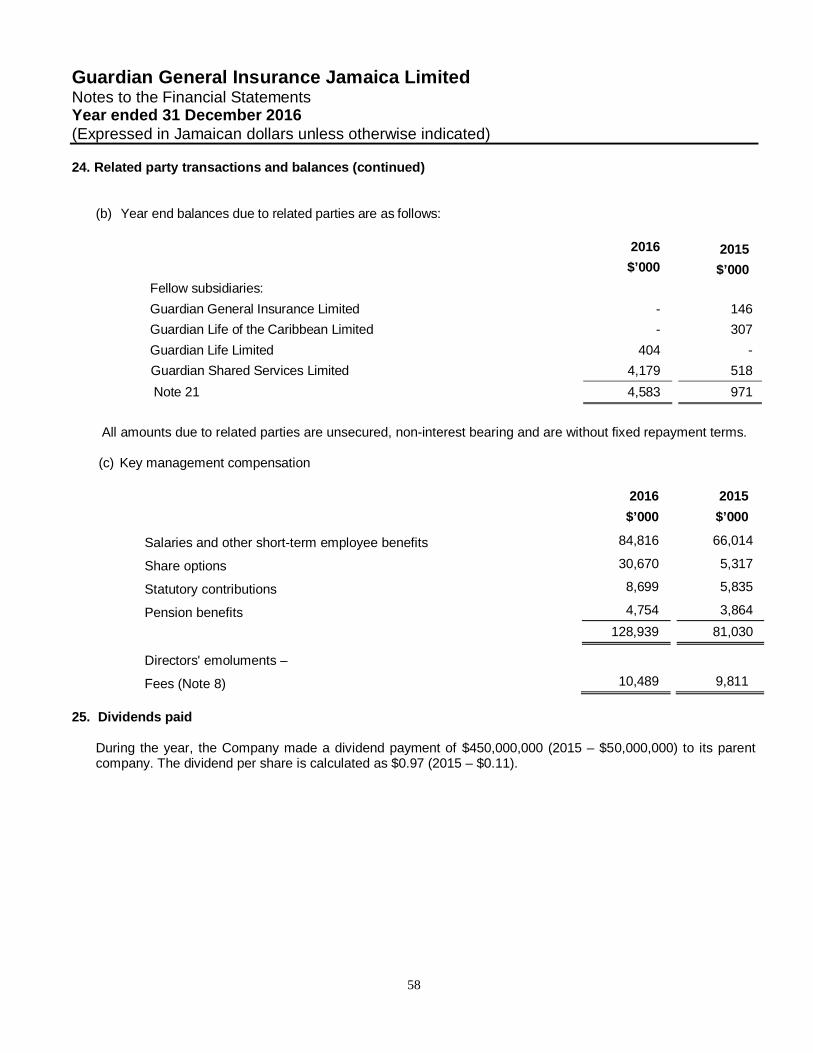

Guardian General Insurance Jamaica Limitedmyguardiangroup.com/jamaica/gloc_forms/GGIJL_Audited...9...

62

Guardian General Insurance Jamaica Limited Financial Statements For the Year Ended 31 December 2016 (Expressed in Jamaican dollars unless otherwise indicated)

Transcript of Guardian General Insurance Jamaica Limitedmyguardiangroup.com/jamaica/gloc_forms/GGIJL_Audited...9...

Guardian General InsuranceJamaica Limited

Financial Statements

For the Year Ended 31 December 2016

(Expressed in Jamaican dollars unlessotherwise indicated)

Guardian General Insurance Jamaica LimitedIndexYear ended 31 December 2016

Page

Independent Auditor’s Report 1 – 3

Financial Statements

Statement of Comprehensive Income 4

Statement of Financial Position 5

Statement of Changes in Equity 6

Statement of Cash Flows 7 - 8

Notes to the Financial Statements 9 - 60

1

INDEPENDENT AUDITOR’S REPORT

To the Shareholders of Guardian General Insurance Jamaica Limited

Report on the Financial Statements

Opinion

We have audited the financial statements of Guardian General Insurance Jamaica Limited (theCompany), which comprise the statement of financial position as at 31 December 2016, thestatements of comprehensive income, changes in equity and cash flows for the year then ended,and notes, comprising significant accounting policies and other explanatory information.

In our opinion, the accompanying financial statements give a true and fair view of the financialposition of the Company as at 31 December 2016 and of its financial performance and cash flowsfor the year then ended in accordance with International Financial Reporting Standards (IFRS) andthe Jamaican Companies Act.

Basis for Opinion

We conducted our audit in accordance with International Standards on Auditing (“ISAs”). Ourresponsibilities under those standards are further described in the Auditor’s Responsibilities for theAudit of the Financial Statements section of our report. We are independent of the Company inaccordance with the International Ethics Standards Board for Accountants’ Code of Ethics forProfessional Accountants (“IESBA Code”) and we have fulfilled our other ethical responsibilities inaccordance with the IESBA Code. We believe that the audit evidence we have obtained is sufficientand appropriate to provide a basis for our opinion.

Responsibilities of Management and the Board of Directors for the Financial Statements

Management is responsible for the preparation of the financial statements that give a true and fairview in accordance with IFRS and the Jamaican Companies Act, and for such internal control asmanagement determines is necessary to enable the preparation of financial statements that arefree from material misstatement, whether due to fraud or error.

In preparing the financial statements, management is responsible for assessing the Company’sability to continue as a going concern, disclosing, as applicable, matters related to going concernand using the going concern basis of accounting unless management either intends to liquidate theCompany or to cease operations, or has no realistic alternative but to do so.

The Board of Directors is responsible for overseeing the financial reporting process.

8 Olivier RoadKingston 8Jamaica, W.I.

Tel: +1 876 925 2501Fax: +1 876 755 0413ey.com

Chartered Accountants

A member firm of Ernst & Young Global LimitedPartners: Allison Peart, Linval Freeman, Winston Robinson, Anura Jayatillake, Kayann

2

INDEPENDENT AUDITOR’S REPORT (CONTINUED)

To the Shareholders of Guardian General Insurance Jamaica Limited (Continued)

Auditor’s Responsibilities for the Audit of the Financial Statements

Our objectives are to obtain reasonable assurance about whether the financial statements as awhole are free from material misstatement, whether due to fraud or error, and to issue an auditor’sreport that includes our opinion. Reasonable assurance is a high level of assurance, but is not aguarantee that an audit conducted in accordance with ISAs will always detect a materialmisstatement when it exists. Misstatements can arise from fraud or error and are consideredmaterial if, individually or in the aggregate, they could reasonably be expected to influence theeconomic decisions of users taken on the basis of these financial statements.

As part of an audit in accordance with ISAs, we exercise professional judgment and maintainprofessional skepticism throughout the audit. We also:

• Identify and assess the risks of material misstatement of the financial statements, whetherdue to fraud or error, design and perform audit procedures responsive to those risks, andobtain audit evidence that is sufficient and appropriate to provide a basis for our opinion.The risk of not detecting a material misstatement resulting from fraud is higher than for oneresulting from error, as fraud may involve collusion, forgery, intentional omissions,misrepresentations, or the override of internal control.

• Obtain an understanding of internal control relevant to the audit in order to design auditprocedures that are appropriate in the circumstances, but not for the purpose of expressingan opinion on the effectiveness of the Company’s internal control.

• Evaluate the appropriateness of accounting policies used and the reasonableness ofaccounting estimates and related disclosures made by management.

• Conclude on the appropriateness of management’s use of the going concern basis ofaccounting and, based on the audit evidence obtained, whether a material uncertainty existsrelated to events or conditions that may cast significant doubt on the Company’s ability tocontinue as a going concern. If we conclude that a material uncertainty exists, we arerequired to draw attention in our auditor’s report to the related disclosures in the financialstatements or, if such disclosures are inadequate, to modify our opinion. Our conclusionsare based on the audit evidence obtained up to the date of our auditor’s report. However,future events or conditions may cause the Company to cease to continue as a goingconcern.

• Evaluate the overall presentation, structure and content of the financial statements,including the disclosures, and whether the financial statements represent the underlyingtransactions and events in a manner that presents a true and fair view.

A member firm of Ernst & Young Global Limited

3

INDEPENDENT AUDITOR’S REPORT (CONTINUED)

To the Shareholders of Guardian General Insurance Jamaica Limited (Continued)

Auditor’s Responsibilities for the Audit of the Financial Statements (Continued)

We communicate with the Board of Directors regarding, among other matters, the planned scopeand timing of the audit and significant audit findings, including any significant deficiencies ininternal control that we identify during our audit.

Report on additional requirements of the Jamaican Companies Act

We have obtained all the information and explanations which, to the best of our knowledge andbelief, were necessary for the purposes of our audit. In our opinion, proper accounting recordshave been maintained, so far as appears from our examination of those records, and the financialstatements which are in agreement therewith, give the information required by the JamaicanCompanies Act, in the manner required.

Ernst & YoungKingston, Jamaica

21 March 2017

A member firm of Ernst & Young Global Limited

4

Guardian General Insurance Jamaica LimitedStatement of Comprehensive IncomeYear ended 31 December 2016(Expressed in Jamaican dollars unless otherwise indicated)

Notes2016$’000

2015$’000

Gross premiums written 6,747,435 5,493,189Outward reinsurance premiums (5,075,976) (3,894,949)Premiums written, net of reinsurance 1,671,459 1,598,240Change in provision for unearned premiums 6,591 45,288Premiums earned, net of reinsurance 1,678,050 1,643,528Claims incurred, net of reinsurance (1,109,088) (1,153,279)Commissions earned 630,182 665,566Commissions paid (483,650) (492,231)Change in net deferred policy acquisition costs (5,958) (19,865)Administrative expenses 8 (575,728) (559,975)Underwriting profit 133,808 83,744Investment income 10 399,144 403,558Other income 2,177 3,260Foreign exchange gains 120,934 89,766Profit before taxation 656,063 580,328Taxation 11 (177,109) (166,497)Net profit attributable to owners of the parent 478,954 413,831Other comprehensive income:Amount not to be reclassified to profit or loss in future periods:Re-measurement of employee benefit obligation, net of taxes 26 (200) (600)

Amount to be reclassified to profit or loss in future periods:Investment fair value gain, net of taxes 27 91,869 57,241Total other comprehensive income 91,669 56,641

Total comprehensive income attributable to owners of the parent 570,623 470,472

The accompanying notes form an integral part of these financial statements.

Guardian General Insurance Jamaica LimitedStatement of Financial PositionAs at 31 December 2016(Expressed in Jamaican dollars unless otherwise indicated)

5

Notes2016$’000

2015$’000

ASSETSProperty and equipment 12(a) 88,364 113,948Intangible assets 12(b) - 4,348Investments 13 5,956,353 5,639,352Due from policyholders, brokers and agents 913,792 862,626Deferred policy acquisition costs 14 208,796 226,928Recoverable from reinsurers 15 3,026,806 1,934,787Other receivables 16 23,269 17,657Cash and bank 17 653,101 890,330Total assets 10,870,481 9,689,976

EQUITYShare capital 18(a) 1,138,500 1,138,500Share options 19 2,289 2,289Other capital reserves 18(b) 213,167 213,167Revaluation reserves 27 292,160 200,291Retained earnings 1,808,427 1,779,673Total equity 3,454,543 3,333,920

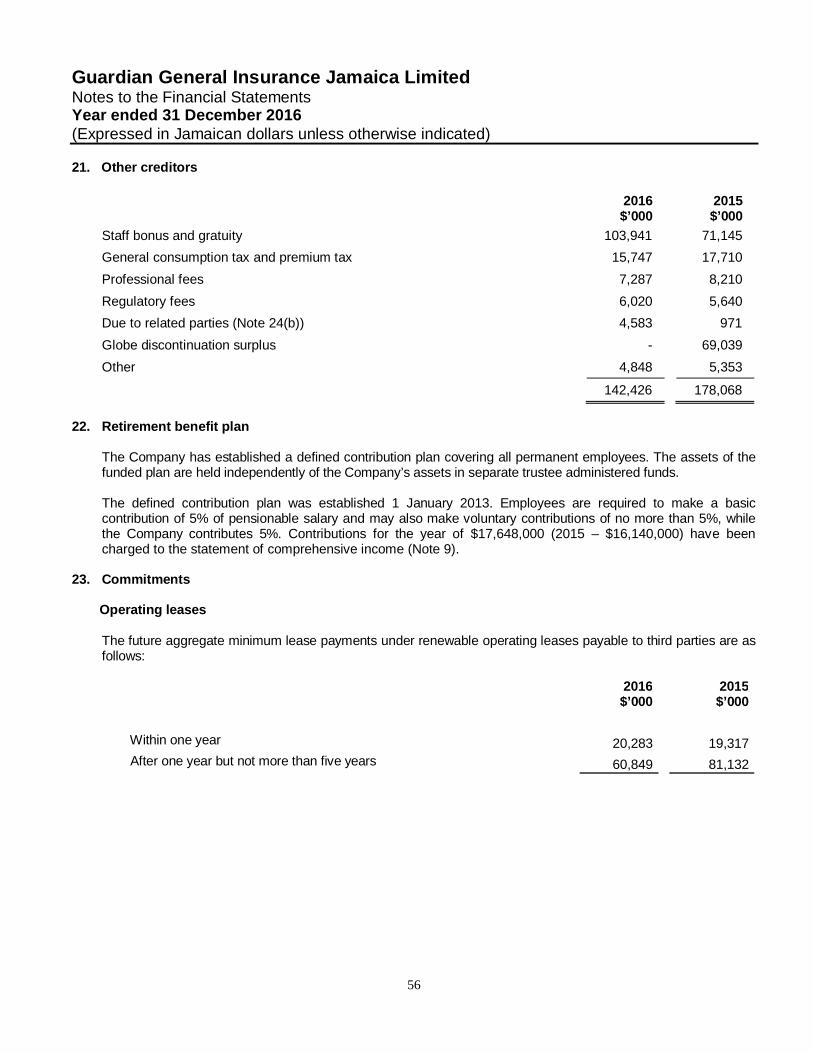

LIABILITIESInsurance reserves 15 6,667,586 5,550,307Deferred tax liabilities, net 20 161,155 124,165Due to reinsurers and co-insurers 341,073 439,006Other creditors 21 142,426 178,068Employee benefit obligation 26 11,100 10,500Taxation payable 92,598 54,010Total liabilities 7,415,938 6,356,056Total equity and liabilities 10,870,481 9,689,976

The accompanying notes form an integral part of these financial statements.

On 21 March 2017, the Board of Directors authorised these financial statements for issue.

David Henriques Director Peter John Thwaites Director

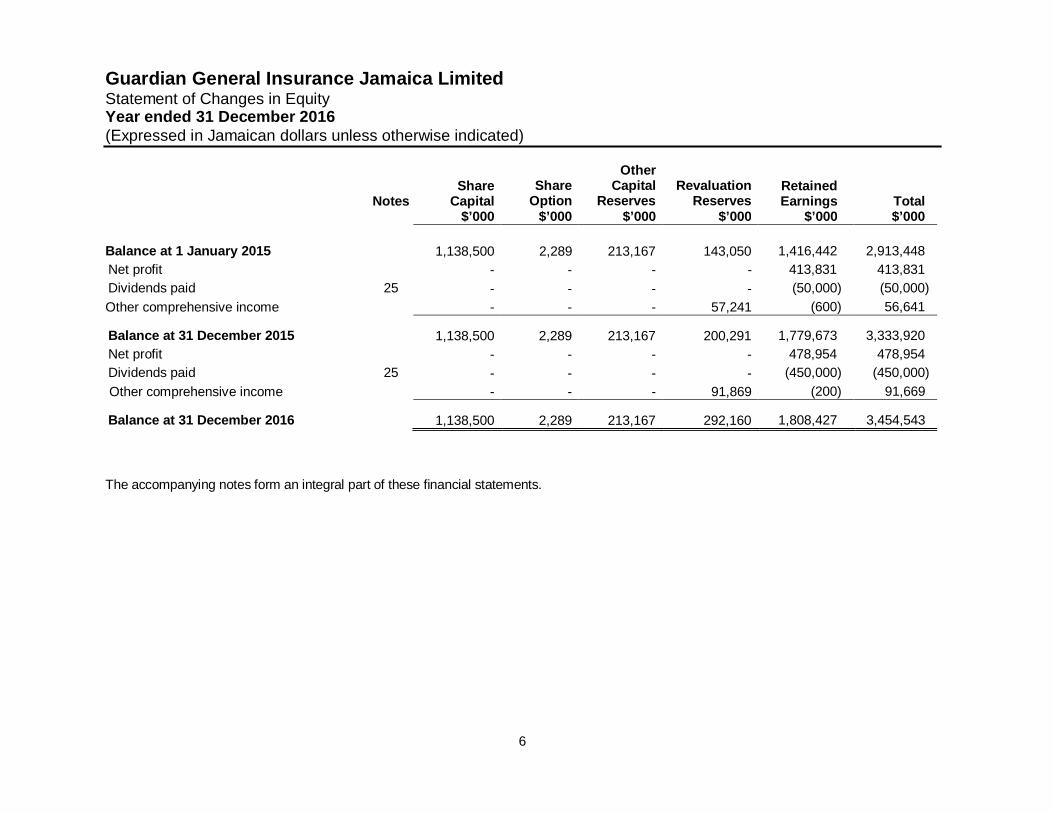

Guardian General Insurance Jamaica LimitedStatement of Changes in EquityYear ended 31 December 2016(Expressed in Jamaican dollars unless otherwise indicated)

6

NotesShare

CapitalShare

Option

OtherCapital

ReservesRevaluation

ReservesRetainedEarnings Total

$’000 $’000 $’000 $’000 $’000 $’000

Balance at 1 January 2015 1,138,500 2,289 213,167 143,050 1,416,442 2,913,448Net profit - - - - 413,831 413,831Dividends paid 25 - - - - (50,000) (50,000)Other comprehensive income - - - 57,241 (600) 56,641

Balance at 31 December 2015 1,138,500 2,289 213,167 200,291 1,779,673 3,333,920Net profit - - - - 478,954 478,954Dividends paid 25 - - - - (450,000) (450,000) Other comprehensive income - - - 91,869 (200) 91,669

Balance at 31 December 2016 1,138,500 2,289 213,167 292,160 1,808,427 3,454,543

The accompanying notes form an integral part of these financial statements.

Guardian General Insurance Jamaica LimitedStatement of Cash FlowsYear ended 31 December 2016(Expressed in Jamaican dollars unless otherwise indicated)

7

2016 2015Notes $’000 $’000

Cash flows from operating activities

Net cash provided by operating activities (page 8) 243,368 476,218

Cash flows from investing activities

Purchase of property and equipment 12(a) (7,409) (34,325)

Proceeds from disposal of property and equipment - 1,591

Proceeds from disposal of non-current assets held for sale - 42,781

Investments, net (550,497) 704,137

Net cash (used in)/provided by investing activities (557,906) 714,184

Cash flows from financing activities

Dividends paid 25 (450,000) (50,000)

Net cash used in financing activities (450,000) (50,000)

Net (decrease)/increase in cash and cash equivalents (764,538) 1,140,402

Effect of exchange rate on cash and cash equivalents 45,573 29,127

Cash and cash equivalents at beginning of year 2,860,267 1,690,738

Cash and cash equivalents at end of year 2,141,302 2,860,267

Cash and cash equivalents comprise:

Short-term investments 13 1,488,201 1,969,937

Cash and bank 17 653,101 890,330

2,141,302 2,860,267

The accompanying notes form an integral part of these financial statements.

Guardian General Insurance Jamaica LimitedStatement of Cash Flows (Continued)Year ended 31 December 2016(Expressed in Jamaican dollars unless otherwise indicated)

8

Notes2016$’000

2015$’000

Cash flows from operating activitiesNet profit 478,954 413,831Adjustments for:Depreciation of property and equipment 12(a) 32,897 31,956Amortisation of intangible assets 12(b) 4,348 4,348Loss on sale of property and equipment 96 242Loss on write off of website 12(b) - 15,933Net interest and dividend income 10 (329,185) (337,788)Income tax expense 11 172,199 154,337Deferred tax expense 11 4,910 12,160Employee benefit obligations 26 900 900Unrealised exchange gains on foreign currency (103,489) (62,995)Unrealised fair value gain on investments 10 (69,959) (65,770)Increase in insurance reserves 1,117,279 135,068Changes in operating assets and liabilities:Due from policyholders, brokers and agents (51,166) (114,088)Deferred policy acquisition costs 18,132 6,726Recoverable from reinsurers (1,092,019) (145,655)Taxation paid (133,611) (79,965)Other receivables (5,612) 1,428Due to related parties 3,612 (1,109)Due to reinsurers and co-insurers (97,933) 91,558Other creditors (39,254) 78,530Net cash (used in)/provided by operating activities (88,901) 139,647Interest and dividend received 332,269 336,571

Net cash provided by operating activities (page 7) 243,368 476,218

The accompanying notes form an integral part of these financial statements.

Guardian General Insurance Jamaica LimitedNotes to the Financial StatementsYear ended 31 December 2016(Expressed in Jamaican dollars unless otherwise indicated)

9

1. Identification and activity

Guardian General Insurance Jamaica Limited (the “Company”) is a limited liability company, incorporated anddomiciled in Jamaica, with registered office at 19 Dominica Drive, Kingston 5, Jamaica. The Company is a wholly-owned subsidiary of Globe Holdings Limited which is incorporated in St. Lucia. Globe Holdings Limited is awholly-owned subsidiary of Guardian Holdings Limited, the ultimate parent company which is incorporated in theRepublic of Trinidad and Tobago.

The Company is licensed to operate as a general insurance company under the Insurance Act, 2001. Its principalactivity is the underwriting of property and casualty risks.

2. Significant accounting policies

The principal accounting policies applied in the preparation of these financial statements are set out below. Thesepolicies have been consistently applied to all the years presented, unless otherwise stated.

(a) Basis of preparation

Statement of complianceThese financial statements have been prepared in accordance with International Financial Reporting Standards(“IFRS”) as issued by the International Accounting Standards Board (“IASB”), and the requirements of theJamaican Companies Act.

The Company presents its statement of financial position broadly in order of liquidity. An analysis regardingrecovery or settlement within twelve months after the statement of financial position date (current) and morethan 12 months after the statement of financial position date (non-current) is presented in the notes. Financialassets and financial liabilities are offset and the net amount reported in the statement of financial positiononly when there is a legally enforceable right to offset the recognised amounts and there is an intention tosettle on a net basis, or to realise the assets and settle the liability simultaneously. Income and expense willnot be offset in the statement of comprehensive income unless required or permitted by an accountingstandard or interpretation, as specifically disclosed in the accounting policies of the Company.

Basis of measurementThe financial statements have been prepared under the historical cost convention as modified by therevaluation of investment securities classified as fair value through profit or loss and available for sale, and non-current asset held for sale.

JudgementsThe preparation of financial statements in conformity with IFRS requires the use of certain critical accountingestimates. It also requires management to exercise its judgement in the process of applying the Company’saccounting policies. The areas involving a higher degree of judgement or complexity, or areas whereassumptions and estimates are significant to the financial statements are disclosed in Note 6.

Guardian General Insurance Jamaica LimitedNotes to the Financial StatementsYear ended 31 December 2016(Expressed in Jamaican dollars unless otherwise indicated)

10

2. Significant accounting policies (continued)

(b) Adoption of new and revised International Financial Reporting Standards:

The Company applied for the first time certain standards and amendments, which are effective for annualperiods beginning on or after 1 January 2016. The Company has not early adopted any other standard,interpretation or amendment that has been issued but is not yet effective.

The nature and the effect of these changes are disclosed below. Although these new standards andamendments applied for the first time in 2016, they did not have a material impact on the financial statementsof the Company. The nature and the impact of each new standard or amendment is described below:

IFRS 14 Regulatory Deferral AccountsIFRS 14 is an optional standard that allows an entity, whose activities are subject to rate-regulation, tocontinue applying most of its existing accounting policies for regulatory deferral account balances upon itsfirst-time adoption of IFRS. Entities that adopt IFRS 14 must present the regulatory deferral accounts asseparate line items on the statement of financial position and present movements in these account balancesas separate line items in the statement of profit or loss and OCI. The standard requires disclosure of thenature of, and risks associated with, the entity’s rate-regulation and the effects of that rate-regulation on itsfinancial statements.

Since the Company is an existing IFRS preparer and is not involved in any rate-regulated activities, thisstandard does not apply.

Amendments to IFRS 11 Joint Arrangements: Accounting for Acquisitions of InterestsThe amendments to IFRS 11 require that a joint operator accounting for the acquisition of an interest in ajoint operation, in which the activity of the joint operation constitutes a business, must apply the relevant IFRS3 Business Combinations principles for business combination accounting. The amendments also clarify that apreviously held interest in a joint operation is not remeasured on the acquisition of an additional interest in thesame joint operation if joint control is retained. In addition, a scope exclusion has been added to IFRS 11 tospecify that the amendments do not apply when the parties sharing joint control, including the reportingentity, are under common control of the same ultimate controlling party.

The amendments apply to both the acquisition of the initial interest in a joint operation and the acquisition ofany additional interests in the same joint operation and are applied prospectively. These amendments do nothave any impact on the Company as there has been no interest acquired in a joint operation during theperiod.

Amendments to IAS 16 and IAS 38: Clarification of Acceptable Methods of Depreciation andAmortisationThe amendments clarify the principle in IAS 16 Property, Plant and Equipment and IAS 38 Intangible Assetsthat revenue reflects a pattern of economic benefits that are generated from operating a business (of whichthe asset is a part) rather than the economic benefits that are consumed through use of the asset. As aresult, a revenue-based method cannot be used to depreciate property, plant and equipment and may onlybe used in very limited circumstances to amortise intangible assets. The amendments are appliedprospectively and do not have any impact on the Company, given that it has not used a revenue-basedmethod to depreciate its non-current assets.

Guardian General Insurance Jamaica LimitedNotes to the Financial StatementsYear ended 31 December 2016(Expressed in Jamaican dollars unless otherwise indicated)

11

2. Significant accounting policies (continued)

(b) Adoption of new and revised International Financial Reporting Standards (continued)

Amendments to IAS 16 and IAS 41 Agriculture: Bearer PlantsThe amendments change the accounting requirements for biological assets that meet the definition of bearerplants. Under the amendments, biological assets that meet the definition of bearer plants will no longer bewithin the scope of IAS 41 Agriculture. Instead, IAS 16 will apply. After initial recognition, bearer plants will bemeasured under IAS 16 at accumulated cost (before maturity) and using either the cost model or revaluationmodel (after maturity). The amendments also require that produce that grows on bearer plants will remain inthe scope of IAS 41 measured at fair value less costs to sell. For government grants related to bearer plants,IAS 20 Accounting for Government Grants and Disclosure of Government Assistance will apply. Theamendments are applied retrospectively and do not have any impact on the Company as it does not haveany bearer plants.

Amendments to IAS 27: Equity Method in Separate Financial StatementsThe amendments allow entities to use the equity method to account for investments in subsidiaries, jointventures and associates in their separate financial statements. Entities already applying IFRS and electing tochange to the equity method in their separate financial statements have to apply that change retrospectively.

These amendments do not have any impact on the Company’s financial statements.

Annual Improvements 2012-2014 CycleThese improvements include:

IFRS 5 Non-current Assets Held for Sale and Discontinued OperationsAssets (or disposal groups) are generally disposed of either through sale or distribution to the owners. Theamendment clarifies that changing from one of these disposal methods to the other would not be considereda new plan of disposal, rather it is a continuation of the original plan. There is, therefore, no interruption of theapplication of the requirements in IFRS 5. This amendment is applied prospectively.

IFRS 7 Financial Instruments: Disclosures

(i) Servicing contractsThe amendment clarifies that a servicing contract that includes a fee can constitute continuinginvolvement in a financial asset. An entity must assess the nature of the fee and the arrangement againstthe guidance for continuing involvement in IFRS 7 in order to assess whether the disclosures arerequired. The assessment of which servicing contracts constitute continuing involvement must be maderetrospectively. However, the required disclosures need not be provided for any period beginning beforethe annual period in which the entity first applies the amendments.

(ii) Applicability of the amendments to IFRS 7 to condensed interim financial statementsThe amendment clarifies that the offsetting disclosure requirements do not apply to condensed interimfinancial statements, unless such disclosures provide a significant update to the information reported inthe most recent annual report. This amendment is applied retrospectively.

IAS 19 Employee BenefitsThe amendment clarifies that market depth of high quality corporate bonds is assessed based on thecurrency in which the obligation is denominated, rather than the country where the obligation is located.When there is no deep market for high quality corporate bonds in that currency, government bond rates mustbe used. This amendment is applied prospectively.

Guardian General Insurance Jamaica LimitedNotes to the Financial StatementsYear ended 31 December 2016(Expressed in Jamaican dollars unless otherwise indicated)

12

2. Significant accounting policies (continued)

(b) Adoption of new and revised International Financial Reporting Standards (continued)

Annual Improvements 2012-2014 Cycle (continued)

IAS 34 Interim Financial ReportingThe amendment clarifies that the required interim disclosures must either be in the interim financialstatements or incorporated by cross-reference between the interim financial statements and wherever theyare included within the interim financial report (e.g., in the management commentary or risk report). The otherinformation within the interim financial report must be available to users on the same terms as the interimfinancial statements and at the same time. This amendment is applied retrospectively. These amendmentsdo not have any impact on the Company.

Amendments to IAS 1 Disclosure InitiativeThe amendments to IAS 1 clarify, rather than significantly change, existing IAS 1 requirements. Theamendments clarify:

· The materiality requirements in IAS 1· That specific line items in the statement(s) of profit or loss and OCI and the statement of financial position

may be disaggregated· That entities have flexibility as to the order in which they present the notes to financial statements· That the share of OCI of associates and joint ventures accounted for using the equity method must be

presented in aggregate as a single line item, and classified between those items that will or will not besubsequently reclassified to profit or loss.

Furthermore, the amendments clarify the requirements that apply when additional subtotals are presented inthe statement of financial position and the statement(s) of profit or loss and OCI. These amendments do nothave any impact on the Company.

Amendments to IFRS 10, IFRS 12 and IAS 28 Investment Entities: Applying the ConsolidationExceptionThe amendments address issues that have arisen in applying the investment entities exception under IFRS 10Consolidated Financial Statements. The amendments to IFRS 10 clarify that the exemption from presentingconsolidated financial statements applies to a parent entity that is a subsidiary of an investment entity, whenthe investment entity measures all of its subsidiaries at fair value.

Furthermore, the amendments to IFRS 10 clarify that only a subsidiary of an investment entity that is not aninvestment entity itself and that provides support services to the investment entity is consolidated. All othersubsidiaries of an investment entity are measured at fair value. The amendments to IAS 28 Investments inAssociates and Joint Ventures allow the investor, when applying the equity method, to retain the fair valuemeasurement applied by the investment entity associate or joint venture to its interests in subsidiaries.

These amendments are applied retrospectively and do not have any impact on the Company as the Companydoes not apply the consolidation exception.

Guardian General Insurance Jamaica LimitedNotes to the Financial StatementsYear ended 31 December 2016(Expressed in Jamaican dollars unless otherwise indicated)

13

2. Significant accounting policies (continued)

(b) Adoption of new and revised International Financial Reporting Standards (continued)

New revised and amended standards and interpretations that are not yet effectiveThe standards and interpretations that are issued, but not yet effective, are disclosed below. The Companyintends to adopt these standards, if applicable, when they become effective.

IFRS 9 Financial InstrumentsIn July 2014, the IASB issued the final version of IFRS 9 Financial Instruments that replaces IAS 39 FinancialInstruments: Recognition and Measurement and all previous versions of IFRS 9. IFRS 9 brings together allthree aspects of the accounting for the financial instruments project: classification and measurement;impairment; and hedge accounting. IFRS 9 is effective for annual periods beginning on or after 1 January2018, with early application permitted. Except for hedge accounting, retrospective application is required, butproviding comparative information is not compulsory. For hedge accounting, the requirements are generallyapplied prospectively, with some limited exceptions.

The Company plans to adopt the new standard on the required effective date. During 2016, the Companyhas performed a high-level impact assessment of all three aspects of IFRS 9. This preliminary assessment isbased on currently available information and may be subject to changes arising from further detailedanalyses or additional reasonable and supportable information being made available to the Company in thefuture. Overall, the Company expects no significant impact on its statement of financial position and equityexcept for the effect of applying the impairment requirements of IFRS 9. The Company expects a higher lossallowance resulting in a negative impact on equity and will perform a detailed assessment in the future todetermine the extent.

(a) Classification and measurementThe Company does not expect a significant impact on its statement of financial position or equity onapplying the classification and measurement requirements of IFRS 9. It expects to continue measuring atfair value all financial assets currently held at fair value. Quoted equity shares currently held as available-for-sale with gains and losses recorded in OCI will be measured at fair value through profit or lossinstead, which will increase volatility in recorded profit or loss. The AFS reserve currently presented asaccumulated OCI will be reclassified to opening retained earnings. Debt securities are expected to bemeasured at fair value through OCI under IFRS 9 as the Company expects not only to hold the assets tocollect contractual cash flows, but also to sell a significant amount on a relatively frequent basis.

Loans as well as trade receivables are held to collect contractual cash flows and are expected to giverise to cash flows representing solely payments of principal and interest. Thus, the Company expects thatthese will continue to be measured at amortised cost under IFRS 9. However, the Company will analysethe contractual cash flow characteristics of those instruments in more detail before concluding whether allthose instruments meet the criteria for amortised cost measurement under IFRS 9.

Guardian General Insurance Jamaica LimitedNotes to the Financial StatementsYear ended 31 December 2016(Expressed in Jamaican dollars unless otherwise indicated)

14

2. Significant accounting policies (continued)

(b) Adoption of new and revised International Financial Reporting Standards (continued)

New revised and amended standards and interpretations that are not yet effective (continued)

IFRS 9 Financial Instruments (Continued)

(b) ImpairmentIFRS 9 requires the Company to record expected credit losses on all of its debt securities, loans andtrade receivables, either on a 12-month or lifetime basis. The Company expects to apply the simplifiedapproach and record lifetime expected losses on all trade receivables. The Company does not expect asignificant impact on its equity but it will need to perform a more detailed analysis which considers allreasonable and supportable information, including forward-looking elements to determine the extent ofthe impact.

(c) Hedge accountingThis amendment would not apply as the Company does not apply hedge accounting.

IFRS 15 Revenue from Contracts with CustomersIFRS 15 was issued in May 2014 and establishes a five-step model to account for revenue arising fromcontracts with customers. Under IFRS 15, revenue is recognised at an amount that reflects the considerationto which an entity expects to be entitled in exchange for transferring goods or services to a customer.

The new revenue standard will supersede all current revenue recognition requirements under IFRS. Either afull retrospective application or a modified retrospective application is required for annual periods beginningon or after 1 January 2018. Early adoption is permitted. The Company plans to adopt the new standard onthe required effective date using the full retrospective method. During 2016, the Company performed apreliminary assessment of IFRS 15, which is subject to changes arising from a more detailed ongoinganalysis. Furthermore, the Company is considering the clarifications issued by the IASB in April 2016 and willmonitor any further developments.

Amendments to IFRS 10 and IAS 28: Sale or Contribution of Assets between an Investor and itsAssociate or Joint VentureThe amendments address the conflict between IFRS 10 and IAS 28 in dealing with the loss of control of asubsidiary that is sold or contributed to an associate or joint venture. The amendments clarify that the gain orloss resulting from the sale or contribution of assets that constitute a business, as defined in IFRS 3, betweenan investor and its associate or joint venture, is recognised in full. Any gain or loss resulting from the sale orcontribution of assets that do not constitute a business, however, is recognised only to the extent of unrelatedinvestors’ interests in the associate or joint venture. The IASB has deferred the effective date of theseamendments indefinitely, but an entity that early adopts the amendments must apply them prospectively. TheCompany will apply these amendments when they become effective.

Guardian General Insurance Jamaica LimitedNotes to the Financial StatementsYear ended 31 December 2016(Expressed in Jamaican dollars unless otherwise indicated)

15

2. Significant accounting policies (continued)

(b) Adoption of new and revised International Financial Reporting Standards (continued)

New revised and amended standards and interpretations that are not yet effective (continued)

IAS 7 Disclosure Initiative – Amendments to IAS 7The amendments to IAS 7 Statement of Cash Flows are part of the IASB’s Disclosure Initiative and requirean entity to provide disclosures that enable users of financial statements to evaluate changes in liabilitiesarising from financing activities, including both changes arising from cash flows and non-cash changes. Oninitial application of the amendment, entities are not required to provide comparative information forpreceding periods. These amendments are effective for annual periods beginning on or after 1 January 2017,with early application permitted. Application of the amendments will result in additional disclosures providedby the Company.

IAS 12 Recognition of Deferred Tax Assets for Unrealised Losses – Amendments to IAS 12The amendments clarify that an entity needs to consider whether tax law restricts the sources of taxableprofits against which it may make deductions on the reversal of that deductible temporary difference.Furthermore, the amendments provide guidance on how an entity should determine future taxable profits andexplain the circumstances in which taxable profit may include the recovery of some assets for more than theircarrying amount.

Entities are required to apply the amendments retrospectively. However, on initial application of theamendments, the change in the opening equity of the earliest comparative period may be recognised in theopening retained earnings (or in another component of equity, as appropriate), without allocating the changebetween opening retained earnings and other components of equity. Entities applying this relief must disclosethat fact. These amendments are effective for annual periods beginning on or after 1 January 2017 with earlyapplication permitted. If an entity applies the amendments for an earlier period, it must disclose that fact.These amendments are not expected to have any impact on the Company.

IFRS 2 Classification and Measurement of Share-based Payment Transactions — Amendments toIFRS 2The IASB issued amendments to IFRS 2 Share-based Payment that address three main areas: the effects ofvesting conditions on the measurement of a cash-settled share-based payment transaction; the classificationof a share-based payment transaction with net settlement features for withholding tax obligations; andaccounting where a modification to the terms and conditions of a share-based payment transaction changesits classification from cash settled to equity settled.

On adoption, entities are required to apply the amendments without restating prior periods, but retrospectiveapplication is permitted if elected for all three amendments and other criteria are met. The amendments areeffective for annual periods beginning on or after 1 January 2018, with early application permitted. Theseamendments have no impact on the Company’s financial position or performance.

Guardian General Insurance Jamaica LimitedNotes to the Financial StatementsYear ended 31 December 2016(Expressed in Jamaican dollars unless otherwise indicated)

16

2. Significant accounting policies (continued)

(b) Adoption of new and revised International Financial Reporting Standards (continued)

New revised and amended standards and interpretations that are not yet effective (continued)

IFRS 16 LeasesIFRS 16 was issued in January 2016 and it replaces IAS 17 Leases, IFRIC 4 Determining whether anArrangement contains a Lease, SIC-15 Operating Leases-Incentives and SIC-27 Evaluating the Substance ofTransactions Involving the Legal Form of a Lease. IFRS 16 sets out the principles for the recognition,measurement, presentation and disclosure of leases and requires lessees to account for all leases under asingle on-balance sheet model similar to the accounting for finance leases under IAS 17. The standardincludes two recognition exemptions for lessees – leases of ’low-value’ assets (e.g., personal computers) andshort-term leases (i.e., leases with a lease term of 12 months or less). At the commencement date of a lease,a lessee will recognise a liability to make lease payments (i.e., the lease liability) and an asset representingthe right to use the underlying asset during the lease term (i.e., the right-of-use asset). Lessees will berequired to separately recognise the interest expense on the lease liability and the depreciation expense onthe right-of-use asset.

Lessees will be also required to remeasure the lease liability upon the occurrence of certain events (e.g., achange in the lease term, a change in future lease payments resulting from a change in an index or rate usedto determine those payments). The lessee will generally recognise the amount of the remeasurement of thelease liability as an adjustment to the right-of-use asset.

Lessor accounting under IFRS 16 is substantially unchanged from today’s accounting under IAS 17. Lessorswill continue to classify all leases using the same classification principle as in IAS 17 and distinguish betweentwo types of leases: operating and finance leases.

IFRS 16 also requires lessees and lessors to make more extensive disclosures than under IAS 17. IFRS 16is effective for annual periods beginning on or after 1 January 2019. Early application is permitted, but notbefore an entity applies IFRS 15. A lessee can choose to apply the standard using either a full retrospectiveor a modified retrospective approach. The standard’s transition provisions permit certain reliefs.

In 2017, the Company plans to assess the potential effect of IFRS 16 on its financial statements.

(c) Revenue recognition

Underwriting incomePremiums are recognised over the life of the policies written. The portion of premiums written in the currentyear which relates to coverage in subsequent years is deferred as unearned premiums (Note 2(f)).Commissions earned on the reinsurance of risks are credited to revenue over the life of the policies.

Interest incomeInterest income for all interest bearing financial instruments is recognised within investment income in thestatement of comprehensive income using the effective interest method.

DividendDividend income for equities is recognised when the right to receive payment is established.

Guardian General Insurance Jamaica LimitedNotes to the Financial StatementsYear ended 31 December 2016(Expressed in Jamaican dollars unless otherwise indicated)

17

2. Significant accounting policies (continued)

(d) Insurance contracts

Insurance contracts are those contracts that transfer significant insurance risk. The Company’s insurancecontracts are classified as short-term insurance contracts which include casualty and property insurancecontracts.

Casualty insurance contracts protect the Company’s customers against the risk of causing harm to thirdparties as a result of their legitimate activities. Damages covered include both contractual andnon-contractual events. The typical protection offered is designed for employers who become legally liable topay compensation to injured employees (employer’s liability) and business customers who become liable topay compensation to a third party for bodily harm or property damage (public liability).

Property insurance contracts mainly compensate the Company’s customers for damage suffered to theirproperties or for the value of property lost. Customers who undertake commercial activities on their premisescould also receive compensation for loss of earnings caused by the inability to use the insured properties intheir business activities (business interruption cover).

Premiums are recognised as revenue (earned premiums) proportionally over the period of coverage. Theportion of premium received on in-force contracts that relates to unexpired risk at the statement of financialposition date is reported as the unearned premium liability. Premiums are shown before deductiblecommission.

Claims and loss adjustments expenses are charged to the statement of comprehensive income as incurredbased on estimated liability for compensation owed to contract holders or third parties damaged by thecontract holders. They include direct and indirect claims settlement costs and arise from events that haveoccurred up to the statement of financial position date even if they have not yet been reported to theCompany. The Company does not discount its liabilities for unpaid claims other than for disability claims.Liabilities for unpaid claims are estimated using the input of assessments for individual cases reported to theCompany. Statistical analysis is used to estimate claims incurred but not reported, as well as the expectedultimate cost of more complex claims that may be affected by external factors.

(e) Receivables and payables related to insurance contracts

Receivables and payables are recognised when due. These include amounts due to and from agents,brokers and insurance contract holders.

If there is objective evidence that the insurance receivable is impaired, the Company reduces the carryingamount of the insurance receivable accordingly and recognises the impairment loss in the statement ofcomprehensive income.

(f) Provision for unearned premiums

The provision for unearned premiums represents the proportion of premiums written relating to periods ofinsurance subsequent to the statement of financial position date and is calculated on the “365th” basis.

(g) Provision for unexpired risks

The provision for unexpired risks is determined by the appointed actuary and represents the expected futurecosts associated with the unexpired portion of policies in force as of the statement of financial position date,in excess of the net unearned premium minus net deferred policy acquisition costs.

Guardian General Insurance Jamaica LimitedNotes to the Financial StatementsYear ended 31 December 2016(Expressed in Jamaican dollars unless otherwise indicated)

18

2. Significant accounting policies (continued)

(h) Provision for claims outstanding

The provision for claims outstanding represents estimates of the cost of settling claims made, but not paidas of the statement of financial position date, less expected reinsurance recoveries. The provision forclaims incurred but not reported (“IBNR”) is actuarially determined by the appointed actuary in accordancewith the actuarial regulations of the Insurance Act, 2001.

(i) Reinsurance

Contracts entered into by the Company with reinsurers under which the Company is compensated forlosses on one or more contracts issued by the Company are classified as reinsurance contracts.

The benefits to which the Company is entitled under its reinsurance contracts held are recognised asreinsurance assets. These assets consist of short–term balances due from reinsurers as well as longerterm receivables that are dependent on the expected claims and benefits arising under the relatedreinsurance contracts. Amounts recoverable from or due to reinsurers are measured consistently withamounts associated with the reinsured insurance contracts and in accordance with the terms of eachreinsurance contract. Reinsurance liabilities are primarily premiums payable for reinsurance contracts andare recognised as an expense when due.

Estimated amounts of reinsurance recoverable, which represent the unearned portion of premiums cededto the reinsurers are included in recoverable from reinsurers on the statement of financial position.

The Company relies upon reinsurance agreements to limit the potential for losses and to increase itscapacity to write insurance. Reinsurance arrangements are effected under reinsurance treaties and bynegotiation on individual risks. Reinsurance does not relieve the Company from liability to its policyholders.To the extent that a reinsurer may be unable to pay losses for which it is liable under the terms of thereinsurance agreement, the Company is exposed to the risk of continued liability for such losses. However,in an effort to reduce the risk of non-payment, the Company requires all of its reinsurers to have a Standard& Poor or equivalent rating of A- or better.

The Company assesses its reinsurance assets for impairment. If there is objective evidence that thereinsurance asset is impaired, the Company reduces the carrying amount of the reinsurance asset to itsrecoverable amount and recognises that impairment loss in the statement of comprehensive income.

(j) Unearned commission

The unearned commission represents the actual commission income on premium ceded on proportionalreinsurance contracts relating to the unexpired period of risk carried. The income is deferred as unearnedcommission reserves, and amortised over the period in which the commissions are expected to be earned.These reserves are calculated on the 365th method.

(k) Deferred policy acquisition costs (“DAC”)

Commissions and other acquisition costs that vary with and are related to securing new contracts andrenewing existing contracts are deferred and recognised as an asset. All other costs are recognised asexpenses when incurred. The DAC is subsequently amortised as premium is earned over the life of thecontracts.

Guardian General Insurance Jamaica LimitedNotes to the Financial StatementsYear ended 31 December 2016(Expressed in Jamaican dollars unless otherwise indicated)

19

2. Significant accounting policies (continued)

(l) Property and equipment and intangible assets

Property and equipment are stated at historical cost less depreciation. Intangible assets are stated athistorical cost less amortisation. Historical cost includes expenditure directly attributable to the acquisitionof the items.

Acquired computer software licences and website development costs are capitalised as intangible assetson the basis of the costs incurred to acquire and bring to use the specific software. Costs that are directlyassociated with the development of identifiable and unique software products controlled by the Company,and that will probably generate economic benefits exceeding costs beyond one year, are also recognisedas intangible assets.

Subsequent costs are included in the asset’s carrying amount or recognised as a separate asset, asappropriate, only when it is probable that future economic benefits associated with the item will flow to theCompany and the cost of the item can be measured reliably. Repairs and maintenance are charged to thestatement of comprehensive income during the financial period in which they are incurred.

Property and equipment and intangible assets with the exception of freehold land, on which no depreciationis provided, are depreciated/amortised on a straight-line basis over the estimated useful lives of the assetsas follows:

Computer equipment 33 1/3%Furniture and fixtures 10% - 20%Motor vehicles 20%Leasehold improvements Shorter of period of lease or useful life of assetIntangible assets 33 1/3%

The residual values and useful lives are reviewed, and adjusted if appropriate, at each statement offinancial position date.

An asset’s carrying amount is written down immediately to its recoverable amount if the asset’s carryingamount is greater than its estimated recoverable amount.

Gains and losses on disposals are determined by comparing the proceeds with their carrying amount.These are included in the statement of comprehensive income.

(m) Foreign currency translation

(i) Functional and presentation currencyItems included in the financial statements of the Company are measured using the currency of theprimary economic environment in which the Company operates (‘the functional currency’). The financialstatements are presented in Jamaican dollars, which is the Company’s functional and presentationcurrency.

(ii) Transaction and balancesForeign currency transactions are translated into the functional currency using the exchangerates prevailing at the dates of the transactions. Foreign exchange gains and losses resultingfrom the settlement of such transactions and from the translation at year-end exchange rates ofmonetary assets and liabilities denominated in foreign currencies are recognised in the statement ofcomprehensive income.

Guardian General Insurance Jamaica LimitedNotes to the Financial StatementsYear ended 31 December 2016(Expressed in Jamaican dollars unless otherwise indicated)

20

2. Significant accounting policies (continued)

(n) Investments

Investment securities are classified as financial assets at fair value through profit or loss and available-for-sale. Management determines the appropriate classification of investments at the time of purchase.

Financial assets classified as fair value through profit or loss have two sub-categories: financial assets heldfor trading and those designated at fair value through profit or loss at inception.

A financial asset is classified as held for trading if acquired principally for the purpose of selling in the shortterm or if it forms part of a portfolio of financial assets in which there is evidence of short term profit-taking.

Financial assets designated as fair value through profit or loss at inception by the Company, are those thatare managed and whose performance is evaluated on a fair value basis. Information about these financialassets is provided internally on a fair value basis to the Company’s key management personnel.

Investments classified as fair value through profit or loss are initially recognized and subsequentlymeasured at fair value. All related transaction costs for these investments are expensed. Investments arederecognised when the rights to receive cash flows from the investments have expired or have beentransferred and the Company transfers all risks and rewards of ownership.

Gains or losses arising from changes in the fair value of financial assets at fair value through profit or lossare presented in the statement of comprehensive income within investment and finance income in theperiod in which they arise.

Available-for-sale investments are stated at fair value, except where fair value cannot be reliablydetermined, in which case they are stated at cost, with any movements in fair value included in investmentrevaluation reserve.

The fair value of available-for-sale investments is based on their quoted market bid price at the reportingdate. Where a quoted market price is not available, fair value is estimated using discounted cash flowtechniques.

All purchases and sales of investment securities are recognised at settlement date.

(o) Income taxes

Taxation expense in the statement of comprehensive income comprises current and deferred income taxcharges.

Current income tax charges are based on taxable profits for the year, which differ from the profit before taxreported because it excludes items that are taxable or deductible in other years, and items that are nevertaxable or deductible. The Company’s liability for current income tax is calculated at tax rates that havebeen enacted at statement of financial position date.

Deferred tax is the tax expected to be paid or recovered on differences between the carrying amounts ofassets and liabilities and the corresponding tax bases. Deferred tax is provided in full, using the liabilitymethod, on temporary differences arising between the tax bases of assets and liabilities and their carryingamounts in the financial statements. Currently enacted tax rates are used in the determination of deferredincome tax.

Guardian General Insurance Jamaica LimitedNotes to the Financial StatementsYear ended 31 December 2016(Expressed in Jamaican dollars unless otherwise indicated)

21

2. Significant accounting policies (continued)

(o) Income taxes (continued)

Deferred tax assets are recognised to the extent that it is probable that future taxable profit will be availableagainst which the temporary differences can be utilised.

Deferred tax is charged or credited in the statement of comprehensive income, except in instances wheredeferred tax relates to items recognised directly in other comprehensive income, in which case, deferred taxis charged or credited to other comprehensive income.

Deferred tax assets and liabilities are offset when there is a legally enforceable right to offset current taxassets against current income tax liabilities and when the deferred taxes relate to the same fiscal liability.

(p) Employee benefits

(i) Pension schemeThe Company operates a defined contribution scheme. A defined contribution scheme is a pensionplan under which the Company pays fixed contributions into a separate entity. The Company has nolegal obligations to pay further contributions if the fund does not hold sufficient assets to pay allemployees the benefits relating to employee service in the current and prior periods. The contributionsare recognised as employees’ benefit expense when they are due. Prepaid contributions arerecognised as an asset to the extent that a cash refund or reduction in the future payments is available.

(ii) Leave accrualEmployees’ entitlements to annual leave are recognised when they accrue to employees. A provisionis made for the estimated liability for annual leave as a result of services rendered by employees up tothe statement of financial position date.

(iii) Termination benefitsTermination benefits are payable whenever an employee’s employment is terminated before thenormal retirement date or whenever an employee accepts voluntary redundancy in exchange for thesebenefits. The Company recognises termination benefits when it is demonstrably committed to eitherterminate the employment of current employees according to a detailed formal plan without thepossibility of withdrawal or to provide termination benefits as a result of an offer made to encouragevoluntary redundancy. Benefits falling due more than twelve (12) months after the statement offinancial position date are discounted to present value.

(iv) Employee benefit obligationsPost retirement medical benefits are provided for the pensioners of the Company. Post retirementobligation included in the financial statements has been actuarially determined by an independentqualified actuary that was appointed by management. The actuarial valuation was conducted inaccordance with the requirements of IAS 19, using the projected unit credit method.

Remeasurements, comprising of actuarial gains and losses, excluding amounts included in net intereston the net defined benefit liability and the return on plan assets (excluding amounts included in netinterest on the net defined benefit liability), are recognised immediately in the statement of financialposition with a corresponding debit or credit to retained earnings through the statement ofcomprehensive income in the period in which they occur. Remeasurements are not reclassified to profitor loss in subsequent periods.

Guardian General Insurance Jamaica LimitedNotes to the Financial StatementsYear ended 31 December 2016(Expressed in Jamaican dollars unless otherwise indicated)

22

2. Significant accounting policies (continued)

(p) Employee benefits (continued)

(iv) Employee benefit obligations

Past service costs are recognised in profit or loss on the earlier of:

· The date of the plan amendment or curtailment, and· The date that the Company recognises related restructuring costs

Net interest is calculated by applying the discount rate to the net defined benefit liability or asset. TheCompany recognises the following changes in the net defined benefit obligation under expenses instatement of comprehensive income:

· Service costs comprising current service costs, past-service costs, gains and losses oncurtailments and non-routine settlements

· Net interest expense or income

(v) Share-based compensationGuardian Holdings Limited and its subsidiaries (the “Group”) participate in an equity-settled share-based compensation plan operated by the holding company. The fair value of the employee servicesreceived in exchange for the grant of the options is recognised as an expense. The total amount to beexpensed over the vesting period is determined by reference to the fair value of options granted,excluding the impact of any non-market vesting conditions (for example, net profit growth target). Non-market vesting conditions are included in the assumptions about the number of options that areexpected to become exercisable. At the statement of financial position date, the Group revises itsestimate of the number of options that are expected to become exercisable. It recognises the impact ofthe revision of original estimates, if any, in the statement of comprehensive income, and acorresponding adjustment to equity over the remaining vesting period. When the options are exercised,the proceeds received net of any transaction costs are credited to the share options reserve.

(q) Provisions

Provisions are recognised when there is a present legal or constructive obligation as a result of past events, ifit is probable that an outflow of resources will be required to settle the obligation and a reliable estimate of theamount of the obligation can be made.

(r) Leases

Leases in which a significant portion of the risks and rewards of ownership are retained by the lessor areclassified as operating leases. Payments made under operating leases (net of any incentives received fromthe lessor) are charged to the statement of comprehensive income on a straight-line basis over the period ofthe lease.

(s) Impairment of non-financial assets

Assets that have an indefinite useful life, are not subject to amortisation and are tested annually forimpairment. Assets that are subject to amortisation are reviewed for impairment whenever events or changesin circumstances indicate that the carrying amount may not be recoverable. An impairment loss is recognisedfor the amount by which the asset’s carrying amount exceeds its recoverable amount. The recoverableamount is the higher of an asset’s fair value less costs to sell and value in use. For the purposes of assessingimpairment, assets are grouped at the lowest levels for which there are separately identifiable cash flows(cash-generating units).

Guardian General Insurance Jamaica LimitedNotes to the Financial StatementsYear ended 31 December 2016(Expressed in Jamaican dollars unless otherwise indicated)

23

2. Significant accounting policies (continued)

(t) Cash and cash equivalents

For the purposes of the statement of cash flows, cash and cash equivalents comprise cash and bankbalances, deposits held at call with banks, and other short-term highly liquid investments with maturities of 90days or less, net of bank overdrafts.

(u) Impairment of financial assets

The Company assesses at each reporting date whether there is any objective evidence that a financial assetis deemed to be impaired if there is objective evidence of impairment as a result of one or more events thathas occurred after the initial recognition of the asset (an incurred ‘loss event’) and that loss event has animpact on the estimated future cash flows of the financial asset or the group of financial assets that can bereliably estimated. Evidence of impairment may include indications that the debtors or a group of debtors isexperiencing significant financial difficulty, default or delinquency in interest or principal payments, theprobability that they will enter bankruptcy or other financial reorganisation and where observable dataindicate that there is a measurable decrease in the estimated future cash flows, such as changes in arrearsor economic conditions that correlate with defaults.

If there is objective evidence that an impairment loss on assets carried at amortized cost has been incurred,the amount of the impairment loss is measured as the difference between the asset's carrying amount andthe present value of the estimated future cash flows (excluding future expected credit losses that have notbeen incurred) discounted at the financial asset's original effective interest rate. The carrying amount of theasset is reduced and the loss is recognised in the statement of profit or loss.

The Company first assesses whether objective evidence of impairment exists individually for financial assetsthat are individually significant, and individually or collectively for financial assets that are not individuallysignificant. If it is determined that no objective evidence of impairment exists for an individually assessedfinancial asset, whether significant or not, the asset is included in a group of financial assets with similarcredit risk characteristics and that group of financial assets is collectively assessed for impairment. Assetsthat are individually assessed for impairment and for which an impairment loss is, or continues to be,recognised are not included in a collective assessment of impairment. The impairment assessment isperformed at each statement of financial position date.

If in a subsequent period, the amount of the impairment loss decreases and the decrease can be relatedobjectively to an event occurring after the impairment was recognised, the previously recognised impairmentloss is reversed. Any subsequent reversal of an impairment loss is recognised in the statement of profit orloss, to the extent that the carrying value of the asset does not exceed its amortized cost at the reversal date.

Guardian General Insurance Jamaica LimitedNotes to the Financial StatementsYear ended 31 December 2016(Expressed in Jamaican dollars unless otherwise indicated)

24

2. Significant accounting policies (continued)

(v) Fair value measurement

The Company measures financial instruments and non-financial assets at fair value at each statement offinancial position date.

Fair value is the price that would be received to sell an asset or paid to transfer a liability in an orderlytransaction between market participants at the measurement date. The fair value measurement is based onthe presumption that the transaction to sell the asset or transfer the liability takes place either:

· in the principal market for the asset or liability, or· in the absence of a principal market, in the most advantageous market for the asset or liability

The principal or the most advantageous market must be accessible to the Company.

The fair value of an asset or a liability is measured using the assumptions that market participants woulduse when pricing the asset or liability, assuming that market participants act in their economic best interest.

A fair value measurement of a non-financial asset takes into account a market participant's ability togenerate economic benefits by using the asset in its highest and best use or by selling it to another marketparticipant that would use the asset in its highest and best use.

The Company uses valuation techniques that are appropriate in the circumstances and for which sufficientdata are available to measure fair value, maximising the use of relevant observable inputs and minimisingthe use of unobservable inputs.

All assets and liabilities for which fair value is measured or disclosed in the financial statements arecategorized within the fair value hierarchy, described as follows, based on the lowest level input that issignificant to the fair value measurement as a whole:

(i) Level 1 — Quoted (unadjusted) market prices in active markets for identical assets or liabilities.Financial assets in this category are measured in whole or in part by reference to published quotes inan active market. A financial instrument is regarded as quoted in an active market if quoted prices arereadily and regularly available from an exchange, dealer, broker, industry group, pricing service orregulatory agency and those prices represent actual and regularly occurring market transactions on anarm's length basis.

(II) Level 2 — Valuation techniques for which the lowest level input that is significant to the fair valuemeasurement is directly or indirectly observable.Financial assets are measured using a valuation technique based on assumptions that are supportedby prices from observable current market transactions, and for which pricing is obtained via pricingservices, but where prices have not been determined in an active market. This includes financial assetswith fair values based on broker quotes, investments in mutual funds with published net asset valuesand evidence of trades and assets that are valued using the Company's own modelswhereby themajority of assumptions are market observable.

(iii) Level 3 — Valuation techniques for which the lowest level input that is significant to the fair valuemeasurement is unobservable.Assets and liabilities included in level 3 are held at cost, being the fair value of the consideration paidon acquisition and are regularly assessed for impairment. These financial assets are not quoted asthere are no active markets to determine a price. The main asset class in this category is unlistedequity instruments.

Guardian General Insurance Jamaica LimitedNotes to the Financial StatementsYear ended 31 December 2016(Expressed in Jamaican dollars unless otherwise indicated)

25

2. Significant accounting policies (continued)

(v) Fair value measurement (continued)

For assets and liabilities that are recognized in the financial statements on a recurring basis, the Companydetermines whether transfers have occurred between levels in the hierarchy by re-assessing categorization(based on the lowest level input that is significant to the fair value measurement as a whole) at the end ofeach reporting period.

(w) Financial instruments

Financial instruments carried on the statement of financial position include cash, investments, otherreceivables, and other liabilities. The particular recognition methods adopted are disclosed in the individualpolicy statements associated with each item. The determination of the fair values of the Company’sfinancial instruments is discussed in Note 5.

(x) Dividend distribution

Dividends are recorded as a deduction from shareholders’ equity in the period in which they are approved.

3. Insurance and financial risk management

The Company’s activities expose it to a variety of insurance and financial risks and those activities involve theanalysis, evaluation, acceptance and management of some degree of risk or combination of risks. Taking risk iscore to the financial business, and the operational risks are an inevitable consequence of being in business. TheCompany’s aim is therefore to achieve an appropriate balance between risk and return and minimize potentialadverse effects on the Company’s financial performance.

The Company’s risk management policies are designed to identify and analyse these risks, to set appropriaterisk limits and controls, and to monitor the risks and adherence to limits by means of reliable and up-to-dateinformation systems. The Company regularly reviews its risk management policies and systems to reflectchanges in markets, products and emerging best practice.

The Board of Directors is ultimately responsible for the establishment and oversight of the Company’s riskmanagement framework. The Board has established committees/departments for managing and monitoringrisks, as follows:

(i) Finance DepartmentThe Finance Department is responsible for managing the Company’s assets and liabilities and the overallfinancial structure. It is also primarily responsible for managing the funding and liquidity risks of theCompany.

(ii) Investment CommitteeThe Investment Committee is responsible for monitoring the investment portfolio, and the development ofinvestment strategies for the Company. The Investment Committee is also responsible for theestablishment of appropriate trading limits, reports and compliance controls to ensure that its mandate isproperly followed.

Guardian General Insurance Jamaica LimitedNotes to the Financial StatementsYear ended 31 December 2016(Expressed in Jamaican dollars unless otherwise indicated)

26

3. Insurance and financial risk management (continued)

(ii) Audit CommitteeThe Audit Committee oversees how management monitors compliance with the Company’s riskmanagement policies and procedures and reviews the adequacy of the risk management framework inrelation to the risks faced by the Company. The Audit Committee is assisted in its oversight role byInternal Audit. Internal Audit undertakes both regular and ad hoc reviews of risk management controls andprocedures, the results of which are reported to the Audit Committee.

The most important types of risk faced by the Company are insurance risk, credit risk, liquidity risk andmarket risk. Market risk includes currency risk, interest rate and equity price risk.

(a) Insurance risk

The risk under any one insurance contract is the possibility that the insured event occurs and the uncertaintyof the amount of the resulting claim. By the very nature of an insurance contract, this risk is random andtherefore unpredictable.

For a portfolio of insurance contracts where the theory of probability is applied to pricing and provisioning, theprincipal risk that the Company faces under its insurance contracts is that the actual claim payments exceedthe carrying amount of the insurance liabilities.

Experience shows that the larger the portfolio of similar insurance contracts, the smaller the relative variabilityabout the expected outcome will be. In addition, a more diversified portfolio is less likely to be affected acrossthe board by a change in any subset of the portfolio. The Company has developed its insurance underwritingstrategy to diversify the type of insurance risks accepted and within each of these categories to achieve asufficiently large population of risks to reduce the variability of the expected outcome.

Management maintains an appropriate balance between commercial and personal policies and type ofpolicies based on guidelines set by the Board of Directors. Insurance risk arising from the Company’sinsurance contracts is, however, concentrated within Jamaica.

The Company has the right to re-price the risk on renewal. It also has the ability to impose deductibles andreject fraudulent claims. Where applicable, contracts are underwritten by reference to the commercialreplacement value of the properties or other assets and contents insured. Claims payment limits are alwaysincluded to cap the amount payable on occurrence of the insured event. The cost of rebuilding properties, ofreplacement or indemnity for other assets and contents and the time taken to restart operations for businessinterruption are the key factors that influence the level of claims under these policies.

The frequency or severity of claims and benefits can be affected by the increasing number of cases that aregoing to court for settlement and the level of awards. Estimated inflation is also a significant factor due to thelong period typically required to settle these cases.

Claims on insurance contracts are payable on a claims-occurrence basis. The Company is liable for allinsured events that occurred during the term of the contract, even if the loss is discovered after the end of thecontract term. As a result, liability claims are settled over a long period of time and a portion of the claimsprovision relates to IBNR claims.

There are several variables that affect the amount and timing of cash flows from these contracts. Thesemainly relate to the inherent risks of the business activities carried out by individual contract holders and therisk management procedures they adopted.

Guardian General Insurance Jamaica LimitedNotes to the Financial StatementsYear ended 31 December 2016(Expressed in Jamaican dollars unless otherwise indicated)

27

3. Insurance and financial risk management (continued)

(a) Insurance risk (continued)

The compensation paid on these contracts is the monetary awards granted for bodily injury suffered byemployees (for employer’s liability covers) or members of the public (for public liability covers). Such awardsare lump-sum payments that are calculated as the present value of the lost earnings and rehabilitationexpenses that the injured party will incur as a result of the accident.

The estimated cost of claims includes direct expenses to be incurred in settling claims, net of the expectedsubrogation value and other recoveries. The Company takes all reasonable steps to ensure that it hasappropriate information regarding its claims exposures. However, given the uncertainty in establishing claimsprovisions, it is likely that the final outcome will prove to be different from the original liability established. Theliability for these contracts comprises a provision for IBNR, a provision for reported claims not yet paid and aprovision for unexpired risks at the statement of financial position date. The amount of casualty claims isparticularly sensitive to the level of court awards and to the development of legal precedent on matters ofcontract and tort. Casualty contracts are also subject to the emergence of new types of latent claims, but noallowance is included for this at the statement of financial position date.

In calculating the estimated cost of unpaid claims (both reported and not), the Company uses estimationtechniques that are a combination of loss-ratio-based estimates (where the loss ratio is defined as the ratiobetween the ultimate cost of insurance claims and insurance premiums earned in a particular financial year inrelation to such claims) and an estimate based upon actual claims experience using predetermined formulaewhere greater weight is given to actual claims experience as time passes.

The initial loss-ratio estimate is an important assumption in the estimation technique and is based onprevious years’ experience, adjusted for factors such as premium rate changes, anticipated marketexperience and historical claims inflation. The initial estimate of the loss ratios used for the current year(before reinsurance) is analysed by type of risk and industry where the insured operates for current and prioryear premiums earned.

The estimation of IBNR is generally subject to a greater degree of uncertainty than the estimation of the costof settling claims already notified to the Company, where information about the claim event is available. IBNRclaims may not be apparent to the insured until many years after the event that gave rise to the claims. Forcasualty contracts, the IBNR proportion of the total liability is high and will typically display greater variationsbetween initial estimates and final outcomes because of the greater degree of difficulty of estimating theseliabilities.

In estimating the liability for the cost of reported claims not yet paid, the Company considers any informationavailable from loss adjusters and information on the cost of settling claims with similar characteristics inprevious periods. Large claims are assessed on a case-by-case basis or projected separately in order toallow for the possible distortive effect of their development and incidence on the rest of the portfolio.

Sensitivity analysis of actuarial liabilitiesActuarial liabilities comprise 100% of total insurance liabilities. The determination of actuarial liabilities issensitive to a number of assumptions, and changes in those assumptions could have a significant effect onthe valuation results. These factors are discussed below.

Guardian General Insurance Jamaica LimitedNotes to the Financial StatementsYear ended 31 December 2016(Expressed in Jamaican dollars unless otherwise indicated)

28

3. Insurance and financial risk management (continued)

(a) Insurance risk (continued)

Actuarial assumptions

(i) In applying the noted methodologies, the following assumptions were made:

· With respect to the analysis of the incurred claims development history, the level of outstandingclaims reserve adequacy is relatively consistent (in inflation adjusted terms) over the experienceperiod.

· With respect to the analysis of the paid claims development history, the rate of payment of ultimateincurred losses for the recent history is indicative of future settlement patterns. The pattern of netdevelopment factors is very stable and there is no evident trend in the factors.

· The claims inflation rate implicit in the valuation is equivalent to the rate which is part of the historicaldata.

· Claims are expressed at their estimated ultimate undiscounted value, in accordance with therequirement of the Insurance Act, 2001.