Half-Year Financial Report 2016haniel.corporate-reports.net/haniel/quarter/2016/q...ELG TAKKT METRO...

60

Half-Year Financial Report 2016

Transcript of Half-Year Financial Report 2016haniel.corporate-reports.net/haniel/quarter/2016/q...ELG TAKKT METRO...

Half-Year Financial Report 2016

6

8

35

54

565658

The Haniel Group

Haniel Group interim management report

Consolidated interim financial statements

Responsibility statement

Additional informationContactPublication details

Haniel Key Figures

SUMMARY OF THE CONSOLIDATED INTERIM FINANCIAL STATEMENTS

EUR million 1st half-year 2015 1st half-year 2016 Change

Revenue 1,982 1,800 -9%

Operating profit 109 115 +6%

Profit before taxes 13 57 >+100%

Profit after taxes -21 25 >+100%

Haniel cash flow 204 233 +14%

Buy & build strategy successful

Encouraging growth in all Haniel Group earnings figures

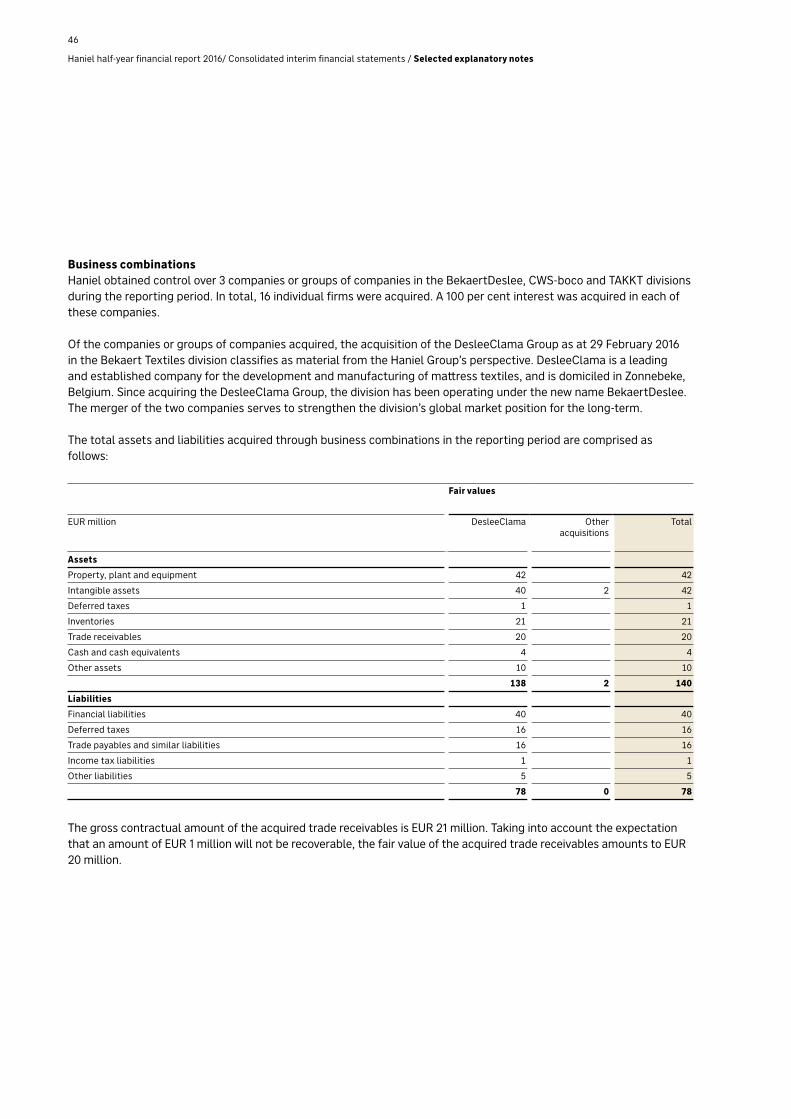

Bekaert Textiles integrates DesleeClama

Sales initiative stimulates growth at CWS-boco

Revenue weighed down by cyclical ELG business

Strong revenue and earnings growth at TAKKT

Investment result lifted by Metro

Haniel establishes Schacht One digital unit and invests in digital- focussed venture capital funds

The Franz Haniel & Cie. Holding Com-pany is a tradition-steeped German family-equity company. It maintains a diversified portfolio and pursues a long-term investment strategy as a value developer. Its objective is to continually increase the value of the Company while also strengthening its social and environmental values. The Company has always been headquartered in Duis-burg-Ruhrort, where it has been shaping the future since 1756. www.haniel.de/en

Franz Haniel & Cie. GmbH

BekaertDeslee

BekaertDeslee is the leading specialist for the development and manufacturing of woven and knitted mattress textiles.www.bekaertdeslee.com

CWS-boco

CWS-boco ranks among the leading international full-service providers of washroom hygiene products, dust control mats, workwear and textile services.www.cws-boco.com

EQUITY INTEREST 100%

EUR million 30 Jun. 2015* 30 Jun. 2016

Revenue 20 146

Operating profit 2 10

Employees (average headcount) 1,498 2,337

Haniel half-year financial report 2016 / The Haniel Group

6

EQUITY INTEREST 100%

EUR million 30 Jun. 2015 30 Jun. 2016

Revenue 382 393

Operating profit 36 37

Employees (average headcount) 7,574 7,608

* Bekaert Textiles was acquired by Franz Haniel & Cie. GmbH in the first half of 2015. These figures therefore relate exclusively to June 2015.

EQUITY INTEREST 25.00%

EUR million 30 Jun. 2015 30 Jun. 2016

Haniel investment result -60 -30

METRO GROUP

METRO GROUP is among the premier international merchandisers.www.metrogroup.de

ELG

ELG is a global leader in the trading, processing and recycling of raw mate-rials for the stainless steel industry as well as high performance materials such as superalloys, titanium and car-bon fibres.www.elg.de

TAKKT

TAKKT bundles a portfolio of B2B direct marketing specialists for business equipment in Europe and North Amer-ica in a single company.www.takkt.com

7

Haniel half-year financial report 2016 / The Haniel Group

EQUITY INTEREST 100%

EUR million 30 Jun. 2015 30 Jun. 2016

Revenue 1,074 707

Operating profit 11 2

Employees (average headcount) 1,301 1,188

EQUITY INTEREST 50.25%

EUR million 30 Jun. 2015 30 Jun. 2016

Revenue 506 554

Operating profit 65 81

Employees (average headcount) 2,348 2,485

Haniel Group Interim Management Report

8

10

1212

192224262830

32

Group structure and business models

Report on business situationHaniel Group12 Revenue and earnings performance14 Financial position17 Assets and liabilities18 Employees

Holding Company Franz Haniel & Cie. BekaertDesleeCWS-bocoELGTAKKTMETRO GROUP

Report on expected developments

10

Group structure and business models

The Haniel Group combines four divisions and one financial investment. Franz Haniel & Cie. GmbH functions as a strategic management holding company and is responsible for portfolio management. The operating business is in the hands of the five investments, which act independently of one another and which each occupy a leading market position.

Holding Company designs the portfolioFranz Haniel & Cie. GmbH is a tradition-steeped German family-equity company whose objective is to sustainably increase the value of its investment portfolio over the long term. Since the family shareholders have provided equity for an unlimited term, Haniel can pursue a long-term investment strategy. This strategy is aimed to-wards generating returns which permanently exceed the cost of capital. Haniel strives to achieve this economic goal in harmony with ecological and social goals. The Company is pursuing this goal by following the guiding principle of the “honourable businessman”. In addi-tion, capital and management are separated at Haniel: Although the Company is 100 per cent family owned, no member of the Haniel family works at the Company.

Haniel is family equity. Family equity combines the best of both worlds,

uniting the professionalism of private equity with the values of a family-owned business.

When structuring the portfolio, Haniel concentrates on business models that are supported by global mega-trends and therefore have a high potential for increases in value over the long term. Promising markets and business models are analysed continually in order to detect growth opportunities. In February 2016, the Bekaert Textiles division – which has been part of the Haniel Group since June 2015 – acquired the DesleeClama Group, significantly expanding its global market position. As a consequence, the company has since traded as BekaertDeslee. The Holding Company actively supports the corresponding integration measures. This once again demonstrates Haniel’s buy & build approach: to acquire new divisions and promote their growth, both organically and through their own acquisitions.

Haniel as strategic catalystIn addition to portfolio management, the Holding Com-pany is also responsible for setting strategic guidelines for the operating divisions – in this respect the Holding Company considers itself as a strategic catalyst. Stra-tegic initiatives are agreed on in discussion with the

Haniel half-year financial report 2016 / Haniel Group interim management report / Group structure and business models

Haniel portfolio

Financial investment

Equity interest 100%

Equity interest 100%

Equity interest 100%

Equity interest 50.25%

Equity interest 25.00%

BekaertDeslee is the leading specialist for the develop-ment and manufacturing of woven and knitted mattress textiles.

CWS-boco ranks among the leading international full-service providers of washroom hygiene products, dust control mats, workwear and textile services.

ELG is a global leader in the trading, processing and re-cycling of raw materials for the stainless steel industry as well as high perfor-mance materials such as superalloys, titanium and carbon fibres.

TAKKT bundles a portfolio of B2B direct marketing specialists for business equipment in Europe and North America in a single company.

METRO GROUP is among the premier international merchandisers.

BekaertDeslee CWS-boco ELG TAKKT METRO GROUP

Divisions

Haniel half-year financial report 2016 / Haniel Group interim management report / Group structure and business models

11

divisions; these are implemented by the divisions under their own responsibility. The divisional management teams report regularly to Haniel’s Management Board on their progress. The Holding Company is also respon-sible for selecting and developing top executives for the divisions, providing the divisions with proven tools and offering selected services. The high relevance of digitalisation and the opportunities that it presents have motivated Haniel to provide a team of experts to sup-port all divisions in their implementation of appropriate digitalisation projects. Since April 2016, these activities have been bundled in Schacht One GmbH which, with its headquarters in the Zollverein Coal Mine Industrial Com-plex with a rich tradition in Essen, builds on the dynamic for change and innovative spirit in Haniel’s history.

Haniel’s specific role as an active investment holding company ensures that all divisions use their respective business models to contribute to the value enhance-ment of the investment portfolio in the best manner possible.

No risks jeopardising the going concern assumptionAt present, no risks which may jeopardise the Group as a going concern have been identified, nor have notable risks exceeding those normally encountered in busi-ness. The risks and opportunities of future development discussed in detail starting on page 65 of the 2015 annual report remain relevant to the Haniel Group. For a discussion of expected developments in the current financial year, please refer to the report on expected developments starting on page 32 of this Half-year Financial Report.

Haniel half-year financial report 2016 / Haniel Group interim management report / Report on business situation / Haniel Group / Revenue and earnings performance

12

Essentially stable market environmentIn the first months of 2016, the economic environment proved essentially stable in the markets relevant for the Haniel Group. There was slight growth in the developed economies, where the divisions are primarily active. In this regard, economic growth and the resultant stimuli for business development remained stronger in the US than in Europe. Europe continued to record stable growth following the moderate but constant recovery in the prior year. In Europe, the Haniel Group benefited in particular from the continuing steady growth in Ger-many. Global economic growth was also characterised by reduced momentum in the emerging markets and de-veloping countries, particularly China. The uncertainties in the market environment were fuelled by the “Brexit” referendum in the United Kingdom on 23 June, which re-sulted in a vote to leave the European Union in the fore-seeable future. A number of political developments and conflicts in the Arab world and in Africa also contributed to a worsening of the economic environment.

In addition to the macroeconomic environment, the conditions in the stainless steel market segment are of great significance to the Haniel Group. These conditions were substantially worse in the first half of 2016 than in the previous year. A major cause of this was the sus-tained economic cooling in China. Dampened economic expectations and the worldwide oversupply of primary nickel resulted in a persistent price decline for nickel, the most significant price driver in stainless steel. On average, prices were down 37 per cent year on year. However, there was also a year-on-year decrease in the commodity prices relevant for the ELG division, e.g. iron, chrome and titanium.

Although the positive economic trend in the US and Ger-many had a positive effect on the Haniel Group’s revenue and earnings performance, the negative conditions in the stainless steel and superalloy market segments and the reduced momentum in the emerging markets and developing countries had offsetting effects.

Revenue boosted by acquisitionsDuring the first half of 2016, the Haniel Group recorded a 9 per cent decline in revenue, to EUR 1,800 million. This is attributable solely to ELG. The significantly lower prices for all relevant commodities – in particular the considerable drop in nickel prices – and the reduced out-put tonnage due to the difficult market environment af-fected this development. Revenue was primarily boosted by the positive contribution made by the BekaertDeslee division, which covered an entire half-year period for the first time. The newly acquired division had only been included in the figures for one month during the same period of the previous year. Bekaert Textiles’ acquisition of the DesleeClama Group in February 2016 also made a positive contribution to revenue growth in the four months that followed. TAKKT’s acquisitions of Post-Up Stand and BiGDUG also contributed to additional revenue, as did other smaller acquisitions by CWS-boco in the previous year. Organic growth in the TAKKT and CWS-boco divisions was also encouraging. Currency translation effects only had a minor impact. Adjusted for business combinations and disposals as well as currency

30 Jun. 2015 30 Jun. 2015

REVENUEEUR million

1,982 1,800

30 Jun. 2016 30 Jun. 2016

-9% +6%

OPERATING PROFITEUR million

109 115

Haniel GroupRevenue and earnings performance

Group revenue declined in the first six months of the financial year due to the continuing weak performance of the commodity markets in the ELG divi-sion, which had been expected. All other divisions saw growth in their contribu-tions to revenue in the first half of 2016. In addition, the Haniel Group was able to generate encouraging growth in all earnings figures.

Haniel half-year financial report 2016 / Haniel Group interim management report / Report on business situation / Haniel Group / Revenue and earnings performance

13

translation effects, the Haniel Group’s revenue was down year on year by 16 per cent.

Buy & build strategy a success: BekaertDeslee division makes a positive

contribution to revenue and earnings growth.

Operating profit improvedIn the first half of 2016, the Haniel Group’s profit was boosted by the fact that the new BekaertDeslee division was included for the first time over six months. However, growth at TAKKT also made a significant contribution. CWS-boco also generated slightly higher operating profit. The reduction in output tonnage and the significant drop in the price of nickel meant a considerably weaker operating profit for ELG than in the first half of 2015. In the aggregate, however, ELG’s deficit was more than offset; as a consequence, operating profit amounted to an encouraging EUR 115 million in the first half of 2016, up on the prior-year figure of EUR 109 million.

Profit before taxes significantly higherProfit before taxes increased significantly from EUR 13 million to EUR 57 million. In addition to the improved operating profit, this is attributable in particular to a higher investment result and an improved result from financing activities.

The investment result improved from EUR -60 million in the same period of the previous year to EUR -31 mil-lion in the first half of 2016. This was caused by the METRO GROUP, which firstly reported a year-on-year increase in operating profit due to lower one-off factors, and secondly generated improved net financial income. By contrast, the METRO GROUP’s less favourable tax result as against the first half of 2015 had an adverse effect. With a view to the negative investment result, it should be taken into account that the essentially pos-itive contribution to earnings from the METRO GROUP regularly does not occur until the Christmas season during the fourth quarter of Haniel’s financial year.

The result from financing activities, comprising the finance costs and other net financial income, amounted to EUR -27 million in the reporting period. In the same period of the previous year, this figure had amounted to EUR -36 million. A significant reason for this improve-ment was the year-on-year decrease in finance costs due to the lower level of indebtedness. Haniel thus contin-ued to benefit from the systematic debt reduction.

Significant rise in profit after taxesWith a slight drop in the tax expense, the growth in profit before taxes had a significant impact on profit after taxes. This rebounded from EUR -21 million in the prior-year period to EUR 25 million in the first half of 2016, an improvement of EUR 46 million.

PROFIT BEFORE TAXESEUR million

13 57

>+100% >+100%

PROFIT AFTER TAXES EUR million

-21 25

30 Jun. 2015 30 Jun. 2016 30 Jun. 2015 30 Jun. 2016

Financial governance between the Holding Company and the divisionsThe ultimate objective of financial management is to cover the financing and liquidity needs at all times while maintaining entrepreneurial independence and limiting financial risks. The Holding Company prescribes principles to the divisions in order to establish minimum organisational requirements and to govern the structure of key financial management processes, including finan-cial risk management. These directives are documented in guidelines for the treasury departments of the Hold-ing Company and the divisions. The Holding Company and the divisions use this basis to identify, analyse and evaluate the financial risks that each operating business is responsible for – in particular liquidity, credit, interest rate and currency risks – and take measures to avoid or limit these risks. In addition, the Holding Company sets the financing and financial risk management strategy and approves the financial counterparties and financial instruments used, as well as limits and reports.

While staying within these guidelines, the divisions man-age their own financing based on their own financial and liquidity planning. Cash management is also the respon-sibility of the divisions. In order to leverage economies of scale, the Holding Company and its finance companies support the divisions and, together with partner banks, offer cash pools in various countries. Combining central directives with the autonomy of the divisions in terms of their financing takes into account both the different levels of investment by the Holding Company in the divisions as well as the divisions’ individual requirements for financial management.

Trusting cooperation with financing partnersAs a family business with stable but limited equity financing, access to sources of debt capital are of high importance to Haniel. Accordingly, a good reputa-tion with financial partners is essential. A significant aspect of this is providing rating agencies and business partners with timely and transparent information and the equal treatment of banks and investors. Only if this is ensured can a company earn a high degree of trust from banks and investors as a long-standing and reliable business partner, such as Haniel has enjoyed for many years.

Scope and S&P affirm investment grade ratingHaniel submits itself to external rating assessments voluntarily, thus ensuring broad access to capital mar-kets. European rating agency Scope assessed Haniel’s creditworthiness for the first time in February 2016. The future-oriented approach used for the analysis convinced Haniel to provide the Scope rating to its in-vestors as a further opinion. Haniel received a long-term issuer rating of BBB- with a stable outlook, with Scope therefore classifying it as investment grade. In April 2016, Standard & Poor’s (S&P) raised its Long and Short Term Corporate Credit Rating from BB+/B (positive outlook) to BBB-/A-3 (stable outlook). This improved rating also corresponds to an investment grade rating. Both ratings are a result of Haniel’s sustained conserva-tive financial policy. This is distinguished by a moderate target net financial debt level of EUR 1 billion at the level of the Holding Company coupled with a solid long-term financing structure. The improvement in the rating also marked a positive assessment of Haniel’s cautious financial investment policy and its prudent approach to investments.

The ratings improvements were also supported by the sound development of the total cash cover and market value gearing, key figures which are crucial to the rating. Total cash cover is calculated as the ratio of proceeds from dividends and profit transfers to payments for cur-rent costs incurred by the Holding Company, as well as interest and dividends to the Haniel family. Market value gearing corresponds to the ratio of net debt to the value of the Haniel investment portfolio. It amounted to 17 per cent as at the 30 June 2016 reporting date and was thus within very comfortable territory.

Haniel GroupFinancial position

Haniel’s financial strategy is bearing fruit: after European rating agency Scope had already classified Haniel as investment grade, Standard & Poor’s followed suit and raised its rating. Both ratings take account of Haniel’s sus-tained conservative financial policy: the Holding Company remains de facto debt-free and is thus well equipped for further investments to expand its portfolio.

Haniel half-year financial report 2016 / Haniel Group interim management report / Report on business situation / Haniel Group / Financial position

14

Broad-based financingThe Haniel Group’s financial management relies on di-versification of financing: various financing instruments with a broad range of business partners ensure access to liquidity at all times and reduce the dependency on individual financial instruments and business partners. Overall, the Haniel Group had used and unused credit facilities on the scale of EUR 2 billion at the end of the first half of 2016. This exemplifies the active pursuit of security and independence.

A balanced maturity profile with an appropriate, long-term orientation guarantees additional financial stability. A further key pillar of financial management is the ability to obtain funding on the capital market. To that end, the Holding Company updates its commercial paper programme at longer intervals and its debt issuance programme (still in the amount of EUR 2 billion) annually. Based on information contained therein, bonds can be placed very flexibly in terms of the timing and amount and adjusted to the respective market conditions.

Overall, the financial liabilities reported in the Haniel Group’s Statement of Financial Position were EUR 1,637 million as at 30 June 2016. Of that amount, EUR 597 million has a maturity of more than one year. Of the EUR 1,040 million in liabilities reported as current liabilities, EUR 473 million were attributable to the exchangeable bond linked to ordinary shares in METRO AG. Although

this only reaches maturity in 2020, it is reported as a current liability due to the right of the bondholders to exchange the bond for shares, which can be exercised at any time.

The value of outstanding bonds as at 30 June 2016 remained level with the figure of EUR 0.9 billion recorded at the end of 2015. In addition, the CWS-boco, ELG and TAKKT divisions have also financed themselves on the market for promissory notes in recent years, thus broadening their financing base. As at 30 June 2016, the value of promissory note loans, commercial paper and other securitised liabilities in the Haniel Group remained unchanged as against 31 December 2015, at EUR 0.2 bil-lion. In addition, the BekaertDeslee, CWS-boco and ELG divisions maintain programmes for the continual sale of trade receivables to third parties.

Solid financial buffer despite increased net debtThe net financial liabilities of the Haniel Group, i.e., finan-cial liabilities less cash and cash equivalents, increased slightly to EUR 1,393 million as at 30 June 2016 com-pared to EUR 1,338 million at the end of 2015. The Haniel Group’s net financial position also rose, increasing to EUR 546 million in the first half of 2016 versus EUR 445 million as at 31 December 2015. The net financial position equals the net financial liabilities less the investment position of the Holding Company – excluding current and non-current receivables from affiliated companies. The rise in both net financial debt and the net financial posi-tion is due in particular to the use of financial resources for the DesleeClama Group acquisition.

At the level of the Holding Company, net financial lia-bilities also increased, rising from EUR 849 million as of 31 December 2015 to EUR 960 million as of 30 June 2016. This is also due to the fact that the Holding Company provided the divisions with financial resources, thus reducing its own cash and cash equivalents. Thanks to the financial support provided by the Holding Company, the Bekaert Textiles division acquired last year was able to complete the above-mentioned DesleeClama Group acquisition and further accelerate its growth.

The net debt is offset by a portfolio of financial assets that will be used in the coming years to acquire addi-tional divisions as well as to redeem outstanding bonds.

+14%204 233

-64%754 275

Haniel half-year financial report 2016 / Haniel Group interim management report / Report on business situation / Haniel Group / Financial position

15

30 Jun. 2015 30 Jun. 2016 30 Jun. 2015 30 Jun. 2016

HANIEL CASH FLOWEUR million

CAPITAL EXPENDITUREEUR million

16

Including current and non-current receivables from affiliated companies, the Holding Company had financial assets valued at EUR 1,226 million as at 30 June 2016. Since financial assets continue to exceed net financial debt, the Holding Company remains de facto debt-free and has a solid financial buffer.

Haniel cash flow increases furtherThe Haniel Group uses the performance indicator Haniel cash flow to assess the strength of its liquidity position in its current business activities. Haniel cash flow is first and foremost available for the purpose of financing current net assets* and investments. In the first half of 2016, Haniel cash flow increased from EUR 204 million in the prior-year period to EUR 233 million. This was primarily due to the encouraging performance in the operating business in almost all divisions.

Cash flow from operating activities, which supplement Haniel cash flow in depicting the change in current net assets, amounted to EUR 164 million in the first half of 2016, and were thus lower than Haniel cash flow. This is mainly attributable to the increase in trade receivables due to lower sales of receivables at CWS-boco and higher tax receivables. In the same period of the previous year, cash flow from operating activities amounted to EUR 243 million, which was higher than the Haniel cash flow. This is attributable to the fact that financial resources were freed up as a result of the decrease in current net assets. In turn, this was due primarily to a lower price for nickel and reduced output tonnages at ELG, which resulted in declining inventories and reduced trade receivables.

EUR million 30. Jun. 2015 30. Jun. 2016

Haniel cash flow 204 233

Cash flow from operating activities 243 164

Cash flow from investing activities -218 -123

Cash flow from financing activities 253 -137

DesleeClama Group acquisition as largest single investmentCash flow from investing activities, i.e. the net outlays for capital expenditure and proceeds from divesting activities, amounted to EUR -123 million in the first half of 2016. Payments for investments amounted to EUR 275 million, which includes the DesleeClama Group acqui-

sition as the largest single investment. This figure also includes acquisitions of financial investments by the Holding Company in addition to the divisions’ invest-ments in intangible assets and in property, plant and equipment. The payments compare to proceeds from divestment activities amounting to EUR 152 million. These were primarily attributable to the sale of financial investments by the Holding Company. During the same period of the previous year, cash flow from investing ac-tivities had amounted to EUR -218 million. This included higher payments with the figure of EUR 754 million – in comparison with the first half of 2016 – primarily for the Holding Company’s acquisition activities and those of the divisions, their investments in intangible assets and in property, plant and equipment, and the Holding Com-pany’s financial investments. In the prior-year period, the payments compared to likewise higher proceeds from divestment activities amounting to EUR 536 million. In the first half of 2015, that figure primarily consisted of a cash inflow from the disposal of Metro shares.

Cash flow from financing activities amounted to EUR -137 million, as against EUR 253 million in the first half of 2015. A dividend in the amount of EUR 50 million was paid out to the shareholders of Franz Haniel & Cie. GmbH in 2016, and debt was repaid, primarily at TAKKT and ELG. In the prior-year period, cash inflows from financing activities exceeded the corresponding cash outflows due to the fact that Haniel had generated a high cash inflow from the issue of the exchangeable bond linked to Metro shares.

* Net current assets consist essentially of trade receivables and inventories less trade payables.

Haniel half-year financial report 2016 / Haniel Group interim management report / Report on business situation / Haniel Group / Financial position

31 Dec. 2015 31 Dec. 201530 Jun. 2016 30 Jun. 2016

Haniel GroupAssets and liabilities

6,847

16%

61%

23%

6,726

22% Current liabilities

18% Non-current liabilities

60% Equity

6,847

24%

76%

6,726

24% Current assets

76% Non-current assets

Lower total assetsThe Haniel Group’s total assets declined from EUR 6,847 million as at 31 December 2015 to EUR 6,726 million as at 30 June 2016. This was reflected above all in non-cur-rent assets, which declined from EUR 5,237 million as at 31 December 2015 to EUR 5,129 million. The primary cause was the lower carrying amount of the Metro investment due to the dividend payment. The acquisition of the DesleeClama Group caused a rise in intangible as-sets and property, plant and equipment, which increased non-current assets. A portion of the Holding Company’s cash and cash equivalents was used to finance the DesleeClama Group acquisition; by contrast, the first-time inclusion of the company increased current assets, which remained stable year on year.

High equity ratio underscores investment potential Equity declined slightly from EUR 4,169 million as at 31 December 2015 to EUR 4,035 million as at 30 June 2016. This was caused by negative measurement effects for pensions and currency translation. Despite the decrease, the lower total assets meant that the equity

Even after the DesleeClama Group ac-quisition, the Haniel Group continues to boast a very solid balance sheet. The eq-uity ratio remains high, underscoring the investment potential at Haniel’s disposal.

ratio remained almost constant at 60 per cent. This sustained high level underscores Haniel’s investment potential. Non-current liabilities declined to EUR 1,198 million, primarily due to the reclassification of the Hold-ing Company’s bonds that mature in 2017. By contrast, current liabilities increased from EUR 1,105 million as at 31 December 2015 to EUR 1,493 million, primarily due to the reclassification of these bonds.

Recognised investments down on high prior-year figureThe Haniel Group’s recognised investments declined from EUR 616 million in the same period of the previous year to EUR 283 million in the first half of 2016. This decrease was caused by the high level of recognised investments in the previous year, which was primar-ily due to the acquisition of the new Bekaert Textiles division. This was partly offset in the first half of 2016 by lower acquisition volumes due to the DesleeClama Group acquisition.

Haniel half-year financial report 2016 / Haniel Group interim management report / Report on business situation / Haniel Group / Assets and liabilities

17

EQUITY AND LIABILITY STRUCTUREEUR million

Consolidated statement of financial position

ASSET STRUCTUREEUR million

The number of employees in the Haniel Group increased by 7 per cent, in particular due to the acquisition of DesleeClama by the Bekaert Textiles division. As a result, the number of employees in the Haniel Group averaged 13,829 in the first half of 2016, compared with 12,930 at the end of 2015.

The global headcount in the BekaertDeslee division, which has been operating under this name since March 2016, averaged 2,337 in the first half of 2016.

The average number of employees at CWS-boco was 7,608 in the first half of 2016, versus an average of 7,563 employ-ees in the previous year. The slight increase was primarily due to the strengthening of the sales function, which was systematically pursued as part of the sales initiative.

The average headcount at ELG decreased from 1,282 in the previous year to 1,188 in the first half of 2016. In the stainless steel business, the division further adapted its capacities to the tense market situation.

Haniel GroupEmployees

The number of employees in the Haniel Group increased in the first half of 2016, primarily as a result of the Group’s acqui-sition activity. The Haniel Group’s aver-age headcount amounted to 13,829 in the first half of 2016.

+7%

EMPLOYEESAverage headcount

12,930 13,829

The average number of employees at TAKKT increased slightly from 2,403 in the previous year to 2,485; this was due to the positive business development and the expansion of the digital activities. It was only offset to a limited extent by the decision to withdraw from China in the first half of 2016.

Digitalisation is also affecting human resource requirements: key positions such as Chief Digital Officer or Senior Digital Advisor

were created and newly filled.

Digitalisation will give rise to a qualitative change in hu-man resources requirements in the foreseeable future. In addition, the business culture – primarily the means of co-operation – will be subject to lasting change. In addition to establishing its own digital unit, Schacht One, Haniel has organised training and initiatives to promote dialogue as a first step toward address this trend.

18

Haniel half-year financial report 2016 / Haniel Group interim management report / Report on business situation / Haniel Group / Employees

31 Dec. 2015 30 Jun. 2016

19

Haniel half-year financial report 2016 / Haniel Group interim management report / Report on business situation / Haniel Group / Holding Company Franz Haniel & Cie.

Holding Company Franz Haniel & Cie.

Portfolio successfully enhanced The Holding Company supported Bekaert Textiles, a leading specialist for the development and manufacturing of mattress textiles that it had acquired in June 2015, in acquiring the DesleeClama Group, financing the acquisition and in the subsequent integration process. This supplementary acquisition enabled the company to consolidate its position in established markets and expand its position in new regions. The division has been operating under the name BekaertDeslee since March 2016.

Following the successful portfolio measures initiated in the first half of 2016, more than EUR 1.0 billion is intended to be invested to acquire further new divisions. As a family- equity company, Haniel pursues a long-term investment approach. Its focus lies on well-positioned medium-sized companies which operate in attractive niches which can expand their market-leading position with the help of Haniel, contributing to the diversification of the portfolio. In addition, Haniel gives preference to the acquisition of controlling interests in non-listed companies, which can also take place in stages. In line with Haniel’s objective of being “enkelfähig”, the only candidates for acquisition are companies which already make a positive contribution to the environment and society through their sustainable actions, or which will be able to do so in the future.

The intention is to invest more than EUR 1.0 billion in acquiring further new divisions.

The Holding Company* successfully enhanced the portfolio in the first half of 2016 and provided key momentum for further development: the family equity company supported its market-leading Bekaert Textiles division, which was ac-quired in 2015, in its own acquisition and integration of the DesleeClama Group. The Schacht One digital unit and the in-vestments in digital-focused venture cap-ital funds will provide new momentum to further develop the value of the portfolio.

Haniel will continue to find the right companies by patiently and prudently weighing the options as they arise – the Bekaert Textiles acquisition and its expansion to include the DesleeClama Group illustrates this approach.

Strategic momentum for investments and future value growth In the first half of the year, the Holding Company launched several forward-looking initiatives aimed at developing the future value of the portfolio. These are aligned with Haniel’s objective of acting as a value developer for the investments and keeping both value and values in view.

The Holding Company established Schacht One, Haniel’s own digital unit in the historic Zollverein Coal Mine Industrial Complex in Essen, to help implement the Digital Agenda at the investments. Schacht One will work together with the divisions to develop and directly assess the plausibility of innovative and radical user-oriented ideas and problem-solving approaches. If an approach meets with widespread user interest, an initial minimal viable product (MVP, i.e., an 80 per cent solution) will be developed and tested on the market. Following successful completion of the MVP phase, the product and new business is rapidly rolled out and integrated for scaling in the respective division.

In addition, at the beginning of the year Haniel decided to invest up to EUR 50 million in selected venture capital funds, thereby making indirect investments in start-ups. Aside from pursuing entrepreneurial objectives, the aim is to create learning opportunities relating to new digital business models. For example, Haniel has invested in five different funds in recent months, which in turn invest in a number of new companies. This expertise can for example give rise to innovation processes at the divisions; it also provides momentum as Haniel contin-ues to seek out new investments that will be successful in the long term.

Responsibility for the region and societyTogether with the KfW Foundation, the Prof. Otto Beisheim Foundation and Social Impact gGmbH, Haniel established Social Impact Lab Duisburg. The incubator for social entrepreneurs supports business founders

* Incl. the Holding Company’s financing and service companies. You can find the financial statements of the Franz Haniel & Cie. subgroup under “Creditor Relations” at www.haniel.de/en

who want to use their ideas to solve pressing social challenges; it connects them with other stakeholders and establishes them in the region. The aim of spreading social innovations and establishing social enterprises is to create positive momentum for the ongoing structural transformation in the Rhine-Ruhr region. Haniel is making the Social Impact Lab premises available at its corporate location. In addition, a specialist offering such as a mentoring programme and specialist workshops with experts from Haniel promote an exchange of ideas between the start-up teams and Haniel employees. The Holding Company’s employees benefit from the dialogue with the start-up teams, become familiar with their specific business culture and in doing so gain valuable motivation for their work at the Holding Company.

Haniel does not just provide opportunities for founders of social enterprises, but also for refugees: as a founding member of “We together – The integration initiative of the German economy” (“Wir zusammen – Integrationsin-itiativen der deutschen Wirtschaft”), Haniel was one of the first 35 companies to sign up to this initiative for the integration of refugees. The network has since grown to 96 companies. At its headquarters in Duisburg, Haniel coordinates directly with the city authorities to provide assistance when there are acute shortages in support, and assists the city in developing the organisation and warehousing logistics needed to support integration. There are also future plans to offer professional integra-tion within the Haniel Group for refugees granted rights of residence, as well as cultural, general knowledge and language training, and care for children and young peo-ple. In cooperation with the project partners – the Haniel Foundation, the start-up teams at the Social Impact Lab and the University of Duisburg-Essen – Haniel supports numerous social entrepreneurship activities in the field of integration.

Value of the portfolio increasedThe value of the investment portfolio amounted to EUR 4,985 million as at 30 June 2016. It was therefore higher than the EUR 4,887 million reported at the end of 2015. The value of the investment portfolio is calculated as the sum of the valuations of the divisions, the METRO GROUP financial investment, financial assets and other assets, less net financial liabilities at the Holding Company level. Listed divisions and the financial investment are valued

on the basis of three-month average share prices, while the remainder of the divisions are valued on the basis of market multipliers, and for the financial assets on the basis of fair values as at the reporting date.

The value of Haniel’s investment portfolio increased slightly as against the prior year to

EUR 4,985 million as at 30 June 2016.

Haniel welcomes the strategic decision of Metro’s man-agement to raise internal value potential and supports the plans for a demerger at the METRO GROUP. This opens up the possibility of new growth and development opportunities for the financial investment.

Financial assets higher than net financial liabilitiesThe sale of Celesio, the reduction of the shares in the Metro investment and the placement of the exchangeable bond linked to Metro shares in recent years put the Holding Company in a distinctly comfortable financial situation. Therefore, Haniel invests predominantly in finan-cial assets. As at 30 June 2016, taking into account current and non-current receivables from affiliated companies, there were financial assets valued at EUR 1,226 million versus net financial liabilities amounting to EUR 960 million. The exchangeable bond linked to Metro shares, which was issued in the previous year, is a key component of Haniel’s financing. Haniel has therefore secured the outstanding financing terms in the current capital market environment until 2020. In addition to financing through the capital markets, this will be supplemented by existing, currently unused credit facilities at banks. However, the major part of financing is and remains the equity made permanently available by the Haniel family.

The Holding Company thus retains a solid liquidity buffer, both for the expansion of the portfolio and for the redemption of bonds in the amount of EUR 257 million falling due in February 2017. Over the medium to long term, Haniel’s goal remains to have some EUR 1 bil-lion in net debt after acquiring new divisions.

Investment grade rating received from Scope and S&PHaniel submits itself to external rating assessments voluntarily, thus ensuring broad access to capital

20

Haniel half-year financial report 2016 / Haniel Group interim management report / Report on business situation / Haniel Group / Holding Company Franz Haniel & Cie.

markets. European rating agency Scope assessed Haniel’s creditworthiness for the first time in February 2016. The future-oriented approach used for the analysis convinced Haniel to offer the Scope rating to its inves-tors as a further opinion. Haniel received a long-term issuer rating of BBB- with a stable outlook, with Scope therefore classifying it as investment grade. The rating is a consequence of Haniel’s conservative investment strategy as a family equity company with comparatively low market value gearing (the ratio of net financial debt to the market value of the portfolio), which amounted to 17 per cent as at the 30 June 2016 reporting date and was thus within very comfortable territory. In addition, the Scope rating acknowledged Haniel’s strong liquidity position and solid cash flow profile.

In April 2016, Standard & Poor’s Services (S&P) raised its Long and Short Term Corporate Credit Rating from BB+/B (positive outlook) to BBB-/A-3 (stable outlook). As a result, S&P again classified Haniel as investment grade. The improvement is a result of Haniel’s ongoing conservative financial policy. This is distinguished by a moderate target net financial debt level of EUR 1 billion coupled with a solid long-term financing structure. The improvement in the rating also marked a positive assess-ment of Haniel’s cautious financial investment policy and its prudent approach to investments. Moody’s had already raised the rating to Ba1 with a stable outlook in the second half of 2013. This was also supported by the sound development of the total cash cover and market value gearing, key figures which are crucial to the rating. Total cash cover is calculated as the ratio of proceeds from dividends and profit transfers to payments for current costs incurred by the Holding Company, as well as interest and dividends to the Haniel family.

Earnings contribution of the Holding Company down on prior yearThe amount contributed by the Holding Company to the Group’s operating profit was down year on year in the first half of 2016. In the previous year, operating profit was boosted by higher gains from the reversal of provisions that were no longer needed.

21

Haniel half-year financial report 2016 / Haniel Group interim management report / Report on business situation / Haniel Group / Holding Company Franz Haniel & Cie.

Haniel half-year financial report 2016 / Haniel Group interim management report / Report on business situation / Wholly-owned investment BekaertDeslee

22

BekaertDeslee

BekaertDeslee strengthened through acquisitionBekaertDeslee is a growth-oriented company that seeks the long-term expansion of its global market position through both organic growth and acquisitions. The di-vision significantly strengthened its leading position on the market in the first half of 2016, primarily through the acquisition of the DesleeClama Group.

The DesleeClama Group, which is domiciled in Belgium like Bekaert Textiles, was formed in 1928 and has estab-lished a position in the development and manufacture of woven and knitted mattress textiles. In addition to certain European markets, the company has long served

Bekaert Textiles has been a part of Haniel’s portfolio of divisions since June 2015. In February 2016, the leading spe-cialist for the development and manu-facturing of woven and knitted mattress textiles acquired the DesleeClama Group, thus driving forward the long-term expansion of its global market position. The company now operates under the name BekaertDeslee. For the first time since its acquisition, the division has contributed revenue and profit to the Haniel Group over a complete half year.

>+100%

REVENUEEUR million

20 146

30 Jun. 2015* 30 Jun. 2016

REVENUEby sales region

45% Americas

40% Europe

15% Asia-Pacific

30 Jun. 2016

international markets such as Indonesia and Brazil, where Bekaert Textiles had not been directly repre-sented in the past. The combined company’s broad mar-ket coverage and high degree of customer proximity give it a strong competitive position under the new name BekaertDeslee. They will make it possible for the com-pany to further increase its responsiveness and delivery reliability for all customer groups once the integration has been completed.

The division significantly strengthened its leading position on the market in the first half of 2016

through the acquisition of the DesleeClama Group.

The two companies also complement each other in other ways: DesleeClama’s great capacity for innova-tion meets the excellent design know-how of Bekaert Textiles. In addition, integration enables the division to achieve synergies – particularly in the areas of procure-ment, production and administration.

The division has been working with the Holding Com-pany since February to advance the integration of Bekaert Textiles and DesleeClama. BekaertDeslee is focusing on completely merging the organisations on the one hand and has begun to optimise the global structure of its locations on the other. The first key corporate functions of the two companies have been merged. In addition, the division has begun to relocate DesleeClama’s production activities in the United States to Bekaert Textiles’ existing production locations in the United States and Mexico.

Cost initiatives successfully continuedIn the first half of 2016, BekaertDeslee successfully and systematically continued its work to implement both the procurement initiative and the Lean Manufacturing Initiative, both of which were launched in 2014. While the centralisation and standardisation of yarn purchasing enabled the division to reduce costs, the Lean Manufac-turing Initiative is designed to improve production pro-cesses. The division has begun to expand both initiatives to DesleeClama and has already identified new potential for efficiency enhancement.

* This figure relates exclusively to June 2015.

Haniel half-year financial report 2016 / Haniel Group interim management report / Report on business situation / Wholly-owned investment BekaertDeslee

23

Encouraging contributions to revenue and operating profitIn the first half of 2016, BekaertDeslee generated EUR 146 million in revenue, compared to EUR 20 million in the first half of 2015, during which Bekaert Textiles had only contributed to revenue for a single month. The newly acquired DesleeClama Group also made a note-worthy contribution in this area during the period from March to June 2016. In particular, the growing demand for higher-quality knitted mattress textiles had a positive influence on revenue development. These products, which also generate higher margins, accounted for more than 50 per cent of overall revenue in the first half of 2016. The remaining revenue shares were attributable primarily to woven mattress textiles, but also to a small but rising extent to products with a greater depth of value added such as ready-made mattress covers.

BekaertDeslee’s operating profit amounted to EUR 10 million in the first half of 2016, compared to EUR 2 million in the same period of the previous year. It should be noted that the operating profit was weighed down by the scheduled amortisation arising from the purchase price allocation amounting to EUR 5 million. Adjusted for this, the operating profit was EUR 15 million.

Customer focus sharpened as part of the Digital Agenda In the first half of 2016, BekaertDeslee began to de-velop its own Digital Agenda. Under the Digital Agenda,

the division systematically focuses on the needs of its target groups – from mattress manufacturers to retail-ers through to end consumers. At its core, the Digital Agenda represents the best-possible means to focus product innovation on customers to enable the com-pany to make its business model fit for the future and to further develop it over the long term.

* This figure relates exclusively to June 2015.

>+100%

OPERATING PROFITEUR million

2 10

30 Jun. 2015* 30 Jun. 2016

+59%

EMPLOYEESAverage headcount

1,466 2,337

31 Dec. 2015 30 Jun. 2016

CWS-boco

+3%

REVENUEEUR million

382 393

REVENUEby division in %

52% Washroom hygiene/mats

48% Textile services

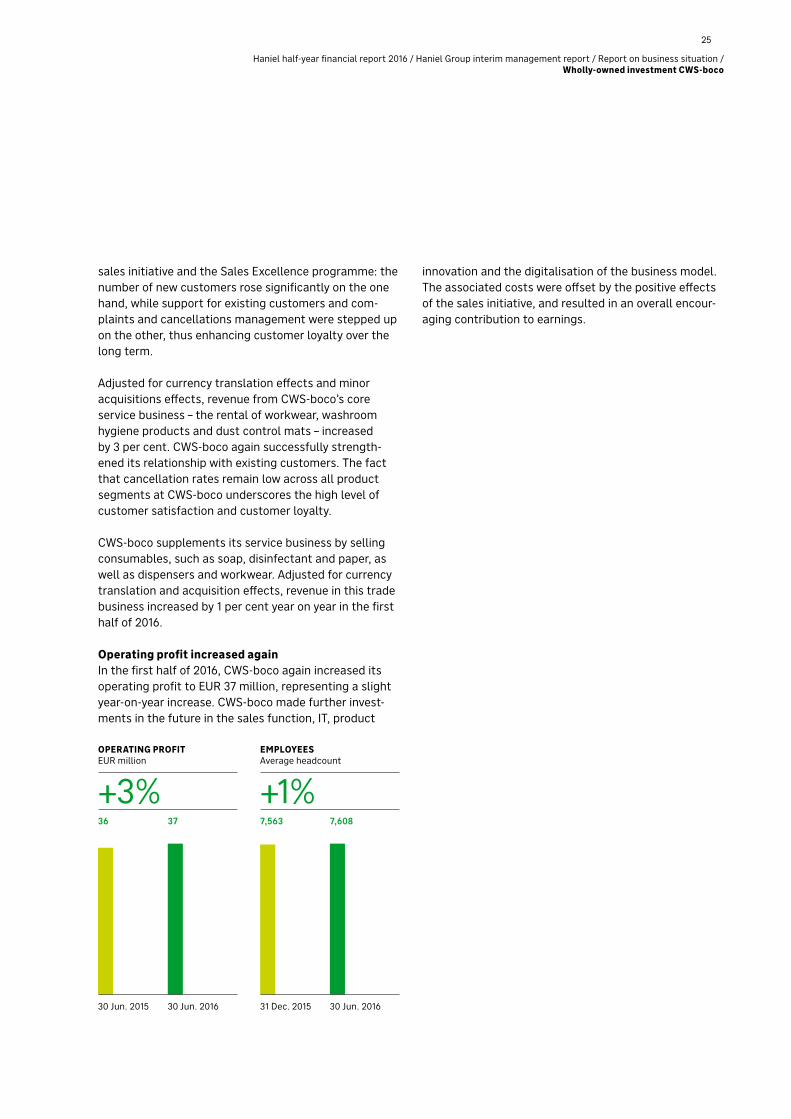

CWS-boco’s sales initiative continued to positively impact the division’s revenue, leading to an encouraging year-on-year increase. Despite additional invest-ments in product innovation and sales functions, CWS-boco’s operating profit (EUR 37 million) once again increased slightly against the prior-year period.

Sales and customer loyalty further strengthenedCWS-boco further strengthened its sales function in the first half of 2016 and again increased the number of sales employees. Furthermore, the long-term Sales Excellence programme positively impacted revenue and sales efficiency. This was attributable primarily to comprehensive training efforts that have helped to sys-tematically enhance the sales function in recent years. CWS-boco further improved its sales team’s perfor-mance by implementing other measures to systemati-cally attract new and manage relationships with existing customers.

In the first half of 2016, the division continued the project to revamp its IT systems that has been launched in the previous year. The objective of this project is to realise high, uniform standards of customer service and processes within the company with the help of a

software application that is used throughout Europe. In addition, this software application is designed to support the cross-border integration of warehouse and service processes.

Decision on new, divisional structureIn the first half of 2016, the division decided that in the current financial year it would introduce a new, divisional organisational structure. Two divisions would be estab-lished across all countries: the Washroom Care division will provide washroom hygiene products and dust control mats, while the Textile Care division’s service portfolio will cover hire and COG linens, cleanroom products and flat linen. The new structure will enable the company to pursue a market strategy with an even greater focus on customers, thereby allowing it to address its customers’ needs on a more individualised basis.

The long-term sales initiative positively impacted revenue. This was attributable primarily to comprehensive training efforts that have helped

to systematically enhance the sales organisation in recent years.

Focus on digitalisation and new products CWS-boco is working hard to digitalise its products and services. The division presented the CWS Washroom Information Service (WIS) 2.0 in the first half of the year. WIS 2.0 is a system that connects washroom dispensers and provides up-to-date information about the function-ing, fill levels and usage frequency of the dispensers. This allows CWS’ customers to operate their washrooms much more efficiently and on a more use-oriented basis. In addition, in the first half of 2016, CWS-boco further developed its business with service offerings relating to high-quality public washrooms that are available to users for a fee.

Encouraging revenue growthRevenue of CWS-boco in the first half of 2016 was EUR 393 million, 3 per cent over the figure in the prior-year period. Adjusted for these currency translation effects and minor acquisition effects, revenue increased by 3 per cent as compared to the prior-year period. This very clearly illustrates the positive effects from the

Haniel half-year financial report 2016 / Haniel Group interim management report / Report on business situation / Wholly-owned investment CWS-boco

24

30 Jun. 2015 30 Jun. 2016 30 Jun. 2016

sales initiative and the Sales Excellence programme: the number of new customers rose significantly on the one hand, while support for existing customers and com-plaints and cancellations management were stepped up on the other, thus enhancing customer loyalty over the long term.

Adjusted for currency translation effects and minor acquisitions effects, revenue from CWS-boco’s core service business – the rental of workwear, washroom hygiene products and dust control mats – increased by 3 per cent. CWS-boco again successfully strength-ened its relationship with existing customers. The fact that cancellation rates remain low across all product segments at CWS-boco underscores the high level of customer satisfaction and customer loyalty.

CWS-boco supplements its service business by selling consumables, such as soap, disinfectant and paper, as well as dispensers and workwear. Adjusted for currency translation and acquisition effects, revenue in this trade business increased by 1 per cent year on year in the first half of 2016.

Operating profit increased againIn the first half of 2016, CWS-boco again increased its operating profit to EUR 37 million, representing a slight year-on-year increase. CWS-boco made further invest-ments in the future in the sales function, IT, product

innovation and the digitalisation of the business model. The associated costs were offset by the positive effects of the sales initiative, and resulted in an overall encour-aging contribution to earnings.

Haniel half-year financial report 2016 / Haniel Group interim management report / Report on business situation / Wholly-owned investment CWS-boco

25

+3%

OPERATING PROFITEUR million

36 37

+1%

EMPLOYEESAverage headcount

7,563 7,608

30 Jun. 2015 30 Jun. 2016 31 Dec. 2015 30 Jun. 2016

ELG

In the first half of 2016, ELG was con-fronted with an ongoing difficult mar-ket environment and thus experienced a significant overall decrease in its revenue and operating profit. This was attributable primarily to considerably lower commodity prices and stainless steel scrap output tonnage. Increases in the tonnage for superalloys toll process-ing had a stabilising effect.

Ongoing difficult market environment in the stainless steel scrap businessGlobal stainless steel production in the first half of 2016 was slightly higher than in the prior-year period. How-ever, there were significant regional differences. While the production of stainless steel in ELG’s key markets – the US and Europe – decreased in the first half of 2016, production increased slightly in China. Suppliers such as ELG, however, were not able to fully satisfy manufac-turers’ global demand for stainless steel scrap. This is because the sustained low commodity prices meant that less scrap material was available on the procurement market than had been in the prior-year period. Overall, this situation had a negative impact on ELG’s stainless steel scrap output tonnage, which fell by 15 per cent year on year.

In addition to the decline in quantity, the stainless steel scrap business also had to cope with a substan-tial deterioration of commodity prices of the most important stainless steel components. In the first half of 2016, the price of nickel averaged USD 8,600 per tonne, before increasing briefly to just under USD 10,000 per tonne in the days leading up to the end of first half of the year. In the first half of 2015, the aver-age price per tonne had been USD 13,700. The price of commodities not subject to hedging on the capital market such as iron and chrome were also significantly lower year on year.

Robust demand in the superalloys businessIn the first half of 2016, Utica Alloys, ELG’s division spe-cialising in superalloys, benefited from robust demand in the toll processing programme. While the deterioration in the price of titanium – also a non-hedgeable commod-ity – exerted pressure on the trade business, process-ing agreements strengthened Utica Alloys’ business. The toll processing business is largely not affected by commodity prices and is thus a stabilising component in times of falling or low trading prices. Nevertheless, the output tonnage of superalloys at ELG decreased by a total of 3 per cent year on year due to demand-related declines in shipping tonnage.

In response to shifting demand, Utica Alloys expanded its toll process business with superalloys

and secured new orders.

Operating profit down significantly year on year – but trend is positiveRevenue declined by 34 per cent to EUR 707 million due to the sharp decline in ELG’s output tonnage as com-pared to the first half of 2015 as well as considerably lower prices for nickel and other commodities relevant for ELG. The improved gross margin and a significantly reduced cost base did not completely offset the price and tonnage effects. Operating profit for the first six months of 2016 (EUR 2 million) was significantly below the previous year’s figure (EUR 11 million). However, the operating profit for the first half of 2016 is significantly higher than the operating profit in the second half of 2015. Furthermore, negative measurement effects from

-34%1,074 707

REVENUEby sales region in %

52% Europe

32% Americas

16% Asia

Haniel half-year financial report 2016 / Haniel Group interim management report / Report on business situation / Wholly-owned investment ELG

26

REVENUEEUR million

30 Jun. 2015 30 Jun. 2016 30 Jun. 2016

hedging transactions – due to the jump in the price of nickel as at 30 June 2016 – weighed down the result in the first half of 2016.

Future-facing business segments and projects driven forwardIn reaction to the difficult market environment, the ELG division implemented a strict and systematic cost man-agement programme.

The Carbon Fibre business segment is currently suffering from the tense market situation in its primary customer segment, the oil and gas industry. Carbon Fibre contin-ues to focus on the core issues of customer-oriented product development and on sales, with the objective of further developing the business.

ELG also made advances with respect to digitalisation. The company is focussing on innovating its busi-ness model. A number of projects have already been launched, such as the new “MyELG” app, and others are currently in the test or pilot phase.

Haniel half-year financial report 2016 / Haniel Group interim management report / Report on business situation / Wholly-owned investment ELG

27

-82%11 2

-7%1,282 1,188

30 Jun. 2015 30 Jun. 2016 31 Dec. 2015 30 Jun. 2016

OPERATING PROFITEUR million

EMPLOYEESAverage headcount

+25%

OPERATING PROFITEUR million

65 81

+3%

EMPLOYEESAverage headcount

2,403 2,485

+9%506 554

REVENUEby division

52% TAKKT EUROPE

48% TAKKT AMERICA

TAKKT

TAKKT built on the previous year’s positive development in the first half of 2016, with a further increase in both revenue and operating profit. The di-vision benefited in particular from the continuing positive business climate in the US. TAKKT continued to make progress in its further development into an integrated multi-channel company. Currently, the division is also working systematically on developing its Digital Agenda to further harness the opportu-nities offered by digitalisation.

TAKKT continues encouraging growth courseTAKKT’s revenue increased in the first half of 2016 by 9 per cent to EUR 554 million. Post-Up Stand and BiGDUG, which were acquired in the previous year, also contributed to the increase in revenue. With regard to organic revenue growth (i.e., adjusted for these acquisitions and the activities of the Plant Equipment Group disposed of in the prior-year period, as well as negative currency translation effects), both TAKKT AMERICA and TAKKT EUROPE con-tributed to the 8 per cent increase in revenue.

The organic revenue of TAKKT AMERICA grew by 10 per cent. Both the Specialities Group and the Office Equip-

ment Group again contributed to the very healthy growth. The US portfolio companies are benefiting from the continuing favourable market environment in the US.

TAKKT EUROPE recorded organic revenue growth of 6 per cent. The increase in revenue at the Business Equipment Group was due in particular to strong growth in Switzerland and Scandinavia, as well as eastern and southern Europe. The German market also recorded growth. In the Packaging Solutions Group, Ratioform acquired the customers and inventories of the former franchise partner in Austria at the beginning of the year. The business recorded slight growth in the first half of the year.

TAKKT EUROPE has resolved to terminate the activities in the Chinese market allocated to the business due to the poor growth outlook.

Significant improvement in operating profit TAKKT increased its operating profit from EUR 65 million in the first half of 2015 to EUR 81 million. This was due to strong organic growth and the earnings contribu-tions made by the acquisitions. Positive one-offs also had an effect in both half-year periods. The net disposal gain from the disposal of the Plant Equipment Group in the year 2015 was partly offset in the reporting period by even higher gains on the reduction of outstanding

Haniel half-year financial report 2016 / Haniel Group interim management report / Report on business situation / Majority investment TAKKT

28

REVENUEEUR million

30 Jun. 2015 30 Jun. 2016 30 Jun. 2016

30 Jun. 2015 30 Jun. 2016 31 Dec. 2015 30 Jun. 2016

Haniel half-year financial report 2016 / Haniel Group interim management report / Report on business situation / Majority investment TAKKT

29

variable purchase price liabilities for the Post-Up Stand and BiGDUG acquisitions. In the case of both companies, TAKKT no longer believes that the ambitious growth and earnings figures on which the measurement of the varia-ble liabilities had been based at first-time consolidation will be achieved.

TAKKT records strong organic revenue growth of 8 per cent and increased profitability.

digital@TAKKT builds on the DYNAMIC initiativeTAKKT made further progress in its DYNAMIC growth and modernisation initiative in the first half of 2016. The company is integrating various sales channels in order to address customers as needed: through the catalogue, online, by telephone and via employees in the external sales force. The share of order intake accounted for by e-commerce currently stands at 38 per cent, versus 35 per cent in the prior-year period.

TAKKT is focusing more closely on further digitalising the business and in doing so is emphasising the major strategic importance of digitalisation as a growth oppor-tunity for the company. The company is leveraging the digital@TAKKT initiative to further harness the current and future opportunities offered by digitalisation. This includes the development of a Digital Agenda that includes specific measures to be implemented locally for the individual businesses. This Digital Agenda will form the basis for the company’s further growth over the course of the digital transformation that is already underway.

Haniel half-year financial report 2016 / Haniel Group interim management report / Report on business situation / Financial investment METRO GROUP

30

METRO GROUP

In the first half of 2016, the METRO GROUP made further progress in its strategic realignment and is planning to split the group into two independent companies. Revenue saw slight organic growth year on year, and operating profit increased due to lower one-off factors. As a result, the Haniel Group’s investment result from the METRO GROUP was also above the level re-corded in the prior-year period.

METRO GROUP plans demerger In March 2016, the METRO GROUP announced plans to split the group into two independent companies with a specific focus on their respective market segments: a wholesale and food specialist, and a company focusing on consumer electronics and services. Both would be separate German stock corporations with independ-ent corporate profiles and their own management and supervisory boards, and would be individually listed on the stock exchange. Haniel supports these plans. The planned demerger will yield new growth and develop-ment opportunities for the METRO GROUP.

Implementation of strategic initiatives stepped upThe METRO GROUP made significant progress with its strategic initiatives in the first half of 2016. Delivery revenue at METRO Cash & Carry increased by more than 15 per cent; this was also supported by Classic Fine Foods (CFF), which was acquired in 2015. The acquisition of leading premium food supplier Rungis Express marks a milestone in METRO Cash & Carry’s transition towards becoming Germany’s leading multi-channel food service provider. Revenue generated online by both the Media-markt and Saturn brands at Media-Saturn increased by an encouraging 35 per cent.

To ensure that it identifies new opportunities arising from digitalisation in good time, the METRO GROUP expanded its commitment to the start-up segment and through METRO Accelerator powered by Techstars, at its Berlin location will continue to promote digital and technological innovations that could be groundbreaking for the gastronomy sector in the future. Eleven interna-

tional start-ups took part in the first successful edition. Media-Saturn has also extended its commitment to start-ups with Spacelab, the Media Saturn Accelerator, at its Munich location.

The planned demerger into two companies will yield new growth and development opportunities

for the METRO GROUP.

In addition, in May 2016 METRO GROUP invested in Berlin- based start-up Orderbird, the leading iPad payment solution for the gastronomy sector in German-speaking countries, underscoring its commitment to digitalisation in the gastronomy sector.

Slight organic revenue growthThe METRO GROUP’s revenue amounted to EUR 27,163 million in the first half of 2016, down 2 per cent on the prior year. Organic revenue growth (adjusted for cur-rency translation and portfolio effects; like-for-like) was slightly up on the figure for the first half of 2015.

Revenue at METRO Cash & Carry fell by 4 per cent. This was primarily due to the negative currency translation effects in the prior year, in particular on the back of the exchange rate trend of the Russian rouble and the effects of selling the activities in Greece and Vietnam. METRO Cash & Carry switched over to a new customer segment-related reporting structure at the beginning of 2016. The countries in the Horeca segment focus on hotels, restaurants and caterers. The countries in the Trader segment concentrate primarily on trade cus-tomers such as kiosks, bakeries, market stallholders or butchers, while the countries in the Multispecialists segment serve a wide range of customers. METRO Cash & Carry generated slight organic revenue growth in the first half of 2016, with positive contributions from the Trader and Horeca segments in particular.

Media-Saturn increased revenue by 2 per cent – despite negative currency translation effects in particular as a result of the development of the rouble. The primary causes were firstly organic growth in Germany and eastern Europe, and secondly positive effects from the acquisition of customer service and repair provider

Haniel half-year financial report 2016 / Haniel Group interim management report / Report on business situation / Financial investment METRO GROUP

31

RTS. In Germany, the business benefited in particular from a new customer loyalty programme and the UEFA European Championship. This enabled the company to further expand its market share.

The Real sales division modernised further locations in the first half of 2016 and improved its image with customers. In addition, it increased its competitiveness thanks to an agreement reached in collective wage negotiations. Revenue decreased organically by 1 per cent. Reported revenue declined by 4 per cent due to the lower number of locations.

By contrast, the company made progress in its online revenue. In addition, Real continued to invest in digital expertise, for example through the acquisition of the Hitmeister online shopping portal.

Increase in operating profit due to lower one-offsAfter having generated an operating profit of EUR -382 million during the same period of the previous year, the METRO GROUP’s operating result in the first half of 2016 amounted to EUR -70 million. This significant growth was due to the higher one-off factors in the prior-year period, when operating profit was adversely affected primarily by impairment losses on goodwill at Real Germany. By contrast, lower one-off factors were recognised in the reporting period, in particular for restructuring measures. Adjusted for these one-off fac-

tors, operating profit amounted to EUR 164 million in the first half of 2016, down on the adjusted operating profit of EUR 191 million recorded in the prior-year period. This reduction was chiefly attributable to negative currency translation effects.

Higher earnings contribution for Haniel The higher operating profit had a proportionate impact on the investment result the Haniel Group derives from the METRO GROUP. In addition, the METRO GROUP’s net financial income improved. By contrast, the METRO GROUP’s less favourable tax result as against the first half of 2015 had an adverse effect. Haniel’s result from the Metro investment increased overall from EUR -60 million in the same period of the previous year to EUR -30 million in the first half of 2016. As regards the negative investment result of the first half of the year, it must also be taken into consideration that the significantly positive contribution to earnings from the Metro investment regu-larly does not occur until the Christmas season during the fourth quarter of Haniel’s financial year.

+50%

HANIEL INVESTMENT RESULTEUR million

-60 -30

30 Jun. 2015 30 Jun. 2016

Haniel half-year financial report 2016 / Haniel Group interim management report / Report on business situation / Report on expected developments

32

Report on expected developments

Haniel expects to be able to generate a significant year-on-year increase in operating profit in financial year 2016. Despite the positive performance at TAKKT and CWS-boco, Haniel is now expecting that organic revenue growth will fall short of the forecast. This is due to the persistently difficult market environment in the cyclical ELG division. How-ever, Haniel continues to expect positive earnings development in all divisions.

Increasing uncertainties in the macroeconomic environment The referendum in the United Kingdom, which resulted in a vote to leave the European Union in the foreseeable future, added a further element of uncertainty in fore-casting future economic trends. At the same time, both businesses and consumers are unnerved by geopolitical tensions and their effects.

The International Monetary Fund (IMF) is currently forecasting global gross domestic product (GDP) growth of 3.1 per cent for full-year 2016, with a trend towards decreasing momentum. Growth of 2.2 per cent is now expected for the US, one of the key drivers of the global economy. The IMF’s overall outlook for the euro zone has been reduced to 1.6 per cent due to the Brexit vote. Ger-many, Spain and France are expected to provide the key momentum. For Germany, the IMF forecasts economic growth of 1.6 per cent. Ultimately, it was the United Kingdom that faced a reduction in expectations. Despite initially stabilising, the persistently low commodity prices will continue to adversely affect the less-devel-oped economies, with the IMF forecasting negative growth for both Russia (-1.2 per cent) and Brazil (-3.3 per cent). In contrast to previous year’s economic cooling, growth in China could accelerate to 6.6 per cent on the back of comprehensive economic stimulus packages.

Overall, there are implications for the Haniel Group’s business development based on these assumptions, primarily due to the reduced economic expectations for the US and Europe, the forecast growth in China and the potential repercussions of the Brexit vote.

Persistently difficult conditions in ELG’s market environment The development in the stainless steel market segment is of central significance for the ELG division. For 2016, experts assume that, on average, nickel prices will de-

crease significantly year on year. As a result, the market conditions in the stainless steel segment – particularly in the procurement market for stainless steel scrap – will remain difficult. The commodity prices relevant to ELG Utica Alloys are also expected to remain well below the previous year’s average prices in 2016.

Since all divisions are active internationally, the results of the Haniel Group depend on the development of various exchange rates, particularly the US dollar, the British pound and the Swiss franc. In addition, the result from the Metro investment is impacted significantly by the development of the Russian rouble. Deviations from the assumed economic development and the future ex-change rates compared to the planning assumptions may significantly change the forecasts for revenue and profit.

Operating profit up in all divisionsThe macroeconomic situation influences the divisions to varying degrees. Currently, Haniel’s Management Board continues to expect comparative growth in all divisions, on condition that uncertainties outlined above do not worsen the economic outlook.

2016 will be the first full financial year in which BekaertDeslee is included in the Haniel Group, and the division is now expecting revenue of well over EUR 300 million. The significant improvement in the forecast is due to the acquisition of the DesleeClama Group, the successful integration of which will be continued quickly and systematically, and its contribution to revenue in 2016. The division continues to anticipate operating profit in the order of EUR 30 million. It should be taken into account that this is weighed down by the scheduled amortisation arising from the purchase price allocations amounting to EUR 10 million.

CWS-boco continues to expect revenue in the lower single-digit percentage range for financial year 2016,

Haniel half-year financial report 2016 / Haniel Group interim management report / Report on business situation / Report on expected developments

33

adjusted for business combinations and disposals as well as currency translation effects. In order to achieve this, the division is systematically pursuing its sales initiative. Besides, CWS-boco aims to further maintain contract cancellation rates at the present low level. The division also continues to expect a slight increase in operating profit based on these assumptions. The inten-tion is to offset the costs resulting from the intensified sales initiative and other investments in the future with earnings contributions from the increase in revenue.