Guide to Corporate Environmental Cost Management · Publishers’ Foreword “Environmental...

47

Federal Environment Ministry Federal Environmental Agency Guide to Corporate Environmental Cost Management Berlin 2003 1

Transcript of Guide to Corporate Environmental Cost Management · Publishers’ Foreword “Environmental...

Federal Environment Ministry

Federal Environmental Agency

Guide to CorporateEnvironmental CostManagement

Berlin 2003

1

Thank you!

Special thanks go to the active members of the ex-pert support group for their critical and constructivesuggestions:

Dr. Frauke Druckrey, Verband der chemischenIndustrie e.V. • Dr. Ludwig Glatzner, BUND • PeterHerger, GUT Unternehmens- und UmweltberatungsGmbH • Prof. Stefan Schaltegger, LüneburgUniversity • Norbert Schmid, Lucent Technologies •Dr. Eberhard K. Seifert, Wuppertal Institut für Klima,Umwelt, Energie im Wissenschaftszentrum NRW •Ralph Thurm, Siemens AG • Dr. Udo Weis, ABBManagement Support GmbH • Christian Wucherer,Kunert AG

We also received valuable suggestions and informa-tion from Marion Hitzeroth, Verband der chemischenIndustrie e.V, Axel Angermann, FAZ-Institut, Dr.Christiane von Finkenstein, Volkswagen AG, RainerRauberger, Henkel KGaA, Ursula Lauber and HeinrichSpies, Federal Statistical Office, and Marcus Wagner,Lüneburg University. We should like to express ourthanks for this support as well.

Published byFederal Ministry for the Environment,Nature Conservation and Nuclear Safety (BMU)PO Box 12 06 29 53175 BonnPhone: +49 1888/305-0Fax: +49 1888/305-20 44e-mail: [email protected]

Federal Environmental Agency (UBA)PO Box 33 00 2214191 BerlinPhone: +49 30/8903-0 Fax: +49 30/8903-22 85www.umweltbundesamt.de

The publishers accept no liability for the correctness,accuracy or completeness of the information, nor forany failure to observe private third-party rights. Theopinions expressed in the publication are not neces-sarily those of the publisher.

Graphics and LayoutGary Smitka, Michael Miethe, Berlin

TranslationTerence Oliver, Winsen (Luhe)

Project workersThomas Loew, (Project Manager)Institut für ökologische Wirtschaftsforschung(IÖW) gGmbHPotsdamer Str. 105, D-10785 BerlinPhone: +49 30/884 59 4-0Fax: +49 30/882 54 39e-mail: [email protected]

Dr. Uta Müller, Dr. Markus Strobel, Institut für Management und Umwelt (IMU), GmbHGratzmüller Str. 3, 86150 AugsburgPhone: +49 8121/343 66-0Fax: +49 8121/343 66-39e-mail: [email protected]

Dr. Klaus FichterBorderstep – Institut für Innovations- undNachhaltigkeits-ForschungPO Box 37 02 2814132 BerlinPhone: +49 30/342 31 04Fax: +49 30/30 10 85 55e-mail: [email protected]

Project participantsAs part of the preliminary work on this Guide, anexpertise on the inclusion of external environmentalcosts was prepared by:

Prof. Dr. Werner F. Schulz,Deutsches Kompetenzzentrum für Nachhaltiges Wirt-schaften an der Universität Witten-Herdecke (DKNW)

Martin Kreeb, Hohenheim University

Dr. Peter Letmathe, Ruhr-University Bochum

Project contact / ClientPeter Franz, Stefan Besser, Federal Environment Ministry, G I 2 ([email protected],[email protected])

Andreas Lorenz, Federal Environmental Agency,I 2.2 ([email protected])

Obtainable fromThe Guide to Corporate Environmental CostManagement is obtainable free of charge from theFederal Environmental Agency (UBA), ZentralerAntwortdienst (ZAD), PO Box 33 00 22, 14191 Berlin,Phone: +49 30/8903-0, Fax: +49 30/8903-29 12.

© 2003 BMU/UBA, Berlin

Imprint

2

Publishers’ Foreword

“Environmental protection can cut costs” – in 1996 those were the first words of the foreword by the FederalEnvironment Ministry and the Federal Environmental Agency to the “Manual of Environmental Cost Accounting”.When companies make use of our natural environment, this gives rise to costs. If these can be reduced, it also reducesthe burdens on the environment and at the same time helps to ensure the competitive strength of the companies inthe long term.At that time the focus was still on the costs of corporate environmental protection. The intention was to allocatethese costs to the cost centres and cost units that caused them, in order to obtain a transparent picture of how envi-ronment-related costs originate. The aim was efficient design of corporate environmental protection.

The situation has moved on since then. The growing importance of integrated environmental protection meas-ures has created a need for new rules for differentiating corporate environmental protection expenditure. Therehave also been considerable developments in material and energy flow related approaches such as flow costaccounting. This is focusing more attention on those costs that can be reduced not by lower-cost environmen-tal protection measures, but by improving efficiency in the input of resources. The objective here is more cost-conscious and more environment-conscious management of the entire production chain. This is also reflectedin the new title “Environmental Cost Management”. Environmental relief effects result from reduced resourceinputs and reduced waste outputs.

At the same time expectations – some of them unrealistic – about the size of the potential savings have beenbrought down to earth. No doubt there will always be examples of major savings coupled with very short paybackperiods for the necessary investments. As production becomes increasingly eco-efficient, however, spectacularsavings will tend to become the exception. The success of environmental cost management is rather a matter ofpermanent optimisation of details. At the interface between corporate environmental protection and entre-preneurial profitability objectives, environmental cost accounting has proved its value many times.From an environmental policy point of view, the significance of environmental cost management lies primarilyin the way it systematically brings to light potential for environmental relief within companies. It exploits theentrepreneur’s self-interest in reducing costs to maintain a high standard of environmental protection and helpsgive effect to the “polluter pays” principle. The publishers therefore take the view that environmental cost man-agement can make an important contribution to achieving sustainability in economic activity.This Guide is intended for practitioners in companies. It is intended not only for environmental experts, butabove all for the responsible persons in accounting and controlling departments and for company management.The aim is to familiarise them with the methodological approaches of environmental cost management in rela-tion to specific business tasks – investment planning, use of environmental protection technology, productioncontrol, environmental reporting – and help them with the selection of suitable approaches.The publishers wish to thank the institutes responsible for preparing the Guide – the Institute for Ecological EconomyResearch (IÖW), Berlin, the Institute for Management and Environment (IMU), Augsburg, and Borderstep – Institutefor Sustainability Research, Berlin – and also the members of the expert support group and all others who in thecourse of the project have contributed to its success. We hope the Guide to Environmental Cost Management willbe widely accepted and used in the business world.

Federal Environment Ministry and Federal Environmental Agency

Table of Contents

PUBLISHERS’ FOREWORD . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3

TABLE OF CONTENTS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5

1 ENVIRONMENTAL COST MANAGEMENT: COMBINING

COST-EFFECTIVENESS AND ENVIRONMENTAL PROTECTION . . . . . . . . . . . . . . . . 6

2 COST-EFFECTIVE PLANNING AND IMPLEMENTATION OF

ENVIRONMENTAL PROTECTION MEASURES . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10

2.1 Special features of environmental protection investments . . . . . . . . . . . . . . . 10

2.2 Procedure . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10

2.3 Benefits . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

3 ENVIRONMENTAL STATISTICS AND MONITORING

ENVIRONMENTAL PROTECTION COSTS . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14

3.1 Focus of statistics . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14

3.2 Procedure . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15

3.3 Benefits and limits . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16

3.4 Environmental protection costs in voluntary reporting . . . . . . . . . . . . . . . . . . 18

4 ECO-EFFICIENT CONTROL OF MATERIAL AND ENERGY FLOWS . . . . . . . . . . . . 20

4.1 Objective of flow cost accounting . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20

4.2 Concept and forms of flow cost accounting . . . . . . . . . . . . . . . . . . . . . . . . . . 22

4.3 Procedure for integrating flow cost accounting . . . . . . . . . . . . . . . . . . . . . . . . 27

4.4 Cost management and organisational development . . . . . . . . . . . . . . . . . . . . 29

4.5 Benefits . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 30

5 IDENTIFYING AND IMPLEMENTING ECO-EFFICIENT INVESTMENTS . . . . . . . . . . 32

5.1 Optimising conventional investment calculations . . . . . . . . . . . . . . . . . . . . . . 32

5.2 Procedure . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 32

5.3 Benefits . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 37

6 BUSINESS CALCULATIONS WITH EXTERNAL COSTS? . . . . . . . . . . . . . . . . . . . . . 38

6.1 Significance of external costs . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 38

6.2 Decisions with binding effects in the future . . . . . . . . . . . . . . . . . . . . . . . . . . 39

6.3 Public relations work with external costs . . . . . . . . . . . . . . . . . . . . . . . . . . . . 40

6.4 Typical questions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 40

7 GLOSSARY . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 42

8 BIBLIOGRAPHY . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 46

5

Environmental cost management: combining cost-effectiveness and environmental protection

Fig. 1: Key environmental policy areas and environmental cost accounting concepts

2000

Environmental focus of corporate measures Environmental cost accounting concepts

Dev

elop

men

t of

env

iron

men

tal

cost

acc

ount

ing

Sustainable economic activity:Strategic control of

environmental protection performance (product,

innovation, investment policy)

Eco-efficiency: Operational control of environmental protection performance

by means of plant and inter-plant management of substance streams

Environmental management systems: Embedding environmental protection in organisation throughaudits, environmental controlling, environmental

management systems (EMAS, ISO 14001)

Production-integrated environmental protection:Use of plant-integrated and process-integrated

environmental protection technologies

Emission reduction: Use of end-of-pipe technologies

• Flow cost accounting for prod-uct innovations, investments,site selection

• Determining and takingaccount of external costs

• Flow cost accounting for pro-duction, product and packag-ing optimisation

• Residues cost accounting

• Input/output cost indicators:energy costs, waste costs etc.

• Environmental protection costs:costs of additive and integrat-ed environmental measuresand environmental charges(VDI 3800, Version 2001)

• Costs of emission reduction:costs of additive environmentalprotection measures(Environmental Statistics Act,VDI 3800, Version 1979)

Since the 1970s, numerous corporate environmentalcost accounting concepts have been developed for avariety of purposes and decision situations. The devel-opment of environmental cost management has gonehand in hand with shifts of emphasis on different issuesin environmental policy and focuses in corporateenvironmental management. In the 1970s, for exam-ple, environmental policy and corporate environ-mental protection measures centred round emissionreduction. It was against this background that in1979 the German Engineers’ Association (VDI) pub-

lished VDI Guideline 3800 “Determining the cost ofemission reduction systems and measures”. Today,by contrast, the debate revolves around questions ofeco-efficient steering of entire product life-cycle chainsand strategic issues concerning sustainable businessactivity. To support such endeavours, a good deal hasbeen done in recent years to develop and improveapproaches to environment-oriented cost accounting.The development of key environmental policy areas andenvironmental cost accounting concepts is illustratedin Fig. 1.

1Environmental cost management

6

Fig. 2: Benefits of environmental cost management

Benefits of environmental cost management

Eco-EfficiencyReducing costs and environmental

burdens by means of material-efficient and/or energy-efficientprocesses, systems and products

Flow cost management (FCM) Eco-efficient control of materialand energy flows• Linking substance and energy

balances with material purchasecosts and disposal costs (entryvariant of FCM)

• Residues cost accounting: focuson material/disposal costs

• Comprehensive FCM on the basisof Enterprise Resource Planning(ERP) systems

� Guide Chapter 4

Improving investment decisionsand resource efficiency• Investment calculations based on

material and energy flows

� Guide Chapter 5

Compliance EfficiencyCost-effective implementationof environmental protectionprovisions and self-imposed

environmental objectives

Cost-effective planning andimplementation of environ-mental protection investments• VDI Guideline 3800• Systematic comparison of

alternatives

� Guide Chapter 2

Recording and communicatingenvironmental protectionexpenditure• VDI Guideline 3800• Environmental Statistics Act• Voluntary environmental

reporting

� Guide Chapter 3

Strategy SafeguardsInvestigating economic/ecological

risks of long-term investmentprojects.

Presenting special environmentalprotection achievements

Safeguarding investmentdecisions• Taking account of external

environmental costs that couldbecome internal costs duringthe planning period as a resultof stricter legislation

� Guide Chapter 6

Eco-pioneers: Improving market positioningand image• Presenting successes by draw-

ing attention to external costsprevented

� Guide Chapter 6

Environmental cost management performs three cen-

tral functions:

• It supports environmental protection by helping toensure cost-effective implementation of environ-mental provisions or self-imposed environmentalobjectives (compliance efficiency)

• It promotes “win-win solutions” by supporting thesearch for eco-efficient processes and products andthereby linking cost reduction with savings inresources (eco-efficiency)

• It helps safeguard corporate strategies by helping toidentify and take account of investment-relevant envi-ronmental costs and supporting the marketing ofenvironmentally sound products

Not every cost accounting approach is equally suit-able for these tasks. This brochure is intended to helpcompany management, controllers and environmentalmanagers to find the approach that is appropriate totheir purposes and their business situation. Fig. 2 showsthe uses to which the successive approaches of envi-ronmental cost management can be put.

This Guide is structured in terms of the tasks that canbe supported effectively by means of environmentalcost management, and provides an introductoryoverview of the approaches suitable for such calcula-tions. For each method it outlines the basic idea, theprocedures and the expenditure and benefits. Sincethe brochure is primarily intended to provide a rapid

overview of the various approaches and assist in select-ing a suitable strategy, it does not go into any greatdetail, but lists further sources of information in theindividual chapters.

Table 1 supplements Fig. 2 by giving a summary ofthe practical business issues where environmentalcost management can be of assistance and indicatingthe benefits that can be achieved in each case.

The environmental cost accounting approaches set outin this Guide not only differ in the business purposesfor which they are used, but to some extent focus ondifferent costs. It is basically possible to distinguishthree different ways of looking at costs:

• Environmental protection costs: these are costs for envi-ronmental protection systems and for the measuresdesigned to prevent, reduce, eliminate, monitor ordocument adverse environmental impacts.

• Material and energy flow costs comprise all thosecosts which are associated with the purchase, use anddisposal of material and energy.

• External costs of business activities: these are envi-ronmental costs that are borne not by the compa-ny that causes them, but by the parties affected bythem (e.g. neighbours) or by society as a whole.

Each of these cost focuses offers different businessopportunities: the focus on environmental protectioncosts serves to ensure cost-effective planning and

Environmental protectioncosts, flow costs – for theseand other definitions see the Glossary.

7

Basic questions

1. Environmental protection investments:How can I find the lowest-cost invest-ment alternative?

2. Environmental statistics:How can I satisfy the reporting require-ments of the Environmental Statistics Act in a way that benefits the company?

3. Voluntary environmental reporting:How can I improve the company’s credi-bility and image in the eyes of the targetgroups by presenting environmental pro-tection expenditure in environmentalreports or environmental statements?

4. Material and energy balances:How can I use the data from material and energy balances for cost manage-ment and cost reduction purposes?

5. Large quantities of waste:How can I make further reductions inwaste quantities and residues costs?

6. Reducing material costs:How can I reduce material costs forproduction locations with complexproduction structures and a multiplicity of internal materials movements?

7. New and replacement investments:How can I improve investment decisionsand resource efficiency?

8. New business fields:How can I ensure even better safe-guards for decisions on long-term in-vestments in new business fields orinnovative product segments?

9. Eco-pioneers:How can I make customers and the public aware of the benefits to society ofthe company’s environmental protectionefforts?

What is thebusiness benefit?

VDI 3800 offers clearly structuredinstructions for recording all expenditureassociated with an environmental pro-tection investment and makes it possibleto compare various investment options.

VDI 3800 helps with the calculation ofinvestment expenditure and with dis-tinguishing integrated environmentalprotection measures. Creating environ-mental protection cost centres permitsbetter control of the costs arising thereand allows cost comparisons betweendifferent systems (benchmarking).

Compliance with reporting principlescreates transparency, makes it easier tointerpret the information and therebyenhances credibility in the eyes of thetarget groups.

Short-term improvements and costreductions can be achieved at low coston the basis of existing data.

Creates good transparency of internalmaterial flows and of the factors thatcause and increase material losses, andusually offers a cost reduction potentialin the region of 1 - 2% of productioncosts.

Detects and deals with inconsistentmaterial data in ERP systems. IT andorganisational integration brings sub-stantial improvements in efficiency(reductions in material losses and inquantities of materials used in productsand packaging etc.).

Systematic consideration of investment-relevant material flows improves thedata and information basis for invest-ment decisions and thereby increasesprofitability.

For many sectors (energy, transport etc.)scientific studies have already yieldedreliable data on external costs that canbe used in an investment planning con-text.

Eco-pioneers, e.g. in the construction,energy supply or food sectors, can usetheir marketing and PR activities toshow in monetary terms the extent towhich they prevent environmentaldamage by means of their products and production processes.

Which approach ismost helpful here?

VDI Guideline 3800 "Determining the cost of corporate environmental protection measures"(Guide Chapter 2)

Information from Federal StatisticalOffice and VDI Guideline 3800.Another recommendation, for cost-relevant systems that are used solely for environmental protection purposes,is to set up a separate cost centre(Guide Chapter 3)

Principles for voluntary reporting onenvironmental protection costs (Guide Chapter 3.4)

Linking material and energy balanceswith material purchase and disposalcosts (entry variant of flow costaccounting) (Guide Chapter 4, especially p. 27 ff.)

Flow cost accounting with focus onmaterial and disposal costs (residues cost accounting (Guide Chapter 4, especially p. 27 ff.)

Comprehensive flow cost accounting on the basis of Enterprise ResourcePlanning (ERP) systems (Guide Chapter 4)

Investment calculations based on material and energy flows(Guide Chapter 5)

Taking account of external environ-mental costs that might become internalcosts during the planning period as aresult of stricter legislation etc.(Guide Chapter 6)

Publicising avoidance of external costs(Guide Chapter 6)

Table 1: Navigating through environmental cost management: When does which approach help?

implementation of statutory environmental protectionrequirements or of self-imposed environmental objec-tives of industrial associations and individual compa-nies. Recording and steering of material and energyflow costs helps to reduce or avoid costs by means ofmaterial-efficient processes, systems or products. Here

cost reduction and eco-efficiency are combined in awin-win strategy. In individual cases it may also makebusiness sense to consider external costs, for exam-ple if external costs become internal costs within aplanning period as a result of public charges, liabilityprovisions or official conditions, or if a company sells

When does which approachhelp?

8

Fig. 3: Environmental cost accounting as part of the management cycle

9

Opinions from industry andthe Federal EnvironmentalAgency

environmentally sound products that make it possi-ble to avoid external costs.

Environmental cost accounting as a player in the

“orchestra” of management instruments

The special potential of environment-related costand investment accounting methods lies in the factthat it links physical and monetary parameters. Aspectsof environmental relevance can be expressed in mon-etary units and translated into a “business language”.In this way environmental cost accounting can sup-port the controlling functions and serve as a usefulsupplement to other instruments of environmentalmanagement such as audits, eco-balances or envi-ronmental indicators. Thus environmental costaccounting is not to be regarded as an isolated “tool”,but as an indispensable player in the “orchestra” ofthe various management instruments.

The following chapters set out to indicate the purposesfor which the strategies of environmental cost account-ing can offer “added value” compared with otherinstruments, and how they can be used to combinecost-effectiveness with environmental protection.

Define cost orenvironmental

objectives

Performance controland correction

Determine costs(environmental cost accounting)

Evaluate anddistribute results

Implementmeasures

Devisecost-reducing and/or

cost-effective measures orinvestment alternatives

Environmental costmanagement

“Anyone who regards statutory reporting on environmental

protection expenditure as no more than a tedious duty hardly

does justice to the opportunities it offers. Given appropriate

preparation of the data, merely looking at the expenditure

side is in itself often enough to reveal relief effects that have

been achieved in the course of time thanks to integrated and

more efficient environmental protection solutions. And these

improvements have created scope for further measures.

Analysing and monitoring environmental protection expenditure

is only a first building block in the edifice of environmental cost

management, however. Especially in the case of material-

intensive and energy-intensive production operations, it makes

sense to employ further environmental cost management

techniques to take account of the cost behaviour of material

flows. In most cases it is advisable to integrate this in the

corporate cost accounting system in order to minimise the

work involved in recording and managing the data.”

Ralph Thurm, Corporate Environmental

Protection Division, Siemens AG

“Companies that stay successful in the long term are

environmentally aware companies. Determining external

costs helps the company to see the environmental burdens

it causes in relation to its economic success. This enables

it to identify long-term financial risks at an early stage

and avoid them. External costs can also be used as a

marketing argument: falling external costs are evidence

of a company’s environmental protection endeavours.“

Prof. Andreas Troge, President, Federal Environmental Agency

“The introduction of flow cost accounting in Sortimo has

led to a marked improvement in material flow transparency

and data quality. This puts us in a position to systematically

cut material costs and reduce environmental burdens.

We also expect a pay-off in the form of optimised materials

management and improved production planning”

Andreas Manntz, Commercial Director,

Sortimo International GmbH (Zusmarshausen)

Now that sewage works and air quality control sys-tems have been installed throughout Germany overthe past three decades, the need for investment insuch end-of-pipe environmental protection systemsis a much less frequent occurrence than it used to be.Nevertheless, there will always be situations in whicha new environmental protection system becomesnecessary.

2.1 Special features ofenvironmental protection investments

If there are several alternative options for an invest-ment decision, investment calculations support theeconomic approach in the decision-making process.In conventional investments such as new productionfacilities, the investment calculation sets expenditureagainst expected revenue in order to compare alter-natives on the basis of internal discounting rates orpayback periods. Chapter 5 shows how the decisionprocess can be improved for conventional investmentsof this kind.Unlike conventional investments, however, end-of-pipe environmental protection systems do not usual-ly generate any revenue or produce any relevant costreductions. For measures of this kind, which result inhigher costs, only the size of the investment and theregular annual expenditure is determined. On this basisit is possible to calculate the cost per environmentalburden avoided, in other words the efficiency of thefunds spent. This procedure is in line with the revisedVDI Guideline 3800 “Determination of costs for indus-trial environmental protection measures”. The Guide-

line is concerned on the one hand with identifyingand distinguishing regular environmental protectionexpenditure, and on the other with preparing invest-ment calculations for environmental protection meas-ures.

2.2 Procedure

The calculation described in the VDI Guideline can beused where there is a need for a technological envi-ronmental protection measure. The aim may be tocomply with official environmental requirements or

This chapter indicates ways of systematically comparing available options for investment in environmental

protection systems to ensure reliable identification of the least expensive and most efficient solutions.

Cost-effective planning and implementationof environmental protection measures

Planning environmental protection measures

10

2

Fig. 4: Steps in selecting low-cost environmental protectionmeasures

Ermittlung und technische Beschreibungvon Lösungsalternativen

Ausgangssituation: Umweltschutzziel erfordert technische Umweltschutzmaßnahmen

Initial situation: environmental protection objective calls for technical environmental protection measures

Ermittlung der InvestitionshöheErmittlung der jährlichen laufenden Aufwendungen

Ermittlung von Kennzahlen(Siehe Beispiel Kläranlage)

Determining size of investmentDetermining regular annual expenditure

Determining indicators(see example: sewage plant)

Vergleich der LösungsalternativenEntscheidungsfindung

Comparison of alternative solutionsInvestment decision

UmsetzungImplementation

kontinuierliche KostenüberwachungAusweis der UmweltschutzkostenContinuous monitoring of costs

Statement of environmental protection costs

Identification and technical description ofalternative solutions

to meet a self-imposed environmental objective set,for example, in the context of an EMAS or ISO 14001environmental management system. It therefore con-siders investment projects for sewage plants, air filtersystems, catalytic converters, waste management sys-tems, or plant-integrated environmental protectionmeasures.

In the ideal case there are various possible solutionswhich are drawn up in preparation for the decision.To be able to compare them properly later, it is firstnecessary to describe their consumption data (oper-ating supplies including energy) and their performancedata (e.g. filter capacity).

Determining the size of the investment

The size of the investment is then determined foreach alternative solution. An investment in an end-of-pipe environmental protection solution comprisesall expenditure from planning to commissioning. Aswell as the cost of acquisition there are a number ofother items to be taken into account, e.g. delivery,measuring equipment or training courses. An overviewof such items can be found in the checklist “Additionalcosts of environmental protection systems”.

Determining regular expenditure

The operation of an environmental protection systemgives rise to various kinds of regular expenditure, whichare determined on an annual basis. The main cate-gories are:

• Expenditure arising from the investment. This kindof expenditure arises independently of the actualoperation of the system. It includes depreciation,interest, insurance premiums, impersonal taxes, ashare of administrative costs, expected maintenanceand repair costs.

• Operation-related expenditure. This essentially com-prises expenditure on operating supplies consumed(including energy) and on personnel. The quantitieslikely to be consumed can be worked out from theplanned utilisation of the system.

In addition, follow-up expenditure may be incurred ifthe investment project gives rise to alterations in theproduction processes themselves (e.g. changes inefficiency). In some cases fees or services, e.g. for wastedisposal and emission measurements, or even revenuefrom the sale of recycling materials, may be an aspectof relevance to the decision; these can be subsumedunder “Other income and expenditure”. The regular expenditure is calculated by determiningand totalling the expected annual figures for all theindividual items.

Indicators and selection decision

As a rule, different alternative solutions involve notonly different costs, but also different benefits. Thebenefit of environmental protection systems usuallyconsists in the prevention of emissions. To permit abetter comparison of the relationship between costsand benefits, it is therefore necessary to compile notonly the costs of the various systems, but also thesum of the emissions they prevent. These figures canbe used to arrive at two indicators for each alternativesolution, namely the amount of capital invested peremission unit prevented, and the level of regular costsper emission unit prevented.Once the calculation procedure described here (seealso the example of an “Industrial wastewater treat-ment plant” on page 13) has been carried out for

VDI Guideline 3800 – help with investment decisions

11

Checklist“Additional costs of environmental protection systems”

The following cost items may arise in addition to theactual purchase price when installing an environmentalprotection system:

• Site acquisition (including property transfer tax, anydemolition costs,…)

• Buildings (foundations, site development, rehabilita-tion,...)

• Delivery (including instrumentation and control sys-tems, freight, packing, insurance)

• Assembly (including assembly insurance and commis-sioning)

• Peripheral equipment (e.g. pipework, conveyor sys-tems)

• Painting, insulation• Energy supply and other supply facilities• Sewers, roads, railways, amenity rooms• Additional investments (transport facilities,building

site facilities,...)• Raw materials store (including increases in current

assets, e.g. due to minimum stocks necessary forensuring long-term operation)

• Spare parts store• Startup costs for system or parts thereof• Measuring equipment for emission and immission

measurements (air, water, soil)• Interest until commissioning (e.g. interest on building

finance)• Engineering and consulting (including expenditure on

own planning work)• Customs duty• Licences• Cost of approval procedures (including any expert

opinions obtained)• Instruction and training of personnel needed to oper-

ate the system

If environmental protection systems are subsequentlyinstalled in existing production processes, such integrationmay give rise to additional capital expenditure and regularexpenditure. To make it possible to compare costs for iden-tical or similar systems within the company or within theindustry, such integration investments should be recordedand shown separately.

Source: VDI 3800

Bibliography

Verein Deutscher Ingenieure (publ.): VDI Richtlinie 3800, Determination of costs for industrial environmentalprotection measures, Berlin 2001

Bundesumweltministerium, Umweltbundesamt (publ.): A guide to corporate environmental indicators, Bonn, Berlin1997

12

each alternative solution, the figures for capital expen-diture, regular expenditure, emissions avoided and thecost-benefit indicators are known. As a rule thesefigures constitute the essential core information forthe selection decision that now has to be taken.

2.3 Benefits

The investment calculation described in the VDI Guide-line has several advantages to offer. For example, theGuideline makes for the use of a standardised proce-dure within the company and, with its detailed check-lists, ensures timely inclusion of all costs incurred. Atthe same time it ensures the compatibility of the invest-ment calculation with the Environmental Statistics Act.This has the advantage that cost monitoring is basedon the cost categories that have to be used for envi-ronmental statistics. The figures from cost control

can thus be used directly for the purpose of Environ-mental Statistics.

If modifications to cost accounting are made when thesystem goes into service, the environmental statisticsshould also be taken into account. As explained inChapter 3, it is advisable to create a separate costcenter or at least a separate cost location for the newenvironmental protection system. This not only per-mits better monitoring of regular costs, but also sim-plifies the preparation of statistical returns.

Table 2: Comparison of investment alternatives

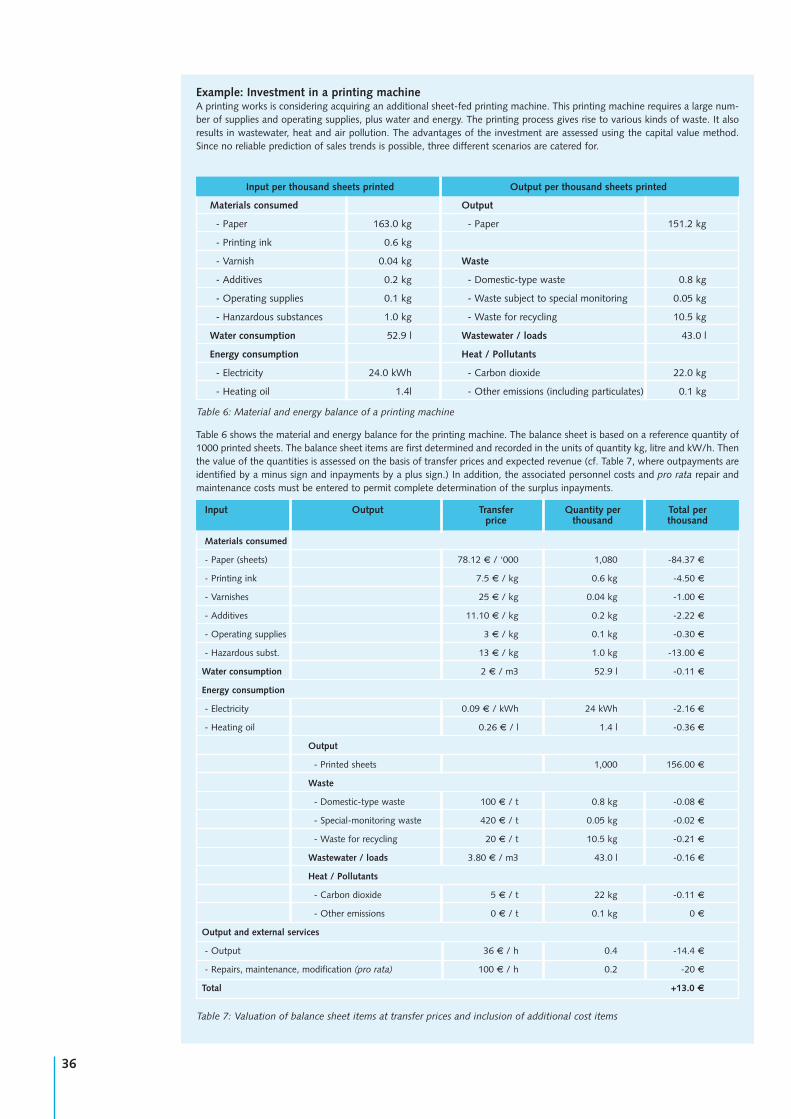

Example: Industrial wastewater treatment plantA new treatment plant is needed to clean the wastewater from a planned paint shop. The usual treatment stages – neutralisa-tion, sedimentation and filtration – are to be used to remove heavy metals, in particular sizeable quantities of zinc and nickel,from the wastewater. The wastewater treatment plant, which can remove up to 10 tonnes of heavy metals a year, is assumedto have an operating life of 25 years and an average utilisation of 90%. The example shows how the relevant expenditure andindicators can be calculated in accordance with VDI 3800.

Fig. 5: Determining expenditure and indicators for environmental protection investments in accordance with VDI 3800

Plant type

Plant A

Plant B

Comparisonof plants

Emissionsavoided p.a.

9,000 kg

9,000 kg

same

Purchase price[ thousand E ]

1500

2200

+700

Total investmentincl. ancillaries[ thousand E ]

4000

4700

+700

Regularexpend. p.a.

[ thousand E ]

805

730

-75

Specificinvestment[ E / kg ]

17.78

20.89

+3.11

Specificregular

expenditure[ E / kg ]

89.44

81.11

-8.33

In addition to the treatment plant considered above costing D1.5 million, an alternative offer, plant B, was also investigated.Plant B has a more modern process management system and various ancillary units that reduce personnel costs and consump-tion of operating supplies. As a result, capital expenditure increases to D2.2 million and regular annual expenditure decreasesto D730,000 (see Table 2). A comparison of the figures for the two plants reveals that the higher initial expenditure is offset bythe lower regular expenditure. Interest effects are taken into account by applying statistical interest when determining regularexpenditure.

Specific capital expenditure [ D / kg ]- in relation to the emissions avoided- in relation to the products manufactured

Example:17.78 J/kg(= capital expenditure per kg heavy metal avoided)

Specific regular expenditure [ D / kg ]- in relation to the emissions avoided- in relation to the product volume manufactured

Example:89.45 J/kg(= regular expenditure per kg heavy metal avoided)

Technical environ-mental protection

capacity

- Technical perform-ance data

- Planned produc-tion quantity

- Planned technicalutilisation

- Lifetime

Example:Lifetime oftreatment plant25 yearsMax. capacity10 t p.a.Planned capacity9 t p.a.

Emissionsavoided [t, kg]Example: 9 theavy metals p.a.

Capital expenditure[ TD = D’000 ]

- Main components- Ancillary components- Assembly- Sites- Buildings- Engineering and own

planning- Building finance interest- Licences

Example:Plant 1,500 TJAssembly 100 TJBuildings 2,000 TJPlanning 400 TJ

Total investment [ Tg ]Example: 4,000 TJ

Regular expenditure[ D / year ]

Expenditure due to size of invest-ment:- Interest- Depreciation- Insurance- Administration- Maintenance and repairs

Example:Depreciation 160 TJ(25 years)Maintenance 75 TJ(5% of plant costs)Interest 120 TJ

Operation-related expenditure- Operating supplies- Personnel

Example:Operating supplies 200 TJPersonnel 250 TJ

Follow-up expenditure

Other expenditure

Total regular expenditure[ TD / year ]Example: 805 TJ

Model calculationin accordance withVDI Guideline 3800

13

This chapter shows how to determine environmental protection costs for statistical returns in such a way

that they can also be used for improved cost control of environmental protection systems.

Environmental statistics and monitoring of environmental protection costs

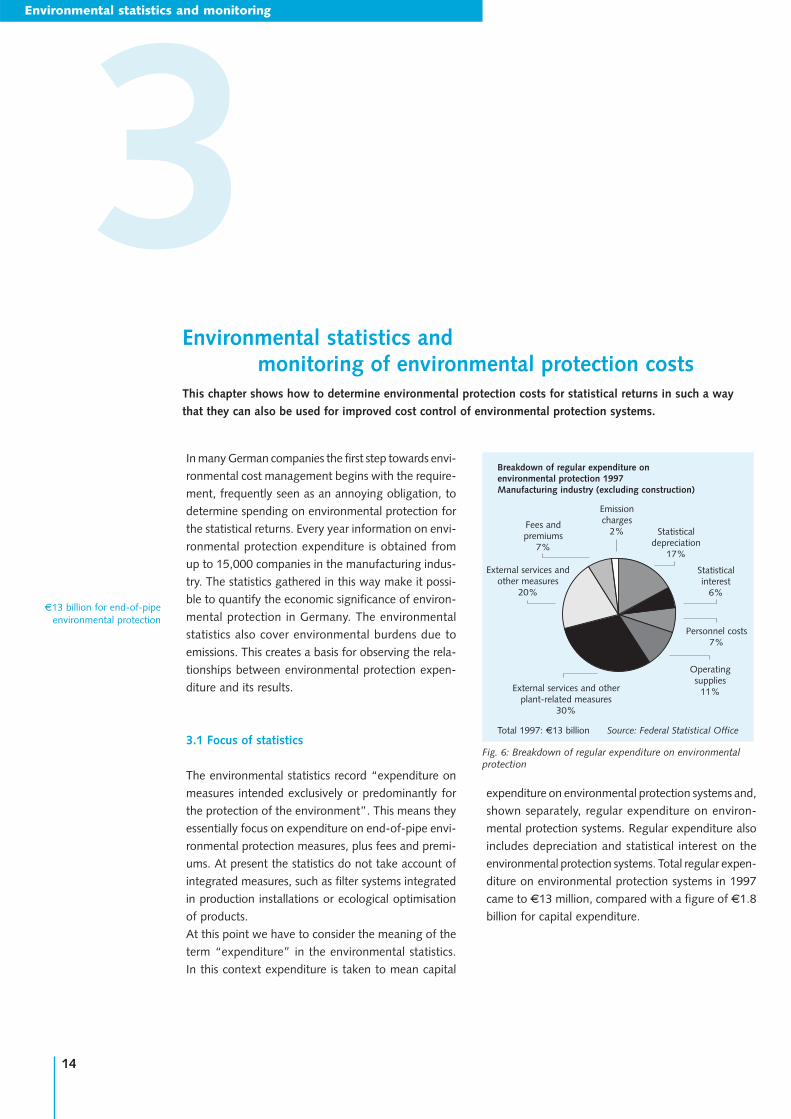

3D13 billion for end-of-pipe

environmental protection

In many German companies the first step towards envi-ronmental cost management begins with the require-ment, frequently seen as an annoying obligation, todetermine spending on environmental protection forthe statistical returns. Every year information on envi-ronmental protection expenditure is obtained fromup to 15,000 companies in the manufacturing indus-try. The statistics gathered in this way make it possi-ble to quantify the economic significance of environ-mental protection in Germany. The environmentalstatistics also cover environmental burdens due toemissions. This creates a basis for observing the rela-tionships between environmental protection expen-diture and its results.

3.1 Focus of statistics

The environmental statistics record “expenditure onmeasures intended exclusively or predominantly forthe protection of the environment”. This means theyessentially focus on expenditure on end-of-pipe envi-ronmental protection measures, plus fees and premi-ums. At present the statistics do not take account ofintegrated measures, such as filter systems integratedin production installations or ecological optimisationof products. At this point we have to consider the meaning of theterm “expenditure” in the environmental statistics.In this context expenditure is taken to mean capital

expenditure on environmental protection systems and,shown separately, regular expenditure on environ-mental protection systems. Regular expenditure alsoincludes depreciation and statistical interest on theenvironmental protection systems. Total regular expen-diture on environmental protection systems in 1997came to D13 million, compared with a figure of D1.8billion for capital expenditure.

14

Fig. 6: Breakdown of regular expenditure on environmentalprotection

Breakdown of regular expenditure onenvironmental protection 1997Manufacturing industry (excluding construction)

Operatingsupplies

11%

Fees and premiums

7%

Emissioncharges

2% Statisticaldepreciation

17%

Statisticalinterest

6%

Personnel costs7%

External services and otherplant-related measures

30%

External services andother measures

20%

Total 1997: D13 billion Source: Federal Statistical Office

Environmental statistics and monitoring

3.2 Procedure

The companies in the environmental statistics report-ing group have to compile information about their cap-ital expenditure on environmental protection projectsand their regular expenditure on environmental pro-tection. Since small and medium enterprises at least donot regularly make extensive capital expenditure on envi-ronmental protection projects, the information on thiscategory should be relatively easy to determine. Thesituation is different when it comes to determiningregular environmental protection expenditure. The fig-ures needed for this purpose can either be estimatedor determined with the help of cost accounting.

More precise determination of the data naturally takesmore time initially. This may pay off if environmentalprotection costs occur on a significant scale in variousplaces, because it yields sound figures that also per-mit better internal cost control and transparency.

To make it as easy as possible to determine environ-mental protection expenditure1 on a periodic basis, itis advisable to modify the cost centre structure. Firstof all, separate cost centres should be created for allcost-relevant systems that are used solely for envi-ronmental protection (e.g. sewage treatment plantsor waste separation systems). The costs arising for thesecost centres can then be used without difficulty for theenvironmental statistics.

In the case of small and medium enterprises withoutappreciable environmental protection systems oftheir own, external services (e.g. environment-relat-ed consulting, emission monitoring etc.) and feesmay be charged to separate accounts and thus record-ed under new cost categories. In such cases thesecost categories could be evaluated when compilingdetails of environmental protection costs.

Is industry doing less for the environment?The findings of the environmental statistics show that Ger-man industry is investing less and less in environmental pro-tection measures. Whereas DM 5.08 billion was invested inenvironmental protection technologies in 1996, two yearslater the figure stood at only DM 3.29 billion. Has environ-mental protection become less important? As a rule this isnot the case. The reason for the decline seen here lies in thefocus of the statistics. They only include expenditure onend-of-pipe environmental protection measures. In the mean-time, however, there is evidence of a clear trend towardsintegrated environmental protection technologies, which makefor reduced environmental pollution in the course of theproduction process. As a result, the need for additional filtersor sewage plants is steadily diminishing. The statistics, how-ever, do not take account of such investment in integratedtechnologies. In assessing the trend, moreover, one has toconsider the large numbers of existing environmental pro-tection systems. Whereas in the past many companies havehad to invest in first-time projects for sewage plants, filtersor waste management systems, today only replacement invest-ments or upgrades are necessary.

Finally there is another indication that companies are keep-ing up their environmental protection efforts. The figure forregular expenditure on environmental protection measuresshows only a slight drop.

Fig. 7: Capital expenditure and regular expenditure

14.013.3

2.6 1.8 1.7

12.7Regular expenditure

Capital expenditure

12.0

10.0

8.0

6.0

4.0

2.0

0.0

16.0

Bill

ion

Euro

1996 1997 1998

Capital expenditure and regular expenditure on environmentalprotection (manufacturing sector), excluding emission charges

Source: Federal Statistical Office

1 For the distinction between costs and expenditure, see the Glossary.

If the creation and administration of a separate cost centreis not considered worthwhile in the case of less cost-relevantenvironmental protection systems, it is advisable to use anddocument an allocation procedure for determining environ-mental protection costs. This ensures that the figures obtainedare always comparable. If cost locations are distinguished with-in cost centres, it is also possible to use these cost locationsfor systematic recording of environmental protection costs.

Fig. 8: EP cost centres or allocation procedures

Cost-relevant environmentalprotection system

e.g. air filter system

Set up separate cost centre

Less cost-relevantenvironmental protection sys-

tem

Define allocation procedure,e.g. 20% of personnel,

energy and maintenance costs charged to cost centre 4711

Procedure for less cost-relevant environmental protection systems

15

3.3 Benefits and limits

Regular determination of environmental protectioncosts does more than merely provide figures for thestatistics. The newly created environmental protectioncost locations can also be used to ensure better con-trol of the costs incurred there. They permit early iden-tification by cost accounting of problems in theseend-of-pipe areas, such as excessive consumption ofoperating supplies or increasing maintenance costs.Where there are several comparable plants within acompany it is possible to make regular cost compar-isons, a kind of internal benchmarking. And finally,separate cost centres make it possible to allocate thecosts of environmental protection systems to theproduction cost centres that use them. This helps toachieve greater cost transparency.

It is however essential to bear in mind the limits ofthis costs perspective. Three aspects are of specialimportance here:

1. An exclusive focus on environmental protectioncosts is not a good way of systematically exploitingeco-efficiency potentials. This is because environmentalprotection costs account for only a small proportionof the costs caused by the materials used and by wasteand emissions. As a rule the original material costs ofthe substances contained in the waste and wastewaterare several times the cost of disposal. To systemati-cally identify cases of cost-reduction potential inenvironmentally relevant material flows, it is essentialto take account of the associated material and pro-duction costs. This finding has led to the develop-ment of flow cost accounting, in which ancillarycalculations systematically provide information for tap-ping development potential. Flow cost accounting isdescribed in Chapter 4, starting at p. 20.

2. The cost of end-of-pipe environmental protectionmeasures as recorded in the environmental statisticspresents an incomplete picture of the company’senvironmental protection performance. This is because

companies today are increasingly taking production-integrated environmental protection measures whichprevent harmful environmental impacts arising in thecourse of the production processes. These integratedtechnologies have the attractive feature that they areoften more efficient and less expensive than end-of-pipe measures. At the same time, however, they aremuch more difficult to differentiate in cost account-ing. The VDI Guideline 3800 described below takesa detailed look at this differentiation problem.

3. Information about environmental protection costscan also be used for corporate communication on envi-ronmental issues. Where such figures are published,they should specify which environmental protectioncosts are covered – and which are not. The last sec-tion of this chapter shows how to provide informa-tion about environmental protection costs in a waythat enables experts and the interested public tointerpret the figures correctly.

Further development of environmental statistics:

VDI Guideline 3800

The revised edition of VDI Guideline 3800 “Deter-mining expenditure on corporate environmental pro-tection measures”, published in 2000, takes a closelook at how to differentiate expenditure on environ-mental protection measures. In particular, it providesassistance with systematic differentiation in the caseof integrated environmental protection measures.For this purpose it distinguishes:

• Plant-integrated environmental protection meas-ures, (e.g. built-in catalytic converters, additionalcombustion chambers) and

• Process-integrated environmental protection meas-ures (e.g. converting coating technologies from sol-vent-based paints to powder coatings). (See Fig. 10)

The cost components for plant-integrated environ-mental protection measures are comparatively easyto identify. This means they can basically be allocat-ed to environmental protection costs in accordance

Better cost control in end-of-pipe environmental

protection makes sense, but it is not enough.

Fig. 9: Limits to consideration of environmental protection costs

Limits and problems when considering corporate

environmental protection costs

Eco-efficiency potential is often difficult to identify.

Solution:Flow cost accounting

Integrated environmental protectioncosts are difficult to distinguish.

Solution:Allocation rules in

VDI 3800

Environmental protection costs are difficult to interpret.

Solution:Explanatory notes on cost

components included

16

with the new VDI Guideline. It is much more difficult,however, to assess process-integrated environmentalprotection measures, because as a rule changes in aproduction process pursue not only environmentalobjectives, but also a variety of other objectives suchas cost reductions, quality improvements etc.

In such cases, therefore, the environmental protec-tion components can only be estimated. In order toavoid gross differences as a result of individual assess-ments, either industries or the typical users of theprocess-integrated technology under consideration arerecommended to agree standard percentages for theenvironmental protection component of installationsof this kind. If no such convention exists, no envi-ronmental protection expenditure should be shownfor the process-integrated measure in question.

As already mentioned, environmental statistics inGermany do not at present take account of the costsof integrated environmental protection measures. Dis-cussions are in progress at European level about thepossibility of widening the scope of national statisticsaccordingly, which may possibly result in the inclu-sion of plant-integrated environmental protectionmeasures. Until then companies must decide for them-

selves whether it is worth their while to determine theirown integrated environmental protection costs. Theprincipal benefit is seen in the improved basis of datafor environmental reporting. The cost of integratedenvironmental protection measures can be used toshow the public the significance of this block of costsby comparison with the possibly falling costs of end-of-pipe measures.

At present the statistics onlytake account of expenditureon end-of-pipe measures andremediation of contaminatedsites.

Fig. 10: Differentiation of environmental protection measures in VDI Guideline 3800

Taking account of integrated measuresin cost accountingIt does not make sense to create separate cost centres forintegrated environmental protection measures, as they arecomponents of production installations. If integrated envi-ronmental protection costs are to be determined on aregular basis, suitable cost locations can be set up. Or thecosts can be determined in an ancillary calculation as afixed percentage of the costs for the relevant cost cen-tre.

Corporate environmental protection measures for which• capital expenditure is made• regular expenditure arises

Production-relatedmeasures

Product-relatedmeasures

Othermeasures

End-of-pipemeasures

Integratedmeasures

Plant-integratedmeasures

Process-integratedmeasures

Environmentalmanagement

Legacy remediation

Emission Trading,Joint Implementation,CDM

Limits ondetermination ofexpenditure

D i f f e r e n t i a t e d b y e n v i r o n m e n t a l s e c t o r s

Air qualitycontrol

Noise abatement

Nature andlandscapeconservation

Wastemanage-ment

Soil protec-tion / waterconservation

Limits ondetermination ofexpenditure

17

Example: Presenting environmental protection costs in an environmental reportIn an environmental report the environmental protection costs disclosed could be explained as follows:“We determine our ongoing operating expenses and our capital expenditure on environmental protection in accordance withthe requirements of the German Environmental Statistics Act. In the last financial year we spent D45.8 million on operatingexpenses and D11.3 million on end-of-pipe environmental protection measures (e.g. filters, wastewater treatment systems etc.)and environmental management. As in the past, the largest items are waste management and water conservation. The item‘Miscellaneous’ comprises all items that cannot be directly allocated to the categories of the environmental statistics. These areessentially the expenditure on our environmental management systems.“

25

20

15

10

5

0

Mio

E

Abf

allw

irtsc

haft

Gew

ässe

rsch

utz

Lärm

bekä

mpf

ung

Luft

rein

haltu

ng

Bode

nsan

ieru

ng

Nat

ursc

hutz

und

Land

scha

ftsp

flege

Sons

tige

laufende Aufwendungen

Investitionen

Fig. 11: Breakdown of environmental protection expenditure – Possible presentation in environmental report

3.4 Environmental protection costs in voluntary reporting

Even if the company has “only” complied with theEnvironmental Statistics Act and merely determinedits expenditure on end-of-pipe environmental pro-tection measures, it is a logical step to make use ofthis information in environmental reports or other formsof environmental communication as well. To enablethe readers to assess and interpret this informationcorrectly, it is advisable to bear in mind the followingaspects:

• The information should make it clear what kindsof environmental protection measures (end-of-pipe,integrated) and what cost categories (depreciation,personnel costs) have been included.

• Where costs are shown for end-of-pipe environ-mental protection measures, the differentiation rulesused as a basis for the environmental statistics shouldbe complied with. Attention should be drawn tothis procedure.

• Where costs are shown for integrated measures,the differentiation rules set out in the VDI Guide-line should be complied with. Here too, drawingthe attention of the interested public to such com-pliance with the VDI differentiation rules can helpthem to interpret the figures.

• Supplementary information on the savings achievedas a result of environmental protection measuresis recommended in order to convey a completepicture of the costs situation. A look at the savingsachieved can be used to make it clear that future-oriented solutions lie in more efficient utilisation ofinput materials.

Taking account of these aspects makes it consider-ably easier for the reader to interpret the publishedfigures. Explanatory notes about trends over time, thesignificance of environmental protection costs for inter-nal management or the findings of the environmentalstatistics may be used to round off the picture for thereader.

18

Operating expenses and capital expenditure on environmental protection in financial year

Operating expenses

Capital expenditure

Was

te m

anag

emen

t

Wat

er c

onse

rvat

ion

Noi

se a

bate

men

t

Air

qual

ity c

ontr

ol

Soil

rem

edia

tion

Nat

ure

/lan

dsca

peco

nser

vatio

n

Mis

cella

neou

s

Mill

ion D

Fig. 12: Development of environmental protection expenditure – Possible presentation in environmental report

50

60

70

40

30

20

10

0

Mio

E

Entwicklung der laufenden Aufwendungen und Investitionen für den Umweltschutz

1995 1998 1999 2000 2001

laufende Aufwendungen

Investitionen

Bibliography

Verein Deutscher Ingenieure (publ.): VDI Guideline 3800, Determination of costs for industrial environmentalprotection measures, Berlin 2001

Fichter, K., Loew, T., Systeme der Umweltkostenrechnung, in: Handbuch Umweltcontrolling, 2nd edition,published by Federal Environment Ministry and Federal Environmental Agency, Vahlen Verlag, Munich 2001

Presenting environmental protection costs in an environmental report (continued)“The costs of integrated environmental protection measures are not determined, as they cannot always be clearly identified andare not required for the official statistics. Nevertheless, integrated environmental protection measures are growing increasinglyimportant. They avoid environmental burdens at source or prevent them occurring in the first place. As a rule, therefore, theyare more efficient and less expensive than end-of-pipe environmental protection technologies. For example, we were able toswitch off the central exhaust air cleaning system for a production hall because all the systems in the hall were equipped withintegrated extraction facilities and filters. The costs for central exhaust air cleaning are no longer incurred and are therefore nolonger recorded. However, the costs of the measures integrated in the plants are not included in the statistics either.

This example makes it clear that the decrease in environmental protection expenditure revealed by the statistics is not due toany slackening of our efforts, but is a sign of increasing efficiency in the environmental protection sector.

Thanks to efficiency improvements of this kind in the past three years we are saving about D2 million a year on regular coststhroughout the group and have been able to make further reductions in environmental pollution at the same time.”

Falling environmental protection costs may be a sign of success.

19

Mill

ion D

Capital expenditure

Operating expenses

Trends in operating expenses and capital expenditure on environmental protection

Ever since the Rio environmental conference in 1992,people have been discussing – under the headings of“eco-efficiency” and “sustainable development” –concepts that meet with a broad measure of accept-ance in industry and politics. Essentially these conceptsseek to resolve the conflicts between environmentaland business interests and to develop ways of actingthat achieve greater harmony of business, social andecological objectives.

The days are gone when environmental protection wasregarded solely as a locational disadvantage thatpushed up costs. Particularly in the past ten years alarge number of examples have shown that profes-sional, precaution-oriented environmental manage-ment can also bring about considerable reductions incosts. This is surprising when one considers that exploit-ing cost-reduction potential is one of the most basicfunctions of businesses. Accordingly, the controllingfunction with extensive cost accounting instrumentsspecialises in this task. How was it nevertheless pos-sible to discover such cost reduction potentials bymeans of environmental management projects?

Environmental aspects of businesses are closely con-nected with their flows of materials and energy. Forthis reason many environmental management proj-ects have first made a close scrutiny of internal mate-rial flows. This resulted in a degree of transparency ofsuch flows that had previously not existed in thesebusinesses, and thus led to the now familiar cost reduc-tions.

This revealed the basic problem that efficient start-to-finish design of material and energy flows frequentlyfalls through the grid of functional organisation formsand static cost accounting systems.

In order to permit systematic localisation of the poten-tial that exists for cost reductions and environmentalrelief (eco-efficiency), new cost accounting approach-es that seek to remedy precisely this deficit have beendeveloped in recent years, among them flow costaccounting and residues cost accounting. As an exam-ple of these approaches, this chapter describes flowcost accounting. Residues cost accounting andinput/output cost indicators are outlined as the needarises, as simplified variants of flow cost accounting.

4.1 Objective of flow cost accounting

Especially in manufacturing companies, material costsare by far the biggest block and are thus of great rel-evance in any cost context. In the manufacturingsector in Germany, material costs average around 56%.In many industries, such as the pharmaceutical or carindustries, they are actually substantially higher. Inthe past, most companies’ cost-cutting activities havenevertheless concentrated to a large extent on per-sonnel costs. It is generally agreed, however, that alower limit has been reached in this field, unless cutsare to be made in production. It can therefore beassumed that in the years to come the focus of cost-reduction programmes will shift towards material costs.

This chapter shows how to identify environmental relief potentials and cost reduction potentials in the field

of energy and materials management. Transparent information about material and energy flows in terms of

quantities and values enables employees in a wide variety of functional areas to take systematic measures

to increase efficiency.

Eco-efficient control of material and energy flows

4Eco-efficient control

Cost-reduction potential is closely connected with material costs.

20

Major obstacles to systematic reduction of materialcosts are presented by lack of transparency of inter-nal material flow structures and of the costs directlyconnected with material and energy flows. Althoughthe corporate accounting system is able to provideoverall period-specific information about the value ofthe materials entering the company and the materi-als consumed, it can hardly say anything about whatuse is made of the material and where it ends up.This deficit is reflected in the allocation of costs tocost centres, for example, which is an important ele-ment of internal cost transparency. Whereas most com-panies practise a detailed allocation of personnelcosts and depreciation to cost centres, the greater

part of the material costs (and especially the directmaterial costs) bypass the cost centres and hencealso the cost-reduction pressure they exert. As a rule,conventional cost accounting is unable to representmaterial costs in the required structure and degree ofdetail.

Flow cost accounting is intended to supplement con-ventional cost accounting in order to increase thecost transparency of material flows. The aims of flowcost accounting are to

• bring about transparency of flow structures for allinternal material flows, from the supplier (incomingmaterials) through internal production to the cus-tomer (products and packaging) or waste manager(material losses),

• allocate the corresponding quantities, values andcosts to all internal material flows and stocks,

• provide decision makers in purchasing, production,development, sales, despatch and logistics with theinformation about flow quantities and costs that theyneed for their activities,

• initiate cost-effective measures to reduce materialflows, by reducing material losses and developingmaterial-reduced products and packagings,

• help reduce product-related and site-related envi-ronmental burdens by implementing such measures.

Flow cost accounting is part of a comprehensivemanagement approach – flow management – aimedat efficient design of the entire material and infor-mation flows relating to the company. Unlike processcost accounting, in which the primary focus is on reduc-ing personnel costs, flow cost accounting concentrateson reducing material costs.

Flow cost accounting closes the gaps in conventional cost accounting.

21

Miscellaneous13%

Material costs56%

Depreciation, rents and leases

6%

Personnel costs25%

Fig. 13: Cost structure in the manufacturing sector (Source: Federal Statistical Office)

Tom Sidlik (head of purchasing at DaimlerChrysler) point-ed out that about 78 percent of all Chrysler’s costs weredue to materials. “This means material costs are the wayto cut costs quickly“.

Source: Stuttgarter Zeitung, 09.12.2000

Environmental management(EMAS, ISO 14001, ...)

Classicenvironmentalprotection

Flow management

• Environmental law• Environmental technology• End-of-pipe

• Eco-controlling• Environmental audit• Environmental accounting• Environmental organisation• Environmental cost accounting• Environmental PR

• Flow models• Flow cost accounting• Integration in organisation (flow organisation)• Eco-efficiency• Start-of-pipe

Fig. 14: From environmental protection to flow management

Fig. 15: Simplified material flow model

MaterialProductsPackagings

Residues:- Waste- Wastewater- Exhaust air- Heat / Noise

Incomingstore

Production Outgoingstore

Environmentaltechnology

Cus

tom

erW

aste

man

ager

Intermediate product store

Material losses

Supp

lier

� expanding the “logistics chain” to include material losses

4.2 Concept and forms of flow cost accounting

Basic concept

Flow cost accounting regards the relevant materialflows as cost collectors, and therefore allocates thecosts of the company’s production operations tothese material flows. For this purpose it is first neces-sary to determine the structure of the material flowsin a simplified form. A material flow model is used todescribe the structure of the internal material flowsand thus at the same time define the framework forflow cost accounting. The material flow model is madeup of internal and external quantity locations and ofmaterial flows. Internal quantity locations are all spa-tial or functional units within the company where mate-rials are stored, worked on or otherwise transformed.Thus typical quantity locations are goods reception,the raw materials store, the various production areasor despatch. In the same way as the quantity loca-tions of the classic logistics chain, however, all envi-ronmentally relevant systems and facilities, such asresidue centres, water treatment plants or filter plants,are also treated as quantity locations. External quan-tity locations such as suppliers and customers, and alsowaste disposers or municipal sewage plants, repre-sent material flow related external interfaces of thecompany. Material flows link the quantity locationsand thus symbolise movements of materials fromone quantity location to another. Fig. 15 shows a high-ly simplified example of a material flow model.

In the context of flow cost accounting the costs ofthe company’s production operations are allocated tothe material flow model. The main focus here is onperiod-related transparency of the material valuesmoved; on the basis of the value of materials enter-ing the company within a given period, questions ariseas to the use and whereabouts of this value. Whatvalue of materials entered production during thisperiod? What value of materials left production as aproduct? What value of materials went as a productto the customer? What value of materials was lost intotal? To be able to answer these questions, flowcost accounting must not, as is usual in conventionalcost accounting, mix material costs and productioncosts for intermediate and finished products. Instead,flow cost accounting initially shows merely the valueof materials moved for every material flow at purchaseprice.

Thus for every material entering the company, flowcost accounting shows in a high degree of detail itsdistribution within the company. In simplified form itmust be possible to divide the incoming materialvalue among the following reference quantities (seealso Fig. 16):

• Change in material stocks(in the example: D5 million)

• Material in product (example: D112 million)• Material lost (example: D19 million).

Expanding the logistics chainto include material losses

22

Table 3: Simplified flow costs matrix

Costsin million D

Product

Packaging

Material losses

Total

Material costs

85

27

19

131

System costs(Personnel, de-preciation etc.)

22

18

4

44

Delivery,disposal

costs

0

2

1

3

Total

107

47

24

178

As well as the pure material value, it is also possiblein flow cost accounting to assign to the materialflows the costs of storage, processing or administra-tion of materials, such as personnel costs and depre-ciation (system costs), and the disposal costs of thematerials. In particular, flow costs and other adminis-tration costs of units that are not physically involvedin the material flow can be allocated to the materialflows in the same way as in process cost accounting.

The flow costs matrix provides an overview of all costsassociated with the material flows (Table 3). The firsttwo rows show what costs were due to material andpackaging for the products and how these costs aredistributed among purchasing, internal added valueand delivery. The third row shows the costs of mate-rial losses. The material costs arose from buying thematerial contained in the material losses. The systemcosts show the added value that is already containedin the material losses. The delivery and disposal costsindicate what costs are incurred for disposal of thematerial lost.

Implementation variants

Flow cost accounting is a comprehensive cost account-ing approach and can therefore assume very substantialproportions in practical implementation within thecompany. It therefore makes sense to take a look atdifferent variants of flow cost accounting, in order tofind a variant that is appropriate to the company interms of affordable expenditure and targeted bene-fits. The following are important parameters that deter-mine which individual design of flow cost accountingis used:

• the size and degree of detail of the material flowmodel,

• the cost categories covered (partial or full costaccounting) and

• the data taken as a basis.

Design factor: Material flow model

The decision in favour of a particular material flowmodel dictates important specifications for the sub-sequent calculation of the flow costs. It is therefore

Different practical variantspermit individually tailoredflow cost accounting

23

Fig. 16: Flow model with material values

122 121

3 11 5

105 4

19

112

6055

Incomingstore

IS FS18 16

IS FS51 43

IS FS0 0

IS FS0 0

Production Outgoingstore

Environmentaltechnology

Cus

tom

erW

aste

man

ager

Intermediate product store

Supp

lier

IS = Initial stockFS = Final stock

IS 15FS 20

of crucial importance to first arrive at a clear idea ofthe size and degree of detail of the material flow model.It is possible to distinguish a variety of material flowmodels that either represent only the material-relat-ed inputs and outputs (environmental balance), onlythe material losses flows (residues) or the entire flowof materials within the company.

Compiling the inputs and outputs in a corporateenvironmental balance sheet yields the simplest viewof the material and energy flows. Flow cost account-ing on this basis allocates flow costs to the inputs andoutputs only, and thus offers a highly simplified entryversion. A considerably more comprehensive versionis offered by the model for flows of residues, whichrepresents material losses and energy consumption fig-ures. While focusing on material flows which do notadd value, this keeps expenditure on flow cost account-ing within limits. The development of cost-reductionmeasures is however confined to reducing materiallosses. Only a model of all internal material flows givesa complete picture of the “paths” taken by the mate-rials through the company from arrival through allinternal stages to departure. Only this kind of overallapproach makes it possible to judge the consistencyof the material flow data in the existing informationsystems and improve it if necessary. Furthermore, flowcost accounting on the basis of all material flowsgenerates data not only on energy and residues, butalso on products and packaging, thereby consider-ably broadening the scope for developing cost-reduc-tion measures.

Design factor: Cost categories

Flow costs may be defined as all costs incurred as aresult of the flows of material and energy throughthe company. To this extent flow costs are more orless identical with the costs of production of goodsby the company. What is new is the flow-oriented per-spective, which results in a specific subdivision of thecosts. Flow cost accounting distinguishes between:

• Material costs• System costs• Supply and disposal costs.

Exact representation of material costs is the most impor-tant and at the same time the most difficult part offlow cost accounting from a methodological point ofview. Indeed, this component could be described asthe central aspect of flow cost accounting. In con-ventional cost accounting, a material can only berecorded as costs once. This results in a highly sim-plified view of the complex material flows. In orderto increase the transparency of material flows, flowcost accounting first of all assigns the associated mate-rial values to all material flows considered. This ispossible because these values, unlike the costs, are notadded together to yield a total. It is only on the basisof a material flow model with material values that aclear definition of the material costs in view is made.Allocation of material values to material flows is a fun-damental component of flow cost accounting and shouldtherefore always be taken into account when makingthe company-specific selection of the practical variantto be implemented. Moreover, it is in the materials sec-tor that the greatest eco-efficiency potential lies.

System costs are the costs that are incurred to keepthe company going and put it in a position to design,control and transform the flows of materials. Essen-tially, therefore, system costs consist of personnel costs,depreciation and other costs (e.g. for external servic-es). The system costs are invested in the materialflows and make these more expensive after everyprocessing stage. Thus system costs can basically beallocated to the flows of materials. Frequently, how-ever, the work involved in exact allocation of systemcosts outweighs the benefits that result from theincreased transparency.

Supply and disposal costs result from the fact that prod-ucts are delivered to customers and residues to wastemanagement firms. They consist primarily of costsfor carrier services, special transport packaging, costsof transboundary transport, and the charges such asrecycling and disposal costs involved in the disposalof residues.

24

ERP system

Separate database

Material costs

Disposal costs

System costs

Input and output

Residue flows

Material flows

Fig. 17: Criteria for variant formation

Cost categories

Data basis

Flow model

Material flowmodel

Input-Output

Residueflows

Entire flow ofmaterials

Var

iant

1

2

3

Cost categories

Material costs, dis-posal costs

Material costs, sys-tem costs,disposal costs