How to Lower Healthcare Costs in the Face of Healthcare Reform Uncertainty

Upload

dennis-shortCategory

view

213download

0

HEALTH INSURANCE

BASIC FACTS

Healthcare costs continue to increase Even with insurance, consumers are asked to

pay a larger amount of healthcare costs. 40% of the US citizens are uninsured One of the largest age groups uninsured is

young people b/w ages 20 – 29

MOST COMMON INJURY (MILD CONCUSSION)

Physician $186.00 Laboratory $156.00 CAT Scan $1,444.00 X-Ray $461.00 Emergency Room $359.00 Physician (Urgent Care) $186.00 Physician (Hospital) $410.00 Radiologist $282.00 Total $3,604.00

HEALTH INSURANCE HOW IT WORKS:

Law of Large Numbers (KT) Healthier Families. High Risk means no insurance or higher

premiums Pre-existing Conditions (KT)

Look at past 6 -12 months If possible conditions may not cover for a year or

more Network & Non-Network Two basic Plan of insurance

Group Plans Individual Plans

GROUP INSURANCE

Everyone in group is covered. Usually offered through work, unions,

religious organizations. Employer not required to offer Employer may pay part, or all of the

insurance premiums, or none of the insurance premiums

May cover employee but not dependents.

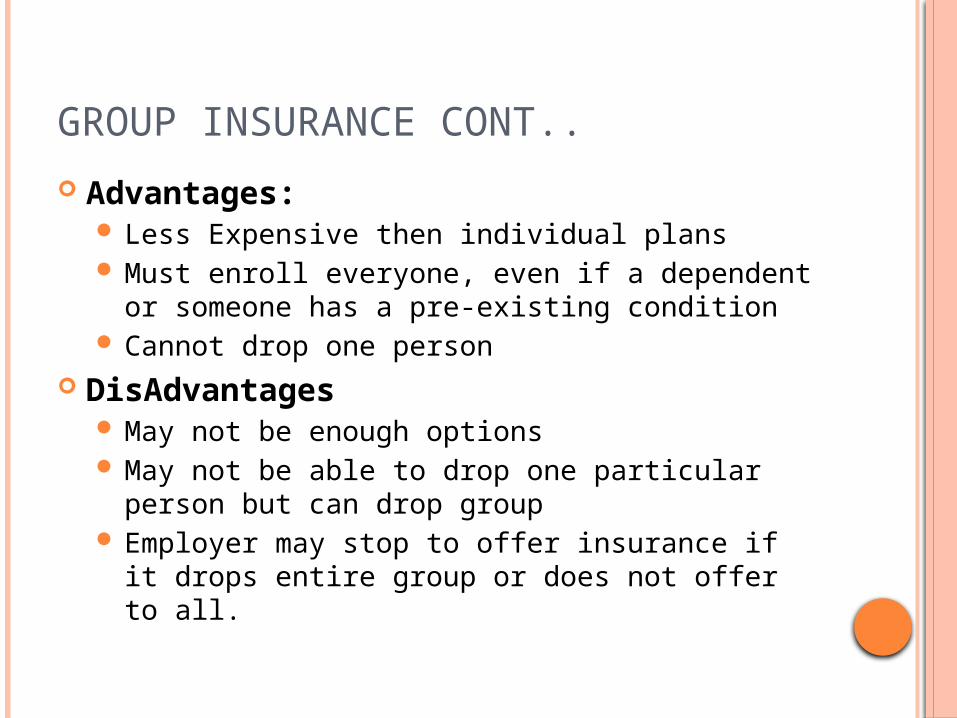

GROUP INSURANCE CONT..

Advantages: Less Expensive then individual plans Must enroll everyone, even if a dependent or

someone has a pre-existing condition Cannot drop one person

DisAdvantages May not be enough options May not be able to drop one particular person

but can drop group Employer may stop to offer insurance if it drops

entire group or does not offer to all.

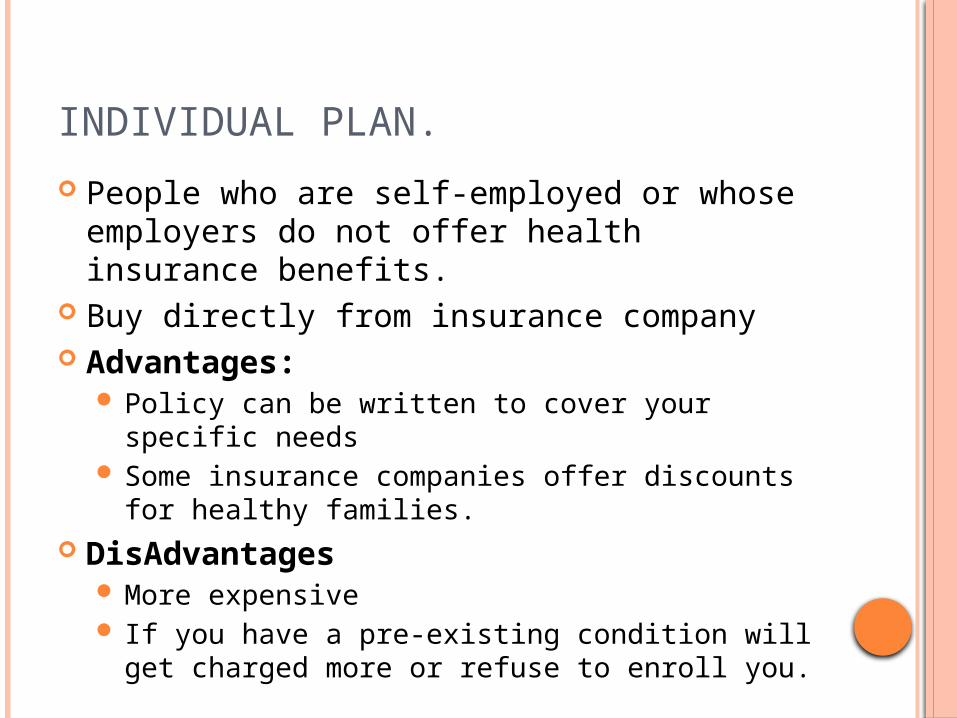

INDIVIDUAL PLAN.

People who are self-employed or whose employers do not offer health insurance benefits.

Buy directly from insurance company Advantages:

Policy can be written to cover your specific needs Some insurance companies offer discounts for

healthy families. DisAdvantages

More expensive If you have a pre-existing condition will get

charged more or refuse to enroll you.

MAKING SENSE OF IT ALL

Binding legal contract b/w the insured and insurer

You must always be truthful in your dealings, if not then can void your policy

Obama Care Obama Care Was 40-80 now 80-40 (This means before

insurance spending half, on health and more on CEO salary, Now spending more on health and less on CEO Salary

Can’t deny for finding errors Co-payments (KT): small payment at the time

of service

MAKING SENSE OF IT ALL CONT…

Co-payments (KT): small payment at the time of service

Deductible (KT): what you have to pay first then depending on insurance 20%-80%

Prescriptions $10, $20, $35 Underwriting Factors

Age, health, occupation, habits, lifestyle,

MAKING SENSE OF IT ALL CONT…

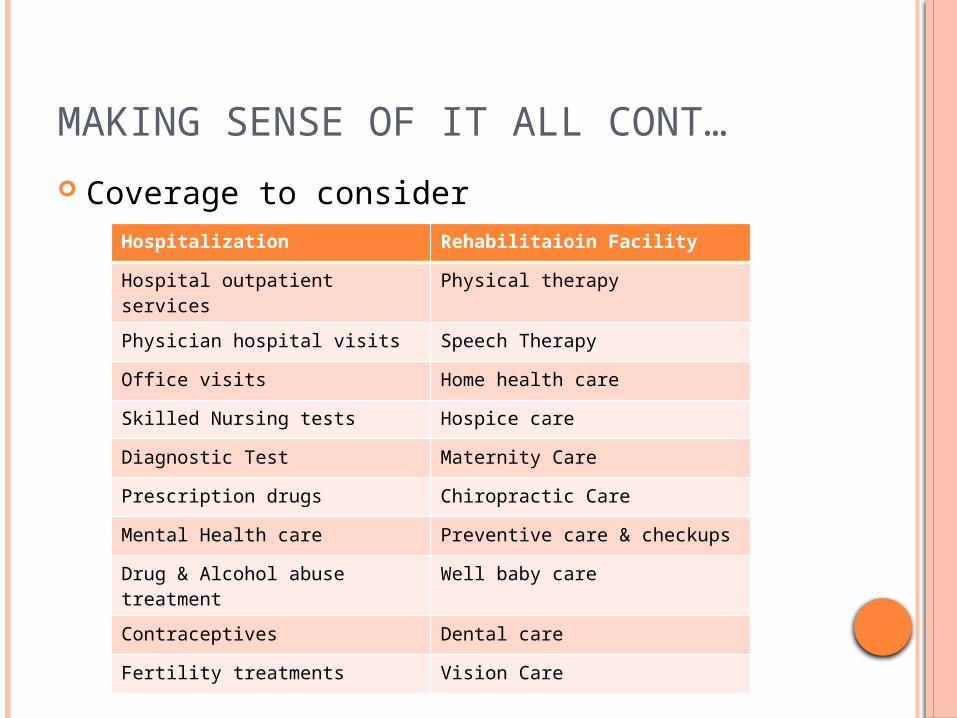

Coverage to considerHospitalization Rehabilitaioin Facility

Hospital outpatient services Physical therapy

Physician hospital visits Speech Therapy

Office visits Home health care

Skilled Nursing tests Hospice care

Diagnostic Test Maternity Care

Prescription drugs Chiropractic Care

Mental Health care Preventive care & checkups

Drug & Alcohol abuse treatment

Well baby care

Contraceptives Dental care

Fertility treatments Vision Care

MAKING SENSE OF IT ALL CONT…

Health insurance policies are usually written with a dollar maximum limits: per claim max or Lifetime limits

Per claim max (KT): max amount the insurer will pay for any single claim.

Lifetime Limits (KT): the dollar amount paid in claims over life and future.

Also sometimes limits on certain things like $150 a day for hospitalization, $250 a day for intensive care.

TYPES OF INSURANCE PLANS

Fee-for-Service Plan (FFS) Managed Care Plan Health Maintenance Organization (HMO) Preferred Provider Organization (PPO)

FEE-FOR-SERVICE PLAN (KT)

Closets thing to the traditional type of insurance Traditional: you go to doctor and you pay.

You can go to any doctor, lab, hospital, pharmacy you want and you share costs Usually 20-80 after you satisfy deductible

Most designate that it has to be reasonable and customary fee. What this means if a doctor over charges you will

have to pay more

FEE-FOR-SERVICE PLAN CONT..,

Usually they put a cap on how much you pay out of pocket in a year.

Advantage: Flexibility: you can choose any doctor, any

hospital, and so forth. Disadvantage:

Costs in premiums Cost of deductible higher And out-of-pocket payments above reasonable

and customary fee.

MANAGED CARE PLAN (KT)

Provides comprehensive medical care to members

Members pay a set premium and can receive almost all care they need through the providers

The managed care has preset physicians or providers that must be used.

The key to this type of plan is volume. Physicians can charge reduced fees because

they are guaranteed a certain number of patients.

HEALTH MAINTENANCE ORGANIZATION (HMO) (KT)

Most common type of plan Physicians are employed by HMO which is

known as primary care physician (PCP) (KT)

HMO will not pay for specialists if PCP does not recommend.

This means HMO will not pay for extra doctor visit is the PCP does not refer you to them

IF you do see someone then you pay all. Also if you do have to see someone outside

then they have to be in the Network or you pay

HEALTH MAINTENANCE ORGANIZATION (HMO) CONT…

Advantages: Low costs Covers a wide range of preventive health

improvement services Less paperwork

Disadvantages: Main disadvantage is LACK OF FLEXIBILITY Covers a wide range of preventive health If a catastrophic or rare illness members may

have difficulty receiving state of art care Exp Cancer

PREFERRED PROVIDER ORGANIZATION (PPO) (KT)

Combines HMO and FFS Physicians and other providers are listed in a

network Can visit any provider in Network and pay

small copayment No referral necessary to see specialists If out of network is seen still pays portion of

bill You have to pay up front and ask for

reimbursement PPO tend to cost more than HMO but less

than FFS plans

CONSOLIDATED OMNIBUS BUDGET REDUCTION ACT (COBRA) (KT)

Give the employees or a company with 20 or more the right to continue their group coverage for 18 to 36 months depending on circumstances If you leave your job or are terminated *** Divorced from the covered employee If you work hours are reduced below minimum

hours required Become eligible for Medicare Become disabled If employee of whom you are covered dies

CONSOLIDATED OMNIBUS BUDGET REDUCTION ACT (COBRA) CONT…

You have to pay both your premium and employers premium share if they paid

If employers stops offering insurance or goes out of business then it stops for you.

Varies from state to state

HEALTH INSURANCE PORTABILITY AND ACCOUNTABILITY ACT (HIPPA) (KT)

Applies to all group health policies no matter what size, employer-based or not

Covers individual policies sold by insurance companies or HMO’s

You take your eligibility with you if you and only if your new employer offers health insurance Moving from one job w/insurance to new job

w/insurance. Must cover any family member covered in

last plan, cannot be rejected or charged higher premiums b/c of health problems.

MEDICAID

Became law in 1963 under Social Security Act

Medical assistants for eligible individuals with low income and resources

Each state sets its own eligibility

MEDICARE

Age 65 and over Have to fill out paperwork for it. They just don’t give it to you. If you miss the

open enrollment then you don’t get benefits Plan A: free but you must pay % of hospital

bills and pay a deductible & copay Plan B: covers parts of your non-hospital

expenses. monthly premium, deductible, copayments, and small monthly premium

MEDICARE CONT…

If you don’t enroll you still pay anyway. Most insurance companies won’t pay out what Medicare would have

Medicare plan A & B does not cover everything so that is where Medigap (KT) came into play.

You have 6 months open enrollment and if you don’t get then may refuse because of high risk health conditions.