Half Year 2016 Results Presentation WIP mostly relates to work in progress on B737 passenger to...

24

Airwork Holdings Limited February 2016 Half Year 2016 Results Presentation

-

Upload

truongnguyet -

Category

Documents

-

view

212 -

download

0

Transcript of Half Year 2016 Results Presentation WIP mostly relates to work in progress on B737 passenger to...

Airwork Holdings Limited

February 2016

Half Year 2016 Results Presentation

IMPORTANT NOTICE

This presentation contains not only a review of operations, but also some forward looking statements

about Airwork Holdings Limited (Airwork) and the environment in which the company operates. These

forward looking statements are based on current expectations, and involve assumptions, risks and

uncertainties. Airwork’s actual results could be affected by a number of factors and accordingly could

differ materially. There can be no assurance that any result contemplated in any forward looking

statement will be realised and Airwork gives no warranty or representation as to future performance.

Media releases, management commentary, Airwork’s 2013 investment statement and other information

is available in respect of the company and these contain additional information about matters which

could cause Airwork’s performance to differ from any forward looking statements in this presentation.

Please read this presentation in the wider context of material previously published by Airwork.

The information in this presentation is in a summary form, and accordingly is not necessarily complete.

No representation or warranty is made as to the accuracy or completeness of the information contained.

A number of non-GAAP financial measures are used in this presentation due to the fact they are widely

accepted financial indicators used by investors and analysts to analyse and compare companies. You

should not consider any of these in isolation from, or as a substitute for, the information provided in the

consolidated financial statements.

All amounts are in New Zealand dollars unless otherwise stated.

2

3

CONTENTS

• Executive Summary

• Interim HY 2016 Result

o Highlights

o Financial Summary

• Interim HY 2016 Divisional Review

o Helicopter Review

o Fixed Wing Review

o Operating Cash Flows

o Capex

o Net Debt

• Strategy and Outlook

• Conclusion

Appendices

EXECUTIVE SUMMARY

4

• Airwork has delivered an improved first half result for the 2016 financial year

o Significant EBIT growth of 76% in the Fixed Wing division driven by the successful

commencement of B737-400 dry leasing contracts announced in FY15

o Helicopter division EBIT growth of 22% despite challenging market conditions in some sectors,

notably Oil & Gas

• The result highlights the benefits of Airwork’s diversified businesses, global footprint and revenue

streams

• The Directors have approved a fully imputed Interim Dividend of 9.0 cents per share

• FY16 NPAT guidance in excess of $21m

• Outlook: continue expansion of global footprint to identify and secure further growth opportunities

• The Directors would like to acknowledge the significant efforts and dedication of the Airwork team

located around the world who have delivered this result, whilst managing a significant amount of

change

INTERIM HY 2016 RESULT – FINANCIAL SUMMARY

5

1. Return on Capital Employed: EBIT / Average funds employed (shareholders’ funds plus net debt)

2. Return on Shareholders’ Funds: NPAT / Average shareholders’ funds

HY16

$’000s

FY15

$’000s

HY15

$’000sChange

Total Revenue 83,365 70,260 18.7%

EBITDA 33,897 22,439 51.1%

EBIT 18,436 11,832 55.8%

NPAT 11,607 7,885 47.2%

Return on Capital Employed 1 14.6% 14.0% 15.2% (0.6 ppt)

Return on Capital Employed (excl. Capital WIP) 17.7% 16.5% 15.9% 1.8 ppt

Return on Shareholders' Funds 2 22.3% 16.5% 17.0% 5.3 ppt

Earnings per share - basic (cps) 23.1 15.7 47.2%

Dividends (cps) 9.0 8.0 1.0

OPERATING REVENUE

6

Revenue growth reflects aircraft leasing additions across both Fixed Wing and

Helicopter businesses

7

EBIT: UNDERLYING PERFORMANCE

Underlying EBIT shows continued growth

Note: Underlying EBIT is a non GAAP measure. It is determined based on reported operating profit after depreciation, amortisation and

impairment expenses adjusted for: IPO costs in HY14.

EBIT: DIVISIONAL REVIEW

8

• Increase in Fixed Wing earnings from expansion of B737-400 dry leases in Europe

• Profitable Helicopter growth due to high yielding short term contracts offsetting reduced

flying in Oil & Gas sector; fleet redeployed to target specific opportunities

Note: Underlying EBIT is a non GAAP measure. It is determined based on reported operating profit after

depreciation, amortisation and impairment expenses adjusted for: IPO costs in HY14 (Corporate)

HELICOPTER REVIEW

9

HY16

$’000s

FY15

$’000s

HY15

$’000s

HY14

$’000s

Revenue - Engineering 24,486 26,536 21,010

Revenue - Leasing 19,556 15,656 10,292

Revenue - Total 44,042 42,192 31,302

EBITDA 16,081 13,854 9,568

EBIT 12,122 9,902 6,641

EBITDA Margin 36.5% 33.8% 32.8% 30.6%

Return on invested capital 1 23.7% 22.8% 23.3% 17.5%

Return on invested capital (excluding THL) n/a 24.9% 25.6% 19.5%

Percentage of revenue generated from new customers

• Engineering 23% 3% 2% 20%

• Leasing 2% 4% 4% 3%

Total helicopter fleet (owned and operated) 42 41 37 28

• 22% growth in Helicopter division EBIT despite a difficult market, particularly in Oil & Gas with significant

reduction in PNG flying hours compared to prior period

• Leasing revenue increased by 25% included significant short-term non-recurring leases utilising existing

assets

• Decline in Engineering external revenue reflects change of mix with increased internal support to enable

Leasing growth and slowdown from existing customers (particularly helicopter sales to the Oil & Gas

industry) netted off with significant new customer wins and workshop revenue growth

1. Return on Invested Capital: EBIT / Average Capital Employed

• Further investment in emerging Oil & Gas projects in South America

• Two helicopters redeployed during the period from PNG following slow-down in projects –

one further helicopter removed to date in H2

• Redeployment of 5 tourism aircraft to new NZ based tourism and charter operators

HELICOPTER REVIEW

10

Continued Leasing Fleet Growth and redeployment of assets

HELICOPTER REVIEW

11

• New customers signed off the back of ongoing certification expansion:

o FY14 – Europe, Africa, Canada, Asia

o FY15 – South America, South Africa

o FY16 – USA certification expected in March

• New Zealand market share expansion across leasing and maintenance activities

• Reduced revenue from European Support Contract as expected, in line with customer fleet

reduction schedule

• No decision received regarding outcome of The Helicopter Line legal action

• Capacity expansion of Ardmore Engineering facility to meet demand

o Stage 1 – new hangar; completed June 2015

o Stage 2 – overhaul capacity increase; completion delayed to April 2016

o FAA approval – expected March 2016

Continued expansion

HELICOPTER REVIEW

12

Leasing revenue by industry Engineering revenue by industry

• 11% reduction in Oil and Gas revenue share

reflects softer market conditions in that industry

• Challenges faced by Oil and Gas industry affected

the business, but were made up by increases in

other industry sectors

HY16

HY15

HY16

HY15

• 31% reduction in Oil and Gas revenue share

reflects fewer helicopter sales into industry

• Emergency and government services (including

defence) increase

• Excludes throughput increase supporting Leasing

fleet

FIXED WING REVIEW

13

• Expansion of dry leasing fleet in Europe, plus impact of leases commenced in the prior year; all

dry lease aircraft delivered

• Increased activity in New Zealand and Australia with delivery of two B737-400 freighters; four

further aircraft to be delivered in H2

• Increased Fixed Wing MRO activity with expansion of customer base

• Disposal of two surplus non-Boeing aircraft and customer disposal of one operated aircraft

HY16

$’000s

FY15

$’000s

HY15

$’000s

HY14

$’000s

Total revenue 39,279 28,007 34,475

EBITDA 21,097 12,144 14,531

EBIT 9,760 5,548 6,922

EBITDA Margin 53.7% 43.4% 42.1%

Return on invested capital 1 12.8% 11.3% 14.1% 15.7%

Return on invested capital (excl Capital WIP) 2 17.9% 15.6% 15.5% 17.3%

Fleet: number of aircraft at end of period (owned and operated)

• Boeing 737 - 400/300 18 17 9 9

• Other 7 10 10 11

• Total 25 27 19 20

Percentage change of flying hours from prior period 3 7% (5%) 4% 12%

1. Return on Invested Capital: EBIT / Average Capital Employed

2. Capital WIP mostly relates to work in progress on B737 passenger to cargo conversions

3. The change in flying hours are shown for owned and leased aircraft, excluding fixed rate leases where flying hours do not impact revenue

FIXED WING REVIEW

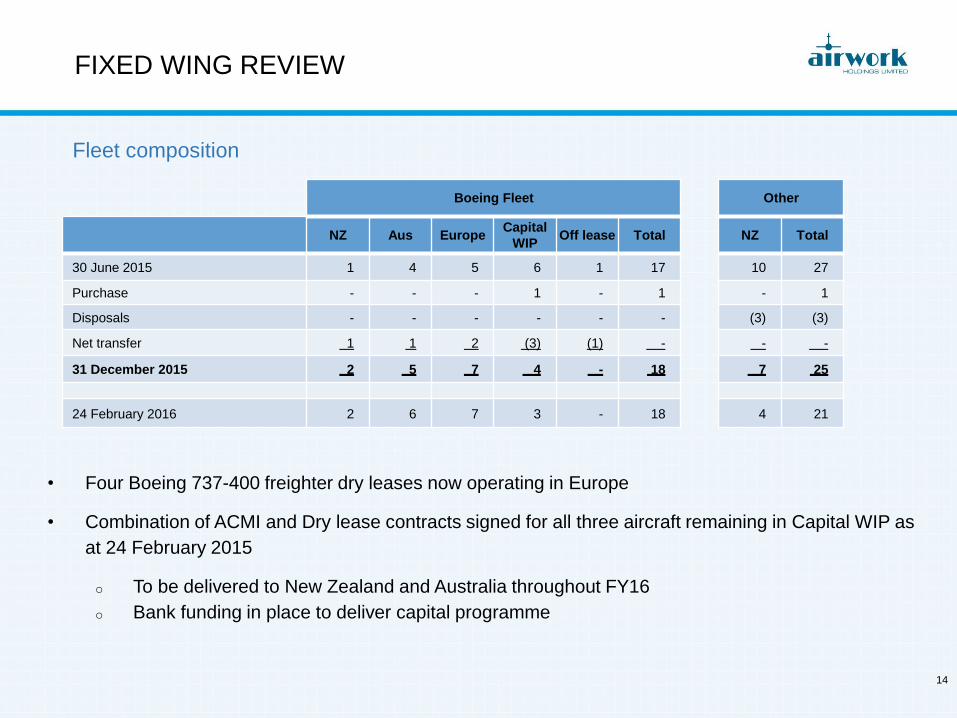

14

NZ Aus EuropeCapital

WIPOff lease Total

30 June 2015 1 4 5 6 1 17

Purchase - - - 1 - 1

Disposals - - - - - -

Net transfer 1 1 2 (3) (1) -

31 December 2015 2 5 7 4 - 18

24 February 2016 2 6 7 3 - 18

• Four Boeing 737-400 freighter dry leases now operating in Europe

• Combination of ACMI and Dry lease contracts signed for all three aircraft remaining in Capital WIP as

at 24 February 2015

o To be delivered to New Zealand and Australia throughout FY16

o Bank funding in place to deliver capital programme

Fleet composition

NZ Total

10 27

- 1

(3) (3)

- -

7 25

4 21

Boeing Fleet Other

FIXED WING REVIEW

15

• Continued exceptional operational performance: 97% On Time Performance

• Continued margin improvement through Dry Leasing and expansion of MRO activity in New Zealand

• Performance aided by:

o one B737-400 passenger aircraft positioned with European customer for short-term green time

lease, pending freighter conversion;

o addition of 5th aircraft on short-term charter work in Australia

• First B737-400 delivered for the Freightways Joint Venture and in service with Freightways and NZ Post

from December 2015; two more deliveries scheduled in H2

• Two Boeing 737-300 freighters to be redeployed once ACMI fleet makeup is confirmed

• Ceased operating NZ Post Metroliner fleet in January 2016 (3 aircraft) as part of transition to new NZ

airfreight network

OPERATING CASH FLOW ANALYSIS

HY16

$’000s

HY15

$’000s

HY14

$’000s

Reported operating cash flows 19,077 14,604 14,641

Adjust for:

• IPO costs - - 1,254

• Maintenance capex (4,884) (5,555) (6,198)

Underlying operating cash flows 14,193 9,049 9,697

• Scheduled debt amortisation (4,195) (2,188) (2,678)

Free cash flow 9,998 6,861 7,019

Strong underlying Cash Flows

• Cash flows remain strong but are affected by working capital increase of $8.7 million from 30 June

2015, including:

o Trade debtor increase of $3.7 million, reflecting revenue growth, advance billings, and

customer credit extension

o Inventory and WIP increase of $5.6 million, due to increased Helicopter Leasing and

Engineering activity and phasing of purchases for upcoming sales

o Net increase in payables and other liabilities of $0.7 million, relating to customer deposits and

prepayments for new B737-400 dry leases and supplier deferred payment arrangements16

CAPEX

17

• Total capex during HY16 ($57.0m), funded through operating cash flows and debt

• Maintenance capex HY16: Fixed Wing ($2.4m) and Helicopters ($2.4m)

• Growth capex:

o Helicopter ($3.4m): fleet growth; Ardmore facility expansion; certification development

o Fixed Wing ($48.5m): B737-400 freighter conversion programme; MRO system

implementation

o Group ($0.2m): Finance and IT systems upgrades

HY16

$’000s

HY15

$’000s

HY14

$’000s

Property, plant & equipment capex 56,687 30,383 19,247

Intangible asset capex 286 307 600

Group capital expenditure 56,973 30,690 19,847

Comprising:

Maintenance capex 4,884 5,555 6,198

Growth capex 1 52,089 25,135 13,649

Group capital expenditure 56,973 30,690 19,847

1. The Group defines growth capex as investments in new assets or product development to increase the

Group’s earning capacity, all other capex is defined as maintenance capex.

• Net debt as at 31 December 2015 was $159.7m, an increase of $41.6m since 30 June 2015 ($118.1m):

o Includes $0.5m reduction due to FX with corresponding reduction in B737 aircraft values

o Balance due to continued high Growth Capex, especially with respect to the expansion of the

Fixed Wing dry leasing fleet

• Future earnings from fleet expansion will reduce initial increase in gearing required to fund aircraft

investment

• Forecast Net Debt at 30 June 2016, following completion of B737-400 freighter conversion programme

and other capex initiatives, including Ardmore facility expansion: approx. $175m

31 Dec 15 30 Jun 15 31 Dec 14

Equity ratio 1 33.7% 37.1% 43.6%

Debt ratio 2 66.3% 62.9% 56.4%

1. Equity ratio is: Net Assets / (Total Assets less Cash)

2. Debt ratio is: (Total liabilities less Cash) / (Total Assets less Cash)

18

NET DEBT

STRATEGY AND OUTLOOK

19

H1 result ahead of expectation, which sets platform for solid full year result

Forecast FY16 NPAT in excess of $21m

Fixed Wing: completion of B737-400 freighter conversion programme

• Deliver remaining B737-400 aircraft to wet lease customers

• Assess further fleet expansion opportunities

• Redeployment of B737-300 freighter aircraft

• Continue to deliver World Class on-time performance and focus on core customer requirements

• Target continued growth opportunities in MRO business

Helicopters: continued focus on organic growth of helicopter business in a challenging market

• Engineering / maintenance capacity expansion through facility development

• Further extend certifications (FAA certification expected in year)

• Continue to partner with OEMs

• Continue to focus on markets outside of Oil and Gas (e.g. firefighting, utility, Government services)

• Progressive fleet expansion in NZ and offshore, including new and emerging markets

• Challenges faced by Oil and Gas industry may lead to a decline in growth rate in helicopter

division, however there remains potential for greater leasing opportunities through providing cost

effective solutions

Pursue new opportunities that complement existing businesses

Appendix 1: PERFORMANCE BY DIVISION

20

HY16

$’000s

HY15

$’000s

HY16

Growth

HY14

$’000s

HY15

Growth

Revenue:

Helicopters 44,042 42,192 4% 31,302 35%

Fixed Wing 39,279 28,007 40% 34,459 (19%)

Corporate 44 61 - 5 -

Total Revenue 83,365 70,260 19% 65,766 7%

EBITDA:

Helicopters 16,081 13,854 16% 9,568 45%

Fixed Wing 21,097 12,144 74% 14,531 (16%)

Corporate & Other 1 (3,281) (3,559) (8%) (3,680) (3%)

Total EBITDA 33,897 22,439 51% 20,419 10%

EBIT:

Helicopters 12,122 9,902 22% 6,641 49%

Fixed Wing 9,760 5,548 76% 6,922 (20%)

Corporate & Other 1 (3,446) (3,618) (5%) (3,707) (2%)

Total EBIT 18,436 11,832 56% 9,856 20%

1. Corporate and Other includes head office costs, group shared costs and the elimination of the results

of inter-segment trading.

Appendix 2: HELICOPTER FLEET

21

HY16 HY15 HY14

Leasing fleet

Number of helicopters at end of period:

• Owned 37 32 24

• Leased 2 3 2

Total leasing fleet 39 35 26

• Operated (not owned or leased) 3 2 2

Total helicopter fleet 42 37 28

Average number of helicopters during the period 42.2 35.7 30.2

Average revenue per helicopter equivalent ($'000s) 464 439 341

Fleet flying hours - Percentage increase / (decrease) over prior year

• Fleet Total 16% 25% (26%)

• Excluding Allway and THL 16% 40% (5%)

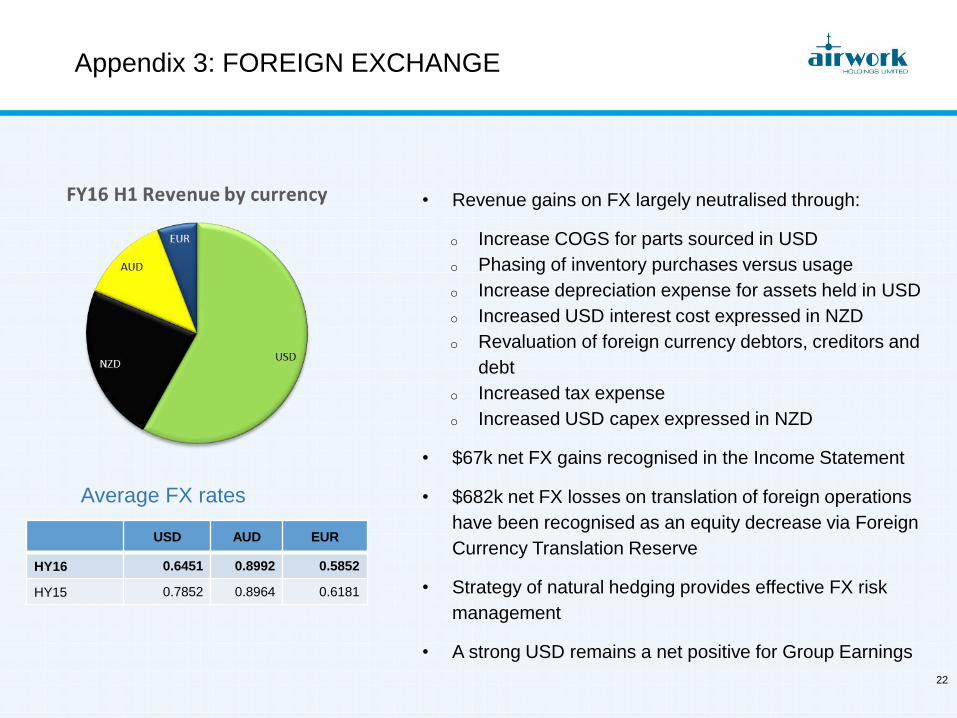

Appendix 3: FOREIGN EXCHANGE

22

USD AUD EUR

HY16 0.6451 0.8992 0.5852

HY15 0.7852 0.8964 0.6181

Average FX rates

• Revenue gains on FX largely neutralised through:

o Increase COGS for parts sourced in USD

o Phasing of inventory purchases versus usage

o Increase depreciation expense for assets held in USD

o Increased USD interest cost expressed in NZD

o Revaluation of foreign currency debtors, creditors and

debt

o Increased tax expense

o Increased USD capex expressed in NZD

• $67k net FX gains recognised in the Income Statement

• $682k net FX losses on translation of foreign operations

have been recognised as an equity decrease via Foreign

Currency Translation Reserve

• Strategy of natural hedging provides effective FX risk

management

• A strong USD remains a net positive for Group Earnings

23

Integrated Business with Highly Regulated Environment

Established Business – Long Term Contracts

Helicopter Engineering – Niche Market with High Barriers to Entry

Growth Track Record and Significant Opportunities

Experienced Board and Management

Highly Diversified – Operations, Industries and Geographies

Strong Cash Flow Business

Appendix 4: KEY ATTRIBUTES OF THE BUSINESS

Canadian Overhaul

Approval

BK117 Engine

Upgrade Program

Approval in NZ

BK117 Engine

Upgrade Program

European approval

European

maintenance approval

Capability now covers:

Europe, Canada,

South America, rest of

Asia and middle-East

BK117 Engine

Upgrade Program

USA approval

Canadian (Top 3)

Major BK117

Modifications

Acquisition of

helicopter operation

in Africa extends

engineering and

operating capability

American maintenance

Approval (FAA Part 145)

est. March 2016

European Aircraft Design

Approval (Modifications)

est. March 2016

FAA and EASA (Top 3)

Major BK117 Modifications

BK117 Glass Cockpit and

Evolution Certification

(CAANZ)

NZCAA Approval

Limited approvals

covering NZ, Australia

and parts of AsiaPac

2010 2011 2012 2013 2014 Future

Available BK117 market size

55 61 61 170 170 305

Certification and IP expansion delivers new customers

2015

BK117 Engine

Upgrade Program

Indonesian approval

South African

Maintenance

Approval

Papua New Guinea

Maintenance and

Design Approval

Cayman Islands

Maintenance

Approval (Super

Yacht aircraft in NZ)

I-Plus Structural

Repair Certification

(Airbus Helicopters)

190

Appendix 5: HELICOPTER MAINTENANCE CERTIFICATION

25