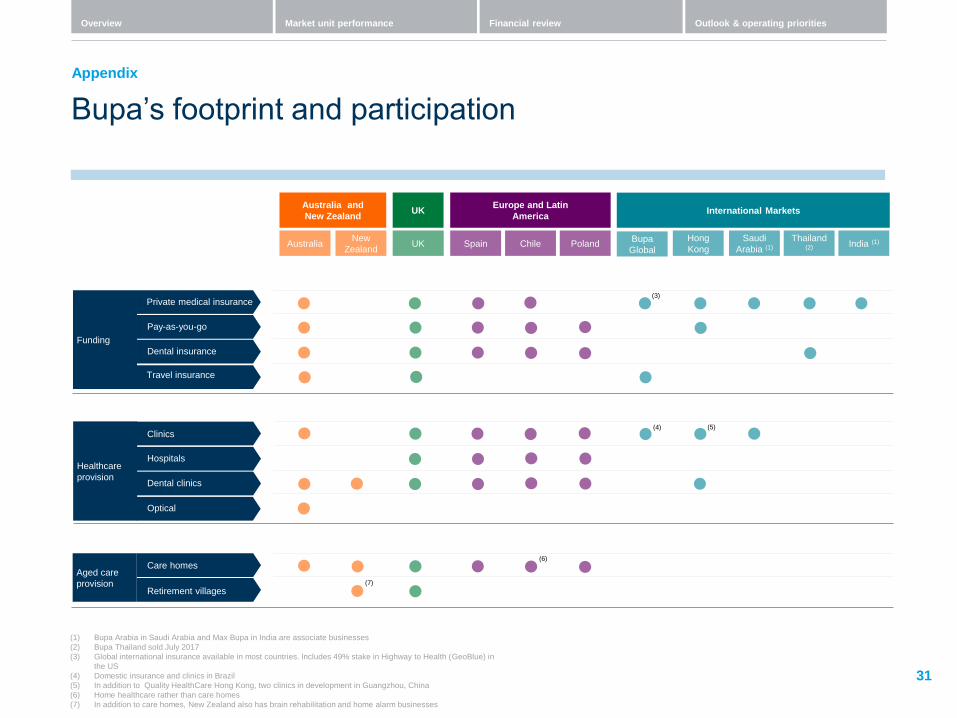

Bupa’s footprint and participation

31

Appendix

Hong

Kong

Thailand (2)

India (1) Saudi

Arabia (1) Poland

International Markets

Funding

Healthcare

provision

UK

UK

Spain

Europe and Latin

America

Chile Australia New

Zealand

Australia and

New Zealand

Private medical insurance

Pay-as-you-go

Dental insurance

Clinics

Hospitals

Dental clinics

Bupa

Global

Optical

Travel insurance

Aged care

provision

Care homes

Retirement villages

(1) Bupa Arabia in Saudi Arabia and Max Bupa in India are associate businesses

(2) Bupa Thailand sold July 2017

(3) Global international insurance available in most countries. Includes 49% stake in Highway to Health (GeoBlue) in

the US

(4) Domestic insurance and clinics in Brazil

(5) In addition to Quality HealthCare Hong Kong, two clinics in development in Guangzhou, China

(6) Home healthcare rather than care homes

(7) In addition to care homes, New Zealand also has brain rehabilitation and home alarm businesses

(7)

(3)

(4) (5)

(6)

Overview Financial review Outlook & operating priorities Market unit performance

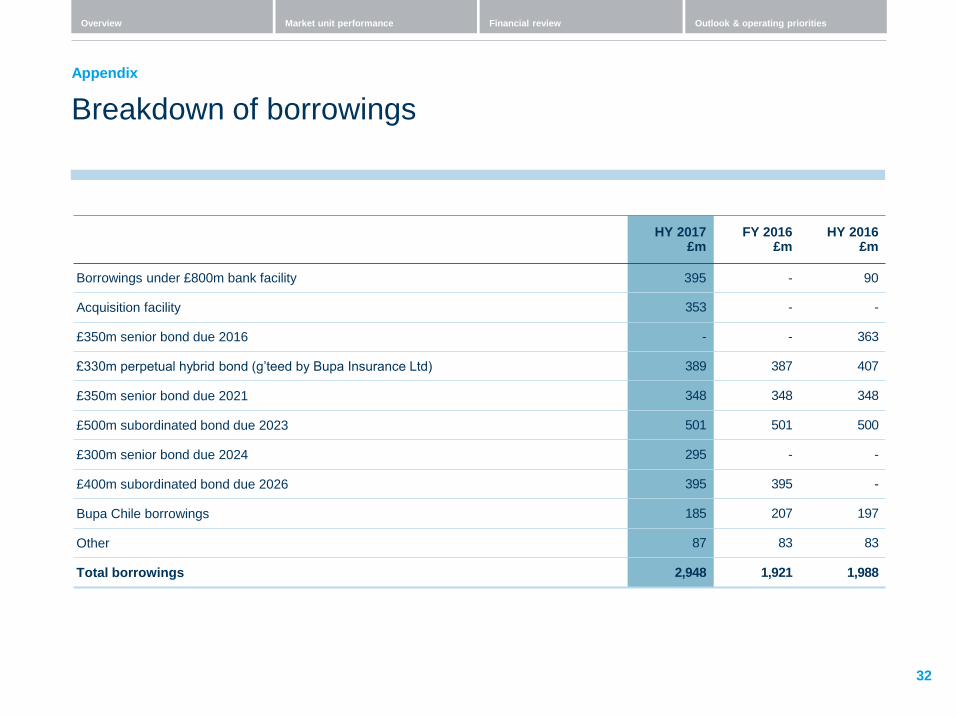

Breakdown of borrowings

32

HY 2017 £m

FY 2016 £m

HY 2016 £m

Borrowings under £800m bank facility 395 - 90

Acquisition facility 353 - -

£350m senior bond due 2016 - - 363

£330m perpetual hybrid bond (g’teed by Bupa Insurance Ltd) 389 387 407

£350m senior bond due 2021 348 348 348

£500m subordinated bond due 2023 501 501 500

£300m senior bond due 2024 295 - -

£400m subordinated bond due 2026 395 395 -

Bupa Chile borrowings 185 207 197

Other 87 83 83

Total borrowings 2,948 1,921 1,988

Appendix

Overview Financial review Outlook & operating priorities Market unit performance

Cautionary statement concerning forward-looking statements

33

This document may contain certain “forward-looking statements”. Statements that are not historical facts, including statements about the beliefs and expectations of the British United Provident Association Limited Group (“Bupa”) and Bupa’s directors or management, are forward-looking statements. In particular, but not exclusively, these may relate to Bupa’s plans, current goals and expectations relating to future financial condition, performance and results.

By their nature, forward-looking statements involve risk and uncertainty because they relate to events and depend upon future circumstances that may or may not occur, many of which are beyond Bupa’s control and all of which are solely based on Bupa’s current beliefs and expectations about future events. These circumstances include, among others, global economic and business conditions, market related risks such as fluctuations in interest rates and exchange rates, the policies and actions of governmental and regulatory authorities, the impact of competition, the timing, impact and other uncertainties of future mergers or combinations within relevant industries. Such forward-looking statements involve known and unknown risks, uncertainties and other factors, which may cause the actual future condition, results, performance or achievements of Bupa or its industry to be materially different to those expressed or implied by such forward looking statements. Other than as required by law, Bupa expressly disclaims any obligations or undertakings to release publicly any updates or revisions to any forward-looking statements to reflect any change in the expectations of Bupa with regard thereto or any change in events, conditions or circumstances on which any such statement is based.

The information contained in this presentation is intended to be read in conjunction with, and not as a substitute for, Bupa’s half year statement for the six months ended 30 June 2017 (the “HY17 Report”). In the event of any inconsistency, the HY17 Report should be considered to prevail.

Disclaimer