HALCÓN RESOURCES · This communication contains forward-looking information regarding Halcón...

25

HALCÓN RESOURCES Johnson Rice Energy Conference September 27, 2017

Transcript of HALCÓN RESOURCES · This communication contains forward-looking information regarding Halcón...

HALCÓN RESOURCES

Johnson Rice Energy Conference September 27, 2017

This communication contains forward-looking information regarding Halcón Resources that is intended to be covered by the safe harbor for "forward-looking statements" provided by the Private Securities Litigation Reform Act of 1995. Forward-looking statements are based on Halcón Resources’ current expectations beliefs, plans, objectives, assumptions and strategies. Forward-looking statements often, but not always, can be identified by words such as "expects", "anticipates", "plans", “guidance”, "estimates", "potential", "possible", "probable", or "intends", or where Halcón Resources states that certain actions, events or results "may", "will", "should", or "could" be taken, occur or be achieved. Statements concerning oil, natural gas liquids and gas reserves also may be deemed to be forward-looking in that they reflect estimates based on certain assumptions, including that the reserves involved can be economically exploited. Statements regarding pending acquisitions and dispositions or possible acquisitions and dispositions are forward-looking statements; there can be no guarantee that acquisitions or dispositions close on the terms or within the timeframe described, if at all. Forward-looking statements are subject to risks and uncertainties which could cause actual results to differ materially from those reflected in the statements. These risks include, but are not limited to: operational risks in exploring for, developing and producing crude oil and natural gas; uncertainties involving geology of oil and natural gas deposits; the timing and amount of potential proceeds from planned divestitures; uncertainty of reserve estimates; uncertainty of estimates and projections relating to future production, costs and expenses; potential delays or changes in plans with respect to exploration or development projects or capital expenditures; health, safety and environmental risks and risks related to weather such as hurricanes and other natural disasters; uncertainties as to the availability and cost of financing; fluctuations in oil and natural gas prices; risks associated with derivative positions; inability to realize expected value from acquisitions, inability of our management team to execute our plans to meet our goals; shortages of drilling equipment, oil field personnel and services; unavailability of gathering systems, pipelines and processing facilities; and the possibility that laws, regulations or government policies may change or governmental approvals may be delayed or withheld. Additional information on these and other factors which could affect Halcón Resources' operations or financial results are included in Halcón Resources’ reports on file with the SEC. Investors are cautioned that any forward-looking statements are not guarantees of future performance and actual results or developments may differ materially from those expressed in forward-looking statements. Forward-looking statements are based on assumptions, estimates and opinions of management at the time the statements are made. Halcón Resources does not assume any obligation to update forward-looking statements should circumstances or such assumptions, estimates or opinions change.

Forward-Looking Statements

The SEC requires oil and gas companies, in their filings with the SEC, to disclose proved reserves, which are those quantities of oil and gas, which, by analysis of geoscience and engineering data, can be estimated with reasonable certainty to be economically producible—from a given date forward, from known reservoirs, and under existing economic conditions (using unweighted average 12-month first day of the month prices), operating methods, and government regulations—prior to the time at which contracts providing the right to operate expire, unless evidence indicates that renewal is reasonably certain, regardless of whether deterministic or probabilistic methods are used for the estimation. The SEC also permits the disclosure of separate estimates of probable or possible reserves that meet SEC definitions for such reserves. These estimates are by their nature more speculative than estimates of proved reserves and are subject to greater uncertainties and, accordingly, the likelihood of recovering those reserves is subject to substantially greater risks. We may use the terms “resource potential” and “EUR” in this presentation to describe estimates of potentially recoverable hydrocarbons that the SEC rules prohibit from being included in filings with the SEC. These are based on the Company’s internal estimates of hydrocarbon quantities that may be potentially discovered through exploratory drilling or recovered with additional drilling or recovery techniques. These quantities do not constitute “reserves” within the meaning of the Society of Petroleum Engineer’s Petroleum Resource Management System or SEC rules and are subject to substantially greater uncertainties relating to recovery than reserves. “EUR,” or Estimated Ultimate Recovery, refers to our management’s internal estimates based on per well hydrocarbon quantities that may be potentially recovered from a hypothetical future well completed as a producer in the area. For areas where the Company has no or very limited operating history, EURs are based on publicly available information relating to operations of producers operating in such areas. For areas where the Company has sufficient operating data to make its own estimates, EURs are based on internal estimates by the Company’s management and reserve engineers. “Drilling locations” represent the number of locations that we currently estimate could potentially be drilled in a particular area estimated by well spacing assumptions applicable to that area. The actual number of locations drilled and quantities that may be ultimately recovered from the Company’s interests will differ substantially. There is no commitment by the Company to drill the drilling locations which have been attributed to any area. We may use the term “de-risked” in this presentation to refer to certain acreage and well locations where we believe the relative geological risks related to recovery have been reduced as a result of drilling operations to date. However, only a small portion of such acreage and locations may have been attributed proved undeveloped reserves and ultimate recovery from such acreage and locations remains subject to all of the recovery risks applicable to unproved acreage. Factors affecting ultimate recovery include: (1) the scope of our on-going drilling program, which will be directly affected by factors that include the availability of capital, drilling and production costs, availability of drilling services and equipment, drilling results, lease expirations, transportation constraints, regulatory approvals and other factors; and (2) actual drilling results, including geological and mechanical factors affecting recovery rates. In addition, our production forecasts and expectations for future periods are dependent upon many assumptions, including estimates of production decline rates from existing wells and the undertaking and outcome of future drilling activity, which will be affected by changes in commodity prices and costs.

Cautionary Statements

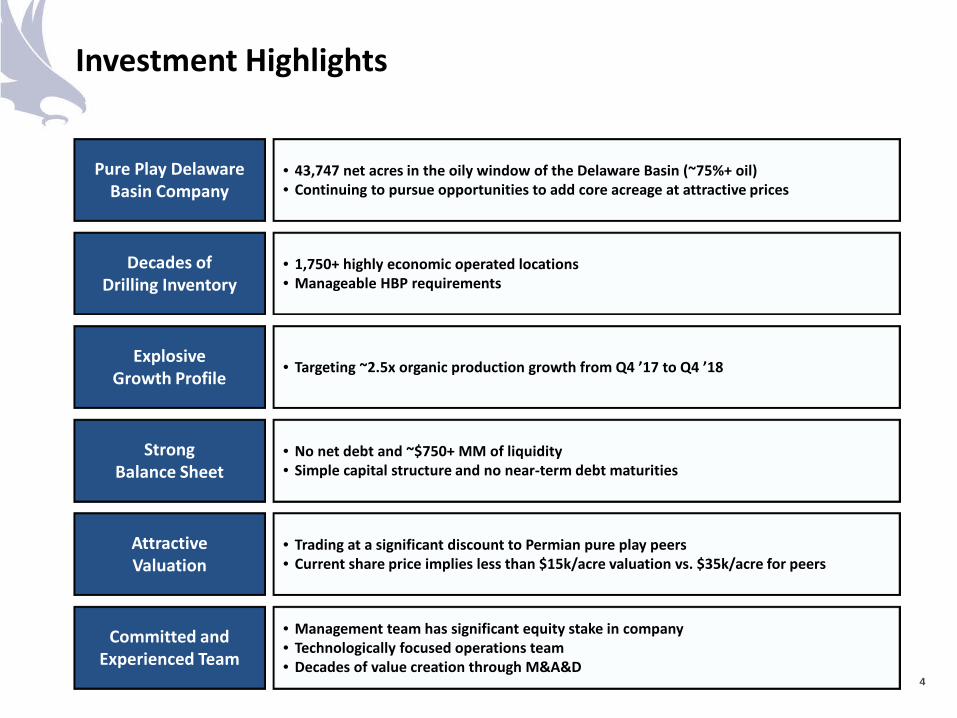

Investment Highlights

Pure Play Delaware Basin Company

Decades of Drilling Inventory

Explosive Growth Profile

Strong Balance Sheet

Attractive Valuation

• 43,747 net acres in the oily window of the Delaware Basin (~75%+ oil) • Continuing to pursue opportunities to add core acreage at attractive prices

• 1,750+ highly economic operated locations • Manageable HBP requirements

• Targeting ~2.5x organic production growth from Q4 ’17 to Q4 ’18

• No net debt and ~$750+ MM of liquidity • Simple capital structure and no near-term debt maturities

• Trading at a significant discount to Permian pure play peers • Current share price implies less than $15k/acre valuation vs. $35k/acre for peers

Committed and Experienced Team

• Management team has significant equity stake in company • Technologically focused operations team • Decades of value creation through M&A&D

4

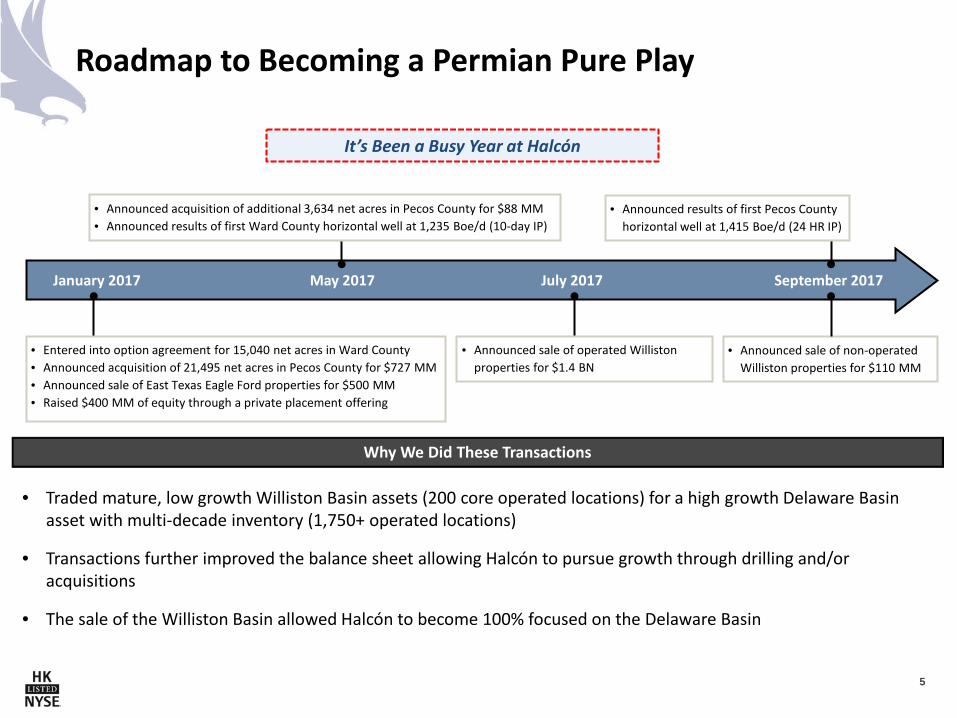

Roadmap to Becoming a Permian Pure Play

Why We Did These Transactions

September 2017

• Entered into option agreement for 15,040 net acres in Ward County • Announced acquisition of 21,495 net acres in Pecos County for $727 MM • Announced sale of East Texas Eagle Ford properties for $500 MM • Raised $400 MM of equity through a private placement offering

July 2017 May 2017 January 2017

• Traded mature, low growth Williston Basin assets (200 core operated locations) for a high growth Delaware Basin asset with multi-decade inventory (1,750+ operated locations)

• Transactions further improved the balance sheet allowing Halcón to pursue growth through drilling and/or acquisitions

• The sale of the Williston Basin allowed Halcón to become 100% focused on the Delaware Basin

It’s Been a Busy Year at Halcón

• Announced acquisition of additional 3,634 net acres in Pecos County for $88 MM • Announced results of first Ward County horizontal well at 1,235 Boe/d (10-day IP)

• Announced results of first Pecos County horizontal well at 1,415 Boe/d (24 HR IP)

• Announced sale of operated Williston properties for $1.4 BN

• Announced sale of non-operated Williston properties for $110 MM

5

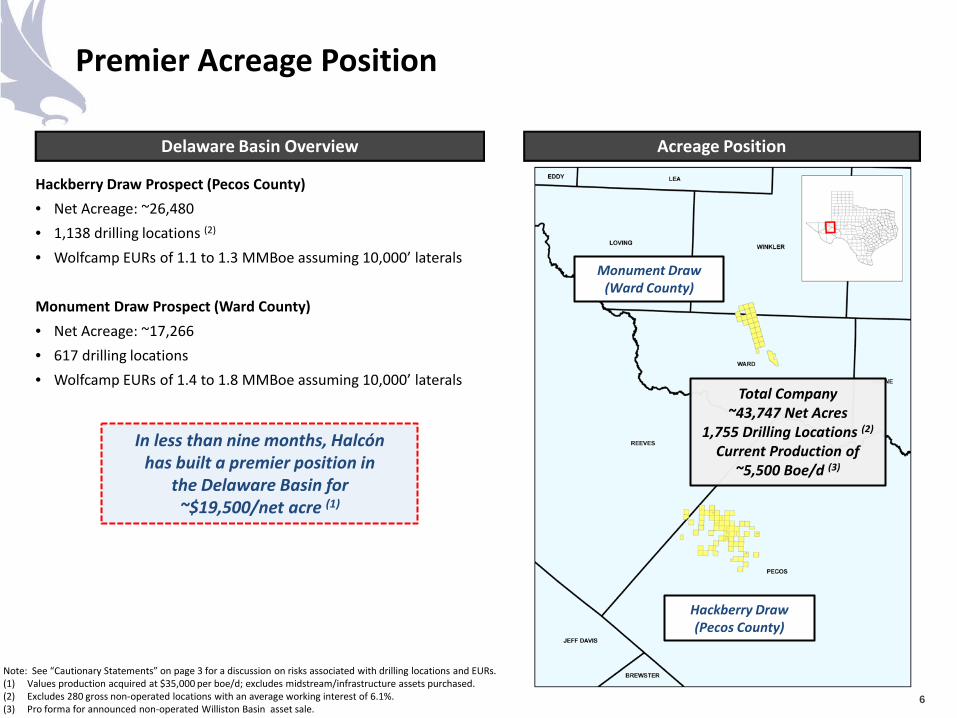

Premier Acreage Position

6

Note: See “Cautionary Statements” on page 3 for a discussion on risks associated with drilling locations and EURs. (1) Values production acquired at $35,000 per boe/d; excludes midstream/infrastructure assets purchased. (2) Excludes 280 gross non-operated locations with an average working interest of 6.1%. (3) Pro forma for announced non-operated Williston Basin asset sale.

Delaware Basin Overview Acreage Position

Monument Draw (Ward County)

Hackberry Draw (Pecos County)

Total Company ~43,747 Net Acres

1,755 Drilling Locations (2)

Current Production of ~5,500 Boe/d (3)

In less than nine months, Halcón has built a premier position in

the Delaware Basin for ~$19,500/net acre (1)

Hackberry Draw Prospect (Pecos County) • Net Acreage: ~26,480 • 1,138 drilling locations (2)

• Wolfcamp EURs of 1.1 to 1.3 MMBoe assuming 10,000’ laterals Monument Draw Prospect (Ward County) • Net Acreage: ~17,266 • 617 drilling locations • Wolfcamp EURs of 1.4 to 1.8 MMBoe assuming 10,000’ laterals

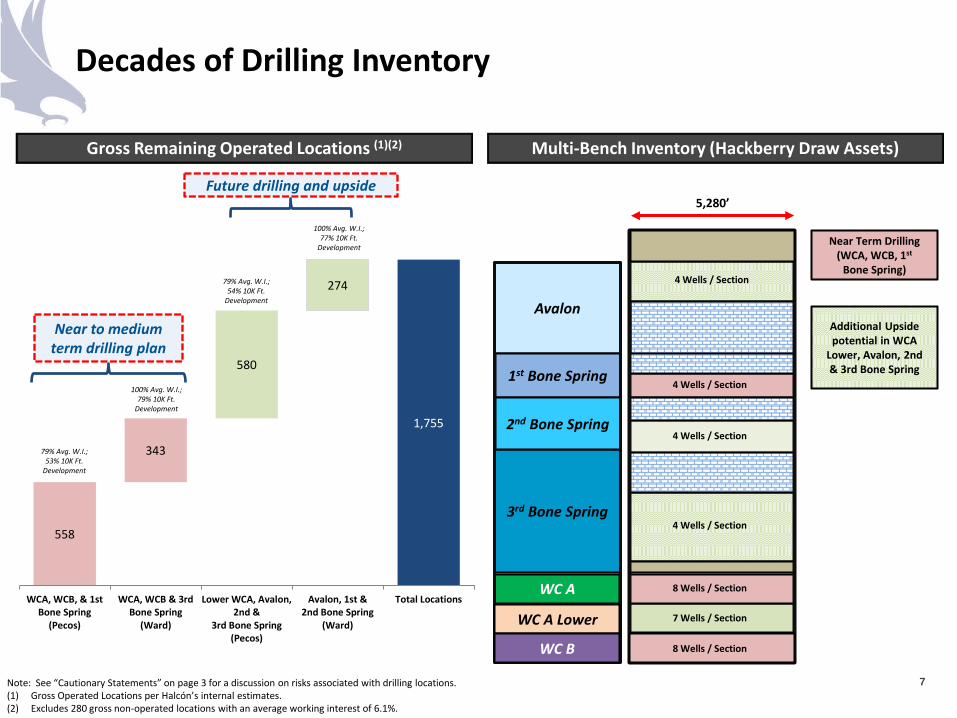

558

343

580

274

1,755

WCA, WCB, & 1stBone Spring

(Pecos)

WCA, WCB & 3rdBone Spring

(Ward)

Lower WCA, Avalon,2nd &

3rd Bone Spring(Pecos)

Avalon, 1st &2nd Bone Spring

(Ward)

Total Locations

Decades of Drilling Inventory

7

Gross Remaining Operated Locations (1)(2) Multi-Bench Inventory (Hackberry Draw Assets)

Note: See “Cautionary Statements” on page 3 for a discussion on risks associated with drilling locations. (1) Gross Operated Locations per Halcón’s internal estimates. (2) Excludes 280 gross non-operated locations with an average working interest of 6.1%.

5,280’

4 Wells / Section

4 Wells / Section

8 Wells / Section

7 Wells / Section

WC A

3rd Bone Spring

Avalon

1st Bone Spring

2nd Bone Spring

WC A Lower

Near Term Drilling (WCA, WCB, 1st

Bone Spring)

8 Wells / Section WC B

Additional Upside potential in WCA

Lower, Avalon, 2nd & 3rd Bone Spring

4 Wells / Section

4 Wells / Section

Near to medium term drilling plan

Future drilling and upside

79% Avg. W.I.; 53% 10K Ft.

Development

100% Avg. W.I.; 79% 10K Ft.

Development

79% Avg. W.I.; 54% 10K Ft.

Development

100% Avg. W.I.; 77% 10K Ft.

Development

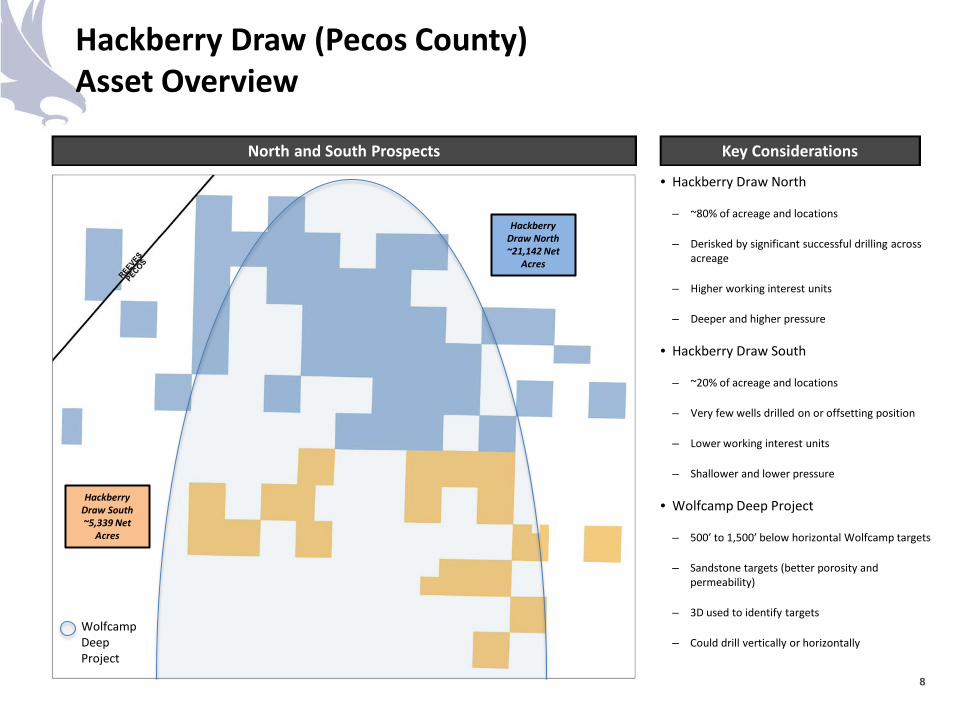

Hackberry Draw (Pecos County) Asset Overview

North and South Prospects

8

Key Considerations

• Hackberry Draw North

– ~80% of acreage and locations

– Derisked by significant successful drilling across acreage

– Higher working interest units

– Deeper and higher pressure

• Hackberry Draw South

– ~20% of acreage and locations

– Very few wells drilled on or offsetting position

– Lower working interest units

– Shallower and lower pressure

• Wolfcamp Deep Project

– 500’ to 1,500’ below horizontal Wolfcamp targets

– Sandstone targets (better porosity and permeability)

– 3D used to identify targets

– Could drill vertically or horizontally

Hackberry Draw North ~21,142 Net

Acres

Hackberry Draw South ~5,339 Net

Acres

Wolfcamp Deep Project

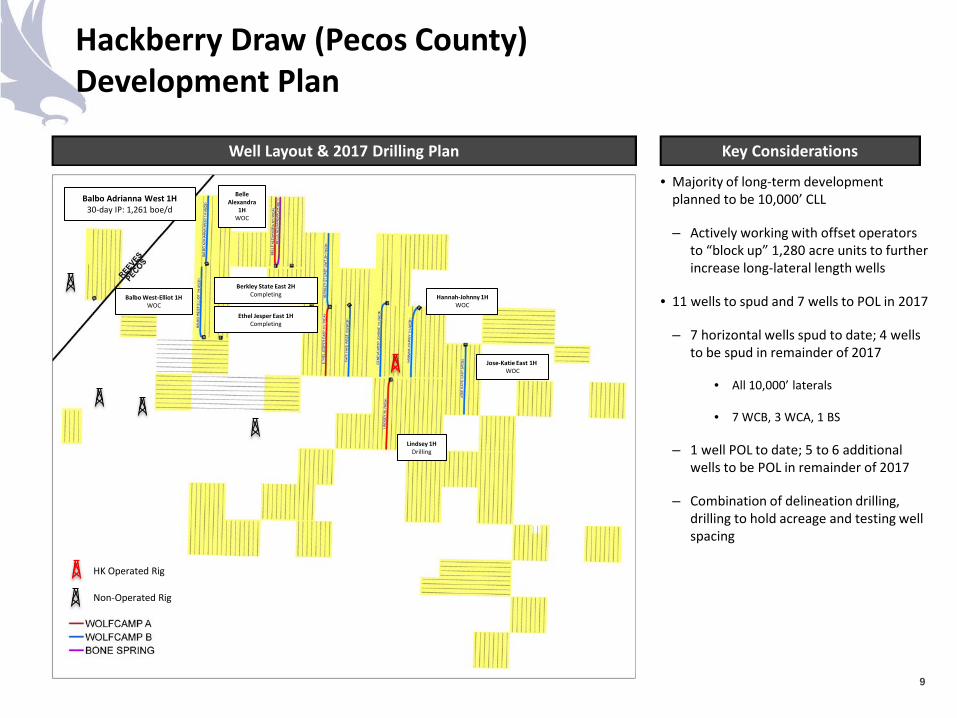

Hackberry Draw (Pecos County) Development Plan

Well Layout & 2017 Drilling Plan

9

Key Considerations

• Majority of long-term development planned to be 10,000’ CLL

– Actively working with offset operators to “block up” 1,280 acre units to further increase long-lateral length wells

• 11 wells to spud and 7 wells to POL in 2017

– 7 horizontal wells spud to date; 4 wells to be spud in remainder of 2017

• All 10,000’ laterals

• 7 WCB, 3 WCA, 1 BS

– 1 well POL to date; 5 to 6 additional wells to be POL in remainder of 2017

– Combination of delineation drilling, drilling to hold acreage and testing well spacing

Balbo West-Elliot 1H WOC

Balbo Adrianna West 1H 30-day IP: 1,261 boe/d

Belle Alexandra

1H WOC

Berkley State East 2H Completing Hannah-Johnny 1H

WOC

Jose-Katie East 1H WOC

Non-Operated Rig

Ethel Jesper East 1H Completing

HK Operated Rig

Lindsey 1H Drilling

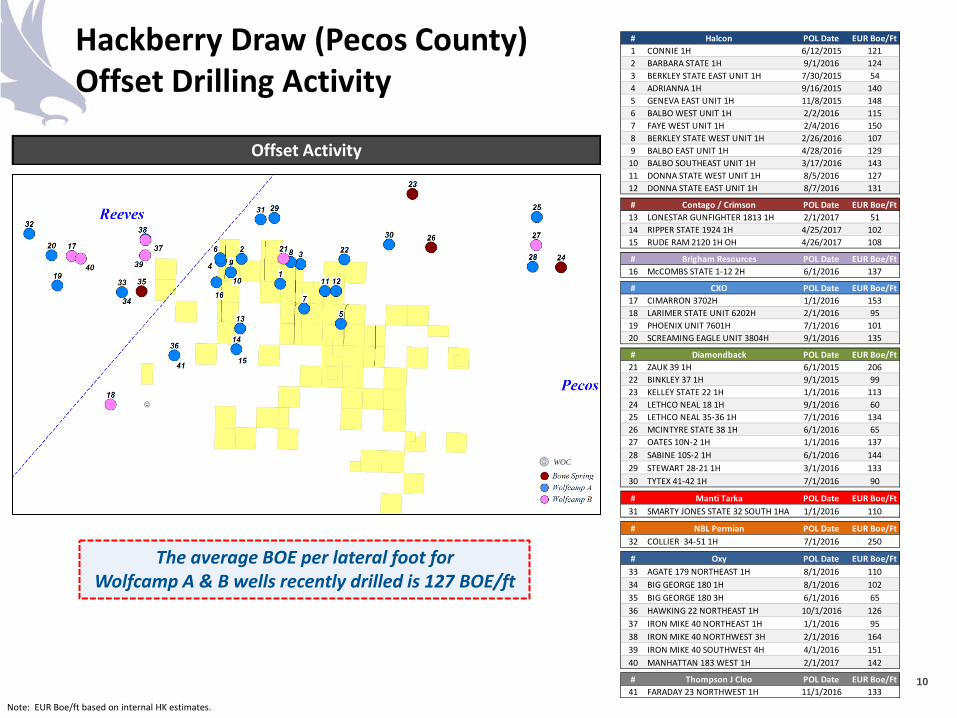

Hackberry Draw (Pecos County) Offset Drilling Activity

10

The average BOE per lateral foot for Wolfcamp A & B wells recently drilled is 127 BOE/ft

Note: EUR Boe/ft based on internal HK estimates.

Offset Activity

WOC

# Halcon POL Date EUR Boe/Ft1 CONNIE 1H 6/12/2015 1212 BARBARA STATE 1H 9/1/2016 1243 BERKLEY STATE EAST UNIT 1H 7/30/2015 544 ADRIANNA 1H 9/16/2015 1405 GENEVA EAST UNIT 1H 11/8/2015 1486 BALBO WEST UNIT 1H 2/2/2016 1157 FAYE WEST UNIT 1H 2/4/2016 1508 BERKLEY STATE WEST UNIT 1H 2/26/2016 1079 BALBO EAST UNIT 1H 4/28/2016 12910 BALBO SOUTHEAST UNIT 1H 3/17/2016 14311 DONNA STATE WEST UNIT 1H 8/5/2016 12712 DONNA STATE EAST UNIT 1H 8/7/2016 131

# Contago / Crimson POL Date EUR Boe/Ft13 LONESTAR GUNFIGHTER 1813 1H 2/1/2017 5114 RIPPER STATE 1924 1H 4/25/2017 10215 RUDE RAM 2120 1H OH 4/26/2017 108

# Brigham Resources POL Date EUR Boe/Ft16 McCOMBS STATE 1-12 2H 6/1/2016 137

# CXO POL Date EUR Boe/Ft17 CIMARRON 3702H 1/1/2016 15318 LARIMER STATE UNIT 6202H 2/1/2016 9519 PHOENIX UNIT 7601H 7/1/2016 10120 SCREAMING EAGLE UNIT 3804H 9/1/2016 135

# Diamondback POL Date EUR Boe/Ft21 ZAUK 39 1H 6/1/2015 20622 BINKLEY 37 1H 9/1/2015 9923 KELLEY STATE 22 1H 1/1/2016 11324 LETHCO NEAL 18 1H 9/1/2016 6025 LETHCO NEAL 35-36 1H 7/1/2016 13426 MCINTYRE STATE 38 1H 6/1/2016 6527 OATES 10N-2 1H 1/1/2016 13728 SABINE 10S-2 1H 6/1/2016 14429 STEWART 28-21 1H 3/1/2016 13330 TYTEX 41-42 1H 7/1/2016 90

# Manti Tarka POL Date EUR Boe/Ft31 SMARTY JONES STATE 32 SOUTH 1HA 1/1/2016 110

# NBL Permian POL Date EUR Boe/Ft32 COLLIER 34-51 1H 7/1/2016 250

# Oxy POL Date EUR Boe/Ft33 AGATE 179 NORTHEAST 1H 8/1/2016 11034 BIG GEORGE 180 1H 8/1/2016 10235 BIG GEORGE 180 3H 6/1/2016 6536 HAWKING 22 NORTHEAST 1H 10/1/2016 12637 IRON MIKE 40 NORTHEAST 1H 1/1/2016 9538 IRON MIKE 40 NORTHWEST 3H 2/1/2016 16439 IRON MIKE 40 SOUTHWEST 4H 4/1/2016 15140 MANHATTAN 183 WEST 1H 2/1/2017 142

# Thompson J Cleo POL Date EUR Boe/Ft41 FARADAY 23 NORTHWEST 1H 11/1/2016 133

0200400600800

1,0001,2001,4001,6001,800

1 3 5 7 9 11 13 15 17 19 21 23 25 27

Nor

mal

ized

Rat

e (B

oe/d

)

Normalized Time (Months)

0

200

400

600

800

1,000

1,200

1,400

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16

Nor

mal

ized

Rat

e (B

oe/d

)

Normalized Time (Months)

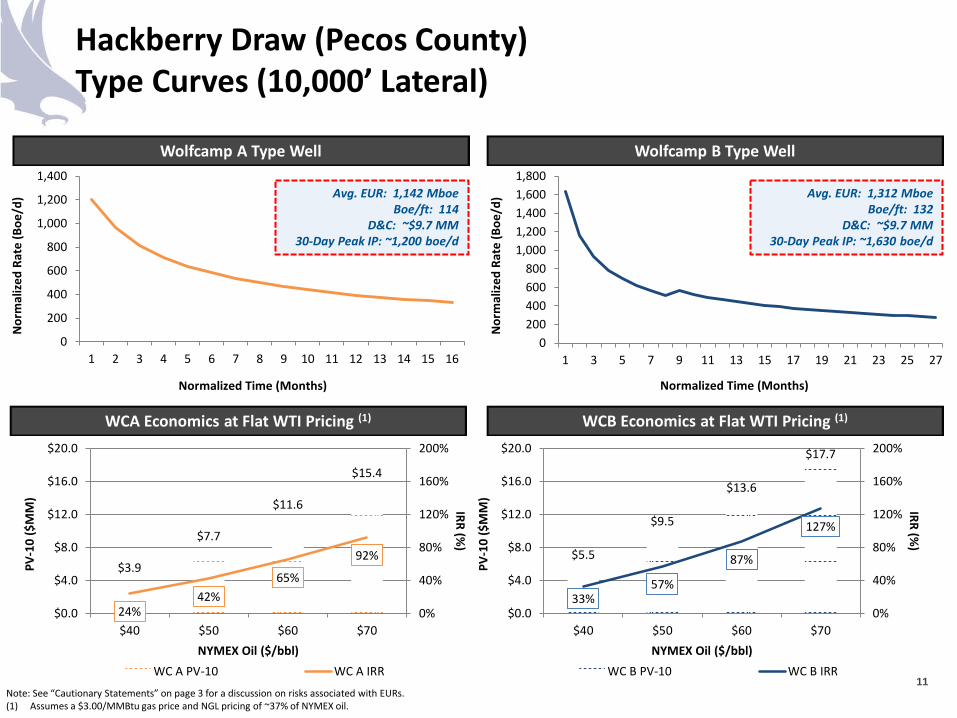

Hackberry Draw (Pecos County) Type Curves (10,000’ Lateral)

Note: See “Cautionary Statements” on page 3 for a discussion on risks associated with EURs. (1) Assumes a $3.00/MMBtu gas price and NGL pricing of ~37% of NYMEX oil.

Wolfcamp A Type Well Wolfcamp B Type Well

WCB Economics at Flat WTI Pricing (1)

11

Avg. EUR: 1,142 Mboe Boe/ft: 114

D&C: ~$9.7 MM 30-Day Peak IP: ~1,200 boe/d

Avg. EUR: 1,312 Mboe Boe/ft: 132

D&C: ~$9.7 MM 30-Day Peak IP: ~1,630 boe/d

WCA Economics at Flat WTI Pricing (1)

$3.9

$7.7

$11.6

$15.4

24% 42%

65%

92%

0%

40%

80%

120%

160%

200%

$0.0

$4.0

$8.0

$12.0

$16.0

$20.0

$40 $50 $60 $70

IRR (%)

PV-1

0 ($

MM

)

NYMEX Oil ($/bbl) WC A PV-10 WC A IRR

$5.5

$9.5

$13.6

$17.7

33% 57%

87%

127%

0%

40%

80%

120%

160%

200%

$0.0

$4.0

$8.0

$12.0

$16.0

$20.0

$40 $50 $60 $70

IRR (%)

PV-1

0 ($

MM

)

NYMEX Oil ($/bbl) WC B PV-10 WC B IRR

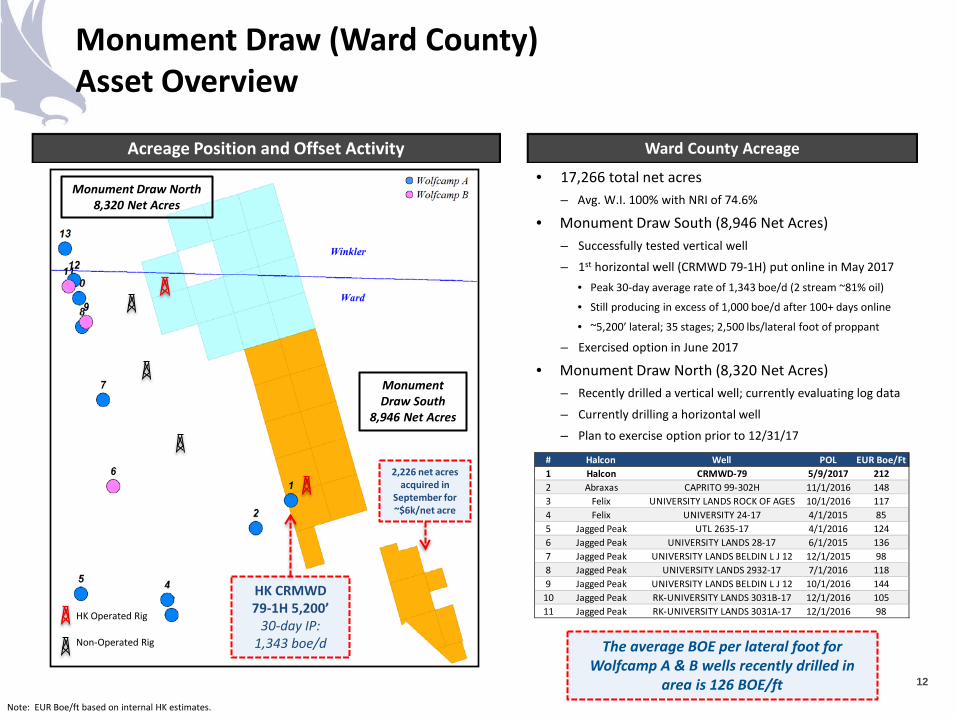

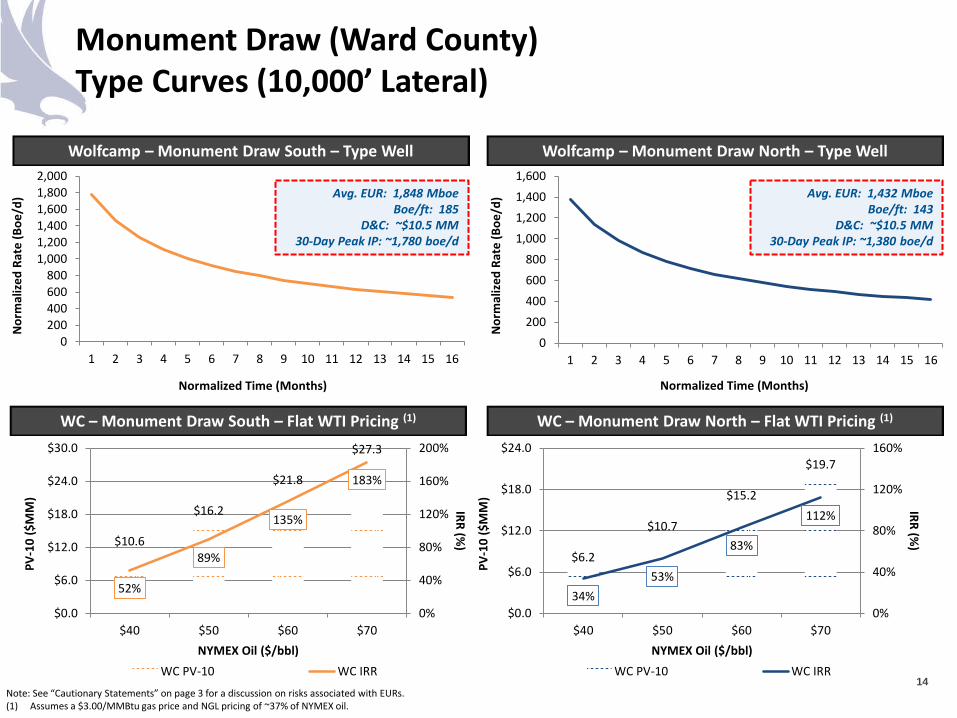

Monument Draw (Ward County) Asset Overview

12

Acreage Position and Offset Activity

• 17,266 total net acres – Avg. W.I. 100% with NRI of 74.6%

• Monument Draw South (8,946 Net Acres) – Successfully tested vertical well

– 1st horizontal well (CRMWD 79-1H) put online in May 2017 • Peak 30-day average rate of 1,343 boe/d (2 stream ~81% oil)

• Still producing in excess of 1,000 boe/d after 100+ days online

• ~5,200’ lateral; 35 stages; 2,500 lbs/lateral foot of proppant

– Exercised option in June 2017

• Monument Draw North (8,320 Net Acres) – Recently drilled a vertical well; currently evaluating log data

– Currently drilling a horizontal well

– Plan to exercise option prior to 12/31/17

Ward County Acreage

HK CRMWD 79-1H 5,200’

30-day IP: 1,343 boe/d The average BOE per lateral foot for

Wolfcamp A & B wells recently drilled in area is 126 BOE/ft

Note: EUR Boe/ft based on internal HK estimates.

Non-Operated Rig

HK Operated Rig

# Halcon Well POL EUR Boe/Ft1 Halcon CRMWD-79 5/9/2017 2122 Abraxas CAPRITO 99-302H 11/1/2016 1483 Felix UNIVERSITY LANDS ROCK OF AGES 10/1/2016 1174 Felix UNIVERSITY 24-17 4/1/2015 855 Jagged Peak UTL 2635-17 4/1/2016 1246 Jagged Peak UNIVERSITY LANDS 28-17 6/1/2015 1367 Jagged Peak UNIVERSITY LANDS BELDIN L J 12 12/1/2015 988 Jagged Peak UNIVERSITY LANDS 2932-17 7/1/2016 1189 Jagged Peak UNIVERSITY LANDS BELDIN L J 12 10/1/2016 14410 Jagged Peak RK-UNIVERSITY LANDS 3031B-17 12/1/2016 10511 Jagged Peak RK-UNIVERSITY LANDS 3031A-17 12/1/2016 98

Monument Draw North 8,320 Net Acres

Monument Draw South

8,946 Net Acres

2,226 net acres acquired in

September for ~$6k/net acre

Monument Draw (Ward County) Development Plan

Well Layout Key Considerations

• 79% of drilling locations planned to be 10,000’ laterals

• 10 horizontal wells to spud and 4 wells to POL in 2017

– 2 vertical pilots and 4 horizontal wells spud to date; 6 horizontal wells to be spud in remainder of 2017

– 1 well POL to date; 3 wells to POL in remainder of 2017

• Contiguous acreage footprint provides benefits

– Ideal for multi-well pad development

– Maximum efficiency in D&C operations

– Simultaneous frac operations maximizes reservoir drainage

• Efficient and cost-effective infrastructure development underway

– Concentrated gas and water gathering lines

13

Sealy Ranch 6901 Pilot

CRMWD 79 1H Producing

Sealy Ranch 7902 H & Sealy Ranch 7903 H

Drilling

Sealy Ranch 9301 H Drilling

0200400600800

1,0001,2001,4001,6001,8002,000

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16

Nor

mal

ized

Rat

e (B

oe/d

)

Normalized Time (Months)

0200400600800

1,0001,2001,4001,600

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16

Nor

mal

ized

Rat

e (B

oe/d

)

Normalized Time (Months)

Monument Draw (Ward County) Type Curves (10,000’ Lateral)

Note: See “Cautionary Statements” on page 3 for a discussion on risks associated with EURs. (1) Assumes a $3.00/MMBtu gas price and NGL pricing of ~37% of NYMEX oil.

Wolfcamp – Monument Draw South – Type Well Wolfcamp – Monument Draw North – Type Well

WC – Monument Draw North – Flat WTI Pricing (1)

14

Avg. EUR: 1,848 Mboe Boe/ft: 185

D&C: ~$10.5 MM 30-Day Peak IP: ~1,780 boe/d

Avg. EUR: 1,432 Mboe Boe/ft: 143

D&C: ~$10.5 MM 30-Day Peak IP: ~1,380 boe/d

WC – Monument Draw South – Flat WTI Pricing (1)

$10.6

$16.2

$21.8

$27.3

52%

89%

135%

183%

0%

40%

80%

120%

160%

200%

$0.0

$6.0

$12.0

$18.0

$24.0

$30.0

$40 $50 $60 $70

IRR (%)

PV-1

0 ($

MM

)

NYMEX Oil ($/bbl) WC PV-10 WC IRR

$6.2

$10.7

$15.2

$19.7

34% 53%

83%

112%

0%

40%

80%

120%

160%

$0.0

$6.0

$12.0

$18.0

$24.0

$40 $50 $60 $70

IRR (%)

PV-1

0 ($

MM

)

NYMEX Oil ($/bbl) WC PV-10 WC IRR

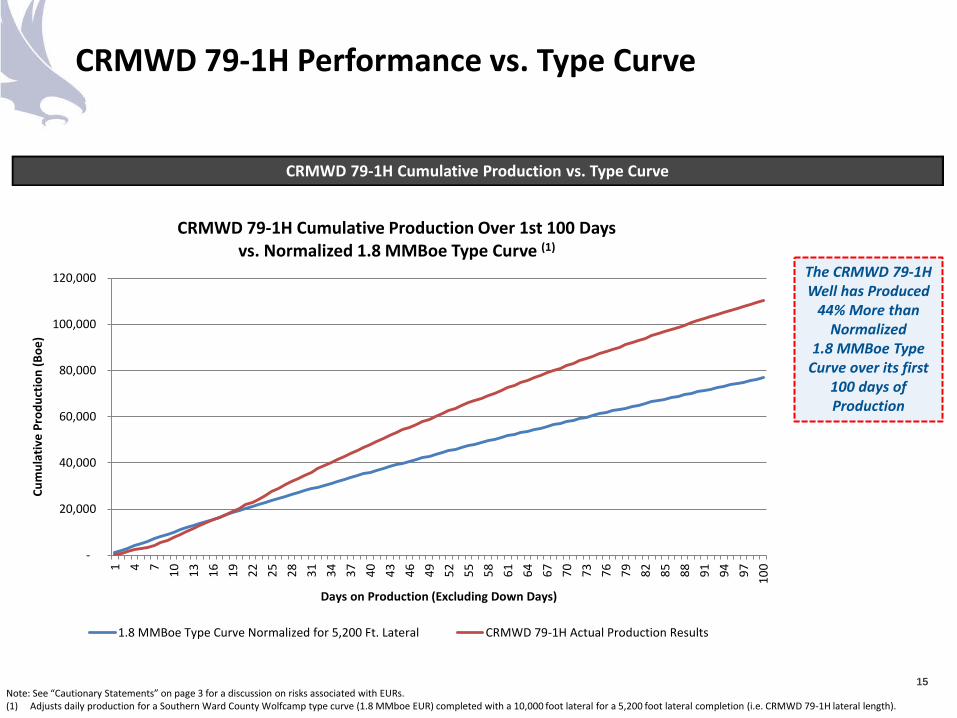

CRMWD 79-1H Performance vs. Type Curve

Note: See “Cautionary Statements” on page 3 for a discussion on risks associated with EURs. (1) Adjusts daily production for a Southern Ward County Wolfcamp type curve (1.8 MMboe EUR) completed with a 10,000 foot lateral for a 5,200 foot lateral completion (i.e. CRMWD 79-1H lateral length).

15

CRMWD 79-1H Cumulative Production vs. Type Curve

The CRMWD 79-1H Well has Produced

44% More than Normalized

1.8 MMBoe Type Curve over its first

100 days of Production

-

20,000

40,000

60,000

80,000

100,000

120,000

1 4 7 10 13 16 19 22 25 28 31 34 37 40 43 46 49 52 55 58 61 64 67 70 73 76 79 82 85 88 91 94 97 100

Cum

ulat

ive

Prod

uctio

n (B

oe)

Days on Production (Excluding Down Days)

CRMWD 79-1H Cumulative Production Over 1st 100 Days vs. Normalized 1.8 MMBoe Type Curve (1)

1.8 MMBoe Type Curve Normalized for 5,200 Ft. Lateral CRMWD 79-1H Actual Production Results

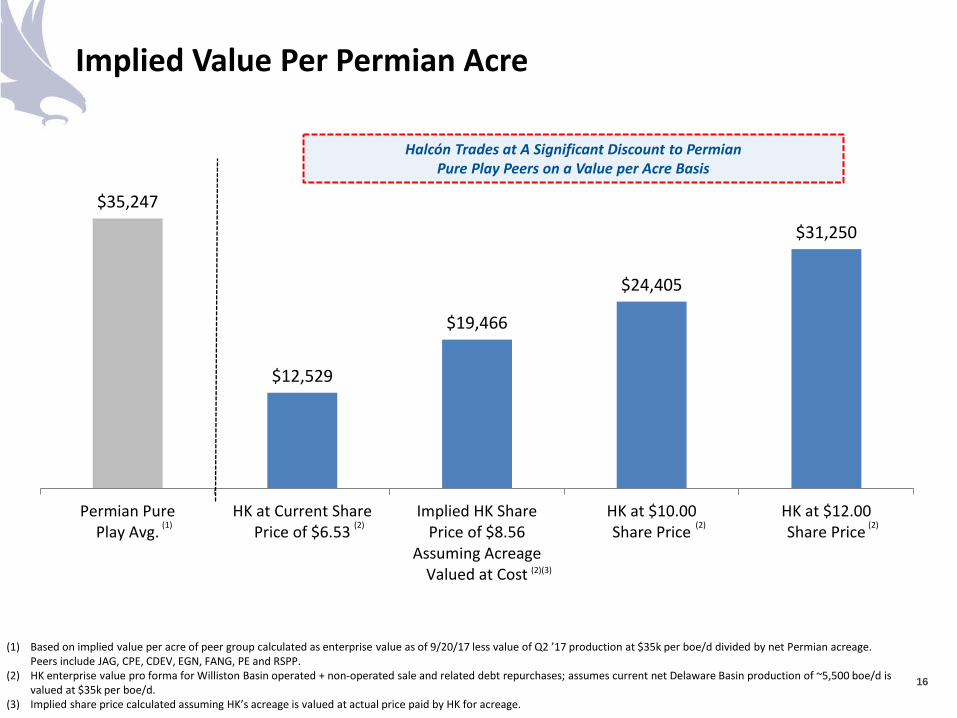

$35,247

$12,529

$19,466

$24,405

$31,250

Permian PurePlay Avg.

HK at Current SharePrice of $6.53

Implied HK SharePrice of $8.56

Assuming AcreageValued at Cost

HK at $10.00Share Price

HK at $12.00Share Price

Implied Value Per Permian Acre

16

Halcón Trades at A Significant Discount to Permian Pure Play Peers on a Value per Acre Basis

(1) (2) (2) (2)

(1) Based on implied value per acre of peer group calculated as enterprise value as of 9/20/17 less value of Q2 ’17 production at $35k per boe/d divided by net Permian acreage. Peers include JAG, CPE, CDEV, EGN, FANG, PE and RSPP.

(2) HK enterprise value pro forma for Williston Basin operated + non-operated sale and related debt repurchases; assumes current net Delaware Basin production of ~5,500 boe/d is valued at $35k per boe/d.

(3) Implied share price calculated assuming HK’s acreage is valued at actual price paid by HK for acreage.

(2)(3)

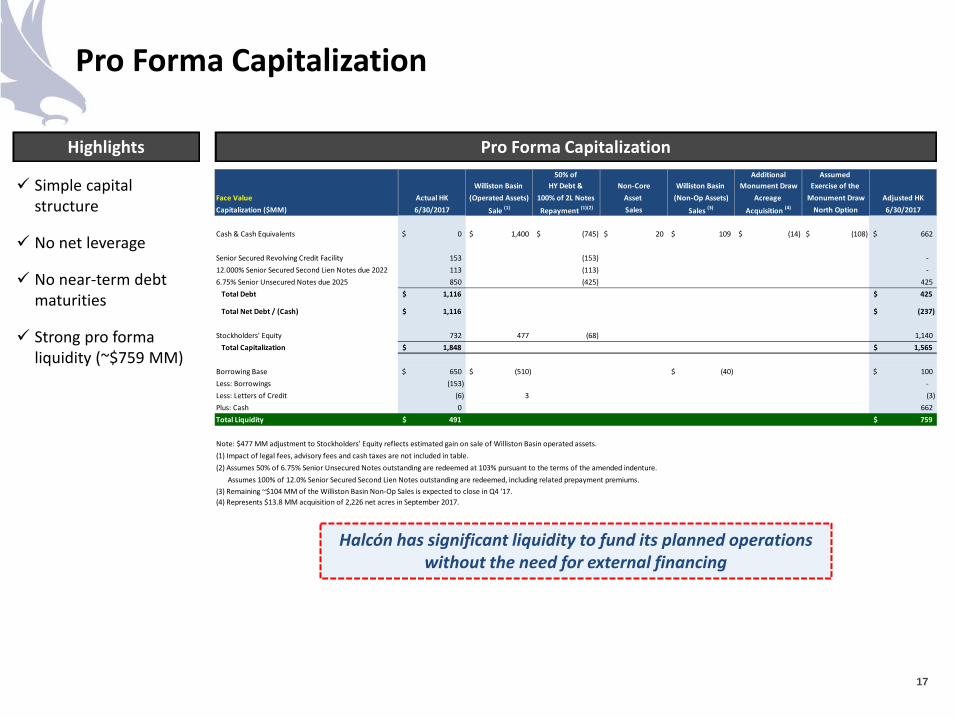

Pro Forma Capitalization

17

Simple capital structure

No net leverage

No near-term debt maturities

Strong pro forma liquidity (~$759 MM)

Highlights Pro Forma Capitalization

Halcón has significant liquidity to fund its planned operations without the need for external financing

50% of Additional Assumed Williston Basin HY Debt & Non-Core Williston Basin Monument Draw Exercise of the

Face Value Actual HK (Operated Assets) 100% of 2L Notes Asset (Non-Op Assets) Acreage Monument Draw Adjusted HKCapitalization ($MM) 6/30/2017 Sale (1) Repayment (1)(2) Sales Sales (3) Acquisition (4) North Option 6/30/2017

Cash & Cash Equivalents 0$ 1,400$ (745)$ 20$ 109$ (14)$ (108)$ 662$

Senior Secured Revolving Credit Facility 153 (153) - 12.000% Senior Secured Second Lien Notes due 2022 113 (113) - 6.75% Senior Unsecured Notes due 2025 850 (425) 425

Total Debt 1,116$ 425$

Total Net Debt / (Cash) 1,116$ (237)$

Stockholders' Equity 732 477 (68) 1,140 Total Capitalization 1,848$ 1,565$

Borrowing Base 650$ (510)$ (40)$ 100$ Less: Borrowings (153) - Less: Letters of Credit (6) 3 (3) Plus: Cash 0 662 Total Liquidity 491$ 759$

Note: $477 MM adjustment to Stockholders' Equity reflects estimated gain on sale of Williston Basin operated assets.(1) Impact of legal fees, advisory fees and cash taxes are not included in table.(2) Assumes 50% of 6.75% Senior Unsecured Notes outstanding are redeemed at 103% pursuant to the terms of the amended indenture.(3) Assumes 100% of 12.0% Senior Secured Second Lien Notes outstanding are redeemed, including related prepayment premiums.(3) Remaining ~$104 MM of the Williston Basin Non-Op Sales is expected to close in Q4 '17.(4) Represents $13.8 MM acquisition of 2,226 net acres in September 2017.

Appendix

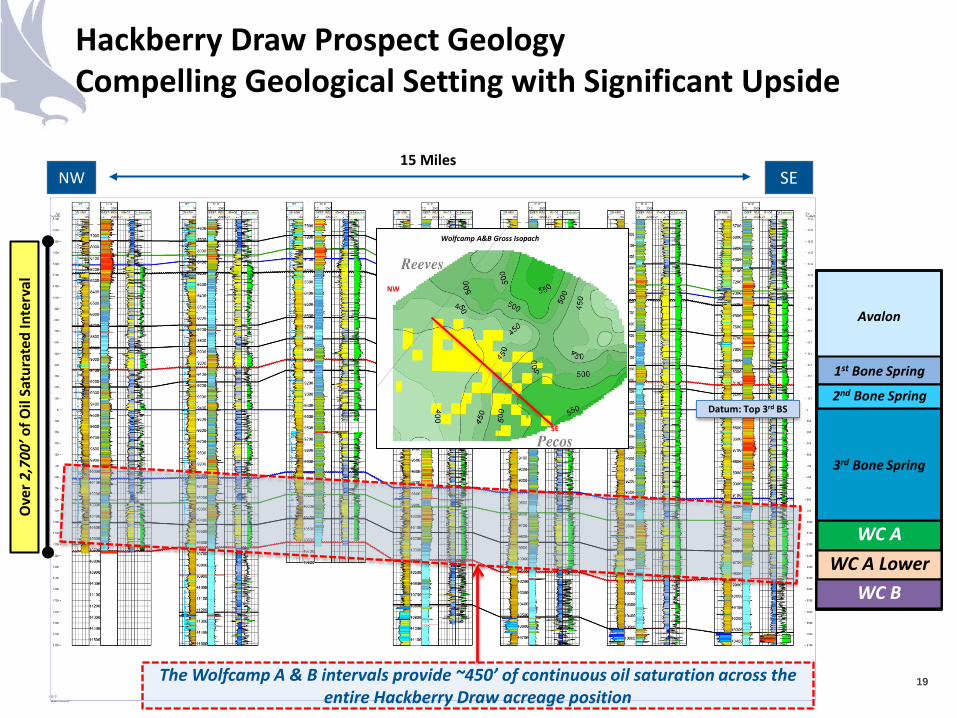

Hackberry Draw Prospect Geology Compelling Geological Setting with Significant Upside

19

Ove

r 2,7

00’ o

f Oil

Satu

rate

d In

terv

al

WC A

3rd Bone Spring

Avalon

1st Bone Spring

2nd Bone Spring

NW SE 15 Miles

Datum: Top 3rd BS

NW

SE

Wolfcamp A&B Gross Isopach

The Wolfcamp A & B intervals provide ~450’ of continuous oil saturation across the entire Hackberry Draw acreage position

WC A Lower WC B

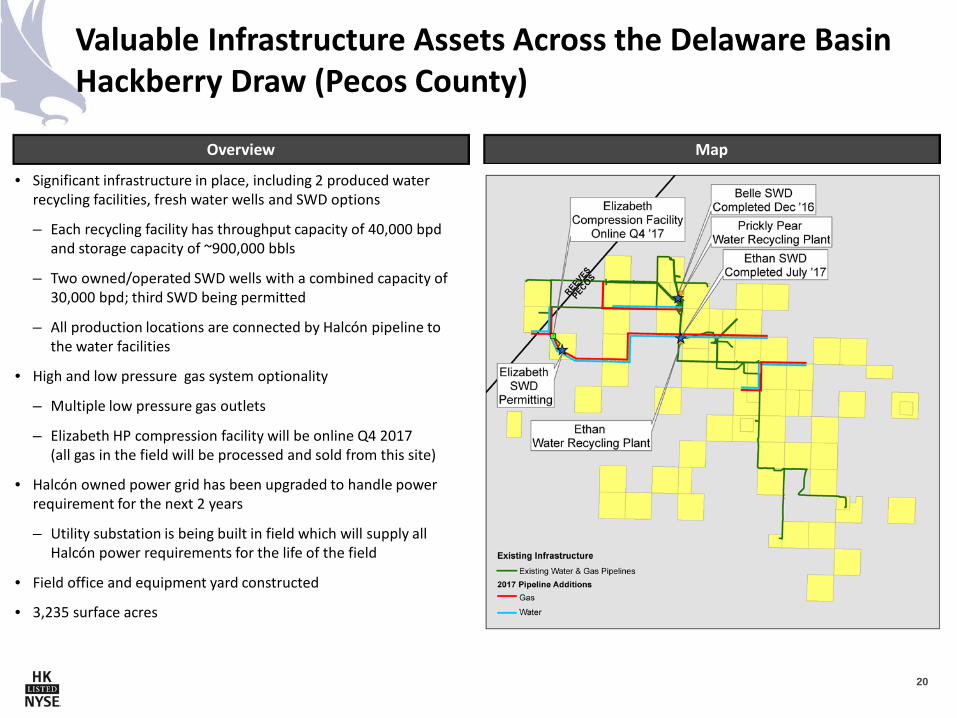

Valuable Infrastructure Assets Across the Delaware Basin Hackberry Draw (Pecos County)

20

• Significant infrastructure in place, including 2 produced water recycling facilities, fresh water wells and SWD options

– Each recycling facility has throughput capacity of 40,000 bpd and storage capacity of ~900,000 bbls

– Two owned/operated SWD wells with a combined capacity of 30,000 bpd; third SWD being permitted

– All production locations are connected by Halcón pipeline to the water facilities

• High and low pressure gas system optionality

– Multiple low pressure gas outlets

– Elizabeth HP compression facility will be online Q4 2017 (all gas in the field will be processed and sold from this site)

• Halcón owned power grid has been upgraded to handle power requirement for the next 2 years

– Utility substation is being built in field which will supply all Halcón power requirements for the life of the field

• Field office and equipment yard constructed

• 3,235 surface acres

Overview Map

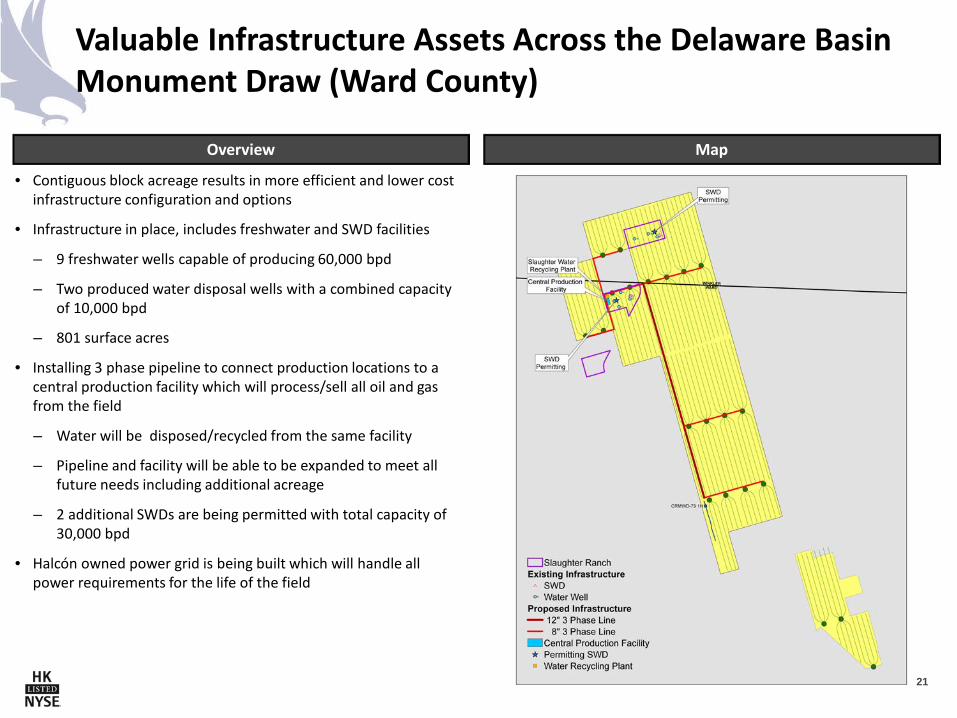

Valuable Infrastructure Assets Across the Delaware Basin Monument Draw (Ward County)

21

Overview Map

• Contiguous block acreage results in more efficient and lower cost infrastructure configuration and options

• Infrastructure in place, includes freshwater and SWD facilities

– 9 freshwater wells capable of producing 60,000 bpd

– Two produced water disposal wells with a combined capacity of 10,000 bpd

– 801 surface acres

• Installing 3 phase pipeline to connect production locations to a central production facility which will process/sell all oil and gas from the field

– Water will be disposed/recycled from the same facility

– Pipeline and facility will be able to be expanded to meet all future needs including additional acreage

– 2 additional SWDs are being permitted with total capacity of 30,000 bpd

• Halcón owned power grid is being built which will handle all power requirements for the life of the field

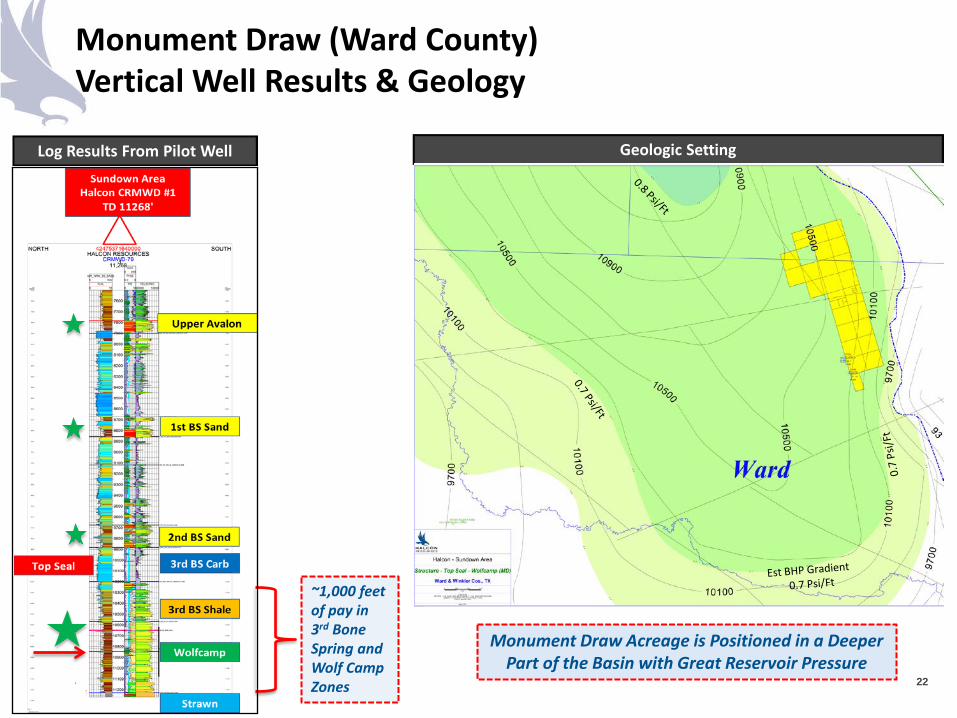

Monument Draw (Ward County) Vertical Well Results & Geology

Log Results From Pilot Well

22

~1,000 feet of pay in 3rd Bone Spring and Wolf Camp Zones

Geologic Setting

Monument Draw Acreage is Positioned in a Deeper Part of the Basin with Great Reservoir Pressure

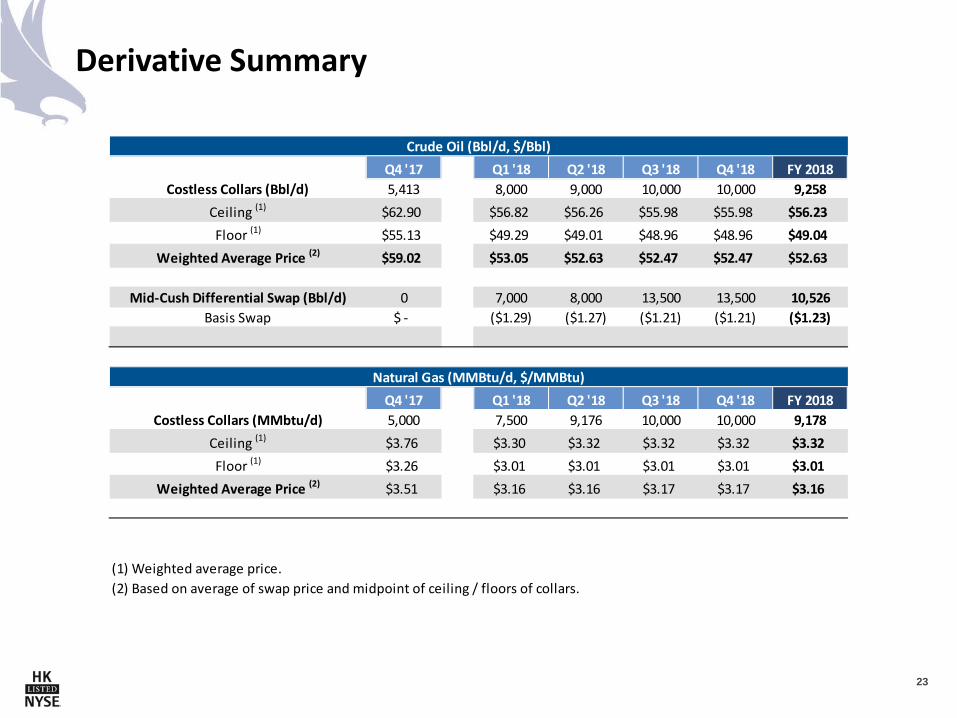

Derivative Summary

23

Crude Oil (Bbl/d, $/Bbl)Q4 '17 Q1 '18 Q2 '18 Q3 '18 Q4 '18 FY 2018

Costless Collars (Bbl/d) 5,413 8,000 9,000 10,000 10,000 9,258Ceiling (1) $62.90 $56.82 $56.26 $55.98 $55.98 $56.23Floor (1) $55.13 $49.29 $49.01 $48.96 $48.96 $49.04

Weighted Average Price (2) $59.02 $53.05 $52.63 $52.47 $52.47 $52.63

Mid-Cush Differential Swap (Bbl/d) 0 7,000 8,000 13,500 13,500 10,526Basis Swap $ - ($1.29) ($1.27) ($1.21) ($1.21) ($1.23)

Natural Gas (MMBtu/d, $/MMBtu)Q4 '17 Q1 '18 Q2 '18 Q3 '18 Q4 '18 FY 2018

Costless Collars (MMbtu/d) 5,000 7,500 9,176 10,000 10,000 9,178Ceiling (1) $3.76 $3.30 $3.32 $3.32 $3.32 $3.32Floor (1) $3.26 $3.01 $3.01 $3.01 $3.01 $3.01

Weighted Average Price (2) $3.51 $3.16 $3.16 $3.17 $3.17 $3.16

(1) Weighted average price.(2) Based on average of swap price and midpoint of ceiling / floors of collars.

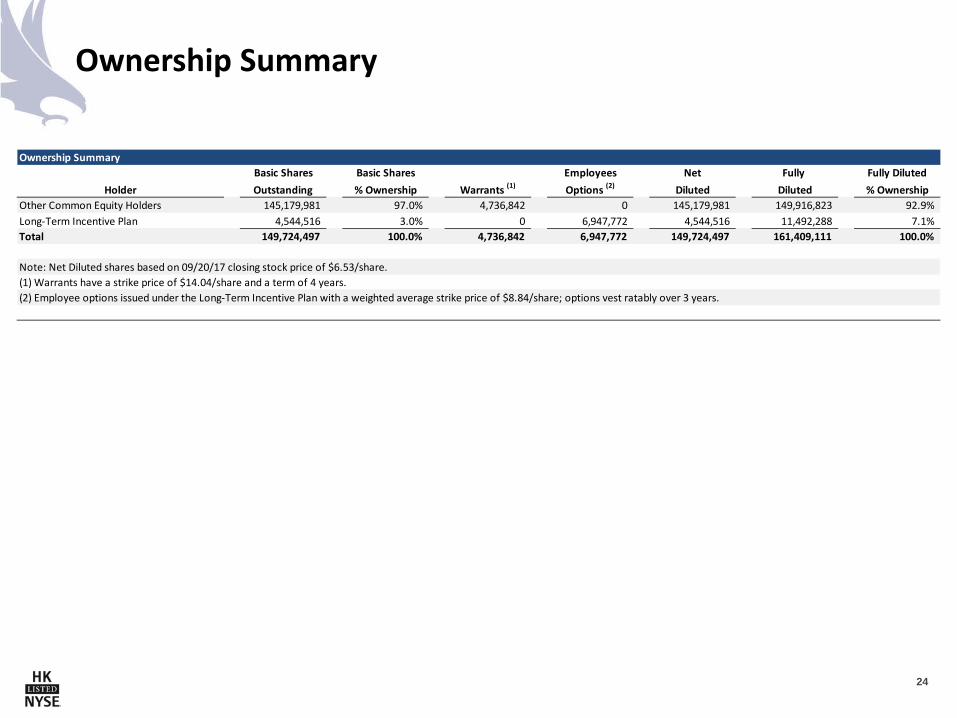

Ownership Summary

24

Ownership SummaryBasic Shares Basic Shares Employees Net Fully Fully Diluted

Holder Outstanding % Ownership Warrants (1) Options (2) Diluted Diluted % OwnershipOther Common Equity Holders 145,179,981 97.0% 4,736,842 0 145,179,981 149,916,823 92.9%Long-Term Incentive Plan 4,544,516 3.0% 0 6,947,772 4,544,516 11,492,288 7.1%Total 149,724,497 100.0% 4,736,842 6,947,772 149,724,497 161,409,111 100.0%

Note: Net Diluted shares based on 09/20/17 closing stock price of $6.53/share.(1) Warrants have a strike price of $14.04/share and a term of 4 years.(2) Employee options issued under the Long-Term Incentive Plan with a weighted average strike price of $8.84/share; options vest ratably over 3 years.

Contact Information Quentin Hicks

SVP – Finance and Investor Relations 832.538.0557